Embed Size (px)

Citation preview

CONSTRUCTING AN OPTIMAL PORTFOLIO USING SHARPE

SINGLE INDEX MODEL

Dr. SAROJ KANTA BISWAL

Assistant Professor (Finance & Control), Institute of Business & Computer Studies, Faculty of

Management Sciences, Siksha „O‟ Anusandhan University, Bhubaneswar 751003, Odisha, India

ABSTRACT

To make wise decisions in investment, there is a need for knowledge on security analysis and

portfolio management. A rational investor aims at attaining maximum return with minimum risk. As

the scope of investment avenues with varying degrees of risk is vast, the scope of the present study is

relating to equity portfolio construction with selected stocks from the BSE. Constructing an optimal

portfolio is a challenging task for the individual as well as the institutional investors. This study is

aimed at creating awareness in the minds of investors regarding the utility of Sharpe‟s Single Index

Model in portfolio construction. The Indian investors also may reap the benefits of Sharpe‟s Single

Index Model (SIM) as the number of companies traded in the stock exchanges is increasing year after

year. 40 S&P 100 BSE Sensex index listed companies having large market capitalization were

selected for the study. Among the 40 sample companies, 23 were selected for optimal portfolio using

SIM. The results of the present study and such micro level studies have more utility value to the fund

managers.

Introduction

Investment in the equity market is a risky and quick way of maximizing returns rather than investing

in the financial instruments at a risk-free rate. The aim of the risk-averse investors is always to

maximize return at a given level of risk or to minimize risk at a given level of return. Risks in the

stock market can be classified into two types: Systematic risk or Non-Diversifiable risk and

Unsystematic risk or Firm-Specific risk. Investment is the employment of funds on assets with the

aim of earning income or capital appreciation. Every investment involves a return and risk. The

possibility of variation in the actual return is known as investment risk. To make wise decisions in

investment, there is a need for knowledge on security analysis and portfolio management. A portfolio

is a combination of securities. Any portfolio constructed, either by an individual investor or a fund

manager is expected to meet the investor‟s goals. A rational investor aims at attaining maximum

return with minimum risk. It is, therefore, important to construct a portfolio using either of the two

popular approaches, namely, traditional and modern. In the traditional approach, investor‟s needs in

terms of income and capital appreciation are evaluated and appropriate securities are selected to meet

the needs of the investor. Investors usually invest in a portfolio of stocks to eliminate non-systematic

risk, but systematic risk cannot be avoided as it arises out of the market factors like GDP, inflation,

exchange rate fluctuations. Portfolio theory was originally proposed by Harry Markowitz who

attempted to quantify the risk of a portfolio and developed a procedure for determining the optimal

portfolio. However, the Markowitz theory was to complex and cumbersome to determine the optimal

portfolio. Markowitz model is used in selection of securities based on to the risk and return analysis.

Markowitz laid foundation for quantifying risk and his contribution is popularly known as „Modern

Portfolio Theory‟. He has provided analytical tools for analysis and selection of optimal portfolio. He

won Nobel Prize for this contribution to portfolio management in 1990.

But, William Sharpe extended the work done by Markowitz. He considered market index while

analyzing the portfolio. He simplified the amount and type of input data required to perform portfolio

analysis. He made the numerous and complex computations easy which were essential to attain the

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 17 [email protected]

optimal portfolio. He developed the Single Index Model to make these computations easy and

construct an optimal portfolio. Till today, fund managers use this model in portfolio analysis and

construction. Hence, William Sharpe developed the single index model to determine the optimal

portfolio, which made the calculations based on the statistical concept of regression between stock

returns and market returns. Sharpe‟s model expresses the returns on each security as a function of a

return on the market index. Thus this study is fully based on Sharpe index model aiming at

constructing an optimal portfolio of selected stocks by choosing from different sectors in the Indian

economy in the period June 2005 to June 2015. Indian investors also may reap the benefits of

Sharpe‟s Single Index Model as the number of companies traded in the stock exchanges is increasing

year after year. The Bombay Stock Exchange Ltd (BSE) that was established in 1875 is the Asia‟s

First Stock Exchange and one of the leading exchanges in India. Over the past 137 years, the BSE has

facilitated the growth of the Indian corporate sector by providing it an efficient capital-raising

platform. It provides an efficient and transparent market for trading in equity, debt instruments,

derivatives, mutual funds. More than 5000 companies are listed on BSE making it world's No. 1

exchange in terms of listed members. BSE‟s popular equity index - the S&P BSE SENSEX - is India's

most widely tracked stock market benchmark index. As on 25th

June 2015 the total turnover of the

index being Rs. 6,522,378.74 and the index value 27780.83. Bearing these in mind, the present

study was undertaken to facilitate effective decision making by the investors.

Assumptions

All investors have homogeneous expectations.

A uniform holding period is used in estimating risk and return for each security.

The price movements of a security in relation to another do not depend primarily upon the

nature of those two securities alone. They could reflect a greater influence that might have

cropped up as a result of general business and economic conditions.

The relation between securities occurs only through their individual influences along with

some indices of business and economic activities.

The indices, to which the returns of each security are correlated, are likely to be some

securities‟ market proxy.

The random disturbance terms „Ɛi‟ has an expected value zero and a finite variance. It is not

correlated with the rate of return on market portfolio „Rm‟ as well as with the error term of

any other securities.

Objective of the Study

To construct an optimal portfolio empirically using the Sharpe‟s Single Index Model.

To determine return and risk of the optimal portfolio constructed by using Sharpe‟s

Single Index Model.

Review of Literature

Tripathy, Sasikanta (2011) applied the model on selected Indian banks‟ securities. The author

assumed that there is a positive relationship between the banked and individual stocks. Fifteen

securities selected of the banks comprised in BANKEX as a sample. The data is based on secondary

source for the period from 1st April 2011 to 31st march 2012. It was found that there is a linear

relationship between security returns and the common factor that there is no difference among the

return of all the banks from the ANOVA.

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 18 [email protected]

Varadharajan and Ganesh (2012) applied the SIM on equity portfolio of large caps companies of

selected sectors in India. The main aim of this study is to find out the optimum portfolio from the

selected companies in three major sectors like power sector, shipping sector and textile sector. From

each sector six companies have been selected and so a total of eighteen companies are selected as

samples. The companies with the largest market capitalization in each sector have been selected. Data

for five financial years were used for constructing the portfolio; i.e. from 1st April 2006 to 31st march

2011. All calculations have been done using MS Excel. From the analysis it was found that only five

companies were included in the portfolio constructed out of the eighteen companies.

Varadharajan and Ganesh (2012) applied the SIM on equity portfolio of large caps companies of

selected sectors in India. The main aim of this study is to find out the optimum portfolio from the

selected companies in three major sectors like power sector, shipping sector and textile sector. From

each sector six companies have been selected and so a total of eighteen companies are selected as

samples. The companies with the largest market capitalization in each sector have been selected. Data

for five financial years were used for constructing the portfolio; i.e. from 1st April 2006 to 31st march

2011. All calculations have been done using MS Excel. From the analysis it was found that only five

companies were included in the portfolio constructed out of the eighteen companies. the fifty

companies in S&P CNX Nifty only six securities were selected for the optimal portfolio construction.

The percentage of investment to be made in the selected securities has been calculated using Sharpe‟s

Single Index Model. The study reveals that stock prices and market index move in the same direction.

Sarker, Mokta Rani (2013) conducted a study to construct an optimal portfolio using Sharpe‟s Single

Index Model considering no short sales. The study has been conducted on individual securities listed

in Dhaka Stock Exchange, where short sales are not allowed. The monthly closing prices of one

hundred and sixty four companies listed in Dhaka Stock Exchange and share price index for the

period of July 2007 to June 2012 have been considered in this study. This method formulates a unique

cut-off point, selects stocks having excess return to beta ratio surpassing this cut-off point and

determines the percentage of investment to be made in in each of selected stocks. The optimum

portfolio consists of thirty three stocks selected out of one hundred and sixty four stocks giving the

return of 6.17%. From this empirical analysis to some extent, an investor can forecast individual

securities return through the market movement and can make use of it.

Desai, Radhika and Surti, Manisha (2013) constructed an optimal portfolio using fifty companies

which were listed on the NSE and the time duration of the study is three years. Among the fifty

companies only ten companies were selected for the optimum portfolio. The proportion of investment

made in each security has been calculated using the Sharpe‟s Single Index Model. The volatility of

security has been analysed. The research provides direction to investors regarding performance of

securities. Once the performance is analyzed and optimum portfolio of securities is constructed, it

enables the investor to take appropriate decisions. Gopalakrishna, Muthu (2014) explains the

investment alternatives available for rational investor. A comparison of traditional portfolio theory

with that of modern portfolio theory is made in this study. This study aims to test whether single index

model offers an appropriate explanation of stock returns on IT stocks. The samples included in this

study consists of 13 actively traded securities listed in the National Stock Exchange Limited, Bombay

(NSE).The securities in the sample are selected from NSE IT index. The secondary data for a period

2004-2008 has been used for the study. By applying regression on the market return and excess

security return it is found that IT index has a phenomenal amount of sensitiveness over S&P CNX

Nifty. The study investigated that there are four aggressive stocks having beta coefficient of more

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 19 [email protected]

than one. It is recommended that among the sample companies all the stocks are undervalued except

one stock and thus the investors can pick these stocks to revise their portfolio.

Methodology

This is a descriptive study on the construction of portfolio of stocks. The data taken for the study is

Secondary in nature. The data has been collected from various websites like BSE India &

MoneyControl.com. Taking the computed return of each security and the market, the proposed

method formulates a unique Cut off Rate and selects those securities whose „Excess Return-to-Beta

Ratio‟ is greater than the cut off rate. Then to arrive at the optimal portfolio, the proportion of

investment in each of the selected securities in the optimal portfolio is computed on the basis of beta

value, unsystematic risk, excess return to beta ratio and the cut off rate of the security concerned.

Different Statistical and Financial tools and techniques, charts and diagrams have been used for the

purpose of analysis and interpretation of data. For this study the following methodology / model is

used to construct an Optimal Portfolio:

Sharpe’s Single Index Model

Sharpe‟s Model proposes that the relationship between each pair of securities can indirectly be

measured by comparing each security to a common factor „market performance index‟ that is shared

amongst all the securities. This helps in reducing the burden of large input requirements and difficult

calculations required in Markowitz‟s mean- variance approach. While Markowitz Model requires n

(n−1)/ 2 data inputs, the Sharpe‟s Model requires only (3n+2) data inputs, namely, the estimates of

returns for each security, estimates for expected return on market index and estimates of variance of

return. This forms the essence of Sharpe‟s Model which has made financial analysts and researchers

to consider it superior to the Markowitz Model. It is based on the assumption that when the market

moves up most of the stock prices also tends to increase and vice versa. Therefore, securities returns

are correlated and there might be co-movement between securities because of common response to

market changes.

This co-movement of stocks with the market index is studied with the help a simple regression

analysis:

R i = αi +βi Rm + ei

Where R I = Return on individual security

αi = Independent of the market performance

βi = Measure of the expected change in individual stock return to the change in market return

Rm = Return of the market index

ei = Error term representing the random disturbance.

Beta

Beta coefficient is the relative measure of systematic risk. Beta of an investment is a measure of the

risk arising from exposure to general market movements as opposed to idiosyncratic factors. The

market portfolio has a beta of exactly one.

βi = COV(I, m) = σi * σm * Correl (I, m)

Var (Rm) σm 2

Return

The total gain or loss experienced on an investment over a given period of time, calculated by

dividing the difference in ending price and beginning Price during the period with the total period of

investment value is termed as return.

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 20 [email protected]

Risk-Free Rate of Return (Rf)

Risk-free rate of return is the return on a security that is free from default risk and is uncorrelated with

returns from anything else in the economy. A 364 day treasury bill rate.

Excess Return to Beta

Excess return-to-beta ratio = Ri - Rf

βi

Where Rf = risk free return

Ri = return on security

βi = the expected change in the rate of return on stock associated with one unit change in the

market return

Cutoff Point (C*)

Where σ2

m= Variance of market

σ2ei = Unsystematic Risk

Proportion to Be Invested

Where Xi= Proposed invested to be made on any security

Where C* = Cut-off point

Limitations

Portfolio is constructed based only on risk and return assuming that stock returns are

normally distributed.

Study is restricted to only 40 securities from BSE 100 with respect to large market

capitalization.

Stock prices considered are restricted to only the previous 10 year‟s monthly closing

prices.

The portfolio is constructed purely on the basis of Sharpe‟s model which basically

considers the stock price movements and does not take into consideration company

specific factors, industry specific factors and economic specific factors

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 21 [email protected]

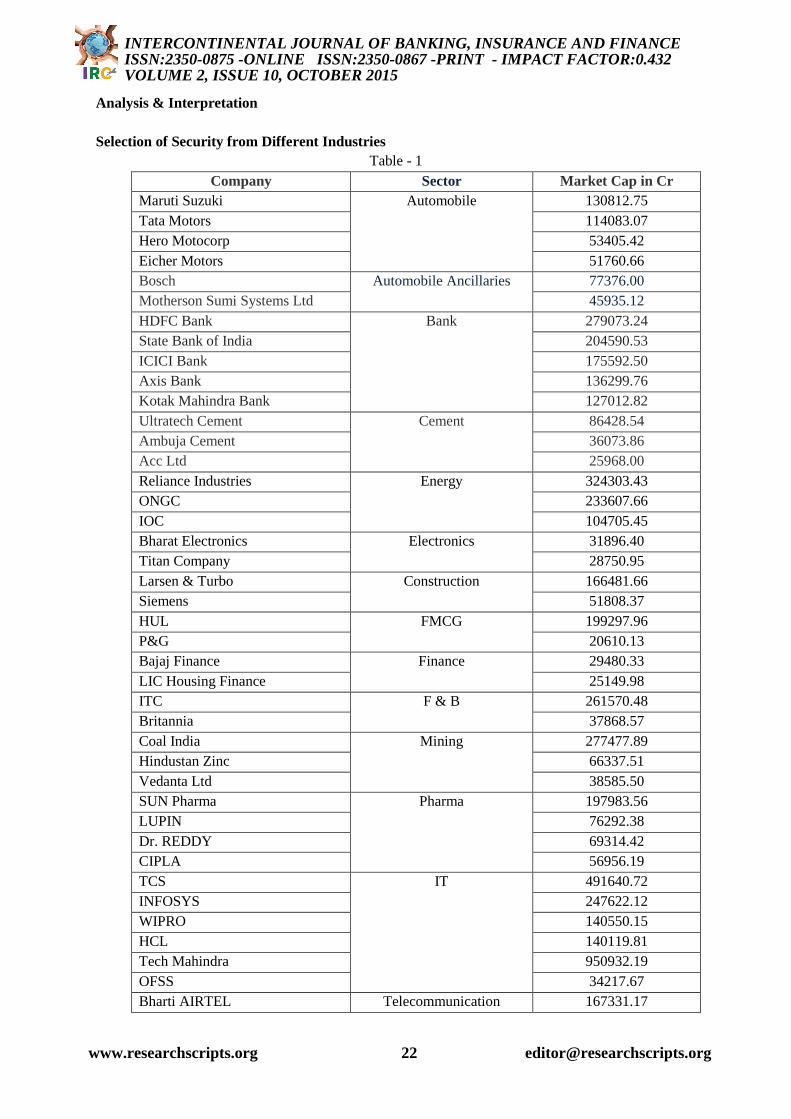

Analysis & Interpretation

Selection of Security from Different Industries

Table - 1

Company Sector Market Cap in Cr

Maruti Suzuki Automobile 130812.75

Tata Motors 114083.07

Hero Motocorp 53405.42

Eicher Motors 51760.66

Bosch Automobile Ancillaries 77376.00

Motherson Sumi Systems Ltd 45935.12

HDFC Bank Bank 279073.24

State Bank of India 204590.53

ICICI Bank 175592.50

Axis Bank 136299.76

Kotak Mahindra Bank 127012.82

Ultratech Cement Cement 86428.54

Ambuja Cement 36073.86

Acc Ltd 25968.00

Reliance Industries Energy 324303.43

ONGC 233607.66

IOC 104705.45

Bharat Electronics Electronics 31896.40

Titan Company 28750.95

Larsen & Turbo Construction 166481.66

Siemens 51808.37

HUL FMCG 199297.96

P&G 20610.13

Bajaj Finance Finance 29480.33

LIC Housing Finance 25149.98

ITC F & B 261570.48

Britannia 37868.57

Coal India Mining 277477.89

Hindustan Zinc 66337.51

Vedanta Ltd 38585.50

SUN Pharma Pharma 197983.56

LUPIN 76292.38

Dr. REDDY 69314.42

CIPLA 56956.19

TCS IT 491640.72

INFOSYS 247622.12

WIPRO 140550.15

HCL 140119.81

Tech Mahindra 950932.19

OFSS 34217.67

Bharti AIRTEL Telecommunication 167331.17

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 22 [email protected]

TABLE 2: Return on Market Index i.e BSE 100

BSE 100 MARKET INDICES

Mean Return .01443772984

Standard Deviation 0.073963027

Variance 0.005470529

The above table shows the return on Market index being selected that is BSE 100. Monthly data is being

considered and return is being calculated.

Rm = Mean (return)

Table 3: Return on Security

SECURITY αi βi Rm βi*Rm Error term Ri

TCS 2.451234031 0.448897144 0.01443773 0.006481056 0 2.457715087

INFOSYS 1.817751352 1.044335965 0.01443773 0.015077841 0 1.832829193

RELIANCE 1.87619113 1.049073404 0.01443773 0.015146238 0 1.891337368

HDFC BANK 2.806807257 0.645212301 0.01443773 0.009315401 0 2.816122658

SBI 2.220513511 1.232359113 0.01443773 0.017792468 0 2.238305979

SUN PHARMA 3.170838356 0.524741022 0.01443773 0.007576069 0 3.178414425

ICICI 2.303594383 1.526522055 0.01443773 0.022039513 0 2.325633896

LARSEN 3.25517341 1.509290131 0.01443773 0.021790723 0 3.276964134

AXIS 3.428259981 1.393530211 0.01443773 0.020119413 0 3.448379394

ITC 2.089953093 0.467667115 0.01443773 0.006752051 0 2.096705145

TATA MOTORS 2.824642078 1.459165373 0.01443773 0.021067035 0 2.845709113

WIPRO 1.471901452 0.787351949 0.01443773 0.011367575 0 1.483269027

ONGC 1.25334961 0.970491274 0.01443773 0.014011691 0 1.267361301

HCL 2.983352695 0.777932315 0.01443773 0.011231577 0 2.994584271

MARUTI SUZUKI 2.819303236 0.439400067 0.01443773 0.006343939 0 2.825647176

BOSCH 2.588465563 0.310569145 0.01443773 0.004483913 0 2.592949476

HERO MOTO CORP 1.927633752 0.609289733 0.01443773 0.008796761 0 1.936430512

OFSS 2.546216744 0.780873834 0.01443773 0.011274045 0 2.557490789

HUL 2.225700162 0.407560174 0.01443773 0.005884244 0 2.231584406

BHARTI AIRTEL 1.827256971 0.763055176 0.01443773 0.011016784 0 1.838273755

KOTAK MAHINDRA 3.964039724 1.490407195 0.01443773 0.021518096 0 3.98555782

LUPIN 3.860971324 0.46319365 0.01443773 0.006687465 0 3.867658789

Dr. REDDY 2.830317452 0.55573222 0.01443773 0.008023512 0 2.838340963

EICHER MOTORS 5.040621784 0.862577941 0.01443773 0.012453667 0 5.053075452

CIPLA 2.051992928 0.410829285 0.01443773 0.005931442 0 2.05792437

BRITANNIA 3.181048062 0.401861962 0.01443773 0.005801974 0 3.186850036

SIEMENS 3.076748669 1.497617725 0.01443773 0.0216222 0 3.09837087

ULTRA TECH CEMENT 3.050132896 1.030900531 0.01443773 0.014883863 0 3.065016759

P&G 2.7082025 0.3307633 0.01443773 0.004775471 0 2.712977971

BAJAJ FINANCE 4.40748051 1.202054609 0.01443773 0.01735494 0 4.424835449

ACC 1.951868637 0.900389661 0.01443773 0.012999583 0 1.964868219

TITAN 4.03512204 1.017602094 0.01443773 0.014691864 0 4.049813904

BHARAT ELECTRONICS 2.3502451 1.066165894 0.01443773 0.015393015 0 2.365638115

COAL INDIA 0.914262981 0.752528511 0.01443773 0.010864803 0 0.925127785

HINDUSTAN ZINC 3.762820913 1.257420921 0.01443773 0.018154304 0 3.780975217

IOC 1.36149231 0.881188824 0.01443773 0.012722366 0 1.374214676

AMBUJA CEMENT 1.905053808 0.935018772 0.01443773 0.013499548 0 1.918553357

LIC HOUSING FINANCE 3.45279152 1.489796679 0.01443773 0.021509282 0 3.474300802

MOTHERSON SUMI 3.912806205 1.030655294 0.01443773 0.014880323 0 3.927686528

VEDANTA 3.871020026 1.500592035 0.01443773 0.021665142 0 3.892685168

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 23 [email protected]

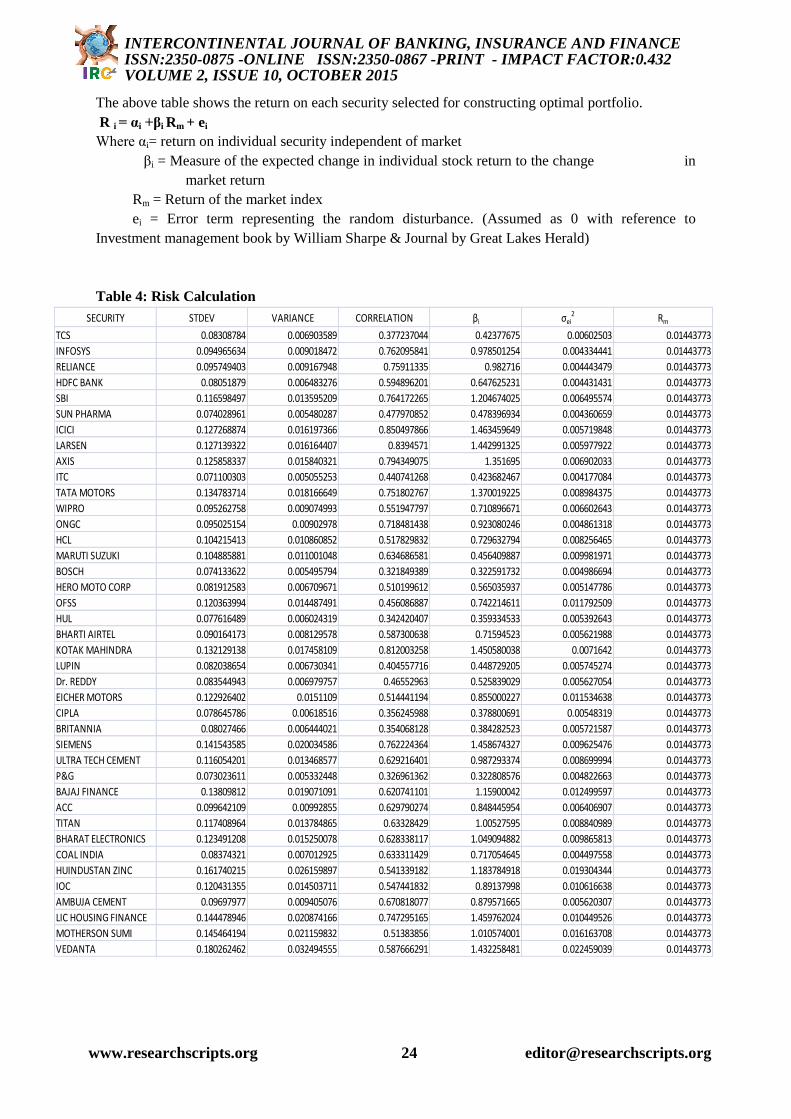

The above table shows the return on each security selected for constructing optimal portfolio.

R i = αi +βi Rm + ei

Where αi= return on individual security independent of market

βi = Measure of the expected change in individual stock return to the change in

market return

Rm = Return of the market index

ei = Error term representing the random disturbance. (Assumed as 0 with reference to

Investment management book by William Sharpe & Journal by Great Lakes Herald)

Table 4: Risk Calculation

SECURITY STDEV VARIANCE CORRELATION βi σei2 Rm

TCS 0.08308784 0.006903589 0.377237044 0.42377675 0.00602503 0.01443773

INFOSYS 0.094965634 0.009018472 0.762095841 0.978501254 0.004334441 0.01443773

RELIANCE 0.095749403 0.009167948 0.75911335 0.982716 0.004443479 0.01443773

HDFC BANK 0.08051879 0.006483276 0.594896201 0.647625231 0.004431431 0.01443773

SBI 0.116598497 0.013595209 0.764172265 1.204674025 0.006495574 0.01443773

SUN PHARMA 0.074028961 0.005480287 0.477970852 0.478396934 0.004360659 0.01443773

ICICI 0.127268874 0.016197366 0.850497866 1.463459649 0.005719848 0.01443773

LARSEN 0.127139322 0.016164407 0.8394571 1.442991325 0.005977922 0.01443773

AXIS 0.125858337 0.015840321 0.794349075 1.351695 0.006902033 0.01443773

ITC 0.071100303 0.005055253 0.440741268 0.423682467 0.004177084 0.01443773

TATA MOTORS 0.134783714 0.018166649 0.751802767 1.370019225 0.008984375 0.01443773

WIPRO 0.095262758 0.009074993 0.551947797 0.710896671 0.006602643 0.01443773

ONGC 0.095025154 0.00902978 0.718481438 0.923080246 0.004861318 0.01443773

HCL 0.104215413 0.010860852 0.517829832 0.729632794 0.008256465 0.01443773

MARUTI SUZUKI 0.104885881 0.011001048 0.634686581 0.456409887 0.009981971 0.01443773

BOSCH 0.074133622 0.005495794 0.321849389 0.322591732 0.004986694 0.01443773

HERO MOTO CORP 0.081912583 0.006709671 0.510199612 0.565035937 0.005147786 0.01443773

OFSS 0.120363994 0.014487491 0.456086887 0.742214611 0.011792509 0.01443773

HUL 0.077616489 0.006024319 0.342420407 0.359334533 0.005392643 0.01443773

BHARTI AIRTEL 0.090164173 0.008129578 0.587300638 0.71594523 0.005621988 0.01443773

KOTAK MAHINDRA 0.132129138 0.017458109 0.812003258 1.450580038 0.0071642 0.01443773

LUPIN 0.082038654 0.006730341 0.404557716 0.448729205 0.005745274 0.01443773

Dr. REDDY 0.083544943 0.006979757 0.46552963 0.525839029 0.005627054 0.01443773

EICHER MOTORS 0.122926402 0.0151109 0.514441194 0.855000227 0.011534638 0.01443773

CIPLA 0.078645786 0.00618516 0.356245988 0.378800691 0.00548319 0.01443773

BRITANNIA 0.08027466 0.006444021 0.354068128 0.384282523 0.005721587 0.01443773

SIEMENS 0.141543585 0.020034586 0.762224364 1.458674327 0.009625476 0.01443773

ULTRA TECH CEMENT 0.116054201 0.013468577 0.629216401 0.987293374 0.008699994 0.01443773

P&G 0.073023611 0.005332448 0.326961362 0.322808576 0.004822663 0.01443773

BAJAJ FINANCE 0.13809812 0.019071091 0.620741101 1.15900042 0.012499597 0.01443773

ACC 0.099642109 0.00992855 0.629790274 0.848445954 0.006406907 0.01443773

TITAN 0.117408964 0.013784865 0.63328429 1.00527595 0.008840989 0.01443773

BHARAT ELECTRONICS 0.123491208 0.015250078 0.628338117 1.049094882 0.009865813 0.01443773

COAL INDIA 0.08374321 0.007012925 0.633311429 0.717054645 0.004497558 0.01443773

HUINDUSTAN ZINC 0.161740215 0.026159897 0.541339182 1.183784918 0.019304344 0.01443773

IOC 0.120431355 0.014503711 0.547441832 0.89137998 0.010616638 0.01443773

AMBUJA CEMENT 0.09697977 0.009405076 0.670818077 0.879571665 0.005620307 0.01443773

LIC HOUSING FINANCE 0.144478946 0.020874166 0.747295165 1.459762024 0.010449526 0.01443773

MOTHERSON SUMI 0.145464194 0.021159832 0.51383856 1.010574001 0.016163708 0.01443773

VEDANTA 0.180262462 0.032494555 0.587666291 1.432258481 0.022459039 0.01443773

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 24 [email protected]

The above table shows the calculation of standard deviation, variance, systematic risk and

unsystematic risk of each security.

σi = sqrt ((xi-xi)/N)

βi= Cov(I,m)

σei2= σi- βi

2 Rm

2

Table 5: Risk Free Return Or 364 Day T-Bill Rate

YEAR T-BILL RATE

2005 6.17

2006 7.23

2007 7.66

2008 4.78

2009 4.72

2011 7.48

2012 8.68

2013 8.26

2014 7.78

2015 7.56

70.32

Mean 0.07032

The above table shows the risk free return which is being calculating the average of 364 days T Bill

rate to calculate excess return to Beta.

Rf = Avg (10yr T bill)

Table 5: Excess Return to Beta

The above table shows the calculation of excess return to beta. This single value exists in Sharpe‟s

Single Index Model where it is found that the desirability of any security is directly related to its

„excess return to beta ratio‟. This means that the desirability of any security is solely a function of its

excess return-to-beta ratio (Fischer & Jordan Book). If securities are ranked on the basis of excess

return-to-beta ratio (from highest to lowest), the ranking represents the desirability of including a

security in the portfolio.

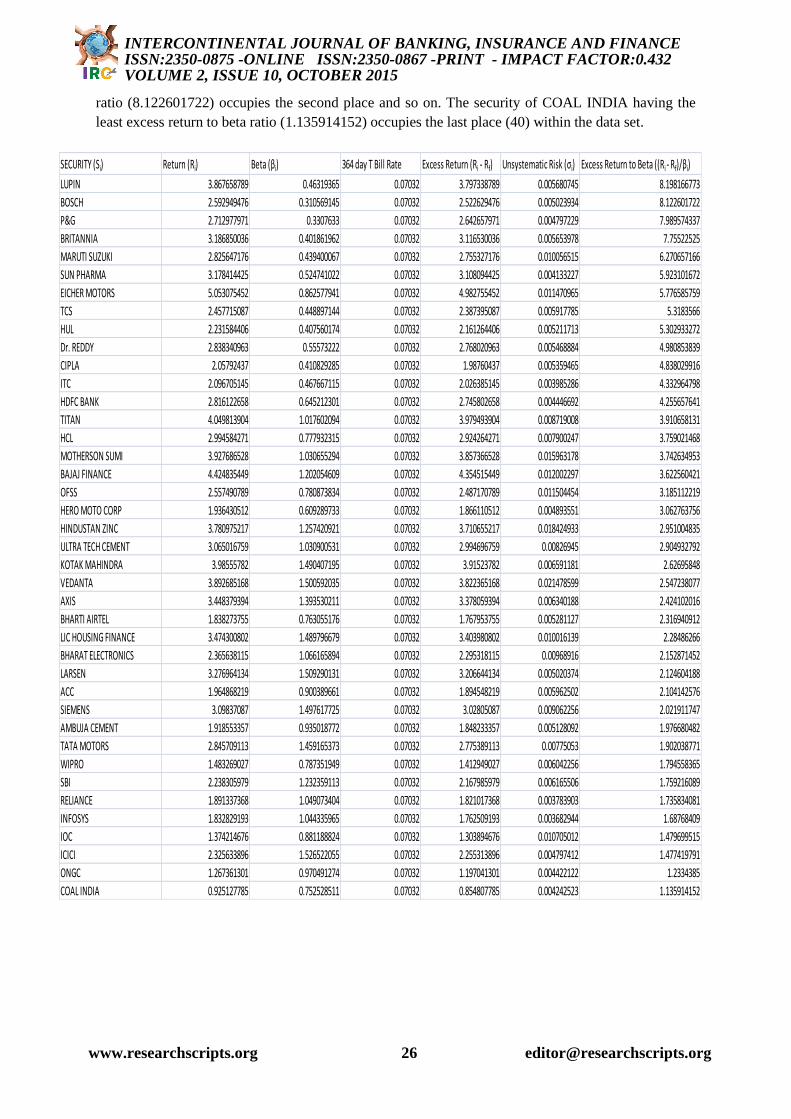

LUPIN yielded the maximum return among the companies selected and COAL INDIA yielded lower

return. Pharma have shown a higher return in all the companies chosen for the analysis. It shows that

Pharma is the growing sector and it is most preferred investable securities in India. Beta is greater

than 1 in 17 companies, which shows that these securities have more risk and at the same time the

reward per unit of risks is also more. But in case of other companies with regards to beta is less than 1

which shows it is less risky when compared to market risk.

Sharpe has provided a model for the selection of appropriate securities in a portfolio. The excess

return of any stock is directly related to its excess return to beta ratio. It measures the additional return

on a security (excess of the risk less asset return) per unit of systematic risk. The ratio provides a

relationship between potential risk and reward. Ranking of the stocks are done on the basis of their

excess return to beta. Based on the excess return to beta ratio the scrip‟s are ranked from 1 to 40, with

LUPIN being in the first rank and COAL INDIA being in the last. The excess return to beta ratio was

calculated using 7.032% as risk free rate of return.

It is clearly seen that the security of LUPIN, having the highest excess return to beta ratio

(8.198166773) occupies the first place. The security having the second highest excess return to beta

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 25 [email protected]

ratio (8.122601722) occupies the second place and so on. The security of COAL INDIA having the

least excess return to beta ratio (1.135914152) occupies the last place (40) within the data set.

SECURITY (Si) Return (Ri) Beta (βi) 364 day T Bill Rate Excess Return (Ri - Rf) Unsystematic Risk (σi) Excess Return to Beta ((Ri - Rf)/βi)

LUPIN 3.867658789 0.46319365 0.07032 3.797338789 0.005680745 8.198166773

BOSCH 2.592949476 0.310569145 0.07032 2.522629476 0.005023934 8.122601722

P&G 2.712977971 0.3307633 0.07032 2.642657971 0.004797229 7.989574337

BRITANNIA 3.186850036 0.401861962 0.07032 3.116530036 0.005653978 7.75522525

MARUTI SUZUKI 2.825647176 0.439400067 0.07032 2.755327176 0.010056515 6.270657166

SUN PHARMA 3.178414425 0.524741022 0.07032 3.108094425 0.004133227 5.923101672

EICHER MOTORS 5.053075452 0.862577941 0.07032 4.982755452 0.011470965 5.776585759

TCS 2.457715087 0.448897144 0.07032 2.387395087 0.005917785 5.3183566

HUL 2.231584406 0.407560174 0.07032 2.161264406 0.005211713 5.302933272

Dr. REDDY 2.838340963 0.55573222 0.07032 2.768020963 0.005468884 4.980853839

CIPLA 2.05792437 0.410829285 0.07032 1.98760437 0.005359465 4.838029916

ITC 2.096705145 0.467667115 0.07032 2.026385145 0.003985286 4.332964798

HDFC BANK 2.816122658 0.645212301 0.07032 2.745802658 0.004446692 4.255657641

TITAN 4.049813904 1.017602094 0.07032 3.979493904 0.008719008 3.910658131

HCL 2.994584271 0.777932315 0.07032 2.924264271 0.007900247 3.759021468

MOTHERSON SUMI 3.927686528 1.030655294 0.07032 3.857366528 0.015963178 3.742634953

BAJAJ FINANCE 4.424835449 1.202054609 0.07032 4.354515449 0.012002297 3.622560421

OFSS 2.557490789 0.780873834 0.07032 2.487170789 0.011504454 3.185112219

HERO MOTO CORP 1.936430512 0.609289733 0.07032 1.866110512 0.004893551 3.062763756

HINDUSTAN ZINC 3.780975217 1.257420921 0.07032 3.710655217 0.018424933 2.951004835

ULTRA TECH CEMENT 3.065016759 1.030900531 0.07032 2.994696759 0.00826945 2.904932792

KOTAK MAHINDRA 3.98555782 1.490407195 0.07032 3.91523782 0.006591181 2.62695848

VEDANTA 3.892685168 1.500592035 0.07032 3.822365168 0.021478599 2.547238077

AXIS 3.448379394 1.393530211 0.07032 3.378059394 0.006340188 2.424102016

BHARTI AIRTEL 1.838273755 0.763055176 0.07032 1.767953755 0.005281127 2.316940912

LIC HOUSING FINANCE 3.474300802 1.489796679 0.07032 3.403980802 0.010016139 2.28486266

BHARAT ELECTRONICS 2.365638115 1.066165894 0.07032 2.295318115 0.00968916 2.152871452

LARSEN 3.276964134 1.509290131 0.07032 3.206644134 0.005020374 2.124604188

ACC 1.964868219 0.900389661 0.07032 1.894548219 0.005962502 2.104142576

SIEMENS 3.09837087 1.497617725 0.07032 3.02805087 0.009062256 2.021911747

AMBUJA CEMENT 1.918553357 0.935018772 0.07032 1.848233357 0.005128092 1.976680482

TATA MOTORS 2.845709113 1.459165373 0.07032 2.775389113 0.00775053 1.902038771

WIPRO 1.483269027 0.787351949 0.07032 1.412949027 0.006042256 1.794558365

SBI 2.238305979 1.232359113 0.07032 2.167985979 0.006165506 1.759216089

RELIANCE 1.891337368 1.049073404 0.07032 1.821017368 0.003783903 1.735834081

INFOSYS 1.832829193 1.044335965 0.07032 1.762509193 0.003682944 1.68768409

IOC 1.374214676 0.881188824 0.07032 1.303894676 0.010705012 1.479699515

ICICI 2.325633896 1.526522055 0.07032 2.255313896 0.004797412 1.477419791

ONGC 1.267361301 0.970491274 0.07032 1.197041301 0.004422122 1.2334385

COAL INDIA 0.925127785 0.752528511 0.07032 0.854807785 0.004242523 1.135914152

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 26 [email protected]

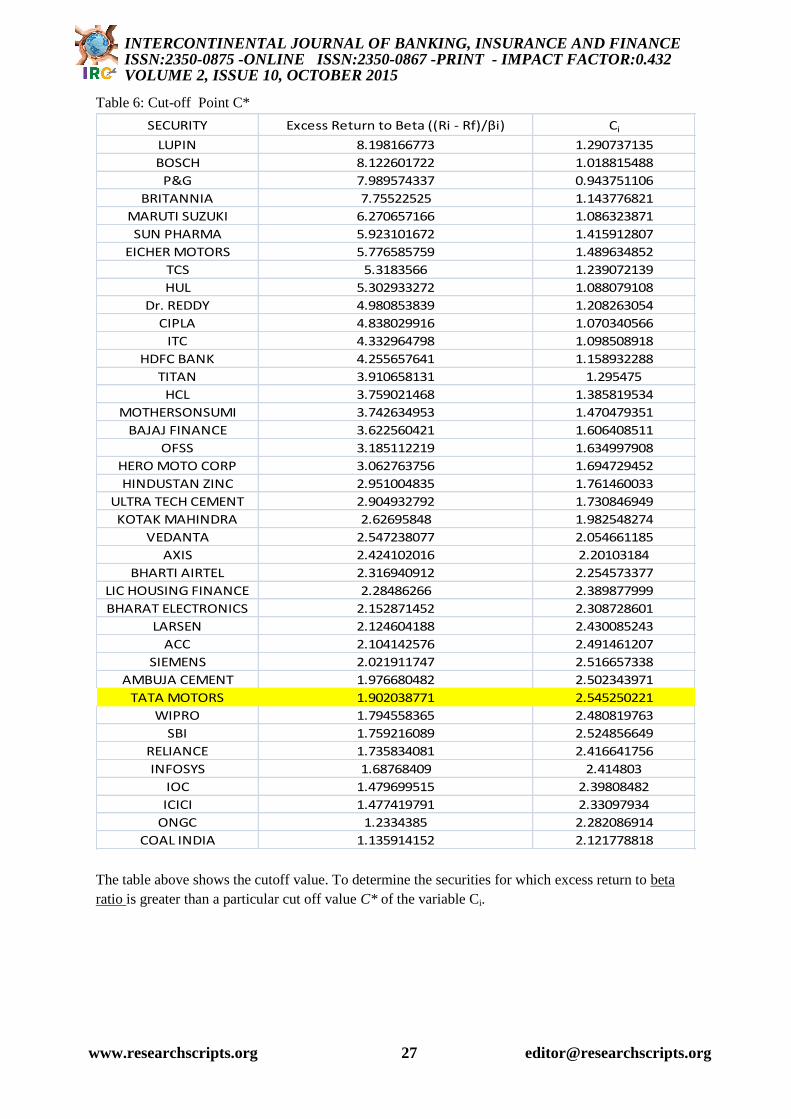

Table 6: Cut-off Point C*

SECURITY Excess Return to Beta ((Ri - Rf)/βi) Ci

LUPIN 8.198166773 1.290737135

BOSCH 8.122601722 1.018815488

P&G 7.989574337 0.943751106

BRITANNIA 7.75522525 1.143776821

MARUTI SUZUKI 6.270657166 1.086323871

SUN PHARMA 5.923101672 1.415912807

EICHER MOTORS 5.776585759 1.489634852

TCS 5.3183566 1.239072139

HUL 5.302933272 1.088079108

Dr. REDDY 4.980853839 1.208263054

CIPLA 4.838029916 1.070340566

ITC 4.332964798 1.098508918

HDFC BANK 4.255657641 1.158932288

TITAN 3.910658131 1.295475

HCL 3.759021468 1.385819534

MOTHERSONSUMI 3.742634953 1.470479351

BAJAJ FINANCE 3.622560421 1.606408511

OFSS 3.185112219 1.634997908

HERO MOTO CORP 3.062763756 1.694729452

HINDUSTAN ZINC 2.951004835 1.761460033

ULTRA TECH CEMENT 2.904932792 1.730846949

KOTAK MAHINDRA 2.62695848 1.982548274

VEDANTA 2.547238077 2.054661185

AXIS 2.424102016 2.20103184

BHARTI AIRTEL 2.316940912 2.254573377

LIC HOUSING FINANCE 2.28486266 2.389877999

BHARAT ELECTRONICS 2.152871452 2.308728601

LARSEN 2.124604188 2.430085243

ACC 2.104142576 2.491461207

SIEMENS 2.021911747 2.516657338

AMBUJA CEMENT 1.976680482 2.502343971

TATA MOTORS 1.902038771 2.545250221

WIPRO 1.794558365 2.480819763

SBI 1.759216089 2.524856649

RELIANCE 1.735834081 2.416641756

INFOSYS 1.68768409 2.414803

IOC 1.479699515 2.39808482

ICICI 1.477419791 2.33097934

ONGC 1.2334385 2.282086914

COAL INDIA 1.135914152 2.121778818

The table above shows the cutoff value. To determine the securities for which excess return to beta

ratio is greater than a particular cut off value C* of the variable Ci.

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 27 [email protected]

Where

σm

2 indicates the market index .

σei2 indicates the unsystematic risk.

Table 6: Selection of Securities for Optimal Portfolio

SECURITY Excess Return to Beta ((Ri - Rf)/βi) Ci

LUPIN 8.198166773 1.290737135

BOSCH 8.122601722 1.018815488

P&G 7.989574337 0.943751106

BRITANNIA 7.75522525 1.143776821

MARUTI SUZUKI 6.270657166 1.086323871

SUN PHARMA 5.923101672 1.415912807

EICHER MOTORS 5.776585759 1.489634852

TCS 5.3183566 1.239072139

HUL 5.302933272 1.088079108

Dr. REDDY 4.980853839 1.208263054

CIPLA 4.838029916 1.070340566

ITC 4.332964798 1.098508918

HDFC BANK 4.255657641 1.158932288

TITAN 3.910658131 1.295475

HCL 3.759021468 1.385819534

MOTHERSONSUMI 3.742634953 1.470479351

BAJAJ FINANCE 3.622560421 1.606408511

OFSS 3.185112219 1.634997908

HERO MOTO CORP 3.062763756 1.694729452

HINDUSTAN ZINC 2.951004835 1.761460033

ULTRA TECH CEMENT 2.904932792 1.730846949

KOTAK MAHINDRA 2.62695848 1.982548274

VEDANTA 2.547238077 2.054661185

In the above table it is seen that first 23 securities exceeds Ci value of the respective securities. The Ci

value of the 25th security is the cutoff value C* which is (2.254573377). This value is compared with

excess return to Beta value of each security. This collection will help in constructing an OPTIMAL

PORTFOLIO. After identifying the composition of the optimal portfolio, the next step is to

determine the proportion of investment in each of the securities in the optimal portfolio.

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 28 [email protected]

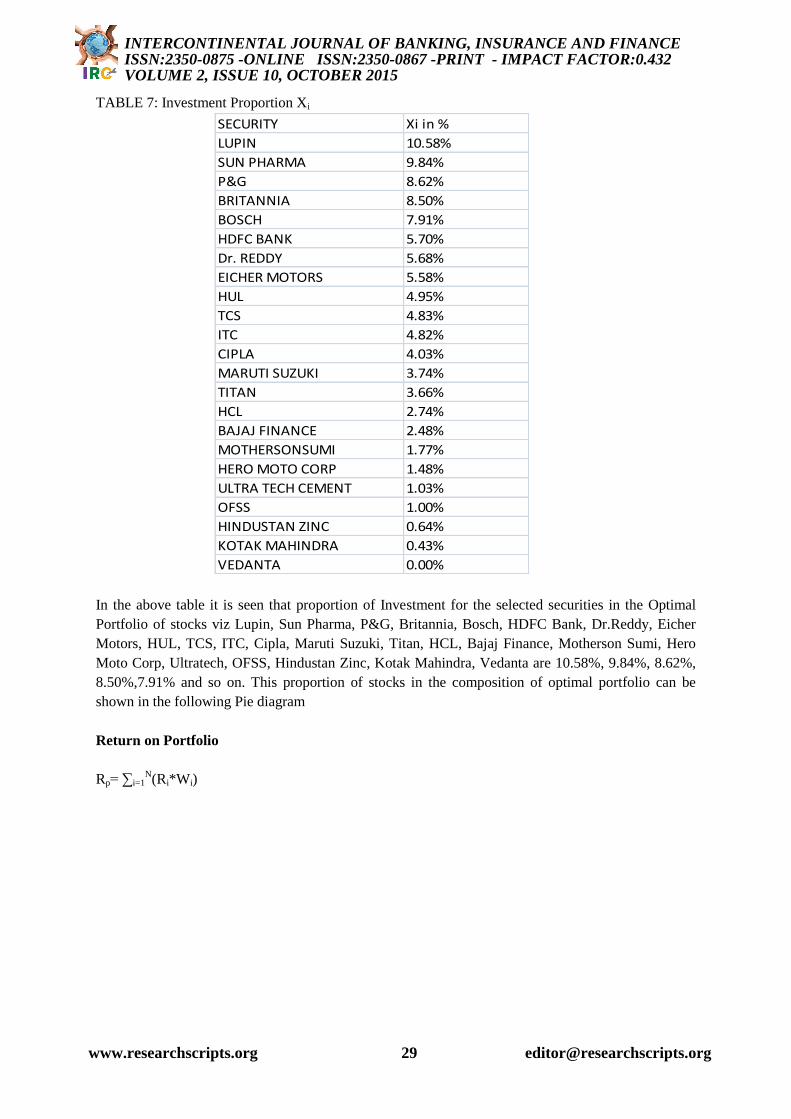

TABLE 7: Investment Proportion Xi

SECURITY Xi in %

LUPIN 10.58%

SUN PHARMA 9.84%

P&G 8.62%

BRITANNIA 8.50%

BOSCH 7.91%

HDFC BANK 5.70%

Dr. REDDY 5.68%

EICHER MOTORS 5.58%

HUL 4.95%

TCS 4.83%

ITC 4.82%

CIPLA 4.03%

MARUTI SUZUKI 3.74%

TITAN 3.66%

HCL 2.74%

BAJAJ FINANCE 2.48%

MOTHERSONSUMI 1.77%

HERO MOTO CORP 1.48%

ULTRA TECH CEMENT 1.03%

OFSS 1.00%

HINDUSTAN ZINC 0.64%

KOTAK MAHINDRA 0.43%

VEDANTA 0.00%

In the above table it is seen that proportion of Investment for the selected securities in the Optimal

Portfolio of stocks viz Lupin, Sun Pharma, P&G, Britannia, Bosch, HDFC Bank, Dr.Reddy, Eicher

Motors, HUL, TCS, ITC, Cipla, Maruti Suzuki, Titan, HCL, Bajaj Finance, Motherson Sumi, Hero

Moto Corp, Ultratech, OFSS, Hindustan Zinc, Kotak Mahindra, Vedanta are 10.58%, 9.84%, 8.62%,

8.50%,7.91% and so on. This proportion of stocks in the composition of optimal portfolio can be

shown in the following Pie diagram

Return on Portfolio

Rp= ∑i=1N(Ri*Wi)

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 29 [email protected]

TABLE 8: Return on Portfolio

SECURITY Ri WI Ri*Wi

LUPIN 3.867658789 10.57989969 40.91944201

SUN PHARMA 3.178414425 9.843712937 31.2873992

P&G 2.712977971 8.616346216 23.37595747

BRITANNIA 3.186850036 8.499854055 27.0877602

BOSCH 2.592949476 7.913968534 20.52052056

HDFC BANK 2.816122658 5.697106551 16.04375084

Dr. REDDY 2.838340963 5.681285903 16.1254265

EICHER MOTORS 5.053075452 5.577560653 28.18383481

HUL 2.231584406 4.950218662 11.04683077

TCS 2.457715087 4.828616932 11.86736468

ITC 2.096705145 4.81573338 10.09717295

CIPLA 2.05792437 4.034389685 8.302468853

MARUTI SUZUKI 2.825647176 3.736340241 10.55757925

TITAN 4.049813904 3.658273155 14.81532549

HCL 2.994584271 2.743779543 8.216479064

BAJAJ FINANCE 4.424835449 2.476973883 10.96020185

MOTHERSONSUMI 3.927686528 1.774761744 6.970707793

HERO MOTO CORP 1.936430512 1.479567228 2.865079125

ULTRA TECH CEMENT 3.065016759 1.029795015 3.156338979

OFSS 2.557490789 0.997195736 2.550318909

HINDUSTAN ZINC 3.780975217 0.635917003 2.404386427

KOTAK MAHINDRA 3.98555782 0.425175619 1.694562012

VEDANTA 3.892685168 0.003527637 0.013731982

309.0626397

From the above table it seen that the portfolio return is higher than the average returns of the

individual stocks in the optimal portfolio with the exception of Hindustan Zinc, Kotak Mahindra,

Vedanta.

Findings

It is observed that the Sharpe‟s Single Index model gives an easy mechanism of constructing

an optimal portfolio of stocks for a rational investor by analyzing the reason behind the

inclusion of securities in the portfolio with their respective weights.

From the study, it is observed that only 23 securities out of 40 sampled securities are

allowed to be included in the optimal portfolio using the steps behind its construction under

SIM.

LUPIN has the highest excess return to Beta of 8.18% and VEDANTA has the lowest return

of 2.54%.

If the investor wants to earn a maximum return without considering the risk aspect then

investment can be made on those securities which yield high returns. Even though the return

is high, the risk involved in the stock return should be considered while taking investment

decisions.

The risk can be reduced if the portfolio is diversified. The point of diversity is to achieve a

given level of expected return while bearing the least possible risk.

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 30 [email protected]

The return from VEDANTA security has the highest beta value of 1.5 which means that it is

highly volatile & a minimum amount should be invested i.e. 0035%.

7 companies out of 40 INCLUDED IN THE PORTFOLIO have the beta values greater than 1

which means that they are also volatile.

The excess return to beta ratio measures the additional return on a security per unit of

systematic risk. This ratio provides the relationship between potential risk and reward

involved in a security's return.

As per the calculation the return on portfolio and the risk on portfolio is

Rp= 309.062 and σp= 95.96.

Risk takers will select this portfolio because having maximum risk it yields 3 times more

return.

Conclusion

Stock markets are more volatile and investment in the stock market depends on the investor‟s

knowledge and reaction to various market factors like GDP, inflation, exchange rate fluctuations,

monetary policies, government policies, etc. Investors always expect higher return on their investment

made in the stock market as compared to riskless securities. Portfolio construction is beneficial in

diversifying risk rather than holding a single stock. An optimal portfolio is efficient when all the risk

is diversified. Investors should hold a portfolio of stocks to minimize their risk and maximize their

return. The above study conducted on the construction of optimal portfolio of stocks by using Sharpe

index model would guide the investors in their investment decisions. Investors can make use of this

study in deciding the stocks to be included in their portfolio as well as they can also determine the

required proportion to be invested in each stock. The study is further left to the coming generation of

the financial world to undertake researches and develop new theories and models to the portfolio

management.

Reference

Fundamentals of Investment by Alexander & Sharpe.

www.wikipedia.com

www.bseindia.com

www.moneycontrol.com

Journal by Great Lakes Herald

International Journal of Financial management.

International Journal of Advanced Research in ISSN: 2278-6236 Management and Social

Sciences

INTERCONTINENTAL JOURNAL OF BANKING, INSURANCE AND FINANCEISSN:2350-0875 -ONLINE ISSN:2350-0867 -PRINT - IMPACT FACTOR:0.432VOLUME 2, ISSUE 10, OCTOBER 2015

www.researchscripts.org 31 [email protected]