Embed Size (px)

Citation preview

Concevoir et produire des semiconducteurs en Europe: une Utopie ?

Let’s have a look…

Gérard MATHERON

MIDIS MINATEC24 avril 2009

1 – Advanced Wafer ManufacturingChallenges

3Midis Minatec – 24 april 2009 _GM

Advanced Wafer Manufacturing Challenges

Nano-Manufacturing faces three main challenges:

1. Continuous pressure on Manufacturing Costs2. Availability of Fast-Yielding Leading-Edge

Nano-Technologies3. Maintain a high degree of Flexibility and Agility

Note that these challenges are worldwide, i.e. the same everywhere…

4Midis Minatec – 24 april 2009 _GM

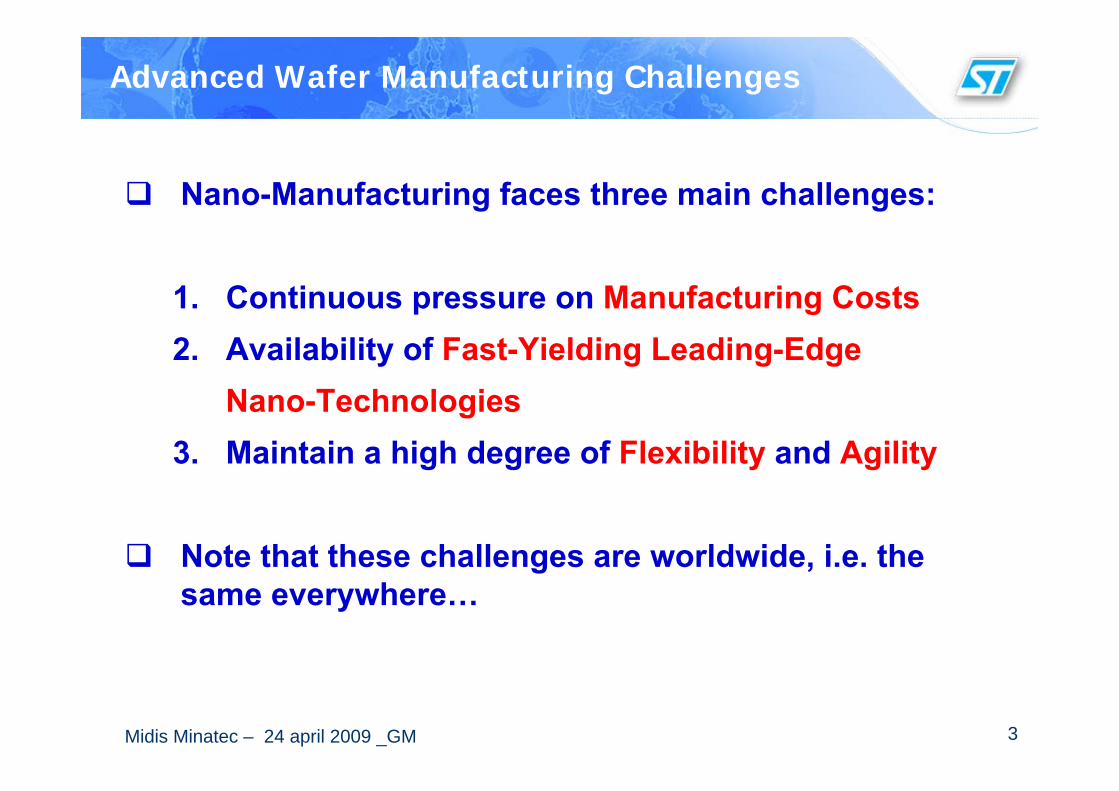

Moore’s law

0.01

0.10

1.00

10.00

J D D D D D D D D D D D D D D D D D D D D D D D D D D D D D D

19801980 19851985 19901990 1995 2000 2005 2010

Mic

rons

0.01

0.10

1.00

10.00

Years

0.15 μm0.15 μm0.18 μm0.18 μm

0.13 μm0.13 μm0.10 μm0.10 μm

0.07 μm0.07 μm0.05 μm0.05 μm

0.35 μm0.35 μm0.25 μm0.25 μm

3.0 μm3.0 μm2.0 μm2.0 μm

1.5 μm1.5 μm

1.0 μm1.0 μm

0.6 μm0.6 μm0.5 μm0.5 μm

0.4 μm0.4 μm

0.03 μm

Minimum Feature SizeMinimum Feature Size

20.000 Transistors

200.000 Transistors

8.000.000 Transistors

40.000.000 Transistors

Moore’s lawstill valid

1B Transistorsper Chip

5Midis Minatec – 24 april 2009 _GM

1 Mégabit Silicon memory

Integration doubling every 18 months enables a dramatic drop in prices per function

Moore’ s law Economic Impact

6Midis Minatec – 24 april 2009 _GM

1. Continuous pressure on Manufacturing Costs1. Continuous pressure on Manufacturing Costs

Advanced Wafer Manufacturing Challenges (1)

ASP decrease:Typically -10% per year

CostCost remains the main competitive differentiatorin Advanced Manufacturing

$0

$1 000

$2 000

$3 000

$4 000

$5 000

$6 000

$7 000

$8 000

Q1-

05

Q2-

05

Q3-

05

Q4-

05

Q1-

06

Q2-

06

Q3-

06

Q4-

06

Q1-

07

Q2-

07

Q3-

07

Q4-

07

Q1-

08

Q2-

08

Q3-

08

Q4-

08

0.25µ, Metal - 05

0.18µ, Metal - 06

0.13µ, Metal - 06

130nm, Metal - 06

90nm, Metal - 06

65nm, Metal - 08

300mm

200mm

Foundry Wafer Pricing Trend 2005-2008

Source: Gartner Dataquest

7Midis Minatec – 24 april 2009 _GM

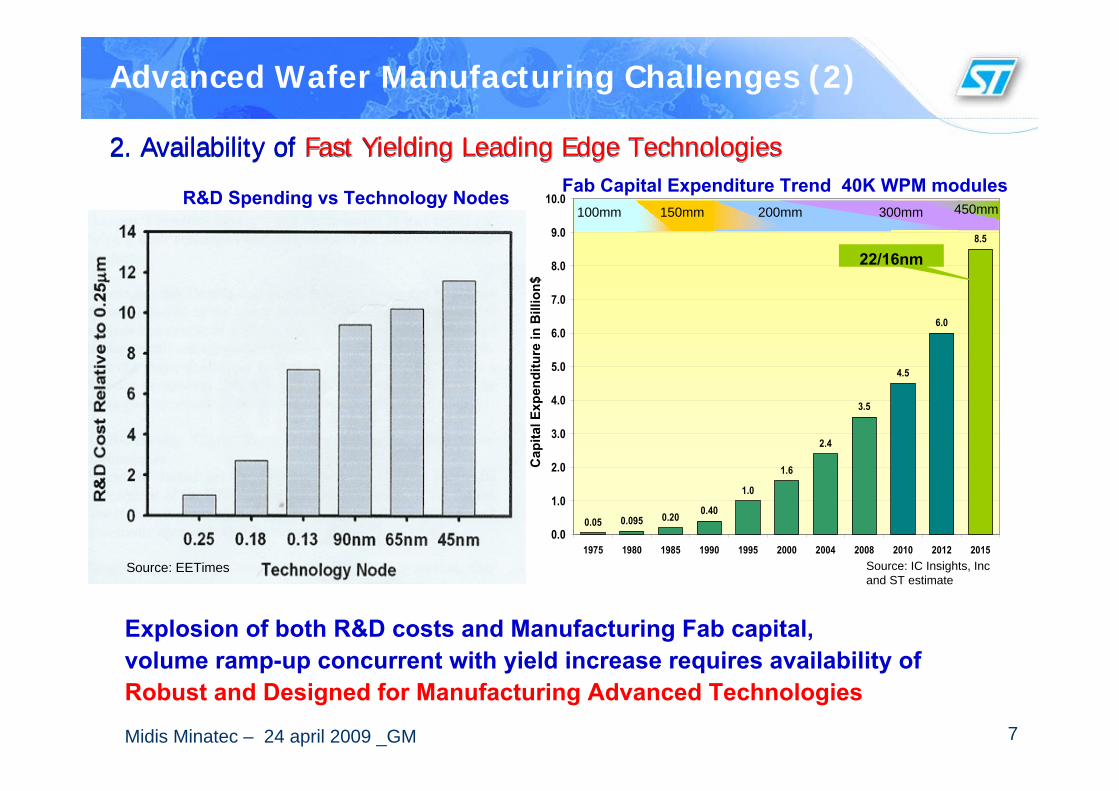

Advanced Wafer Manufacturing Challenges (2)

Explosion of both R&D costs and Manufacturing Fab capital, volume ramp-up concurrent with yield increase requires availability ofRobust and Designed for Manufacturing Advanced Technologies

2. Availability of Fast Yielding Leading Edge Technologies2. Availability of Fast Yielding Leading Edge TechnologiesFast Yielding Leading Edge Technologies

1.0

1.6

2.4

3.5

4.5

6.0

8.5

0.400.200.05 0.0950.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

1975 1980 1985 1990 1995 2000 2004 2008 2010 2012 2015

Source: EETimes

R&D Spending vs Technology Nodes

Cap

ital E

xpen

ditu

re in

Bill

ion$

22/16nm

Source: IC Insights, Incand ST estimate

Fab Capital Expenditure Trend 40K WPM modules100mm 150mm 200mm 300mm 450mm

8Midis Minatec – 24 april 2009 _GM

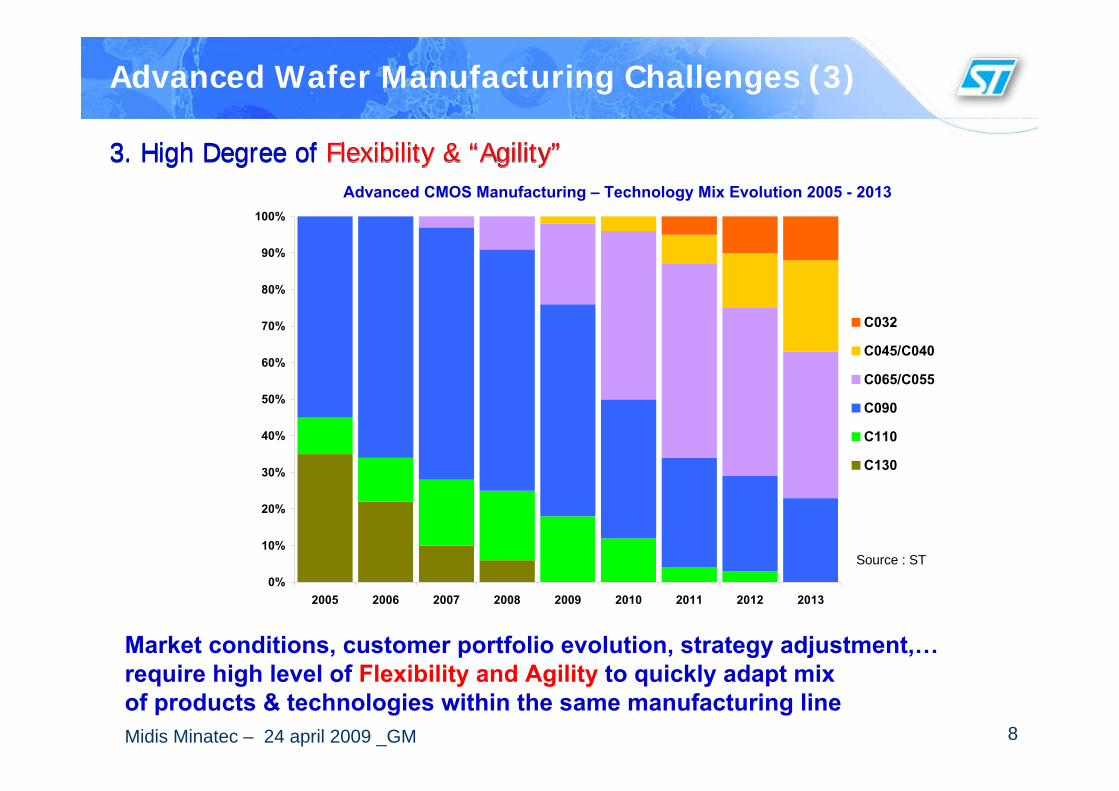

3. High Degree of Flexibility & “Agility”3. High Degree of Flexibility & Flexibility & ““AgilityAgility””

Advanced Wafer Manufacturing Challenges (3)

Market conditions, customer portfolio evolution, strategy adjustment,…require high level of Flexibility and Agility to quickly adapt mix of products & technologies within the same manufacturing line

Advanced CMOS Manufacturing – Technology Mix Evolution 2005 - 2013

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2005 2006 2007 2008 2009 2010 2011 2012 2013

C032

C045/C040

C065/C055

C090

C110

C130

Source : ST

2 – Europe positioning in Advanced Wafer Manufacturing

10Midis Minatec – 24 april 2009 _GM

Threats on Advanced Wafer Manufacturing in Europe

Costs– Currencies (€/$ exchange rate )– Labor cost– Excessive external equipment maintenance – Economical environment (taxes, incentives…) despite

some local improvements (eg Nano2012)

Dimension of Scale– Too many small size Fabs, mainly for historical reasons

Cultural– Weak education in Manufacturing Sciences and Industrial

Engineering

Constraints– Labor policies, limited flexibility in employment conditions– Legislative environment on ESH (eg REACH)

11Midis Minatec – 24 april 2009 _GM

Opportunities for Advanced Wafer Manufacturing in Europe

Leadership in R&D– World-Class industrial Laboratories & Institutes (LETI…)– High count of PhDs in process development & design– High level of R&D efforts from SC companies– Significant funding support from National & EU Authorities

Clustering– Regional Excellence Centers in R&D, Design & Manufacturing

with proximity of Suppliers and Application Centers

Market– European leadership in several strategic markets where IC’s are

providing innovation (Medical, Power, Automotive, Wireless and Environment)

Human Resources– Undisputed expertise, stability & engagement

12Midis Minatec – 24 april 2009 _GM

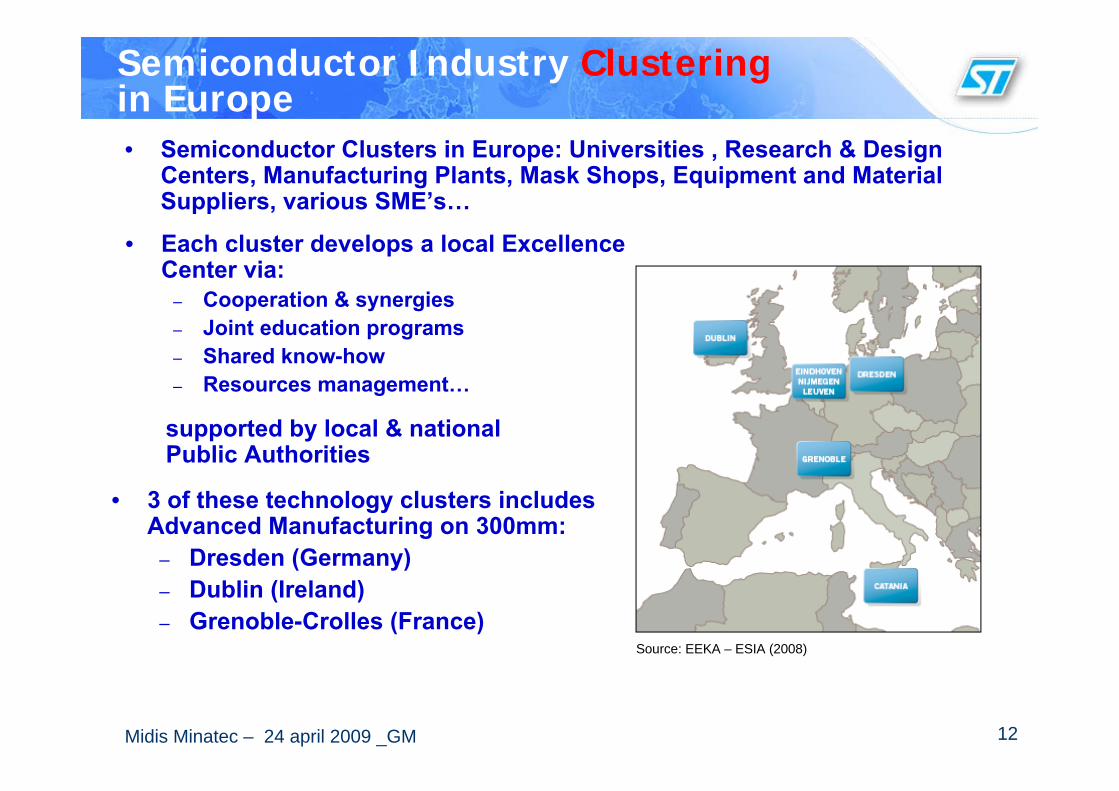

Semiconductor Industry Clusteringin Europe• Semiconductor Clusters in Europe: Universities , Research & Design

Centers, Manufacturing Plants, Mask Shops, Equipment and Material Suppliers, various SME’s…

supported by local & national Public Authorities

• 3 of these technology clusters includes Advanced Manufacturing on 300mm:

– Dresden (Germany)– Dublin (Ireland)– Grenoble-Crolles (France)

• Each cluster develops a local Excellence Center via:

– Cooperation & synergies– Joint education programs– Shared know-how– Resources management…

Source: EEKA – ESIA (2008)

13Midis Minatec – 24 april 2009 _GM

European Semiconductor Industry fueled by European Market Leaderships

European Leadership in key industry sectors helps semiconductorcompanies to keep leading edge as well, due to stronger than everprocess-system design integration

Electronic systems OEM rankings

3 - ST Strategy versus AdvancedWafer Manufacturing Industry

Slide 14

15Midis Minatec – 24 april 2009 _GM

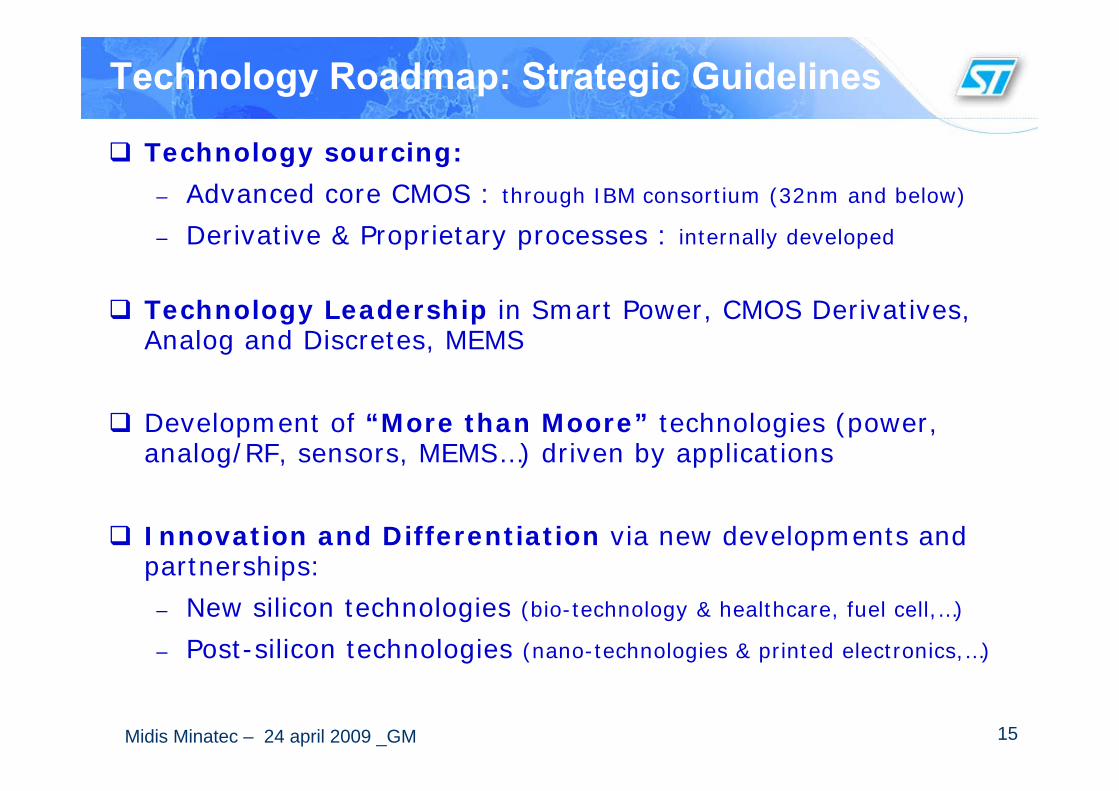

Technology Roadmap: Strategic Guidelines

Technology sourcing:

– Advanced core CMOS : through IBM consortium (32nm and below)

– Derivative & Proprietary processes : internally developed

Technology Leadership in Smart Power, CMOS Derivatives, Analog and Discretes, MEMS

Development of “More than Moore” technologies (power, analog/RF, sensors, MEMS…) driven by applications

Innovation and Differentiation via new developments and partnerships:

– New silicon technologies (bio-technology & healthcare, fuel cell,…)

– Post-silicon technologies (nano-technologies & printed electronics,…)

16Midis Minatec – 24 april 2009 _GM

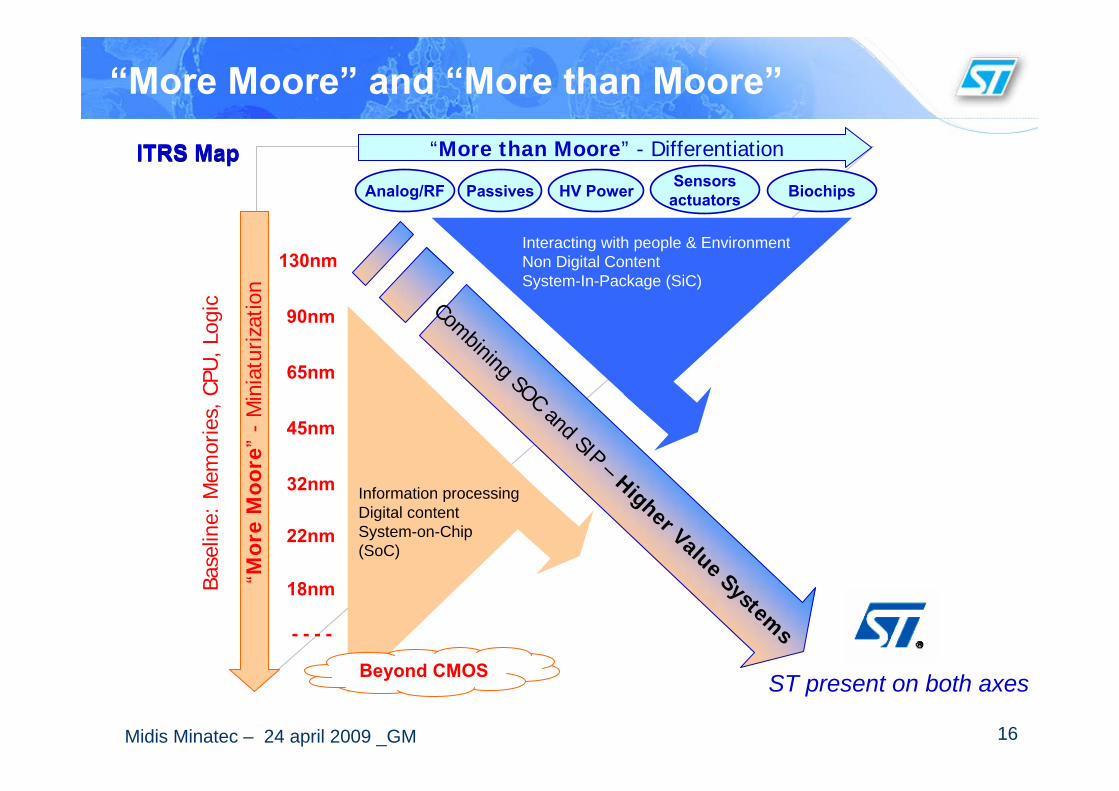

“More Moore” and “More than Moore”

ITRS MapITRS Map “More than Moore” - Differentiation

“Mor

e M

oore

”-

Min

iatu

rizat

ion

130nm

90nm

65nm

45nm

32nm

22nm

18nm

- - - -

Analog/RF Passives HV Power Sensorsactuators Biochips

Base

line:

Mem

orie

s, C

PU, L

ogic Combining SOC and SIP – Higher Value System

s

Interacting with people & EnvironmentNon Digital ContentSystem-In-Package (SiC)

Information processingDigital contentSystem-on-Chip(SoC)

Beyond CMOS ST present on both axes

17Midis Minatec – 24 april 2009 _GM

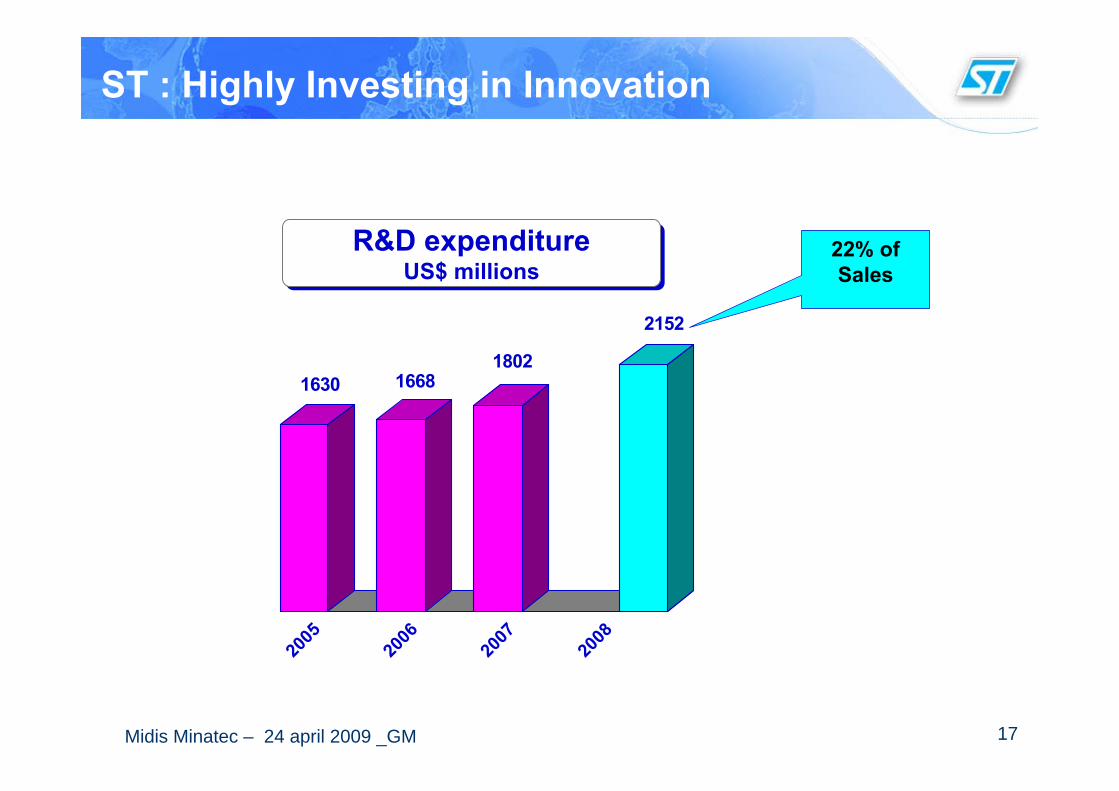

ST : Highly Investing in Innovation

R&D expenditureUS$ millions

R&D expenditureUS$ millions

1630 16681802

2152

2005

2006

2007

2008

22% of Sales

18Midis Minatec – 24 april 2009 _GM

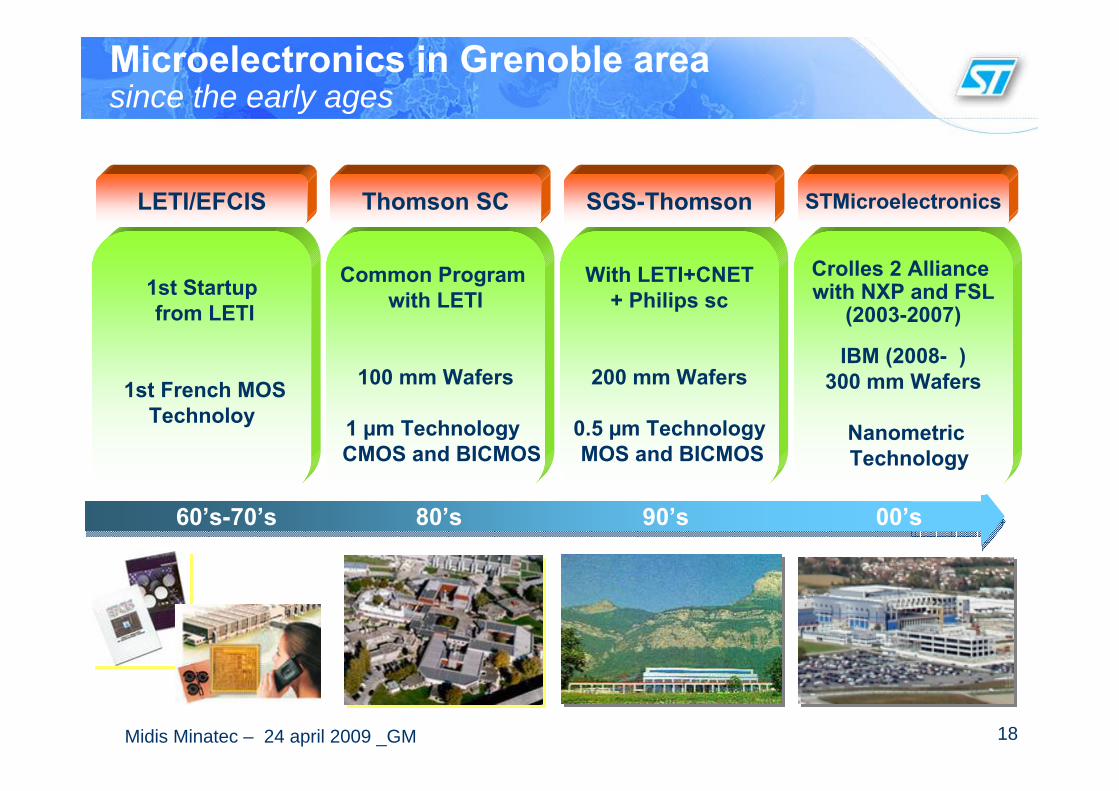

Microelectronics in Grenoble area since the early ages

60’s-70’s 80’s 90’s 00’s

1st Startupfrom LETI

1st French MOSTechnoloy

LETI/EFCIS

Common Program with LETI

100 mm Wafers

1 µm Technology CMOS and BICMOS

Thomson SC

With LETI+CNET+ Philips sc

200 mm Wafers

0.5 µm TechnologyMOS and BICMOS

SGS-Thomson

Crolles 2 Alliance with NXP and FSL

(2003-2007)

IBM (2008- )300 mm Wafers

NanometricTechnology

STMicroelectronics

19Midis Minatec – 24 april 2009 _GM

ST Crolles site

Crolles200Crolles200 Crolles300Crolles300

20Midis Minatec – 24 april 2009 _GM

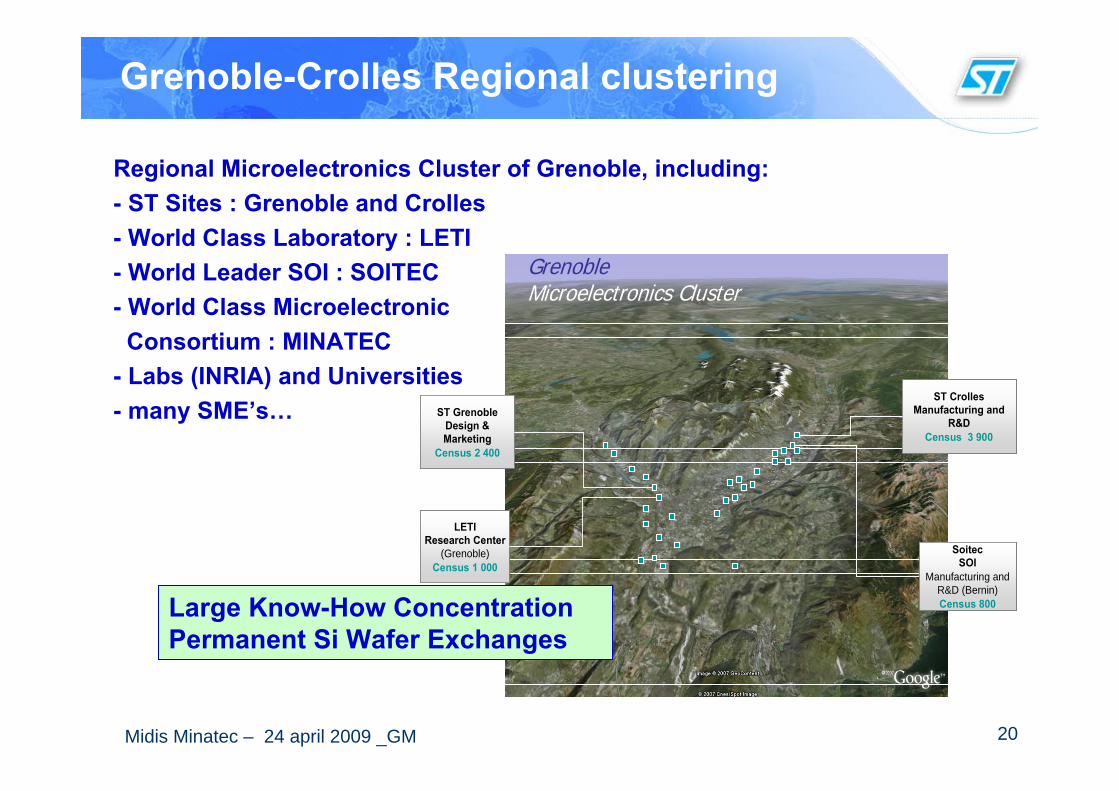

Grenoble-Crolles Regional clustering

Regional Microelectronics Cluster of Grenoble, including:- ST Sites : Grenoble and Crolles - World Class Laboratory : LETI - World Leader SOI : SOITEC - World Class MicroelectronicConsortium : MINATEC

- Labs (INRIA) and Universities- many SME’s…

GrenobleMicroelectronics Cluster

ST Grenoble Design & Marketing

Census 2 400

LETIResearch Center

(Grenoble)Census 1 000

ST Grenoble Design & Marketing

Census 2 400

LETIResearch Center

(Grenoble)Census 1 000

ST CrollesManufacturing and

R&DCensus 3 900

SoitecSOI

Manufacturing and R&D (Bernin)Census 800

ST CrollesManufacturing and

R&DCensus 3 900

ST CrollesManufacturing and

R&DCensus 3 900

SoitecSOI

Manufacturing and R&D (Bernin)Census 800

SoitecSOI

Manufacturing and R&D (Bernin)Census 800Large Know-How Concentration

Permanent Si Wafer Exchanges

21Midis Minatec – 24 april 2009 _GM

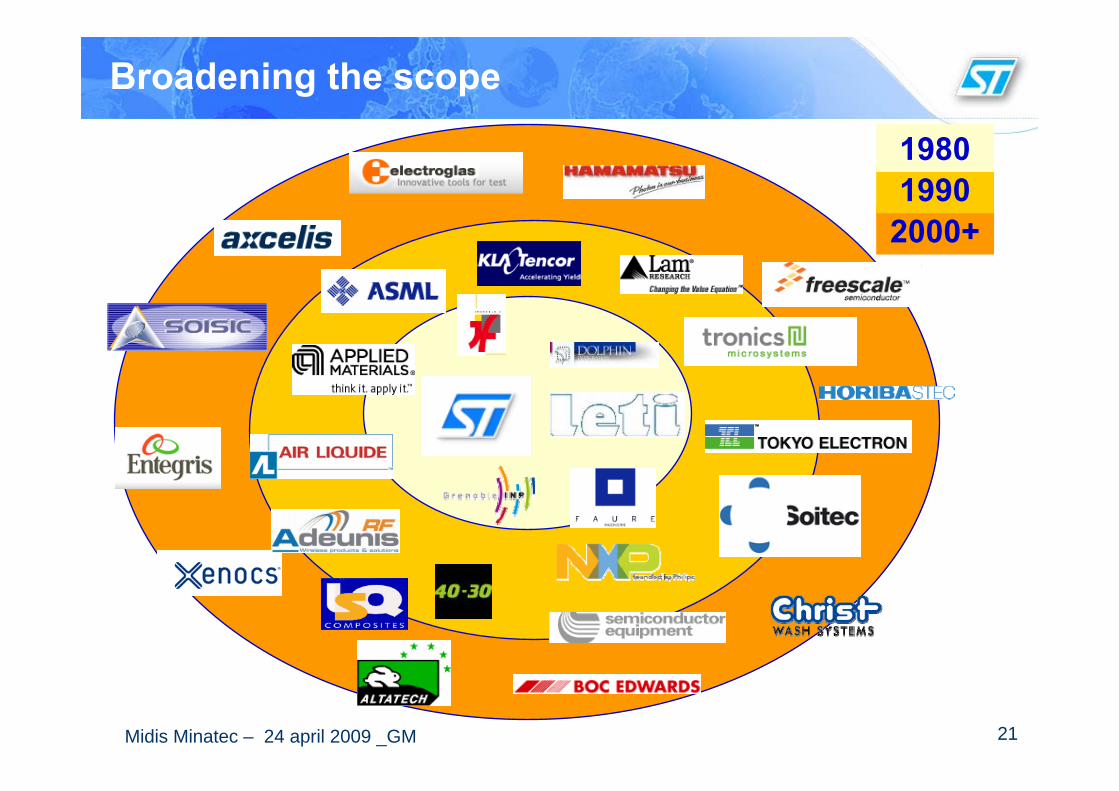

Broadening the scope

2000+19901980

22Midis Minatec – 24 april 2009 _GM

ST Crolles Impact on Jobs creation

+ Indirect 8000

+ Direct 4000

ST Crolles4074

Total Rhône-Alpes ~ 16000 p

plus 9000 p in France

Total Rhône-Alpes ~ 16000 p

plus 9000 p in France

23Midis Minatec – 24 april 2009 _GM

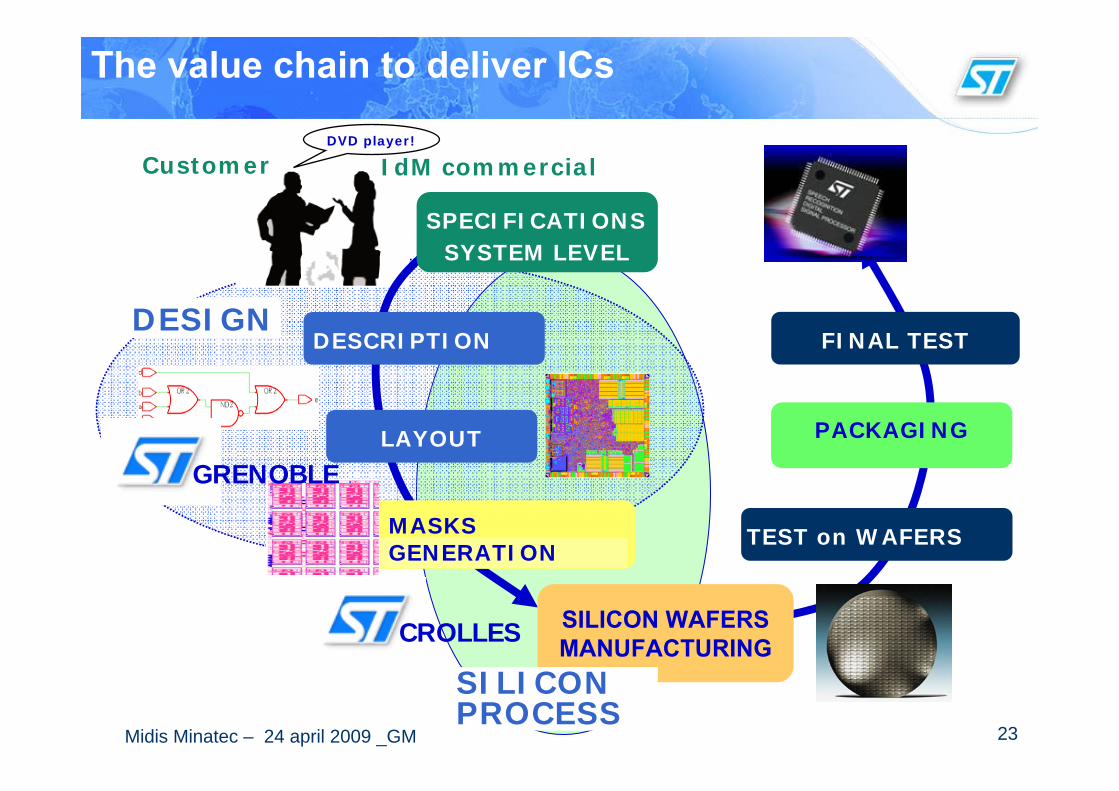

DVD player!

Customer

DESIGN

SPECIFICATIONSSYSTEM LEVEL

DESCRIPTION

LAYOUT

SILICON WAFERSMANUFACTURING

TEST on WAFERS

PACKAGING

FINAL TEST

The value chain to deliver ICs

SILICON PROCESS

IdM commercial

MASKS GENERATION

CROLLES

GRENOBLE

24Midis Minatec – 24 april 2009 _GM

R&D: a Global Alliance for Core CMOS Process development

for Bulk CMOS Technology developmentInternational Silicon Development Alliance

CharteredSamsung

InfineonToshiba

FreescaleST

AMD/Foundry co

25Midis Minatec – 24 april 2009 _GM

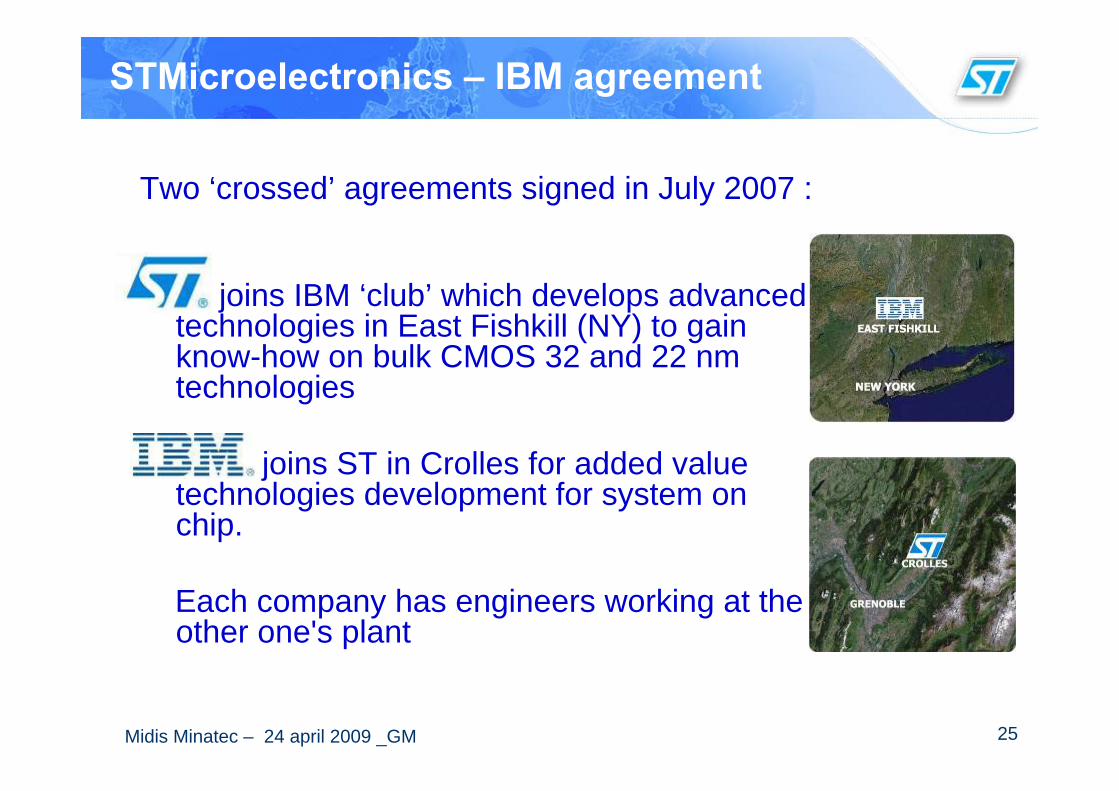

STMicroelectronics – IBM agreement

Two ‘crossed’ agreements signed in July 2007 :

joins IBM ‘club’ which develops advanced technologies in East Fishkill (NY) to gain know-how on bulk CMOS 32 and 22 nm technologies

joins ST in Crolles for added value technologies development for system on chip.

Each company has engineers working at the other one's plant

26Midis Minatec – 24 april 2009 _GM

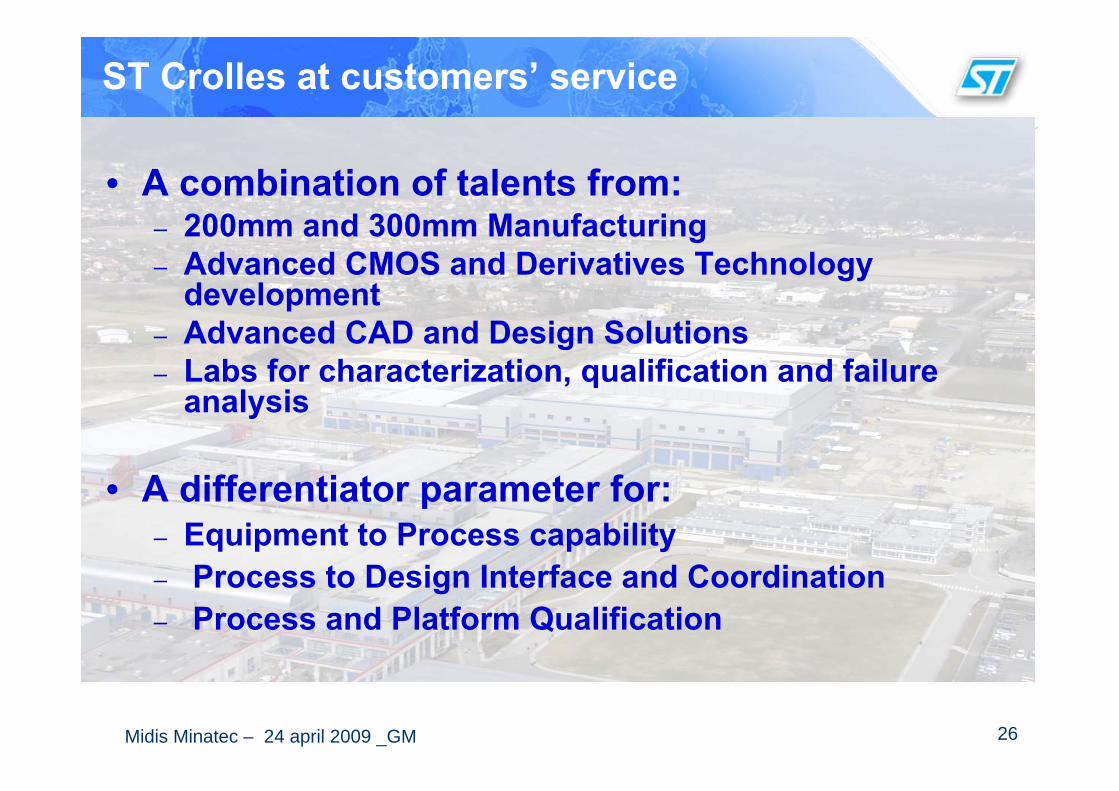

• A combination of talents from:– 200mm and 300mm Manufacturing– Advanced CMOS and Derivatives Technology

development– Advanced CAD and Design Solutions– Labs for characterization, qualification and failure

analysis

• A differentiator parameter for:– Equipment to Process capability– Process to Design Interface and Coordination– Process and Platform Qualification

ST Crolles at customers’ service

27Midis Minatec – 24 april 2009 _GM

Characterization

ManufacturingTechnology

Design Solutions

…to match all their requirements

28Midis Minatec – 24 april 2009 _GM

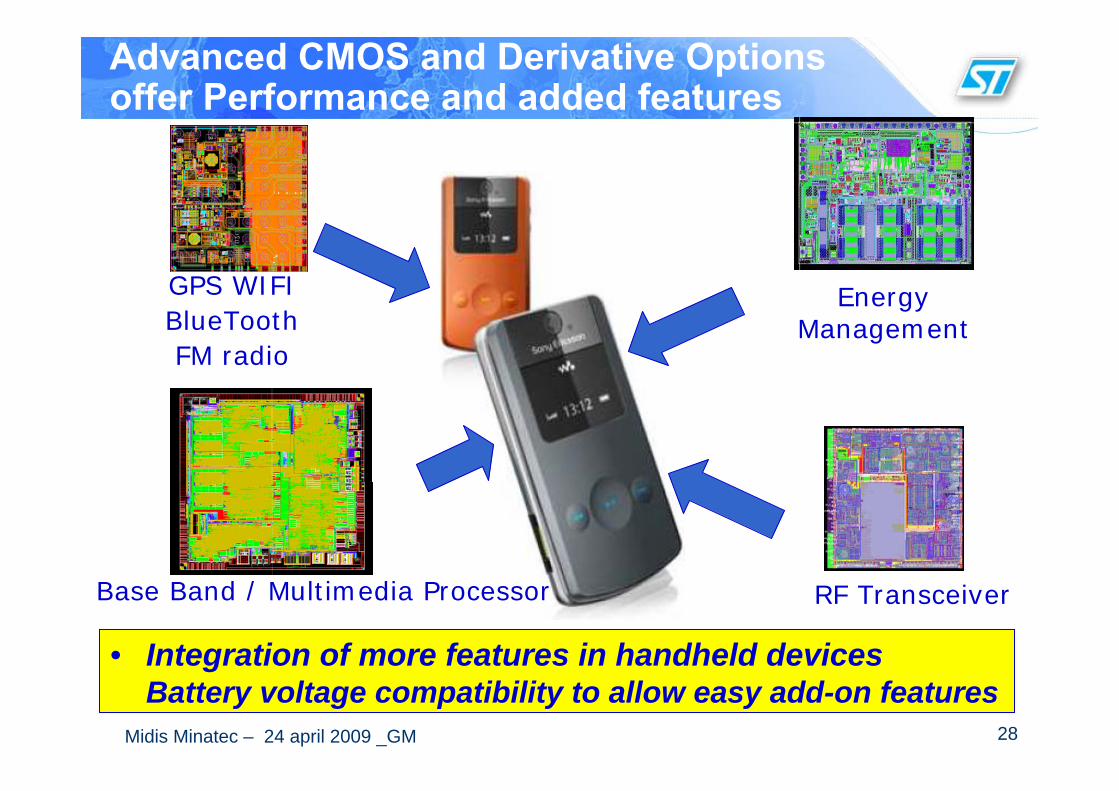

Advanced CMOS and Derivative Options offer Performance and added features

• Integration of more features in handheld devicesBattery voltage compatibility to allow easy add-on features

GPS WIFIBlueToothFM radio

Base Band / Multimedia Processor RF Transceiver

EnergyManagement

29Midis Minatec – 24 april 2009 _GM

ST Crolles products and customers

Communications Computer Peripherals AutomotiveDigital Consumer

30Midis Minatec – 24 april 2009 _GM

R&D, Design, Applications, ManufacturingST clustering in Europe• Clustering of R&D, Design , Applications, and Manufacturing on the

same site provides significant advantages:

– Speed & Acceleration of the learning curve:• Close loop between various teams

• Fast Design/Silicon prototyping

• Reduce communication barriers

– Excellence Center driven by Business & Customer Application:

• All activities in convergence

• Knowledge & experience sharing

• Innovation enabler across each organization

– Efficiency:• Focus

• Synergy

• Reactivity

31Midis Minatec – 24 april 2009 _GM

9000 m2

6700 m2

1900 m2

Clean link

Facilities

Cleanroom C300

Cleanroom C200

32Midis Minatec – 24 april 2009 _GM

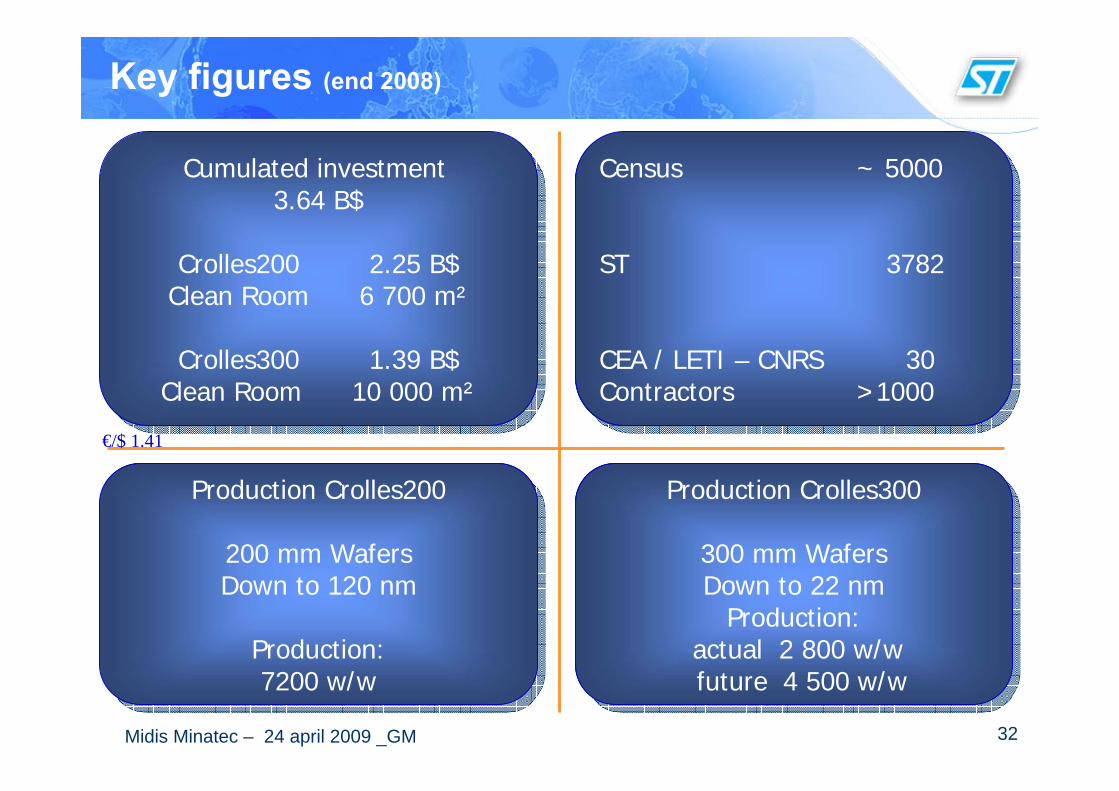

Key figures (end 2008)

Cumulated investment 3.64 B$

Crolles200 2.25 B$Clean Room 6 700 m²

Crolles300 1.39 B$Clean Room 10 000 m²

Cumulated investment 3.64 B$

Crolles200 2.25 B$Clean Room 6 700 m²

Crolles300 1.39 B$Clean Room 10 000 m²

Census ~ 5000

ST 3782

CEA / LETI – CNRS 30Contractors >1000

Census ~ 5000

ST 3782

CEA / LETI – CNRS 30Contractors >1000

Production Crolles300

300 mm WafersDown to 22 nm

Production:actual 2 800 w/wfuture 4 500 w/w

Production Crolles300

300 mm WafersDown to 22 nm

Production:actual 2 800 w/wfuture 4 500 w/w

Production Crolles200

200 mm WafersDown to 120 nm

Production:7200 w/w

Production Crolles200

200 mm WafersDown to 120 nm

Production:7200 w/w

€/$ 1.41

33Midis Minatec – 24 april 2009 _GM

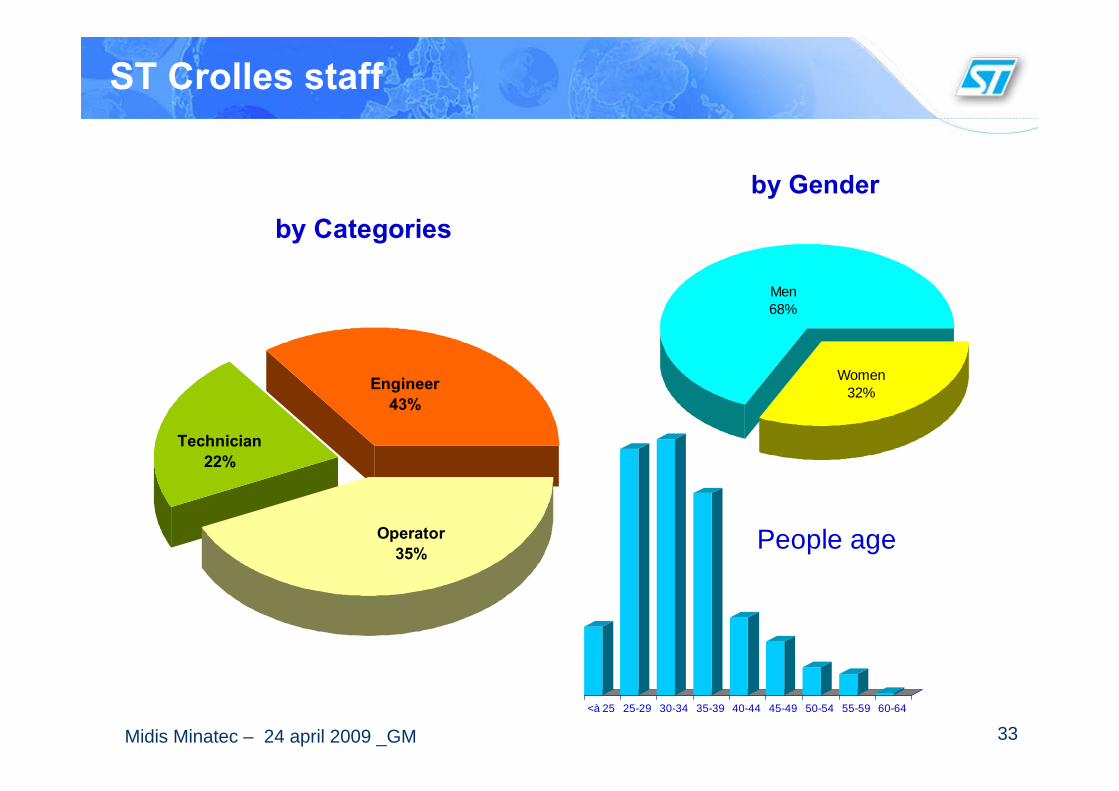

ST Crolles staff

by Categories

Engineer43%

Operator35%

Technician22%

by Gender

Women32%

Men68%

<à 25 25-29 30-34 35-39 40-44 45-49 50-54 55-59 60-64

People age

34Midis Minatec – 24 april 2009 _GM

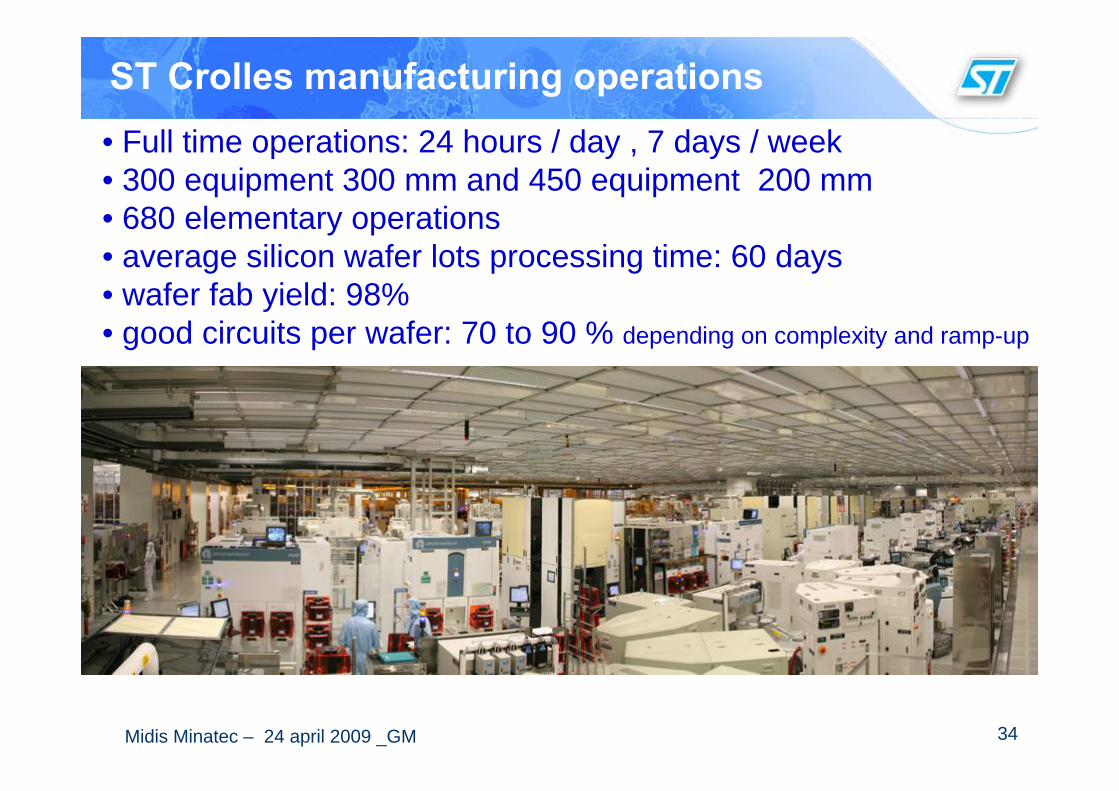

ST Crolles manufacturing operations• Full time operations: 24 hours / day , 7 days / week• 300 equipment 300 mm and 450 equipment 200 mm • 680 elementary operations• average silicon wafer lots processing time: 60 days• wafer fab yield: 98%• good circuits per wafer: 70 to 90 % depending on complexity and ramp-up

35Midis Minatec – 24 april 2009 _GM

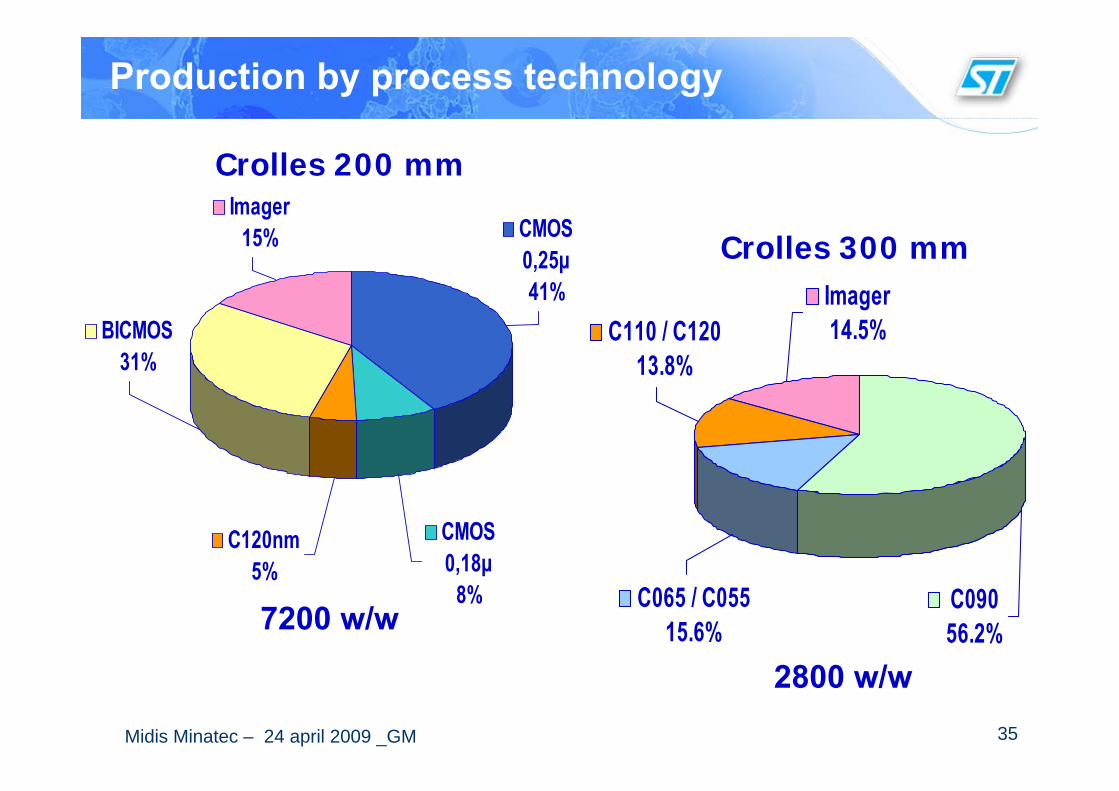

Production by process technology

C120nm5%

CMOS 0,18µ

8%

CMOS 0,25µ41%

BICMOS31%

Imager15%

Imager14.5%

C09056.2%

C065 / C05515.6%

C110 / C12013.8%

Crolles 200 mm

Crolles 300 mm

7200 w/w

2800 w/w

36Midis Minatec – 24 april 2009 _GM

ST Crolles answers to the Manufacturing challenges

• Labor Cost : High Productivity via Full Automation• Direct Labor Productivity : via Operator Tasks

Elimination (eg lot dispatching by computers) andIntegrated WIP Management (MES, AMHS)

• Labor Productivity and Flexibility :via Computer Integrated Wafer Manufacturing

• Dimension of Scale : via competitive Fab sizing

37Midis Minatec – 24 april 2009 _GM

• ST Crolles 300mm Fab at 20 K Wafer/Month cancombine efficiently R&D and Manufacturing ofDifferentiated Technologies:– CMOS Analog / RF process– Embedded Memories (DRAM, NVM)– CMOS Imagers with Colorization line– TSV process– 3 D integration

• Benefits of R&D ‘embedded’ within Manufacturing :– Fast Silicon close loops– Fast prototyping– Fast Yield learning curve– Same tools R&D – Mfg– Concentration of Expertise (Design, Process, Manufacturing)

ST Crolles Focus on Differentiated Technologies

38Midis Minatec – 24 april 2009 _GM

Summary

• Top-class silicon process devt via local and ww alliances

• On-site Platform expertise for complex system-on chip development

• Service-oriented manufacturing

• Completed with close contacts with ST and ST- Ericsson design teams at Grenoble and many other ST and customers’ sites

NO, designing and manufacturing advancedsemiconductors in Europe is not an Utopy !It’s happening HERE and NOW