Embed Size (px)

Citation preview

Consumer Choice With Uncertainty Part II: Examples

Agenda:

1. The Used Car Game

2. Insurance & The Death Spiral

3. The Market for Information

4. The Price of Risk

The Used Car Game

Buyers: If you buy a car for LESS than what it is worth you get a bonus point!

BUT If you buy a care for MORE than what it is worth you LOSE a bonus point.

Sellers: If you sell a car for MORE than what it is worth you get a bonus point!

BUT If you sell a care for LESS than what it is worth you LOSE a bonus point.

Good used cars are worth $10,000Bad used cars are worth $2,000 The market has both good and bad cars.

“The Market for Lemons: Quality Uncertainty and the Market Mechanism” by George A. Akerlof (1970)

QJE 84(3) 488 - 500 http://en.wikipedia.org/wiki/The_Market_for_Lemons

If a good car is worth $10,000 and a “lemon” car is worth $2,000 how much would you be willing to pay for a car if you think 20% of cars are lemons and your utility = sqrt(M)?

.8 10,000 .2 2,000

7911

X

X

Test Yourself: If you owned a “good” car would you be willing to sell it for the “market” price? If you want to buy a car and know this (owners of good cars won’t sell) then how much would you be willing to pay?

What units?

Market Failure!Is your $10,000 car worth $10,000 if you can’t sell it?

Because we are risk averse we are willing to pay MORE than the expected loss to reduce risk!

→ gains from trade!!

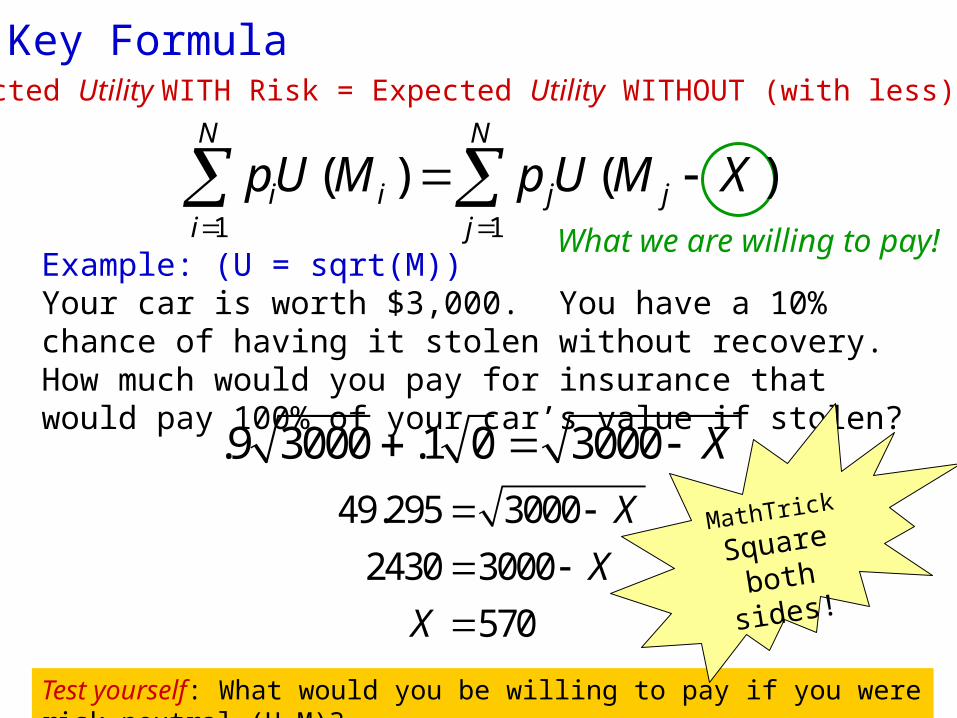

Key FormulaExpected Utility WITH Risk = Expected Utility WITHOUT (with less) Risk

1 1

( ) ( )N N

i i j ji j

pU M p U M X

Example: (U = sqrt(M))Your car is worth $3,000. You have a 10% chance of having it stolen without recovery. How much would you pay for insurance that would pay 100% of your car’s value if stolen?

.9 3000 .1 0 3000 X 49.295 3000

2430 3000

570

X

X

X

Test yourself: What would you be willing to pay if you were risk neutral (U=M)?

What we are willing to pay!

MathTrick

Square

both sides!

Math Trick

Multiply probabilities on each

“branch” of the tree.

Insurance – Adverse Selection & “The Insurance Death Spiral”Assume there are two groups in the population: healthy people have a 10% chance of having $360 in expenses and sick people have a 50% chance of having $360 in expenses. If everyone starts with $1000 in wealth and U = sqrt(M), what is the most each group would be willing to pay for insurance?

$39.60 $190

healthy sick

.9 .5.5.1

$1,000 $1,000$640 $640

.5 .5

If a risk-neutral insurer could not tell who is in which group, what premium would it have to charge to cover expected losses?

.5*.1*$360 + .5*.5*360 = $108

What will happen to the market if they charge this?

Mark Pauly The Economics of Moral Hazard: CommentThe American Economic Review 58(3):1968

D2’: mild illness D3’: serious illness

Marginal cost

D2 D3’

50 150 200 300 Quantity ofMedical Care

Price of Medical Care

1

D2 and D3: Elastic demandLower price, higher quantity

EfficiencyLoss

EfficiencyLoss

AFP for D2’& D3’: ½ * 0 + ¼*$50 + ¼*$200 = $62.5

AFP for D2 & D3 : ½ *$ 0+ ¼*$150 + ¼*$300 = $112.5

People may be unwilling to pay 112.5. This is not market failure!Forcing people to have insurance does not improve social welfare.

D2’ and D3’: Inelastic demand no change in quantity at any price

Signaling!

Test yourself: Can you come up with a question that determines how much a company would be willing to pay for “brand” identity? How about how much more a consumer would be willing to pay for a branded rather than generic item?

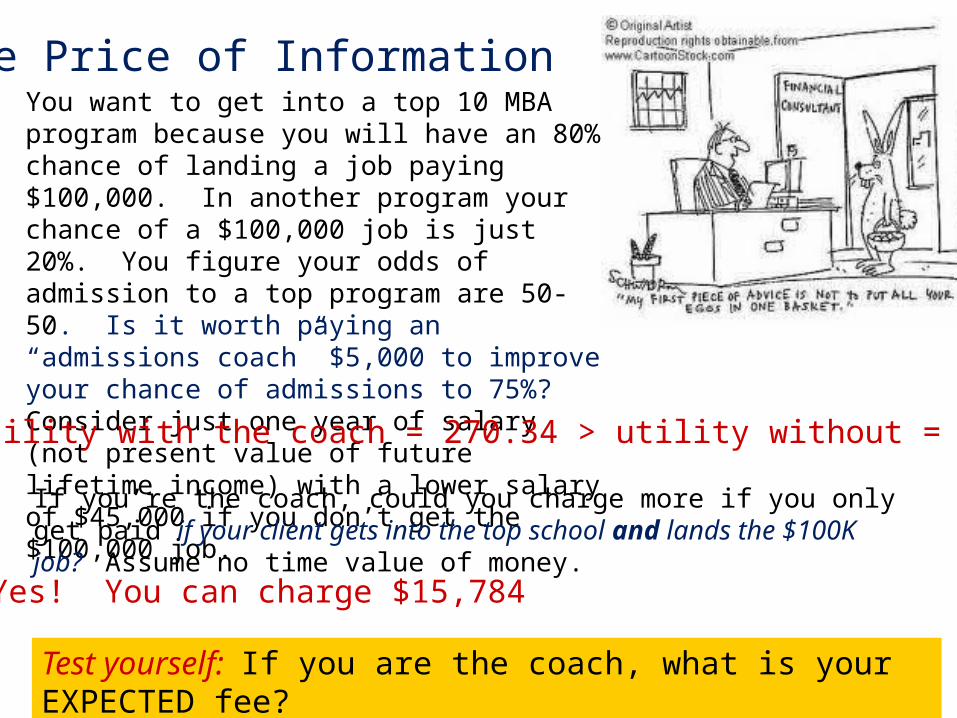

The Price of InformationYou want to get into a top 10 MBA program because you will have an 80% chance of landing a job paying $100,000. In another program your chance of a $100,000 job is just 20%. You figure your odds of admission to a top program are 50-50. Is it worth paying an “admissions coach” $5,000 to improve your chance of admissions to 75%? Consider just one year of salary (not present value of future lifetime income) with a lower salary of $45,000 if you don’t get the $100,000 job.

Yes! Utility with the coach = 270.34 > utility without = 264.18

If you’re the coach, could you charge more if you only get paid if your client gets into the top school and lands the $100K job? Assume no time value of money.

Yes! You can charge $15,784

Test yourself: If you are the coach, what is your EXPECTED fee?

Top school Other School

.8 .8.2.2

.75 .25

100,000 X 45,000 45,000100,000

If you’re the coach, could you charge more if you only get paid if your client gets into the top school and lands the $100K job? Again, assume no time value of money.

0.6 100,000 .15(212.13) 0.05(316.23) .2(212.13) 264.18

0.6 100,000 31.82 15.81 42.43 264.18

0.6 100,000 90.06 264.18

0.6 100,000 174.12 (divide by 0.6)

100,000 290.2 (square both sides)

100,000 84,

X

X

X

X

X

X

216.04

15,783.96 Expected value 0.6(15,783.96) = 9,470.38X

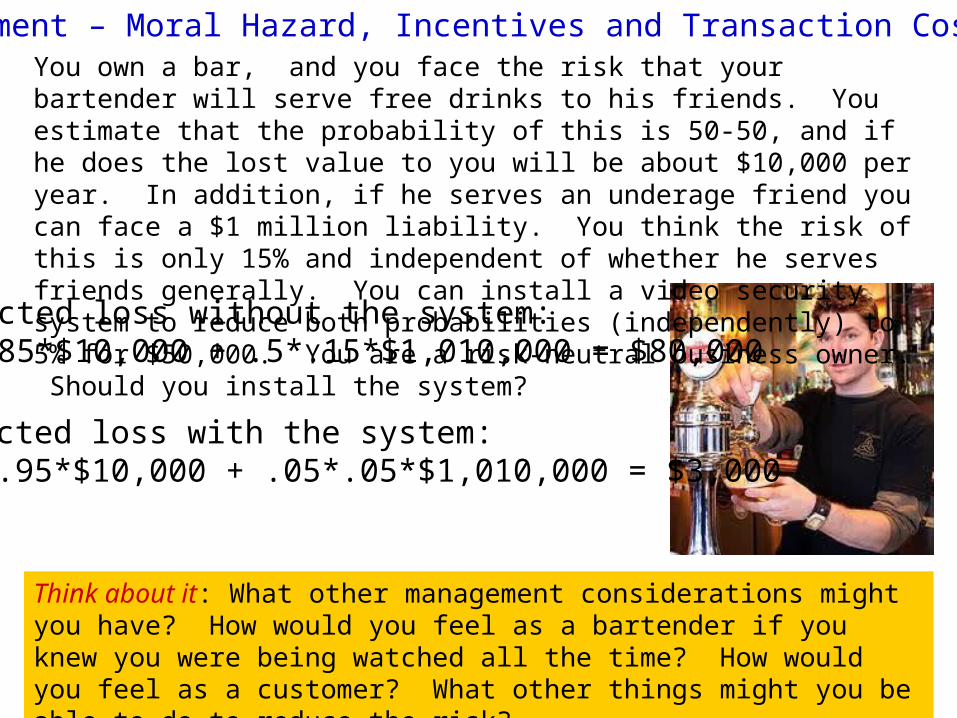

You own a bar, and you face the risk that your bartender will serve free drinks to his friends. You estimate that the probability of this is 50-50, and if he does the lost value to you will be about $10,000 per year. In addition, if he serves an underage friend you can face a $1 million liability. You think the risk of this is only 15% and independent of whether he serves friends generally. You can install a video security system to reduce both probabilities (independently) to 5% for $50,000. You are a risk-neutral business owner. Should you install the system?

Expected loss without the system:.5*.85*$10,000 + .5*.15*$1,010,000 = $80,000

Expected loss with the system:.05*.95*$10,000 + .05*.05*$1,010,000 = $3,000

Think about it: What other management considerations might you have? How would you feel as a bartender if you knew you were being watched all the time? How would you feel as a customer? What other things might you be able to do to reduce the risk?

Management – Moral Hazard, Incentives and Transaction Costs

Conclusion

Uncertainty is everywhere!

But we can deal with it!!

Expected Value 1

N

i ii

E X X p

Expected Utility

1

( ) ( )N

i ii

E U M p u M

1 1

( ) ( )N N

i i j ji j

pU M p U M X

Willingness to Pay to reduce risk!