Embed Size (px)

Citation preview

Conference call First nine months of fiscal year 2014 »

Karlsruhe, 11 November 2014Thomas Kusterer, Chief Financial OfficerIngo Peter Voigt, Senior Vice President, Head of Finance / Investor Relations

EnBW EnergieBaden-Württemberg AG

Important note

2Conference Call on the first nine months of fiscal year 2014, 11 November 2014

Unless indicated otherwise, all data contained hereinafter refers to the EnBW group and is calculated according to IFRS.

No offer or investment recommendation

This presentation has been prepared for information purposes only. It does not constitute an offer, an invitation or a recommendation to purchase or sell securities issued by EnBW Energie Baden-Württemberg AG (EnBW), a company of the EnBW group or any other company. This presentation does not constitute a request, instruction or recommendation to vote or give consent. All descriptions, examples and calculations are included in this presentation for illustration purposes only.

Future-oriented statements

This presentation contains future-oriented statements that are based on current assumptions, plans, estimates and forecasts of the management of EnBW. Such future-oriented statements are therefore only valid at the time at which they are published for the first time. Future-oriented statements are indicated by the context, but may also be

identified by the use of the words “may”, “will”, “should”, “plans”, “intends”, “expects”, “believes”, “assumes”, “forecasts”, “potentially” or “continued” and similar expressions.

By nature, future-oriented statements are subject to risks and uncertainties that cannot be controlled or accurately predicted by EnBW. Actual events, future results, the financial position, development or performance of EnBWand the companies of the EnBW group may therefore diverge considerably from the future-oriented statements made in this presentation. Therefore it cannot be guaranteed nor can any liability be assumed otherwise that these future-oriented statements will prove complete, correct or precise or that expected and forecast results will actually occur in the future.

No obligation to update the information

EnBW assumes no obligation of any kind to update the information contained in this presentation or to adjust or update future-oriented statements to future events or developments.

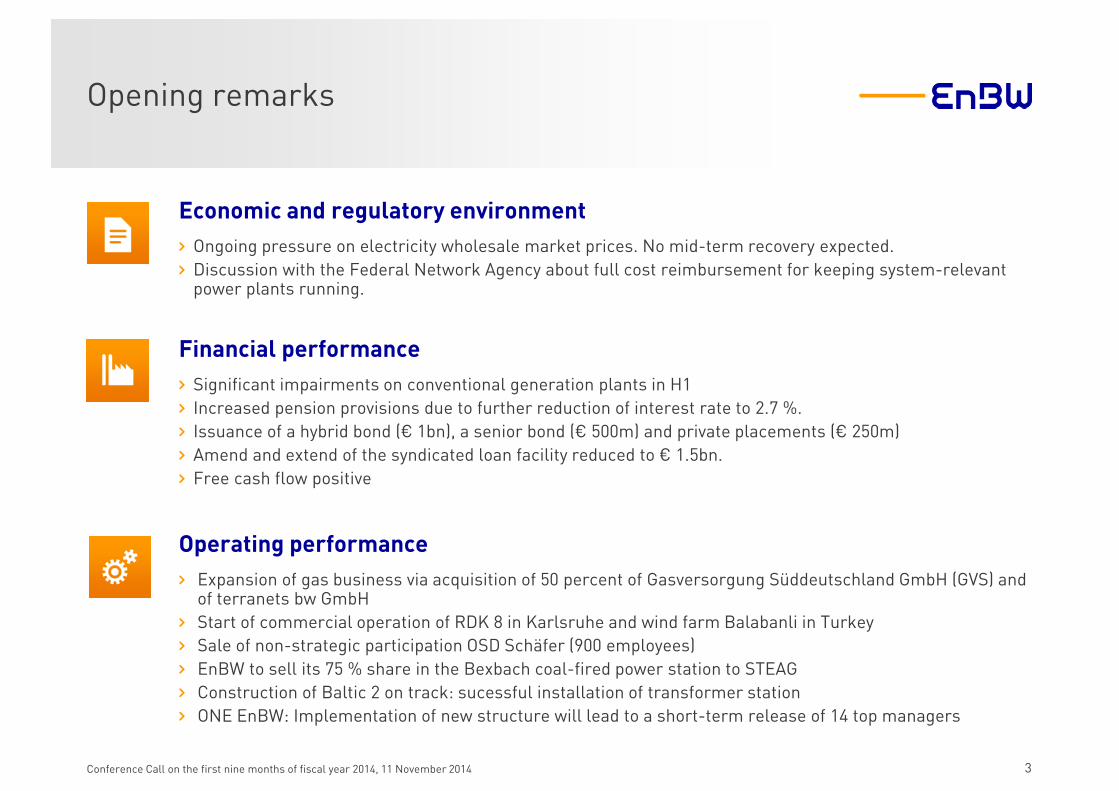

Opening remarks

3Conference Call on the first nine months of fiscal year 2014, 11 November 2014

Economic and regulatory environment

› Ongoing pressure on electricity wholesale market prices. No mid-term recovery expected.

› Discussion with the Federal Network Agency about full cost reimbursement for keeping system-relevant power plants running.

Financial performance

› Significant impairments on conventional generation plants in H1

› Increased pension provisions due to further reduction of interest rate to 2.7 %.

› Issuance of a hybrid bond (€ 1bn), a senior bond (€ 500m) and private placements (€ 250m)

› Amend and extend of the syndicated loan facility reduced to € 1.5bn.

› Free cash flow positive

Operating performance

› Expansion of gas business via acquisition of 50 percent of Gasversorgung Süddeutschland GmbH (GVS) andof terranets bw GmbH

› Start of commercial operation of RDK 8 in Karlsruhe and wind farm Balabanli in Turkey

› Sale of non-strategic participation OSD Schäfer (900 employees)

› EnBW to sell its 75 % share in the Bexbach coal-fired power station to STEAG

› Construction of Baltic 2 on track: sucessful installation of transformer station

› ONE EnBW: Implementation of new structure will lead to a short-term release of 14 top managers

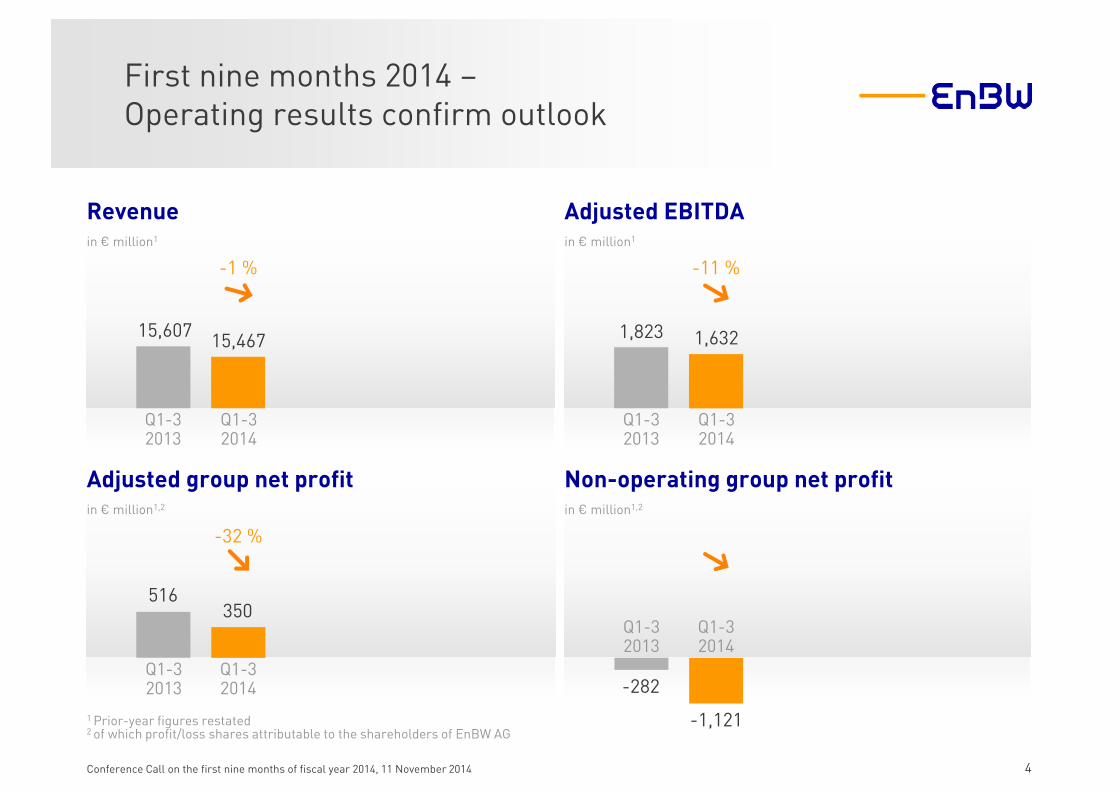

Non-operating group net profit in € million1,2

Revenue in € million1

Adjusted EBITDA in € million1

Adjusted group net profitin € million1,2

First nine months 2014 –Operating results confirm outlook

4Conference Call on the first nine months of fiscal year 2014, 11 November 2014

-32 %

Q1-32014

Q1-32013

Q1-3 2014

Q1-3 2013

-282

-1,1211 Prior-year figures restated2 of which profit/loss shares attributable to the shareholders of EnBW AG

Q1-3 2014

Q1-3 2013

15,60715,467 1,823 1,632

516350

Q1-3 2014

Q1-32013

-1 % -11 %

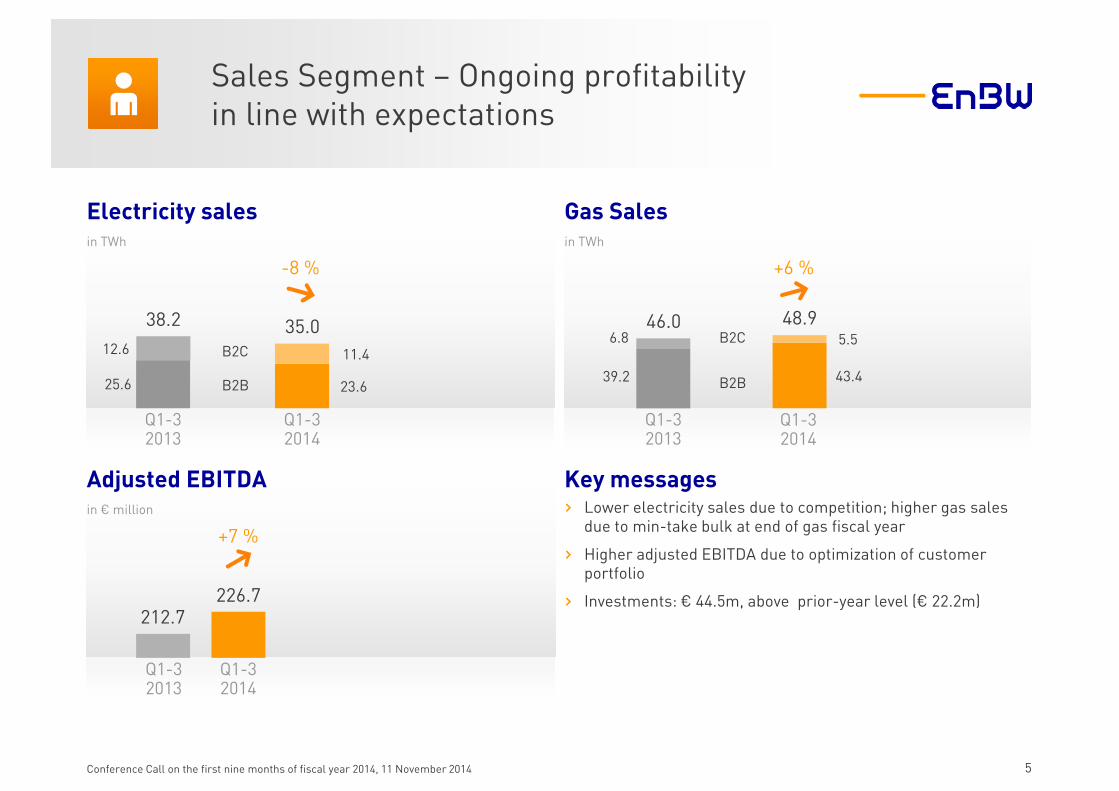

Electricity sales in TWh

Gas Salesin TWh

Adjusted EBITDA in € million

Sales Segment – Ongoing profitabilityin line with expectations

5Conference Call on the first nine months of fiscal year 2014, 11 November 2014

38.2 35.0

212.7226.7

46.0 48.9

12.6

25.6

11.4

23.639.2

6.8

43.4

5.5

Q1-32014

Q1-3 2014

B2C

B2B

B2C

B2B

› Lower electricity sales due to competition; higher gas sales due to min-take bulk at end of gas fiscal year

› Higher adjusted EBITDA due to optimization of customer portfolio

› Investments: € 44.5m, above prior-year level (€ 22.2m)

Key messages

Q1-32014

Q1-32013

+7 %

-8 %

Q1-3 2013

+6 %

Q1-3 2013

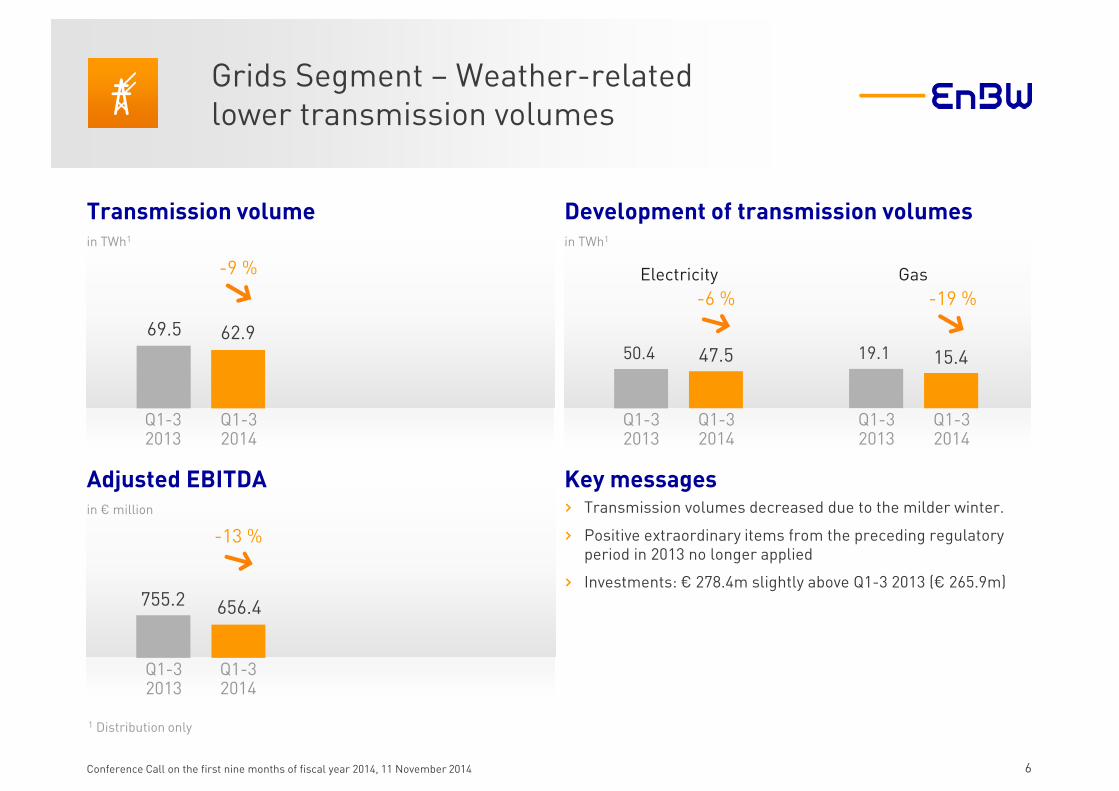

Transmission volume in TWh1

Development of transmission volumesin TWh1

Adjusted EBITDA in € million

1 Distribution only

69.5 62.9

Grids Segment – Weather-related lower transmission volumes

6Conference Call on the first nine months of fiscal year 2014, 11 November 2014

755.2 656.4

19.150.4 15.447.5

Electricity Gas

› Transmission volumes decreased due to the milder winter.

› Positive extraordinary items from the preceding regulatory period in 2013 no longer applied

› Investments: € 278.4m slightly above Q1-3 2013 (€ 265.9m)

Key messages

Q1-32014

Q1-32013

Q1-3 2014

Q1-3 2013

Q1-3 2014

Q1-3 2013

-9 %

-6 % -19 %

Q1-3 2014

Q1-3 2013

-13 %

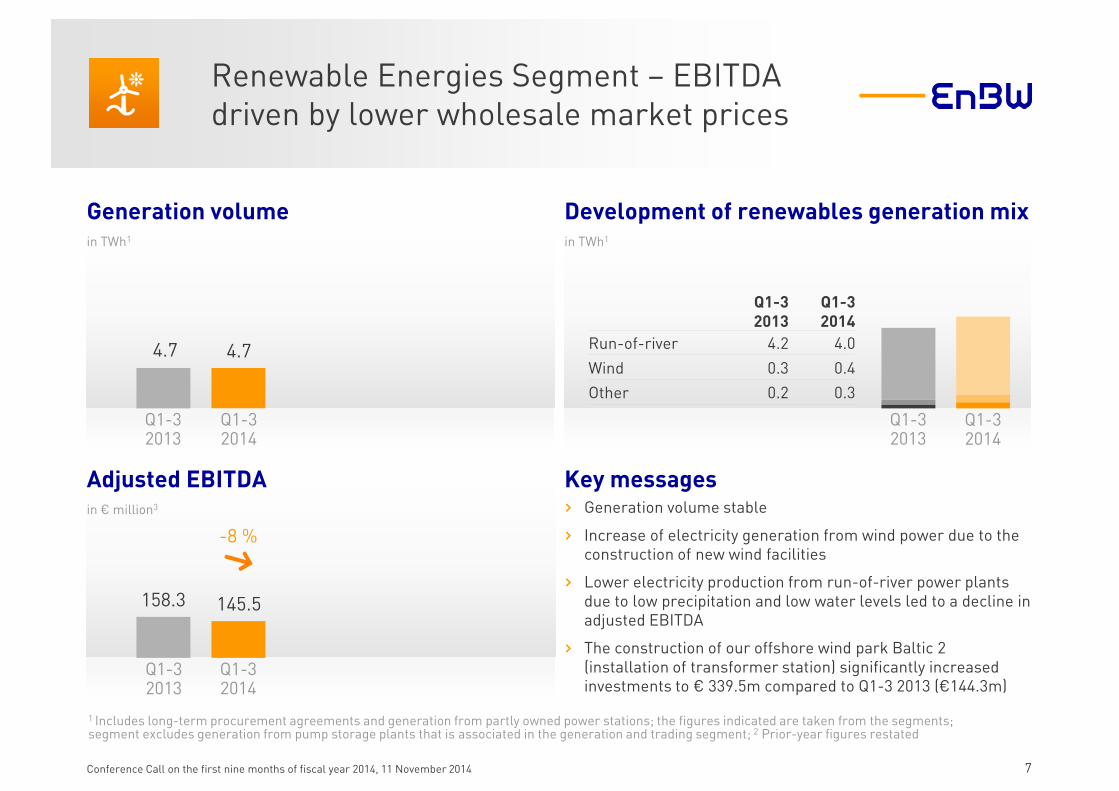

Generation volume in TWh1

Development of renewables generation mixin TWh1

Adjusted EBITDA in € million3

1 Includes long-term procurement agreements and generation from partly owned power stations; the figures indicated are taken from the segments;segment excludes generation from pump storage plants that is associated in the generation and trading segment; 2 Prior-year figures restated

4.7 4.7

Renewable Energies Segment – EBITDA driven by lower wholesale market prices

7Conference Call on the first nine months of fiscal year 2014, 11 November 2014

158.3 145.5

Q1-32014

Q1-32013

› Generation volume stable

› Increase of electricity generation from wind power due to the construction of new wind facilities

› Lower electricity production from run-of-river power plants due to low precipitation and low water levels led to a decline in adjusted EBITDA

› The construction of our offshore wind park Baltic 2 (installation of transformer station) significantly increased investments to € 339.5m compared to Q1-3 2013 (€144.3m)

Key messages

Q1-32014

Q1-32013

-8 %

Q1-3 2014

Q1-3 2013

Q1-3 2013

Q1-3 2014

Run-of-river 4.2 4.0

Wind 0.3 0.4

Other 0.2 0.3

1 Includes long-term procurement agreements and generation from partly owned power stations; the figures indicated are taken from the segments2 Segment includes pump storage plants; 3 Prior-year figures restated

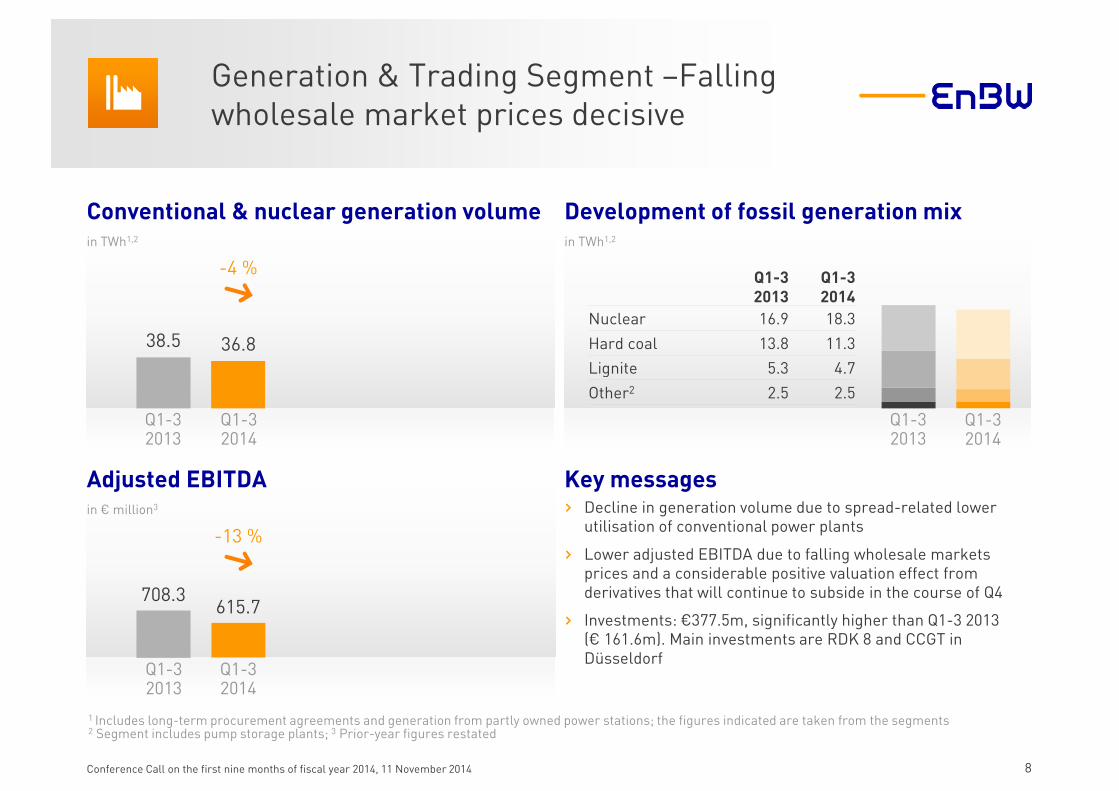

38.5 36.8

Generation & Trading Segment –Fallingwholesale market prices decisive

8Conference Call on the first nine months of fiscal year 2014, 11 November 2014

› Decline in generation volume due to spread-related lower utilisation of conventional power plants

› Lower adjusted EBITDA due to falling wholesale markets prices and a considerable positive valuation effect from derivatives that will continue to subside in the course of Q4

› Investments: €377.5m, significantly higher than Q1-3 2013(€ 161.6m). Main investments are RDK 8 and CCGT in Düsseldorf

708.3615.7

Q1-3 2013

Q1-3 2014

Nuclear 16.9 18.3

Hard coal 13.8 11.3

Lignite 5.3 4.7

Other2 2.5 2.5

Conventional & nuclear generation volume in TWh1,2

Development of fossil generation mixin TWh1,2

Adjusted EBITDA in € million3

Key messages

Q1-3 2014

Q1-3 2013

-4 %

Q1-32014

Q1-32013

Q1-32014

Q1-32013

-13 %

1 Prior-year figures restated

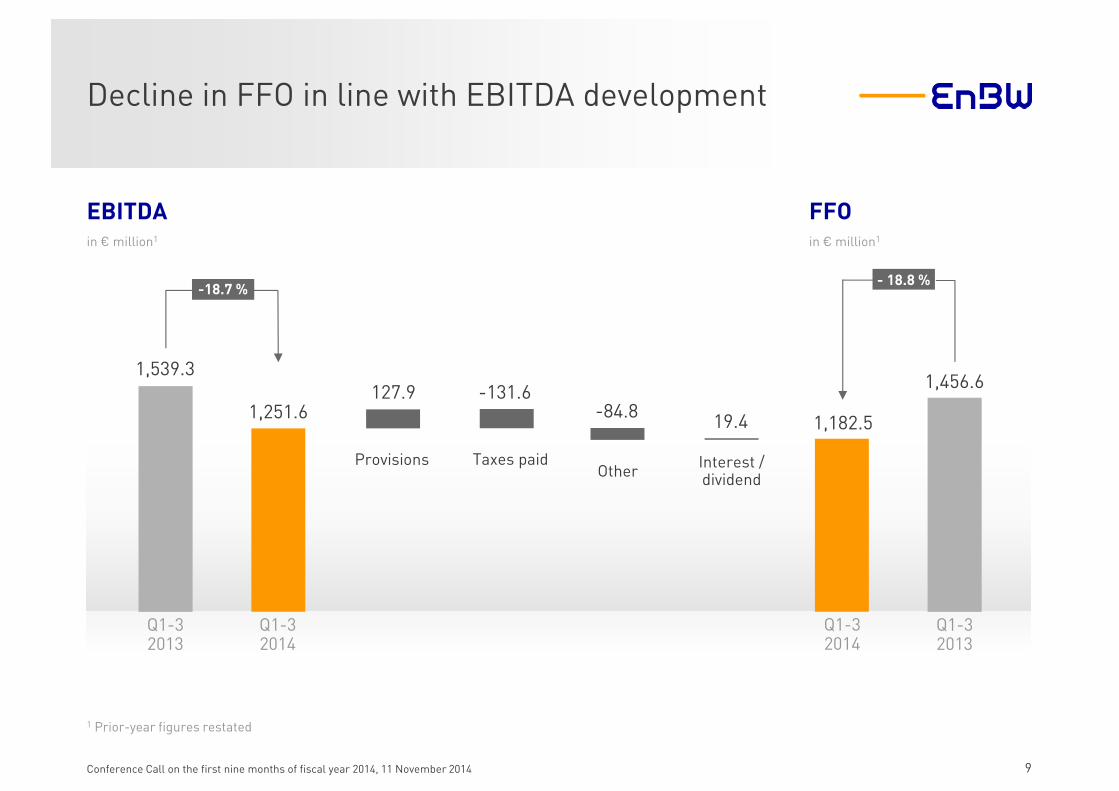

1,539.3

1,251.6

Decline in FFO in line with EBITDA development

9Conference Call on the first nine months of fiscal year 2014, 11 November 2014

Q1-3 2013

Q1-32014

ProvisionsOther

Interest /dividend

Taxes paid

1,182.5

1,456.6

- 18.8 %-18.7 %

127.9 -131.6-84.8

19.4

Q1-3 2014

Q1-3 2013

EBITDAin € million1

FFOin € million1

1 Prior-year figures restated; 2 For intangible assets and property, plant and equipment; 3 Cash received from disposals of intangible assets and property, plant and equipment, as well as cash received from construction costs and investment subsidies

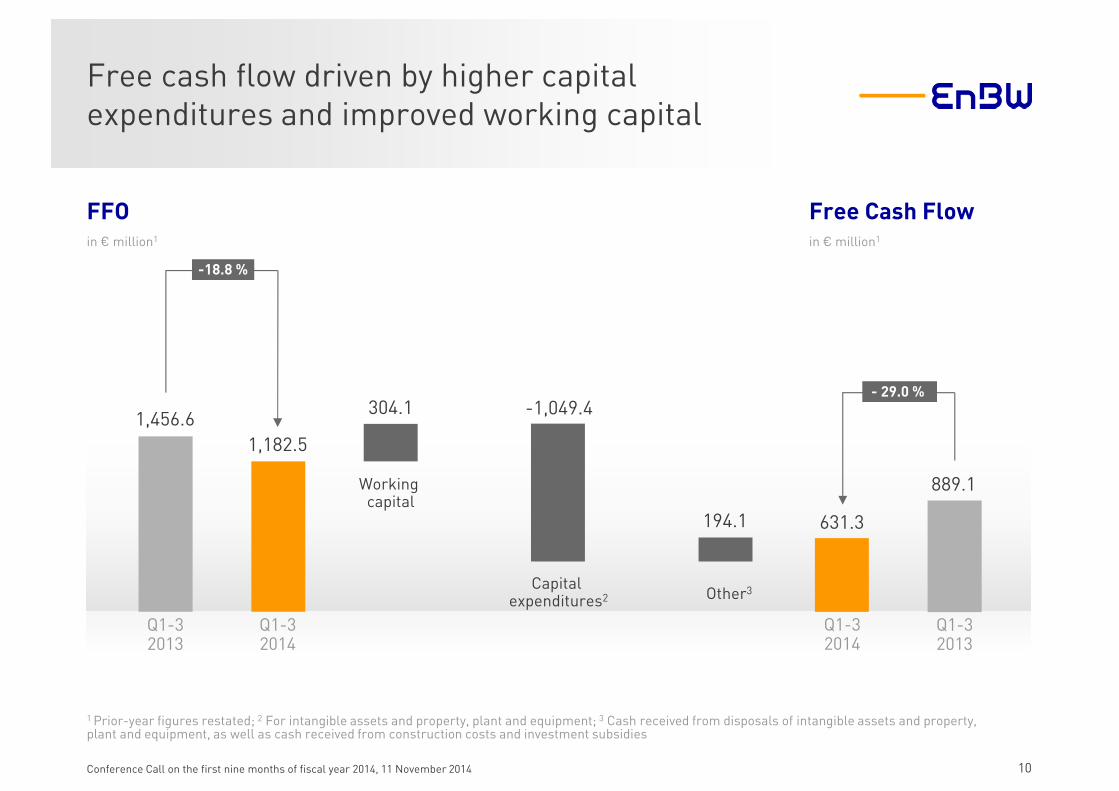

1,456.6

1,182.5

Free cash flow driven by higher capital expenditures and improved working capital

10Conference Call on the first nine months of fiscal year 2014, 11 November 2014

Working capital

Capital expenditures2 Other3

631.3

889.1

-18.8 %

304.1 -1,049.4

194.1

- 29.0 %

Q1-3 2013

Q1-3 2014

Q1-3 2014

Q1-3 2013

FFOin € million1

Free Cash Flowin € million1

1 Prior-year figures restated

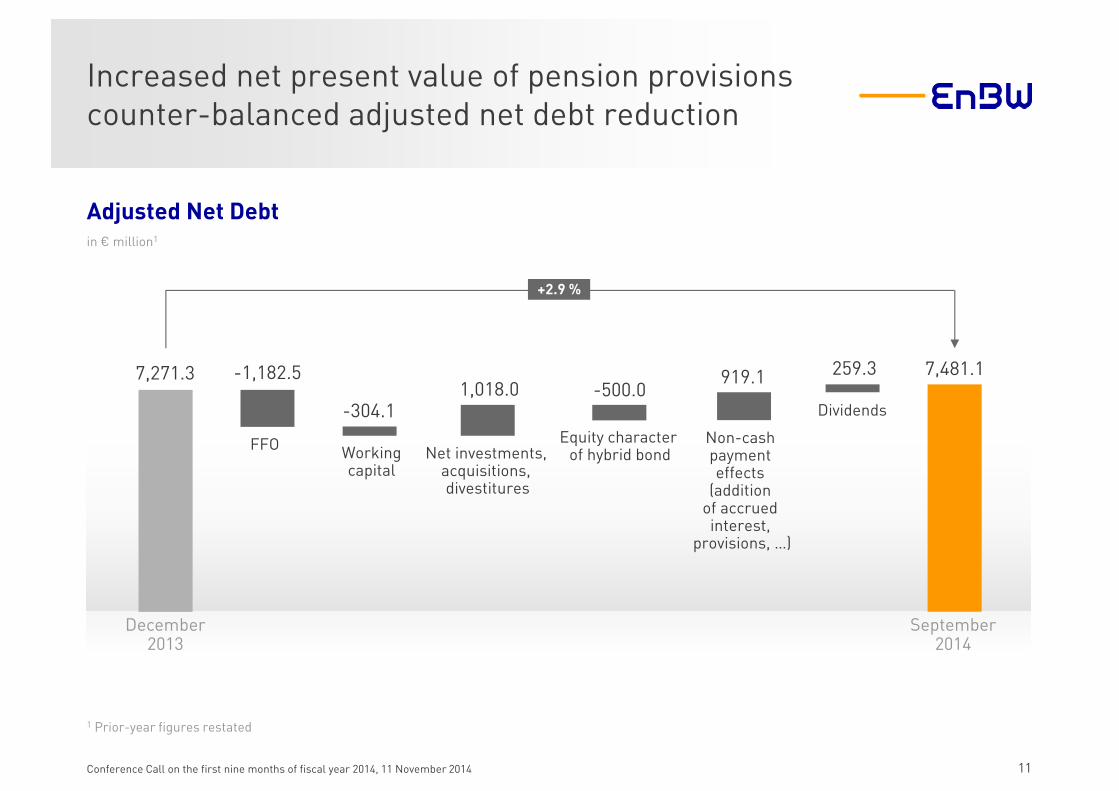

7,271.3 -1,182.5

Increased net present value of pension provisions counter-balanced adjusted net debt reduction

11Conference Call on the first nine months of fiscal year 2014, 11 November 2014

Workingcapital

Net investments, acquisitions, divestitures

Equity character of hybrid bond

919.1 7,481.1

+2.9 %

-304.11,018.0 -500.0

FFO Non-cash payment effects

(addition of accrued interest,

provisions, …)

December2013

September2014

Dividends

259.3

Adjusted Net Debtin € million1

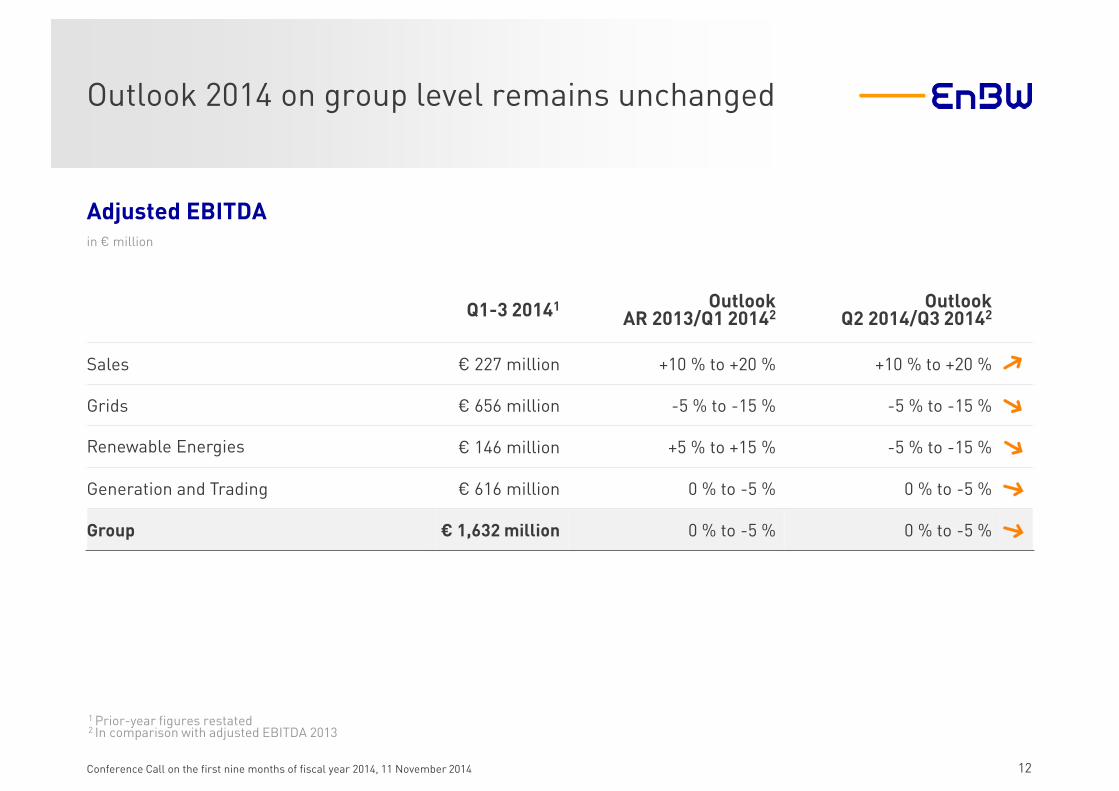

Outlook 2014 on group level remains unchanged

12Conference Call on the first nine months of fiscal year 2014, 11 November 2014

1 Prior-year figures restated 2 In comparison with adjusted EBITDA 2013

Q1-3 20141 Outlook AR 2013/Q1 20142

Outlook Q2 2014/Q3 20142

Sales € 227 million +10 % to +20 % +10 % to +20 %

Grids € 656 million -5 % to -15 % -5 % to -15 %

Renewable Energies € 146 million +5 % to +15 % -5 % to -15 %

Generation and Trading € 616 million 0 % to -5 % 0 % to -5 %

Group € 1,632 million 0 % to -5 % 0 % to -5 %

Adjusted EBITDAin € million

Conference Call on the first nine months of fiscal year 2014, 11 November 2014

Questions& Answers »

Appendix

14Conference Call on the first nine months of fiscal year 2014, 11 November 2014

› Additional information.................................................................... page 15

› Financial calendar............................................................................. page 23

› IR contacts ............................................................................................. page 24

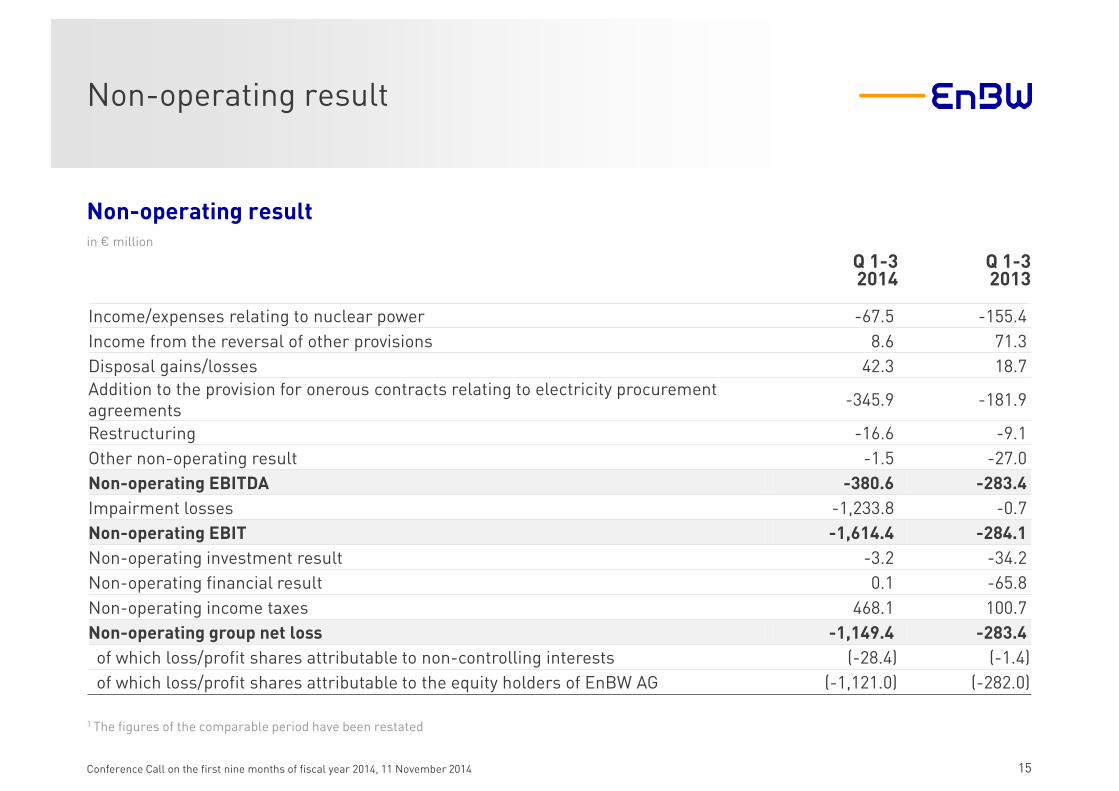

Non-operating result

15Conference Call on the first nine months of fiscal year 2014, 11 November 2014

1 The figures of the comparable period have been restated

Q 1-3 2014

Q 1-32013

Income/expenses relating to nuclear power -67.5 -155.4

Income from the reversal of other provisions 8.6 71.3

Disposal gains/losses 42.3 18.7

Addition to the provision for onerous contracts relating to electricity procurement agreements

-345.9 -181.9

Restructuring -16.6 -9.1

Other non-operating result -1.5 -27.0

Non-operating EBITDA -380.6 -283.4

Impairment losses -1,233.8 -0.7

Non-operating EBIT -1,614.4 -284.1

Non-operating investment result -3.2 -34.2

Non-operating financial result 0.1 -65.8

Non-operating income taxes 468.1 100.7

Non-operating group net loss -1,149.4 -283.4

of which loss/profit shares attributable to non-controlling interests (-28.4) (-1.4)

of which loss/profit shares attributable to the equity holders of EnBW AG (-1,121.0) (-282.0)

Non-operating resultin € million

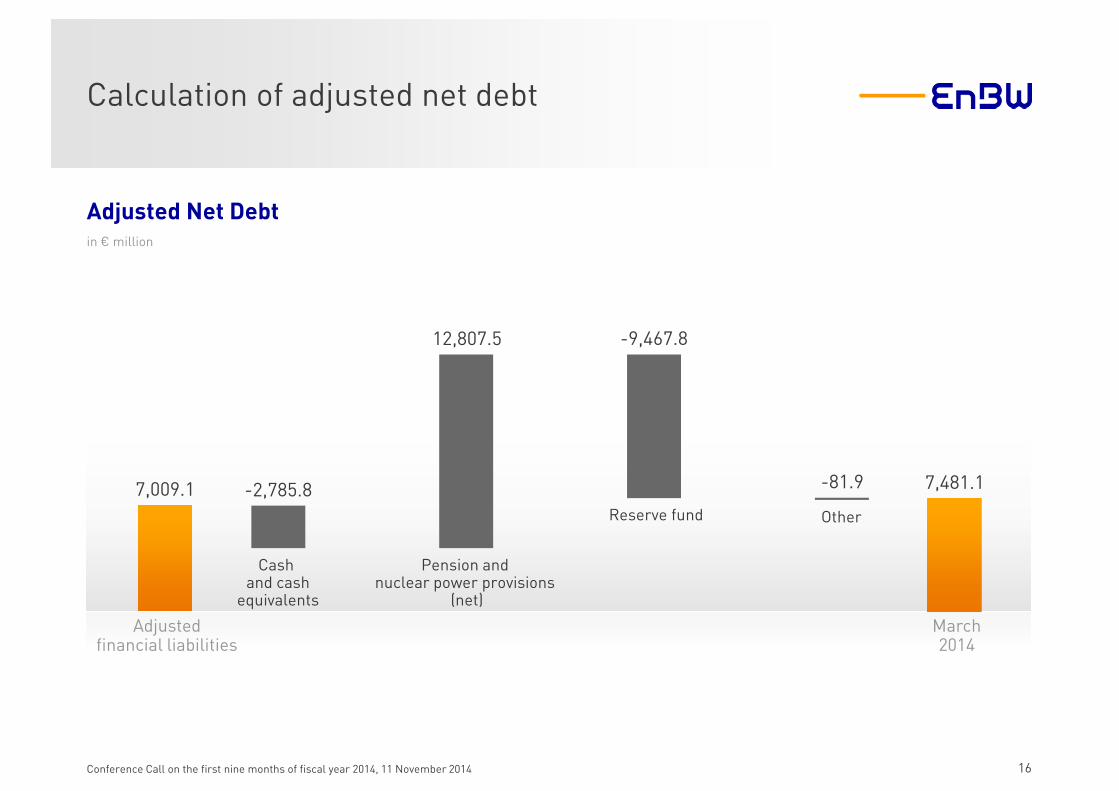

Other

7,009.1 -2,785.8

Calculation of adjusted net debt

16Conference Call on the first nine months of fiscal year 2014, 11 November 2014

Pension and nuclear power provisions

(net)

Reserve fund

-81.9 7,481.1

12,807.5 -9,467.8

Cash and cash

equivalents

Adjustedfinancial liabilities

March2014

Adjusted Net Debtin € million

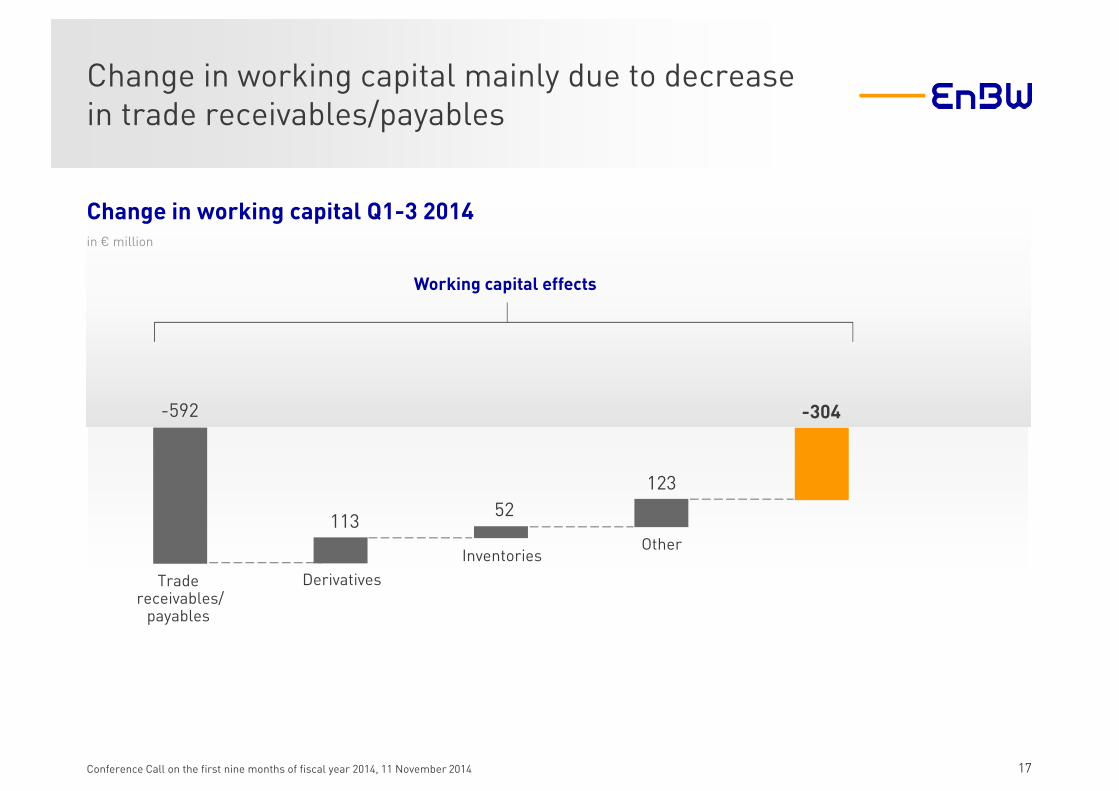

Change in working capital mainly due to decrease in trade receivables/payables

17Conference Call on the first nine months of fiscal year 2014, 11 November 2014

Working capital effects

Inventories

113

Derivatives

52

-304-592

Trade receivables/

payables

Other

123

Change in working capital Q1-3 2014in € million

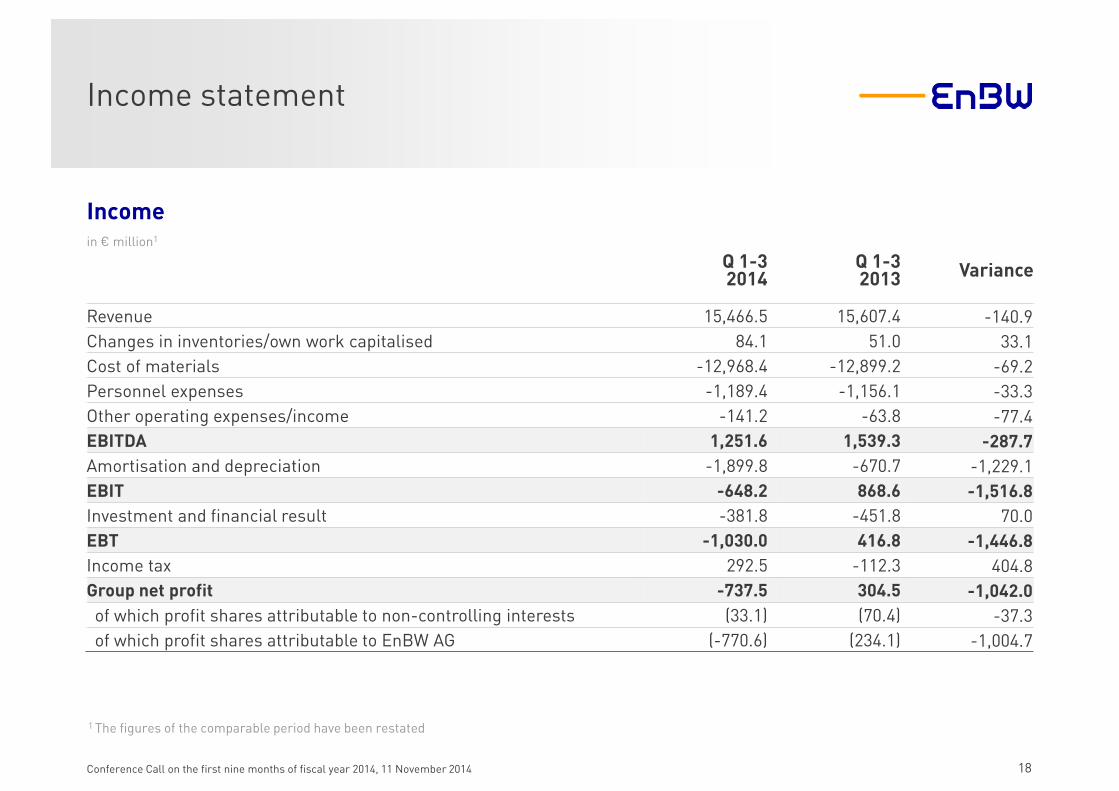

Income statement

18Conference Call on the first nine months of fiscal year 2014, 11 November 2014

1 The figures of the comparable period have been restated

Q 1-32014

Q 1-32013 Variance

Revenue 15,466.5 15,607.4 -140.9

Changes in inventories/own work capitalised 84.1 51.0 33.1

Cost of materials -12,968.4 -12,899.2 -69.2

Personnel expenses -1,189.4 -1,156.1 -33.3

Other operating expenses/income -141.2 -63.8 -77.4

EBITDA 1,251.6 1,539.3 -287.7

Amortisation and depreciation -1,899.8 -670.7 -1,229.1

EBIT -648.2 868.6 -1,516.8

Investment and financial result -381.8 -451.8 70.0

EBT -1,030.0 416.8 -1,446.8

Income tax 292.5 -112.3 404.8

Group net profit -737.5 304.5 -1,042.0

of which profit shares attributable to non-controlling interests (33.1) (70.4) -37.3

of which profit shares attributable to EnBW AG (-770.6) (234.1) -1,004.7

Incomein € million1

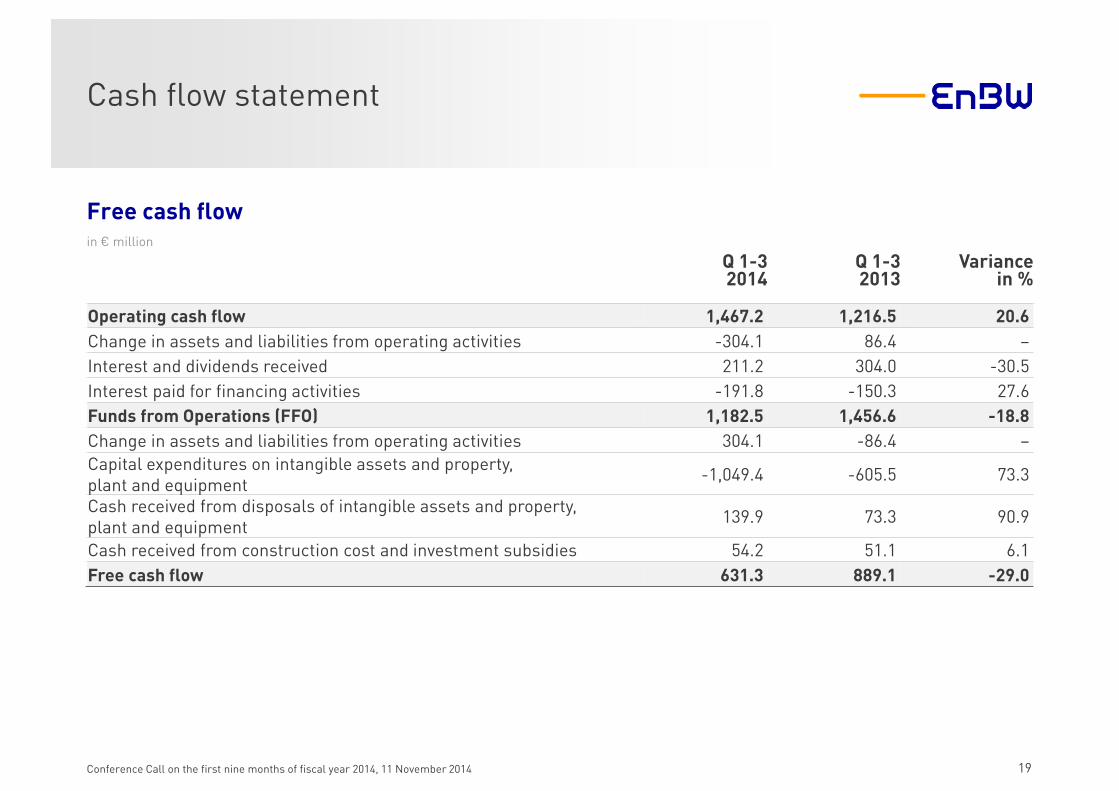

Cash flow statement

19Conference Call on the first nine months of fiscal year 2014, 11 November 2014

Q 1-32014

Q 1-32013

Variancein %

Operating cash flow 1,467.2 1,216.5 20.6

Change in assets and liabilities from operating activities -304.1 86.4 –

Interest and dividends received 211.2 304.0 -30.5

Interest paid for financing activities -191.8 -150.3 27.6

Funds from Operations (FFO) 1,182.5 1,456.6 -18.8

Change in assets and liabilities from operating activities 304.1 -86.4 –

Capital expenditures on intangible assets and property, plant and equipment

-1,049.4 -605.5 73.3

Cash received from disposals of intangible assets and property, plant and equipment

139.9 73.3 90.9

Cash received from construction cost and investment subsidies 54.2 51.1 6.1

Free cash flow 631.3 889.1 -29.0

Free cash flow in € million

1 As of 30 Septmber 2014

Hedge levels

20Conference Call on the first nine months of fiscal year 2014, 11 November 2014

10 %

20 %

30 %

40 %

50 %

60 %

70 %

80 %

90 %

100 %

2014

100 %

2015 2016

50 – 75 %

100 %

Hedge levels1

in %

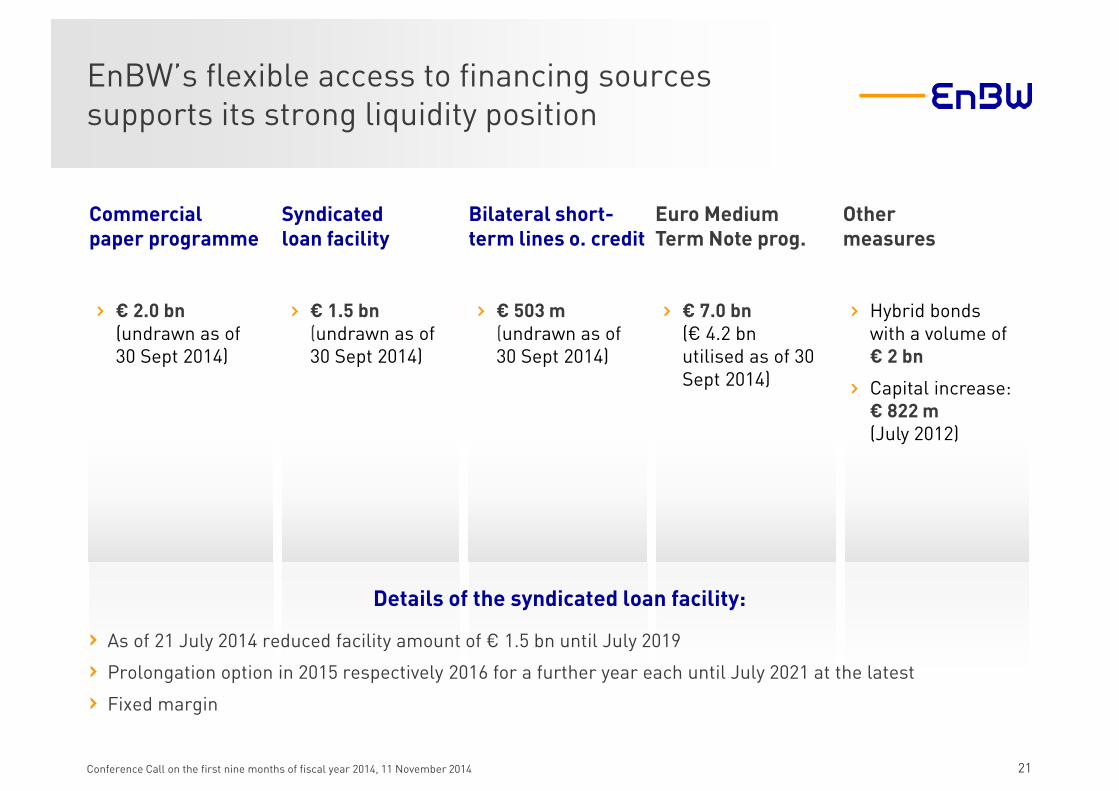

EnBW’s flexible access to financing sourcessupports its strong liquidity position

21Conference Call on the first nine months of fiscal year 2014, 11 November 2014

Commercial paper programme

Details of the syndicated loan facility:

› As of 21 July 2014 reduced facility amount of € 1.5 bn until July 2019

› Prolongation option in 2015 respectively 2016 for a further year each until July 2021 at the latest

› Fixed margin

Syndicatedloan facility

Bilateral short-term lines o. credit

Euro Medium Term Note prog.

Other measures

› € 2.0 bn(undrawn as of 30 Sept 2014)

› € 1.5 bn(undrawn as of 30 Sept 2014)

› € 503 m (undrawn as of 30 Sept 2014)

› € 7.0 bn(€ 4.2 bnutilised as of 30 Sept 2014)

› Hybrid bondswith a volume of € 2 bn

› Capital increase: € 822 m(July 2012)

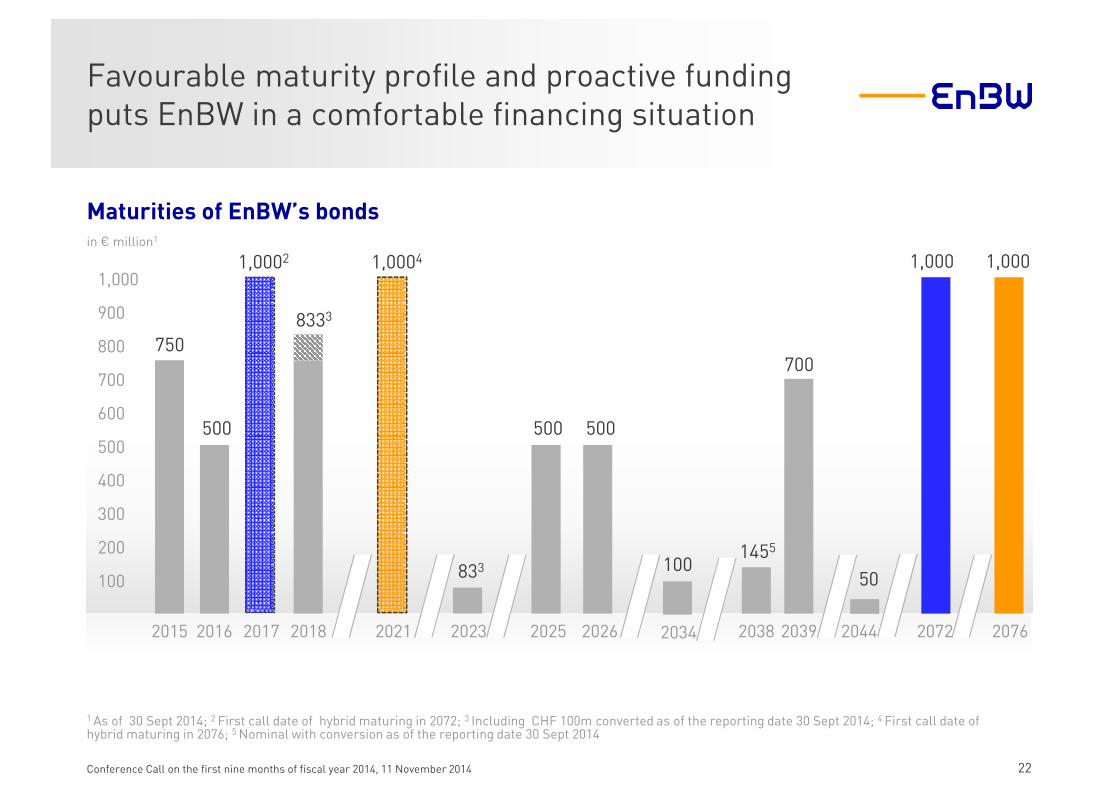

Favourable maturity profile and proactive funding puts EnBW in a comfortable financing situation

22Conference Call on the first nine months of fiscal year 2014, 11 November 2014

1 As of 30 Sept 2014; 2 First call date of hybrid maturing in 2072; 3 Including CHF 100m converted as of the reporting date 30 Sept 2014; 4 First call date of hybrid maturing in 2076; 5 Nominal with conversion as of the reporting date 30 Sept 2014

100

200

300

400

500

600

700

800

900

1,000

750

2015

500

2016

1,0002

2017

8333

2018

833

2023 2025

1455

2038

700

2039

1,000

2072

500

1,0004

2021 2076

1,000

2026

500

100

2034

50

2044

Maturities of EnBW’s bondsin € million1

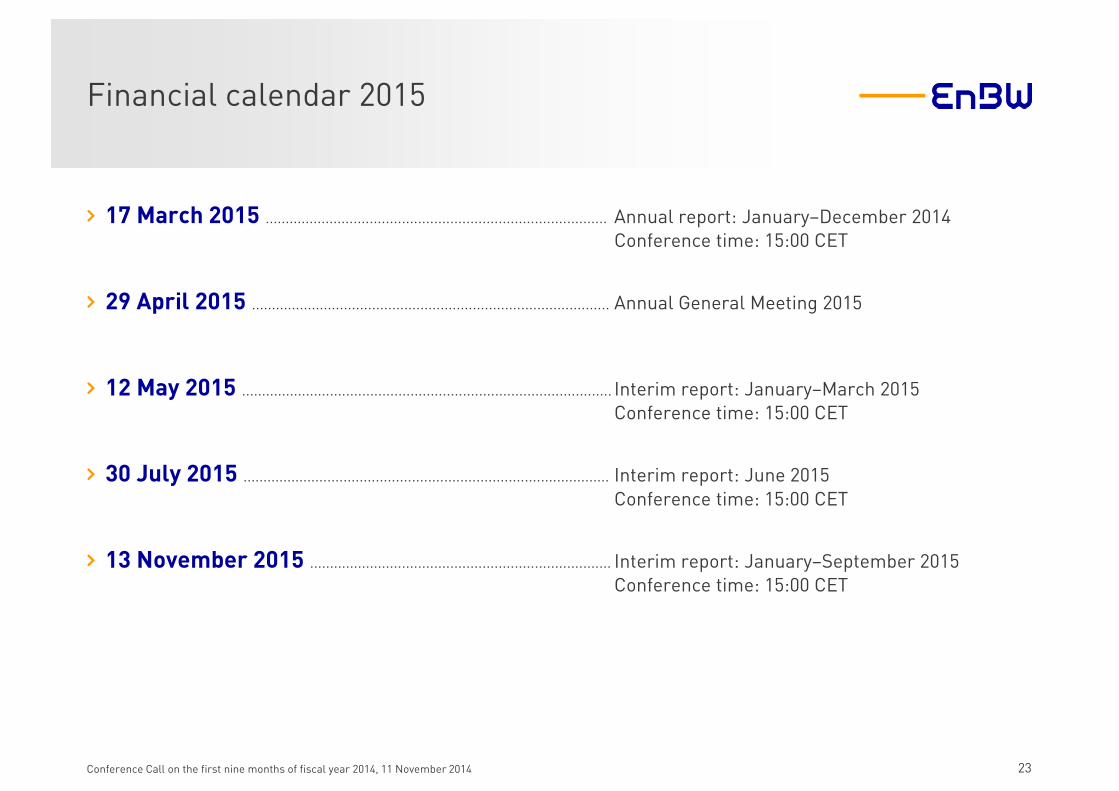

Financial calendar 2015

23Conference Call on the first nine months of fiscal year 2014, 11 November 2014

› 17 March 2015 ..................................................................................... Annual report: January–December 2014Conference time: 15:00 CET

› 29 April 2015 ......................................................................................... Annual General Meeting 2015

› 12 May 2015 ............................................................................................ Interim report: January–March 2015Conference time: 15:00 CET

› 30 July 2015 ........................................................................................... Interim report: June 2015Conference time: 15:00 CET

› 13 November 2015 ........................................................................... Interim report: January–September 2015Conference time: 15:00 CET

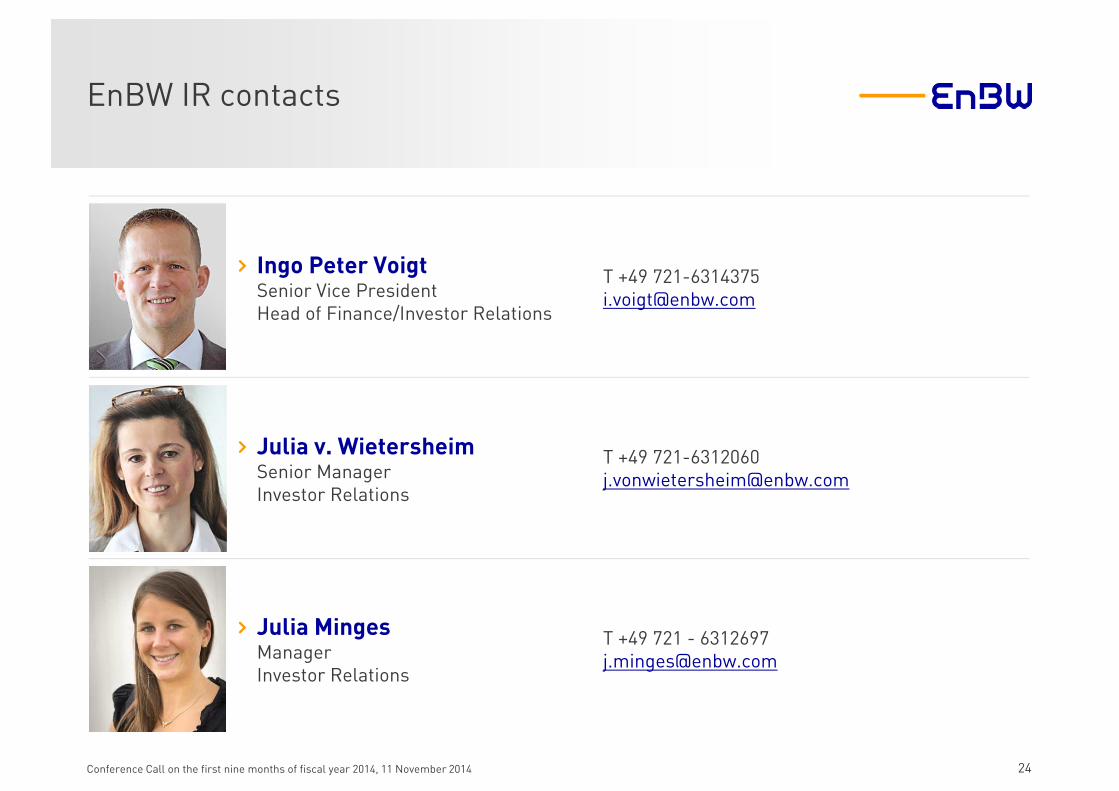

EnBW IR contacts

24Conference Call on the first nine months of fiscal year 2014, 11 November 2014

› Ingo Peter VoigtSenior Vice PresidentHead of Finance/Investor Relations

› Julia v. WietersheimSenior Manager Investor Relations

› Julia MingesManager Investor Relations

T +49 [email protected]

T +49 [email protected]

T +49 721 - [email protected]