Embed Size (px)

DESCRIPTION

consumer ed

Citation preview

Learning Objectives

After completing this chapter, you’ll be able to:

1. Define Credit.

2. Know the difference between good and bad debt.

Credit

What is Credit?

Your credit goal is to obtain a good credit score!

Why It’s Important

You’ll probably borrow money (use credit) some day. When you do, it will be helpful to know what credit is and the types of credit you can use.

What is Credit?

Credit is an agreement to get

money, goods, or services now

in exchange for a promise to

pay in the future.

Credit: The Promise to Pay

The one who lends money or

provides credit is called the creditor.

The one who

borrows money or uses credit is

called the debtor.

Credit is a Loan (borrowing money)

How much do you know about borrowing

money? Take the car loan quiz.

http://auto.howstuffworks.com/buying-

selling/applying-car-loan-quiz.htm

Credit Costs you Money

Creditors charge a fee for using their

money, which is called interest.

What is Debt?

There are people who are debt free. It does happen.

But, sometimes, it is not possible to be completely

debt free. You may need to borrow money to buy a

house, finance a car, or pay for your college

education. It is important to know what type of debt is

good, and what type of debt is bad. Eventually all

debts will need to be paid back to the creditor with

interest.

What is Debt?

Debt is money that is owed. You could owe money

to your parents, friends, or a credit card company.

There are many businesses and people that you

could borrow money from and need to pay back.

Staying out of debt is a financial goal.

A debt occurs when a creditor loans money to a

debtor and the borrower agrees to pay that

person, business, or company back, usually with

interest (additional money). The lower the

interest rate, the less money you will

need to pay back to your creditor.

How much money will credit cost you?

The amount of interest is based on

three factors:

• Interest Rate

• Time of the loan

• Amount of the loan -

Principle

I = PxRxT

For example, if you took out a loan for $1000 and

the annual (yearly) interest rate was 10%, then you

would owe $1100 at the end of the first year. (1000

x .10 x 1 = $100). $100 is the amount of interest

(additional money) you owe for the loan of $1000.

(You also have to pay back the $1000).

But, if the annual (yearly) interest rate was 5%,

then you would owe $1050 at the end of the first

year. ($1000 x .05 x 1 = $50.)

Credit scores help determine what your interest

rate is, but we’ll get to that later.

How much will credit cost you?

It’s important to shop around for credit

because creditors may charge different

rates. BMO Harris Cary Bank Chase

Auto Loan 3% 3.5% 6%

Home Loan 5.2% 5.5% 4%

Personal

Loan

6% 6% 6.5%

Home Equity 7% 6% 5%

A lower rate means lower cost (interest) to you.

How much will credit cost you? Interest rates change daily.

BMO Harris Cary Bank Chase

Auto Loan 3.7% 3.5% 4.3%

Home Loan 6.2% 5.38% 4.98%

Personal

Loan

8.5% 8.3% 8.4%

Home Equity 9.3% 8.7% 7.65%

The day you finalize your loan you should lock in

your rate IF you applied for a fixed rate loan.

How much will credit cost you?

Variable rate loan changes on a periodic (monthly,

yearly) basis. BMO Harris Cary Bank Chase

Auto Loan 3.3% 3.2% 3.3%

Home Loan 5.8% 5.3% 4.7%

Personal

Loan

9% 9.2% 9.4%

Home Equity 8.68% 8.54% 7.73%

If the rate of your loan goes down, you get the lower rate

until the next change. If the rate of your loan goes up, you

get the higher rate until the next change.

Which type of loan does the interest rate

stay the same?

A. Fixed

B. Variable

Why should you shop around for credit?

To find the

lowest interest

rate so you can

save money.

Learning Objectives

After completing this chapter, you’ll be able to:

1. Distinguish between good debt and bad debt.

2. Know the advantages and disadvantages of credit.

Credit

Debt – The amount of money you owe

Before you can learn how to build, manage, and use credit,

it is important that you know about debt.

Determining the difference between good and

bad debt and learning the right time to finance

something is the key to your financial well-

being.

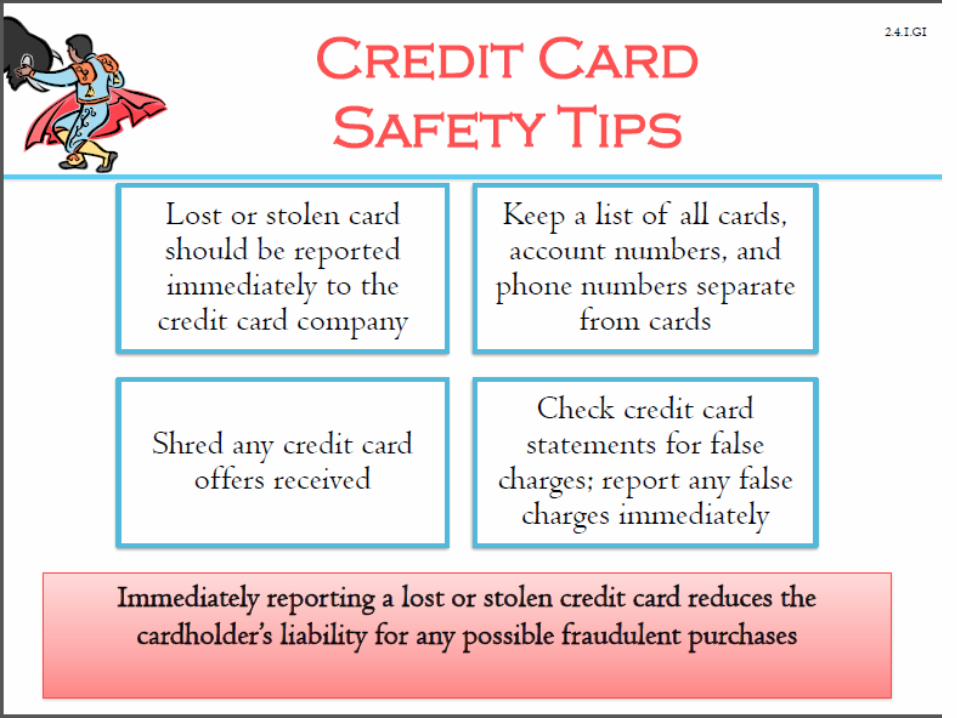

Protecting your credit, using caution when banking and

preventing identity theft will help prevent money troubles in

the future.

Complete Worksheet

Good Debt Before you begin to think about good debt, it is always

important to remember to never let debt get out of hand. If

you spend within your means and do not finance things you

will never be able to pay back, then some amount of debt is

alright. Incurring good debt can also increase your credit

score, which will help you buy expensive items later on.

Buying a home that you can afford is an example of a good debt.

Good Debt

Good debt includes necessities that you can’t afford to pay

for up front. Buying a car to get to your job or purchasing a

home to live in are examples of taking on good debt. Good

debt is debt that increases your personal wealth in some

way. Good debt can also help your credit score. Because

public transportation in the United States may not get you

everywhere you need to go, personal transportation may

be a necessity in order to manage life. While cars

depreciate (decrease in value with time), they allow their

owners to earn a living and manage other aspects of their

lives. Homes generally increase in value over the long

spans of time and are considered an investment.

Good Debt

What about a college education? On average, according to

the College Board, a private four year university tuition

costs $30,094 annually (yearly) and a public four year in

state resident college tuition costs $8,893 a year.

In addition to tuition, there are

also room and board charges as

well as books and other fees.

Good Debt Not everyone can afford to pay that much money per year

for an education. Student loans are an alternative but it is

always wise to never borrow more than you will be able

to pay back. Remember, investing in college is investing in

your future. The average college graduate will earn over

$1 million more than someone who just has a high

school diploma, during their lifetime. Thus, college loans

are generally considered good debt since they generate

income in the future for those who use them to gain a

degree.

What is an example of Good Debt?

1. House

2. Cary

3. School Loan (only what you need)

Complete Worksheet

Bad Debt

Bad debt is when you finance things that you consume

and do not have the money or a plan to repay the debts

within a reasonable amount of time. A car or home is a

lasting item, and it doesn’t just disappear when you use it.

You can also use these things to increase your overall

wealth. However, when you use your credit card to

pay for your dinner night after night, you will

then need to pay off something you already

consumed and cannot get back.

Bad Debt

Credit cards are generally seen as a bad debt because of

the things that credit cards are usually used to purchase.

Buying a new outfit each week will accumulate debt and a

large balance at the end of the month. Most people cannot

afford to pay off their credit card bill each month—that’s

when it becomes a bad debt. Bad debt will hurt

your overall credit score.

Bad Debt

What if you want to go on vacation? Do

you really want to spend the next 10

years paying off a vacation you took

one summer? No, so it is generally

unwise to go into debt to pay for a

vacation.

Vacation Cost – $2,000

Bad Debt

Once the vacation is over, money

can’t be saved for the next vacation

since the consumer is still paying

for the first vacation.

Secondly, making payments to a

credit card company increases the

cost of the vacation (because of

the added interest payments) and

then makes it more difficult to take a

second vacation.

Save for the Vacation

It is much better to make payments to a

vacation savings account and then go

on vacation, than to take a vacation and

then make payments to a credit card

company.

Turning Bad Debt into Good Debt If you use your credit card to pay for all of your food, clothing, and other

items during the month, it can be a good debt, if you can

pay your balance off in full each month. This can happen with proper budgeting and if you have already the

money set aside for the credit purchases you make. It is good debt if

you already have the money and using credit just makes life easier.

Paying off your credit cards each month actually increases your credit

score.

What is an example of Bad Debt?

1. Consumables (food, drinks)

2. Entertaining friends

3. Purchases you don’t need (clothes)

4. Vacation

Figure

25.1

Advantages vs. Disadvantages

C

R

E

D

I

T

ADVANTAGES DISADVANTAGES

Learning Objectives

Students will be able to:

Credit

1. Explain the advantages and disadvantages of using credit.

Who Uses Credit?

The type of credit used by people for

personal reasons is called consumer

credit.

Who Uses Credit?

Credit used by a business is called

commercial credit.

When businesses borrow

money, they often pass along

the cost of credit to consumers

by charging higher prices on

their products.

Who Uses Credit?

The federal government uses

credit to pay for many of the

services and programs it provides to

its citizens.

National Debt

Who Uses Credit?

State and local governments use credit to pay

for such things as highways,

public housing, stadiums,

and water systems.

Why should I use credit?

There are some things in life that you just can’t have if you

don’t have credit, such as major purchases for big ticket

items or airfare, hotel, car rental.

Advantages of Credit

The main advantage of credit is that it’s

convenient.

Credit is especially useful in an

emergency.

Advantages of Credit

Without credit, there are some things you

can’t buy.

Make a major

purchase.

Advantages of Credit

.

If you don't like to carry large amounts of

cash with you or if a company doesn't

accept cash purchases (for example

most airlines, hotels, and car rental

agencies), putting purchases on a credit

card can make buying things

easier.

Advantages of Credit

Using credit wisely establishes a good

credit rating. A credit rating is a

measure of a person's ability and

willingness to pay debts on time.

It helps establish a credit history.

Advantages of Credit

A good credit rating tells other lenders

that you are a responsible borrower and a

good credit risk.

A good credit rating leads to

guaranteed loan at a low interest rate.

Advantages of Credit

You can take advantage of sales.

Some stores offer special sales for

credit card customers only.

Advantages of Credit

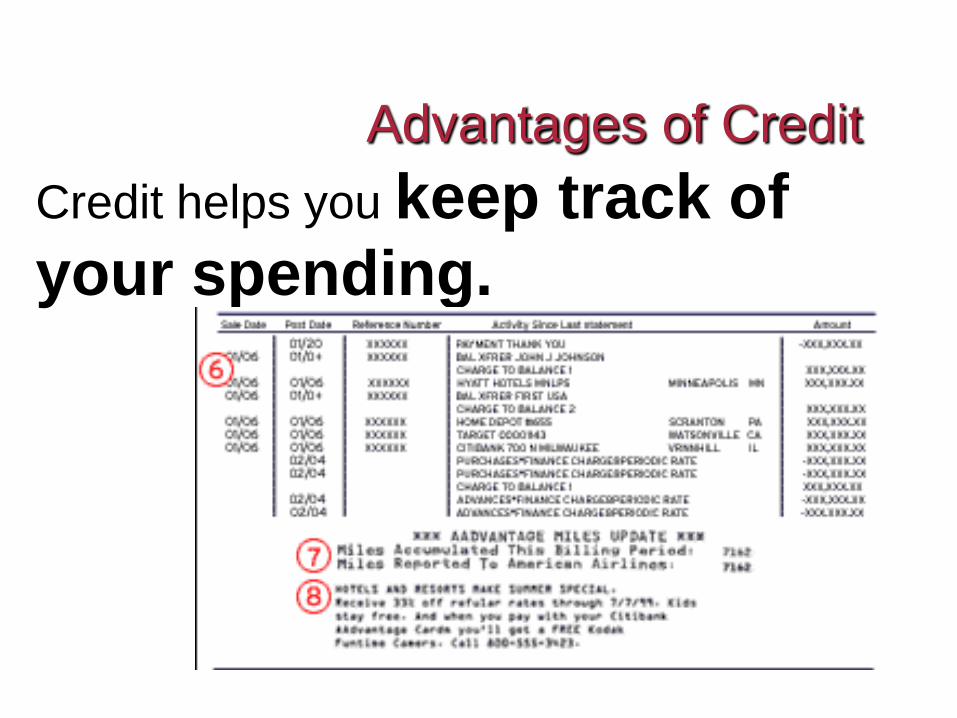

Credit helps you keep track of

your spending.

Advantages of Credit

Credit contributes to the growth of our

economy.

More people are able to spend money

now and pay in the future.

What is an Advantage to Credit?

1. Convenient

2. Make a major purchase

3. Easier to buy things

4. Establish credit history

5. Credit rating

6. Special Sales

7. Keep track of spending

8. GDP goes up – helps economy

Disadvantages of Credit

The more items you charge and the

longer you take to pay off your credit

cards, the more you pay in interest.

Disadvantages of Credit

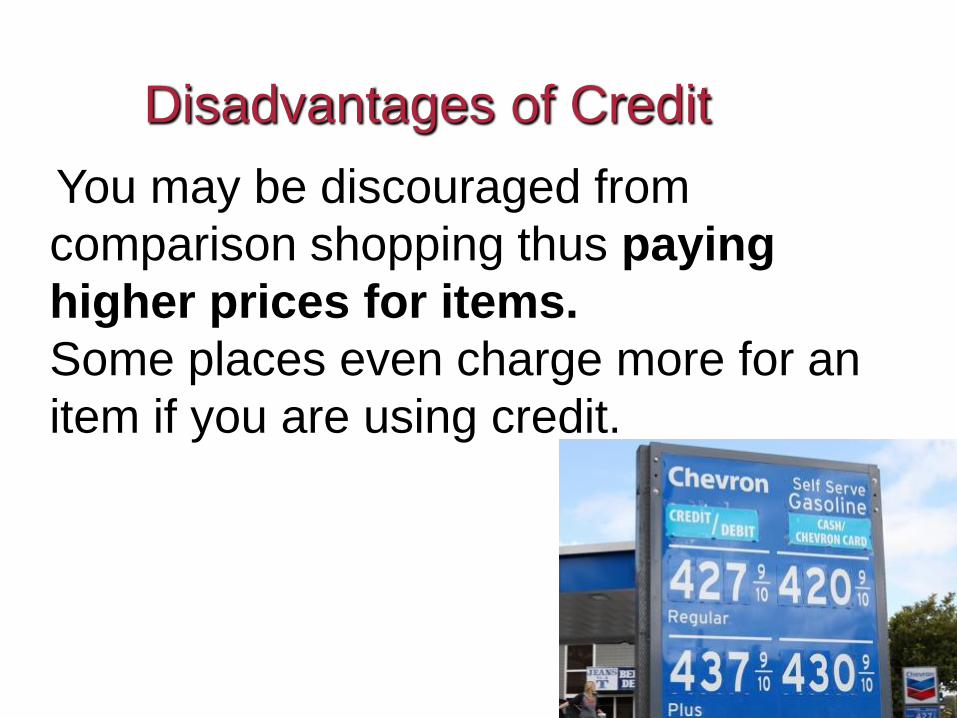

You may be discouraged from

comparison shopping thus paying

higher prices for items.

Some places even charge more for an

item if you are using credit.

Disadvantages of Credit

Credit contracts

(rules) may

be difficult to

understand.

Disadvantages of Credit

Overuse leads to a poor credit rating.

Disadvantages of Credit

Your future

income is tied

up repaying

previous debts.

Disadvantages of Credit

Late or missed payments lower

your credit rating, which will make it

difficult for you to get credit in the future.

What is disadvantage to Credit?

1. Pay interest if you don’t pay it off on time, in full.

2. Pay higher prices

3. Difficult credit rules

4. Overuse = poor credit rating

5. Future income pays past debts

6. Late or missed payments = lower

credit rating.

End of Questions?

Learning Objectives

Identify the different types of credit.

Let’s learn how to get the most of the

advantages of credit by differentiating

the types of credit.

Types of Credit

Short-term loans last for one year or

less.

Medium-term loans last for one to five

years.

Long-term loans last longer than five

years.

Types of Loans

Vehicle Loan House Loan

Student Loan

Personal Loan

Signature Loan

Credit Card and

Cash Advance

Payday Loan

Vehicle Loan

If you don’t have enough money saved to

buy a vehicle, you might want to finance the

vehicle (get a loan).

Banks and other financial institutions may

offer you a loan. This is a secured loan,

because the vehicle will be used as

collateral. If you don’t make the loan

payments (delinquency), the bank can

come and repossess (take away) your car

and resell it to someone else.

Let’s Buy a Car

You have saved $1,000.

That will be your down

payment for the car.

$6,999 - $1,000 =

$5,999.

The $5,999 is the

principal amount you will

need to borrow (get a

loan).

How much will this loan

cost you?

Only

$6,999

2006

Chevrolet

Impala

Calculating the Finance Charge

Finance Charge = Principal x Interest Rate x

Time

The amount a loan costs is known as the

finance charge. This charge can be calculated

by using the following formula:

Finance Charge = Principal x Interest Rate x Time

The higher the Interest Rate the more money you will owe

in finance charges.

The longer the Time period the more money you will owe in

finance charges.

Principal Interest Rate Time Finance

Charge

Home State

Bank

$5999 X 2.69% X 3 = $484.12

Chase Bank $5999 X 2.69% X 4 = $645.49

Harris Bank $5999 X 2% X 7 = $839.86

Which bank is offering you the lowest finance charge? That

is the bank you should get your loan from to purchase your

car.

How much is the Finance Charge? Finance Charge = Principal x Interest Rate x

Time

Only

$6,999

2006

Chevrolet

Impala

Finance Charge = $5,999 x 2.69% x 3

Finance Charge = $484.12

This is your total

finance charge. How

much it will cost you

to borrow this money

for 3 years at the

2.69% interest rate.

Car Payment Your car loan is known as an Installment

loan because this loan will be repaid in

regular (same amount) payments over a

period of time.

How much will you pay each month?

You have to repay $5,999 plus the $484.12 in total

finance charges.

$5,999 + $484.12 = $6,483.12.

Car Payment

You will make equal monthly

payments, to cover the amount of

the loan and the interest.

$5,999 + $484.12 = $6,483.12.

$6,483.12 / 36 months = $180.09 (rounded up)

Only $180.09

per month

(with $1,000

down)

2006

Chevrolet

Impala

Which type of loan is a 5 year car loan?

A. Short term

B. Medium term

C. Long term

Buying a House

House/Property Vocabulary

Land, houses, & condominiums are forms

of investments.

Buy low and sell high!

Equity – means how much ownership

you have in your home

Down payment – amount you pay in cash

to reduce your monthly loan payments

Interest – amount you pay the bank for a

loan

House/Condo Loan

A home loan is known as a mortgage. This loan is a

secured loan because if you don’t repay the loan on time

every month, the finance company can repossess (take

back) your home and resell it to someone else

(foreclosure).

The interest rate on a home loan is usually the lowest

rate for any secured loan because the value of the

home is higher than any other secured loan, such as a car.

If the creditor repossessed your home because of failure to

pay, they would most likely recover their losses from your

lack of payment.

Fixed Loan vs. A.R.M. Loan

• Mortgage – long term property loan

• Typical length is 15 or 30 years

• (click here) Calculator (see how much interest you

pay on a $200,000 House)

• Fixed Mortgage – your interest rate never

changes and the monthly payment remains the

same

• A.R.M. (Adjustable Rate Mortgage)- your

interest rate can fluctuate based on market

conditions

• See article (click here for article)

Interest on a $160,000 loan 30 year fixed loan mortgage

Which type of loan is a 15 year mortgage?

A. Short term

B. Medium term

C. Long term

Home Equity

• Home Equity – the difference between the

market value of your home (what it could

sell for) and what you owe in loan(s) on

the home.

Equity Example

Cost of House

Down Payment

(paid in cash)

Total Loan

Amount (minus

down payment)

Interest on 30

year mortgage

$200,000 $20,000 $180,000 5%

Since you paid $20,000 in cash you now have $20,000 of equity in the House. If your home is worth $250,000 after 5 years and you owe $175,000 on your mortgage loan, you now have $75,000 of equity in the house. ($250,000 - $175,000 = $75,000)

The principal for your loan is $180,000 so the bank is going to charge you 5% interest for borrowing that money.

Refinance a Loan

Refinance – reduce your monthly payments by obtaining a

lower interest rate

If you initially take a loan out for $180,000 from a bank at

a 5% rate

You can refinance and if your credit score is high, you can get a lower rate.

5%

3.5%

This will save you money because you will pay the bank less money in interest on your loan

Interest rates are LOW right NOW so it is a good

time to refinance

Click here to watch a video.

Refinance

You can refinance your:

• Mortgage loans

• Car loans

• Boat loans

• Student loans

The goal is to get a lower interest rate to

SAVE money!

Interest rates are low now because the government

wants us to SPEND money to help the economy

Student Loan

A student loan is an unsecured loan and is designed to

help students pay for college tuition, books, and living

expenses. It may differ from other types of unsecured

loans because the interest rate is lower. There is less risk

of the student not paying back this loan. All student

loans must be paid back. You cannot declare

bankruptcy on this loan.

Students do not have to start paying on this loan until they

have completed their education.

Government

Student

loan interest

is low.

Personal Loans

Banks or other financial institutions may offer

you a personal loan. You can use this money

for personal reasons.

This is an unsecured loan, so therefore the

interest rate will be higher than for a secured

loan. Unsecured

Loan

Personal Loan

Personal loans are often used to pay down and consolidate

debt on high interest credit cards, cover emergency or

unexpected expenses, medical bills, home

improvements bills, moving costs, weddings, paying

taxes, and more.

This is an unsecured personal loan, with no collateral

being promised in consideration for the loan. The creditor

is usually known by the financial institution lending the

credit. For example, they may have a checking or savings

account at the bank in which they are obtaining credit.

Although the interest rate is higher than it is for a secured

loan, it won’t be as high as a signature loan or cash

advance loan.

High

Interest

Signature Loan

This is an unsecured loan often used for small purchases

such as computers, and vacations.

An unsecured loan means the lender relies on the

borrower's promise to pay it back. Due to the increased

risk involved, interest rates for unsecured loans tend to

be higher than they are for secured loans.

This type of loan is usually obtained by creditors whom are

not known very well. Their credit report will not be

analyzed before they receive the credit. Because of these

risk factors, the interest rate on this loan will be higher

than on a personal loan.

Which of the following loans offers the lowest interest to an excellent

creditor?

A. Personal

B. Government Student Loan

C. Signature

Charge Accounts

One of the most common types of

short-term and medium-term credit is

the charge account.

Charge Accounts

The three main types of charge

accounts are:

• Regular

• Revolving

• Budget

Regular Charge Accounts

If the bill is paid on time, you don’t

have to pay interest.

If you don’t pay the entire bill,

interest is charged on the

amount that hasn’t been paid.

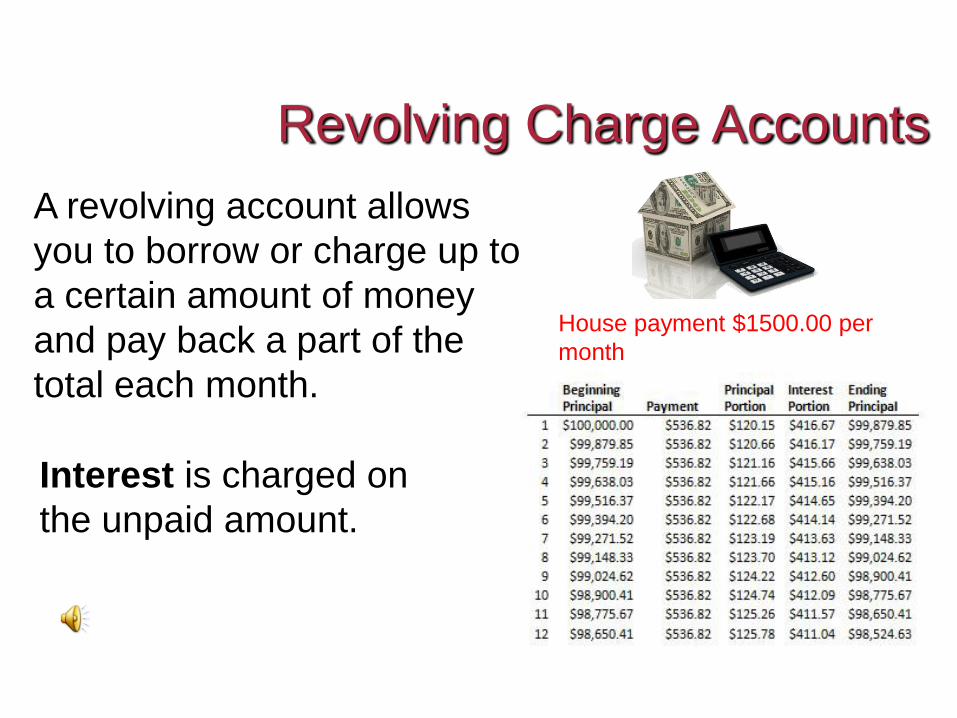

Revolving Charge Accounts

A revolving account allows

you to borrow or charge up to

a certain amount of money

and pay back a part of the

total each month.

Interest is charged on

the unpaid amount.

House payment $1500.00 per

month

Budget Charge Accounts

Budget charge accounts let

you pay for costly items in

equal payments spread out

over a period of time.

Each payment includes

part of the total due on the

item and sometimes

includes interest.

4 payments of

$75.00 each

$300

Which of the following is not a type of

charge account?

A. Budget

B. Convenient

C. Regular

D. Revolving

Which of the following credit accounts always offers no interest?

A. Regular

B. Revolving

C. Budget

Credit Cards

Credit cards are like charge accounts

but some can be used in many

different places.

Credit Cards

The three basic types of credit cards

are:

• Single-purpose

• Multipurpose

• Travel and entertainment

Single Purpose Card = Seller-Provided Credit

Many stores provide credit

for their customers.

One of the reasons they

provide such credit is to

make it easier for

consumers to buy their

products.

Single-Purpose Cards

Single-purpose cards can only be

used to buy goods or services at the

business that issued the card.

NO INTEREST

if paid in full

before the

due date

Multipurpose Cards

Multipurpose cards are also called

bank credit cards because banks

issue them.

Multipurpose cards are designed

to work like a revolving charge

account but you can pay it off in

full each month when it is due and

make it a regular charge account.

NO INTEREST.

NO

INTEREST if

paid in full

before the

due date

3% Rule

Single-Purpose Card Multipurpose Card

3% of transaction remains

with the seller (store).

3% of transaction goes to the multipurpose card company.

You purchase an item for $100.00. You use

a multipurpose credit card. The multipurpose

credit card company ONLY pays the store

$97.00. The store loses $3.00.

Cash Advance on a Credit Card

Cash Advance Loan

A cash advance is a cash loan from a credit card, using an

ATM, a bank withdrawal or "convenience" checks. The

interest rate on cash advances is usually the highest for

any type of loan.

Money obtained for cash advances can be used for anything.

Credit Cards

Some credit cards

have annual fees,

which might range

from $25 to $80.

Credit card companies earn

money from the interest they

charge. Interest rates vary.

VISA

Travel and Entertainment Cards

Travel and

entertainment cards

usually work like regular

charge accounts.

You must pay the full amount

due each month. NO

INTEREST. You will have an

annual fee.

If you are looking for a credit card that can be

used at many different places, you should

apply for which of the following cards?

A. Single Purpose

B. Multi Purpose

C. Travel and Entertainment

D. All of the above

Credit Card Offers How many credit card offers do you think a family

of 4, with excellent credit and has 2 small home

businesses, will receive in one year?

Single Payment Loan

The debtor pays back

this type of loan in one

payment, including

interest (at the end of

the loan period).

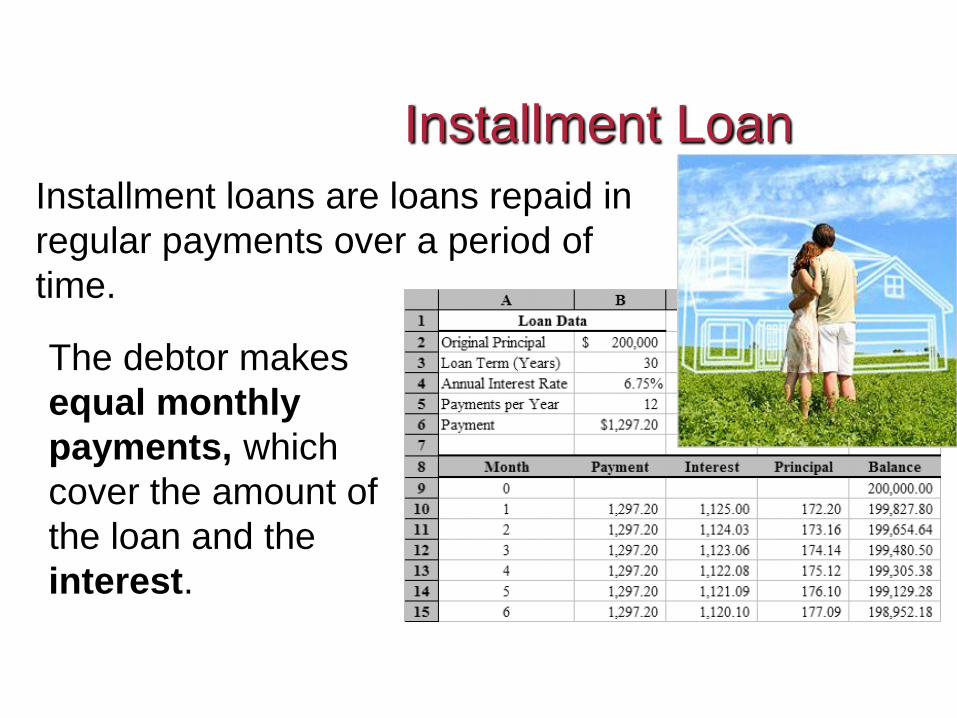

Installment Loan

Installment loans are loans repaid in

regular payments over a period of

time.

The debtor makes

equal monthly

payments, which

cover the amount of

the loan and the

interest.

Which of the following types of loans would be

an installment loan?

A. Mortgage

B. Vehicle Loan

C. Revolving Charge Account

D. All of the above

What is the difference between a

single payment loan and an

installment loan?

A. A single payment loan is

paid in 1 payment and

includes interest.

B. An installment loan is

paid in equal payments.

C. Both A&B

End of Questions?

Activity: Types of Loans

Loan

1. Car

2. House

3. Student (Government

Loan)

4. Personal

5. Signature

6. Cash Advance

Expected Interest Rate

A. 19%

B. 17%

C. 2.25%

D. 14%

E. 2.69%

F. 6%

Directions: Match the loan in the first column with the

expected interest rate in the second column.

Hint: secured loans have lower interest rates.

Activity: Types of Loans

Loan

1. Car

E

2. House C

3. Student F

4. Personal D

5. Signature B

6. Cash Advance A

Expected Interest Rate

A. 19%

B. 17%

C. 2.25%

D. 14%

E. 2.69%

F. 6%

Answers

Learning Objectives

After completing this chapter, you’ll be able to:

1. Name the places where you can get credit. 2. Compare and contrast credit places and

choose the lowest interest.

Where do you borrow money from?

1. Banks

2. Savings and Loans

3. Credit Unions

4. Finance Companies

5. Payday Advance

6. Pawnshops

Making the right decision on where to borrow

money from, can save you money (interest

money).

Banks and Other Financial Institutions

Financial institutions, such

as banks, savings and

loans, and credit unions

offer many types of loans.

Lowest interest rates

available IF you have

and excellent credit

report.

Banks and Other Financial Institutions

More demands on the borrower,

but worth it because the interest

rate should be as low as

possible.

Paperwork

1. Application

2. Check stubs

3. References

4. Tax forms

Consumer Finance Companies

Consumer finance

companies specialize

in loans to people who

might not be able to

get credit elsewhere

because of their poor

credit record. Since you are riskier the

interest rate goes up.

Consumer Finance Companies

Read the disclaimer at the end of this commercial.

Payroll Advance Services

If you don’t have

any savings and

an unexpected

expense occurs,

you might look for

a short-term

loan until

payday.

Also known as “Borrow Until Payday” Loan

A payday loan is made without a

credit check but you must have proof

of a checking account and employment.

These places charge higher interest (because you have extremely poor

credit),

Payroll Advance Services

You write a check to

them for $300 that they

can cash on your next

pay day (1 week) and

they give you $270

today. Not secure

because your

check might

bounce.

$30 in interest for a loan for 1 week! That’s 10%

interest a week.

“Borrow Until Payday” Loan

These businesses provide very short-term

loans, usually for 7 to 14 days. The interest on this kind of loan gets higher because of

the additional time.

Pawnshop Loan A pawnshop loan is based on the

value of something you own.

Generally, the interest of this type of loan is very high

depending on how long you leave your

items at the pawn shop.

Pawnshop Loan Although the interest at a Pawnshop is the

highest for any loan, some people

continue to use a Pawnshop over and over again.

Pawnshop Loan – Court Case

If you have good credit and want a low

interest loan you should apply at which of

the following places?

A. Bank

B. Payday advance

C. Pawnshop

D. American General Finance

Why is it important to have a good credit

rating?

It shows that a consumer is a responsible

borrower and a good credit risk.

Activity: Places to Get a Loan

1. Bank

2. Pawn shop

3. American General

Finance

4. Payday Advance

Expected Interest Rate

A. 3%

B. 15%

C. 50%

D. 10%

Directions: You need a $2,000 car loan that you can repay

in full with interest in 6 months.

Match the place to get a $2,000 car loan in the first column

with the expected interest rate in the second column.

Activity: Places to Get a Loan

Loan

1. Bank

2. Pawn shop

3. American General

Finance

4. Payday Advance

Expected Interest Rate

A. 3%

B. 10%

C. 25%

D. 6%

Directions: You need a $2,000 car loan that you can repay

in full with interest in 6 months.

Match the place to get a $2,000 car loan in the first column

with the expected interest rate in the second column.

A

C

D

B

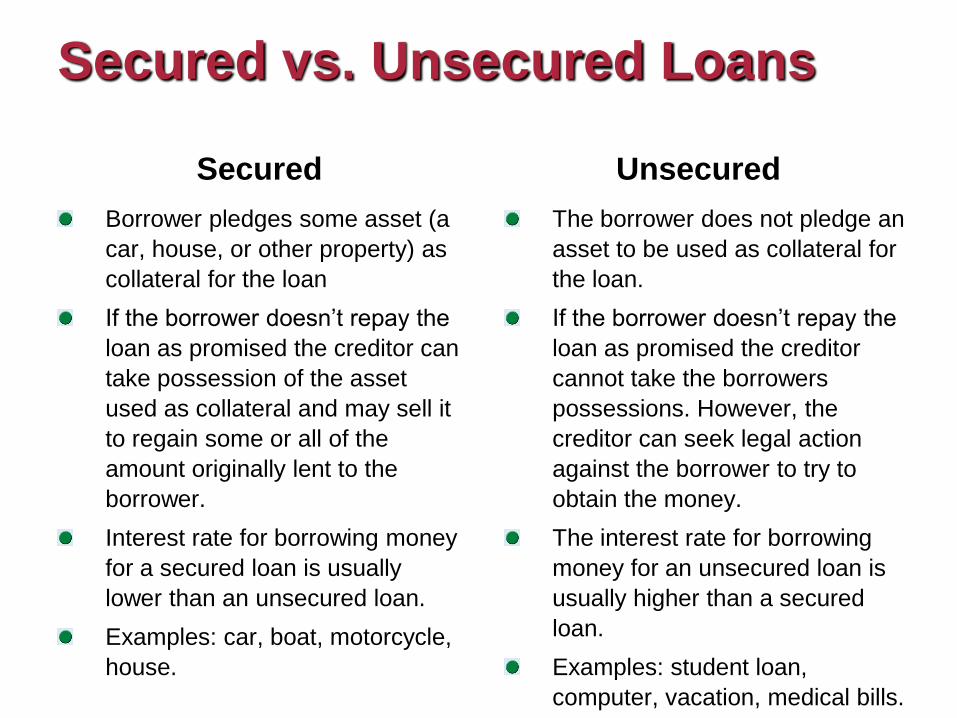

Secured vs. Unsecured Loans

Secured

Borrower pledges some asset (a

car, house, or other property) as

collateral for the loan

If the borrower doesn’t repay the

loan as promised the creditor can

take possession of the asset

used as collateral and may sell it

to regain some or all of the

amount originally lent to the

borrower.

Interest rate for borrowing money

for a secured loan is usually

lower than an unsecured loan.

Examples: car, boat, motorcycle,

house.

Unsecured

The borrower does not pledge an

asset to be used as collateral for

the loan.

If the borrower doesn’t repay the

loan as promised the creditor

cannot take the borrowers

possessions. However, the

creditor can seek legal action

against the borrower to try to

obtain the money.

The interest rate for borrowing

money for an unsecured loan is

usually higher than a secured

loan.

Examples: student loan,

computer, vacation, medical bills.

True Life: I’m in Debt

Click on the link below to watch the video.

Credit Cards

Take Notes

Learning Objectives

After completing this chapter, you’ll be able to:

1. Complete a credit card application.

2. Understand how to use a credit card wisely.

Credit

Credit Card Terms

Credit

Interest

Credit Limit

Annual Percentage Rate

Finance Charge

Annual Fees

Minimum Payment

Due Date

Late Payment Fee

Cash Advance Fee

College Credit Video

1. What does the credit card company offer to college

students which makes its card appealing to the students?

2. How does the college benefit from allowing the credit card

company to solicit on campus?

3. List on criticism that either of the two parents said about

the credit card companies?

4. What explanation did the bank, university, or credit card

solicitor give to justify their action of marketing credit cards

to college students?

Figure

26.1 CREDIT CARD SOLICITATION

First Bank of PR

Prairie Ridge

High School Student

Dear Student:

Applying for Credit

To open a credit or

charge account,

you’ll have to fill out

an application form.

Figure

26.1 CREDIT APPLICATION

When you sign the bottom of the

credit application, it allows the

creditor to access financial

information about you from a credit

bureau.

How old must you be to apply for this

credit card?

Applying for Credit

Security agreement.

This is the most

important piece

of information

and is required

by law. Most

people don’t read

it.

Annual Percentage Rate

The annual percentage rate (APR)

determines the cost of your credit on a

yearly basis.

Changes in Interest Rates In many cases, a credit card might offer a low introductory

rate. This is known as the teaser rate.

After a few months, the rate goes higher (after you’ve

accumulated debt.)

Figure

26.1 SECURITY AGREEMENT

0% for 6 months.

16.99% Variable (That

means it changes

periodically. Could go

up or down.)

Why should you beware of low

introductory interest rates?

They are a teaser to get you to

use the credit card. If you don’t

pay your balance off in full, the

interest rate increases after a

few months.

This will cost you

money!

Other APRs

Default Rates: You did

not pay the minimum

payment on time.

Figure

26.1 SECURITY AGREEMENT

Default Rate: (YOU’RE

LATE ON A PAYMENT)

Up to 21.99% variable

for purchases; up to

28.99% variable for

cash advances.*

Changes in Interest Rates

With a variable rate, the rate changes

as interest rates in the banking system

change.

With a fixed rate, the interest rate

always remains the same.

Figure

26.1 SECURITY AGREEMENT

Purchases - Prime Rate + 13.74% - it

may always be over 13.74%

Purchases Default – Prime Rate +

18.74% - it may always be over

18.74%

Cash Advances – Prime Rate +

20.74% - it may always be over

20.74%

Cash Advances Default – prime Rate

+ up to 25.74% - it may always be

over 25.74%

Figure

26.1 SECURITY AGREEMENT

Method of Computing the Balance for Purchases

Figure

26.1 SECURITY AGREEMENT

Cash Advance: 23.99%

Interest rate until you

pay this money back.

Minimum Finance Charges

A minimum finance charge

could be added to your

credit card if you carry a

balance. This is similar to a

processing fee for

calculating your statement,

mailing it to you, etc.

Figure

26.1 SECURITY AGREEMENT

.50

Other APRs

Cash Advances – You go to the bank

and charge cash.

Figure

26.1 SECURITY AGREEMENT

Cash Advance: 23.99%

Interest rate until you

pay this money back.

Figure

26.1 SECURITY AGREEMENT

Cash Advance – 5%

for each cash

advance, with a

minimum of $10 and

NO MAXIMUM.

Fees

Figure

26.1 SECURITY AGREEMENT

Cash Advance Transaction Fee:

5% for each cash advance.

$1000x.05 = $50

Harris Bank bills Credit Card Company

$1050

You pay $100 next month.

Your new Principal is $950

I = P x R x T

How much interest do you owe?

Fees

With a cash advance you borrow

money on a credit card rather than use

it to make a purchase.

There is often a

separate fee for a cash

advance.

It cost me

$50.00 extra to

get this money.

Figure

26.1 SECURITY AGREEMENT

No Annual Fee

Annual Fee

Annual Fee

In some cases, you have to pay an

annual fee just to have the credit card.

This fee is paid every year and is just

part of the privilege to have the card.

Fees

A late or missed

payment fee is

charged when you

miss a payment or

don’t make a

payment on time.

Figure

26.1 SECURITY AGREEMENT

Late Fee: $19 on

balances up to $250

and $39 on

balances over $250.

You pay

interest on

this late fee.

What are some types of fees credit

cards charge?

Late payment

Missed Payment

Cash Advance

Annual Fee

Grace Period

The grace period is amount of time you get

to pay off a debt without having to pay

interest charges.

Use credit to

your

advantage.

Figure

26.1 SECURITY AGREEMENT

25 days after the

close of each billing

period. NO

FINANCE CHARGE

if you pay IN FULL

by the due date on

your current billing

statement.

Rewards

In some cases, you earn rewards

based on how much you “CHARGE”

on your card.

Use credit to

your

advantage.

Rewards

1 reward point

for each dollar

charged on

credit card.

Rewards

Cash is credited to my credit card

account. Can be used towards

future purchases.

NBC 5 – Credit Card Signatures - Video

Credit Card Offer

2015

Credit Card Review

Credit Card Offer

2015

This is the amount of

interest you will pay

for any purchase

balances not paid in

full by the due date.

2015 Cash Advances is the interest rate

you will pay for using your credit

card at a bank or at an ATM and

borrowing money. The interest rates on

this credit card are

variable (they can

change).

Grace Period – You

have 25 days to pay

your balance in full from

the time the bill is

mailed to you and then

you will not have to pay

interest.

Annual Fee: This is the amount of money

you must pay each year to the credit card

company whether you use the card or not.

If you do not pay your credit card bill in full

by the due date, then the minimum amount

of finance/interest money you will pay is .50

cents, even if the balance multiplied by the

rate of interest is lower.

Credit Card Application

New

Credit

Card

Law

2010

or the APR will be calculated on the balance

(amount you don’t pay) and you will owe more

money.

Note: If you cannot pay the balance in full, pay

as much as you possibly can to keep the interest

charges as low as possible.

Evaluate these Credit Card Offers

Which one

would you

choose?

Credit Worthiness

Learning Targets

After you have completed this unit, you

will be able to:

Explain what creditors look for in

applicants when they apply for credit.

Identify the 5 C’s of Credit.

Explain the Equal Credit Opportunity Act

(ECOA).

Evaluate credit applications and decide

whether to approve or deny credit.

Your Credit Worthiness: The Five Cs

There are several factors

creditors consider before

giving you credit, which

are usually referred to as

the “five Cs of credit.”

Your Credit Worthiness: The Five Cs

The five Cs of credit are:

1. Character

2. Capacity

3. Capital

4. Collateral

5. Credit History Credit History

Character

Creditors might ask for credit references from businesses

or people you’ve borrowed from in the past who can testify

to your reliability when you fill out a credit application.

If this section is

left blank, you

may be denied

credit. Complete

as much of it as

you can.

Do you

move

around

a lot?

Capacity

Creditors will also consider your capacity to pay

back the credit before they decide to give you

credit.

Creditors will check to see whether you have a job,

how much money you make, and how long you’ve been

employed when considering your capacity to repay the

loan.

Capital

Your capital is how much

you have beyond what you

owe. It is also known as your

assets.

A creditor will want to know if you

have valuable assets such as

personal property, investments,

or savings with which to repay

the debt if income is unavailable.

Capital Own

Retirement $30,000

Savings $4,000

Stocks $10,000

Collateral

Collateral consists of property,

or valuables. It can be used as

security for a loan.

If you fail to pay back a loan, the

creditor can take whatever you

pledged (agreed to on the loan

document) as collateral, such as

a car, jewelry, or house and resell

it to try to get their money back

that you owe them.

Credit History

The creditor then checks with a credit bureau, which

is an agency that collects information about you and

other consumers of credit. The credit bureau report

tells whether you pay bills on time and how much

you owe.

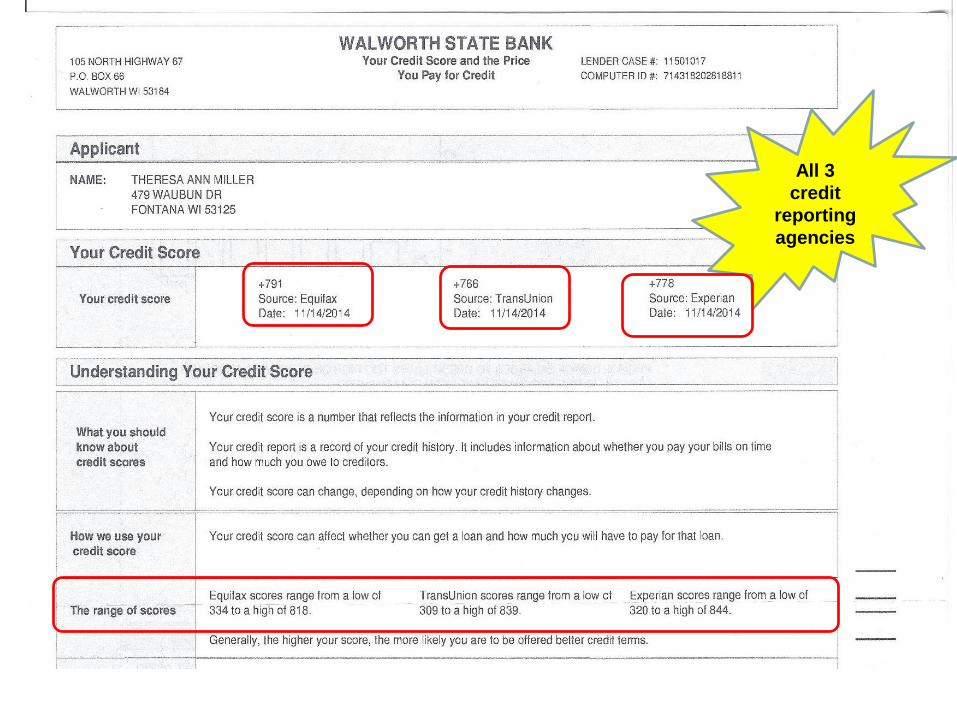

There are 3 authorized credit bureaus:

1. Trans Union

2. Equifax

3. Experian

All 3

credit

reporting

agencies

You have the

right to 1 free

credit report

every year

from each

agency.

40 Million Mistakes: Is your credit report

accurate?

Click on the picture below to view the video.

Your Credit Report

The only

FREE way to

get your

credit

report.

The Equal Credit

Opportunity Act (ECOA)

ensures that all consumers

are given an equal chance

to obtain credit. This

doesn’t mean all

consumers who apply

for credit get it.

Equal Credit

Opportunity Act

Factors such as income, expenses, debt, and credit history are considerations for

credit worthiness.

Equal Credit Opportunity Act

Consumers cannot be denied credit because of:

Gender, marital status (widowed, separated, divorced,

single, married), age, race, national origin, because

they receive public assistance income (welfare), or

because they do or do not have children or how many

children they have.

Consumers can be denied credit because of:

1.Low income

2.Large current debts

3.Poor record of payments in the past

End of Questions?

Discussion Activity: Evaluate Credit Applicants

Directions: Each applicant

described on the next two

pages has applied for a $4,000

loan to purchase a more fuel-

efficient car.

Imagine you are a loan officer at the bank, and you must

decide whether to approve or deny loans for each of the

four applicants. You have been given five pieces of

information about each applicant. Using this information,

evaluate each applicant’s ability and willingness to repay

(use the 5 C’s of credit) and make the “best” decision you

can. Approve or Deny each applicant. Consider the ECOA

law in making your decision. Explain your answers in a

discussion.

Credit Applicants

Applicant 1

1. Has 10 open charge

accounts

2. Address has not

changed for 5 years.

3. Has 6 children

4. 62 years old.

5. Owns stock.

Applicant 2

1. Annual income of

$25,000

2. Caucasian

3. Behind on paying

installment loan

4. Owns or is buying a

home

5. Has an overdrawn

checking account.

Credit Applicants

Applicant 3

1. Receives a welfare

check (money from the

government) each month

2. Divorced

3. Pays bills on time

4. Works part time

5. Female

Applicant 4

1. 21 years old

2. Has no credit history

3. Has been at present job

for 10 months

4. Has a savings account

5. Mexican-American

End of Questions?

Learning Targets

After you have completed this unit, you

will be able to:

1. Explain what to do if you are having

credit problems.

Credit Problems

What can you do when you have a credit problem

or when you’ve gone too far in your use of credit?

If you can’t make your credit payments the first

thing you should do is contact the creditor and

explain the situation to them. They may be able to

work out a plan that will make your payments

easier. (They may even stop charging interest).

Credit Counseling

Credit Counselors help consumers with their credit

problems.

They can help you revise your budget, contact

creditors to arrange new payment plans, or help

you find other sources of income.

Consolidating Debts

A consolidation loan combines all your debts into

one loan with lower payments.

Monthly Credit Payments

Kohls $50.00

Shell $75.00

Menards $100.00

Target $60.00

Visa $325.00

Master Card $180.00

Total $790.00

Interest on these credit payments

ranges from 10-20%. Current balance

to pay off all this credit is $7500.00.

You can go to a bank and get a personal loan for

$7500 at a lower interest rated and pay off all these

creditors. Your bank monthly payment should be

much lower than the total for all these creditors.

Bankruptcy

The last resort is to declare bankruptcy.

This is a legal process in which you either

pay back your debts on a timed schedule or

don’t pay back your debts at all.

You should get an attorney that specializes

in bankruptcy cases. You will have to pay a

fee to the attorney and to file the proper

documents at the federal court .

Bankruptcy A federal judge will decide any of the following:

1. You pay back the debts in smaller amounts

which will take a longer period of time.

2. You do not pay back certain debts (complete

relief).

3. You give up (sell if necessary) your personal

assets, such as a car, savings, or business and

give the money to the creditors.

REMEMBER: You must pay back your student

loan.

Bankruptcy stays

on your credit

report 7-10 years.

End of Questions?