Embed Size (px)

Citation preview

Conference Call

Santander Acquiring /

Conta Integrada

São Paulo, 18th March of 2010

2Positive Macroeconomic Scenario

Favorable economic conditions for the development of Cards industry

GDP (yoy growth %)

Inflation under control

Unemployment Rate (%)

Lula 2Lula 1FHC 2FHC 1

Investment

Grade

11.5

9.8 10.09.3

7.9 8.17.4

2004 2005 2006 2007 2008 2009 2010 (e)

4.9%4.3%5.9%4.5%3.1%

5.7%7.6%9.3%12.5%

7.7%6.0%8.9%

1.7%5.2%

9.6%22.5%

916.4%

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

Source: IBGE

Source: IPCA-IBGE & Central Bank of Brazil Consensus

Source: IBGE

3

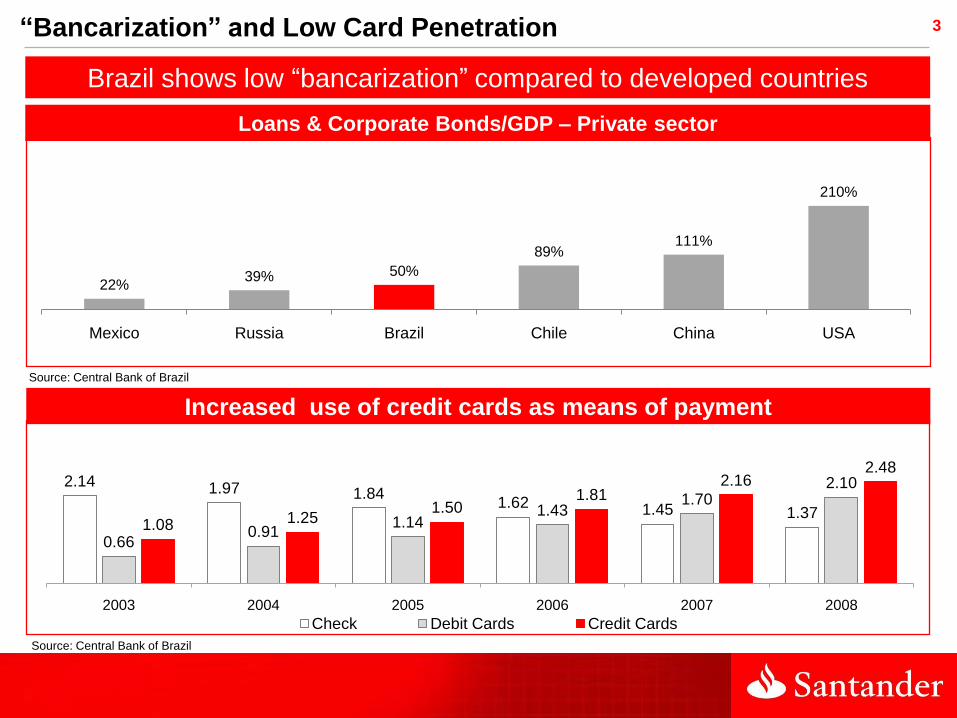

Brazil shows low “bancarization” compared to developed countries

Loans & Corporate Bonds/GDP – Private sector

“Bancarization” and Low Card Penetration

EUA

Reino Unido

Brasil

França

México

Source: Central Bank of Brazil

2.14 1.97 1.841.62 1.45 1.37

0.660.91

1.141.43

1.702.10

1.08 1.251.50

1.812.16

2.48

2003 2004 2005 2006 2007 2008

Check Debit Cards Credit Cards

Increased use of credit cards as means of payment

Source: Central Bank of Brazil

22%39% 50%

89%111%

210%

Mexico Russia Brazil Chile China USA

4

47%43%

34%

Canada United Kingdom USA

12.4% 14.0% 15.8% 17.1% 19.1% 21.4%

2003 2004 2005 2006 2007 2008

Higher utilization of cards in private consumption

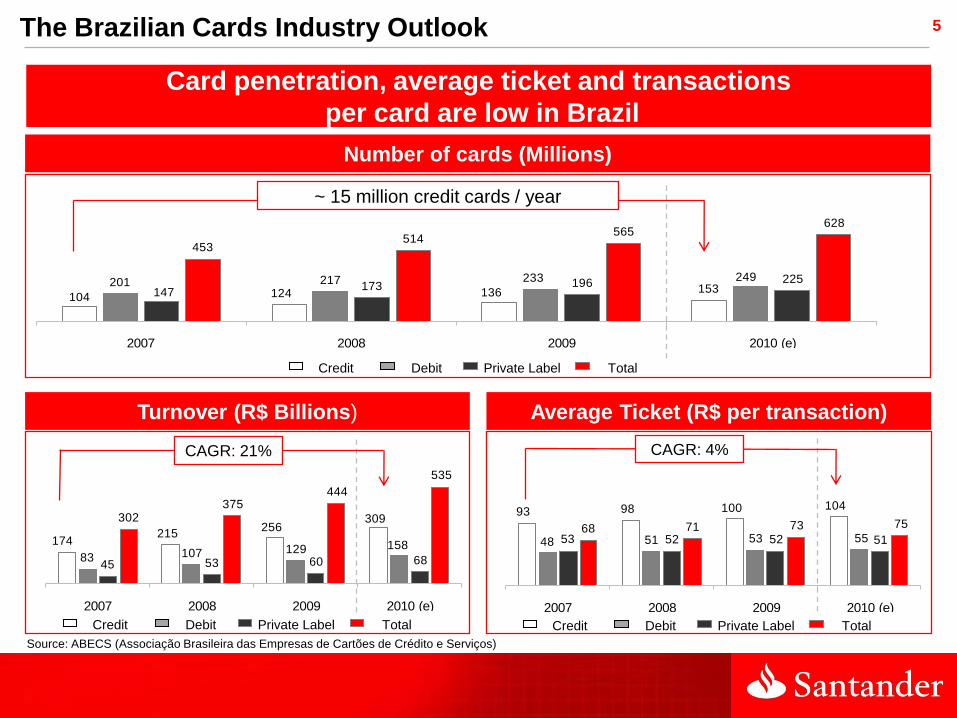

The Brazilian Cards Industry Outlook

Source : Abecs e IBGE

...but below developed countries

Source: ABECS, Bank of International Settlements,(2007) United Nations, IBGE

2X

5

104 124 136 153201 217 233 249

147173 196 225

453514

565628

2007 2008 2009 2010 (e)

93 98 100 104

48 51 53 5553 52 52 5168 71 73 75

2007 2008 2009 2010 (e)

Source: ABECS (Associação Brasileira das Empresas de Cartões de Crédito e Serviços)

Card penetration, average ticket and transactions

per card are low in Brazil

Number of cards (Millions)

Turnover (R$ Billions) Average Ticket (R$ per transaction)

174215

256309

83 107 129 158

45 53 60 68

302375

444

535

2007 2008 2009 2010 (e)

Credit Debit Private Label Total

The Brazilian Cards Industry Outlook

Credit Debit Private Label Total Credit Debit Private Label Total

~ 15 million credit cards / year

CAGR: 21% CAGR: 4%

6Participants of Cards Industry

Issuers

Merchants

Captures and

processes transactions

Issues credit and

debit cards

Use credit and debit

cards

Clients

Acquirers

Sets rules for

issuers and

acquirers

Card Brands

7

Santander

Santander + Acquiring Partners

Colombia

Argentina

Sovereign

Puerto RicoUK

Totta

Spain

Portugal

Mexico

Santander’s Experience in Other Countries

8

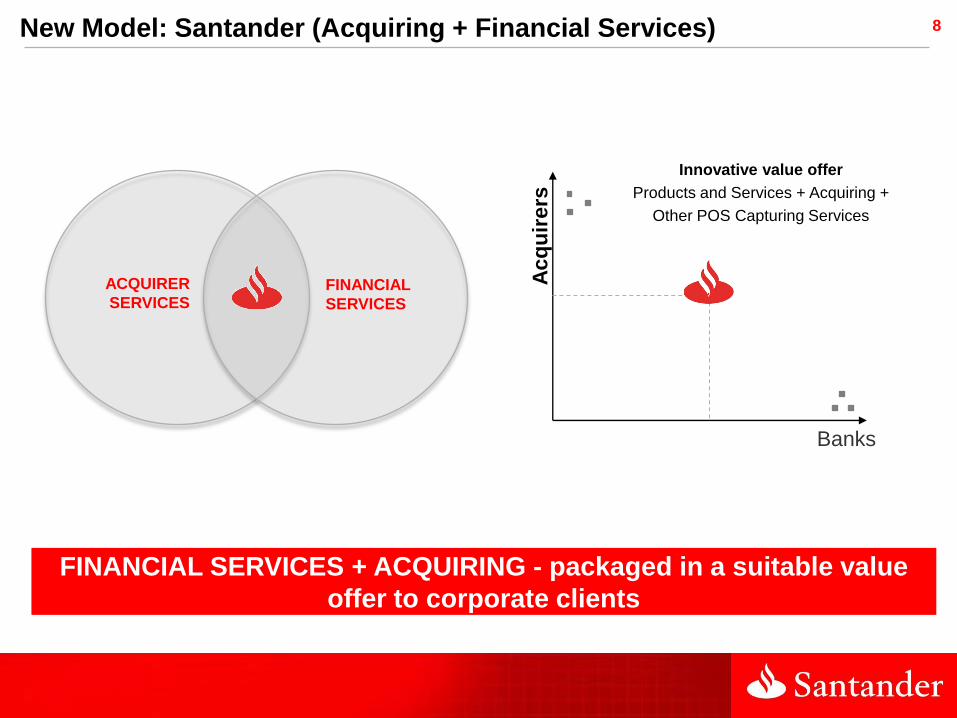

FINANCIAL SERVICES + ACQUIRING - packaged in a suitable value

offer to corporate clients

New Model: Santander (Acquiring + Financial Services)

Acq

uir

ers

Innovative value offer

Products and Services + Acquiring +

Other POS Capturing Services

Banks

ACQUIRER

SERVICESFINANCIAL

SERVICES

9

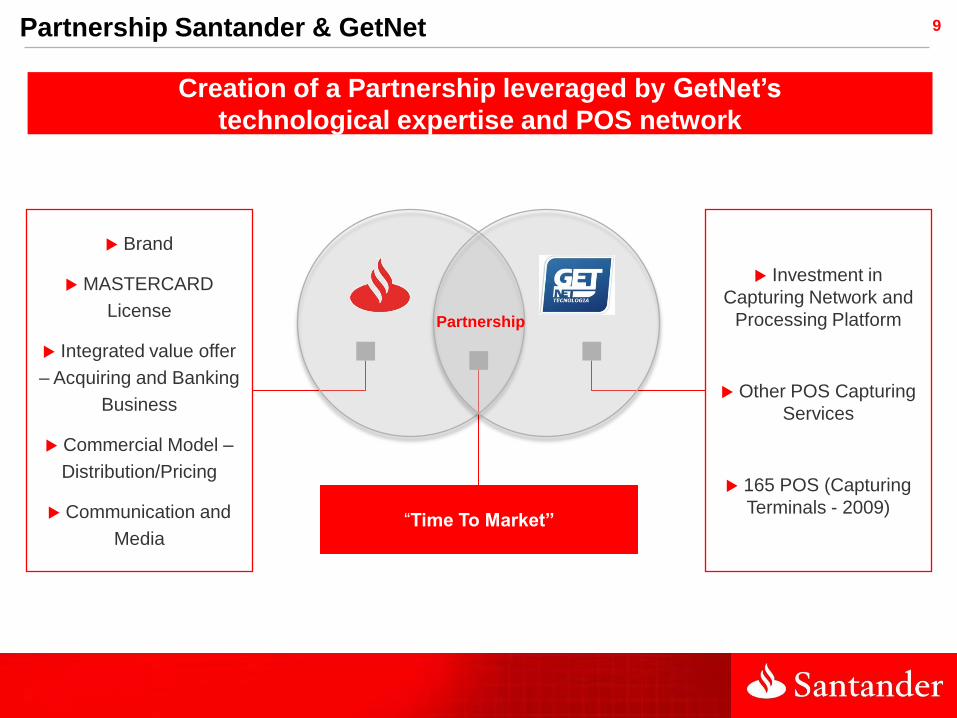

Brand

MASTERCARD

License

Integrated value offer

– Acquiring and Banking

Business

Commercial Model –

Distribution/Pricing

Communication and

Media

Investment in

Capturing Network and

Processing Platform

Other POS Capturing

Services

165 POS (Capturing

Terminals - 2009)

Partnership

Partnership Santander & GetNet

Creation of a Partnership leveraged by GetNet’s

technological expertise and POS network

“Time To Market”

10

Technological Platform for capturing,

authorizing and the processing of

transactions

165 thousand POS

Services at Capturing Terminals:

- Mobile Recharge

- “Vale Transporte” (transportation ticket)

Recharge

- “PAT Alimentação e Refeição” (meal ticket)

- “Cartão Convênio” / Private Label / Cobrand

GETNET TECNOLOGIA

Campo Bom – RS

CORREA DA SILVA GROUP

Domestic Capital

N&SP – Network and Service Provider

Customized solutions for capturing, authorization and processing of

transactions and information

Main Clients: Goodcard, Banco BNG, Serasa, Microsoft, Base Card, Wal-

Mart, Brasil Telecom, Claro, Tim, Vivo, Telefonica, Oi, Embratel, CTBC,

Amazonia Celular, Banco Matone, etc.

Over 800 employees

Annual turnover of R$ 2,29 Bn (2009)

GetNet Tecnologia

Entrance in the Acquirer industry through a technological

partner - GetNet Tecnologia

11Santander as Issuer and Acquirer

Issuer

Merchant

Issues credit and

debit cards

Uses credit and

debit cards

Clients

Acquirers

Sets rules for

issuers and

acquirers

Captures and processes

transactions

Card Brand

12

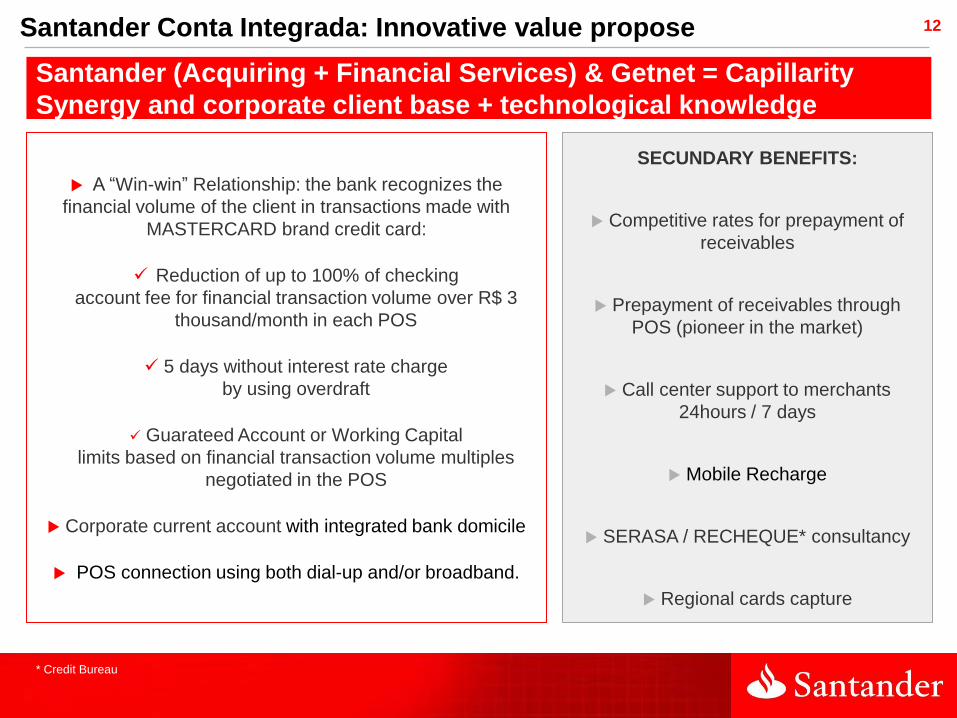

SECUNDARY BENEFITS:

Competitive rates for prepayment of

receivables

Prepayment of receivables through

POS (pioneer in the market)

Call center support to merchants

24hours / 7 days

Mobile Recharge

SERASA / RECHEQUE* consultancy

Regional cards capture

A “Win-win” Relationship: the bank recognizes the

financial volume of the client in transactions made with

MASTERCARD brand credit card:

Reduction of up to 100% of checking

account fee for financial transaction volume over R$ 3

thousand/month in each POS

5 days without interest rate charge

by using overdraft

Guarateed Account or Working Capital

limits based on financial transaction volume multiples

negotiated in the POS

Corporate current account with integrated bank domicile

POS connection using both dial-up and/or broadband.

Santander Conta Integrada: Innovative value propose

Santander (Acquiring + Financial Services) & Getnet = Capillarity

Synergy and corporate client base + technological knowledge

* Credit Bureau

13Santander Conta Integrada: products offering engine for companies

Besides seizing the value of a high

profitability business, it also provides:

Higher transaction financial volume from

corporate clients.

Loan portfolio growth mitigating the risks.

Increase of corporate client base and

improvement of the competitive market position.

Improvement on the relationship with

corporate customers and, consequently, increase

of number of products and services per client.

Be the first bank of our corporate client.

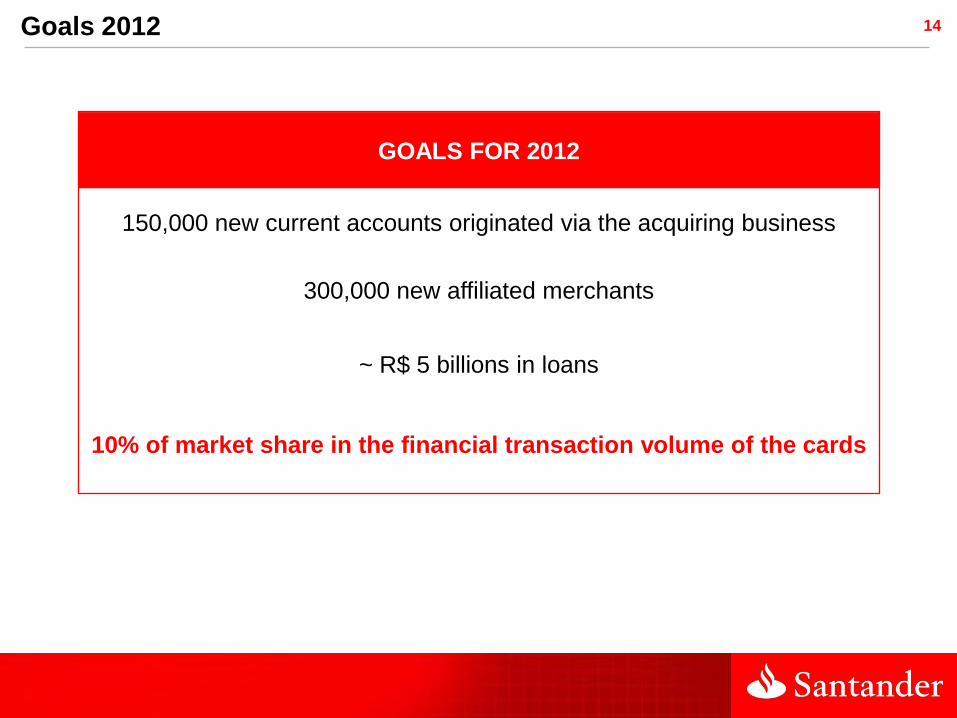

14Goals 2012

GOALS FOR 2012

150,000 new current accounts originated via the acquiring business

300,000 new affiliated merchants

~ R$ 5 billions in loans

10% of market share in the financial transaction volume of the cards

15Conclusion

Santander is the pioneer in launching this acquiring model in

Brazil

The partnership provides the bank access to a network of more

than 160,000 merchants and to GetNet’s know how

The credit card industry is expected to grow around ~20% p.y.

and double its size in 4 years

This strategy focuses on strengthening the relationship with

SME clients – main competitors are banks

Santander Conta Integrada – “Win-Win” relationship between

the bank and small and middle market companies (SMEs)

Investor Relations

Avenida Juscelino Kubitschek, 2,235, 10th floor

São Paulo | SP | Brazil | 04543-011

Tel. (55 11) 3553-3300

e-mail: [email protected]