Embed Size (px)

Citation preview

Comprehensive Financial Plan

Prepared for

Richard and Linda Jones(Main Scenario)

December 12, 2005

Provided by

Piper Jaffray Financial Advisor

Piper Jaffray800 Nicollet Mall

Minneapolis, MN 55402

Disclosure

The following comprehensive analysis report has been prepared with information provided by you to guide youin selecting an appropriate asset allocation strategy. It may contain asset allocation models that reflect broadgeneralizations and are not intended as investment recommendations. Each of the allocation models representsone possible asset allocation strategy, which is based on responses to questions regarding personalcircumstances, financial goals and investment risk tolerance. The use of the terms financial forecast, expectedreturn, and risk (standard deviation) are not intended to be either an expressed or implied guarantee of actualperformance. Past performance does not guarantee future results.

An Asset Allocation Analysis is a tool that may assist you in determining if you have the right mix ofinvestments for your personal situation. Development of a personalized Asset Allocation Analysis is designedto assist you in positioning your assets based on your financial objectives, time horizons and risk tolerance. Thefollowing report is a hypothetical illustration using assumed rates of return that are based on information youhave provided to your advisor and from sources we believe to be reliable. Depicted rates of return are notrepresentative of the actual rate of return that you will experience with any particular insurance or financialproduct. This illustration is based on the concepts of Modern Portfolio Theory, which states that throughdiversification you may be able to minimize the effects of investment risks and that gains in one investmentclass may help offset losses in another. There is no certainty that any investment or strategy will be profitable orsuccessful in achieving your specific investment objectives. The illustrations shown should not be considered asa prediction of any investment results. Principal values of your investments will fluctuate and when redeemed,may be worth more or less than your original investment. Asset allocation does not ensure a profit or protectagainst losses in a declining market.

Asset mixes presented throughout this analysis are derived using available historical information for each assetclass based on the selected index for that class. They are meant only to illustrate the relative experience betweenasset classes and portfolios. Other asset classes and indices may have characteristics similar or superior to thosebeing analyzed here.

IMPORTANT: The projections or other information generated by AllocationMaster regarding the likelihood ofvarious investment outcomes are hypothetical in nature, do not reflect actual investment results and are notguarantees of future results. The results of this analysis may vary with each use and over time. Monte CarloSimulation is a mathematical model for computing the probability of an outcome by testing hundreds uponhundreds of possible results. Monte Carlo simulation takes into investment returns, volatility, correlations, andother factors, all based on historical statistical estimates. The simulation is created by running a large number ofprojections utilizing randomly selected rates of return to illustrate variable future economic conditions. Theprocess selects random rates of return for each year of each projection to simulate a large number of possiblefuture financial market environments. By using random rates from a statistically appropriate collection ofprobable returns, and repeating the process hundreds of times, the resulting projections can be viewed as arepresentative set of potential future results.

MUTUAL FUNDS, UNIT INVESTMENT TRUSTS OR VARIABLE ANNUITIES

If any mutual fund, unit investment trust, or variable annuity is mentioned in this report, this report must bepreceded or accompanied by the investment product's current prospectus. The prospectus contains morecomplete information, including fees, expenses, investment objectives, and risks. Please read the prospectuscarefully before investing or sending money. Investment return and principal will fluctuate with marketconditions and you may have a gain or a loss when you sell the investment product(s).

ALTERNATIVE INVESTMENTS

Comprehensive Financial Plan Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 2 Piper Jaffray

Alternative Investments such as fund of hedge funds, managed futures funds are intended only for investorswho meet certain minimum qualifications. Alternative Investments are allowed to use aggressive, complexstrategies, and they are not subject to the same regulatory requirements as other investments. They carry risksand concerns not always associated with other investments, including restricted liquidity, less regulatoryoversight, tax inefficiency, delays in distributing tax information and higher fees.

An investment in a hedge fund is speculative and involves a high degree of risk, which each investor mustcarefully consider. Returns generated from an investment in a hedge fund may not adequately compensateinvestors for the business and financial risks assumed. No assurance can be given that the hedge fund willachieve its investment objectives or avoid substantial losses including loss of all or a substantial amount of hisor her investment. Fund of hedge funds are subject to many market risks including market volatility fund ofhedge funds employ certain trading techniques, such as, the use of leveraging and other speculative investmentpractices that may increase the risk of investment loss. Other risks associated with fund of hedge fundsinvestments include, but are not limited to, the fact that fund of hedge funds:

Can be highly illiquid are not required to provide periodic pricing or valuation information to investors mayinvolve complex tax structures and delays in distributing important tax information are not subject to the sameregulatory requirements as mutual funds often charge higher fees and the high fees may offset the fund's tradingprofits may have a limited operating history can have performance that is volatile may have a fund managerwho has total trading authority over the fund and the use of a single adviser applying generally similar tradingprograms could mean a lack of diversification, and consequentially, higher risk may not have a secondarymarket for an investor's interest in the fund and none may be expected to develop may have restrictions ontransferring interests in the fund and may trade a substantial portion of their trades on foreign exchanges.

INDEX BENCHMARKS

Index benchmarks are provided for illustrative purposes only. Comparisons to benchmarks have limitationsbecause benchmarks have volatility and other material characteristics that may differ from the underlyinginvestment product they track. Benchmarks are not managed and you can not invest directly in an index.Because of these differences, benchmarks should not be relied upon as an accurate measure of comparison. Youcannot invest directly in these indices, which include no expenses or transaction charges.

You are under no obligation to act upon, or implement all or any portion of the guidance contained in thisreport. If you elect to act upon, or implement any of the guidance in this report, you are under no obligation toeffect any resulting transaction through or purchase any products or services from Piper Jaffray. To the extentthat you do implement in whole or in part any of the guidance in the report by executing transactions throughPiper Jaffray as a broker or purchasing other products or services offered by Piper Jaffray, a potential conflict ofinterest may arise between your interest and the interest of Piper Jaffray and its financial advisors. For example,in connection with any transactions that you may effect through Piper Jaffray or other products or services youmay purchase from Piper Jaffray, Piper Jaffray will collect asset-based fees, commissions, transaction fees,mark-ups and mark-downs, and receive other compensation. In addition, Piper Jaffray may be the investmentbanker or the company whose securities you purchase or sell or have a financial interest in products or servicesyou purchase. Piper Jaffray, in addition to acting as investment banking, acts as a market maker, which mayresult in Piper Jaffray's interests conflicting with your interests.

This report is not intended to offer tax or legal advice. There is no solicitation and no recommendation for anyaction based upon its results. The report is based on data obtained from sources we consider to be reliablehowever, it is not guaranteed as to accuracy and does not purport to be complete.

Piper Jaffray & Co. Since 1895. Member SIPC and NYSE.

Comprehensive Financial Plan Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 3 Piper Jaffray

.

Comprehensive Financial PlanTable of Contents

Title Page 1. .

Disclosure 2. .

Table Of Contents 5. .

Financial Planning Overview 6. .

Executive Summary - Title Page 7Executive Summary - Financial Position 8. .

Financial Statements - Title Page 9Financial Statements - Overview 10Financial Statements - Current Net Worth 11Financial Statements - Current Net Worth Detail 12Financial Statements - Current Cash Flow 15Financial Statements - Current Cash Flow Detail. .

Asset Allocation - Title Page 16Asset Allocation - Overview 17Asset Allocation - Risk Tolerance 18Asset Allocation - EF Present 21Asset Allocation - EF Proposed 22Asset Allocation - Comparison Composite 23Asset Allocation - Comparison Non-Qualified 24Asset Allocation - Comparison Qualified 25Asset Allocation - Backtest Compound Actual 26Asset Allocation - Histories Risk 27Asset Allocation - Scenario Assumptions 28. .

Retirement - Title Page 29Retirement - Overview 30Retirement - Asset and Income Summary 31Retirement - Retirement Spending Goal 33Retirement - Projected Assets Graph 34Retirement - Projected Assets Table 35Retirement - Projected Income Graph 36Retirement - Projected Income Table 37Retirement - Funding Synopsis 38. .

Estate Advisor - Overview 39Estate Advisor - Estate Assumptions 40Estate Advisor - Current Estate Flowchart 41Estate Advisor - Current Gross Estate 42Estate Advisor - Current Estate Tax & Settlement Costs 43Estate Advisor - Current Estate Distribution 44. .

Data and Assumptions - Title Page 45Data and Assumptions 46. .

Glossary - Title Page 65

Table of Contents Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 4 Piper Jaffray

Glossary - Asset Allocation 66Glossary - Accumulation 68Glossary - Financial Statements 70Glossary - Retirement 72Glossary - Estate 74. .

Notes 76

Table of Contents Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 5 Piper Jaffray

Your Personal Comprehensive Financial Plan

This comprehensive financial plan has been prepared specifically for you using your current financial data. Itspurpose is to help you establish and prioritize your financial goals and to help plan for future financial security.This plan compares your current financial situation to your projected needs in the following areas:

· Financial statements· Personal goal planning· Retirement planning· Portfolio analysis· Estate preservation planning

You can use this plan in several ways. First, you can use it to get an overall view of your present financialsituation: where you stand now. For example, this plan will show your estimated current income taxes andcash flows, and clearly state your balance sheet and estate positions.

Second, you can use the illustrated financial projections to gain an idea of how well your future financial needswill be covered. For example, this plan will project your retirement income based on your current preparationsand your future assumptions.

Third, you can explore and choose to implement the actions suggested in this plan to help improve your presentfinancial situation and your future financial situation.

Recommended Actions

This plan will introduce specific actions that could improve your financial situation. However, the actions thatmay help you now may not be the same actions that you should take a year from now. Changes in your lifesituation may change recommended actions, particularly if changes are experienced in any of the followingareas:

· Your family· Your level of income or wealth· Your objectives· Tax laws and rulings· The economy

If changes are experienced in any of these areas, you should re-evaluate your financial plan. Implementing yourrecommended plan of action can help you on the path to financial security.

Financial Planning Overview Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 6 Piper Jaffray

.

Executive Summary

Prepared by Piper Jaffray Financial Advisor 7 Piper Jaffray

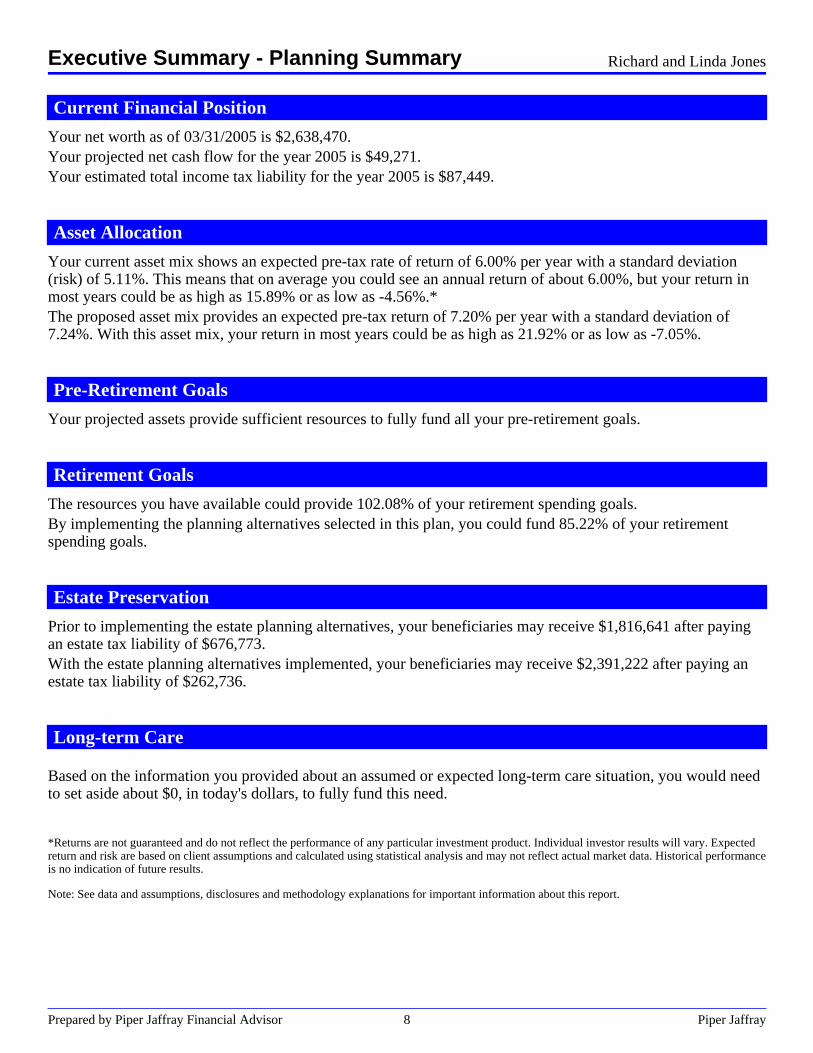

Current Financial Position

Your net worth as of 03/31/2005 is $2,638,470.Your projected net cash flow for the year 2005 is $49,271.Your estimated total income tax liability for the year 2005 is $87,449.

Asset Allocation

Your current asset mix shows an expected pre-tax rate of return of 6.00% per year with a standard deviation(risk) of 5.11%. This means that on average you could see an annual return of about 6.00%, but your return inmost years could be as high as 15.89% or as low as -4.56%.*The proposed asset mix provides an expected pre-tax return of 7.20% per year with a standard deviation of7.24%. With this asset mix, your return in most years could be as high as 21.92% or as low as -7.05%.

Pre-Retirement Goals

Your projected assets provide sufficient resources to fully fund all your pre-retirement goals.

Retirement Goals

The resources you have available could provide 102.08% of your retirement spending goals.By implementing the planning alternatives selected in this plan, you could fund 85.22% of your retirementspending goals.

Estate Preservation

Prior to implementing the estate planning alternatives, your beneficiaries may receive $1,816,641 after payingan estate tax liability of $676,773.With the estate planning alternatives implemented, your beneficiaries may receive $2,391,222 after paying anestate tax liability of $262,736.

Long-term Care

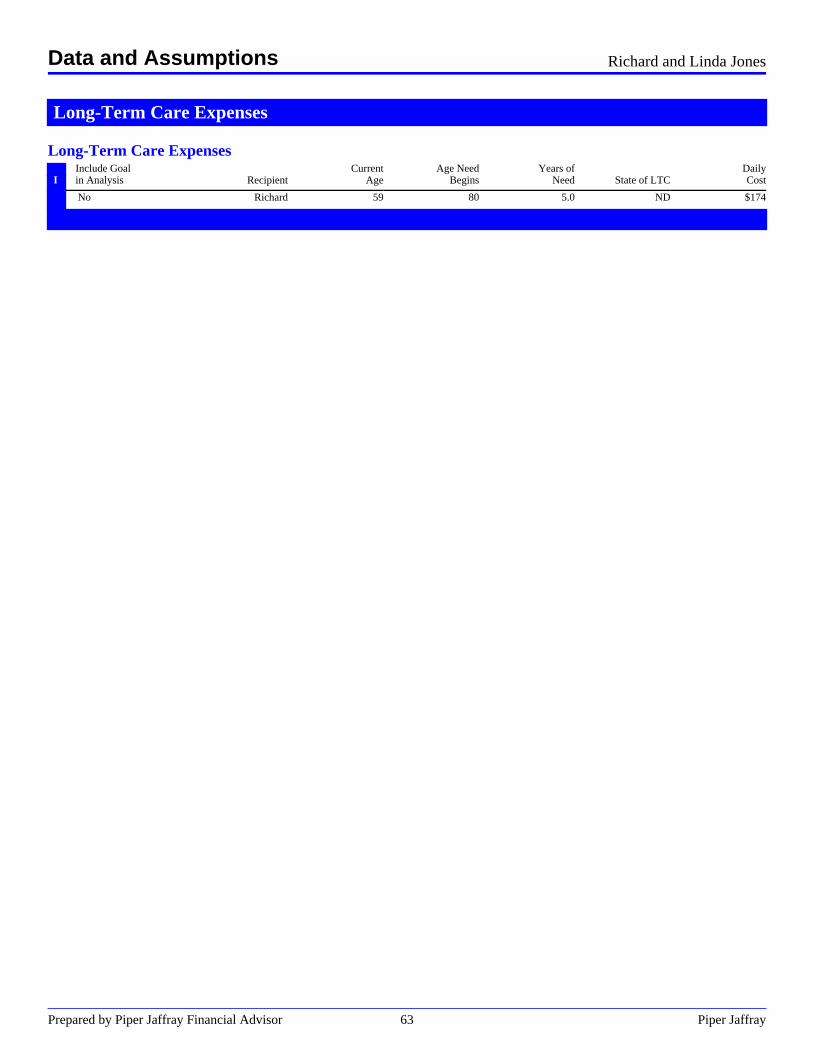

Based on the information you provided about an assumed or expected long-term care situation, you would needto set aside about $0, in today's dollars, to fully fund this need.

*Returns are not guaranteed and do not reflect the performance of any particular investment product. Individual investor results will vary. Expectedreturn and risk are based on client assumptions and calculated using statistical analysis and may not reflect actual market data. Historical performanceis no indication of future results.

Note: See data and assumptions, disclosures and methodology explanations for important information about this report.

Executive Summary - Planning Summary Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 8 Piper Jaffray

.

Financial Statements

Prepared by Piper Jaffray Financial Advisor 9 Piper Jaffray

Financial Statements Introduction

A financial statement deals with cash management. Your access to cash influences your level of financialcomfort and the range of investment decisions that you can make. Personal financial statements help youcarefully manage your cash by providing a cash flow statement, and your assets and liabilities by providing anet worth statement. How you manage your cash, assets, and liabilities can largely determine whether you reachyour financial objectives. Monitoring your financial statements can help you achieve your financial goals.

This section of the report includes the following financial statements:

· Net worth statement· Insurance schedule· Current year cash flow statement· Income tax estimate with supporting statements· Pro forma financial statements

Financial Statements Defined

Net worth statement- A statement of net worth, which is sometimes called a balance sheet, provides anoverview of an individual's current financial situation. In this report, the Assets section represents what youcurrently own, stated at market values. The Liabilities section illustrates your current debt balances. The NetWorth section shows the approximate amount that would be left if you sold all your assets and paid off yourdebts. Your Net Worth Statement is an estimate of your current wealth. One of the main objectives of financialplanning is to increase your net worth.

Cash flow statement- A cash flow statement, which is sometimes called an income statement, summarizes anindividual's financial activity over a given period of time. The cash flow statement in this report tracks yourincome (cash inflows) and uses of cash (cash outflows) during the current year. The difference between theincome you receive and the cash you use is your net cash flow.

Income tax estimate- The income tax estimate included in this report is not a substitute for the advice of aqualified tax consultant. It is provided to give you a general idea of the portion of your income that goes toincome taxes. This report also includes schedules that will help you gain a general understanding of howincome taxes are estimated. The schedules include:· Schedule of capital gains and losses· Schedule of itemized deductions· Schedule of personal exemptions

Pro forma financial statements- Pro forma financial statements project an individual's current financialsituation for many years into the future. The statements in this report can help you estimate and then monitor thechanges in your wealth over your lifetime.

Benefits of Regular Review

Regular review of your personal financial statements can help you confirm that you are on track to achieve yourfinancial goals. Your cash flow statement will help you monitor your spending so you can make any neededadjustments in the future. The balance sheet helps you see how well you are working toward achieving yourobjectives.

Financial Statements Overview Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 10 Piper Jaffray

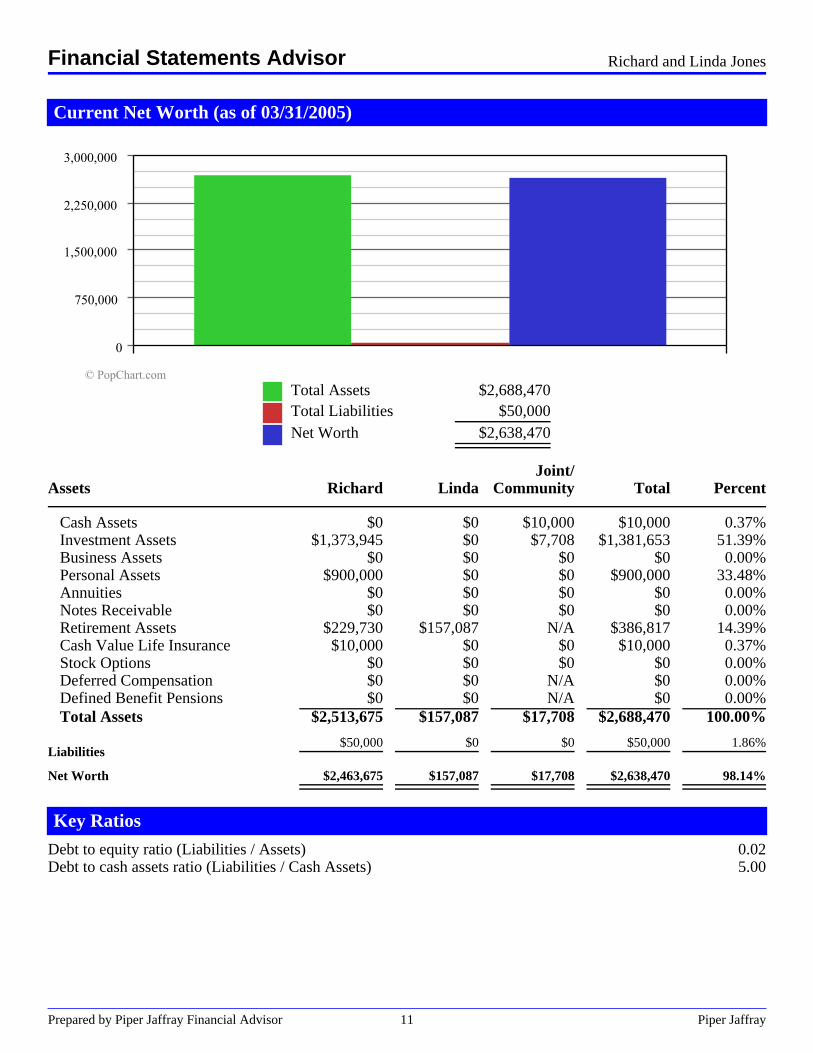

Current Net Worth (as of 03/31/2005)

.

. Total Assets $2,688,470..

. Total Liabilities $50,000.

. . Net Worth $2,638,470.

.

. Joint/ .Assets Richard Linda Community Total Percent.

Cash Assets $0 $0 $10,000 $10,000 0.37%Investment Assets $1,373,945 $0 $7,708 $1,381,653 51.39%Business Assets $0 $0 $0 $0 0.00%Personal Assets $900,000 $0 $0 $900,000 33.48%Annuities $0 $0 $0 $0 0.00%Notes Receivable $0 $0 $0 $0 0.00%Retirement Assets $229,730 $157,087 N/A $386,817 14.39%Cash Value Life Insurance $10,000 $0 $0 $10,000 0.37%Stock Options $0 $0 $0 $0 0.00%Deferred Compensation $0 $0 N/A $0 0.00%Defined Benefit Pensions . $0 . $0 . N/A . $0 . 0.00%Total Assets $2,513,675 $157,087 $17,708 $2,688,470 100.00%

Liabilities.

$50,000.

$0.

$0.

$50,000.

1.86%

Net Worth.

$2,463,675.

$157,087.

$17,708.

$2,638,470.

98.14%. .

.

.

.

.

.

.

.

.

.

Key Ratios

Debt to equity ratio (Liabilities / Assets) 0.02Debt to cash assets ratio (Liabilities / Cash Assets) 5.00

Financial Statements Advisor Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 11 Piper Jaffray

Current Net Worth Detail (as of 03/31/2005).

. . . . . .

Cash Assets.

Description Value Basis Ownerche cking $10,000 $10,000 JTWROSTotal $10,000 $10,000

.

Investment Assets.

Description Value Basis OwnerCASH $5,000 $5,000 ClientALLIED HEALTHCARE PRODS INC $10,000 $10,000 ClientMEDTRONIC INC $10,000 $10,000 Client

$100,000 $100,000 ClientCASH $250,000 $250,000 Client

$10,000 $10,000 ClientATT CORP $5,000 $5,000 ClientGROWTH FD OF AMERICA $75,000 $75,000 ClientCASH $7,708 $7,708 JTWROSAUSTIN MN 5.25 100114 $52,146 $50,000 ClientMN ST HSG 3.25 070111 $48,344 $50,433 ClientMN ST HI ED 4.375 100117 $24,516 $25,000 ClientMN ST REF UT 5.0 060108 $26,503 $25,260 ClientCASH $15,798 $15,798 ClientSTILLWTR MN 4.1 020112 $41,106 $40,000 ClientCFB CAPITAL IV PFD 7.6% $25,900 $25,000 ClientTODD MRRIS MN3.15 040112 $52,993 $55,632 ClientCHASKA MN 5.125 020107 $26,022 $25,179 ClientUST STRIP INT 0.0 081508 $74,171 $32,172 ClientCROW WING MN 2.0 020106 $49,732 $50,762 ClientUST STRIP INT 0.0 111506 $117,625 $62,688 ClientDULUTH MN 4.875 021533 $28,319 $29,428 ClientWATONWAN MN 5.75 020115 $26,220 $25,000 ClientFHLB BOND 2.125 090705 $99,550 $99,933 Client

$0 $0 ClientTARGET CORP $10,000 $10,000 Client

$50,000 $0 ClientIRA $90,000 $0 ClientDD $50,000 $50,000 ClientTotal $1,381,653 $1,144,993

.

Personal Assets.

Description Value Basis OwnerHOME $900,000 $500,000 ClientTotal $900,000 $500,000

.

Financial Statements Advisor Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 12 Piper Jaffray

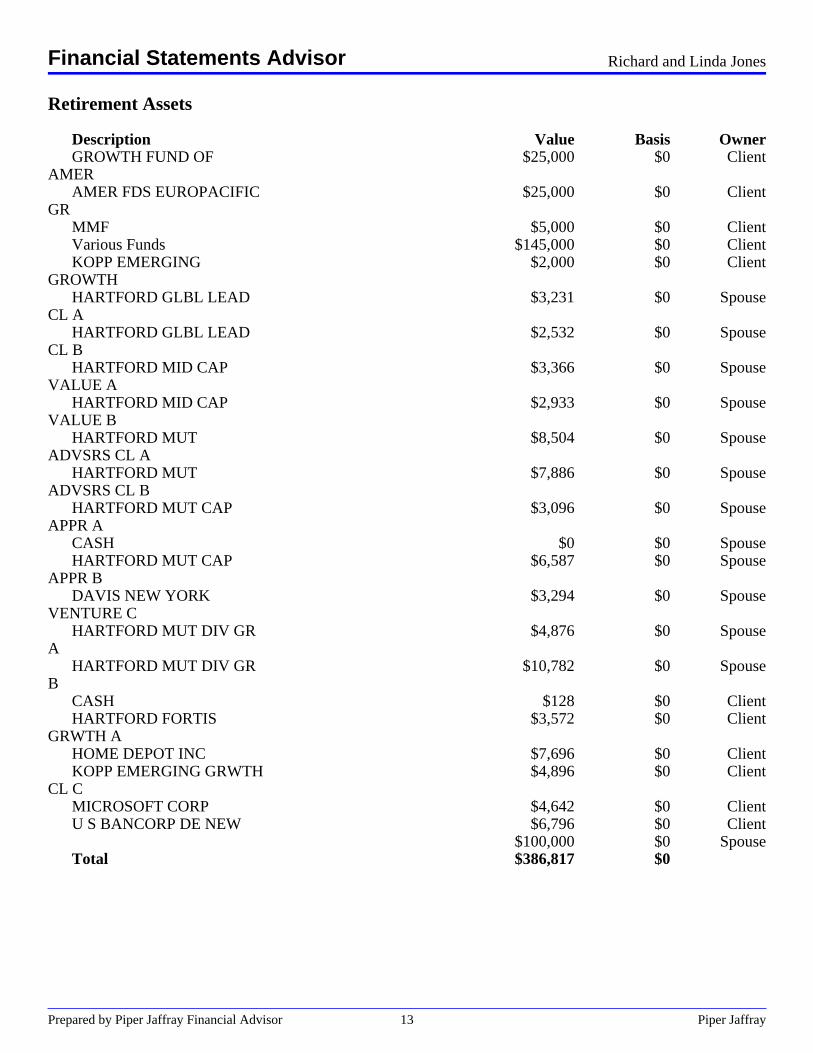

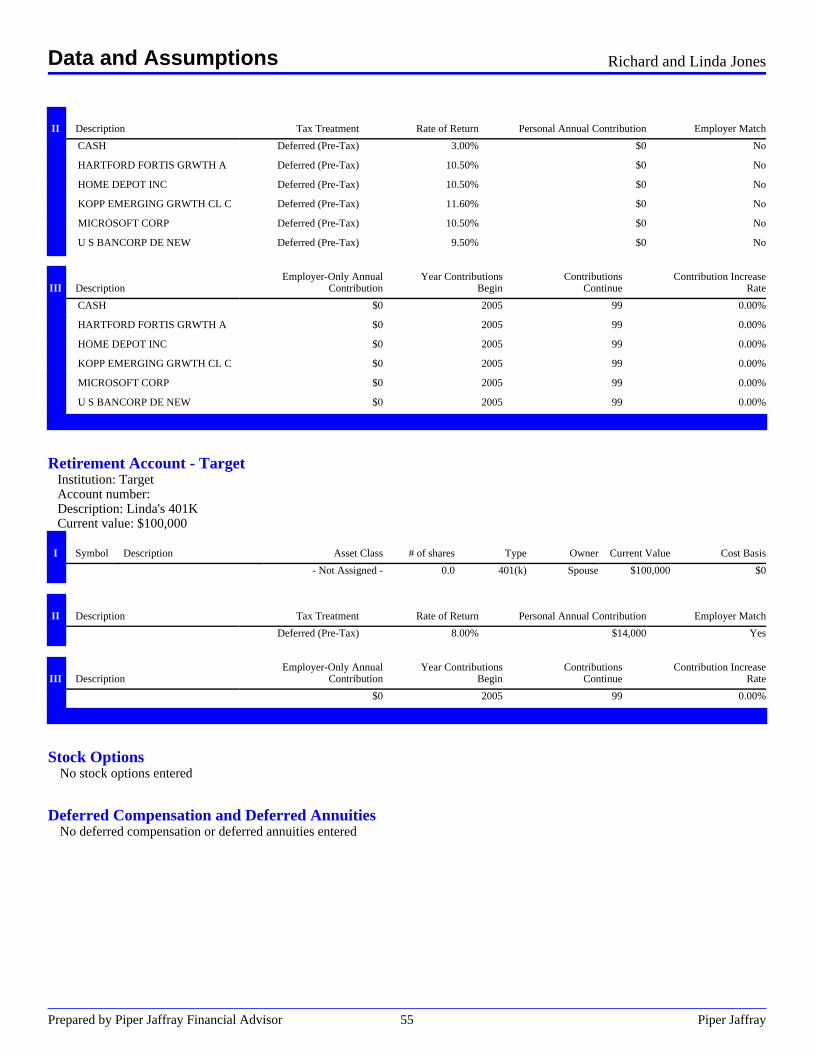

Retirement Assets.

Description Value Basis OwnerGROWTH FUND OF

AMER$25,000 $0 Client

AMER FDS EUROPACIFICGR

$25,000 $0 Client

MMF $5,000 $0 ClientVarious Funds $145,000 $0 ClientKOPP EMERGING

GROWTH$2,000 $0 Client

HARTFORD GLBL LEADCL A

$3,231 $0 Spouse

HARTFORD GLBL LEADCL B

$2,532 $0 Spouse

HARTFORD MID CAPVALUE A

$3,366 $0 Spouse

HARTFORD MID CAPVALUE B

$2,933 $0 Spouse

HARTFORD MUTADVSRS CL A

$8,504 $0 Spouse

HARTFORD MUTADVSRS CL B

$7,886 $0 Spouse

HARTFORD MUT CAPAPPR A

$3,096 $0 Spouse

CASH $0 $0 SpouseHARTFORD MUT CAP

APPR B$6,587 $0 Spouse

DAVIS NEW YORKVENTURE C

$3,294 $0 Spouse

HARTFORD MUT DIV GRA

$4,876 $0 Spouse

HARTFORD MUT DIV GRB

$10,782 $0 Spouse

CASH $128 $0 ClientHARTFORD FORTIS

GRWTH A$3,572 $0 Client

HOME DEPOT INC $7,696 $0 ClientKOPP EMERGING GRWTH

CL C$4,896 $0 Client

MICROSOFT CORP $4,642 $0 ClientU S BANCORP DE NEW $6,796 $0 Client

$100,000 $0 SpouseTotal $386,817 $0

.

Financial Statements Advisor Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 13 Piper Jaffray

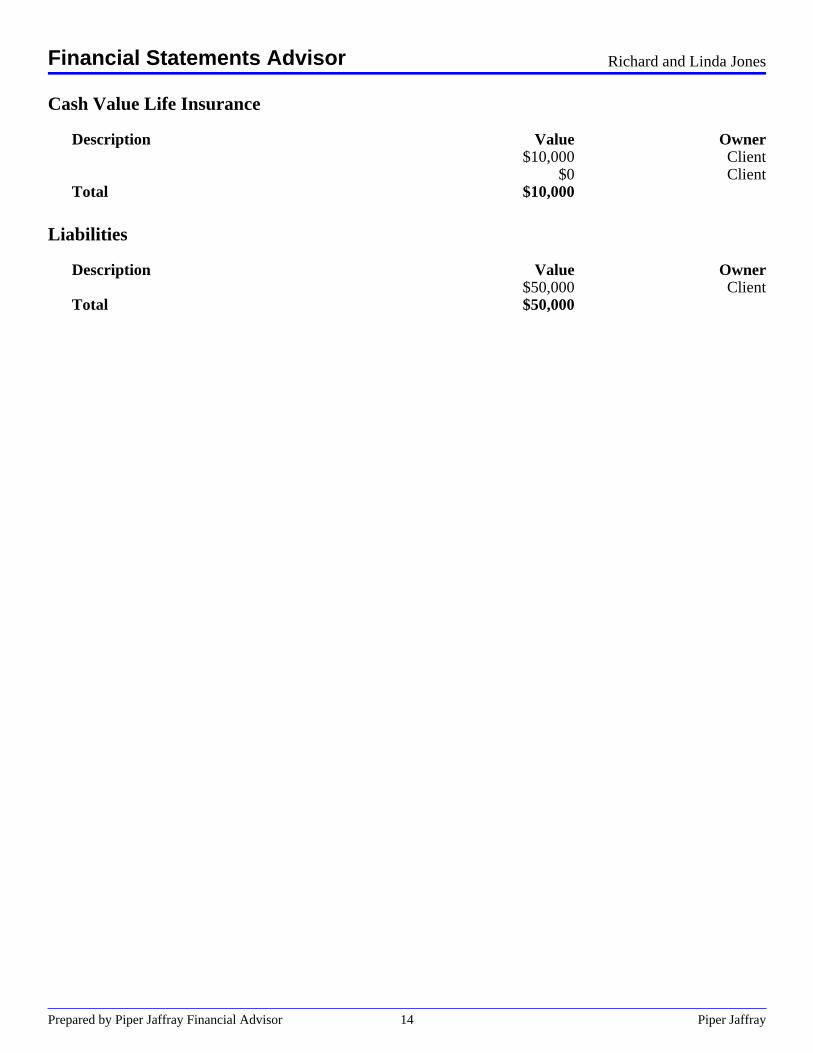

Cash Value Life Insurance.

Description Value Owner$10,000 Client

$0 ClientTotal $10,000

.

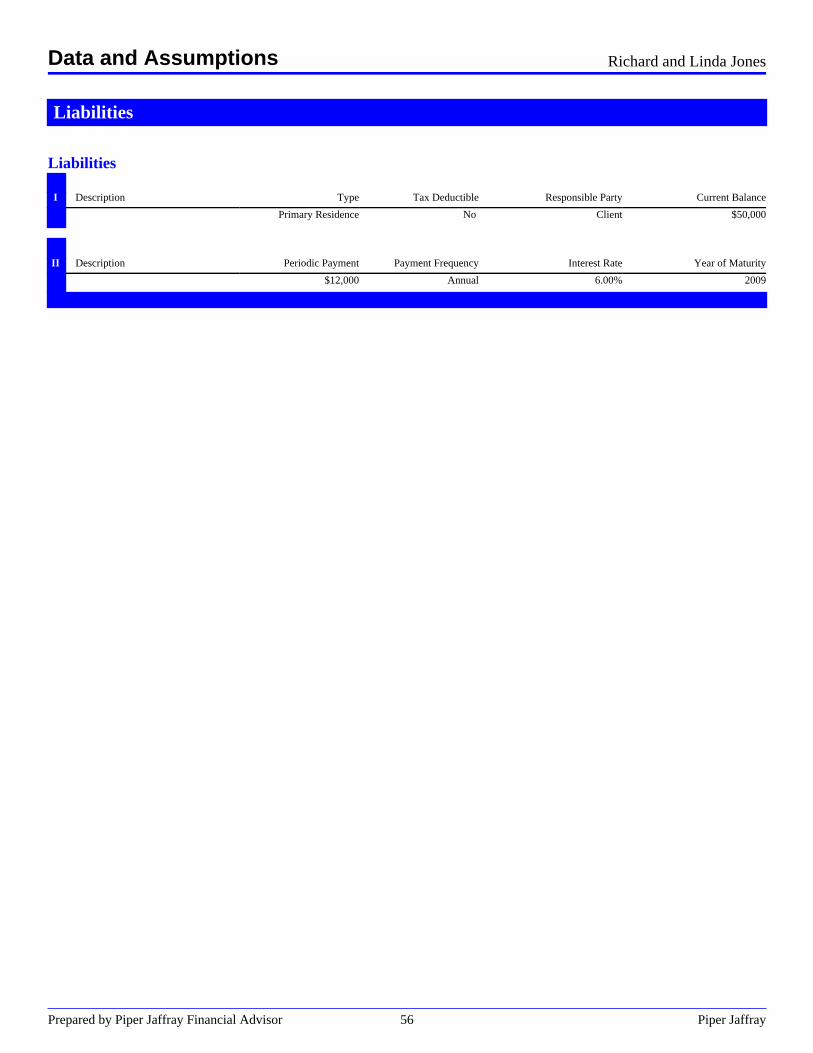

Liabilities.

Description Value Owner$50,000 Client

Total $50,000

Financial Statements Advisor Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 14 Piper Jaffray

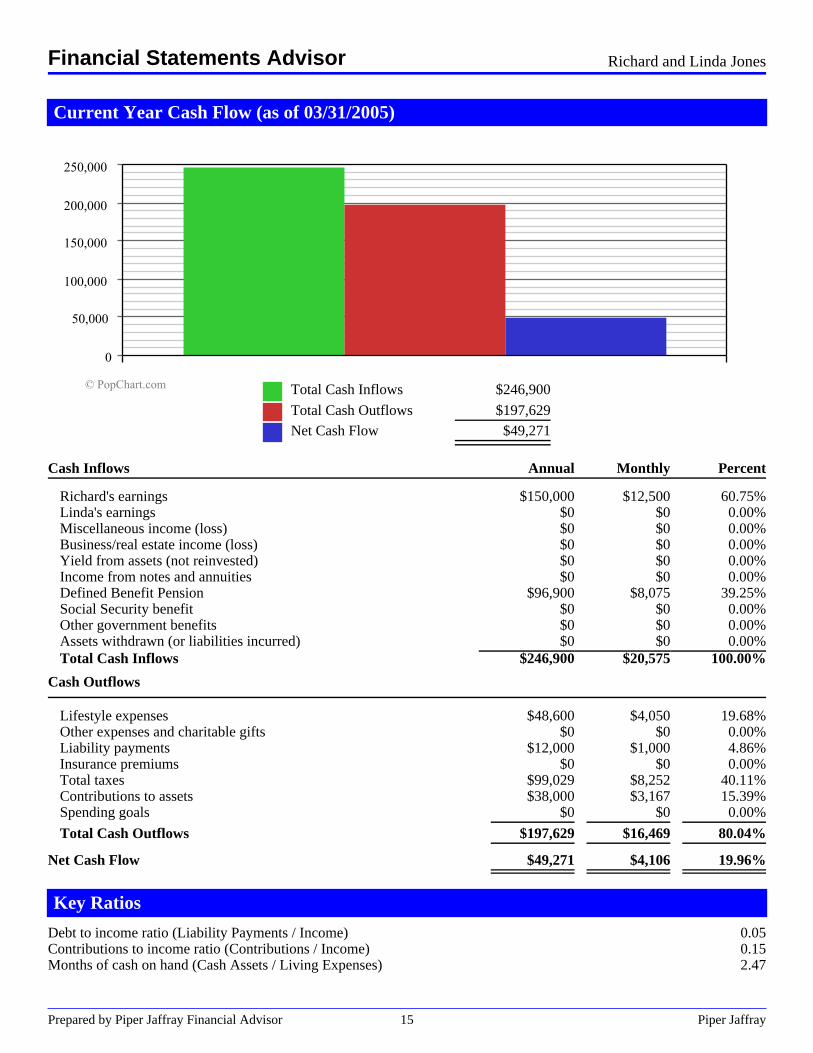

Current Year Cash Flow (as of 03/31/2005)

.

. Total Cash Inflows $246,900..

. Total Cash Outflows $197,629.

. . Net Cash Flow $49,271. .

Cash Inflows Annual Monthly Percent.

Richard's earnings $150,000 $12,500 60.75%Linda's earnings $0 $0 0.00%Miscellaneous income (loss) $0 $0 0.00%Business/real estate income (loss) $0 $0 0.00%Yield from assets (not reinvested) $0 $0 0.00%Income from notes and annuities $0 $0 0.00%Defined Benefit Pension $96,900 $8,075 39.25%Social Security benefit $0 $0 0.00%Other government benefits $0 $0 0.00%Assets withdrawn (or liabilities incurred) $0 $0 0.00%Total Cash Inflows $246,900 $20,575 100.00%

Cash Outflows . . ..

Lifestyle expenses $48,600 $4,050 19.68%Other expenses and charitable gifts $0 $0 0.00%Liability payments $12,000 $1,000 4.86%Insurance premiums $0 $0 0.00%Total taxes $99,029 $8,252 40.11%Contributions to assets $38,000 $3,167 15.39%Spending goals . $0 . $0 . 0.00%

Total Cash Outflows . $197,629 . $16,469 . 80.04%

Net Cash Flow.

$49,271.

$4,106.

19.96%. . . . . .

Key Ratios

Debt to income ratio (Liability Payments / Income) 0.05Contributions to income ratio (Contributions / Income) 0.15Months of cash on hand (Cash Assets / Living Expenses) 2.47

Financial Statements Advisor Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 15 Piper Jaffray

.

Asset AllocationAnalysis

Prepared by Piper Jaffray Financial Advisor 16 Piper Jaffray

Allocating Your Portfolio

This report has been prepared to help you create an asset allocation plan specific to your situation. It can guideyou through the allocation process from defining your personal investment objectives to helping determine asuitable portfolio.

Your Recommended Allocation

The asset allocation plan presented in this report is based on the Nobel-prize winning concepts of ModernPortfolio Theory. This theory holds that you can minimize the effects of investment risk through intelligentdiversification. In a properly diversified portfolio, gains in one investment class may help offset losses inanother.

Remember that this asset allocation plan is designed to help you meet long-term investment objectives, whichare generally assumed to be five or more years in the future. Investing over extended periods of time allows youto assume a reasonable amount of risk with the expectation of higher returns and take advantage of themoderating effect of time on investment risk. In general, The longer an investment's time horizon, the morelikely the investment has the potential to earn a positive return.

Adherence to this asset allocation plan can play a key role in helping you achieve your financial objectives.Like any financial plan, it should be reviewed periodically.

Asset Allocation Analysis - Overview Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 17 Piper Jaffray

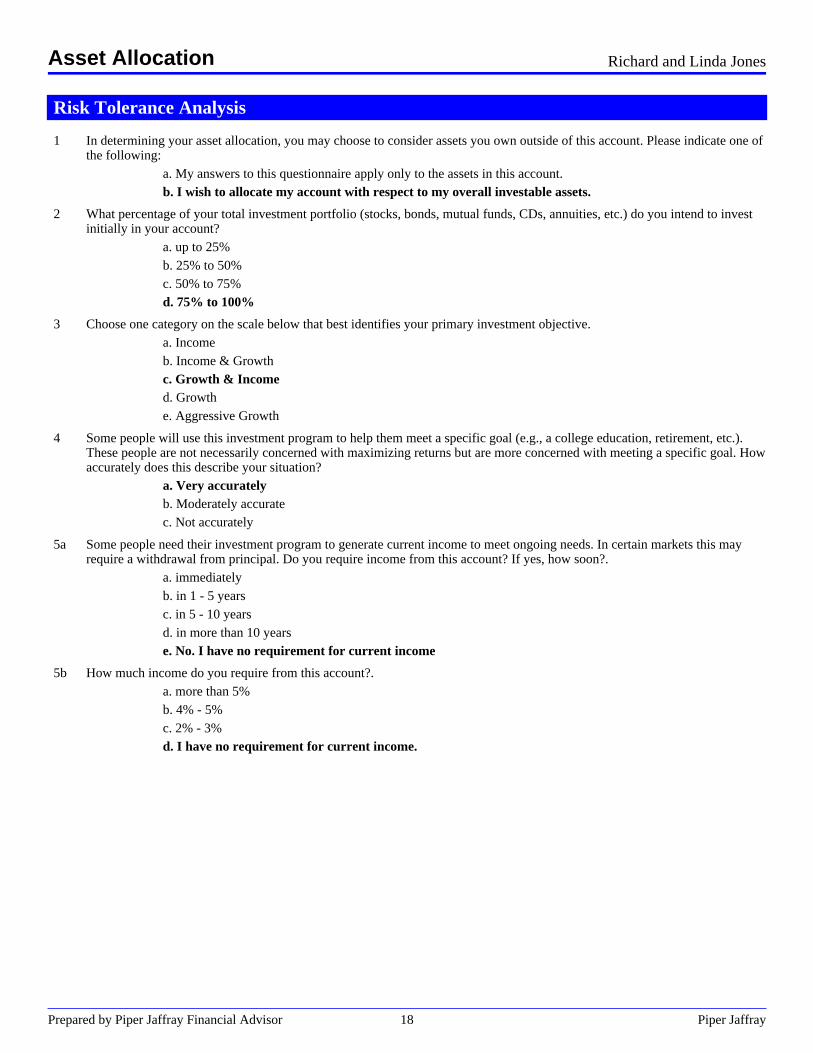

Risk Tolerance Analysis

1 In determining your asset allocation, you may choose to consider assets you own outside of this account. Please indicate one ofthe following:

a. My answers to this questionnaire apply only to the assets in this account.b. I wish to allocate my account with respect to my overall investable assets.

2 What percentage of your total investment portfolio (stocks, bonds, mutual funds, CDs, annuities, etc.) do you intend to investinitially in your account?

a. up to 25%b. 25% to 50%c. 50% to 75%d. 75% to 100%

3 Choose one category on the scale below that best identifies your primary investment objective.a. Incomeb. Income & Growthc. Growth & Incomed. Growthe. Aggressive Growth

4 Some people will use this investment program to help them meet a specific goal (e.g., a college education, retirement, etc.).These people are not necessarily concerned with maximizing returns but are more concerned with meeting a specific goal. Howaccurately does this describe your situation?

a. Very accuratelyb. Moderately accuratec. Not accurately

5a Some people need their investment program to generate current income to meet ongoing needs. In certain markets this mayrequire a withdrawal from principal. Do you require income from this account? If yes, how soon?.

a. immediatelyb. in 1 - 5 yearsc. in 5 - 10 yearsd. in more than 10 yearse. No. I have no requirement for current income

5b How much income do you require from this account?.a. more than 5%b. 4% - 5%c. 2% - 3%d. I have no requirement for current income.

Asset Allocation Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 18 Piper Jaffray

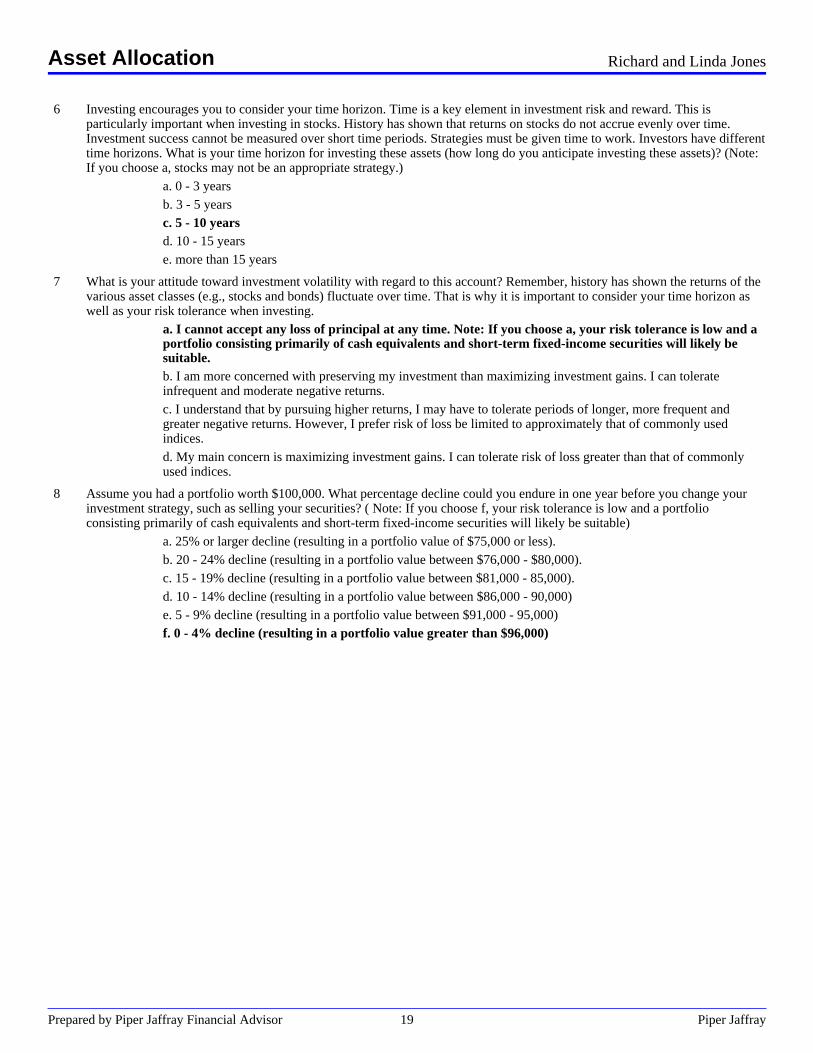

6 Investing encourages you to consider your time horizon. Time is a key element in investment risk and reward. This isparticularly important when investing in stocks. History has shown that returns on stocks do not accrue evenly over time.Investment success cannot be measured over short time periods. Strategies must be given time to work. Investors have differenttime horizons. What is your time horizon for investing these assets (how long do you anticipate investing these assets)? (Note:If you choose a, stocks may not be an appropriate strategy.)

a. 0 - 3 yearsb. 3 - 5 yearsc. 5 - 10 yearsd. 10 - 15 yearse. more than 15 years

7 What is your attitude toward investment volatility with regard to this account? Remember, history has shown the returns of thevarious asset classes (e.g., stocks and bonds) fluctuate over time. That is why it is important to consider your time horizon aswell as your risk tolerance when investing.

a. I cannot accept any loss of principal at any time. Note: If you choose a, your risk tolerance is low and aportfolio consisting primarily of cash equivalents and short-term fixed-income securities will likely besuitable.b. I am more concerned with preserving my investment than maximizing investment gains. I can tolerateinfrequent and moderate negative returns.c. I understand that by pursuing higher returns, I may have to tolerate periods of longer, more frequent andgreater negative returns. However, I prefer risk of loss be limited to approximately that of commonly usedindices.d. My main concern is maximizing investment gains. I can tolerate risk of loss greater than that of commonlyused indices.

8 Assume you had a portfolio worth $100,000. What percentage decline could you endure in one year before you change yourinvestment strategy, such as selling your securities? ( Note: If you choose f, your risk tolerance is low and a portfolioconsisting primarily of cash equivalents and short-term fixed-income securities will likely be suitable)

a. 25% or larger decline (resulting in a portfolio value of $75,000 or less).b. 20 - 24% decline (resulting in a portfolio value between $76,000 - $80,000).c. 15 - 19% decline (resulting in a portfolio value between $81,000 - 85,000).d. 10 - 14% decline (resulting in a portfolio value between $86,000 - 90,000)e. 5 - 9% decline (resulting in a portfolio value between $91,000 - 95,000)f. 0 - 4% decline (resulting in a portfolio value greater than $96,000)

Asset Allocation Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 19 Piper Jaffray

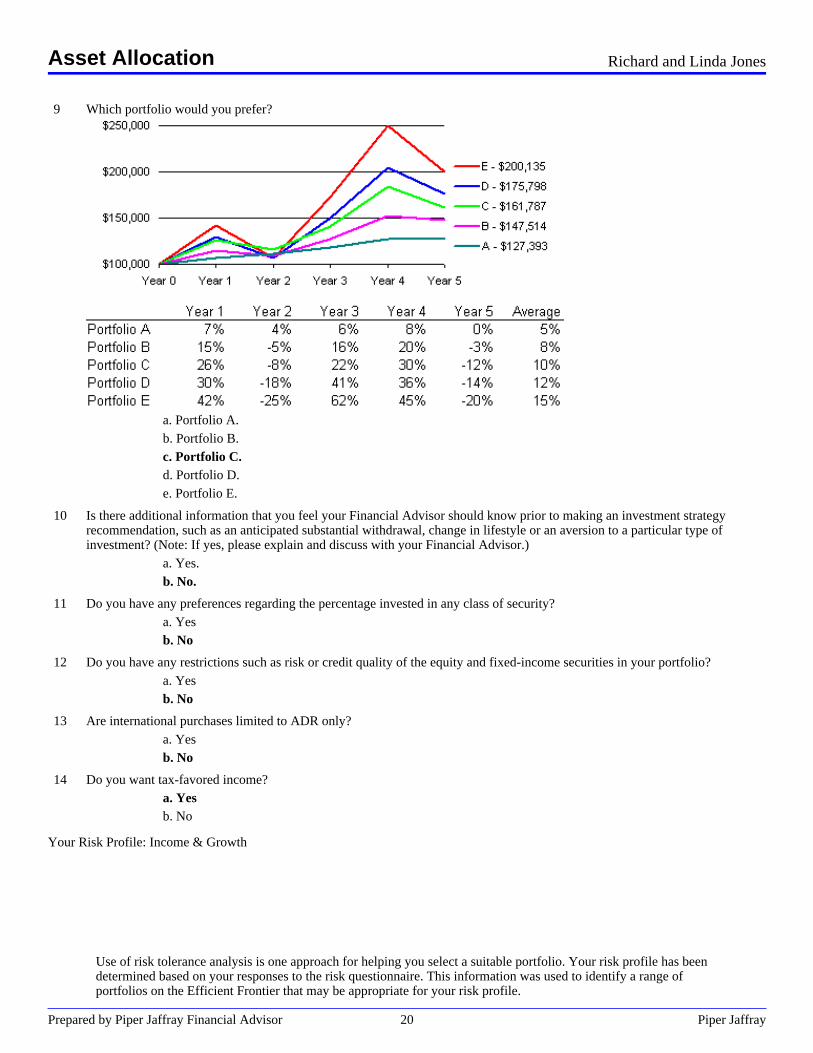

9 Which portfolio would you prefer?

a. Portfolio A.b. Portfolio B.c. Portfolio C.d. Portfolio D.e. Portfolio E.

10 Is there additional information that you feel your Financial Advisor should know prior to making an investment strategyrecommendation, such as an anticipated substantial withdrawal, change in lifestyle or an aversion to a particular type ofinvestment? (Note: If yes, please explain and discuss with your Financial Advisor.)

a. Yes.b. No.

11 Do you have any preferences regarding the percentage invested in any class of security?a. Yesb. No

12 Do you have any restrictions such as risk or credit quality of the equity and fixed-income securities in your portfolio?a. Yesb. No

13 Are international purchases limited to ADR only?a. Yesb. No

14 Do you want tax-favored income?a. Yesb. No

Your Risk Profile: Income & Growth

Use of risk tolerance analysis is one approach for helping you select a suitable portfolio. Your risk profile has beendetermined based on your responses to the risk questionnaire. This information was used to identify a range ofportfolios on the Efficient Frontier that may be appropriate for your risk profile.

Asset Allocation Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 20 Piper Jaffray

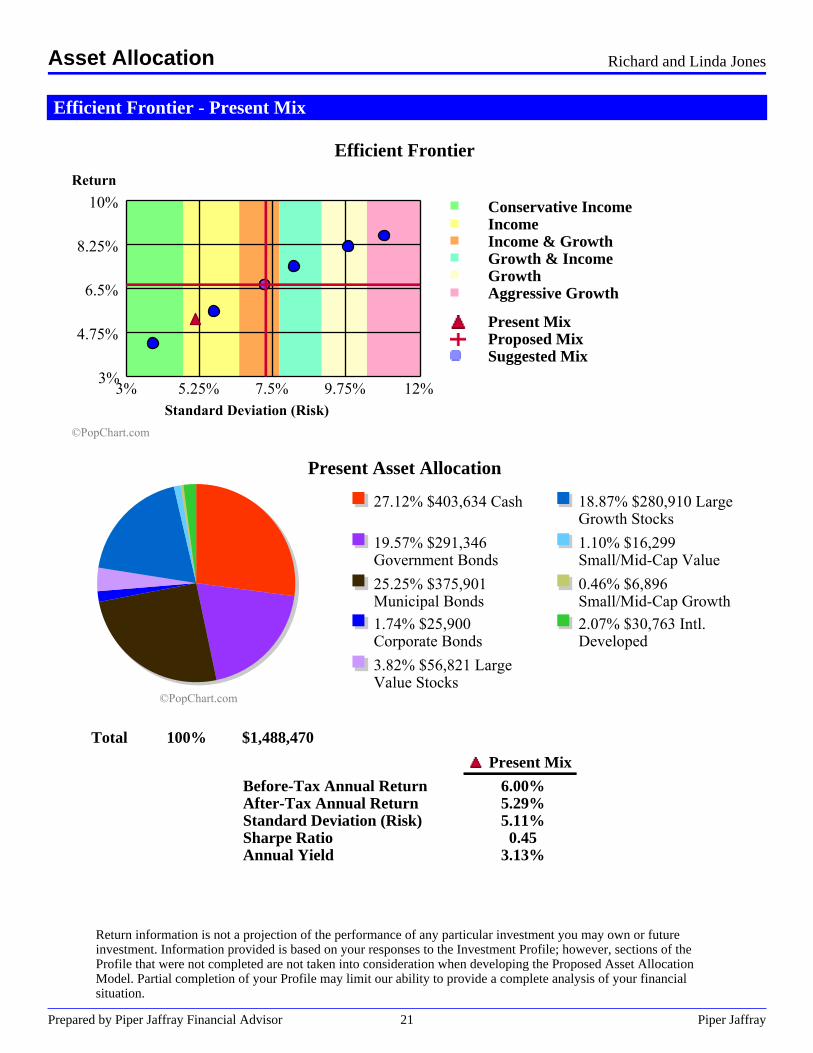

Efficient Frontier - Present Mix

Efficient Frontier

Conservative IncomeIncomeIncome & GrowthGrowth & IncomeGrowthAggressive Growth

Present MixProposed MixSuggested Mix

Present Asset Allocation

Total 100% $1,488,470

Present Mix

Before-Tax Annual Return 6.00%After-Tax Annual Return 5.29%Standard Deviation (Risk) 5.11%Sharpe Ratio 0.45Annual Yield 3.13%

Return information is not a projection of the performance of any particular investment you may own or futureinvestment. Information provided is based on your responses to the Investment Profile; however, sections of theProfile that were not completed are not taken into consideration when developing the Proposed Asset AllocationModel. Partial completion of your Profile may limit our ability to provide a complete analysis of your financialsituation.

Asset Allocation Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 21 Piper Jaffray

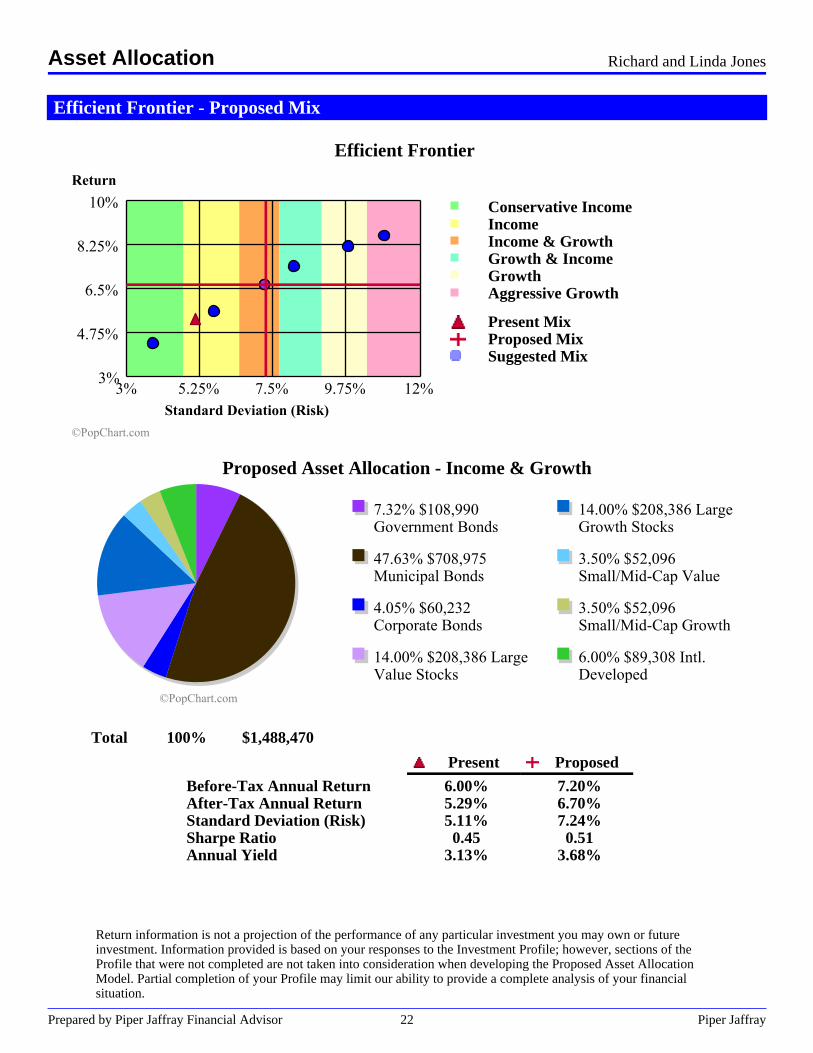

Efficient Frontier - Proposed Mix

Efficient Frontier

Conservative IncomeIncomeIncome & GrowthGrowth & IncomeGrowthAggressive Growth

Present MixProposed MixSuggested Mix

Proposed Asset Allocation - Income & Growth

Total 100% $1,488,470

Present Proposed

Before-Tax Annual Return 6.00% 7.20%After-Tax Annual Return 5.29% 6.70%Standard Deviation (Risk) 5.11% 7.24%Sharpe Ratio 0.45 0.51Annual Yield 3.13% 3.68%

Return information is not a projection of the performance of any particular investment you may own or futureinvestment. Information provided is based on your responses to the Investment Profile; however, sections of theProfile that were not completed are not taken into consideration when developing the Proposed Asset AllocationModel. Partial completion of your Profile may limit our ability to provide a complete analysis of your financialsituation.

Asset Allocation Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 22 Piper Jaffray

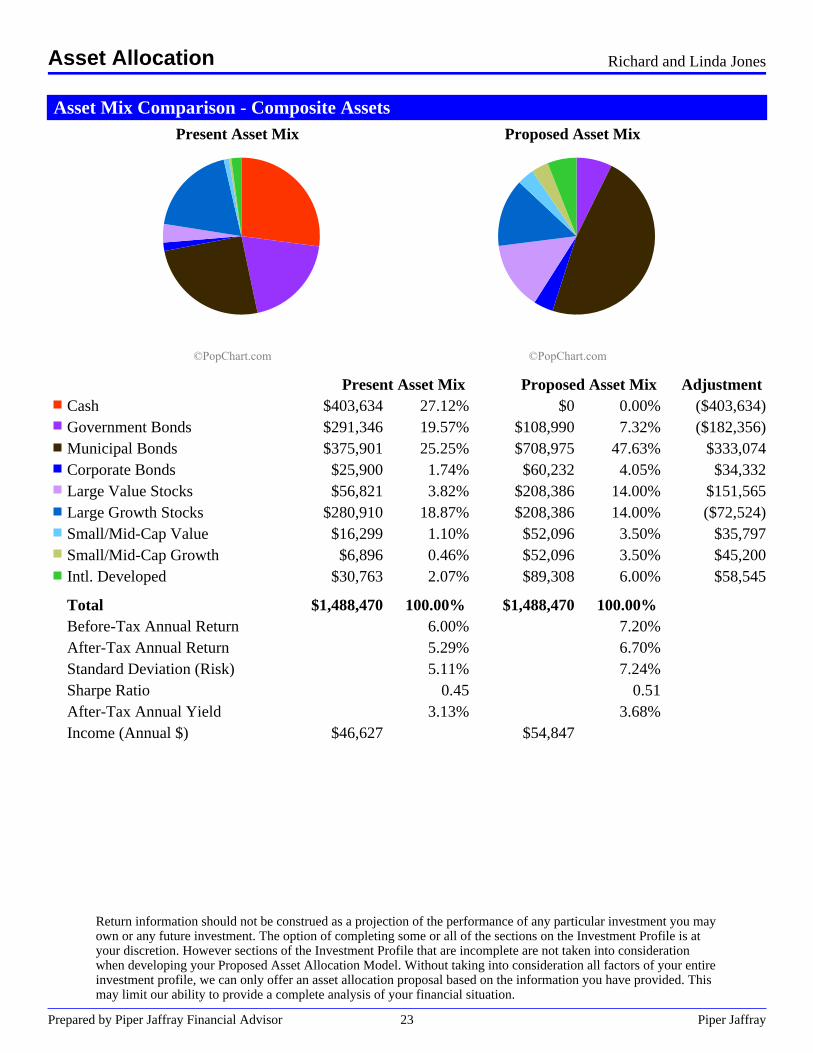

Asset Mix Comparison - Composite AssetsPresent Asset Mix Proposed Asset Mix

Present Asset Mix Proposed Asset Mix AdjustmentCash $403,634 27.12% $0 0.00% ($403,634)Government Bonds $291,346 19.57% $108,990 7.32% ($182,356)Municipal Bonds $375,901 25.25% $708,975 47.63% $333,074Corporate Bonds $25,900 1.74% $60,232 4.05% $34,332Large Value Stocks $56,821 3.82% $208,386 14.00% $151,565Large Growth Stocks $280,910 18.87% $208,386 14.00% ($72,524)Small/Mid-Cap Value $16,299 1.10% $52,096 3.50% $35,797Small/Mid-Cap Growth $6,896 0.46% $52,096 3.50% $45,200Intl. Developed $30,763 2.07% $89,308 6.00% $58,545

Total $1,488,470 100.00% $1,488,470 100.00%Before-Tax Annual Return 6.00% 7.20%After-Tax Annual Return 5.29% 6.70%Standard Deviation (Risk) 5.11% 7.24%Sharpe Ratio 0.45 0.51After-Tax Annual Yield 3.13% 3.68%Income (Annual $) $46,627 $54,847

Return information should not be construed as a projection of the performance of any particular investment you mayown or any future investment. The option of completing some or all of the sections on the Investment Profile is atyour discretion. However sections of the Investment Profile that are incomplete are not taken into considerationwhen developing your Proposed Asset Allocation Model. Without taking into consideration all factors of your entireinvestment profile, we can only offer an asset allocation proposal based on the information you have provided. Thismay limit our ability to provide a complete analysis of your financial situation.

Asset Allocation Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 23 Piper Jaffray

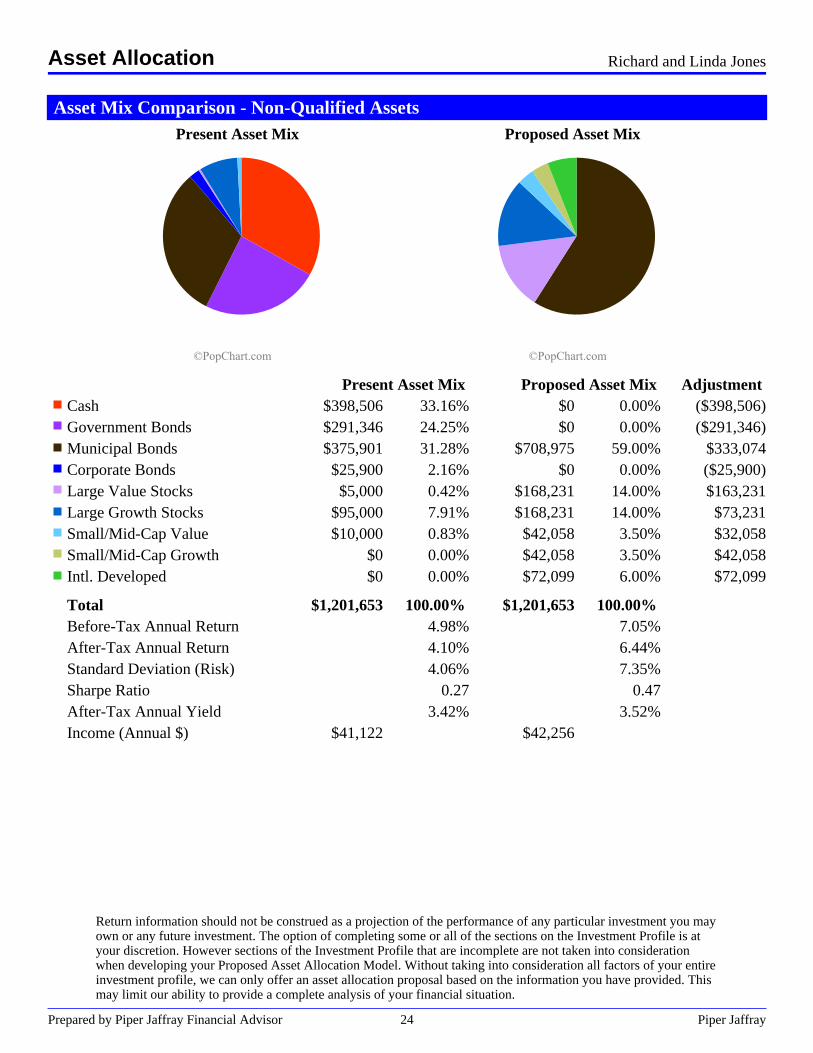

Asset Mix Comparison - Non-Qualified AssetsPresent Asset Mix Proposed Asset Mix

Present Asset Mix Proposed Asset Mix AdjustmentCash $398,506 33.16% $0 0.00% ($398,506)Government Bonds $291,346 24.25% $0 0.00% ($291,346)Municipal Bonds $375,901 31.28% $708,975 59.00% $333,074Corporate Bonds $25,900 2.16% $0 0.00% ($25,900)Large Value Stocks $5,000 0.42% $168,231 14.00% $163,231Large Growth Stocks $95,000 7.91% $168,231 14.00% $73,231Small/Mid-Cap Value $10,000 0.83% $42,058 3.50% $32,058Small/Mid-Cap Growth $0 0.00% $42,058 3.50% $42,058Intl. Developed $0 0.00% $72,099 6.00% $72,099

Total $1,201,653 100.00% $1,201,653 100.00%Before-Tax Annual Return 4.98% 7.05%After-Tax Annual Return 4.10% 6.44%Standard Deviation (Risk) 4.06% 7.35%Sharpe Ratio 0.27 0.47After-Tax Annual Yield 3.42% 3.52%Income (Annual $) $41,122 $42,256

Return information should not be construed as a projection of the performance of any particular investment you mayown or any future investment. The option of completing some or all of the sections on the Investment Profile is atyour discretion. However sections of the Investment Profile that are incomplete are not taken into considerationwhen developing your Proposed Asset Allocation Model. Without taking into consideration all factors of your entireinvestment profile, we can only offer an asset allocation proposal based on the information you have provided. Thismay limit our ability to provide a complete analysis of your financial situation.

Asset Allocation Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 24 Piper Jaffray

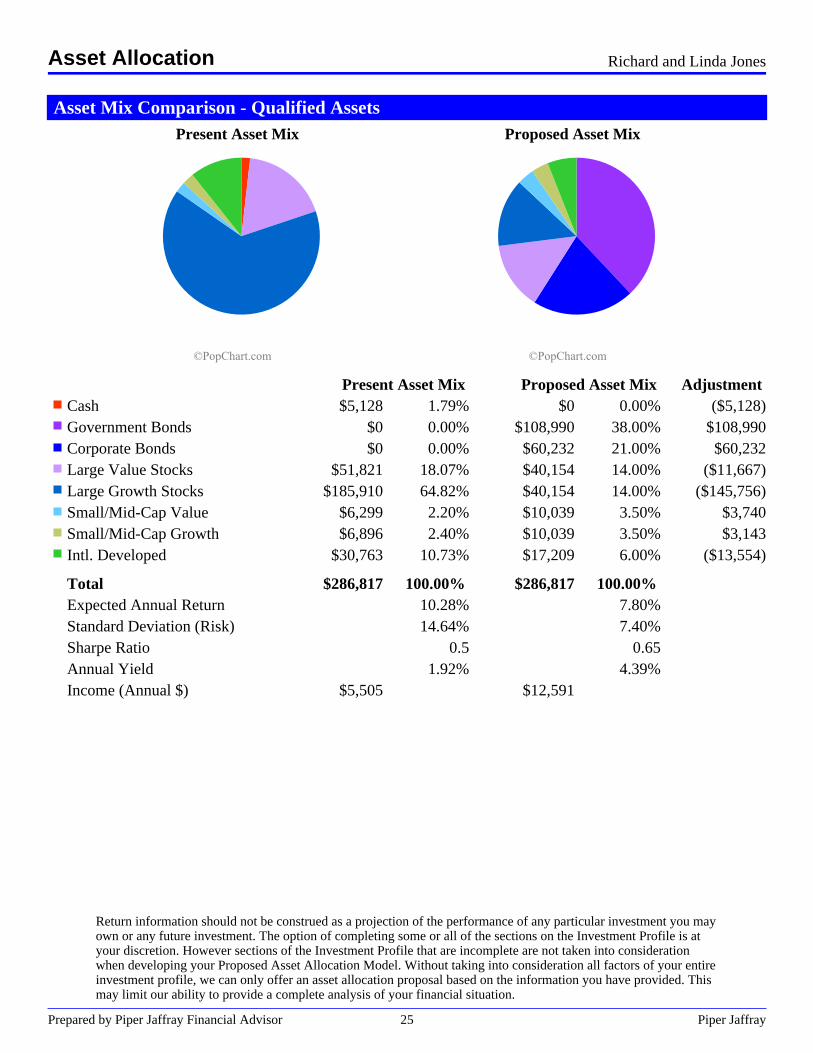

Asset Mix Comparison - Qualified AssetsPresent Asset Mix Proposed Asset Mix

Present Asset Mix Proposed Asset Mix AdjustmentCash $5,128 1.79% $0 0.00% ($5,128)Government Bonds $0 0.00% $108,990 38.00% $108,990Corporate Bonds $0 0.00% $60,232 21.00% $60,232Large Value Stocks $51,821 18.07% $40,154 14.00% ($11,667)Large Growth Stocks $185,910 64.82% $40,154 14.00% ($145,756)Small/Mid-Cap Value $6,299 2.20% $10,039 3.50% $3,740Small/Mid-Cap Growth $6,896 2.40% $10,039 3.50% $3,143Intl. Developed $30,763 10.73% $17,209 6.00% ($13,554)

Total $286,817 100.00% $286,817 100.00%Expected Annual Return 10.28% 7.80%Standard Deviation (Risk) 14.64% 7.40%Sharpe Ratio 0.5 0.65Annual Yield 1.92% 4.39%Income (Annual $) $5,505 $12,591

Return information should not be construed as a projection of the performance of any particular investment you mayown or any future investment. The option of completing some or all of the sections on the Investment Profile is atyour discretion. However sections of the Investment Profile that are incomplete are not taken into considerationwhen developing your Proposed Asset Allocation Model. Without taking into consideration all factors of your entireinvestment profile, we can only offer an asset allocation proposal based on the information you have provided. Thismay limit our ability to provide a complete analysis of your financial situation.

Asset Allocation Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 25 Piper Jaffray

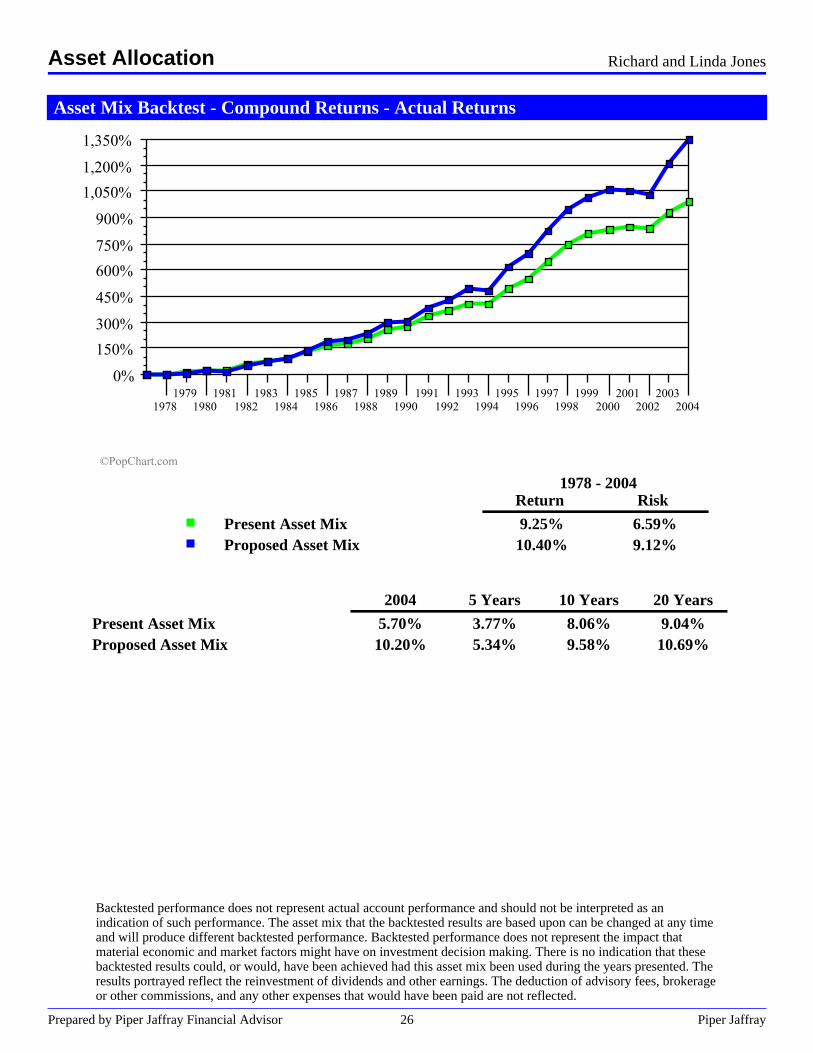

Asset Mix Backtest - Compound Returns - Actual Returns

1978 - 2004Return Risk

Present Asset Mix 9.25% 6.59%Proposed Asset Mix 10.40% 9.12%

2004 5 Years 10 Years 20 Years

Present Asset Mix 5.70% 3.77% 8.06% 9.04%Proposed Asset Mix 10.20% 5.34% 9.58% 10.69%

Backtested performance does not represent actual account performance and should not be interpreted as anindication of such performance. The asset mix that the backtested results are based upon can be changed at any timeand will produce different backtested performance. Backtested performance does not represent the impact thatmaterial economic and market factors might have on investment decision making. There is no indication that thesebacktested results could, or would, have been achieved had this asset mix been used during the years presented. Theresults portrayed reflect the reinvestment of dividends and other earnings. The deduction of advisory fees, brokerageor other commissions, and any other expenses that would have been paid are not reflected.

Asset Allocation Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 26 Piper Jaffray

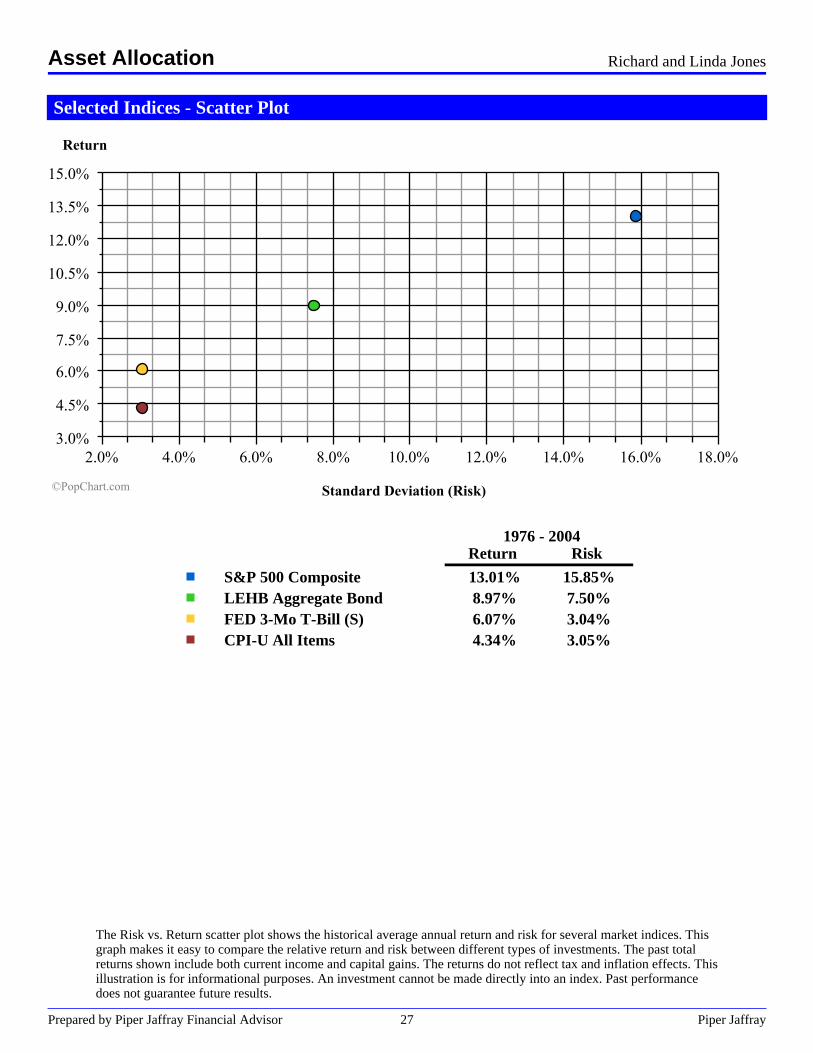

Selected Indices - Scatter Plot

1976 - 2004Return Risk

S&P 500 Composite 13.01% 15.85%LEHB Aggregate Bond 8.97% 7.50%FED 3-Mo T-Bill (S) 6.07% 3.04%CPI-U All Items 4.34% 3.05%

The Risk vs. Return scatter plot shows the historical average annual return and risk for several market indices. Thisgraph makes it easy to compare the relative return and risk between different types of investments. The past totalreturns shown include both current income and capital gains. The returns do not reflect tax and inflation effects. Thisillustration is for informational purposes. An investment cannot be made directly into an index. Past performancedoes not guarantee future results.

Asset Allocation Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 27 Piper Jaffray

Scenario Assumptions

Scenario AssumptionsAsset Class Index Proxy Return Risk Yield Dividend TurnoverCash CITI 3-mo T-bill 3.00% 2.00% 3.00% 0.00% 100.00%T-Notes/CDs FED 6-Month CD 3.50% 3.00% 3.50% 0.00% 100.00%Government Bonds LEHB Government Bond 5.75% 6.00% 5.75% 0.00% 40.00%Municipal Bonds LEHB Municipal Bond 4.75% 8.00% 4.75% 0.00% 40.00%Corporate Bonds LEHB Credit Bond 6.50% 8.50% 6.50% 0.00% 40.00%High Yield Bonds LEHB High Yield 9.25% 16.00% 9.50% 0.00% 40.00%International Bonds CITI NonUS WGBI-All$ 7.00% 13.25% 7.00% 0.00% 40.00%Large Value Stocks BARA S&P500 Value 9.50% 13.25% 0.00% 2.50% 40.00%Large Growth Stocks BARA S&P500 Growth 10.50% 16.25% 0.00% 1.75% 40.00%Small/Mid-Cap Value WILS Tgt Small Value 11.00% 18.75% 0.00% 2.00% 40.00%Small/Mid-Cap Growth WILS Tgt Small Grth 11.60% 21.75% 0.00% 2.00% 40.00%Intl. Developed MSCI EAFE Index-$ 11.00% 22.25% 0.00% 1.75% 40.00%Emerging Equities MSCI Emerg Free-$ 11.50% 40.25% 0.00% 0.75% 40.00%REITs NAR REITs-All 7.50% 14.00% 5.50% 0.00% 10.00%Managed Futures CISDM-Fund/Pool-$ 8.00% 30.00% 0.00% 0.00% 100.00%Hedge Funds HFRI Fund of Funds 8.50% 12.00% 2.00% 0.00% 60.00%Venture Capital/L.P. CAMB US Venture Cap 12.50% 35.25% 0.00% 0.00% 10.00%

Inflation Rate: 3.00%

Holding LimitsNon-Qualified Assets Qualified Assets Non-Qualified Tax-Def

AssetsAsset Class Min % Max % Min % Max % Min % Max %Cash 0.00% 35.00% 0.00% 35.00% 0.00% 35.00%T-Notes/CDs 0.00% 20.00% 0.00% 20.00% 0.00% 20.00%Government Bonds 0.00% 60.00% 0.00% 60.00% 0.00% 60.00%Municipal Bonds 0.00% 60.00% 0.00% 0.00% 0.00% 0.00%Corporate Bonds 0.00% 35.00% 0.00% 35.00% 0.00% 35.00%High Yield Bonds 0.00% 25.00% 0.00% 25.00% 0.00% 25.00%International Bonds 0.00% 10.00% 0.00% 10.00% 0.00% 10.00%Large Value Stocks 0.00% 50.00% 0.00% 50.00% 0.00% 50.00%Large Growth Stocks 0.00% 50.00% 0.00% 50.00% 0.00% 50.00%Small/Mid-Cap Value 0.00% 50.00% 0.00% 50.00% 0.00% 50.00%Small/Mid-Cap Growth 0.00% 50.00% 0.00% 50.00% 0.00% 50.00%Intl. Developed 0.00% 25.00% 0.00% 25.00% 0.00% 25.00%Emerging Equities 0.00% 10.00% 0.00% 10.00% 0.00% 10.00%REITs 0.00% 10.00% 0.00% 10.00% 0.00% 10.00%Managed Futures 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Hedge Funds 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%Venture Capital/L.P. 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

Scenario assumptions are based on the estimates of the future performance for each major asset class, which isrepresented by each of its respective market index. These estimates are based on the estimated long-term averagemedian total annual return. These estimates do not rely solely on historical performance and past performance is notindicative of future results. Indexes are unmanaged and an investment cannot be made directly into an index.

Asset Allocation Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 28 Piper Jaffray

.

Retirement PlanningAnalysis

Prepared by Piper Jaffray Financial Advisor 29 Piper Jaffray

Planning For Your Retirement

The purpose of retirement planning is to determine the level of funding needed to help meet your retirementgoals and identify the actions you will need to take to achieve that level of funding. A good retirement plan willanswer the following questions about your current retirement preparations and objectives:

· What would my spendable income during retirement be if I maintain my current patterns of income,spending, and saving?

· How much would I have to save annually in order to achieve my annual retirement spending objective?· How will varying the assumed rates of return on my assets affect the results of the analysis?· What can I do to facilitate more rapid growth of wealth?

Your Retirement Plan

In this report, your retirement plan is analyzed in two different ways, as summarized below, using two sets ofassumptions.

· First, your current commitment to saving and investing is assumed to remain constant, and your currentsituation is projected into the future. This illustrates the income you might have available during retirement ifyour current saving and investment patterns do not change.

· Second, changes are made to your current level of saving and investing, as well as to your assumed returnsand alternatives, that may enhance your projected retirement situation. The results of these changes arecompared to your desired retirement spending objective and to the original projection.

Benefits of Retirement Planning

Among other benefits, a proper retirement plan can:

· Help you set attainable spending goals for retirement· Help you understand where you are in relationship to your goals· Illustrate the impact of changing your current spending and saving patterns· Help you utilize planning concepts such as tax deferral, time horizons, and tax reduction.

Retirement Planning Analysis - Overview Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 30 Piper Jaffray

FYI

People are living longerand spending more timein retirement than ageneration ago.

If you retire at age 65,you can expect to livean additional 20 years(male) to 23 years(female).

Some people will livebeyond their lifeexpectancy, perhapseven past age 100. Youmay want to consider along life expectancy inyour planning.

Source: Society ofActuaries Annuity 2000Mortality Table

Inflation rates havevaried from year to yearand will vary in thefuture. The generalinflation rate used forthis analysis should bean average rate tocompensate for annualvariations.

The rate of return onyour assets can have asignificant impact onthe balance of youraccounts over time. Besure to monitor youractual returns regularlyto see how closely theymatch your plan.

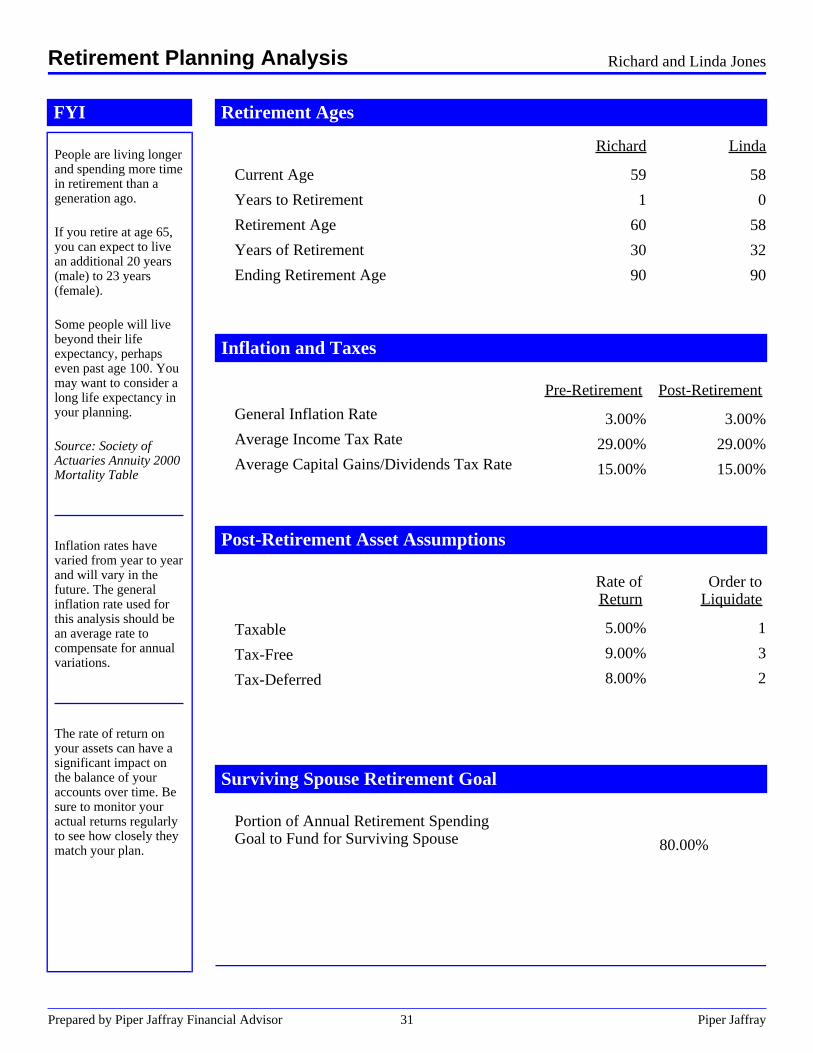

Retirement Ages

Current Age

Years to Retirement

Retirement Age

Years of Retirement

Ending Retirement Age

Richard

59

1

60

30

90

Linda

58

0

58

32

90

Inflation and Taxes

General Inflation Rate

Average Income Tax Rate

Average Capital Gains/Dividends Tax Rate

Pre-Retirement

3.00%

29.00%

15.00%

Post-Retirement

3.00%

29.00%

15.00%

Post-Retirement Asset Assumptions

Taxable

Tax-Free

Tax-Deferred

Rate ofReturn

5.00%

9.00%

8.00%

Order toLiquidate

1

3

2

Surviving Spouse Retirement Goal

Portion of Annual Retirement SpendingGoal to Fund for Surviving Spouse 80.00%

Retirement Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 31 Piper Jaffray

FYI

Cash assets may includecash, savings accounts,CDs, and short-termbonds.

Investment assets mayinclude taxablebrokerage accounts,stocks, mutual funds,and bonds.

Retirement assetsinclude your currentIRAs, 401(k)s, andother plans dedicated toretirement funding.These funds may be in avariety of differentinvestments, includingcash.

Business assets mayinclude real estate,business inventory, andother business interests.

Personal assets mayinclude a home,artwork, or collectibles.

Government programsinclude Social Security,military service income,and civil serviceincome. To receive apersonal estimate ofbenefits, contact theSocial SecurityAdministration at1-800-772-1213, or visittheir website atwww.ssa.gov (2004).

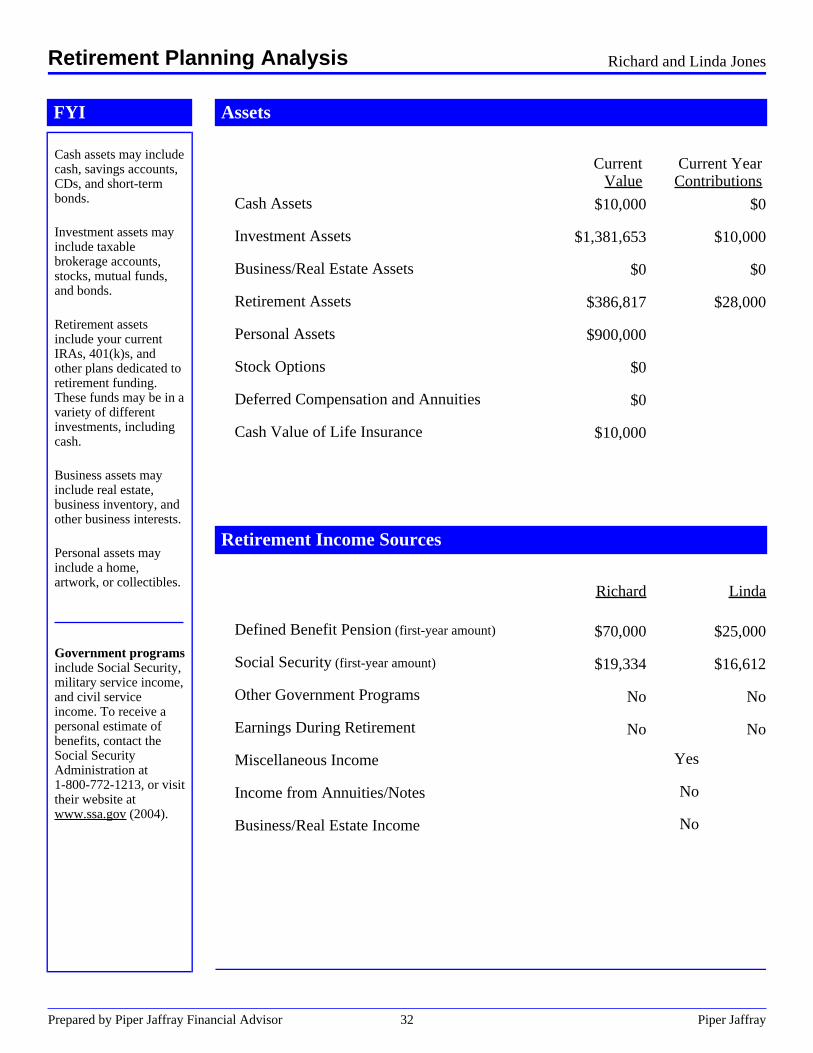

Assets

Cash Assets

Investment Assets

Business/Real Estate Assets

Retirement Assets

Personal Assets

Stock Options

Deferred Compensation and Annuities

Cash Value of Life Insurance

.Current

Value

$10,000

$1,381,653

$0

$386,817

$900,000

$0

$0

$10,000

.Current Year

Contributions

$0

$10,000

$0

$28,000

Retirement Income Sources

Defined Benefit Pension (first-year amount)

Social Security (first-year amount)

Other Government Programs

Earnings During Retirement

Miscellaneous Income

Income from Annuities/Notes

Business/Real Estate Income

Richard

$70,000

$19,334

No

No

Yes

No

No

Linda

$25,000

$16,612

No

No

Retirement Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 32 Piper Jaffray

FYI

Setting financial goalsis the first step toreaching them.

Knowing where you arein relation to yourretirement goals mayhelp you plan moreeffectively forretirement.

Most people need 60% -80% of theirpre-retirement incometo maintain theirstandard of livingduring retirement.

However, a fixedpercentage may not beright for everyone. Theamount you will needdepends on your visionof retirement, includinga variety of optionssuch as work, travel,hobbies, relocation,expenses, and more.

The financial resourcesneeded to meet a majorgoal like retirement canbe overwhelming. Somepeople might prefer toignore the issue. Othersface the issue and builda plan to reach theirgoals. With a plan inplace, even largeobstacles andchallenges can beovercome.

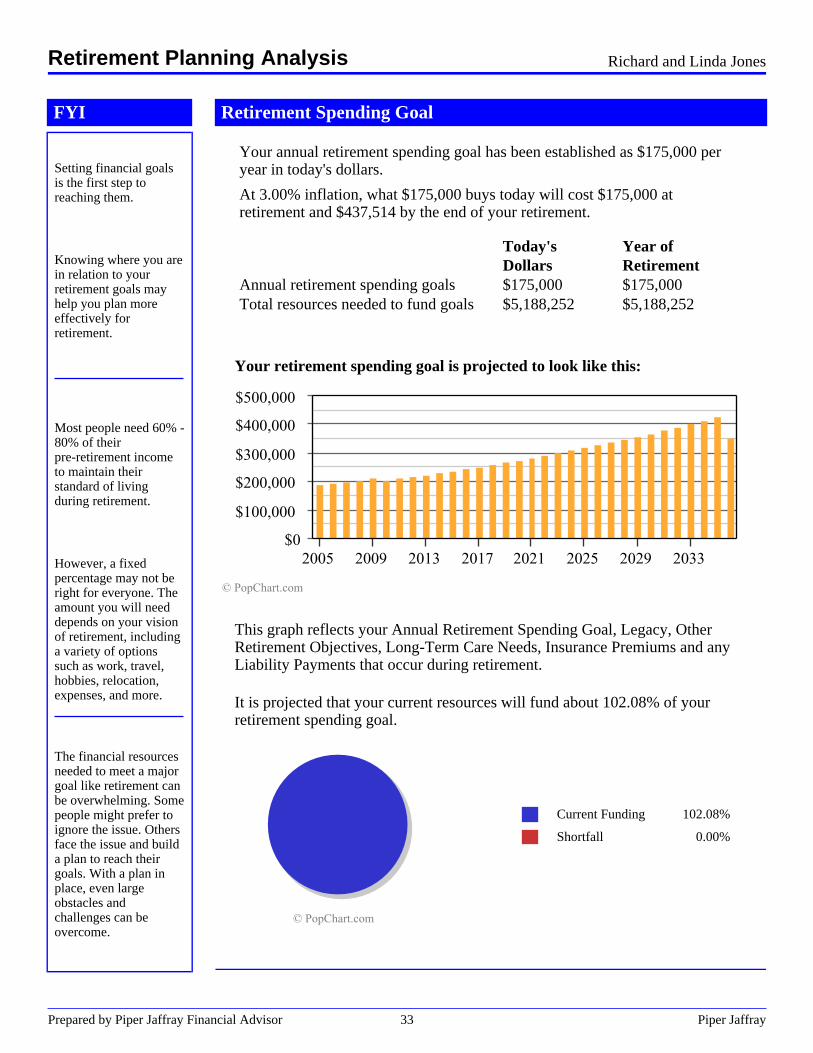

Retirement Spending Goal

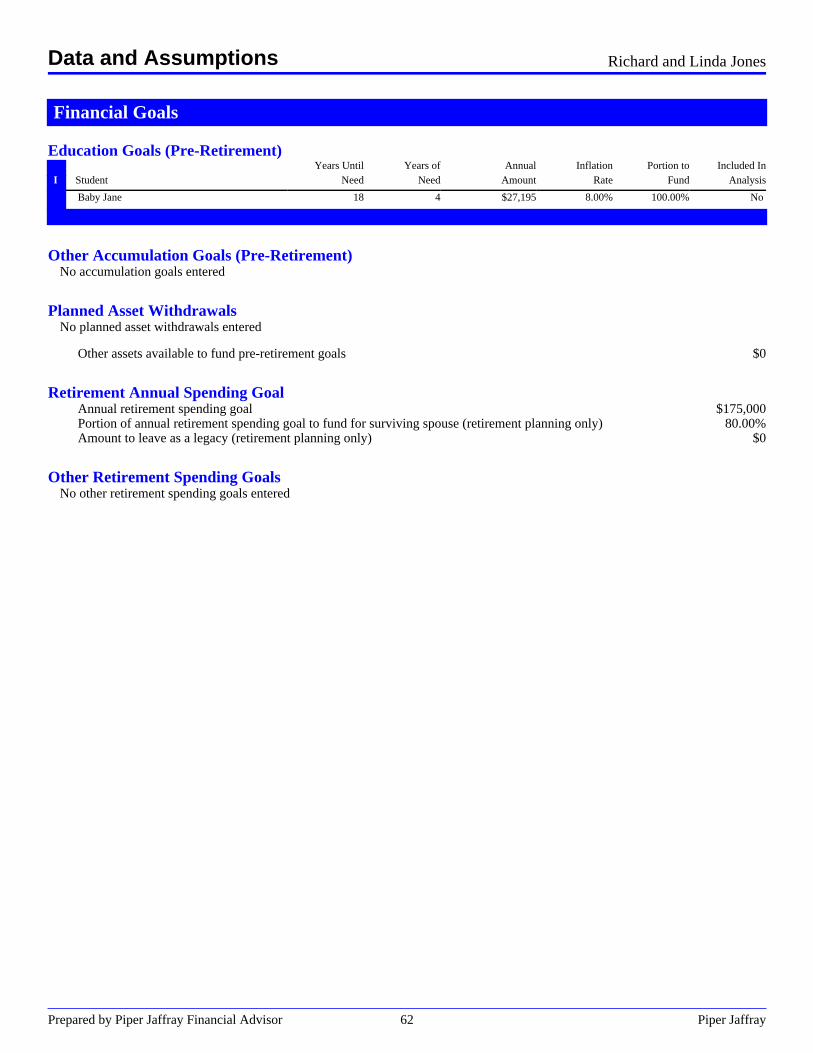

Your annual retirement spending goal has been established as $175,000 peryear in today's dollars.

At 3.00% inflation, what $175,000 buys today will cost $175,000 atretirement and $437,514 by the end of your retirement.

Today's Year ofDollars Retirement

Annual retirement spending goals $175,000 $175,000Total resources needed to fund goals $5,188,252 $5,188,252

Your retirement spending goal is projected to look like this:

This graph reflects your Annual Retirement Spending Goal, Legacy, OtherRetirement Objectives, Long-Term Care Needs, Insurance Premiums and anyLiability Payments that occur during retirement.

It is projected that your current resources will fund about 102.08% of yourretirement spending goal.

. Current Funding 102.08%

. Shortfall 0.00%

Retirement Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 33 Piper Jaffray

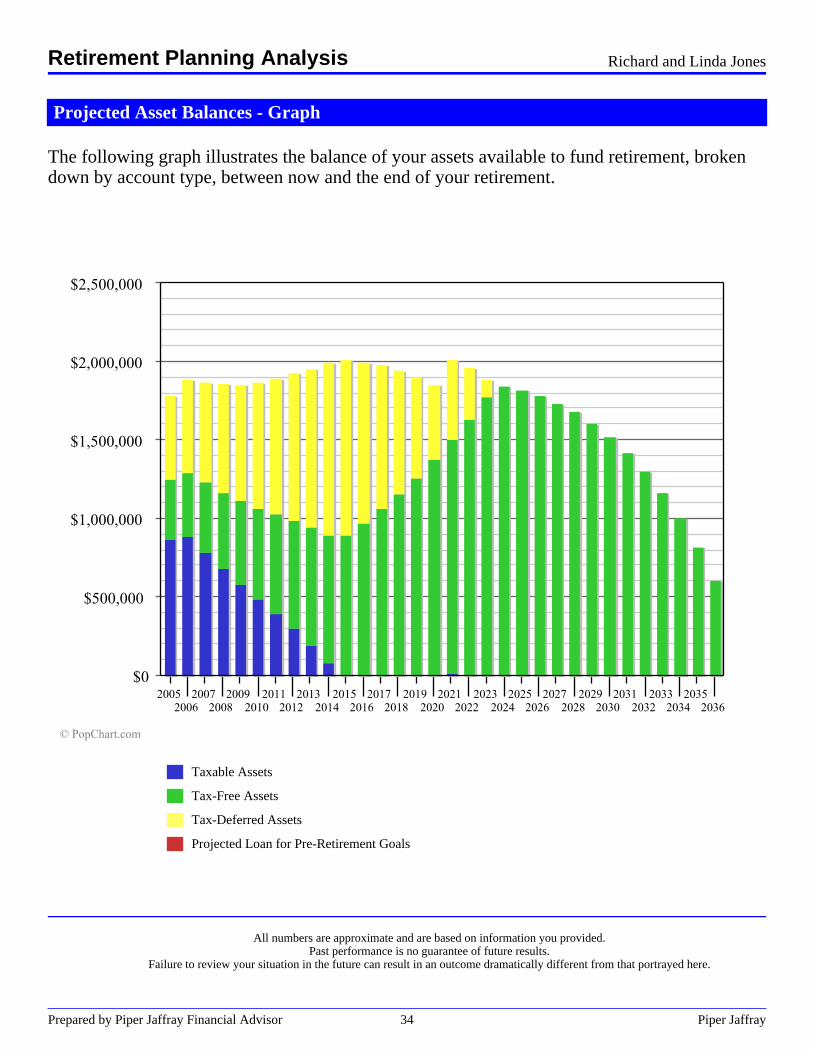

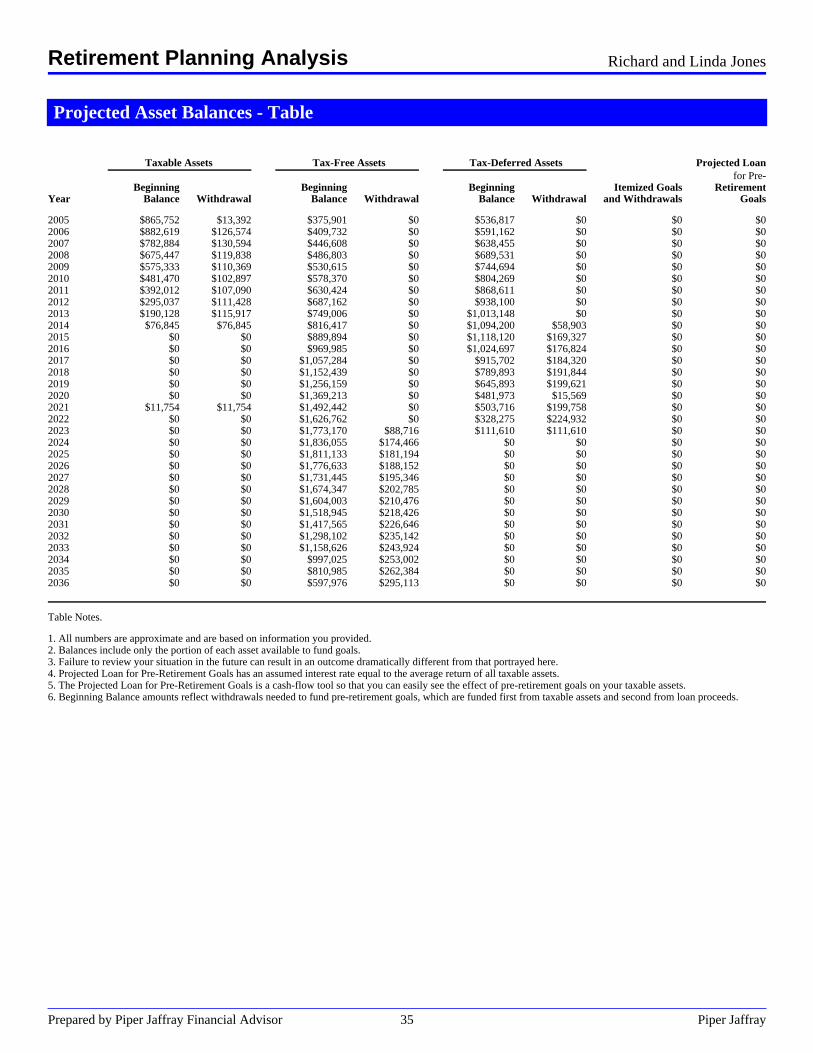

Projected Asset Balances - Graph

The following graph illustrates the balance of your assets available to fund retirement, brokendown by account type, between now and the end of your retirement.

. Taxable Assets

. Tax-Free Assets

. Tax-Deferred Assets

. Projected Loan for Pre-Retirement Goals

All numbers are approximate and are based on information you provided.Past performance is no guarantee of future results.

Failure to review your situation in the future can result in an outcome dramatically different from that portrayed here.

Retirement Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 34 Piper Jaffray

Projected Asset Balances - Table.

. ..............Taxable Assets ..............Tax-Free Assets ..........Tax-Deferred Assets . Projected Loan

. . . . . for Pre-

. Beginning Beginning Beginning Itemized Goals RetirementYear Balance Withdrawal Balance Withdrawal Balance Withdrawal and Withdrawals Goals

2005 $865,752 $13,392 $375,901 $0 $536,817 $0 $0 $02006 $882,619 $126,574 $409,732 $0 $591,162 $0 $0 $02007 $782,884 $130,594 $446,608 $0 $638,455 $0 $0 $02008 $675,447 $119,838 $486,803 $0 $689,531 $0 $0 $02009 $575,333 $110,369 $530,615 $0 $744,694 $0 $0 $02010 $481,470 $102,897 $578,370 $0 $804,269 $0 $0 $02011 $392,012 $107,090 $630,424 $0 $868,611 $0 $0 $02012 $295,037 $111,428 $687,162 $0 $938,100 $0 $0 $02013 $190,128 $115,917 $749,006 $0 $1,013,148 $0 $0 $02014 $76,845 $76,845 $816,417 $0 $1,094,200 $58,903 $0 $02015 $0 $0 $889,894 $0 $1,118,120 $169,327 $0 $02016 $0 $0 $969,985 $0 $1,024,697 $176,824 $0 $02017 $0 $0 $1,057,284 $0 $915,702 $184,320 $0 $02018 $0 $0 $1,152,439 $0 $789,893 $191,844 $0 $02019 $0 $0 $1,256,159 $0 $645,893 $199,621 $0 $02020 $0 $0 $1,369,213 $0 $481,973 $15,569 $0 $02021 $11,754 $11,754 $1,492,442 $0 $503,716 $199,758 $0 $02022 $0 $0 $1,626,762 $0 $328,275 $224,932 $0 $02023 $0 $0 $1,773,170 $88,716 $111,610 $111,610 $0 $02024 $0 $0 $1,836,055 $174,466 $0 $0 $0 $02025 $0 $0 $1,811,133 $181,194 $0 $0 $0 $02026 $0 $0 $1,776,633 $188,152 $0 $0 $0 $02027 $0 $0 $1,731,445 $195,346 $0 $0 $0 $02028 $0 $0 $1,674,347 $202,785 $0 $0 $0 $02029 $0 $0 $1,604,003 $210,476 $0 $0 $0 $02030 $0 $0 $1,518,945 $218,426 $0 $0 $0 $02031 $0 $0 $1,417,565 $226,646 $0 $0 $0 $02032 $0 $0 $1,298,102 $235,142 $0 $0 $0 $02033 $0 $0 $1,158,626 $243,924 $0 $0 $0 $02034 $0 $0 $997,025 $253,002 $0 $0 $0 $02035 $0 $0 $810,985 $262,384 $0 $0 $0 $02036 $0 $0 $597,976 $295,113 $0 $0 $0 $0.

Table Notes.

1. All numbers are approximate and are based on information you provided.2. Balances include only the portion of each asset available to fund goals.3. Failure to review your situation in the future can result in an outcome dramatically different from that portrayed here.4. Projected Loan for Pre-Retirement Goals has an assumed interest rate equal to the average return of all taxable assets.5. The Projected Loan for Pre-Retirement Goals is a cash-flow tool so that you can easily see the effect of pre-retirement goals on your taxable assets.6. Beginning Balance amounts reflect withdrawals needed to fund pre-retirement goals, which are funded first from taxable assets and second from loan proceeds.

Retirement Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 35 Piper Jaffray

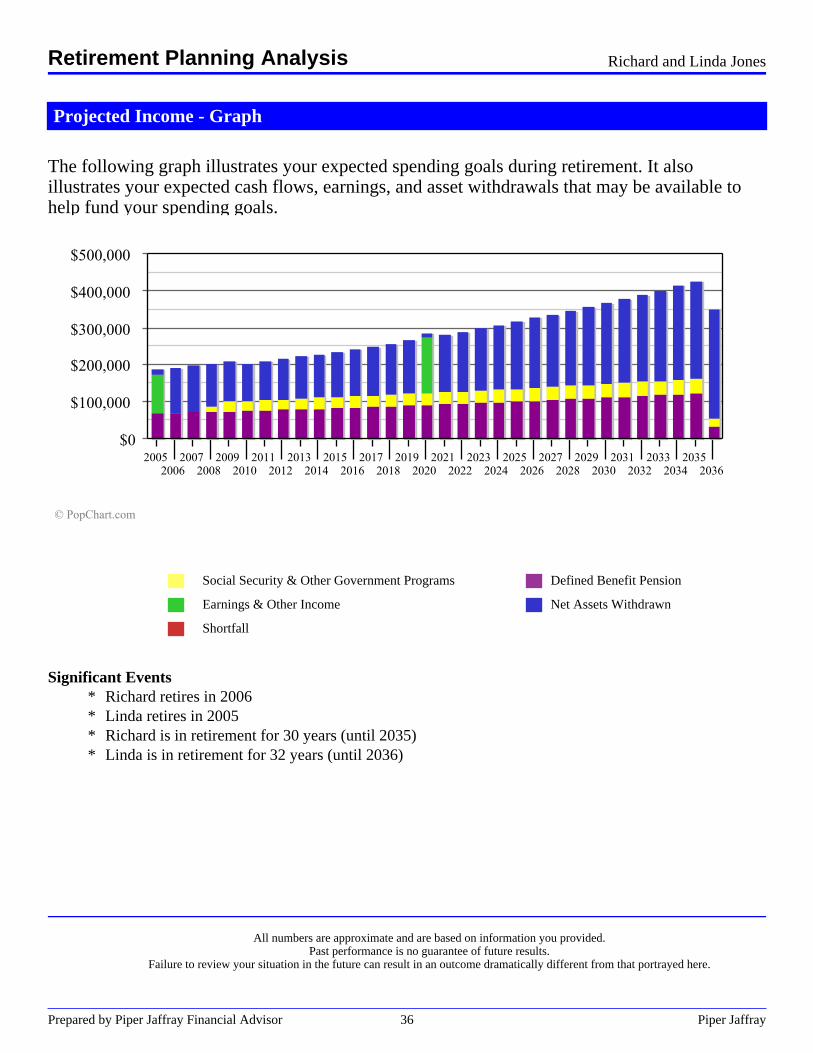

Projected Income - Graph

The following graph illustrates your expected spending goals during retirement. It alsoillustrates your expected cash flows, earnings, and asset withdrawals that may be available tohelp fund your spending goals.

. Social Security & Other Government Programs . Defined Benefit Pension

. Earnings & Other Income . Net Assets Withdrawn

. Shortfall

Significant Events* Richard retires in 2006* Linda retires in 2005* Richard is in retirement for 30 years (until 2035)* Linda is in retirement for 32 years (until 2036)

All numbers are approximate and are based on information you provided.Past performance is no guarantee of future results.

Failure to review your situation in the future can result in an outcome dramatically different from that portrayed here.

Retirement Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 36 Piper Jaffray

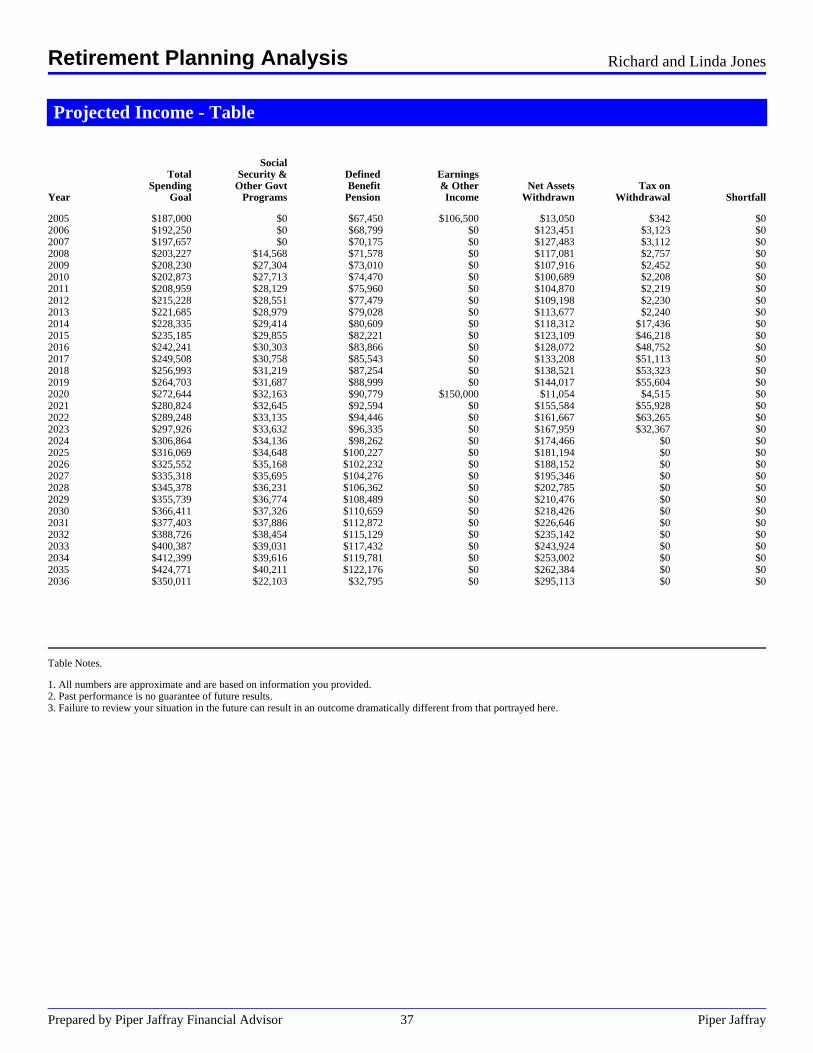

Projected Income - Table

.Social

Total Security & Defined EarningsSpending Other Govt Benefit & Other Net Assets Tax on

Year Goal Programs Pension Income Withdrawn Withdrawal Shortfall

2005 $187,000 $0 $67,450 $106,500 $13,050 $342 $02006 $192,250 $0 $68,799 $0 $123,451 $3,123 $02007 $197,657 $0 $70,175 $0 $127,483 $3,112 $02008 $203,227 $14,568 $71,578 $0 $117,081 $2,757 $02009 $208,230 $27,304 $73,010 $0 $107,916 $2,452 $02010 $202,873 $27,713 $74,470 $0 $100,689 $2,208 $02011 $208,959 $28,129 $75,960 $0 $104,870 $2,219 $02012 $215,228 $28,551 $77,479 $0 $109,198 $2,230 $02013 $221,685 $28,979 $79,028 $0 $113,677 $2,240 $02014 $228,335 $29,414 $80,609 $0 $118,312 $17,436 $02015 $235,185 $29,855 $82,221 $0 $123,109 $46,218 $02016 $242,241 $30,303 $83,866 $0 $128,072 $48,752 $02017 $249,508 $30,758 $85,543 $0 $133,208 $51,113 $02018 $256,993 $31,219 $87,254 $0 $138,521 $53,323 $02019 $264,703 $31,687 $88,999 $0 $144,017 $55,604 $02020 $272,644 $32,163 $90,779 $150,000 $11,054 $4,515 $02021 $280,824 $32,645 $92,594 $0 $155,584 $55,928 $02022 $289,248 $33,135 $94,446 $0 $161,667 $63,265 $02023 $297,926 $33,632 $96,335 $0 $167,959 $32,367 $02024 $306,864 $34,136 $98,262 $0 $174,466 $0 $02025 $316,069 $34,648 $100,227 $0 $181,194 $0 $02026 $325,552 $35,168 $102,232 $0 $188,152 $0 $02027 $335,318 $35,695 $104,276 $0 $195,346 $0 $02028 $345,378 $36,231 $106,362 $0 $202,785 $0 $02029 $355,739 $36,774 $108,489 $0 $210,476 $0 $02030 $366,411 $37,326 $110,659 $0 $218,426 $0 $02031 $377,403 $37,886 $112,872 $0 $226,646 $0 $02032 $388,726 $38,454 $115,129 $0 $235,142 $0 $02033 $400,387 $39,031 $117,432 $0 $243,924 $0 $02034 $412,399 $39,616 $119,781 $0 $253,002 $0 $02035 $424,771 $40,211 $122,176 $0 $262,384 $0 $02036 $350,011 $22,103 $32,795 $0 $295,113 $0 $0

.

.

Table Notes.

1. All numbers are approximate and are based on information you provided.2. Past performance is no guarantee of future results.3. Failure to review your situation in the future can result in an outcome dramatically different from that portrayed here.

Retirement Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 37 Piper Jaffray

FYI

Conditions affectingyour retirement planchange frequently.Today's economicconditions may indicatea retirement fundingsurplus, but futureconditions may not.

It is important to meetwith your financialadvisor periodically tomake sure you are ontrack to meet yourretirement goals.

Before changing yourplans, you shouldrealize that any changesto the assumptions ofyour retirement plan(such as thoserepresented by theconsiderations listedhere) may project adifferent ending result.

Consider asking youradvisor to run theanalysis again withmore conservativeassumptions. If you arestill comfortable withany projected surpluses,the actions shown heremay be appropriate.

Retirement Goal Funded

Congratulations! Based on the information you provided, and theassumptions you chose, you should be able to fully fund your retirementgoals.

Your excess funding may afford you some additional flexibility with yourretirement goals and your assets. Some things you may want to considerinclude:

- Retire early

Because you have excess funds, you may be able to retire sooner than youare currently planning.

- Increase your spending goals

You may want to include some additional travel plans or other spendingobjectives during your retirement years.

- Gift assets

Your benefactors can enjoy your gifts during your lifetime while youreduce potential estate taxes.

- Reallocate your portfolio to take on more conservative asset mix

A more conservative asset mix can reduce the fluctuations in yourportfolio. This provides more confidence that your expected returns will bemet and increases the likelihood that your assets will grow as projected.

Please note the cautions in the FYI box to the left.

Retirement Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 38 Piper Jaffray

Overview

Planning Your Estate

Building your estate requires a lifetime of effort and careful planning. Similar careful planning is required toachieve your estate planning goals. If you do not make appropriate estate planning provisions during your life,your estate may be unduly diminished by taxes and suffer from poor management, administrative delays, and/orincreased settlement costs.

If you plan your estate properly, you may increase your ability to achieve lifelong goals and provide for yourfamily, charities, and others. You may also reduce the transfer taxes and settlement costs that may be assessedat your death. Estate and income tax laws change frequently, which means that you will need to review yourplans on a regular basis in order to adjust to these changes.

Your Estate Plan

The analysis contained in this report will provide you with information to help you understand general estateplanning rules and concepts. It is for illustrative purposes only and may not reflect all the specifics of yoursituation, such as individual state inheritance or estate taxes. This analysis illustrates your current estatesituation and discusses estate planning alternatives that may benefit you and your heirs. Your estate plan shouldbe centered on your financial situation and what you want to accomplish. Because these factors may changewith time, you should periodically review your estate plan with your financial advisor, attorney, and tax advisor.You will need the assistance of an estate attorney to implement many of the recommendations put forth in thisreport.

Benefits of Estate Planning

A proper estate plan may do the following:

· Reduce your estate tax liability· Reduce your asset transfer costs· Direct your financial resources to those you choose· Ease your family's burden during a time of stress

Comprehensive Financial Plan Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 39 Piper Jaffray

Estate Assumptions

Personal InformationRichard and Linda Jones

General AssumptionsScenario name Market CyclePlan date 03/31/2005

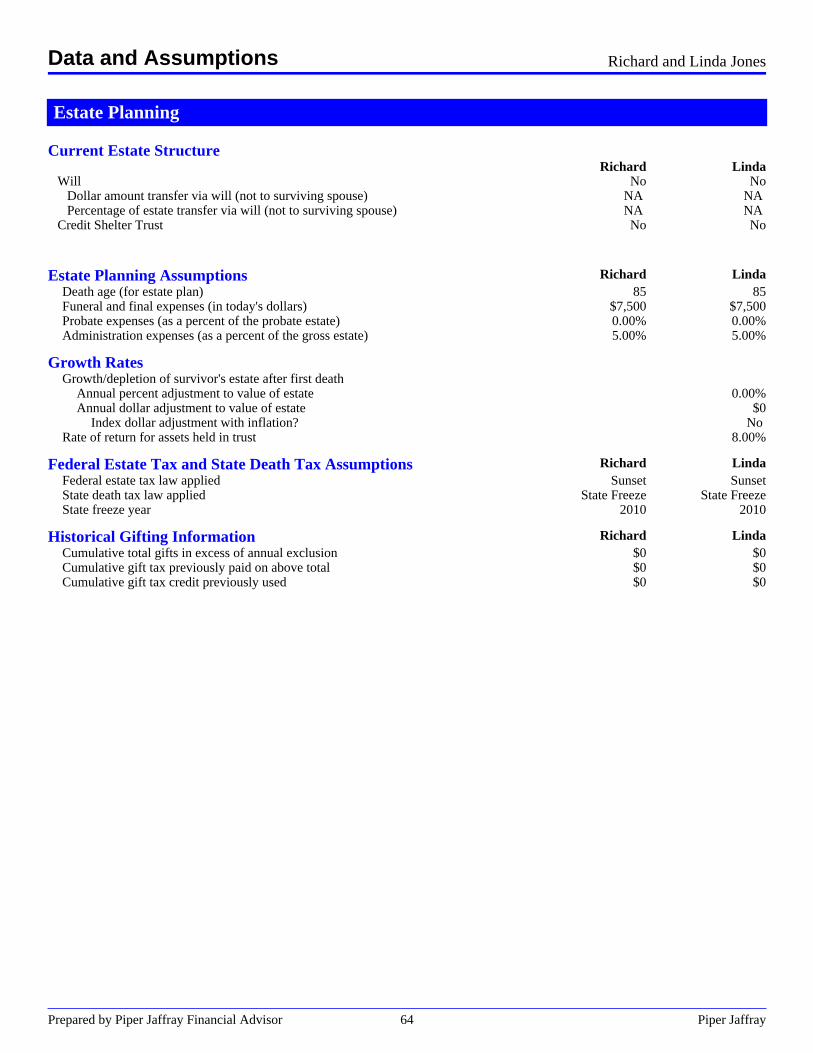

Current Estate Structure Richard LindaWill No No

Bequests to someone other than the surviving client (dollar amount) $0 $0Bequests to someone other than the surviving client (percent) 0.00% 0.00%

Credit shelter trust No No

Estate Planning Assumptions Richard LindaDeath age (for estate plan) 85 85Funeral and final expenses (in today's dollars) $7,500 $7,500Probate expenses (as a percent of the probate estate) 0.00% 0.00%Administration expenses (as a percent of the gross estate) 5.00% 5.00%

Growth RatesGrowth/depletion of survivor's estate after first death

Annual percent adjustment to value of estate 0.00%Annual dollar adjustment to value of estate $0

Index dollar adjustment with inflation? NoRate of return for assets held in trust 8.00%

Federal Estate Tax and State Death Tax Assumptions Richard LindaFederal estate tax law applied Sunset SunsetState death tax law applied State Freeze State FreezeState freeze year 2010 2010

Historical Gifting Information Richard LindaCumulative total gifts in excess of annual exclusion $0 $0Cumulative gift tax previously paid on above total $0 $0Cumulative gift tax credit previously used $0 $0

Estate Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 40 Piper Jaffray

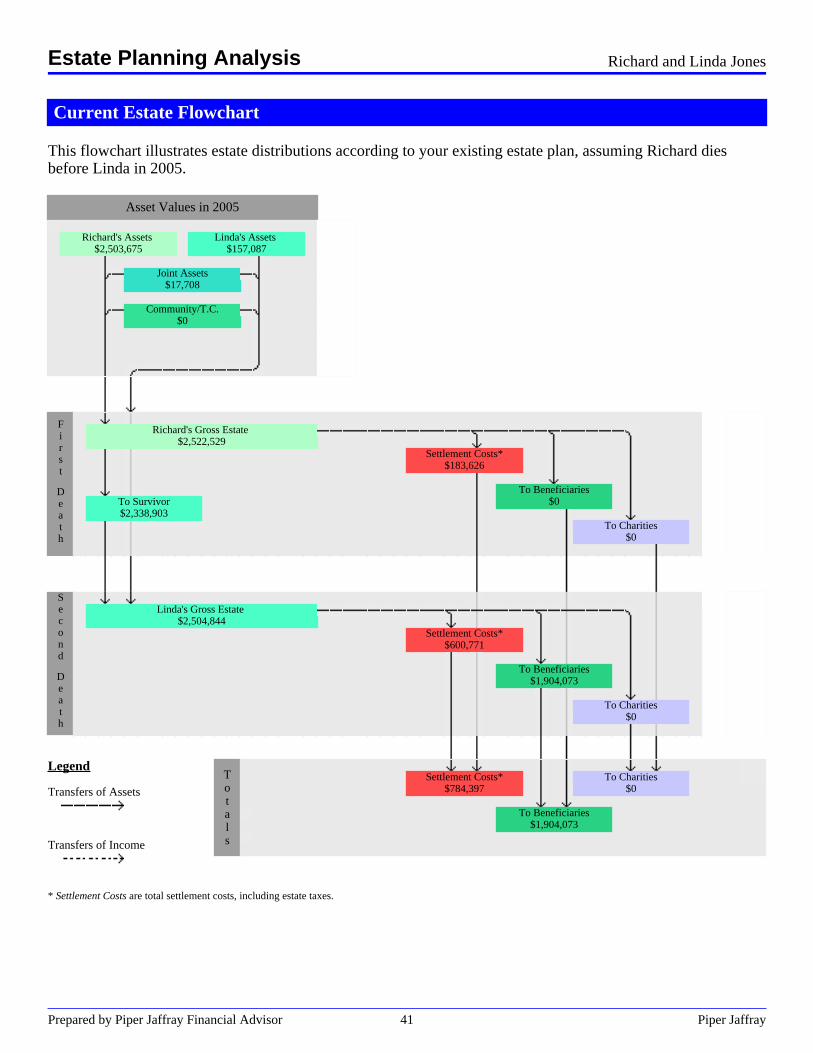

Current Estate Flowchart

This flowchart illustrates estate distributions according to your existing estate plan, assuming Richard diesbefore Linda in 2005.

Asset Values in 2005

Richard's Assets$2,503,675

Linda's Assets$157,087

Joint Assets$17,708

Community/T.C.$0

First

Death

Richard's Gross Estate$2,522,529

Settlement Costs*$183,626

To Beneficiaries$0To Survivor

$2,338,903To Charities

$0

Second

Death

Linda's Gross Estate$2,504,844

Settlement Costs*$600,771

To Beneficiaries$1,904,073

To Charities$0

Legend

Transfers of Assets

Transfers of Income

Totals

Settlement Costs*$784,397

To Charities$0

To Beneficiaries$1,904,073

* Settlement Costs are total settlement costs, including estate taxes.

Estate Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 41 Piper Jaffray

FYI

You have worked hardto accumulate thefinancial resources tosupport your familytoday and leave alegacy for tomorrow.

When you die, yourestate executor willcalculate your grossestate by determiningthe value of your assetsand any assets in whichyou have an 'incident ofownership.' The rulesconcerning what isincluded in the value ofyour gross estate arecomplex. To avoidfuture difficulties, makecertain this report listsall assets in which youhave incidents ofownership.

Current Assets by Owner

.

.Richard

.

.Linda

.

.Joint Assets

Community/T. Common

AssetsCash assets $0 $0 $10,000 $0Investment assets $1,373,945 $0 $7,708 $0Retirement assets $229,730 $157,087 N/A N/AStock options $0 $0 N/A $0Annuities $0 $0 $0 $0Deferred compensation $0 $0 N/A N/ANotes receivable $0 $0 $0 $0Business assets $0 $0 $0 $0Personal assets $900,000 $0 $0 $0Total assets $2,503,675 $157,087 $17,708 $0

Current Gross Estate

Richard LindaIndividually owned assets $2,503,675 $157,08750% of joint assets $8,854 $8,85450% of community assets/tenancy in common assets $0 $0Life insurance included in estate $10,000 $0Assets received at Richard's death N/A $2,338,903Current gross estate $2,522,529 $2,504,844

Estate Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 42 Piper Jaffray

FYI

The numbers on thispage show estimatedsettlement costs,assuming you were todie today.

Federal estate tax andstate death tax amountsare also estimatedbelow.

The federal governmentallows you to deductcertain transfers fromyour gross estate whencalculating yourtentative tax base.Funeral expenses,probate andadministrationexpenses, and liabilitiespaid at your death maybe deducted.

Additionally, amountstransferred to asurviving spouse oramounts transferred tocharity serve to reduceyour tentative tax base,thus reducing yourestate taxes.

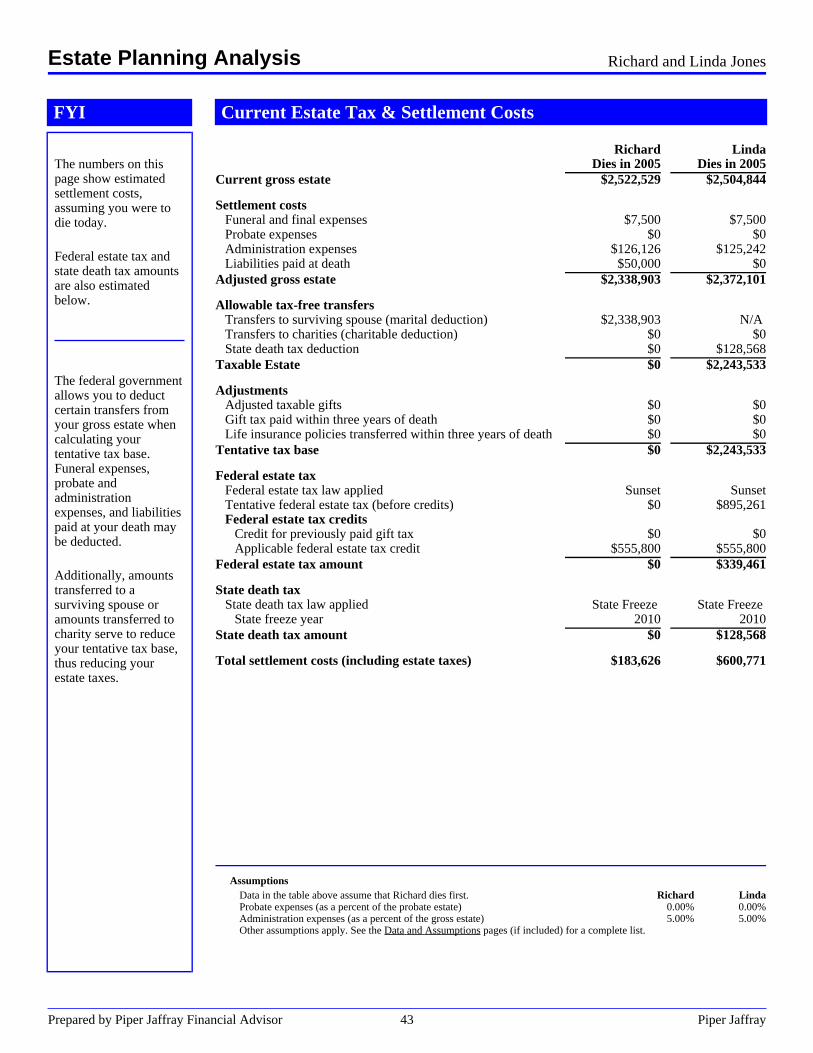

Current Estate Tax & Settlement Costs

RichardDies in 2005

LindaDies in 2005

Current gross estate $2,522,529 $2,504,844

Settlement costsFuneral and final expenses $7,500 $7,500Probate expenses $0 $0Administration expenses $126,126 $125,242Liabilities paid at death $50,000 $0

Adjusted gross estate $2,338,903 $2,372,101

Allowable tax-free transfersTransfers to surviving spouse (marital deduction) $2,338,903 N/ATransfers to charities (charitable deduction) $0 $0State death tax deduction $0 $128,568

Taxable Estate $0 $2,243,533

AdjustmentsAdjusted taxable gifts $0 $0Gift tax paid within three years of death $0 $0Life insurance policies transferred within three years of death $0 $0

Tentative tax base $0 $2,243,533

Federal estate taxFederal estate tax law applied Sunset SunsetTentative federal estate tax (before credits) $0 $895,261Federal estate tax credits

Credit for previously paid gift tax $0 $0Applicable federal estate tax credit $555,800 $555,800

Federal estate tax amount $0 $339,461

State death taxState death tax law applied State Freeze State Freeze

State freeze year 2010 2010State death tax amount $0 $128,568

Total settlement costs (including estate taxes) $183,626 $600,771

AssumptionsData in the table above assume that Richard dies first. Richard LindaProbate expenses (as a percent of the probate estate) 0.00% 0.00%Administration expenses (as a percent of the gross estate) 5.00% 5.00%Other assumptions apply. See the Data and Assumptions pages (if included) for a complete list.

Estate Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 43 Piper Jaffray

FYI

Settlement Costsinclude funeralexpenses, probateexpenses,administrationexpenses, and liabilitiespaid at death.

Estate Taxes includeboth federal estate taxesand state death taxes.Federal estate taxes arecalculated based onmarginal tax ratesestablished by thefederal government, andare applied based on theoption chosen forFederal estate tax lawapplied.

Amount to Beneficiariesincludes all assetstransferred through anymethod (by intestacylaws, probate, contract,or law) to anybeneficiary, includingcharitable beneficiaries.

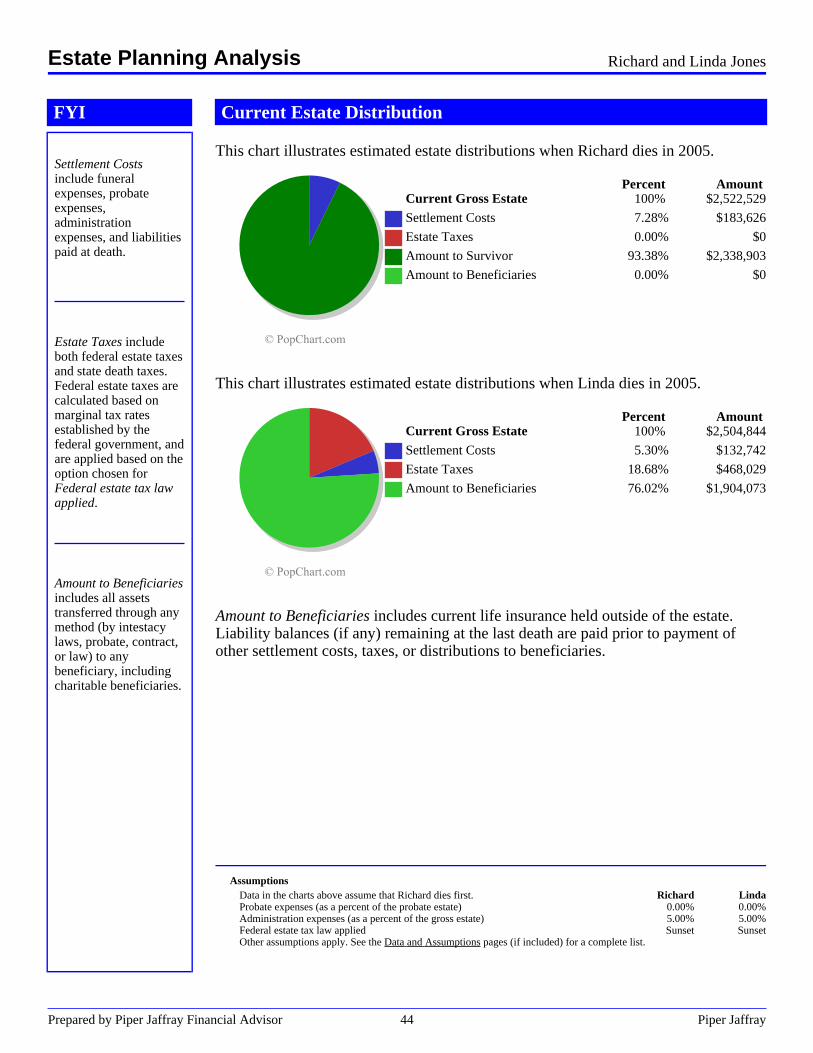

Current Estate Distribution

This chart illustrates estimated estate distributions when Richard dies in 2005..

Percent AmountCurrent Gross Estate 100% $2,522,529

.

. Settlement Costs 7.28% $183,626.

. Estate Taxes 0.00% $0.

. Amount to Survivor 93.38% $2,338,903.

. Amount to Beneficiaries 0.00% $0

This chart illustrates estimated estate distributions when Linda dies in 2005..

Percent AmountCurrent Gross Estate 100% $2,504,844

.

. Settlement Costs 5.30% $132,742.

. Estate Taxes 18.68% $468,029.

. Amount to Beneficiaries 76.02% $1,904,073

Amount to Beneficiaries includes current life insurance held outside of the estate.Liability balances (if any) remaining at the last death are paid prior to payment ofother settlement costs, taxes, or distributions to beneficiaries.

AssumptionsData in the charts above assume that Richard dies first. Richard LindaProbate expenses (as a percent of the probate estate) 0.00% 0.00%Administration expenses (as a percent of the gross estate) 5.00% 5.00%Federal estate tax law applied Sunset SunsetOther assumptions apply. See the Data and Assumptions pages (if included) for a complete list.

Estate Planning Analysis Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 44 Piper Jaffray

.

Data and Assumptions

Prepared by Piper Jaffray Financial Advisor 45 Piper Jaffray

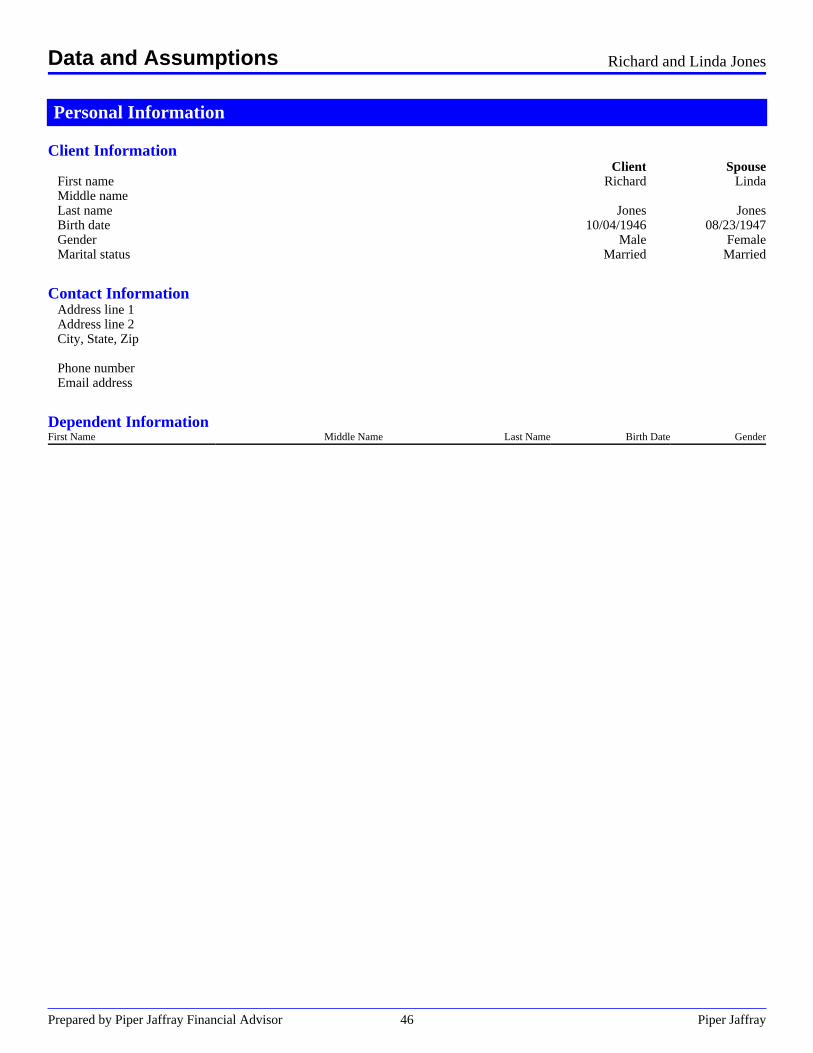

Personal Information

Client InformationClient Spouse

First name Richard LindaMiddle nameLast name Jones JonesBirth date 10/04/1946 08/23/1947Gender Male FemaleMarital status Married Married

.Contact Information

Address line 1Address line 2City, State, Zip

.Phone numberEmail address

.Dependent InformationFirst Name Middle Name Last Name Birth Date Gender

Data and Assumptions Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 46 Piper Jaffray

Assumptions

General AssumptionsScenario Main ScenarioPlan date 03/31/2005

.Richard Linda

Earned income growth rate 3.00% 3.00%Desired retirement age 60 58Life expectancy 90 90

.Pre-Retirement Post-Retirement

General inflation rate 3.00% 3.00%Average income tax rate (state and federal) 29.00% 29.00%Average capital gains/dividends tax rate 15.00% 15.00%

.Discount rate 5.00%

.Allocated assets grow at the rate of return from the Present Allocation.

.Post-Retirement Assumptions

Rate of Return Order to LiquidateTaxable accounts 5.00% 1Tax-free accounts 9.00% 3Tax-deferred accounts 8.00% 2Percent of non-retired working spouses income available for retirement 100.00%

.Employer Matching Information - Richard

100.00% match on employee's first 4.00% of pay0.00% match on employee's next 0.00% of pay

.Employer Matching Information - Linda

0.00% match on employee's first 0.00% of pay0.00% match on employee's next 0.00% of pay

Data and Assumptions Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 47 Piper Jaffray

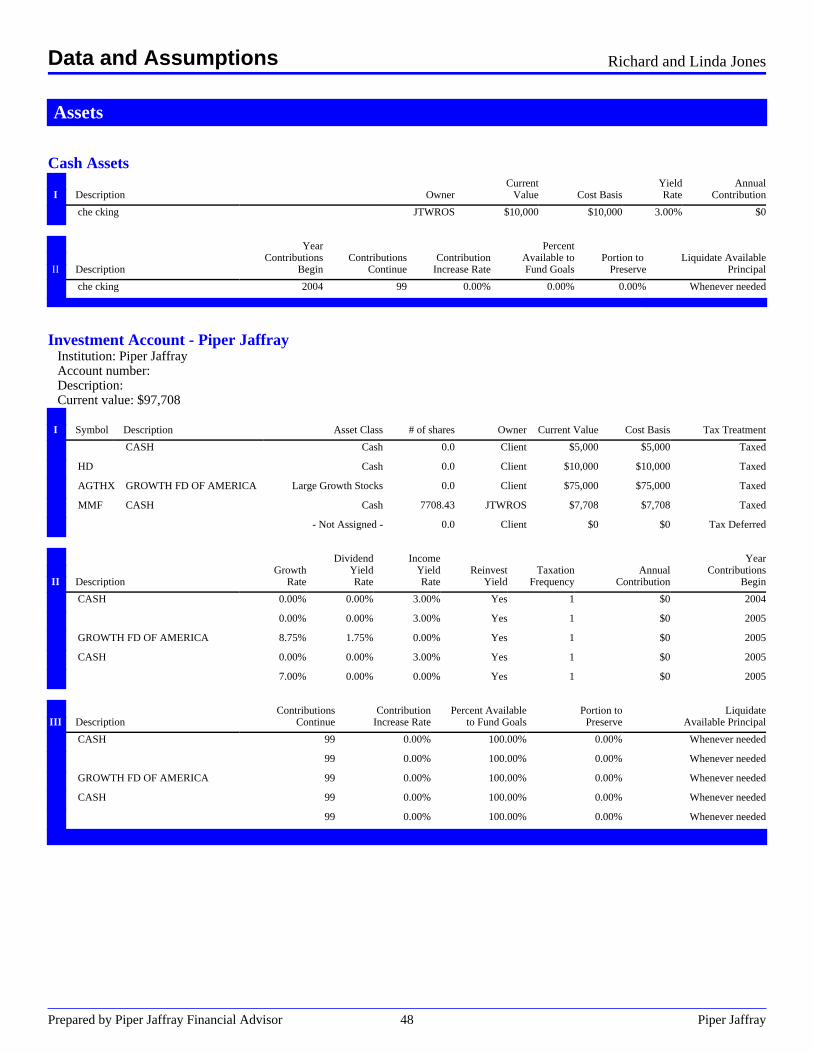

Assets. . . . . . . .

Cash Assets . . .. . . . Current . Yield AnnualI Description . Owner Value Cost Basis Rate Contribution

. che cking JTWROS $10,000 $10,000 3.00% $0

.

. . Year . . Percent . .

. . Contributions Contributions Contribution Available to Portion to Liquidate AvailableII Description Begin Continue Increase Rate Fund Goals Preserve Principal

. che cking 2004 99 0.00% 0.00% 0.00% Whenever needed. .. . . . . . . . .

.Investment Account - Piper Jaffray

Institution: Piper JaffrayAccount number:Description:Current value: $97,708

. .I Symbol Description Asset Class # of shares Owner Current Value Cost Basis Tax Treatment

. CASH Cash 0.0 Client $5,000 $5,000 Taxed

. HD Cash 0.0 Client $10,000 $10,000 Taxed

. AGTHX GROWTH FD OF AMERICA Large Growth Stocks 0.0 Client $75,000 $75,000 Taxed

. MMF CASH Cash 7708.43 JTWROS $7,708 $7,708 Taxed

. - Not Assigned - 0.0 Client $0 $0 Tax Deferred

.

. . Dividend Income Year

. . Growth Yield Yield Reinvest Taxation Annual ContributionsII Description Rate Rate Rate Yield Frequency Contribution Begin

. CASH 0.00% 0.00% 3.00% Yes 1 $0 2004

. 0.00% 0.00% 3.00% Yes 1 $0 2005

. GROWTH FD OF AMERICA 8.75% 1.75% 0.00% Yes 1 $0 2005

. CASH 0.00% 0.00% 3.00% Yes 1 $0 2005

. 7.00% 0.00% 0.00% Yes 1 $0 2005

.

. . Contributions Contribution Percent Available Portion to LiquidateIII Description Continue Increase Rate to Fund Goals Preserve Available Principal

. CASH 99 0.00% 100.00% 0.00% Whenever needed

. 99 0.00% 100.00% 0.00% Whenever needed

. GROWTH FD OF AMERICA 99 0.00% 100.00% 0.00% Whenever needed

. CASH 99 0.00% 100.00% 0.00% Whenever needed

. 99 0.00% 100.00% 0.00% Whenever needed

.. . . . . . . . .

.

Data and Assumptions Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 48 Piper Jaffray

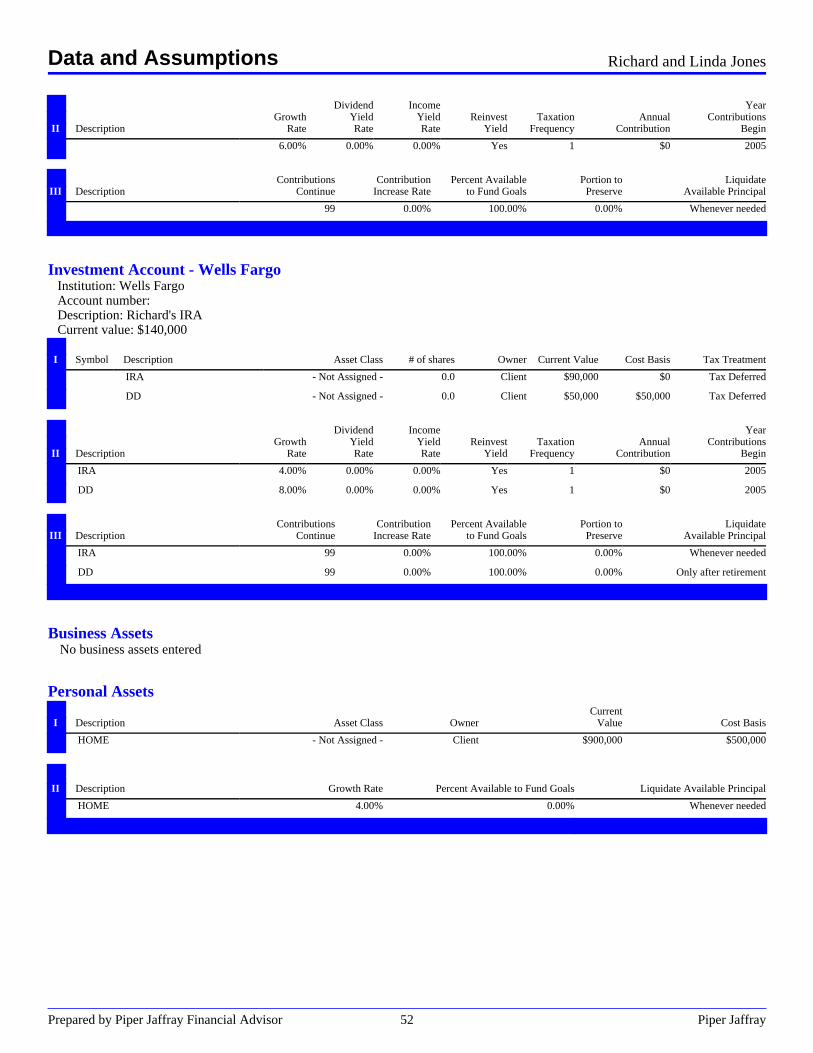

Investment Account - Wells FargoInstitution: Wells FargoAccount number: 111111111Description: Joint AccountCurrent value: $30,000

. .I Symbol Description Asset Class # of shares Owner Current Value Cost Basis Tax Treatment

. AHPI ALLIED HEALTHCAREPRODS INC

Small/Mid-Cap Value 0.0 Client $10,000 $10,000 Taxed

. MDT MEDTRONIC INC Large Growth Stocks 0.0 Client $10,000 $10,000 Taxed

. TGT TARGET CORP Large Growth Stocks 0.0 Client $10,000 $10,000 Taxed

.

. . Dividend Income Year

. . Growth Yield Yield Reinvest Taxation Annual ContributionsII Description Rate Rate Rate Yield Frequency Contribution Begin

. ALLIED HEALTHCARE PRODSINC

9.00% 2.00% 0.00% Yes 1 $0 2004

. MEDTRONIC INC 8.75% 1.75% 0.00% Yes 1 $0 2004

. TARGET CORP 8.75% 1.75% 0.00% Yes 1 $0 2005

.

. . Contributions Contribution Percent Available Portion to LiquidateIII Description Continue Increase Rate to Fund Goals Preserve Available Principal

. ALLIED HEALTHCARE PRODSINC

99 0.00% 100.00% 0.00% Whenever needed

. MEDTRONIC INC 99 0.00% 100.00% 0.00% Whenever needed

. TARGET CORP 99 0.00% 100.00% 0.00% Whenever needed

.. . . . . . . . .

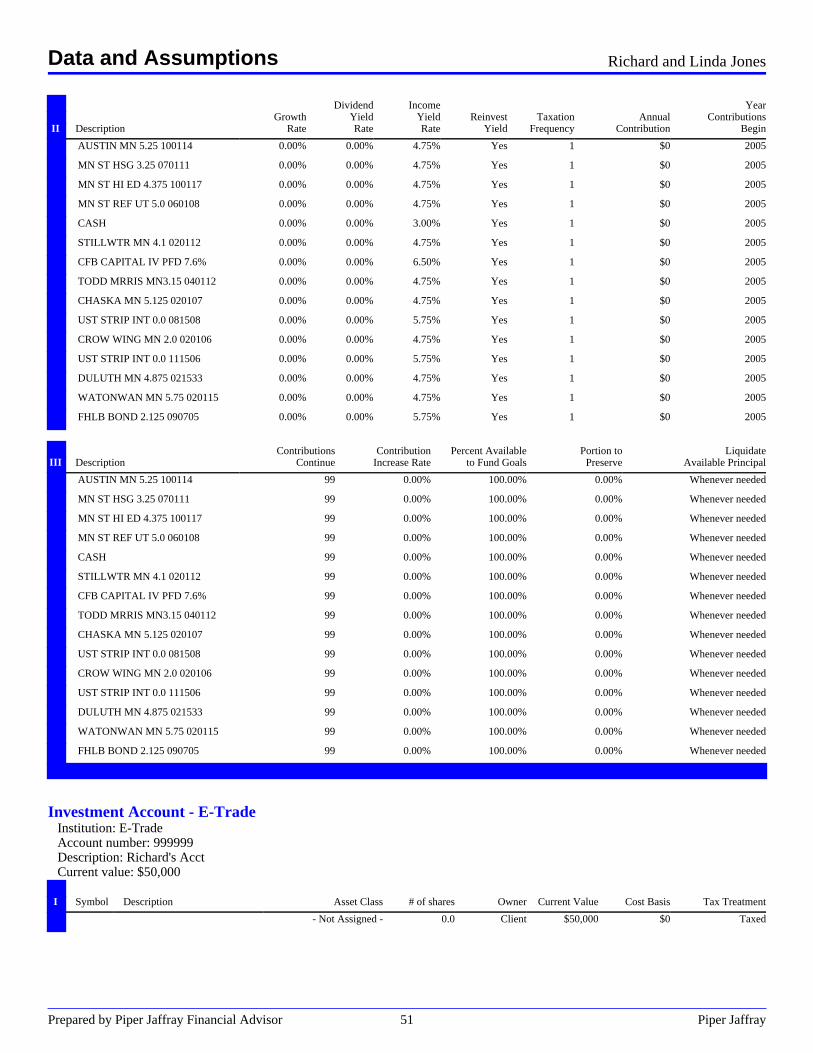

.Investment Account - E-Trade

Institution: E-TradeAccount number:Description:Current value: $100,000

. .I Symbol Description Asset Class # of shares Owner Current Value Cost Basis Tax Treatment

. Cash 0.0 Client $100,000 $100,000 Taxed

.

. . Dividend Income Year

. . Growth Yield Yield Reinvest Taxation Annual ContributionsII Description Rate Rate Rate Yield Frequency Contribution Begin

. 0.00% 0.00% 3.00% Yes 1 $10,000 2005

.

. . Contributions Contribution Percent Available Portion to LiquidateIII Description Continue Increase Rate to Fund Goals Preserve Available Principal

. 3 0.00% 100.00% 0.00% Whenever needed

.. . . . . . . . .

.Investment Account - RBC Dain

Institution: RBC DainAccount number:Description: Joint AccountCurrent value: $255,000

. .I Symbol Description Asset Class # of shares Owner Current Value Cost Basis Tax Treatment

. CASH Cash 0.0 Client $250,000 $250,000 Taxed

. T ATT CORP Large Value Stocks 0.0 Client $5,000 $5,000 Taxed

Data and Assumptions Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 49 Piper Jaffray

.

. . Dividend Income Year

. . Growth Yield Yield Reinvest Taxation Annual ContributionsII Description Rate Rate Rate Yield Frequency Contribution Begin

. CASH 0.00% 0.00% 3.00% Yes 1 $0 2004

. ATT CORP 7.00% 2.50% 0.00% Yes 1 $0 2005

.

. . Contributions Contribution Percent Available Portion to LiquidateIII Description Continue Increase Rate to Fund Goals Preserve Available Principal

. CASH 99 0.00% 100.00% 0.00% Whenever needed

. ATT CORP 99 0.00% 100.00% 0.00% Whenever needed

.. . . . . . . . .

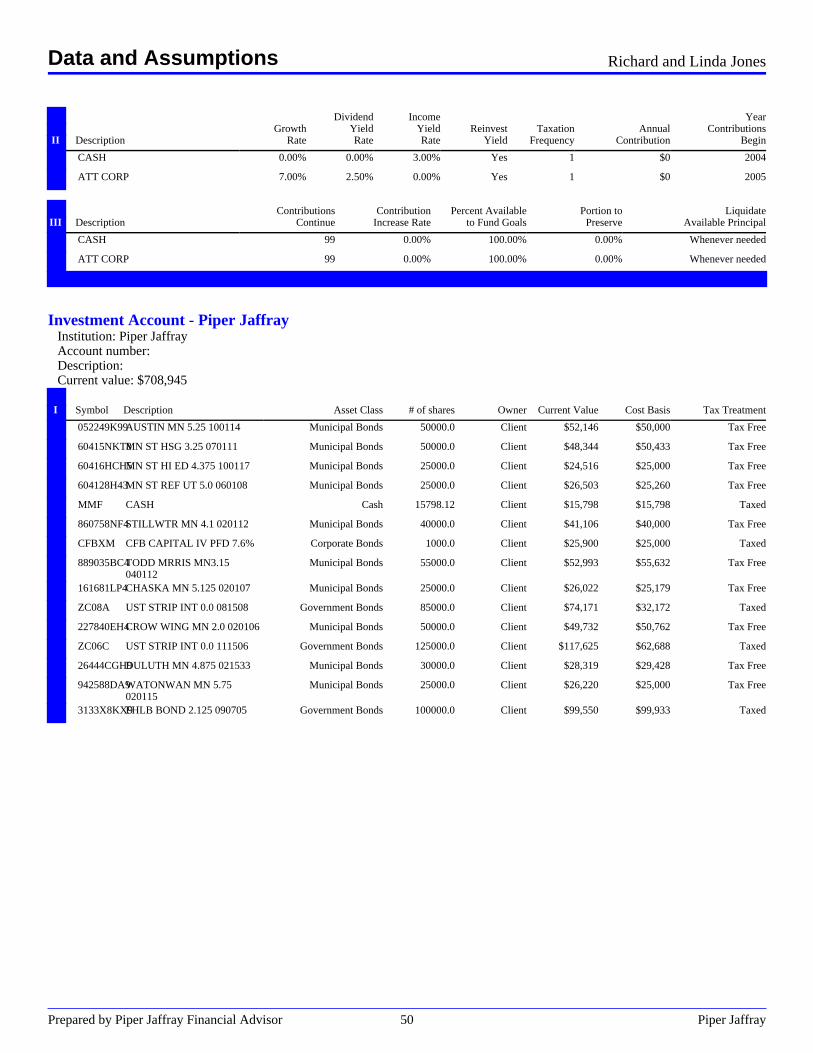

.Investment Account - Piper Jaffray

Institution: Piper JaffrayAccount number:Description:Current value: $708,945

. .I Symbol Description Asset Class # of shares Owner Current Value Cost Basis Tax Treatment

. 052249K99AUSTIN MN 5.25 100114 Municipal Bonds 50000.0 Client $52,146 $50,000 Tax Free

. 60415NKT8MN ST HSG 3.25 070111 Municipal Bonds 50000.0 Client $48,344 $50,433 Tax Free

. 60416HCH5MN ST HI ED 4.375 100117 Municipal Bonds 25000.0 Client $24,516 $25,000 Tax Free

. 604128H43MN ST REF UT 5.0 060108 Municipal Bonds 25000.0 Client $26,503 $25,260 Tax Free

. MMF CASH Cash 15798.12 Client $15,798 $15,798 Taxed

. 860758NF4STILLWTR MN 4.1 020112 Municipal Bonds 40000.0 Client $41,106 $40,000 Tax Free

. CFBXM CFB CAPITAL IV PFD 7.6% Corporate Bonds 1000.0 Client $25,900 $25,000 Taxed

. 889035BC4TODD MRRIS MN3.15040112

Municipal Bonds 55000.0 Client $52,993 $55,632 Tax Free

. 161681LP4CHASKA MN 5.125 020107 Municipal Bonds 25000.0 Client $26,022 $25,179 Tax Free

. ZC08A UST STRIP INT 0.0 081508 Government Bonds 85000.0 Client $74,171 $32,172 Taxed

. 227840EH4CROW WING MN 2.0 020106 Municipal Bonds 50000.0 Client $49,732 $50,762 Tax Free

. ZC06C UST STRIP INT 0.0 111506 Government Bonds 125000.0 Client $117,625 $62,688 Taxed

. 26444CGH9DULUTH MN 4.875 021533 Municipal Bonds 30000.0 Client $28,319 $29,428 Tax Free

. 942588DA9WATONWAN MN 5.75020115

Municipal Bonds 25000.0 Client $26,220 $25,000 Tax Free

. 3133X8KX9FHLB BOND 2.125 090705 Government Bonds 100000.0 Client $99,550 $99,933 Taxed

.

Data and Assumptions Richard and Linda Jones

Prepared by Piper Jaffray Financial Advisor 50 Piper Jaffray

. . Dividend Income Year

. . Growth Yield Yield Reinvest Taxation Annual ContributionsII Description Rate Rate Rate Yield Frequency Contribution Begin

. AUSTIN MN 5.25 100114 0.00% 0.00% 4.75% Yes 1 $0 2005

. MN ST HSG 3.25 070111 0.00% 0.00% 4.75% Yes 1 $0 2005

. MN ST HI ED 4.375 100117 0.00% 0.00% 4.75% Yes 1 $0 2005

. MN ST REF UT 5.0 060108 0.00% 0.00% 4.75% Yes 1 $0 2005

. CASH 0.00% 0.00% 3.00% Yes 1 $0 2005

. STILLWTR MN 4.1 020112 0.00% 0.00% 4.75% Yes 1 $0 2005

. CFB CAPITAL IV PFD 7.6% 0.00% 0.00% 6.50% Yes 1 $0 2005

. TODD MRRIS MN3.15 040112 0.00% 0.00% 4.75% Yes 1 $0 2005

. CHASKA MN 5.125 020107 0.00% 0.00% 4.75% Yes 1 $0 2005

. UST STRIP INT 0.0 081508 0.00% 0.00% 5.75% Yes 1 $0 2005

. CROW WING MN 2.0 020106 0.00% 0.00% 4.75% Yes 1 $0 2005

. UST STRIP INT 0.0 111506 0.00% 0.00% 5.75% Yes 1 $0 2005

. DULUTH MN 4.875 021533 0.00% 0.00% 4.75% Yes 1 $0 2005

. WATONWAN MN 5.75 020115 0.00% 0.00% 4.75% Yes 1 $0 2005

. FHLB BOND 2.125 090705 0.00% 0.00% 5.75% Yes 1 $0 2005

.

. . Contributions Contribution Percent Available Portion to LiquidateIII Description Continue Increase Rate to Fund Goals Preserve Available Principal

. AUSTIN MN 5.25 100114 99 0.00% 100.00% 0.00% Whenever needed

. MN ST HSG 3.25 070111 99 0.00% 100.00% 0.00% Whenever needed

. MN ST HI ED 4.375 100117 99 0.00% 100.00% 0.00% Whenever needed

. MN ST REF UT 5.0 060108 99 0.00% 100.00% 0.00% Whenever needed

. CASH 99 0.00% 100.00% 0.00% Whenever needed

. STILLWTR MN 4.1 020112 99 0.00% 100.00% 0.00% Whenever needed

. CFB CAPITAL IV PFD 7.6% 99 0.00% 100.00% 0.00% Whenever needed

. TODD MRRIS MN3.15 040112 99 0.00% 100.00% 0.00% Whenever needed

. CHASKA MN 5.125 020107 99 0.00% 100.00% 0.00% Whenever needed

. UST STRIP INT 0.0 081508 99 0.00% 100.00% 0.00% Whenever needed

. CROW WING MN 2.0 020106 99 0.00% 100.00% 0.00% Whenever needed

. UST STRIP INT 0.0 111506 99 0.00% 100.00% 0.00% Whenever needed

. DULUTH MN 4.875 021533 99 0.00% 100.00% 0.00% Whenever needed

. WATONWAN MN 5.75 020115 99 0.00% 100.00% 0.00% Whenever needed

. FHLB BOND 2.125 090705 99 0.00% 100.00% 0.00% Whenever needed

.. . . . . . . . .