Embed Size (px)

DESCRIPTION

Consumer Credit Vehicle Finance. Ruy M. Abreu Executive Director Banco Itaú. August 25 th 2003. Vehicle Finance Market. Banco Itaú and the Logic behind the Acquisitions of Fináustria and Fiat. Vehicle Financing Operation. Fiat “Consortium”. Acquisitions’ Synergies. - PowerPoint PPT Presentation

Citation preview

1

Consumer CreditVehicle Finance

August 25th 2003

Ruy M. Abreu Executive Director

Banco Itaú

2

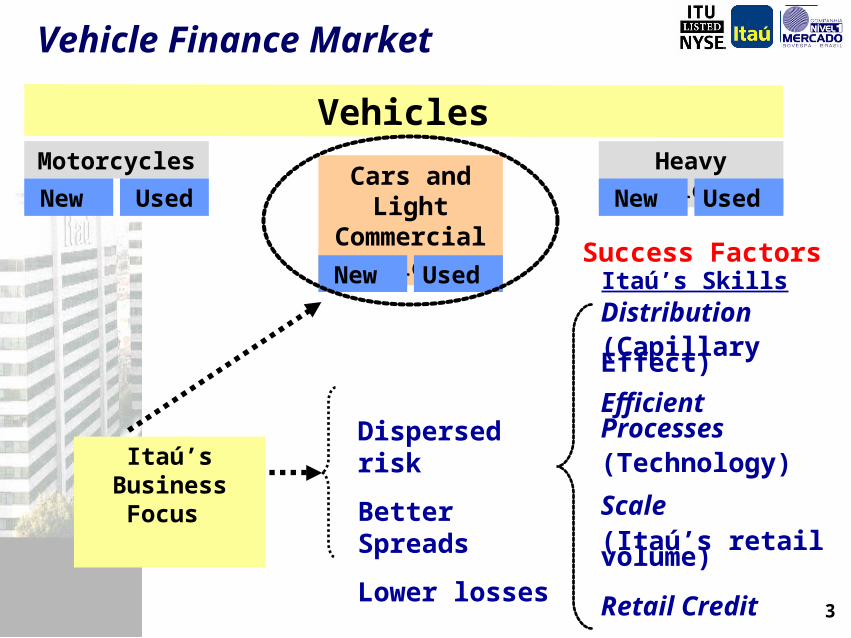

Vehicle Finance Market

Banco Itaú and the Logic behind the Acquisitions of Fináustria and Fiat

Acquisitions’ Synergies

Fiat “Consortium”

Vehicle Financing Operation

3

VehiclesMotorcycles Heavy Vehicles

Cars and Light Commercial

Vehicles

New Used

New Used

New Used

Itaú’s Business Focus

Dispersed risk

Better Spreads

Lower losses

Distribution(Capillary Effect)

Efficient Processes(Technology)

Scale(Itaú’s retail volume)

Retail Credit

(Itaú’s Customer Base)

Success FactorsItaú’s Skills

Vehicle Finance Market

4

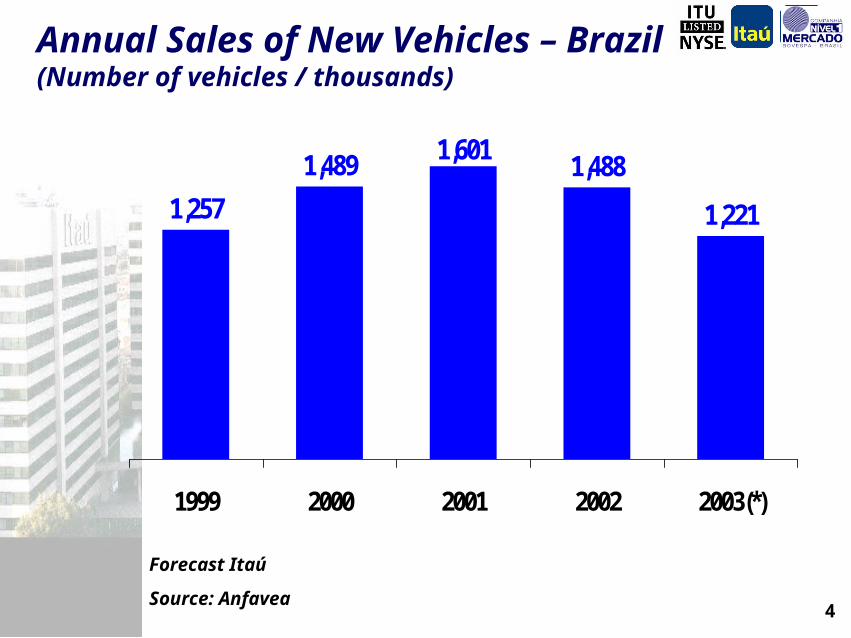

Forecast Itaú

Source: Anfavea

1,257

1,489 1,6011,488

1,221

1999 2000 2001 2002 2003(*)

Annual Sales of New Vehicles – Brazil(Number of vehicles / thousands)

5

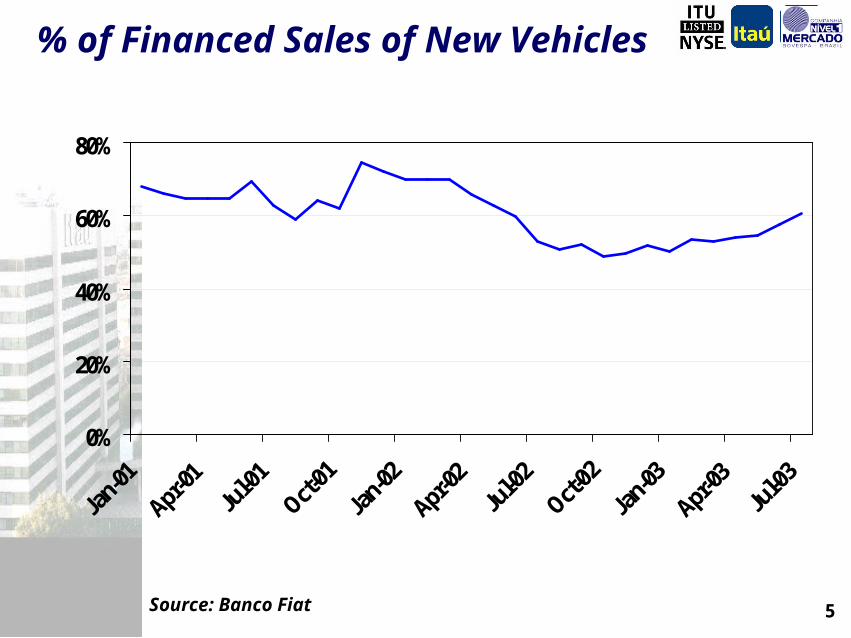

% of Financed Sales of New Vehicles

Source: Banco Fiat

0%

20%

40%

60%

80%

Jan-01

Apr-01

Jul-0

1

Oct-01

Jan-02

Apr-02

Jul-0

2

Oct-02

Jan-03

Apr-03

Jul-0

3

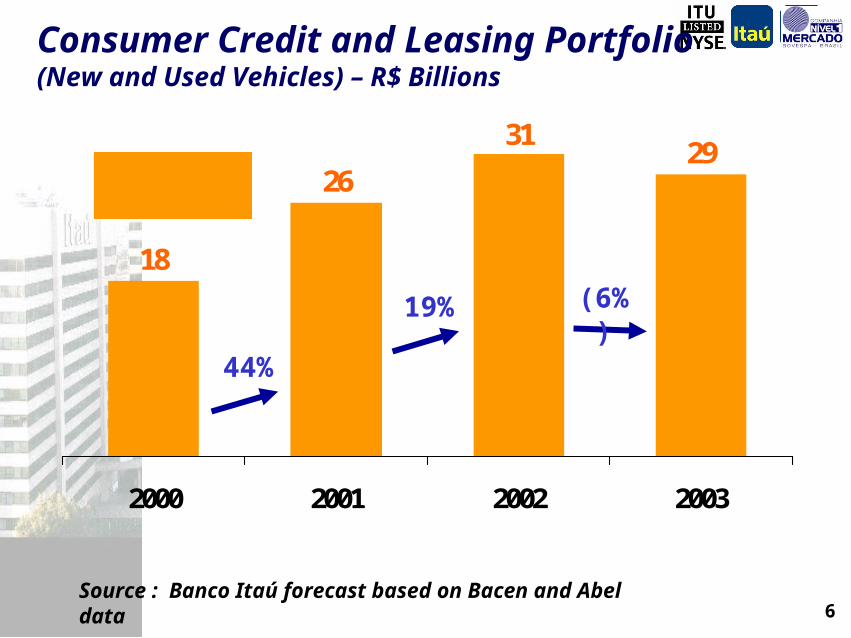

6

18

26

3129

2000 2001 2002 2003

Source : Banco Itaú forecast based on Bacen and Abel data

Consumer Credit and Leasing Portfolio (New and Used Vehicles) – R$ Billions

44%

19% (6%)

CAGR = 12.7%

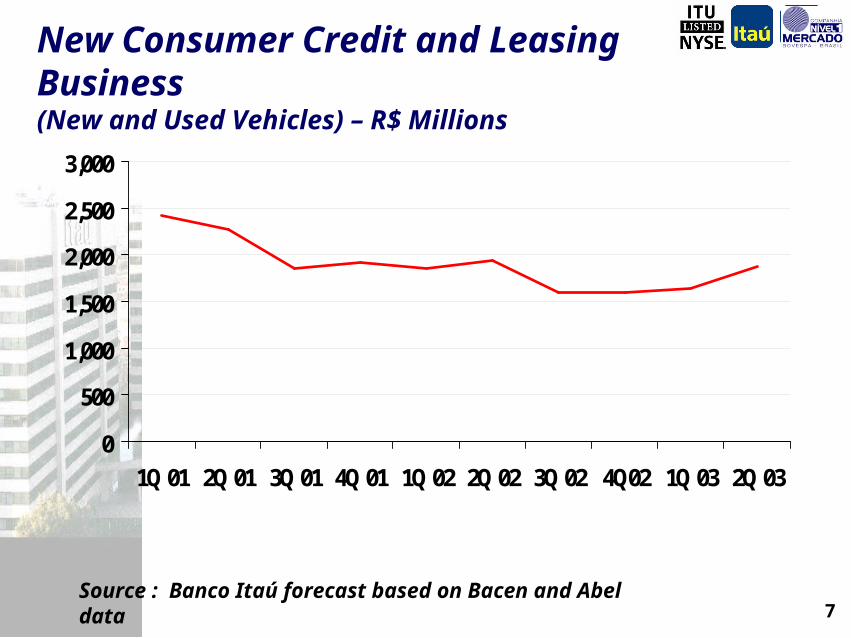

7Source : Banco Itaú forecast based on Bacen and Abel data

New Consumer Credit and Leasing Business(New and Used Vehicles) – R$ Millions

0

500

1,000

1,500

2,000

2,500

3,000

1Q 01 2Q 01 3Q 01 4Q 01 1Q 02 2Q 02 3Q 02 4Q02 1Q 03 2Q 03

8

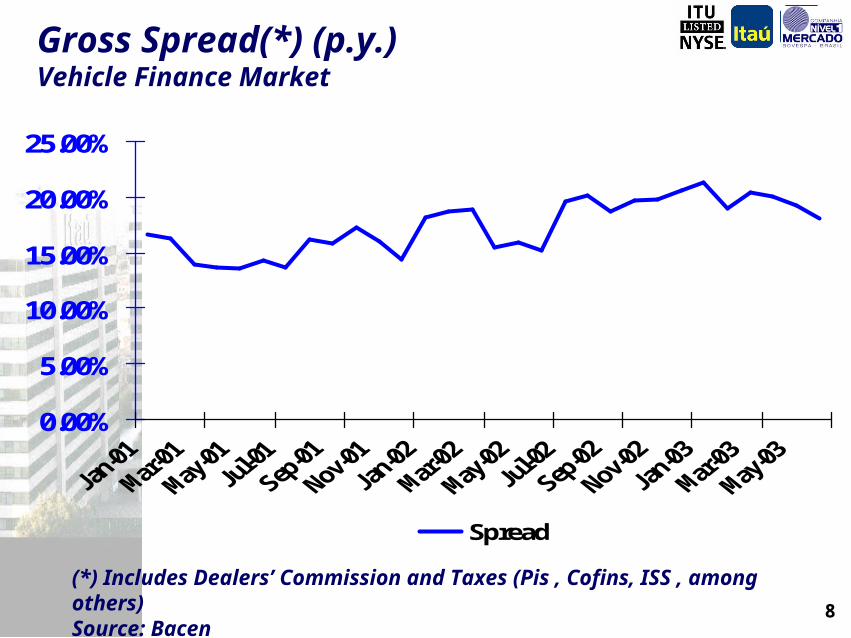

(*) Includes Dealers’ Commission and Taxes (Pis , Cofins, ISS , among others)Source: Bacen

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

Spread

Gross Spread(*) (p.y.)Vehicle Finance Market

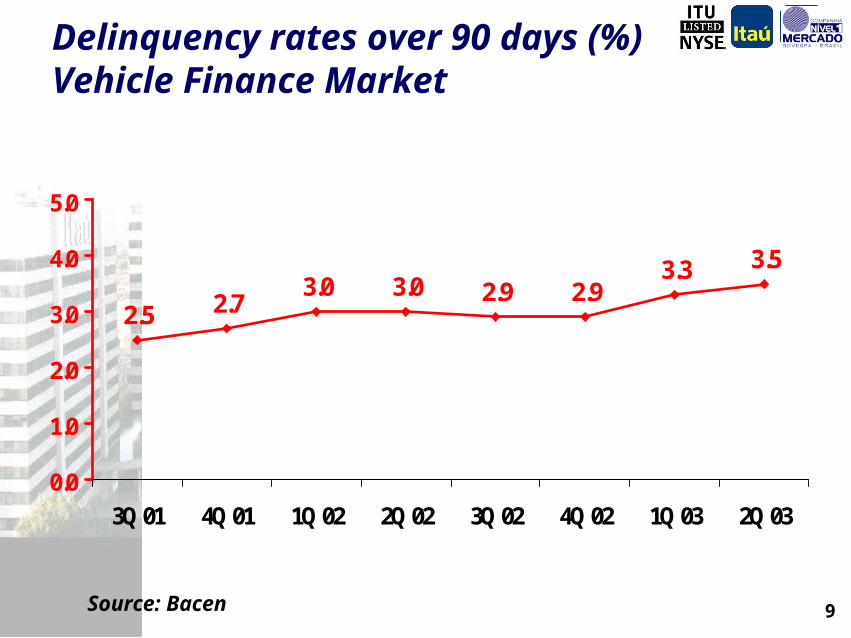

9

2.5 2.73.0 3.0 2.9 2.9

3.3 3.5

0.0

1.0

2.0

3.0

4.0

5.0

3Q 01 4Q 01 1Q 02 2Q 02 3Q 02 4Q 02 1Q 03 2Q 03

Source: Bacen

Delinquency rates over 90 days (%)Vehicle Finance Market

10

Vehicle Finance Market

Banco Itaú and the Logic behind the Acquisitions of Fináustria and Fiat

Acquisitions’ Synergies

Fiat “Consortium”

Vehicle Finance Operation

11

4.5 5.0 5.6 5.6 5.6

3.5 3.5

7.0

1Q 00 1Q 01 1Q 02 Dec 2002(1) Mar 2003(2)

Itaú Fináustria Fiat

Source : Banco Itaú forecasts based on Bacen , Abel , Itaú, Fiat and Fináustria data

In %

9.0

16.0

(1) Acquisition of Fináustria CFI(2) Acquisição of Banco Fiat

Itaú’s Market Share Consumer Credit and Vehicle Leasing Market

12

Bahia

Minas GeraisGoiás

Rio de JaneiroEspírito Santo

Paraná

Santa Catarina

São PauloBrasília

Rio Grande do Sul

Mato Grosso do Sul

Mato Grosso

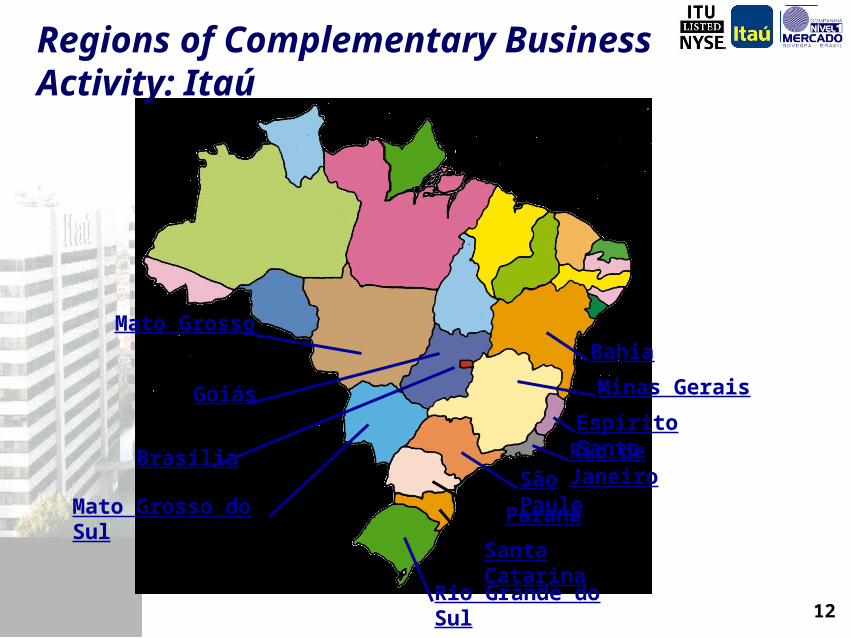

Regions of Complementary Business Activity: Itaú

13

CearáCearáRio Grande do NorteRio Grande do Norte

ParaíbaParaíbaPernambucoPernambuco

BahiaBahia

Minas GeraisMinas GeraisGoiásGoiás

Rio de JaneiroRio de JaneiroEspírito SantoEspírito Santo

ParanáParaná

Santa CatarinaSanta Catarina

São PauloSão PauloBrasíliaBrasília

Rio Grande do SulRio Grande do Sul

Mato Grosso do SulMato Grosso do Sul

MaranhãoMaranhão

Mato GrossoMato Grosso

PiauíPiauí

SergipeSergipeAlagoasAlagoas

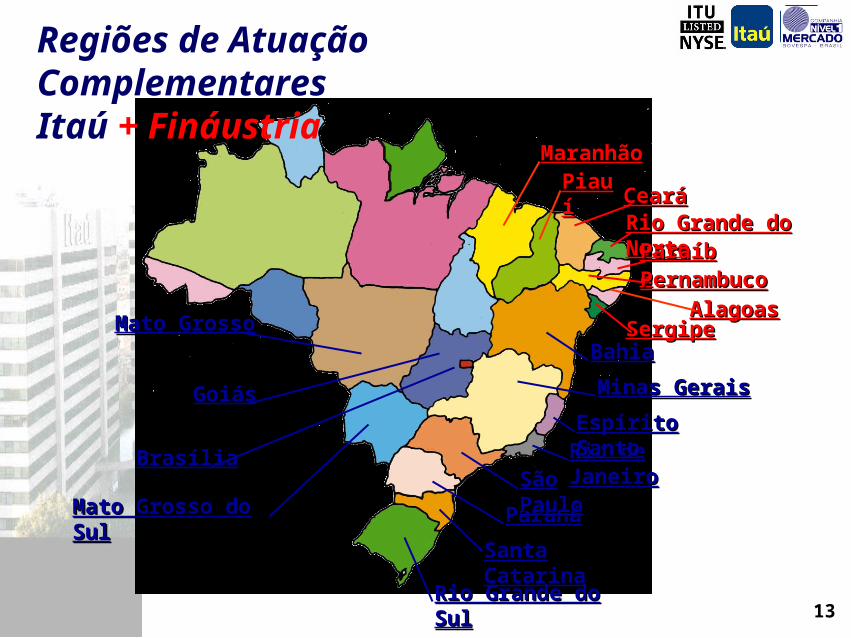

Regiões de Atuação Complementares Itaú + Fináustria

14

CearáCeará

Rio Grande do NorteRio Grande do Norte

ParaíbaParaíbaPernambucoPernambuco

BahiaBahia

Minas GeraisMinas GeraisGoiásGoiás

Rio de JaneiroRio de Janeiro

Espírito SantoEspírito Santo

ParanáParaná

Santa CatarinaSanta Catarina

São PauloSão PauloBrasíliaBrasília

Rio Grande do SulRio Grande do Sul

Mato Grosso do SulMato Grosso do Sul

MaranhãoMaranhão

Mato GrossoMato Grosso

PiauíPiauí

SergipeSergipe

AmazonasAmazonas

RoraimaRoraima ParáPará AmapáAmapá

RondôniaRondônia

AlagoasAlagoasAcreAcre

TocantinsTocantins

Regions of Complementary Business Activity:Itaú + Fináustria + Fiat

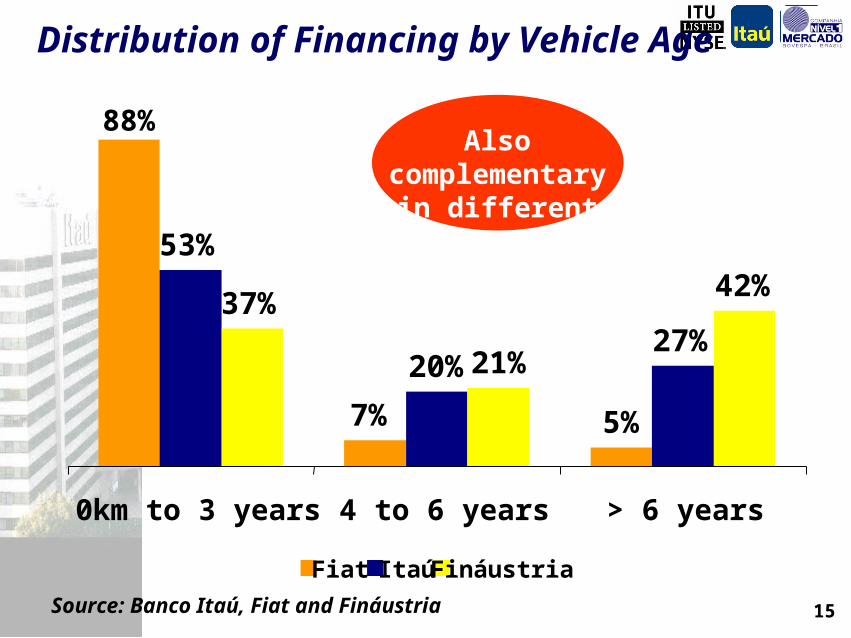

15Source: Banco Itaú, Fiat and Fináustria

Distribution of Financing by Vehicle Age

88%

7% 5%

53%

20%27%

37%

21%

42%

0km to 3 years 4 to 6 years > 6 years

Fiat Itaú Fináustria

Also complementary in different types of

market

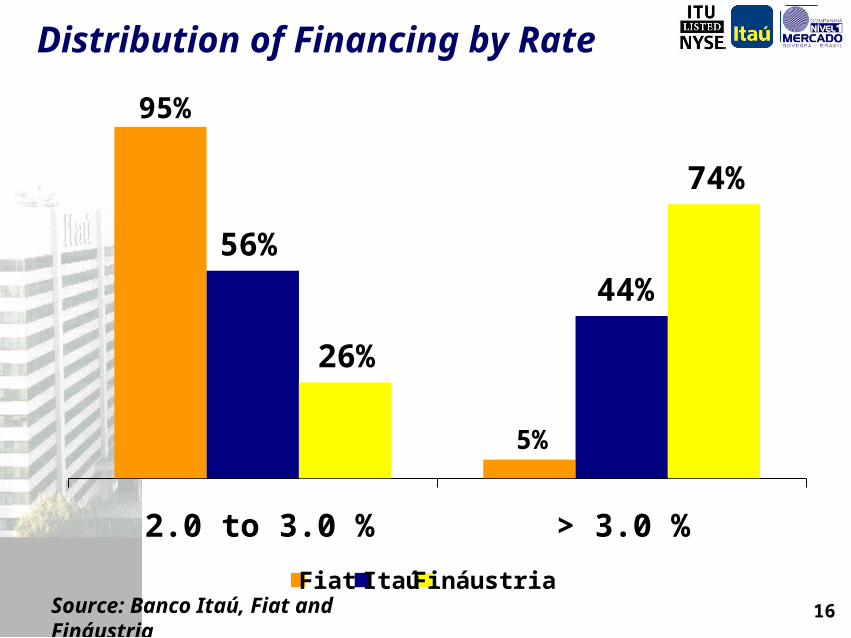

16Source: Banco Itaú, Fiat and Fináustria

Distribution of Financing by Rate

95%

5%

56%

44%

26%

74%

2.0 to 3.0 % > 3.0 %

Fiat Itaú Fináustria

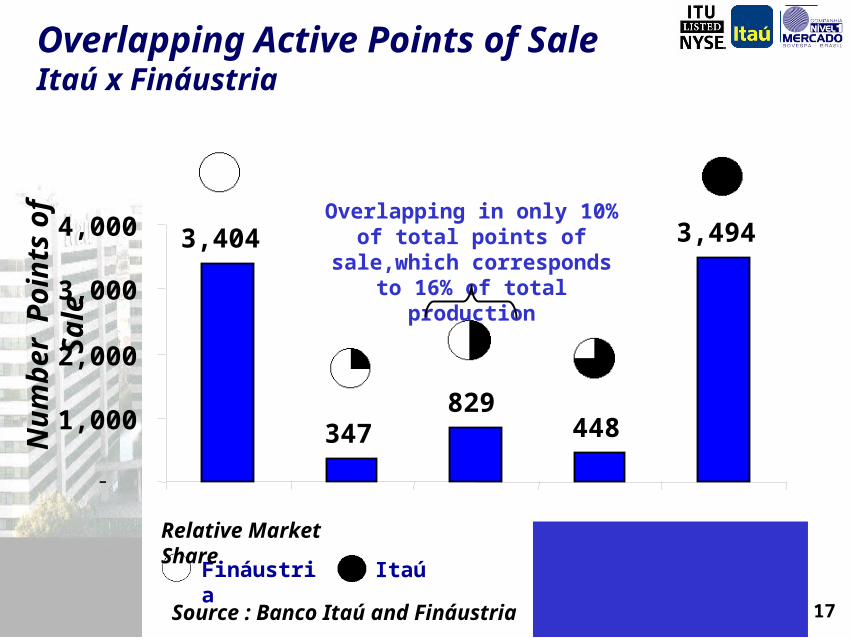

17

Num

ber

Poin

ts o

f Sal

e

Fináustria Itaú

Relative Market Share

3,404

347829

448

3,494

-

1,000

2,000

3,000

4,000Overlapping in only 10% of total

points of sale,which corresponds to 16% of total production

Source : Banco Itaú and Fináustria

Overlapping Active Points of SaleItaú x Fináustria

Banco Fiat: active overlapping points of sale

irrelevant

18

Vehicle Finance Market

Banco Itaú and the Logic behind the Acquisitions of Fináustria and Fiat

Acquisitions’ Synergies

Fiat “Consortium”

Vehicle Financing Operation

19

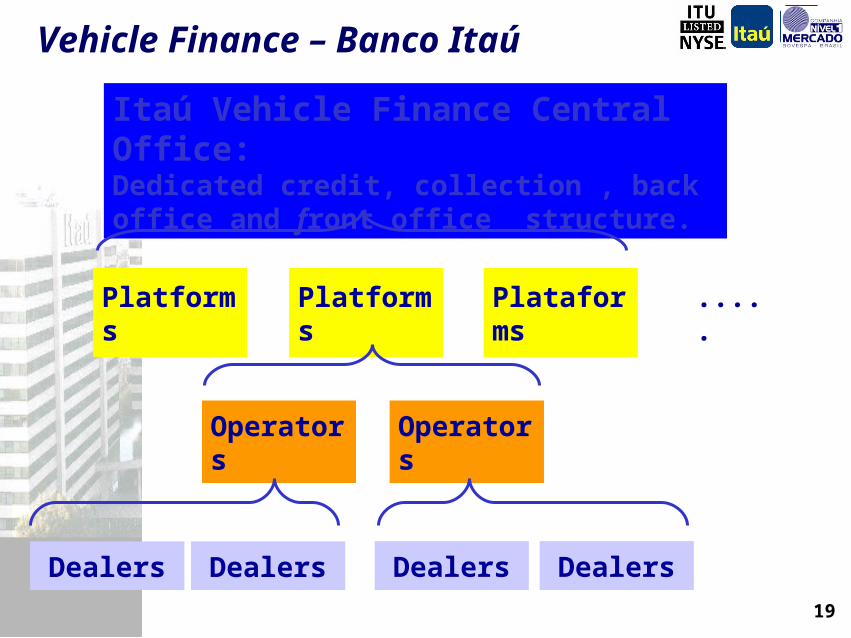

Itaú Vehicle Finance Central Office: Dedicated credit, collection , back office and front office structure.

Platforms Platforms Plataforms .....

Operators Operators

Dealers Dealers Dealers Dealers

Vehicle Finance – Banco Itaú

20Source : Banco Itaú, Fiat and Fináustria

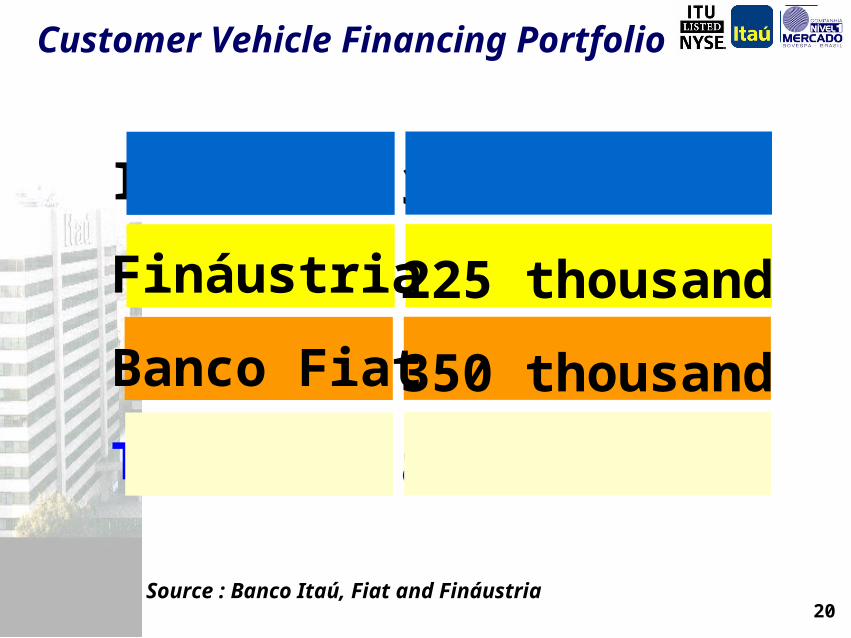

Customer Vehicle Financing Portfolio

ITAÚ

Fináustria

Banco Fiat

TOTAL

325 thousand

225 thousand

350 thousand

895 thousand

21

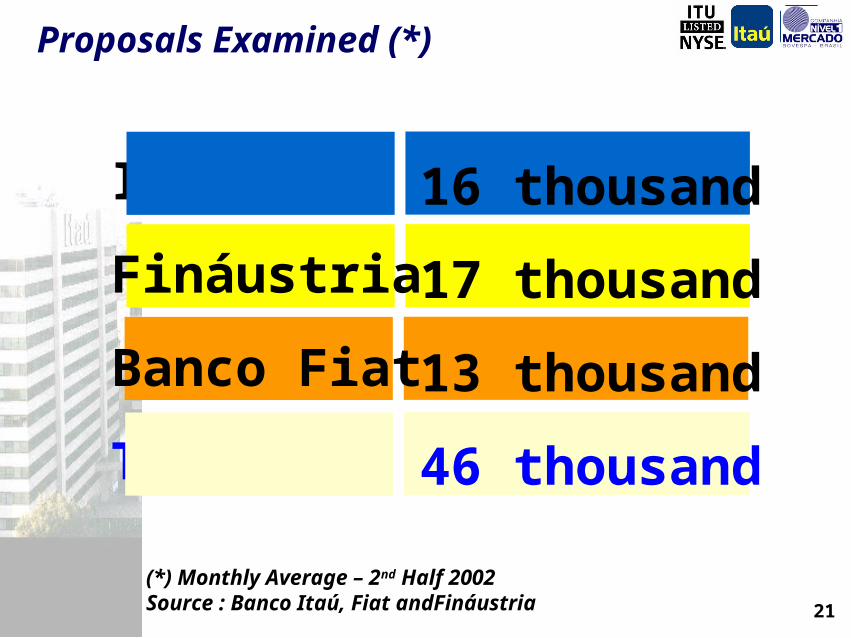

Proposals Examined (*)

ITAÚ

Fináustria

Banco Fiat

TOTAL

16 thousand

17 thousand

13 thousand

46 thousand

(*) Monthly Average – 2nd Half 2002Source : Banco Itaú, Fiat andFináustria

22

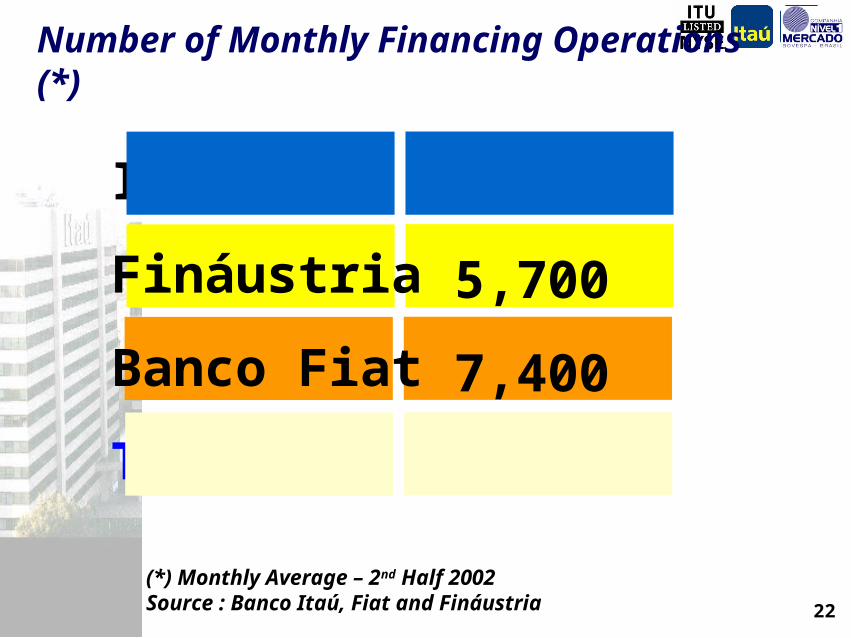

(*) Monthly Average – 2nd Half 2002Source : Banco Itaú, Fiat and Fináustria

Number of Monthly Financing Operations (*)

ITAÚ

Fináustria

Banco Fiat

TOTAL

7,500

5,700

7,400

20,600

23

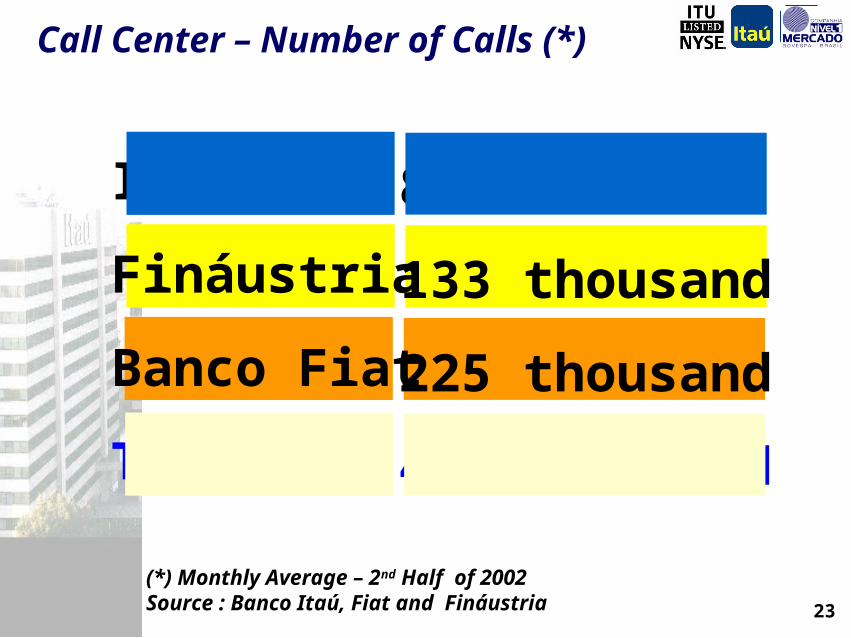

Call Center – Number of Calls (*)

ITAÚ

Fináustria

Banco Fiat

TOTAL

83 thousand

133 thousand

225 thousand

448 thousand

(*) Monthly Average – 2nd Half of 2002Source : Banco Itaú, Fiat and Fináustria

24

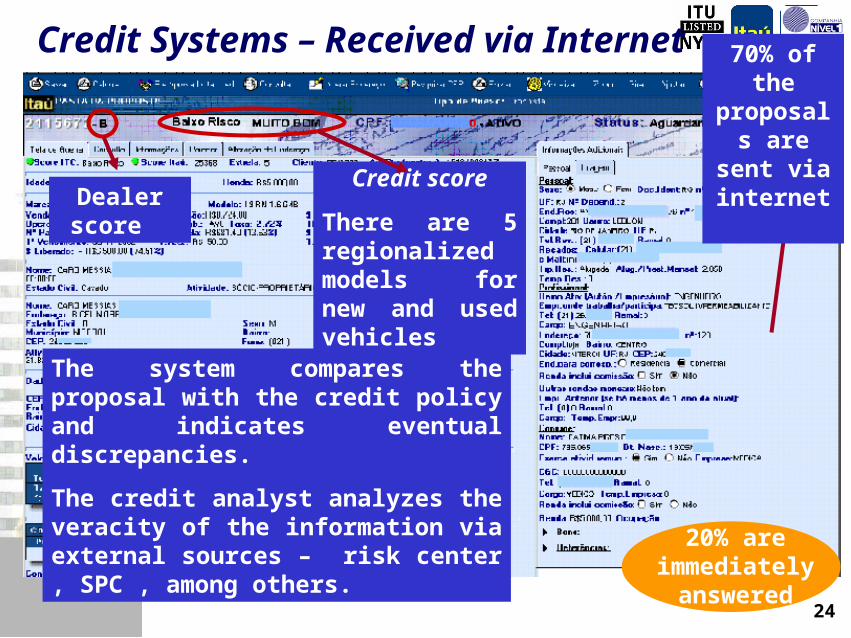

Credit score

There are 5 regionalized models for new and used vehicles

The system compares the proposal with the credit policy and indicates eventual discrepancies.

The credit analyst analyzes the veracity of the information via external sources – risk center , SPC , among others.

Dealer score

70% of the proposals

are sent via internet

Credit Systems – Received via Internet

20% are immediately

answered

25

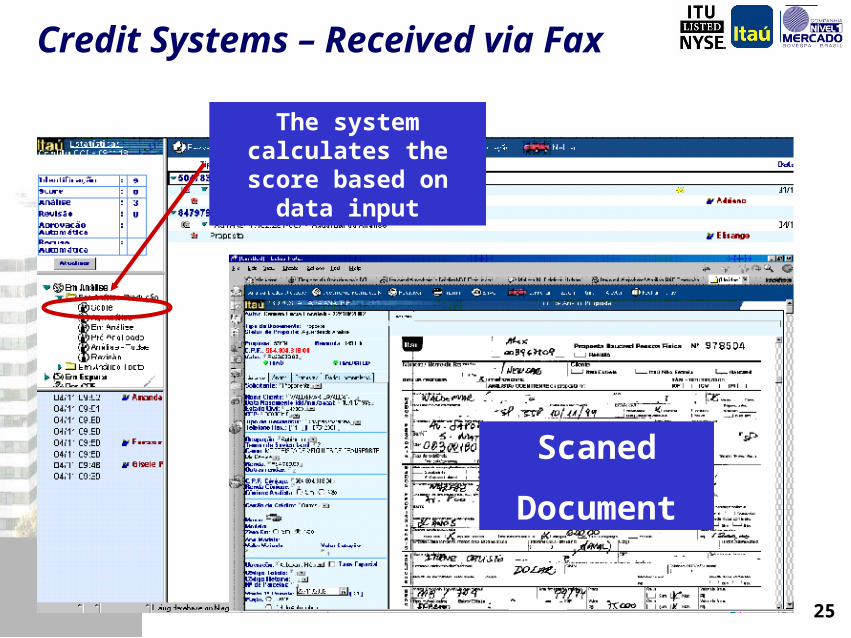

The system calculates the score based on data input

Credit Systems – Received via Fax

Scaned

Document

26

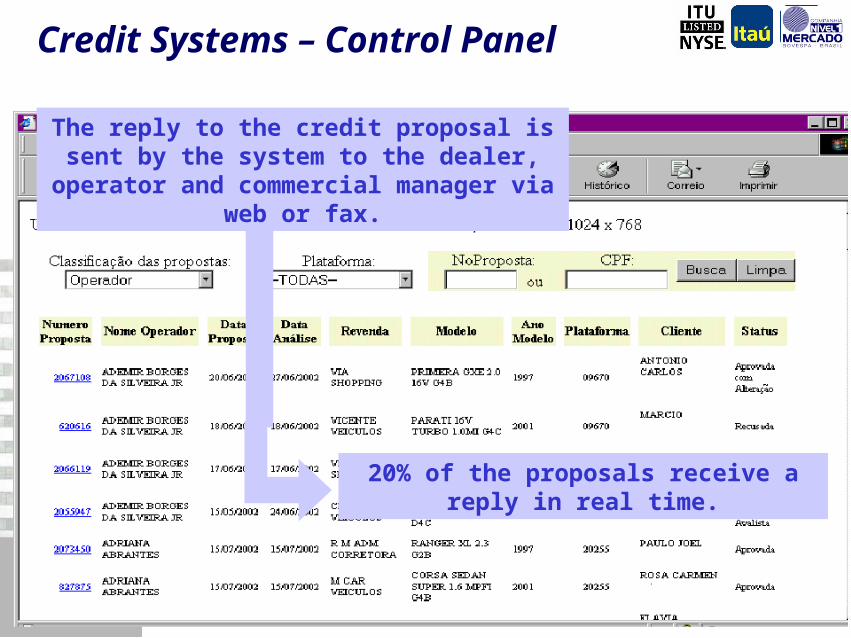

The reply to the credit proposal is sent by the system to the dealer, operator and commercial manager via

web or fax.

20% of the proposals receive a reply in real time.

Credit Systems – Control Panel

27

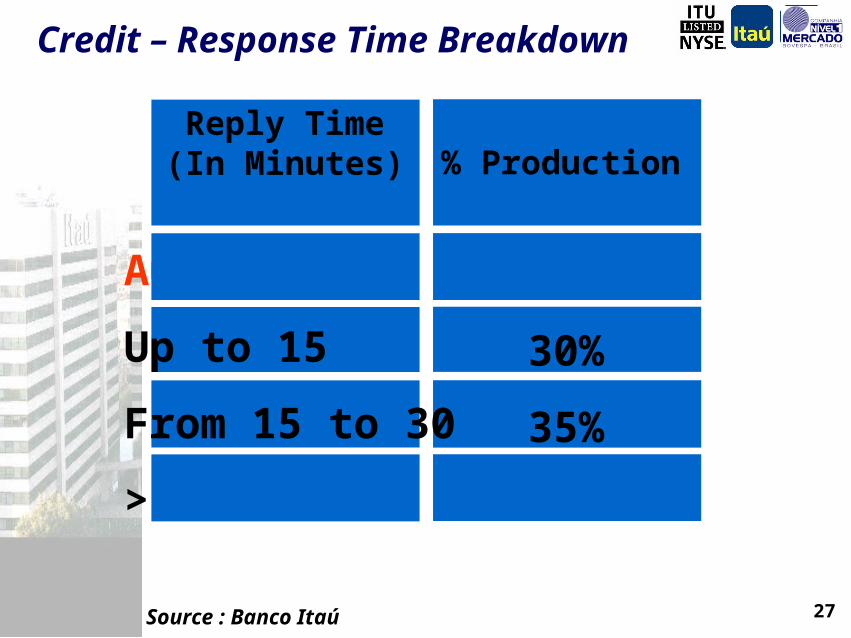

Credit – Response Time Breakdown

Automatic

Up to 15

From 15 to 30

> 30

20%

30%

35%

15%

Source : Banco Itaú

Reply Time(In Minutes) % Production

28

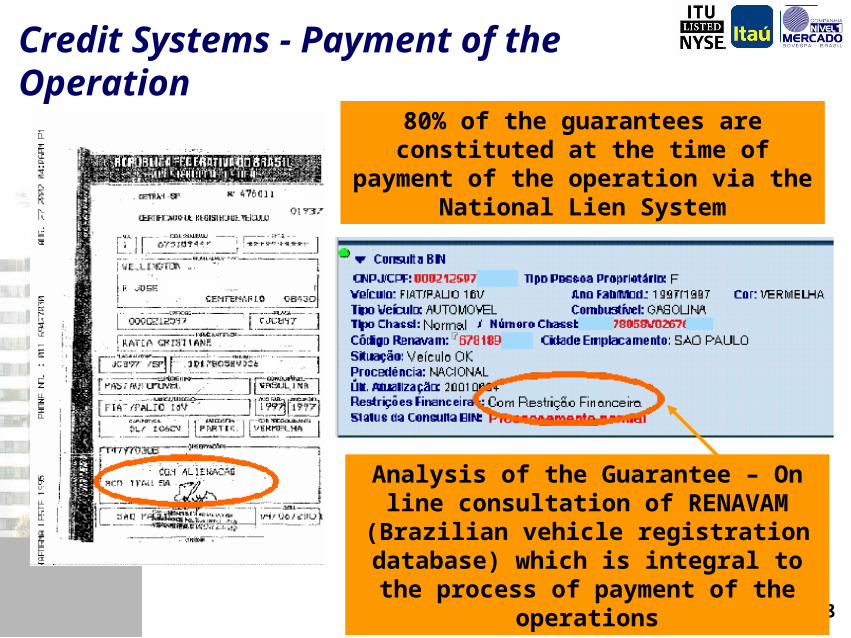

80% of the guarantees are constituted at the time of payment of the operation via the National Lien

System

Credit Systems - Payment of the Operation

Analysis of the Guarantee – On line consultation of RENAVAM (Brazilian vehicle registration

database) which is integral to the process of payment of the operations

29

Back office system for this operation was established based on the factory

concept using the technology employed in the processing of bulk volumes for the

Itaú Branch Network

Back Office – Digitalization of Documents

30

Vehicle Finance Market

Banco Itaú and the Logic behind the Acquisitions of Fináustria and Fiat

Acquisitions’ Synergies

Fiat “Consortium”

Vehicle Financing Operation

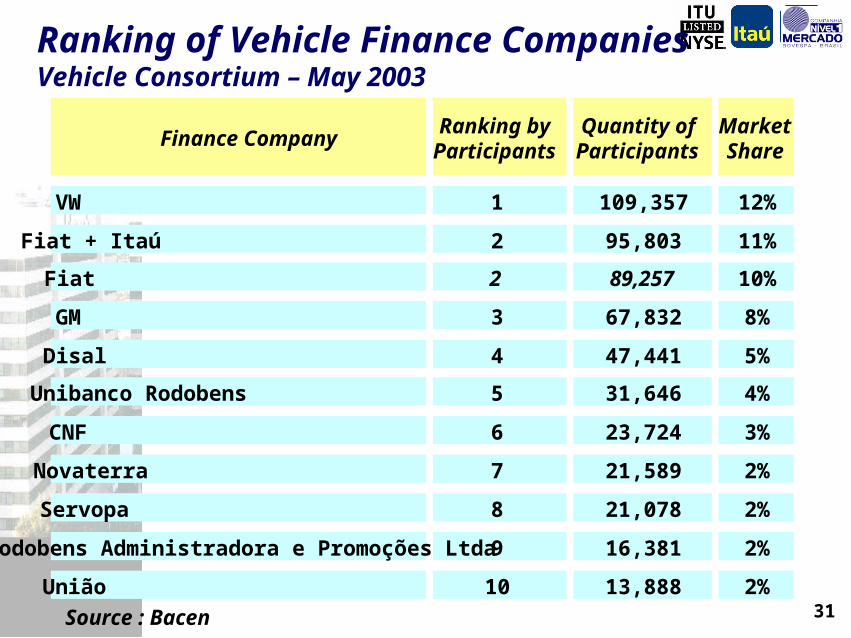

31Source : Bacen

Ranking of Vehicle Finance Companies Vehicle Consortium – May 2003

Finance CompanyRanking by Participants

Quantity of Participants

Market Share

VW 1 109,357 12%

Fiat + Itaú 2 95,803 11%

Fiat 2 89,257 10%

GM 3 67,832 8%

Disal 4 47,441 5%

Unibanco Rodobens 5 31,646 4%

CNF 6 23,724 3%

Novaterra 7 21,589 2%

Servopa 8 21,078 2%

Rodobens Administradora e Promoções Ltda 9 16,381 2%

União 10 13,888 2%

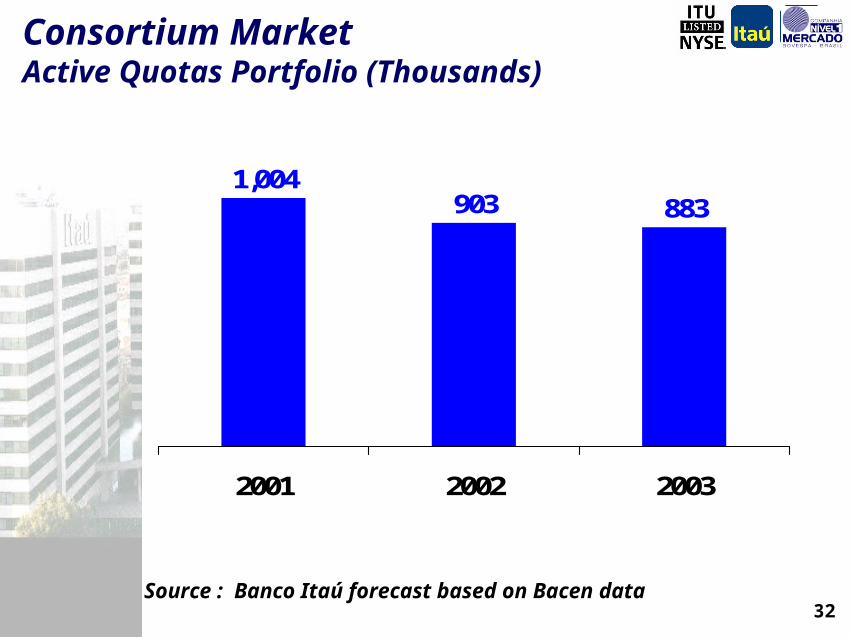

32Source : Banco Itaú forecast based on Bacen data

Consortium Market Active Quotas Portfolio (Thousands)

1,004903 883

2001 2002 2003

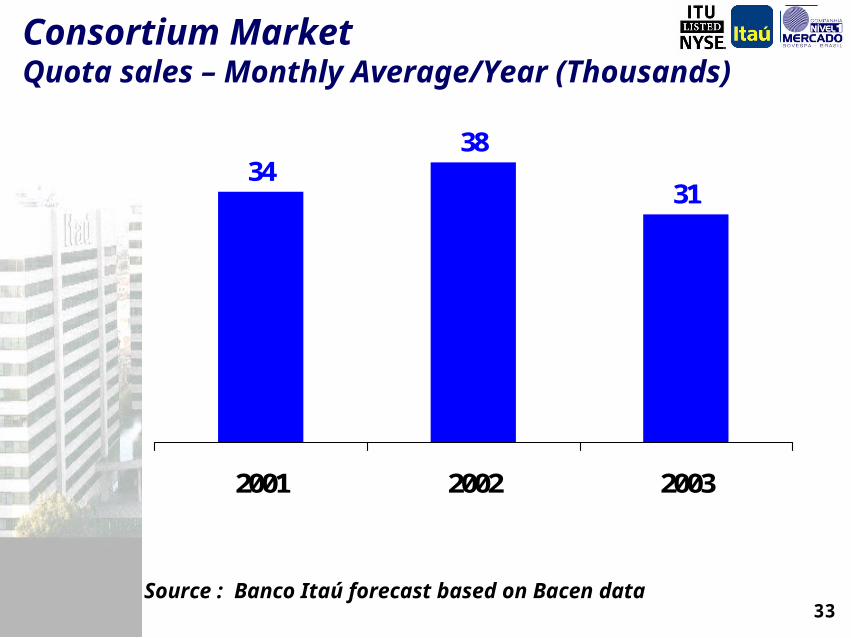

33Source : Banco Itaú forecast based on Bacen data

Consortium Market Quota sales – Monthly Average/Year (Thousands)

3438

31

2001 2002 2003

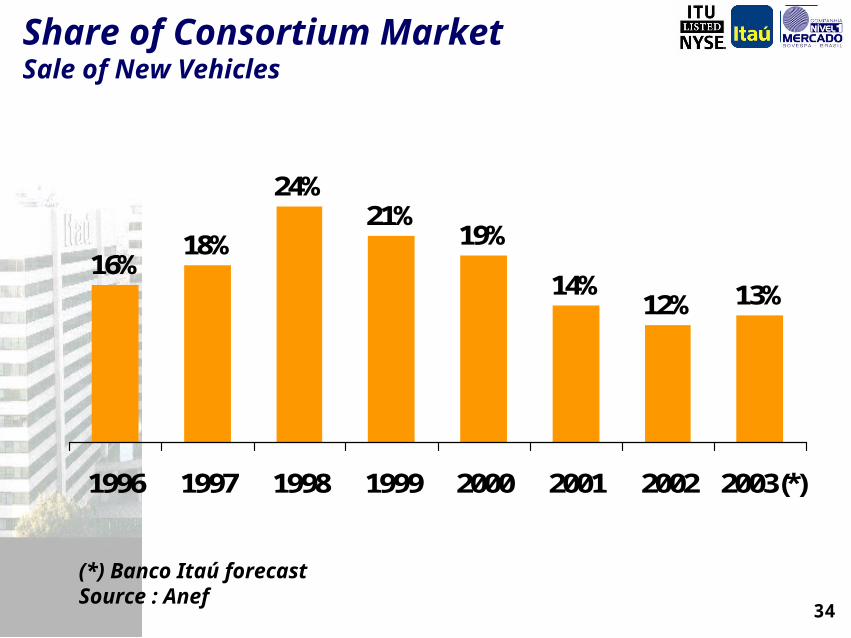

34

(*) Banco Itaú forecastSource : Anef

Share of Consortium MarketSale of New Vehicles

16%18%

24%21%

19%

14%12% 13%

1996 1997 1998 1999 2000 2001 2002 2003(*)

35

Vehicle Finance Market

Banco Itaú and the Logic behind the Acquisitions of Fináustria and Fiat

Acquisitions’Synergies

Fiat “Consortium”

Vehicle Finance Operation

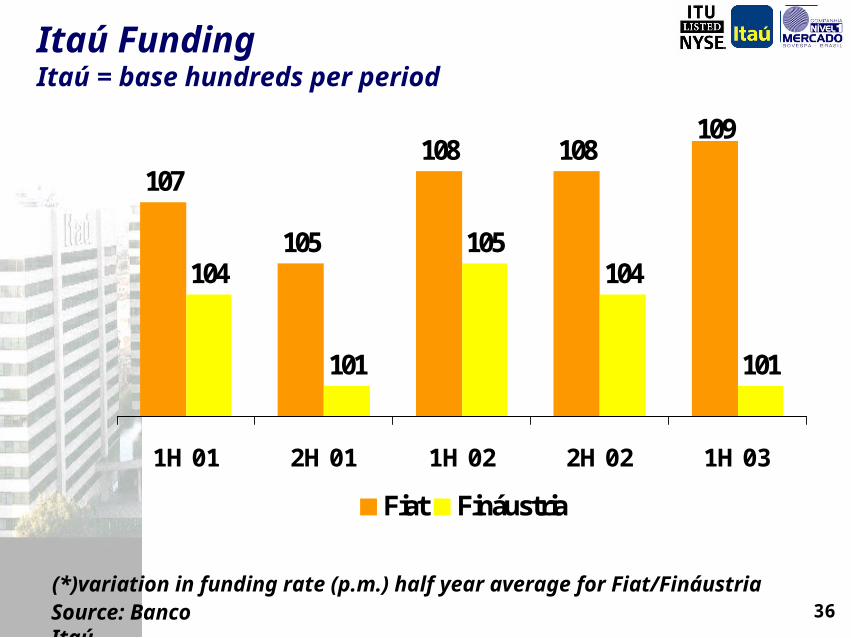

36(*)variation in funding rate (p.m.) half year average for Fiat/FináustriaSource: Banco Itaú

107

105

108 108109

104

101

105104

101

1H 01 2H 01 1H 02 2H 02 1H 03

Fiat Fináustria

Itaú FundingItaú = base hundreds per period

37

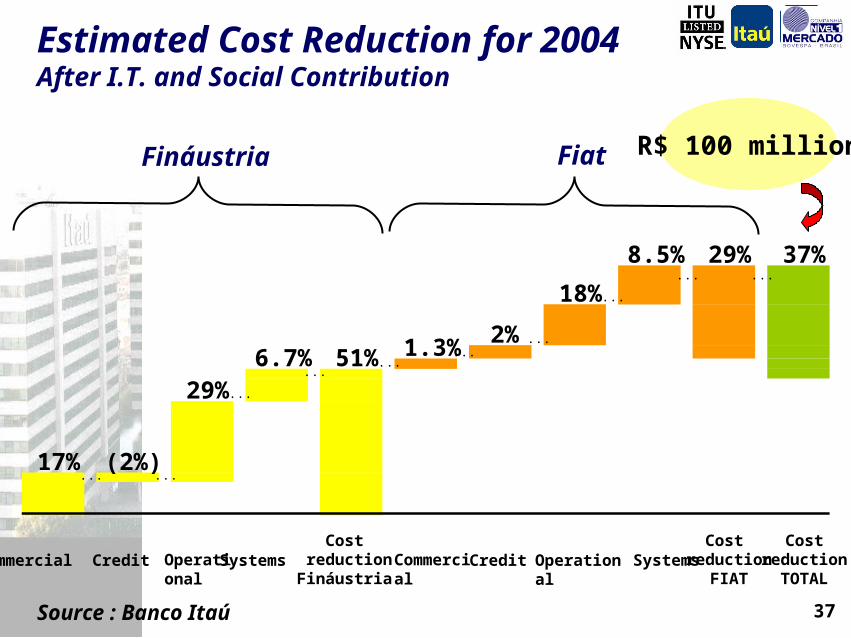

R$ 100 million

8.5% 29% 37%... ...

18% ...

......

......

29% ...

17% (2%)... ...

51%6.7% 1.3% 2%

Commercial Credit Operational Systems Cost

reductionFináustria

Commercial

Credit Operational

Systems

Cost reduction

FIAT

Costreduction

TOTAL

Fináustria Fiat

Source : Banco Itaú

Estimated Cost Reduction for 2004After I.T. and Social Contribution

38

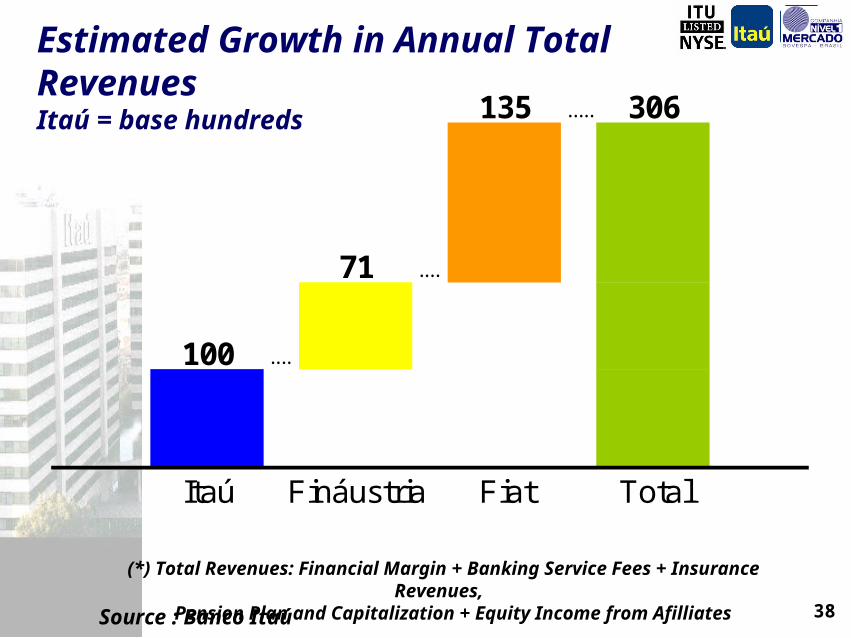

135 ..... 306

71 ....

100 ....

Itaú Fináustria Fiat Total

Source : Banco Itaú

Estimated Growth in Annual Total RevenuesItaú = base hundreds

(*) Total Revenues: Financial Margin + Banking Service Fees + Insurance Revenues, Pension Plan and Capitalization + Equity Income from Afilliates

39

Consumer CreditVehicle Finance

August 25th 2003

Ruy M. Abreu Executive Director

Banco Itaú