Embed Size (px)

Citation preview

©FSTP fstp.co.uk

Condensed Summary on Extending the Senior

Managers & Certification Regime to FCA firms

incorporating CP17/25, CP17/40 and PS18/14-

near final rules This paper provides you with a condensed summary of the key factors you will need to consider within your

firm to implement the requirements of the Senior Managers and Certification Regime. The implementation

date has been set for the 9th December 2019.

As with the other Papers on these highly impactful regulatory requirements, we have looked to condense the

content to give you valuable insight into the regulator s proposals for firms other than Banks, Building

societies, Credit Unions, Designated Investment Firms and Insurance Companies.

We have extracted the key information and presented it in a tabularised format for ease of reference. The four

main areas:

• The Senior Managers Regime

• The Certification Regime

• The Conduct Rules

• Fitness and Propriety Requirements

Within those four areas we have disseminated the information further into:

• Firms affected Core Regime, Enhanced Regime or Limited scope

• Individuals affected

• Key implications

The Senior Managers Regime

Firms who will

be affected by

2018

All sole regulated firms i.e. those only regulated by the FCA.

All firms will be affected by the Core Regime requirements apart from those firms who are

identified as Limited Scope (currently Limited Application of the Approved Persons

scheme):

• Limited Permission Consumer Credit Firms

• all sole traders

• authorised professional firms whose only regulated activities are in non-mainstream

regulated activities

• oil market participants

• service companies

• energy market participants

• subsidiaries of local authorities or registered social landlords

• insurance intermediaries whose principal business is not insurance intermediation and

who only have permission to carry on insurance mediation activity in relation to non-

investment insurance contracts

• authorised internally managed Alternative Investment Funds

©FSTP fstp.co.uk

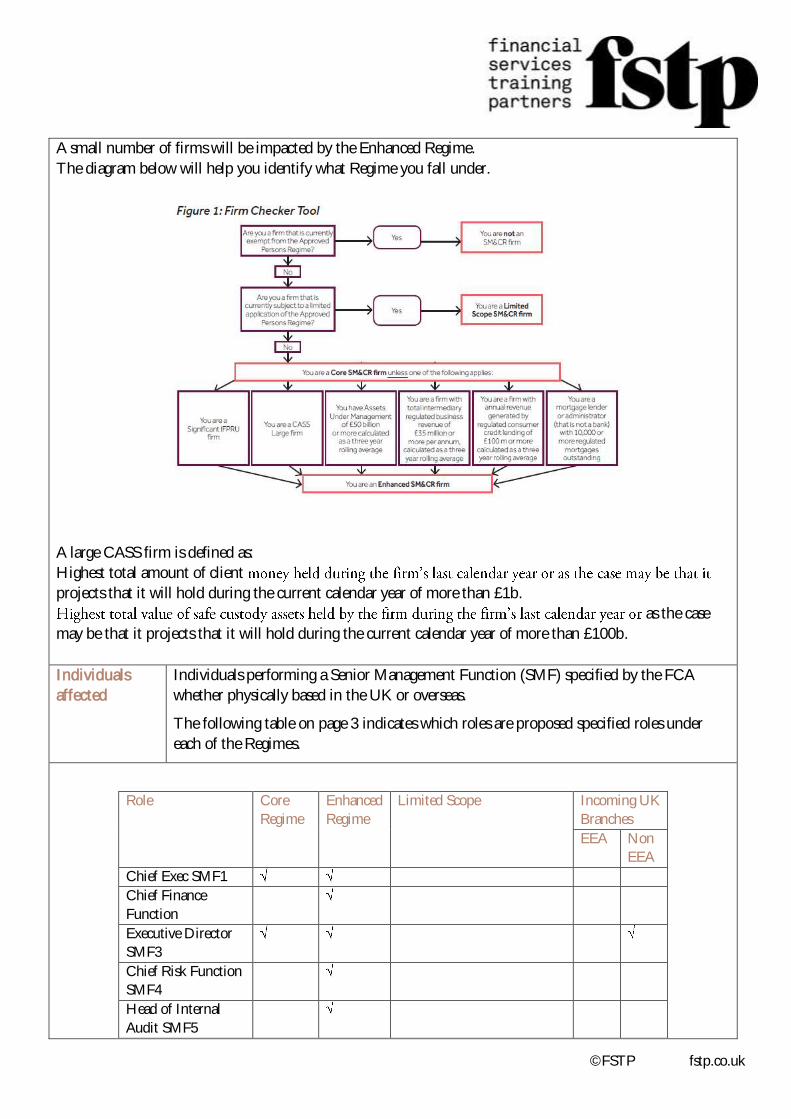

A small number of firms will be impacted by the Enhanced Regime.

The diagram below will help you identify what Regime you fall under.

A large CASS firm is defined as:

Highest total amount of client

projects that it will hold during the current calendar year of more than £1b.

as the case

may be that it projects that it will hold during the current calendar year of more than £100b.

Individuals

affected

Individuals performing a Senior Management Function (SMF) specified by the FCA

whether physically based in the UK or overseas.

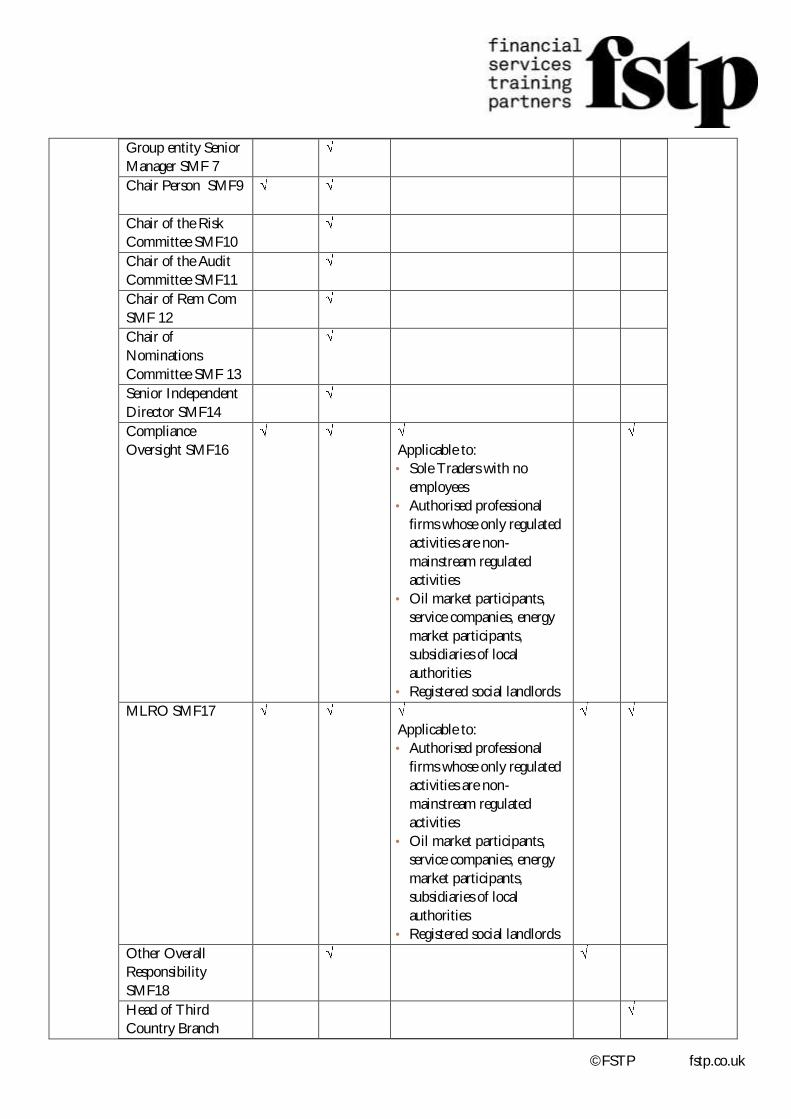

The following table on page 3 indicates which roles are proposed specified roles under

each of the Regimes.

Role Core

Regime

Enhanced

Regime

Limited Scope Incoming UK

Branches

EEA Non

EEA

Chief Exec SMF1

Chief Finance

Function

Executive Director

SMF3

Chief Risk Function

SMF4

Head of Internal

Audit SMF5

©FSTP fstp.co.uk

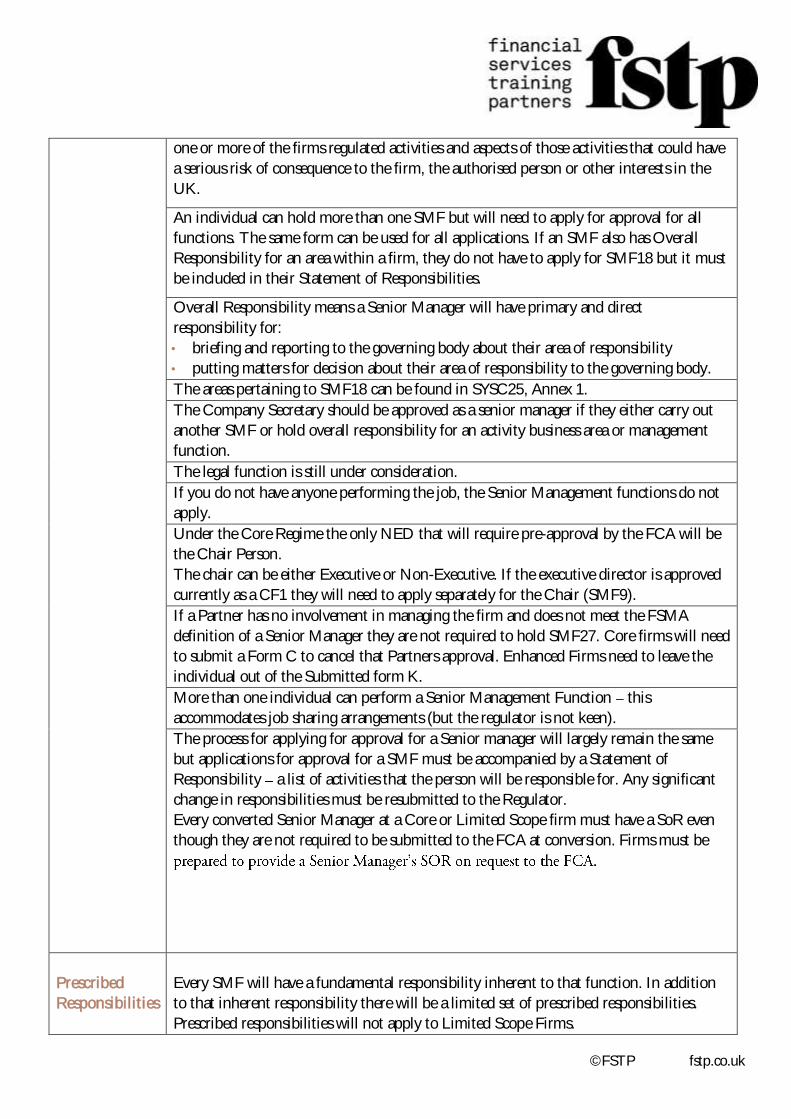

Group entity Senior

Manager SMF 7

Chair Person SMF9

Chair of the Risk

Committee SMF10

Chair of the Audit

Committee SMF11

Chair of Rem Com

SMF 12

Chair of

Nominations

Committee SMF 13

Senior Independent

Director SMF14

Compliance

Oversight SMF16

Applicable to:

• Sole Traders with no

employees

• Authorised professional

firms whose only regulated

activities are non-

mainstream regulated

activities

• Oil market participants,

service companies, energy

market participants,

subsidiaries of local

authorities

• Registered social landlords

MLRO SMF17

Applicable to:

• Authorised professional

firms whose only regulated

activities are non-

mainstream regulated

activities

• Oil market participants,

service companies, energy

market participants,

subsidiaries of local

authorities

• Registered social landlords

Other Overall

Responsibility

SMF18

Head of Third

Country Branch

©FSTP fstp.co.uk

SMF19

EEA Branch Senior

Manager SMF21

Chief Operations

Function SMF24

Partner SMF27

Limited Scope

SMF29

(This is the same as the

Apportionment and

Oversight Function under

the Approved Persons

Limited Permission)

Applicable to: • Consumer Credit firms

that have a CF8 under the

Approved Persons Regime

• Insurance intermediaries

whose principal business is

not insurance

intermediation and who

only have permission to

carry on insurance

mediation activity in

relation to non-investment

insurance contracts

• Authorised professional

firms whose only regulated

activities are non-

mainstream regulated

activities

• Oil market participants,

service companies, energy

market participants,

subsidiaries of local

authorities

• Registered social landlords

Key

implications

Significant Influence Functions will be replaced with Senior Management Functions,

SMFs.

A person performing a Senior Management Function will be responsible for managing

©FSTP fstp.co.uk

one or more of the firms regulated activities and aspects of those activities that could have

a serious risk of consequence to the firm, the authorised person or other interests in the

UK.

An individual can hold more than one SMF but will need to apply for approval for all

functions. The same form can be used for all applications. If an SMF also has Overall

Responsibility for an area within a firm, they do not have to apply for SMF18 but it must

be included in their Statement of Responsibilities.

Overall Responsibility means a Senior Manager will have primary and direct

responsibility for:

• briefing and reporting to the governing body about their area of responsibility

• putting matters for decision about their area of responsibility to the governing body.

The areas pertaining to SMF18 can be found in SYSC25, Annex 1.

The Company Secretary should be approved as a senior manager if they either carry out

another SMF or hold overall responsibility for an activity business area or management

function.

The legal function is still under consideration.

If you do not have anyone performing the job, the Senior Management functions do not

apply.

Under the Core Regime the only NED that will require pre-approval by the FCA will be

the Chair Person.

The chair can be either Executive or Non-Executive. If the executive director is approved

currently as a CF1 they will need to apply separately for the Chair (SMF9).

If a Partner has no involvement in managing the firm and does not meet the FSMA

definition of a Senior Manager they are not required to hold SMF27. Core firms will need

to submit a Form C to cancel that Partners approval. Enhanced Firms need to leave the

individual out of the Submitted form K.

More than one individual can perform a Senior Management Function this

accommodates job sharing arrangements (but the regulator is not keen).

The process for applying for approval for a Senior manager will largely remain the same

but applications for approval for a SMF must be accompanied by a Statement of

Responsibility a list of activities that the person will be responsible for. Any significant

change in responsibilities must be resubmitted to the Regulator.

Every converted Senior Manager at a Core or Limited Scope firm must have a SoR even

though they are not required to be submitted to the FCA at conversion. Firms must be

Prescribed

Responsibilities

Every SMF will have a fundamental responsibility inherent to that function. In addition

to that inherent responsibility there will be a limited set of prescribed responsibilities.

Prescribed responsibilities will not apply to Limited Scope Firms.

©FSTP fstp.co.uk

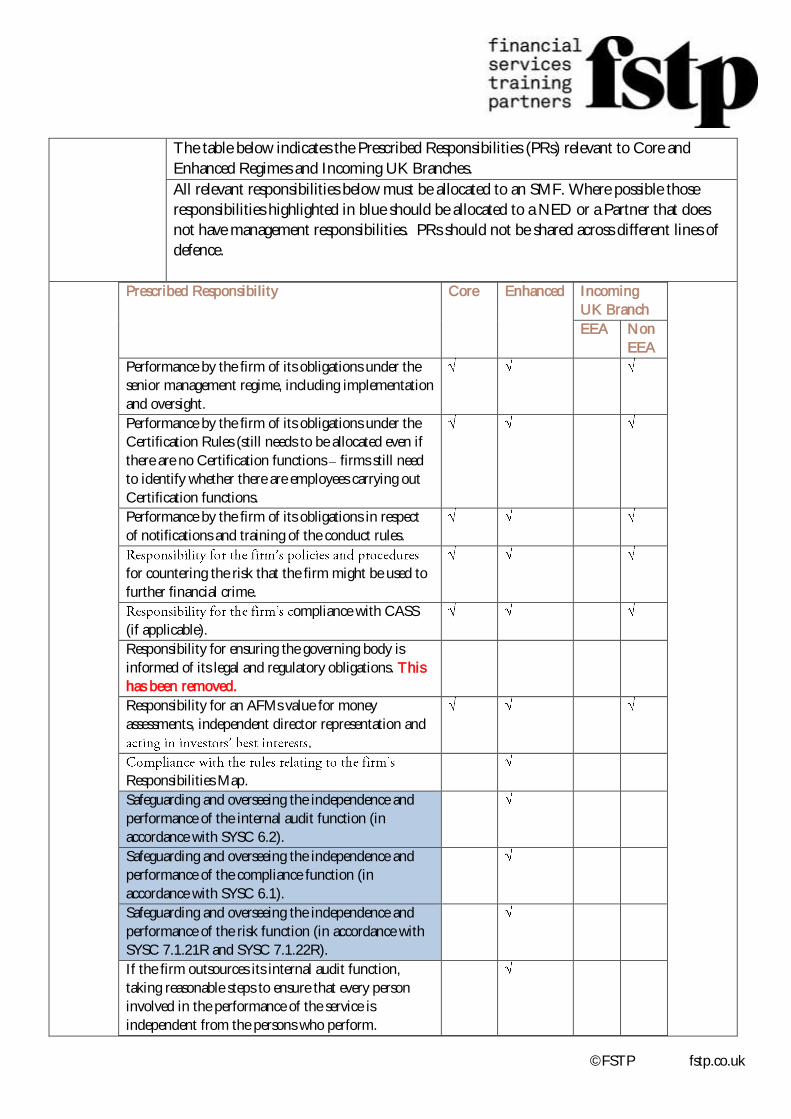

The table below indicates the Prescribed Responsibilities (PRs) relevant to Core and

Enhanced Regimes and Incoming UK Branches.

All relevant responsibilities below must be allocated to an SMF. Where possible those

responsibilities highlighted in blue should be allocated to a NED or a Partner that does

not have management responsibilities. PRs should not be shared across different lines of

defence.

Prescribed Responsibility Core Enhanced Incoming

UK Branch

EEA Non

EEA

Performance by the firm of its obligations under the

senior management regime, including implementation

and oversight.

Performance by the firm of its obligations under the

Certification Rules (still needs to be allocated even if

there are no Certification functions firms still need

to identify whether there are employees carrying out

Certification functions.

Performance by the firm of its obligations in respect

of notifications and training of the conduct rules.

for countering the risk that the firm might be used to

further financial crime.

ompliance with CASS

(if applicable).

Responsibility for ensuring the governing body is

informed of its legal and regulatory obligations. This

has been removed.

Responsibility for an AFMs value for money

assessments, independent director representation and

.

Responsibilities Map.

Safeguarding and overseeing the independence and

performance of the internal audit function (in

accordance with SYSC 6.2).

Safeguarding and overseeing the independence and

performance of the compliance function (in

accordance with SYSC 6.1).

Safeguarding and overseeing the independence and

performance of the risk function (in accordance with

SYSC 7.1.21R and SYSC 7.1.22R).

If the firm outsources its internal audit function,

taking reasonable steps to ensure that every person

involved in the performance of the service is

independent from the persons who perform.

©FSTP fstp.co.uk

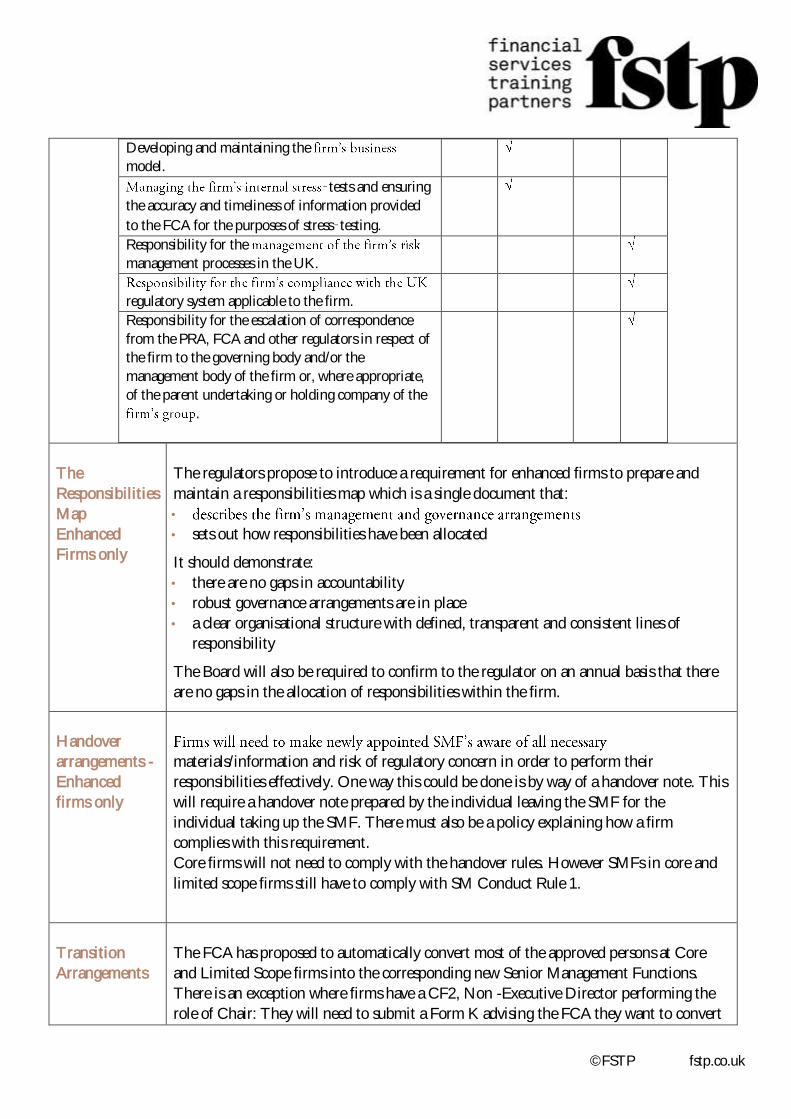

Developing and maintaining the

model.

‑tests and ensuring

the accuracy and timeliness of information provided

to the FCA for the purposes of stress‑testing.

Responsibility for the

management processes in the UK.

regulatory system applicable to the firm.

Responsibility for the escalation of correspondence

from the PRA, FCA and other regulators in respect of

the firm to the governing body and/or the

management body of the firm or, where appropriate,

of the parent undertaking or holding company of the

.

The

Responsibilities

Map

Enhanced

Firms only

The regulators propose to introduce a requirement for enhanced firms to prepare and

maintain a responsibilities map which is a single document that:

•

• sets out how responsibilities have been allocated

It should demonstrate:

• there are no gaps in accountability

• robust governance arrangements are in place

• a clear organisational structure with defined, transparent and consistent lines of

responsibility

The Board will also be required to confirm to the regulator on an annual basis that there

are no gaps in the allocation of responsibilities within the firm.

Handover

arrangements -

Enhanced

firms only

materials/information and risk of regulatory concern in order to perform their

responsibilities effectively. One way this could be done is by way of a handover note. This

will require a handover note prepared by the individual leaving the SMF for the

individual taking up the SMF. There must also be a policy explaining how a firm

complies with this requirement.

Core firms will not need to comply with the handover rules. However SMFs in core and

limited scope firms still have to comply with SM Conduct Rule 1.

Transition

Arrangements

The FCA has proposed to automatically convert most of the approved persons at Core

and Limited Scope firms into the corresponding new Senior Management Functions.

There is an exception where firms have a CF2, Non -Executive Director performing the

role of Chair: They will need to submit a Form K advising the FCA they want to convert

©FSTP fstp.co.uk

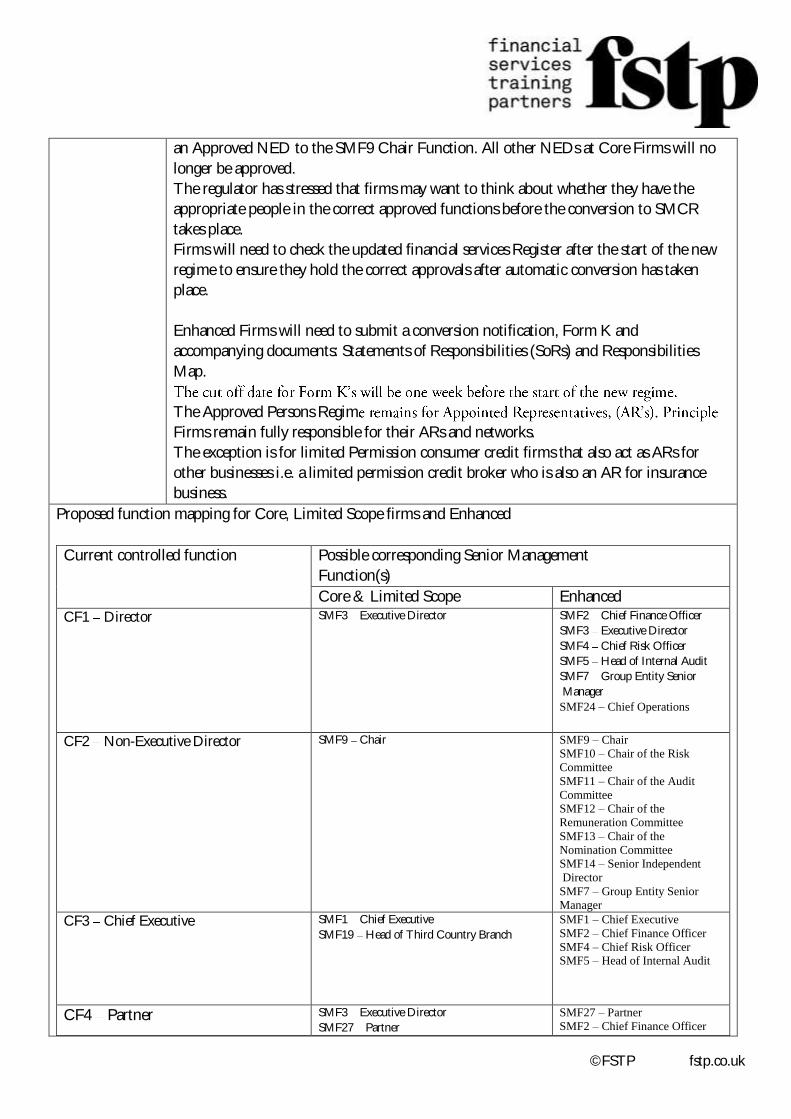

an Approved NED to the SMF9 Chair Function. All other NEDs at Core Firms will no

longer be approved.

The regulator has stressed that firms may want to think about whether they have the

appropriate people in the correct approved functions before the conversion to SMCR

takes place.

Firms will need to check the updated financial services Register after the start of the new

regime to ensure they hold the correct approvals after automatic conversion has taken

place.

Enhanced Firms will need to submit a conversion notification, Form K and

accompanying documents: Statements of Responsibilities (SoRs) and Responsibilities

Map.

The Approved Persons Regim

Firms remain fully responsible for their ARs and networks.

The exception is for limited Permission consumer credit firms that also act as ARs for

other businesses i.e. a limited permission credit broker who is also an AR for insurance

business.

Proposed function mapping for Core, Limited Scope firms and Enhanced

Current controlled function Possible corresponding Senior Management

Function(s)

Core & Limited Scope Enhanced

CF1 Director SMF3 Executive Director SMF2 Chief Finance Officer

SMF3 Executive Director

SMF4 Chief Risk Officer

SMF5 Head of Internal Audit

SMF7 Group Entity Senior

Manager

SMF24 – Chief Operations

CF2 Non-Executive Director SMF9 Chair SMF9 – Chair

SMF10 – Chair of the Risk

Committee

SMF11 – Chair of the Audit

Committee

SMF12 – Chair of the

Remuneration Committee

SMF13 – Chair of the

Nomination Committee

SMF14 – Senior Independent

Director

SMF7 – Group Entity Senior

Manager

CF3 Chief Executive SMF1 Chief Executive

SMF19 Head of Third Country Branch SMF1 – Chief Executive

SMF2 – Chief Finance Officer

SMF4 – Chief Risk Officer SMF5 – Head of Internal Audit

CF4 Partner SMF3 Executive Director

SMF27 Partner SMF27 – Partner

SMF2 – Chief Finance Officer

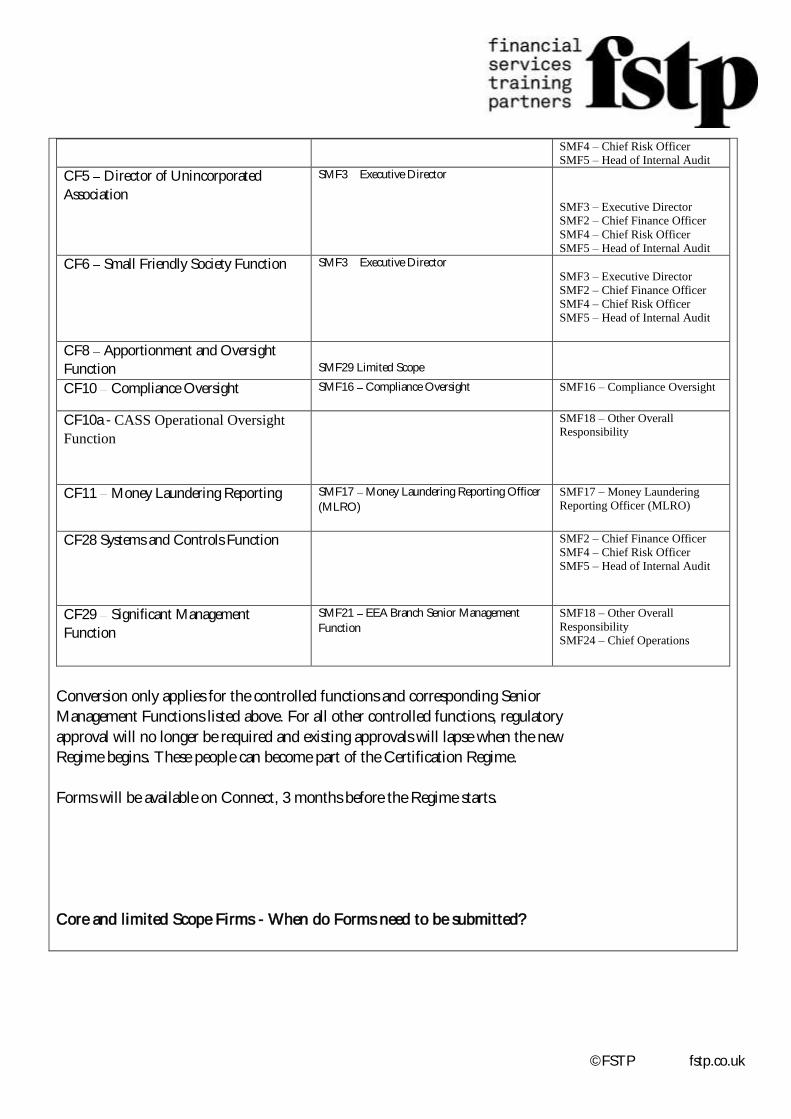

©FSTP fstp.co.uk

SMF4 – Chief Risk Officer

SMF5 – Head of Internal Audit

CF5 Director of Unincorporated

Association

SMF3 Executive Director

SMF3 – Executive Director

SMF2 – Chief Finance Officer

SMF4 – Chief Risk Officer

SMF5 – Head of Internal Audit

CF6 Small Friendly Society Function SMF3 Executive Director

SMF3 – Executive Director

SMF2 – Chief Finance Officer

SMF4 – Chief Risk Officer

SMF5 – Head of Internal Audit

CF8 Apportionment and Oversight

Function

SMF29 Limited Scope

CF10 Compliance Oversight SMF16 Compliance Oversight SMF16 – Compliance Oversight

CF10a - CASS Operational Oversight

Function

SMF18 – Other Overall Responsibility

CF11 Money Laundering Reporting SMF17 Money Laundering Reporting Officer

(MLRO) SMF17 – Money Laundering

Reporting Officer (MLRO)

CF28 Systems and Controls Function SMF2 – Chief Finance Officer

SMF4 – Chief Risk Officer

SMF5 – Head of Internal Audit

CF29 Significant Management

Function

SMF21 EEA Branch Senior Management

Function

SMF18 – Other Overall

Responsibility

SMF24 – Chief Operations

Conversion only applies for the controlled functions and corresponding Senior

Management Functions listed above. For all other controlled functions, regulatory

approval will no longer be required and existing approvals will lapse when the new

Regime begins. These people can become part of the Certification Regime.

Forms will be available on Connect, 3 months before the Regime starts.

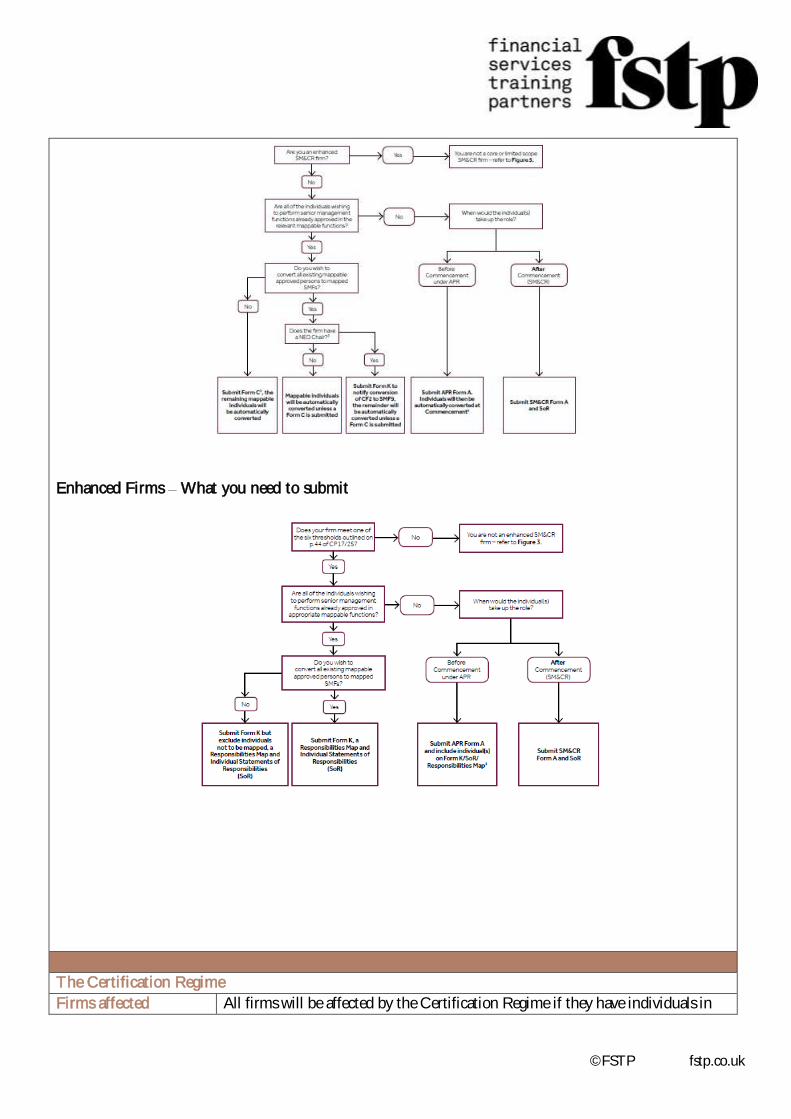

Core and limited Scope Firms - When do Forms need to be submitted?

©FSTP fstp.co.uk

Enhanced Firms What you need to submit

The Certification Regime

Firms affected All firms will be affected by the Certification Regime if they have individuals in

©FSTP fstp.co.uk

the roles below.

Individuals affected activities

• Significant Management Function (based on current CF29)

• Proprietary traders (based on Current CF29)

• CASS oversight (based on current CF10a)

• Certain material risk takers people whose actions could have a material

impact on the risk profile of the firm

• Functions subject to qualification requirement e.g. Financial Advisers,

Investment Managers and Mortgage Advisers

• The Client Dealing function

• Individuals who supervise or manage another person who is covered by the

certification regime (not applicable if they are already an SMF)

• Algorithmic trading

The term Significant Harm function has now changed to FCA Certification

Function.

Certification only applies to individuals if they perform their function from an

establishment in the UK or are dealing with a client in the UK. Individuals

should be certified if they work more than 30 days a year in the UK.

Material risk takers under the Remuneration code are an exception Certification

applies even if they are based overseas and do not deal with a UK client.

Key implications Individuals covered by the Certification Regime will not be registered individually

with the FCA.

Firms will certification

function are fit and proper to do so. If the person was performing the role prior

to it becoming a certification function references from previous employers does

not apply.

The Regulators will not approve employees within the scope of the certification

regime but will require a Senior Manager within the firm to assume

responsibility for the internal assessment and certification process.

More than one individual can perform a function in scope of the Certification

Regime at the same firm accommodates job sharing arrangements.

If an employee performs multiple certification functions within their role each

certification function will need to be assessed against the specific fit and proper

standards, but one certificate may be used detailing all functions.

Certification will need to be renewed on an annual basis.

The treasury intends to commence the requirement for firms to certify relevant

employees for the first time 12 months after the commencement of the main

©FSTP fstp.co.uk

SMCR.

CASS A firm can allocate the CASS Prescribed Responsibility to any of the Senior

Managers, but this should be the Senior Manager who is the most senior person

responsible for this area. Once the Prescribed Responsibility has been allocated, it

might be the case that this Senior Manager also performs the CASS Oversight

Function. In this situation, as the person is an SMF there is no need for the firm

to also apply the Certification Regime to them.

Alternatively, as the CASS Oversight Function is often operationally focused, the

person performing it might not be a Senior Manager. In this case, the person with

the CASS Oversight Function will fall under the Certification Regime and will

not need pre approval by the FCA.

The New Conduct Rules

Firms affected All firms will be affected by the Conduct Rules.

Individuals affected All staff will be affected by the Conduct Rules apart from ancillary staff, such as

catering staff, which would be the same role in a non-financial service sector firm.

commencement of the SMCR Regime.

Other employees will have 12 months from the commencement date to be

trained and for the rules to apply.

Key implications The existing statements of Principle and Code of Practice for Approved Persons

will be replaced by a set of Conduct Rules.

Conduct Rules First tier Individual Conduct Rules

Rule 1: You must act with integrity.

Rule 2: You must act with due skill, care and diligence.

Rule 3: You must be open and cooperative with the FCA, the PRA and other

regulators.

Rule 4: You must pay due regard to the interests of customers and treat them

fairly.

Rule 5: You must observe proper standards of market conduct.

Second tier Senior Manager Conduct Rules

SC1: You must take reasonable steps to ensure that the business of the firm for

which you are responsible is controlled effectively.

SC2: You must take reasonable steps to ensure that the business of the firm for

which you are responsible complies with relevant requirements and standards of

the regulatory system.

SC3: You must take reasonable steps to ensure that any delegation of your

responsibilities is to an appropriate person and that you oversee the discharge of

the delegated responsibility effectively.

SC4: You must disclose appropriately any information of which the FCA or PRA

would reasonably expect notice.

©FSTP fstp.co.uk

The regulators expect all staff who are subject to the rules to be trained on the

rules so they are able to understand them. Additional training should be given to

staff on specific examples pertinent to the areas in which they work.

Firms should notify the regulators when an individual has breached the conduct

rules and/or they have taken formal disciplinary action in response to a breach of

the rules.

This needs to be completed within 7 business days of the firm becoming aware if

the person in breach is a SMF.

If the individual concerned is not an SMF then it is reported annually. The

reporting period is 1 September to 31st August and submissions need to be in

within 2 months of the end of the reporting date.

Limited permission Consumer Credit Firms will need to submit their return in

line with their annual reporting cycle.

There will be a late returns fee if the submission of the annual return is late.

Fitness and Propriety

Firms affected All firms will be affected by the Fitness and Propriety requirements.

Individuals Impacted Applicants for SMFs, holders of SMFs and individuals falling within the

Certification regime.

Key implications Assessment of fitness and propriety will need to be conducted on an annual basis.

Firms will need to advise the regulator of SMFs failing the fitness and propriety

assessment.

If an individual covered by the Certification Regime fails the fitness and propriety

assessment their certificate must not be renewed.

The rules in the FCA handbook will remain generally the same as they are

currently for assessing fitness and propriety but there will be amendments to make

the requirements clear for initial assessment and ongoing assessment especially the

evidence firms should collect as part of the process.

Criminal record checks will be required to be carried out by the firm; this will

mean firms will need to sign up to the Disclosure and Barring Service (DBS).

A criminal record check is only mandatory when a candidate is applying for a

SMF

Where candidates have spent a considerable time abroad working or living outside

the UK firms should consider doing an equivalent check with the appropriate

regulatory body if available.

If a firm wants to appoint an individual into a SMF or a Certification function

they will have to undertake references for the last 6 years employment history.

©FSTP fstp.co.uk

If a reference is requested by one relevant firm of another relevant firm they will

need to disclose if relevant:

• The candidate breached a conduct rule

• A description of the basis and outcome of disciplinary action in relation to a

breach.

• Disclose of any other information that is relevant to assessing whether

someone is fit and proper

The above are the near final rules so in all respects are good to go.

following questions helpful as the workload is bigger than you think just ask anyone who was

involved in the implementation in the Banks, Building Societies, Designated Investment Firms,

Credit Unions and Insurance Firms?

• Who are the Senior Management that will be affected?

• Who are the population affected by the Certification Regime?

• How will we assess the people affected by the Certification Regime as competent?

• Have we got the correct systems and controls in place to implement the requirements effectively?

• Do we need to revise or enhance our recruitment and other HR processes?

• Have we got the resource to undertake the implications of a project with this magnitude of change?

• How will we train people on the New Conduct rules especially considering the number of people

affected?

• How does the work we have already done for MiFID II align with the requirements for SMCR?

If you would like to talk further about the implications of the SMCR please contact:

Philippa Grocott,

Business Development Partner at FSTP

07515944636 or email [email protected]

Julia Kirkland,

Senior Partner at FSTP

07743726766 or email [email protected]