Embed Size (px)

Citation preview

Dr. David Hughes Emeritus Professor of Food Marketing

Global Agribusiness & Food Industry Conference International Institute of Agri-Food Security Curtin University, WA, Australia The Rendezvous Observation City Hotel Perth, Monday, September 10th, 2012

Consumer and Other Trends in The Global Food Value Chain: Implications for Agribusiness

Population Projections for Japan and Proportion of Population 65+ years

20

22

24

26

28

30

32

34

36

million people

Proportion pop 65 + years

Source: National Institute of Population & Social Security, Gov. of Japan

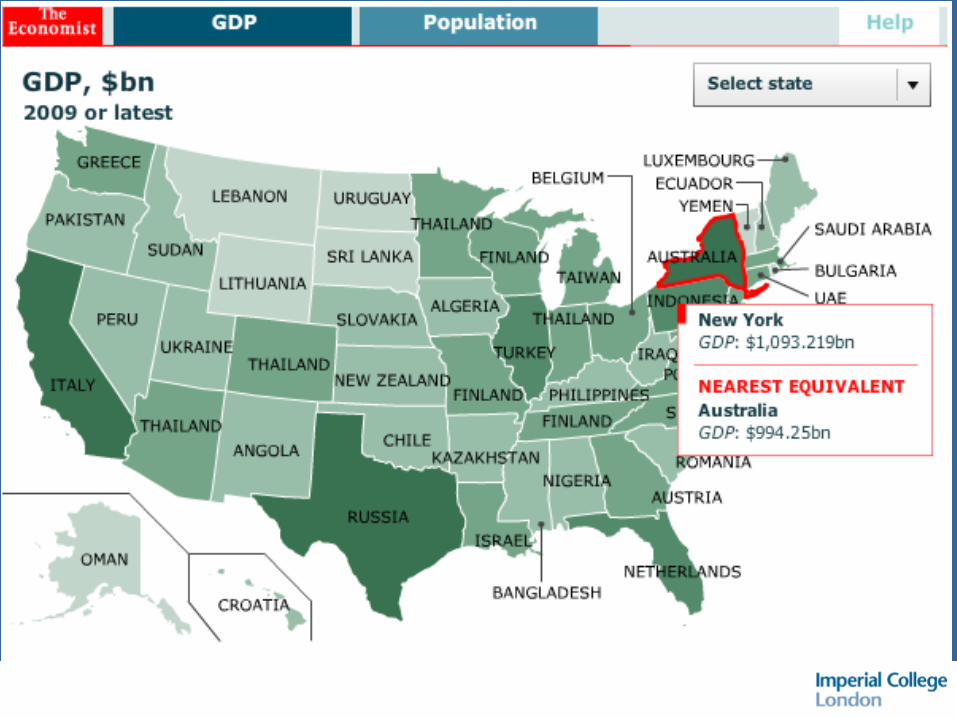

U.S. Protein Availability

Low/No Market Growth in Developed Countries with Existing High Meat and Dairy Product Consumption

• Population growth slow or declining • Ageing population with reduced food intake • Concerns re. impact of saturated fat on health* • Social pressures: concern about GHG/climate-

friendly diets, animal welfare, guilt re. grain-fed beef • For lower income groups, migration to lower-priced

products (e.g. white meats, processed cheese) • But, for higher income groups, premium “special

treat” meats, dairy nutraceuticals, weight management/muscle-building products have appeal

* Particularly, older consumers; exacerbated by periodic food industry safety scares * Clear threat of “satfat taxes” on butter/cheese/full fat products

World Population: Who's Going Up and Who’s Going Down?

2010 2030 2050 - billion-

World 6.9 8.2 9.0 Africa 1.0 1.5 2.0 Asia 4.1 4.8 5.1 Europe 0.7 0.7 0.7 LAC* 0.6 0.7 0.8 North America 0.3 0.4 0.5 Oceania 0.04 0.04 0.05

*Latin America & Caribbean Source: UN (population scenario planning)

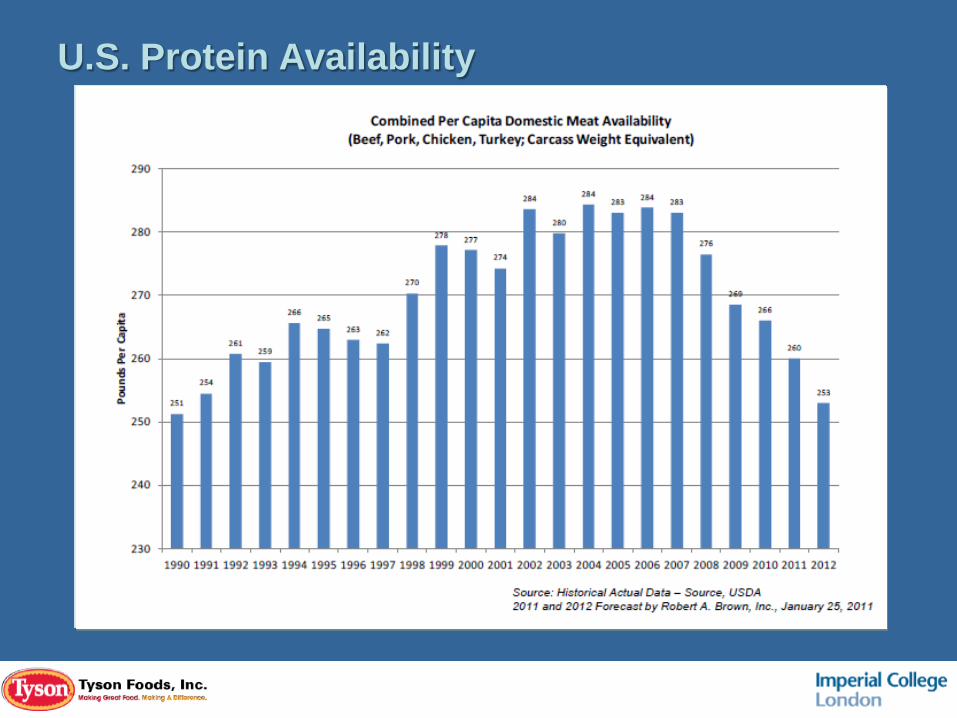

Source: Financial Times, 24/4/12

Market Size of Infant Nutrition Business by Major Region

World Meat Consumption* 2007-2012 2007 2012 p.a.%

Total meat consumption 223 mill. t. 239 1.3

Of which %: % Pork 40 41 Poultry 32 34 Beef 24 21 Sheep/lamb 4 3 Global meat consumption increased by 16 million tonnes

between 2007 and 2012 and most of growth was in emerging countries and was for chicken

* Not including fish and seafood

World Meat Consumption* Excluding China

2007 2012 p.a.%

Total meat consumption 158 mill. t. 164 <1 Of which %: % Pork 30 29 Poultry 38 41 Beef 29 28 Sheep/lamb 3 3 But 10 of 16 million tonnes global growth is in China!

* Not including fish and seafood

China: Share of Global Meat Consumption by Species

Species % Global Consumption Pork 52 Sheep/lamb 40 Fish & seafood 30 Poultry 18 Beef 9

FAO Global Food Price Index: 1990 to 2012*

Source: FAO * to August 2012 (September 4th, 2012)

Drought Areas in the USA, July 2012

Source: The Economist July 21st-27th, 2012

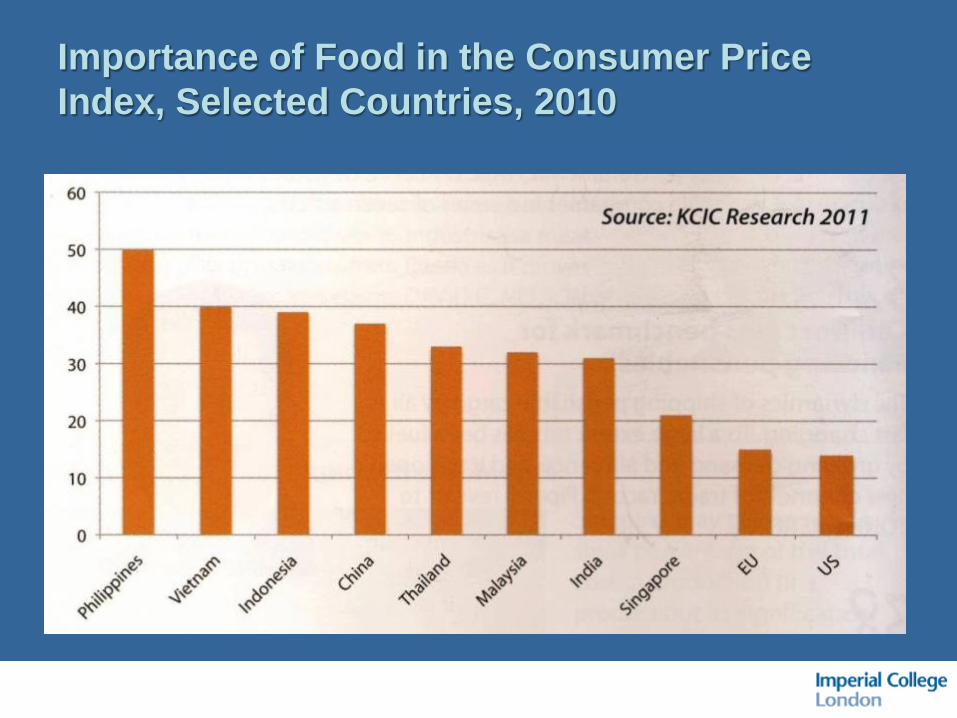

Importance of Food in the Consumer Price Index, Selected Countries, 2010

May 2011

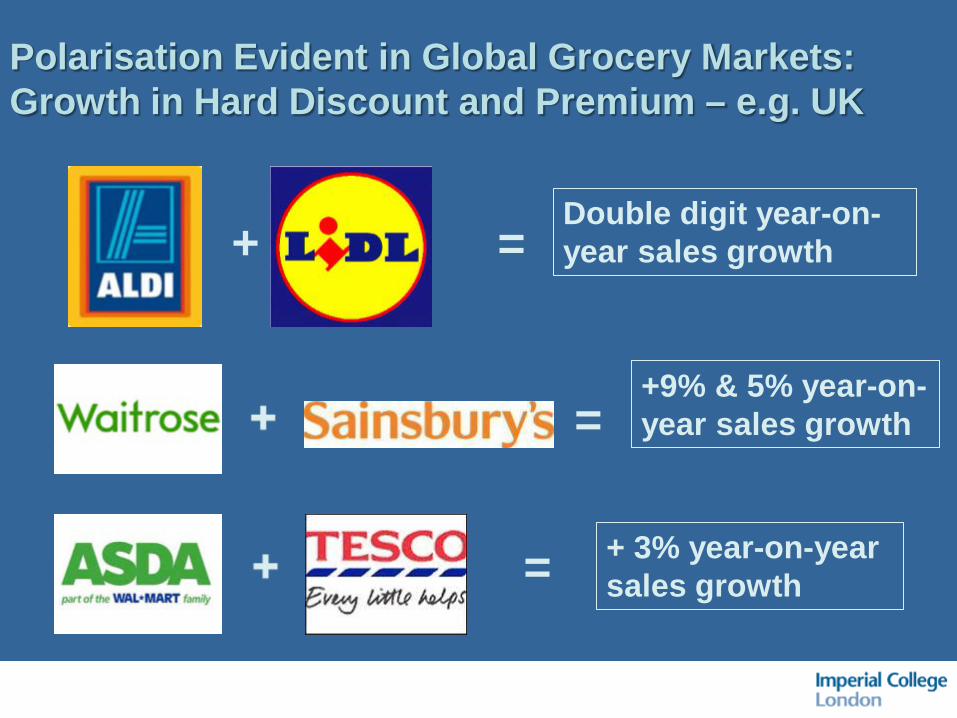

Polarisation Evident in Global Grocery Markets: Growth in Hard Discount and Premium – e.g. UK

+ Double digit year-on-year sales growth

+9% & 5% year-on-year sales growth

+ 3% year-on-year sales growth

=

=

=

On-line shopping and integration with store pick-up

Focus on smaller stores

Food Retail Evolving and Converging with Food Service

Reinventing the hypermarket

Strong retail specialists

Food retail and food service converge

Virtual Shopping in Gatwick Airport North Terminal

UK Waitrose Supermarket: £10 (AUD15) Meal for Two: one main; one side, one dessert; and a bottle of wine. Good Deal or What!

The Notion of “Eating Out In”! See, also, in Woolies: “5 Dishes for R150”

VALUE VALUES

HERITAGE PROVENANCE

PACK SIZE

ETHICS SUSTAINABILITY

PERFORMANCE

PROMOTIONS

PRICE

Values: For Shoppers, It’s Not ONLY about Price

Source: IGD 2012

Customer Hierarchy at Coles Supermarket…

Kind to others

Back to Nature

Good for me, my family

Legal & safe

Source: Coles Supermarket, Australia

Jamie Oliver: Not Everyone’s Favourite Celebrity Chef in USA

Shoppers: not always rational/logical

Warning: This Product May Explode on March 12th, 2023 at 4.30 pm!

It’s a Challenge to Claim “All Natural Ingredients” with a 12 Year Shelf Life!

41%

36%

27%

25%

22%

21%

14%

10%

9%

7%

6%

4%

3%

2%

0% 5% 10% 15% 20% 25% 30% 35% 40% 45%

They Are Better Quality

Healthier

They Are A Treat

I Can Afford Them

They Are For Special Occasions

I Know I Will Like Them

Organic/ Natural Ingredients

More Ethically Produced

They Are Better For The Environment

I Will Spend More On Food For My Children

Special Dietary Needs E.G Gluten Free

Endorsed By A Brand Or An Organisation I Like And Trust

Religious Beliefs Eg Halal, Kosher

I Want To Impress My Friends

Reasons for paying more for food and drink

Thinking about food and drink that you are willing to pay more for, what are the most important reasons for doing so?

• Key Findings

• As many as 1 in 7 (14%) shoppers are willing to pay more for organic food

• 1 in 10 are willing to pay more for ethically produced goods and a similar number (9%) for goods that are better for the environment .

Business, Academia, Governments and NGO’s seeking new directions for green strategies

Business Members Include:

"We want to grow from the respected and trustworthy food company that we are known as now, into a respected and

trustworthy food, nutrition and wellness company“

Peter Brabeck-Letmathe Blue Print for the Future, October 2001

Nestlé Health Science S.A. and Nestlé Institute of Health Sciences established to target new opportunity between food and pharma Vevey, Switzerland, September 27, 2010

Creating Corporate and Social Value Through Sharing Values with Partners in the Supply Chain

• “Big Food” is “under the gun”! The bigger the brand, the bigger the risks for the brand owner

• brand owners will require supply chain partners who understand, share and live core values

• major suppliers of all inputs will carry the “brand integrity torch” for the brand owners

• branded supply chain partnerships will be closer and longer-lasting than commodity supply chains

• business models are changing, led by global fmcg firms, Major retailers, QSR and manufacturers will be expected to lead on safety and sustainability initiatives

•

For Food and Drink Products, Taste/Smell is Paramount but What About the Story? • When it comes to communicating the story to the

consumer, who is the hero/heroine?: - the country of production; - the region/local area; - the processor and/or farmer; - the production process; - the product; - the animals/produce/the ingredients; - the heritage/tradition/terroir; - all of the above?!

From a Consumer Perspective, What Are You Famous For in Global Export Markets?

Country Famous For Best Known Food Germany Engineering Sausage, beer, sauerkraut Mexico Hats, illicit drugs Tequila. burritos Italy Racing cars, fashion Pasta, olive oil, cheese, ham …. Ireland St. Patrick’s Day, charm Guinness, potatoes Japan Cars, electrical goods Sushi England Royalty, pop music Cream teas, fish & chips USA High tech, Hollywood Burgers, hot dogs, big portions Australia Sport, swimwear Wine, barbies (BBQ) South Africa Mandela, diamonds, gold Biltong!

Some Concluding Thoughts

• Don’t write off the old developed countries – that’s where the wealth is but not the growth

• If China stutters, we’ll all stumble! • Volatile global food price outlook will constrain

demand for protein foods and exacerbate political instability in emerging countries

• “The Green Train” has left the station get on board! • Big fmcg changing their business models – from

CSR to CSV • Supply chain relationships mature and strengthen

driven by the need to protect brand value

CONTACT POINTS: e-mail

telephone numbers office +44(0)1600 715957 fax +44(0)1600 712544 mobile +44(0)7798 558276

Check my latest podcast at www.profdavidhughes.com

Bye Bye Corporate Social Responsibility (CSR) and Welcome to Creating Shared Value (CSV) Value: doing good Citizenship, philanthropy,

sustainability Discretionary or in response to

external pressure Separate from profit

maximization Agenda is determined by

external reporting and personal preferences

Impact limited by corporate footprint and CSR budget

Example: Fair Trade purchasing

Value: economic and societal benefits relative to cost

Joint company and community value creation

Integral to competing Integral to profit maximization

Agenda is company specific

and internally generated

Realigns the entire company budget

Example: Transforming procurement in tea/coffee to increase quality and yield

Source: Harvard Business Review ”Creating Shared Values”, Porter, etc. 2011

Michael Porter’s “Big Idea” for Business What’s Good for Global Business is Good for the World Turned on Its Head: What’s Good for Our World – its citizens’ health, the environment, future generations, disadvantaged groups ....., etc. - is Good for Global Business

M. Porter and M. Kramer, “Creating Shared Value”, Harvard Business Review, Jan/Feb, 2011