Embed Size (px)

Citation preview

KPMG.com/in

June 2018

KPMG Advisory Services Private Limited

Consolidation in Steel sector

Disclaimer• We have prepared this note solely for the purpose of discussion.

• This presentation sets forth our views based on the completeness and accuracy of the facts and any assumptions that were included. If any of the facts and assumptions is

not complete or accurate, it is imperative that we be informed accordingly, as the inaccuracy or incompleteness thereof could have a material effect on our conclusions.

• We have not performed an audit and do not express an opinion or any other form of assurance. Further, comments in our presentation are not intended, nor should they be

interpreted to be legal advice or opinion.

• While information obtained from the public domain or external sources have not been verified for authenticity, accuracy or completeness, we have obtained information, as far

as possible, from sources generally considered to be reliable. We assume no responsibility for such information.

• Our views are not binding on any person, entity, authority or Court, and hence, no assurance is given that a position contrary to the opinions expressed herein will not be

asserted by any person, entity, authority and/or sustained by an appellate authority or a court of law.

• In accordance with its policy, KPMG advises that neither it nor any partner, director or employee undertakes any responsibility arising in any way whatsoever, to any person in

respect of the matters dealt with in this presentation, including any errors or omissions therein, arising through negligence or otherwise, howsoever caused.

• In connection with our presentation or any part thereof, KPMG does not owe duty of care (whether in contract or in tort or under statute or otherwise) to any person or party to

whom the presentation is circulated to and KPMG shall not be liable to any party who uses or relies on this presentation. KPMG thus disclaims all responsibility or liability for

any costs, damages, losses, liabilities, expenses incurred by such third party arising out of or in connection with the presentation or any part thereof.

• By reading our presentation, the reader shall be deemed to have accepted the terms mentioned hereinabove.

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 3

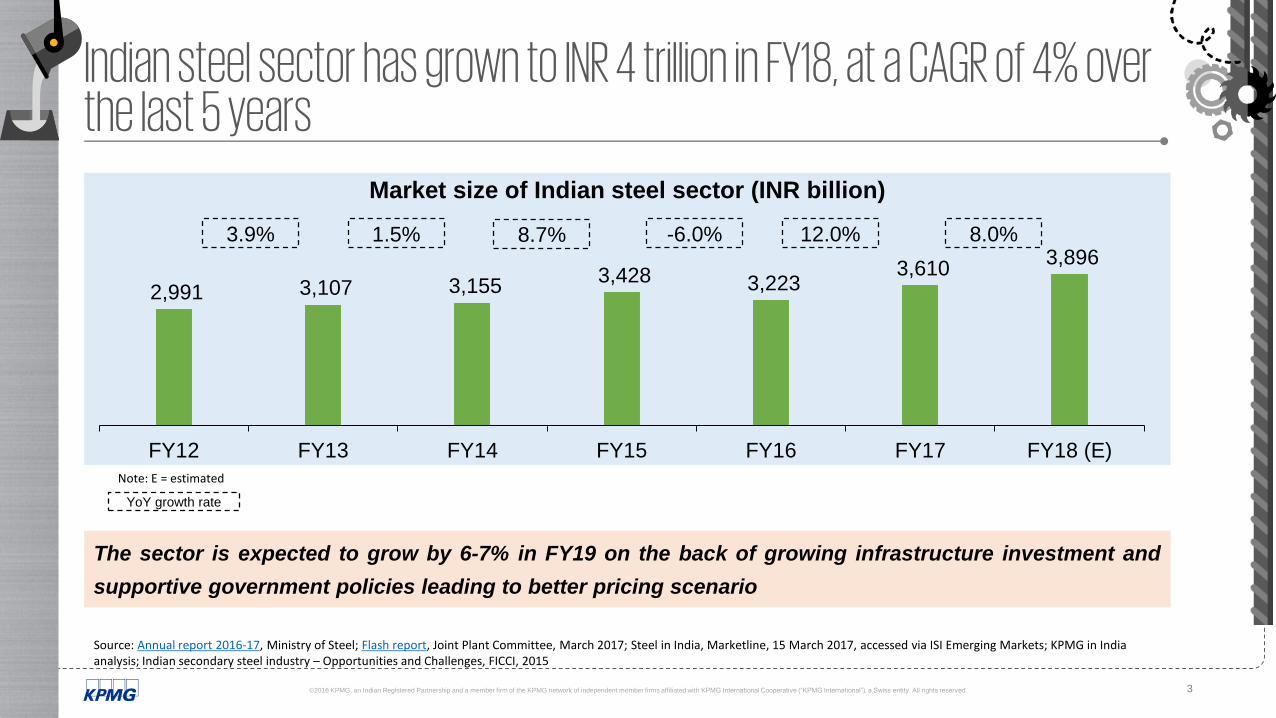

2,991 3,107 3,155 3,428 3,223

3,610 3,896

FY12 FY13 FY14 FY15 FY16 FY17 FY18 (E)

Market size of Indian steel sector (INR billion)

Indian steel sector has grown to INR 4 trillion in FY18, at a CAGR of 4% over the last 5 years

The sector is expected to grow by 6-7% in FY19 on the back of growing infrastructure investment and

supportive government policies leading to better pricing scenario

3.9% 8.7% -6.0% 12.0%

YoY growth rate

1.5%

Note: E = estimated

Source: Annual report 2016-17, Ministry of Steel; Flash report, Joint Plant Committee, March 2017; Steel in India, Marketline, 15 March 2017, accessed via ISI Emerging Markets; KPMG in India analysis; Indian secondary steel industry – Opportunities and Challenges, FICCI, 2015

8.0%

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 4

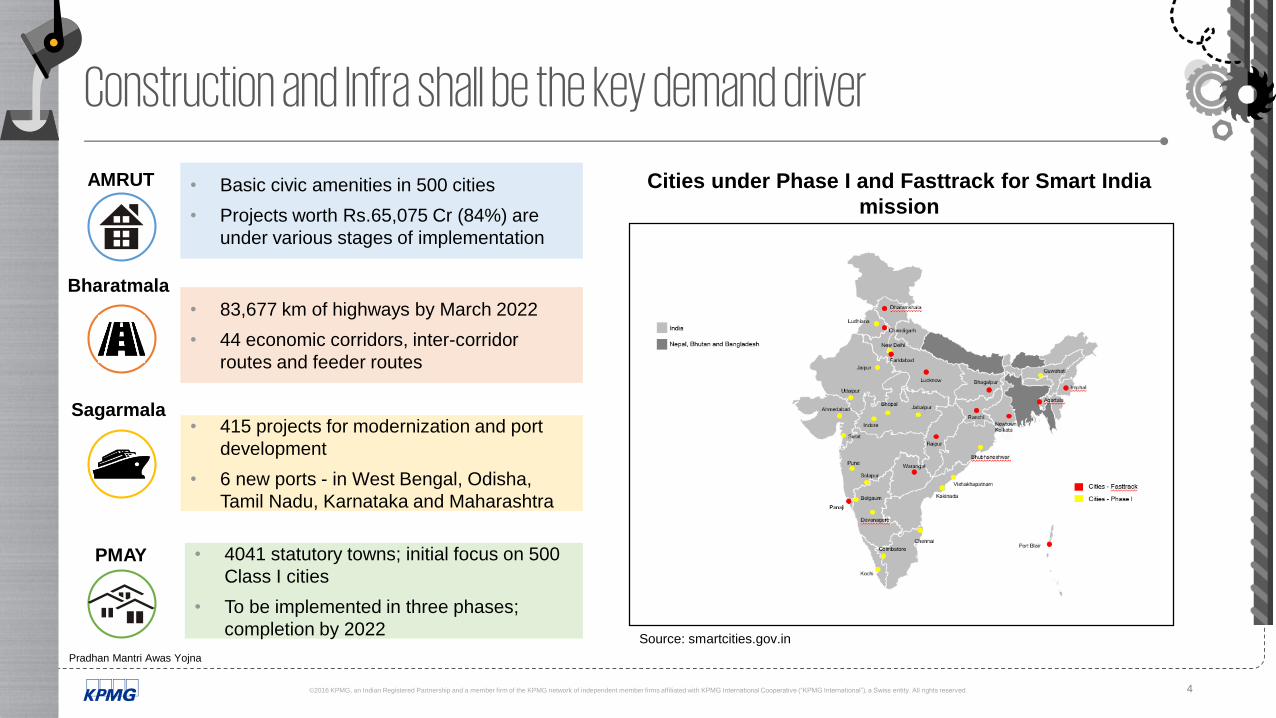

Construction and Infra shall be the key demand driver

• Basic civic amenities in 500 cities

• Projects worth Rs.65,075 Cr (84%) are

under various stages of implementation

• 83,677 km of highways by March 2022

• 44 economic corridors, inter-corridor

routes and feeder routes

• 415 projects for modernization and port

development

• 6 new ports - in West Bengal, Odisha,

Tamil Nadu, Karnataka and Maharashtra

Source: smartcities.gov.in

• 4041 statutory towns; initial focus on 500

Class I cities

• To be implemented in three phases;

completion by 2022

Cities under Phase I and Fasttrack for Smart India

mission

AMRUT

Bharatmala

Sagarmala

Pradhan Mantri Awas Yojna

PMAY

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 5

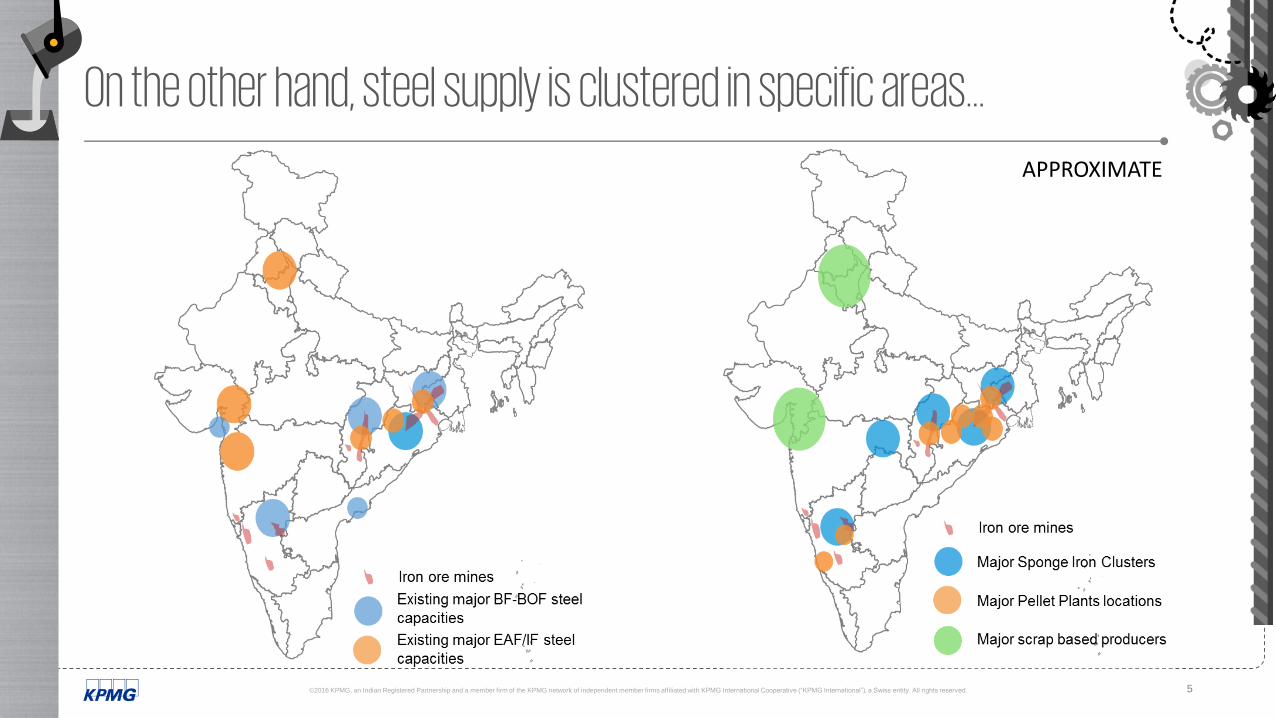

On the other hand, steel supply is clustered in specific areas…APPROXIMATE

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 6

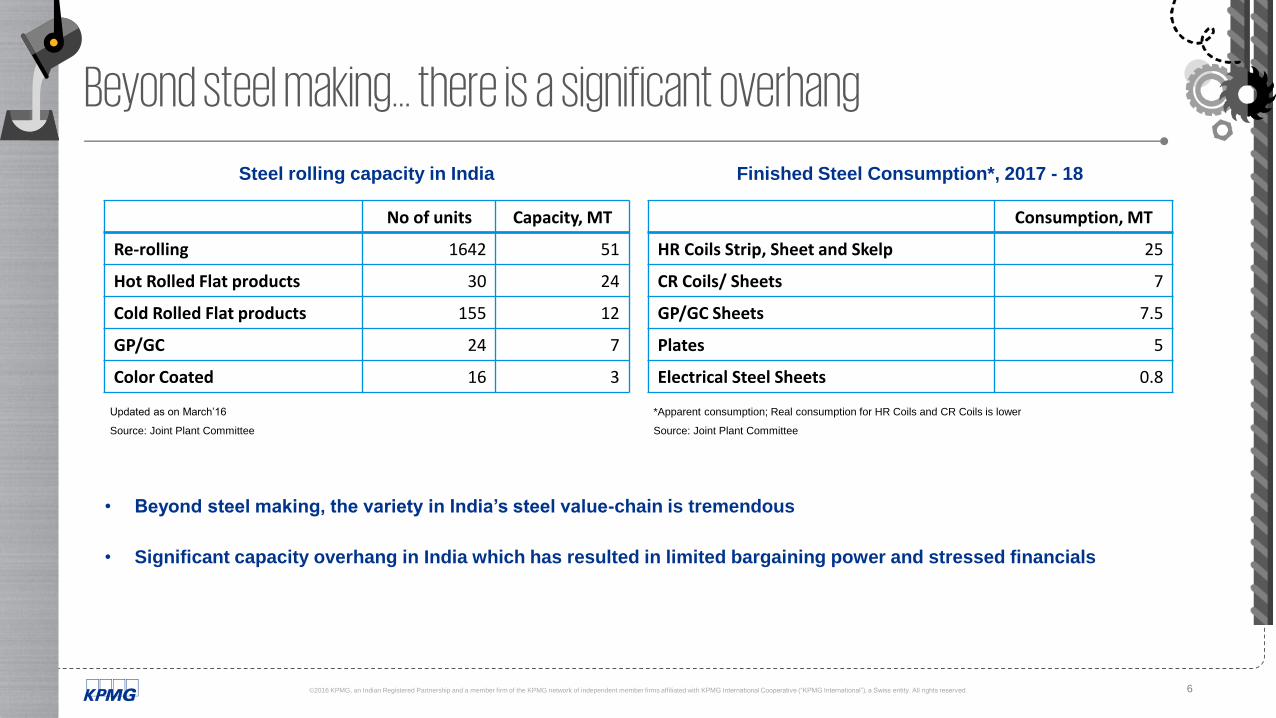

Beyond steel making… there is a significant overhang

No of units Capacity, MT

Re-rolling 1642 51

Hot Rolled Flat products 30 24

Cold Rolled Flat products 155 12

GP/GC 24 7

Color Coated 16 3

Steel rolling capacity in India

Source: Joint Plant Committee

Updated as on March’16

Finished Steel Consumption*, 2017 - 18

Consumption, MT

HR Coils Strip, Sheet and Skelp 25

CR Coils/ Sheets 7

GP/GC Sheets 7.5

Plates 5

Electrical Steel Sheets 0.8

Source: Joint Plant Committee

*Apparent consumption; Real consumption for HR Coils and CR Coils is lower

• Beyond steel making, the variety in India’s steel value-chain is tremendous

• Significant capacity overhang in India which has resulted in limited bargaining power and stressed financials

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 7

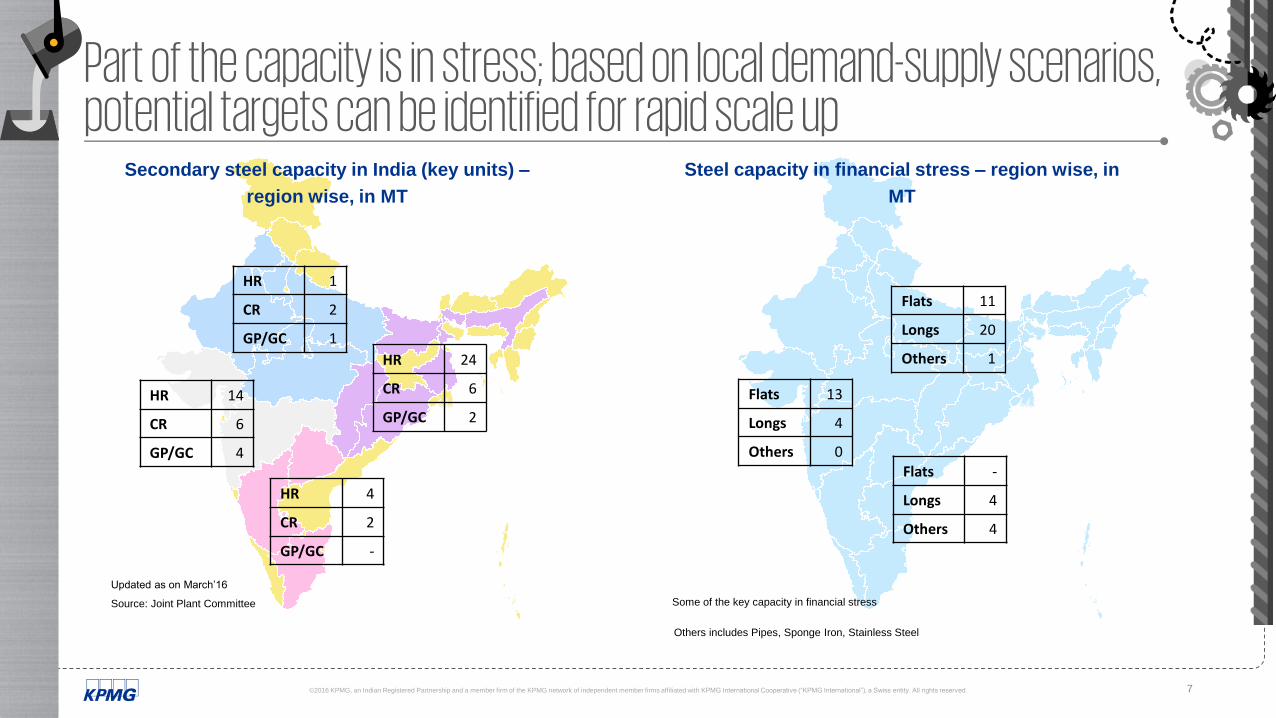

Part of the capacity is in stress; based on local demand-supply scenarios, potential targets can be identified for rapid scale up

Source: Joint Plant Committee

Updated as on March’16

Secondary steel capacity in India (key units) –

region wise, in MT

HR 1

CR 2

GP/GC 1

HR 14

CR 6

GP/GC 4

HR 4

CR 2

GP/GC -

HR 24

CR 6

GP/GC 2

Some of the key capacity in financial stress

Steel capacity in financial stress – region wise, in

MT

Flats 11

Longs 20

Others 1

Flats 13

Longs 4

Others 0Flats -

Longs 4

Others 4

Others includes Pipes, Sponge Iron, Stainless Steel

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 8

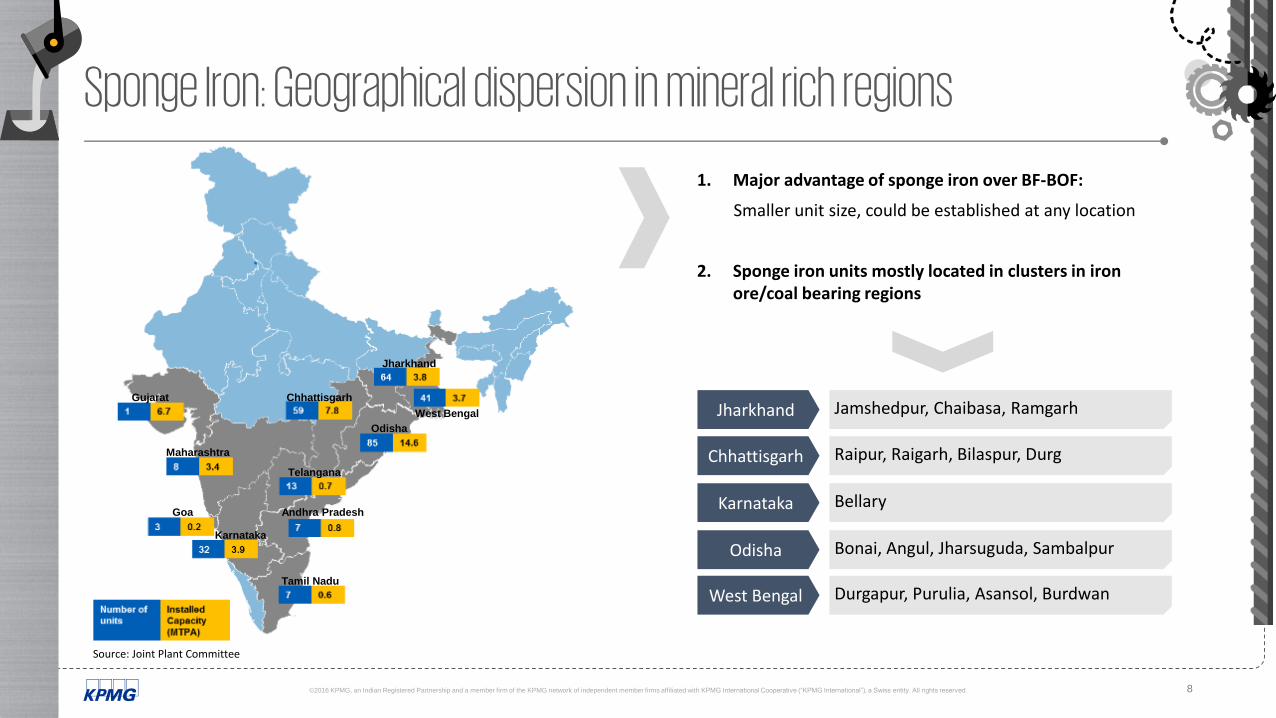

Sponge Iron: Geographical dispersion in mineral rich regions

1. Major advantage of sponge iron over BF-BOF:

Smaller unit size, could be established at any location

2. Sponge iron units mostly located in clusters in iron ore/coal bearing regions

Jharkhand Jamshedpur, Chaibasa, Ramgarh

Chhattisgarh Raipur, Raigarh, Bilaspur, Durg

Karnataka Bellary

Odisha Bonai, Angul, Jharsuguda, Sambalpur

West Bengal Durgapur, Purulia, Asansol, Burdwan

Gujarat

Maharashtra

Karnataka

Tamil Nadu

Goa

Chhattisgarh

Jharkhand

West Bengal

Odisha

Telangana

Andhra Pradesh

Source: Joint Plant Committee

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 9

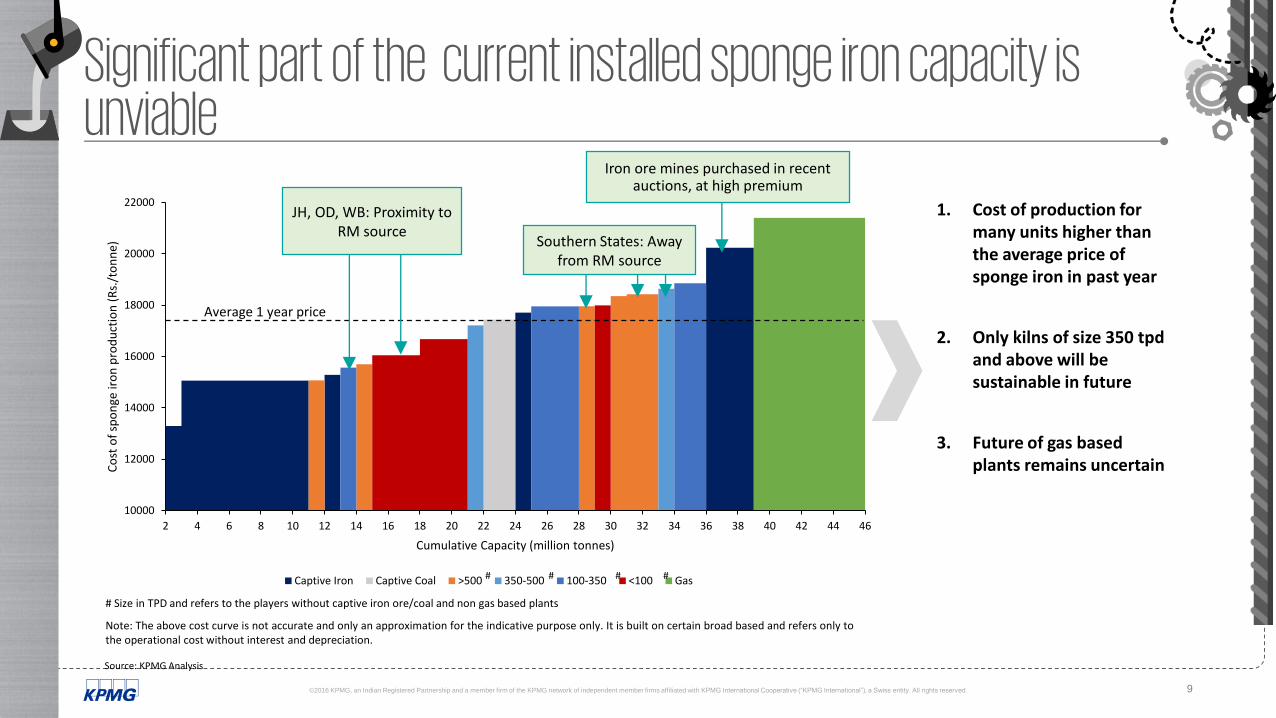

Significant part of the current installed sponge iron capacity is unviable

10000

12000

14000

16000

18000

20000

22000

2 4 6 8 10 12 14 16 18 20 22 24 26 28 30 32 34 36 38 40 42 44 46

Co

st o

f sp

on

ge ir

on

pro

du

ctio

n (

Rs.

/to

nn

e)

Cumulative Capacity (million tonnes)

Captive Iron Captive Coal >500 350-500 100-350 <100 Gas

Average 1 year price

# Size in TPD and refers to the players without captive iron ore/coal and non gas based plants

Note: The above cost curve is not accurate and only an approximation for the indicative purpose only. It is built on certain broad based and refers only tothe operational cost without interest and depreciation.

Source: KPMG Analysis

1. Cost of production for many units higher than the average price of sponge iron in past year

2. Only kilns of size 350 tpd and above will be sustainable in future

3. Future of gas based plants remains uncertain

JH, OD, WB: Proximity to RM source

Iron ore mines purchased in recent auctions, at high premium

Southern States: Away from RM source

# # # #

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 10

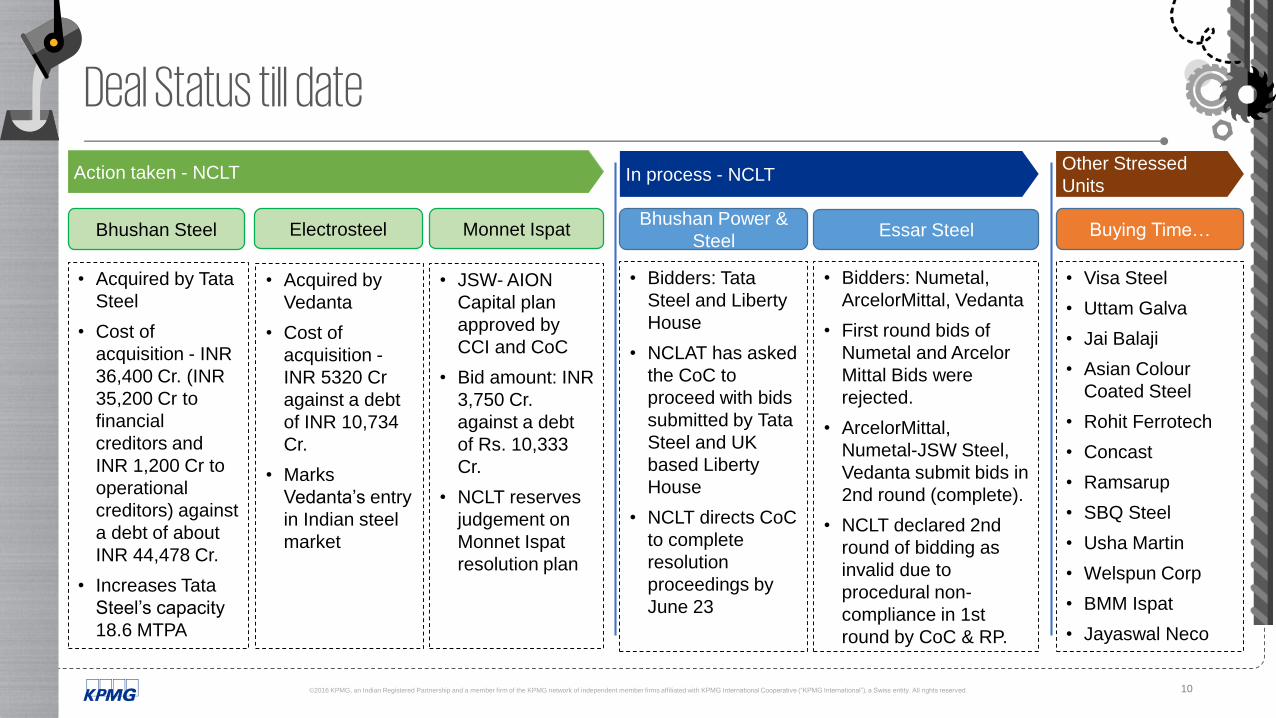

Deal Status till dateAction taken - NCLT In process - NCLT

Bhushan Steel

• Acquired by Tata

Steel

• Cost of

acquisition - INR

36,400 Cr. (INR

35,200 Cr to

financial

creditors and

INR 1,200 Cr to

operational

creditors) against

a debt of about

INR 44,478 Cr.

• Increases Tata

Steel’s capacity

18.6 MTPA

Electrosteel

• Acquired by

Vedanta

• Cost of

acquisition -

INR 5320 Cr

against a debt

of INR 10,734

Cr.

• Marks

Vedanta’s entry

in Indian steel

market

Monnet Ispat

• JSW- AION

Capital plan

approved by

CCI and CoC

• Bid amount: INR

3,750 Cr.

against a debt

of Rs. 10,333

Cr.

• NCLT reserves

judgement on

Monnet Ispat

resolution plan

• Bidders: Tata

Steel and Liberty

House

• NCLAT has asked

the CoC to

proceed with bids

submitted by Tata

Steel and UK

based Liberty

House

• NCLT directs CoC

to complete

resolution

proceedings by

June 23

Bhushan Power &

SteelEssar Steel

• Bidders: Numetal,

ArcelorMittal, Vedanta

• First round bids of

Numetal and Arcelor

Mittal Bids were

rejected.

• ArcelorMittal,

Numetal-JSW Steel,

Vedanta submit bids in

2nd round (complete).

• NCLT declared 2nd

round of bidding as

invalid due to

procedural non-

compliance in 1st

round by CoC & RP.

Other Stressed

Units

• Visa Steel

• Uttam Galva

• Jai Balaji

• Asian Colour

Coated Steel

• Rohit Ferrotech

• Concast

• Ramsarup

• SBQ Steel

• Usha Martin

• Welspun Corp

• BMM Ispat

• Jayaswal Neco

Buying Time…

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 11

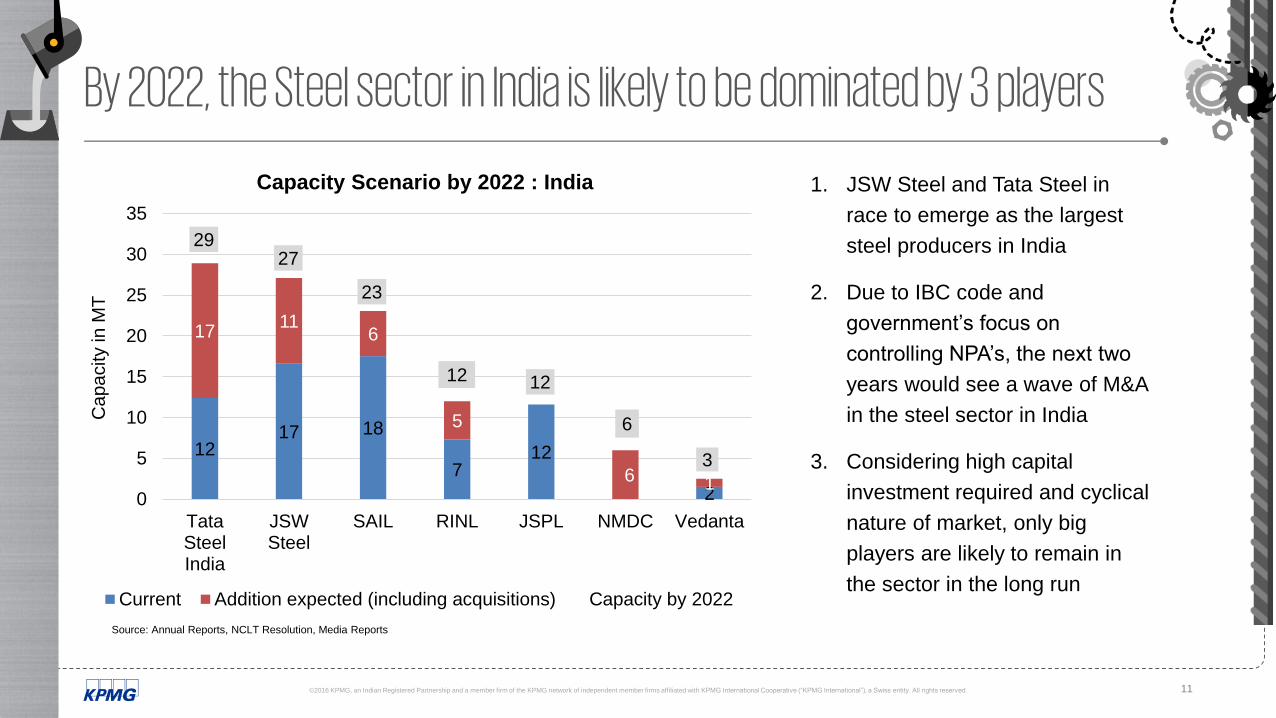

By 2022, the Steel sector in India is likely to be dominated by 3 players

1. JSW Steel and Tata Steel in

race to emerge as the largest

steel producers in India

2. Due to IBC code and

government’s focus on

controlling NPA’s, the next two

years would see a wave of M&A

in the steel sector in India

3. Considering high capital

investment required and cyclical

nature of market, only big

players are likely to remain in

the sector in the long run

1217 18

712

2

1711

6

5

6 1

2927

23

12 12

6

3

0

5

10

15

20

25

30

35

TataSteelIndia

JSWSteel

SAIL RINL JSPL NMDC Vedanta

Ca

pa

city in

MT

Current Addition expected (including acquisitions) Capacity by 2022

Capacity Scenario by 2022 : India

Source: Annual Reports, NCLT Resolution, Media Reports

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 12

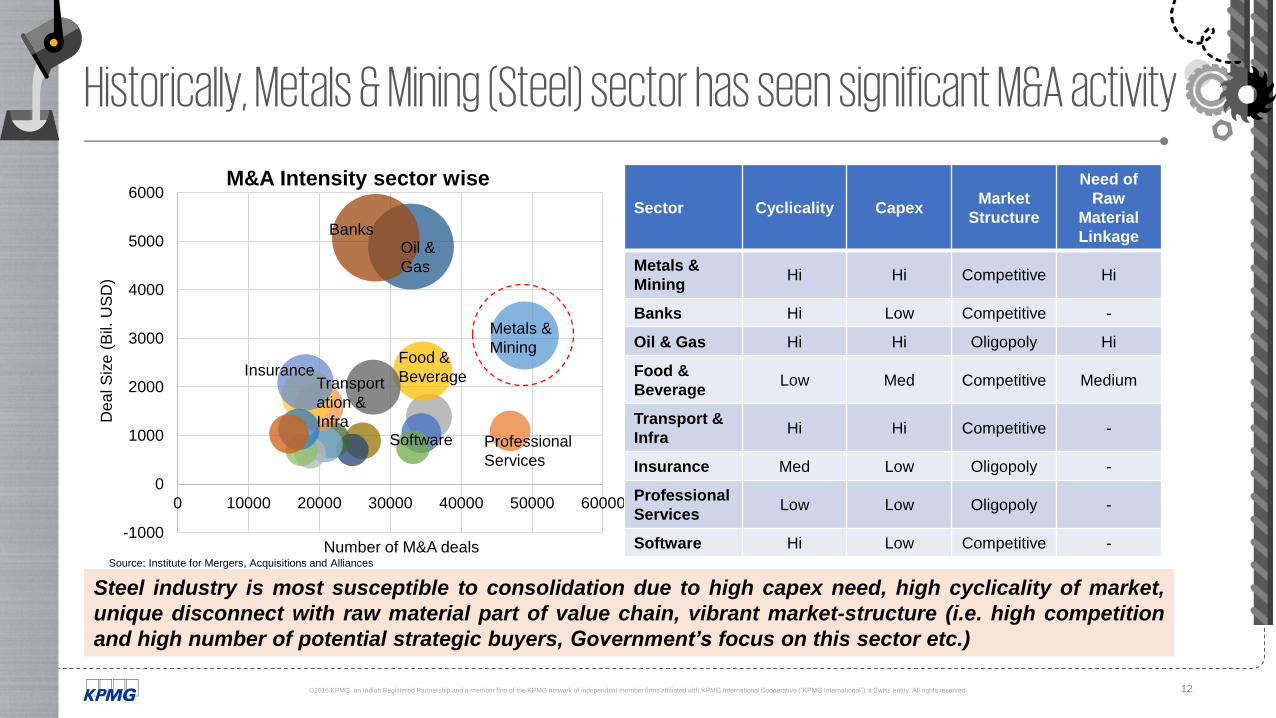

Historically, Metals & Mining (Steel) sector has seen significant M&A activity

Steel industry is most susceptible to consolidation due to high capex need, high cyclicality of market,

unique disconnect with raw material part of value chain, vibrant market-structure (i.e. high competition

and high number of potential strategic buyers, Government’s focus on this sector etc.)

-1000

0

1000

2000

3000

4000

5000

6000

0 10000 20000 30000 40000 50000 60000

Dea

l S

ize

(B

il. U

SD

)

Number of M&A deals

M&A Intensity sector wise

Metals &

Mining

BanksOil &

Gas

Food &

Beverage

Professional

Services

Transport

ation &

Infra

Insurance

Software

Sector Cyclicality CapexMarket

Structure

Need of

Raw

Material

Linkage

Metals &

MiningHi Hi Competitive Hi

Banks Hi Low Competitive -

Oil & Gas Hi Hi Oligopoly Hi

Food &

BeverageLow Med Competitive Medium

Transport &

InfraHi Hi Competitive -

Insurance Med Low Oligopoly -

Professional

ServicesLow Low Oligopoly -

Software Hi Low Competitive -Source: Institute for Mergers, Acquisitions and Alliances

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 13

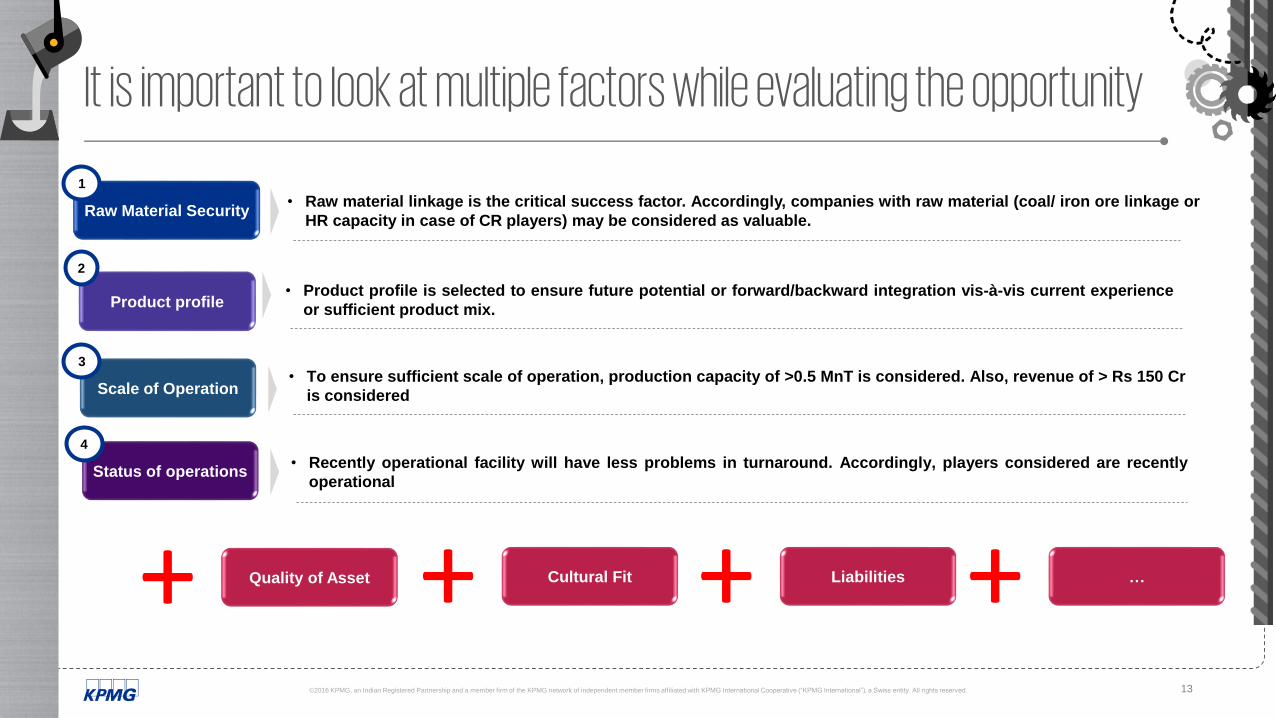

It is important to look at multiple factors while evaluating the opportunity

Raw Material Security

Product profile

1

2

• Raw material linkage is the critical success factor. Accordingly, companies with raw material (coal/ iron ore linkage or

HR capacity in case of CR players) may be considered as valuable.

• Product profile is selected to ensure future potential or forward/backward integration vis-à-vis current experience

or sufficient product mix.

Status of operations

4

• Recently operational facility will have less problems in turnaround. Accordingly, players considered are recently

operational

Scale of Operation

3

• To ensure sufficient scale of operation, production capacity of >0.5 MnT is considered. Also, revenue of > Rs 150 Cr

is considered

+ Quality of Asset + Cultural Fit + Liabilities + …

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 14

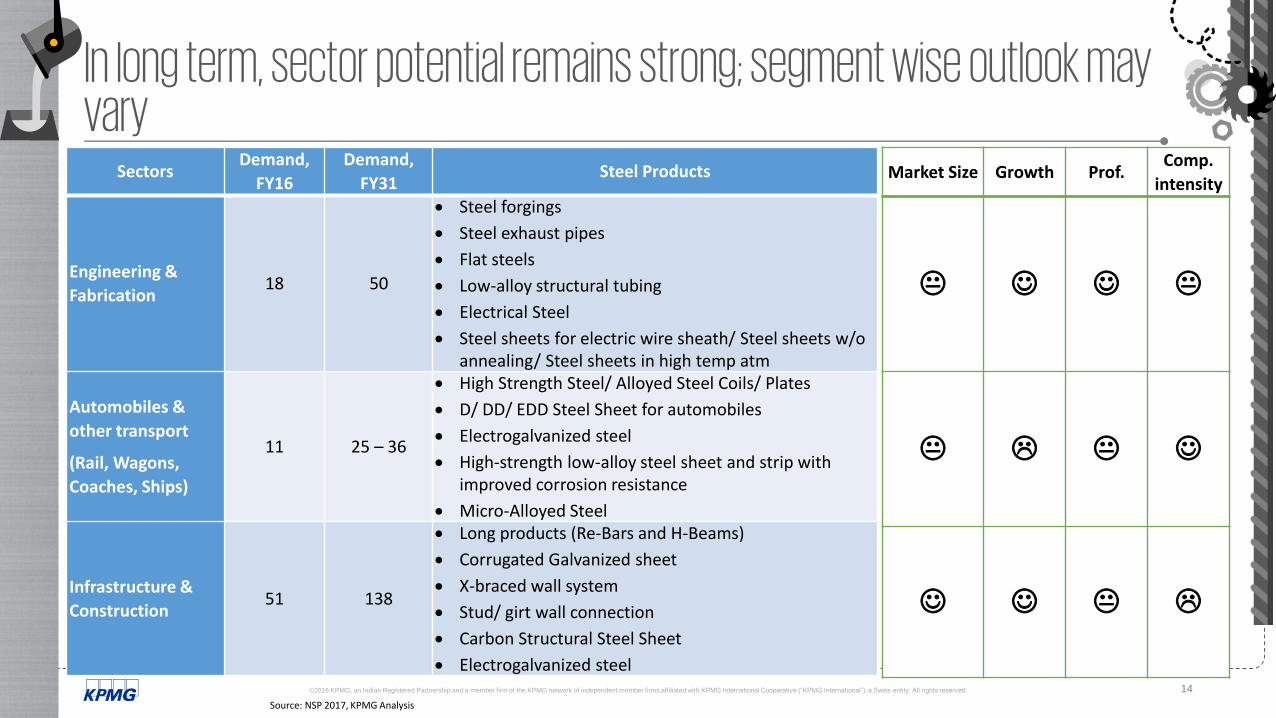

In long term, sector potential remains strong; segment wise outlook may vary

SectorsDemand,

FY16

Demand,

FY31Steel Products

Engineering &

Fabrication18 50

Steel forgings

Steel exhaust pipes

Flat steels

Low-alloy structural tubing

Electrical Steel

Steel sheets for electric wire sheath/ Steel sheets w/o annealing/ Steel sheets in high temp atm

Automobiles &

other transport

(Rail, Wagons,

Coaches, Ships)

11 25 – 36

High Strength Steel/ Alloyed Steel Coils/ Plates

D/ DD/ EDD Steel Sheet for automobiles

Electrogalvanized steel

High-strength low-alloy steel sheet and strip with improved corrosion resistance

Micro-Alloyed Steel

Infrastructure &

Construction51 138

Long products (Re-Bars and H-Beams)

Corrugated Galvanized sheet

X-braced wall system

Stud/ girt wall connection

Carbon Structural Steel Sheet

Electrogalvanized steel

Market Size Growth Prof.Comp.

intensity

Source: NSP 2017, KPMG Analysis

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 15

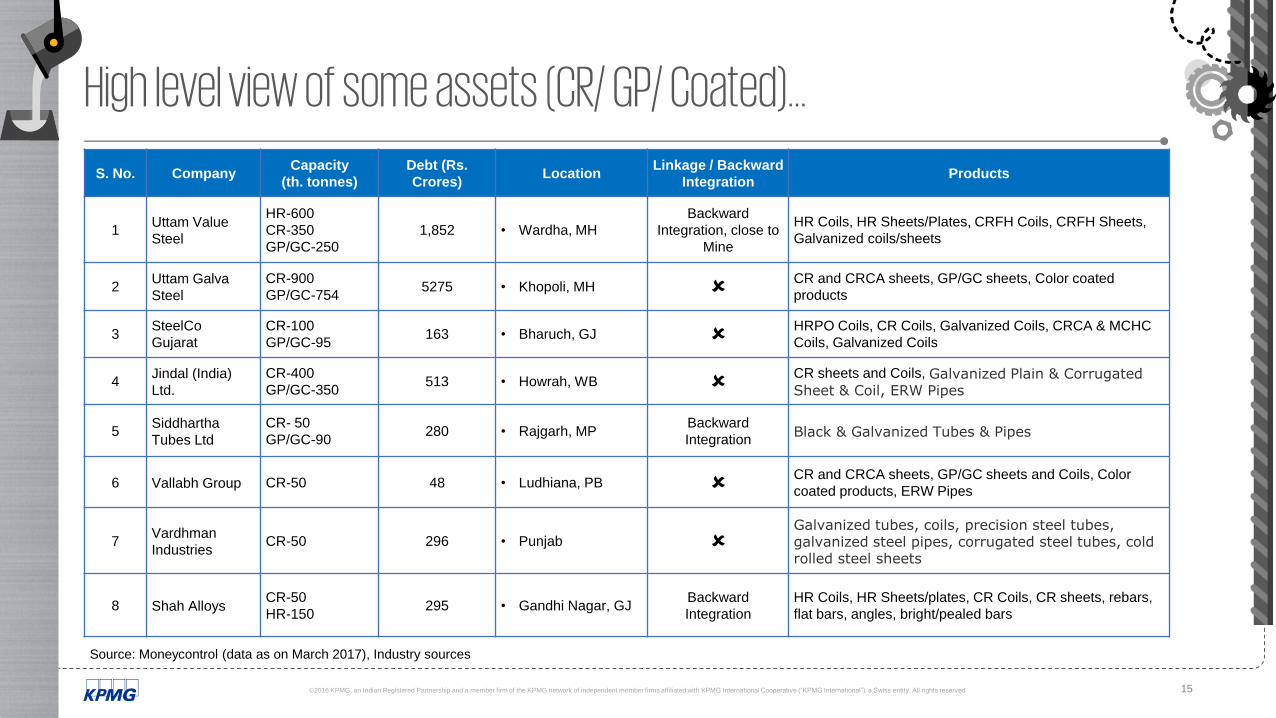

High level view of some assets (CR/ GP/ Coated)…S. No. Company

Capacity

(th. tonnes)

Debt (Rs.

Crores)Location

Linkage / Backward

IntegrationProducts

1Uttam Value

Steel

HR-600

CR-350

GP/GC-250

1,852 • Wardha, MH

Backward

Integration, close to

Mine

HR Coils, HR Sheets/Plates, CRFH Coils, CRFH Sheets,

Galvanized coils/sheets

2Uttam Galva

Steel

CR-900

GP/GC-7545275 • Khopoli, MH

CR and CRCA sheets, GP/GC sheets, Color coated

products

3SteelCo

Gujarat

CR-100

GP/GC-95163 • Bharuch, GJ

HRPO Coils, CR Coils, Galvanized Coils, CRCA & MCHC

Coils, Galvanized Coils

4Jindal (India)

Ltd.

CR-400

GP/GC-350513 • Howrah, WB

CR sheets and Coils, Galvanized Plain & Corrugated Sheet & Coil, ERW Pipes

5Siddhartha

Tubes Ltd

CR- 50

GP/GC-90280 • Rajgarh, MP

Backward

IntegrationBlack & Galvanized Tubes & Pipes

6 Vallabh Group CR-50 48 • Ludhiana, PB CR and CRCA sheets, GP/GC sheets and Coils, Color

coated products, ERW Pipes

7Vardhman

IndustriesCR-50 296 • Punjab

Galvanized tubes, coils, precision steel tubes, galvanized steel pipes, corrugated steel tubes, cold rolled steel sheets

8 Shah AlloysCR-50

HR-150295 • Gandhi Nagar, GJ

Backward

Integration

HR Coils, HR Sheets/plates, CR Coils, CR sheets, rebars,

flat bars, angles, bright/pealed bars

Source: Moneycontrol (data as on March 2017), Industry sources

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 16

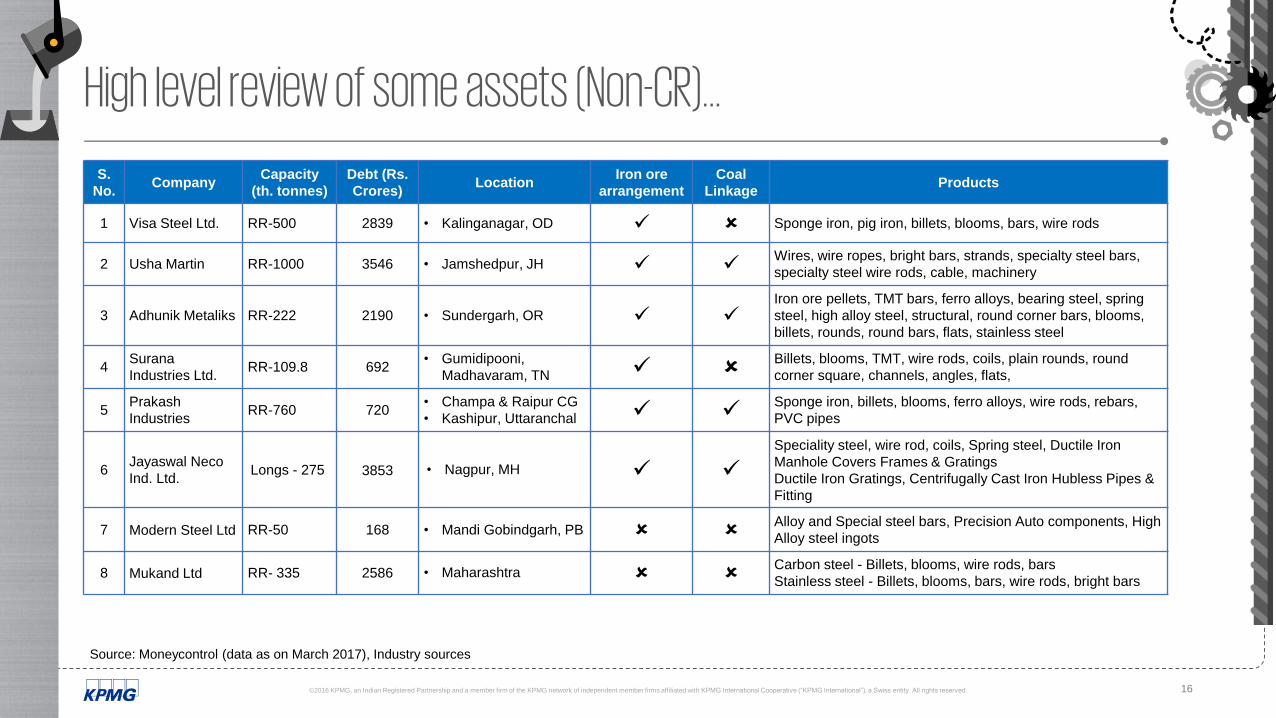

High level review of some assets (Non-CR)…S.

No.Company

Capacity

(th. tonnes)

Debt (Rs.

Crores)Location

Iron ore

arrangement

Coal

LinkageProducts

1 Visa Steel Ltd. RR-500 2839 • Kalinganagar, OD Sponge iron, pig iron, billets, blooms, bars, wire rods

2 Usha Martin RR-1000 3546 • Jamshedpur, JH Wires, wire ropes, bright bars, strands, specialty steel bars,

specialty steel wire rods, cable, machinery

3 Adhunik Metaliks RR-222 2190 • Sundergarh, OR

Iron ore pellets, TMT bars, ferro alloys, bearing steel, spring

steel, high alloy steel, structural, round corner bars, blooms,

billets, rounds, round bars, flats, stainless steel

4Surana

Industries Ltd.RR-109.8 692

• Gumidipooni,

Madhavaram, TN Billets, blooms, TMT, wire rods, coils, plain rounds, round

corner square, channels, angles, flats,

5Prakash

IndustriesRR-760 720

• Champa & Raipur CG

• Kashipur, Uttaranchal Sponge iron, billets, blooms, ferro alloys, wire rods, rebars,

PVC pipes

6Jayaswal Neco

Ind. Ltd. Longs - 275 3853 • Nagpur, MH

Speciality steel, wire rod, coils, Spring steel, Ductile Iron

Manhole Covers Frames & Gratings

Ductile Iron Gratings, Centrifugally Cast Iron Hubless Pipes &

Fitting

7 Modern Steel Ltd RR-50 168 • Mandi Gobindgarh, PB Alloy and Special steel bars, Precision Auto components, High

Alloy steel ingots

8 Mukand Ltd RR- 335 2586 • Maharashtra Carbon steel - Billets, blooms, wire rods, bars

Stainless steel - Billets, blooms, bars, wire rods, bright bars

Source: Moneycontrol (data as on March 2017), Industry sources

©2016 KPMG, an Indian Registered Partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved. 17

Next phase of M&A likely to happen sooner than later

1 Private Players like Tata Steel and JSW Steel likely to be the largest players in Indian Steel sector; the

dominance may be disrupted by an international player finding its feet in the present wave of consolidation

2 With technological evolution and increased global interdependency, Indian steel sector is witnessing shorter

business cycles; repeated consolidation may be a reality

3 Multiple scenarios feasible,

Scenario 1 – Tata Steel & JSW are able to turnaround the acquisitions in current round early, maintain operational

and financial advantage – a key player in subsequent waves

Scenario 2 – Indian players saddled with major acquisitions make way for other entities, particularly AM & Vedanta

Scenario 3 – Tier-2 and Value-chain consolidation happens with players building geographic diversity in their

portfolio with a lot of action by non-strategic investors (primarily sell-offs)

4 Action will shift to expiring merchant iron/ chrome ore/ manganese ore leases in 2020 – clarity in regulatory

environment required

Thank YouNiladri Bhattacharjee

Partner and Sector Leader – Metals & Mining,

+91 90510 61645