Embed Size (px)

DESCRIPTION

In this report we discuss 5 megatrends that are directly impacting the Consumer Business Industry in 2020. With these five megatrends we strive to inspire you to think ahead, create scenarios and translate these developments into priorities for your organization.

Citation preview

Consumer Business Predictions & Priorities 2012

2

Content

Executive Summary

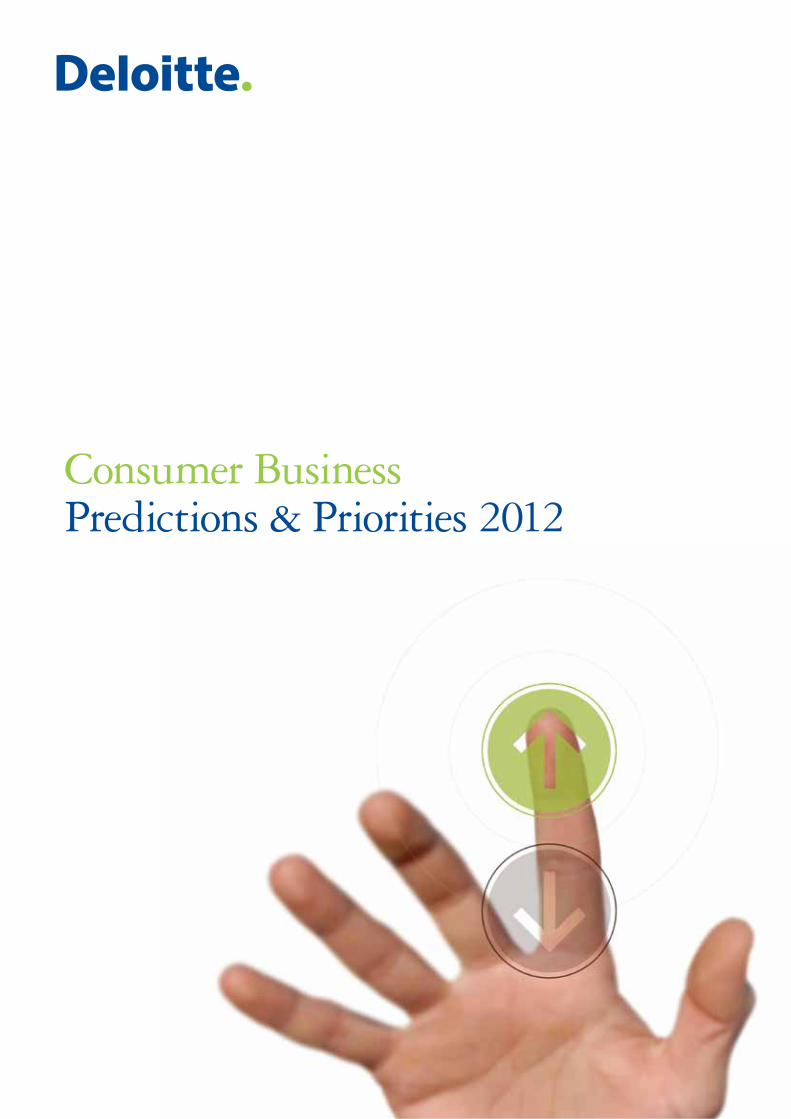

5 key predictions for growth development in 2020

Changing global economy

Demographic changes

Consumers’ changing menu

Sustainability as part of daily business

Communicating, connecting and socializing

Recommended reading

For more information, please contact us

3

5

6

8

10

12

14

16

18

Consumer Business Predictions & Priorities 2012 3

Executive Summary

In recent months, the major areas of uncertainty for the

global economy have revolved around the crisis in the

Eurozone, the future path of monetary and fiscal policy

in the United States, political instability in the Middle

East and Northern Africa and the fight against inflation

in emerging markets. As a result of this uncertainty key

decision makers in the consumer business industry have

been primarily focused on navigating their companies

securely through a turbulent global business

environment.

In addition, as the insecure global outlook is not

expected to clear in the short term it also complicates

decision making concerning long term growth

strategies.

However, aside from the economic turmoil there are

also plenty of opportunities for growth. When looking

at the long term global developments a number of key

mega-trends can be identified, which provide direction

for long term growth.

We believe that future decision making will be

increasingly driven by predictions, data-analytics and

fact-based understanding of (mega)trends. For

businesses to set their priorities and growth strategies,

solid predictions or scenarios are required to describe

what the future is expected to look like.

In this report we discuss 5 megatrends that are directly

impacting the Consumer Business Industry in 2020.

With these five megatrends we strive to inspire you to

think ahead, create scenarios and translate these

developments into priorities for your organization.

Is your organization ready to anticipate on these

changes?

4

Consumer Business Predictions & Priorities 2012 5

Prediction #1

Changing global economy

Women in emerging markets spend more than Europe

Prediction #2

Demographic changes

The elderly will be the largest growth market in the U.S.

and Europe

Prediction #3

Consumers’ changing menu

Fats and sugar products will be replaced by healthier

products

Prediction #4

Sustainability imperative

Businesses will work in collaboration with regulators to

define sustainabilitystandards, going beyond regulation

Prediction #5

Communicating, connecting and socializing

Online retail sales in Western Europe and the US will have

doubled versus 2011

5 key predictions for growth development in 2020

6

Changing global economyIn 2020 women in emerging markets spend more than Europe

Emerging markets are characterized by good

demographics (e.g. rapid rise of young consumers and

a surge of the young workforce) and strong (industrial)

growth prospects. These features foster an increase of

the number of households that will move from poverty

into the middle class and beyond. It is in fact expected

that the number of people moving into the middle class

tends to grow even faster than the overall economies of

these countries. When bearing this in mind, it is not

surprising that of the 70 million new consumers that

are expected to enter the global middle class each year

a great majority will come from emerging markets;

resulting in a substantial rise of consumer spending

growth in these markets. This is in line with the

anticipation that a disproportionate share of global

growth of consumer spending will indeed take place in

emerging markets.

Enhancement of favorable governmental policies in

these markets - such as increased liberalization of

consumer finance, improved social safety nets (to

discourage customer saving), and allowance of currency

depreciation- will stimulate consumer spending even

further.

Additionally, besides the fact that the workforce is

young and growing in emerging markets, the amount

of women that become s educated rises rapidly as well;

in many of the BRIC countries girl and boy enrollments

of primary and secondary schools are almost equal1.

This development speeds up the increase in female

labor participation. Currently, on average 39%2 of the

labor force of the emerging countries is female, hence

this trend will increase the amount of two-income

households and result in an increase of discretionary

income; hence, consumer spending.

Discretionary income, and thus consumer spending, is

spurred even more because of the fact that fertility

rates are dropping in emerging markets, women’s

overall health is significantly improving (women’s life

expectancy has been prolonged with 10 years since

19901) and they increasingly decide to have children

later in live. Consequently, disposable income to spend

on consumer products and services increases.

Now consider the fact that the four BRIC countries plus

the tier 2 emerging markets together account for 3,4

billion people, more than half of the current world

population of which the top 20% already have similar

purchasing power as the average citizen of developed

countries. Taking this into account one can imagine

that the increase in expected consumer spending

within the emerging markets is tremendous.

Contrarily to the developments in the emerging

markets, it is anticipated that the European market will

offer limited growth opportunities; producing value-

conscious consumers, who are unlikely to return to

their pre-recession spending levels due to among

others tighter credits and loss of wealth.

Additionally, these consumers will be very price

sensitive and be characterized by decreased or slowly

growing discretionary spending/ consumer spending.

Another fact to take into account is that while the

workforce in emerging markets is young and increasing,

the European workforce is old and decreasing.

The prosperous outlook of emerging markets with

regard to increased consumer spending linked to the

contradictory developments in the European markets,

provides emerging markets with the opportunity to

catch up and even supersede European spending levels.

Although this trend has been ongoing since the past

decade a particularly interesting development is the rise

in income of women in emerging markets. This trend is

twofold as in the first place we see an increase in labor

participation in areas like India, Latin America and Africa.

Secondly, as women in these areas have increasingly

engaged in education this has given them access to

educated jobs which are also getting better paid.

Is your organization ready for an increase in female spending power in emerging markets?

Consumer Business Predictions & Priorities 2012 7

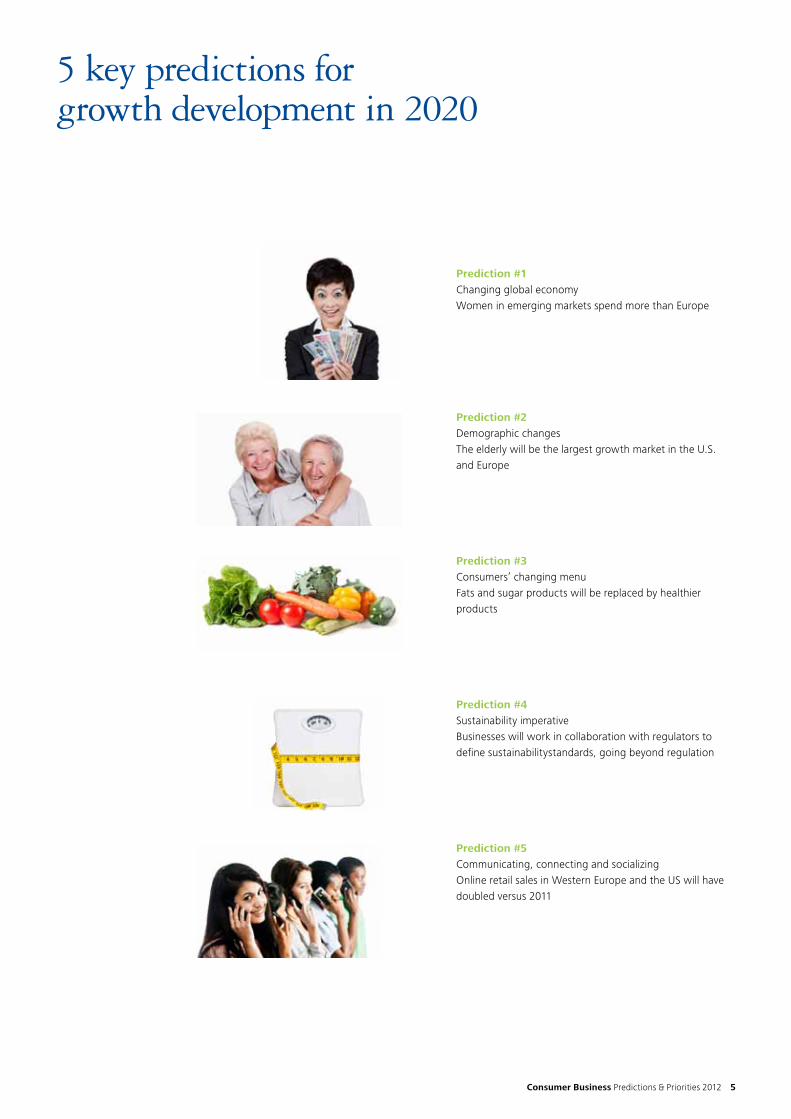

To put these developments into perspective, European

disposable income in 2011 is 11,6 3 trio US Dollars 3,

which is expected to grow to 13,7 trio US Dollars in

2020 4. Respectively, disposable income in the four BRIC

countries plus tier 2 emerging markets currently is 10,2 3

trio US dollars, which is expected to grow to 30,3 trio

US dollars in 2020 4. On average 39% of the labor force

in these countries is currently female. As stipulated,

labor participation of women is increasing rapidly.

Therefore it can be expected that female participation

in emerging markets will grow towards the Western

average of 45% by 2020.

Years

Forecasted income Europe versus Emerging Markets

Dis

po

sab

le in

com

e in

$tr

io

■ Europe

■ Emerging Markets

■ Europe (forecasted)

■ Emerging Markets (forecasted)

2010

0

5

15

25

35

10

20

30

20202018201620142012

1 Source: World Bank

2 Source: International Labour Organization

3 Source: Economist Intelligence Uni

4 Source: Economist Intelligence Uni & Deloite researc Emerging markets: Brazil, Russia, India, China, Indonesia, Mexico, Vietnam, Turkey,

Chile, Egypt, Malaysia and Taiwan,

Assuming that disposable income equals consumer

spending and is attributed to the person who earned it,

the conclusion can be drawn that in 2020 spending of

women in emerging countries will have risen to 13,6

trio US Dollar. Accounting for the fact that only the

main emerging countries are included in this number,

the total amount of spending will even be higher and

likely supersede the 13,7 trio US Dollar of Europe.

This results in the prediction that in 2020 spending of

women in emerging markets will have superseded

European spending.

Is your organization ready for this rise in female

spending power?

8

Demographic changesIn 2020 the elderly will be the largest growth market in the U.S. and Europe

In both Europe and the US the national fertility rates 1

have fallen below the replacement rate 2 of 2.1 children,

which is the replacement rate of many industrialized

nations. In many European countries fertility rates are

between 1.3 and 1.4. In the US this is 2,06 1. Besides,

given the fact that the replacement rate is currently

below the average rate of 2.1 in both Europe and the

US, it is expected that this trend will continue in the

coming decades; resulting in population decline.

Next to population decline, population aging will have

a major impact on both Europe and the US as well; it is

predicted that in 2020 the average age in Europe will

be 42,2 years 4 and in the US 37,5 years 7 compared to

39,8 years 4 and 35,5 years 7 respectively in 2010. Aging

of the population results in increased retirement rates

of which the impact in the next decade will be even

stronger due to the fact that the Baby Boom generation

will move fully into retirement in the 2020s 3.

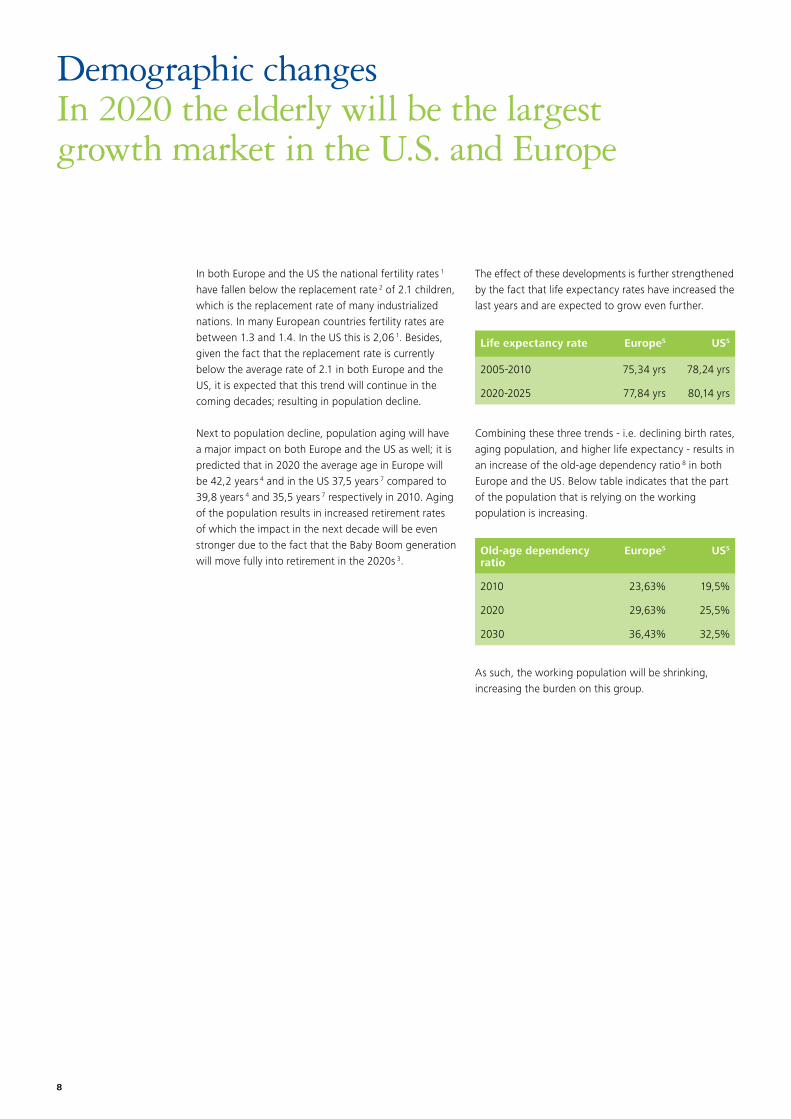

The effect of these developments is further strengthened

by the fact that life expectancy rates have increased the

last years and are expected to grow even further.

Life expectancy rate Europe5 US5

2005-2010 75,34 yrs 78,24 yrs

2020-2025 77,84 yrs 80,14 yrs

Combining these three trends - i.e. declining birth rates,

aging population, and higher life expectancy - results in

an increase of the old-age dependency ratio 8 in both

Europe and the US. Below table indicates that the part

of the population that is relying on the working

population is increasing.

Old-age dependency ratio

Europe5 US5

2010 23,63% 19,5%

2020 29,63% 25,5%

2030 36,43% 32,5%

As such, the working population will be shrinking,

increasing the burden on this group.

Consumer Business Predictions & Priorities 2012 9

1 The fertility rate is ‘the average number of children that would be born per woman if all women lived to the end of their childbearing

years and bore children according to a given fertility rate at each age. Source: CIA World Factbook

2 The replacement rate represents the average number of children that a couple needs in order to replace themselves in a population

3 Source: Investor Insight

4 Source: Eurostat

5 Source: World Research Institute

6 Source: Deloitte Research: Consumer 2020

7 Source: http://www.doleta.gov/seniors/other_docs/AgingBoomers.pdf

8 The old-age dependency ratio refers to ‘the ratio of older dependents (people older than 64) to the working-age population (ages

15-64). Source: World Bank

9 Source: UN World Population Prospects: The 2008 Revision population by age, medium variant

The burden will grow even more in the coming years as

more Baby Boomers will retire; in essence relatively

fewer people will pay taxes and more people will

receive pensions and health care.

In addition, the working population’s disposable

income will also be negatively affected due to the fact

that this group of people is encouraged to save for their

own retirement rather than to enjoy all of their

disposable income (as government and employment

pension systems are not guaranteed to be in place

when this group retires).

These trends result in the conclusion that the elderly

will be the largest growth market both in the US and

Europe.

As with all developments, growth in markets and shifts

in consumer segments go hand in hand with

opportunities. When defining these opportunities take

the following into account: elderly value their time

more and seek solutions that help them maintain their

quality of life. They, therefore, are likely to spend more

on healthcare, leisure, travel and utilities such as for

instance air conditioning. Moreover, they typically

spend more on their grandchildren and are

characterized by a ‘forever young’ attitude; resulting in

increased demand for e.g. anti-aging products and

healthy food products.

When considering the above; Is your organization ready

for the opportunities of the aging population?

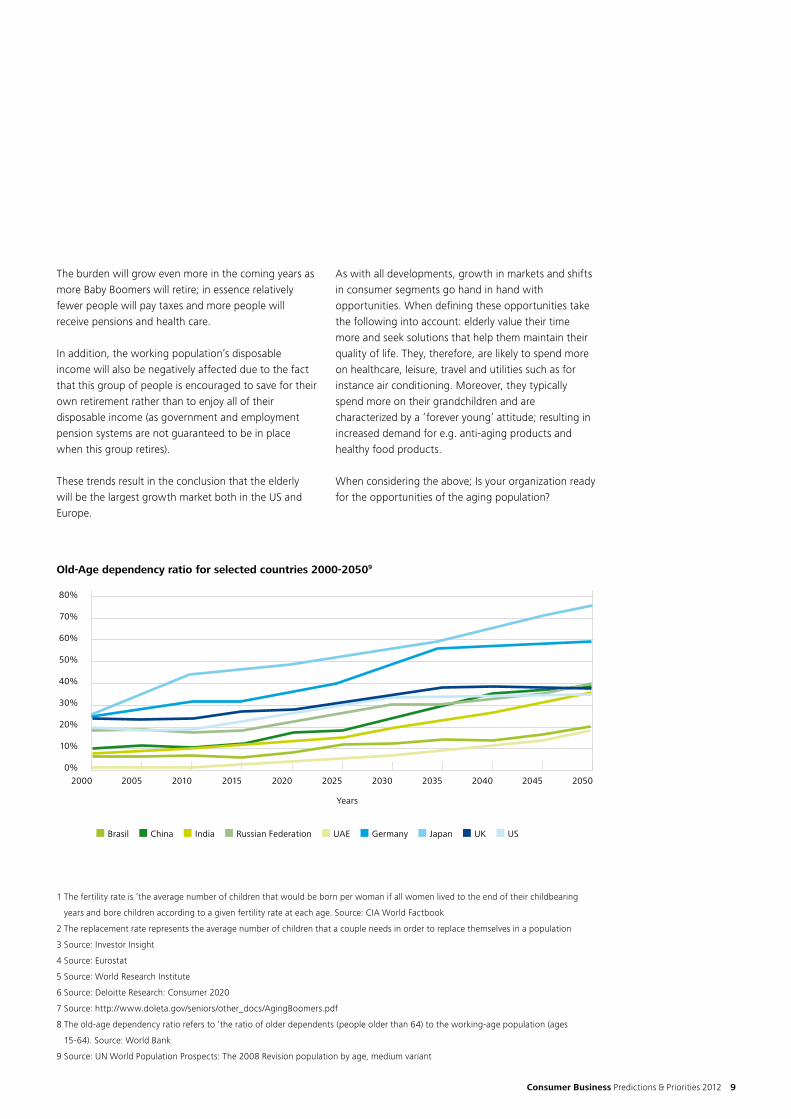

Years

Old-Age dependency ratio for selected countries 2000-20509

■ Brasil ■ China ■ India ■ Russian Federation ■ UAE ■ Germany ■ Japan ■ UK ■ US

2000

0%

10%

30%

50%

70%

20%

40%

60%

80%

2050204520402035203020252020201520102005

10

Consumers’ changing menu…In 2020 fats and sugar products will be replaced by healthier products

For the coming 10 years it is projected that the world’s

population will increase with 11 percent 1, resulting in

766 million1 more mouths to feed in 2020. Moreover,

at least 70 million 1 consumers will enter the global

middle class each year. Finally, in addition to the fact

that the number of consumers and their disposable

income is increasing, there will be a shift in

consumption habits as well.

When income rises, people shift from grain-based diets

to diets dominated by ‘high-value’ foods such as e.g.

dairy products, meat, fish, fruits and vegetables. As

people shift to these more varied diets, their

consumption of fats, saturated fats and sugar increases

as well. This combined with changing living standards

due to urbanization – like less physically demanding

work, automated transportation and passive leisure

pursuits such as playing video games- results in an

increase of obesity rates.

As obesity increases, consequently the costs assigned

to this disease increase as well; Public funds and

healthcare providers are negatively affected by the

consequences of obesity. This combined with rising

health care costs due to the aging population (as

described in prediction two) implies that at a certain

moment governments’ interventions focusing on

improving consumers’ eating habits will be inevitable.

Governments intervene through, for instance,

education and the introduction and enforcement of

policy acts; increasing consumers awareness of obesity

and of the negative effects of fats and sugar products.

As a result, the demand for healthier eating, functional

foods and increased transparency of food products

increases. So, following this line of reasoning, changing

diets will eventually result in the replacement of fats

and sugar products by healthier products.

1 Source: Deloitte Consumer 2020

2 Source: World Health Organization

3 Source: Department of Health and Human Services

4 Source: Reuters

5 Source: Hive Health Media

6 Source: USA Today

7 Source: McKinsey Quarterly

8 Source: Preventative Health Taskforce

9 Source: Volkskrant

10 World Obesity Statistics for OECD countries 2010

However, globally this statement is not confirmed yet,

as not all countries around the globe are at the same

point of the cycle. The more developed countries are,

the further they will be in their way towards meeting

this prediction. Nevertheless, although countries:

• are at different stages of the cycle

• move at varied paces, and

• are impacted differently from each other on all stages

it is believed that eventually they all follow the same path.

Additionally, it is predicted that by 2020 a significant

part of the developed countries will already clearly

show signs that confirm the predicted trend of

replacing fats and sugar products by healthier products.

Governments’ interventions focusing on improving consumers’ eating habits will be inevitable’

Consumer Business Predictions & Priorities 2012 11

That countries are at different stages of the cycle and

are impacted differently is shown by the following facts

and figures:

Obesity:

• Currently, in the United States more than 33 percent

of adolescents and children are overweight or obese 3.

• Globally, 2010 counted more than 1 billion

overweight adults of which at least 300 million were

obese 1. Also, 43 million children under the age of five

were overweight in 2010 2.

• In both China and Japan, 1 in 20 women is obese,

which is respectively: 1 in 4 in Australia, 1 in 10 in the

Netherlands, and 7 in 10 in Tongo 4.

Cost of Obesity:

• 2 to 6 percent of healthcare costs are directed to

obesity in many countries4. Moreover, health care

expenditure for an obese person is at least 25 percent

higher than for a normal weight person 5.

• The total cost of overweight and obesity in Canada

was about 30 billion US dollars in 2011 6.

• The total cost of obesity in the US is at least 450

billion 7 per year of which 160 billion 7 is assigned to

obesity-related medical costs; these costs are

predicted to double by 2018.

Governmental Intervention:

• ‘In Mauritius, a government-led effort lowered the

population’s cholesterol largely by promoting

soybean oil rather than palm oil for cooking’ 8.

• In Norway, governmental interventions like price

manipulation and food subsidies proved to be

effective in turning around the shift towards high-fat

diets 8.

• Recently, the Dutch minister of public health

prioritized fighting obesity when developing

prevention policy with regard to combatting diseases

stemming from obesity 9.

In conclusion, both regulation and consumer awareness

will cause consumption habits to change, implying a

shift towards healthier diets. This trend will impact

product portfolios of food producing industries,

affecting the end-to-end value chain. Moreover, it is

expected that clear labeling by means of providing

more detailed nutritional information will become

increasingly important in the near future.

Is your organization ready for healthy diets?

Onl

ine

reta

il sa

les

($ b

illio

n)

Years

Past and projected future overweight rates in selected OECD countries10

■ USA ■ England ■ Canada ■ Spain ■ Austria ■ Italy ■ France ■ Korea

1970 1980

20%

30%

40%

50%

60%

70%

80%

1990 2000 2010 2020

12

Sustainability as part of daily business…In 2020 business will work with regulators to define sustainability standards

Recent studies 1 on regulation in the Consumer Business

Industry show a clearly identifiable cascade in the

regulatory and tax burden from more harmful to less

harmful product categories. These regulatory changes,

typically lead by developed economies, are quickly

followed by countries that are developing or emerging.

Two main drivers can be determined that cause

increasing regulation to be enforced on consumer

products:

• Health: the increasing problem of obesity and the

fast growing healthcare costs

• Environment: resource intensive industries face

scarcity of natural resources and increasing

awareness for carbon emissions and other

environmental impacts

In essence, governments have been increasingly

stimulated to develop new regulations in the form of

price policies, advertising bans or other instruments.

Case examples: The Sustainable Apparel Coalition and Electrical Cars

Recent examples have proven that collaboration and self-regulation are the key to success in overcoming or

even preventing regulation issues."The Sustainable Apparel Coalition is an industry-wide group consisting of

leading apparel and footwear brands, retailers, manufacturers, non-governmental organizations, academic

experts and the U.S. Environmental Protection Agency. These parties have joined forces to reduce the

environmental and social impacts of apparel and footwear products around the world. They are creating a

sustainability index that will measure the impact of a product throughout its life. The tool ensures

consistency across the industry regarding environmental product performance. The coalition started the

initiative with the aim to be ahead of the legislation and in that way influence the governments to shape the

standard.

Another example is the development of the electrical cars that started over 10 years ago. Today the first

commercial models are starting to become a success. New brands such as Tesla Cars successfully set the

standard for the future car industry. While today’s governments are considering setting-up measures to

reduce carbon-emissions, the industry already set the next step. Following these examples we expect the

industry to keep setting the next step in these developments and as such being able to define the standards

for their industry rather then being enforced.

1 Source: Deloitte Research: Strategy Insights, 2011

However, in the near future we will see the business

relationship with environmental regulators change;

As the societal need for sustainable products increases,

organizations will become more proactive in

incorporating the sustainability agenda in their growth

strategies. In addition, recent examples have shown

that sustainability initiatives can go hand-in-hand with

benefits realization as well. As such, in many areas

regulation will become a minimum standard, with most

businesses seeing the benefits of going beyond.

In addition, as organizations become more proactive in

defining their own industry standards, the traditional

role of regulatory parties will change as well. Instead of

playing an enforcement role, governments will start to

play one of collaboration and monitoring and

facilitating best practice between parties to manage

consumption.

Consumer Business Predictions & Priorities 2012 13

Call for action: Pro-actively engage with

governmental institutions in defining sustainable

growth criteria

1.

Explore regulatory

collaboration

2.

Align your internal

capabilities

3.

Be ahead of

the game

1. Collaborate; explore the opportunities in your field to

start regulatory collaboration among other players in

the industry. We encourage businesses to proactively

engage with regulators, either collectively or

individually, to establish a level-playing field based on

industry best practices

2. Align your internal capabilities; those businesses that

recognize the potential impact of regulatory change

in an early stage, and align internal resources, R&D

and tools to influence or steer these changes, will

reap the long term benefits.

3. Be ahead of the game, first movers will enjoy early

mover advantage. Successful businesses will be those

that move quickly to develop - and commit to - a

strategic approach to assessing and shaping the

regulatory environment rather than reacting to it.

Now is the time to pro-actively engage with

governments, share best practices and collaboratively

set the standard for sustainability and other regulation

fields.

14

Communicating, connecting and socializing…In 2020 online retail sales in Western Europe and the U.S. will have doubled versus 2011

In the last decades, the Internet -and thereby the

introduction of e-commerce- has brought about a shift

in consumer behavior within the consumer-focused

industries. The Internet provides consumers with

instant access to information needed to compare, shop

and purchase items anytime and anywhere. The

increase in access to information results in consumers

who are better informed about companies, products,

services, pricing and product availability. Moreover,

they are increasingly aware of problems, recalls, and

scandals. All the above indicates that the landscape is

changing and the line between online and offline

shopping is blurring. In addition, this change is taking

effect more rapidly than expected and is impacting

tomorrow’s way of doing business.

Change is in particularly noticeable in certain categories

of consumer products. The European top 7 consumer

products that are bought online are represented in the

table below 1:

Rank Product "Online" Revenue in 2011 in Western

Europe (bln) 1

1 Electronics € 36.4

2 Apparel € 16.3

3 Groceries € 11.8

4 Automotive € 11.3

5 Media € 9.2

6 Recreation € 8.9

7 Household goods € 5.7

It is predicted that online retail sales and orientation

will grow further in the coming decade 2. Expected

growth comes forth out 3 factors:

1. More people are going online (with broadband

access or mobile broadband)

2. As people start to recognize the benefits of online

shopping channel, more consumers are shopping

online

3. As consumers are getting used to online shopping

they are spending more while shopping online

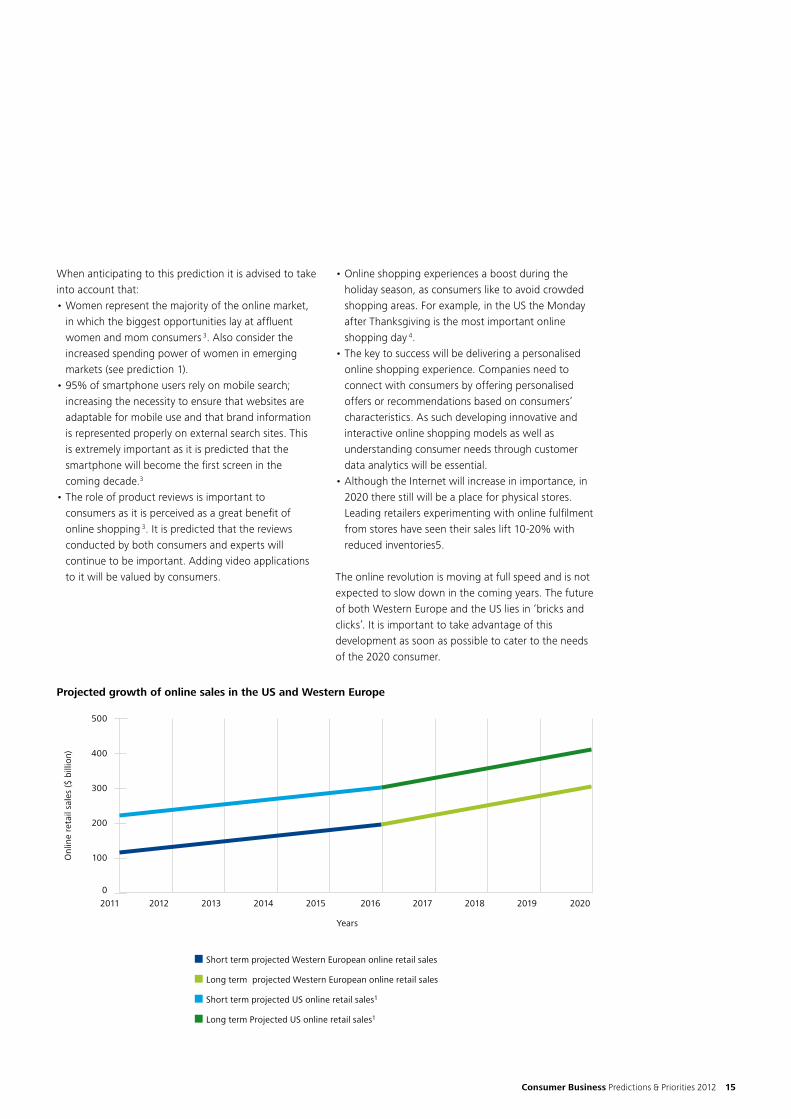

Forrester Research shows that online sales are growing;

In the US online retail sales are predicted to grow from

202 billion US dollars in 2011 to 327 billion US dollars in

2016 1. For Western Europe this is 125 billion US dollars

and 223 billon dollars respectively 1. As the impact of

the Internet will further increase in the coming years,

continued growth is expected. When taking a cautious

approach and assuming that the online retail sales

growth rate will continue at the same pace the next

decade, it results in predicted online retail sales in the

US of 444 billion US dollars in 2020 and respectively

327 billion US dollars in Western Europe. Together this

results in the prediction that in 2020 online retail sales

of Western Europe and the US together will have

doubled versus 2011.

1 Source: Forrester Research

2 Source: Emerce

3 Source: Branding Magazine

4 Source: Statista

5 Source: Deloitte US e-commerce assessment 2012

Consumer Business Predictions & Priorities 2012 15

When anticipating to this prediction it is advised to take

into account that:

• Women represent the majority of the online market,

in which the biggest opportunities lay at affluent

women and mom consumers 3. Also consider the

increased spending power of women in emerging

markets (see prediction 1).

• 95% of smartphone users rely on mobile search;

increasing the necessity to ensure that websites are

adaptable for mobile use and that brand information

is represented properly on external search sites. This

is extremely important as it is predicted that the

smartphone will become the first screen in the

coming decade.3

• The role of product reviews is important to

consumers as it is perceived as a great benefit of

online shopping 3. It is predicted that the reviews

conducted by both consumers and experts will

continue to be important. Adding video applications

to it will be valued by consumers.

• Online shopping experiences a boost during the

holiday season, as consumers like to avoid crowded

shopping areas. For example, in the US the Monday

after Thanksgiving is the most important online

shopping day 4.

• The key to success will be delivering a personalised

online shopping experience. Companies need to

connect with consumers by offering personalised

offers or recommendations based on consumers’

characteristics. As such developing innovative and

interactive online shopping models as well as

understanding consumer needs through customer

data analytics will be essential.

• Although the Internet will increase in importance, in

2020 there still will be a place for physical stores.

Leading retailers experimenting with online fulfilment

from stores have seen their sales lift 10-20% with

reduced inventories5.

The online revolution is moving at full speed and is not

expected to slow down in the coming years. The future

of both Western Europe and the US lies in ‘bricks and

clicks’. It is important to take advantage of this

development as soon as possible to cater to the needs

of the 2020 consumer.

Onl

ine

reta

il sa

les

($ b

illio

n)

Years

Projected growth of online sales in the US and Western Europe

■ Short term projected Western European online retail sales

■ Long term projected Western European online retail sales

■ Short term projected US online retail sales1

■ Long term Projected US online retail sales1

2011 2012

0

100

200

300

400

500

2013 2014 2015 2016 2017 2018 2019 2020

1 Source: Forrester Research

2 Source: Emerce

3 Source: Branding Magazine

4 Source: Statista

5 Source: Deloitte US e-commerce assessment 2012

16

Recommended reading

Thought Leadership/Research Samples

Consumer 2020: Reading the signs

There is no such thing as a global consumer but this report

examines how the global trend will most likely shape

consumer spending patterns and the world of consumers

more broadly.

Global Power of the CPI 2012

– Connecting the dots

This report examines trends for companies to consider as

they plan their growth strategies, provides a global

economic outlook for retail, and discusses "Q" ratio - a way

of drawing inferences about the future performance of

retailers by examining current financial information.

Consumer Business Predictions & Priorities 2012 17

Global Power of retailing 2012

– Switching Channels

This report identifies the 250 largest retailers and provides

an outlook for the global economy including trends to

consider for the retail industry

European eCommerce Assessment 2012

This European study presents the current state of online

retail across Europe. To produce this white paper, Deloitte

benchmarked and analyzed Europe’s top 200 online

retailers on 140 eCommerce capabilities.

18

For more information, please contact us

Erik Nanninga

Partner & Consumer Business Leader

Deloitte Consulting

Laan van Kronenburg 2

1183 AS Amstelveen

The Netherlands

Tel: +31 (0)88 288 0276

Mobile:+31 (0)6 558 53 772

Randy Jagt

Director – Growth Strategy & Emerging Markets

Deloitte Consulting

Laan van Kronenburg 2

1183 AS Amstelveen

The Netherlands

Tel: +31 (0)88 288 2371

Mobile:+31 (0)6 109 80 178

Eric Bobek

Manager – Customer Markets Strategy

Deloitte Consulting

Laan van Kronenburg 2

1183 AS Amstelveen

The Netherlands

Tel: +31 (0)88 288 4293

Mobile:+31 (0)6 123 42 671

Consumer Business Predictions & Priorities 2012 19

Is your organization ready to anticipate on these changes?

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms.

Deloitte provides audit, tax, consulting, and financial advisory services to public and private clients spanning multiple industries. With a globally connected network of member firms in more than 150 countries, Deloitte brings world-class capabilities and high-quality service to clients, delivering the insights they need to address their most complex business challenges. Deloitte's approximately 182,000 professionals are committed to becoming the standard of excellence.

This publication contains general information only, and none of Deloitte Touche Tohmatsu Limited, its member firms, or their related entities (collectively, the “Deloitte Network”) is, by means of this publication, rendering professional advice or services. Before making any decision or taking any action that may affect your finances or your business, you should consult a qualified professional adviser. No entity in the Deloitte Network shall be responsible for any loss whatsoever sustained by any person who relies on this publication.

© 2012 Deloitte The Netherlands