Embed Size (px)

Citation preview

Confidential Draft

Embassy Row Acquisition Update

November 2008

2

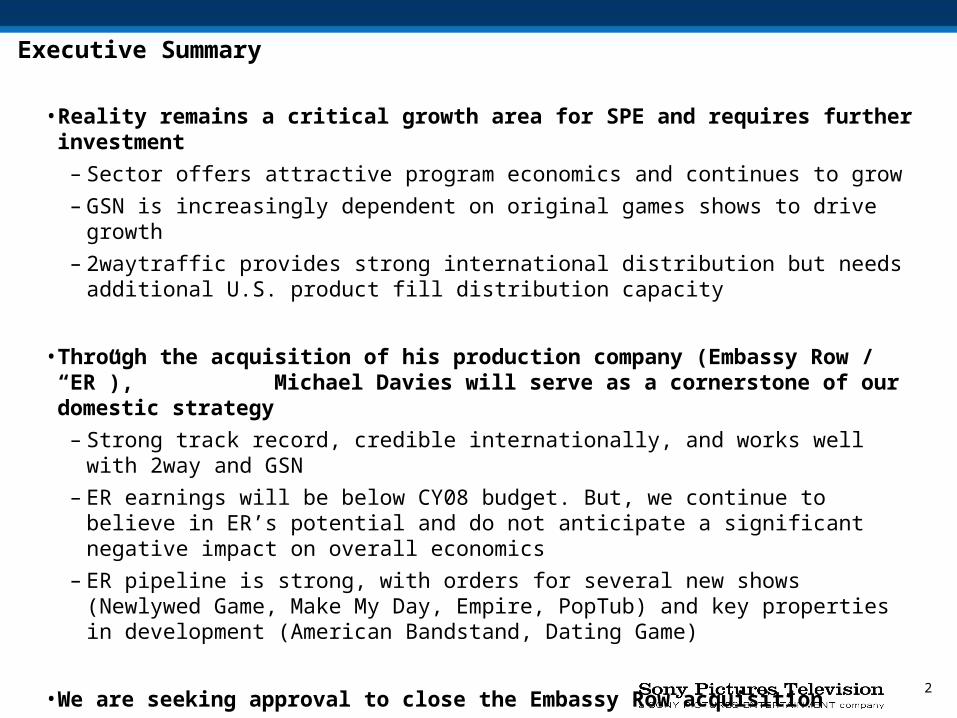

• Reality remains a critical growth area for SPE and requires further investment

– Sector offers attractive program economics and continues to grow

– GSN is increasingly dependent on original games shows to drive growth

– 2waytraffic provides strong international distribution but needs additional U.S. product fill distribution capacity

• Through the acquisition of his production company (Embassy Row / “ER”), Michael Davies will serve as a cornerstone of our domestic strategy

– Strong track record, credible internationally, and works well with 2way and GSN

– ER earnings will be below CY08 budget. But, we continue to believe in ER’s potential and do not anticipate a significant negative impact on overall economics

– ER pipeline is strong, with orders for several new shows (Newlywed Game, Make My Day, Empire, PopTub) and key properties in development (American Bandstand, Dating Game)

• We are seeking approval to close the Embassy Row acquisition

– Long-form negotiated in-line terms previously discussed ($25MM at close, up to an additional $50MM of earn-outs)

– RAD to be signed by [date]; deal to be closed by [date]

Executive Summary

3

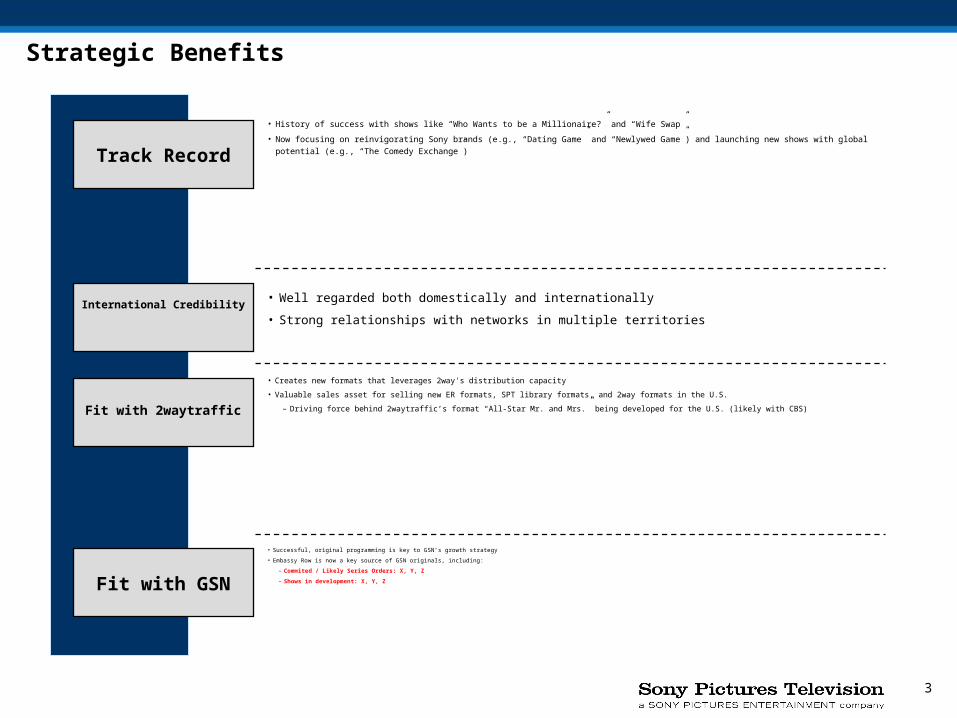

• Creates new formats that leverages 2way's distribution capacity

• Valuable sales asset for selling new ER formats, SPT library formats, and 2way formats in the U.S.

– Driving force behind 2waytraffic’s format “All-Star Mr. and Mrs.” being developed for the U.S. (likely with CBS)

Strategic Benefits

International Credibility• Well regarded both domestically and internationally

• Strong relationships with networks in multiple territories

Fit with 2waytraffic

Fit with GSN

• Successful, original programming is key to GSN’s growth strategy

• Embassy Row is now a key source of GSN originals, including:

– Commited / Likely Series Orders: X, Y, Z

– Shows in development: X, Y, Z

Track Record

• History of success with shows like “Who Wants to be a Millionaire?” and “Wife Swap”

• Now focusing on reinvigorating Sony brands (e.g., “Dating Game” and “Newlywed Game”) and launching new shows with global potential (e.g., “The

Comedy Exchange”)

4

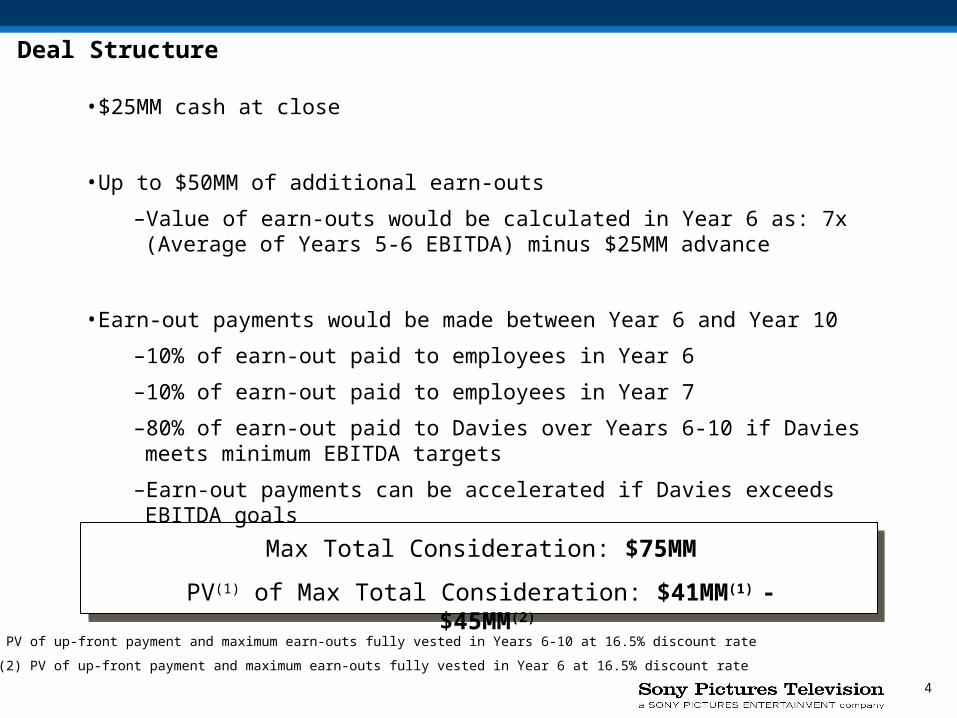

Deal Structure

• $25MM cash at close

• Up to $50MM of additional earn-outs

–Value of earn-outs would be calculated in Year 6 as: 7x (Average of Years 5-6 EBITDA) minus $25MM advance

• Earn-out payments would be made between Year 6 and Year 10

–10% of earn-out paid to employees in Year 6

–10% of earn-out paid to employees in Year 7

–80% of earn-out paid to Davies over Years 6-10 if Davies meets minimum EBITDA targets

–Earn-out payments can be accelerated if Davies exceeds EBITDA goals

Max Total Consideration: $75MM

PV(1) of Max Total Consideration: $41MM(1) - $45MM(2)

Note: (1) PV of up-front payment and maximum earn-outs fully vested in Years 6-10 at 16.5% discount rate

(2) PV of up-front payment and maximum earn-outs fully vested in Year 6 at 16.5% discount rate

5

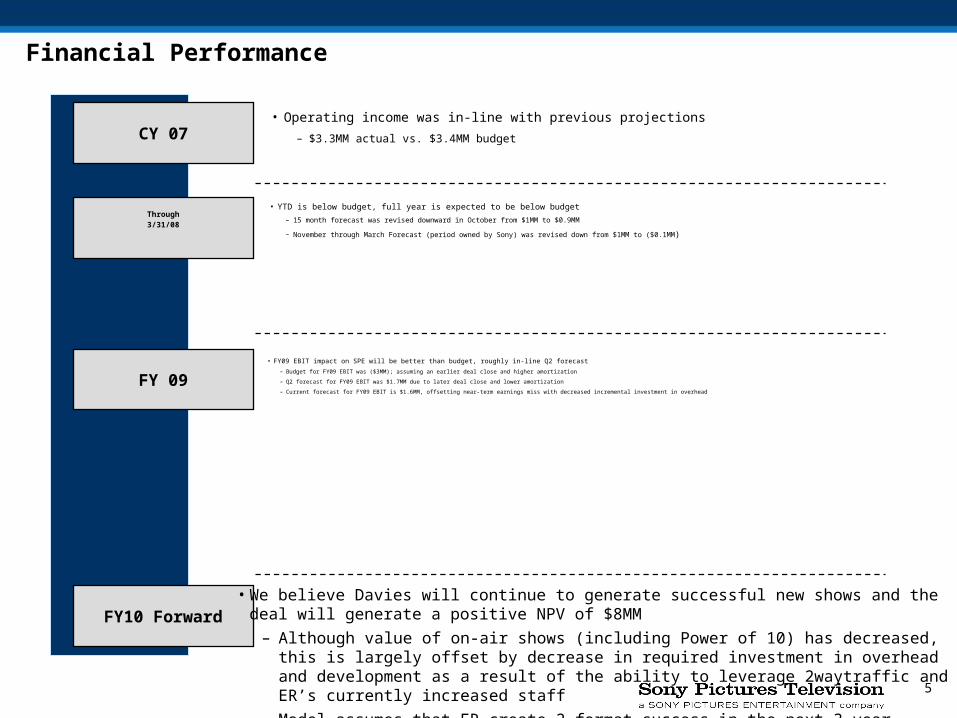

• FY09 EBIT impact on SPE will be better than budget, roughly in-line Q2 forecast

– Budget for FY09 EBIT was ($3MM); assuming an earlier deal close and higher amortization

– Q2 forecast for FY09 EBIT was $1.7MM due to later deal close and lower amortization

– Current forecast for FY09 EBIT is $1.6MM, offsetting near-term earnings miss with decreased incremental investment in overhead

Financial Performance

Through3/31/08

• YTD is below budget, full year is expected to be below budget

– 15 month forecast was revised downward in October from $1MM to $0.9MM

– November through March Forecast (period owned by Sony) was revised down from $1MM to ($0.1MM)

FY 09

FY10 Forward

CY 07• Operating income was in-line with previous projections

– $3.3MM actual vs. $3.4MM budget

• We believe Davies will continue to generate successful new shows and the deal will generate a positive NPV of $8MM

– Although value of on-air shows (including Power of 10) has decreased, this is largely offset by decrease in required investment in overhead and development as a result of the ability to leverage 2waytraffic and ER’s currently increased staff

– Model assumes that ER create 2 format success in the next 3 year

6

Pipeline Remains StrongPilot & Series Orders Shows in Development

Show Network Show Network

Newlywed

Make My Day

Empire

The Comedy Exchange

BBC America / UKTV

National Bible

Grand Masters ff Pop Culture Vh1

Pop Tub

America's Strongest

Hold on to Your Seat GSN

Hogs

It’s A Knockout: U.S. vs. France GSN / TBD

Honey Please GSN / TBD

Game Show Talk Show GSN

Please format / check / clean-up

7

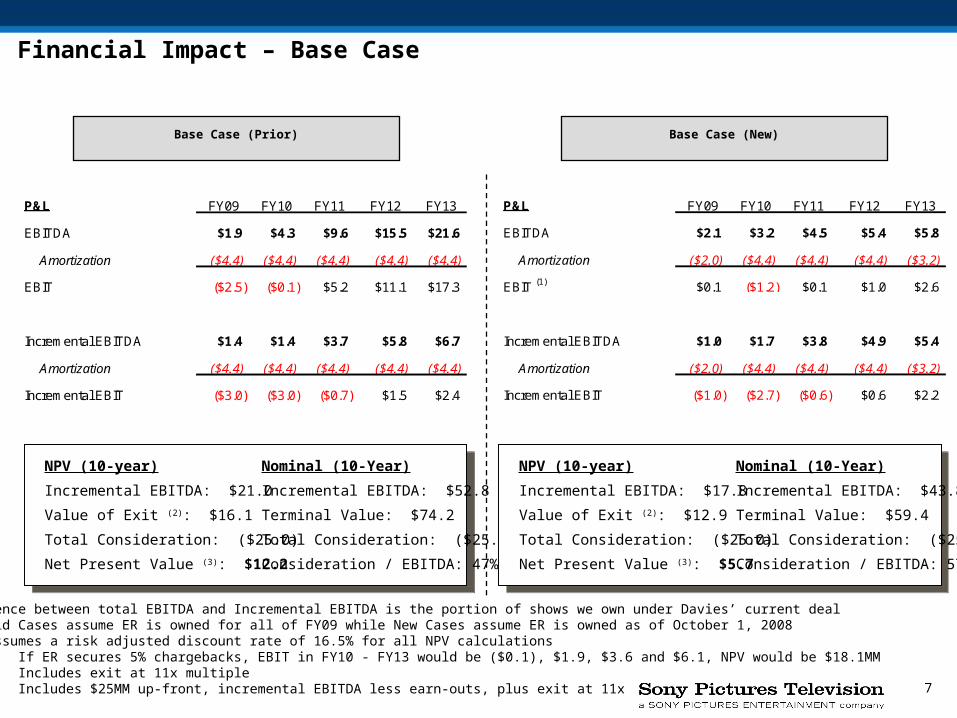

Financial Impact – Base Case

Notes: Difference between total EBITDA and Incremental EBITDA is the portion of shows we own under Davies’ current deal Old Cases assume ER is owned for all of FY09 while New Cases assume ER is owned as of October 1, 2008 Assumes a risk adjusted discount rate of 16.5% for all NPV calculations (1) If ER secures 5% chargebacks, EBIT in FY10 - FY13 would be ($0.1), $1.9, $3.6 and $6.1, NPV would be $18.1MM (2) Includes exit at 11x multiple (3) Includes $25MM up-front, incremental EBITDA less earn-outs, plus exit at 11x

Base Case (New)Base Case (Prior)

NPV (10-year)

Incremental EBITDA: $21.0

Value of Exit (2): $16.1

Total Consideration: ($25.0)

Net Present Value (3): $12.2

Nominal (10-Year)

Incremental EBITDA: $52.8

Terminal Value: $74.2

Total Consideration: ($25.0)

Consideration / EBITDA: 47%

NPV (10-year)

Incremental EBITDA: $17.8

Value of Exit (2): $12.9

Total Consideration: ($25.0)

Net Present Value (3): $5.7

Nominal (10-Year)

Incremental EBITDA: $43.8

Terminal Value: $59.4

Total Consideration: ($25.0)

Consideration / EBITDA: 57%

P&L FY09 FY10 FY11 FY12 FY13

EBITDA $1.9 $4.3 $9.6 $15.5 $21.6

Amortization ($4.4) ($4.4) ($4.4) ($4.4) ($4.4)

EBIT ($2.5) ($0.1) $5.2 $11.1 $17.3

Incremental EBITDA $1.4 $1.4 $3.7 $5.8 $6.7

Amortization ($4.4) ($4.4) ($4.4) ($4.4) ($4.4)

Incremental EBIT ($3.0) ($3.0) ($0.7) $1.5 $2.4

P&L FY09 FY10 FY11 FY12 FY13

EBITDA $2.1 $3.2 $4.5 $5.4 $5.8

Amortization ($2.0) ($4.4) ($4.4) ($4.4) ($3.2)

EBIT (1) $0.1 ($1.2) $0.1 $1.0 $2.6

Incremental EBITDA $1.0 $1.7 $3.8 $4.9 $5.4

Amortization ($2.0) ($4.4) ($4.4) ($4.4) ($3.2)

Incremental EBIT ($1.0) ($2.7) ($0.6) $0.6 $2.2

8

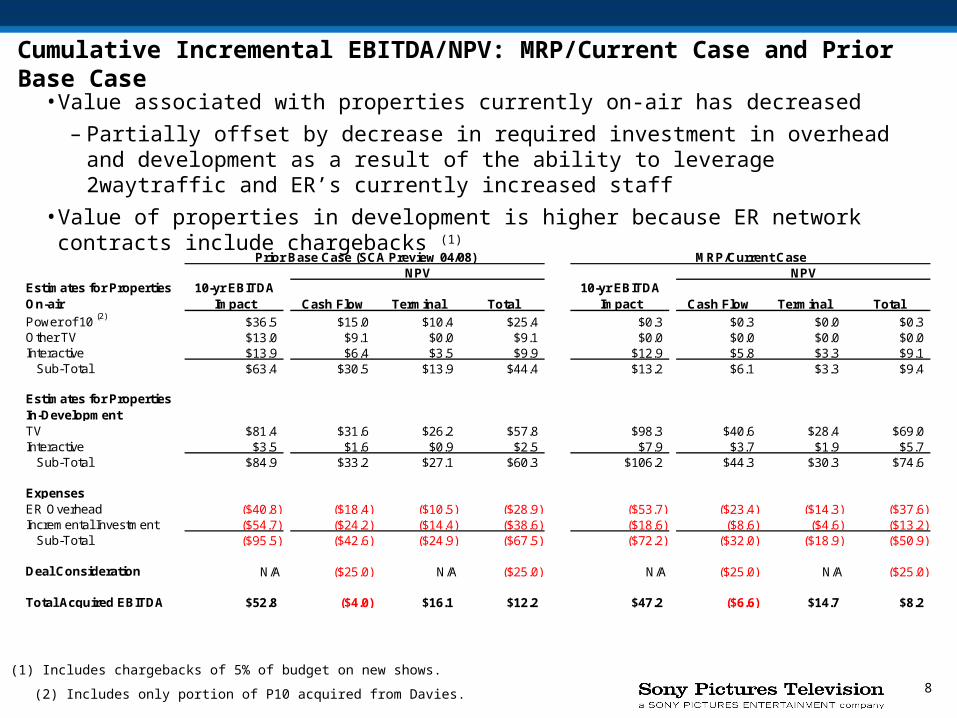

Cumulative Incremental EBITDA/NPV: MRP/Current Case and Prior Base Case

• Value associated with properties currently on-air has decreased

– Partially offset by decrease in required investment in overhead and development as a result of the ability to leverage 2waytraffic and ER’s currently increased staff

• Value of properties in development is higher because ER network contracts include chargebacks (1)

Note: (1) Includes chargebacks of 5% of budget on new shows.

(2) Includes only portion of P10 acquired from Davies.

Prior Base Case (SCA Preview 04/08) MRP/Current CaseNPV NPV Base Case (Prior)

Estimates for Properties On-air

10-yr EBITDA Impact Cash Flow Terminal Total

10-yr EBITDA Impact Cash Flow Terminal Total

Power of 10 (2) $36.5 $15.0 $10.4 $25.4 $0.3 $0.3 $0.0 $0.3Other TV $13.0 $9.1 $0.0 $9.1 $0.0 $0.0 $0.0 $0.0Interactive $13.9 $6.4 $3.5 $9.9 $12.9 $5.8 $3.3 $9.1

Sub-Total $63.4 $30.5 $13.9 $44.4 $13.2 $6.1 $3.3 $9.4

Estimates for Properties In-DevelopmentTV $81.4 $31.6 $26.2 $57.8 $98.3 $40.6 $28.4 $69.0Interactive $3.5 $1.6 $0.9 $2.5 $7.9 $3.7 $1.9 $5.7

Sub-Total $84.9 $33.2 $27.1 $60.3 $106.2 $44.3 $30.3 $74.6

ExpensesER Overhead ($40.8) ($18.4) ($10.5) ($28.9) ($53.7) ($23.4) ($14.3) ($37.6)Incremental Investment ($54.7) ($24.2) ($14.4) ($38.6) ($18.6) ($8.6) ($4.6) ($13.2)

Sub-Total ($95.5) ($42.6) ($24.9) ($67.5) ($72.2) ($32.0) ($18.9) ($50.9)

Deal Consideration N/A ($25.0) N/A ($25.0) N/A ($25.0) N/A ($25.0)

Total Acquired EBITDA $52.8 ($4.0) $16.1 $12.2 $47.2 ($6.6) $14.7 $8.2

9

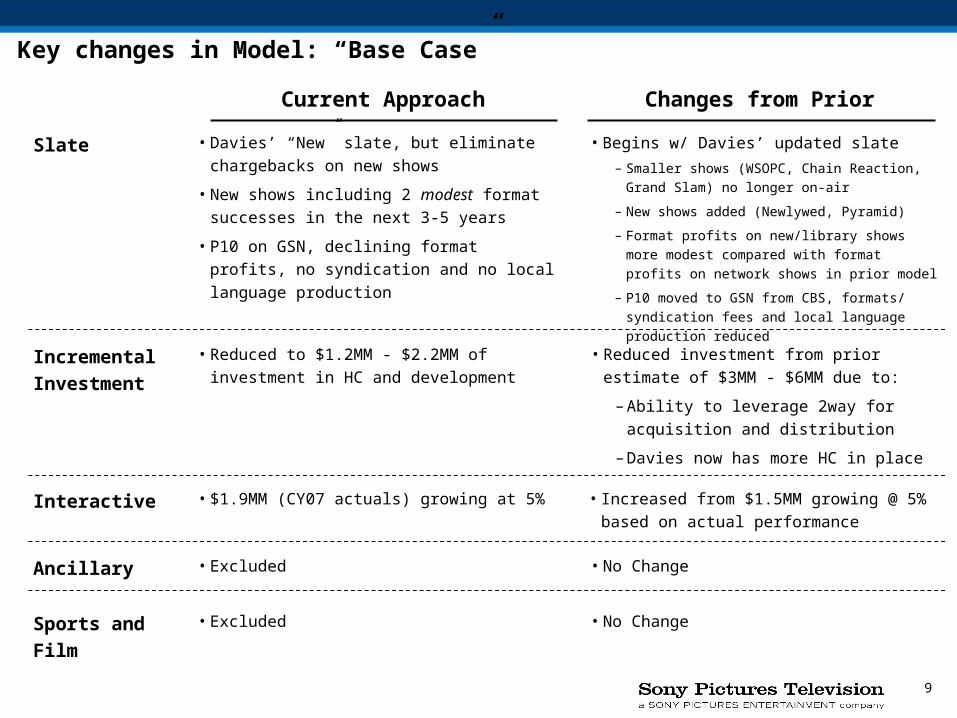

Key changes in Model: “Base Case”

Changes from PriorCurrent Approach

• Davies’ “New” slate, but eliminate chargebacks

on new shows

• New shows including 2 modest format successes

in the next 3-5 years

• P10 on GSN, declining format profits, no

syndication and no local language production

• Begins w/ Davies’ updated slate

– Smaller shows (WSOPC, Chain Reaction, Grand

Slam) no longer on-air

– New shows added (Newlywed, Pyramid)

– Format profits on new/library shows more modest

compared with format profits on network shows in

prior model

– P10 moved to GSN from CBS, formats/ syndication

fees and local language production reduced

Slate

• Reduced to $1.2MM - $2.2MM of investment in

HC and development

• Reduced investment from prior estimate of

$3MM - $6MM due to:

– Ability to leverage 2way for acquisition and

distribution

– Davies now has more HC in place

Incremental

Investment

• $1.9MM (CY07 actuals) growing at 5% • Increased from $1.5MM growing @ 5% based on

actual performanceInteractive

• Excluded • No ChangeAncillary

• Excluded • No ChangeSports and Film

10

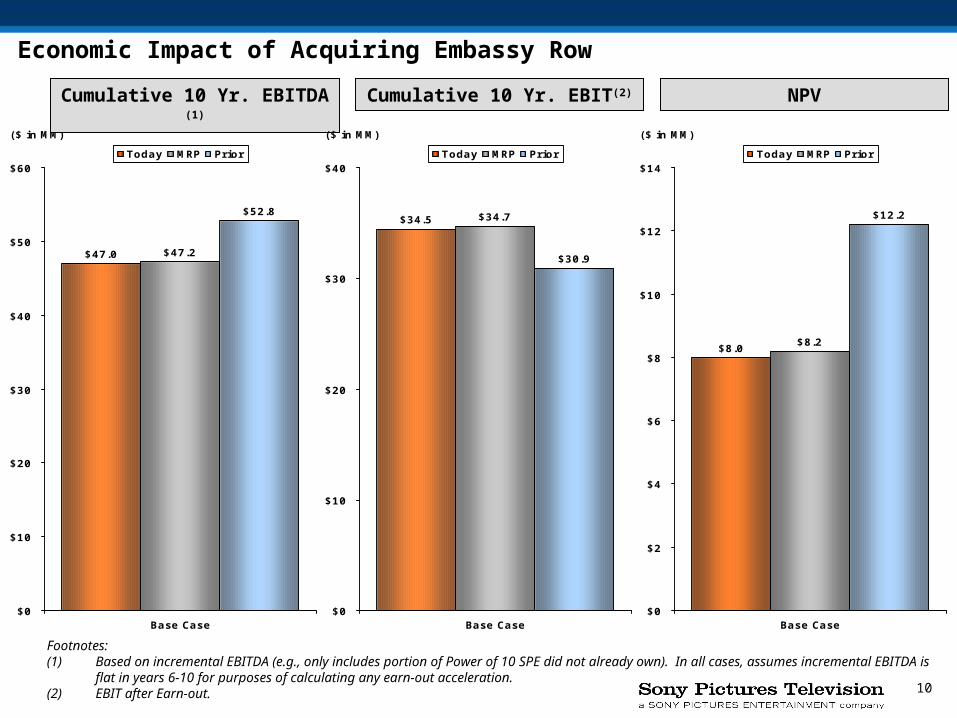

Economic Impact of Acquiring Embassy Row

$47.0 $47.2

$52.8

$0

$10

$20

$30

$40

$50

$60

Base Case

($ in MM)

Today MRP Prior

Cumulative 10 Yr. EBITDA (1) Cumulative 10 Yr. EBIT(2) NPV

Footnotes:(1) Based on incremental EBITDA (e.g., only includes portion of Power of 10 SPE did not already own). In all cases, assumes incremental EBITDA

is flat in years 6-10 for purposes of calculating any earn-out acceleration.(2) EBIT after Earn-out.

$34.5 $34.7

$30.9

$0

$10

$20

$30

$40

Base Case

($ in MM)

Today MRP Prior

$8.0$8.2

$12.2

$0

$2

$4

$6

$8

$10

$12

$14

Base Case

($ in MM)

Today MRP Prior

11

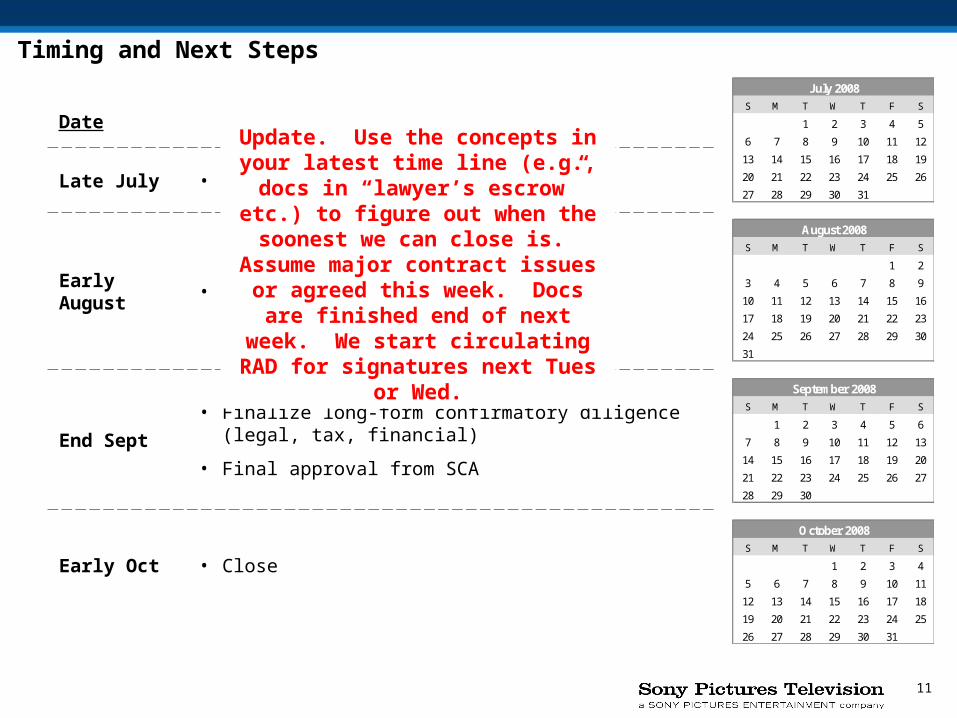

Date

Late July • Lynton / Hendler review

Early August • Formalize / sign term sheet

End Sept

• Finalize long-form confirmatory diligence (legal, tax, financial)

• Final approval from SCA

Early Oct • Close

Timing and Next Steps

S M T W T F S

1 2 3 4 5

6 7 8 9 10 11 12

13 14 15 16 17 18 19

20 21 22 23 24 25 26

27 28 29 30 31

S M T W T F S

1 2

3 4 5 6 7 8 9

10 11 12 13 14 15 16

17 18 19 20 21 22 23

24 25 26 27 28 29 30

31

S M T W T F S

1 2 3 4 5 6

7 8 9 10 11 12 13

14 15 16 17 18 19 20

21 22 23 24 25 26 27

28 29 30

S M T W T F S

1 2 3 4

5 6 7 8 9 10 11

12 13 14 15 16 17 18

19 20 21 22 23 24 25

26 27 28 29 30 31

August 2008

September 2008

October 2008

July 2008

Update. Use the concepts in your latest time line (e.g.,

docs in “lawyer’s escrow” etc.) to figure out when the soonest we can close is. Assume major contract issues or agreed this

week. Docs are finished end of next week. We start

circulating RAD for signatures next Tues or Wed.

12

• Appendix

13

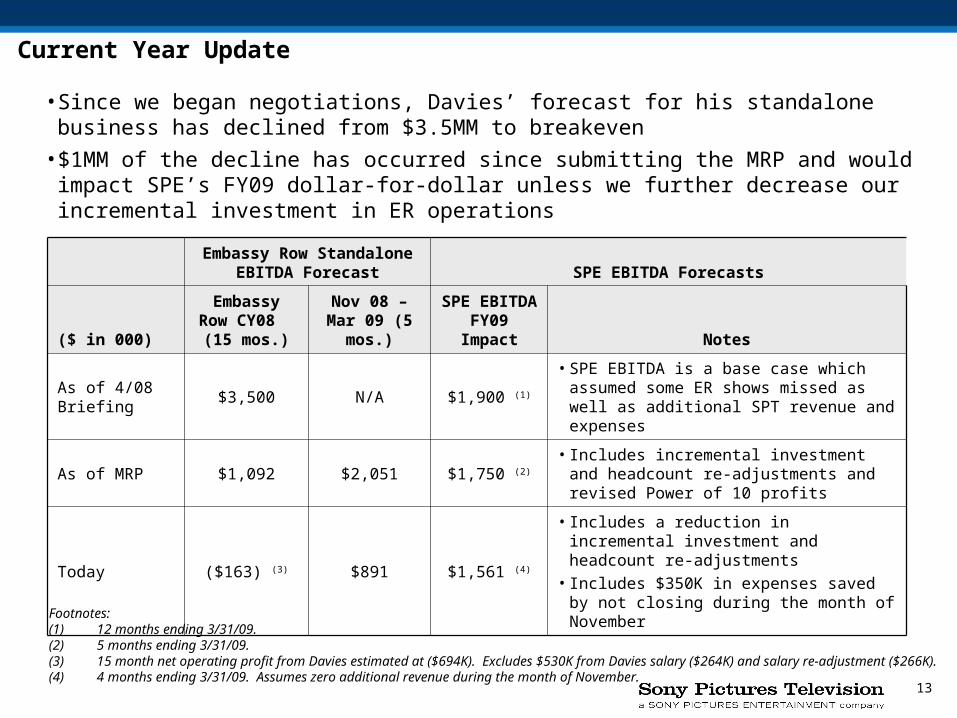

Current Year Update

Embassy Row Standalone EBITDA Forecast SPE EBITDA Forecasts

($ in 000)

Embassy Row CY08 (15 mos.)

Nov 08 – Mar 09 (5 mos.)

SPE EBITDA FY09 Impact Notes

As of 4/08 Briefing

$3,500 N/A $1,900 (1)

• SPE EBITDA is a base case which assumed some ER shows missed as well as additional SPT revenue and expenses

As of MRP $1,092 $2,051 $1,750 (2)

• Includes incremental investment and headcount re-adjustments and revised Power of 10 profits

Today ($163) (3) $891 $1,561 (4)

• Includes a reduction in incremental investment and headcount re-adjustments

• Includes $350K in expenses saved by not closing during the month of November

Footnotes:(1) 12 months ending 3/31/09.(2) 5 months ending 3/31/09.(3) 15 month net operating profit from Davies estimated at ($694K). Excludes $530K from Davies salary ($264K) and salary re-adjustment ($266K).(4) 4 months ending 3/31/09. Assumes zero additional revenue during the month of November.

• Since we began negotiations, Davies’ forecast for his standalone business has declined from $3.5MM to breakeven

• $1MM of the decline has occurred since submitting the MRP and would impact SPE’s FY09 dollar-for-dollar unless we further decrease our incremental investment in ER operations

14

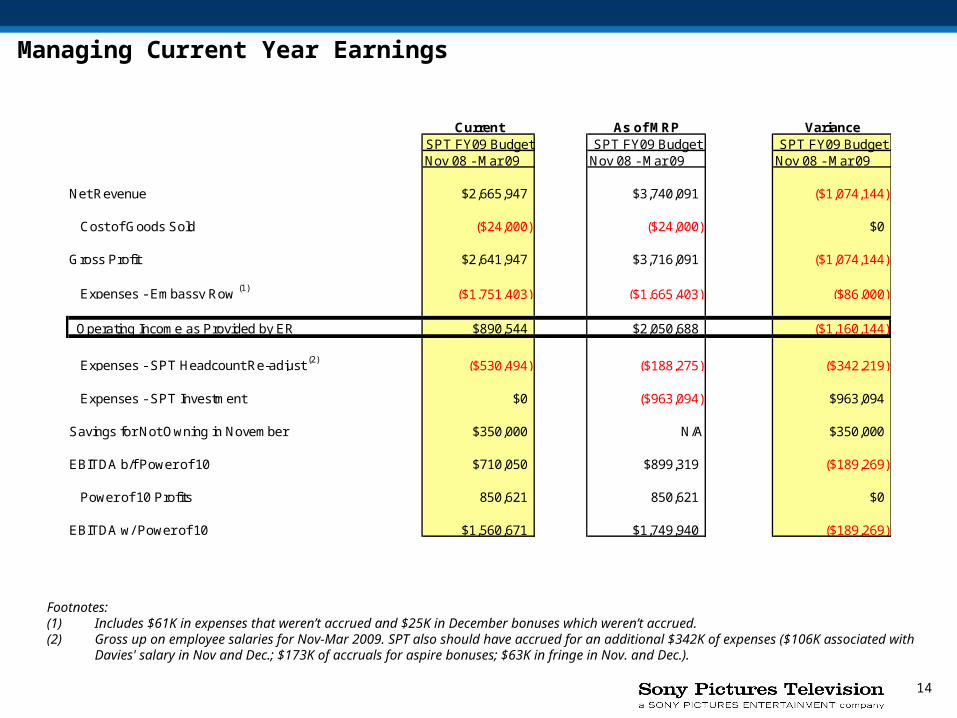

Managing Current Year Earnings

Footnotes:(1) Includes $61K in expenses that weren’t accrued and $25K in December bonuses which weren’t accrued.(2) Gross up on employee salaries for Nov-Mar 2009. SPT also should have accrued for an additional $342K of expenses ($106K associated

with Davies' salary in Nov and Dec.; $173K of accruals for aspire bonuses; $63K in fringe in Nov. and Dec.).

Current As of MRP VarianceSPT FY09 Budget SPT FY09 Budget SPT FY09 BudgetNov 08 - Mar 09 Nov 08 - Mar 09 Nov 08 - Mar 09

Net Revenue $2,665,947 $3,740,091 ($1,074,144)

Cost of Goods Sold ($24,000) ($24,000) $0

Gross Profit $2,641,947 $3,716,091 ($1,074,144)

Expenses - Embassy Row (1) ($1,751,403) ($1,665,403) ($86,000)

Operating Income as Provided by ER $890,544 $2,050,688 ($1,160,144)

Expenses - SPT Headcount Re-adjust (2) ($530,494) ($188,275) ($342,219)

Expenses - SPT Investment $0 ($963,094) $963,094

Savings for Not Owning in November $350,000 N/A $350,000

EBITDA b/f Power of 10 $710,050 $899,319 ($189,269)

Power of 10 Profits 850,621 850,621 $0

EBITDA w/ Power of 10 $1,560,671 $1,749,940 ($189,269)

15

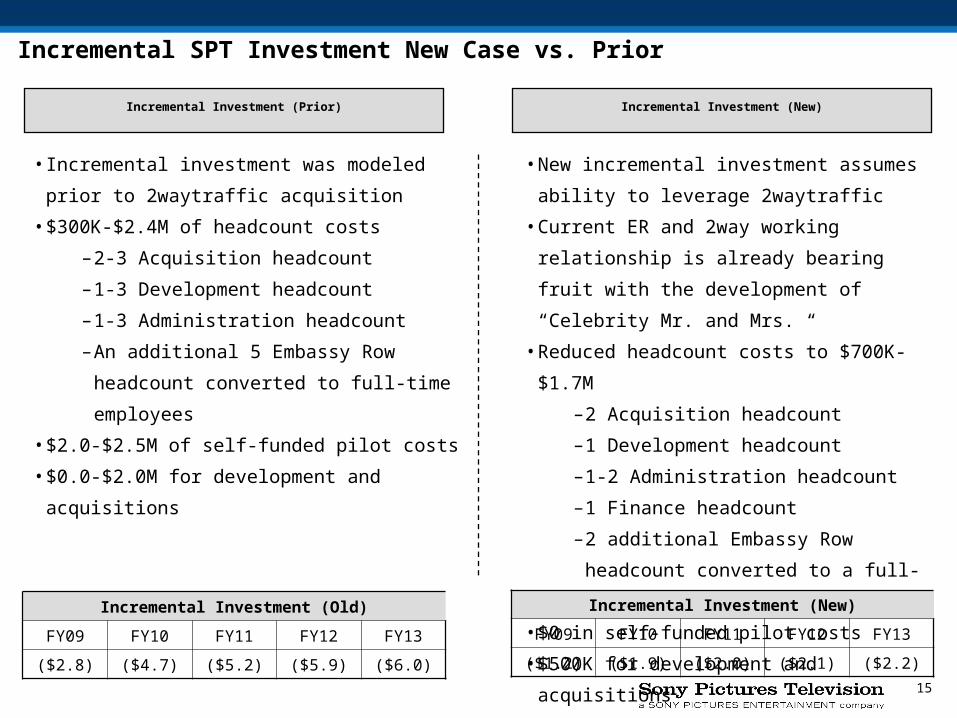

Incremental SPT Investment New Case vs. Prior

Incremental Investment (New)Incremental Investment (Prior)

• New incremental investment assumes ability to

leverage 2waytraffic

• Current ER and 2way working relationship is

already bearing fruit with the development of

“Celebrity Mr. and Mrs. “

• Reduced headcount costs to $700K-$1.7M

–2 Acquisition headcount

–1 Development headcount

–1-2 Administration headcount

–1 Finance headcount

–2 additional Embassy Row headcount

converted to a full-time employees

• $0 in self-funded pilot costs

• $500K for development and acquisitions

• Incremental investment was modeled prior to

2waytraffic acquisition

• $300K-$2.4M of headcount costs

–2-3 Acquisition headcount

–1-3 Development headcount

–1-3 Administration headcount

–An additional 5 Embassy Row headcount

converted to full-time employees

• $2.0-$2.5M of self-funded pilot costs

• $0.0-$2.0M for development and acquisitions

Incremental Investment (Old)

FY09 FY10 FY11 FY12 FY13

($2.8) ($4.7) ($5.2) ($5.9) ($6.0)

Incremental Investment (New)

FY09 FY10 FY11 FY12 FY13

($1.2) ($1.9) ($2.0) ($2.1) ($2.2)