Embed Size (px)

Citation preview

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 1 of 50

CONSOLIDATED DISCLOSURES UNDER BASEL-III CAPITAL REGULATIONSFOR THE YEAR ENDED31st MARCH 2019

1. SCOPE OF APPLICATION

Name of the head of the banking group to which the framework applies:ALLAHABADBANK

(I). QUALITATIVE DISCLOSURES

A: List of group entities considered for consolidation

Name of theentity/[Country ofincorporation]Inclusionunderaccountingscope ofconsolidation

Method ofconsolidationInclusionunderregulatoryscope ofconsolidation

Method ofconsolidation Reasons fordifference inmethod ofconsolidationReasons forconsolidationunder onlyone of thescope ofconsolidationASREC (India)Ltd./[India] Yes Consolidatedinaccordancewith AS 27 Yes Consolidatedin accordancewith AS 27 NotApplicable NotApplicable

Allahabad UPGramin Bank/[India] Yes Consolidatedinaccordancewith AS 23 Yes Consolidatedin accordancewith AS 23 NotApplicable NotApplicableUniversal SompoGeneralInsuranceCompanyLimited/[India]Yes Consolidatedinaccordancewith AS 27 No NotApplicable NotApplicable Regulatoryguidelines

B: List of group entities not considered for consolidation both under the accountingand regulatory scope of consolidation: There are no group entities that are notconsidered for consolidation under both the accounting scope of consolidation andregulatory scope of consolidation.

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 2 of 50

(II) QUANTITATIVE DISCLOSURES (Rs. in Millions)C: List of group entities considered for consolidation

Name of the entity Principle activity of theentity

Total balance sheetequity(as per accountingbalance sheet)

Total balance sheetassets(as per accountingbalance sheet)ASREC (India) Ltd. Asset RecoveryCompany 980 1,668Allahabad UPGramin Bank Banking 619 1,22,010

D: The aggregate amount of capital deficiencies in all subsidiaries which are notincluded in the regulatory scope of consolidation: There is no capital deficiency in anysubsidiary, which is not included in the regulatory scope of consolidation. (Rs. in Millions)

E: The aggregate amounts (e.g. current book value) of the bank’s total interests in insuranceentities, which are risk-weighted

Name of theinsurance entity Principleactivity ofthe entityTotal balancesheet equity(as peraccountingbalance sheet)

Bank's holding inthe total equity orproportion ofvoting power (%)Quantitative impact ofregulatory capital ofusing risk weightingmethods versus using thefull deduction methodUniversal SompoGeneral InsuranceCompany Limited GeneralInsurance 3,682 28.52% Decrease in CRAR by 2bps.

F: Any restrictions or impediments on transfer of funds or regulatory capital withinthe banking group: There are no restrictions or impediments on transfer of funds orregulatory capital within the banking group.

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 3 of 50

CONSOLIDATED DISCLOSURES UNDER BASEL-III CAPITAL REGULATIONSFOR THE YEAR ENDED31stMARCH 2019

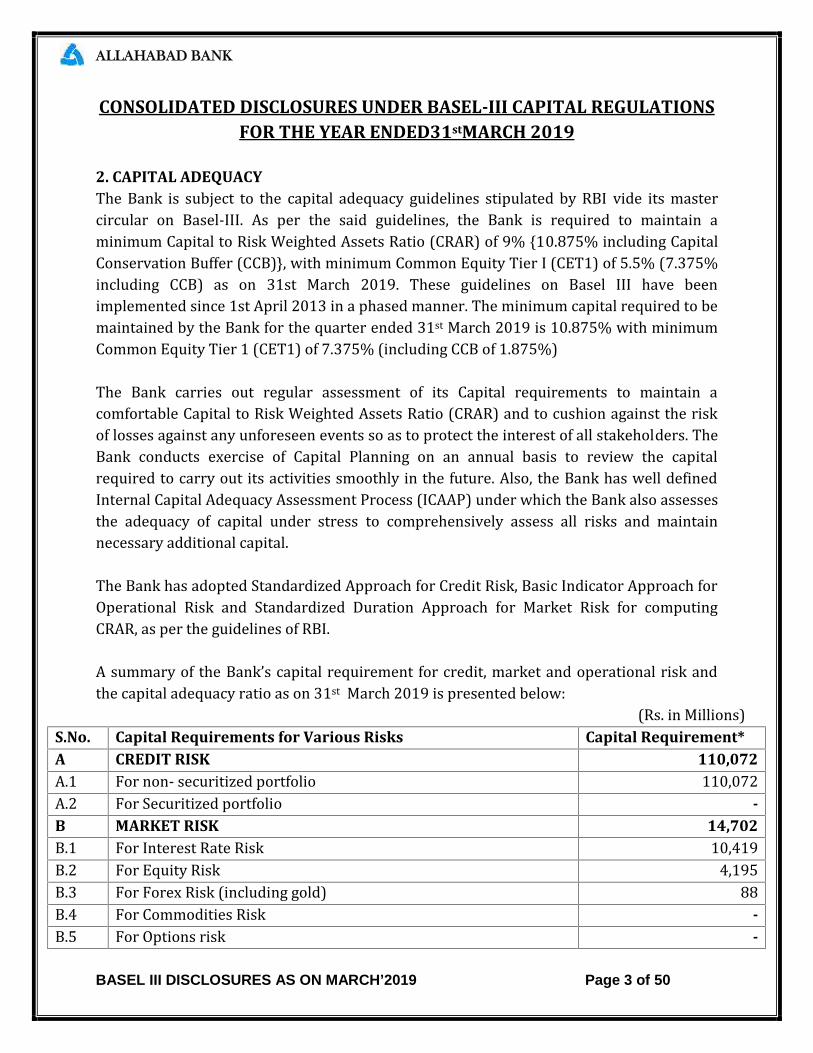

2. CAPITAL ADEQUACYThe Bank is subject to the capital adequacy guidelines stipulated by RBI vide its mastercircular on Basel-III. As per the said guidelines, the Bank is required to maintain aminimum Capital to Risk Weighted Assets Ratio (CRAR) of 9% {10.875% including CapitalConservation Buffer (CCB)}, with minimum Common Equity Tier I (CET1) of 5.5% (7.375%including CCB) as on 31st March 2019. These guidelines on Basel III have beenimplemented since 1st April 2013 in a phased manner. The minimum capital required to bemaintained by the Bank for the quarter ended 31st March 2019 is 10.875% with minimumCommon Equity Tier 1 (CET1) of 7.375% (including CCB of 1.875%)The Bank carries out regular assessment of its Capital requirements to maintain acomfortable Capital to Risk Weighted Assets Ratio (CRAR) and to cushion against the riskof losses against any unforeseen events so as to protect the interest of all stakeholders. TheBank conducts exercise of Capital Planning on an annual basis to review the capitalrequired to carry out its activities smoothly in the future. Also, the Bank has well definedInternal Capital Adequacy Assessment Process (ICAAP) under which the Bank also assessesthe adequacy of capital under stress to comprehensively assess all risks and maintainnecessary additional capital.The Bank has adopted Standardized Approach for Credit Risk, Basic Indicator Approach forOperational Risk and Standardized Duration Approach for Market Risk for computingCRAR, as per the guidelines of RBI.A summary of the Bank’s capital requirement for credit, market and operational risk andthe capital adequacy ratio as on 31st March 2019 is presented below: (Rs. in Millions)S.No. Capital Requirements for Various Risks Capital Requirement*A CREDIT RISK 110,072A.1 For non- securitized portfolio 110,072A.2 For Securitized portfolio -B MARKET RISK 14,702B.1 For Interest Rate Risk 10,419B.2 For Equity Risk 4,195B.3 For Forex Risk (including gold) 88B.4 For Commodities Risk -B.5 For Options risk -

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 4 of 50

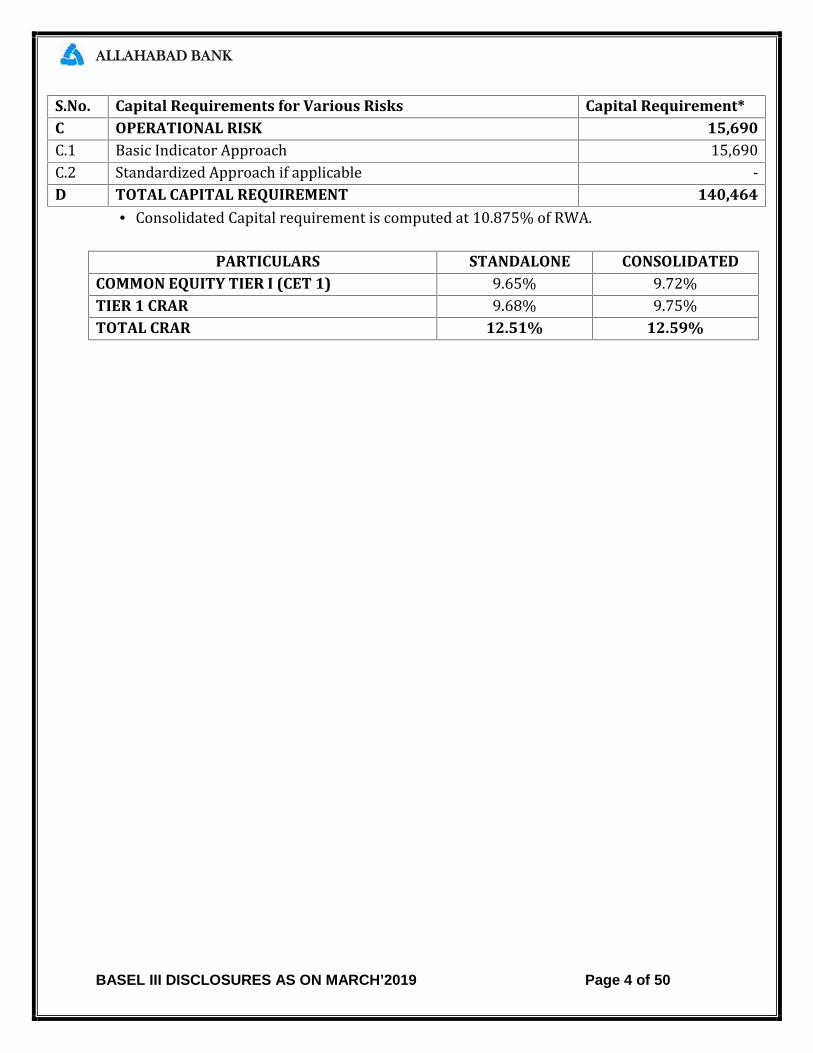

S.No. Capital Requirements for Various Risks Capital Requirement*C OPERATIONAL RISK 15,690C.1 Basic Indicator Approach 15,690C.2 Standardized Approach if applicable -D TOTAL CAPITAL REQUIREMENT 140,464

Consolidated Capital requirement is computed at 10.875% of RWA.PARTICULARS STANDALONE CONSOLIDATED

COMMON EQUITY TIER I (CET 1) 9.65% 9.72%TIER 1 CRAR 9.68% 9.75%TOTAL CRAR 12.51% 12.59%

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 5 of 50

3. CREDIT RISK: GENERAL DISCLOSURE

A. RISK MANAGEMENT: OBJECTIVES AND ORGANISATION STRUCTUREA.1.The Bank identifies, measures, control, monitor and report risk effectively. The keyparameters of the Bank’s risk management activities rely on the risk governancearchitecture, comprehensive processes and internal control mechanism based onBoard approved policies and guidelines.

B. ARCHITECTURE AND SYSTEMS OF THE BANKB.1.The Bank has nominated Chief Risk Officer, who reports to the Managing Directorand CEO.B.2.A Sub-Committee of Board of Directors termed as Risk Management Committee(RMC) has been constituted to specifically oversee and co-ordinate RiskManagement functions in the bank.B.3.A Credit Risk Management Committee of executives has been set up to formulateand implement various credit risk strategies including lending policy and tomonitor Bank’s Credit Risk Management functions on a regular basis.B.4.A Market Risk Management Committee of executives has been set up formanagement and to monitor Bank’s Market Risk Management functions on aregular basis.B.5.An Operational Risk Management Committee of executives has been set up forcontrol and monitoring of Bank’s Operational Risk Management functions on aregular basis.

C. CREDIT RISKCredit risk is defined as the possibility of losses associated with default by or diminution inthe credit quality of Borrowers or Counterparties arising from outright default due toinability or unwillingness of a borrower or counterparty to meet commitments in relationto lending, trading, settlement and other financial transactions; or Reduction in portfoliovalue arising from actual or perceived deterioration in credit quality of borrowers orcounterparties. Credit Risk emanates from a bank’s dealings with an individual, non-corporate, corporate, bank, financial institution or sovereign.D. BANK’S CREDIT RISK MANAGEMENT POLICY

D.1.The Bank has put in place a well-structured Credit Risk Management Policy dulyapproved by the Board. The Policy document defines organizational structure, roleand responsibilities and the processes whereby the Credit Risks carried by theBank can be identified, quantified, managed and controlled within the frameworkwhich the Bank considers consistent with its mandate and risk tolerance limits.

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 6 of 50

D.2.Credit Risk is monitored by the Bank account wise and compliance with the risklimits / exposure cap approved by the Board is ensured. The quality of internalcontrol system is also monitored and in-house expertise has been built up to tackleall the facets of Credit Risk.D.3.The Bank has taken earnest steps to put in place best Credit Risk Managementpractices. In addition to Credit Risk Management Policy, the Bank has also framedBoard approved Lending Policy, Investment Policy, Country Risk ManagementPolicy, Credit Monitoring Policy, Recovery Management Policy etc. which formintegral part in monitoring of credit risk and ensures compliance with variousregulatory requirements, more particularly in respect of Exposure norms, PrioritySector norms, Income Recognition and Asset Classification guidelines, CapitalAdequacy, Credit Risk Management guidelines etc. of RBI/other StatutoryAuthorities.D.4.Besides, the Bank has also put in place a Board approved policy on Credit RiskMitigation & Collateral Management which lays down the details of securities andadministration of such securities to protect the interests of the Bank. Thesesecurities act as mitigants against the credit risk to which the Bank is exposed.

E. CREDIT APPRAISAL / INTERNAL RATINGE.1. The Bank manages its credit risk by continuously measuring and monitoring ofrisks at each obligor (borrower) and portfolio level. The Bank has robust internallydeveloped credit risk grading / rating modules and well-established creditappraisal / approval processes.E.2. The internal risk rating / grading modules capture quantitative and qualitativeissues relating to management risk, business risk, industry risk, financial risk andproject risk. The data on industry risk is constantly updated based on marketconditions.E.3. The rating for every borrower is reviewed. As a measure of robust credit riskmanagement practices, the bank has implemented a four-tier system of creditrating process for the loan proposals sanctioned at Head Office Level, three tiersystems at Circle office/ Zonal Office level.Validation of rating for proposalssanctioned at Branch level is done at Zonal office level/Circle office level. For theproposals falling under the powers of Bank’s Head Office, the validation of ratings isdone at Risk Management Department.E.4. The Bank follows a well-defined multi layered discretionary power structure forsanction of loans. Various committees have been formed at ZO, FGMO & HO Level.ZLCC AGM/DGM headed by Zonal Head, FGMLCC headed by Field General Manager,HLCC GM headed by GM (Credit), HLCC ED headed by ED (Executive Director), CACheaded by MD & CEO and MCBOD (Management Committee of the Board) headedby MD& CEO. A structure named New Business Group (NBG) headed by MD& CEO

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 7 of 50

has been constituted at Head Office level for considering in-principle approval fortaking up fresh credit proposals above a specified cut-off point.E.5. Bank is introducing Retail & MSME processing cell to centralize the process andsanction of Retail & MSME loans. Similarly, Large Corporate branches, TradeFinance branches and Agriculture Finance branches are established for processingand sanction of specialized loans of the Bank.

F. DEFINITION OF PAST DUE AND IMPAIRED (FOR ACCOUNTING PURPOSES)The Bank follows Reserve Bank of India regulations, which are summed up below.F.1. NON-PERFORMING ASSETSAn asset, including a leased asset, becomes non-performing when it ceases to generateincome for the bank.

A non-performing asset (NPA) is a loan or an advance where;

I. Either Interest and/ or installment of principal dues remain 'overdue' for a period ofmore than 90 days in respect of a term loan,II. The account remains ‘out of order’ for 90 days as indicated below at paragraph F.2,in respect of an Overdraft/Cash Credit (OD/CC). Besides this CC/OD accounts canalso be declared NPA in undernoted condition.a. If the regular/ad-hoc limits are not reviewed/ renewed within 180 days fromthe due date of review/renewal or sanctioning of adhoc limit,b. If the stock statements are not submitted continuously for a period of 90days and limits/ drawings are allowed on such irregular drawing powercontinuously for 90 days.

III. The bill remains overdue and unpaid for a period of more than 90 days in the case ofbills purchased and discounted,IV. The installment of principal or interest thereon remains unpaid for two cropseasons beyond the due date for short duration crops,V. The installment of principal or interest thereon remains unpaid for one crop seasonbeyond the due date for long duration crops.

VI. The amount of liquidity facility remains outstanding for more than 90 days, inrespect of a securitization transaction undertaken in terms of guidelines onsecuritization dated February 1, 2006.VII. An account is classified as NPA only if the interest due &charged during any quarteris not serviced fully within 90 days from the end of the quarter.

F.2. 'OUT OF ORDER' STATUSAn account is treated as 'out of order' if the outstanding balance remains continuously inexcess of the sanctioned limit/drawing power for 90 days. In cases where the outstandingbalance in the principal operating account is less than the sanctioned limit/drawing power,

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 8 of 50

but there are no credits continuously for 90 days as on the date of Balance Sheet or creditsare not enough to cover the interest debited during the same period, these accounts aretreated as 'out of order'.F.3. OVERDUEAny amount due to the bank under any credit facility is ‘overdue’ if it is not paid on the duedate fixed by the bank.Bank identifies Special Mention Accounts (SMA) having principal or interest payment orany other amount wholly or partly overdue even for one day.F.4. NON-PERFORMING INVESTMENTSIn respect of securities, where interest/ principal is in arrears, the Bank does not reckonincome on the securities and makes appropriate provisions for the depreciation in thevalue of the investment.

A non-performing investment (NPI), similar to a non-performing advance (NPA), isone where:

I. Interest/ installment (including maturity proceeds) is due and remains unpaid formore than 90 days.II. This applies mutatis-mutandis to preference shares where the fixed dividend is notpaid.

III. In the case of equity shares, in the event the investment in the shares of anycompany is valued at Re.1 per company on account of the non-availability of thelatest balance sheet in accordance with the Reserve Bank of India instructions, thoseequity shares are also reckoned as NPI.IV. If any credit facility availed by the issuer is NPA in the books of the bank, theinvestments in any of the securities issued by the same issuer is also treated as NPIand vice versa.V. The investments in debentures / bonds, which are deemed to be in the nature ofadvance, are subjected to NPI norms as applicable to investments.

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 9 of 50

QUANTITATIVE DISCLOSURES

A. GROSS CREDIT RISK EXPOSURE Including Geographic Distribution of Exposure(Rs. in Millions)**Funded Exposure include Credit exposure and investment exposure#Non-Funded Exposure includes Bank Guarantee, LC and Forward ContractSl. No. Exposure* Type Domestic Overseas Total1. Fund Based 2,189,358 39,523 2,228,8812. Non-Fund Based 238,196 35 238,2313. Total 2,427,554 39,558 2,467,112

B. RESIDUAL CONTRACTUAL MATURITY BREAKDOWN OF ASSETS (Rs. in Millions)Buckets

Cash &RBI

Balances

BankBalances

#Advances Investments Fixed

AssetsOtherAssets

GrandTotalNext day 8814 3459 6908 134652 0 93 1539262 – 7 days 2736 12415 20908 16145 0 366 525708 –14 days 2752 0 21433 13244 0 399 3782815 – 30 days 770 0 49075 3148 0 541 53534Over 1 month– 2 months 950 0 36787 26980 0 1197 65914Over 2months – 3months 1274 0 90997 28000 0 1702 121973Over 3months – 6months 2778 0 88884 14287 0 3389 109338Over 6months – 1year 4935 0 129295 27456 0 6327 168013Over 1 year –3 years 28959 23343 344470 161371 0 23985 582128Over 3 years –5 years 14547 6395 176903 78214 0 22085 298144Over 5 years 28208 0 456461 290107 35383 29884 840043

Total 96723 45612 1422121 793604 35383 89968 2483411#Includes Balances with other banks and money at call & short notice.

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 10 of 50

C. NON-PERFORMING ASSETS (NPA) AND ITS MOVEMENTS. No. Particulars Amount in MillionsA. Amount of Gross NPA 287,048A. 1 Substandard 65,589A. 2 Doubtful 1 43,265A. 3 Doubtful 2 80,322A. 4 Doubtful 3 40,220A. 5 Loss 57,652B Net NPA 74,193C NPA RatiosC. 1 Gross NPAs to Gross Advances 17.55%C. 2 Net NPAs to Net Advances 5.22%D Movement of Gross NPAD. 1 Opening balance at the beginning of the year 2,65,628D. 2 Additions during the period 107,263D. 3 Reductions during the period 85,843D. 4 Closing balance as at end of the period 2,87,048

D. NON-PERFORMING INVESTMENTS (NPI) AND MOVEMENT OF PROVISION FORDEPRECIATION ON INVESTMENTS (Rs. in Millions)

S. No. Particulars AmountA. Amount of Non-Performing Investments 6,405B Amount of Provision held for Non-Performing Investments 6,078C Movement of provisions for depreciation on investmentsC. 1 Opening balance at the beginning of the year 13,221C. 2 Provisions made during the period 4,374C. 3 Write-off during the period -C. 4 Write-back of excess provisions during the period 0.00C. 5 Closing balance as at end of the period 17,595

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 11 of 50

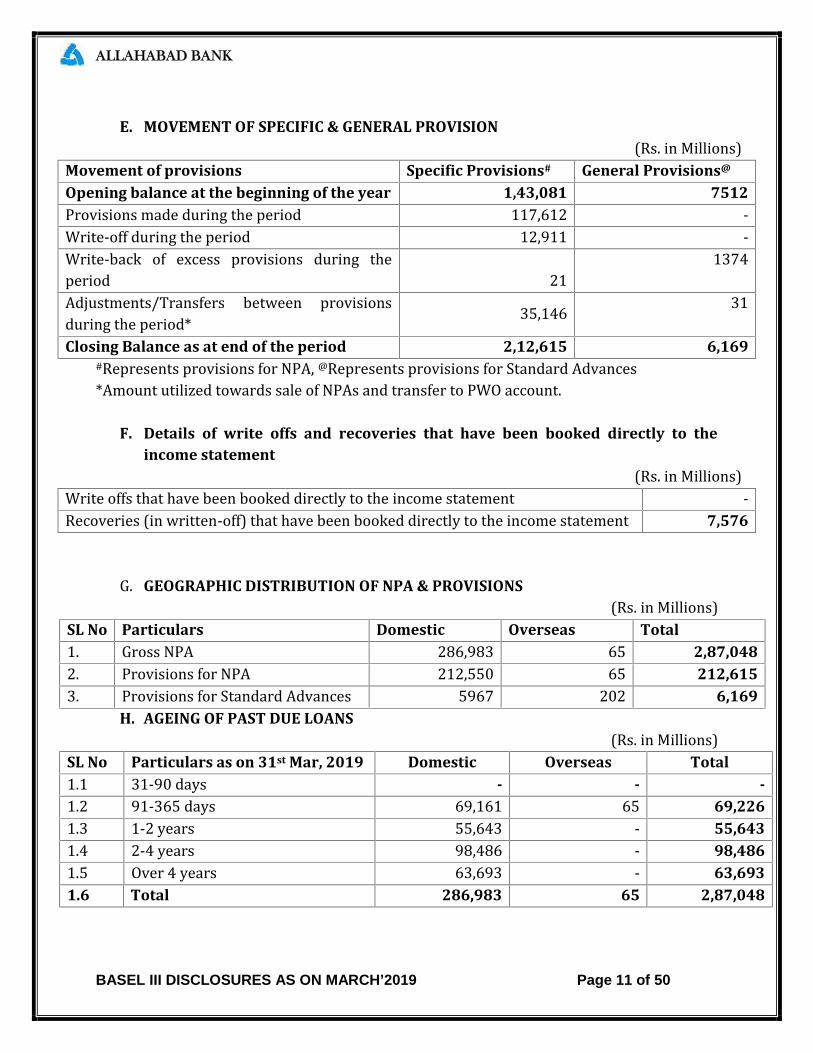

E. MOVEMENT OF SPECIFIC & GENERAL PROVISION (Rs. in Millions)Movement of provisions Specific Provisions# General Provisions@

Opening balance at the beginning of the year 1,43,081 7512Provisions made during the period 117,612 -Write-off during the period 12,911 -Write-back of excess provisions during theperiod 21 1374Adjustments/Transfers between provisionsduring the period* 35,146 31Closing Balance as at end of the period 2,12,615 6,169#Represents provisions for NPA, @Represents provisions for Standard Advances*Amount utilized towards sale of NPAs and transfer to PWO account.

F. Details of write offs and recoveries that have been booked directly to theincome statement (Rs. in Millions)Write offs that have been booked directly to the income statement -Recoveries (in written-off) that have been booked directly to the income statement 7,576

G. GEOGRAPHIC DISTRIBUTION OF NPA & PROVISIONS (Rs. in Millions)SL No Particulars Domestic Overseas Total1. Gross NPA 286,983 65 2,87,0482. Provisions for NPA 212,550 65 212,6153. Provisions for Standard Advances 5967 202 6,169

H. AGEING OF PAST DUE LOANS (Rs. in Millions)SL No Particulars as on 31st Mar, 2019 Domestic Overseas Total1.1 31-90 days - - -1.2 91-365 days 69,161 65 69,2261.3 1-2 years 55,643 - 55,6431.4 2-4 years 98,486 - 98,4861.5 Over 4 years 63,693 - 63,6931.6 Total 286,983 65 2,87,048

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 12 of 50

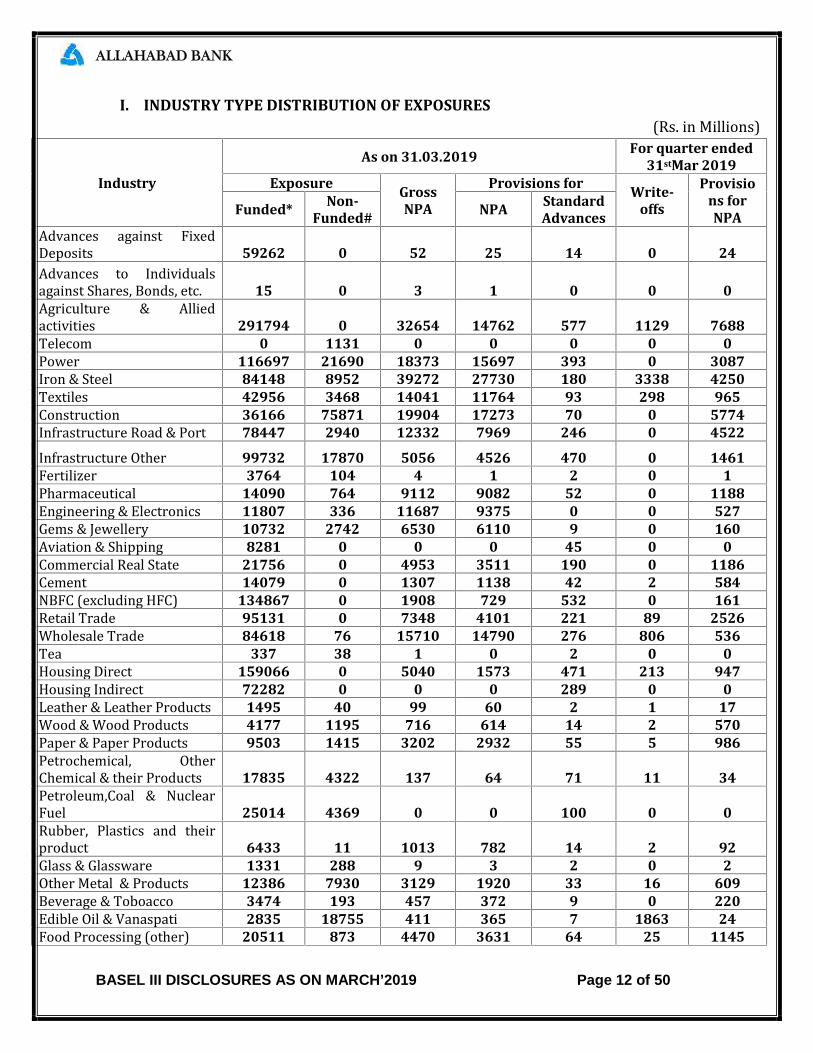

I. INDUSTRY TYPE DISTRIBUTION OF EXPOSURES (Rs. in Millions)Industry

As on 31.03.2019 For quarter ended31stMar 2019

Exposure GrossNPA

Provisions for Write-offs

Provisions forNPAFunded* Non-

Funded# NPA StandardAdvancesAdvances against FixedDeposits 59262 0 52 25 14 0 24Advances to Individualsagainst Shares, Bonds, etc. 15 0 3 1 0 0 0Agriculture & Alliedactivities 291794 0 32654 14762 577 1129 7688Telecom 0 1131 0 0 0 0 0Power 116697 21690 18373 15697 393 0 3087Iron & Steel 84148 8952 39272 27730 180 3338 4250Textiles 42956 3468 14041 11764 93 298 965Construction 36166 75871 19904 17273 70 0 5774Infrastructure Road & Port 78447 2940 12332 7969 246 0 4522Infrastructure Other 99732 17870 5056 4526 470 0 1461Fertilizer 3764 104 4 1 2 0 1Pharmaceutical 14090 764 9112 9082 52 0 1188Engineering & Electronics 11807 336 11687 9375 0 0 527Gems & Jewellery 10732 2742 6530 6110 9 0 160Aviation & Shipping 8281 0 0 0 45 0 0Commercial Real State 21756 0 4953 3511 190 0 1186Cement 14079 0 1307 1138 42 2 584NBFC (excluding HFC) 134867 0 1908 729 532 0 161Retail Trade 95131 0 7348 4101 221 89 2526Wholesale Trade 84618 76 15710 14790 276 806 536Tea 337 38 1 0 2 0 0Housing Direct 159066 0 5040 1573 471 213 947Housing Indirect 72282 0 0 0 289 0 0Leather & Leather Products 1495 40 99 60 2 1 17Wood & Wood Products 4177 1195 716 614 14 2 570Paper & Paper Products 9503 1415 3202 2932 55 5 986Petrochemical, OtherChemical & their Products 17835 4322 137 64 71 11 34Petroleum,Coal & NuclearFuel 25014 4369 0 0 100 0 0Rubber, Plastics and theirproduct 6433 11 1013 782 14 2 92Glass & Glassware 1331 288 9 3 2 0 2Other Metal & Products 12386 7930 3129 1920 33 16 609Beverage & Toboacco 3474 193 457 372 9 0 220Edible Oil & Vanaspati 2835 18755 411 365 7 1863 24Food Processing (other) 20511 873 4470 3631 64 25 1145

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 13 of 50

Industry

As on 31.03.2019 For quarter ended31stMar 2019

Exposure GrossNPA

Provisions for Write-offs

Provisions forNPAFunded* Non-

Funded# NPA StandardAdvancesMining & Quarrying 25647 93 11067 10326 58 609 39Vehicl and VehicleComponent 7735 1617 5616 5565 6 1122 1523Other Industry/ sectors notincluded above 650478 61148 51435 35824 1560 2067 11721

Total 2,228,881 238,231 287,048 212,615 6,169 11,598 52,569*Funded Exposure include Credit exposure and investment exposure#Non-Funded Exposure includes Bank Guarantee, LC and Forward ContractExposures to industries in excess of 5% of total Funded & Non-Funded of the Bank as

on Mar 31, 2019 (Rs. in Millions)S. No. Industry % of Funded &Non-Funded Exposure1. Infrastructure 13.67%1.1 Out of which: Power 5.61%3. Non-Banking Finance Companies 8.39%

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 14 of 50

4. CREDIT RISK: DISCLOSURES FOR PORTFOLIOS SUBJECT TO THE STANDARDIZEDAPPROACHThe Bank has used the Standardized Approach under the RBI’s Basel III capital regulationsfor calculation of risk-weighted assets of its credit portfolio. The RBI guidelines requirebanks to use ratings assigned by specified External Credit Rating Agencies (ECRA) namelyBrickworks, CARE, CRISIL, ICRA, India Ratings, SMERA and Infomerics for domesticcounterparties and Standard & Poor’s, Moody’s and Fitch for foreign counterparties.The Bank is using issuer ratings and short-term and long-term instrument/bank facilities’ratings which are assigned by the accredited rating agencies, i.e. ECRA, published in thepublic domain to assign risk-weights in terms of RBI guidelines. In respect of claims onnon-resident corporates and foreign banks, ratings assigned by international ratingagencies i.e. Standard & Poor’s, Moody’s and Fitch is used.

QUANTITATIVE DISCLOSURESThe Bank’s exposureon its advance portfolio (rated and unrated) bifurcated in three majorrisk buckets are as follows: (Rs. in Millions)Sl No Risk Weight Fund Based Non-Fund Based1 Below 100% risk weight 1,466,949 126,7712 100% risk weight 205,488 64,6823 More than 100% risk weight 556,444 46,7784 Deduction from capital funds - -5 Total Exposure 2,228,881 238,231

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 15 of 50

5. CREDIT RISK MITIGATION: DISCLOSURES FOR STANDARDIZED APPROACHESThe Bank uses various collaterals both financial as well as non-financial, guarantees andcredit insurance as credit risk mitigants based on its board approved Credit Risk Mitigationand Collateral Management policy which include detailed guidelines for risk mitigation andcollateral management. The policy covers aspects such as the nature of riskmitigants/collaterals acceptable to the Bank, the documentation and custodialarrangement of the collateral, the valuation approach and periodicity etc.For the purpose of computation of capital requirement for Credit Risk, the Bank recognizesonly those collaterals that are considered as eligible for risk mitigation in the RBI Basel IIIguidelines on standardized approach, which are as follows: Cash deposit with the Bank Gold, including bullion and jewelry Securities issued by Central and State Governments Kisan Vikas Patra and National Savings Certificates Life insurance policies with a declared surrender value Debt securities rated at least BBB (-)/PR3/P3/F3/A3 Units of Mutual FundsThe Bank uses the comprehensive approach in capital assessment. In the comprehensiveapproach, when taking collateral, the Bank calculates the adjusted exposure tocounterparty for capital adequacy purposes by netting off the effects of that collateral. TheBank adjusts the value of any collateral by a haircut, as prescribed by RBI, to take intoaccount possible future fluctuations in the value of the security occasioned by marketmovements.For purposes of capital calculation, the Bank recognizes the credit protection i.e.guarantees, given by the following entities, considered eligible as per RBI guidelines: Sovereigns i.e. Central and State Governments Sovereign entities which include Export Credit Guarantee Corporation(ECGC), Credit Guarantee Fund Trust for Micro and Small Enterprises(CGTMSE) and other guarantees covered under National Credit GuaranteeTrustee Company Limited (NCGTC).The credit risk mitigation taken is largely in the form of cash deposit with the Bank andthus the risk (credit and market) concentration of the mitigants is low.

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 16 of 50

QUANTITATIVE DISCLOSURES

Exposure covered by Credit MitigantsParticulars Rs.in MillionsTotal exposure covered by eligible financial collateral 132,530Total exposure covered by guarantees 97,863

6. SECURITIZATION: DISCLOSURE FOR STANDARDIZED APPROACH QUALITATIVEDISCLOSURES: The Bank/Group does not have any securitization exposure.

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 17 of 50

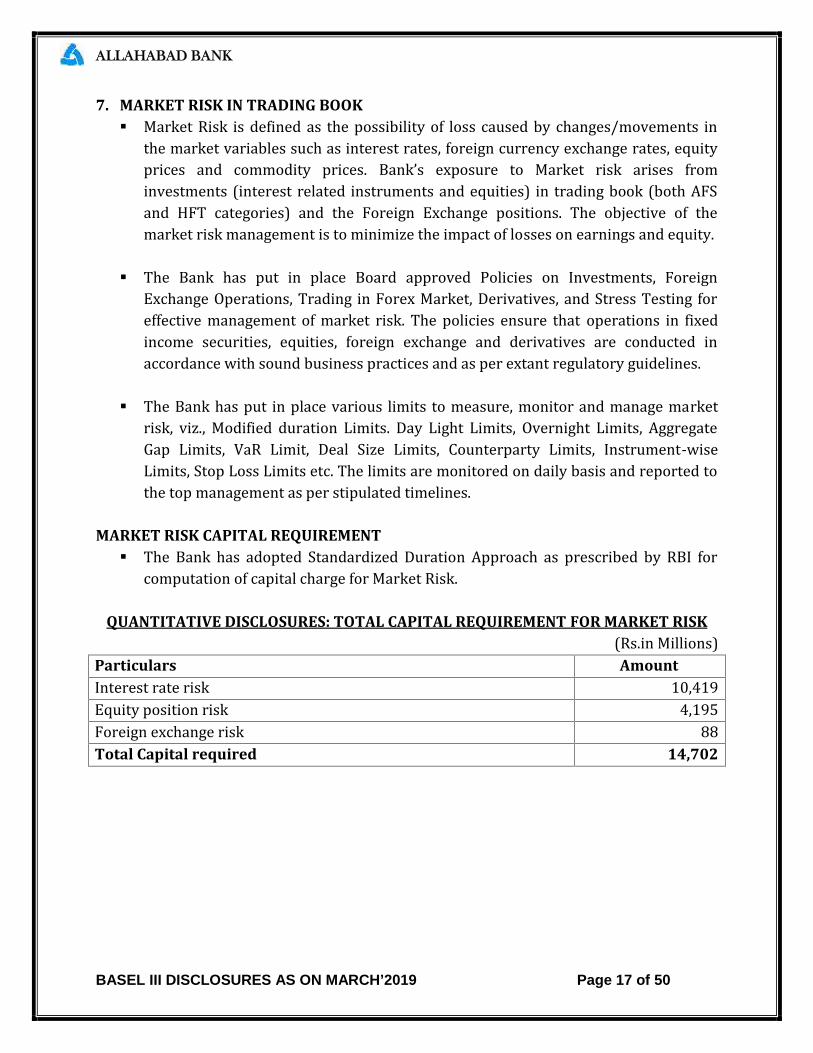

7. MARKET RISK IN TRADING BOOK Market Risk is defined as the possibility of loss caused by changes/movements inthe market variables such as interest rates, foreign currency exchange rates, equityprices and commodity prices. Bank’s exposure to Market risk arises frominvestments (interest related instruments and equities) in trading book (both AFSand HFT categories) and the Foreign Exchange positions. The objective of themarket risk management is to minimize the impact of losses on earnings and equity. The Bank has put in place Board approved Policies on Investments, ForeignExchange Operations, Trading in Forex Market, Derivatives, and Stress Testing foreffective management of market risk. The policies ensure that operations in fixedincome securities, equities, foreign exchange and derivatives are conducted inaccordance with sound business practices and as per extant regulatory guidelines. The Bank has put in place various limits to measure, monitor and manage marketrisk, viz., Modified duration Limits. Day Light Limits, Overnight Limits, AggregateGap Limits, VaR Limit, Deal Size Limits, Counterparty Limits, Instrument-wiseLimits, Stop Loss Limits etc. The limits are monitored on daily basis and reported tothe top management as per stipulated timelines.

MARKET RISK CAPITAL REQUIREMENT The Bank has adopted Standardized Duration Approach as prescribed by RBI forcomputation of capital charge for Market Risk.

QUANTITATIVE DISCLOSURES: TOTAL CAPITAL REQUIREMENT FOR MARKET RISK(Rs.in Millions)Particulars AmountInterest rate risk 10,419Equity position risk 4,195Foreign exchange risk 88Total Capital required 14,702

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 18 of 50

8. OPERATIONAL RISK Operational Risk is the risk of loss resulting from inadequate or failed internalprocesses, people and systems or from external events. Operational risk includeslegal risk but excludes strategic and reputation risks. The Bank has framed Operational Risk Management Policy duly approved by theBoard. Supporting policies adopted by the Board which deal with management ofvarious areas of operational risk are (a) Compliance Risk Management Policy (b)Forex Risk Management Policy (c) Policy Document on Know Your Customers (KYC)and Anti Money Laundering (AML) Procedures (d) Business Continuity and DisasterRecovery Policy (e) Fraud Risk Management Policy etc. The Operational Risk Management Policy adopted by the Bank outlines organizationstructure and detailed processes for management of operational risk. The basicobjective of the policy is to closely integrate operational risk management systeminto the day-to-day risk management processes of the Bank by clearly assigningroles for effectively identifying, assessing, monitoring and controlling / mitigatingoperational risks and by timely reporting of operational risk exposures, includingmaterial operational losses. Operational risks in the Bank are managed throughcomprehensive and well-articulated internal control frameworks.

CAPITAL REQUIREMENT The Bank has adopted the Basic Indicator Approach for computing capital forOperational Risk. As per the guidelines, the capital for operational risk is equal to15% of average positive annual Gross Income of previous three years as defined byRBI. Accordingly, the capital requirement for operational risk as on 31.03.2019 is

Rs. 15,690Million.

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 19 of 50

9. INTEREST RATE RISK IN THE BANKING BOOK (IRRBB) Interest Rate Risk is the risk where changes in market interest rates might adverselyaffect a Bank’s financial condition. The immediate impact of changes in interestrates is on Bank’s earnings i.e. Net Interest Income (NII). A long -term impact ofchanging interest rates is on Bank’s Market Value of Equity (MVE) or Net Worth asthe economic value of Bank’s assets, liabilities and off-balance sheet positions getaffected due to variation in market interest rates. The impact on income (Earnings perspective) is measured through use ofTraditional Gap analysis, which measures mismatch between rate sensitiveliabilities and rate sensitive assets (including off-balance sheet positions) overdifferent time intervals, as at a given date. The impact of interest rate risk on NII isassessed by applying notional rate shock of 100,200 & 300 bps on gaps in varioustime bucket up to a period of one year as prescribed in Bank’s ALM Policy. The Bank has adopted Duration Gap Analysis (DGA) to measure interest rate risk inits balance sheet from the economic value perspective. The Bank computes bucket-wise Modified Duration of Rate Sensitive Liabilities and Assets using the suggestedcommon maturity, coupon and yield parameters, prescribed by RBI/BOARD. TheModified Duration Gap is computed from weighted average modified duration oftotal rate sensitive assets and rate sensitive liabilities. The impact of change ininterest rate on net worth is analyzed by applying a notional interest rate shock of100, 200 & 300 bps. The analysis & reporting of Interest rate risk is done by the Bank on a monthlybasis.

QUANTITATIVE DISCLOSURES Rs in Millions1. Change in Interest Rate Earnings at Risk (NII)1.00% 11612. Change in Interest Rate Economic Value of Equity at Risk

(Net Worth)1.00% 7776

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 20 of 50

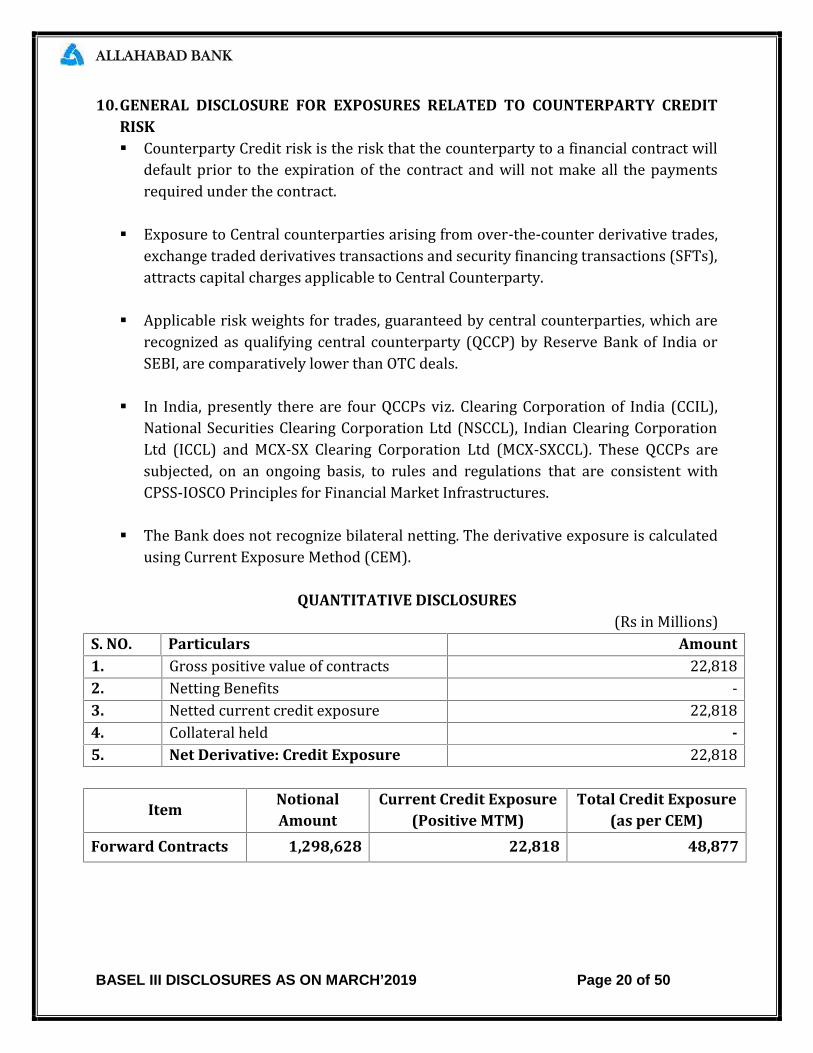

10.GENERAL DISCLOSURE FOR EXPOSURES RELATED TO COUNTERPARTY CREDITRISK Counterparty Credit risk is the risk that the counterparty to a financial contract willdefault prior to the expiration of the contract and will not make all the paymentsrequired under the contract. Exposure to Central counterparties arising from over-the-counter derivative trades,exchange traded derivatives transactions and security financing transactions (SFTs),attracts capital charges applicable to Central Counterparty. Applicable risk weights for trades, guaranteed by central counterparties, which arerecognized as qualifying central counterparty (QCCP) by Reserve Bank of India orSEBI, are comparatively lower than OTC deals. In India, presently there are four QCCPs viz. Clearing Corporation of India (CCIL),National Securities Clearing Corporation Ltd (NSCCL), Indian Clearing CorporationLtd (ICCL) and MCX-SX Clearing Corporation Ltd (MCX-SXCCL). These QCCPs aresubjected, on an ongoing basis, to rules and regulations that are consistent withCPSS-IOSCO Principles for Financial Market Infrastructures. The Bank does not recognize bilateral netting. The derivative exposure is calculatedusing Current Exposure Method (CEM).

QUANTITATIVE DISCLOSURES (Rs in Millions)S. NO. Particulars Amount1. Gross positive value of contracts 22,8182. Netting Benefits -3. Netted current credit exposure 22,8184. Collateral held -5. Net Derivative: Credit Exposure 22,818

Item NotionalAmount

Current Credit Exposure(Positive MTM)

Total Credit Exposure(as per CEM)

Forward Contracts 1,298,628 22,818 48,877

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 21 of 50

11.Composition of Capital (Rs. in Millions)Particulars Amount

AmountsSubject to Pre-

Basel IIITreatment

Ref No.

Common Equity Tier 1 Capital: Instruments and Reserves1 Directly issued qualifying common share capital plusrelated stock surplus (share premium) 112,850 A1 + A22 Retained earnings (135,740) A33 Accumulated other comprehensive income (and otherreserves) 166,439 B1 + B2+B3+ B4 +B5 + B6+B74 Directly issued capital subject to phase out from CET1(only applicable to non-joint stock companies) -

Public sector capital injections grandfathered until1 January 2018 -5 Common share capital issued by subsidiaries and heldby third parties (amount allowed in group CET1) - -

6 Common Equity Tier 1 capital before regulatoryadjustments 143,549

Common Equity Tier 1 capital: regulatory adjustments7 Prudential valuation adjustments - -8 Goodwill (net of related tax liability) -9 Intangibles other than mortgage-servicing rights(net of related tax liability) 502 - C110 Deferred tax assets 11,290 Part ofC211 Cash-flow hedge reserve -12 Shortfall of provisions to expected losses -13 Securitization gain on sale -14 Gains and losses due to changes in own credit risk onfair valued liabilities -15 Defined-benefit pension fund net assets -16 Investments in own shares (if not already netted offpaid-in capital on reported balance sheet) -17 Reciprocal cross-holdings in common equity 1,036 - C318 Investments in the capital of Banking, financial andinsurance entities that are outside the scope ofregulatory consolidation, net of eligible shortpositions, where the Bank does not own more than -

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 22 of 50

Particulars Amount

AmountsSubject to Pre-

Basel IIITreatment

Ref No.

10% of the issued share capital (amount above 10%threshold)19 Significant investments in the common stock ofBanking, financial and insurance entities that areoutside the scope of regulatory consolidation, net ofeligible short positions (amount above 10%threshold) -

20 Mortgage servicing rights (amount above 10%threshold) -

21 Deferred tax assets arising from temporarydifferences (amount above 10% threshold, net ofrelated tax liability) 4,16122 Amount exceeding the 15% threshold -23 of which: significant investments in the commonstock of financials -24 of which: mortgage servicing rights -25 of which: deferred tax assets arising from temporarydifferences -26 National specific regulatory adjustments(26a+26b+26c+26d) 1,05026a Of which: Investments in the equity capital ofunconsolidated insurance subsidiaries 1,050 Part ofC526b Of which: Investment in the equity capital ofunconsolidated non-financial subsidiaries26c Of which: Shortfall in the equity capital of majorityowned financial entities which have not beenconsolidated with the Bank26d Of which: Unamortized pension funds expendituresREGULATORY ADJUSTMENTS APPLIED TO COMMONEQUITY TIER 1 IN RESPECT OF AMOUNTS SUBJECTTO PRE-BASEL III TREATMENTOF WHICH: Investment in the equity capital ofconsolidated financial subsidiaries -

27 Regulatory adjustments applied to Common EquityTier 1 due to insufficient Additional Tier 1 and Tier 2to cover deductions -

28 Total regulatory adjustments to Common equityTier 1 18,03929 Common Equity Tier 1 capital (CET1) 125,510

Additional Tier 1 capital: instruments30 Directly issued qualifying Additional Tier 1 -

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 23 of 50

Particulars Amount

AmountsSubject to Pre-

Basel IIITreatment

Ref No.

instruments plus related stock surplus (31+32)31 of which: classified as equity under applicableaccounting standards (Perpetual Non-CumulativePreference Shares) -

32 of which: classified as liabilities under applicableaccounting standards (Perpetual debt Instruments) - E533 Directly issued capital instruments subject to phaseout from Additional Tier 1 450 E134 Additional Tier 1 instruments (and CET1 instrumentsnot included in row 5) issued by subsidiaries and heldby third parties (amount allowed in group AT1) -

35 of which: instruments issued by subsidiaries subjectto phase out -36 Additional Tier 1 capital before regulatoryadjustments 450

Additional Tier 1 capital: regulatory adjustments37 Investments in own Additional Tier 1 instruments -38 Reciprocal cross-holdings in Additional Tier 1instruments -

39Investments in the capital of Banking, financial andinsurance entities that are outside the scope ofregulatory consolidation, net of eligible shortpositions, where the Bank does not own more than10% of the issued common share capital of the entity(amount above 10% threshold)

-

40 Significant investments in the capital of Banking,financial and insurance entities that are outside thescope of regulatory consolidation (net of eligible shortpositions) -

41 National specific regulatory adjustments (41a + 41b) -41a Investments in Additional Tier I Capital ofunconsolidated insurance subsidiaries -

41b Shortfall in the Additional Tier 1 capital of majorityowned financial entities which have not beenconsolidated with the Bank -REGULATORY ADJUSTMENTS APPLIED TOADDITIONAL TIER 1 IN RESPECT OF AMOUNTSSUBJECT TO PRE-BASEL III TREATMENT -

42 Regulatory adjustments applied to Additional Tier 1due to insufficient Tier 2 to cover deductions -43 Total regulatory adjustments to Additional Tier 1 -

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 24 of 50

Particulars Amount

AmountsSubject to Pre-

Basel IIITreatment

Ref No.

capital44 Additional Tier 1 capital (AT1) 45045 Tier 1 capital (T1 = CET1 + AT1) (row 29 + row 44) 125,960Tier 2 capital: instruments and provisions46 Directly issued qualifying Tier 2 instruments plusrelated stock surplus 25,000 E447 Directly issued capital instruments subject to phaseout from Tier 2 5,000 E2+ E348 Tier 2 instruments (and CET1 and AT1 instrumentsnot included in rows 5 or 34) issued by subsidiariesand held by third parties (amount allowed in groupTier 2) -49 of which: instruments issued by subsidiaries subjectto phase out -50 Provisions 6,716 D1+ partofD2+D351 Tier 2 capital before regulatory adjustments 36,716Tier 2 capital: regulatory adjustments52 Investments in own Tier 2 instruments -53 Reciprocal cross-holdings in Tier 2 instruments 50 - C454

Investments in the capital of Banking, financial andinsurance entities that are outside the scope ofregulatory consolidation, net of eligible shortpositions, where the Bank does not own more than10% of the issued common share capital of the entity(amount above the 10% threshold)-

55 Significant investments in the capital Banking,financial and insurance entities that are outside thescope of regulatory consolidation (net of eligible shortpositions) -

56 National specific regulatory adjustments (56a+56b) -56a Of which: Investments in the Tier II capital ofunconsolidated subsidiaries -

56b Of which: Shortfall in the Tier 2 capital of majorityowned financial entities which have not beenconsolidated with the Bank -REGULATORY ADJUSTMENTS APPLIED TO TIER 2 INRESPECT OF AMOUNTS SUBJECT TO PRE-BASEL IIITREATMENT -57 Total regulatory adjustments to Tier 2 capital 50

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 25 of 50

Particulars Amount

AmountsSubject to Pre-

Basel IIITreatment

Ref No.

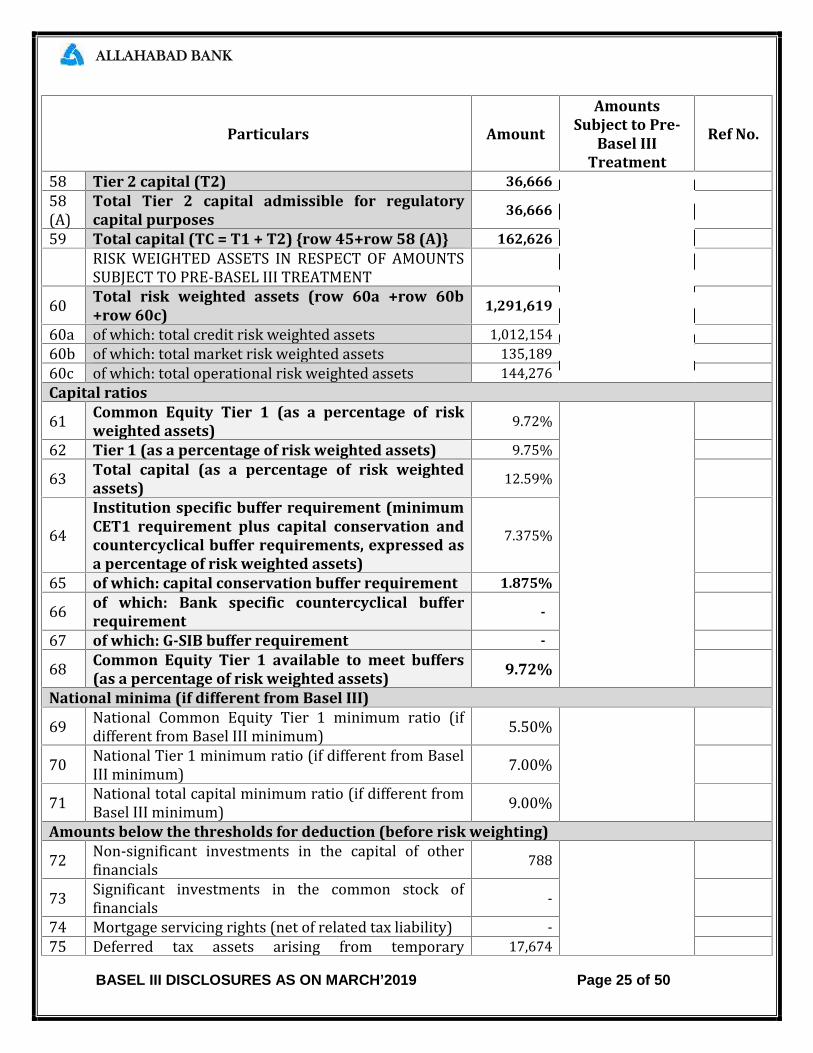

58 Tier 2 capital (T2) 36,66658(A) Total Tier 2 capital admissible for regulatorycapital purposes 36,66659 Total capital (TC = T1 + T2) {row 45+row 58 (A)} 162,626RISK WEIGHTED ASSETS IN RESPECT OF AMOUNTSSUBJECT TO PRE-BASEL III TREATMENT60 Total risk weighted assets (row 60a +row 60b+row 60c) 1,291,61960a of which: total credit risk weighted assets 1,012,15460b of which: total market risk weighted assets 135,18960c of which: total operational risk weighted assets 144,276

Capital ratios61 Common Equity Tier 1 (as a percentage of riskweighted assets) 9.72%62 Tier 1 (as a percentage of risk weighted assets) 9.75%63 Total capital (as a percentage of risk weightedassets) 12.59%

64 Institution specific buffer requirement (minimumCET1 requirement plus capital conservation andcountercyclical buffer requirements, expressed asa percentage of risk weighted assets)

7.375%65 of which: capital conservation buffer requirement 1.875%66 of which: Bank specific countercyclical buffer

requirement -67 of which: G-SIB buffer requirement -68 Common Equity Tier 1 available to meet buffers(as a percentage of risk weighted assets) 9.72%

National minima (if different from Basel III)69 National Common Equity Tier 1 minimum ratio (ifdifferent from Basel III minimum) 5.50%70 National Tier 1 minimum ratio (if different from BaselIII minimum) 7.00%71 National total capital minimum ratio (if different fromBasel III minimum) 9.00%Amounts below the thresholds for deduction (before risk weighting)72 Non-significant investments in the capital of otherfinancials 78873 Significant investments in the common stock offinancials -74 Mortgage servicing rights (net of related tax liability) -75 Deferred tax assets arising from temporary 17,674

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 26 of 50

Particulars Amount

AmountsSubject to Pre-

Basel IIITreatment

Ref No.

differences (net of related tax liability)Applicable caps on the inclusion of provisions in Tier 276 Provisions eligible for inclusion in Tier 2 in respect ofexposures subject to standardized approach (prior toapplication of cap) 6,71677 Cap on inclusion of provisions in Tier 2 understandardized approach 12,65278 Provisions eligible for inclusion in Tier 2 in respect ofexposures subject to internal ratings-based approach(prior to application of cap) NA79 Cap for inclusion of provisions in Tier 2 under internalratings-based approach NACapital instruments subject to phase-out arrangements (only applicable between March 31, 2017and March 31, 2021)80 Current cap on CET1 instruments subject to phase outarrangements NA81 Amount excluded from CET1 due to cap (excess overcap after redemptions and maturities) NA82 Current cap on AT1 instruments subject to phase outarrangements NA83 Amount excluded from AT1 due to cap (excess overcap after redemptions and maturities) NA84 Current cap on T2 instruments subject to phase outarrangements NA85 Amount excluded from T2 due to cap (excess over capafter redemptions and maturities) NA

Notes to the Template

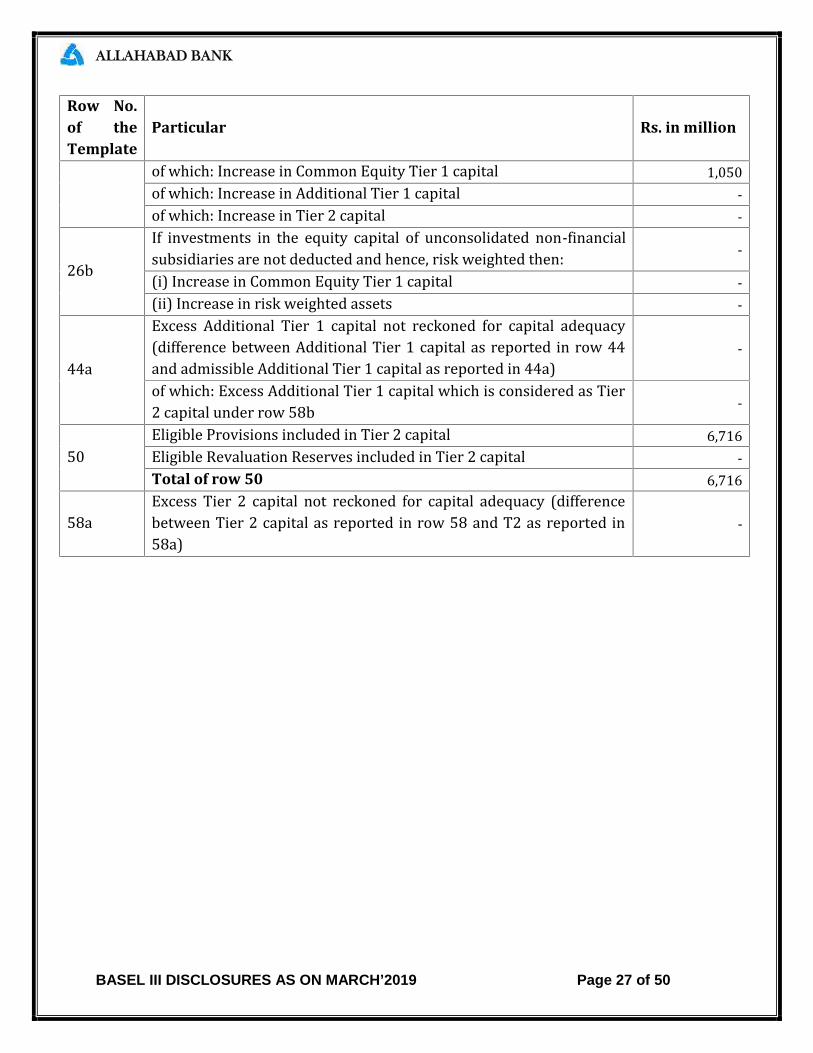

Row No.of theTemplate

Particular Rs. in million

10 Deferred tax assets associated with accumulated losses 11,290Deferred tax assets (excluding those associated with accumulatedlosses) net of Deferred tax liability 17,674Total as indicated in row 10 28,96419 If investments in insurance subsidiaries are not deducted fully fromcapital and instead considered under 10% threshold for deduction,the resultant increase in the capital of bank 1,050

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 27 of 50

Row No.of theTemplate

Particular Rs. in millionof which: Increase in Common Equity Tier 1 capital 1,050of which: Increase in Additional Tier 1 capital -of which: Increase in Tier 2 capital -26b If investments in the equity capital of unconsolidated non-financialsubsidiaries are not deducted and hence, risk weighted then: -(i) Increase in Common Equity Tier 1 capital -(ii) Increase in risk weighted assets -44a Excess Additional Tier 1 capital not reckoned for capital adequacy(difference between Additional Tier 1 capital as reported in row 44and admissible Additional Tier 1 capital as reported in 44a) -of which: Excess Additional Tier 1 capital which is considered as Tier2 capital under row 58b -50 Eligible Provisions included in Tier 2 capital 6,716Eligible Revaluation Reserves included in Tier 2 capital -

Total of row 50 6,71658a Excess Tier 2 capital not reckoned for capital adequacy (differencebetween Tier 2 capital as reported in row 58 and T2 as reported in58a) -

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 28 of 50

12.Composition of Capital- Reconciliation Requirements (Rs. in millions)Step- 1

S. No. ParticularsBalance sheet asin financialstatements

Balance sheet as perregulatory Scope ofconsolidation

A. Capital & Liabilities

i.

Paid-up Capital 20,968 20,968Reserves & Surplus 72,989 71,513of which:Statutory Reserve 32,261 32,261Capital Reserve 5,103 4,625Revenue & Other Reserves 31,956 31,956Investment Reserve Account 1,386 1,386Share Premium 91,881 91,881Special Reserve 14,500 14,500Revaluation Reserve 29,437 29,437Balance in Profit & Loss Account (134,742) (135,740)of which: Balance in Profit & LossAccount as per last financial Year (50,168) (50,779)Foreign Currency TranslationReserves 1,188 1,188I R S Reserve 19 19Minority Interest - -Share application money pendingallotment 68,960 68,960Total Capital 162,917 161,441

ii.

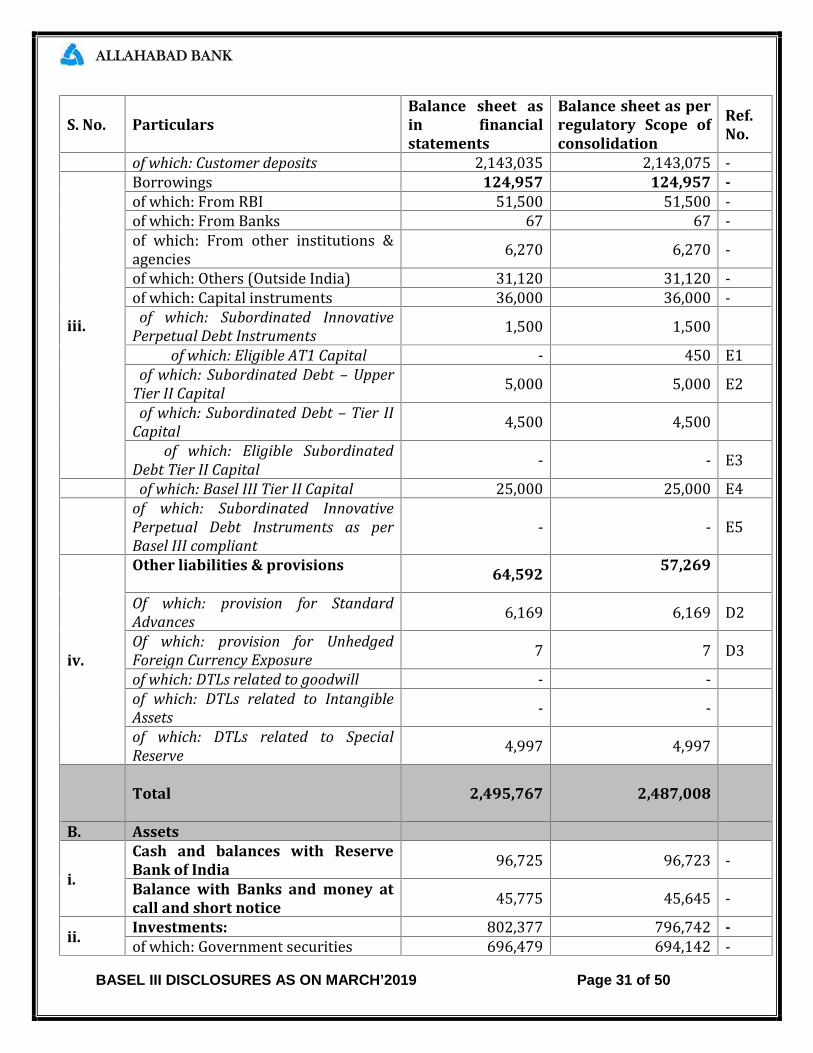

Deposits2,143,301 2,143,341of which: Deposits from Banks 266 266of which: Customer deposits2,143,035 2,143,075

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 29 of 50

S. No. ParticularsBalance sheet asin financialstatements

Balance sheet as perregulatory Scope ofconsolidation

iii.

Borrowings124,957 124,957of which: From RBI 51,500 51,500of which: From Banks 67 67of which: From other institutions&agencies 6,270 6,270of which: Others (Outside India) 31,120 31,120of which: Capital instruments 36,000 36,000of which: Subordinated InnovativePerpetual Debt Instruments 1,500 1,500of which: Subordinated InnovativePerpetual Debt Instruments Basel IIICompliant - -of which: Subordinated Debt – UpperTier II Capital 5,000 5,000of which: Subordinated Debt – Tier IICapital 4,500 4,500of which: Subordinated Debt – Tier IIBasel III Capital 25,000 25,000

iv. Other liabilities & provisions 64,592 57,269Total 2,495,767 2,487,008

B. Assets

i.

Cash and balances with ReserveBank of India 96,725 96,723Balance with Banks and money atcall and short notice 45,775 45,645

ii.

Investments: 802,377 796,742of which: Government securities 696,479 694,142of which: Other approved securities - -of which: Shares 5,471 5,394of which: Debentures & Bonds 55,523 53,359of which: Subsidiaries / Joint Ventures/ Associates 1,312 2,362of which: Others (Commercial Papers,Mutual Funds etc.) 43,592 41,486iii.

Loans and advances 1,422,122 1,422,122of which: Loans and advances toBanks 26,392 26,392of which: Loans and advances tocustomers 1,395,730 1,395,730iv. Fixed assets 35,523 35,410

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 30 of 50

S. No. ParticularsBalance sheet asin financialstatements

Balance sheet as perregulatory Scope ofconsolidation

v.

Other assets 93,245 90,367of which: Goodwill and intangibleassets 509 502of which: Deferred tax assets 28,966 28,968vi. Goodwill on consolidation - -vii. Debit balance in Profit & Loss account - -

Total Assets 2,495,767 2,487,008

Step – 2

S. No. ParticularsBalance sheet asin financialstatements

Balance sheet as perregulatory Scope ofconsolidation

Ref.No.

A. Capital & Liabilities

i.

Paid-up Capital 20,968 20,968of which: Amount eligible for CET1 - 20,968 A1of which: Amount eligible for AT1 - -Reserves & Surplus 72,989 71,513of which:Statutory Reserve 32,261 32,261 B1Capital Reserve 5,103 4,625 B2Revenue & Other Reserves 31,956 31,956 B3Investment Reserve Account 1,386 1,386 D1Share Premium 91,881 91,881 A2Special Reserve 14,500 14,500 B4Revaluation Reserve 29,437 29,437of which: Amount eligible for CET1 - 13247 B5of which: Amount eligible for Tier II - -Balance in Profit & Loss Account (134,742) (135,740) A3of which: Balance in Profit & LossAccount as per last financial Year (50,168) (50,779)Foreign Currency TranslationReserves 1,188 1,188of which: Considered under Capitalfund - 891 B6IRS Reserve 19 19Share application money pendingallotment 68,960 68,960 B7Minority Interest - - -Total Capital 162,917 161,441 -

ii. Deposits 2,143,301 2,143,341 -of which: Deposits from Banks 266 266 -

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 31 of 50

S. No. ParticularsBalance sheet asin financialstatements

Balance sheet as perregulatory Scope ofconsolidation

Ref.No.

of which: Customer deposits 2,143,035 2,143,075 -

iii.

Borrowings 124,957 124,957 -of which: From RBI 51,500 51,500 -of which: From Banks 67 67 -of which: From other institutions &agencies 6,270 6,270 -of which: Others (Outside India) 31,120 31,120 -of which: Capital instruments 36,000 36,000 -of which: Subordinated Innovative

Perpetual Debt Instruments 1,500 1,500of which: Eligible AT1 Capital - 450 E1

of which: Subordinated Debt – UpperTier II Capital 5,000 5,000 E2

of which: Subordinated Debt – Tier IICapital 4,500 4,500

of which: Eligible SubordinatedDebt Tier II Capital - - E3

of which: Basel III Tier II Capital 25,000 25,000 E4of which: Subordinated InnovativePerpetual Debt Instruments as perBasel III compliant

- - E5

iv.

Other liabilities & provisions 64,592 57,269

Of which: provision for StandardAdvances 6,169 6,169 D2Of which: provision for UnhedgedForeign Currency Exposure 7 7 D3of which: DTLs related to goodwill - -of which: DTLs related to IntangibleAssets - -of which: DTLs related to SpecialReserve 4,997 4,997Total 2,495,767 2,487,008

B. Assets

i.

Cash and balances with ReserveBank of India 96,725 96,723 -Balance with Banks and money atcall and short notice 45,775 45,645 -

ii. Investments: 802,377 796,742 -of which: Government securities 696,479 694,142 -

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 32 of 50

S. No. ParticularsBalance sheet asin financialstatements

Balance sheet as perregulatory Scope ofconsolidation

Ref.No.of which: Other approved securities - - -of which: Shares 5,471 5,394

of which: Reciprocal Cross Holding 1,038 1,038 C3of which: Debentures & Bonds 55,523 53,359of which: Reciprocal Cross Holdingunder AT-1 - -

of which: Reciprocal Cross Holdingunder Tier-II 50 50 C4of which: Subsidiaries / JointVentures / Associates 1,312 2,362 C5of which: Others (Commercial Papers,Mutual Funds etc.) 43,592 41,486 -

iii.

Loans and advances 1,422,122 1,422,122 -of which: Loans and advances toBanks 26,392 26,392 -of which: Loans and advances tocustomers 1,395,730 1,395,730 -iv. Fixed assets 35,523 35,410 -

v.

Other assets 93,245 90,367 -of which: Goodwill - -of which: Intangible Assets 509 502 C1of which: Deferred tax assets 28,966 28,968 C2vi. Goodwill on consolidation - - -vii. Debit balance in Profit & Loss account - - -

Total Assets 2,495,767 2,487,008

Step - 3Extract of Basel III common disclosure template (with added column) – Table DF-11Common Equity Tier 1 capital: instruments and reserves

Component ofregulatory capitalreported by bank

Source based on referencenumbers/letters of thebalance sheet under theregulatory scope ofconsolidation from step 21 Directly issued qualifying commonshare (and equivalent for non-jointstock companies) capital plus relatedstock surplus 112,850 A1 + A2

2 Retained earnings (135,740) A3

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 33 of 50

3 Accumulated other comprehensiveincome (and other reserves) 166,439 B1 + B2 + B3+ B4+B5 +B6+B74 Directly issued capital subject to phaseout from CET1 (only applicable to non-joint stock companies)5 Common share capital issued bysubsidiaries and held by third parties(amount allowed in group CET1)6 Common Equity Tier 1 capital before

regulatory adjustments 143,5497 Prudential valuation adjustments -8 Goodwill (net of related tax liability) -

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 34 of 50

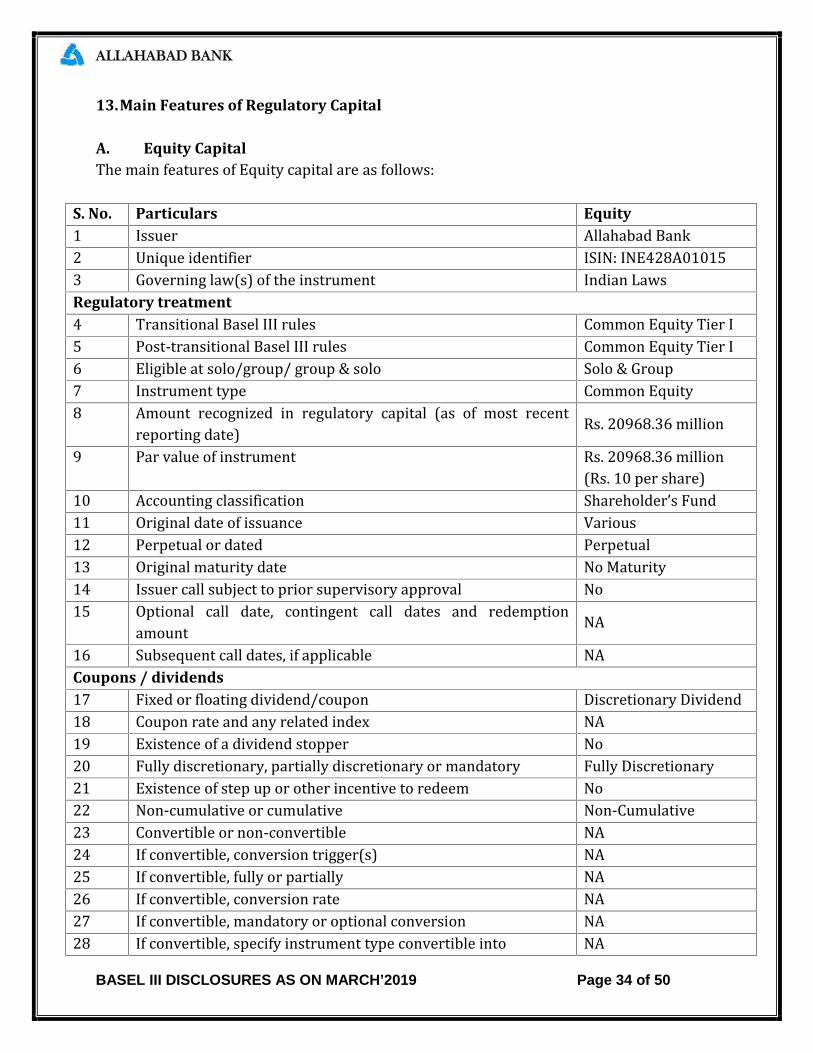

13.Main Features of Regulatory Capital

A. Equity CapitalThe main features of Equity capital are as follows:S. No. Particulars Equity1 Issuer Allahabad Bank2 Unique identifier ISIN: INE428A010153 Governing law(s) of the instrument Indian LawsRegulatory treatment4 Transitional Basel III rules Common Equity Tier I5 Post-transitional Basel III rules Common Equity Tier I6 Eligible at solo/group/ group & solo Solo & Group7 Instrument type Common Equity8 Amount recognized in regulatory capital (as of most recentreporting date) Rs. 20968.36 million9 Par value of instrument Rs. 20968.36 million(Rs. 10 per share)10 Accounting classification Shareholder’s Fund11 Original date of issuance Various12 Perpetual or dated Perpetual13 Original maturity date No Maturity14 Issuer call subject to prior supervisory approval No15 Optional call date, contingent call dates and redemptionamount NA16 Subsequent call dates, if applicable NACoupons / dividends17 Fixed or floating dividend/coupon Discretionary Dividend18 Coupon rate and any related index NA19 Existence of a dividend stopper No20 Fully discretionary, partially discretionary or mandatory Fully Discretionary21 Existence of step up or other incentive to redeem No22 Non-cumulative or cumulative Non-Cumulative23 Convertible or non-convertible NA24 If convertible, conversion trigger(s) NA25 If convertible, fully or partially NA26 If convertible, conversion rate NA27 If convertible, mandatory or optional conversion NA28 If convertible, specify instrument type convertible into NA

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 35 of 50

S. No. Particulars Equity29 If convertible, specify issuer of instrument it converts into NA30 Write-down feature No31 If write-down, write-down trigger(s) NA32 If write-down, full or partial NA33 If write-down, permanent or temporary NA34 If temporary write-down, description of write-up mechanism NA35 Position in subordination hierarchy in liquidation (specifyinstrument type immediately senior to instrument) NA36 Non-compliant transitioned features No37 If yes, specify non-compliant features NAB. Basel II Compliant Tier I capital instrumentsThe main features of Basel II Compliant Tier I capital instruments are as follows:

S. No. Particulars Perpetual Bond Series II1 Issuer Allahabad Bank2 Unique identifier INE428A091253 Governing law(s) of the instrument Indian LawsRegulatory treatment4 Transitional Basel III rules Additional Tier I5 Post-transitional Basel III rules Ineligible6 Eligible at solo/group/ group & solo Solo & Group7 Instrument type Perpetual8 Amount recognized in regulatorycapital Rs.600 million9 Par value of instrument Rs. 1,500 million(Rs. 1 million per Bond)10 Accounting classification Liability11 Original date of issuance 18th December, 200912 Perpetual or dated Perpetual13 Original maturity date No Maturity14 Issuer call subject to prior supervisoryapproval Yes15 Optional call date, contingent call datesand redemption amount Optional Call Date: 18th December2019 and thereafter on eachanniversary date Contingent call dates:NA Redemption at Par16 Subsequent call dates, if applicable On each anniversary date after 18thDecember 2019

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 36 of 50

S. No. Particulars Perpetual Bond Series IICoupons / dividends17 Fixed or floating dividend/coupon Fixed18 Coupon rate and any related index 9.08% p.a., payable annually from issuedate till first call option date and if theBank does not exercise the call option,50 bps over and above coupon rate of9.08% i.e. 9.58% p.a. after 18thDecember, 201919 Existence of a dividend stopper No20 Fully discretionary, partiallydiscretionary or mandatory Partially discretionary21 Existence of step up or other incentiveto redeem Yes22 Noncumulative or cumulative Non-cumulative23 Convertible or non-convertible Non-Convertible24 If convertible, conversion trigger(s) NA25 If convertible, fully or partially NA26 If convertible, conversion rate NA27 If convertible, mandatory or optionalconversion NA28 If convertible, specify instrument typeconvertible into NA29 If convertible, specify issuer ofinstrument it converts into NA30 Write-down feature No31 If write-down, write-down trigger(s) NA32 If write-down, full or partial NA33 If write-down, permanent ortemporary NA34 If temporary write-down, descriptionof write-up mechanism NA35 Position in subordination hierarchy inliquidation The claims of the Bondholders shall be(a) superior to the claims of investorsin equity shares and (b) subordinatedto the claims of all other creditors

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 37 of 50

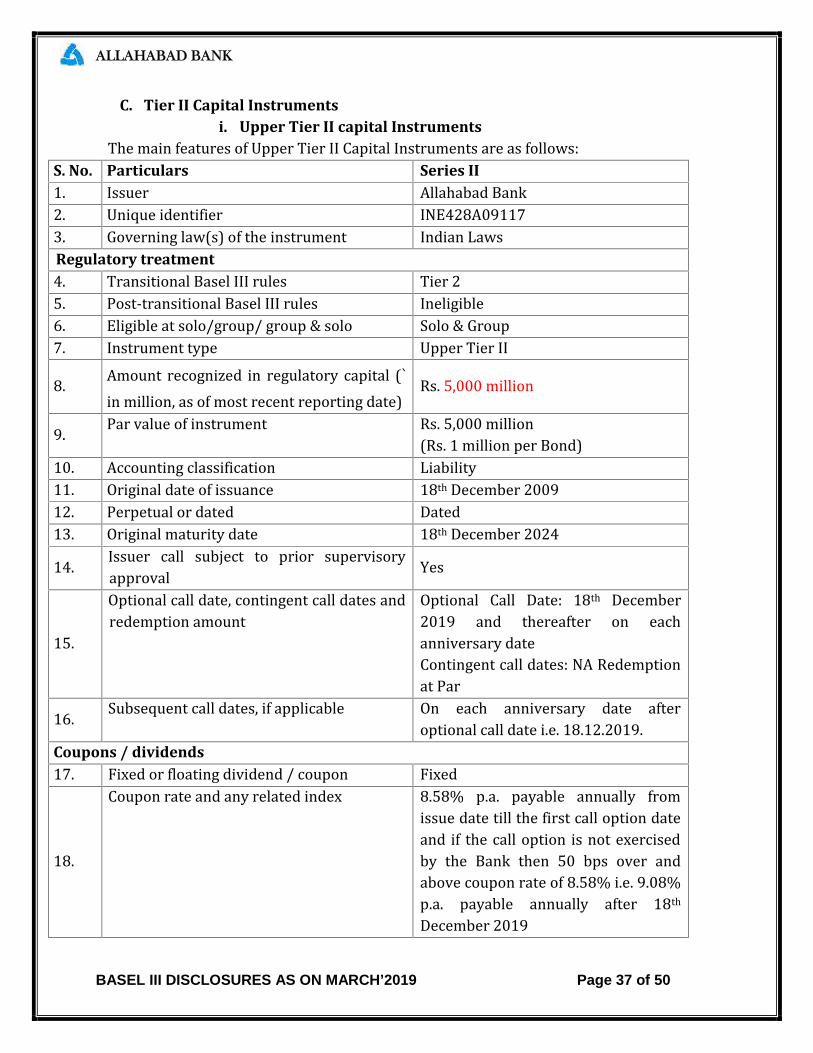

C. Tier II Capital Instrumentsi. Upper Tier II capital InstrumentsThe main features of Upper Tier II Capital Instruments are as follows:

S. No. Particulars Series II1. Issuer Allahabad Bank2. Unique identifier INE428A091173. Governing law(s) of the instrument Indian LawsRegulatory treatment4. Transitional Basel III rules Tier 25. Post-transitional Basel III rules Ineligible6. Eligible at solo/group/ group & solo Solo & Group7. Instrument type Upper Tier II8. Amount recognized in regulatory capital (`in million, as of most recent reporting date) Rs. 5,000 million9. Par value of instrument Rs. 5,000 million(Rs. 1 million per Bond)10. Accounting classification Liability11. Original date of issuance 18th December 200912. Perpetual or dated Dated13. Original maturity date 18th December 202414. Issuer call subject to prior supervisoryapproval Yes15. Optional call date, contingent call dates andredemption amount Optional Call Date: 18th December2019 and thereafter on eachanniversary dateContingent call dates: NA Redemptionat Par16. Subsequent call dates, if applicable On each anniversary date afteroptional call date i.e. 18.12.2019.Coupons / dividends17. Fixed or floating dividend / coupon Fixed18.

Coupon rate and any related index 8.58% p.a. payable annually fromissue date till the first call option dateand if the call option is not exercisedby the Bank then 50 bps over andabove coupon rate of 8.58% i.e. 9.08%p.a. payable annually after 18thDecember 2019

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 38 of 50

S. No. Particulars Series II19. Existence of a dividend stopper No20. Fully discretionary, partially discretionaryor mandatory Partially discretionary21. Existence of step up or other incentive toredeem Yes22. Noncumulative or cumulative Non-Cumulative23. Convertible or non-convertible Non-Convertible24. If convertible, conversion trigger(s) NA25. If convertible, fully or partially NA26. If convertible, conversion rate NA27. If convertible, mandatory or optionalconversion NA28. If convertible, specify instrument typeconvertible into NA29. If convertible, specify issuer of instrumentit converts into NA30. Write-down feature No31. If write-down, write-down trigger(s) NA32. If write-down, full or partial NA33. If write-down, permanent or temporary NA34. If temporary write-down, description ofwrite-up mechanism NA35.

Position in subordination hierarchy inliquidation (specify instrument typeimmediately senior to instrument) The claims of the investors in theseBonds shall be (a) superior to theclaims of investors in instrumentseligible for inclusion in Tier I capital;and (b) subordinate to the claims ofall other creditors.36. Non-compliant transitioned features Yes37. If yes, specify non-compliant features Step up; No Basel III Loss Absorbencyb. Subordinated Bonds, Lower Tier IIThe main features of Subordinate Bonds are as follows:

S. No. Particulars Series IX1. Issuer Allahabad Bank2. Unique identifier INE428A091093. Governing law(s) of the instrument Indian Laws

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 39 of 50

S. No. Particulars Series IXRegulatory treatment4. Transitional Basel III rules Tier 25. Post-transitional Basel III rules Ineligible6. Eligible at solo/group/ group & solo Solo & Group7. Instrument type Tier 2 Instruments8. Amount recognized in regulatory capital(Rs. in million, as of most recent reportingdate) -9. Par value of instrument Rs. 4,500 million(Rs. 1 million per Bond)10. Accounting classification Liability11. Original date of issuance 4th August 200912. Perpetual or dated Dated13. Original maturity date 4th August 201914. Issuer call subject to prior supervisoryapproval No15. Optional call date, contingent call datesand redemption amount No16. Subsequent call dates, if applicable NACoupons / dividends17. Fixed or floating dividend / coupon Fixed18. Coupon rate and any related index 8.45% p.a. payable annually19. Existence of a dividend stopper No20. Fully discretionary, partially discretionaryor mandatory Mandatory21. Existence of step up or other incentive toredeem No22. Non-cumulative or cumulative Non-Cumulative23. Convertible or non-convertible Non-Convertible24. If convertible, conversion trigger(s) NA25. If convertible, fully or partially NA26. If convertible, conversion rate NA27. If convertible, mandatory or optionalconversion NA28. If convertible, specify instrument typeconvertible into NA29. If convertible, specify issuer of instrumentit converts into NA

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 40 of 50

S. No. Particulars Series IX30. Write-down feature No31. If write-down, write-down trigger(s) NA32. If write-down, full or partial NA33. If write-down, permanent or temporary NA34. If temporary write-down, description ofwrite-up mechanism NA35.

Position in subordination hierarchy inliquidation (specify instrument typeimmediately senior to instrument) The claims of the investors in theseBonds shall be (a) superior to theclaims of investors in instrumentseligible for inclusion in Tier I capital;and (b) subordinate to the claims ofall other creditors.36. Non-compliant transitioned features Yes37. If yes, specify non-compliant features No Basel III Loss Absorbency

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 41 of 50

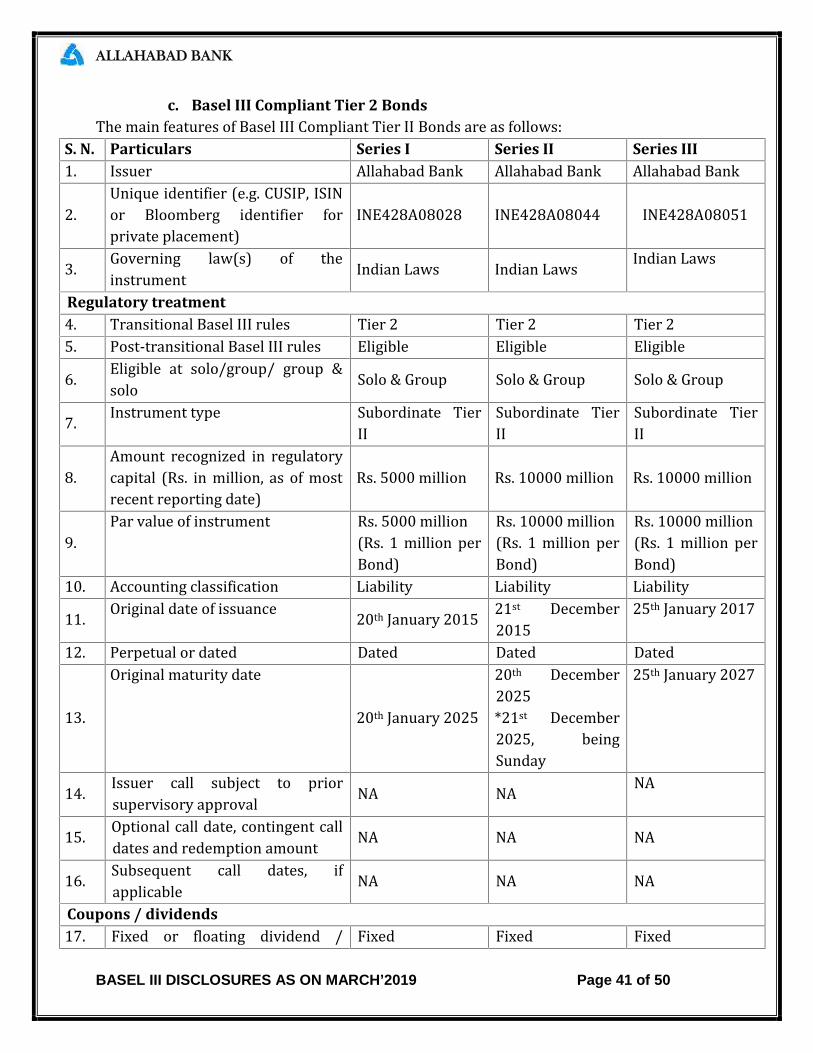

c. Basel III Compliant Tier 2 BondsThe main features of Basel III Compliant Tier II Bonds are as follows:S. N. Particulars Series I Series II Series III1. Issuer Allahabad Bank Allahabad Bank Allahabad Bank2. Unique identifier (e.g. CUSIP, ISINor Bloomberg identifier forprivate placement) INE428A08028 INE428A08044 INE428A080513. Governing law(s) of theinstrument Indian Laws Indian Laws Indian LawsRegulatory treatment4. Transitional Basel III rules Tier 2 Tier 2 Tier 25. Post-transitional Basel III rules Eligible Eligible Eligible6. Eligible at solo/group/ group &solo Solo & Group Solo & Group Solo & Group7. Instrument type Subordinate TierII Subordinate TierII Subordinate TierII8. Amount recognized in regulatorycapital (Rs. in million, as of mostrecent reporting date) Rs. 5000 million Rs. 10000 million Rs. 10000 million9. Par value of instrument Rs. 5000 million(Rs. 1 million perBond) Rs. 10000 million(Rs. 1 million perBond) Rs. 10000 million(Rs. 1 million perBond)10. Accounting classification Liability Liability Liability11. Original date of issuance 20th January 2015 21st December2015 25th January 201712. Perpetual or dated Dated Dated Dated13. Original maturity date 20th January 2025 20th December2025*21st December2025, beingSunday

25th January 2027

14. Issuer call subject to priorsupervisory approval NA NA NA15. Optional call date, contingent calldates and redemption amount NA NA NA16. Subsequent call dates, ifapplicable NA NA NACoupons / dividends17. Fixed or floating dividend / Fixed Fixed Fixed

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 42 of 50

S. N. Particulars Series I Series II Series IIIcoupon18. Coupon rate and any relatedindex 8.78% p.a.payable annuallytill maturity ofBonds

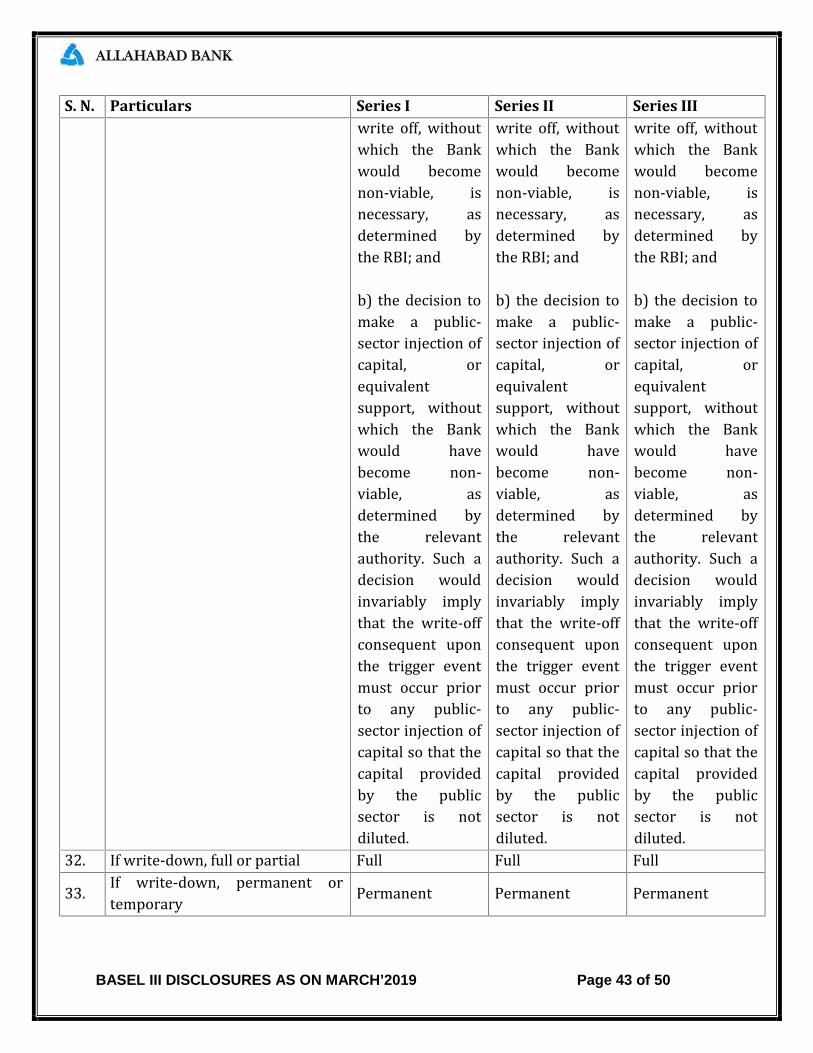

8.64% p.a.payable annuallytill maturity ofBonds8.15% p.a.payable annuallytill maturity ofBonds19. Existence of a dividend stopper No No No20. Fully discretionary, partiallydiscretionary or mandatory Partiallydiscretionary Partiallydiscretionary Partiallydiscretionary21. Existence of step up or otherincentive to redeem NO NO NO22. Noncumulative or cumulative Non-Cumulative Non-Cumulative Non-Cumulative23. Convertible or non-convertible Non-Convertible Non-Convertible Non-Convertible24. If convertible, conversiontrigger(s) NA NA NA25. If convertible, fully or partially NA NA NA26. If convertible, conversion rate NA NA NA27. If convertible, mandatory oroptional conversion NA NA NA28. If convertible, specify instrumenttype convertible into NA NA NA29. If convertible, specify issuer ofinstrument it converts into NA NA NA30. Write-down feature YES YES YES

31.

If write-down, write-downtrigger(s) The Bonds may,at the option ofthe RBI, bepermanentlywritten off uponoccurrence of thetrigger eventcalled the “Pointof Non-ViabilityTrigger”. ThePONV Triggerevent shall be theearlier of:a) a decision thatthe permanent

The Bonds may,at the option ofthe RBI, bepermanentlywritten off uponoccurrence of thetrigger eventcalled the “Pointof Non-ViabilityTrigger”. ThePONV Triggerevent shall be theearlier of:a) a decision thatthe permanent

The Bonds may,at the option ofthe RBI, bepermanentlywritten off uponoccurrence of thetrigger eventcalled the “Pointof Non-ViabilityTrigger”. ThePONV Triggerevent shall be theearlier of:a) a decision thatthe permanent

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 43 of 50

S. N. Particulars Series I Series II Series IIIwrite off, withoutwhich the Bankwould becomenon-viable, isnecessary, asdetermined bythe RBI; andb) the decision tomake a public-sector injection ofcapital, orequivalentsupport, withoutwhich the Bankwould havebecome non-viable, asdetermined bythe relevantauthority. Such adecision wouldinvariably implythat the write-offconsequent uponthe trigger eventmust occur priorto any public-sector injection ofcapital so that thecapital providedby the publicsector is notdiluted.

write off, withoutwhich the Bankwould becomenon-viable, isnecessary, asdetermined bythe RBI; andb) the decision tomake a public-sector injection ofcapital, orequivalentsupport, withoutwhich the Bankwould havebecome non-viable, asdetermined bythe relevantauthority. Such adecision wouldinvariably implythat the write-offconsequent uponthe trigger eventmust occur priorto any public-sector injection ofcapital so that thecapital providedby the publicsector is notdiluted.

write off, withoutwhich the Bankwould becomenon-viable, isnecessary, asdetermined bythe RBI; andb) the decision tomake a public-sector injection ofcapital, orequivalentsupport, withoutwhich the Bankwould havebecome non-viable, asdetermined bythe relevantauthority. Such adecision wouldinvariably implythat the write-offconsequent uponthe trigger eventmust occur priorto any public-sector injection ofcapital so that thecapital providedby the publicsector is notdiluted.32. If write-down, full or partial Full Full Full33. If write-down, permanent ortemporary Permanent Permanent Permanent

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 44 of 50

S. N. Particulars Series I Series II Series III34. If temporary write-down,description of write-upmechanism NA NA NA

35.

Position in subordinationhierarchy in liquidation (specifyinstrument type immediatelysenior to instrument)The claims of theBondholders shallbe (a) senior tothe claims ofinvestors ininstrumentseligible forinclusion in Tier 1capital of theBank; (b)subordinate tothe claims of alldepositors andgeneral creditorsof the Bank; and(c) neithersecured norcovered by aguarantee of theBank or relatedentity or otherarrangement thatlegally oreconomicallyenhances theseniority of theclaim vis-à-viscreditors of theBank. TheBondholders shallhave no rights toaccelerate therepayment offuture scheduledpayments

The claims of theBondholders shallbe (a) senior tothe claims ofinvestors ininstrumentseligible forinclusion in Tier 1capital of theBank; (b)subordinate tothe claims of alldepositors andgeneral creditorsof the Bank; and(c) neithersecured norcovered by aguarantee of theBank or relatedentity or otherarrangement thatlegally oreconomicallyenhances theseniority of theclaim vis-à-viscreditors of theBank. TheBondholders shallhave no rights toaccelerate therepayment offuture scheduledpayments

The claims of theBondholders shallbe (a) senior tothe claims ofinvestors ininstrumentseligible forinclusion in Tier 1capital of theBank; (b)subordinate tothe claims of alldepositors andgeneral creditorsof the Bank; and(c) neithersecured norcovered by aguarantee of theBank or relatedentity or otherarrangement thatlegally oreconomicallyenhances theseniority of theclaim vis-à-viscreditors of theBank. TheBondholders shallhave no rights toaccelerate therepayment offuture scheduledpayments

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 45 of 50

S. N. Particulars Series I Series II Series III(coupon orprincipal) exceptin bankruptcyand liquidation.(coupon orprincipal) exceptin bankruptcyand liquidation.

(coupon orprincipal) exceptin bankruptcyand liquidation.36. Non-compliant transitionedfeatures NO NO NO37. If yes, specify non-compliantfeatures NA NA NA

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 46 of 50

14.FULL TERMS AND CONDITIONS OF REGULATORY CAPITAL INSTRUMENTSDisclosures pertaining to the terms and conditions of regulatory capital instruments havebeen disclosed separately on the Bank's website under the Regulatory Disclosures Section.The link to this section is:https://www.allahabadbank.in/english/Capital_Instruments.aspx

15.DISCLOSURE REQUIREMENTS FOR REMUNERATIONNot Applicable for Public Sector Bank16.EQUITIES – DISCLOSURE FOR BANKING BOOK POSITIONSIn accordance with the RBI guidelines on investment classification and valuation,Investments are classified on the date of purchase into Held for Trading (HFT), Availablefor Sale (AFS) and Held to Maturity (HTM) categories. Investments which the Bank intendsto hold till maturity are classified as HTM securities. In accordance with the RBI guidelines,equity investments held under the HTM category are classified as banking book for capitaladequacy purpose.Investments in equity of subsidiaries and joint ventures are required to be classified underHTM category in accordance with the RBI guidelines. These are held with a strategicobjective to maintain relationships for business purposes.Investments classified under HTM category are carried at their acquisition cost and notmarked to market. Any diminution, other than temporary, in the value of equityinvestments is provided for. Any loss on sale of investments in HTM category is recognizedin the Statement of Profit and Loss. Any gain from sale of investments under HTM categoryis recognized in the Statement of Profit and Loss and is appropriated, net of taxes andstatutory reserve, to “Capital Reserve” in accordance with the RBI Guidelines.

QUANTITATIVE DISCLOSURES

A. Value of Investments (Rs. in millions)Investments Value as per Balance

Sheet Fair ValuePublicly Quoted Share Values(if materially different from

fair value)Unquoted 1,644 2,883 NAQuoted NIL NIL NA

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 47 of 50

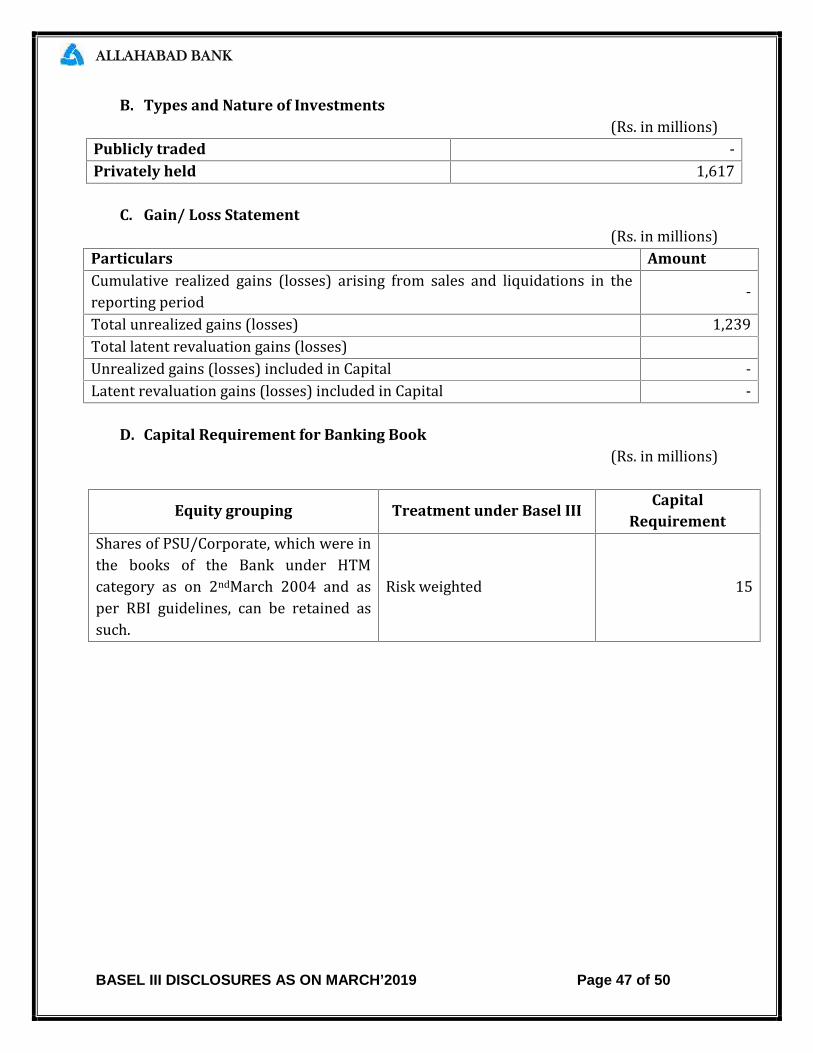

B. Types and Nature of Investments (Rs. in millions)Publicly traded -Privately held 1,617

C. Gain/ Loss Statement (Rs. in millions)Particulars AmountCumulative realized gains (losses) arising from sales and liquidations in thereporting period -Total unrealized gains (losses) 1,239Total latent revaluation gains (losses)Unrealized gains (losses) included in Capital -Latent revaluation gains (losses) included in Capital -

D. Capital Requirement for Banking Book (Rs. in millions)Equity grouping Treatment under Basel III Capital

RequirementShares of PSU/Corporate, which were inthe books of the Bank under HTMcategory as on 2ndMarch 2004 and asper RBI guidelines, can be retained assuch. Risk weighted 15

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 48 of 50

17.SUMMARY COMPARISON OF ACCOUNTING ASSETS VS. LEVERAGE RATIOEXPOSURE MEASURE (Rs. in millions)

ItemAs on Mar 31,

20191 Total consolidated assets as per published financial statements 2,487,0082 Adjustment for investments in banking, financial, insurance or commercialentities that are consolidated for accounting purposes but outside the scopeof regulatory consolidation (1,050)3 Adjustment for fiduciary assets recognized on the balance sheet pursuant tothe operative accounting framework but excluded from the leverage ratioexposure measure (502)4 Adjustments for derivative financial instruments 54,9715 Adjustment for securities financing transactions (i.e. repos and similarsecured lending) 3026 Adjustment for off-balance sheet items (i.e. conversion to credit equivalentamounts of off- balance sheet exposures) 132,7337 Other adjustments (16,888)8 Leverage ratio exposure 2,656,573

Reconciliation with public financial statements (Rs. in millions)Particulars As on Mar 31, 20191 Total assets as per financial statement 2,487,0082 Adjustments for securities financing transactions (12,000)3 Other Adjustments (18,440)

4 On-Balance Sheet exposure under Leverage Ratio 2,456,568

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 49 of 50

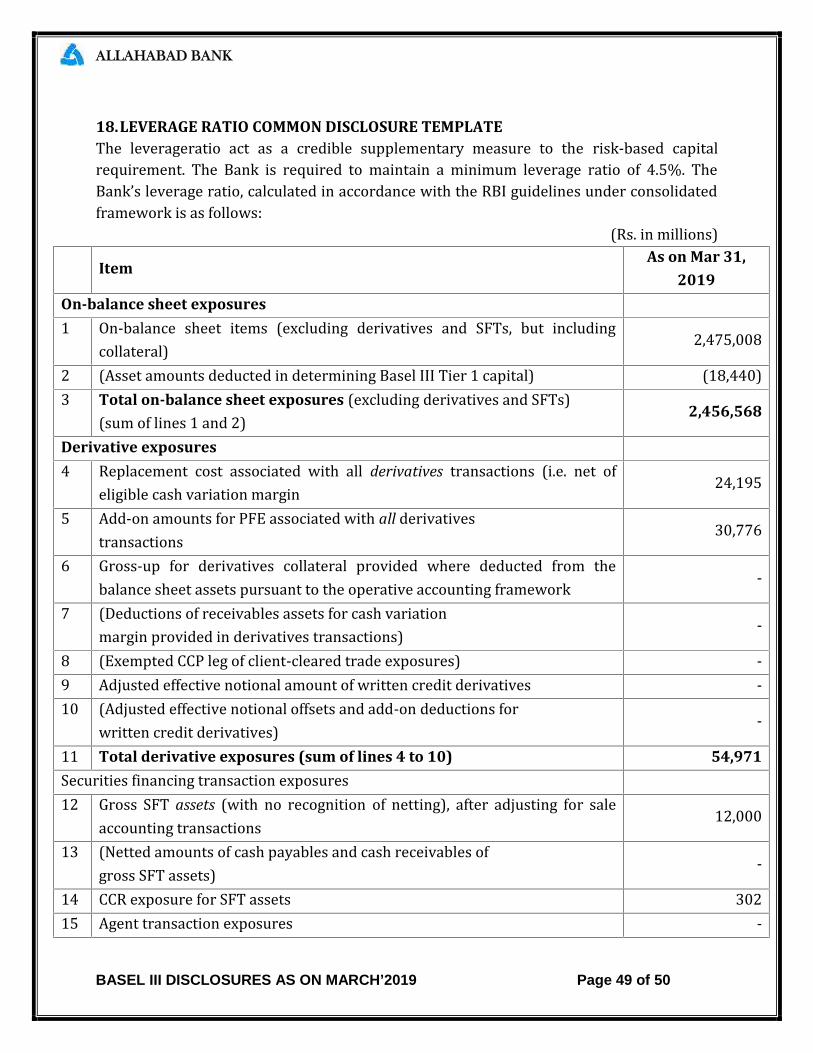

18.LEVERAGE RATIO COMMON DISCLOSURE TEMPLATEThe leverageratio act as a credible supplementary measure to the risk-based capitalrequirement. The Bank is required to maintain a minimum leverage ratio of 4.5%. TheBank’s leverage ratio, calculated in accordance with the RBI guidelines under consolidatedframework is as follows: (Rs. in millions)Item

As on Mar 31,2019

On-balance sheet exposures1 On-balance sheet items (excluding derivatives and SFTs, but includingcollateral) 2,475,0082 (Asset amounts deducted in determining Basel III Tier 1 capital) (18,440)3 Total on-balance sheet exposures (excluding derivatives and SFTs)(sum of lines 1 and 2) 2,456,568

Derivative exposures4 Replacement cost associated with all derivatives transactions (i.e. net ofeligible cash variation margin 24,1955 Add-on amounts for PFE associated with all derivativestransactions 30,7766 Gross-up for derivatives collateral provided where deducted from thebalance sheet assets pursuant to the operative accounting framework -7 (Deductions of receivables assets for cash variationmargin provided in derivatives transactions) -8 (Exempted CCP leg of client-cleared trade exposures) -9 Adjusted effective notional amount of written credit derivatives -10 (Adjusted effective notional offsets and add-on deductions forwritten credit derivatives) -11 Total derivative exposures (sum of lines 4 to 10) 54,971Securities financing transaction exposures12 Gross SFT assets (with no recognition of netting), after adjusting for saleaccounting transactions 12,00013 (Netted amounts of cash payables and cash receivables ofgross SFT assets) -14 CCR exposure for SFT assets 30215 Agent transaction exposures -

ALLAHABAD BANK

BASEL III DISCLOSURES AS ON MARCH’2019 Page 50 of 50

ItemAs on Mar 31,

201916 Total securities financing transaction exposures (sum of lines 12 to15)

12,302

Other off-balance sheet exposures17 Off-balance sheet exposure at gross notional amount 582,54218 (Adjustments for conversion to credit equivalent amounts) (449,809)19 Off-balance sheet items (sum of lines 17 and 18 132,733Capital and total exposures20 Tier 1 capital 125,96021 Total exposures (sum of lines 3, 11, 16 and 19) 2,656,573Leverage ratio22 Basel III leverage ratio 4.74%

LEVERAGE RATIO DISCLOSURE (Rs. in millions)Particulars Mar 31, 2019 Dec 31, 2018 Sep 30, 2018 Jun 30, 2018

Tier 1 capital 125,960 92,745 67,519 65,623Exposure Measure 2,656,573 2,541,885 2,606,228 2,552,193Leverage Ratio 4.74% 3.65% 2.59% 2.57%