Embed Size (px)

Citation preview

Comprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualComprehensive AnnualFinancial ReportFinancial ReportFinancial ReportFinancial ReportFinancial ReportFinancial ReportFinancial ReportFinancial ReportFinancial Report

Comprehensive AnnualFinancial Report

Comprehensive AnnualComprehensive AnnualComprehensive AnnualFinancial Report

Comprehensive AnnualFinancial Report

Comprehensive AnnualFinancial Report

Comprehensive AnnualComprehensive AnnualComprehensive AnnualFinancial Report

Comprehensive AnnualComprehensive AnnualFinancial Report

Comprehensive AnnualComprehensive AnnualComprehensive AnnualFinancial Report

Comprehensive AnnualFinancial Report

Comprehensive AnnualFinancial Report

Comprehensive AnnualComprehensive AnnualComprehensive AnnualFinancial Report

Comprehensive AnnualComprehensive AnnualFinancial Report

Comprehensive AnnualComprehensive AnnualComprehensive AnnualFinancial Report

Comprehensive AnnualFinancial Report

Comprehensive AnnualFinancial Report

Comprehensive AnnualComprehensive AnnualComprehensive AnnualFinancial Report

Comprehensive Annual

For the Year Ended December 31, 2015

City of Thornton, Colorado Comprehensive Annual Financial Report

For the fiscal year ended December 31, 2015

Prepared by the Finance Department:

Maria Ostrom, Finance Director Kim Newhart, Controller

JoAnn Koenig, Accounting Supervisor Rachel Walsh, Project Accountant

Jamie Miller, Accountant Dawn Cartier, Accountant Erika Senna, Accountant Kim Tucker, Accountant

Carla Montoya, Accounting Technician Mindy Gallo, Accounting Specialist

Vanessa Bernal, Accounting Specialist

City of Thornton, Colorado Table of Contents

Introductory Section Page

Letter of Transmittal v

City Officials x

Organizational Chart xi

Certificate of Achievement for Excellence in Financial Reporting xii

Financial Section

Report of Independent Certified Public Accountants 1

Management’s Discussion & Analysis 5

Basic Financial Statements

Government-wide Financial Statements

Statement of Net Position 14

Statement of Activities 15

Fund Financial Statements

Balance Sheet - Governmental Funds 18

Reconciliation of the Balance Sheet of Governmental Funds to the Statement of Net Position 19

Statement of Revenues, Expenditures, and Changes in Fund Balances – Governmental Funds 20

Reconciliation of the Statement of Revenues, Expenditures, and Changes in Fund Balances of Governmental Funds to the Statement of Activities 21

Statement of Net Position – Proprietary Funds 22

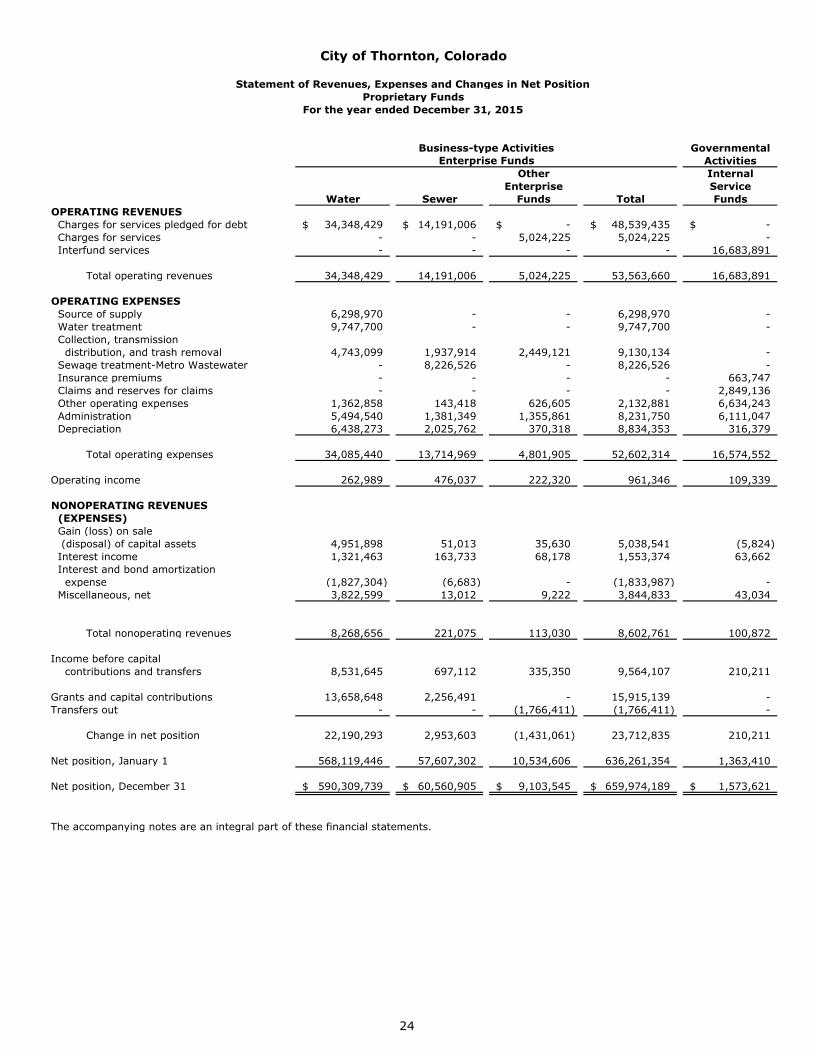

Statement of Revenues, Expenses, and Changes in Net Position – Proprietary Funds 24

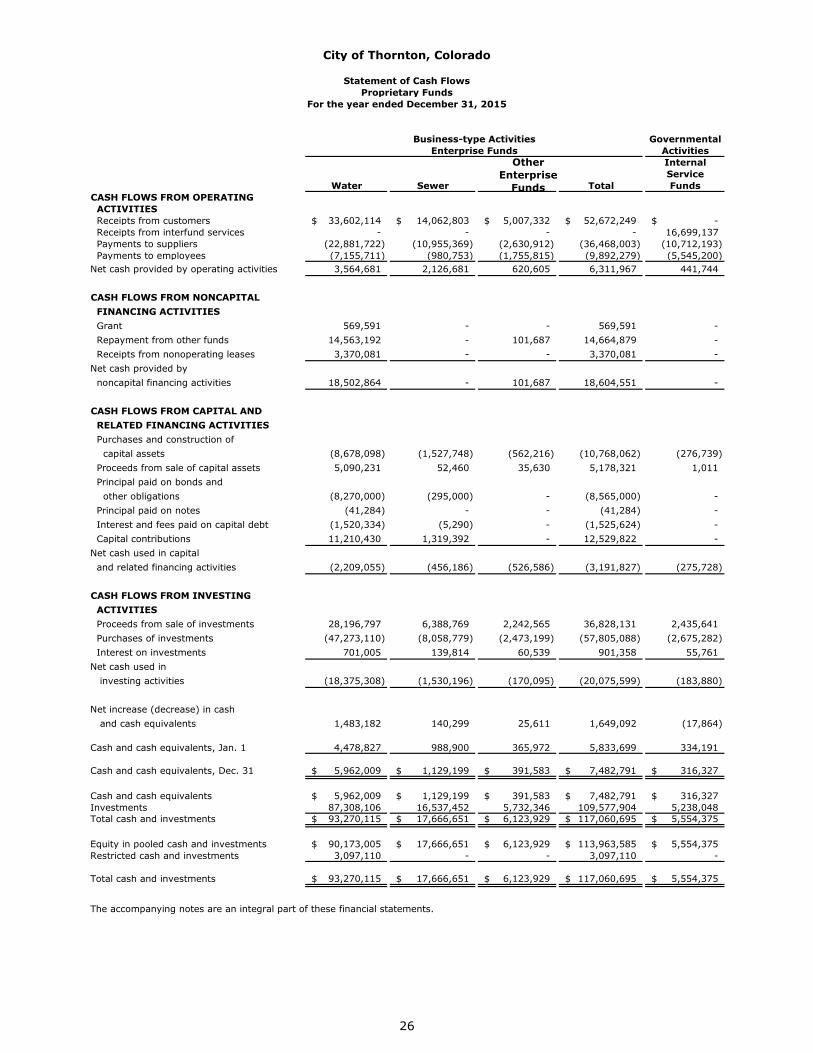

Statement of Cash Flows – Proprietary Funds 26

Notes to Financial Statements 28

Required Supplementary Information

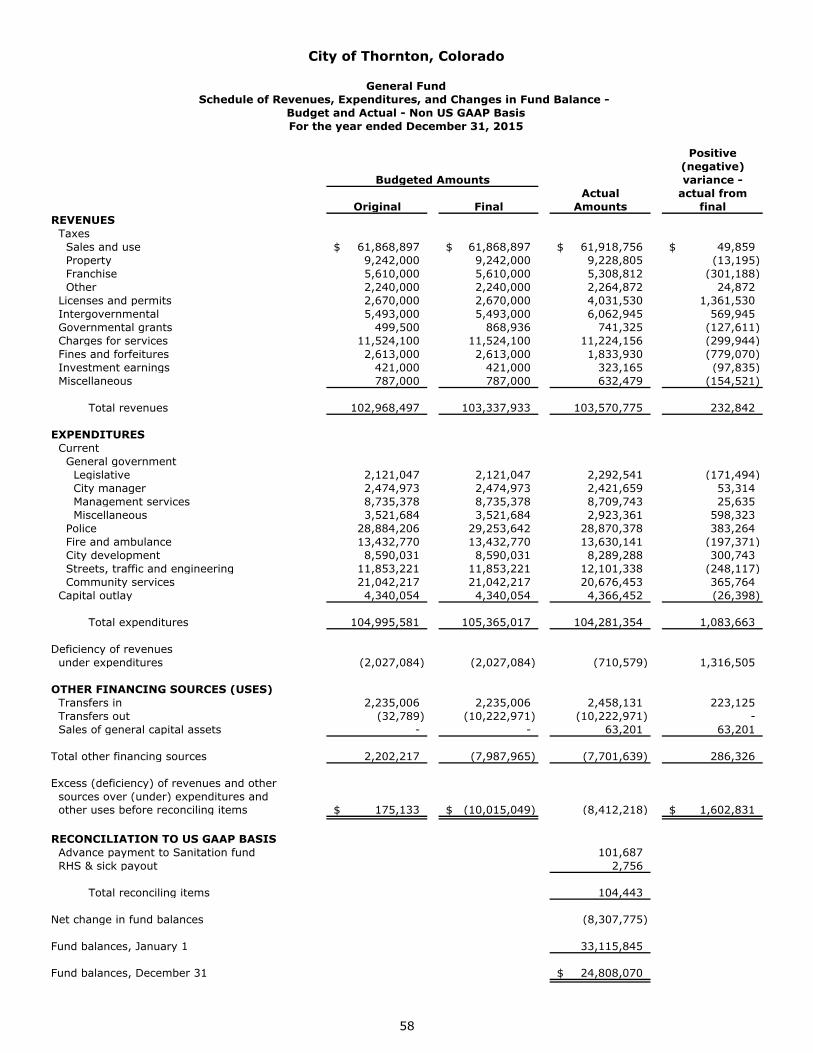

Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual – General Fund – Non US GAAP Basis 58

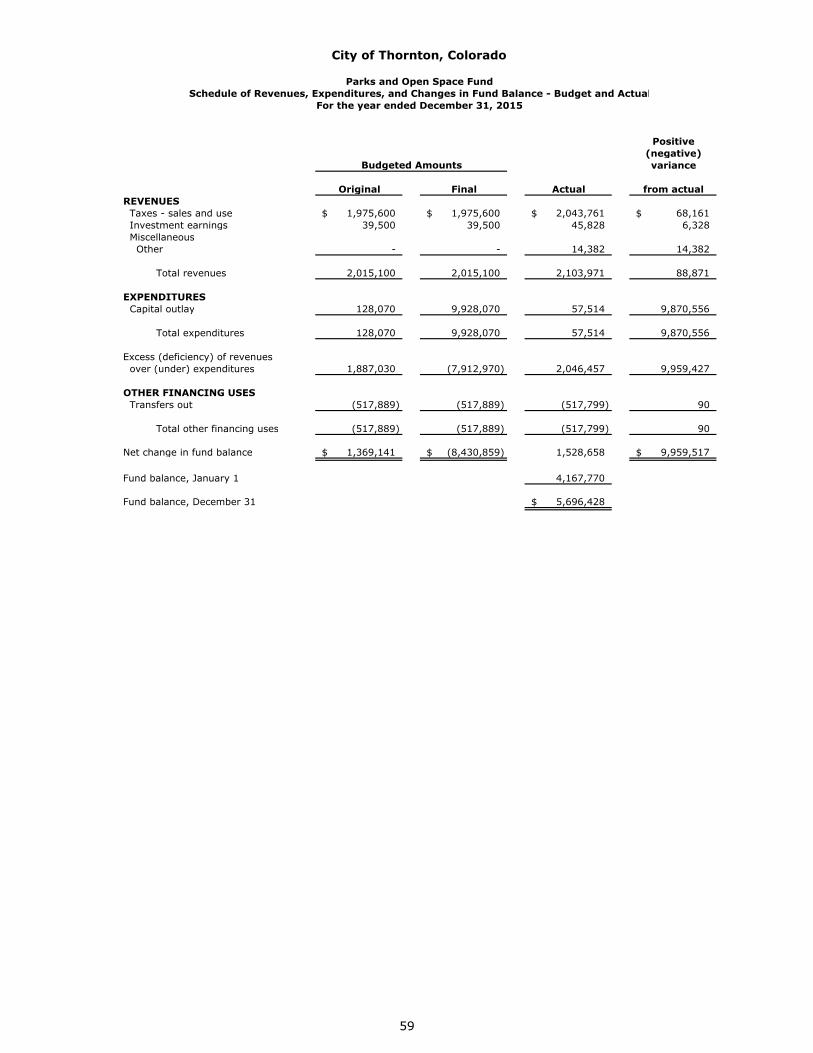

Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual – Parks and Open Space Fund 59

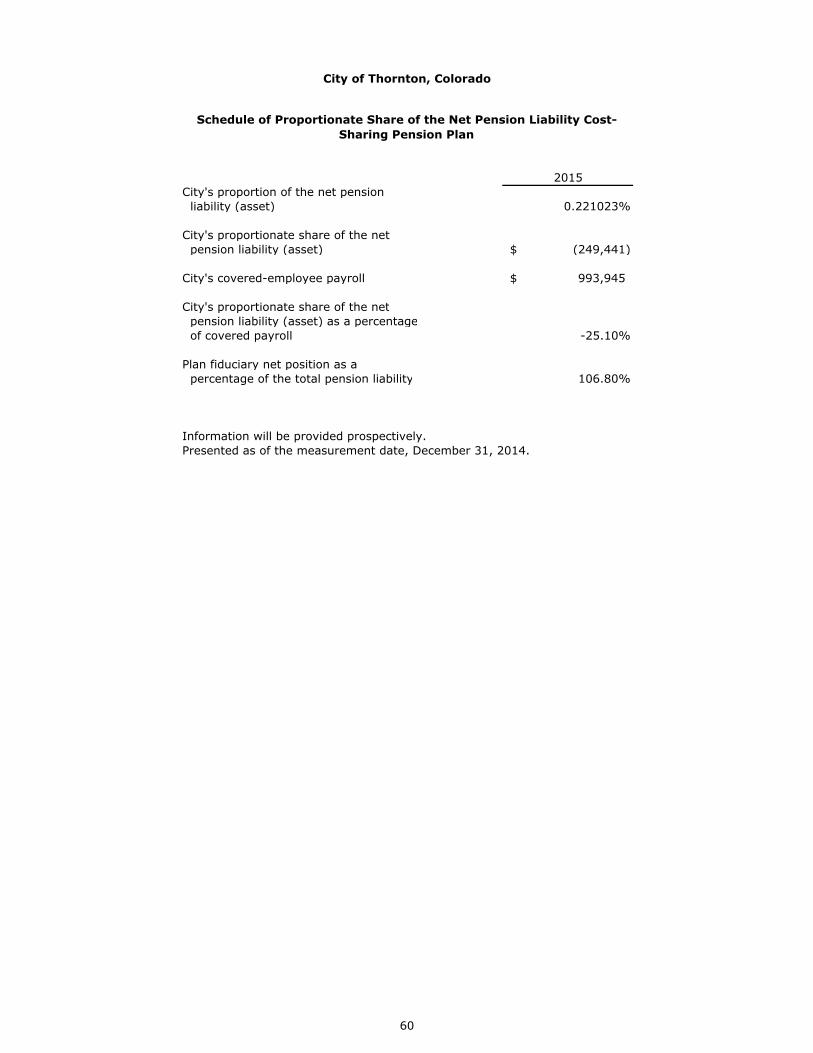

Schedule of Proportionate Share of the Net Pension Liability Cost-Sharing Plan 60

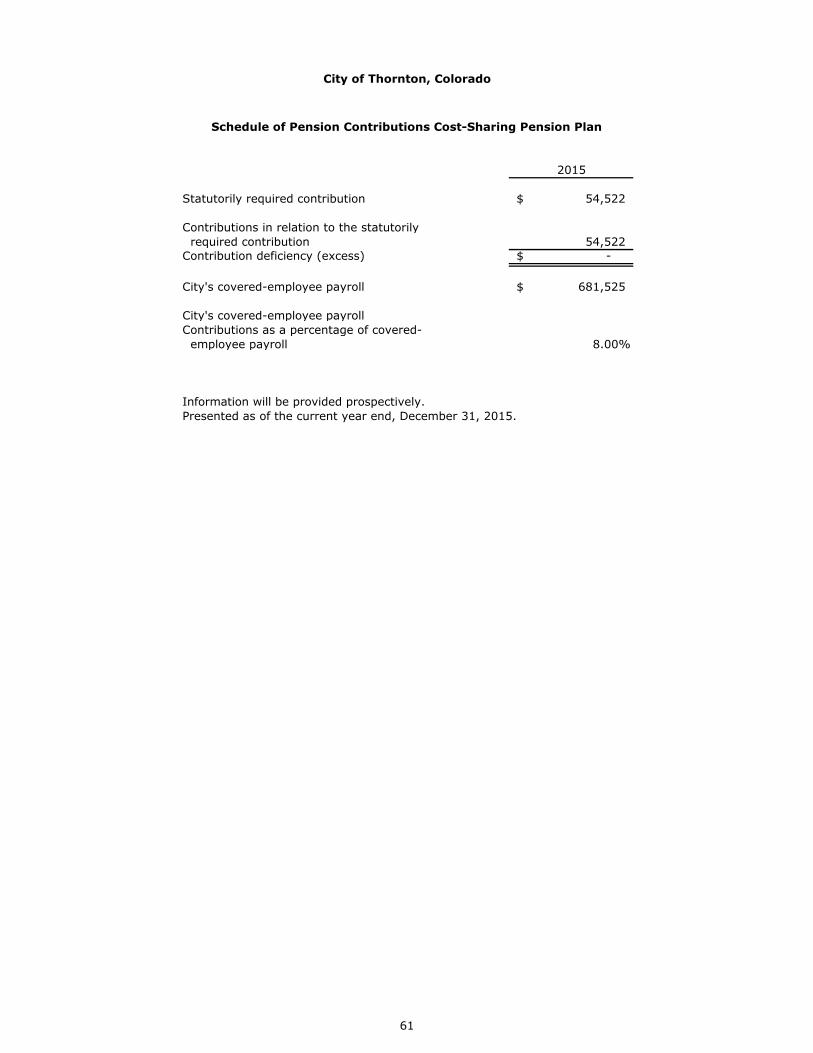

Schedule of Pension Contributions Cost-Sharing Plan 61

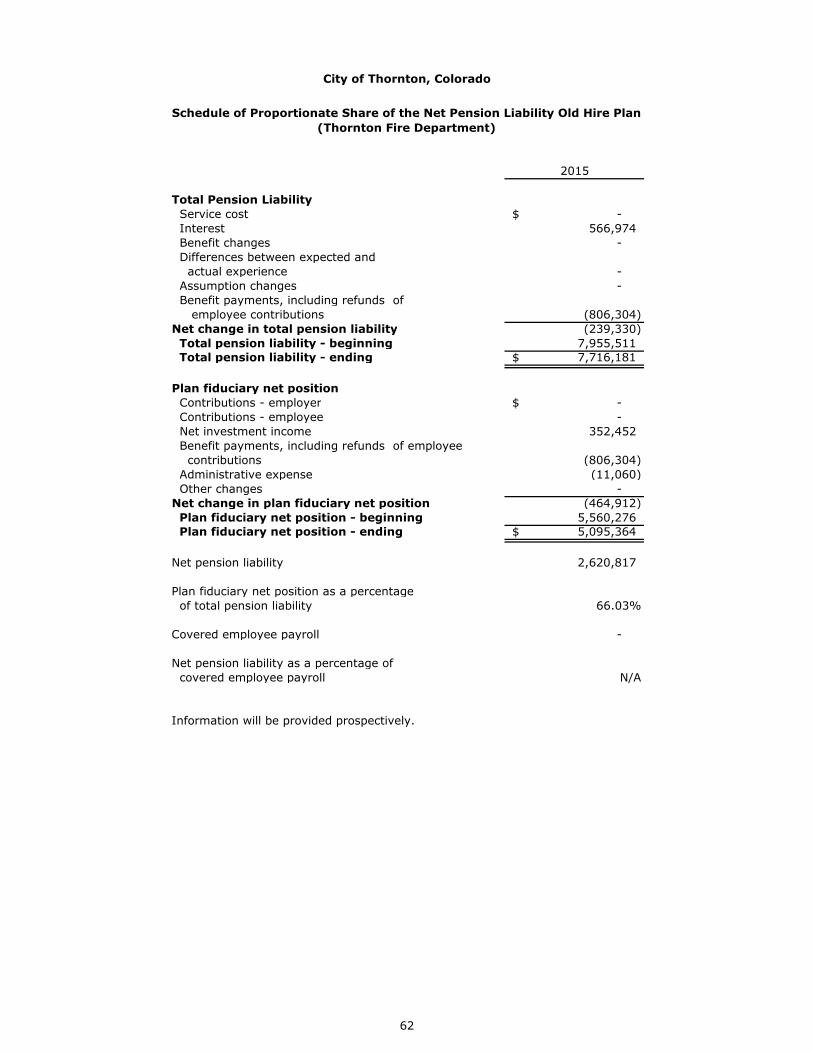

Schedule of Proportionate Share of Net Pension Liability Old Hire Plan (Thornton Fire) 62

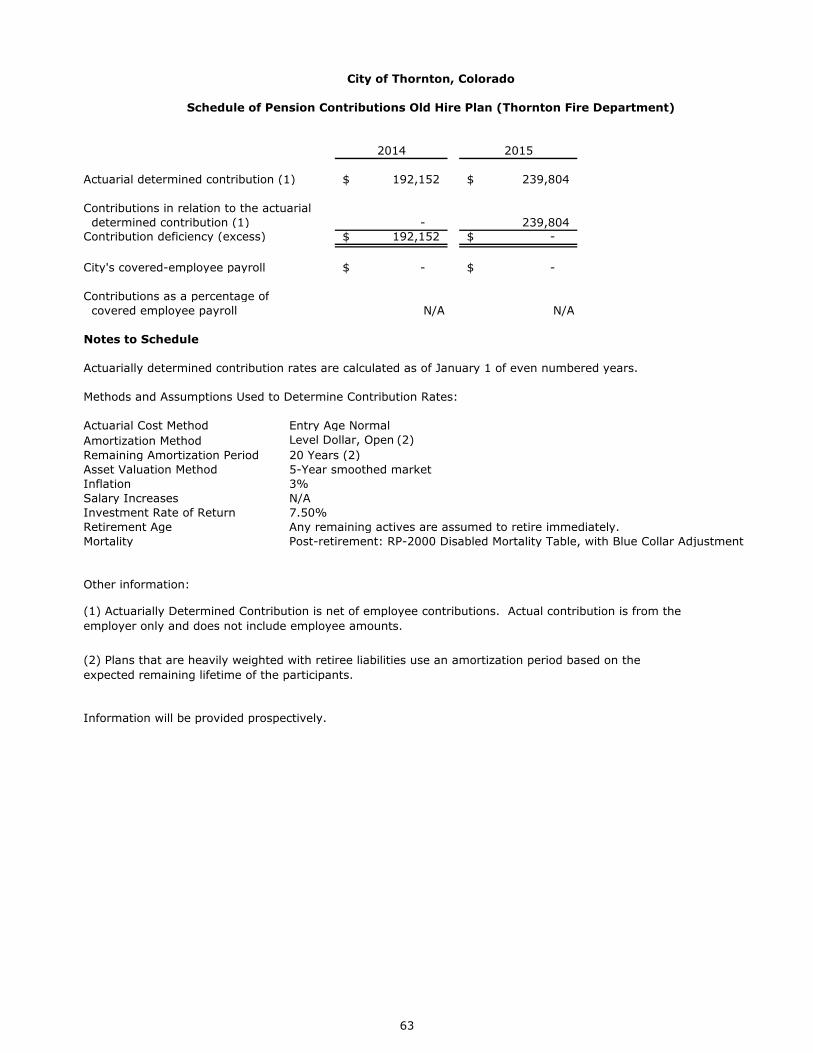

Schedule of Pension Contributions Old Hire Plan (Thornton Fire) 63

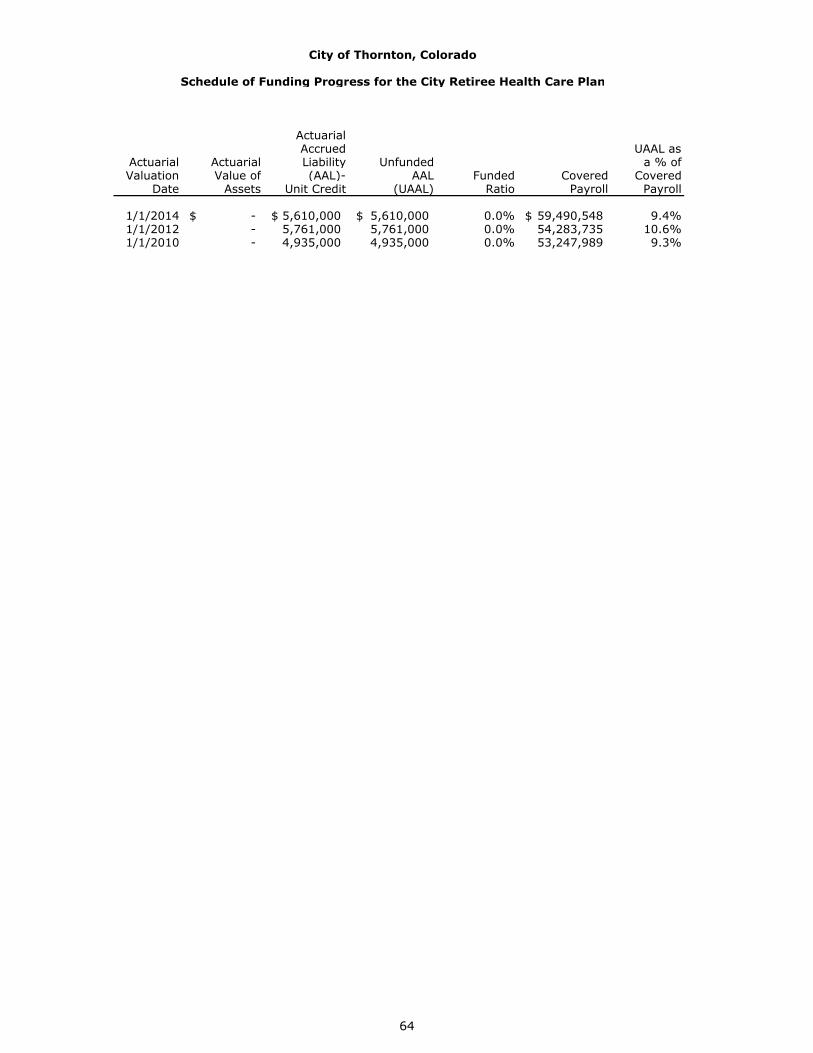

Schedule of Funding Progress for the City Retiree Health Care Plan 64

Combining Statements and Budgetary Schedules

Fund Descriptions – Non-Major Governmental Funds 66

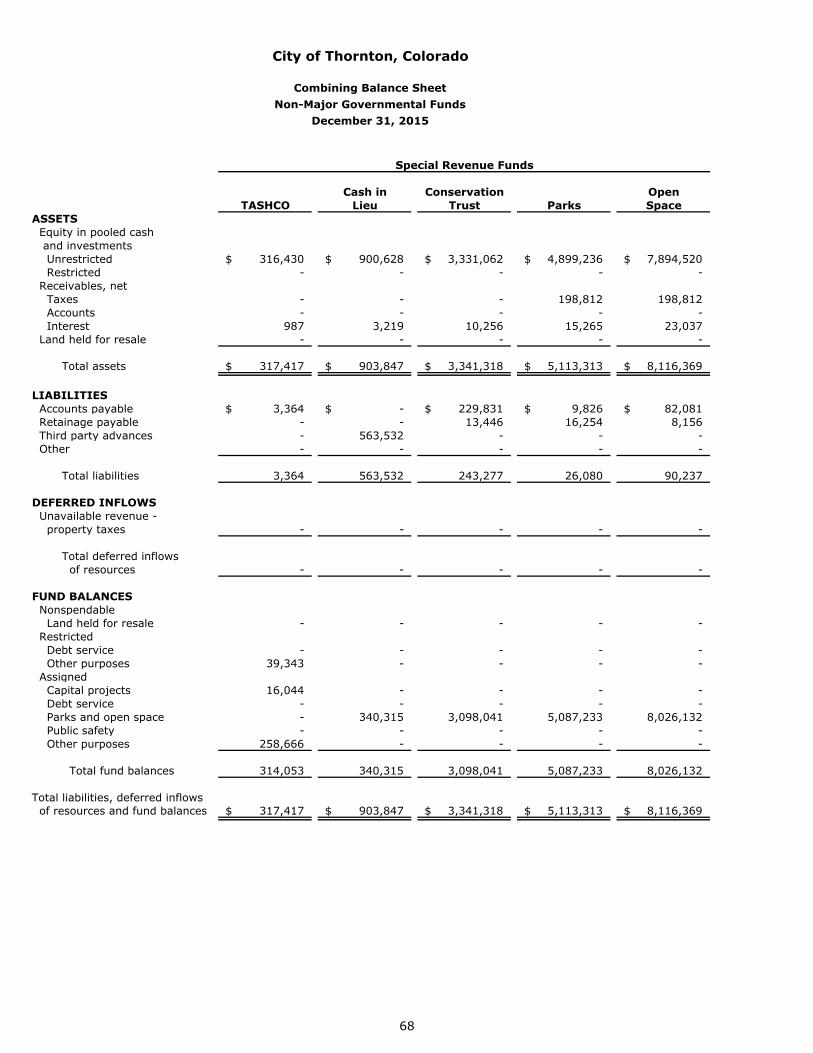

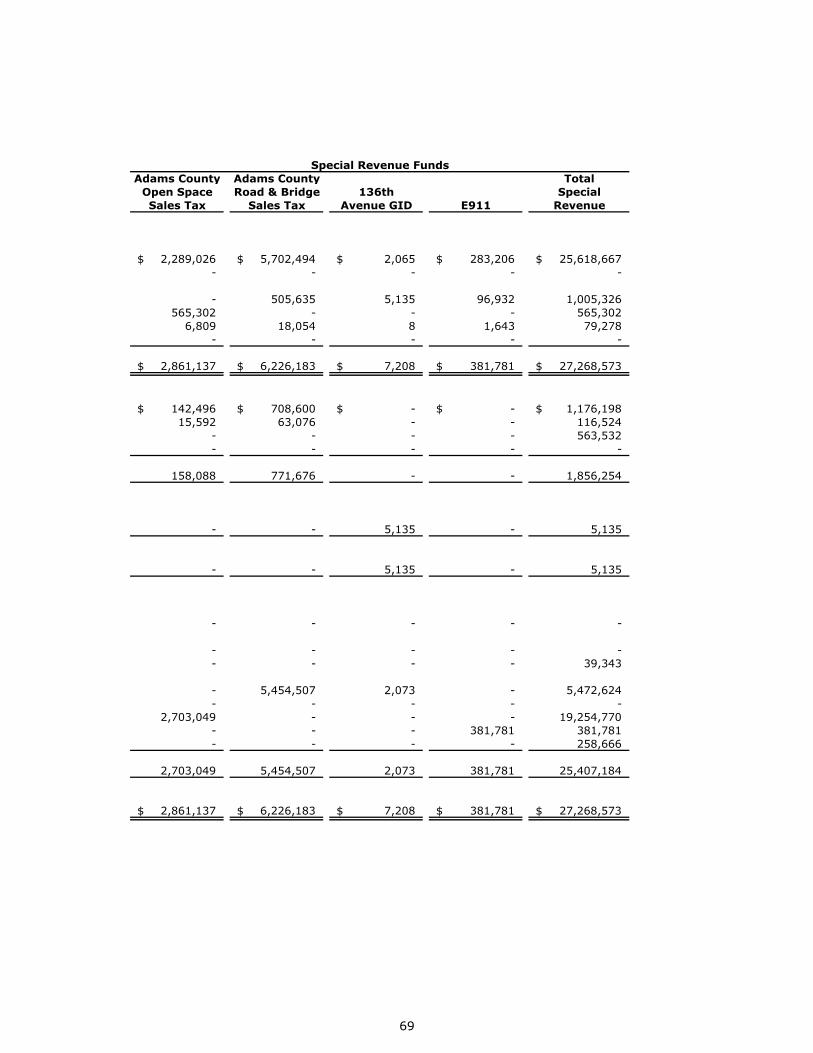

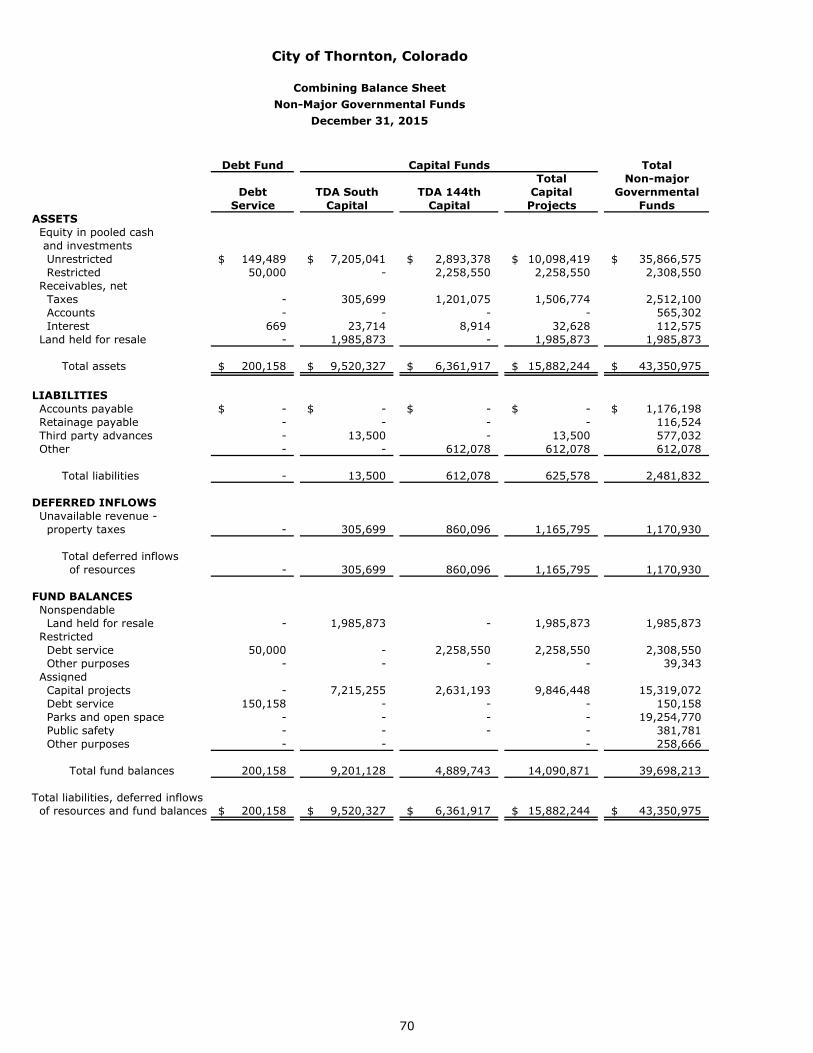

Combining Balance Sheet – Non-Major Governmental Funds 68

i

City of Thornton, Colorado Table of Contents (Continued)

Financial Section (Continued) Page

Combining Statements and Budgetary Schedules (Continued)

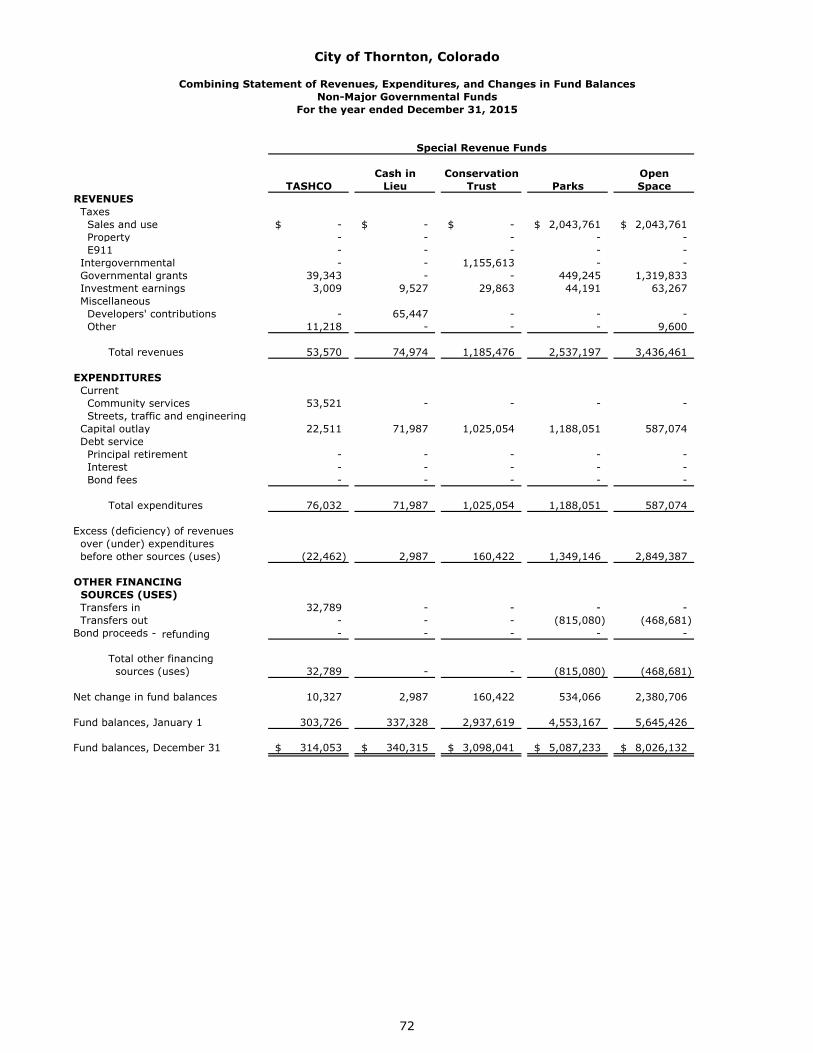

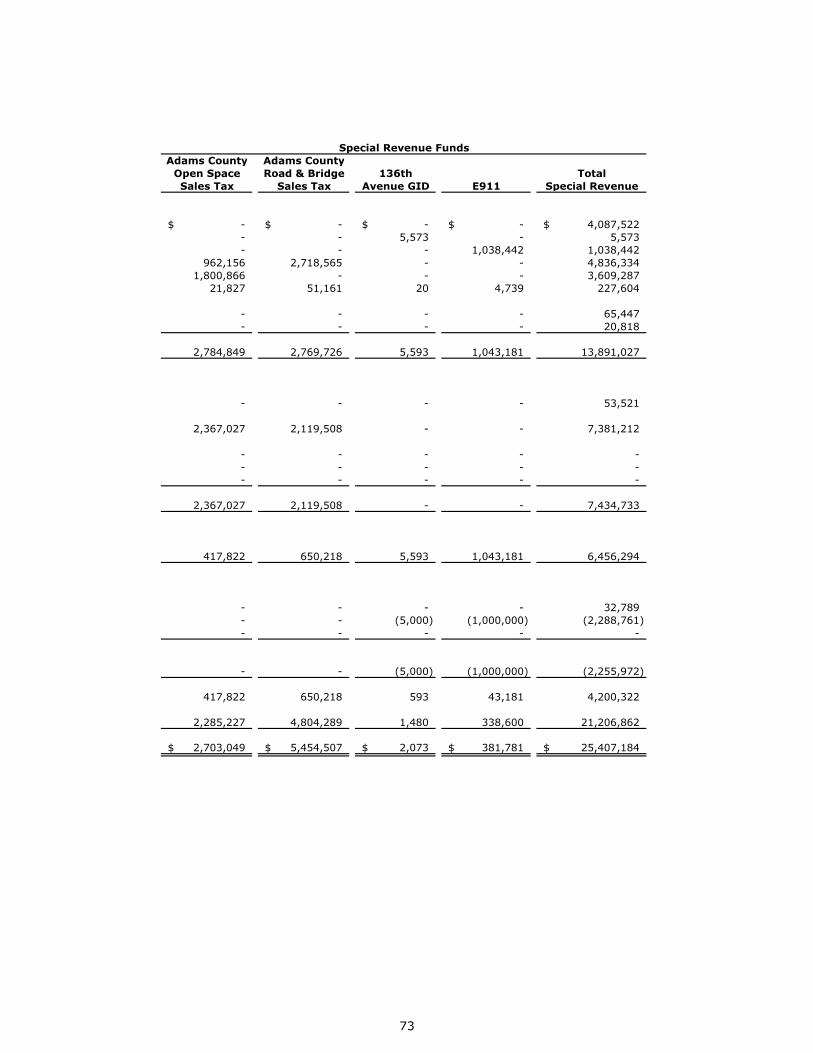

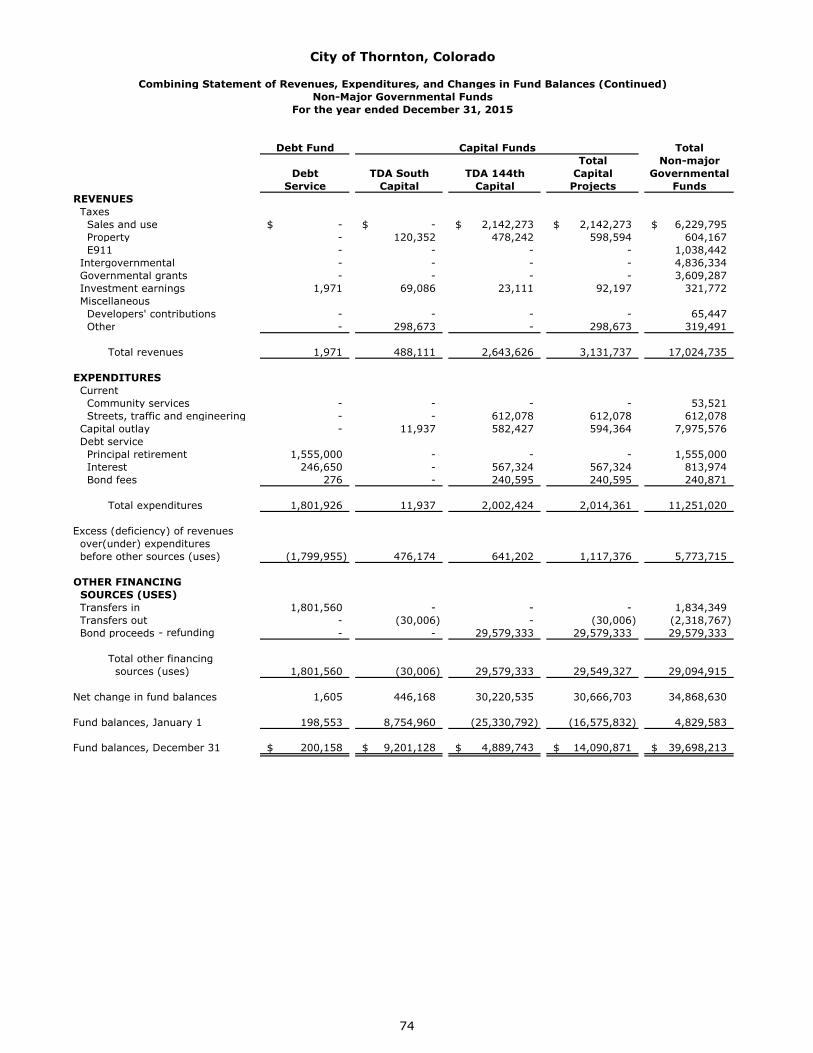

Combining Statement of Revenues, Expenditures, and Changes in Fund Balances – Non-Major Governmental Funds 72

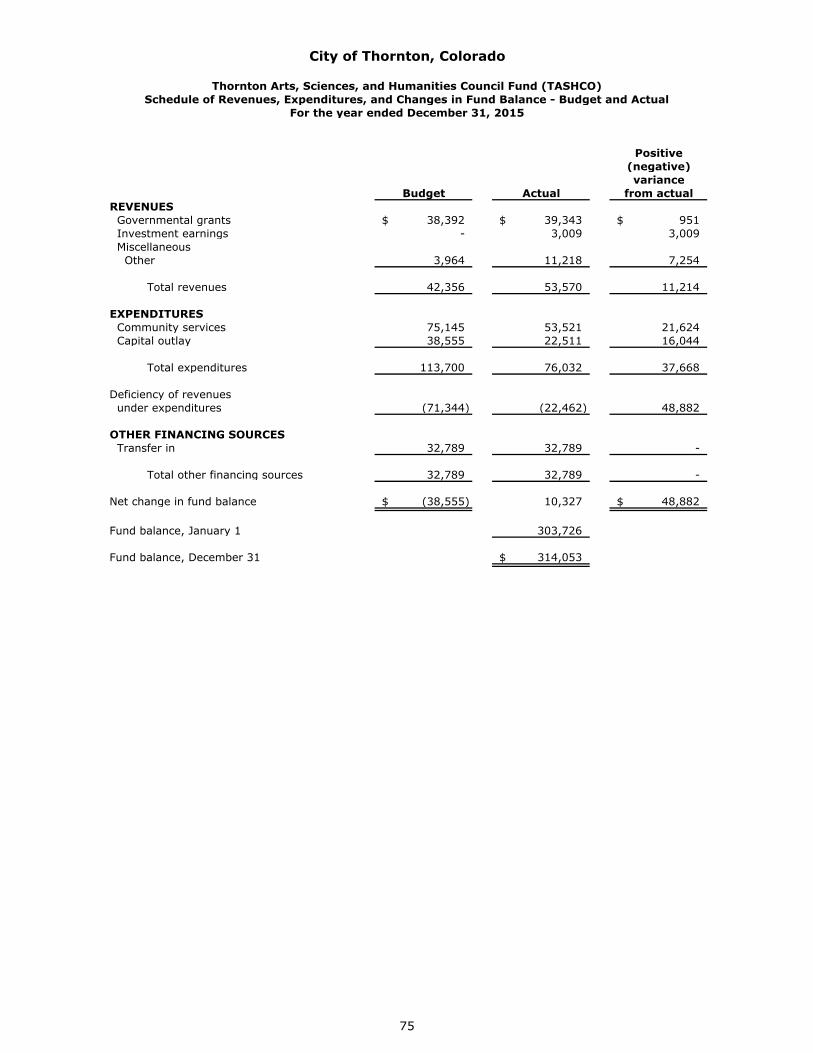

Thornton Arts, Sciences, and Humanities Council Fund (TASHCO) Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 75

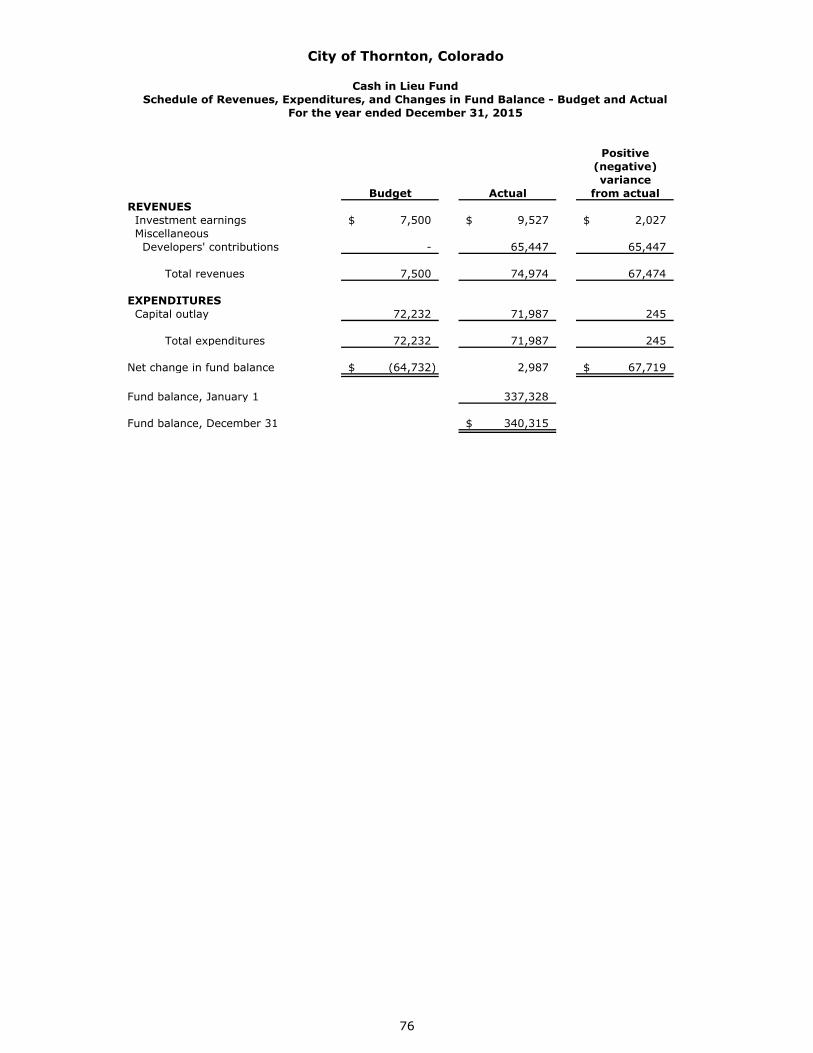

Cash in Lieu Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 76

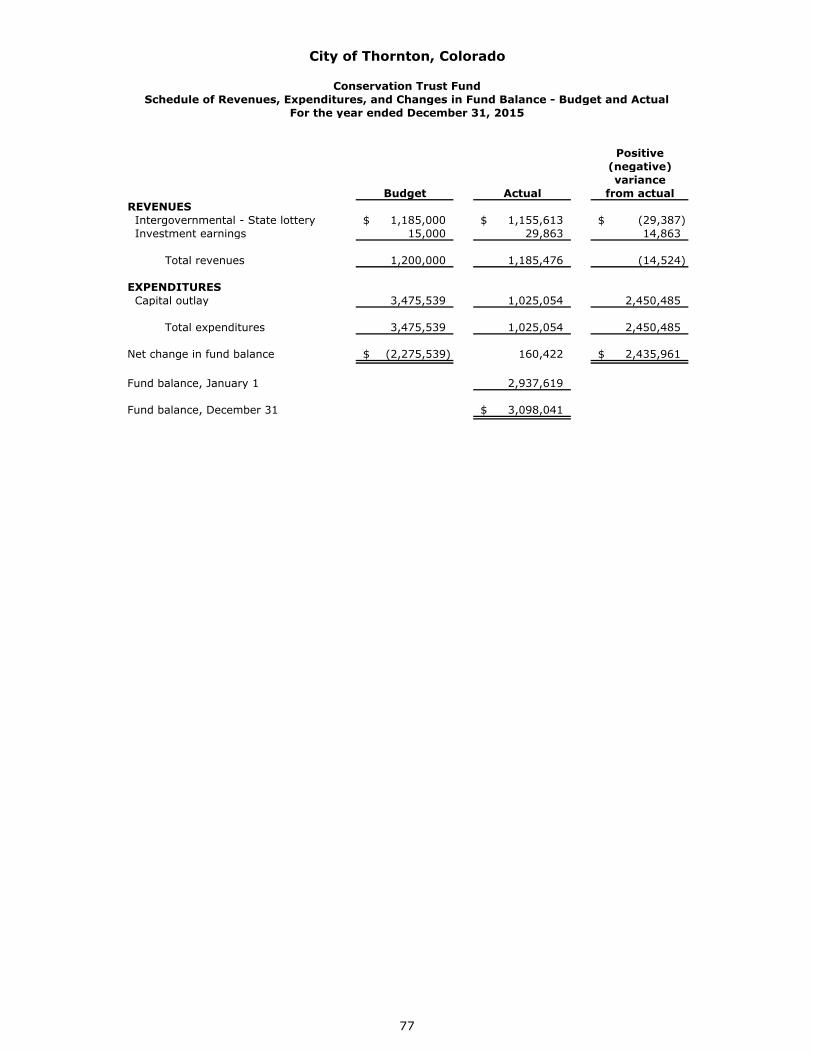

Conservation Trust Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 77

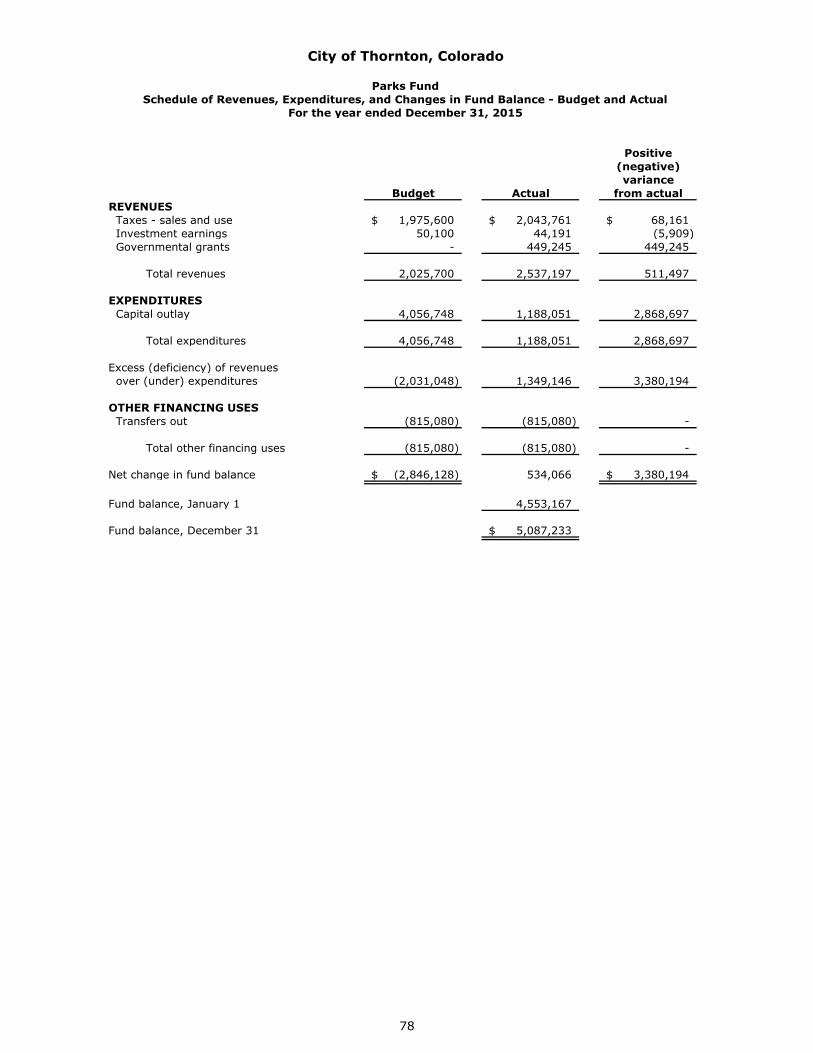

Parks Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 78

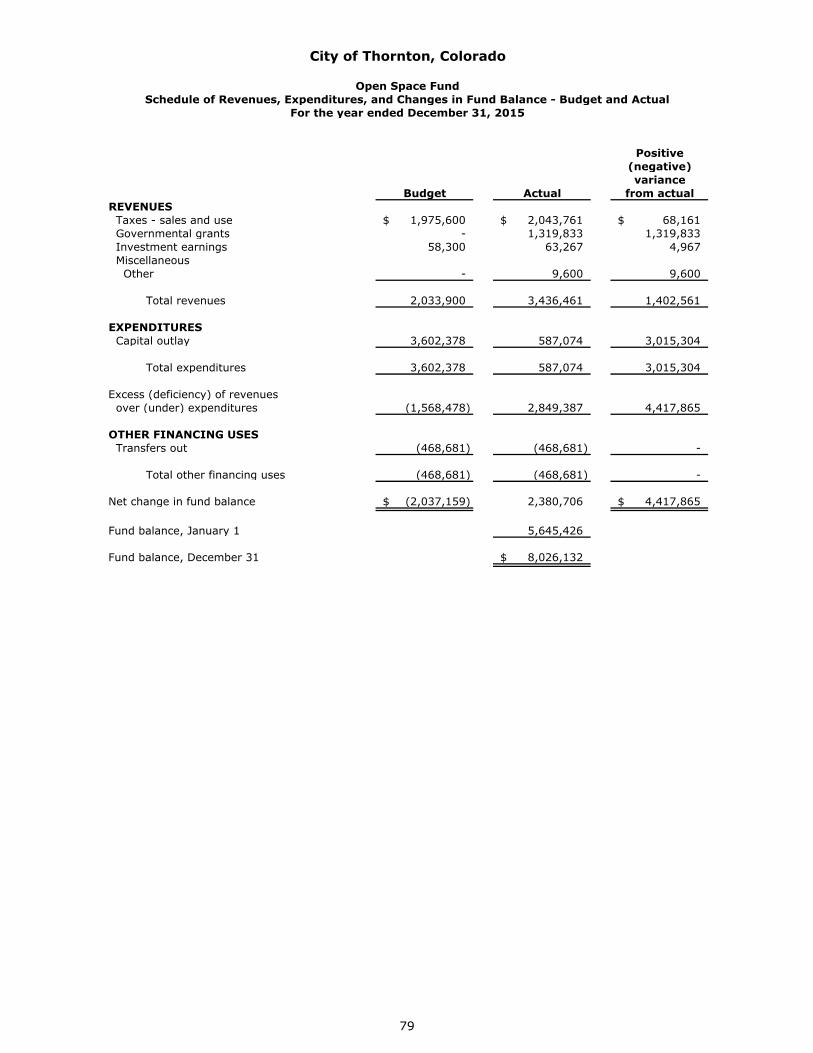

Open Space Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 79

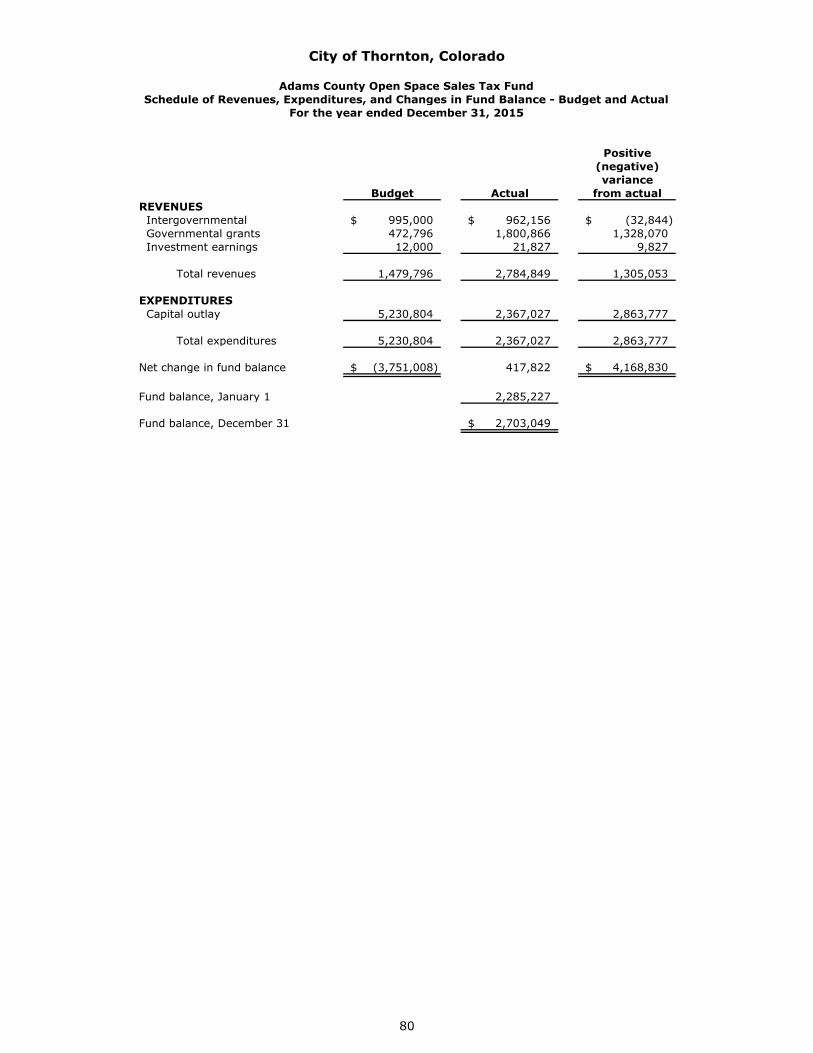

Adams County Open Space Sales Tax Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 80

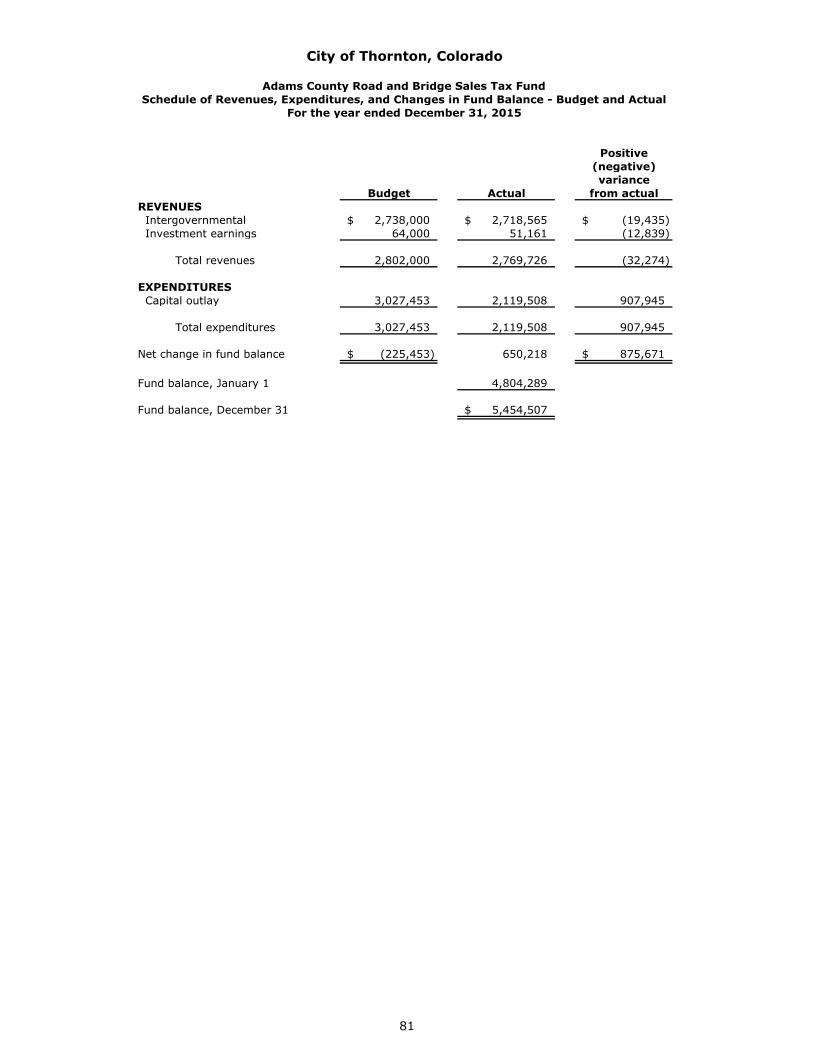

Adams County Road & Bridge Sales Tax Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 81

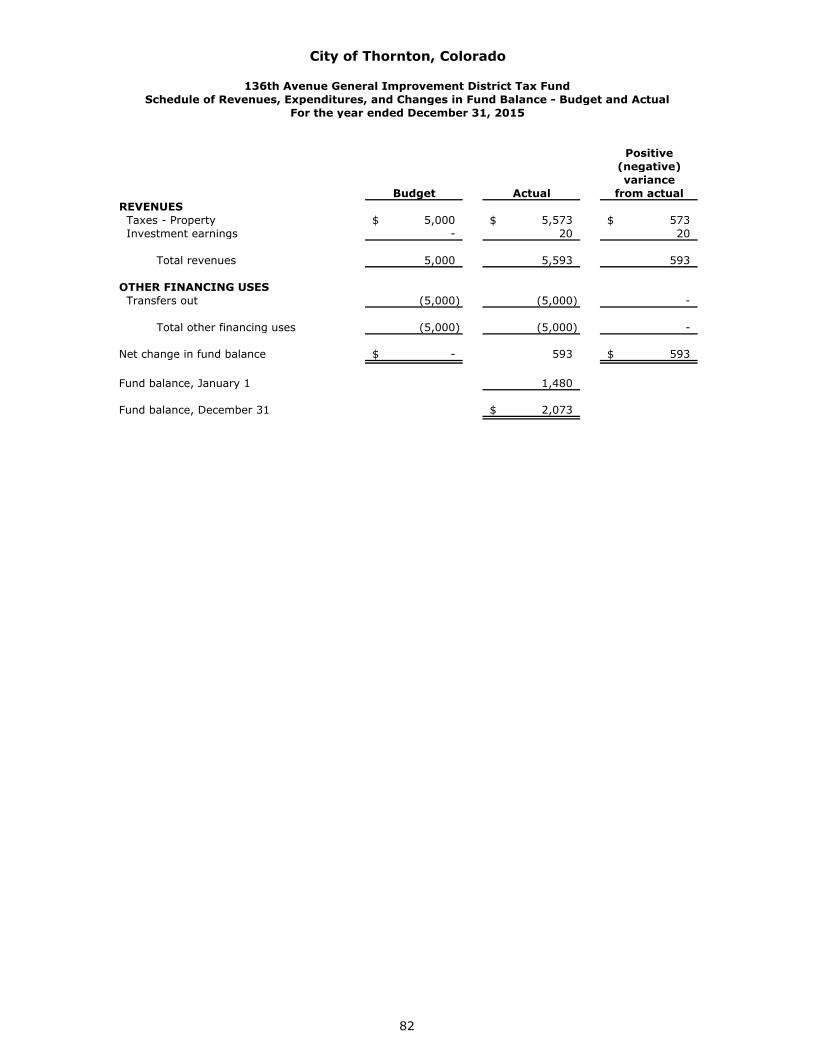

136th Avenue General Improvement District Tax Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 82

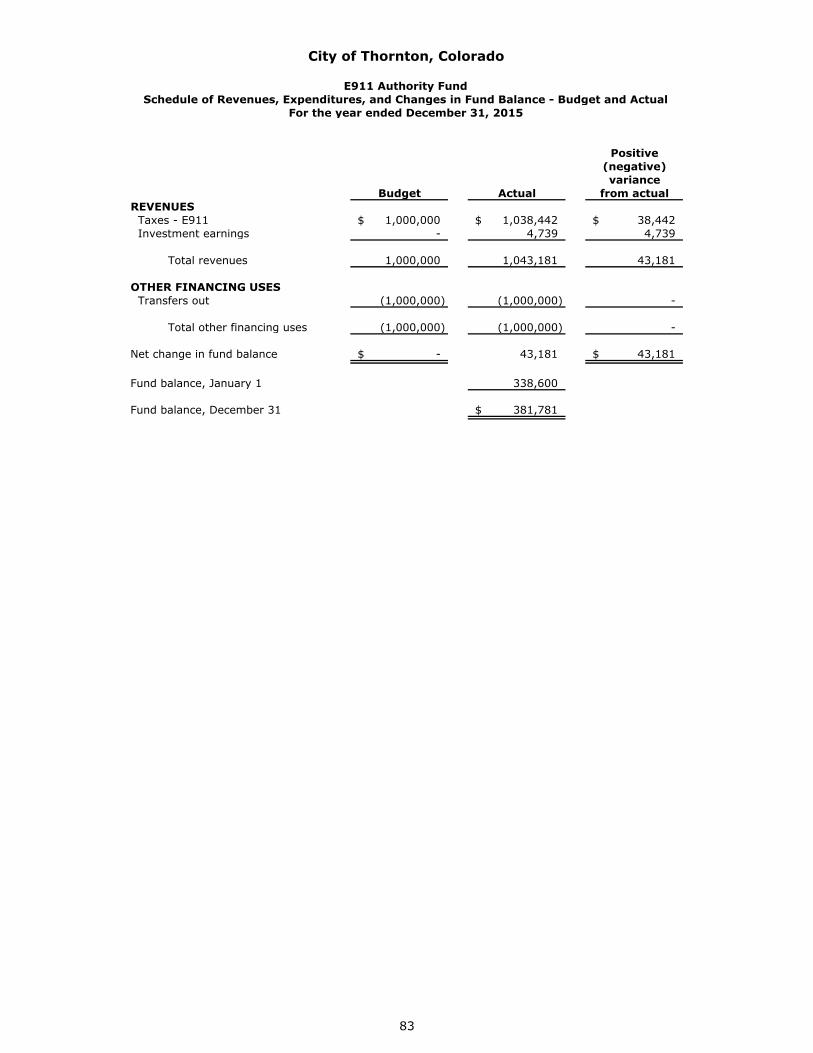

E911 Authority Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 83

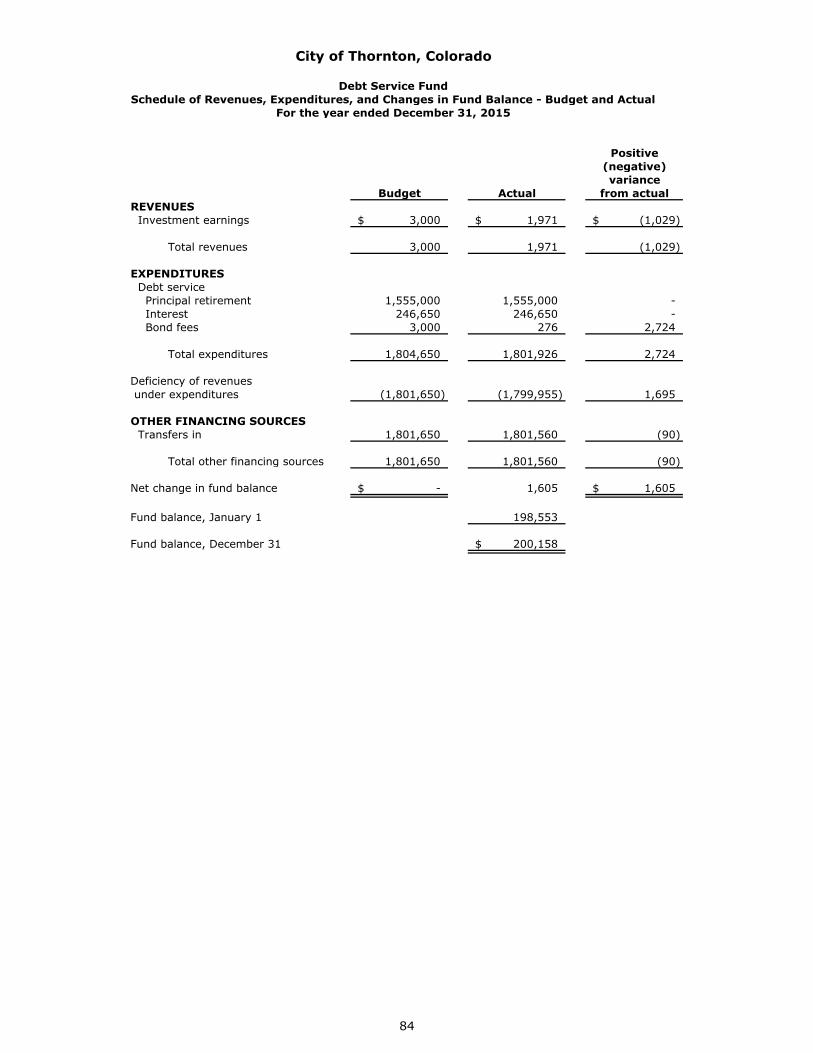

Debt Service Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 84

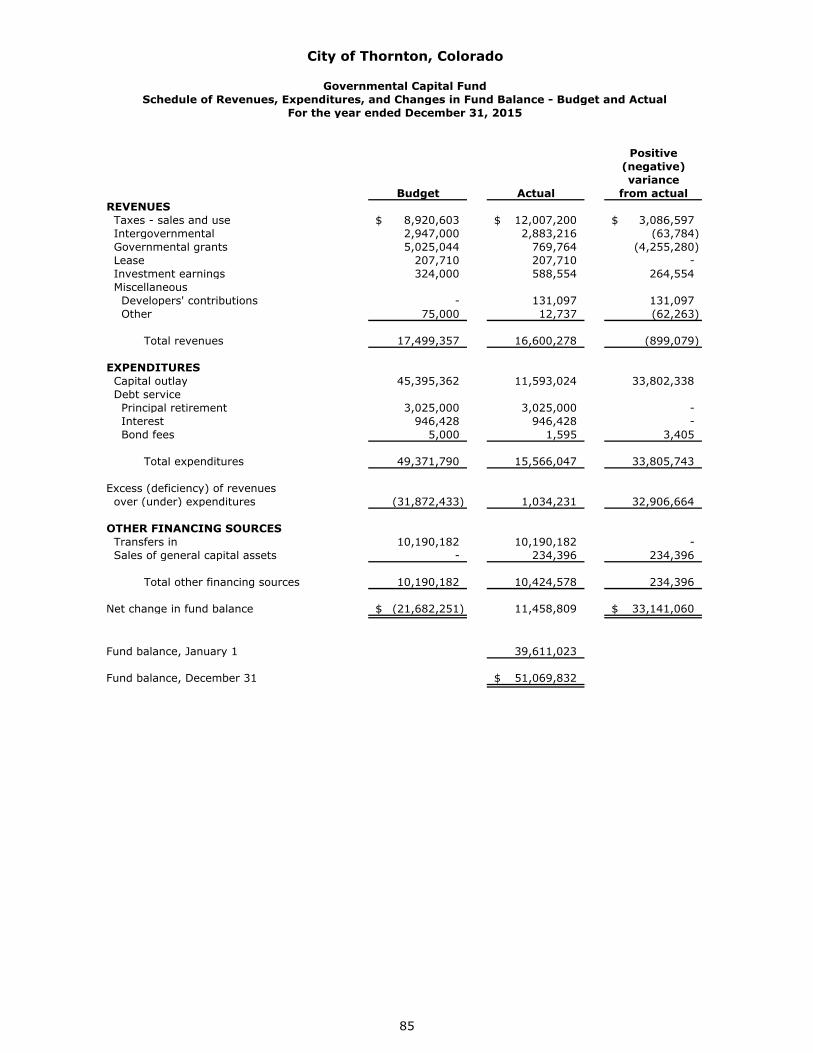

Governmental Capital Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 85

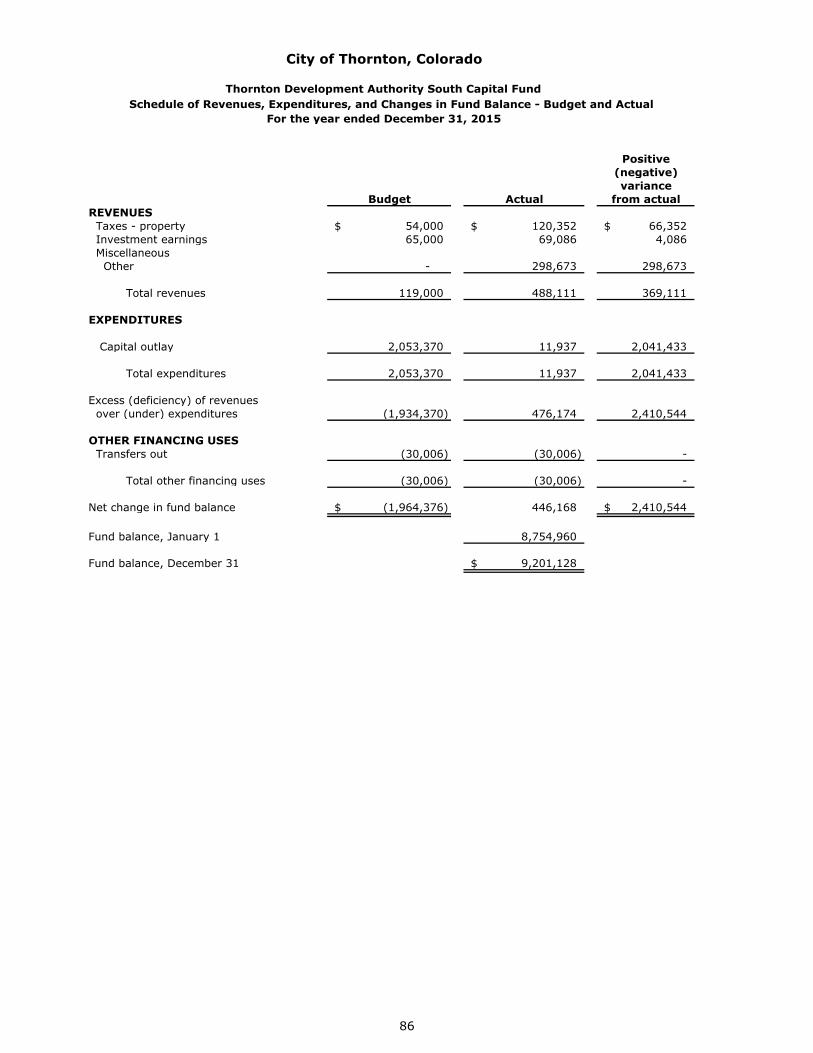

Thornton Development Authority South Capital Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 86

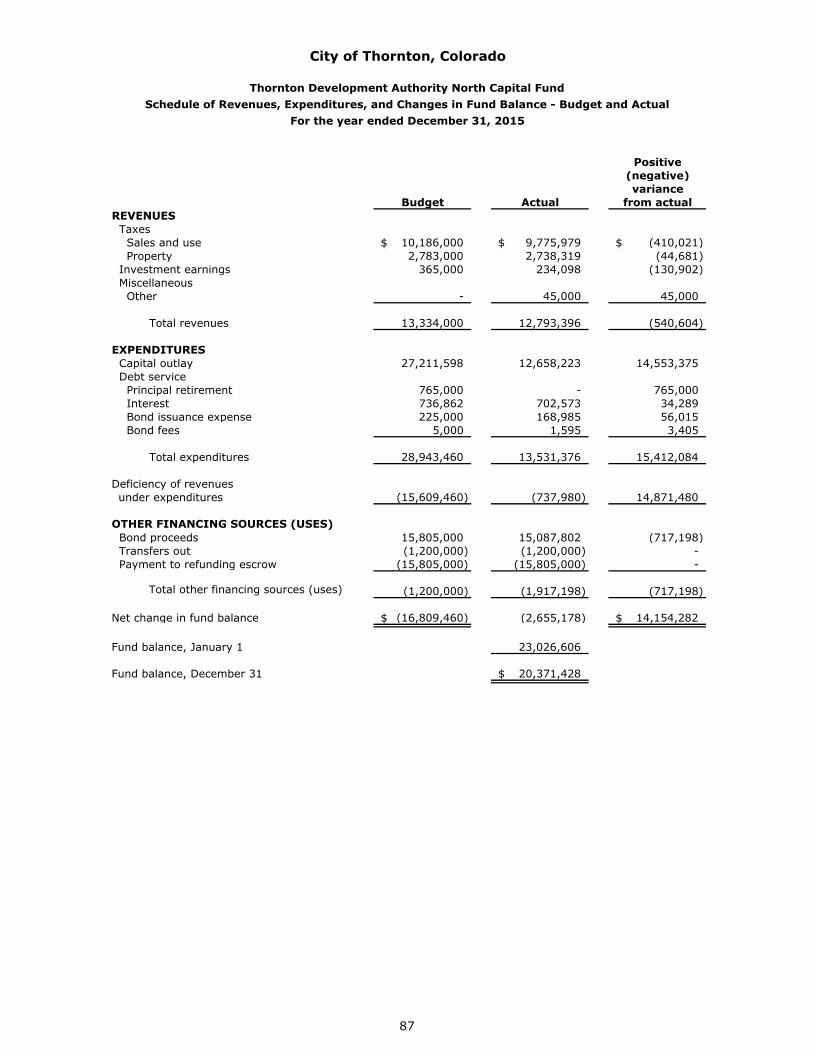

Thornton Development Authority North Capital Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual 87

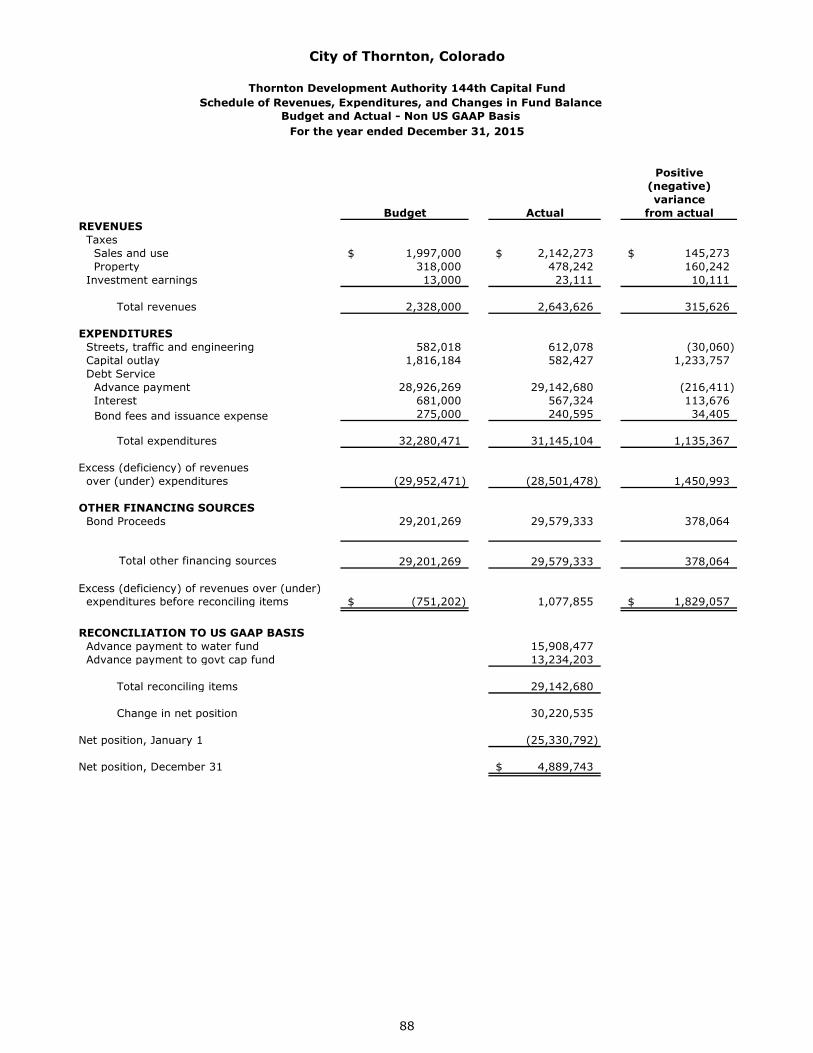

Thornton Development Authority 144th Capital Fund Schedule of Revenues, Expenditures, and Changes in Fund Balance – Budget and Actual

– Non US GAAP Basis 88

Fund Descriptions – Major Enterprise Funds 90

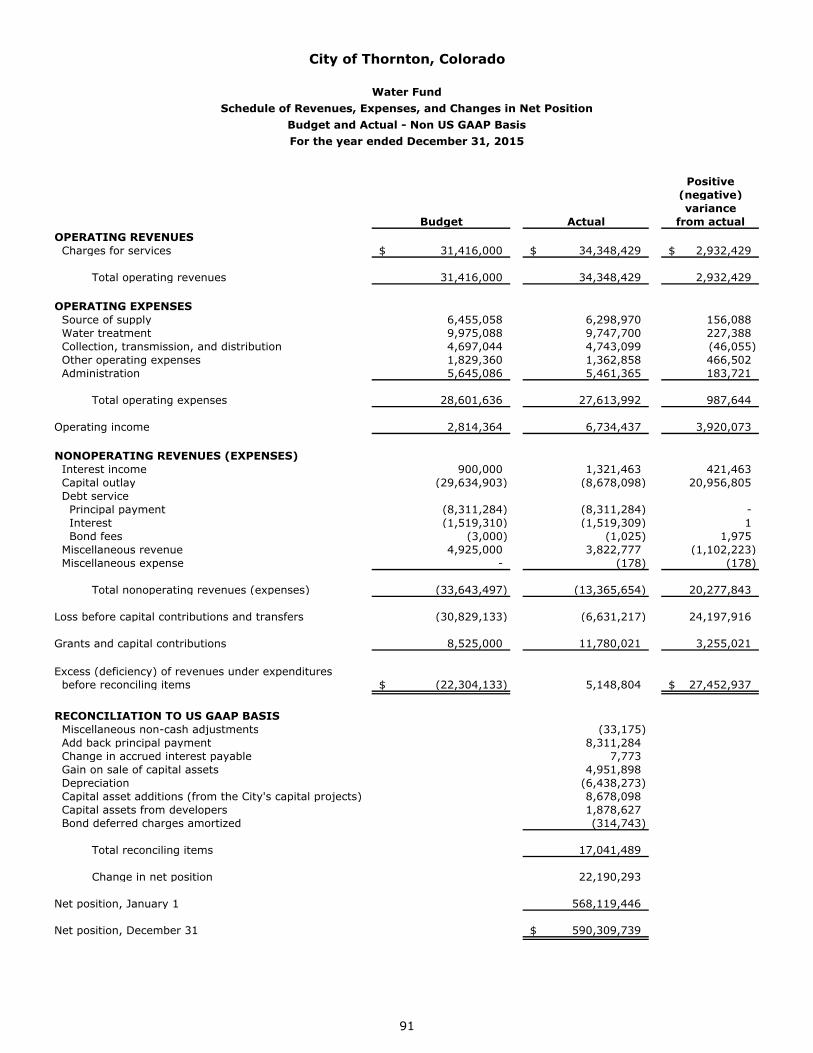

Water Fund Schedule of Revenues, Expenses, and Changes in Net Position – Budget and Actual

– Non US GAAP Basis 91 Sewer Fund

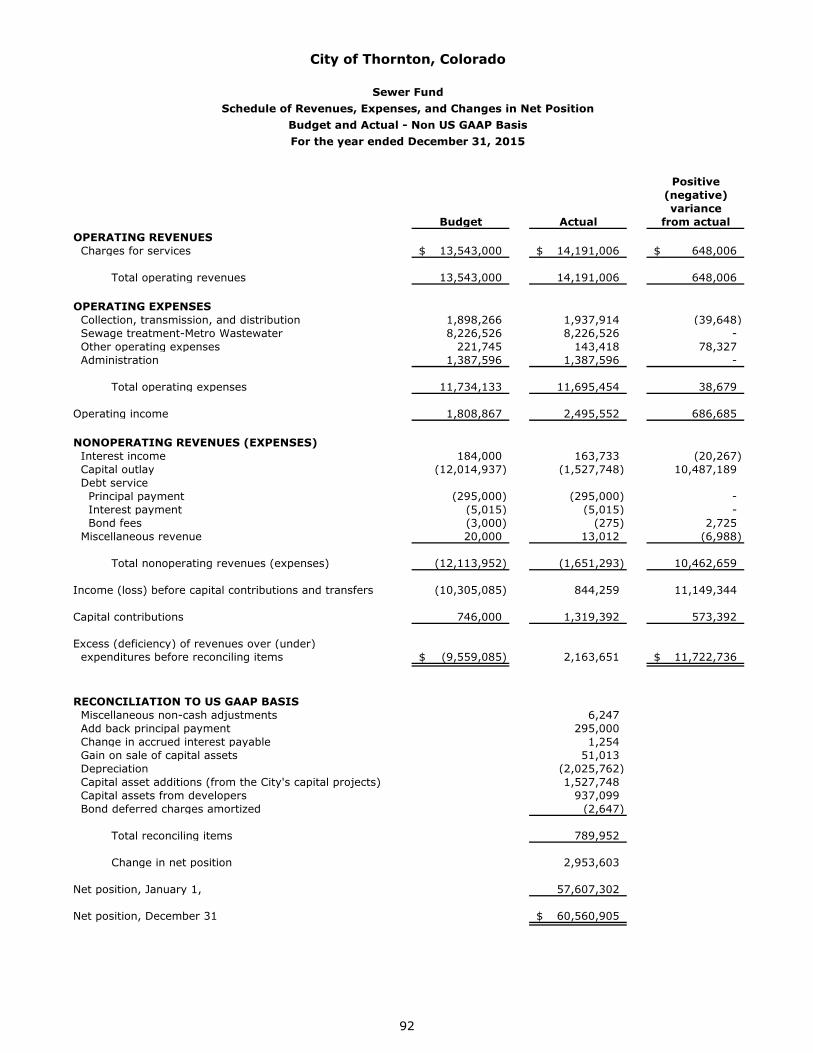

Schedule of Revenues, Expenses, and Changes in Net Position – Budget and Actual – Non US GAAP Basis 92

Fund Descriptions – Non-Major Enterprise Funds 93

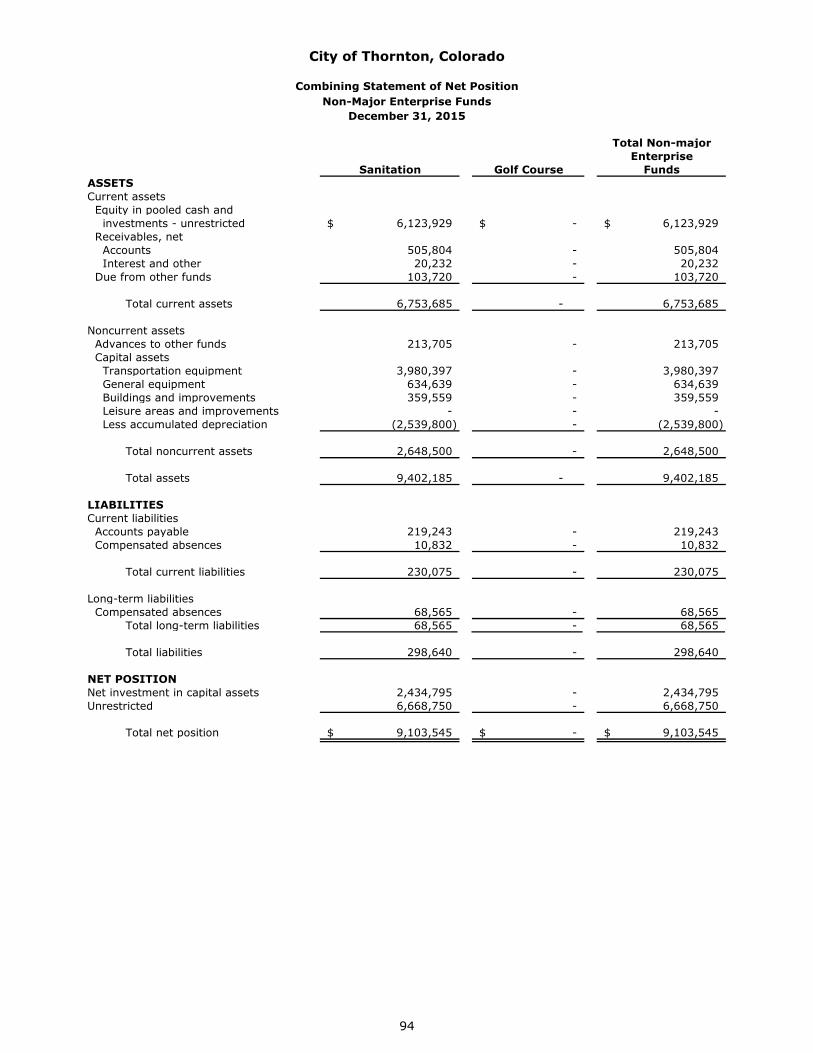

Combining Statement of Net Position – Non-Major Enterprise Funds 94

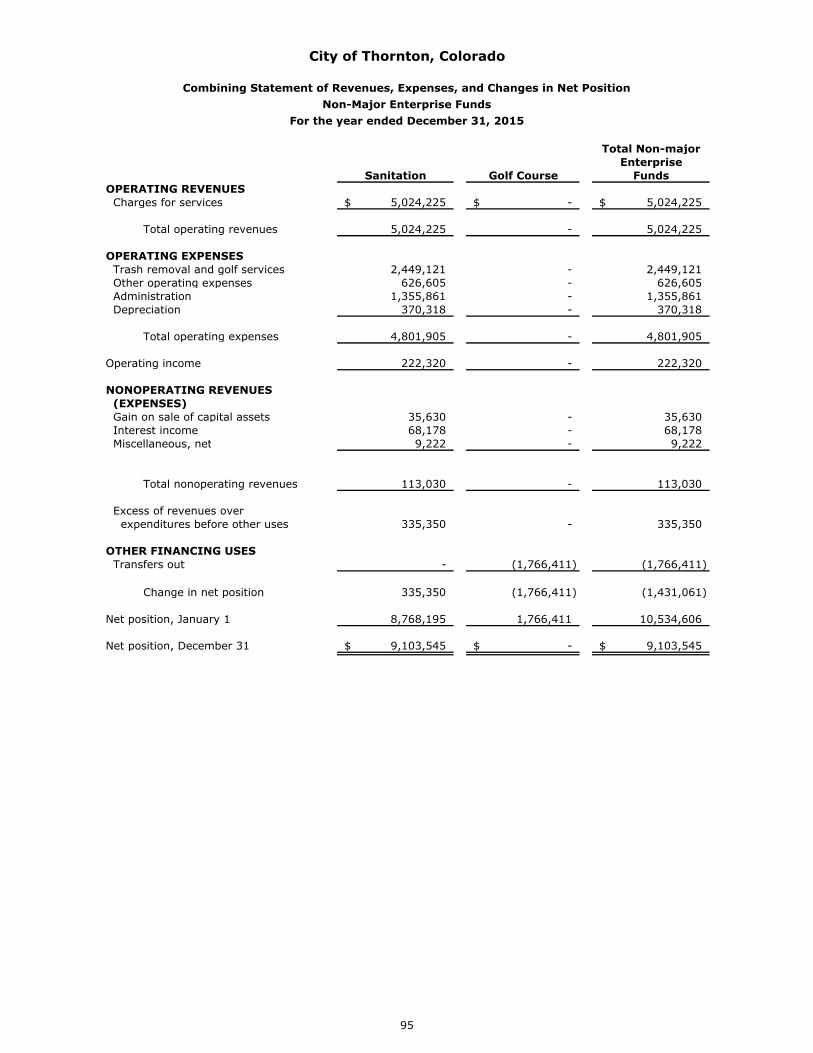

Combining Statement of Revenues, Expenses, and Changes in Net Position - Non-Major Enterprise Funds 95

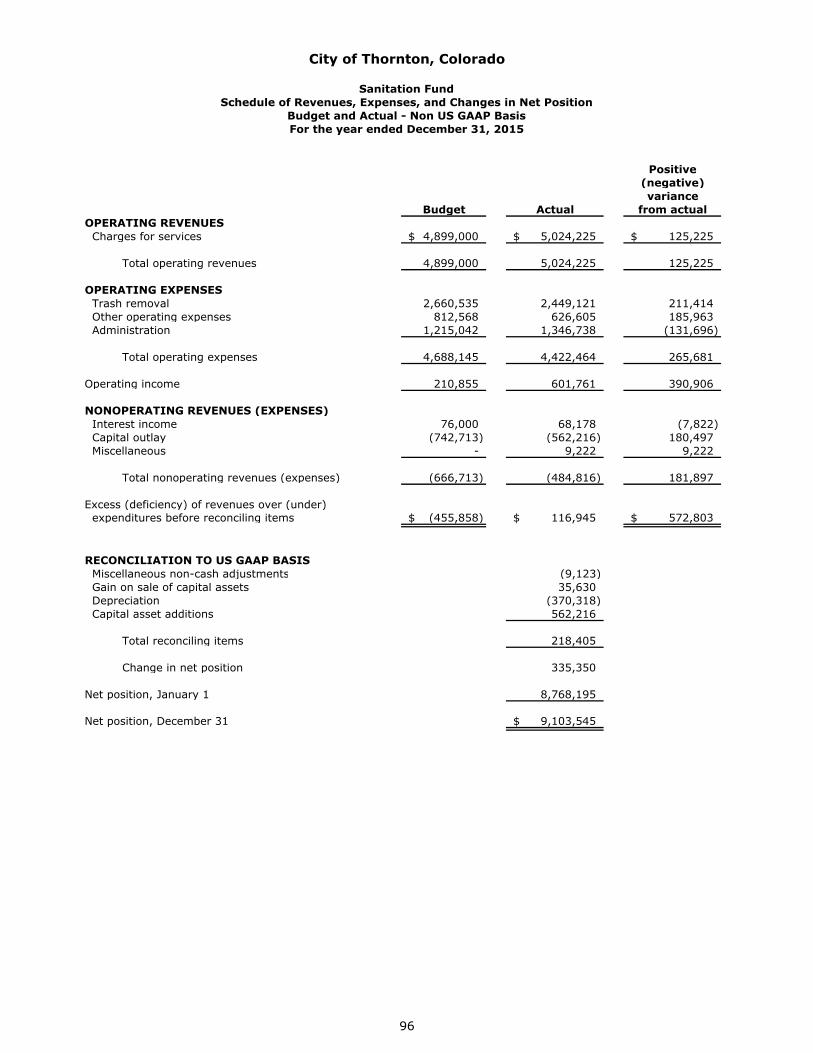

Sanitation Fund Schedule of Revenues, Expenses, and Changes in Net Position – Budget and Actual

– Non US GAAP Basis 96

ii

City of Thornton, Colorado

Table of Contents (Continued)

Financial Section (Continued) Page

Combining Statements and Budgetary Schedules (Continued)

Fund Descriptions – Internal Service Funds 97

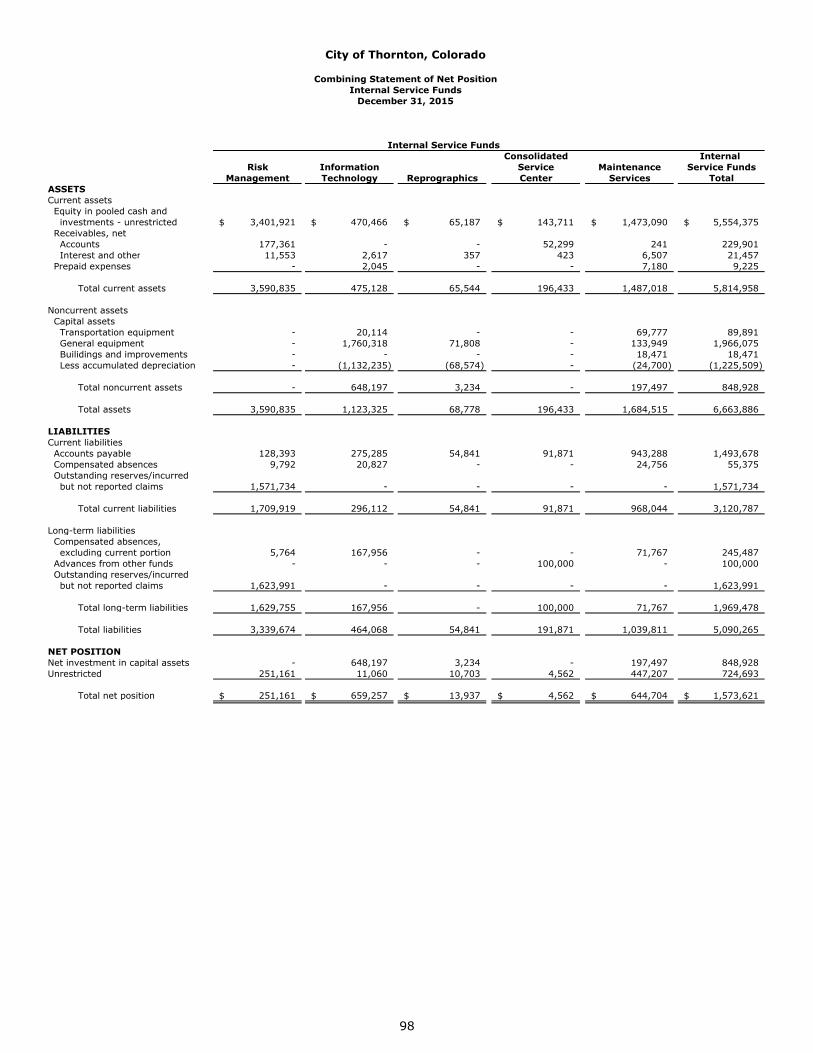

Combining Statement of Net Position – Internal Service Funds 98

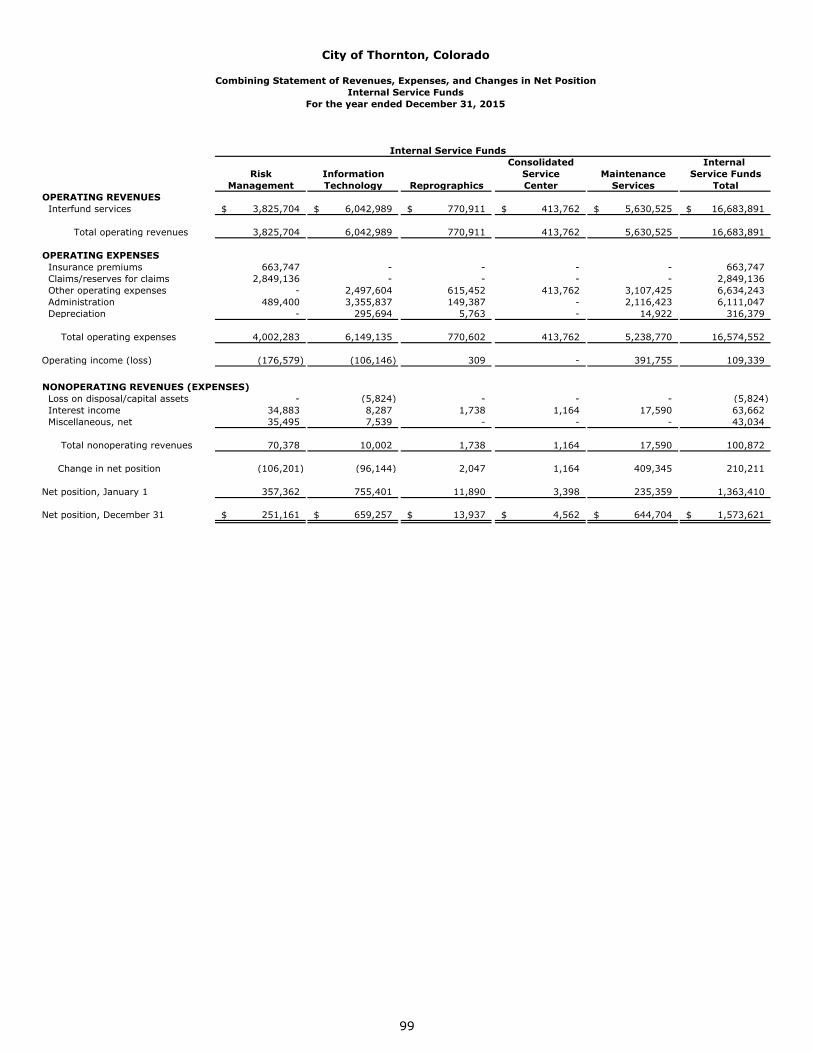

Combining Statement of Revenues, Expenses, and Changes in Net Position – Internal Service Funds 99

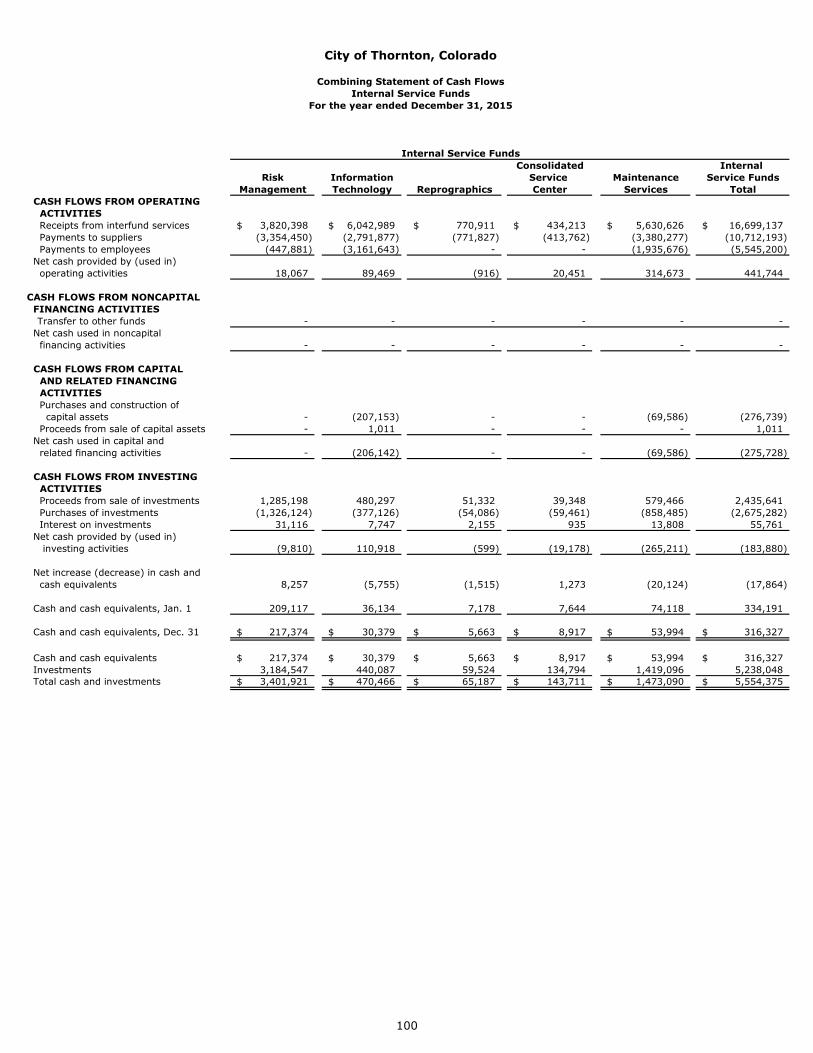

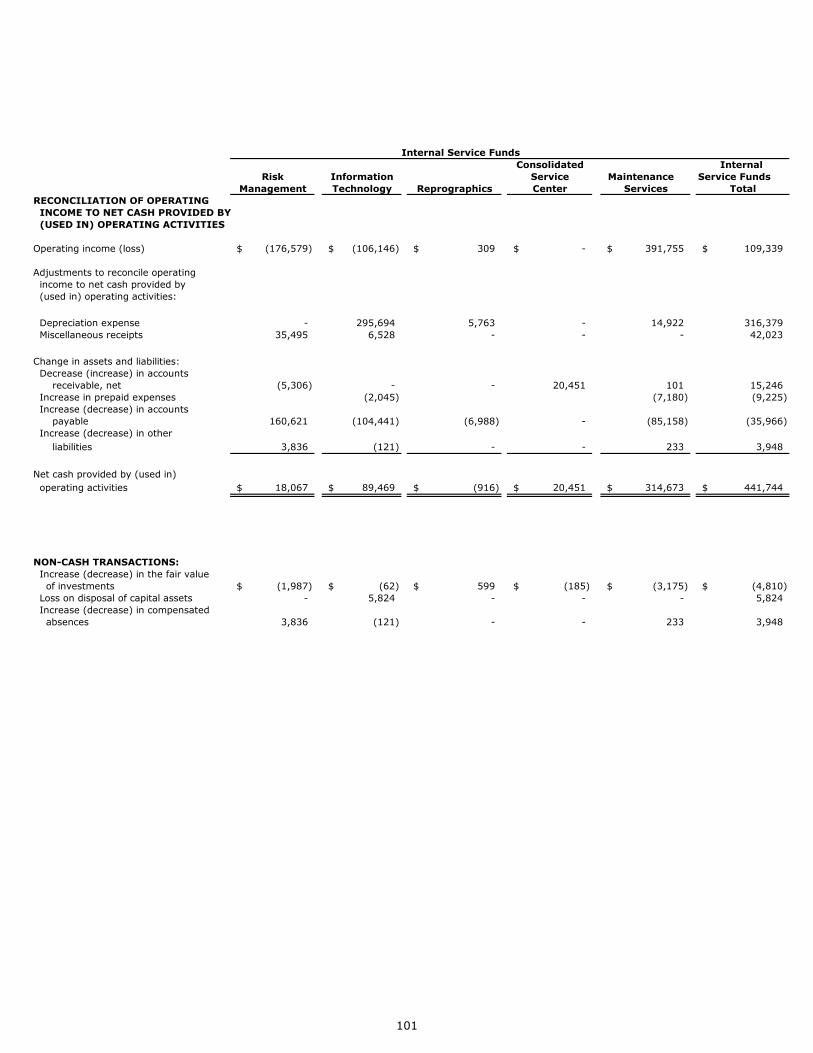

Combining Statement of Cash Flows – Internal Service Funds 100

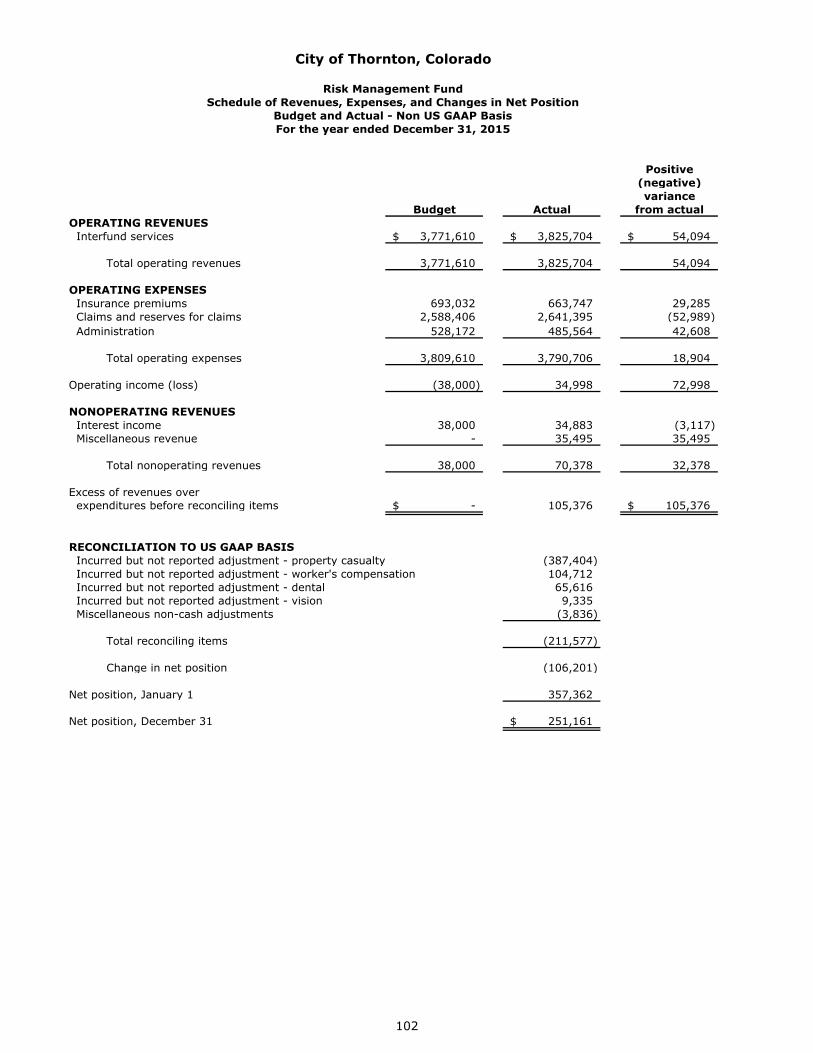

Risk Management Fund Schedule of Revenues, Expenses, and Changes in Net Position – Budget and Actual

– Non US GAAP Basis 102

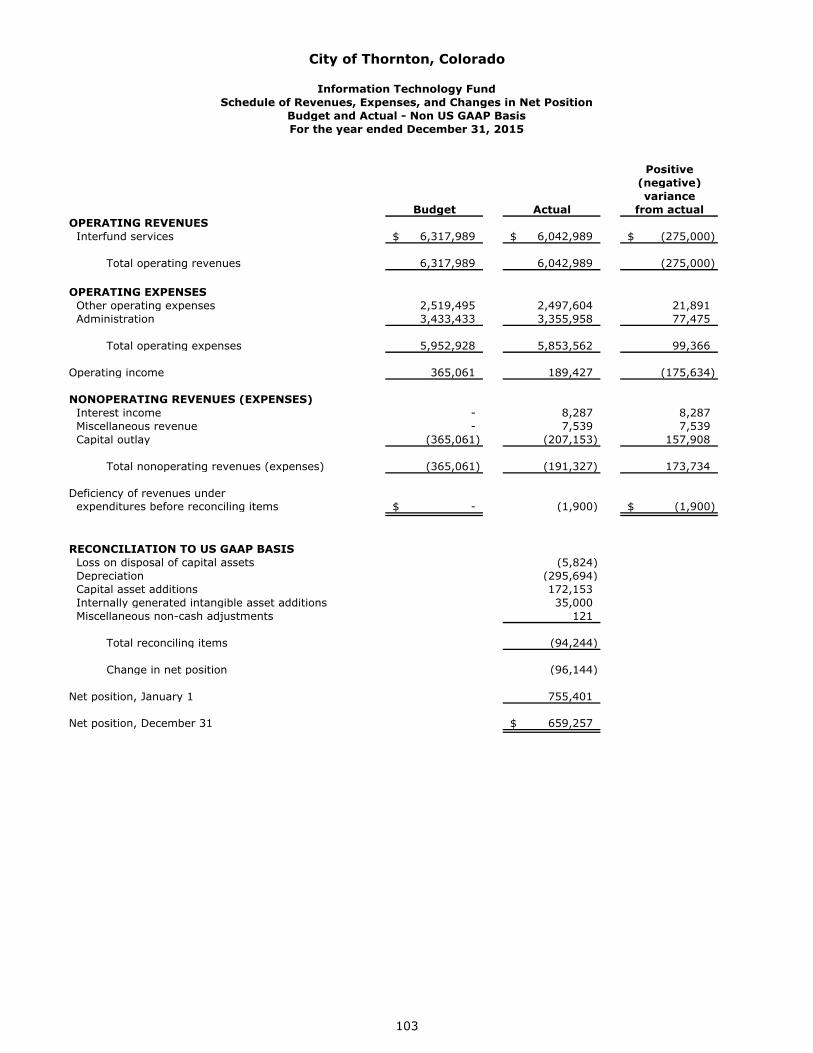

Information Technology Fund Schedule of Revenues, Expenses, and Changes in Net Position – Budget and Actual

– Non US GAAP Basis 103

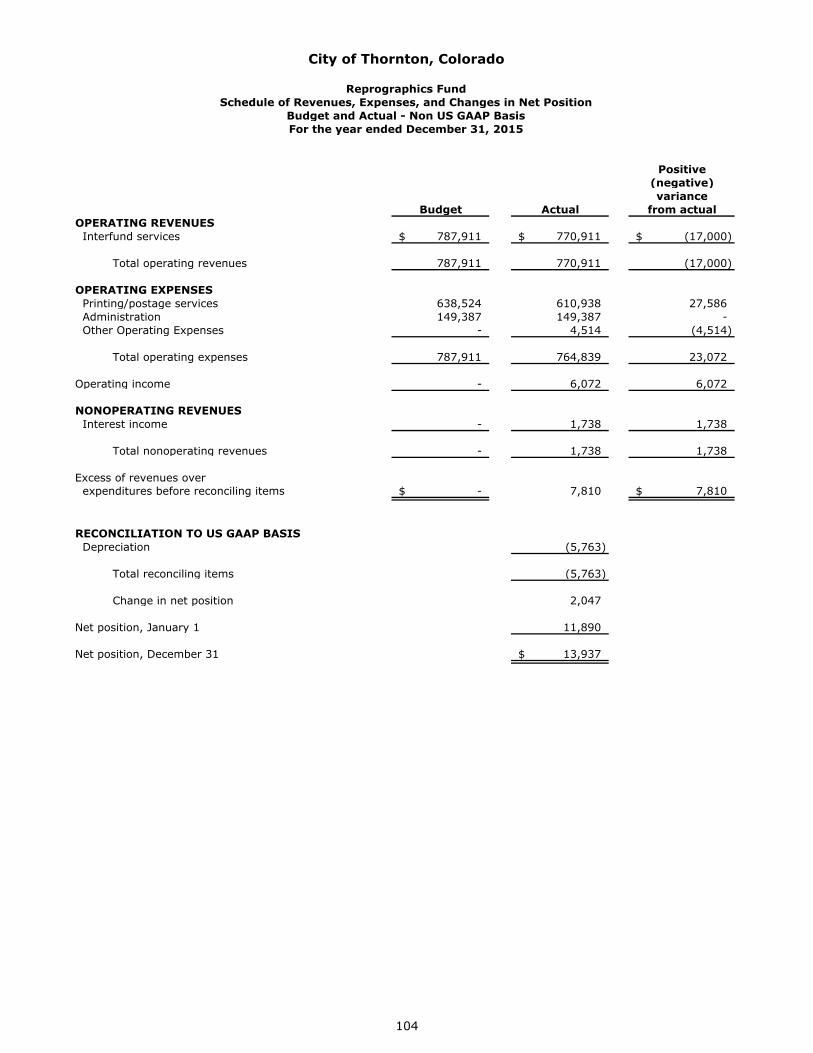

Reprographics Fund Schedule of Revenues, Expenses, and Changes in Net Position – Budget and Actual

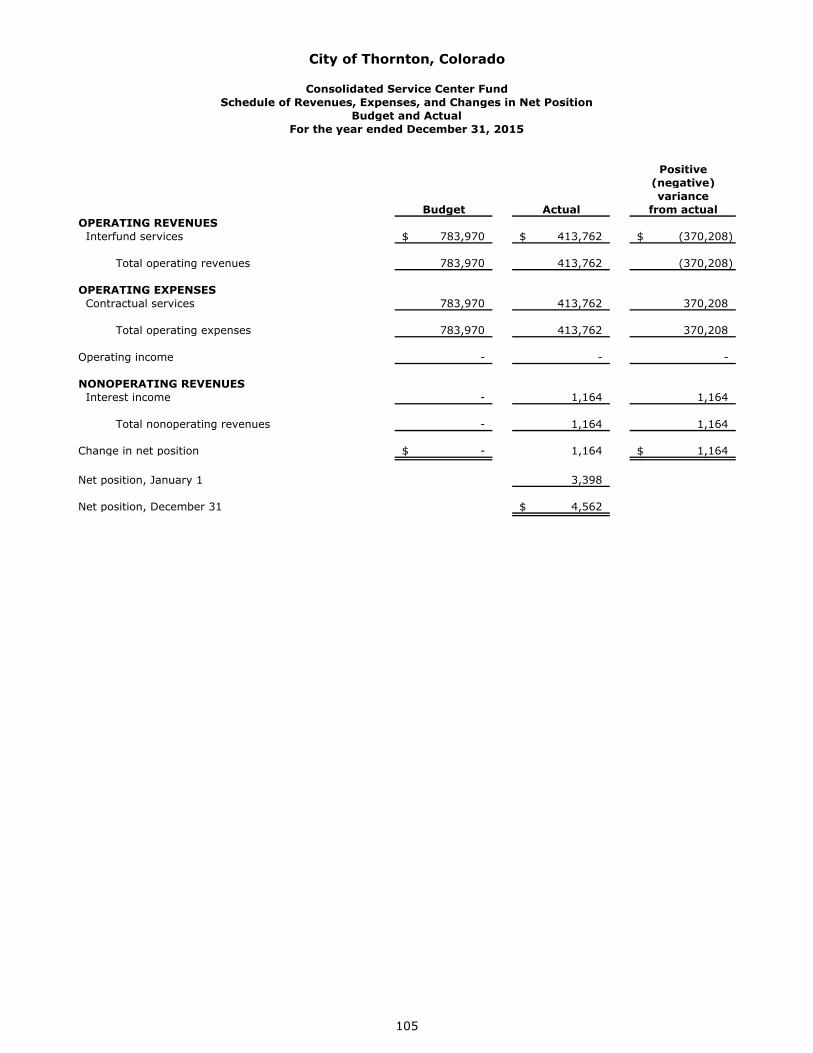

– Non US GAAP Basis 104 Consolidated Service Center Fund

Schedule of Revenues, Expenses, and Changes in Net Position – Budget and Actual 105

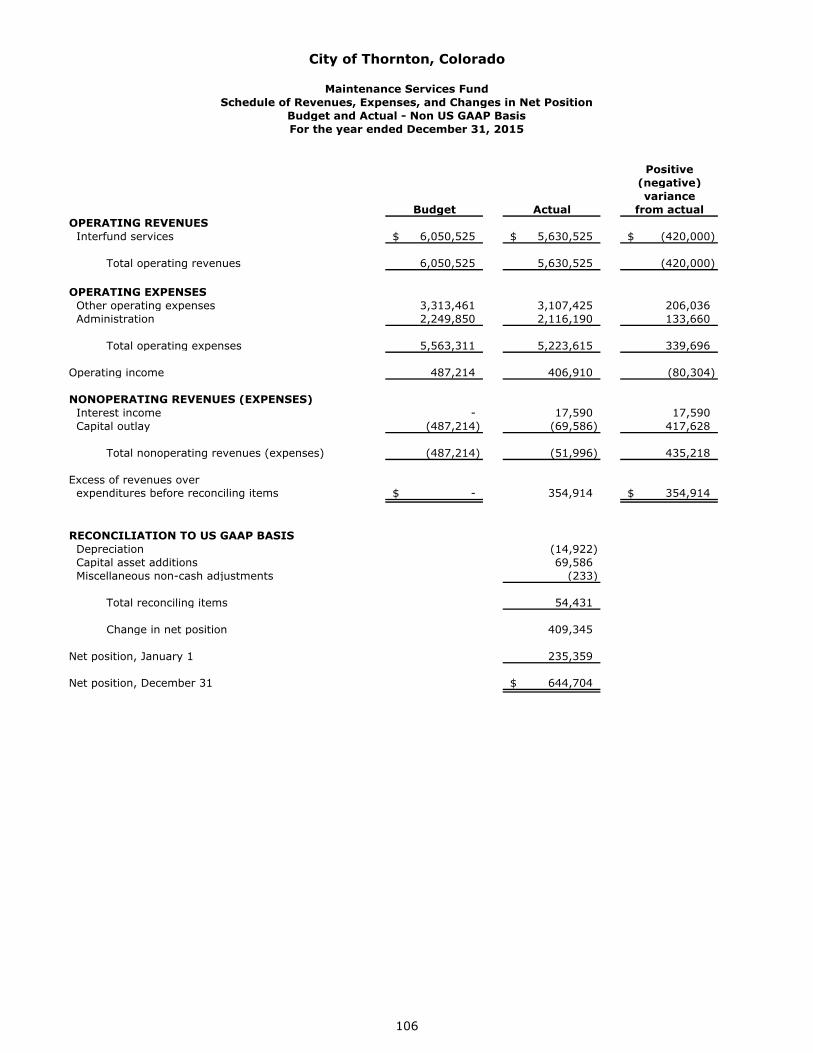

Maintenance Services Fund Schedule of Revenues, Expenses, and Changes in Net Position – Budget and Actual

– Non US GAAP Basis 106 Other Schedules

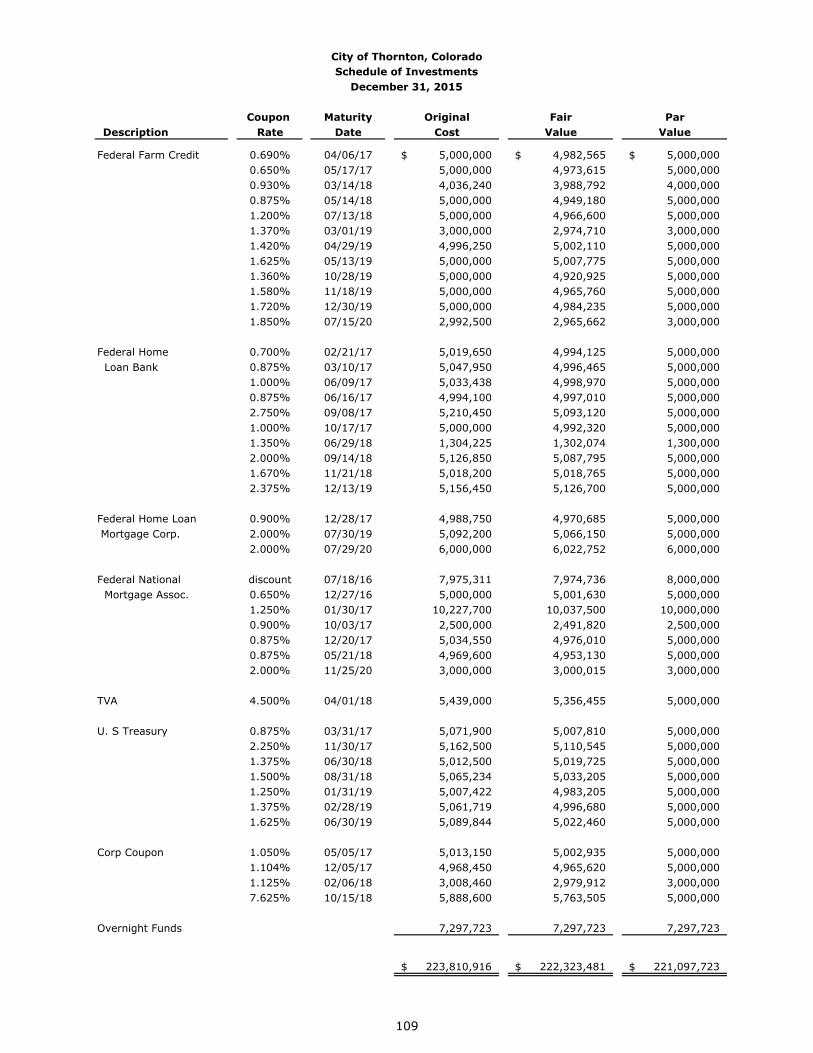

Schedule of Investments 109

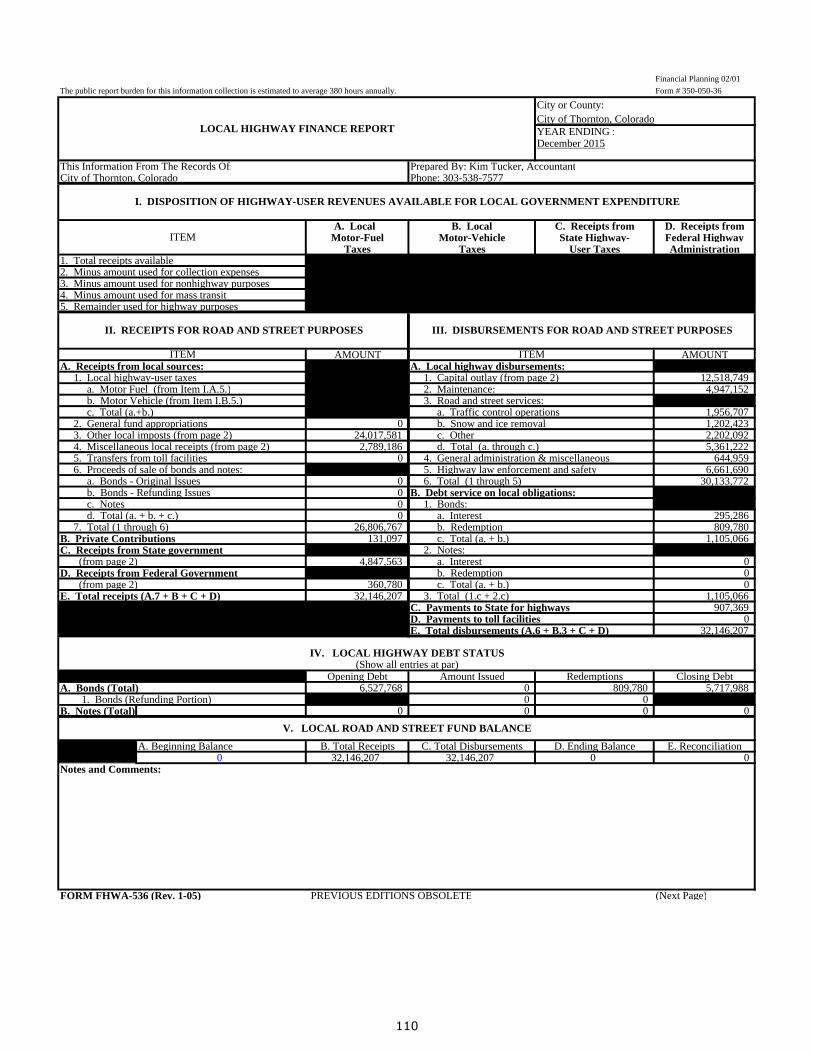

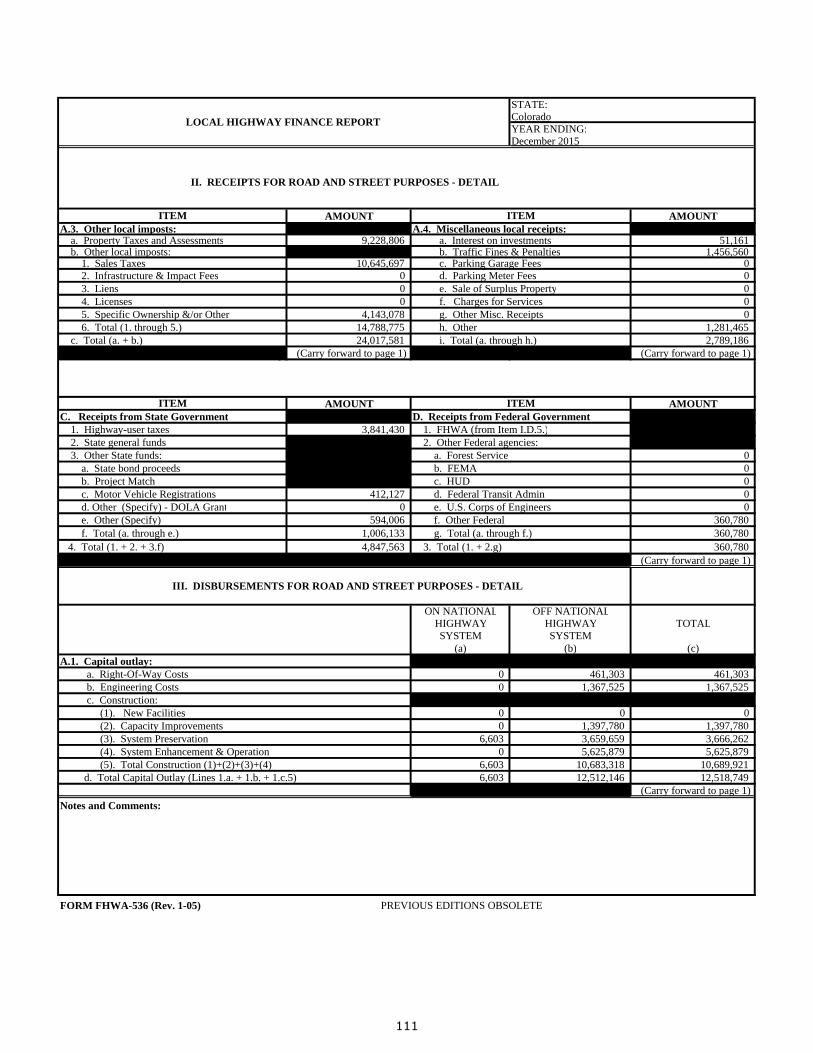

Local Highway Finance Report 110

Statistical Section (Un-audited)

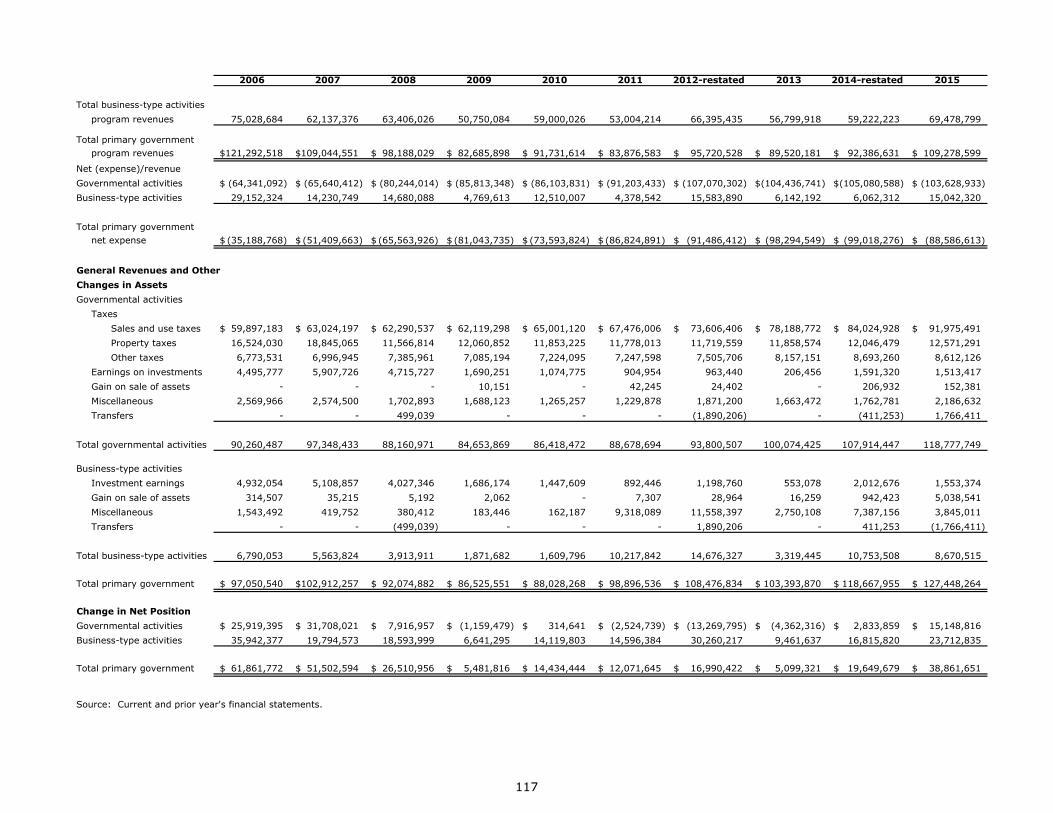

Schedule 1 – Net Position by Component 115

Schedule 2 – Changes in Net Position 116

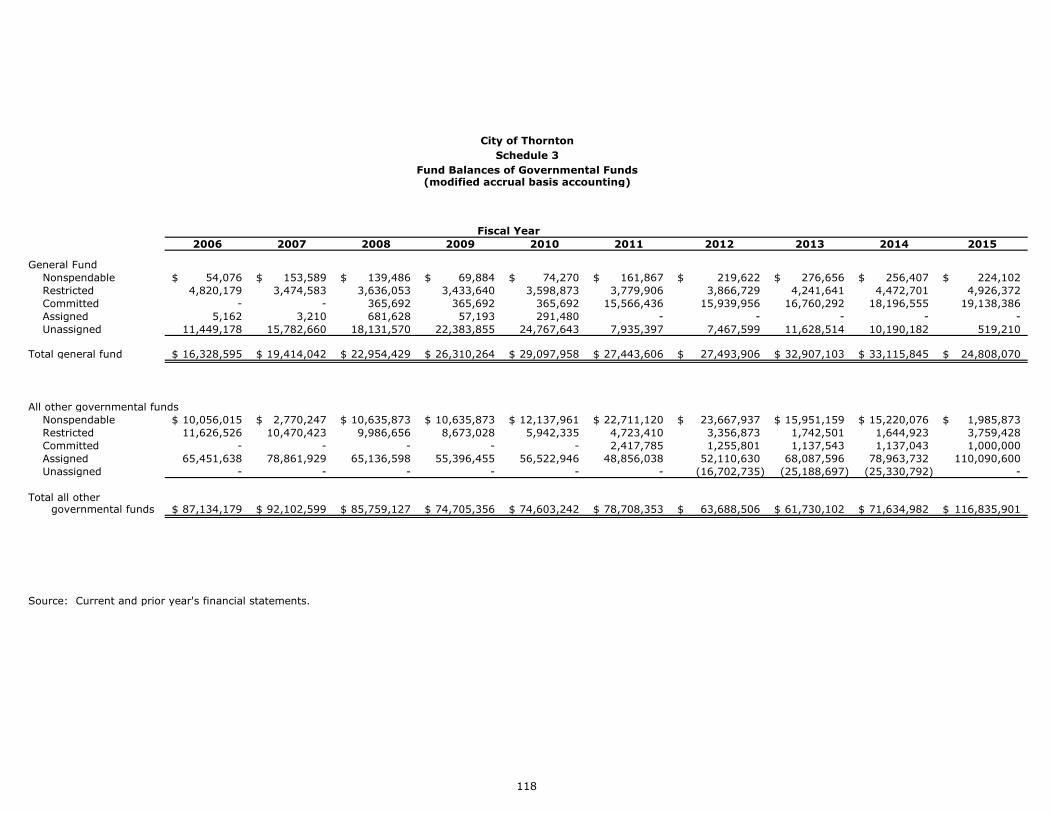

Schedule 3 – Fund Balances of Governmental Funds 118

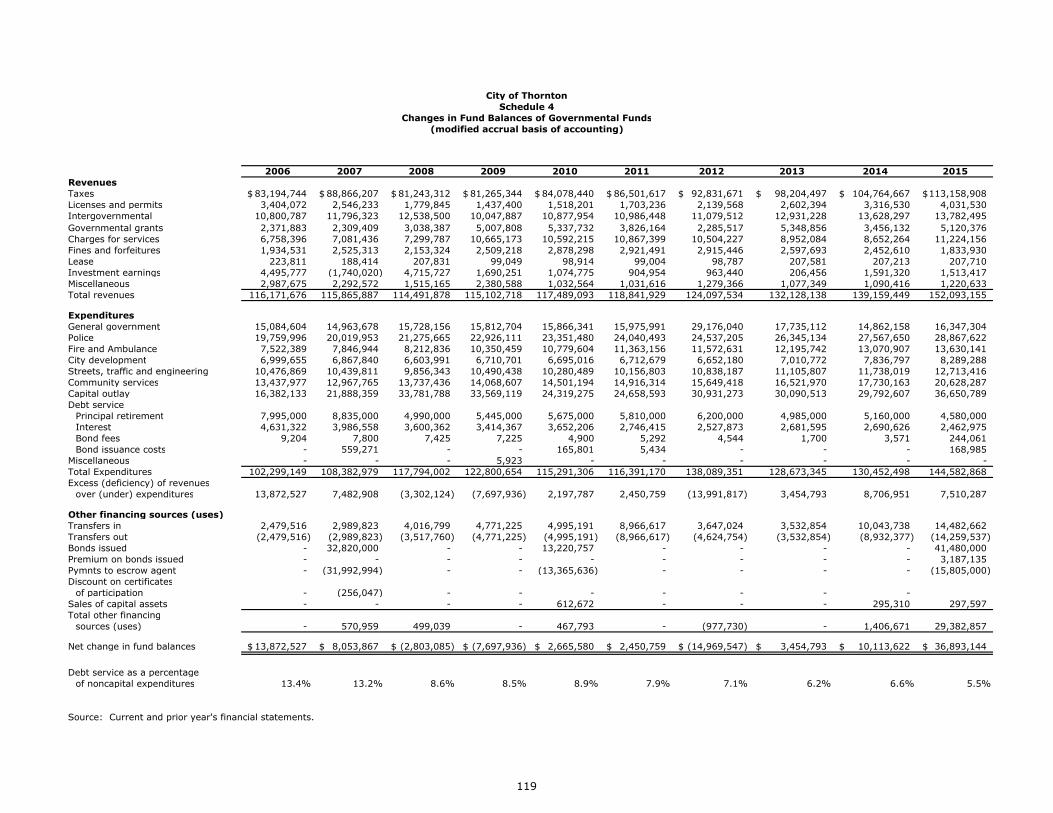

Schedule 4 - Changes in Fund Balances of Governmental Funds 119

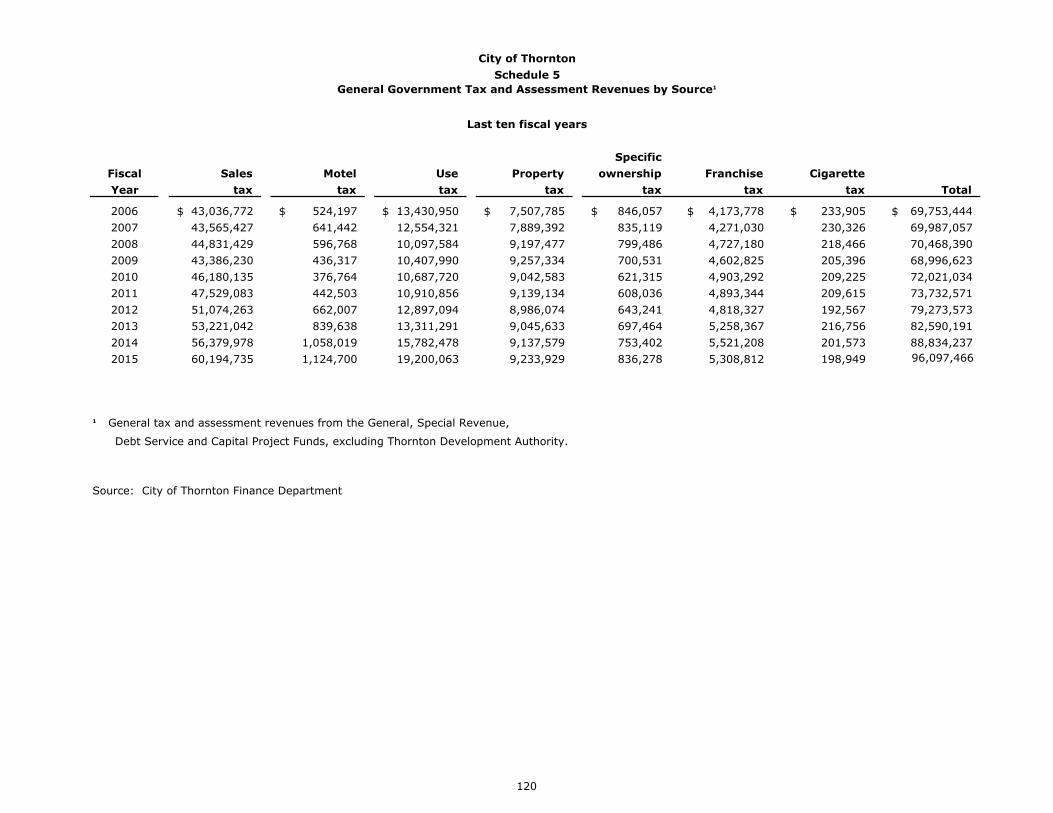

Schedule 5 – General Government Tax and Assessment Revenues by Source 120

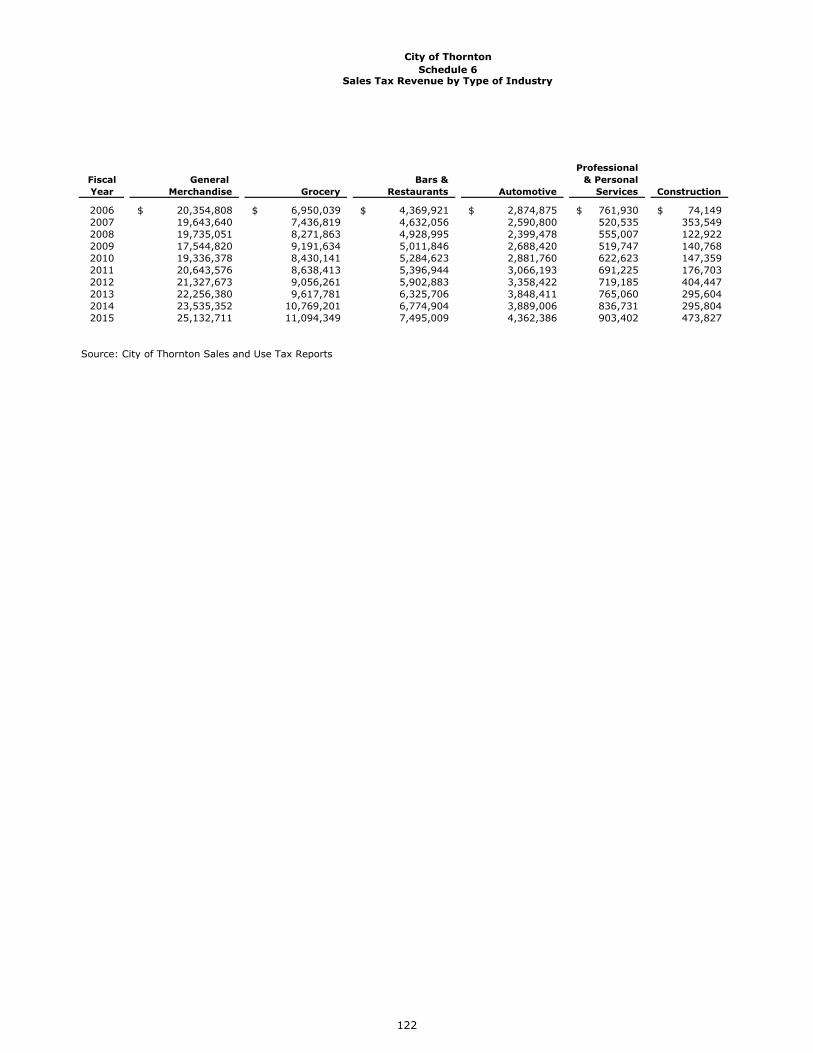

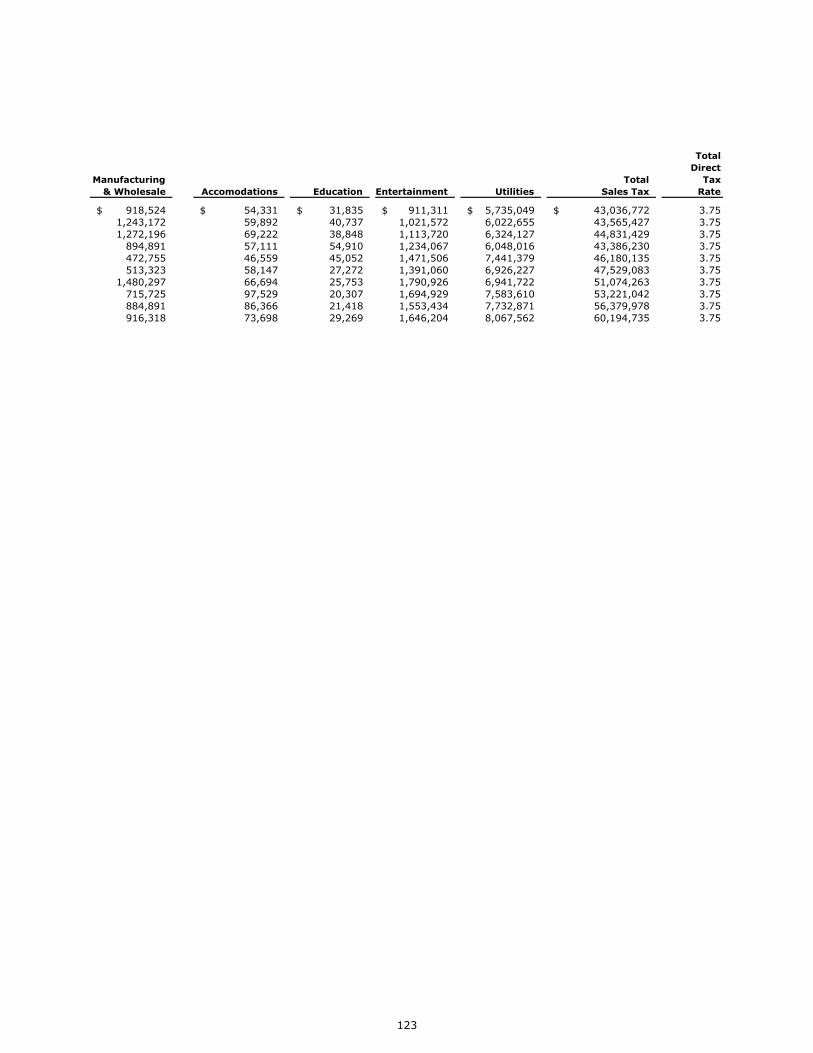

Schedule 6 – Sales Tax Revenue by Type of Industry 122

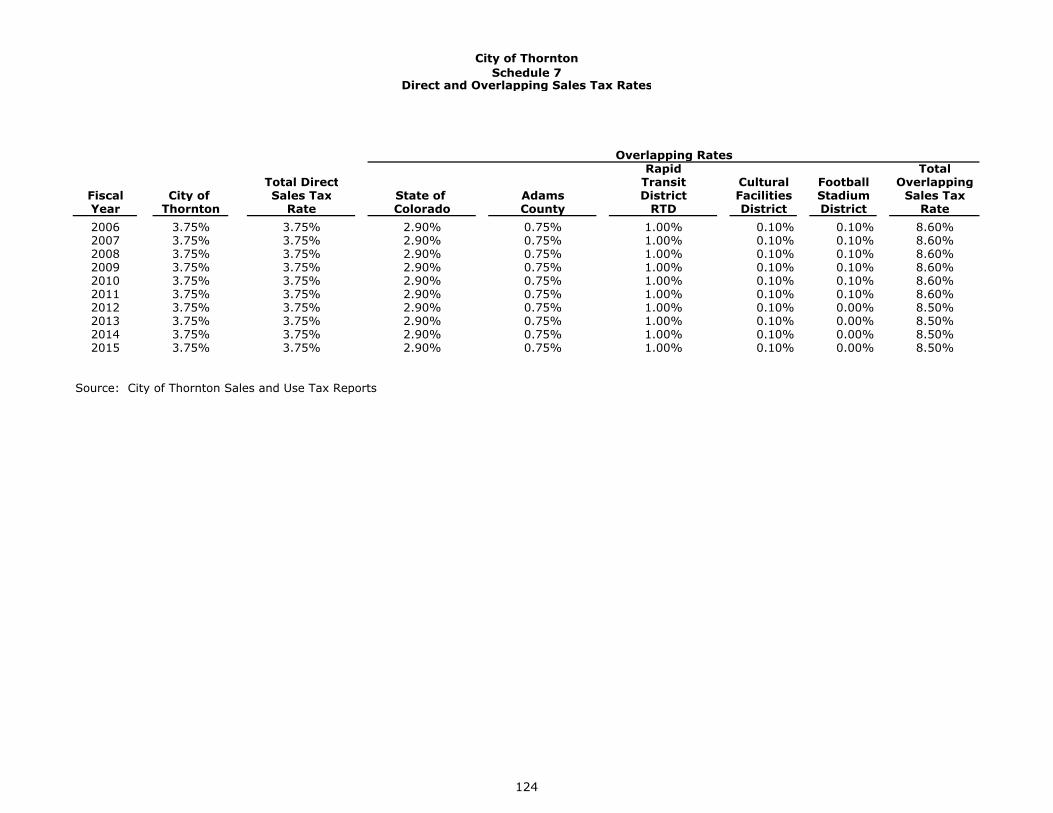

Schedule 7 – Direct and Overlapping Sales Tax Rates 124

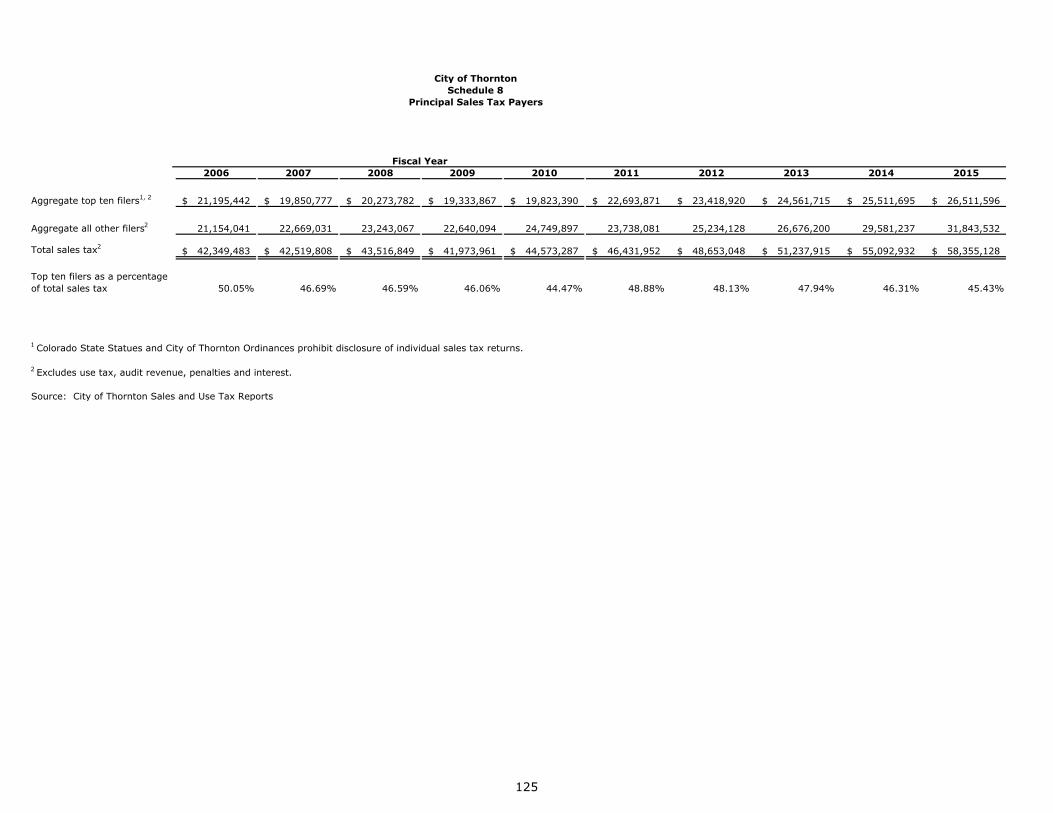

Schedule 8 – Principal Sales Taxpayers 125

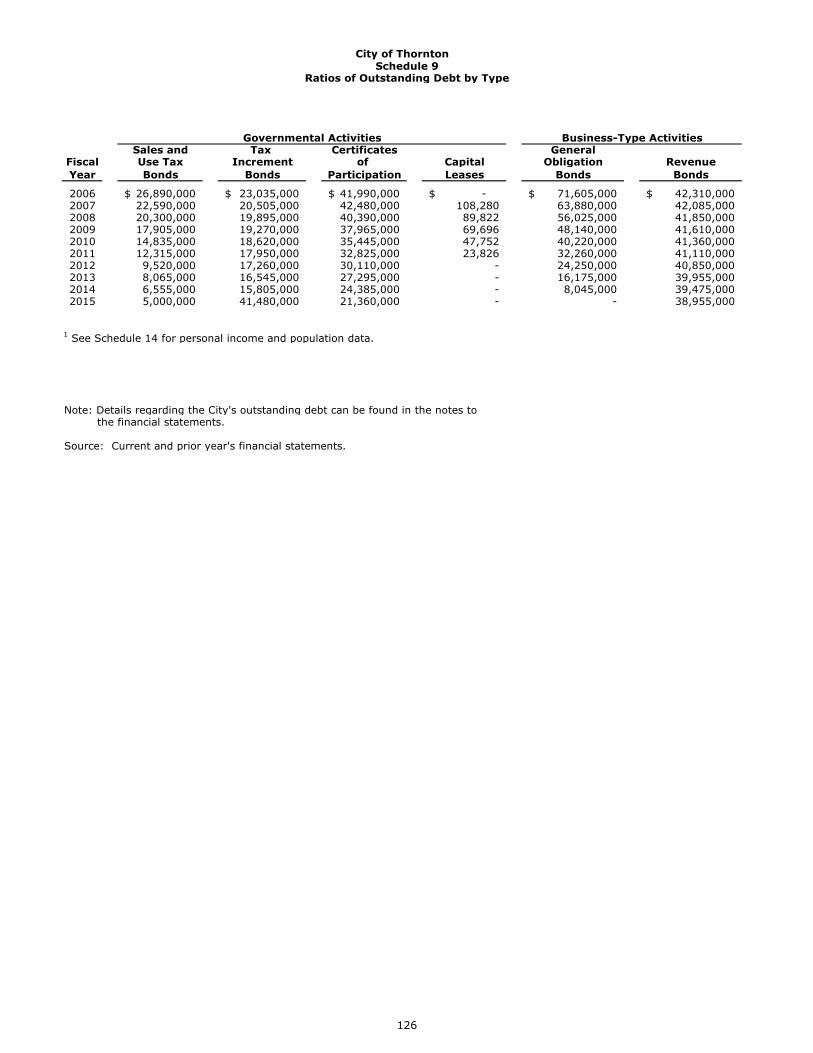

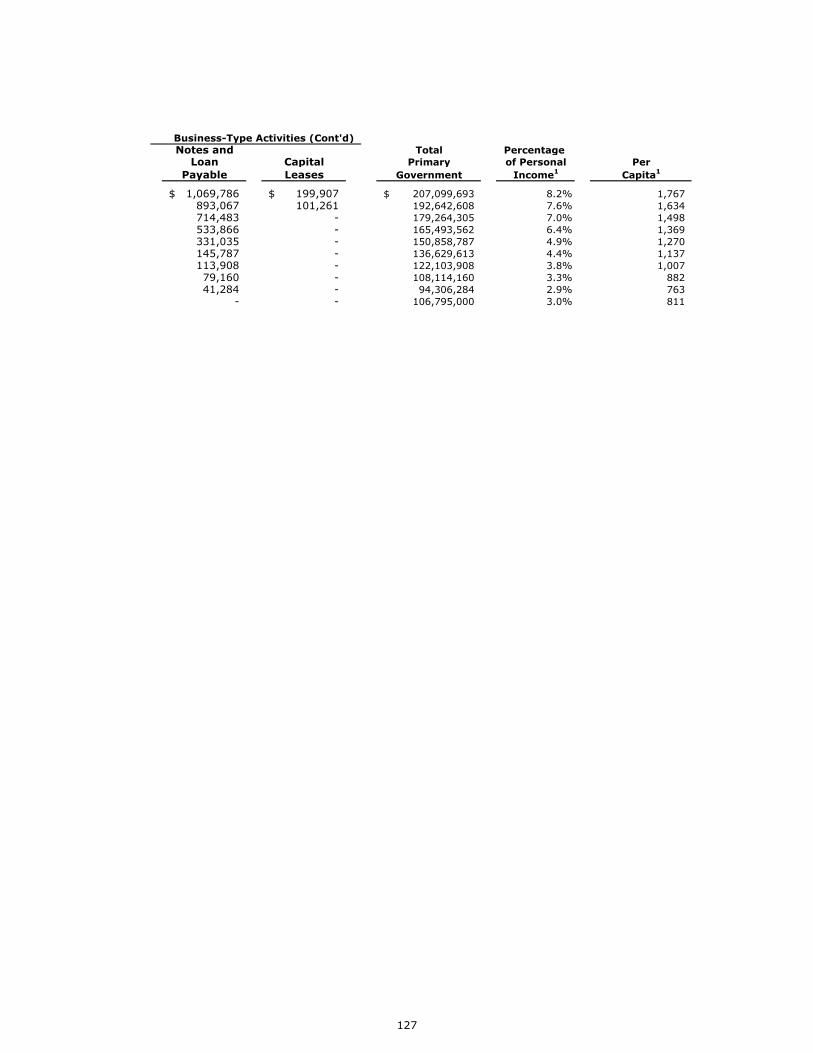

Schedule 9 – Ratios of Outstanding Debt by Type 126

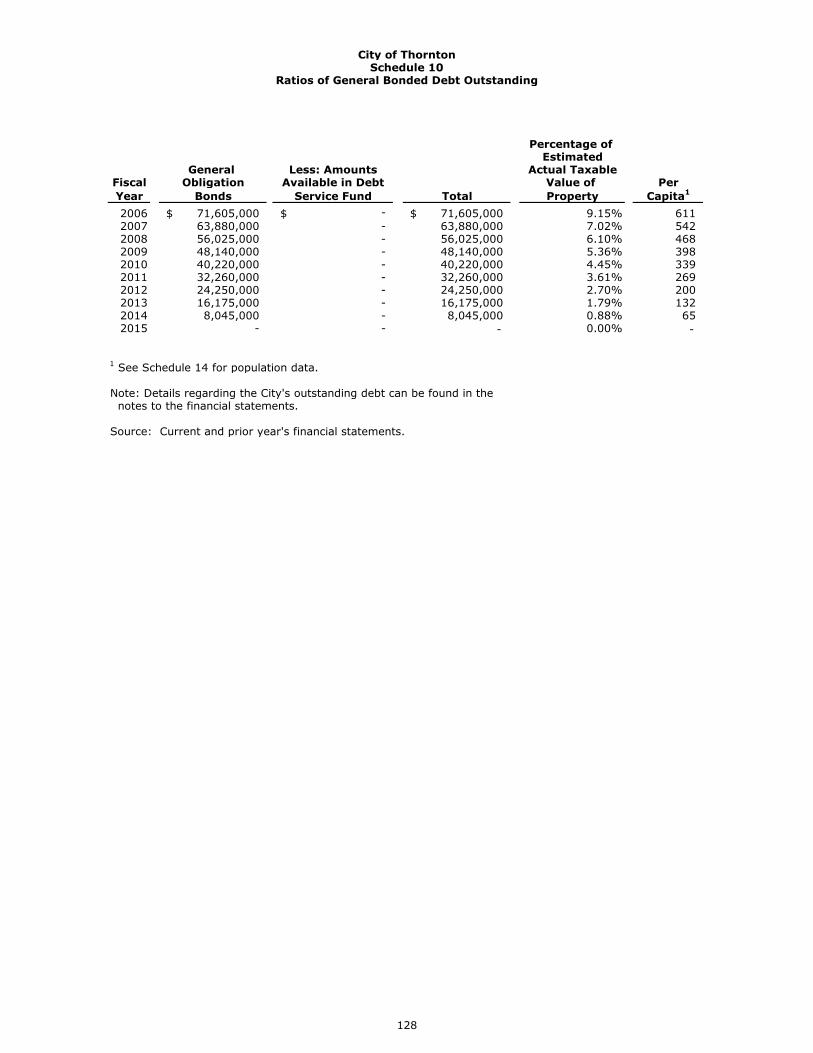

Schedule 10 – Ratios of General Bonded Debt Outstanding 128

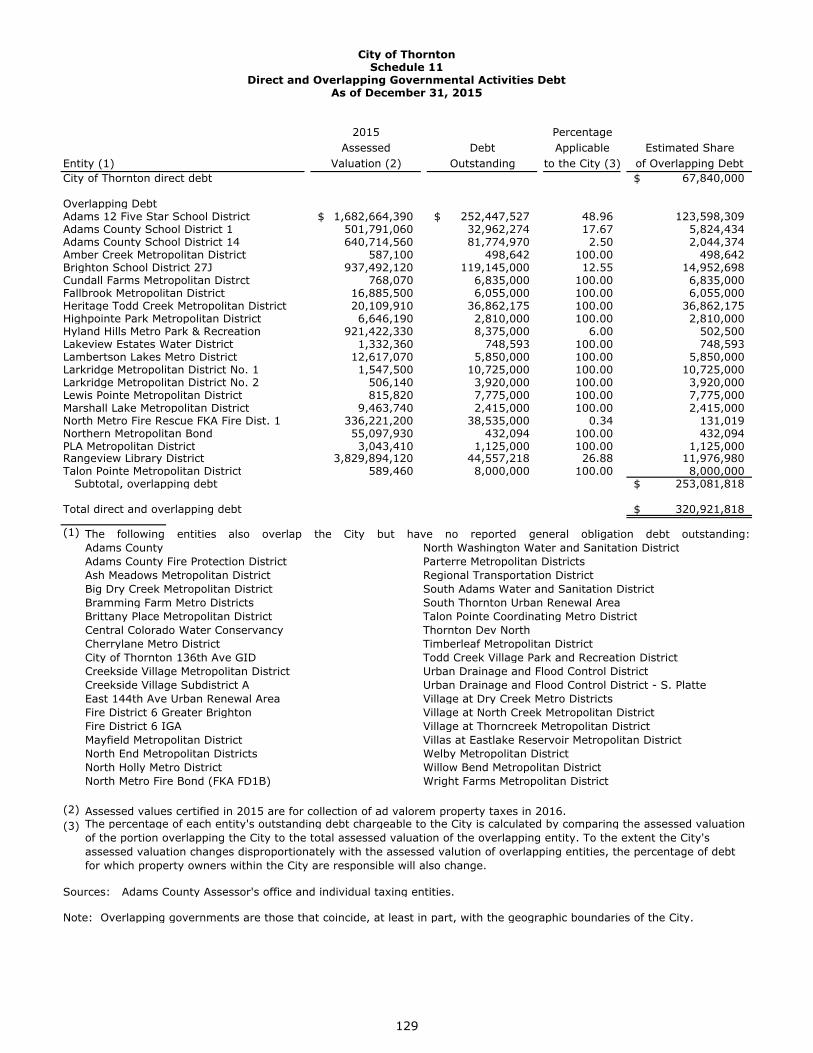

Schedule 11 – Direct and Overlapping Governmental Activities Debt 129

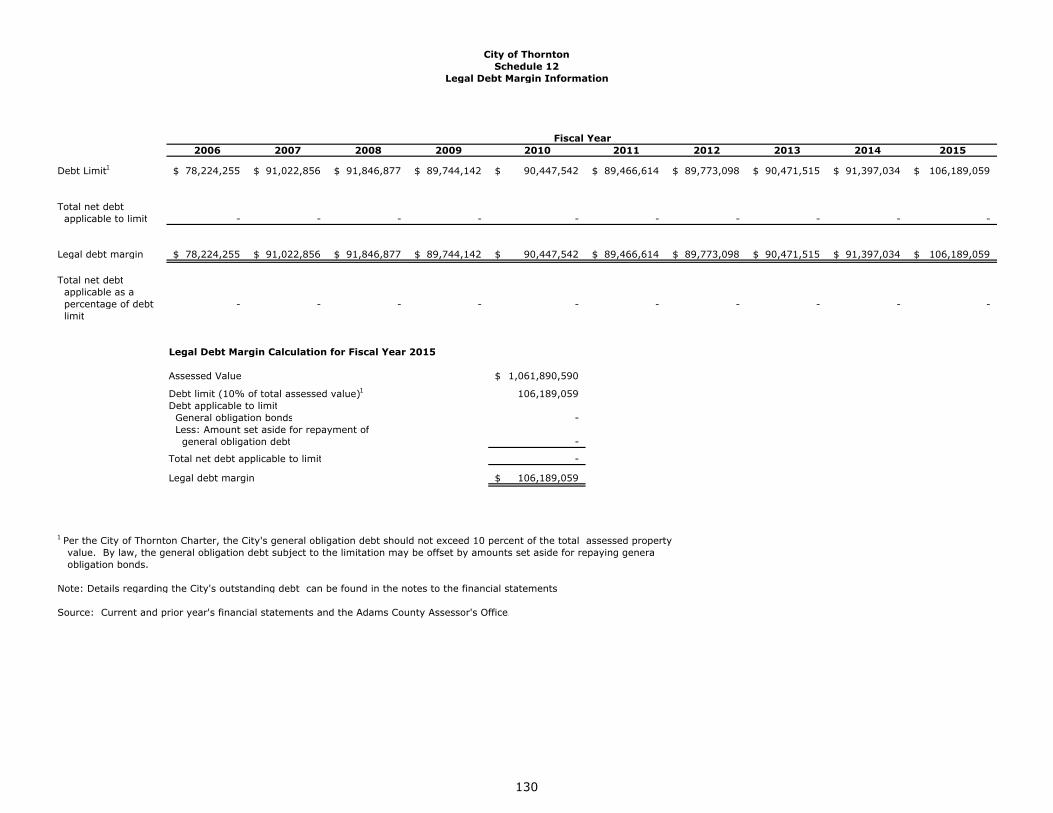

Schedule 12 – Legal Debt Margin Information 130

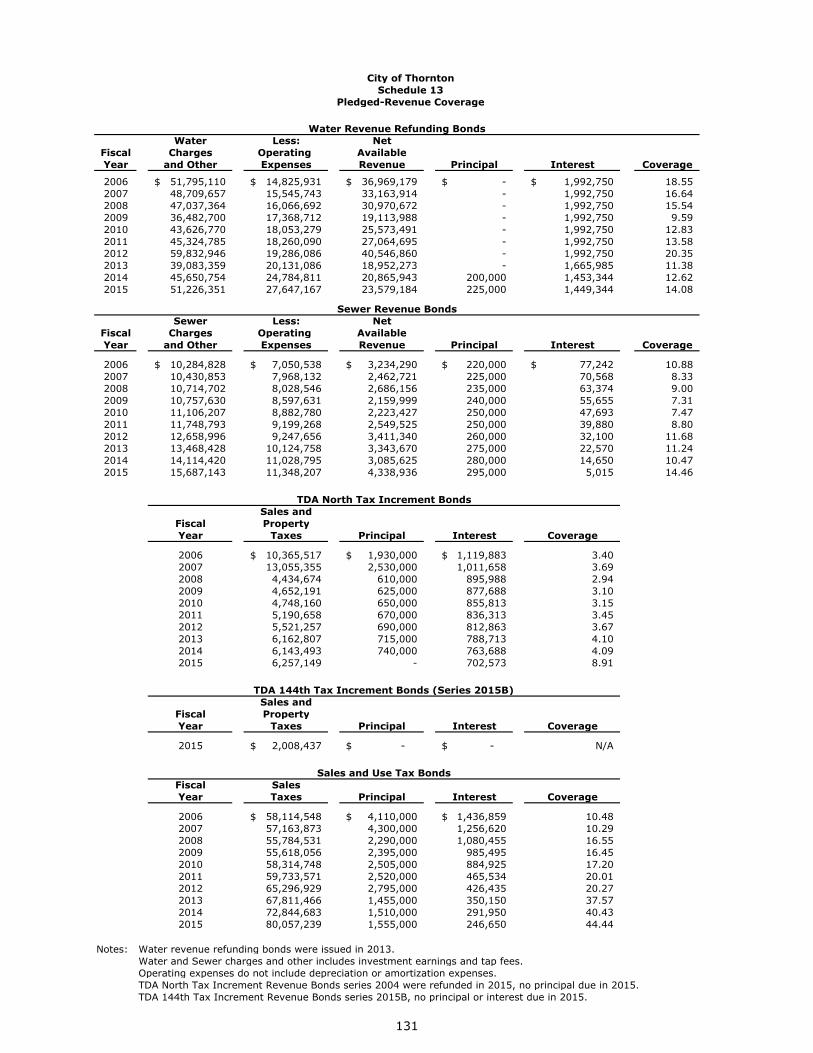

Schedule 13 – Pledged-Revenue Coverage 131

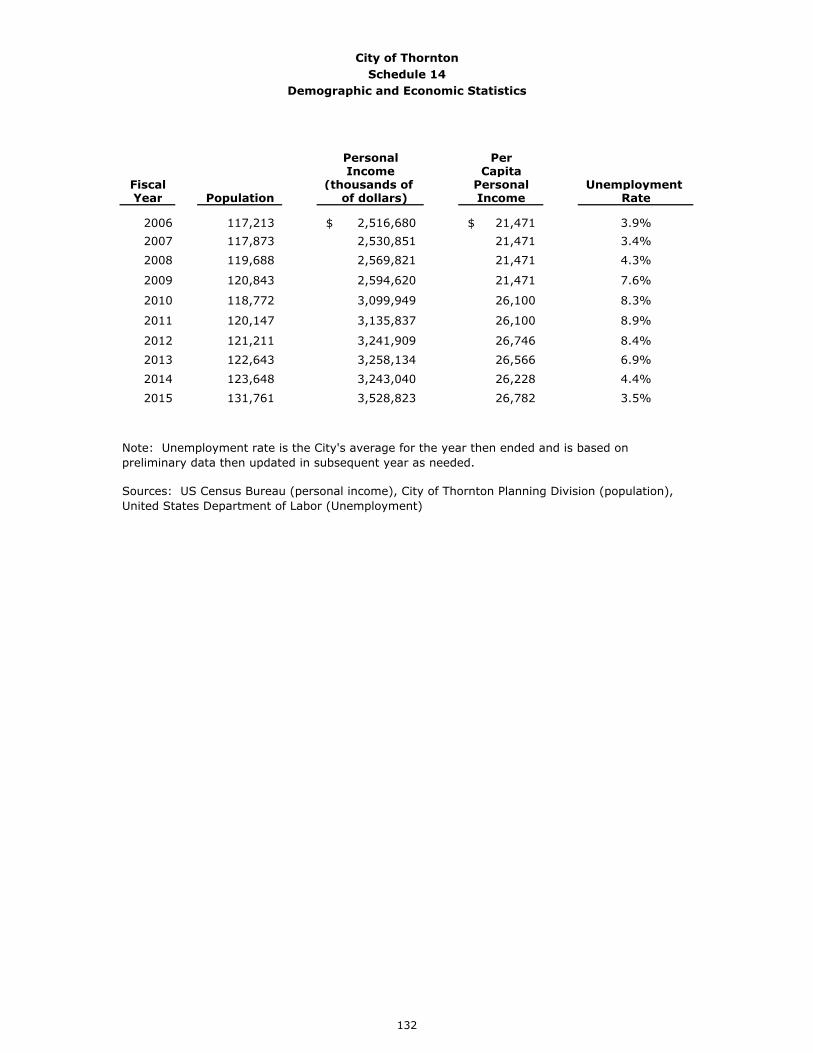

Schedule 14 – Demographic and Economic Statistics 132

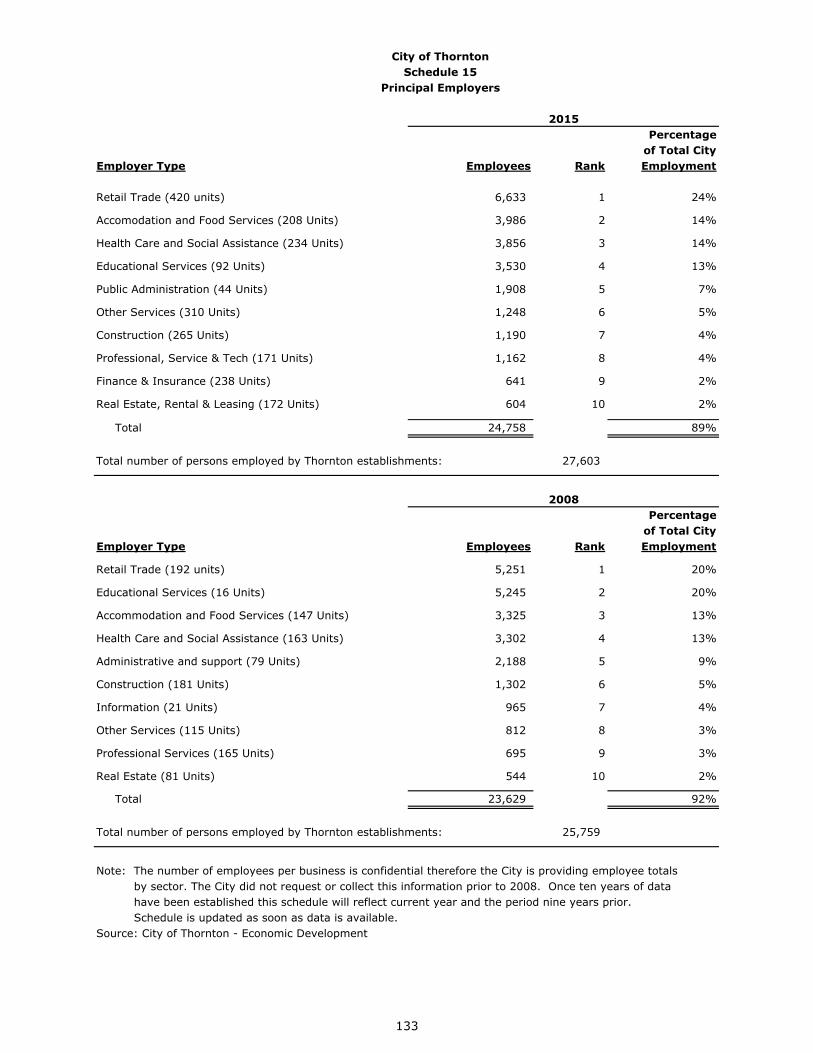

Schedule 15 – Principal Employers 133

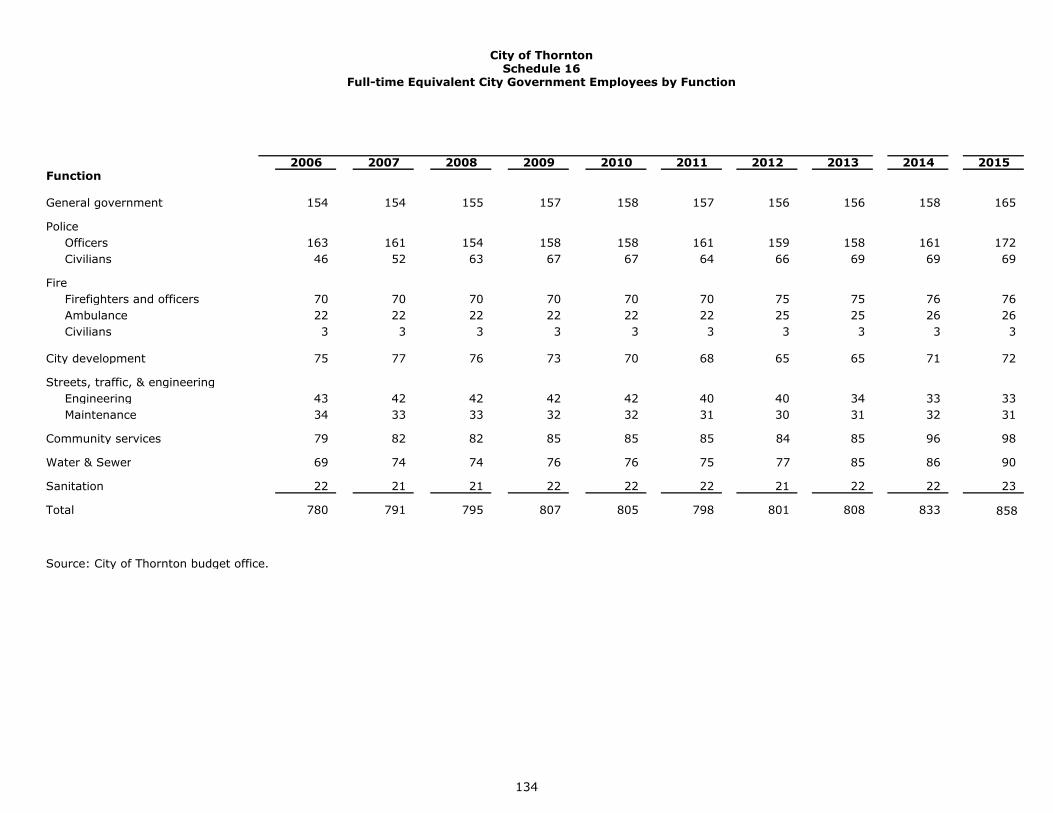

Schedule 16 – Full-time Equivalent City Government Employees by Function 134

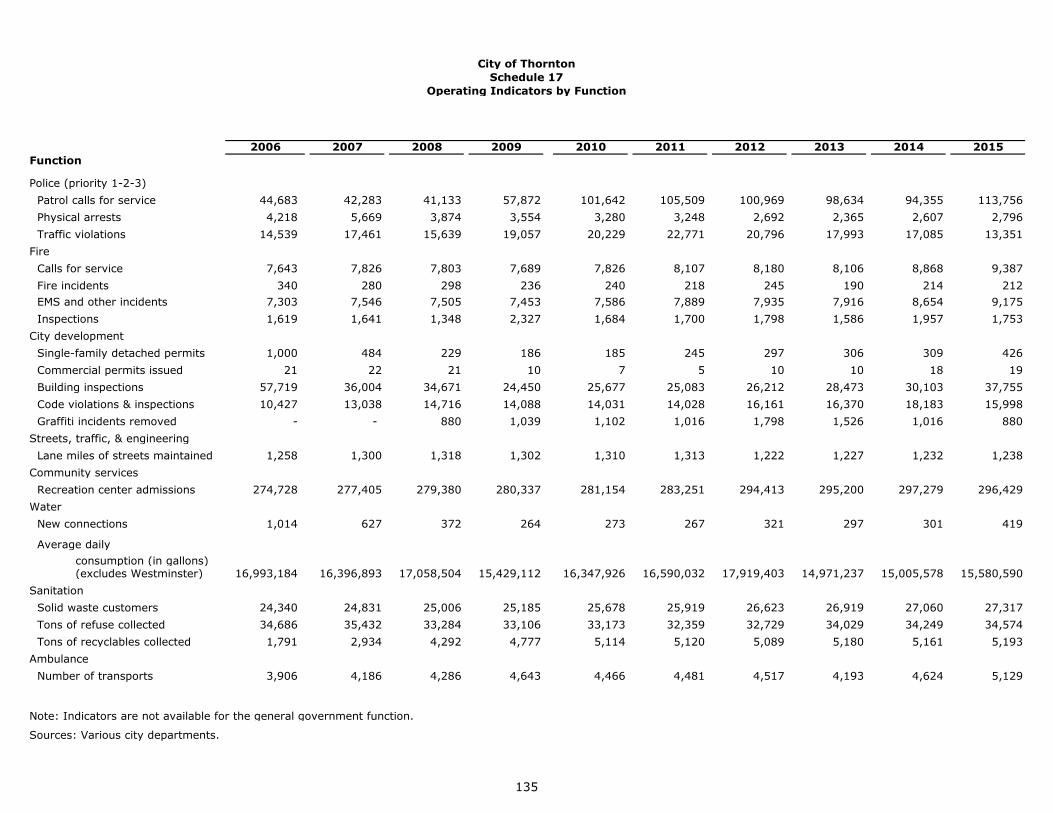

Schedule 17 – Operating Indicators by Function 135

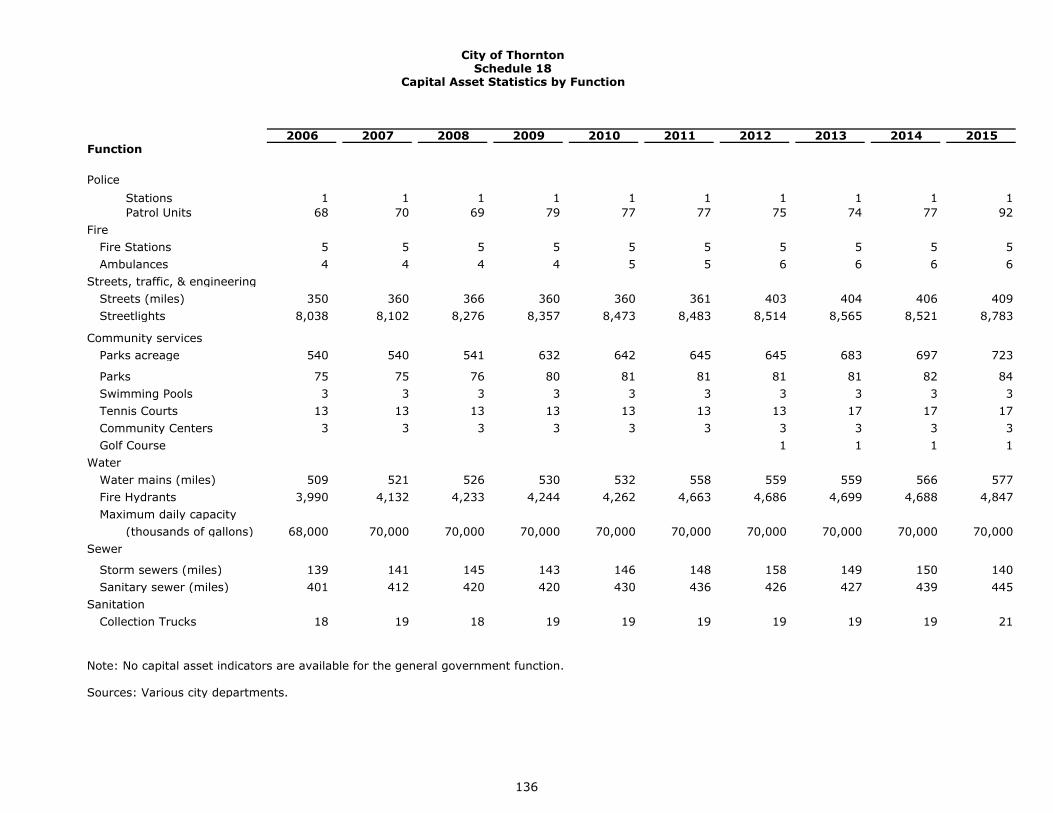

Schedule 18 – Capital Asset Statistics by Function 136

iii

This Page Left Intentionally Blank

iv

v

x

vi

vii

viii

ix

Thornton City Officials December 31, 2015

Mayor and City Council

Mayor Heidi K. Williams

Council Members Ward 1 Mack Goodman Ward 1 Jacque Phillips Ward 2 Eric Montoya Ward 2 Val Vigil Ward 3 Sam Nizam Ward 3 Josh Zygielbaum Ward 4 Janifer Kulmann Ward 4 Adam Matkowsky

Administrative

City Manager Jack Ethredge

City Attorney Margaret Emerich

Municipal Judge Charles Rose

Assistant City Manager Joyce Hunt

Deputy City Manager – City Development Jeff Coder

Deputy City Manager – Infrastructure Bud Elliot

Assistant Executive Director – Infrastructure Brett Henry

Deputy City Manager – Management Services Charlie Long

Assistant Executive Director – Management Services Chris Molison

Executive Director – Community Services Mike Soderberg

Executive Director – Police Randy Nelson

Executive Director – Fire Gordie Olson

Director – Economic Development John Cody

Director – Finance Maria Ostrom

Director – Management and Budget Robb Kolstad

City Clerk Nancy Vincent

Director – Communications Todd Barnes

x

xi

xii

www.eidebai l ly.com

440 Indiana St., Ste. 200 | Golden, CO 80401-5021 | TF 877.882.7929 | T 303.986.2454 | F 303.980.5029 | EOE

1

Independent Auditor’s Report

To the Mayor and City Council City of Thornton, Colorado

Report on the Financial Statements We have audited the accompanying financial statements of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City of Thornton, Colorado, as of and for the year ended December 31, 2015, and the related notes to the financial statements, which collectively comprise the City’s basic financial statements as listed in the table of contents.

Management’s Responsibility for the Financial Statements Management is responsible for the preparation and fair presentation of these financial statements in accordance with accounting principles generally accepted in the United States of America; this includes the design, implementation, and maintenance of internal control relevant to the preparation and fair presentation of financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility Our responsibility is to express opinions on these financial statements based on our audit. We conducted our audit in accordance with auditing standards generally accepted in the United States of America and the standards applicable to financial audits contained in Government Auditing Standards, issued by the Comptroller General of the United States. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. Accordingly, we express no such opinion. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of significant accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinions.

Opinions In our opinion, the financial statements referred to above present fairly, in all material respects, the respective financial position of the governmental activities, the business-type activities, each major fund, and the aggregate remaining fund information of the City of Thornton, Colorado, as of December 31, 2015, and the respective changes in financial position and, where applicable, cash flows thereof for the year then ended in accordance with accounting principles generally accepted in the United States of America.

2

Adoption of New Accounting Standard As described in Note A to the financial statements, the City of Thornton has adopted the provisions of GASB Statement No. 68, Accounting and Financial Reporting for Pensions and GASB Statement No. 71, Pension Transition for Contributions Made Subsequent to the Measurement Date, which has resulted in a restatement of the net position as of January 1, 2015. Our opinions are not modified with respect to this matter.

Other Matters

Required Supplementary Information Accounting principles generally accepted in the United States of America require that management’s discussion and analysis, budgetary comparisons and pension information on pages 5 through 12, 58 through 59, and 60 through 64, be presented to supplement the basic financial statements. Such information, although not a part of the basic financial statements, is required by the Governmental Accounting Standards Board, who considers it to be an essential part of financial reporting for placing the basic financial statements in an appropriate operational, economic, or historical context. We have applied certain limited procedures to the required supplementary information in accordance with auditing standards generally accepted in the United States of America, which consisted of inquiries of management about the methods of preparing the information and comparing the information for consistency with management’s responses to our inquiries, the basic financial statements, and other knowledge we obtained during our audit of the basic financial statements. We do not express an opinion or provide any assurance on the information because the limited procedures do not provide us with sufficient evidence to express an opinion or provide any assurance.

Other Information Our audit was conducted for the purpose of forming opinions on the financial statements that collectively comprise the City of Thornton, Colorado’s financial statements. The introductory section, combining nonmajor fund financial statements, individual budget schedules, schedule of investments, Local Highway Finance Report, and statistical tables are presented for purposes of additional analysis and are not a required part of the basic financial statements.

The combining nonmajor fund financial statements, budget schedules, schedule of investments and Local Highway Finance Report on pages 68 through 111 were derived from and relate directly to the underlying accounting and other records used to prepare the basic financial statements. Such information has been subjected to the auditing procedures applied in the audit of the financial statements and certain additional procedures, including comparing and reconciling such information directly to the underlying accounting and other records used to prepare the financial statements or to the financial statements themselves, and other additional procedures in accordance with auditing standards generally accepted in the United States of America. In our opinion, this information is fairly stated in all material respects in relation to the financial statements as a whole.

The introductory and statistical sections have not been subjected to the auditing procedures applied in the audit of the basic financial statements and, accordingly, we do not express an opinion or provide any assurance on them.

3

Other Reporting Required by Government Auditing Standards In accordance with Government Auditing Standards, we have also issued our report dated May 2, 2016 on our consideration of the City of Thornton, Colorado’s internal control over financial reporting and on our tests of its compliance with certain provisions of laws, regulations, contracts, grant agreements and other matters. The purpose of that report is to describe the scope of our testing of internal control over financial reporting and compliance and the results of that testing, and not to provide an opinion on the internal control over financial reporting or on compliance. That report is an integral part of an audit performed in accordance with Government Auditing Standards in considering the City of Thornton’s internal control over financial reporting and compliance.

Golden, Colorado May 2, 2016

This Page Left Intentionally Blank

4

City of Thornton, Colorado Management’s Discussion and Analysis

December 31, 2015

As management of the City of Thornton (“the City”), we offer readers of the City’s financial statements this narrative overview and analysis of the financial activities of the City for the fiscal year ended December 31, 2015. We encourage readers to consider the information presented here in conjunction with additional information that we have furnished in our letter of transmittal at the front of this report, and the City’s financial statements which follow this section.

Financial Highlights

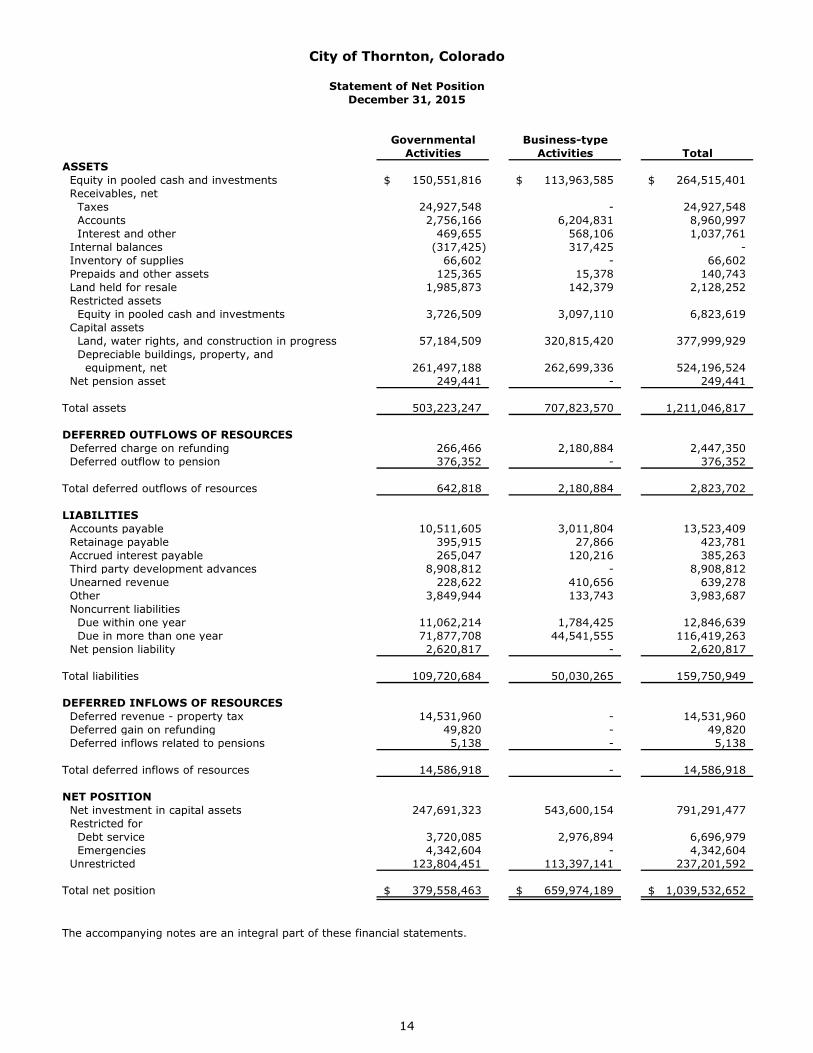

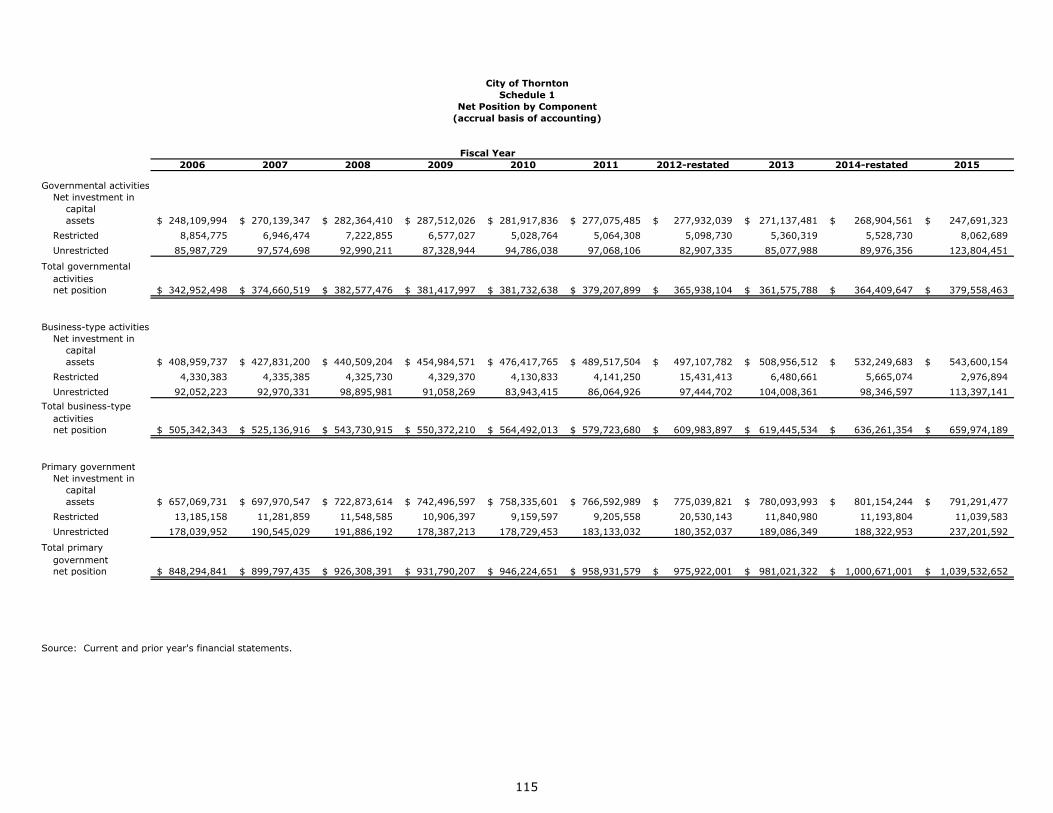

The City’s assets and deferred outflows of resources exceeded its liabilities and deferred inflows of resources atthe close of the most recent fiscal year by $1,039,532,652. This total is divided between Governmental Activitiesof $379,558,463 and Business-type Activities of $659,974,189.

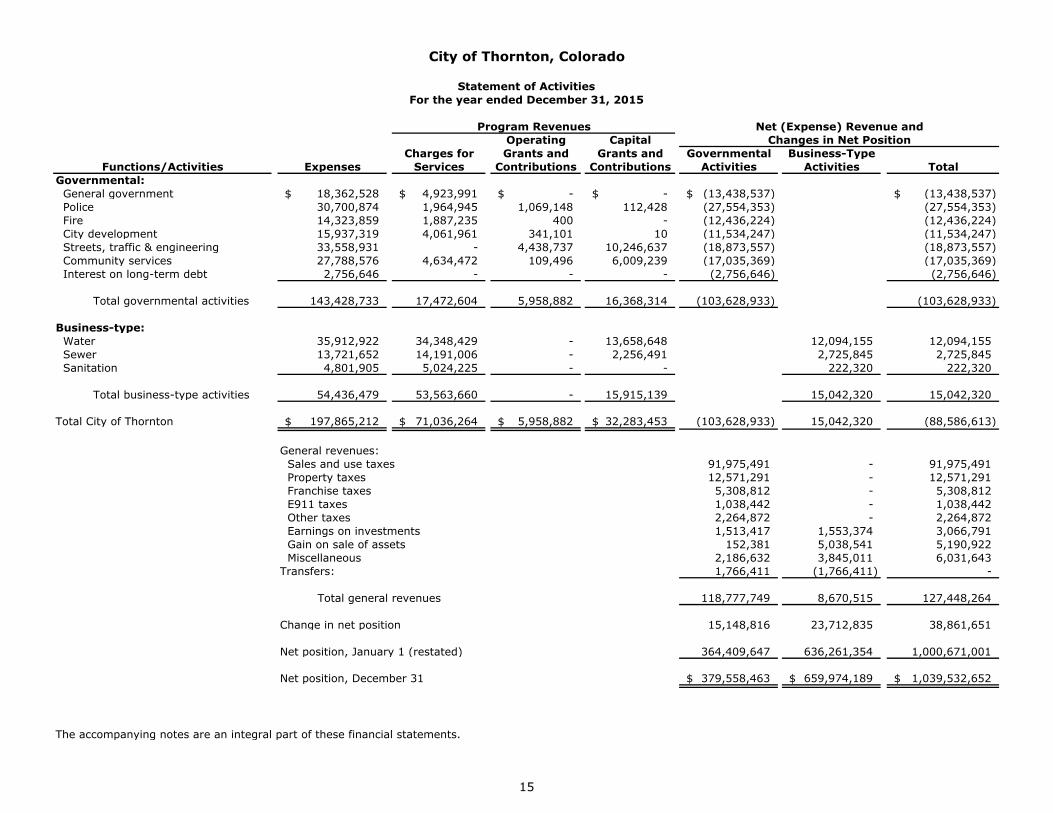

The City’s total net position increased by $38,861,651. This total is divided between an increase in GovernmentalActivities of $15,148,816 and an increase in Business-type Activities of $23,712,835.

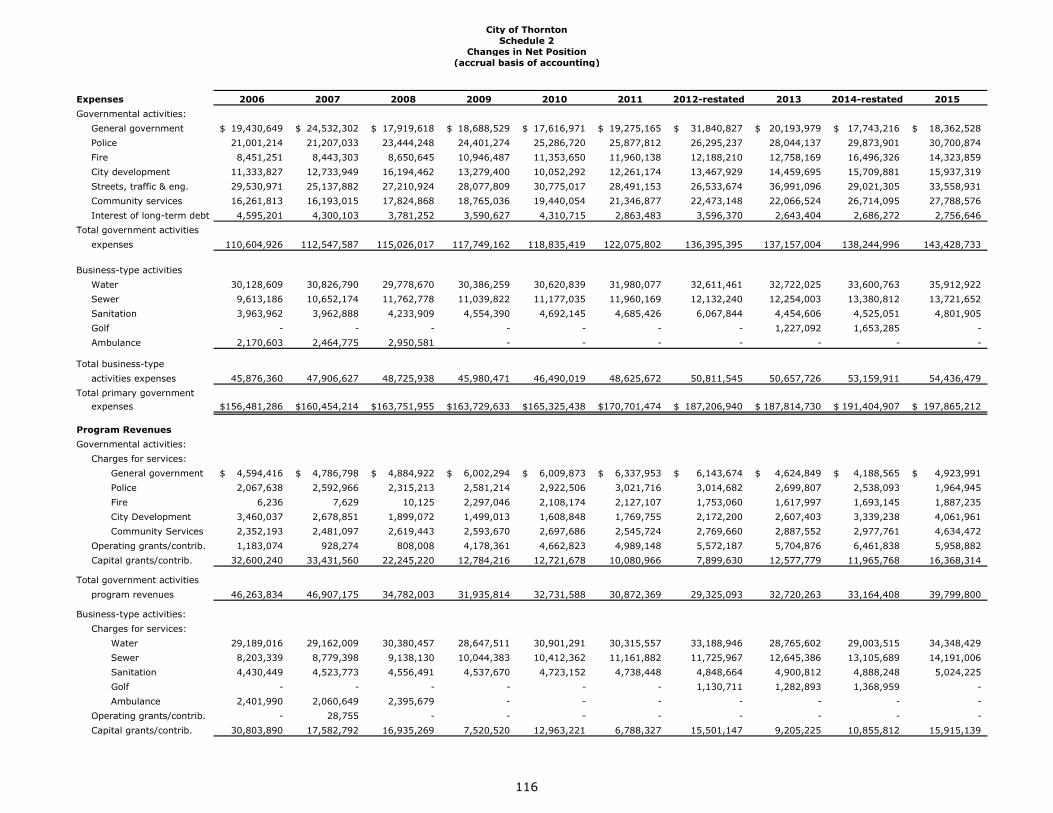

The City’s Governmental Activities show revenues of $156,811,138. The largest revenue source is sales and usetaxes ($91,975,491) followed by charges for services ($17,472,604) and capital grants and contributions($16,368,314). Charges for services consists of the administrative fee charged to the enterprise funds($4,449,136, 25.5%), recreation and related charges ($4,603,976, 26.3%), license, permits and inspection fees($4,031,530, 23.1%), fines and forfeitures ($1,833,930, 10.5%), ambulance charges ($1,859,771, 10.6%), andother miscellaneous charges ($694,261, 4.0%). The Governmental expenses were $143,428,733. More detailsare provided in the Government-wide Financial Analysis section.

The City’s Business-type Activities show revenues of $79,915,725. The largest revenue source is charges forservices ($53,563,660) followed by capital grants and contributions ($15,915,139). Capital grants andcontributions consists of payments for connections to the City’s water and sewer systems ($12,529,822, 78.7%),grants ($569,591, 3.6%), and infrastructure donated to the City by developers ($2,815,726, 17.7%). TheBusiness-type expenses were $54,436,479. More details are provided in the Government-wide Financial Analysissection.

The total fund balance for the General Fund decreased by $8,307,775, (25.1%) from prior year. City Councilpolicy requires the General Fund to maintain a total fund balance at an amount equal to specified percentages ofthe current year budget. (Catastrophic 7%, Stabilization 7%, other 3% and TABOR reserve per State Statute). Atthe end of the current fiscal year, total fund balance was $24,808,070 or 23.5% of General Fund budgetedexpenditures.

Overview of the Financial Statements

This discussion and analysis is intended to serve as an introduction to the City’s basic financial statements. The City’s basic financial statements comprise three components: 1) government-wide financial statements, 2) fund financial statements, and 3) notes to the financial statements. This report also contains other supplementary information in addition to the basic financial statements themselves.

Government-wide financial statements. The government-wide financial statements are designed to provide readers with a broad view of the City’s finances, in a manner similar to a private-sector business.

The statement of net position presents information on all of the City’s assets and deferred outflows of resources and liabilities and deferred inflows of resources, with the difference reported as net position. Over time, increases or decreases in net position may serve as a useful indicator of whether the financial position of the City is improving or deteriorating.

The statement of activities presents information showing how the government’s net position changed during the most recent fiscal year. All changes in net position are reported as soon as the underlying event giving rise to the change occurs, regardless of the timing of related cash flows. Thus, revenues and expenses are reported in this statement for some items that will only result in cash flows in future fiscal periods (e.g., uncollected taxes and earned but unused vacation leave).

Both of the government-wide financial statements distinguish functions of the City that are principally supported by taxes and intergovernmental revenues (governmental activities) from other functions that are intended to recover all or a significant portion of their costs through user fees and charges (business-type activities). The governmental activities of the City include general government, police, fire, ambulance, the golf course, city development, infrastructure, and community services. The business-type activities of the City include water, sewer, and sanitation. On January 1, 2015, the city closed the Golf Fund and transferred net equity into the General Fund to account for it in the governmental activities.

The government-wide financial statements can be found on pages 14-15 of this report.

5

City of Thornton, Colorado Management’s Discussion and Analysis

December 31, 2015

Fund financial statements. A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The City, like other state and local governments, uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. All of the funds of the City can be divided into two categories: governmental funds and proprietary funds.

Governmental funds. Governmental funds are used to account for essentially the same functions reported as governmental activities in the government-wide financial statements. However, unlike the government-wide financial statements, governmental fund financial statements focus on near-term inflows and outflows of spendable resources, as well as on balances of spendable resources available at the end of the fiscal year. Such information may be useful in evaluating a government’s near-term financing requirements.

Because the focus of governmental funds is narrower than that of the government-wide financial statements, it is useful to compare the information presented for governmental funds with similar information presented for governmental activities in the government-wide financial statements. By doing so, readers may better understand the long-term impact of the government’s near-term financing decisions. Both the governmental fund balance sheet and the governmental fund statement of revenues, expenditures, and changes in fund balances provide a reconciliation to facilitate this comparison between governmental funds and governmental activities.

The City maintains 16 individual governmental funds. Information is presented separately in the governmental fund balance sheet and in the governmental fund statement of revenues, expenditures, and changes in fund balances for the General Fund, the Governmental Capital Fund, Parks and Open Space Fund and the Thornton Development Authority North Capital Fund which are considered to be major funds. Data from the other 12 governmental funds are combined into a single, aggregated presentation. Individual fund data for each of these non-major governmental funds is provided in the form of combining statements elsewhere in this report.

The City adopts an annual appropriated budget for its General Fund. A budgetary comparison statement has been provided for the General Fund to demonstrate compliance with this budget, which can be found on page 58 of this report.

The basic governmental fund financial statements can be found on pages 18-21 of this report.

Proprietary funds. The City maintains two different types of proprietary funds; enterprise and internal service. Enterprise funds are used to report the same functions presented as business-type activities in the government-wide financial statements. The City uses enterprise funds to account for water, sewer, and sanitation. Internal service funds are an accounting device used to accumulate and allocate costs internally among the City’s various functions. The City uses five internal service funds: Risk Management to account for the costs related to a comprehensive program to manage the City’s property, liability, work related injury risk, dental and vision; Information Technology to account for computer support and maintenance; Reprographics to account for copying and mailing; the Consolidated Service Center to account for fuel purchased and utilized by Adams County School District 12; and Maintenance Services to account for custodial and building maintenance service costs. Because these services predominately benefit governmental rather than business-type functions, they have been included within governmental activities in the government-wide financial statements.

Proprietary funds provide the same type of information as the government-wide financial statements, only in more detail. The proprietary fund financial statements provide separate information for the Water, Sewer, and Sanitation Funds. Only the Water and Sewer Funds are considered to be major funds of the City. Individual fund data for the internal service funds is provided in the form of combining statements elsewhere in this report.

The basic proprietary fund financial statements can be found on pages 22-27 of this report.

Notes to the financial statements. The notes provide additional information that is essential to a full understanding of the data provided in the government-wide and fund financial statements. The notes to the financial statements can be found on pages 28-56 of this report.

Other information. In addition to the basic financial statements and accompanying notes, this report also presents certain supplementary information. The combining statements referred to earlier in connection with non-major governmental funds and proprietary funds are presented immediately following the basic financial statements. Combining statements and budgetary schedules can be found on pages 68-106 of this report. The Schedule of Investments and Local Highway Finance Report can be found on pages 110-111 of this report.

Government-wide Financial Analysis

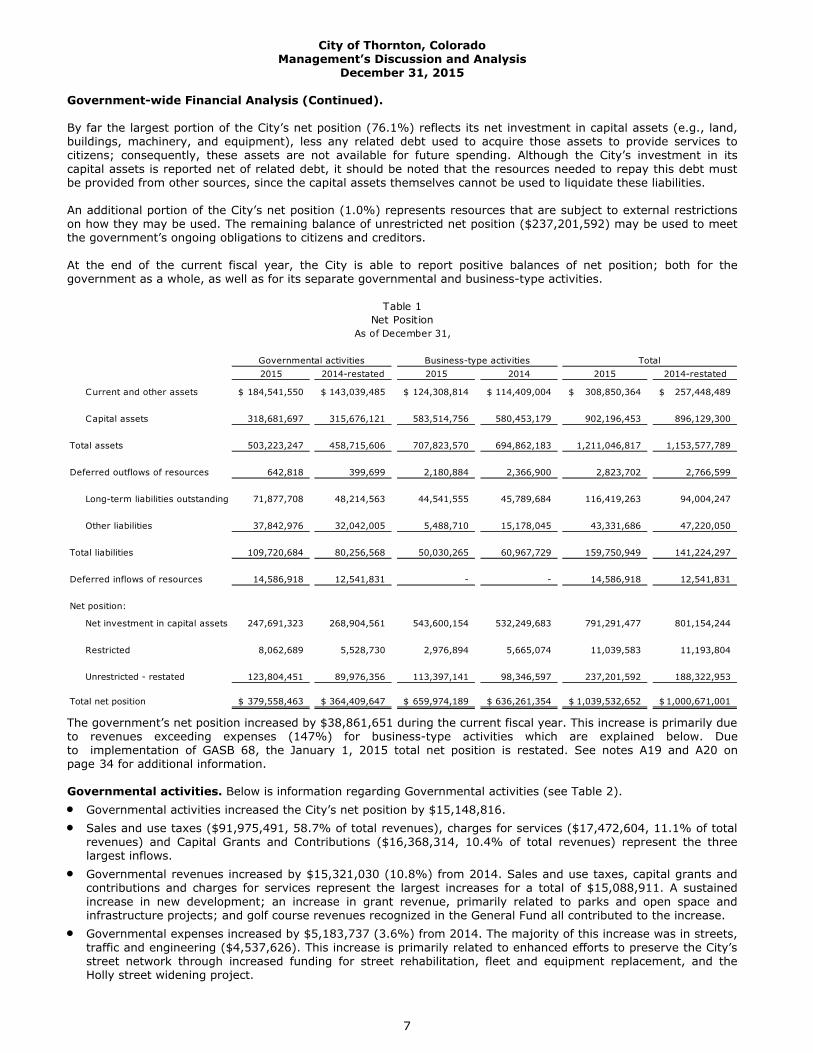

As noted earlier, net position may serve over time as a useful indicator of a government’s financial position. Assets exceeded liabilities by $1,039,532,652 at the close of the most recent fiscal year (see Table 1).

6

City of Thornton, Colorado Management’s Discussion and Analysis

December 31, 2015

Government-wide Financial Analysis (Continued).

By far the largest portion of the City’s net position (76.1%) reflects its net investment in capital assets (e.g., land, buildings, machinery, and equipment), less any related debt used to acquire those assets to provide services to citizens; consequently, these assets are not available for future spending. Although the City’s investment in its capital assets is reported net of related debt, it should be noted that the resources needed to repay this debt must be provided from other sources, since the capital assets themselves cannot be used to liquidate these liabilities.

An additional portion of the City’s net position (1.0%) represents resources that are subject to external restrictions on how they may be used. The remaining balance of unrestricted net position ($237,201,592) may be used to meet the government’s ongoing obligations to citizens and creditors.

At the end of the current fiscal year, the City is able to report positive balances of net position; both for the government as a whole, as well as for its separate governmental and business-type activities.

Governmental activities Business-type activities Total2015 2014-restated 2015 2014 2015 2014-restated

Current and other assets 184,541,550$ 143,039,485$ 124,308,814$ 114,409,004$ 308,850,364$ 257,448,489$

Capital assets 318,681,697 315,676,121 583,514,756 580,453,179 902,196,453 896,129,300

Total assets 503,223,247 458,715,606 707,823,570 694,862,183 1,211,046,817 1,153,577,789

Deferred outflows of resources 642,818 399,699 2,180,884 2,366,900 2,823,702 2,766,599

Long-term liabilities outstanding 71,877,708 48,214,563 44,541,555 45,789,684 116,419,263 94,004,247

Other liabilities 37,842,976 32,042,005 5,488,710 15,178,045 43,331,686 47,220,050

Total liabilities 109,720,684 80,256,568 50,030,265 60,967,729 159,750,949 141,224,297

Deferred inflows of resources 14,586,918 12,541,831 - - 14,586,918 12,541,831

Net position:

Net investment in capital assets 247,691,323 268,904,561 543,600,154 532,249,683 791,291,477 801,154,244

Restricted 8,062,689 5,528,730 2,976,894 5,665,074 11,039,583 11,193,804

Unrestricted - restated 123,804,451 89,976,356 113,397,141 98,346,597 237,201,592 188,322,953

Total net position 379,558,463$ 364,409,647$ 659,974,189$ 636,261,354$ 1,039,532,652$ 1,000,671,001$

Table 1Net Position

As of December 31,

The government’s net position increased by $38,861,651 during the current fiscal year. This increase is primarily due to revenues exceeding expenses (147%) for business-type activities which are explained below. Due to implementation of GASB 68, the January 1, 2015 total net position is restated. See notes A19 and A20 on page 34 for additional information.

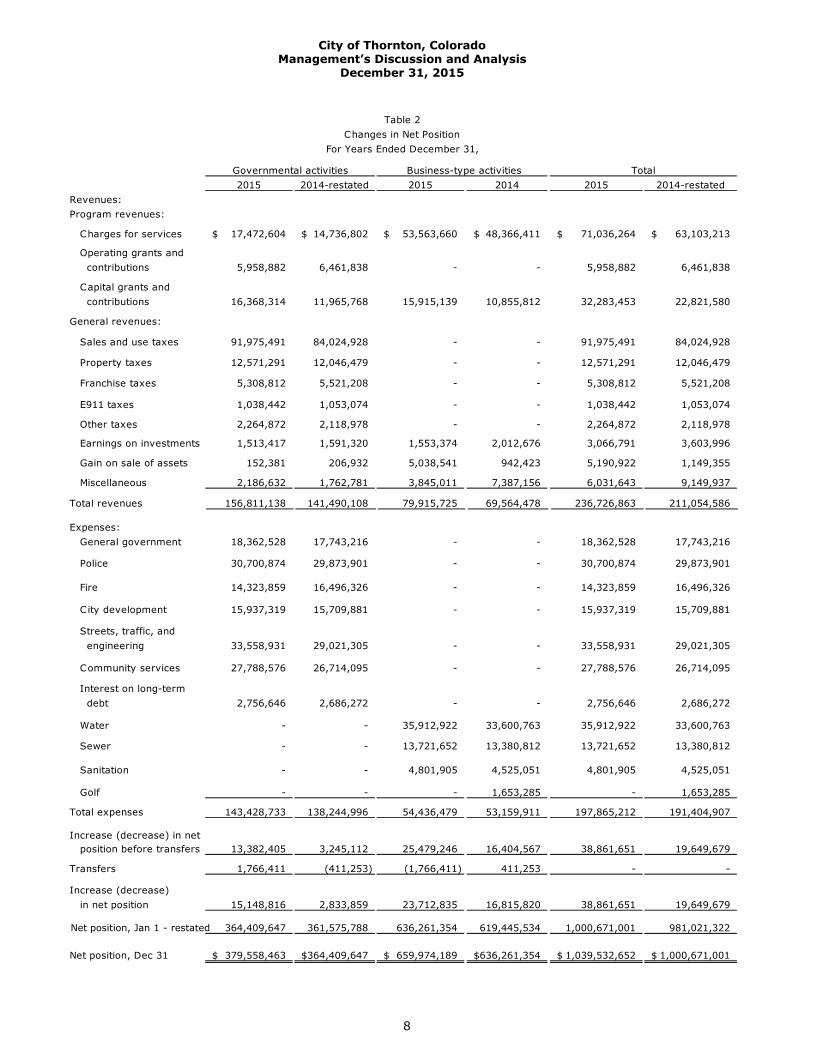

Governmental activities. Below is information regarding Governmental activities (see Table 2). Governmental activities increased the City’s net position by $15,148,816. Sales and use taxes ($91,975,491, 58.7% of total revenues), charges for services ($17,472,604, 11.1% of total

revenues) and Capital Grants and Contributions ($16,368,314, 10.4% of total revenues) represent the threelargest inflows.

Governmental revenues increased by $15,321,030 (10.8%) from 2014. Sales and use taxes, capital grants andcontributions and charges for services represent the largest increases for a total of $15,088,911. A sustainedincrease in new development; an increase in grant revenue, primarily related to parks and open space andinfrastructure projects; and golf course revenues recognized in the General Fund all contributed to the increase.

Governmental expenses increased by $5,183,737 (3.6%) from 2014. The majority of this increase was in streets,traffic and engineering ($4,537,626). This increase is primarily related to enhanced efforts to preserve the City’sstreet network through increased funding for street rehabilitation, fleet and equipment replacement, and theHolly street widening project.

7

City of Thornton, Colorado Management’s Discussion and Analysis

December 31, 2015

Table 2Changes in Net Position

For Years Ended December 31,

Governmental activities Business-type activities Total2015 2014-restated 2015 2014 2015 2014-restated

Revenues:Program revenues:

Charges for services 17,472,604$ 14,736,802$ 53,563,660$ 48,366,411$ 71,036,264$ 63,103,213$

Operating grants and contributions 5,958,882 6,461,838 - - 5,958,882 6,461,838

Capital grants and contributions 16,368,314 11,965,768 15,915,139 10,855,812 32,283,453 22,821,580

General revenues:

Sales and use taxes 91,975,491 84,024,928 - - 91,975,491 84,024,928

Property taxes 12,571,291 12,046,479 - - 12,571,291 12,046,479

Franchise taxes 5,308,812 5,521,208 - - 5,308,812 5,521,208

E911 taxes 1,038,442 1,053,074 - - 1,038,442 1,053,074

Other taxes 2,264,872 2,118,978 - - 2,264,872 2,118,978

Earnings on investments 1,513,417 1,591,320 1,553,374 2,012,676 3,066,791 3,603,996

Gain on sale of assets 152,381 206,932 5,038,541 942,423 5,190,922 1,149,355

Miscellaneous 2,186,632 1,762,781 3,845,011 7,387,156 6,031,643 9,149,937

Total revenues 156,811,138 141,490,108 79,915,725 69,564,478 236,726,863 211,054,586

Expenses: General government 18,362,528 17,743,216 - - 18,362,528 17,743,216

Police 30,700,874 29,873,901 - - 30,700,874 29,873,901

Fire 14,323,859 16,496,326 - - 14,323,859 16,496,326

C ity development 15,937,319 15,709,881 - - 15,937,319 15,709,881

Streets, traffic, and engineering 33,558,931 29,021,305 - - 33,558,931 29,021,305

Community services 27,788,576 26,714,095 - - 27,788,576 26,714,095

Interest on long-term debt 2,756,646 2,686,272 - - 2,756,646 2,686,272

Water - - 35,912,922 33,600,763 35,912,922 33,600,763

Sewer - - 13,721,652 13,380,812 13,721,652 13,380,812

Sanitation - - 4,801,905 4,525,051 4,801,905 4,525,051

Golf - - - 1,653,285 - 1,653,285

Total expenses 143,428,733 138,244,996 54,436,479 53,159,911 197,865,212 191,404,907

Increase (decrease) in net position before transfers 13,382,405 3,245,112 25,479,246 16,404,567 38,861,651 19,649,679

Transfers 1,766,411 (411,253) (1,766,411) 411,253 - -

Increase (decrease) in net position 15,148,816 2,833,859 23,712,835 16,815,820 38,861,651 19,649,679

Net position, Jan 1 - restated 364,409,647 361,575,788 636,261,354 619,445,534 1,000,671,001 981,021,322

Net position, Dec 31 379,558,463$ 364,409,647$ 659,974,189$ 636,261,354$ 1,039,532,652$ 1,000,671,001$

8

City of Thornton, Colorado Management’s Discussion and Analysis

December 31, 2015

Business-type activities. Below is information regarding Business-type activities (see Table 2). Business-type activities increased the City’s net position by $23,712,835, accounting for 61.0% of the total

growth in the government’s net position. Charges for services ($53,563,660, 67.0% of total revenues), gain on sale of capital assets ($5,038,541, 6.3% of

total revenues) and tap fees, which are included in grants and contributions, ($12,529,822, 15.7% of total revenues) represent the three largest inflows to business-type activities.

Revenues increased by $10,351,247 (14.9%) in 2015 compared to 2014. The two largest increases in revenuewere in charges for services ($5,197,249) and in grants and contributions ($5,059,327).

Expenses increased $1,276,568 (2.4%) from 2014. The single largest increase ($2,312,159) was in the WaterFund, primarily due to additional spending on reservoir repairs, pipeline rehab and valve replacements. The Water Fund increase in expenses was offset by the decrease in the Golf Fund ($1,653,285) which was closed on January 1, 2015, and is now accounted for in the General fund.

Financial Analysis of the Government’s Funds

As noted earlier, the City uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements. The following details are contained in the fund financial statements.

Governmental funds. The focus of the City’s governmental funds is to provide information on near-term inflows, outflows, and balances of spendable resources. Such information is useful in assessing the City’s financing requirements. In particular, unreserved fund balance may serve as a useful measure of a government’s net resources available for spending at the end of the fiscal year.

As of the end of the current fiscal year, the City governmental funds reported combined ending fund balances of $141,643,971, an increase of $36,893,144 in comparison with the prior year as a result of revenues exceeding expenses. The reasons for increases in revenues and decreases in expenses are outlined above under the Governmental Activities section. Approximately 78.1% of year end fund balance ($110,609,810) is available for spending at the government’s discretion.

The remainder of fund balance ($31,034,161) is nonspendable, restricted or committed to indicate that it is not available for new spending. The largest component is commitments made by Council ($20,138,386, 64.9%).

The General Fund is the chief operating fund of the City. At the end of the current fiscal year, unassigned fund balance of the General Fund was 2.1% ($519,210) of total fund balance ($24,808,070). As a measure of the General Fund’s liquidity, it may be useful to compare both unassigned fund balance and total fund balance to total fund expenditures. Unassigned fund balance represents less than 1% of total actual General Fund expenditures, while total fund balance represents 23.8% of that same amount. The General fund unassigned fund balance decreased substantially from 2014 ($9,670,972) as a result of the transfer of available monies ($10,190,182) to the Governmental Capital Fund to prepare for the financing of the Council adopted Community Facilities Plan (CFP). The CFP will provide capital investments to meet current and future community demands for services.

In addition to this one time transfer in 2015, the Governmental Capital Projects Fund is funded primarily with sales and use taxes and provides for the repair, replacement and planned growth of infrastructure and other capital assets of the City government. At the end of the current fiscal year, assigned fund balance was 98.0% ($50,069,809) of total fund balance ($51,069,832).

Proprietary funds. The City’s proprietary funds provide the same type of information found in the government-wide financial statements, but in more detail.

Unrestricted net position of the Water, Sewer, and Sanitation Funds at the end of the year amounted to $88,537,708, $18,190,683, $6,668,750 respectively. The change in net position for the funds was an increase in Water of $22,190,293, an increase in Sewer of $2,953,603, and an increase in Sanitation of $335,350. The Golf Fund was closed on January 1, 2015, assets and equity totaling $1,766,411 were transferred out of this fund and activities related to the operation of the golf course are now accounted for in the General Fund.

General Fund Budgetary Highlights

Combined revenues (General Fund and Governmental Capital Fund) were greater than budgetary estimates and General Fund expenditures were less than appropriations. Governmental sales and use taxes were up 9.5% in 2015 compared to 2014. The majority of governmental sales and use tax, approximately 80.4% ($73,925,956) is available for general fund operations and governmental capital projects. In 2015, the City utilized sales and use tax revenue

9

City of Thornton, Colorado Management’s Discussion and Analysis

December 31, 2015

General Fund Budgetary Highlights (Continued).

as needed in the general fund. The remainder of the available sales and use tax revenue was accumulated in the governmental capital fund to prepare for planned improvements and expansion of infrastructure and community facilities in order to keep pace with the current and projected growth in the City.

General Fund expenditures were under budget by $1,083,663 in 2015. Lower than projected fuel prices ($348,018), decreased consumption in utilities ($484,245), and lower than budgeted internal service charges ($582,533) represent the majority of the budgetary savings in 2015. These savings were offset by higher than expected spending for snow & ice supplies ($304,254).

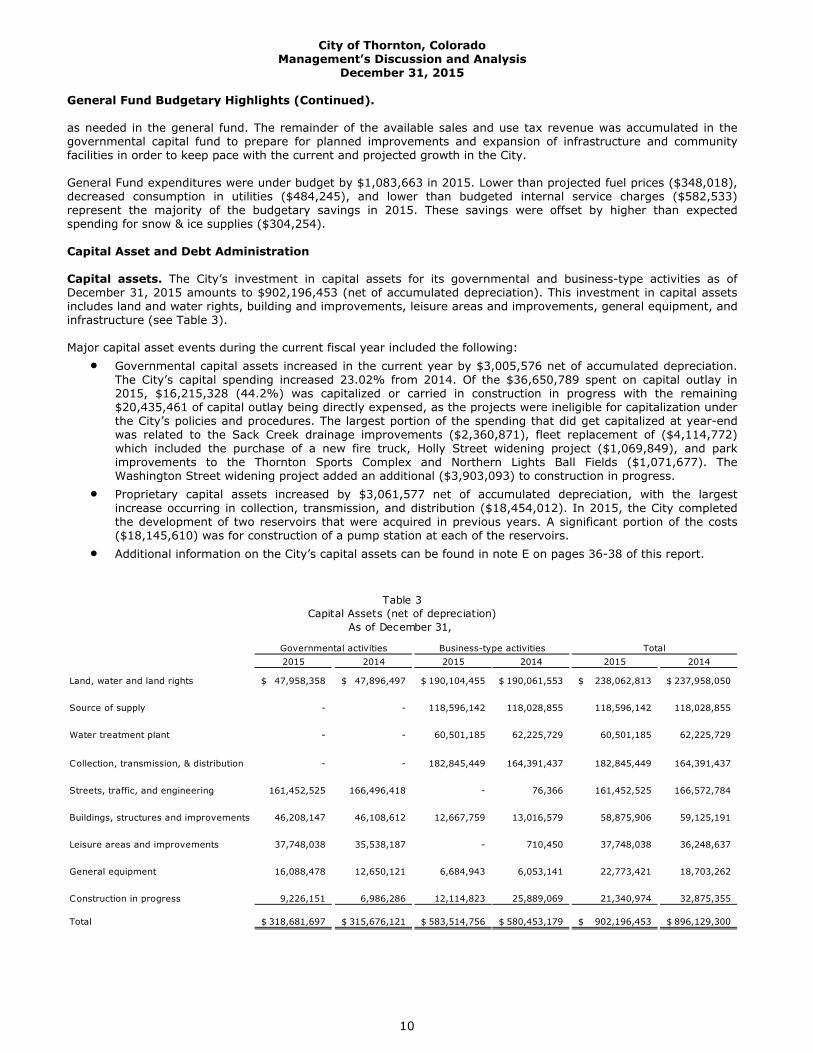

Capital Asset and Debt Administration

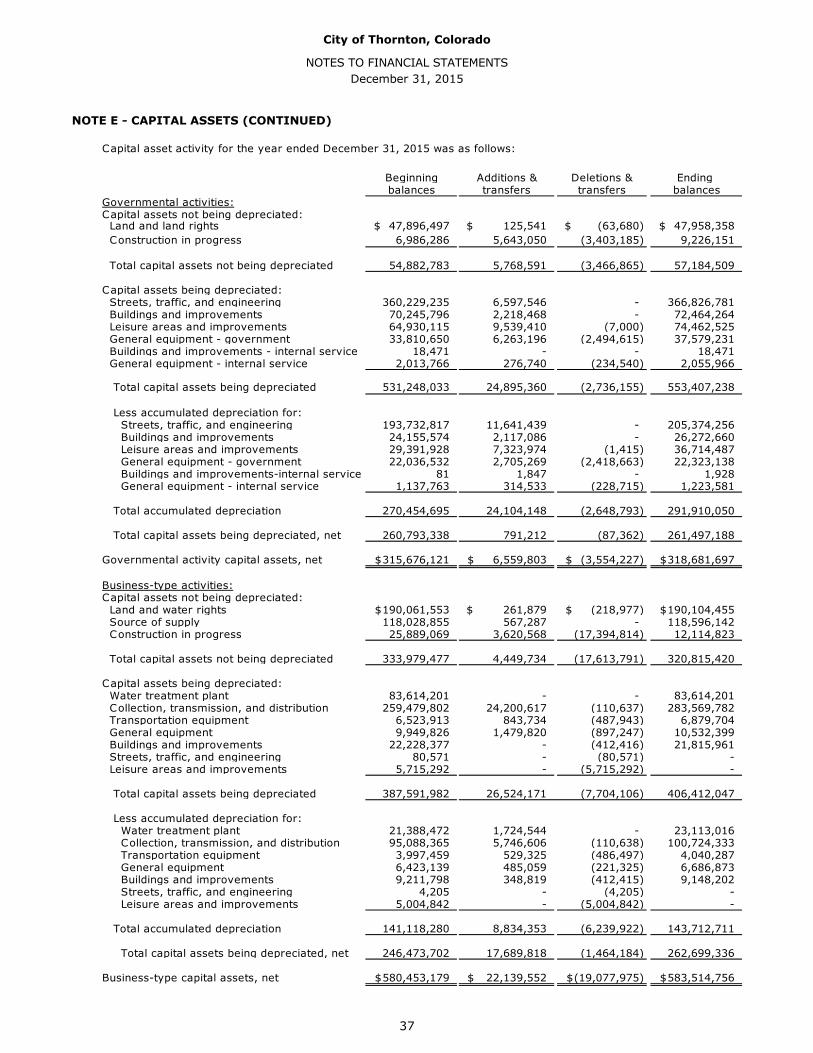

Capital assets. The City’s investment in capital assets for its governmental and business-type activities as of December 31, 2015 amounts to $902,196,453 (net of accumulated depreciation). This investment in capital assets includes land and water rights, building and improvements, leisure areas and improvements, general equipment, and infrastructure (see Table 3).

Major capital asset events during the current fiscal year included the following: Governmental capital assets increased in the current year by $3,005,576 net of accumulated depreciation.

The City’s capital spending increased 23.02% from 2014. Of the $36,650,789 spent on capital outlay in 2015, $16,215,328 (44.2%) was capitalized or carried in construction in progress with the remaining $20,435,461 of capital outlay being directly expensed, as the projects were ineligible for capitalization under the City’s policies and procedures. The largest portion of the spending that did get capitalized at year-end was related to the Sack Creek drainage improvements ($2,360,871), fleet replacement of ($4,114,772) which included the purchase of a new fire truck, Holly Street widening project ($1,069,849), and park improvements to the Thornton Sports Complex and Northern Lights Ball Fields ($1,071,677). The Washington Street widening project added an additional ($3,903,093) to construction in progress.

Proprietary capital assets increased by $3,061,577 net of accumulated depreciation, with the largestincrease occurring in collection, transmission, and distribution ($18,454,012). In 2015, the City completed the development of two reservoirs that were acquired in previous years. A significant portion of the costs ($18,145,610) was for construction of a pump station at each of the reservoirs.

Additional information on the City’s capital assets can be found in note E on pages 36-38 of this report.

Table 3Capital Assets (net of depreciation)

As of December 31,

Governmental activities Business-type activities Total2015 2014 2015 2014 2015 2014

Land, water and land rights 47,958,358$ 47,896,497$ 190,104,455$ 190,061,553$ 238,062,813$ 237,958,050$

Source of supply - - 118,596,142 118,028,855 118,596,142 118,028,855

Water treatment plant - - 60,501,185 62,225,729 60,501,185 62,225,729

Collection, transmission, & distribution - - 182,845,449 164,391,437 182,845,449 164,391,437

Streets, traffic, and engineering 161,452,525 166,496,418 - 76,366 161,452,525 166,572,784

Buildings, structures and improvements 46,208,147 46,108,612 12,667,759 13,016,579 58,875,906 59,125,191

Leisure areas and improvements 37,748,038 35,538,187 - 710,450 37,748,038 36,248,637

General equipment 16,088,478 12,650,121 6,684,943 6,053,141 22,773,421 18,703,262

Construction in progress 9,226,151 6,986,286 12,114,823 25,889,069 21,340,974 32,875,355

Total 318,681,697$ 315,676,121$ 583,514,756$ 580,453,179$ 902,196,453$ 896,129,300$

10

City of Thornton, Colorado Management’s Discussion and Analysis

December 31, 2015

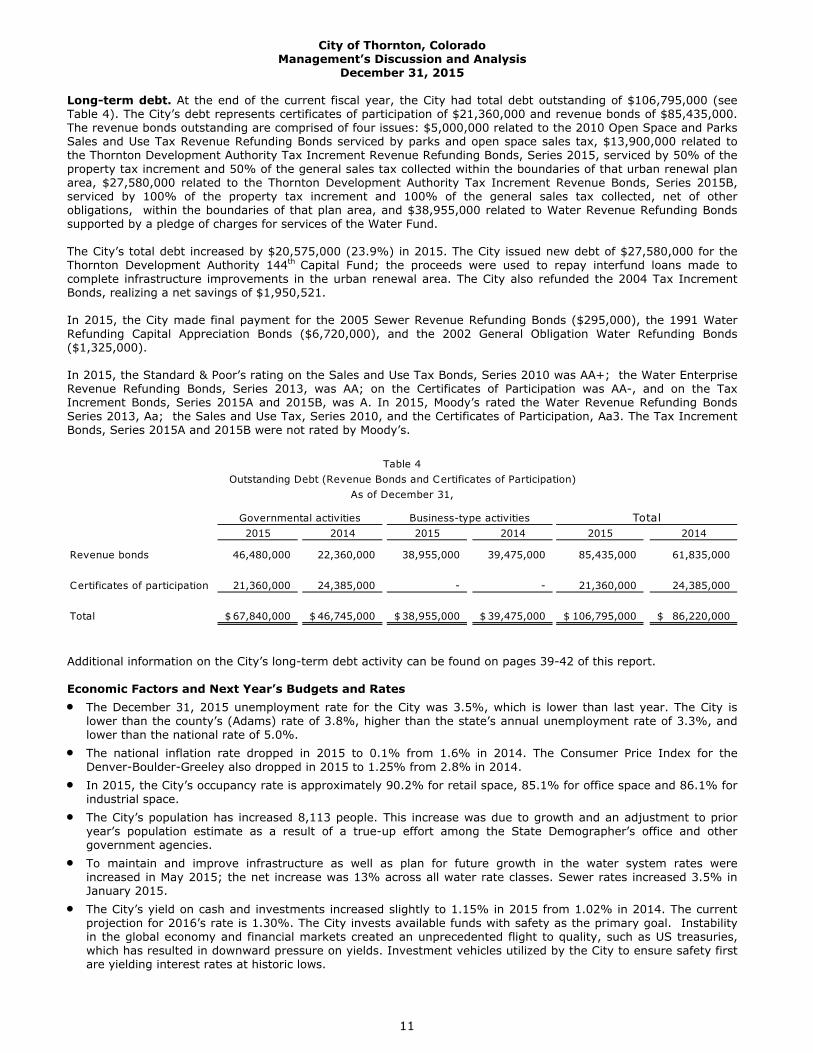

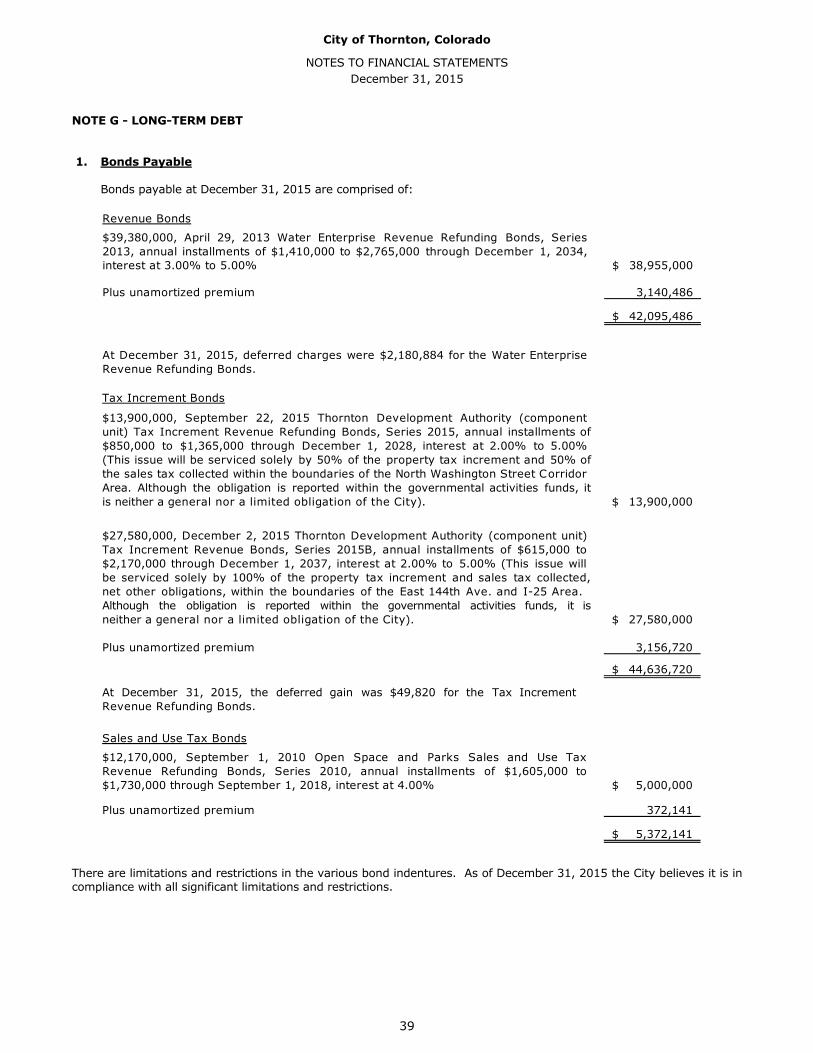

Long-term debt. At the end of the current fiscal year, the City had total debt outstanding of $106,795,000 (see Table 4). The City’s debt represents certificates of participation of $21,360,000 and revenue bonds of $85,435,000. The revenue bonds outstanding are comprised of four issues: $5,000,000 related to the 2010 Open Space and Parks Sales and Use Tax Revenue Refunding Bonds serviced by parks and open space sales tax, $13,900,000 related to the Thornton Development Authority Tax Increment Revenue Refunding Bonds, Series 2015, serviced by 50% of the property tax increment and 50% of the general sales tax collected within the boundaries of that urban renewal plan area, $27,580,000 related to the Thornton Development Authority Tax Increment Revenue Bonds, Series 2015B, serviced by 100% of the property tax increment and 100% of the general sales tax collected, net of other obligations, within the boundaries of that plan area, and $38,955,000 related to Water Revenue Refunding Bonds supported by a pledge of charges for services of the Water Fund.

The City’s total debt increased by $20,575,000 (23.9%) in 2015. The City issued new debt of $27,580,000 for the Thornton Development Authority 144th Capital Fund; the proceeds were used to repay interfund loans made to complete infrastructure improvements in the urban renewal area. The City also refunded the 2004 Tax Increment Bonds, realizing a net savings of $1,950,521.

In 2015, the City made final payment for the 2005 Sewer Revenue Refunding Bonds ($295,000), the 1991 Water Refunding Capital Appreciation Bonds ($6,720,000), and the 2002 General Obligation Water Refunding Bonds ($1,325,000).

In 2015, the Standard & Poor’s rating on the Sales and Use Tax Bonds, Series 2010 was AA+; the Water Enterprise Revenue Refunding Bonds, Series 2013, was AA; on the Certificates of Participation was AA-, and on the Tax Increment Bonds, Series 2015A and 2015B, was A. In 2015, Moody’s rated the Water Revenue Refunding Bonds Series 2013, Aa; the Sales and Use Tax, Series 2010, and the Certificates of Participation, Aa3. The Tax Increment Bonds, Series 2015A and 2015B were not rated by Moody’s.

Table 4Outstanding Debt (Revenue Bonds and Certificates of Participation)

As of December 31,

Governmental activities Business-type activities Total2015 2014 2015 2014 2015 2014

Revenue bonds 46,480,000 22,360,000 38,955,000 39,475,000 85,435,000 61,835,000

Certificates of participation 21,360,000 24,385,000 - - 21,360,000 24,385,000

Total 67,840,000$ 46,745,000$ 38,955,000$ 39,475,000$ 106,795,000$ 86,220,000$

Additional information on the City’s long-term debt activity can be found on pages 39-42 of this report.

Economic Factors and Next Year’s Budgets and Rates The December 31, 2015 unemployment rate for the City was 3.5%, which is lower than last year. The City is

lower than the county’s (Adams) rate of 3.8%, higher than the state’s annual unemployment rate of 3.3%, and lower than the national rate of 5.0%.

The national inflation rate dropped in 2015 to 0.1% from 1.6% in 2014. The Consumer Price Index for theDenver-Boulder-Greeley also dropped in 2015 to 1.25% from 2.8% in 2014.

In 2015, the City’s occupancy rate is approximately 90.2% for retail space, 85.1% for office space and 86.1% forindustrial space.

The City’s population has increased 8,113 people. This increase was due to growth and an adjustment to prioryear’s population estimate as a result of a true-up effort among the State Demographer’s office and other government agencies.

To maintain and improve infrastructure as well as plan for future growth in the water system rates wereincreased in May 2015; the net increase was 13% across all water rate classes. Sewer rates increased 3.5% in January 2015.

The City’s yield on cash and investments increased slightly to 1.15% in 2015 from 1.02% in 2014. The currentprojection for 2016’s rate is 1.30%. The City invests available funds with safety as the primary goal. Instability in the global economy and financial markets created an unprecedented flight to quality, such as US treasuries, which has resulted in downward pressure on yields. Investment vehicles utilized by the City to ensure safety first are yielding interest rates at historic lows.

11

City of Thornton, Colorado Management’s Discussion and Analysis

December 31, 2015

All of these factors were considered in preparing the City’s budget for the 2016 fiscal year.

Ending unassigned fund balance in the General Fund was $519,210. Anticipated revenues and the use of this fund balance are expected to be adequate to fund necessary governmental operations and to keep the fund balance in harmony with the City Council’s fund balance policy.

Requests for Information

This financial report is designed to provide a general overview of the City’s finances for all those with an interest in the government’s finances. Questions concerning any of the information provided in this report or requests for additional financial information should be addressed to the City Treasurer, City of Thornton, 9500 Civic Center Drive, Thornton, CO 80229 or visit the City’s website at www.cityofthornton.net.

12

BASIC FINANCIAL STATEMENTS

13

Governmental Business-typeActivities Activities Total

ASSETS Equity in pooled cash and investments 150,551,816$ 113,963,585$ 264,515,401$ Receivables, net Taxes 24,927,548 - 24,927,548 Accounts 2,756,166 6,204,831 8,960,997 Interest and other 469,655 568,106 1,037,761 Internal balances (317,425) 317,425 - Inventory of supplies 66,602 - 66,602 Prepaids and other assets 125,365 15,378 140,743 Land held for resale 1,985,873 142,379 2,128,252 Restricted assets Equity in pooled cash and investments 3,726,509 3,097,110 6,823,619 Capital assets Land, water rights, and construction in progress 57,184,509 320,815,420 377,999,929 Depreciable buildings, property, and equipment, net 261,497,188 262,699,336 524,196,524 Net pension asset 249,441 - 249,441

Total assets 503,223,247 707,823,570 1,211,046,817

DEFERRED OUTFLOWS OF RESOURCES Deferred charge on refunding 266,466 2,180,884 2,447,350 Deferred outflow to pension 376,352 - 376,352

Total deferred outflows of resources 642,818 2,180,884 2,823,702

LIABILITIES Accounts payable 10,511,605 3,011,804 13,523,409 Retainage payable 395,915 27,866 423,781 Accrued interest payable 265,047 120,216 385,263 Third party development advances 8,908,812 - 8,908,812 Unearned revenue 228,622 410,656 639,278 Other 3,849,944 133,743 3,983,687 Noncurrent liabilities Due within one year 11,062,214 1,784,425 12,846,639 Due in more than one year 71,877,708 44,541,555 116,419,263 Net pension liability 2,620,817 - 2,620,817

Total liabilities 109,720,684 50,030,265 159,750,949

DEFERRED INFLOWS OF RESOURCES Deferred revenue - property tax 14,531,960 - 14,531,960 Deferred gain on refunding 49,820 - 49,820 Deferred inflows related to pensions 5,138 - 5,138

Total deferred inflows of resources 14,586,918 - 14,586,918

NET POSITION Net investment in capital assets 247,691,323 543,600,154 791,291,477 Restricted for Debt service 3,720,085 2,976,894 6,696,979 Emergencies 4,342,604 - 4,342,604 Unrestricted 123,804,451 113,397,141 237,201,592

Total net position 379,558,463$ 659,974,189$ 1,039,532,652$

The accompanying notes are an integral part of these financial statements.

City of Thornton, Colorado

Statement of Net PositionDecember 31, 2015

14

Operating CapitalCharges for Grants and Grants and Governmental Business-Type

Functions/Activities Expenses Services Contributions Contributions Activities Activities TotalGovernmental: General government 18,362,528$ 4,923,991$ -$ -$ (13,438,537)$ (13,438,537)$ Police 30,700,874 1,964,945 1,069,148 112,428 (27,554,353) (27,554,353) Fire 14,323,859 1,887,235 400 - (12,436,224) (12,436,224) City development 15,937,319 4,061,961 341,101 10 (11,534,247) (11,534,247) Streets, traffic & engineering 33,558,931 - 4,438,737 10,246,637 (18,873,557) (18,873,557) Community services 27,788,576 4,634,472 109,496 6,009,239 (17,035,369) (17,035,369) Interest on long-term debt 2,756,646 - - - (2,756,646) (2,756,646)

Total governmental activities 143,428,733 17,472,604 5,958,882 16,368,314 (103,628,933) (103,628,933)

Business-type: Water 35,912,922 34,348,429 - 13,658,648 12,094,155 12,094,155 Sewer 13,721,652 14,191,006 - 2,256,491 2,725,845 2,725,845 Sanitation 4,801,905 5,024,225 - - 222,320 222,320

Total business-type activities 54,436,479 53,563,660 - 15,915,139 15,042,320 15,042,320

Total City of Thornton 197,865,212$ 71,036,264$ 5,958,882$ 32,283,453$ (103,628,933) 15,042,320 (88,586,613)

General revenues: Sales and use taxes 91,975,491 - 91,975,491 Property taxes 12,571,291 - 12,571,291 Franchise taxes 5,308,812 - 5,308,812 E911 taxes 1,038,442 - 1,038,442 Other taxes 2,264,872 - 2,264,872 Earnings on investments 1,513,417 1,553,374 3,066,791 Gain on sale of assets 152,381 5,038,541 5,190,922 Miscellaneous 2,186,632 3,845,011 6,031,643 Transfers: 1,766,411 (1,766,411) -

Total general revenues 118,777,749 8,670,515 127,448,264

Change in net position 15,148,816 23,712,835 38,861,651

Net position, January 1 (restated) 364,409,647 636,261,354 1,000,671,001

Net position, December 31 379,558,463$ 659,974,189$ 1,039,532,652$

The accompanying notes are an integral part of these financial statements.

Changes in Net Position

City of Thornton, Colorado

Statement of ActivitiesFor the year ended December 31, 2015

Program Revenues Net (Expense) Revenue and

15

This Page Left Intentionally Blank

16

FUND FINANCIAL STATEMENTS

17

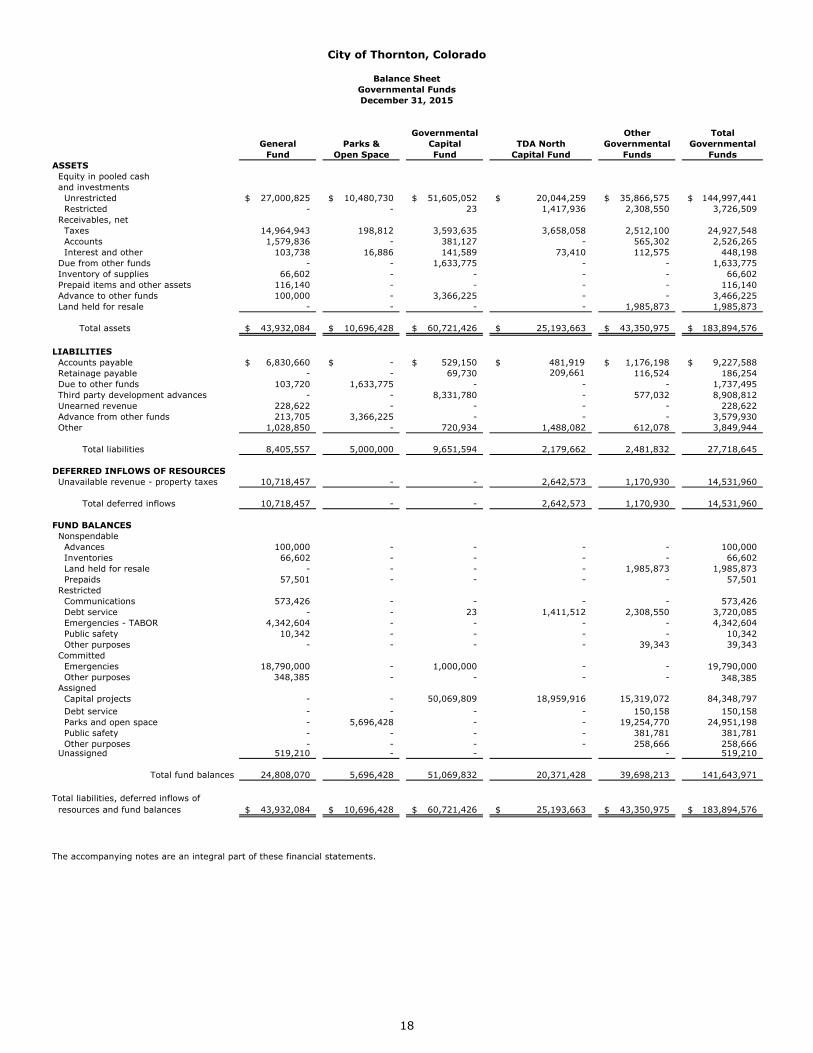

City of Thornton, Colorado

Balance SheetGovernmental FundsDecember 31, 2015

Governmental Other TotalGeneral Parks & Capital TDA North Governmental Governmental

Fund Open Space Fund Capital Fund Funds FundsASSETS Equity in pooled cash and investments Unrestricted 27,000,825$ 10,480,730$ 51,605,052$ 20,044,259$ 35,866,575$ 144,997,441$ Restricted - - 23 1,417,936 2,308,550 3,726,509 Receivables, net Taxes 14,964,943 198,812 3,593,635 3,658,058 2,512,100 24,927,548 Accounts 1,579,836 - 381,127 - 565,302 2,526,265 Interest and other 103,738 16,886 141,589 73,410 112,575 448,198 Due from other funds - - 1,633,775 - - 1,633,775 Inventory of supplies 66,602 - - - - 66,602 Prepaid items and other assets 116,140 - - - - 116,140 Advance to other funds 100,000 - 3,366,225 - - 3,466,225 Land held for resale - - - - 1,985,873 1,985,873

Total assets 43,932,084$ 10,696,428$ 60,721,426$ 25,193,663$ 43,350,975$ 183,894,576$

LIABILITIES Accounts payable 6,830,660$ -$ 529,150$ 481,919$ 1,176,198$ 9,227,588$ Retainage payable - - 69,730 209,661 116,524 186,254 Due to other funds 103,720 1,633,775 - - - 1,737,495 Third party development advances - - 8,331,780 - 577,032 8,908,812 Unearned revenue 228,622 - - - - 228,622 Advance from other funds 213,705 3,366,225 - - - 3,579,930 Other 1,028,850 - 720,934 1,488,082 612,078 3,849,944

Total liabilities 8,405,557 5,000,000 9,651,594 2,179,662 2,481,832 27,718,645

DEFERRED INFLOWS OF RESOURCES Unavailable revenue - property taxes 10,718,457 - - 2,642,573 1,170,930 14,531,960

Total deferred inflows 10,718,457 - - 2,642,573 1,170,930 14,531,960

FUND BALANCES Nonspendable Advances 100,000 - - - - 100,000 Inventories 66,602 - - - - 66,602 Land held for resale - - - - 1,985,873 1,985,873 Prepaids 57,501 - - - - 57,501 Restricted Communications 573,426 - - - - 573,426 Debt service - - 23 1,411,512 2,308,550 3,720,085 Emergencies - TABOR 4,342,604 - - - - 4,342,604 Public safety 10,342 - - - - 10,342 Other purposes - - - - 39,343 39,343 Committed Emergencies 18,790,000 - 1,000,000 - - 19,790,000 Other purposes 348,385 - - - - 348,385 Assigned Capital projects - - 50,069,809 18,959,916 15,319,072 84,348,797 Debt service - - - - 150,158 150,158 Parks and open space - 5,696,428 - - 19,254,770 24,951,198 Public safety - - - - 381,781 381,781 Other purposes - - - - 258,666 258,666 Unassigned 519,210 - - - 519,210

Total fund balances 24,808,070 5,696,428 51,069,832 20,371,428 39,698,213 141,643,971

Total liabilities, deferred inflows of resources and fund balances 43,932,084$ 10,696,428$ 60,721,426$ 25,193,663$ 43,350,975$ 183,894,576$

The accompanying notes are an integral part of these financial statements.

18

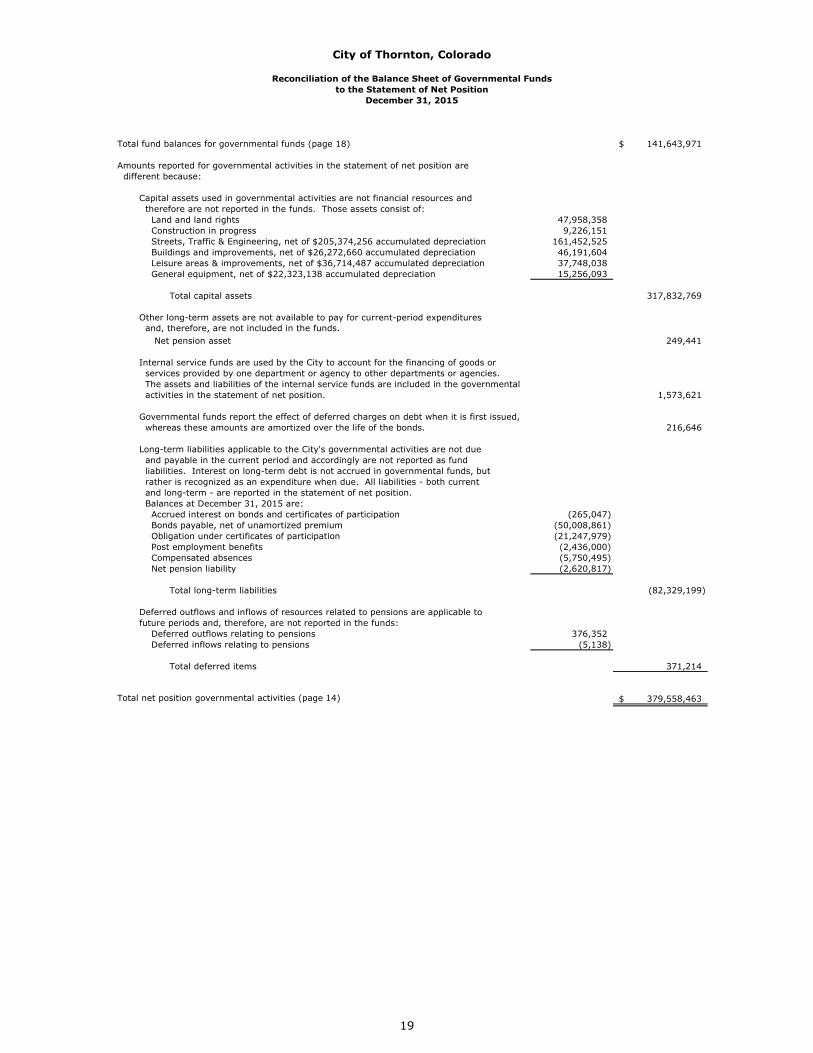

City of Thornton, Colorado

Reconciliation of the Balance Sheet of Governmental Fundsto the Statement of Net Position

December 31, 2015

Total fund balances for governmental funds (page 18) 141,643,971$

Amounts reported for governmental activities in the statement of net position are different because:

Capital assets used in governmental activities are not financial resources and therefore are not reported in the funds. Those assets consist of: Land and land rights 47,958,358 Construction in progress 9,226,151 Streets, Traffic & Engineering, net of $205,374,256 accumulated depreciation 161,452,525 Buildings and improvements, net of $26,272,660 accumulated depreciation 46,191,604 Leisure areas & improvements, net of $36,714,487 accumulated depreciation 37,748,038 General equipment, net of $22,323,138 accumulated depreciation 15,256,093

Total capital assets 317,832,769

Other long-term assets are not available to pay for current-period expenditures and, therefore, are not included in the funds. Net pension asset 249,441

Internal service funds are used by the City to account for the financing of goods or services provided by one department or agency to other departments or agencies. The assets and liabilities of the internal service funds are included in the governmental activities in the statement of net position. 1,573,621

Governmental funds report the effect of deferred charges on debt when it is first issued, whereas these amounts are amortized over the life of the bonds. 216,646

Long-term liabilities applicable to the City's governmental activities are not due and payable in the current period and accordingly are not reported as fund liabilities. Interest on long-term debt is not accrued in governmental funds, but rather is recognized as an expenditure when due. All liabilities - both current and long-term - are reported in the statement of net position. Balances at December 31, 2015 are: Accrued interest on bonds and certificates of participation (265,047) Bonds payable, net of unamortized premium (50,008,861) Obligation under certificates of participation (21,247,979) Post employment benefits (2,436,000) Compensated absences (5,750,495) Net pension liability (2,620,817)

Total long-term liabilities (82,329,199)

Deferred outflows and inflows of resources related to pensions are applicable to future periods and, therefore, are not reported in the funds: Deferred outflows relating to pensions 376,352 Deferred inflows relating to pensions (5,138)

Total deferred items 371,214

Total net position governmental activities (page 14) 379,558,463$

19

City of Thornton, Colorado

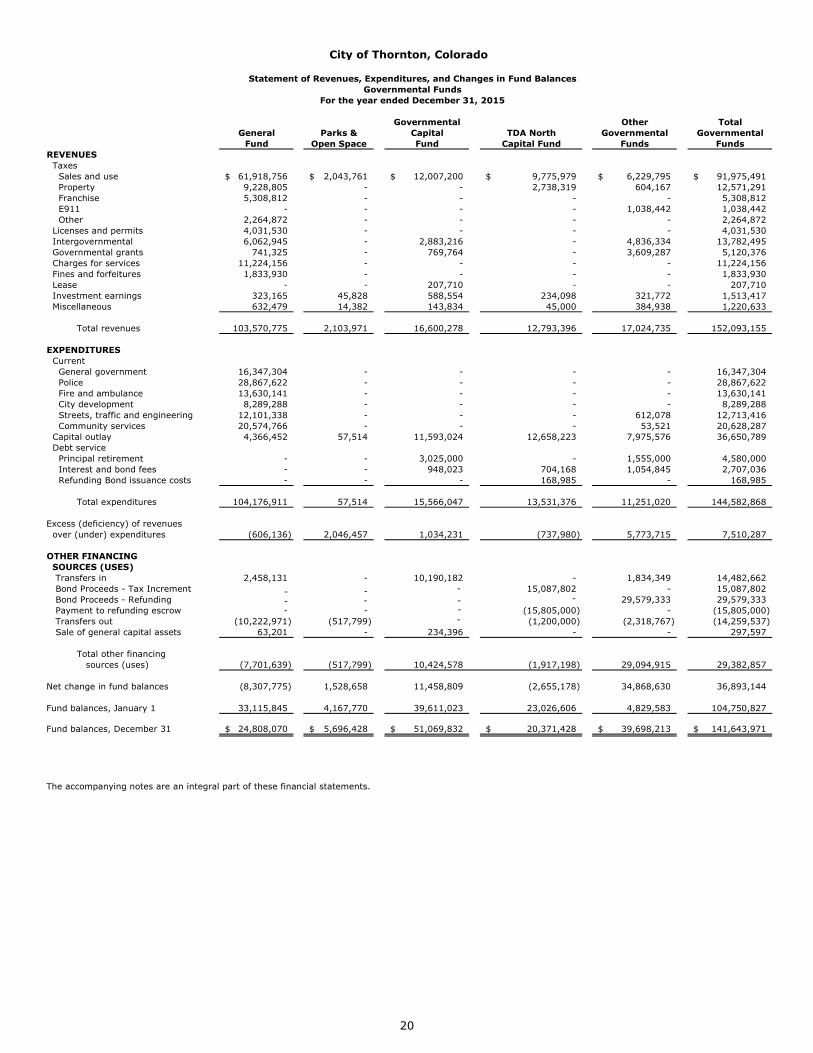

Statement of Revenues, Expenditures, and Changes in Fund BalancesGovernmental Funds

For the year ended December 31, 2015

Governmental Other TotalGeneral Parks & Capital TDA North Governmental Governmental

Fund Open Space Fund Capital Fund Funds FundsREVENUES Taxes Sales and use 61,918,756$ 2,043,761$ 12,007,200$ 9,775,979$ 6,229,795$ 91,975,491$ Property 9,228,805 - - 2,738,319 604,167 12,571,291 Franchise 5,308,812 - - - - 5,308,812 E911 - - - - 1,038,442 1,038,442 Other 2,264,872 - - - - 2,264,872 Licenses and permits 4,031,530 - - - - 4,031,530 Intergovernmental 6,062,945 - 2,883,216 - 4,836,334 13,782,495 Governmental grants 741,325 - 769,764 - 3,609,287 5,120,376 Charges for services 11,224,156 - - - - 11,224,156 Fines and forfeitures 1,833,930 - - - - 1,833,930 Lease - - 207,710 - - 207,710 Investment earnings 323,165 45,828 588,554 234,098 321,772 1,513,417 Miscellaneous 632,479 14,382 143,834 45,000 384,938 1,220,633

Total revenues 103,570,775 2,103,971 16,600,278 12,793,396 17,024,735 152,093,155

EXPENDITURES Current General government 16,347,304 - - - - 16,347,304 Police 28,867,622 - - - - 28,867,622 Fire and ambulance 13,630,141 - - - - 13,630,141 City development 8,289,288 - - - - 8,289,288 Streets, traffic and engineering 12,101,338 - - - 612,078 12,713,416 Community services 20,574,766 - - - 53,521 20,628,287 Capital outlay 4,366,452 57,514 11,593,024 12,658,223 7,975,576 36,650,789 Debt service Principal retirement - - 3,025,000 - 1,555,000 4,580,000 Interest and bond fees - - 948,023 704,168 1,054,845 2,707,036 Refunding Bond issuance costs - - - 168,985 - 168,985

Total expenditures 104,176,911 57,514 15,566,047 13,531,376 11,251,020 144,582,868

Excess (deficiency) of revenues over (under) expenditures (606,136) 2,046,457 1,034,231 (737,980) 5,773,715 7,510,287

OTHER FINANCING SOURCES (USES) Transfers in 2,458,131 - 10,190,182 - 1,834,349 14,482,662 Bond Proceeds - Tax Increment - 15,087,802 - 15,087,802 Bond Proceeds - Refunding 29,579,333 29,579,333 Payment to refunding escrow - - - (15,805,000) - (15,805,000) Transfers out (10,222,971) (517,799) - (1,200,000) (2,318,767) (14,259,537) Sale of general capital assets 63,201 - 234,396 - - 297,597

Total other financingsources (uses) (7,701,639) (517,799) 10,424,578 (1,917,198) 29,094,915 29,382,857

Net change in fund balances (8,307,775) 1,528,658 11,458,809 (2,655,178) 34,868,630 36,893,144

Fund balances, January 1 33,115,845 4,167,770 39,611,023 23,026,606 4,829,583 104,750,827

Fund balances, December 31 24,808,070$ 5,696,428$ 51,069,832$ 20,371,428$ 39,698,213$ 141,643,971$

The accompanying notes are an integral part of these financial statements.

20

- - -

- -

-

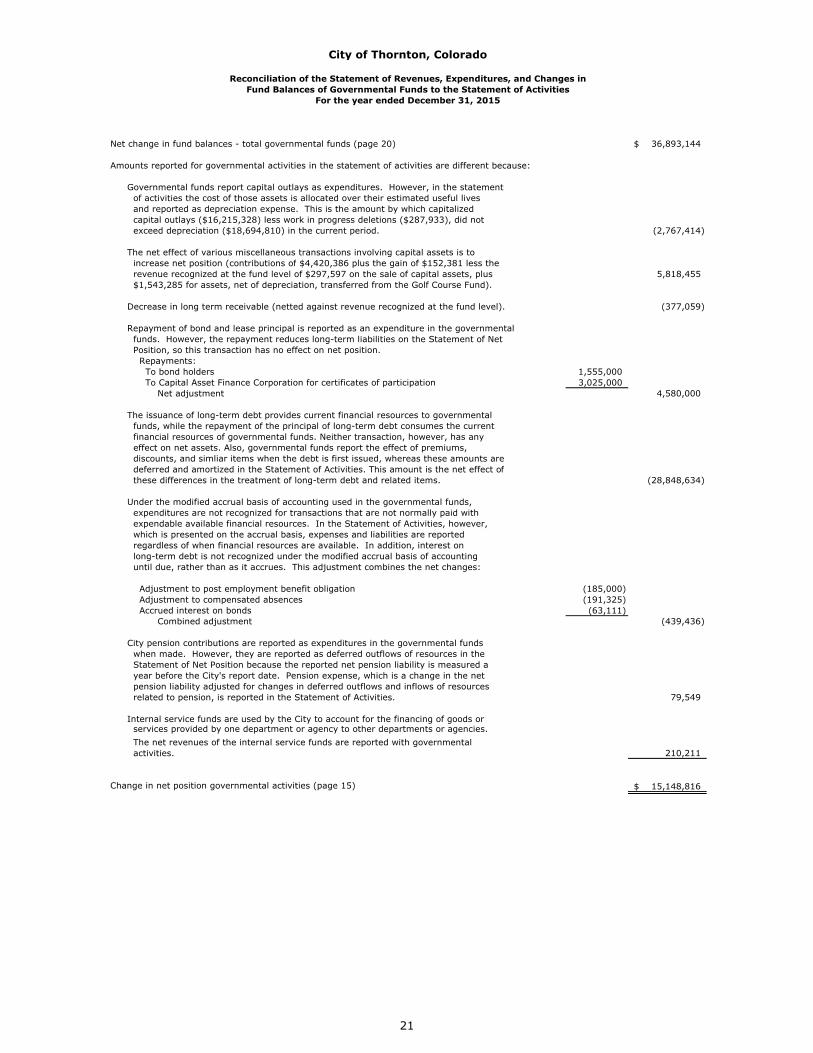

Reconciliation of the Statement of Revenues, Expenditures, and Changes inFund Balances of Governmental Funds to the Statement of Activities

For the year ended December 31, 2015

Net change in fund balances - total governmental funds (page 20) 36,893,144$

Amounts reported for governmental activities in the statement of activities are different because:

Governmental funds report capital outlays as expenditures. However, in the statement of activities the cost of those assets is allocated over their estimated useful lives and reported as depreciation expense. This is the amount by which capitalized capital outlays ($16,215,328) less work in progress deletions ($287,933), did not exceed depreciation ($18,694,810) in the current period. (2,767,414)

The net effect of various miscellaneous transactions involving capital assets is to increase net position (contributions of $4,420,386 plus the gain of $152,381 less the revenue recognized at the fund level of $297,597 on the sale of capital assets, plus 5,818,455 $1,543,285 for assets, net of depreciation, transferred from the Golf Course Fund).

Decrease in long term receivable (netted against revenue recognized at the fund level). (377,059)

Repayment of bond and lease principal is reported as an expenditure in the governmental funds. However, the repayment reduces long-term liabilities on the Statement of Net Position, so this transaction has no effect on net position. Repayments: To bond holders 1,555,000 To Capital Asset Finance Corporation for certificates of participation 3,025,000 Net adjustment 4,580,000

The issuance of long-term debt provides current financial resources to governmental funds, while the repayment of the principal of long-term debt consumes the current financial resources of governmental funds. Neither transaction, however, has any effect on net assets. Also, governmental funds report the effect of premiums, discounts, and simliar items when the debt is first issued, whereas these amounts are deferred and amortized in the Statement of Activities. This amount is the net effect of these differences in the treatment of long-term debt and related items. (28,848,634)

Under the modified accrual basis of accounting used in the governmental funds, expenditures are not recognized for transactions that are not normally paid with expendable available financial resources. In the Statement of Activities, however, which is presented on the accrual basis, expenses and liabilities are reported regardless of when financial resources are available. In addition, interest on long-term debt is not recognized under the modified accrual basis of accounting until due, rather than as it accrues. This adjustment combines the net changes:

Adjustment to post employment benefit obligation (185,000) Adjustment to compensated absences (191,325) Accrued interest on bonds (63,111) Combined adjustment (439,436)

City pension contributions are reported as expenditures in the governmental funds when made. However, they are reported as deferred outflows of resources in the Statement of Net Position because the reported net pension liability is measured a year before the City's report date. Pension expense, which is a change in the net pension liability adjusted for changes in deferred outflows and inflows of resources related to pension, is reported in the Statement of Activities. 79,549

Internal service funds are used by the City to account for the financing of goods or services provided by one department or agency to other departments or agencies. The net revenues of the internal service funds are reported with governmental activities. 210,211

Change in net position governmental activities (page 15) 15,148,816$

City of Thornton, Colorado

21

City of Thornton, Colorado

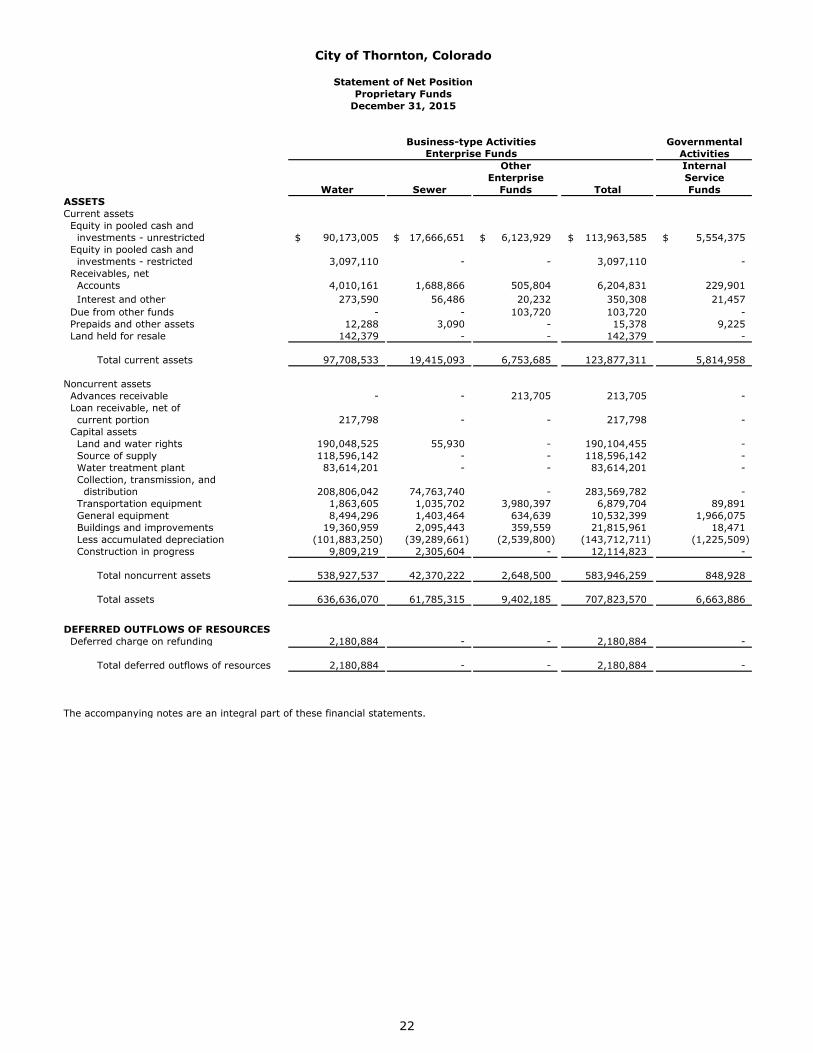

Statement of Net PositionProprietary Funds

December 31, 2015

Business-type Activities GovernmentalActivities

Other InternalEnterprise Service

Water Sewer Funds Total FundsASSETSCurrent assets Equity in pooled cash and investments - unrestricted 90,173,005$ 17,666,651$ 6,123,929$ 113,963,585$ 5,554,375$ Equity in pooled cash and investments - restricted 3,097,110 - - 3,097,110 - Receivables, net Accounts 4,010,161 1,688,866 505,804 6,204,831 229,901 Interest and other 273,590 56,486 20,232 350,308 21,457 Due from other funds - - 103,720 103,720 - Prepaids and other assets 12,288 3,090 - 15,378 9,225 Land held for resale 142,379 - - 142,379 -

Total current assets 97,708,533 19,415,093 6,753,685 123,877,311 5,814,958

Noncurrent assets Advances receivable - - 213,705 213,705 - Loan receivable, net of current portion 217,798 - - 217,798 - Capital assets Land and water rights 190,048,525 55,930 - 190,104,455 - Source of supply 118,596,142 - - 118,596,142 - Water treatment plant 83,614,201 - - 83,614,201 - Collection, transmission, and distribution 208,806,042 74,763,740 - 283,569,782 - Transportation equipment 1,863,605 1,035,702 3,980,397 6,879,704 89,891 General equipment 8,494,296 1,403,464 634,639 10,532,399 1,966,075 Buildings and improvements 19,360,959 2,095,443 359,559 21,815,961 18,471 Less accumulated depreciation (101,883,250) (39,289,661) (2,539,800) (143,712,711) (1,225,509) Construction in progress 9,809,219 2,305,604 - 12,114,823 -

Total noncurrent assets 538,927,537 42,370,222 2,648,500 583,946,259 848,928

Total assets 636,636,070 61,785,315 9,402,185 707,823,570 6,663,886

DEFERRED OUTFLOWS OF RESOURCES Deferred charge on refunding 2,180,884 - - 2,180,884 -

Total deferred outflows of resources 2,180,884 - - 2,180,884 -

The accompanying notes are an integral part of these financial statements.

Enterprise Funds

22

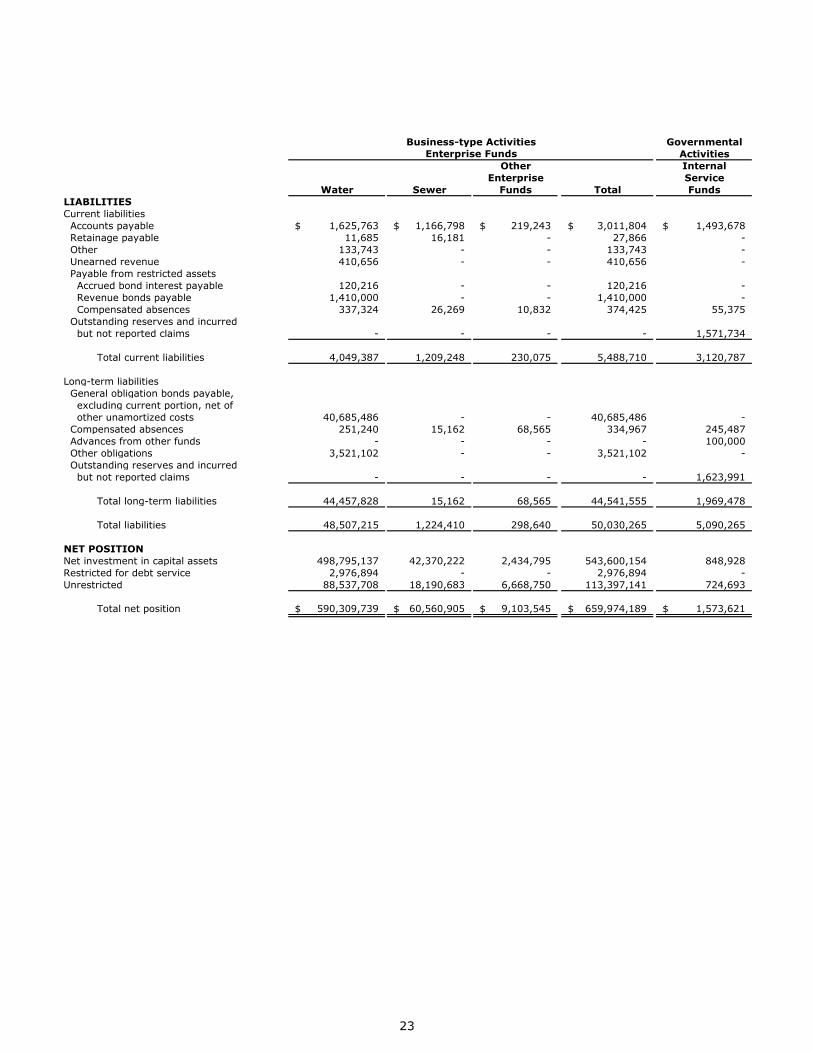

Business-type Activities GovernmentalActivities

Other InternalEnterprise Service

Water Sewer Funds Total FundsLIABILITIESCurrent liabilities Accounts payable 1,625,763$ 1,166,798$ 219,243$ 3,011,804$ 1,493,678$ Retainage payable 11,685 16,181 - 27,866 - Other 133,743 - - 133,743 - Unearned revenue 410,656 - - 410,656 - Payable from restricted assets Accrued bond interest payable 120,216 - - 120,216 - Revenue bonds payable 1,410,000 - - 1,410,000 - Compensated absences 337,324 26,269 10,832 374,425 55,375 Outstanding reserves and incurred but not reported claims - - - - 1,571,734

Total current liabilities 4,049,387 1,209,248 230,075 5,488,710 3,120,787

Long-term liabilities General obligation bonds payable, excluding current portion, net of other unamortized costs 40,685,486 - - 40,685,486 - Compensated absences 251,240 15,162 68,565 334,967 245,487 Advances from other funds - - - - 100,000 Other obligations 3,521,102 - - 3,521,102 - Outstanding reserves and incurred but not reported claims - - - - 1,623,991

Total long-term liabilities 44,457,828 15,162 68,565 44,541,555 1,969,478

Total liabilities 48,507,215 1,224,410 298,640 50,030,265 5,090,265

NET POSITIONNet investment in capital assets 498,795,137 42,370,222 2,434,795 543,600,154 848,928 Restricted for debt service 2,976,894 - - 2,976,894 - Unrestricted 88,537,708 18,190,683 6,668,750 113,397,141 724,693

Total net position 590,309,739$ 60,560,905$ 9,103,545$ 659,974,189$ 1,573,621$

Enterprise Funds

23

City of Thornton, Colorado

Statement of Revenues, Expenses and Changes in Net PositionProprietary Funds

For the year ended December 31, 2015

Business-type Activities GovernmentalActivities

Other InternalEnterprise Service

Water Sewer Funds Total FundsOPERATING REVENUES Charges for services pledged for debt 34,348,429$ 14,191,006$ -$ 48,539,435$ -$ Charges for services - - 5,024,225 5,024,225 - Interfund services - - - - 16,683,891

Total operating revenues 34,348,429 14,191,006 5,024,225 53,563,660 16,683,891

OPERATING EXPENSES Source of supply 6,298,970 - - 6,298,970 - Water treatment 9,747,700 - - 9,747,700 - Collection, transmission distribution, and trash removal 4,743,099 1,937,914 2,449,121 9,130,134 - Sewage treatment-Metro Wastewater - 8,226,526 - 8,226,526 - Insurance premiums - - - - 663,747 Claims and reserves for claims - - - - 2,849,136 Other operating expenses 1,362,858 143,418 626,605 2,132,881 6,634,243 Administration 5,494,540 1,381,349 1,355,861 8,231,750 6,111,047 Depreciation 6,438,273 2,025,762 370,318 8,834,353 316,379

Total operating expenses 34,085,440 13,714,969 4,801,905 52,602,314 16,574,552

Operating income 262,989 476,037 222,320 961,346 109,339

NONOPERATING REVENUES (EXPENSES) Gain (loss) on sale (disposal) of capital assets 4,951,898 51,013 35,630 5,038,541 (5,824) Interest income 1,321,463 163,733 68,178 1,553,374 63,662 Interest and bond amortization expense (1,827,304) (6,683) - (1,833,987) - Miscellaneous, net 3,822,599 13,012 9,222 3,844,833 43,034

Total nonoperating revenues 8,268,656 221,075 113,030 8,602,761 100,872

Income before capital contributions and transfers 8,531,645 697,112 335,350 9,564,107 210,211

Grants and capital contributions 13,658,648 2,256,491 - 15,915,139 - Transfers out - - (1,766,411) (1,766,411) -

Change in net position 22,190,293 2,953,603 (1,431,061) 23,712,835 210,211

Net position, January 1 568,119,446 57,607,302 10,534,606 636,261,354 1,363,410

Net position, December 31 590,309,739$ 60,560,905$ 9,103,545$ 659,974,189$ 1,573,621$

The accompanying notes are an integral part of these financial statements.

Enterprise Funds

24

This Page Left Intentionally Blank

25

City of Thornton, Colorado

Statement of Cash FlowsProprietary Funds

For the year ended December 31, 2015

Business-type Activities GovernmentalActivitiesInternalService

Water Sewer Total FundsCASH FLOWS FROM OPERATING ACTIVITIES Receipts from customers 33,602,114$ 14,062,803$ 5,007,332$ 52,672,249$ -$ Receipts from interfund services - - - - 16,699,137 Payments to suppliers (22,881,722) (10,955,369) (2,630,912) (36,468,003) (10,712,193) Payments to employees (7,155,711) (980,753) (1,755,815) (9,892,279) (5,545,200) Net cash provided by operating activities 3,564,681 2,126,681 620,605 6,311,967 441,744

CASH FLOWS FROM NONCAPITAL FINANCING ACTIVITIES Grant 569,591 - - 569,591 - Repayment from other funds 14,563,192 - 101,687 14,664,879 - Receipts from nonoperating leases 3,370,081 - - 3,370,081 -Net cash provided by noncapital financing activities 18,502,864 - 101,687 18,604,551 -

CASH FLOWS FROM CAPITAL AND RELATED FINANCING ACTIVITIES Purchases and construction of capital assets (8,678,098) (1,527,748) (562,216) (10,768,062) (276,739) Proceeds from sale of capital assets 5,090,231 52,460 35,630 5,178,321 1,011 Principal paid on bonds and other obligations (8,270,000) (295,000) - (8,565,000) - Principal paid on notes (41,284) - - (41,284) - Interest and fees paid on capital debt (1,520,334) (5,290) - (1,525,624) - Capital contributions 11,210,430 1,319,392 - 12,529,822 -Net cash used in capital and related financing activities (2,209,055) (456,186) (526,586) (3,191,827) (275,728)

CASH FLOWS FROM INVESTING ACTIVITIES Proceeds from sale of investments 28,196,797 6,388,769 2,242,565 36,828,131 2,435,641 Purchases of investments (47,273,110) (8,058,779) (2,473,199) (57,805,088) (2,675,282) Interest on investments 701,005 139,814 60,539 901,358 55,761 Net cash used in investing activities (18,375,308) (1,530,196) (170,095) (20,075,599) (183,880)

Net increase (decrease) in cash and cash equivalents 1,483,182 140,299 25,611 1,649,092 (17,864)

Cash and cash equivalents, Jan. 1 4,478,827 988,900 365,972 5,833,699 334,191

Cash and cash equivalents, Dec. 31 5,962,009$ 1,129,199$ 391,583$ 7,482,791$ 316,327$

Cash and cash equivalents 5,962,009$ 1,129,199$ 391,583$ 7,482,791$ 316,327$ Investments 87,308,106 16,537,452 5,732,346 109,577,904 5,238,048 Total cash and investments 93,270,115$ 17,666,651$ 6,123,929$ 117,060,695$ 5,554,375$

Equity in pooled cash and investments 90,173,005$ 17,666,651$ 6,123,929$ 113,963,585$ 5,554,375$ Restricted cash and investments 3,097,110 - - 3,097,110 -

Total cash and investments 93,270,115$ 17,666,651$ 6,123,929$ 117,060,695$ 5,554,375$

The accompanying notes are an integral part of these financial statements.

Enterprise Funds

26

OtherEnterprise

Funds

Business-type Activities GovernmentalActivitiesInternalService

Water Sewer Total FundsRECONCILIATION OF OPERATING INCOME (LOSS) TO NET CASH PROVIDED BY OPERATING ACTIVITIES

Operating income 262,989$ 476,037$ 222,320$ 961,346$ 109,339$

Adjustments to reconcile operating income to net cash provided by operating activities:

Depreciation expense 6,438,273 2,025,762 370,318 8,834,353 316,379 Miscellaneous receipts 452,609 13,012 9,222 474,843 42,023 Other expenses 4,700 - - 4,700 - Change in assets and liabilities: (Increase) decrease in accounts receivable, net (1,472,732) (141,215) (16,893) (1,630,840) 15,246 Decrease in notes receivable 39,872 - - 39,872 - (Increase) in other assets - (3,090) - (3,090) (9,225) (Increase) in inventory (12,288) - - (12,288) - Increase (decrease) in accounts payable (2,424,982) (237,578) 26,515 (2,636,045) (35,966) Increase (decrease) in other liabilities 29,925 (6,247) 9,123 32,801 3,948 Increase in unearned revenue 246,315 - - 246,315 -

Net cash provided by operating activities 3,564,681$ 2,126,681$ 620,605$ 6,311,967$ 441,744$

NON-CASH TRANSACTIONS: Water and sewer lines contributed by developers 1,878,627$ 937,099$ -$ 2,815,726$ -$ (Decrease) in the fair value of investments (55,333) (16,526) (4,771) (76,630) (4,810) Bond amortization expense (314,743) (2,647) - (317,390) - Loss on disposal of capital assets (138,333) (1,447) - (139,780) 5,824 Increase (decrease) in compensated absences 33,175 (6,247) 9,123 36,051 3,948

Enterprise Funds

27

OtherEnterprise

Funds

City of Thornton, Colorado

NOTES TO FINANCIAL STATEMENTS December 31, 2015

NOTE A - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The City of Thornton, Colorado (“the City”) was incorporated May 26, 1956. The citizenry voted to become a home rule city in 1967 under the provisions of Article XX of the Constitution of the State of Colorado. The City operates under a Council-Manager form of government and provides the following services, as authorized by its charter: public safety (police, fire, and ambulance), highways and streets, public improvements, water, sewer, and sanitation, culture and recreation, debt service and general administrative services, including financial, planning and zoning, and municipal court services.

The accounting policies of the City conform to accounting principles generally accepted in the United States of America as applicable to governments in accordance with those promulgated by the Governmental Accounting Standards Board (GASB). The following is a summary of the more significant policies:

1. Reporting Entity

The accompanying financial statements present the activities of the City and its four component units;organizations for which the City is financially accountable. These component units are so intertwined with the Citythat they are, in substance, the same as the City and, therefore, are blended and reported as if they were part ofthe City. None of the component units listed below report their financial statements independent from the City.

The management of the City has operational responsibility for each of the following component units, andtherefore, they are included within the reporting entity (in blended presentation):

Thornton Development Authority (TDA) - The TDA, an Urban Renewal Authority organized pursuant to Part 1,Article 25, Title 31 of the Colorado Revised Statutes, was established to finance the design and construction of theThornton Parkway highway interchange, as well as various other improvements within the TDA's boundaries. TheCity Council is the TDA's governing board. The debt of the TDA is disclosed as tax increment bonds, but is neithera general nor a limited obligation of the City. There are three urban renewal areas within the City, the SouthCapital Fund, the North Capital Fund, and the 144th Capital Fund. For ease of financial management, separatefunds were established for the improvements in each geographical area.