Embed Size (px)

Citation preview

Computerization of

Co-operative Banks, Jharkhand

Jharkhand Agency for Promotion of Information Technology

(JAP-IT), Jharkhand

- Akshay Kumar Singh

Sr. Consultant

Overview of the Project

To develop and implement a web-based Core Banking Solution (CBS)

for the Co-Operative Bank throughout the Jharkhand.

There are 8 District Central Cooperative Banks having 112 branches.

Most of the banks were in the remotest place having very difficult

terrain.

All of these banks were established much before independence

having their own service delivery mechanism.

These banks were established in the following years:

• The Ranchi-Khunti Central Cooperative Bank Estd: 1910

• The Gumla-Simdega Central Cooperative Bank Estd: 1926

• The Dhanbad Central Cooperative Bank Estd: 1929

• The Singhbhum Central Cooperative Bank Estd: 1925

• The Giridih Central Cooperative Bank Estd: 1924

• The Hazaribagh Central Cooperative Bank Estd: 1919

• The Deoghar-Jamtara Central Cooperative Bank Estd: 1960

• The Dumka Central Cooperative Bank Estd: 1965

Ranchi- KhuntiDCCB Ranchi

Branch – 15

A/C - 39786

Gumla- SimdegaDCCB Gumla

Branch – 19

A/C - 75475

Dumka DCCB Dumka

Branch – 09

A/C - 33852

HazaribaghDCCB

Hazaribagh

Branch – 16

A/C - 77461

SinghbhumDCCB Chaibasa, West Singbhum

Branch – 24

A/C - 126216

Dhanbad DCCB Dhanbad

Branch – 13

A/C - 148900

Deoghar-Jamtara DCCB

Deoghar

Branch – 15

A/C - 91350

Giridih DCCB Giridih

Branch – 09

A/C - 27733

Structure of Co-operative Banks,

Jharkhand

Overview of the Project (contd…)

The idea behind this project was to create an atmosphere in the bank so that itcould compete with the other banks, nationalized or private.

These banks had registered their presence in the remotest corners of the State

These banks were registered at the time when there were no other Banks in thearea.

These banks has 6,67,531 account holders.

These banks customers also include 857 PACS, 474 LAMPS & 457 CreditSocieties of Labourers, Teachers, Service holders etc.

The pre-requisite of LAMPS & PACS is to have at least 100 members with acondition of only one member from a family (Majority of them are having more than500 members).

There is a provision of 11 member Governing body of a LAMPS in which 4,including the Chairperson has to be from tribal community.

Apart from these, there are various special types of societies like

Special Societies for Women (225 in total),

Weaver (176 in total),

Disabled (5 in total),

Forest Labourers (152 in total),

Stone Crusher (86 in total),

Fruit & Vegetable growers (359 in total) etc

are the among the most valued customers of the bank.

Many of these societies get subsidies from government which now will be easy todisburse & made for.

Benefits of the Project

In terms of

customers’ satisfaction,

automated report generation,

transparent transaction etc.

The important point to underline here is that –

RBI had given a deadline to all the banks beyond which they may haveconsidered canceling their licenses or non-issue of license, whicheverthe case may be.

And now, through this project Co-operative Banks are having licensefrom RBI.

Geographic & Demographic Coverage

All the District Central Cooperative Banks (for customers The solution DCCBs) ofthe state of Jharkhand.

Enabling centralized banking with ease of transaction is implemented so as tocover whole of Jharkhand.

The beneficiaries are the account holders of these banks.

In case of LAMPS/PACS a/c one account may cater to even 5-10 thousandcitizens.

Now customers can do ease of banking from any branch of that DCCB and neednot to travel to their own branch for a transaction.

Situation before the initiative

Bottlenecks

•Manual operations hindering customer service

•Difficulty in keeping proper track of customer transactions

•Difficulty in prevention of fraud

•Minimum scope for improvement of customer service

Challenges

•Unbalanced Books

•To make ease of customer services

•To prevent delay in various statutory reporting

•Regulators could not monitor the banks due to delay in reporting

•To reduce time elapsed between actual date of reporting and reportreceipt date etc.

•Digitization of old manual data which included Master Data entryfollowed by two level verification from Bank Officials, preparation of trialbalance by branch & tallying the same with the digitally generated report,balance entry feeding, scanning of photo & signature etc.

Constraints

•Lack of IT skill in bank staffs

•Absence of IT and related infrastructure

•Old legacy Data spread over in various bank registers

Sl. no. Topics Manual system CBS system

1 Response time to Customer approx. 10 mnts. Few seconds

2 Employee productivity 50 - 70

transactions/day

More than 150

transactions/ day

3 Withdrawal of payment approx. 10 mnts. within 1 second

4 Passbook updation approx. 10 mnts. 1/2 mnts.

5 Statement of account 1 - 2 days 1 - 2 mnts.

6 MIS reports ( no. of reports 150 - 170

and out of them 6 statutory reports of

RBI and 9/10 reports for NABARD

15 - 20 days for

generating reports

1/2 mnts. Because

it is creating

automatically

7 March Closing operation More than 2 -3

months and in the

month of June/July

and after that they

are publishing

balance sheet

On the day of

closing i.e 31st

March

8 Accuracy Balancing problem 100% accurate

Advantages of current system

contd…

Sl. no. Topics Manual system CBS system

9 Account opening and monitoring 2/3 hours 5 mnts. With more details

10 Loan account monitoring Possible in branch level

and also monitoring is

time taking

Instantly and can be

monitored from branch

and head office

11 Interest application Possible in yearly basis

and taking 2/3 months

Possible in monthly/

quarterly/ half yearly and

yearly and will taking 1/2

mnts.

12 Any Branch Banking Facility Not possible Customer of the Bank

can visit to any of the

bank branches

conveniently during their

traveling and do

transactions on their

account

13 Inter branch reconciliations Manual Process Automatically gets

reconciled

14 Investments Manual process and

decisions

Structured Investments

can be done with system

15 Asset Management of the Bank Manual process Structured processing

can be done with system

Advantages of current system (contd..)

contd…

Sl. No. Topics Manual System CBS System

1 Delivery channel Not possible To add this

people can use

ATM / Kiosk/

Micro ATM etc

2 Online fund transfer Not possible Using NEFT and

RTGS it can be

possible in Core

Some Future Benefits as CBS has inbuilt inerfaces from CBS Side

Advantages of current system (contd..)

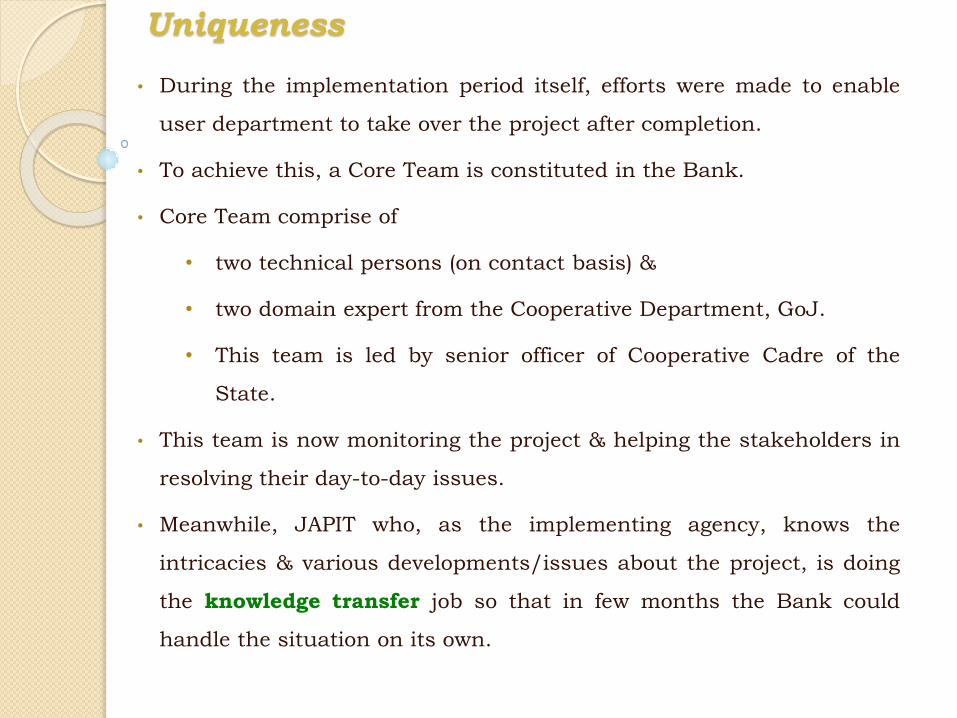

Uniqueness

• During the implementation period itself, efforts were made to enable

user department to take over the project after completion.

• To achieve this, a Core Team is constituted in the Bank.

• Core Team comprise of

• two technical persons (on contact basis) &

• two domain expert from the Cooperative Department, GoJ.

• This team is led by senior officer of Cooperative Cadre of the

State.

• This team is now monitoring the project & helping the stakeholders in

resolving their day-to-day issues.

• Meanwhile, JAPIT who, as the implementing agency, knows the

intricacies & various developments/issues about the project, is doing

the knowledge transfer job so that in few months the Bank could

handle the situation on its own.

Uniqueness (contd…)

• Jharkhand, despite its difficult terrain & other constraints, is the 5th State in

the country & first in North India to complete the CBS process of Cooperative

Banks.

• All stakeholders were kept in confidence during the implementation of the

project.

• Regular interaction and feed-back mechanism was adopted to make the outcome

more beneficial and effective.

• Channel of communication was established at every level so that issues at the

bottom could easily and quickly reach to the apex decision making level.

• Regular hands-on practice by the end user.

• Workshops organized in which the such successful projects champions shared

their ideas.

• Visits of the end users were arranged to get a first hand experience.

• Banks were prepared simultaneously to take over the project with constitution of

Core Team.

• Low Cost.

Way Forward

Establishment of

Jharkhand State Cooperative Bank Ltd.

The Jharkhand State cooperative bank was established vide

State Cabinet Resolution No 6, dated 8.10.2002 whereas

BSCB Ltd transferred Assets and Liabilities of 5 of its

Branches situated in Jharkhand to the JSCB on 31.08.12.

Government of Jharkhand has taken decision to have two tier

co-operative credit structures.

Under this all eight co-operative banks and their branches

will merge and become branches of JSCB.

There will be one Management at JSCB

All affiliated LAMPS/PACS will act as service provider.

All five branches of JSCB and HO have been brought underCBS system.

Now the Cooperative Banks are on the way to serve at parwith the other commercial banks.

Merger of JSCB and all 8 DCCBs is scheduled to becompleted soon under the banner of JSCB to make itsremarkable presence statewide.

Project Management Unit and Network Management Centerestablished in JSCB for effective management.

Implementation of CBS in JSCB

AEPS

/

APB

Internet

BankingATM/ Micro ATM

CTSAML

STEP 3- Implementation of RBI Guidelines

STEP 2- Implementation of other Services

On the verge of implementation

NEFT

/

RTGSCBS

STEP 1- Implementation of Core Banking system

JSCB

Jharkhand State Cooperative Bank

Automation Roadmap

Future Plans

•LAMPS/PACS automation

•Introduction of MicroATM in PACS to work as Business Correspondent.

• Introduction of Anti Money Laundering(AML) and Cheque Truncation System(CTS).

Also there is plan to introduce the subsidy reimbursements to citizens of the state. After achievement of the above the Cooperative Banks may work as a Financial Backbone of the State.

Thanking You