Embed Size (px)

Citation preview

Consumer Connection Beverage Market Insight To Taiwan Beverage Industries Association

Paul Wu, Joy Lin

Kantar Worldpanel Taiwan, Dec-10

1

FAST FACTS

WHO WE ARE

Our status TNS Worldpanel Our previous name

Kantar Group WPP’s Information, Insight & Consultancy group

2

EXPERT IN FMCG ACROSS ASIA AND THE WORLD

OUR COVERAGE IN ASIA

Japan (Marketing collaboration with

INTAGE)

Taiwan

Thailand

Malaysia

South Korea

China

Philippines

* including partners

Indonesia

Vietnam

India (IMRB)

3

Methodology Introduction

WHAT WE DO

4

DEFINITION A UNIQUE PORTFOLIO

CONSUMER PANEL INTRODUCTION KANTAR WORLDPANEL

*An average 20% annual replacement allows panel to

accurately reflect actual population changes.

** i.e. Actual real consumer’s purchases

5

KANTAR WORLDPANEL BEVERAGE PANEL

˃ Since 2006

˃ Sample size: 5,000 individuals

˃ From age 15-55 years old

˃ Universe: 14,000,000 Taiwan consumers

˃ Gender

˃ Age

˃ Region

˃ HH income

˃ Habitat size & People in the HH

˃ Data collection: Every week by diary or on-line

˃ Category: Dairy, Beverage ( package and takeaway)

6

YOU WILL KNOW…..

HOW DOES TAKEAWAY DRINKS IMPACT PACKAGE BAVERAGE?

WHAT MAKES A BRND GROW?

SHOULD I INVEST IN COSTCO OR eCOMMERCE?

DYNAMICS OF BEVERAGE CATEGORIES, WIN OR LOSE & WHY?

HOW IS TAIWAN 14Q1 FMCG FORECAST?

8

TAIWAN FMCG MARKET

OVERVIEW

9

L Low Inflation/Unemployment/GDP Growth

Food Safety incidents cause short term decline

Food market keeps growing

Taiwan Macro Economy Status

Relatively stable in long term

10

08

Q4

09

Q1

09

Q2

09

Q3

09

Q4

10

Q1

10

Q2

10

Q3

10

Q4

11

Q1

11

Q2

11

Q3

11

Q4

12

Q1

12

Q2

12

Q3

12

Q4

13

Q1

13

Q2

13

Q3

GDP Foods $ growth

2011 Plasticizer Incidence (DEPH) 2008 Sep.

Melamine (Milk scandal)

2013 May 毒澱粉

2013 Sep Cooking Oil

FOOD SAFETY INCIDENCE WAS THE MAIN CAUSE TO SLOW DOWN THE FOOD

MARKET GROWTH, OR EVEN LED DECLINE FOR THE VOLUME DEMAND.

11

TAIWAN FOOD CATEGORY (W/O CIGARETTE & ALCOHOL) GETTING FLAT

RECENTLY DUE TO UNCERTAINTY

0

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

4,500,000

5,000,000

52 w

/e 2

008/0

9/0

752 w

/e 2

008/1

0/0

552 w

/e 2

008/1

1/0

252 w

/e 2

008/1

1/3

052 w

/e 2

008/1

2/2

852 w

/e 2

009/0

1/2

552 w

/e 2

009/0

2/2

252 w

/e 2

009/0

3/2

252 w

/e 2

009/0

4/1

952 w

/e 2

009/0

5/1

752 w

/e 2

009/0

6/1

452 w

/e 2

009/0

7/1

252 w

/e 2

009/0

8/1

652 w

/e 2

009/0

9/1

352 w

/e 2

009/1

0/1

152 w

/e 2

009/1

1/0

852 w

/e 2

009/1

2/0

652 w

/e 2

010/0

1/0

352 w

/e 2

010/0

1/3

152 w

/e 2

010/0

2/2

852 w

/e 2

010/0

3/2

852 w

/e 2

010/0

4/2

552 w

/e 2

010/0

5/2

352 w

/e 2

010/0

6/2

052 w

/e 2

010/0

7/1

852 w

/e 2

010/0

8/1

552 w

/e 2

010/0

9/1

252 w

/e 2

010/1

0/1

052 w

/e 2

010/1

1/0

752 w

/e 2

010/1

2/0

552 w

/e 2

011/0

1/0

252 w

/e 2

011/0

1/3

052 w

/e 2

011/0

2/2

752 w

/e 2

011/0

3/2

752 w

/e 2

011/0

4/2

452 w

/e 2

011/0

5/2

252 w

/e 2

011/0

6/1

952 w

/e 2

011/0

7/1

752 w

/e 2

011/0

8/1

452 w

/e 2

011/0

9/1

152 w

/e 2

011/1

0/0

952 w

/e 2

011/1

1/0

652 w

/e 2

011/1

2/0

452 w

/e 2

012/0

1/0

152 w

/e 2

012/0

1/2

952 w

/e 2

012/0

2/2

652 w

/e 2

012/0

3/2

552 w

/e 2

012/0

4/2

252 w

/e 2

012/0

5/2

052 w

/e 2

012/0

6/1

752 w

/e 2

012/0

7/1

552 w

/e 2

012/0

8/1

252 w

/e 2

012/0

9/0

952 w

/e 2

012/1

0/0

752 w

/e 2

012/1

1/0

452 w

/e 2

012/1

2/0

252 w

/e 2

012/1

2/3

052 w

/e 2

013/0

1/2

752 w

/e 2

013/0

2/2

452 w

/e 2

013/0

3/2

452 w

/e 2

013/0

4/2

152 w

/e 2

013/0

5/1

952 w

/e 2

013/0

6/1

652 w

/e 2

013/0

7/1

452 w

/e 2

013/0

8/1

152 w

/e 2

013/0

9/0

8

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

200,000

Sales Volume(Unit)

Sales Value (NT$M)

NT$M

2008 Sep.

Financial

Crisis

2009 Jan.

Consumer

Voucher

2009 July

Sign of bounce

back

Recovery Grow Stable Recovery Stable

Tainted

Starch

M13Q2 vs M13Q3

Val +1%

Vol +0%

52 WEEKS COMPARISON M12Q3 vs M13Q3

Val +9%

Vol +4%

Cooking

Oil

DEHP

Incidence

Melamine

12

Growth Rate ≤ -0.5% -0.5% <Growth Rate≤ 5% Growth Rate> 5%

Food Category Focus

Non Food Category Focus

Biscuit\snack Health Food RTD Tea Instant Coffee Fresh Milk

Liquid

Detergent

Oral Care Skin Care

(35+)

Toilet Paper

M12Q3 VS M13Q3

FMCG MARKET

13

ANNUAL COMPARISON , VALUE%

TAIWAN FMCG KEY ACCOUNT IMPORTANCE

14 14 14 14 15 15 12

9 8 89

6 6 6

7 6 58 6 6

5 4 4

5 6 7

6 7 8

3 3 3

4 5 5

7 7 7

0 0 0

3 2 2

3 3 3

2 2 2

2 2 2

0 0 0

5 5 5

2 2 2

3 3 3

0 0 0

1 1 1

2 1 1

0 0 0

1 1 1

0 0 0

2 2 2

12 12

910

0

10

20

30

40

50

60

MAT

11Q3

MAT

12Q3

MAT

13Q3

MAT

11Q3

MAT

12Q3

MAT

13Q3

MAT

11Q3

MAT

12Q3

MAT

13Q3

PX Carrefour RT Costco 7 Eleven

A Mart Watson's Family Wellcome Poya

TTL FMCG FOOD CATEGORY NON FOOD CATEGORY

14

0

100

200

300

400

500

600

700

800

900

-10 10 30 50 70 90 110 130

Traffic (in million, Occasions)

Ba

ske

t V

alu

e (

NT

$)

PX Mart 7-ELEVEN

Carrefour

Costco

RT Group

A Mart

Wellcome

Family Mart

Watson’s

S. Mart

Matsusei

Cosmed

Poya

ANNUAL COMPARISON, M11Q3~M13Q3

RETAIL HEALTH-TRAFFIC VS BASKET VALUE

M11Q3

M12Q3

M13Q3

15

AVERAGE PACKAGED FMCG SALES PER STORE. (MAT BASE / STORE NUMBER)

REFLECTS IN THEIR SINGLE STORE EFFICIENCY.

IT BECOMES FLATTER RECENTLY

2.0

2.5

3.0

3.5

4.0

08Q3 08Q4 09Q1 09Q2 09Q3 09Q4 10Q1 10Q2 10Q3 10Q4 11Q1 11Q2 11Q3 11Q4 12Q1 12Q2 12Q3 12Q4 13Q1 13Q2

60

65

70

75

08Q3 08Q4 09Q1 09Q2 09Q3 09Q4 10Q1 10Q2 10Q3 10Q4 11Q1 11Q2 11Q3 11Q4 12Q1 12Q2 12Q3 12Q4 13Q1 13Q2

Remodeling

16

POTENTIAL ISSUE WITH SHELF ARRANGMENT

17

WHERE IS THE ? WHICH ONE DO I WANT?

58%

31%

11%

CRUISING STOPPING CLOSING

18

IT’S YOUR BENEFIT/RESPONSIBILITY TO PUSH THEM CHANGE

© Kantar Worldpanel

14 15 15 8 9 11 9 9 11

10 9 9

5 5 5 9 8 9

8 6 6

4 4 4

6 5 5

6 7 8

1 1 1

4 5 5

7 7 7

35 37 35 25 27

29 3 3 3

1 1 2 2 3

3

3 3 3

15 13 12 10 10

9

0

10

20

30

40

50

60

70

80

MAT11Q3

MAT12Q3

MAT13Q3

MAT11Q3

MAT12Q3

MAT13Q3

MAT11Q3

MAT12Q3

MAT13Q3

PX C4 RT Costco 7 Eleven A Mart Family Wellcome On-line

TTL Food TTL Beverage Juice

ANNUAL COMPARISON , VALUE%

COSTCO IS LESS IMPORTANT IN YOUR CATEGORIES EXCEPT IN JUICE

19

0

200

400

600

800

1000

1200

1400

1600

0 100 200 300 400 500 600

Ba

sket V

alu

e (

NT

$)

Traffic (in million, Occasions)

PX-Mart

OK Mart

Carrefour

RT

Wellcome

A-Mart

Costco

ANNUAL COMPARISON, M11Q3~M13Q3

RETAIL HEALTH-TRAFFIC VS AVG SPENDING IN PACKAGE BEVERAGE

FAMILY-Mart

7-11

M11Q3

M12Q3

M13Q3

20

TAIWAN BEVERAGE MARKET

DYNAMIC

21

TOTAL BEVERAGE MARKET SIZE

TOTAL MARKET +5%

+21% +14% +3%

-5% -2% -1%

22

PENETRATION% FREQUENCY/YR BASKET BY L

71

66

57

88

54

63

89

54

63

58

69

57

68

71

91

55

70

70

13

11

22

50

9

11

49

9

11

9

11

20

11

12

48

19

9

12

1.1

1.5

0.6

1.1

3.0

1.6

1.1

3.1

1.6

3.3

1.6

0.6

1.6

1.0

1.1

0.7

1.7

1.0

M13Q3

M12Q3

M11Q3

HOW DID THEY GROW?

+21%

+14%

+3%

-5%

-2%

-1%

23

24

Grow sales

24

THE PATH TO PURCHASE

Awareness

Consideration

Purchase

Repeat

Loyalty

$

25

26

27

TAIWAN Percentage of changing brand at next purchase

Cookies 77%

Instant Noodle 74%

Homecare Cleanser 72%

Shampoo 69%

Carbon Soft Drink 64%

Instant Coffee 63%

Fabric Detergent 63%

RTD Tea 60%

Adult Milk Powder 35%

Herbal Instant Cereal 35%

Liquid Yogurt 35%

Fresh Milk 34%

Facial Moisturizer 34%

GUMP 23%

27

Repeat buying rates

# of people buying the brand

Bra

nd R

epeat

As the # of people

buying the brand

increased, the

repeat rate didn’t’.

28

HOW TO GROW PENETRATION ?

29

INNOVATION/

NEW PRODUCT LAUNCHES

30

One household

will try 6 new SKU

in an year

43,768 FMCG

SKUs available

in 2012 ~ now

(~ 442 SKUs per

category

16,929+ new

SKUs

launched in 2012~

now

Out of 9% value

growth FMCG

2012, 3% made

by new SKUs

In the duration of

our session today,

there will be a new

SKU born! Every 1 hour there’s a new

SKU! 32

After the first year,

a typical launch will have attracted

1 in 25 Households

Of whom,

19% have re-purchased

Source: Kantar Worldpanel Innovation tracker– Taiwan - Total Food & Beverage • Based on 97 new Brand & variant launches from 2012 Jan.

How many you could expect on the 1ST year launch…

INNOVATION TARGET | BENCHMARKS

(~ 306K HHs in total Taiwan)

33

Instant Soup Quick Soup

Canned Dessert

Frz. Dumpling Dim sun

Frz. HMR

Cheese

Cereal Drink

Cookies

Snacks

Yogurt

Instant Cereal Drink

Cooking Oil

Water

Juice CSD

Sports Drink

RTD Tea

Fermanted Drink

Health Food

Soy Sauce

RTD Coffee

Dairy

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

0.0 1.0 2.0 3.0 4.0 5.0 6.0 7.0 8.0 9.0

Ave

rage

Re

pe

at%

in 5

2 w

/e

Average Trial Rate% in 52 w/e

Differs by purchase frequency, category size, existing brand numbers;

but generally more Trial = more Repeat !!

INNOVATION TARGET | BENCHMARKS

Source: Kantar Worldpanel Innovation tracker– Taiwan - Total Food & Beverage • Based on 97 new Brand & variant launches from 2012 Jan.

34

4 wks 8 wks 12 wks 16 wks 20 wks 24 wks 28 wks 32 wks 36 wks 40 wks 44 wks 48 wks 52 wks

Ne

w B

uyer

rec

ruit

men

t S

pee

d

TOTAL F&B

COOKIES

SNAKCS

JUICE

CSD

RTD TEA

FERMANTEDDRINK

RTD COFFEE

DAIRY

INNOVATION TARGET | TRACKING & MONITORING

Recruitment speed dropped dramatically after 2 months

You have 60~90 days of window to

best target the early adopters, or you

need a further campaign after that

This window is smaller than some other countries, indicates TW

consumers’ personality, and even so for Quick Beverage categories

Source: Kantar Worldpanel Innovation tracker– Taiwan - Total Food & Beverage • Based on 97 new Brand & variant launches from 2012 Jan.

36

… After this critical period, the launch’s performance can be fairly

predictable

0

2

4

6

8

10

12

14

0 1 2 3 4 5 6 7

pe

ne

tra

tio

n a

fte

r 5

2 w

ee

ks

Penetration after 12 weeks

INNOVATION TARGET | TRACKING & MONITORING

Source: Kantar Worldpanel Innovation tracker– Taiwan - Total Food & Beverage • Based on 97 new Brand & variant launches from 2012 Jan.

37

NEW PRODUCTS ARE SUBSTANTIAL

TO MARKET GROWTH

Yet, continuous support is

also highly important.

New product survival rate in 2nd -yr

Below

30%?

New product survival rate in 3rd -yr

42%

38

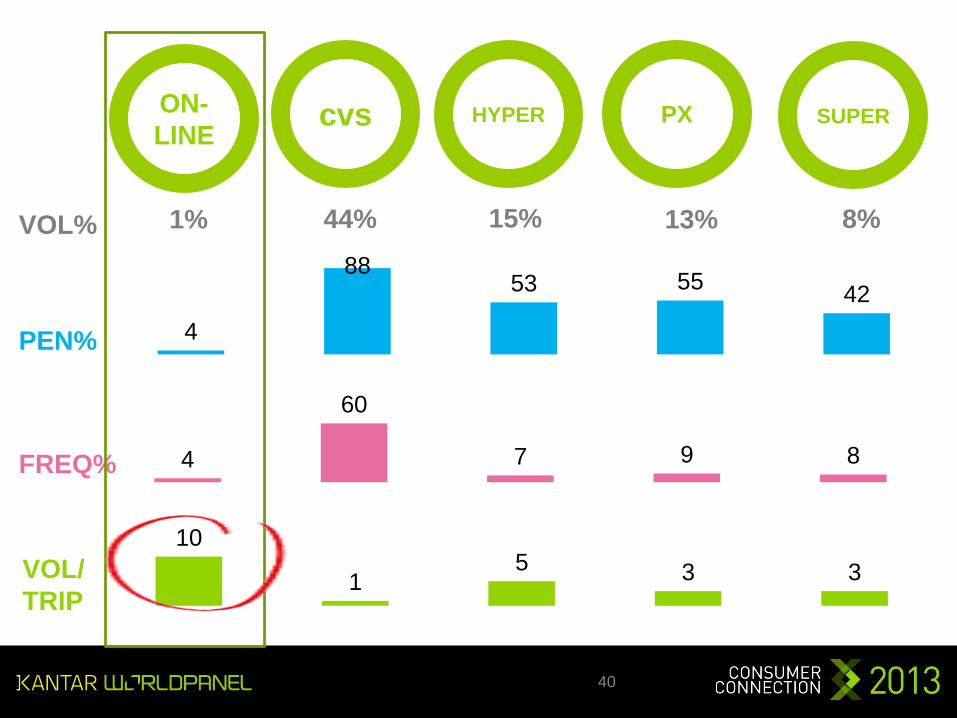

DOES ON-LINE SHOPPING HELP ME

TO GROW PENETRATION??

39

cvs ON-

LINE HYPER SUPER PX

1% 44% 15% 13% 8% VOL%

4

88 53 55

42

4

60

7 9 8

10

1 5 3 3

PEN%

FREQ%

VOL/

TRIP

40

IT CAN HELP YOU LOAD-UP THE SHOPPERS, BUT NOT BUYER BASE

DO IT AFTER YOU HAVE A SIZABLE PENETRATION%!!

41

PENETRATION:58 (+12%)

CUSTOMIZATION

FRESHNESS

INNOVATIVE

42

63 54

89

57 68 71 69

58

91

55 70 70

11 9

49

20 11 12 11 9

48

19 9 12

PEN%

FREQ

M12Q3 M13Q3

M12Q3 M13Q3

43

SALES VOLUME

+10% = 27,000 (KL)

5%

60%

FROM

11%

FROM

5%

44

PENETRATION OF DIFFERENT TYPE OF TEA

ONLY

TAKE-AWAY

TEA 5.7

ONLY

PACKAGE

TEA 40.4

BOTH

48.6

+15% -9%

PEN%

GR% OF PEN -2%

45

PENETRATION OF DIFFERENT TYPE OF COFFEE

ONLY

TAKE-AWAY

COFFEE

21.4

ONLY

PACKAGE

COFFEE

29.5

BOTH

20.6

+1% -6%

PEN%

GR% OF PEN +13%

46

cvs HYPER SUPER PX

49 47

4 4 5

48 45

4 5 5 FREQ%

M12Q3 M13Q3

CVS TAKES THE MOST HIT!!

47

KEY TAKE OUTS

48

4 KEY TAKE AWAY TODAY & 1 QUESTION FOR YOU……

TAKEAWAY CUP: YOU CAN’T FIGHT IT, BUT CAN YOU COEXIST WITH IT?

PENETRATION% IS THE KING!!

COSTCO IS SMALL EXCEPT IN JUICE

eCOMMERCE IS NOT IMPORTANT W/O BIG BUYER BASE

FMCG: CONSERVATIVE BUT POSITIVE

49

For further information please contact:

Contact Us!

Paul Wu, Joy Lin

Telephone: 02-2570 0556 # 306,278

http://www.kantarworldpanel.com/tw