Embed Size (px)

Citation preview

EVENT SUMMARY

ConneCtedhealthSummit.com

eventSpecial event

Hosted By

lunch

Break

registration

Charter

association

STORY OF

By Paul Sonnier

thanK YoU SponSorS

ConneCtedhealthSummit.com

Supporters

ConneCtedhealthSummit.com

John Mattison, Chief Medical Information Officer,Kaiser Permanente

Ronald J. Ozminkowski, Ph.D., SVP and Chief Scientific Officer, Consumer Solutions Group, Optum

Chris Young, Vice President, New Virtual Market Development and Incubations,Ascension Health

Adam Pellegrini, Vice President, Digital Health,Walgreens

James R. Mault, M.D., F.A.C.S., Vice President and Chief Medical Officer, Qualcomm Life

KeYnoteS advISorY BOARDAARP

Keith Epstein, Senior Strategic Advisor

ADTAmy Kabcenell, Sr. Director, Marketing, ADT Health

AlereKent Dicks, CEO of Alere Connect, a division of Alere

American Heart Association Patrick Wayte, Senior Vice President, Patient and Healthcare Innovations

Ascension HealthChris Young, Vice President, New Virtual Market Development and Incubations

Care InnovationsKarissa Price, Chief Marketing Officer

Humana WellnessChris Nicholson, VP and COO

Intermountain HealthcareCraig Kartchner, Senior Director of Marketing

Kaiser PermanenteJohn Mattison, Chief Medical Information Officer

Lowe's Companies, Inc.Kristen T. Bowring, Director of Business Develop-ment, Smart Home Business Unit—New Business

Meridian HealthSandra Elliot, Director, Consumer Technology and Service Development

Northwestern UniversityDavid Curtis Mohr, Ph.D., Professor

Omron Healthcare, Inc.Randy Kellogg, Chief Operating Officer

Qualcomm Life/Continuaa AllianceClint McClellan, Senior Director of Business Development at Qualcomm Life and Chairman of the Continuaa Health Alliance

United Health Bud Flagstad, Senior Vice President, Software Innovation and Technical Product Services, Optum

Walgreens Adam Pellegrini, Vice President, Digital Health

Wellness & Prevention, Inc., a Johnson & Johnson company

John Vander Meulen, General Manager

Chris Nicholson, VP and COO,Humana Wellness

the Shift to Consumer-Centric: Perspectives from Health Systems

Applying Connected Health to the Wellness market: the "triple threat" Driving Growth

Building a Consumer-Centric Connected Health Ecosystem

Consumer Engagement As A Loyalty Strategy

Enhancing the Consumer’s Propensity to Succeed in a Digital Health management World

tHURS—5:00 pm

fRiday—9:45 am

fRiday—11:45 am

tHURS—11:45 am

tHURS—9:45 Am

ConnectedHealthSummit.com 4

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

4

Event Summary ‐ Table of Contents

THURSDAY, SEPTEMBER 4 .................................................................................................................... 5

The Connected Consumer: Current State of the Digital Health Market ...................................................... 5

Healthy Living, Connected Devices, and Wearables .................................................................................... 6

Keynote—The Shift to Consumer‐Centric: Perspectives from Health Systems ........................................... 9

Population Health Management: Tracking Technology’s Impact .............................................................. 10

Keynote—Applying Connected Health to the Wellness Market: The “Triple Threat” Driving Growth ..... 13

Path to Quality of Care: Leveraging Technology for ACOs ......................................................................... 13

Independent Living: Engaging the Elderly and Caregivers ......................................................................... 15

The Role of Connected Devices in Digital Health ....................................................................................... 18

Keynote—Building a Consumer‐Centric Connected Health Ecosystem .................................................... 20

FRIDAY, SEPTEMBER 5 ........................................................................................................................ 22

Connected Devices and Digital Health Services: Consumer Perspectives .................................................. 22

Moving the Digital Health Market Forward: Consumers Take Charge ...................................................... 23

Keynote—Consumer Engagement as a Loyalty Strategy ........................................................................... 26

Incentivizing Behavioral Changes: The Impact of Apps and Big Data ........................................................ 26

Keynote—Enhancing the Consumer’s Propensity to Succeed in a Digital Health Management World .... 29

Healthcare Purchasing Decisions: The Power of the Informed Consumer ................................................ 30

Effective Strategies to Drive Healthy Living through all Life Stages ........................................................... 32

Investment Trends in Consumer Health ..................................................................................................... 33

ConnectedHealthSummit.com 5

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

5

THURSDAY, SEPTEMBER 4

The Connected Consumer: Current State of the Digital Health Market

Parks Associates analysts discussed the business and consumer aspects of the digital health market, with

special insight into the consumer/patient perspective. This presentation set the stage for the conference by

highlighting areas of connected health that have gained traction while also calling out the many barriers to

industry growth. Parks Associates’ survey data show consumers are starting to use digital tools in healthcare—

26% of U.S. broadband households use a website for appointments, lab results, and prescriptions, and 25% use

health apps. This presentation revealed current consumer activities and their demands, interests, and

concerns related to connected health products and services.

SPEAKERS

Stuart Sikes, President, Parks Associates

Harry Wang, Director, Health & Mobile Product Research, Parks Associates

KEY TAKEAWAYS

• The big picture of the digital health industry:

− The Affordable Care Act has brought meaningful changes and reform catalysts to the healthcare

market.

− Health insurers have embraced changes. United Healthcare accelerated its market entry into the

health insurance exchange market, while Aetna envisions retail insurance buyers will be one‐third of

customers in 6‐7 years and its care delivery model will be significantly more consumer‐centric.

− Healthcare providers are building scale through mergers and acquisitions and embracing new care

models; one of the key new care models is population health management.

− Technology industry had a marquee year for health innovations in 2013, and 2014 is shaping up to be

more exciting. Healthcare for consumers 50 and over represents a $30 billion opportunity over five

years, according to a joint study from AARP and Parks Associates.

− The healthcare industry has a long way to go to engage consumers. The industry must understand

consumers’ motivations, pain points, triggers for behavioral changes, and propensity to adopt certain

products and services. For the healthcare industry, the success of their quality‐of‐care, economic, and

business models will all rely more and more on how effectively they can engage consumers and drive

lasting behavioral changes.

ConnectedHealthSummit.com 6

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

6

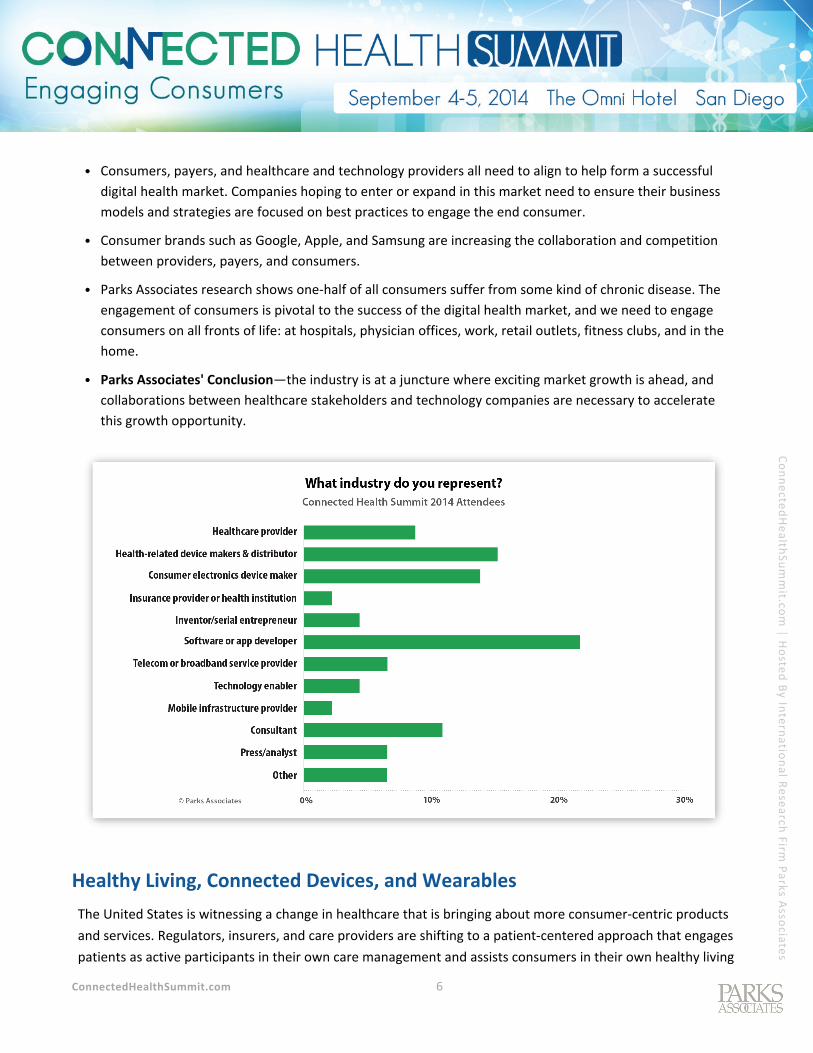

• Consumers, payers, and healthcare and technology providers all need to align to help form a successful

digital health market. Companies hoping to enter or expand in this market need to ensure their business

models and strategies are focused on best practices to engage the end consumer.

• Consumer brands such as Google, Apple, and Samsung are increasing the collaboration and competition

between providers, payers, and consumers.

• Parks Associates research shows one‐half of all consumers suffer from some kind of chronic disease. The

engagement of consumers is pivotal to the success of the digital health market, and we need to engage

consumers on all fronts of life: at hospitals, physician offices, work, retail outlets, fitness clubs, and in the

home.

• Parks Associates' Conclusion—the industry is at a juncture where exciting market growth is ahead, and

collaborations between healthcare stakeholders and technology companies are necessary to accelerate

this growth opportunity.

Healthy Living, Connected Devices, and Wearables

The United States is witnessing a change in healthcare that is bringing about more consumer‐centric products

and services. Regulators, insurers, and care providers are shifting to a patient‐centered approach that engages

patients as active participants in their own care management and assists consumers in their own healthy living

ConnectedHealthSummit.com 7

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

7

pursuits. Concurrently, design breakthroughs, technology advances, and mass adoption of mobile consumer

devices have made consumer‐centric care possible in ways previously impossible.

According to Parks Associates’ estimates, device manufacturers sold more than 40 million personal health and

wellness products in 2013, a figure that will rise to more than 70 million by 2018. As of Q2 2014, 27% of

consumers in U.S. broadband households own and use at least one connected health device, and 13% are very

likely to purchase a device in the next 12 months.

Software and services that come with these connected products will bring additional revenue opportunities to

device makers and healthcare providers. Cost savings, in the forms of reduced hospital admissions, early

detection of severe conditions, and lower‐cost but equally effective care options, will benefit public/private

insurers as well as businesses that insure their employees. These social and economic benefits all hinge on

successfully motivating consumers to modify their behavior to live and stay healthier.

Motivating consumers starts with putting the right information in consumers’ hands and awakening their inner

health consciousness for better living. It also requires proactively engaging consumers and addressing their

practical needs with support and advice as they move through different life stages and face different types of

healthy living challenges. Connected devices are part of the “holy grail” of consumer engagement, with

wearables promising to make the device experience even more personal and less intrusive. But connected

devices alone are not enough; healthcare providers must proactively engage their patients and health insurers

must provide compelling financial incentives to encourage better self‐care among consumers.

ConnectedHealthSummit.com 8

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

8

Parks Associates believes the U.S. healthcare industry is at a critical juncture for change, and effective

collaboration between the technology industry and healthcare constituents is crucial to the execution of

consumer engagement efforts and, ultimately, successfully changing consumer behaviors.

This panel examined innovations in connected devices and new wearable technologies and their role in

enabling healthy living. Speakers also addressed the integration of healthcare applications and services with

these devices and the role of health insurers and care providers in driving consumer adoption.

SPEAKERS

Muhammad Adburrahman, Ph.D., CEO and Co‐Founder, Playtabase

Kris Bowring, Director of Business Development, Smart Home Business Unit ‐ New Business, Lowe's

Companies, Inc.

Keith Epstein, Senior Strategic Advisor, AARP

Paul Jansen, Executive Vice President, Marketing, Masimo

Patrick Wayte, Senior Vice President, Patient and Healthcare Innovations, American Heart Association

Moderator: Harry Wang, Director, Health & Mobile Product Research, Parks Associates

KEY TAKEAWAYS

• AARP views the healthy living market as part of the opportunities in the “Land of Longevity.” As AARP’s

research indicates, investment in new opportunities for health‐related innovations would have a huge

financial and social return. Innovations in products, services, and business models could benefit roughly

106 million people in ways that have been unaddressed by the broader health‐related marketplace.

• Large parts of our population are not being reached at all with information about living healthfully.

• There is a major disconnect between consumers’ understanding of health and their own health status.

Many confuse activity with an improved state of health.

• Consumers need direction on what they should monitor, why they should monitor themselves, if the

monitoring is working, and what to do with the data once they have it.

• The technologies that will work best over time are those that enable access, purchase, and delivery of

services/solutions based on data that is as close to real time as possible.

• Doctors would like to have more information on patients, but generally they are not paid or compensated

to monitor, review, and interpret data from these "outside sources." Doctors also tend to instinctively

discount self‐reported and similar “out‐of‐office datasets” in favor of the more limited data they see from

visits or events.

• Technology, healthcare, and consumer‐facing brands need to make technology simple, easy, and intuitive

to use and provide consumers with a clear, consistent message about the technology’s value.

ConnectedHealthSummit.com 9

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

9

• As an example, Patrick Wayte mentioned that AHA has a Heartscore calculated based on an Ideal CV

Health Model that includes nutrition, physical activity, and BMI as part of seven components. These

components are a mix of health behaviors and health factors that form the basis for rating and ranking an

individual into one of three categories (poor, intermediate, and ideal health).

• Having mechanisms to track one’s health and offering reward schemes, reminders, and prompts can

influence consumer behavior patterns.

• Providers and pharmacists, as trusted providers of services, have an important role in influencing and

engaging consumers to be healthier.

• Providers need to find incentives that motivate behavior change. Technology companies need to create

products that fit into providers’ workflows.

• The app world is currently exploding, and many consumers are inundated with apps.

• Providers are reluctant to prescribe apps to patients. There are currently no regulations on apps; this

condition has helped with the early growth of the market. The caregiver group is one that gets ignored but

has a huge potential.

Keynote—The Shift to Consumer‐Centric: Perspectives from Health Systems

With healthcare spending power gradually shifting to consumers and pressure from government and insurers

to deliver accountable, quality care, U.S. health systems—hospitals and physicians—are facing challenges and

opportunities in multiple fronts: care practice modifications, patient engagement, market transparency, and

quality reporting. This keynote fireside chat shed light on professionals’ thinking and strategies in coping with

upcoming changes, and perspectives about the impact of technology and consumerism on their business

decisions.

SPEAKER

Chris Young, Vice President, New Virtual Market Development and Incubations, Ascension Health

KEY TAKEAWAYS

• Ascension Health is the nation's largest not‐for‐profit health organization. They are patient‐centric and

focused on acute care. Currently, the company is moving towards a consumer‐centric healthcare strategy.

For example, they are using retail (Walgreens, CVS, etc.) for healthcare services.

• Consumer expectation is rising for convenience of care. They expect that the medical records and portals

of all healthcare systems should work together (data needs to be more streamlined, e.g., dashboards for

MDs to get a quick glance of the patient).

ConnectedHealthSummit.com 10

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

10

• Who do healthcare providers trust with the consumer’s data? App developers or data aggregators/

analysts?

• Consumers expect to have some digital communication with their doctors, but not all consumers are ready

for video conferencing, nor are all healthcare systems.

• Consumers really only care about certain aspects of their own healthcare (e.g., some don’t care about

electric health records, they only care about their cholesterol levels).

• It’s difficult for consumers to decipher the information that they need. Currently there’s too much

information, and not all is relevant for their well‐being.

• Deploying new technology does not always solve workflow problems.

• We have to put the “easy button” into technologies if we want consumers to adopt them. Product design

needs to be elegant.

• The industry is moving from fee‐for‐service to fee‐for‐value models. The industry needs to make outcomes

meaningful for new program and device implementation.

• Health Information Exchanges are not set up for consumers to use; they have too much information. Over

time, we will move from data to analytics and actionable intelligence.

• Barriers to consumer adoption of digital technology solutions:

− Many consumers and healthcare systems are not ready for innovation

− Technologies have not fully integrated natural clinician workflows

− Designs need to be more elegant and touch patients’ emotions

− We have not educated patients enough on how to use apps, portals, etc.

− Some physicians are not willing to interface digitally (some will never adopt digital technologies)

• Technology companies should set up controlled pilots and collect data on meaningful outcomes, patient

feedback, and the benefits achieved.

• The trend of sensors in healthcare delivery is making Google, Apple, and Samsung big players in the

healthcare marketplace. Digital imaging will rapidly change in the coming years as a result.

• As Apple and Samsung move into healthcare, they are creating additional competition since they are so

engaged with consumers with their connected device products.

Population Health Management: Tracking Technology’s Impact

The population health management industry has evolved substantially since its inception. Today’s population

health management firms usually offer a broad range of service options, from resource‐intensive case

ConnectedHealthSummit.com 11

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

11

management services to preventive care solutions, from specialties in specific types of chronic conditions to

specialties in transitional care.

At the same time, private payers and integrated health systems have aggressively adopted the disease

management/population health management model. Major insurers such as Aetna, UnitedHealth, and

Humana all have their in‐house care management services serving their members and their business interests

(i.e., a new revenue source and a cost containment strategy).

Then came the Affordable Care Act in 2011, which authorized the establishment of accountable care

organizations (ACOs) as both a core care delivery model and a healthcare financing model. Care providers

working under an ACO will practice care in a coordinated way and get paid based on established quality

standards instead of the traditional fee‐for‐service arrangement. The ACO model and its multiple variants are

heavily influenced by the Patient‐Centered Medical Home (PCMH) care practice model—both emphasizing

coordinated care and addressing preventive care needs, while rewarding doctors for their performance, not

volume of visits.

Under a PCMH or an ACO model, private payers and health systems will benefit from their investment in in‐

house population health management capability. Health systems and large physician groups without prior

experience will find it imperative to work with qualified partners to build up their population health

management capabilities.

Concurrently, technology is rapidly changing how a care provider communicates to and engages with a

consumer/patient. Online and mobile communications tools enable a care provider to discuss patient

conditions and track preventive care measures with patients through phone calls, secure messaging, email, or

video chat. Home health monitoring technology enables remote diagnosis, data capture, and physician alerts.

Software and advanced analytics can analyze patient data and offer digital coaching services to address

consumers’ wellness needs. These technology solutions have become more intelligent and sophisticated to

support deployment of population health management at scale; at the same time, they have also become

more personalized to cater to individual’s unique needs and circumstances.

This panel examined the best practices of population health management in the digital age and how

technology can reshape consumers’ experience with population health management services.

SPEAKERS

Kent Dicks, CEO, Alere Connect

Maneesh Goyal, SVP Corporate Development, Welltok

Ronald J. Ozmnikowski, Ph.D., Senior Vice President and Chief Scientific Officer, Consumer Solutions Group,

Optum

Jacob Sattelmair, Co‐Founder and CEO, Wellframe

ConnectedHealthSummit.com 12

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

12

John Vander Meulen, General Manager, Wellness & Prevention, Inc., a Johnson & Johnson company

Moderator: Harry Wang, Director, Health & Mobile Product Research, Parks Associates

KEY TAKEAWAYS

• There are currently numerous solutions in the market for health and wellness population management. A

key challenge is to keep the patient engaged; even if the motivation is there, the patients will be

constrained by time and energy.

• Population health management companies need to look at aggregate populations—the macro level trends,

disease states, and chronic conditions—to understand health and wellness at a high level.

• At the same time, patient engagement tools and the right business model are critical to success. To

develop these solutions successfully, companies and players must understand individual patient needs and

behavioral motivations.

• Insurers are getting into the private exchange business, which will result in the population interacting with

the exchanges.

• Carefully crafted economic incentives, such as discounts on health premiums for enrolling in programs,

taking biometric tests, etc., can work in the short run to change behaviors.

• It is likely the healthcare industry will move away from widgets to personalized care; analysis of big data

from a consumer perspective will help make this happen.

• Wellness is about managing disease and healthcare appropriately. One solution doesn’t fit all. It’s about

personalized management—offerings must be hands‐off, seamless, easy, and work well. The right business

model is based on analysis of the right data, at the right time, at the right cost.

• Coaching is key to changing behaviors, but there is a lack of understanding of the underlying behavioral

issues that influence intrinsic motivation. Understanding and enhancing intrinsic motivation can be a key

to success.

ConnectedHealthSummit.com 13

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

13

Keynote—Applying Connected Health to the Wellness Market: The “Triple Threat” Driving Growth

The wellness marketplace alone is valued at over $40 billion. The convergence of mobile, healthcare, and SaaS

solutions are providing health and wellness companies with tremendous engagement capabilities and rapid

delivery of solutions that leverage context, personalization, and preferences to improve outcomes for

consumers. This keynote presentation explored this emerging and positive “triple threat” that can be

leveraged across the health and wellness marketplace to deploy connected health solutions, empower

consumers, and accelerate market growth.

SPEAKER

Chris Nicholson, CEO, mPulse Mobile (formerly VP and COO, Humana)

KEY TAKEAWAYS

• The wellness market is less regulated and more outcome‐focused than healthcare delivery. Industry

observers call it “the next billion‐dollar industry.”

• There are high levels of investment, heavy innovation, high growth rate, and agile players.

• A SaaS‐based infrastructure provides agility.

• Over $700M was invested in 1Q 2014, up 87% over the prior year.

• Triple threat: expansion of wellness market, SaaS‐based infrastructure, and solutions that leverage

mobility and mobile technologies

• The “last mile” (from product to patient) is the most expensive. How to get to the consumers is the current

challenge, especially now, when they already have app fatigue.

• SaaS‐based infrastructure: $12 billion to $40 billion in overall revenue

Path to Quality of Care: Leveraging Technology for ACOs

The Affordable Care Act, passed in 2011, authorized the establishment of accountable care organizations

(ACOs) as both a core care delivery model and a healthcare financing model. ACO, in a broad sense, describes

new care approaches in which care is coordinated among different care providers along the continuum of

care. All providers involved are accountable for a patient’s overall health and are paid based on care outcome

instead of volume of care.

ConnectedHealthSummit.com 14

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

14

Since 2011, the momentum to build ACOs or ACO‐like organizations has accelerated. The latest industry data

from the Leavitt Partners Center for Accountable Care Intelligence shows that there were more than 600

private and public ACOs at the beginning of 2014, and they were scattered in all 50 states—California led the

pack with almost 60 ACOs. These ACOs, according to the same source, managed a total of more than 18

million covered lives. When including Patient‐Centered Medical Home practices and other organizations

adopting a pay‐for‐performance arrangement, and factoring in the growth of ACOs in 2014, Parks Associates

expects that the total number of patients covered by these organizations will reach 40 million by the end of

2014.

There is no doubt now that the ACO is gradually becoming a significant care delivery model in the U.S.

healthcare system. Care providers, including hospitals, physician groups, and health systems, are leading ACO

formation, whereas community care providers, retail clinics, home health agencies, and care management

companies will play a supportive role in a typical ACO structure. This structure, involving multiple entities for a

coordinated care model, is great for patient care, but can pose an operational challenge to ACOs.

Specifically, the coordination of patient care and reporting of care outcomes across multiple care

facilities/provider types are complex tasks, and most care providers are less experienced with transformation

at this level/scale. The ACO model will fall apart if patient care experience suffers due to poorly integrated

health information and patchy workflows. For this reason, ACOs are working on the back end for operational

efficiency and on the front end for consumer/patient care experience enhancement.

Their technology partners will play an important role in ACOs’ transformational effort. Solutions that help

ACOs build a consistent patient engagement experience across various practice areas and consumer touch

points have emerged, and most also come with solutions to integrate patient data and streamline practice

workflow at the back end. Specific modules can address the needs of individual divisions in areas such as

discharge management, chronic health management, and patient portals for self‐care support. These

solutions, though still in the early stage of development and adoption, will help providers improve patient care

experience and engage patients more effectively.

This panel looked at the challenges and opportunities that ACOs face in delivering patient‐centered care and

the best practices to proactively engage patients.

SPEAKERS

Julie Cherry, Director of Clinical Services, Intel‐GE Care Innovations

Gaurov Dayal, President, Delivery, Finance and Integration, SSM Health Care

Tammy Richards, Operations Director, Patient and Clinical Engagement, Intermountain Healthcare

Eric Rock, CEO, Vivify Health

Moderator: Harry Wang, Director, Health & Mobile Product Research, Parks Associates

ConnectedHealthSummit.com 15

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

15

KEY TAKEAWAYS

• ACOs will manage 135 million people by 2018.

• ACOs will lower the cost of care and improve care coordination. We need a seamless integration of various

solutions.

• Disruptive technologies don’t usually come from incumbents.

• Challenges in initiating an ACO:

− Effective high‐tech solutions are generally high cost.

− Some physicians do not have an EMR system. They are still operating paper‐based systems.

− EMR vendors have created siloed systems for competitive reasons.

− Clinical analytics is in its infancy.

− Business models still need to shift more to the outpatient setting.

− There is a fear we will replicate the same problems we had without technology.

− Physicians are living in two worlds: fee‐for‐service and fee‐for‐value.

− We need to observe clinician and patient workflows to make improvements.

• There is not a single solution or technology that will work for everyone.

• Healthcare providers need to identify the impact of data collection for technology devices and services.

New solutions will change care delivery, workflow for clinicians, patient engagement strategies, and

physician recommendations.

• Elderly patients are the ones who are the targeted population, but they are not the most tech‐savvy

people, so whatever technologies are used need to be simple.

• The patients who need this the most are the sickest and least educated. There isn’t a technology or

solution that will be a fit for everyone. Upfront assessments and individual focus are key to finding the

right solutions in these circumstances.

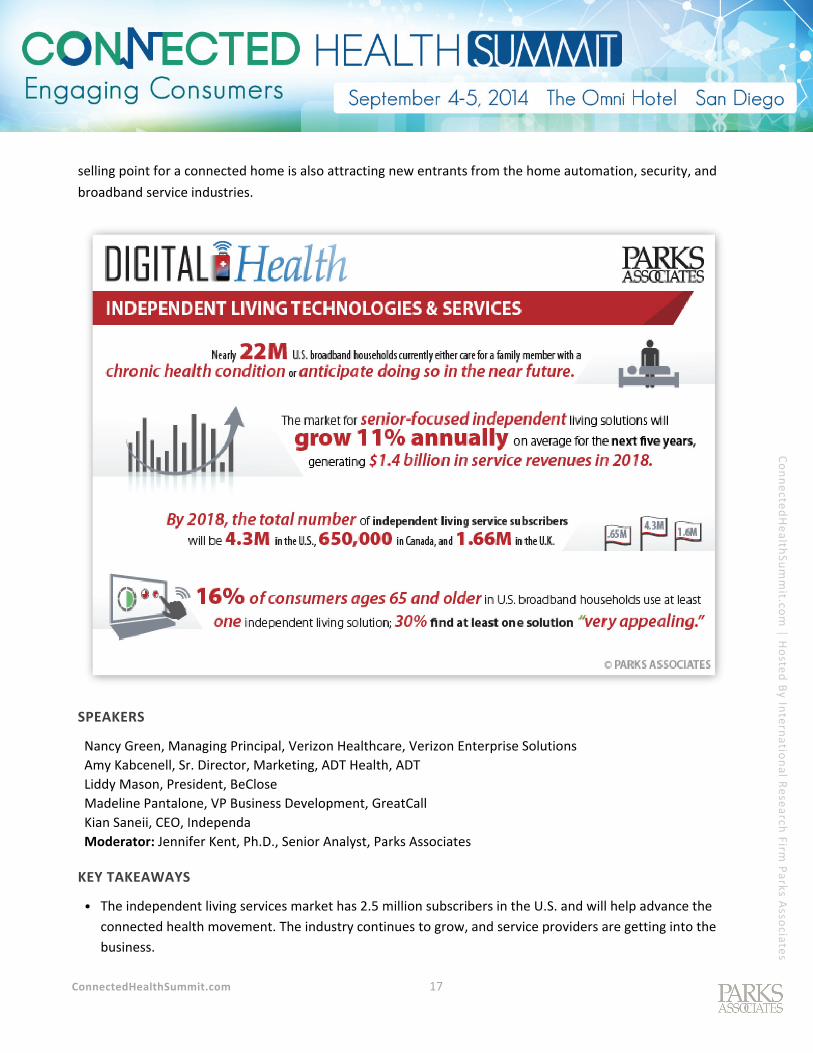

Independent Living: Engaging the Elderly and Caregivers

The U.S. is facing a retirement wave in the coming two decades. The baby boomer generation—76 million

strong—is beginning to hit the 65‐year‐old mark in large numbers. By 2025, the number of people between 65

and 85 will account for 16.6% of total population; compared with an estimated 12.5% in 2013, this represents

a net increase of almost 18 million people. Accompanying this graying of the population is a marked rise in

chronic health conditions that can be difficult and costly to manage and can threaten older consumers’ ability

to live safely in their own homes.

ConnectedHealthSummit.com 16

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

16

Because of the demographic trends and limited availability of long‐term care services, independent living at

home is the only financially viable and technologically feasible option for most people hitting retirement age.

In the U.S. and Canada, the private sector will be the driving force for the development of the independent

living market. Parks Associates categorizes the independent living service market into four major segments:

• Personal Emergency Response System (PERS)

• Medication Reminder and Monitoring

• Home Sensor‐based Activity Tracking

• Location Tracking and Assistance

Technologies and care services exist in all four segments that are designed to help older consumers live safely

and independently in their homes, maintain a healthy lifestyle, manage chronic health conditions, and improve

the overall quality of life. However, current approaches have yet to fully crack open this market. The

independent living service adoption rate of 2.5 million subscribers in the U.S. is tiny compared with the size of

the addressable market.

This panel discussed the biggest barriers to adoption of independent living solutions and highlighted the best

ways to address the needs of elderly consumers and their caregivers. One of the biggest market barriers to

independent living solution adoption, based on Parks Associates’ analysis, is consumers’ low regard for current

solutions. This perception results partly from high prices and partly from consumers’ latent awareness of their

own needs.

The traditional PERS market has received renewed attention not only for its service model but also for its

potential as a service platform for multiple integrated independent living solutions. Independent living as a

ConnectedHealthSummit.com 17

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

17

selling point for a connected home is also attracting new entrants from the home automation, security, and

broadband service industries.

SPEAKERS

Nancy Green, Managing Principal, Verizon Healthcare, Verizon Enterprise Solutions

Amy Kabcenell, Sr. Director, Marketing, ADT Health, ADT

Liddy Mason, President, BeClose

Madeline Pantalone, VP Business Development, GreatCall

Kian Saneii, CEO, Independa

Moderator: Jennifer Kent, Ph.D., Senior Analyst, Parks Associates

KEY TAKEAWAYS

• The independent living services market has 2.5 million subscribers in the U.S. and will help advance the

connected health movement. The industry continues to grow, and service providers are getting into the

business.

ConnectedHealthSummit.com 18

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

18

• The pathway to securing customers is through the younger generation, who are more likely to adopt smart

home services and technologies.

• The value proposition of these technologies should be about the freedom of “being engaged” and not

reliance on these solutions due to “being old.”

• Seniors still really trust and respect their clinicians, so these providers have a huge role to play in

introducing technologies, services, and apps that can help enable independent living.

• Much has to change with all the data that is available to caregivers nowadays. Adult children need to be

informed and have a meaningful conversation with their parents about independent living solutions.

• Robotics has arrived on the scene and will continue to develop new products for this market.

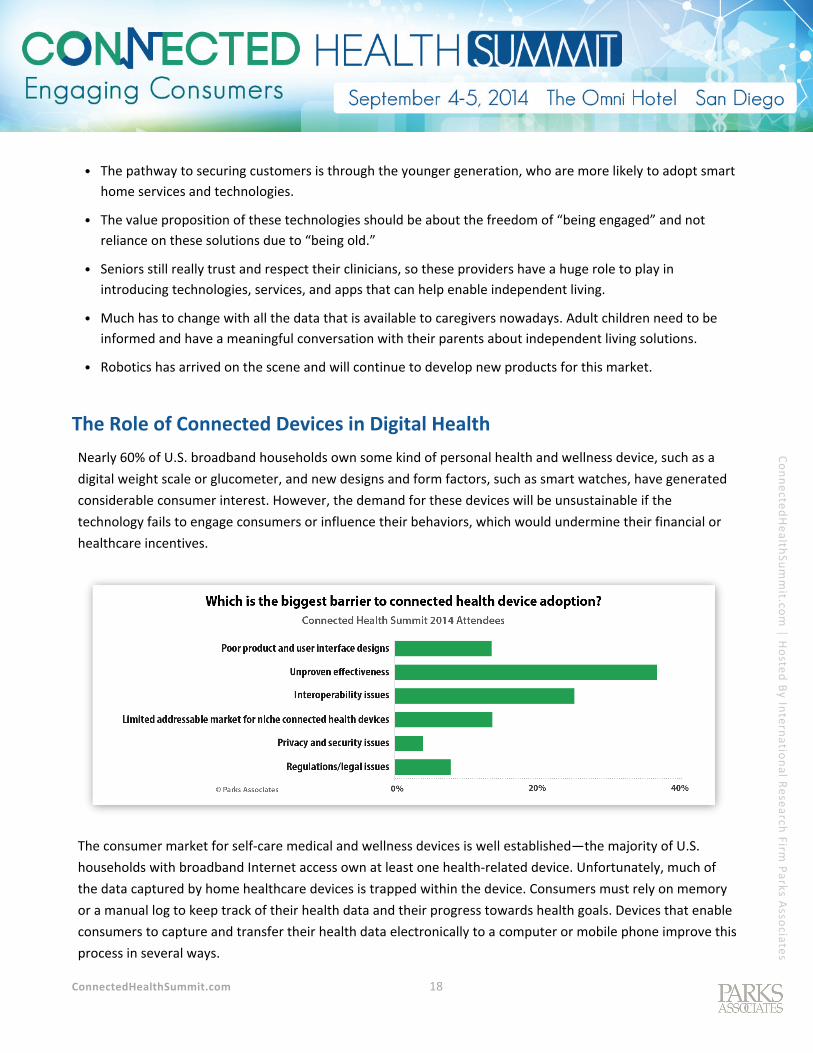

The Role of Connected Devices in Digital Health

Nearly 60% of U.S. broadband households own some kind of personal health and wellness device, such as a

digital weight scale or glucometer, and new designs and form factors, such as smart watches, have generated

considerable consumer interest. However, the demand for these devices will be unsustainable if the

technology fails to engage consumers or influence their behaviors, which would undermine their financial or

healthcare incentives.

The consumer market for self‐care medical and wellness devices is well established—the majority of U.S.

households with broadband Internet access own at least one health‐related device. Unfortunately, much of

the data captured by home healthcare devices is trapped within the device. Consumers must rely on memory

or a manual log to keep track of their health data and their progress towards health goals. Devices that enable

consumers to capture and transfer their health data electronically to a computer or mobile phone improve this

process in several ways.

ConnectedHealthSummit.com 19

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

19

Devices that collect and transfer data digitally have multiple benefits:

• Convenience for the consumer

• Improved data accuracy by removing consumers from the data collection and transfer process

• Extended device functionality; a multitude of consumer‐facing and care provider‐facing applications can be

built upon the collected data

• Potential for new revenue streams for device manufacturers on top of device sales/rental revenues

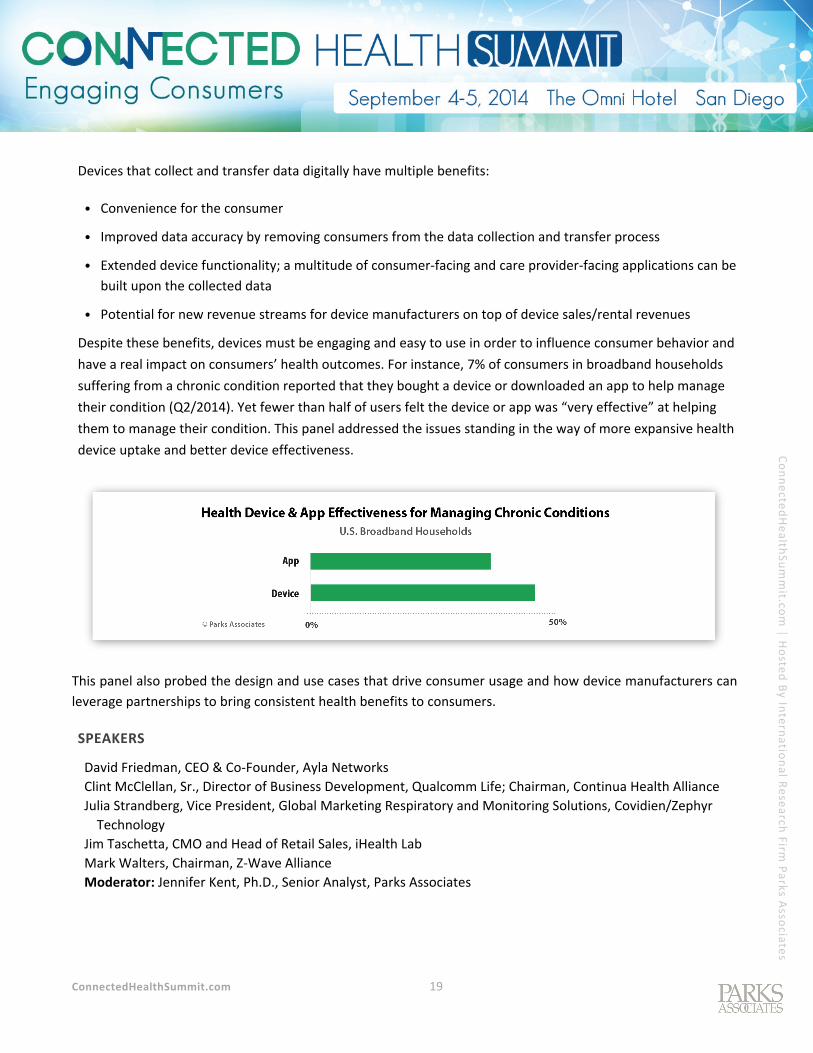

Despite these benefits, devices must be engaging and easy to use in order to influence consumer behavior and

have a real impact on consumers’ health outcomes. For instance, 7% of consumers in broadband households

suffering from a chronic condition reported that they bought a device or downloaded an app to help manage

their condition (Q2/2014). Yet fewer than half of users felt the device or app was “very effective” at helping

them to manage their condition. This panel addressed the issues standing in the way of more expansive health

device uptake and better device effectiveness.

This panel also probed the design and use cases that drive consumer usage and how device manufacturers can

leverage partnerships to bring consistent health benefits to consumers.

SPEAKERS

David Friedman, CEO & Co‐Founder, Ayla Networks

Clint McClellan, Sr., Director of Business Development, Qualcomm Life; Chairman, Continua Health Alliance

Julia Strandberg, Vice President, Global Marketing Respiratory and Monitoring Solutions, Covidien/Zephyr

Technology

Jim Taschetta, CMO and Head of Retail Sales, iHealth Lab

Mark Walters, Chairman, Z‐Wave Alliance

Moderator: Jennifer Kent, Ph.D., Senior Analyst, Parks Associates

ConnectedHealthSummit.com 20

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

20

KEY TAKEAWAYS

• This channel is changing. More and more retailers are asking for a smart home or smart healthcare

representation.

• Devices strengthen the connection and increase the frequency of contact between consumers and health

providers.

• Consumers don’t care about technology standards, they just want devices to work. Simplicity,

convenience, and ease of use are paramount for engagement.

• The trend in connected devices is to move towards a single technology platform. Consumers want a

seamless experience among interoperable systems, but each vendor wants to “own” the customer

relationship. These conditions are going to pose interesting challenges for vendors, which will have to

share data with other vendors to create the truly seamless experience that appeals to consumers.

• The best approach to aggregate data for actionable use:

− Get the consumer’s permission

− Develop standards

− Data must be relevant, viable, accurate

− Data value needs to outweigh cost—benefits need to be great for consumers to want to share

− When used for product usage and behavioral insights, data needs to be anonymous

• What is the tech giant’s role in healthcare services? It doesn’t seem like they are trying to be the experts,

but their role is more in aggregation of data.

• Unproven effectiveness is a top barrier to connected health device adoption.

− There needs to be a distinction between consumer wearables vs. clinical wearables. Accuracy and

effectiveness vary amongst these.

− Can we trust user‐generated data enough to input into EHR?

− Proven cost reduction and/or improved outcomes are important.

− Data integration is important for proven clinical outcome.

Keynote—Building a Consumer‐Centric Connected Health Ecosystem

In this keynote, James R. Mault, M.D., F.A.C.S., discussed the long‐term potential of technology in changing

consumers’ health behaviors as well as best practices to bring technology innovations to the market.

Qualcomm Life shared insight into the challenges of interoperability and aggregating currently disparate

ConnectedHealthSummit.com 21

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

21

consumer data. Dr. Mault also analyzed steps to overcome these hurdles and the importance of making health

apps and devices easier to use for consumers.

SPEAKER:

James R. Mault, M.D., F.A.C.S., Vice President and Chief Medical Officer, Qualcomm Life

KEY TAKEAWAYS

• The current healthcare system is built upon encounter‐based medicine, which is very expensive and

unaffordable.

• It’s time for the health system to leverage consumerism.

• Asynchronous communication enables a continuous care model.

• Team‐based care will become the appropriate approach (leverage technology to enable this).

• 2net™ Platform is liberating health data via wireless networks (simple and convenient to use).

• An open ecosystem is required to enable free flow of data.

• Payment is changed from fee for service to risk‐based captivated payment models

• In circumstances where patients are taking the expensive biologics, the insurance companies paying for

these expensive treatments have a highly vested interest in ensuring patients are compliant to their

treatments.HealthyCircles™ can send reminders to patients to improve medication and care plan

adherence.

• HealthyCircles enables family caregivers, patients and care providers to communicate asynchronously to

better manage a patient's health.

• Exception‐based management: only certain patients will need the virtual doctor’s visit.

ConnectedHealthSummit.com 22

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

22

FRIDAY, SEPTEMBER 5

Connected Devices and Digital Health Services: Consumer Perspectives

Parks Associates analysts explored the impact of the Affordable Care Act and other recent health reforms on

the connected health products and services market. They also shared primary survey data to illustrate

strategies and techniques for engaging different consumers, looking beyond demographics to uncover key

factors that explain how various consumer segments discover, adopt, and use connected health services

differently.

SPEAKER

Jennifer Kent, Ph.D., Senior Analyst, Parks Associates

KEY TAKEAWAYS

• 42% of consumers in U.S. broadband households have used at least one online service offered by their

doctor.

• Connected health devices and services are making health data useful, enabling self‐care, engaging

patients, and expanding patient choices.

• Truly valuable health data is available, and there is a vision that will create value for all players:

− Digitized health data

− Easy consumer access to their own health data

− Consumer data consolidated in one place even if generated by several devices/apps

− Data that is used by service providers/app developers to provide feedback and recommendations to

consumers within context for truly actionable insights

− Data that can be shared with care providers and family members, with patient permission

• Consumers are increasingly using connected health devices and services to engage in self‐care, but there

are two clear places for improvement: consumer confidence in engaging in self‐care and consumers’

perception of the effectiveness of the devices and apps used to manage their health.

− For instance, only 29% of consumers in broadband households who have a chronic condition feel “very

comfortable” selecting a health monitoring device for daily use, and only 28% feel “very comfortable”

designing a care plan for his or her condition.

− Among consumers in broadband households who use a connected device to manage a chronic

condition, 46% feel the device is “very effective”; 37% of health app users feel their app is “very

effective.”

ConnectedHealthSummit.com 23

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

23

• Parks Associates has developed a four‐part segmentation of health consumer groups.

− Healthy & Engaged: consumers who are health‐conscious and do not have a chronic health condition

This segment is the top target for connected wellness/fitness/nutrition devices and apps

This segment is most likely to take the time to exercise.

− Young & Indifferent: consumers who are not health‐conscious, but do not have a chronic health

condition.

This segment is traditionally a good target for new technology, but is a poor target for connected

health devices and apps.

− Challenged but Mindful : consumers who are health conscious but have a chronic health condition

This segment has the motivation to stay health but may need help managing their health.

− Unhealthy & In Denial: consumers who are not health conscious and do suffer from a chronic health

condition

This segment is most likely to lack motivation to exercise and to lose interest in pursuing their

weight goals.

• Industry takeaways for the connected health market:

− Use an open source for data exchange; the industry needs to free health and consumer data from

closed devices and proprietary platforms

− Provide timely, contextually relevant, actionable insights on how consumers can use the data to

improve their health

− Design for the diversity of needs amongst consumer user groups

− Empower consumers to be their own best advocate by understanding their health status through new

technology solutions

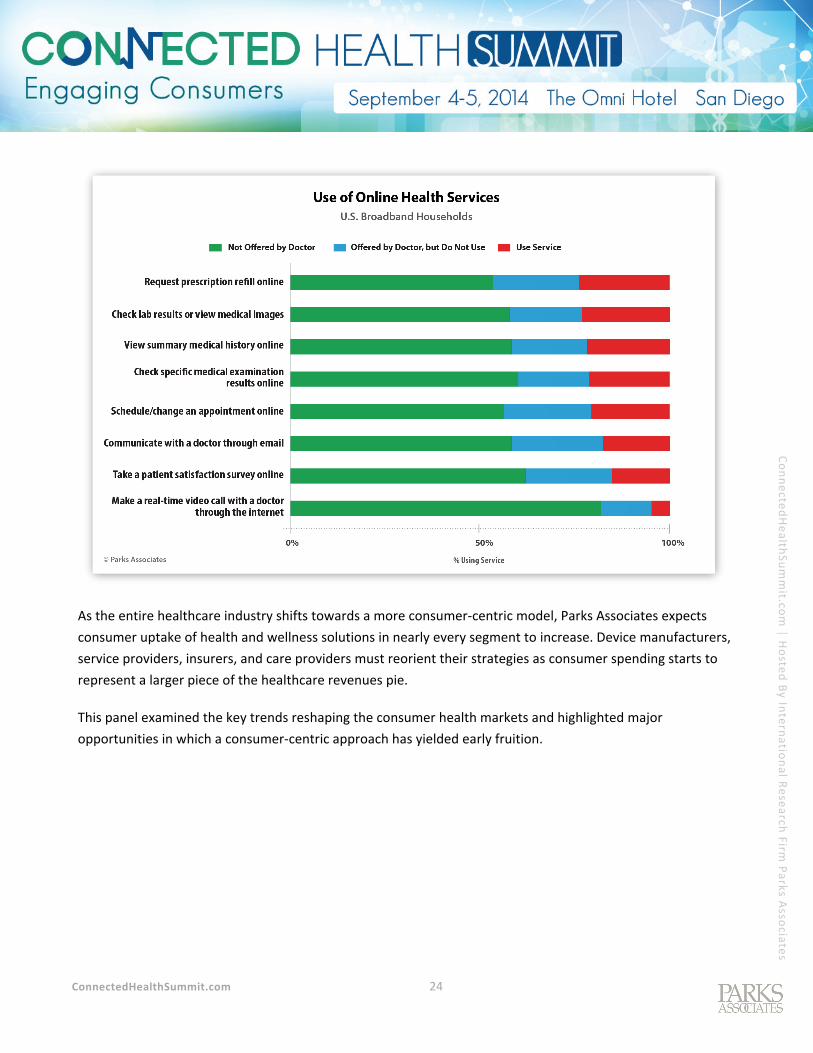

Moving the Digital Health Market Forward: Consumers Take Charge

Consumers are gaining increasingly active roles in their healthcare services. Spending is shifting from

employers to employees, and personal technologies give consumers the ability to make informed decisions

about their healthcare. However, consumer uptake of digital health and wellness solutions is uneven. For

example, 42% of consumers in U.S. broadband households have used at least one online service offered by

their doctors, but usage of specific online tools ranges from 24% of consumers (online prescription refill) to as

low as 5% (real‐time video calling with a doctor). On the fitness side, wearable activity trackers have generated

a lot of press, but usage levels have not yet reached 10%.

ConnectedHealthSummit.com 24

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

24

As the entire healthcare industry shifts towards a more consumer‐centric model, Parks Associates expects

consumer uptake of health and wellness solutions in nearly every segment to increase. Device manufacturers,

service providers, insurers, and care providers must reorient their strategies as consumer spending starts to

represent a larger piece of the healthcare revenues pie.

This panel examined the key trends reshaping the consumer health markets and highlighted major

opportunities in which a consumer‐centric approach has yielded early fruition.

ConnectedHealthSummit.com 25

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

25

SPEAKERS

Christopher Catallo, Senior Vice President, Business Development, Healthgrades

Lena Cheng, MD, Business Development, Doctor on Demand

Jason Donahue, Product Manager for Data & Insights, Jawbone

Patrick Leonard, CTO, iTriage

Philip Marshall, Co‐Founder, Conversa Health

Moderator: Jennifer Kent, Ph.D., Senior Analyst, Parks Associates

KEY TAKEAWAYS

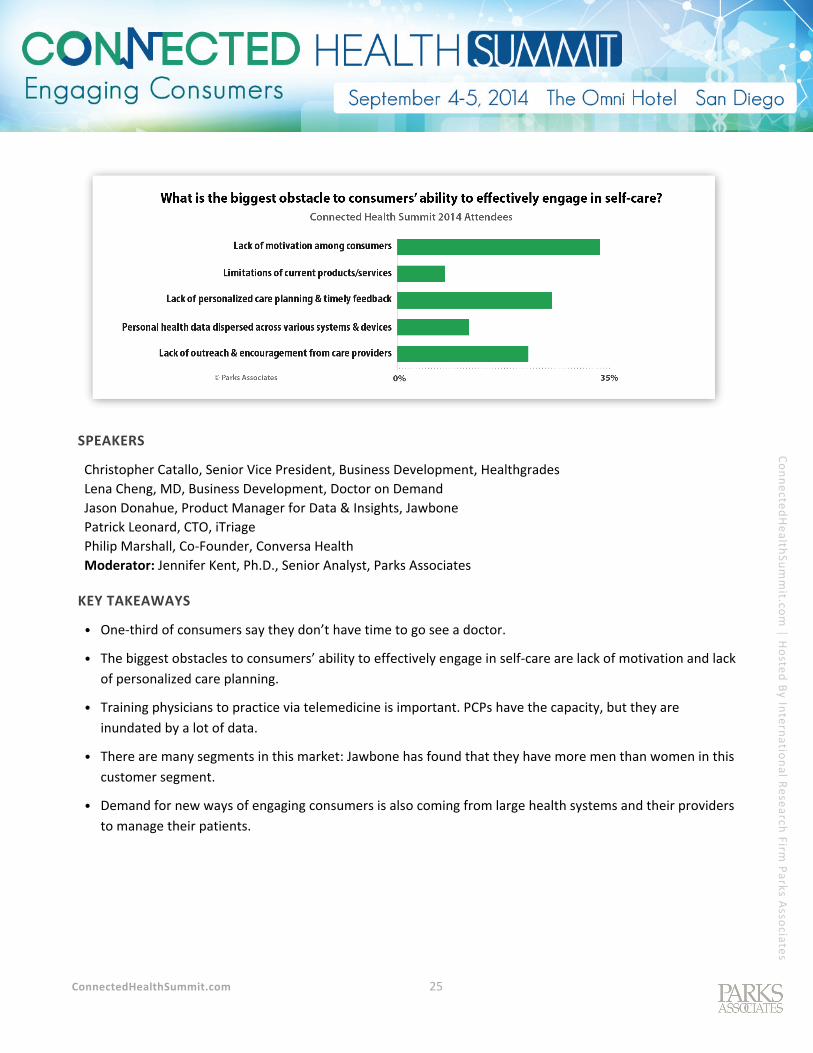

• One‐third of consumers say they don’t have time to go see a doctor.

• The biggest obstacles to consumers’ ability to effectively engage in self‐care are lack of motivation and lack

of personalized care planning.

• Training physicians to practice via telemedicine is important. PCPs have the capacity, but they are

inundated by a lot of data.

• There are many segments in this market: Jawbone has found that they have more men than women in this

customer segment.

• Demand for new ways of engaging consumers is also coming from large health systems and their providers

to manage their patients.

ConnectedHealthSummit.com 26

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

26

Keynote—Consumer Engagement as a Loyalty Strategy

Walgreens has shown the industry how alignment of incentives can accelerate and sustain consumer health

adoption of behavioral change programs. Attendees listened to the best practices Walgreens has developed

and learned how their organization can “Connect with Walgreens” to accelerate initiatives.

SPEAKER

Adam Pellegrini, Vice President, Digital Health, Walgreens

KEY TAKEAWAYS

• The reward program (Balance Rewards; aka, the largest connected pharmacy network) is easy to use and

has a specially designed reward system to encourage consumer participation.

• Walgreens’ digital health strategy is to reduce cost, reduce stress, and provide easy‐to‐use solutions for

consumers.

• Incentives are important for behavioral change.

• Omni‐channel (online, mobile, and in‐store) health experience is crucial.

• Walgreens combines wearables and rewards to drive engagement.

• Small rewards that last all year long are more effective (trials with Walgreens employees have been

successful).

• It’s an ecosystem that attracts many app partners and device partners because of the rapid adoption and

alignment of incentives.

• Digital Coaches/Pharmacy Chat: streamline questions by patients

• Walgreens is working with Google to augment a virtual environment so that consumers will be informed

of all the products in the store.

Incentivizing Behavioral Changes: The Impact of Apps and Big Data

Parks Associates research finds over 50% of U.S. broadband households report having at least one chronic

condition, predominantly obesity or high cholesterol. Digitization and connectivity in the healthcare industry

bring fundamental changes to care practices for these conditions. Patients have multiple digital means to

access health information, self‐evaluate, and communicate with care providers. Care providers have far more

convenient options to engage patients and can better understand consumer needs and motivations through

big data analytics.

ConnectedHealthSummit.com 27

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

27

Mobile health apps are a significant market driver for the mobile health industry. More than 40,000 mobile

health apps have been created, with app adoption and usage benefitting from an expanding smartphone user

base that saw a growing proportion of baby‐boomers and the senior population over the last few years. As a

result, mobile health apps are no longer concentrated in the fitness and wellness category; instead, the health

app market has diversified into categories catering to specific health problems, supporting virtual care

experience between a doctor and a patient, and assisting caregivers to enable independent living at home.

The consumer engagement model with apps has also become more diversified. Although self‐download from

generic app stores remains the dominant way for consumers to get apps, healthcare providers and insurers

have beefed up their efforts to leverage apps for consumer engagement. The Mayo Clinic, for instance, has

worked with app developers to launch several types of apps, including a symptom checker, a meditation tool,

a patient education app, and an e‐concierge service app.

Third‐party app developers are also building more sophisticated apps that offer clinical value to care providers.

WellDoc’s BlueStar diabetes management app is one such example that a doctor can prescribe to patients.

Connected health device makers also strive to differentiate their products with a distinctive experience

through their device‐specific apps. These activities, in Parks Associates’ view, represent a healthy growth of an

emerging industry.

Market barriers still remain, however. The biggest challenge for app developers and their customers is

sustaining consumer app usage and deepening consumer engagement to eventually change consumer

behavior for the good. From a business perspective, increased usage level and engagement depth is a

prerequisite to building a successful business/revenue model. Competition is intense, requiring developers to

differentiate their apps’ experience, which hinges on continued innovations to increase app “stickiness.”

In addition to social and gamification techniques, Parks Associates has identified physician engagement as a

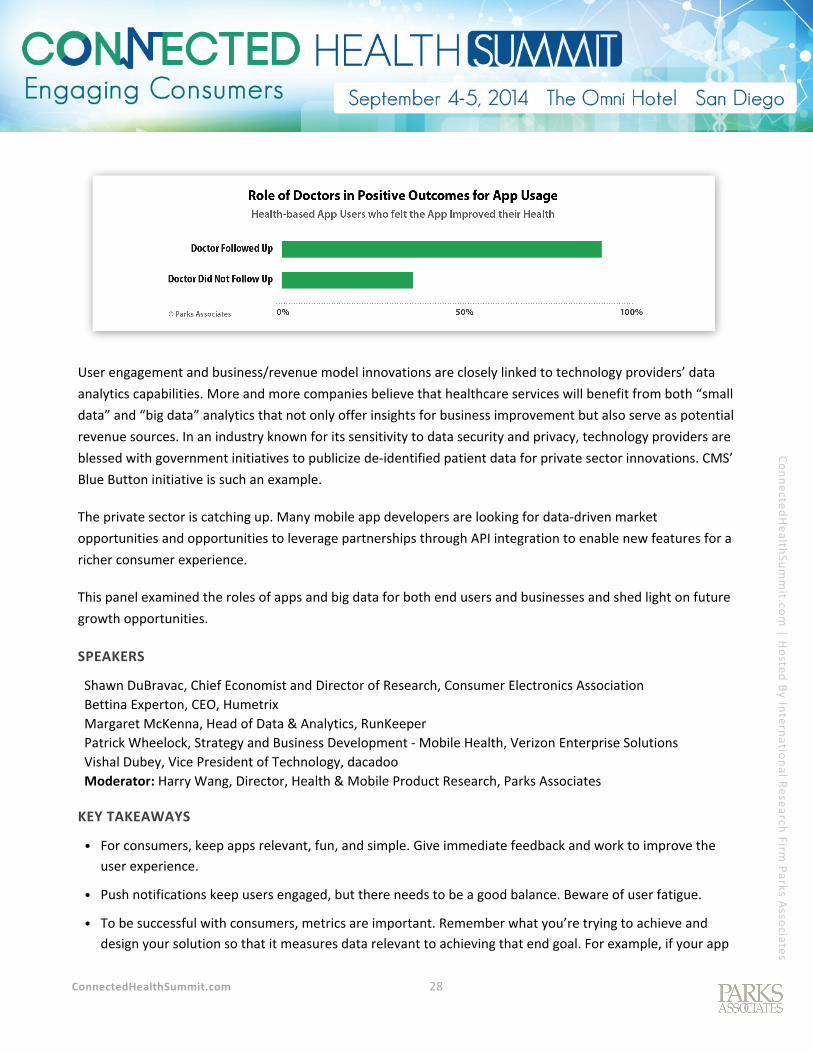

key strategy to ensure continued health app use among consumers. Six percent of consumers in broadband

households reported that a doctor had personally recommended they try a mobile health application.

Seventy‐five percent of all health app users felt the app improved their health condition—among those whose

doctors followed up about their app usage, that rate increased to 91%.

ConnectedHealthSummit.com 28

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

28

User engagement and business/revenue model innovations are closely linked to technology providers’ data

analytics capabilities. More and more companies believe that healthcare services will benefit from both “small

data” and “big data” analytics that not only offer insights for business improvement but also serve as potential

revenue sources. In an industry known for its sensitivity to data security and privacy, technology providers are

blessed with government initiatives to publicize de‐identified patient data for private sector innovations. CMS’

Blue Button initiative is such an example.

The private sector is catching up. Many mobile app developers are looking for data‐driven market

opportunities and opportunities to leverage partnerships through API integration to enable new features for a

richer consumer experience.

This panel examined the roles of apps and big data for both end users and businesses and shed light on future

growth opportunities.

SPEAKERS

Shawn DuBravac, Chief Economist and Director of Research, Consumer Electronics Association

Bettina Experton, CEO, Humetrix

Margaret McKenna, Head of Data & Analytics, RunKeeper

Patrick Wheelock, Strategy and Business Development ‐ Mobile Health, Verizon Enterprise Solutions

Vishal Dubey, Vice President of Technology, dacadoo

Moderator: Harry Wang, Director, Health & Mobile Product Research, Parks Associates

KEY TAKEAWAYS

• For consumers, keep apps relevant, fun, and simple. Give immediate feedback and work to improve the

user experience.

• Push notifications keep users engaged, but there needs to be a good balance. Beware of user fatigue.

• To be successful with consumers, metrics are important. Remember what you’re trying to achieve and

design your solution so that it measures data relevant to achieving that end goal. For example, if your app

ConnectedHealthSummit.com 29

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

29

or solution is designed to encourage activity, create an algorithm that can send encouragements to walk or

stretch at key intervals. If weight loss is the goal, design a solution that can suggest healthier alternatives

to certain foods.

• Trusted sources such as payers and providers will give consumers a sense of confidence about the privacy

of their personal health information.

Keynote—Enhancing the Consumer’s Propensity to Succeed in a Digital Health Management World

How can we help consumers identify and reduce health‐related risks and gaps in care that can adversely affect

the quality of their lives? The best programs designed to do this are grounded in theory and based upon goals

that individual consumers want to achieve. These goals might include improvements in functional status or life

satisfaction, expressed via example such as, “I want to spend more time with my family and less time in the

hospital.” How can we help consumers improve their chances of success in a digital world? Dr. Ozminkowski

addressed this and related questions during this keynote session.

SPEAKER

Ronald J. Ozminkowski, Ph.D., Senior Vice President & Chief Scientific Officer, Consumer Solutions Group, Optum

KEY TAKEAWAYS

• Success occurs when you meet consumers where they want to be met, digitally and otherwise.

• Health programs need to be fun/simple/engaging.

• Consumers want to be functionally independent.

• Ongoing engagement is key (but keep it relevant to the consumer’s needs).

• Mass personalization—solutions need to be person‐oriented but also scalable.

• The 4 Vs of big data will influence how we are able to help consumers:

− Volume

− Velocity

− Variety

− Variability

• Disease management and wellness programs help members who want to feel better, walk and work

without pain, and spend more time with family.

ConnectedHealthSummit.com 30

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

30

• Individual consumers are a lot more interested in their personal health goals than what their employers

and insurance companies are interested in.

• The big question is: how can companies engage users as long as possible, keeping the above point in mind?

• The industry needs to develop better predictive modeling to help personalize the user experience.

• The healthcare industry is most likely to have success when it integrates technology with the clinical

environment.

Healthcare Purchasing Decisions: The Power of the Informed Consumer

Consumer‐centric healthcare represents a radical change in the way the U.S. healthcare industry operates. For

many health industry players, consumer choice, pricing transparency, and patient feedback have been

irrelevant to business operations—until now. New solutions offer consumers the ability to compare, rate, and

review their physicians and care facilities online and even gain insight into the costs of specific procedures. In

other cases, technologies and solutions help consumers make smart choices about health insurance, care

providers, and spending on various wellness‐focused products and services.

Though relatively new, Parks Associates data shows consumers are already showing interest in these solutions.

Over a quarter of consumers in broadband households would check online review and rating sites when

shopping for a new care provider, and more than a fifth would browse physician and care provider websites.

Furthermore, 40% of consumers in broadband households rated the ability to view what a procedure or visit

would cost beforehand to be a “very important” factor in selecting care providers—the most important factor

tested.

ConnectedHealthSummit.com 31

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

31

These new tools arm consumers with knowledge that had been very difficult, if not impossible, to access

previously. Now that consumers can make more informed choices, care providers must evolve their way of

engaging new and existing patients. Providers must demonstrate to consumers that they offer high quality

care that is also responsive, convenient, and cost‐effective.

In this panel, speakers discussed the ways in which greater consumer knowledge in the shopping process,

pricing transparency, and patient reviews will change their business operations and strategies. They also

examined strategies and opportunities for industry players to engage the new population of informed

consumers.

SPEAKERS

Jennifer Griffin, Product Marketing Specialist, Health and Wellness Division, Angie’s List

Amer Haider, CEO, Doctella

Jonathan Ozeran, VP of Product, Zest Health

Moderator: Jennifer Kent, Ph.D., Senior Analyst, Parks Associates

KEY TAKEAWAYS

• The new healthcare model is based on consumer engagement and feedback so doctors can do a better job

in providing care.

• The transition to consumerism in healthcare produces anxiety in care providers. Physicians have not had to

face or publicly address negative consumer feedback in the same way service providers of other industries

deal within their normal business operations.

• Restricting consumer choices as a result of closed insurance networks prevent patient empowerment.

• Physician and care facility rating/review sites challenge the old model and require physicians to actively

engage, serve, and respond to their patients’ feedback in order to protect their reputations.

ConnectedHealthSummit.com 32

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

32

• Reduction in human errors in hospitals is important. Patient checklists can help this problem.

• Understanding and getting meaningful data and pricing transparency are two key obstacles for consumers.

• Zest’s app allows patients to price out medical procedures. Doctella provides checklists for procedures to

help consumers be aware of what to know before getting a procedure. Angie’s List provides reviews of

hospitals and caregivers.

• Consumer awareness of hospital ratings is very low (e.g., awareness of the site Hospitalcompare.gov was

low).

• Hospitals are required to meet the CMS (Center for Medicare & Medicaid Services) standards, otherwise

they are penalized.

Effective Strategies to Drive Healthy Living through all Life Stages

The United States is witnessing a sea‐change in healthcare that is bringing about more consumer‐centric

products and services. Regulators, insurers, and care providers are shifting to a patient‐centered approach that

engages patients as active participants in their own care management and assists consumers in their healthy

living pursuit. Concurrently, design breakthroughs, technology advances, and mass adoption of mobile

consumer devices have made consumer‐centric care possible in ways previously impossible.

A significant shift in strategy is taking place in the healthcare industry to address the “triple aim”—goals to rein

in healthcare spending, enhance care quality, and increase access to care. Different from past efforts that

focused on cost cutting as the leading goal, recent industry efforts reflect a recognition that these three goals

are intrinsically linked and mutually influential. Central to these efforts is the ability to leverage the latest

technology innovations to improve business processes and build user‐friendly healthcare products and

services. Parks Associates believes that technology has the potential to help achieve all three goals

simultaneously if it is implemented correctly, and one of the key requirements is the buy‐in from both

consumers and healthcare providers.

Thus, a practical task for the current round of healthcare transformation is to engage and motivate consumers.

As consumers move through their different life stages, their care needs and the support expected from care

providers will vary. Throughout the care continuum that almost every consumer will go through, it is

imperative to motivate them by putting the right information in their hands and awakening their inner health

consciousness for better living. It also requires proactively engaging consumers and addressing their practical

needs with support and advice as they move through different life stages and face different types of healthy

living challenges.

A new breed of care management firms have emerged to take up these challenges. Unlike traditional disease

management firms that focus on certain types of diseases and a high‐cost patient population, these new

ConnectedHealthSummit.com 33

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

33

companies offer a broader scope of services and excel at addressing preventive care and the healthy living

needs of consumers on behalf of their employers, health plans, and care providers. Leveraging current

communications and patient engagement tools, they build a scalable business to offer cost‐effective solutions

to benefit consumers and their business customers.

This panel examined approaches to design effective and engaging programs and services that cater to the

diverse needs of self‐care and healthy living and discussed strategies and business models for consumer

adoption.

SPEAKERS

Meghan Oates‐Zalesky, Vice President of Marketing, ShapeUp

Lou Ryan, CEO, SelfHelpWorks

Dennis Upah, EVP of Enterprise Markets, Remedy Health Media

Charlotte Yeh, Chief Medical Officer, AARP

Eric Zimmerman, VP Business Development, Redbrick Health

Moderator: Harry Wang, Director, Health & Mobile Product Research, Parks Associates

KEY TAKEAWAYS

• Success in care management is about explaining the value of services to increase their use and create

patient engagement.

• A trigger needs to be invoked to aid behavioral changes.

• There’s a group of consumers who think that they are very healthy, and they are reluctant to use apps to

manage their health. The industry must devise creative ways to engage these consumers without

antagonizing them.

• Sustainability is a key issue for the device industry.

Investment Trends in Consumer Health

The United States, along with many countries worldwide, is witnessing dramatic change in healthcare that is

bringing about more consumer‐centric products and services. Regulators, insurers, and care providers are

shifting to a patient‐centered approach that engages patients as active participants in their own care

management. Concurrently, design breakthroughs, technology advances, and mass adoption of mobile

consumer devices have made consumer‐centric care possible in ways previously impossible.

Consumer electronics companies have taken note; the result is the rise of a young but very dynamic market for

connected health and wellness devices that help care providers better engage their patients as well as assist

ConnectedHealthSummit.com 34

Connecte

dHealth

Summit.co

m | Hoste

d By In

ternatio

nal R

esearch

Firm

Parks A

ssocia

tes

34

consumers with their self‐care needs. This market joins other consumer‐facing health technology market

segments, including aging‐in‐place technologies and disease management.

The dramatic changes to government health legislation are, of course, giving rise to consumerization of health

care services, and giving consumers more visibility and ultimately more control over the healthcare services

they select and purchase. This shift provides significant opportunities for technology products and services to

serve new roles in assisting in the shopping, selection, and delivery of health services.

According to estimates from Parks Associates, device manufacturers will sell more than 40 million personal

health and wellness products in 2013, a figure that will rise to more than 70 million by 2018. Through product

sales and software and service revenues, the health and wellness market alone will generate over $3.3 billion

in 2013 and increase to more than $8 billion by 2018.

This panel of leading investors in the consumer health industry discussed the state of the market and analyzed

the future solutions they find the most intriguing and exciting.

SPEAKERS

Tim Chang, Managing Director, Mayfield Fund

Skip Fleshman, Partner, Asset Management Ventures

Polina Hanin, Academy Director, StartUp Health

Moderator: Stuart Sikes, President, Parks Associates

KEY TAKEAWAYS

• There have been a lot of great ideas channeling through the venture community, but anything that

requires FDA approval provides a greater challenge for the VC community.

• One way to get around the FDA for now is not to promote the diagnosis part, but to promote it as

awareness. For instance, an app my give the consumer insight into their cardiac rhythms but not claim to

diagnose any irregularities.

• Big pharma and payers have not really bought into the connected health market, so the M&A activity is not

very active.

• Other health related ideas/apps: Food 2.0 – most of the current solutions tackle fitness or health

outcomes. There is a very real need to tackle the challenge of making better nutritional decisions and

measuring/modifying food intake.

• Following the ACA is very important. Giving enterprises the tool to navigate the ACA could be a very useful

and successful approach.

• The more repeatable and sustainable model could be one that moves from purely tracking to health

coaching (more like concierge healthcare model).