Embed Size (px)

Citation preview

Conditions for unbundling the electricity sector and the introduction

of RES into the energy mix

By Alberto GonzalezJune 21, 2012

of Jamaica

www.jsea.org.jm

Outline:

1. Current market structure in Jamaica

2. Unbundling the electricity sector

3. Unbundled markets in countries with similar conditions to Jamaica

(cases: Slovenia, New Zealand and Canary Islands)

4. Current proposals to isolated electric systems (islands)

5. Conclusions

Outline:

1. Current market structure in Jamaica

2. Unbundling the electricity sector

3. Unbundled markets in countries with similar conditions to Jamaica

(cases: Slovenia, New Zealand and Canary Islands)

4. Current proposals to isolated electric systems (islands)

5. Conclusions

Yesterday: How electricity flows to its users

JPS

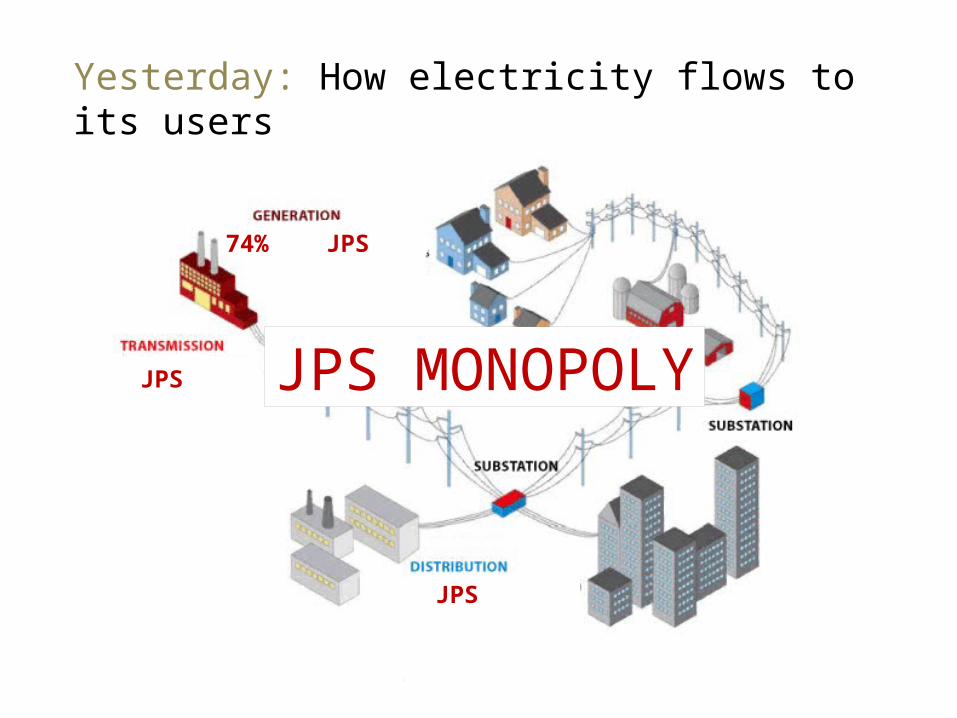

Yesterday: How electricity flows to its users

74% JPS

JPS

JPS

JPS MONOPOLY

JPS

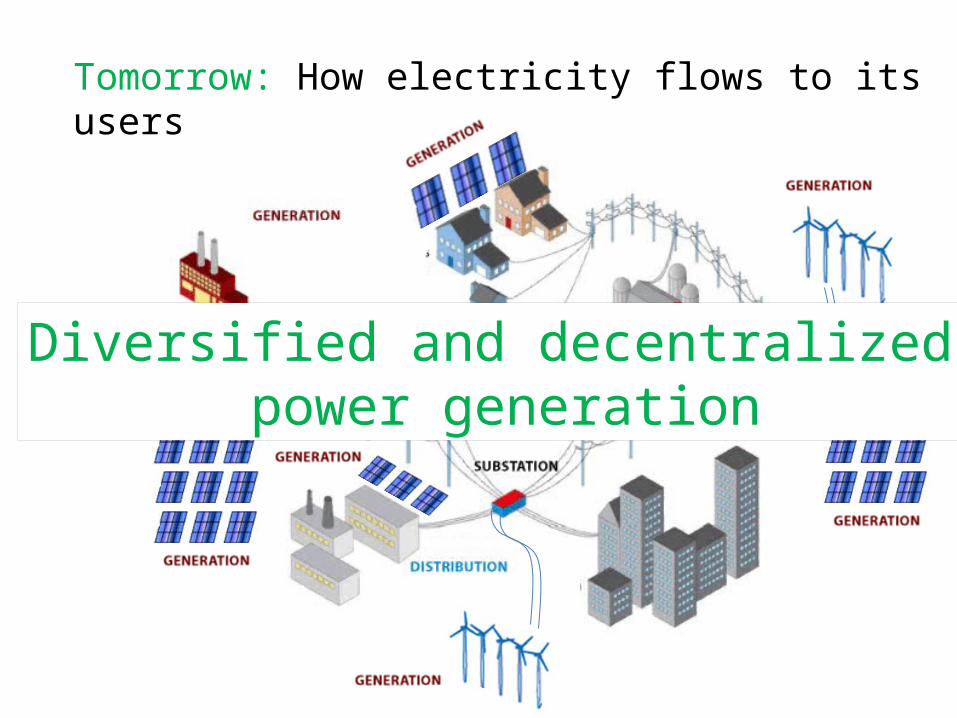

Tomorrow: How electricity flows to its users

Diversified and decentralized power generation

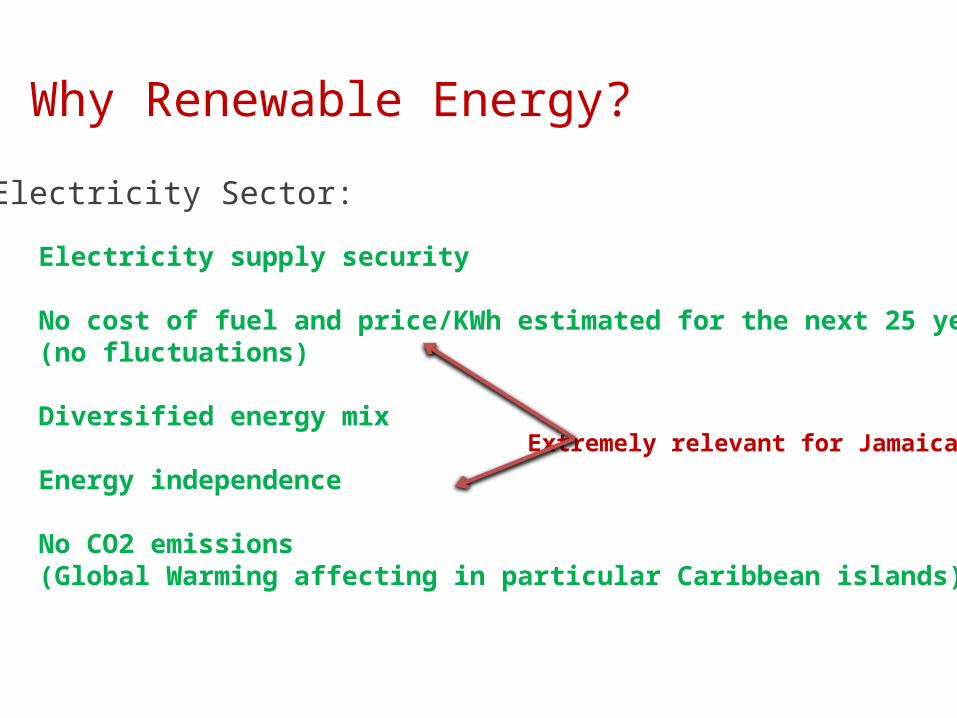

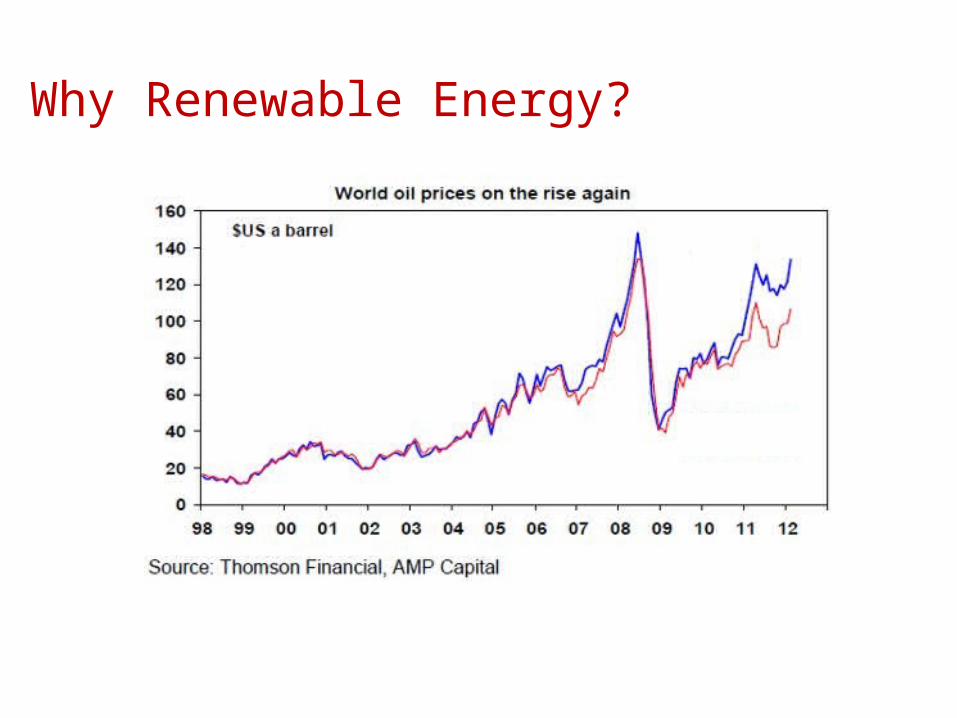

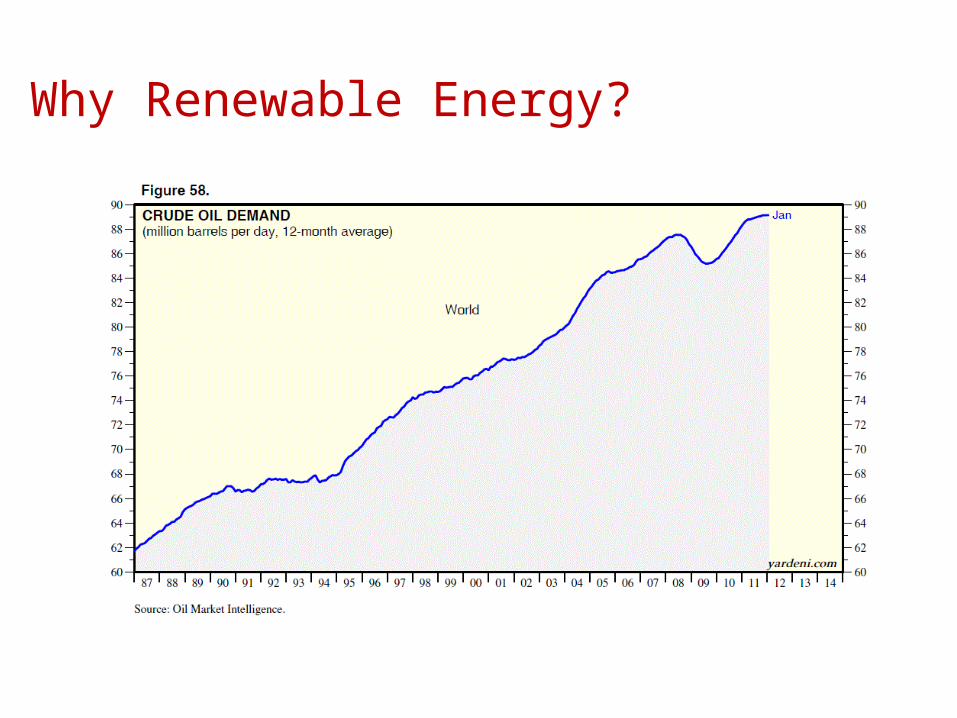

Why Renewable Energy?

Electricity Sector:

Electricity supply security

No cost of fuel and price/KWh estimated for the next 25 years (no fluctuations)

Diversified energy mix

Energy independence

No CO2 emissions (Global Warming affecting in particular Caribbean islands)

Extremely relevant for Jamaica!

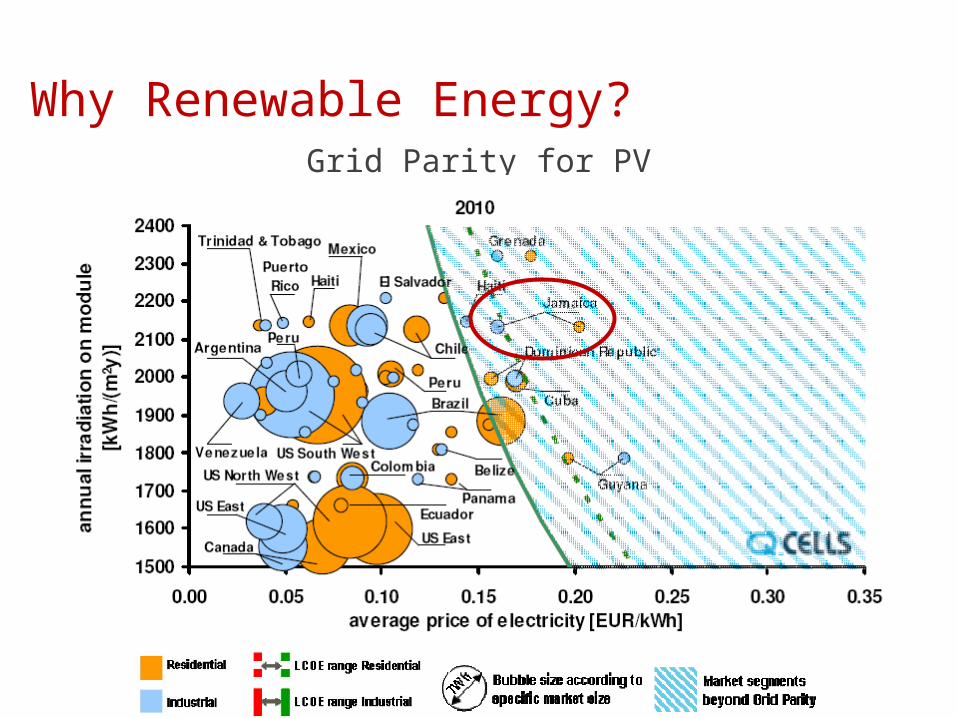

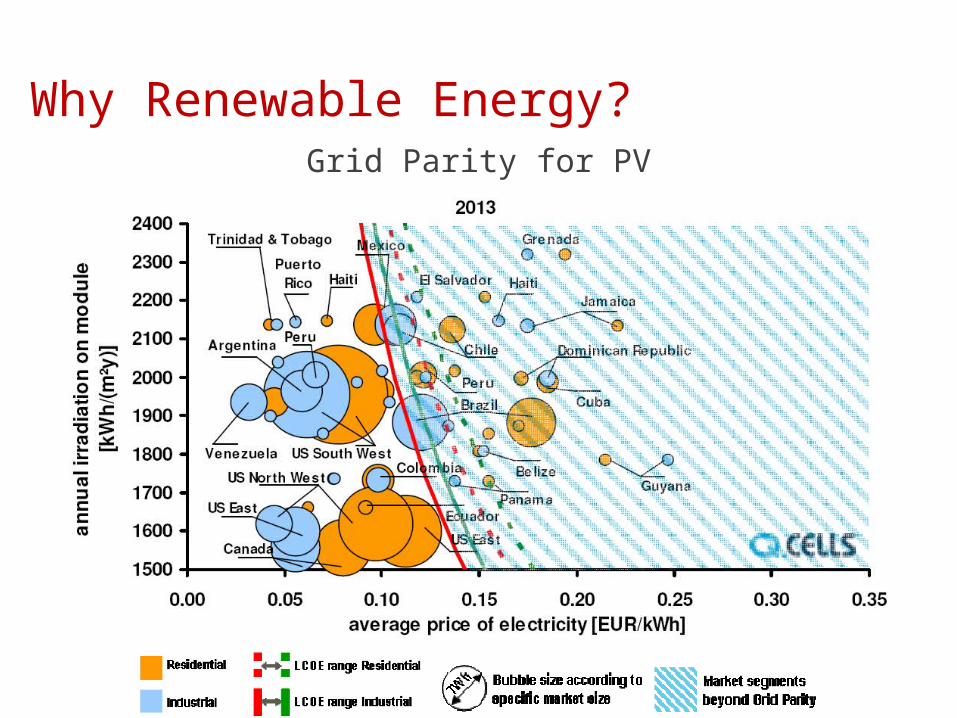

Why Renewable Energy?

Why Renewable Energy?

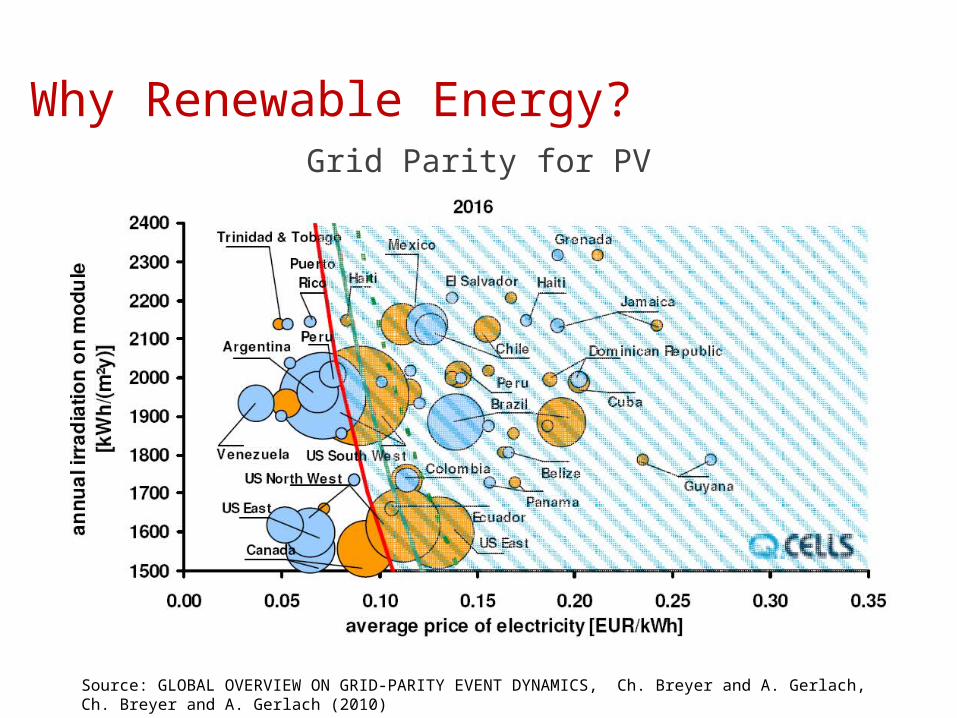

Why Renewable Energy?Grid Parity for PV

Why Renewable Energy?Grid Parity for PV

Why Renewable Energy?

Source: GLOBAL OVERVIEW ON GRID-PARITY EVENT DYNAMICS, Ch. Breyer and A. Gerlach, Ch. Breyer and A. Gerlach (2010)

Grid Parity for PV

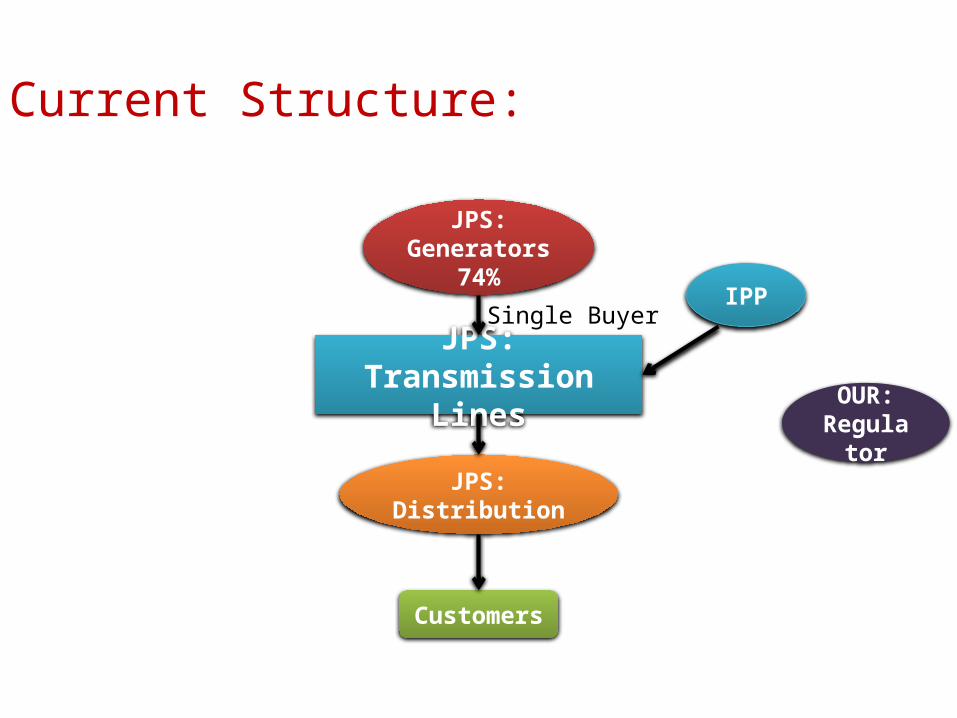

Current Structure:

JPS: Transmission Lines

JPS: Generators

74%

JPS: Distribution

Customers

Single BuyerIPP

OUR: Regulator

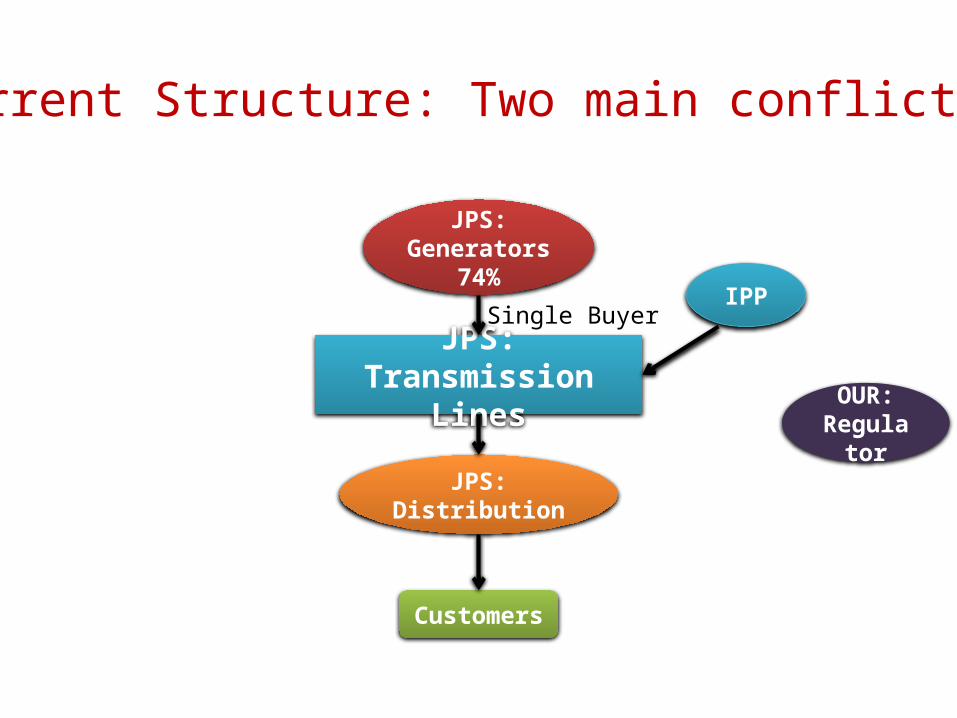

Current Structure: Two main conflicts

JPS: Transmission Lines

JPS: Generators

74%

JPS: Distribution

Single BuyerIPP

Customers

OUR: Regulator

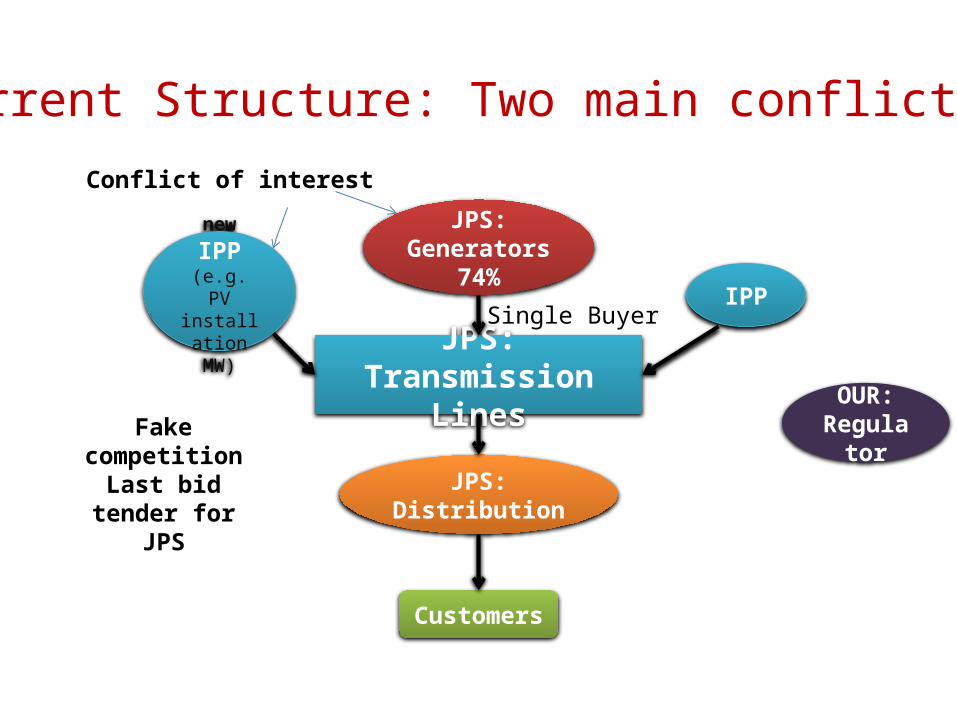

JPS: Transmission Lines

JPS: Generators

74%

JPS: Distribution

Single BuyerIPP

Customers

new IPP(e.g. PV

installation MW)

Conflict of interest

Fake competitionLast bid tender for

JPS

OUR: Regulator

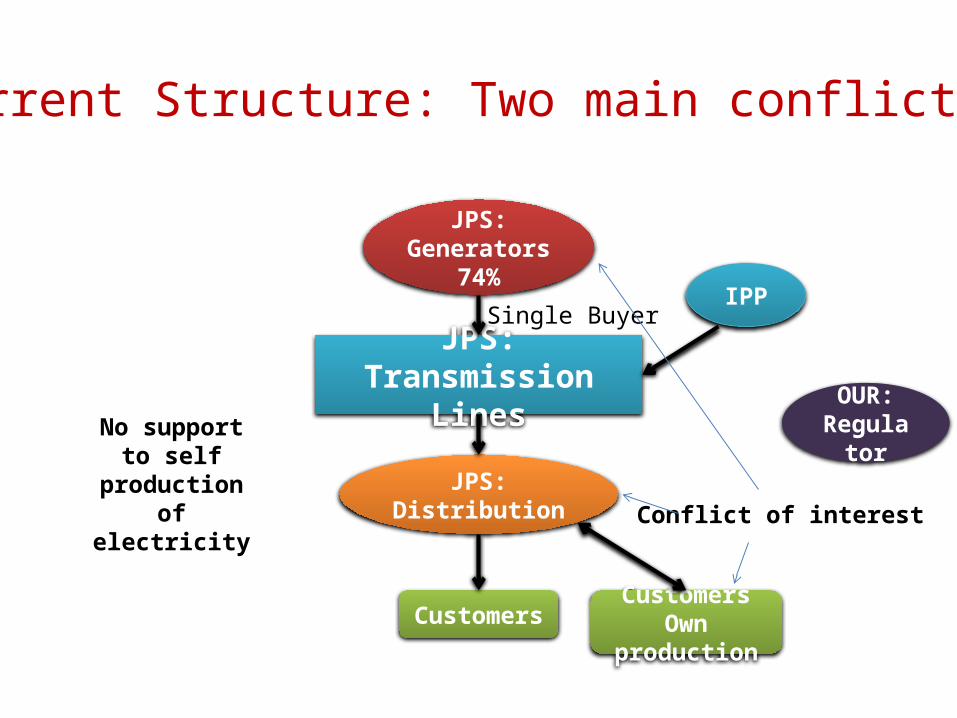

Current Structure: Two main conflicts

JPS: Transmission Lines

JPS: Generators

74%

JPS: Distribution

Single BuyerIPP

Customers

Conflict of interest

CustomersOwn production

No support to self production of

electricity

OUR: Regulator

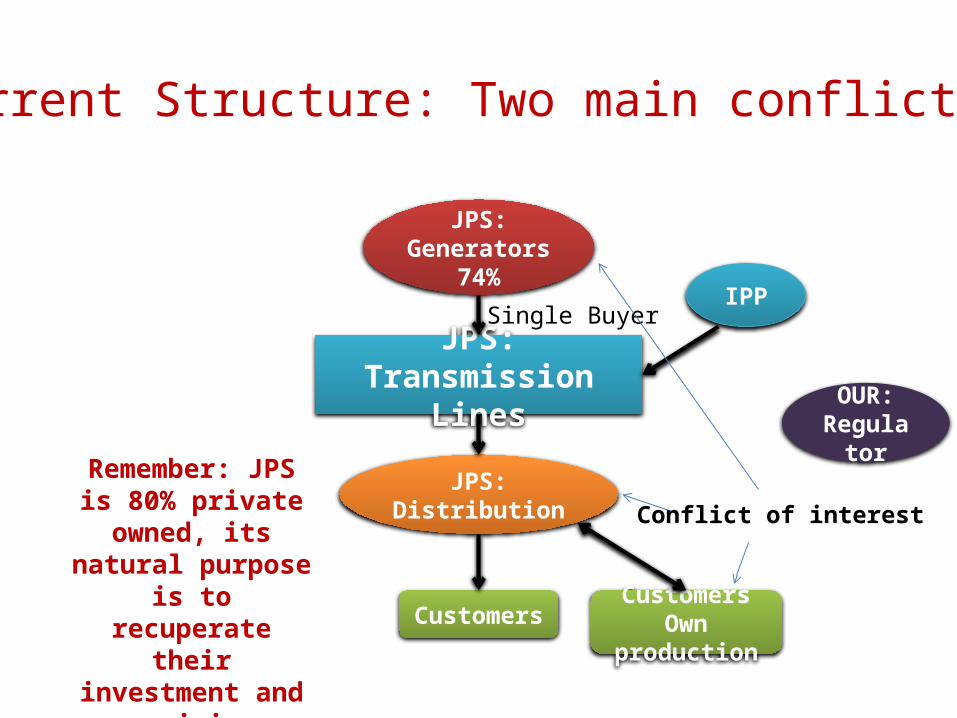

Current Structure: Two main conflicts

JPS: Transmission Lines

JPS: Generators

74%

JPS: Distribution

Single BuyerIPP

Customers CustomersOwn production

Remember: JPS is 80% private owned, its

natural purpose is to recuperate their investment and maximize profits

(license until 2026)

OUR: Regulator

Conflict of interest

Current Structure: Two main conflicts

How renewables will change electricity markets in the next five years Ruggero Schleicher-Tappeser (2012)Sustainable Strategies, Berchtesgadener Str. 8, 10779 Berlin, Germany

In 2010, Germany, 51% of the installed renewable power generation capacity was owned by private persons and farmers, 7% by smaller utilities and only

6.5% by the four large power companiesConclusion: Prepare for a turbulent transformation in the electricity sector

Current Structure: Two main conflicts

Current Structure: JPS position

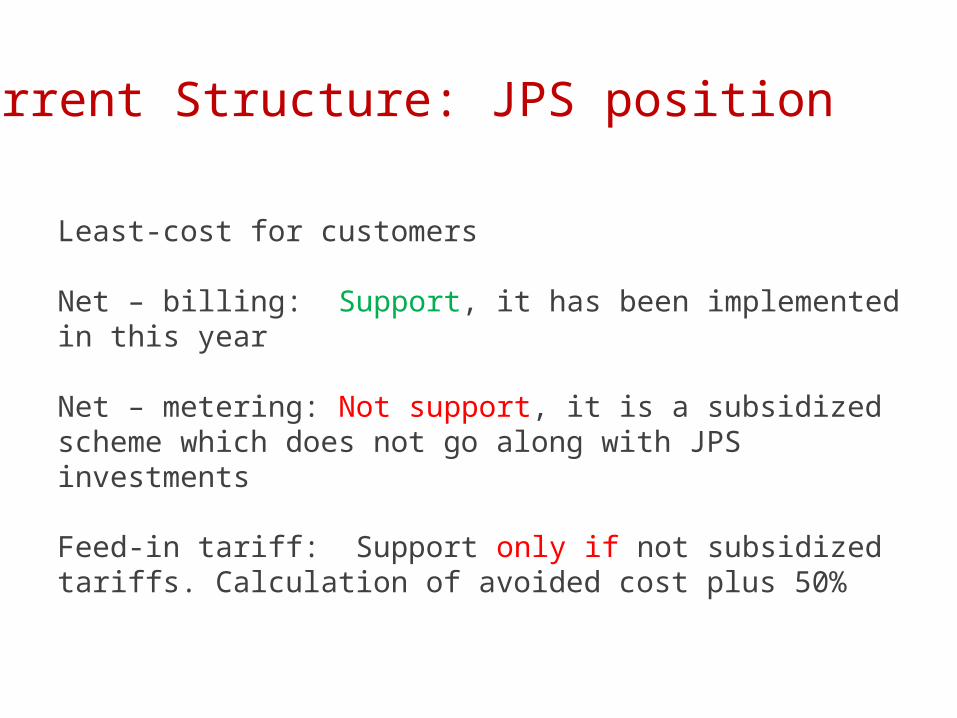

Least-cost for customers

Net – billing: Support, it has been implemented in this year

Net – metering: Not support, it is a subsidized scheme which does not go along with JPS investments

Feed-in tariff: Support only if not subsidized tariffs. Calculation of avoided cost plus 50%

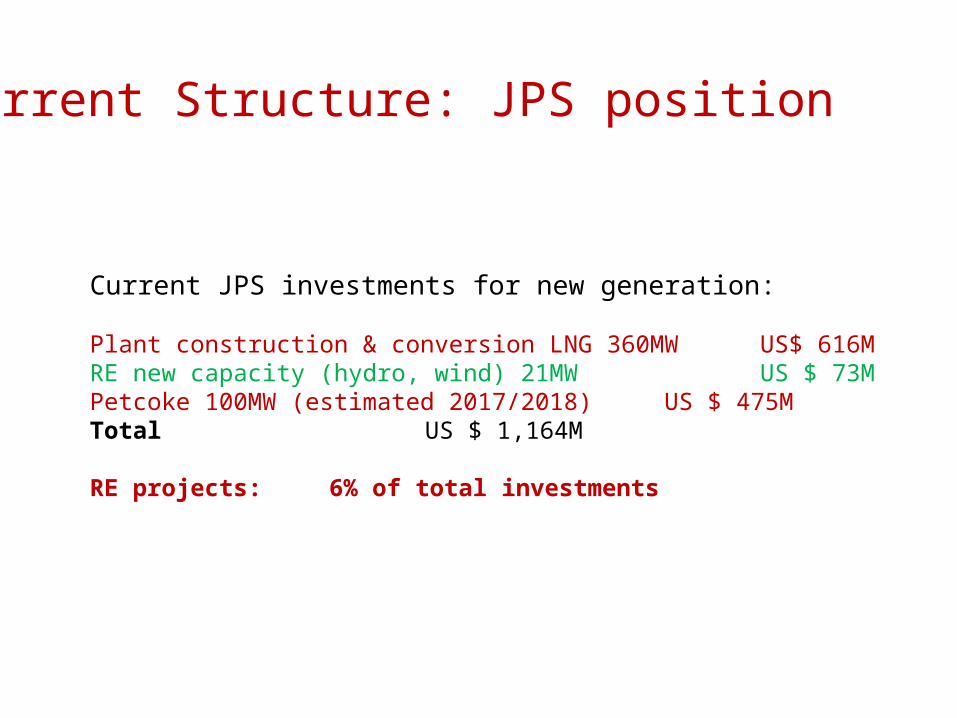

Current Structure: JPS position

Current JPS investments for new generation:

Plant construction & conversion LNG 360MW US$ 616MRE new capacity (hydro, wind) 21MW US $ 73MPetcoke 100MW (estimated 2017/2018) US $ 475MTotal US $ 1,164M

RE projects: 6% of total investments

Policy

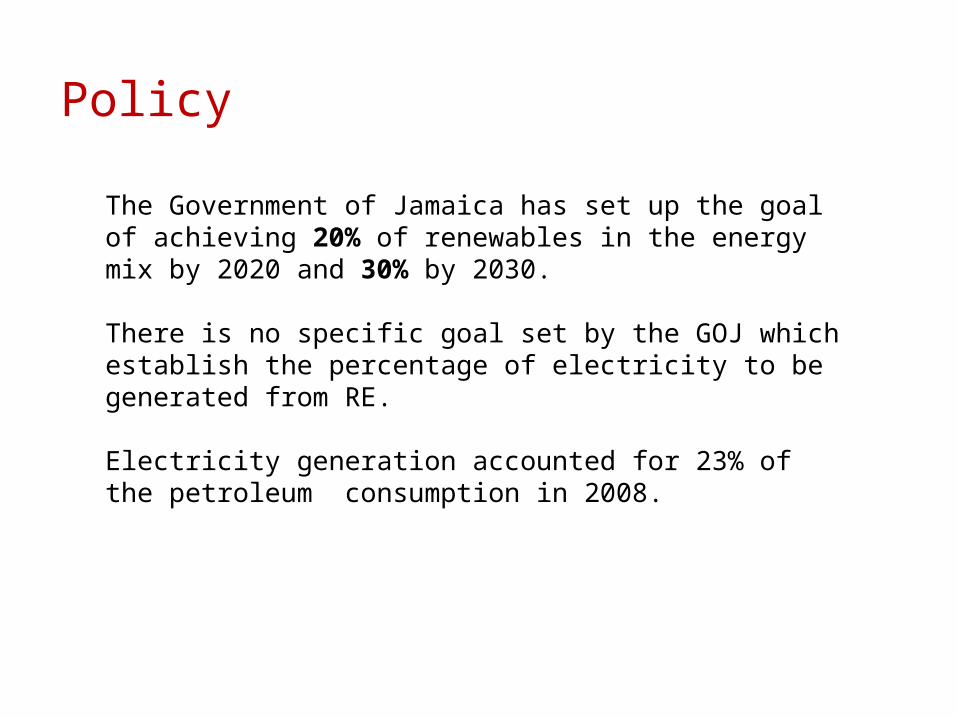

The Government of Jamaica has set up the goal of achieving 20% of renewables in the energy mix by 2020 and 30% by 2030.

There is no specific goal set by the GOJ which establish the percentage of electricity to be generated from RE.

Electricity generation accounted for 23% of the petroleum consumption in 2008.

Current Structure: JPS position and RESQuestions and Answers:

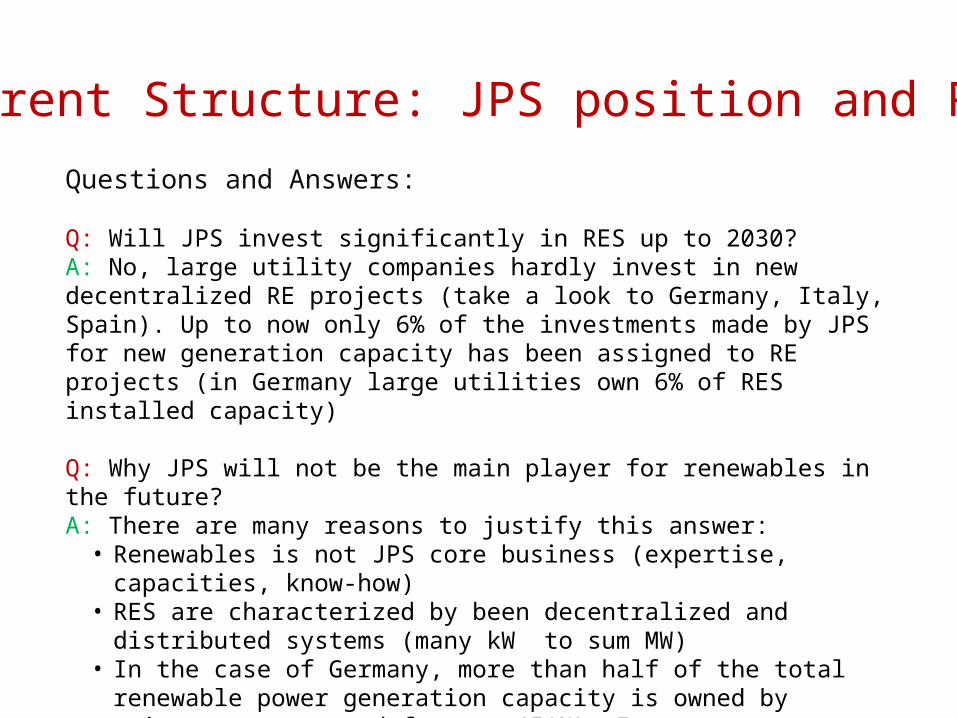

Q: Will JPS invest significantly in RES up to 2030?A: No, large utility companies hardly invest in new decentralized RE projects (take a look to Germany, Italy, Spain). Up to now only 6% of the investments made by JPS for new generation capacity has been assigned to RE projects (in Germany large utilities own 6% of RES installed capacity)

Q: Why JPS will not be the main player for renewables in the future?A: There are many reasons to justify this answer:• Renewables is not JPS core business (expertise, capacities, know-how)• RES are characterized by been decentralized and distributed systems (many kW

to sum MW)• In the case of Germany, more than half of the total renewable power

generation capacity is owned by private persons and farmers (51%). Investments are meant to be done by private persons, farmers, industries, small utilities, households, farmers

Current Structure: JPS position and RES

Questions and Answers:

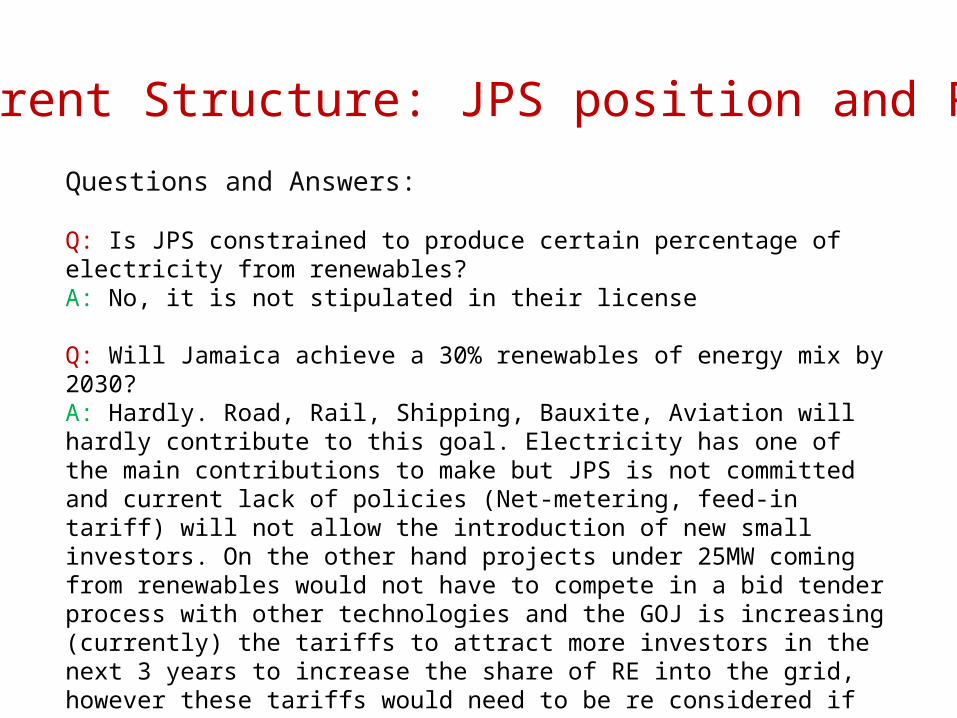

Q: Is JPS constrained to produce certain percentage of electricity from renewables? A: No, it is not stipulated in their license

Q: Will Jamaica achieve a 30% renewables of energy mix by 2030?A: Hardly. Road, Rail, Shipping, Bauxite, Aviation will hardly contribute to this goal. Electricity has one of the main contributions to make but JPS is not committed and current lack of policies (Net-metering, feed-in tariff) will not allow the introduction of new small investors. On the other hand projects under 25MW coming from renewables would not have to compete in a bid tender process with other technologies and the GOJ is increasing (currently) the tariffs to attract more investors in the next 3 years to increase the share of RE into the grid, however these tariffs would need to be re considered if such investors do not come.

Is it convenient for Jamaica to separate its electricity services?

• generation, • transmission • distribution

an horizontal and vertical disaggregation of the electricity sector?

Question:

Outline:

1. Current market structure in Jamaica

2. Unbundling the electricity sector

3. Unbundled markets in countries with similar conditions to Jamaica

(cases: Slovenia, New Zealand and Canary Islands)

4. Current proposals to isolated electric systems (islands)

5. Conclusions

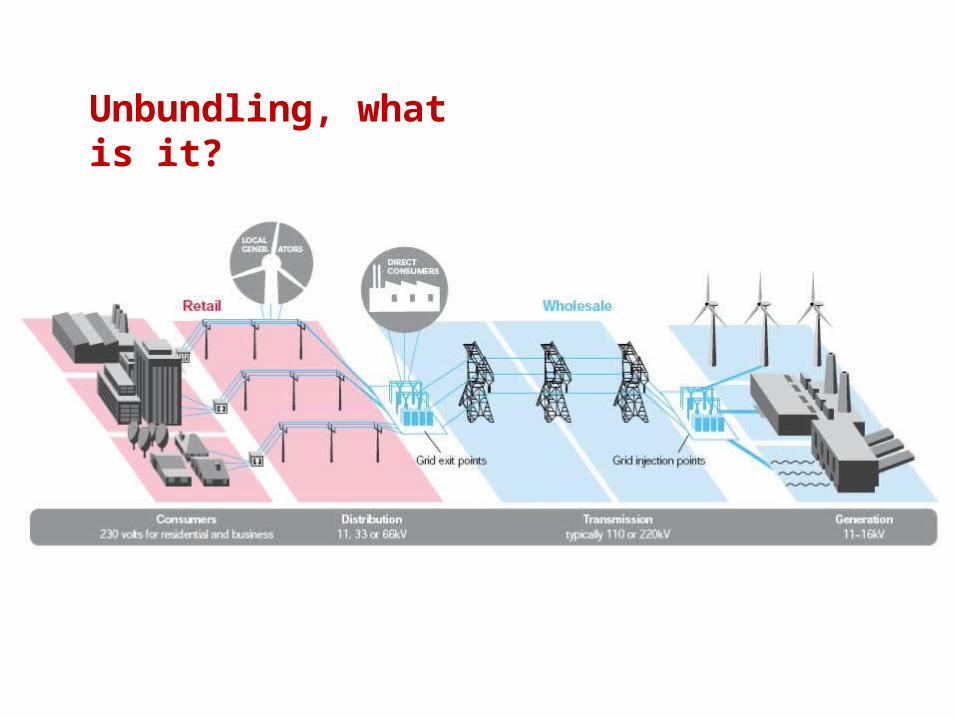

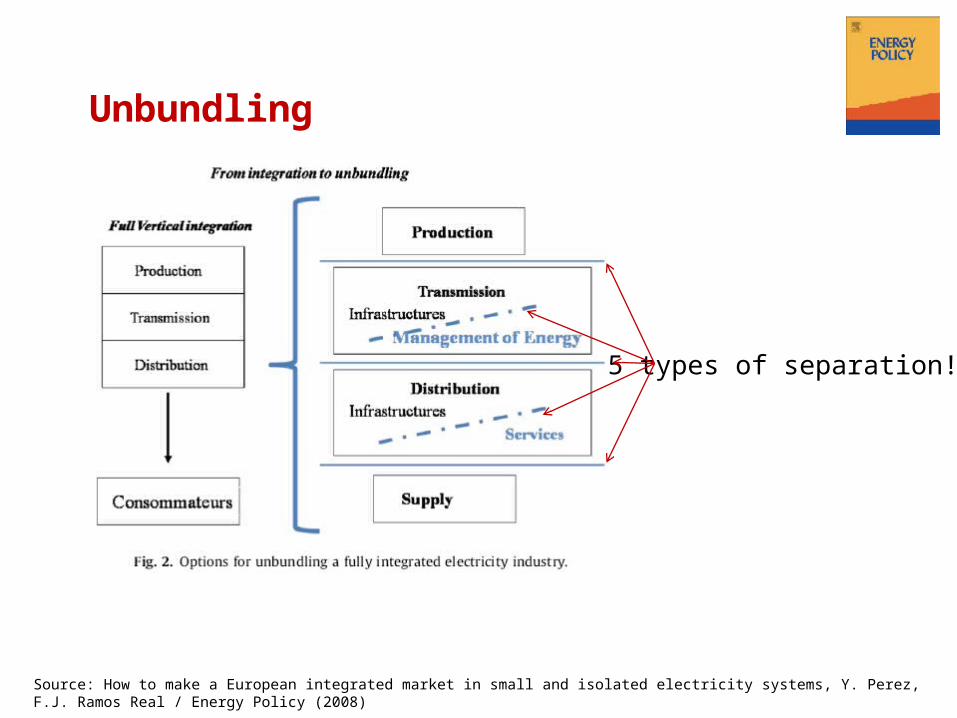

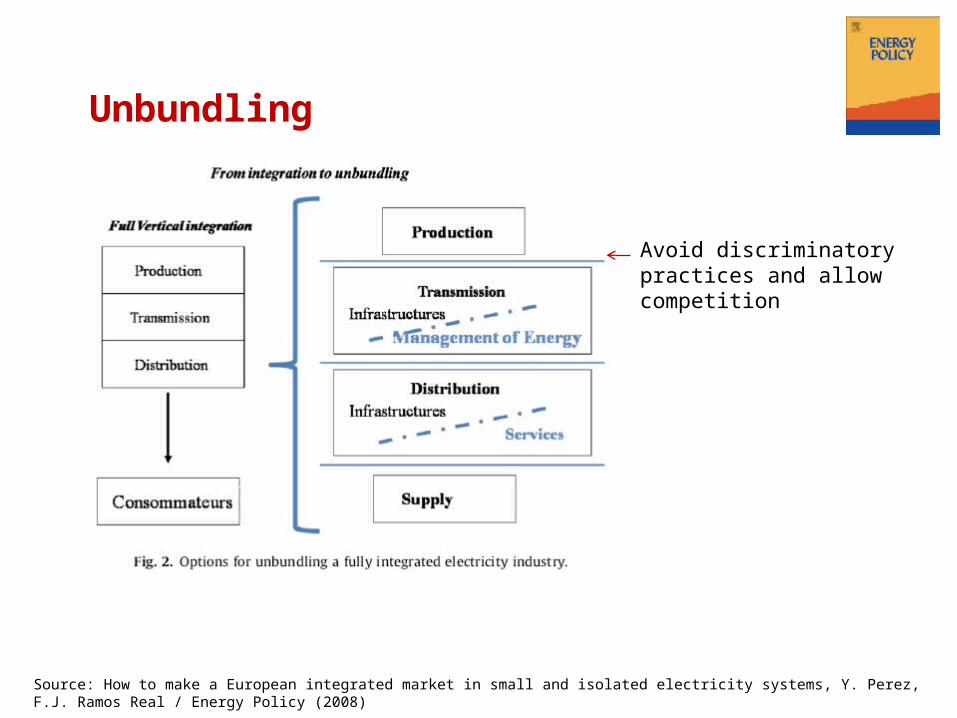

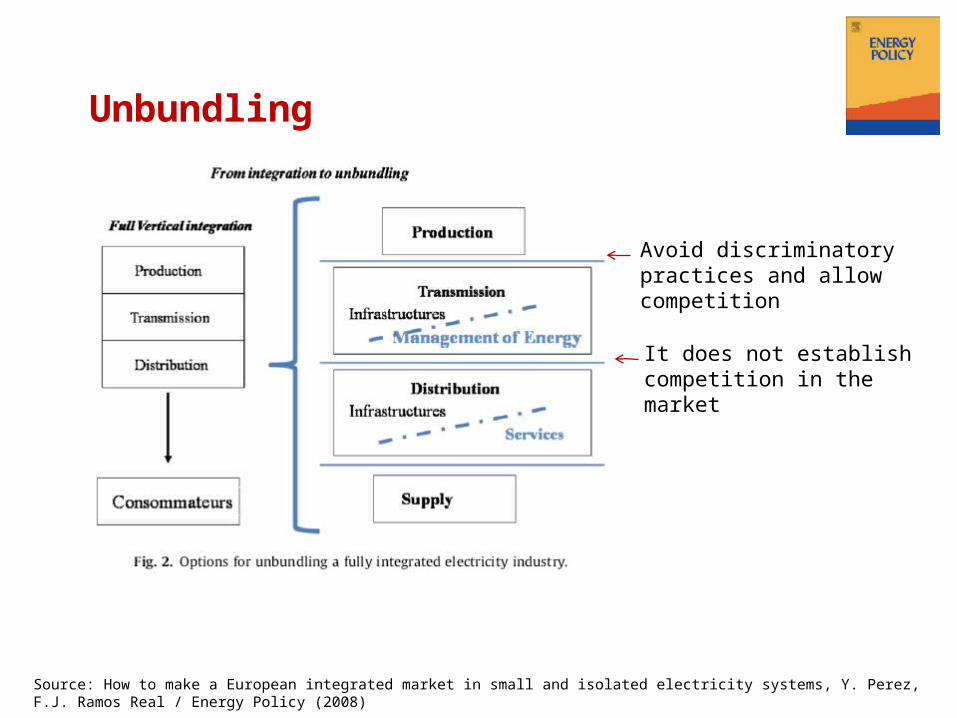

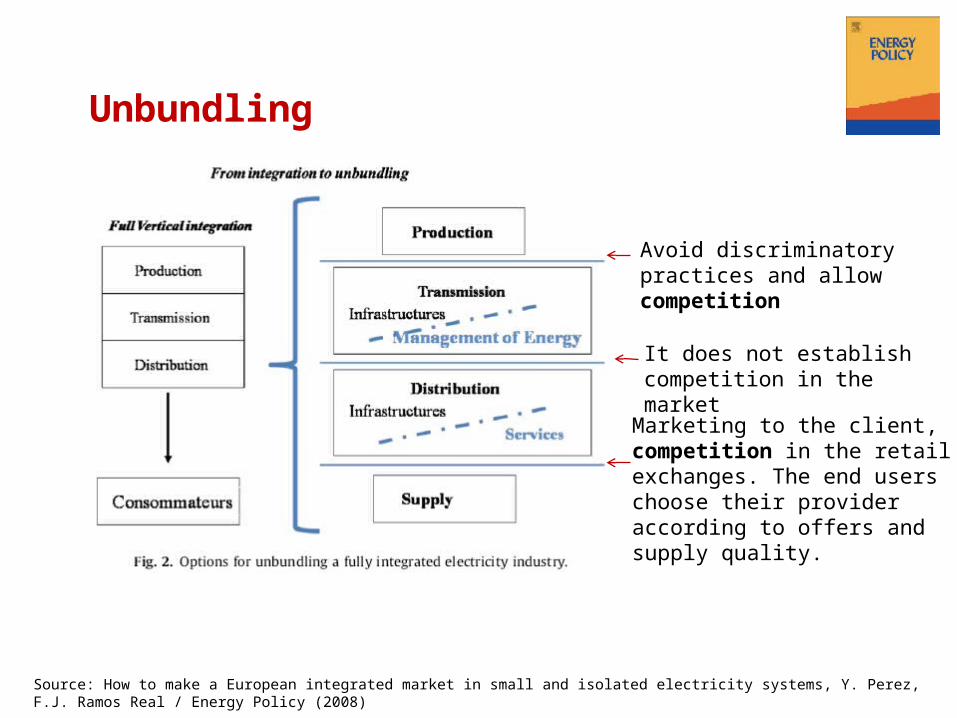

Unbundling, what is it?

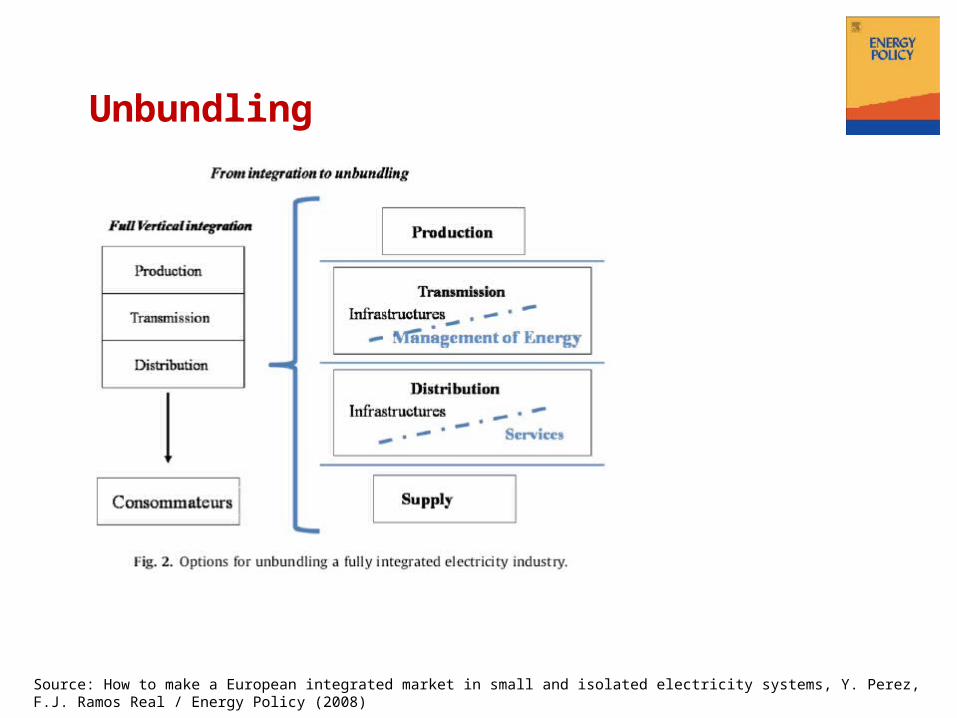

Unbundling

Source: How to make a European integrated market in small and isolated electricity systems, Y. Perez, F.J. Ramos Real / Energy Policy (2008)

5 types of separation!

Unbundling

Source: How to make a European integrated market in small and isolated electricity systems, Y. Perez, F.J. Ramos Real / Energy Policy (2008)

Avoid discriminatory practices and allow competition

Unbundling

Source: How to make a European integrated market in small and isolated electricity systems, Y. Perez, F.J. Ramos Real / Energy Policy (2008)

Avoid discriminatory practices and allow competition

It does not establish competition in the market

Unbundling

Source: How to make a European integrated market in small and isolated electricity systems, Y. Perez, F.J. Ramos Real / Energy Policy (2008)

Avoid discriminatory practices and allow competition

It does not establish competition in the market

Marketing to the client, competition in the retail exchanges. The end users choose their provider according to offers and supply quality.

Unbundling

Source: How to make a European integrated market in small and isolated electricity systems, Y. Perez, F.J. Ramos Real / Energy Policy (2008)

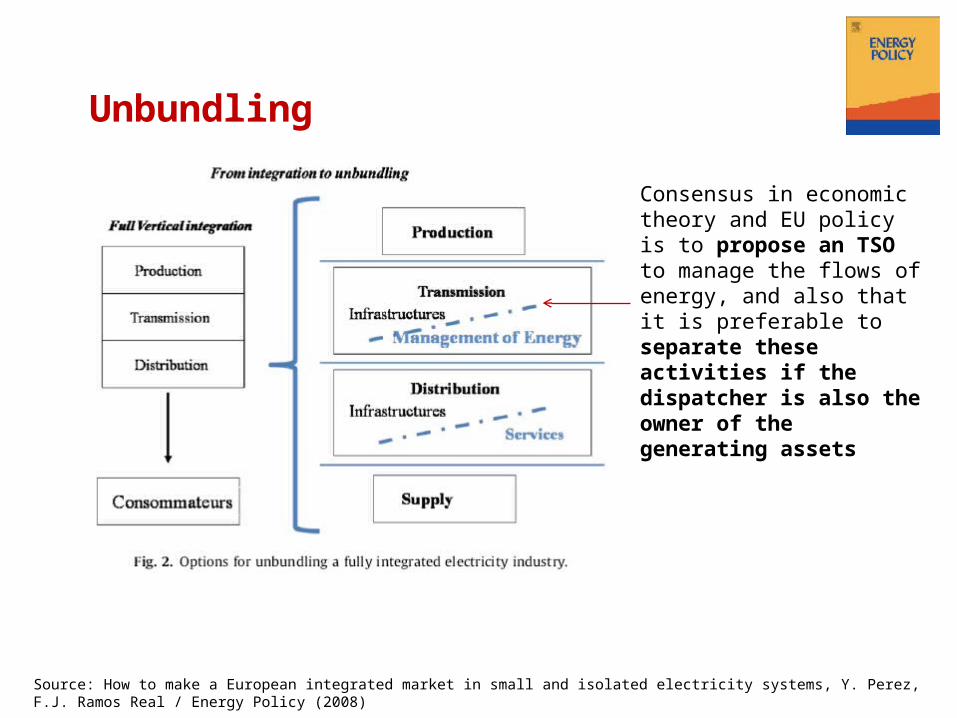

Consensus in economic theory and EU policy is to propose an TSO to manage the flows of energy, and also that it is preferable to separate these activities if the dispatcher is also the owner of the generating assets

Unbundling

Source: How to make a European integrated market in small and isolated electricity systems, Y. Perez, F.J. Ramos Real / Energy Policy (2008)

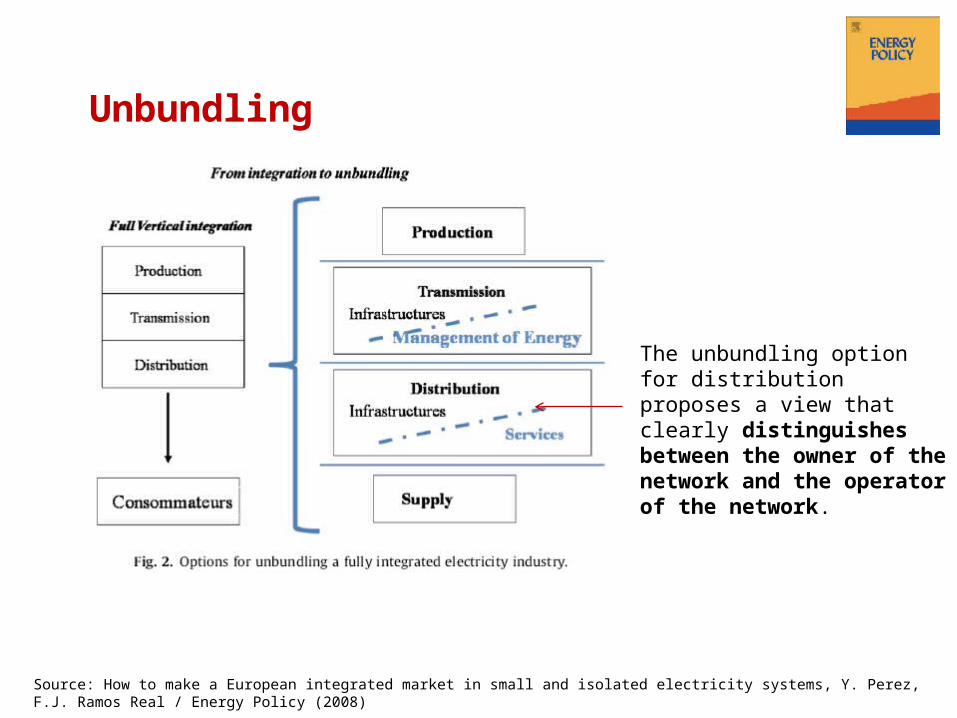

The unbundling option for distribution proposes a view that clearly distinguishes between the owner of the network and the operator of the network.

Unbundling

Source: How to make a European integrated market in small and isolated electricity systems, Y. Perez, F.J. Ramos Real / Energy Policy (2008)

Why unbundling the electricity sector

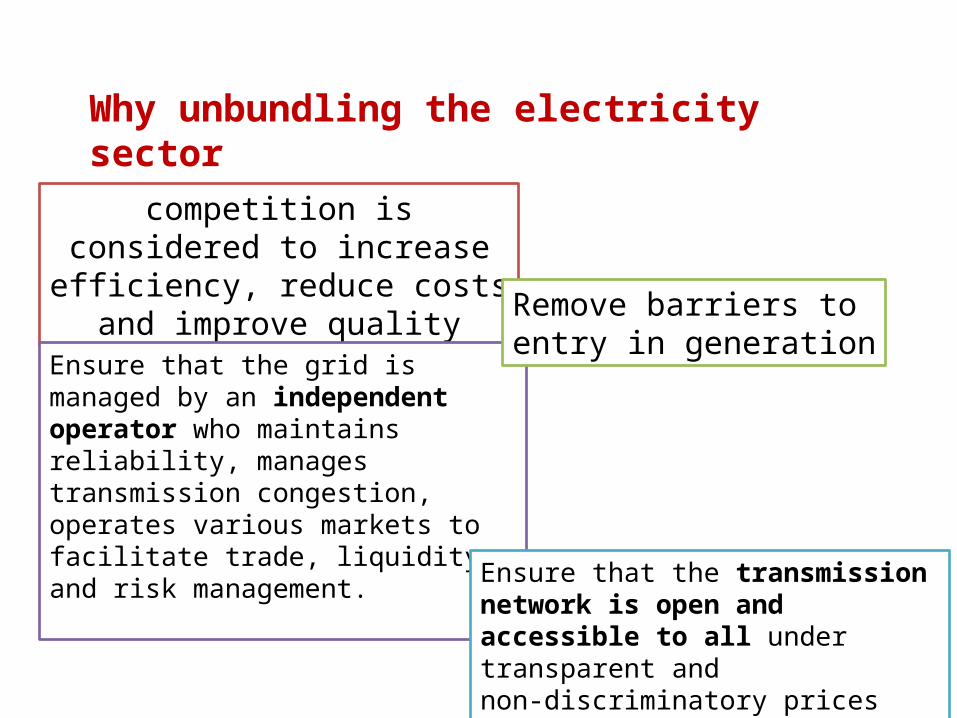

competition is considered to increase efficiency, reduce costs

and improve quality

Ensure that the grid is managed by an independent operator who maintains reliability, manages transmission congestion, operates various markets to facilitate trade, liquidity and risk management.

Remove barriers to entry in generation

Ensure that the transmission network is open and accessible to all under transparent andnon-discriminatory prices

Why unbundling the electricity sector

Pages: 688Year publication: 2006

Analyzing 20 years of electricity market reforms all around the world, including liberalization

and unbundled markets

Good examplesbad examples

Why unbundling the electricity sector

“Philippines Case: reform with private sector participation, liberalizing the market for IPP, increased social welfare”[2]

[1] More competition: Threat or chance for financing renewable electricity?, Sandor Szabo, European Commission, DG Joint Research Center[2] Welfare impacts of electricity generation sector reform in the Philippines, Natsuko Toba, University of Cambridge

“Policies aiming at the expansion of renewable energy technologies should encourage competition in the electricity market” [1]

The question to Jamaica is not only if by unbundling the electricity sector the price/kWh is going to be lower in the near future as a direct consequence (which might be), but if it will provide an appropriate market environment to the introduction of RES and the development of a more diversified energy mix in the long term

“However, the benefits from implementing such reform (separation of electricity services) can only be achieved in markets that are large enough to accommodate sufficient generators to compete with each other. With a small system of the size of Jamaica’s, there is little scope for attracting more than a few generators; thereby resulting in an oligopoly, with prices much higher than under competition”

Castalia report commissioned by JPS: Options to lower electricity prices in Jamaica

The question to Jamaica is not only if by unbundling the electricity sector the price/kWh is going to be lower in the near future as a direct consequence (which might be), but if it will provide an appropriate market environment to the introduction of RES and the development of a more diversified energy mix in the long term

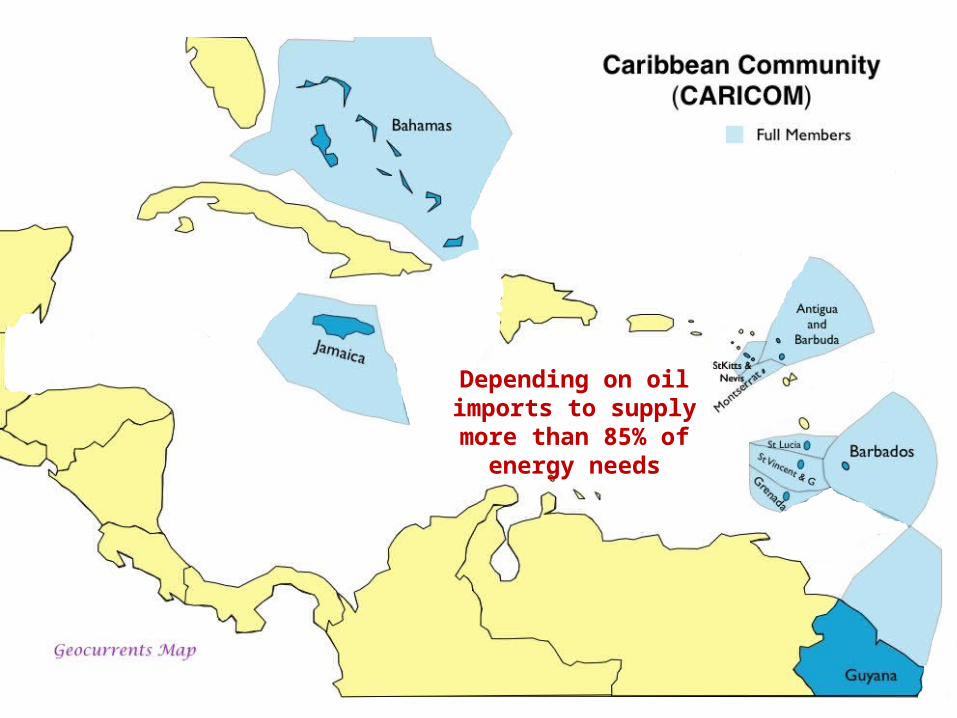

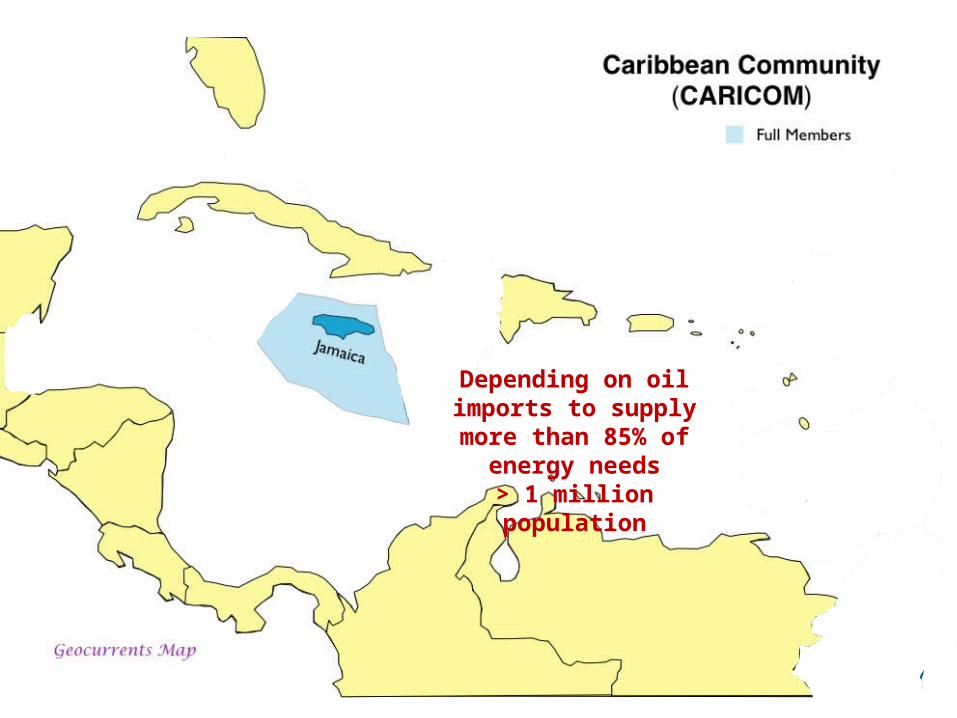

Depending on oil imports to supply more than 85%

of energy needs

Depending on oil imports to supply more than 85%

of energy needs> 1 million population

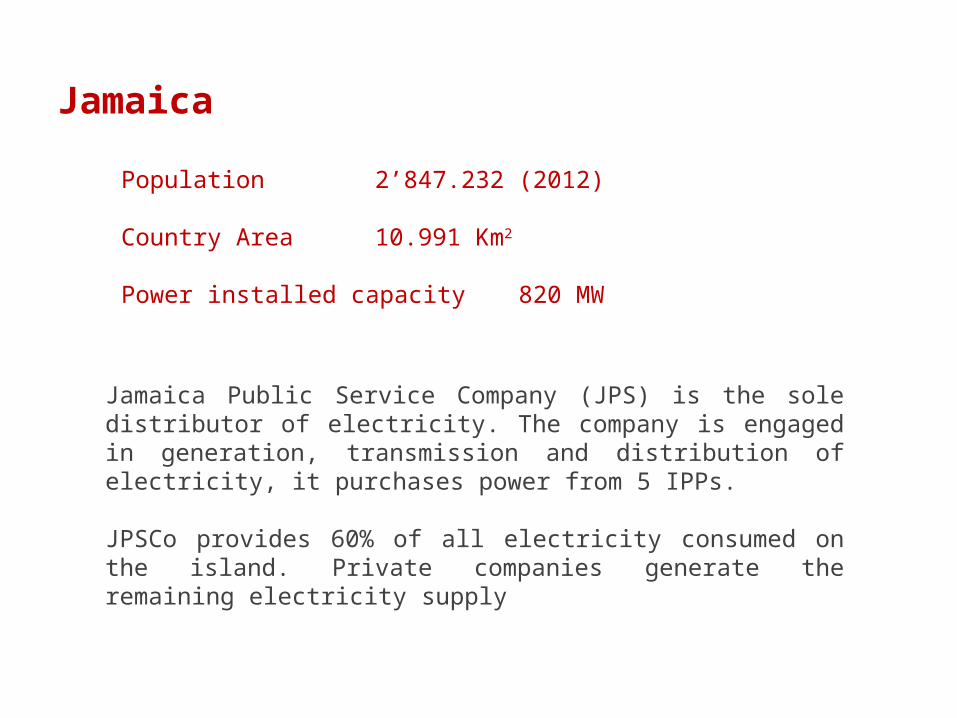

Jamaica

Jamaica Public Service Company (JPS) is the sole distributor of electricity. The company is engaged in generation, transmission and distribution of electricity, it purchases power from 5 IPPs.

JPSCo provides 60% of all electricity consumed on the island. Private companies generate the remaining electricity supply

Population 2’847.232 (2012) Country Area 10.991 Km2

Power installed capacity 820 MW

Comment

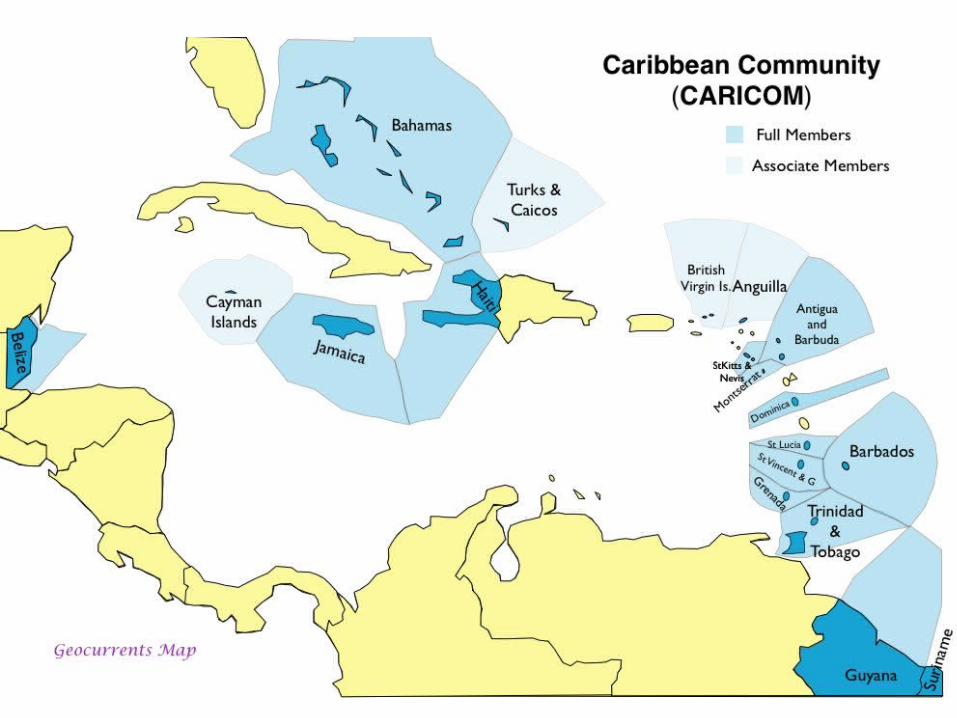

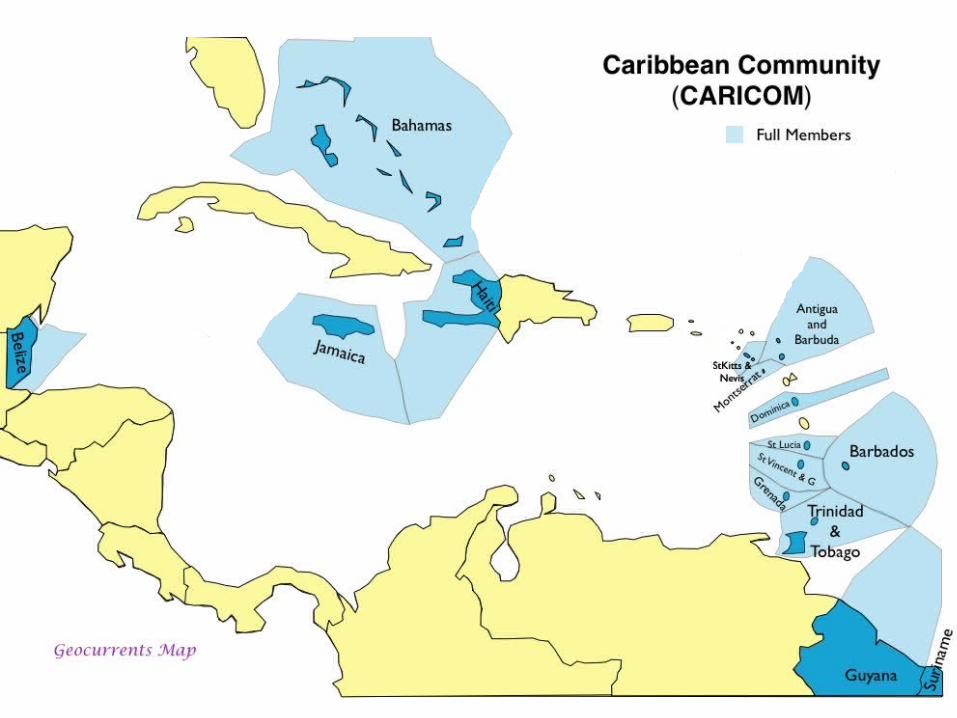

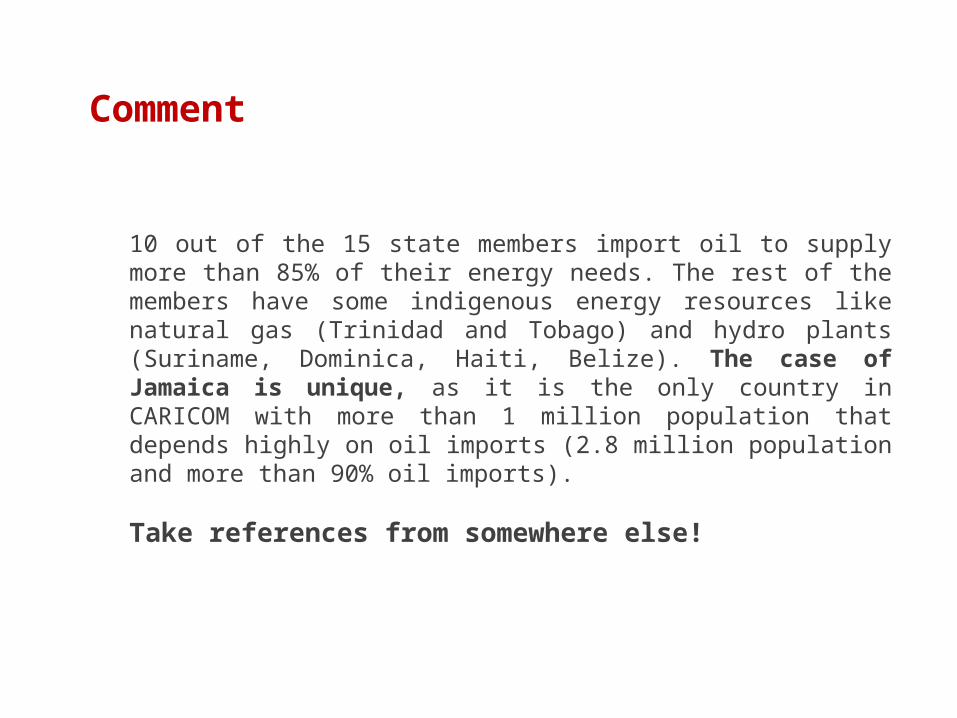

10 out of the 15 state members import oil to supply more than 85% of their energy needs. The rest of the members have some indigenous energy resources like natural gas (Trinidad and Tobago) and hydro plants (Suriname, Dominica, Haiti, Belize). The case of Jamaica is unique, as it is the only country in CARICOM with more than 1 million population that depends highly on oil imports (2.8 million population and more than 90% oil imports).

Take references from somewhere else!

Outline:

1. Current market structure in Jamaica

2. Unbundling the electricity sector

3. Unbundled markets in countries with similar conditions to Jamaica

(cases: Slovenia, New Zealand and Canary Islands)

4. Current proposals to isolated electric systems (islands)

5. Conclusions

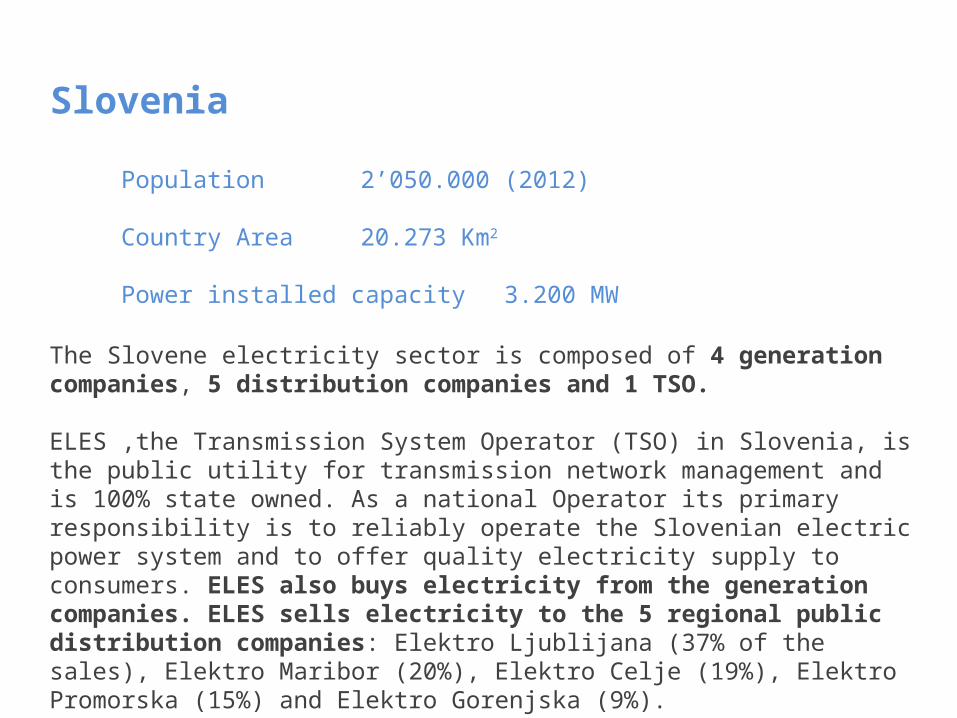

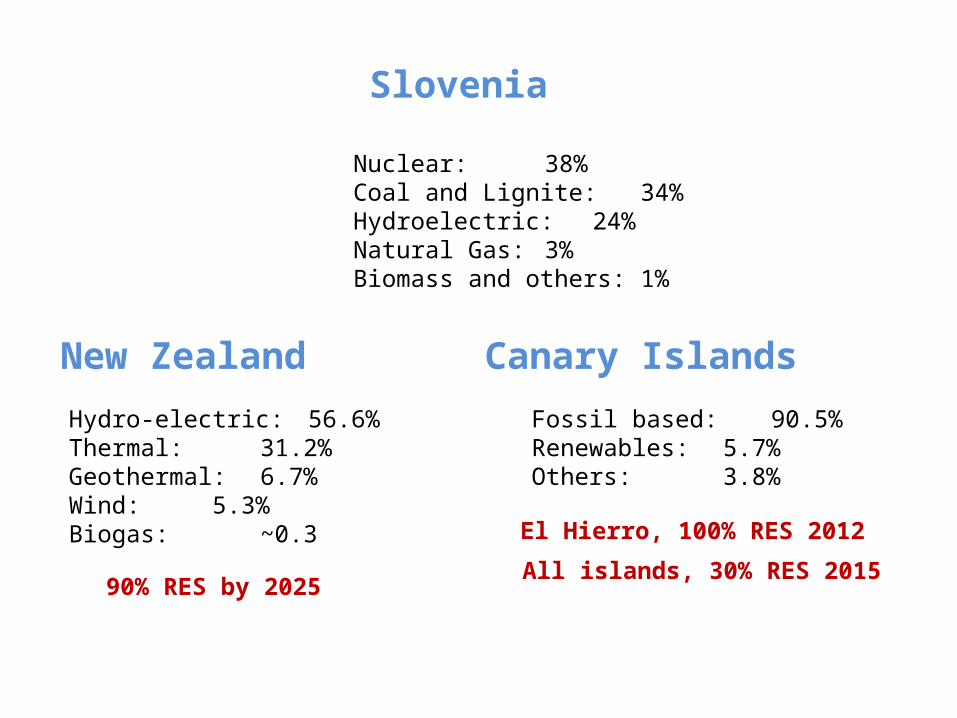

Slovenia

The Slovene electricity sector is composed of 4 generation companies, 5 distribution companies and 1 TSO.

ELES ,the Transmission System Operator (TSO) in Slovenia, is the public utility for transmission network management and is 100% state owned. As a national Operator its primary responsibility is to reliably operate the Slovenian electric power system and to offer quality electricity supply to consumers. ELES also buys electricity from the generation companies. ELES sells electricity to the 5 regional public distribution companies: Elektro Ljublijana (37% of the sales), Elektro Maribor (20%), Elektro Celje (19%), Elektro Promorska (15%) and Elektro Gorenjska (9%).

Population 2’050.000 (2012) Country Area 20.273 Km2

Power installed capacity 3.200 MW

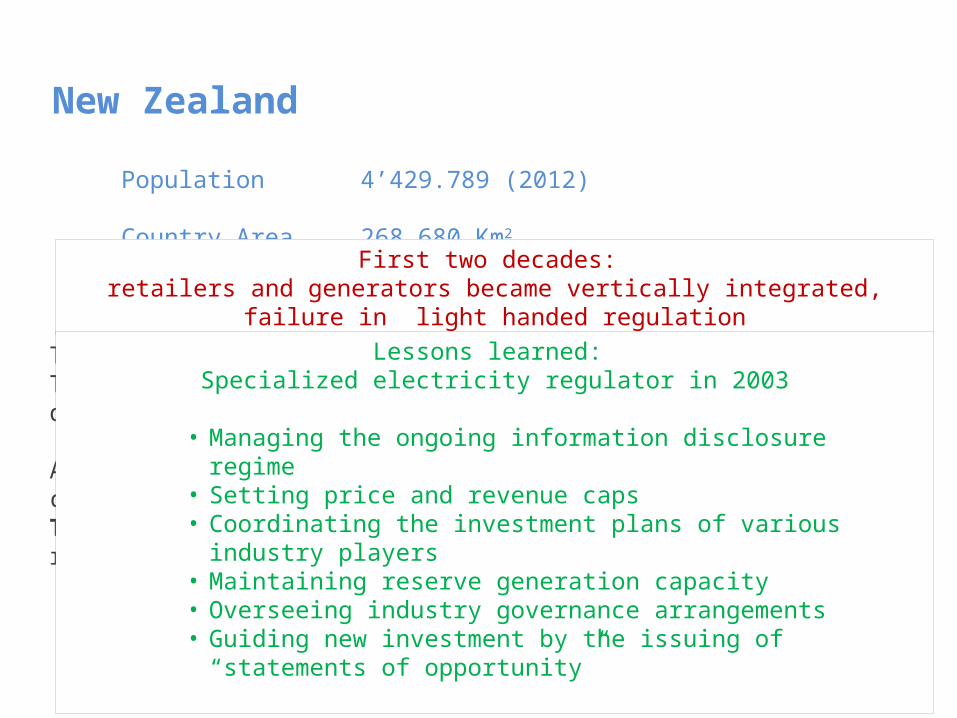

New Zealand

The New Zealand electricity market is a competitive market. There is open entry to the market subject to conditions developed by the Electricity Commission.

As of October 2009, five generation companies operate in the country, the national grid is wholly owned and operated by Transpower, a state-owned company. Distribution is the responsibility of 28 separate distribution companies

Population 4’429.789 (2012) Country Area 268.680 Km2

Power installed capacity 9.485 MWFirst two decades:

retailers and generators became vertically integrated, failure in light handed regulation

Lessons learned: Specialized electricity regulator in 2003

• Managing the ongoing information disclosure regime • Setting price and revenue caps• Coordinating the investment plans of various industry players• Maintaining reserve generation capacity• Overseeing industry governance arrangements• Guiding new investment by the issuing of “statements of opportunity”

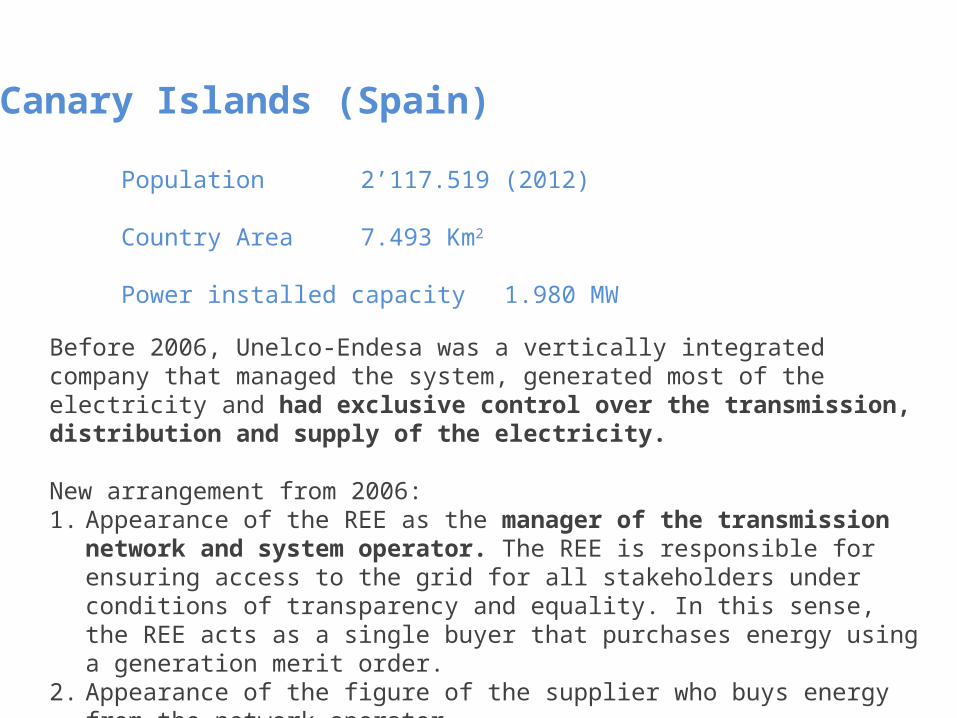

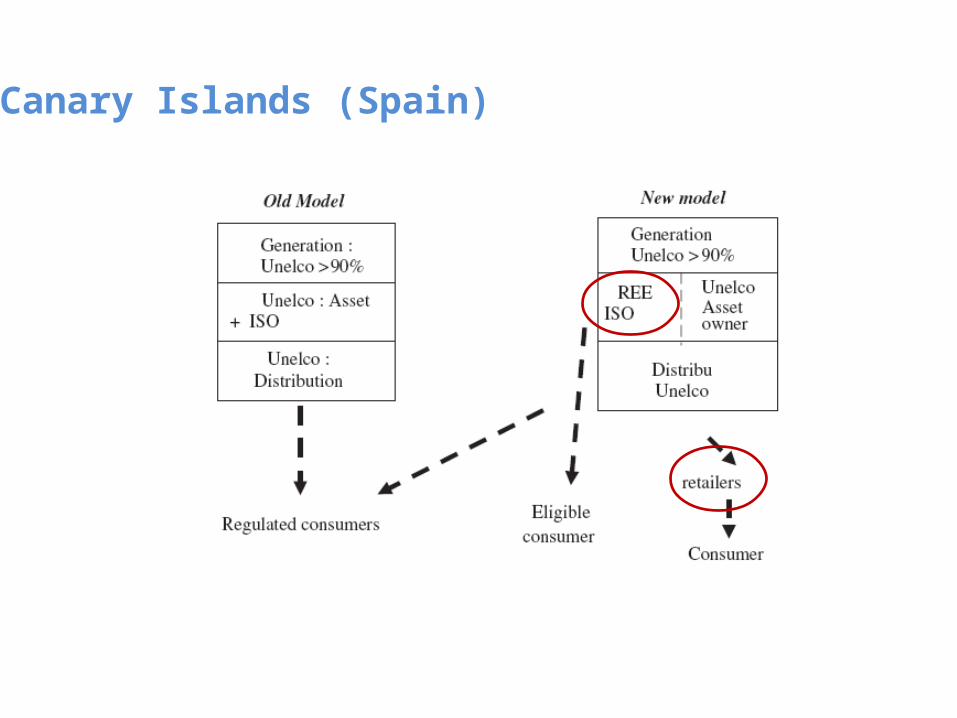

Canary Islands (Spain)

Before 2006, Unelco-Endesa was a vertically integrated company that managed the system, generated most of the electricity and had exclusive control over the transmission, distribution and supply of the electricity.

New arrangement from 2006:1. Appearance of the REE as the manager of the transmission network and system

operator. The REE is responsible for ensuring access to the grid for all stakeholders under conditions of transparency and equality. In this sense, the REE acts as a single buyer that purchases energy using a generation merit order.

2. Appearance of the figure of the supplier who buys energy from the network operator.

Population 2’117.519 (2012) Country Area 7.493 Km2

Power installed capacity 1.980 MW

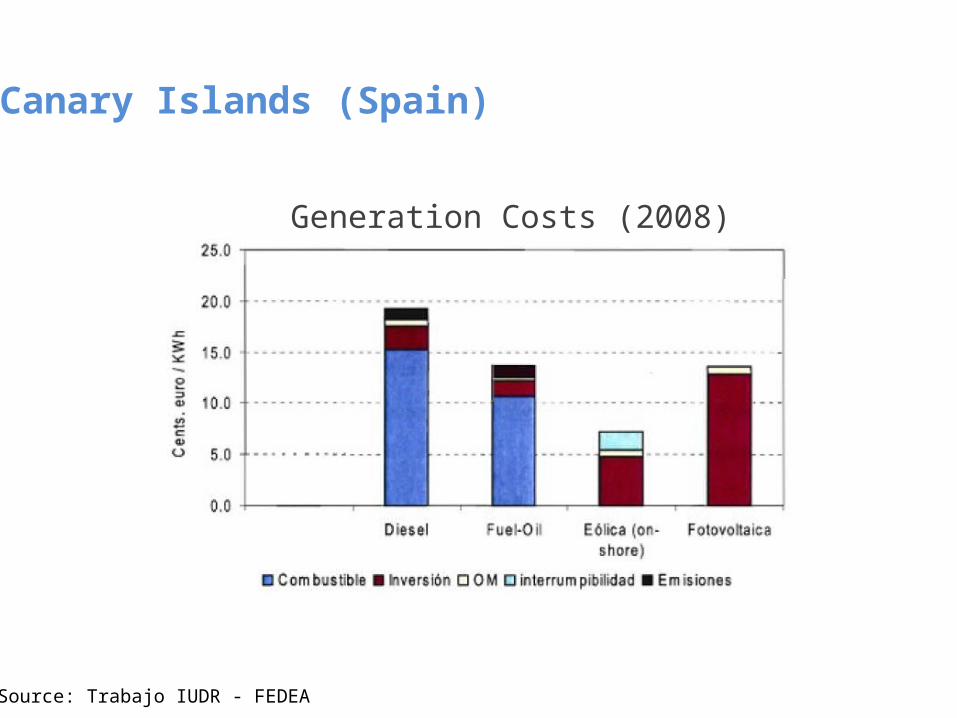

Canary Islands (Spain)

Source: Trabajo IUDR - FEDEA

Generation Costs (2008)

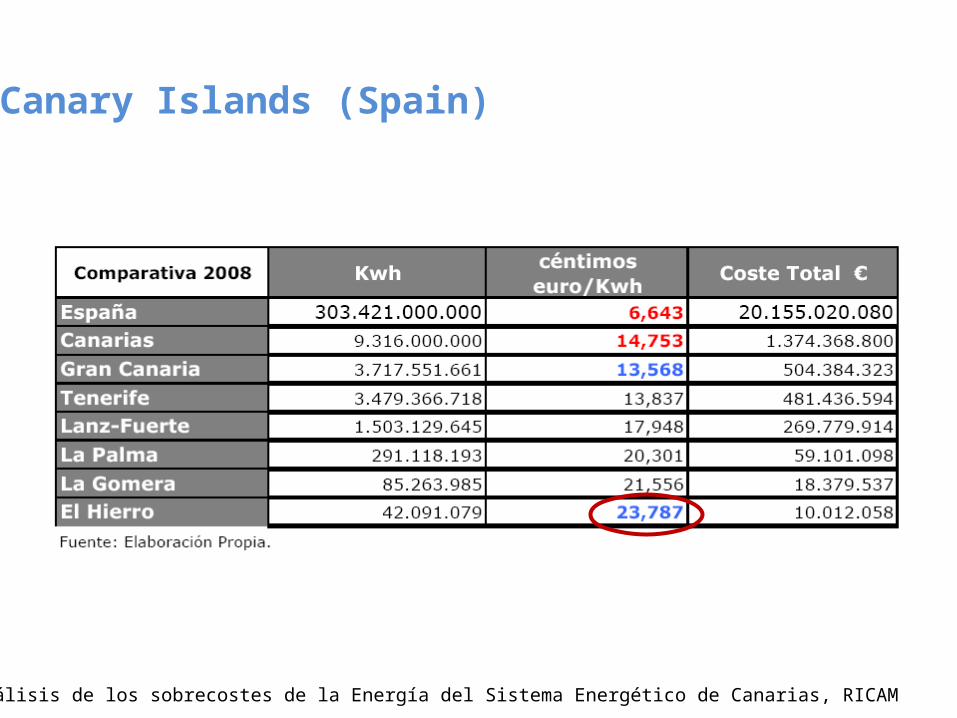

Canary Islands (Spain)

Canary Islands (Spain)

Source: Análisis de los sobrecostes de la Energía del Sistema Energético de Canarias, RICAM

Nuclear: 38%Coal and Lignite: 34%Hydroelectric: 24%Natural Gas: 3%Biomass and others: 1%

Slovenia

Hydro-electric: 56.6%Thermal: 31.2%Geothermal: 6.7%Wind: 5.3%Biogas: ~0.3

New Zealand Canary Islands

Fossil based: 90.5%Renewables: 5.7%Others: 3.8%

90% RES by 2025

El Hierro, 100% RES 2012

All islands, 30% RES 2015

Comment

Convenience for separation of electricity generation, transmission and distribution depends on case by case, including aspects like market size, current competition, companies ownership, geographical conditions and diversity of energy resources: natural gas, hydro, nuclear, oil, coal, solar, wind.

Separation of electricity sector in Jamaica is an option to develop a more diversified energy mix, incentive competition and introduce RES.

Outline:

1. Current market structure in Jamaica

2. Unbundling the electricity sector

3. Current situation in CARICOM

4. Unbundled markets in countries with similar conditions to Jamaica

(cases: Slovenia, New Zealand and Canary Islands)

5. Current proposals to isolated electric systems (islands)

6. Conclusions

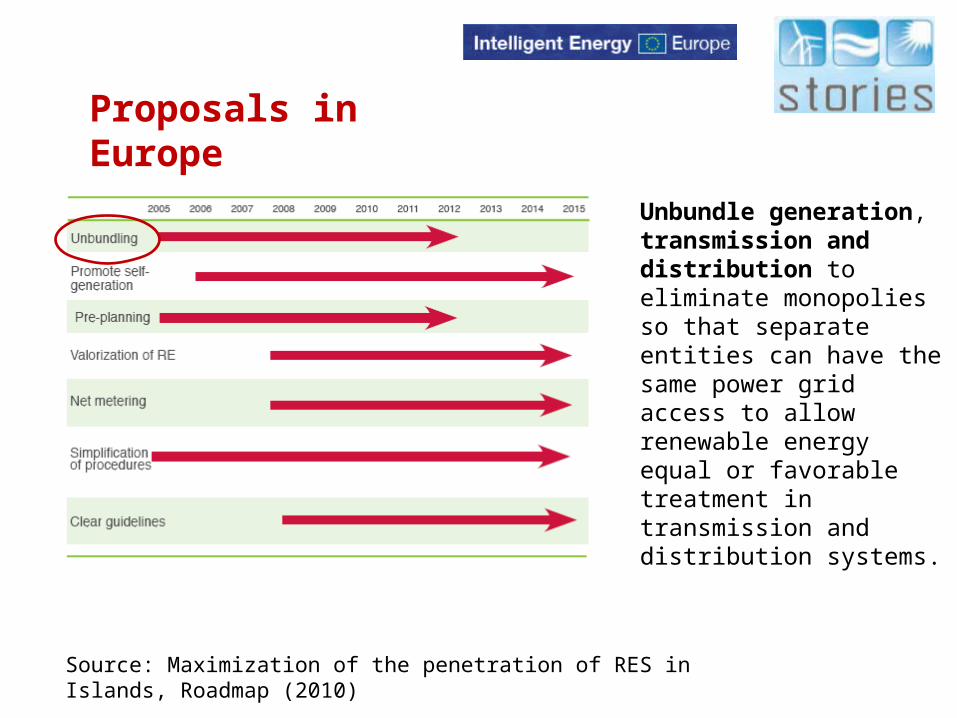

Proposals in Europe

Unbundle generation, transmission and distribution to eliminate monopolies so that separate entities can have the same power grid access to allow renewable energy equal or favorable treatment in transmission and distribution systems.

Source: Maximization of the penetration of RES in Islands, Roadmap (2010)

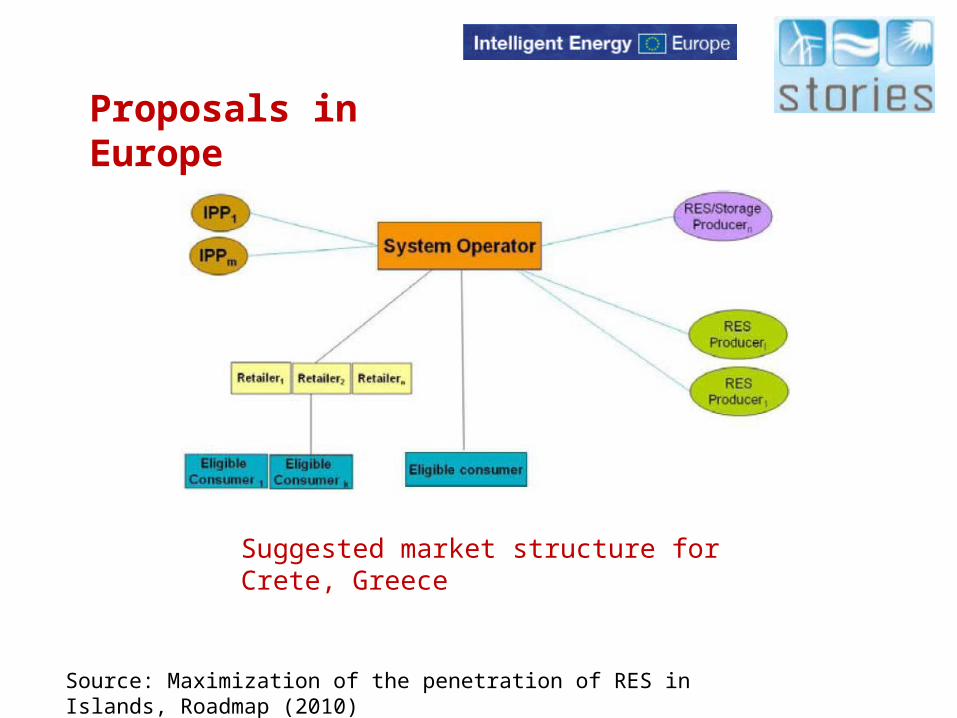

Suggested market structure for Crete, Greece

Source: Maximization of the penetration of RES in Islands, Roadmap (2010)

Proposals in Europe

Outline:

1. Current market structure in Jamaica

2. Unbundling the electricity sector and advantages

3. Unbundled markets in countries with similar conditions to Jamaica

(cases: Slovenia, New Zealand and Canary Islands)

4. Current proposals to isolated electric systems (islands)

5. Conclusions

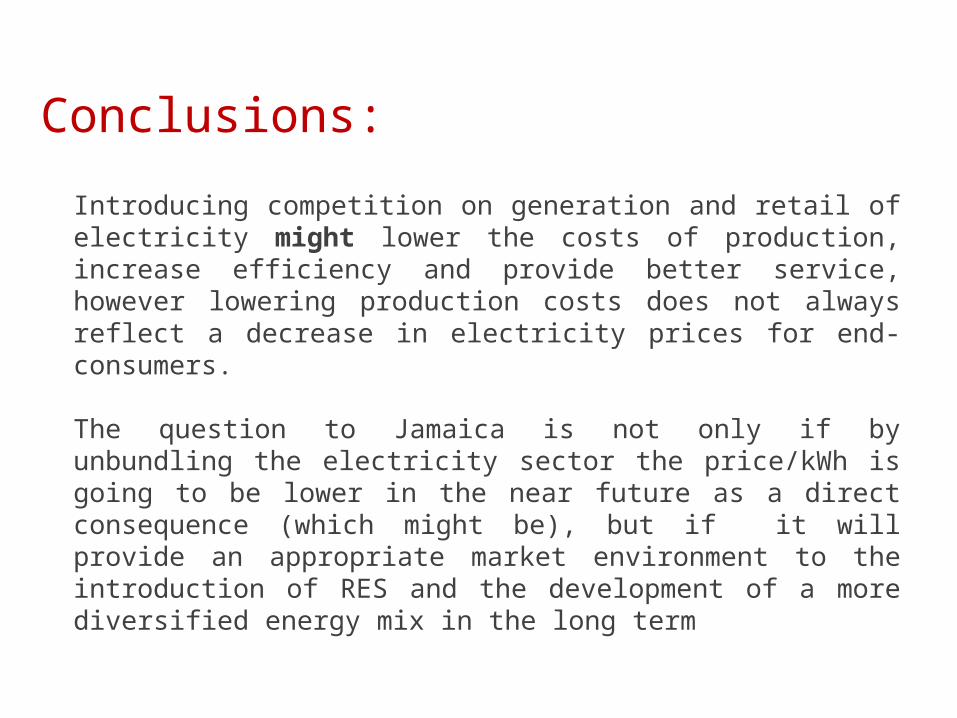

Introducing competition on generation and retail of electricity might lower the costs of production, increase efficiency and provide better service, however lowering production costs does not always reflect a decrease in electricity prices for end-consumers.

The question to Jamaica is not only if by unbundling the electricity sector the price/kWh is going to be lower in the near future as a direct consequence (which might be), but if it will provide an appropriate market environment to the introduction of RES and the development of a more diversified energy mix in the long term

Conclusions:

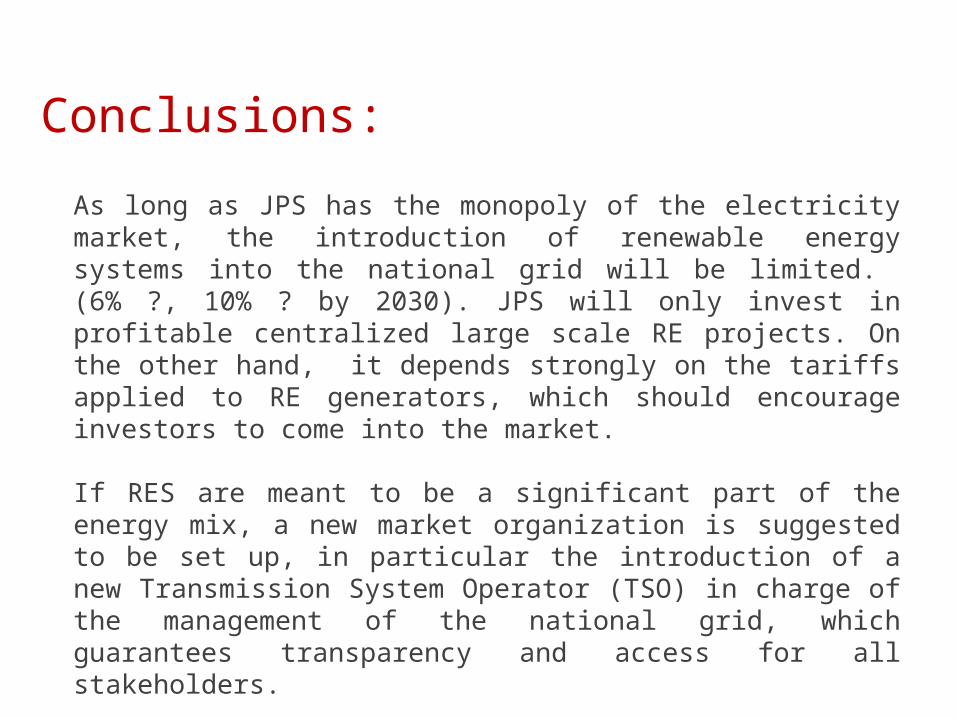

As long as JPS has the monopoly of the electricity market, the introduction of renewable energy systems into the national grid will be limited. (6% ?, 10% ? by 2030). JPS will only invest in profitable centralized large scale RE projects. On the other hand, it depends strongly on the tariffs applied to RE generators, which should encourage investors to come into the market.

If RES are meant to be a significant part of the energy mix, a new market organization is suggested to be set up, in particular the introduction of a new Transmission System Operator (TSO) in charge of the management of the national grid, which guarantees transparency and access for all stakeholders.

Conclusions:

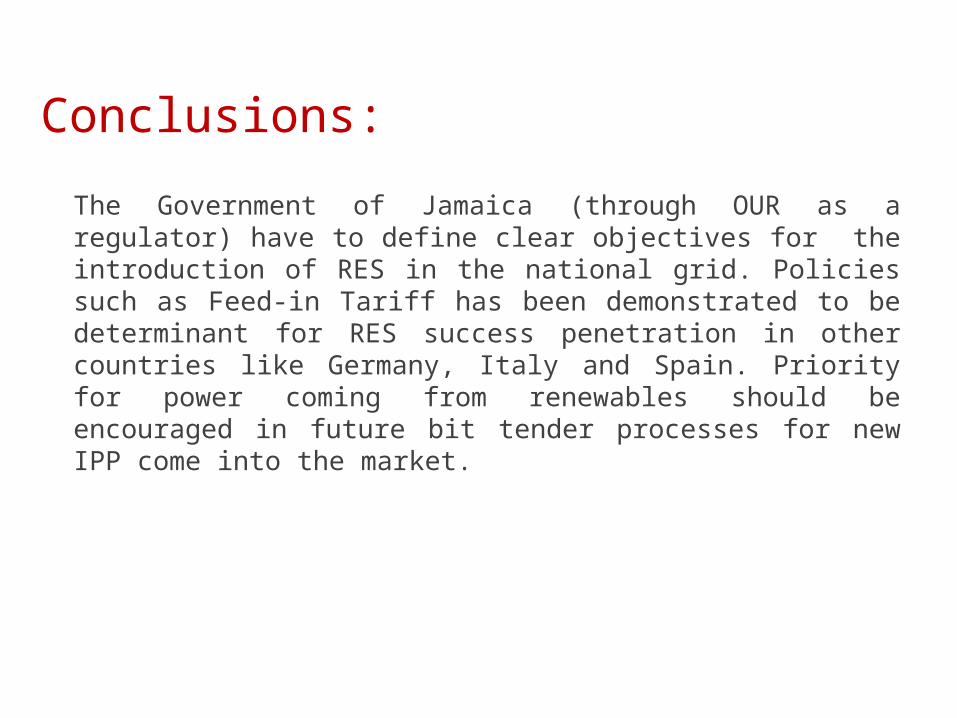

The Government of Jamaica (through OUR as a regulator) have to define clear objectives for the introduction of RES in the national grid. Policies such as Feed-in Tariff has been demonstrated to be determinant for RES success penetration in other countries like Germany, Italy and Spain. Priority for power coming from renewables should be encouraged in future bit tender processes for new IPP come into the market.

Conclusions:

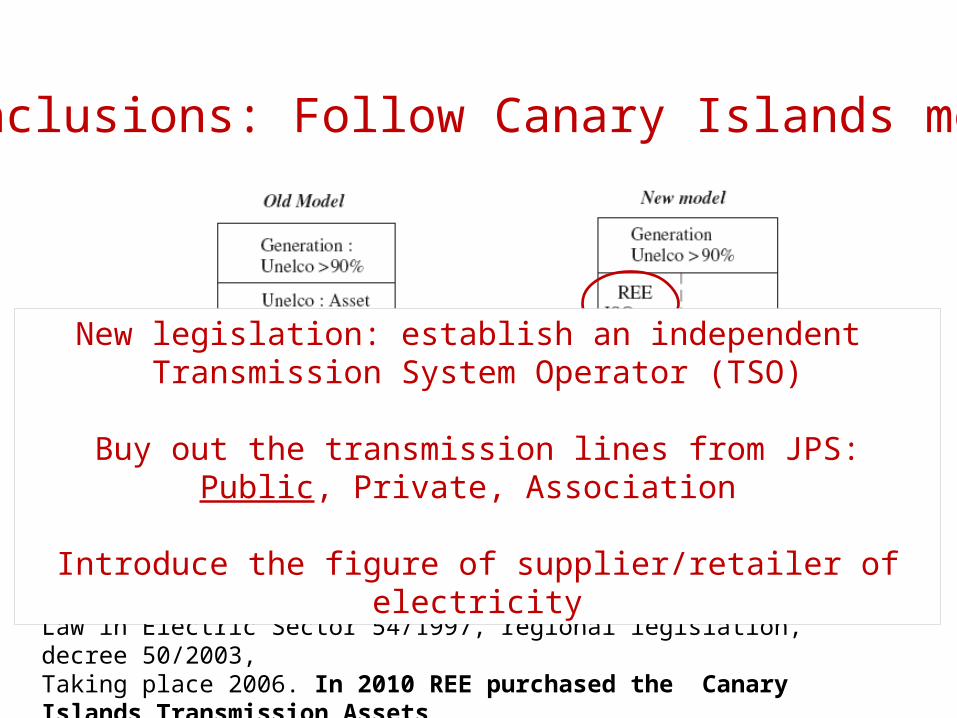

Conclusions: Follow Canary Islands model?

Law in Electric Sector 54/1997, regional legislation, decree 50/2003, Taking place 2006. In 2010 REE purchased the Canary Islands Transmission Assets

New legislation: establish an independent Transmission System Operator (TSO)

Buy out the transmission lines from JPS: Public, Private, Association

Introduce the figure of supplier/retailer of electricity

JPS: Transmission Lines

JPS: Generators

74%?

JPS: Distribution

Single BuyerIPP

Customers

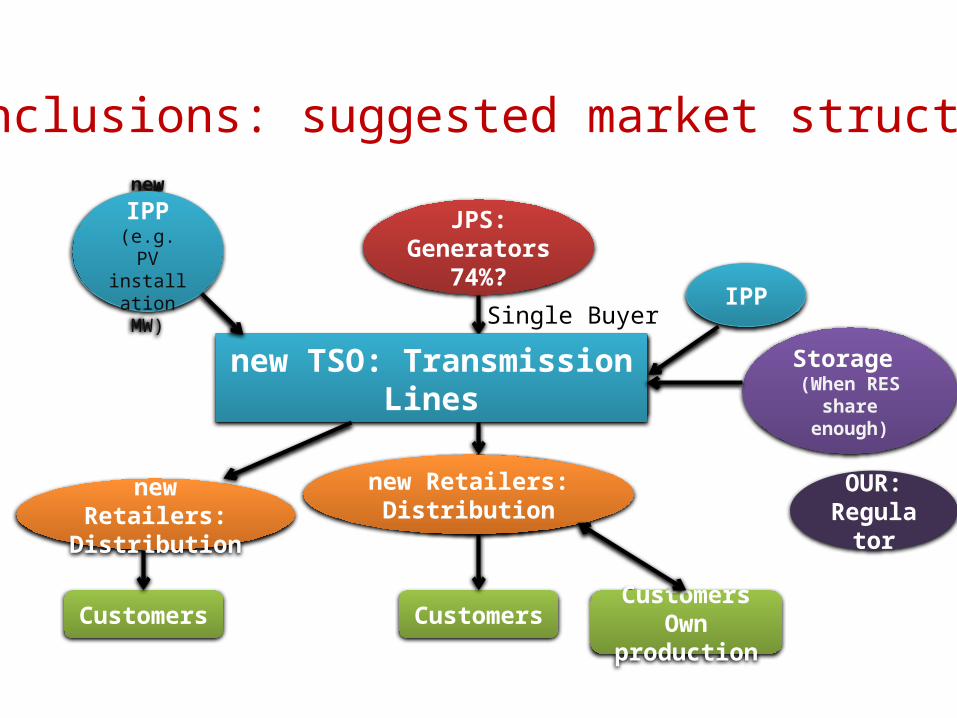

Conclusions: suggested market structure

new TSO: Transmission Lines

new Retailers: Distribution

new IPP(e.g. PV

installation MW)

CustomersOwn production

Storage (When RES share

enough)

new Retailers: Distribution

Customers

OUR: Regulator

Promoting RES in Islands:

Maximization of the penetration of RES in islands: Road Maphttp://www.storiesproject.eu/docs/STORIES_ROAD_MAP_BROCHURE_EN_20042010.pdf

Market organization of autonomous electricity systemshttp://www.storiesproject.eu/docs/Market_organisation_E_Panteri.pdf

Scheme for market organization of autonomous electricity systemshttp://www.storiesproject.eu/docs/STORIES_Deliverable3_4FINAL__2_.pdf

On the economics of electricity consumption in small island developing states: a role for renewable energy technologies?Daniel Weisser, Imperial College London, 2004

Reforms in the electricity sector:How renewables will change electricity markets in the next five years Ruggero Schleicher-Tappeser n Sustainable Strategies, Berchtesgadener Str.8 , 10779 Berlin, Germany (2012)

Electricity Market Reform: An International PerspectiveFereidoon Sioshansi, 2006

Power sector reform in small island developing states: what role for renewable nergytechnologies?Daniel Weisser, Imperial College London, 2003

How to make a European integrated market in small and isolated electricity systems? The case of the Canary IslandsYannick Perez, Francisco Javier Ramos RealEnergy Policyhttp://jsea.org.jm/docs/

Competition, regulation and privatisation of electricity generation in developing countries: does the sequencing of the reforms matter?Yinfang Zhang, University of Manchester 2005

Thank you

Any Questions

Find the presentation in our website: www.jsea.org.jm/docs Contact for questions: Alberto Gonzalez, [email protected]

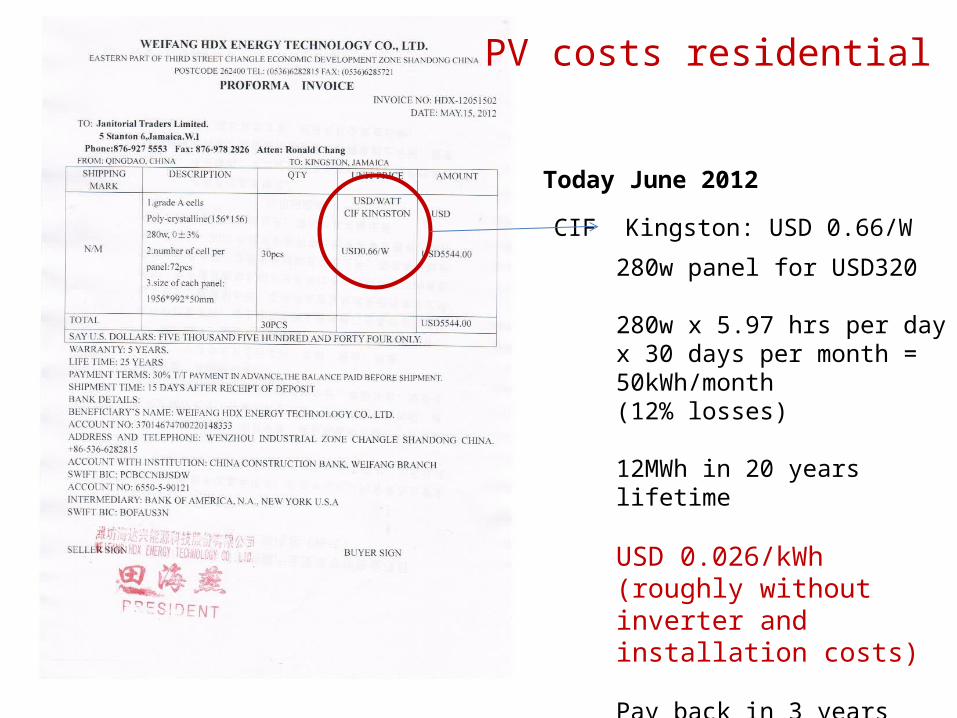

CIF Kingston: USD 0.66/W

280w panel for USD320

280w x 5.97 hrs per day x 30 days per month = 50kWh/month(12% losses)

12MWh in 20 years lifetime

USD 0.026/kWh (roughly without inverter and installation costs)

Pay back in 3 years with Current prices from JPS

Today June 2012

PV costs residential