Embed Size (px)

Citation preview

Ralf Korn (TU Kaiserslautern &Fraunhofer ITWM)

Computational Problems in Pricing, Risk

and Asset Management in Banks and

Insurance Companies FPL 2014 Tutorial: Reconfigurable Architectures in Finance

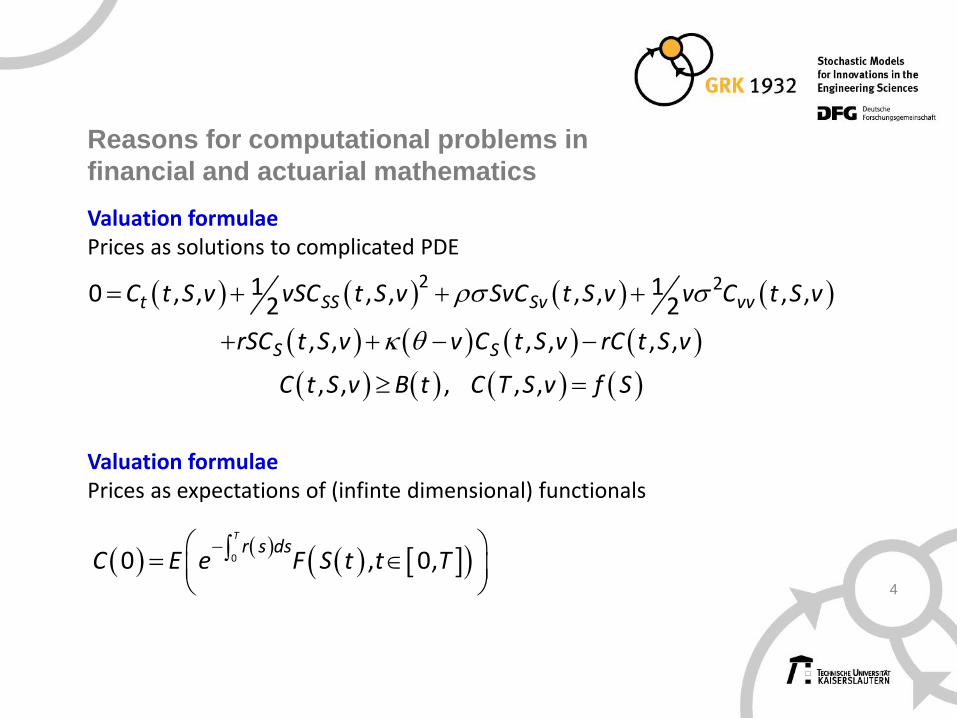

Reasons for computational problems in

financial and actuarial mathematics

2

Stock price dynamics

Reasons for computational problems in

financial and actuarial mathematics

3

Term structure of interest rates

Reasons for computational problems in

financial and actuarial mathematics

4

2 21 10 , , , , , , , ,2 2

, , , , , ,

, , , , ,

t SS Sv vv

S S

C t S v vSC t S v SvC t S v v C t S v

rSC t S v v C t S v rC t S v

C t S v B t C T S v f S

Valuation formulae Prices as solutions to complicated PDE

Valuation formulae Prices as expectations of (infinte dimensional) functionals

00 , 0,Tr s ds

C E e F S t t T

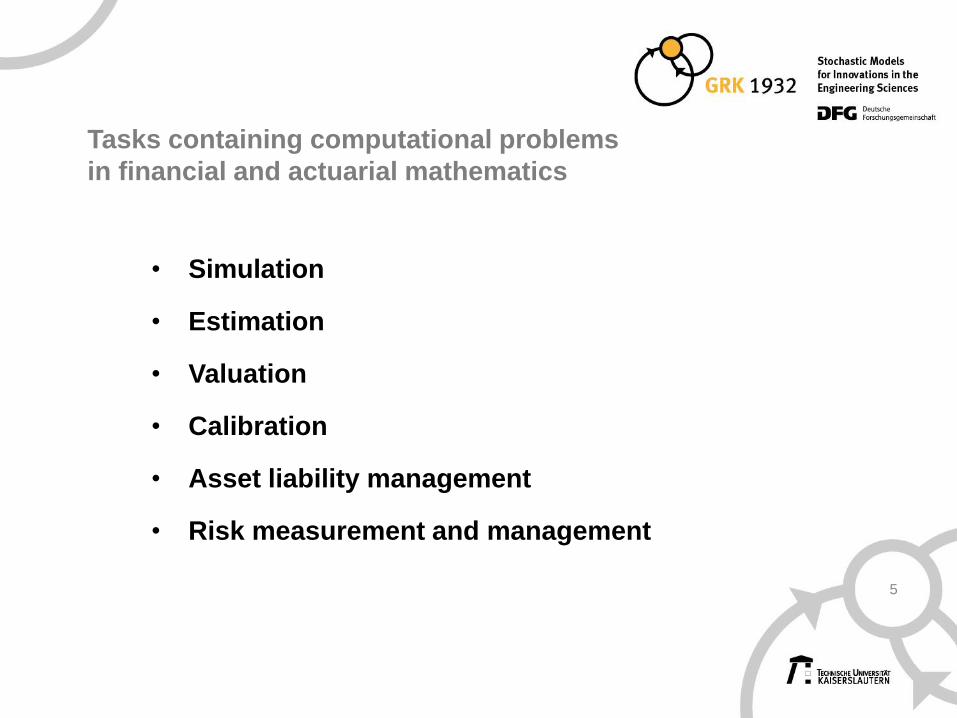

Tasks containing computational problems

in financial and actuarial mathematics

5

• Simulation

• Estimation

• Valuation

• Calibration

• Asset liability management

• Risk measurement and management

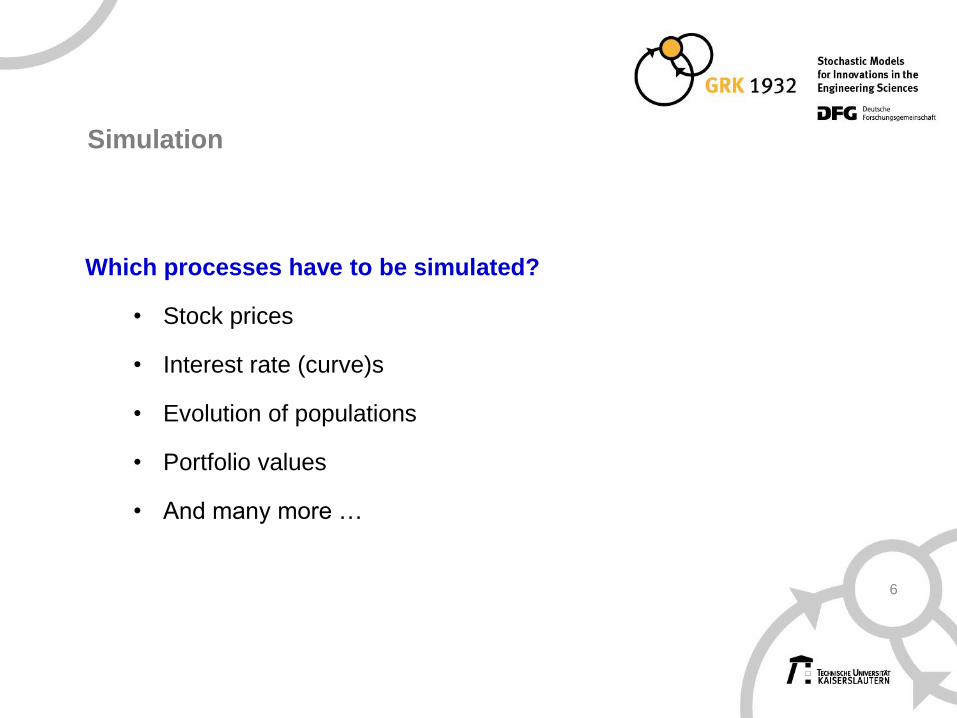

Simulation

6

Which processes have to be simulated?

• Stock prices

• Interest rate (curve)s

• Evolution of populations

• Portfolio values

• And many more …

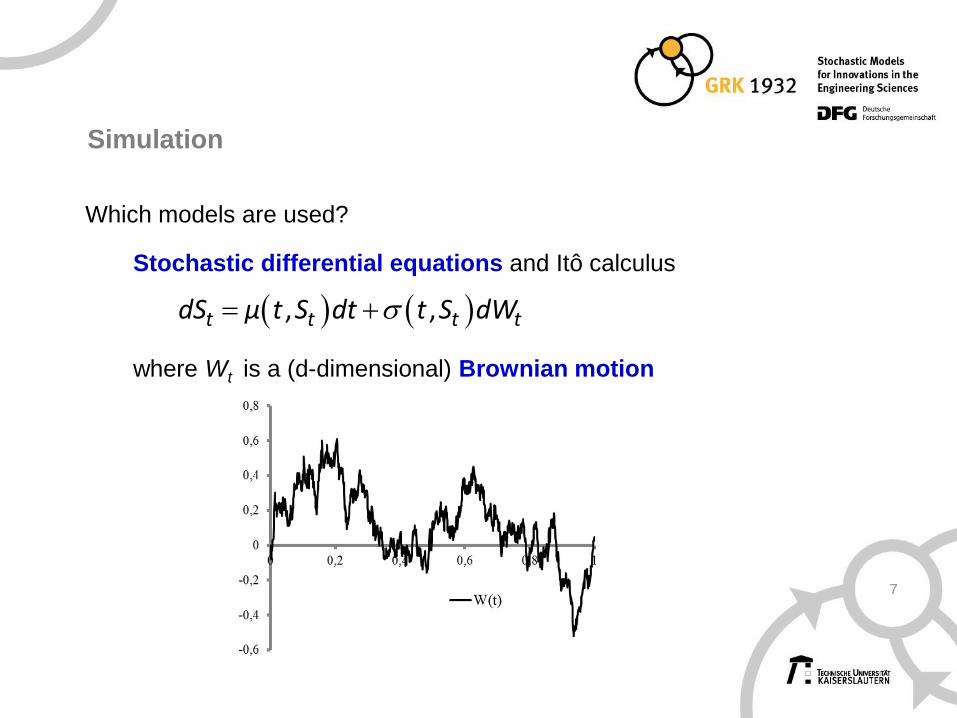

Simulation

7

Which models are used?

Stochastic differential equations and Itô calculus

where Wt is a (d-dimensional) Brownian motion

, ,t t t tdS µ t S dt t S dW

Simulation

8

Examples:

• Bachelier model

• Black-Scholes model

• Heston model

t tdS µdt dW

t t t tdS µS dt S dW

t t t t t

t t t t

dS µS dt v S dW

dv v v dW

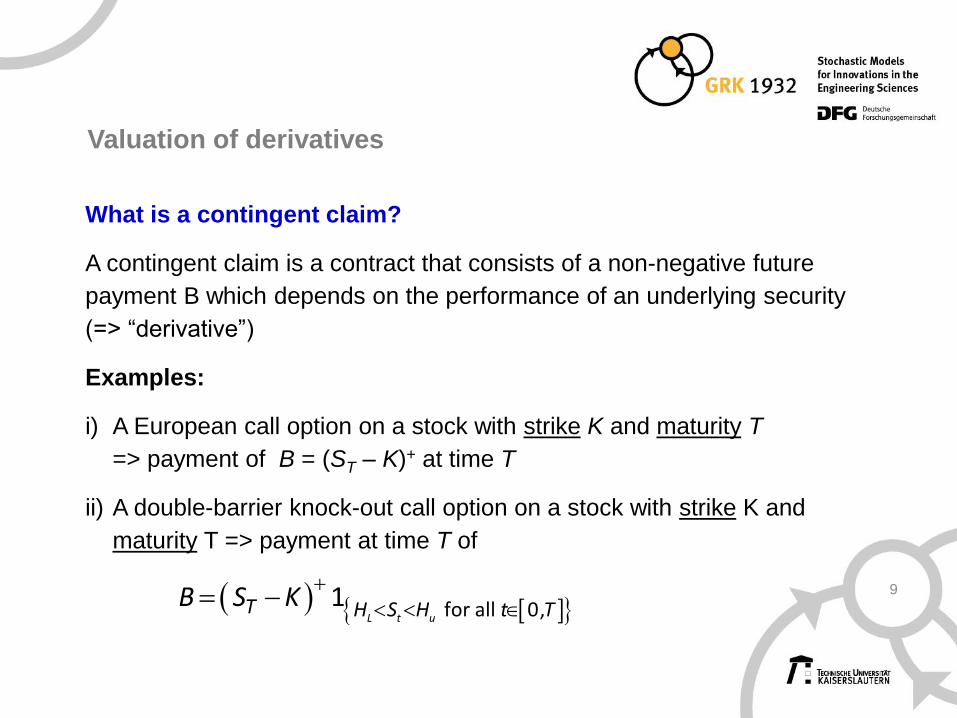

Valuation of derivatives

9

What is a contingent claim?

A contingent claim is a contract that consists of a non-negative future

payment B which depends on the performance of an underlying security

(=> “derivative”)

Examples:

i) A European call option on a stock with strike K and maturity T

=> payment of B = (ST – K)+ at time T

ii) A double-barrier knock-out call option on a stock with strike K and

maturity T => payment at time T of

for all 0,1L t u

T H S H t TB S K

Valuation of derivatives

10

How to determine today’s price of a contingent claim?

Choose a risk-neutral model (i.e. the stock prices has the same drift r as

the evolution of the money market account) and calculate

(1) E(exp(-rT) B)

• Sounds simple, but B can be really nasty!

• All methods for calculating an expectation are possible, e.g.

• Direct integration

• Monte Carlo simulation

• PDE solution

• Tree methods

• ……

Valuation of derivatives

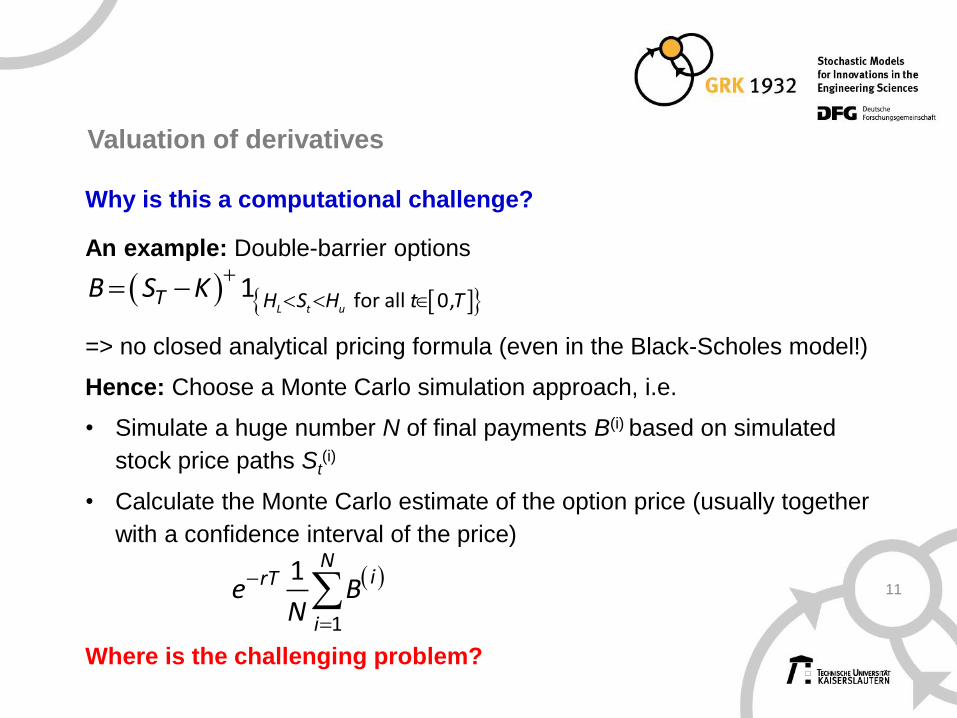

11

Why is this a computational challenge?

An example: Double-barrier options

=> no closed analytical pricing formula (even in the Black-Scholes model!)

Hence: Choose a Monte Carlo simulation approach, i.e.

• Simulate a huge number N of final payments B(i) based on simulated

stock price paths St(i)

• Calculate the Monte Carlo estimate of the option price (usually together

with a confidence interval of the price)

Where is the challenging problem?

for all 0,1L t u

T H S H t TB S K

1

1 NirT

i

e BN

Valuation of derivatives

12

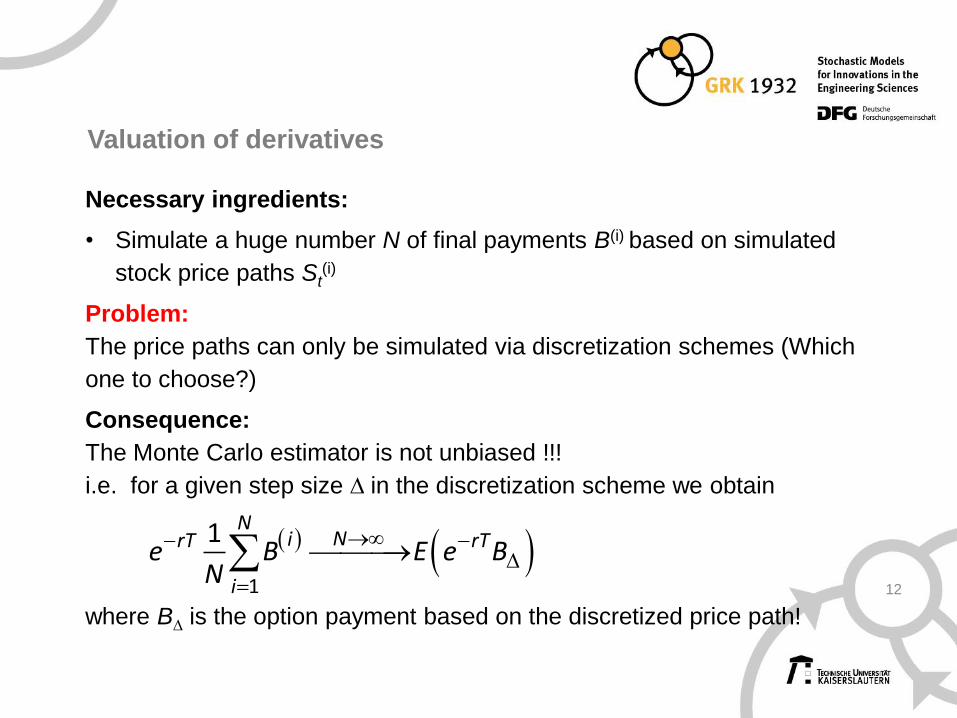

Necessary ingredients:

• Simulate a huge number N of final payments B(i) based on simulated

stock price paths St(i)

Problem:

The price paths can only be simulated via discretization schemes (Which

one to choose?)

Consequence:

The Monte Carlo estimator is not unbiased !!!

i.e. for a given step size ∆ in the discretization scheme we obtain

where B∆ is the option payment based on the discretized price path!

1

1 NNirT rT

i

e B E e BN

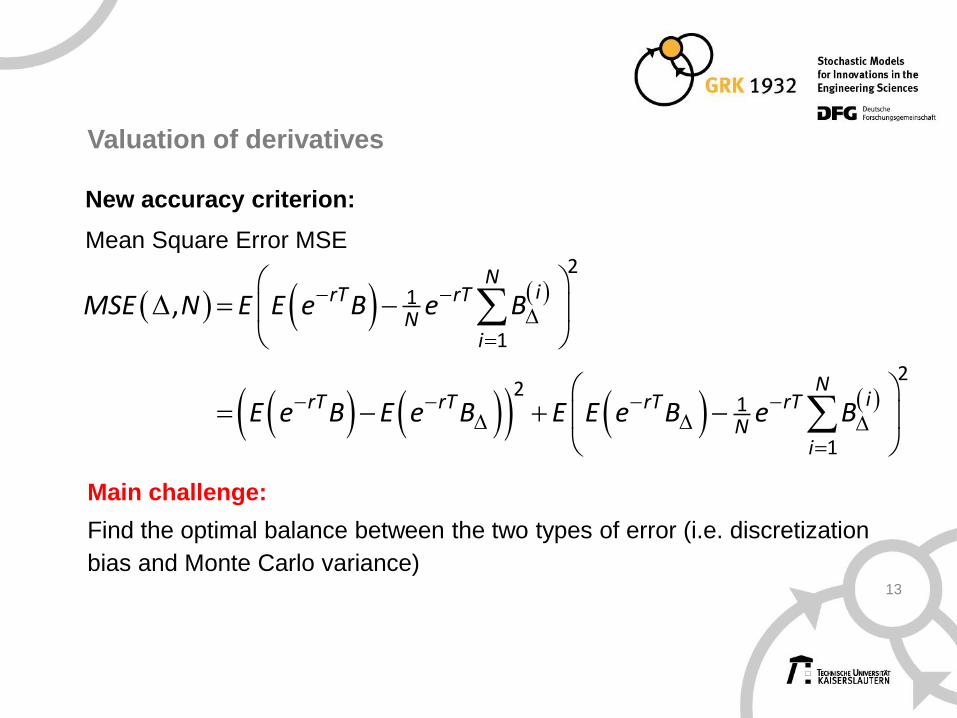

Valuation of derivatives

13

New accuracy criterion:

Mean Square Error MSE

2

1

1

22

1

1

,N

irT rTN

i

NirT rT rT rT

Ni

MSE N E E e B e B

E e B E e B E E e B e B

Main challenge:

Find the optimal balance between the two types of error (i.e. discretization

bias and Monte Carlo variance)

Valuation of derivatives

14

2

1

1

22

1

1

,N

irT rTN

i

NirT rT rT rT

Ni

MSE N E E e B e B

E e B E e B E E e B e B

Main challenge:

Find the optimal balance between the two types of error (i.e. discretization

bias and Monte Carlo variance)

For simple options and a linearly converging discretization scheme:

To obtain an MSE of O(1/n²) , we need ∆ = 1/n, N=n², i.e. an effort of O(n3)

=>

Algorithmical challenge: Find appropriate discretization schemes

Valuation of derivatives

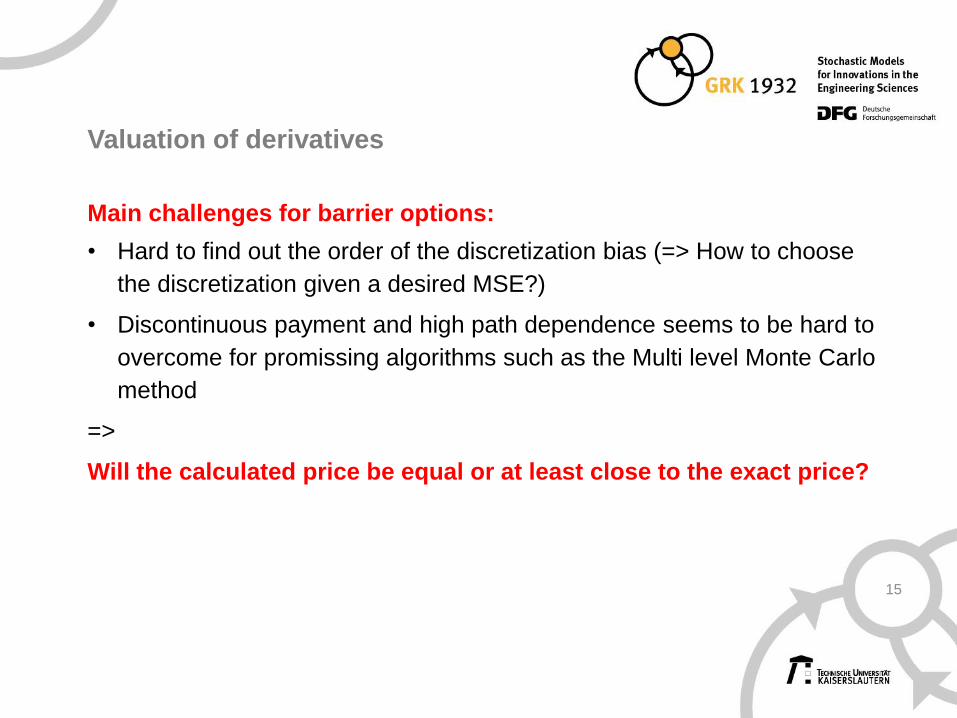

15

Main challenges for barrier options:

• Hard to find out the order of the discretization bias (=> How to choose

the discretization given a desired MSE?)

• Discontinuous payment and high path dependence seems to be hard to

overcome for promissing algorithms such as the Multi level Monte Carlo

method

=>

Will the calculated price be equal or at least close to the exact price?

Valuation of derivatives

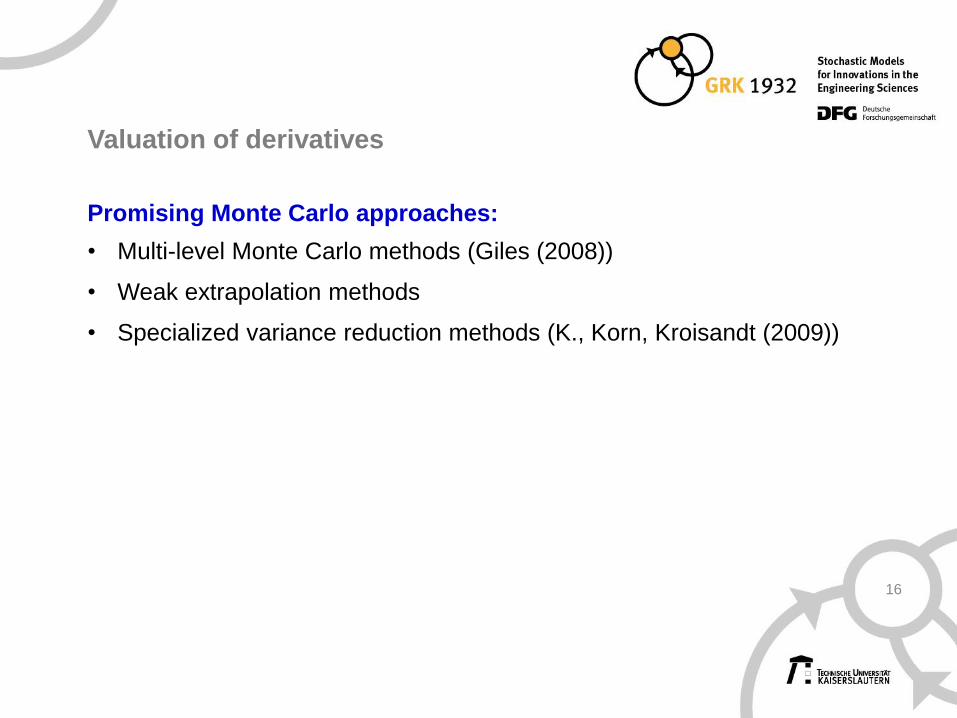

16

Promising Monte Carlo approaches:

• Multi-level Monte Carlo methods (Giles (2008))

• Weak extrapolation methods

• Specialized variance reduction methods (K., Korn, Kroisandt (2009))

Valuation of derivatives

17

Why is this a computational challenge?

General aspects of computational challenges

• Sensitivity analysis (Computing a whole set of prices via varying the

input parameters) can lead to an enormous number of valuation

calculations for just one exotic option

• Calibration

Calibration

18

How to obtain the model parameters?

• Historical estimation (ML-methods, filtering, …)

• Calibration (Method of the market)

Calibration = Determine the set of model parameter such that (for a given

set of market prices) the model prices are as close as possible to the

corresponding actually observed market prices

Why does calibration lead to computational challenges?

• C. requires the solution of a highly non-linear optimization problem

• Each iteration step requires the calculation of many option prices

• C. is an inverse problem

More in the talk of Tilman Sayer!

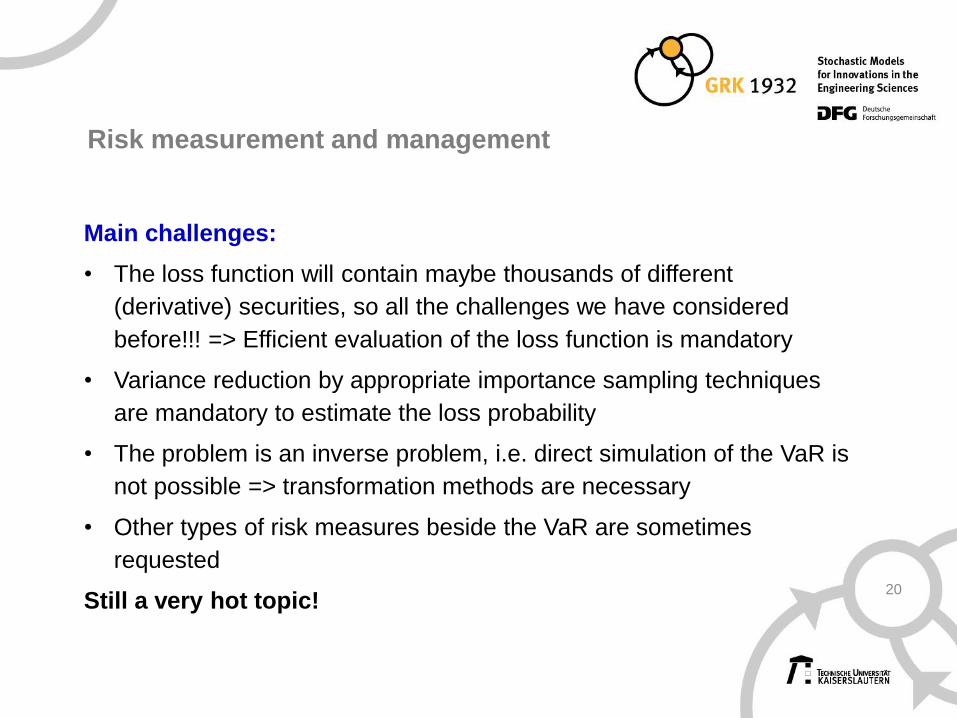

Risk measurement and management

19

How to measure the risk of a whole bank (or of one trading book)?

• Calculate risk measures such as the Value-at-Risk, i.e.

the value of the loss function L(∆S) that will not be exceeded with a

probability of at most .

Main challenges:

The loss function will contain maybe thousands of different (derivative)

securities, so all the challenges we have considered before!!!

=> Efficient evaluation of the loss function is mandatory

: arg infz

z P L S z

Risk measurement and management

20

Main challenges:

• The loss function will contain maybe thousands of different

(derivative) securities, so all the challenges we have considered

before!!! => Efficient evaluation of the loss function is mandatory

• Variance reduction by appropriate importance sampling techniques

are mandatory to estimate the loss probability

• The problem is an inverse problem, i.e. direct simulation of the VaR is

not possible => transformation methods are necessary

• Other types of risk measures beside the VaR are sometimes

requested

Still a very hot topic!

Asset liability management

21

• Life insurers/pension funds have to manage many customers’ accounts

simultaneously (organization of storage!)

• They now receive money and have to pay benefits up to 40 years later

(more complicated models for interest rates are needed)

• They have to deal with many different risks at the same time (interest rates,

stock markets, mortality and longevity risk, lapse risk, …)

• They offer complicated productions with many optionalities

=>

A whole area of computational challenges will come that contains

all the ones talked about today as special cases

For now

22

Thanks for your attention !

Some references:

23

Giles M. (2008) Multi-level Monte Carlo path simulation. Operations Research,

56(3), 607-617.

Glasserman P. (2004) Monte Carlo methods in financial engineering. Springer.

Kloeden P., Platen E. (1999) Numerical Solution of Stochastic Differential

Equations. Springer.

Korn R., Korn E. (2000) Option Pricing and Portfolio Optimization. AMS.

Korn E., Korn R., Kroisandt G. (2009) Monte Carlo Methods and Models in

Finance and Insurance. Chapman & Hall.