Embed Size (px)

Citation preview

S C H O O L B O A R D O F B R E V A R D C O U N T Y V I E R A , F L

COMPREHENSIVE ANNUALFINANCIAL REPORT

for the fiscal year ended June 30, 2007

w w w . b r e v a r d s c h o o l s . o r g

Introductory Section

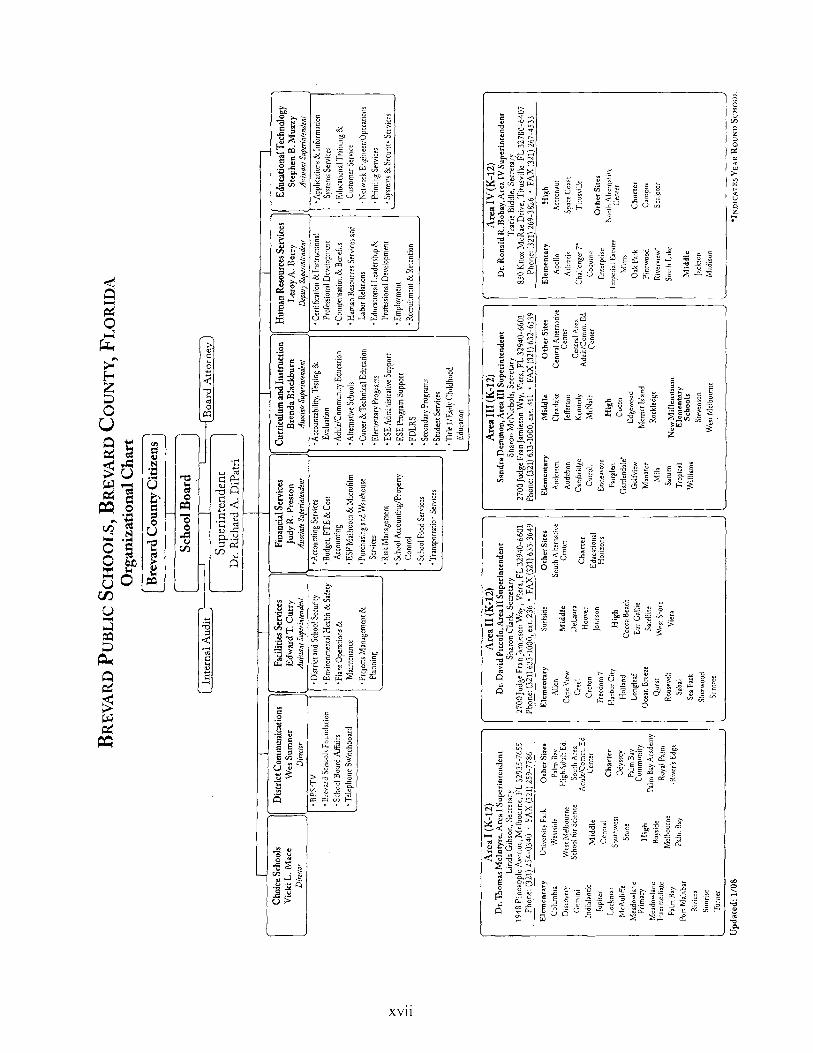

School Board of Brevard County2700 Judge Fran Jamieson Way • Viera, FL 32940-6601Richard A. DiPatri, Ed.D., Superintendent

Phone: (321) 633-1000, ext. 402 • FAX: (321) 633-3432

An Equal Opportunity Employer • A Drug-Free Workplace

January 28, 2008

Dear Chairman, Members of the Board, and the Citizens of Brevard County:

The Comprehensive Annual Financial Report of the School Board of Brevard County, Florida (the “School Board” or the “District”) for the fiscal year ended June 30, 2007, is hereby submitted. We believe the information, as presented, is accurate in all material aspects; that it is presented in a manner designed to set forth fairly, in all material respects, the financial position and results of operations of the District as measured and reported by the financial activity of its various funds; and that all disclosures necessary to enable the reader to gain an adequate understanding of the District’s financial affairs have been included. The responsibility for the preparation of the accompanying financial statements and other information contained in this report, based on the above standards, rests with the District’s management.

The Comprehensive Annual Financial Report is presented here in four sections: 1) introductory, 2) financial, 3) statistical, and 4) single audit. The introductory section includes this transmittal letter, lists of elected Board members and appointed officials, and an organizational chart. The financial section includes the basic financial statements, and the combining and individual fund financial statements and schedules, as well as required supplementary information. Also included in the financial section is the independent auditor’s report on these financial statements. The statistical section consists of unaudited tables, which reflect both financial and demographic data. This information is for the purpose of presenting social and economic information, financial trends, and fiscal capacity of the District, and is generally presented on a multi-year basis.

The District is required to undergo an annual single audit in conformity with the provisions of the Single Audit Act of 1996 and the United States Office of Management and Budget (“OMB”) Circular A-133, Audits of States, Local Governments and Non-Profit Organizations. Information related to this single audit, including the schedule of expenditures of federal awards, findings and questioned costs, and the independent auditor’s report on internal control and compliance with applicable requirements, are included in the single audit section.

Generally accepted accounting principles used in the United States of America also require that management provide a narrative introduction, overview, and analysis to

accompany the basic financial statements in the form of Management’s Discussion and Analysis (MD&A). This letter is designed to complement the MD&A and should be read in conjunction with it. The MD&A can be found immediately following the report of the independent auditors.

The report includes all funds of the District, the Brevard County School Board Leasing Corporation, the Brevard Schools Foundation, and the District’s Charter Schools, which comprise the reporting entity. The Brevard County School Board Leasing Corporation was formed by the School Board to be the lessor in connection with financing the acquisition and/or construction of certain educational facilities. The Brevard Schools Foundation’s purpose is exclusively educational and charitable for the constituents of Brevard County. Charter schools are public schools operating under a performance contract with the School Board. The Brevard County School Board Leasing Corporation was identified as a component unit, requiring blended presentation of the financial statements. The Brevard Schools Foundation and the District’s Charter Schools are included as discretely presented component units.

GENERAL INFORMATION

The District and its governing board were created pursuant to Section 4, Article IX of the Constitution of the State of Florida. The District is an independent taxing and reporting entity managed, controlled, operated, administered, and supervised by the District school officials in accordance with Chapter 1001, Florida Statutes. The Board consists of five elected officials responsible for the adoption of policies, which govern the operation of the District’s public schools. The Superintendent is also specifically delegated the responsibility of maintaining a uniform system of records and accounts in the District by Section 1010.01, Florida Statutes, as prescribed by the Florida Legislature.

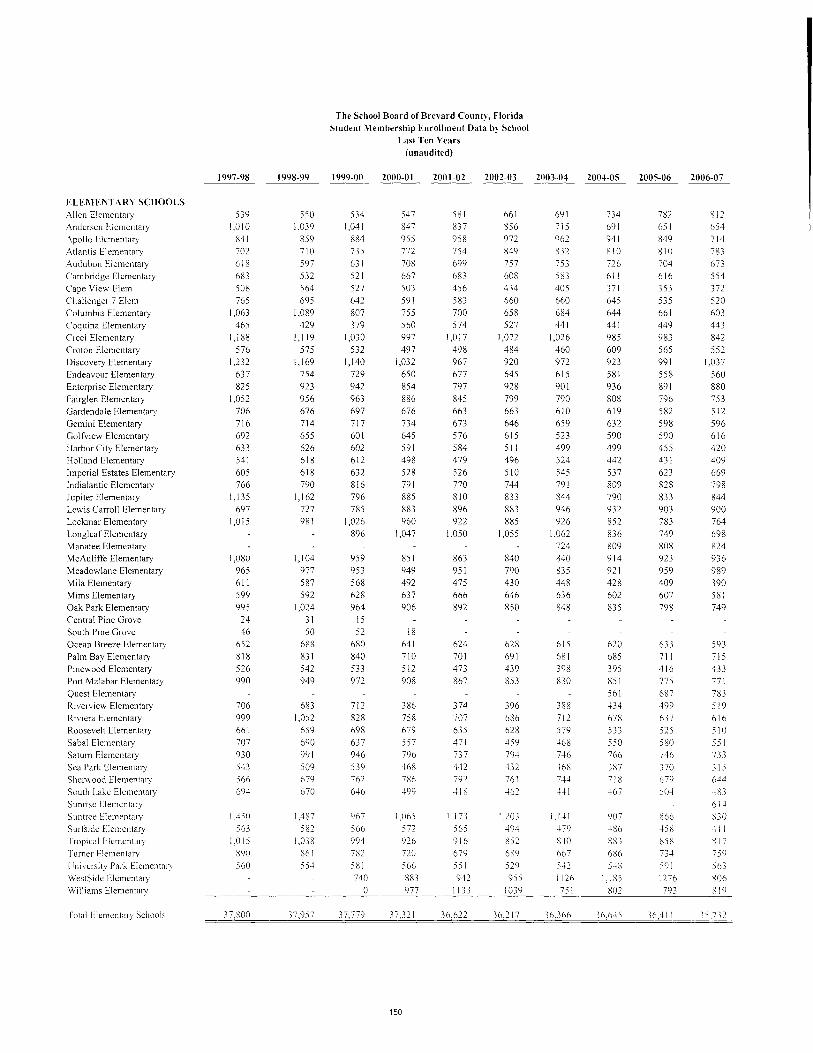

The geographical boundaries of the District are those of Brevard County. During the 2006-07 fiscal year, the District operated 97 schools, including 57 elementary schools, 12 middle schools, 4 Jr/Sr schools, 11 high schools, and 13 charter schools and reported approximately 73,813 unweighted full-time equivalent students. Additionally, the District operated 14 special centers for students and 4 separate adult education centers.

GENERAL DESCRIPTION AND LOCATION

Brevard County encompasses approximately 1,300 square miles along the Atlantic Ocean and is located in the middle of Florida’s East Coast. The County is 72 miles long north to south and is bordered on the north by Volusia County and on the south by Indian River County. The county extends about 20 miles inland from the Atlantic Ocean, with the St. Johns River forming its western boundary. The County is home of the Kennedy Space Center and the Space Shuttle Program. The Titusville-

ii

Melbourne-Palm Bay Metropolitan Statistical Area contains 15 municipalities, but the county has a large amount of unincorporated area representing approximately 39% of the population.

ECONOMIC CONDITIONS AND OUTLOOK

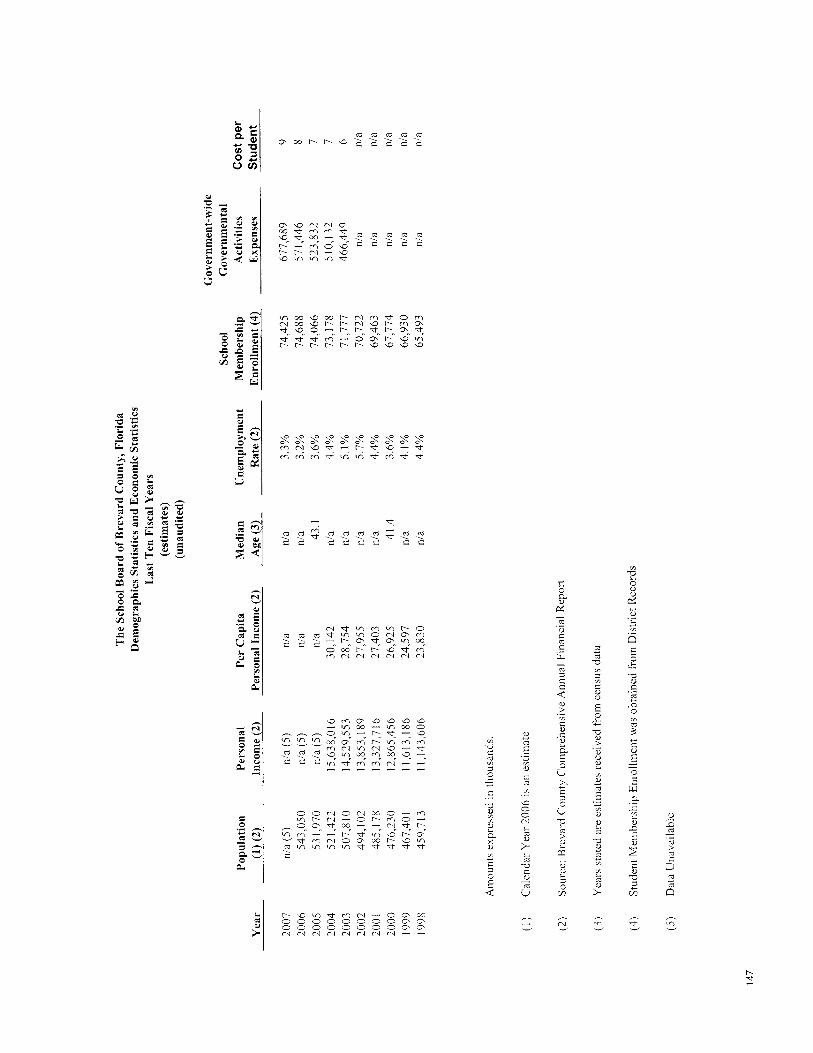

The county continues to experience rapid population growth, increasing 46% during the 1980s and an estimated 36.1% since 1990 to a population of 543,050 for 2006 (estimate). Population growth is projected to increase an additional 6% through 2030, to approximately 757,544. Approximately 23% of the population in the county is between the ages of 25-44 years, with approximately 28% below the age of 25, and 49% above the age of 44.

The presence of NASA and a number of high-tech manufacturing employers drive the economy. The county is diversifying from its heavy dependence on the space program and related industries to smaller manufacturing–based businesses and a growing tourism and service sector. Wealth levels approximate those for the State and nation, and the unemployment rate has generally been lower than the State and national rates. The annual unemployment rate has decreased from 5.7% in 2002, to 4.4% for 2004, and 3.6% in 2005. As of June 2006, the unemployment rate for the county was 3.2%, as compared to the State unemployment rate of 3.3%, and the national rate of 4.8%.

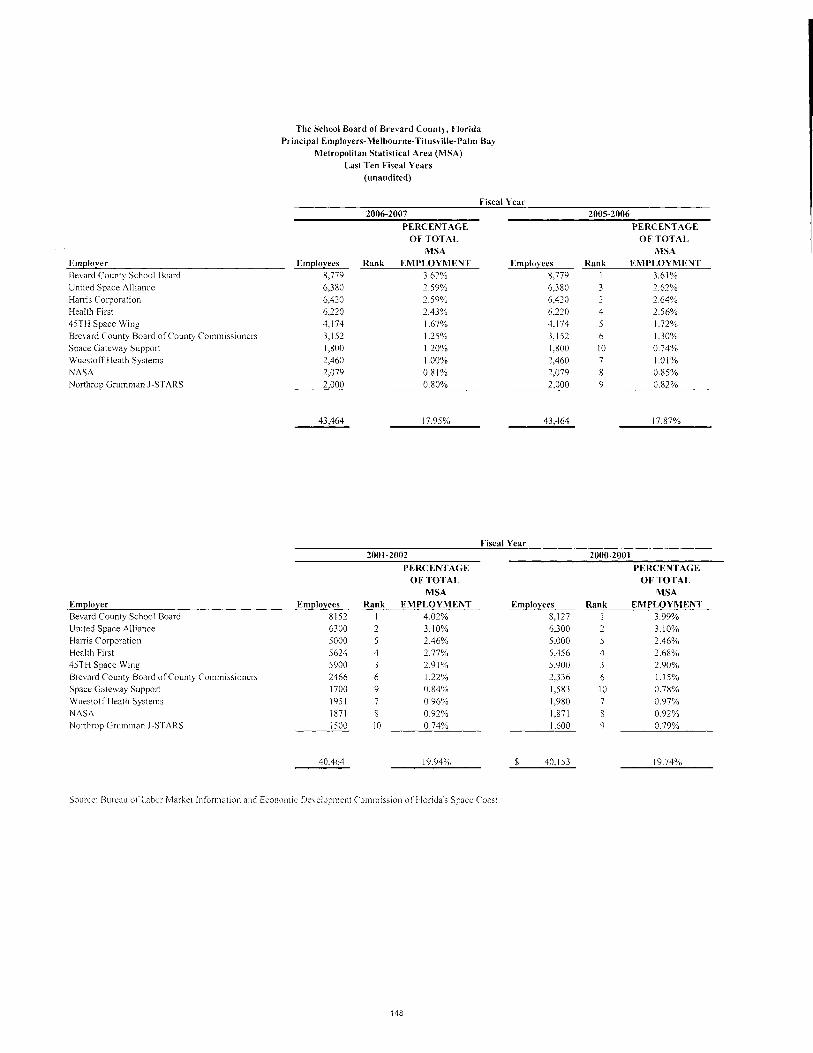

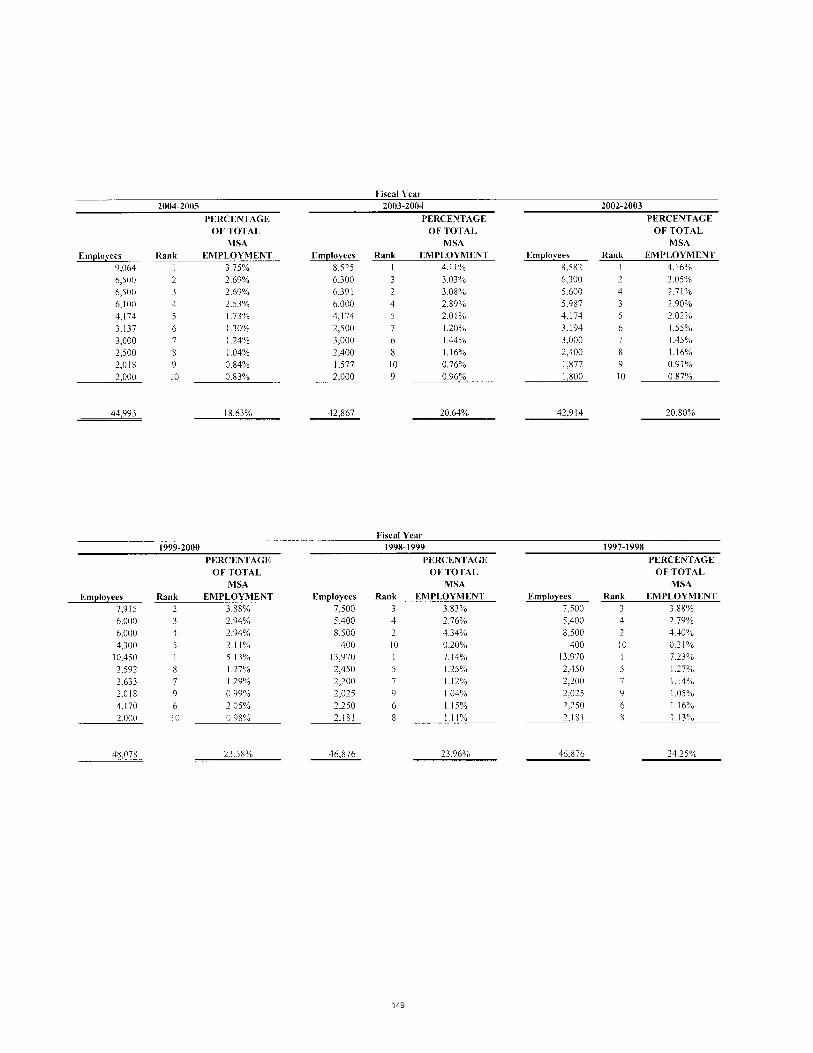

Major private employers include Harris Corporation, United Space Alliance, Health First, Space Gateway Support, Wuestoff Health Systems, Northrop Grumman Corporation, The Boeing Corporation, Intersil Corporation, and Lockheed Martin – Space Systems Company.

MAJOR INITIATIVES

Governor’s Sterling Award – On October 24, 2007, Governor Crist announced that Brevard Public Schools had earned the 2007 Governor’s Sterling Award. The award recognizes organizations and businesses in Florida that have successfully achieved performance superiority within their management and operations. Each winner undergoes an in-depth assessment and evaluation by an expert team of examiners conducting an on-site review. In the 15 years that the award has been presented, BPS is only the second school district to receive the honor at the district level. The last district selected was Pinellas County in 1993.

Class Size Reduction Amendment – In November 2002, the voters of Florida amended the State constitution to limit class size. By the beginning of the 2010-11 school year the amendment established the maximum number of students in core-curricular courses assigned to a teacher in each of the following three grade groupings: (1) Prekindergarten through grade 3, 18 students; (2) grades 4 through 8, 22 students and (3) grades 9 through 12, 25 students. Beginning in 2003-04 fiscal

iii

year, the Legislature began to provide funds to districts to address class size. Brevard Public Schools has a long tradition of making appropriate class size a priority objective, and, as a result, our district average class size was already very close to the amendment mandate. During school year 2004-05, Brevard met the Constitutional mandates at the district average for all grade levels. During school year 2005-06, funded units were used to maintain the mandates at the district average and to begin to address bringing the average class size at individual schools to the required level. For school year 2006-07, all Brevard schools met the Constitutional mandate, at the more restrictive level of the school average, one year in advance of the actual requirement. For the 2007-08 school year, all schools are expected to maintain the Constitutional requirements at the level of the school average.

Every School an “A” – This initiative continues to provide individual schools with in-depth support from the Curriculum Division in order to achieve an "A" grade, as awarded by the state based on a school’s performance on the Florida Comprehensive Assessment Test (FCAT). In fiscal year 2007, 81 of the 84 (96%) Brevard schools received an A or B in the Florida grading system. District resources in terms of personnel and funding have been directed toward supporting the efforts of all schools to obtain an "A" status. Our focus areas for fiscal year 2008 include science, writing, and intensive reading for students who are below grade level and the primary grades. In 2007 our students had the highest average FCAT scores in the state in 6th grade math, 6th grade reading, 5th grade science and 11th grade science.

Desktop Data Reporting System and Data Dashboard – The Desktop Data Reporting System brings student test score data, demographic information and discipline data on an individual student or a class of students directly to the teacher's desk. Schools have had the availability of grouping student data by teacher, class period, levels of performance, etc. for a number of years, but the process was not easy and the documents were sometimes difficult to read. Now, teachers can bring up their former classes during preplanning and see how their students did on the FCAT at the end of the last school year. The teacher can then request the same data on their current class of students to plan instructional strategies. This information is critical to effective teacher planning in order to incorporate strand skills into classroom instruction, to effectively implement the teacher's Professional Development Plan, and to develop meaningful strategies for Pay for Performance. New reports are added regularly in response to school and district requests. All stakeholders have access to Brevard’s Data Dashboard. The Data Dashboard provides quick and easy access to district and school reports for multiple years in areas such as school grades, Scholastic Aptitude Test results, Advanced Placement results, and Dual Enrollment statistics. Links to frequently used state websites are also included.

BPS Scorecard – The BPS Scorecard, unveiled in October, 2007, is an outgrowth of the Results category of the district’s application for the Governor’s Sterling Award. This online accountability tool shows current and past trendline data for key outcome measures relative to an appropriate comparison or benchmark. Although the majority of the measurements reflect student achievement data, the BPS scorecard also includes data for our primary support areas, including human resources, facility

iv

planning and construction, information technology and financial management. Scorecards were developed for each of Brevard’s 84 schools as well as for the district and are available to all stakeholders through Brevard’s home page at http://www.brevard.k12.fl.us/.

SOAR – The 2007 SOAR (Summer Opportunities for Advancement and Remediation) program served more than 16,000 elementary, middle, and high school students with academic deficiencies. The summer program was offered to K-12 students working below grade level in reading and mathematics, and to middle and high school students who needed credit-bearing courses in English and mathematics. During SOAR 2007, a variety of enrichment courses were also offered to elementary, middle, and high schools students. Middle school students had an opportunity to participate in Kids Career Camps and high school students had opportunities to enroll in Brevard Virtual School, Career and Technical Education courses, and Dual Enrollment. Students who live beyond a two-mile limit from their home school were offered transportation. Principals have reported that transportation made a tremendous difference in participation. Child Care services were available for all elementary students attending SOAR. Breakfast and lunch was served in all of our elementary and at many of our secondary sites. The SOAR program got positive reviews from parents, students, teachers and administrators. This gift of time has the potential to make a significant difference for student achievement and, of course, students who achieve tend to be more positive about the entire school experience.

Secondary Schools of National Prominence – Continuing the focus on increased rigor, relevance and relationships for all secondary students, Brevard completed the planning phase and began the transition to full implementation of the first year of Secondary Schools of National Prominence (SSNP) before the end of the 2006-07 school year. All secondary schools were allocated sufficient instructional units to implement a seven period day or block schedule in 2007-08. In addition, all middle schools were allocated a guidance services professional and guidance clerk to support the completion of an Individualized Program of Study for every seventh grader by October 15, 2007. All middle school counselors participated in focused staff development to learn a common protocol for the parent, student and guidance counselor meetings and received parent information materials to distribute at each individual meeting.

Two new courses were developed to meet the increased graduation requirements of SSNP: Middle School Career Exploratory Course (7th grade) and Career Research Decision Making (9th grade). After developing curriculum guides that met the unique requirements of SSNP, course materials and textbooks were ordered, and professional development workshops were offered to all 7th and 9th grade teachers who scheduled to teach the summer pilot program. During the summer program, 40 teachers at 14 middle schools offered the Middle School Career Exploratory Course, and 20 teachers at 11 schools offered Career Research Decision Making, serving over 800 secondary students in June 2007.

v

In addition, high school schools completed planning, professional development and recruitment for additional Small Learning Communities: eight career academies, two Collegiate High School programs, one International Baccalaureate (IB) program and one Advanced International Certificate of Education (AICE) program. To further prepare secondary schools to create and successfully implement additional Small Learning Communities, school leadership teams attended the first of four sessions presented by Southern Regional Education Board (SREB) on Small Learning Communities to insure the use of a common vocabulary and the implementation of best practices that will lead to a high performing learning culture. The implementation of Brevard’s SSNP initiative is well underway to create a generation of students who are prepared to be successful in the work place, in further education and/or in postsecondary degree opportunities.

Career and Technical Education (CTE) – Career and Technical Education programs, including opportunities for expanded program options and the development of Career Academies, are a central piece of Brevard’s Secondary Schools of National Prominence initiative. The requirements for graduation for the Class of 2011 include a requirement that all students either complete three credits in accelerated programs or a series of three Career and Technical credits in a sequential program. This goal supports our focus on the expansion of industry credentialing and a review of our programs for capacity to ensure access for students. Program enhancements in CTE are accomplished through the use of Carl Perkins Vocational and Technical Education Improvement Act federal funds and district funding. Investments have been made to upgrade CTE programs and to address the Brevard Public Schools Strategic Plan priority objective for industry-certification of CTE high school programs. Highlights of this major effort include national certification by the American Culinary Federation (ACF) of all four high schools. Satellite High School’s recent national certification by NATEF makes Brevard Public Schools First in Florida in two CTE program areas with the highest number of ACF certified culinary arts and NATEF auto programs in any Florida school district. The American Drafting and Design Association also certified seven drafting programs this past school year.

Another primary focus for career and technical education focused on middle schools. All seventh grade students will take part in a new career wheel course initiated as a component of the Secondary Schools of National Prominence. These students will move through three career and technical education offerings. In addition, they will investigate different careers and take a personal career inventory to determine their individual career interests. Students in seventh grade will begin planning their high school experiences and develop an Individualized Program of Study.

K-12 Comprehensive Reading Program – Brevard Public Schools' comprehensive reading plan was updated during the 2006-07 school year. The plan outlines instructional expectations for K-6 classrooms as well as Intensive Reading classrooms at the secondary level. In the elementary schools, the core reading program is delivered within an uninterrupted ninety minute block with additional immediate intensive intervention required for those students with documented deficiencies in

vi

reading. At the secondary level, those students who score Level I or II on the FCAT are required to receive reading intervention within a tiered system ranging from 45 minutes to 90 minutes of reading above their required English course. Ongoing progress monitoring is embedded within all grade levels. Brevard Public Schools has an assessment schedule that includes DIBELS and FORF testing as well as Scholastic Reading Inventory testing three times a year.

In order to provide school based support for the reading programs there are reading coaches or "experts” in each of our traditional schools. There is a tiered approach to the coaches as well. Schools have been prioritized according to their numbers of students with reading deficiencies. Reading coaches build capacity for reading expertise, support and mentor the instructional staff. Principals at schools with minimal numbers of students with reading deficiencies will appoint a reading “expert” to assist the administrative team with building capacity within the school. All schools will continue to implement the comprehensive reading plan during the 2007-08 school year.

K-12 Science – As the home of the Kennedy Space Center and NASA, residents have high expectations for science instruction. Lagoon Quest, Space Week and Blast are “being there experiences” that capitalize on Brevard’s strategic location and the interest of the community in creating the next generation of scientists. Brevard students regularly perform at exemplary levels in science competition as evidenced by the number of winners in state, national and international science fairs. During 2006-07 major instructional emphasis was placed on using student inquiry to address the Sunshine State Standards for Science. Professional development, teacher-developed documents, and onsite assistance was available for all science teachers. A district strategic plan objective has been established to create a science lab for every elementary school and the seven-year facilities plan includes a financial commitment to renovate existing secondary science labs. Computer projection systems were provided in every science classroom. As a science community Brevard Public Schools are proud of the many opportunities, including science research classes, science fairs and robotics teams that exist for students to be involved in hands-on science activities.

During 2006-07 Elementary Programs continued to support schools and teachers in the strategic plan goal of “a quality science program in every school.” Initiatives focused on increasing high-quality hands-on, minds-on inquiry experiences for all K-6 students. The Scott Foresman Science program was adopted and implemented K-6. To support the implementation, two documents were created by a team of teachers: CSI: BREVARD Teacher Resource Guide and CSI: BREVARD K-6 Assessment Package. These resources were provided to all schools and many training opportunities were offered to teachers. An additional resource was created, and teacher training offered, in response to our county’s low scores on performance task items from Grade 5 FCAT Science. This TASK-Force Guide–Level 5 addresses performance task writing skills along with the science content that could be assessed with Short or Extended Response FCAT items.

vii

Elementary school leaders received training on science best practices and created Science Plans to improve their science programs and FCAT Science scores. Among the best practices that schools included in their plans were: data analysis, use of Point of Contacts as leaders, integrating science with reading, establishing science committees, improving grade level articulation, increasing Science Fair participation, classroom walk-throughs, and an increased focus on science benchmark instruction, vocabulary development, and performance task writing.

Science results were outstanding. Feedback from schools is very positive toward the resources, training and initiatives implemented. More students are more involved in high-quality science experiences. Brevard students excel in science as demonstrated by being First in Florida on FCAT science for grades five and eleven for the second year, and fifth in the state in the score for 8th grade students. Florida’s A++ Plan added science proficiency to the criteria for the school grade in 2007.

K-12 Comprehensive Writing Program – Brevard continues to review writing results and to refine our approaches to improving student writing as measured by the FCAT Writing +. In October 2006, a new position was created to support elementary writing in grades K-6. The county now has two writing resource teachers, elementary K-6 and secondary 7-12, to support teachers and enhance writing instruction. After identifying specific grade level needs, the resource teachers set up numerous workshops and inservices to support writing instruction. Workshops included topics such as writing mechanics, elaboration, Six Traits, and holistic scoring.

New writing publications were produced to support writing instruction. Developing Ideas (35 elementary elaboration lessons), Mastering Ideas (secondary edition), Developing Writing + Skills (10 lessons each on planning, revising passages, cloze procedures, and conventions for elementary that emulate the actual FCAT Writing + Test) and Mastering Writing + Skills (secondary edition that is a reference guide for teachers on punctuation, capitalization, usage, sentence structure, irregular verbs, prefixes, homonyms, and an overview of FCAT Writing+) were created. Also a parent brochure was created to explain the FCAT writing test for elementary students.

Brevard County scores for 2006-07 were above the state average in the essay portion of the test for grades 4, 8, and 10. Scoring above a 3.5, grades 4 and 10 were above the state average. However, all grades 4, 8, and 10 improved their scoring in the category “3.5 and above” from 2006 to 2007. Fourth grade went from 76% to 78%, eighth grade went from 83% to 86%, and tenth grade went from 78% to 79%. Gains were also noted for grade 8 for their combined essay score. Grade 8 went from a 4 to a 4.1. Grade 10 stayed at 4.1 and grade 4 had a decrease from 4.0 to 3.9.

Brevard County continues to assess students in grades 2-6 four times a year and grades 7-10 twice a year with district-created assessments that include essay and multiple choice questions.

viii

Elementary Mathematics – A mathematics resource for elementary teachers, “Teaching Tools for Mathematics,” was developed for implementation during the 2006 – 07 school year. This document contains activities that focus on developing students’ critical thinking skills while providing practice to reinforce basic skills and concepts.

Workshops were conducted to provide teachers with the opportunity to experience and explore these activities. These workshops were very well attended and teachers were motivated and anxious to implement these activities in their classrooms. Various activities from “Teaching Tools for Mathematics” have also been shared with elementary mathematics contact teachers as well as elementary assistant principals.

An addendum to the Teaching Tools was developed to augment the activities in “Teaching Tools for Mathematics” by focusing on oral and written communication targeting the three higher levels of Bloom’s Taxonomy. Sample questions and recording sheets that will promote discussion to encourage higher-order thinking in mathematics classroom have been included. The goal is for students to question and debate as they become more comfortable with discussions.

Secondary Mathematics - A primary focus for secondary mathematics during the 2006-07 school year centered on identifying essential elements of the mathematics curriculum, teacher training at every secondary school, particularly in the area of FCAT performance task items, and the use of item analysis information to plan instruction in the mathematics classroom. Workshops addressing the use of the graphing calculator to improve teacher content knowledge focused on middle school mathematics teachers. Prioritizing Algebra 2 content skills workshops resulted in a teacher created revised curriculum guide identifying best practices for Algebra 2 and Algebra 2 Honors promoting standards-based instruction. The mathematics community continues to work through feeder system vertical teams to identify essential curriculum in all mathematics courses offered to Brevard students. Brevard students perform at the highest levels in the state in mathematics as evidenced by the fact that all grade levels tested in FCAT Mathematics in 2007 ranked in the top six in the state with the exception of third grade.

“Being There Experiences” – Special experiences that support the curriculum and the Sunshine State Standards are now provided systematically by grade level for students. The experiences capitalize on the vast resources available in our community. Every fourth grade student participates in a field experience in LAGOON QUEST to study our unique lagoon estuary system. Every fifth grade student participates in the BREVARD SYMPHONY ORCHESTRA PROGRAM and attends a performance at the King Center. Every sixth grade student participates in our SPACE WEEK program at the Kennedy Space Center for a day. Every seventh grade student participates in Project BLAST at the Astronaut Hall of Fame in simulated space activities. Select middle schools are piloting Project SEINE in which 8th grade students participate in a study of the history and flora and fauna of the Indian River Lagoon. This is in cooperation with the Brevard County Zoo and the Brevard County Parks Department. Every eleventh grade student attends a live

ix

performance in the form of a play, with the 2008 play being 1776. Plans are in the works to take an entire grade level to the Brevard Zoo. The ultimate goal is to provide a different “Being There Experience” for every grade level.

Music Demonstration Schools – Brevard is home to some of the finest music programs available as proven by the selection of twenty schools as Music Demonstration Schools, the highest number in any district in the state. In fact, Brevard County is home to twenty of the twenty-eight Music Demonstration Schools in the state. Our elementary, middle/junior, and high schools balance diversity, high performance standards, and instructional quality in music education. Our students have been invited to compete in major national and international music festivals and this designation is just one more indication of their success. Our ongoing efforts for improvement include the integration, in every school, of the standards of excellence required to be a Music Demonstration School.

Graduation Rate and Dropout Rate – For 2005-06 (latest available data) Brevard had a graduation rate of 90.7%, the second highest in the state, and at 0.8% Brevard’s dropout rate is the lowest in the state. This data supports our commitment to serving every student with excellence as the standard.

Adult and Community Education – The Office of Adult and Community Education provides educational service to adult students in four major centers, numerous outreach centers throughout the county, and before and after school age child care in 58 elementary schools. In addition to budgeted funding sources, Adult and Community Education is the recipient of several federal grants including a local Geographical Allocation, English Literacy and Civics local activities grant, state leadership projects, and a 21st Century Community Learning Center project. The Geographical Allocation makes it possible to expand and enhance local adult education programs. The English Literacy and Civics projects benefit adult students who have limited English proficiency. State leadership projects include acting as the fiscal agent for the statewide Adult High School and VPI Committee of the Practitioners Task Force, and the Region III Professional Development Advisory Council. The 21st Century Community Learning Center project is a partnership among Adult and Community Education, District School Age Child Care, the Brevard Zoo, Endeavour Elementary and Cambridge Elementary Schools, and the Brevard Museum. Students are also being served through online opportunities in adult basic education and GED. In the 2006-07 school year, 541 students received a high school diploma through Brevard’s GED preparation programs and 219 received an Adult High School diploma.

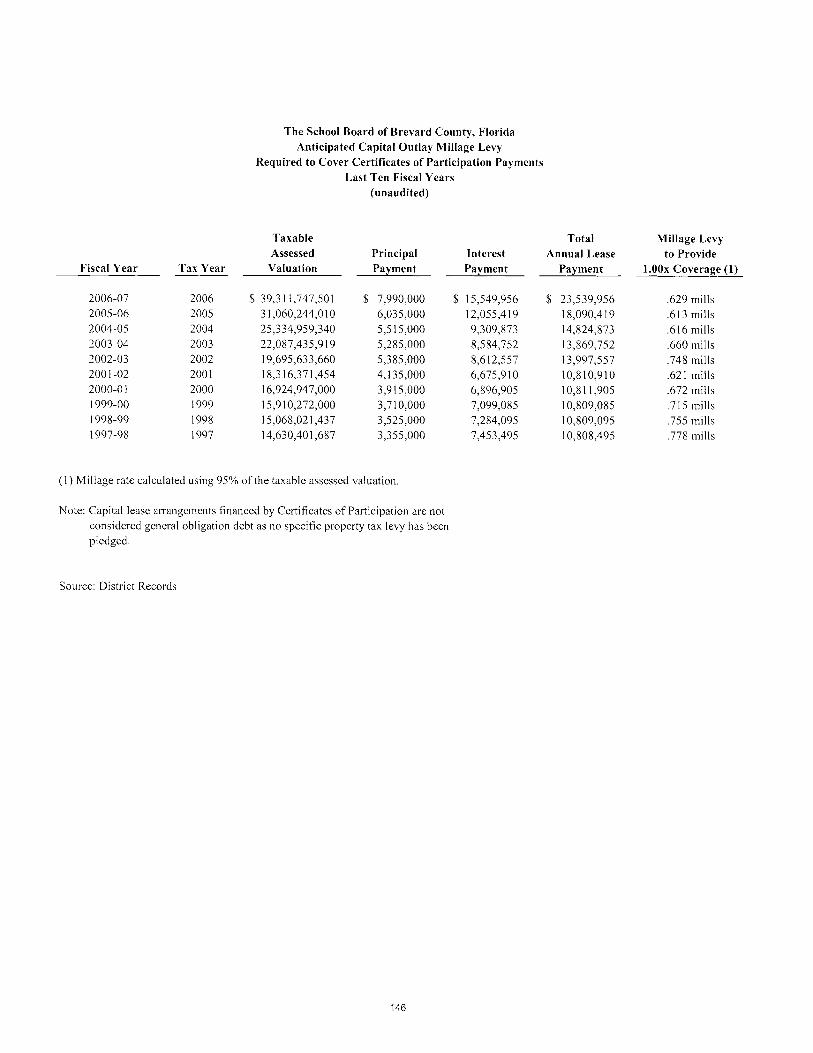

Seven-Year Facilities Improvement Plan - During the 2004-05 school year, the School Board approved a $715 million, seven-year facilities improvement plan. The plan included the construction of seven new schools, 28 additions, competitive sports facility upgrades, the completion of the District’s re-roofing program, infrastructure renewal / upgrades at 80 schools and acquisition of future school sites. Funding for the plan included the issuance of Certificates of Participation (COP) in each of the first four years, with the debt service projected to never be above the Board policy of

x

one mill. State law allows up to one-and-a half mills to be used for debt service on capital projects. During the 2005-06 school year, the School Board issued $128.44 million in COPs to proceed with the projects planned for Year One. During the 2006-07 school year, the School Board issued $ 194.35 million in COPs to proceed with the projects planned for Year Two. This initiative will continue through 2011-12.

FINANCIAL INFORMATION

Internal Control - Management of the District is responsible for establishing and maintaining an internal control system designed to ensure that the assets of the District are protected from loss, theft, or misuse and to ensure that adequate accounting data is compiled and recorded properly to allow for the preparation of financial statements in conformity with generally accepted accounting principles. The internal control system is designed to provide reasonable, but not absolute, assurance that these objectives are met. The concept of reasonable assurance recognizes that: (1) the cost of control should not exceed the benefits likely to be derived, and (2) the valuation of costs and benefits requires estimates and judgements by management. Management believes that the internal controls of the District adequately meet the above objectives.

Single Audit - As a recipient of Federal and State financial assistance, the District is also responsible for ensuring that adequate internal controls are in place to ensure compliance with applicable laws and regulations related to those programs. These internal controls are subject to periodic evaluation by management and the independent auditors.

Budgetary Controls - The District maintains budgetary controls. The objective of these budgetary controls is to ensure compliance with legal provisions embodied in the annual appropriated budget approved by the School Board. Activities of the General Fund, Special Revenue Funds, Debt Service Funds, Capital Projects Funds and the Internal Service Funds are included in the annual appropriated budget. Project-length financial plans are adopted for the Capital Projects Funds. Budgetary control is established at the level of individual accounts or groups of accounts within each school or department.

Budgetary information is integrated into the accounting system and, to facilitate budget control, budget balances are encumbered when purchase orders are issued. Appropriations lapse at year-end and encumbrances are re-appropriated as part of the subsequent year’s budget.

In order to provide budgetary control for salaries, the District utilizes a centralized position control system. On an annual basis, the Board adopts a District staffing plan that establishes teaching positions based on student populations served. Additionally, support and administrative positions are allocated based on established criteria.

xi

As demonstrated by the statements and schedules included in the financial section of this report, the District continues to meet its responsibility for sound financial management.

Cash Management and Investments - To maximize interest earnings on short-term investments, the cash balances of all funds are pooled, except where separate cash and investment accounts are maintained in accordance with legal requirements. Investment portfolios are designed with the objective of attaining a market rate of return throughout budgetary and economic cycles, taking into account the investment risk constraints and liquidity needs. Return on investment is of least importance compared to the safety and liquidity objectives. The core of investments is limited to relatively low risk securities in anticipation of earning a fair return relative to the risk being assumed.

All temporary cash balances of the District are invested to ensure maximum interest earnings. The District has an agreement with a local financial institution that provides for all cash deposits, including the District’s float, to be invested in overnight collateralized money market funds. Other temporary cash balances are invested in authorized investments, which include United States Government Securities, United States Government Agencies, Federal Instrumentalities, Florida Local Government Surplus Funds Trust Fund (SBA), Interest Bearing Time Deposits, Commercial Paper, and Bankers’ Acceptances.

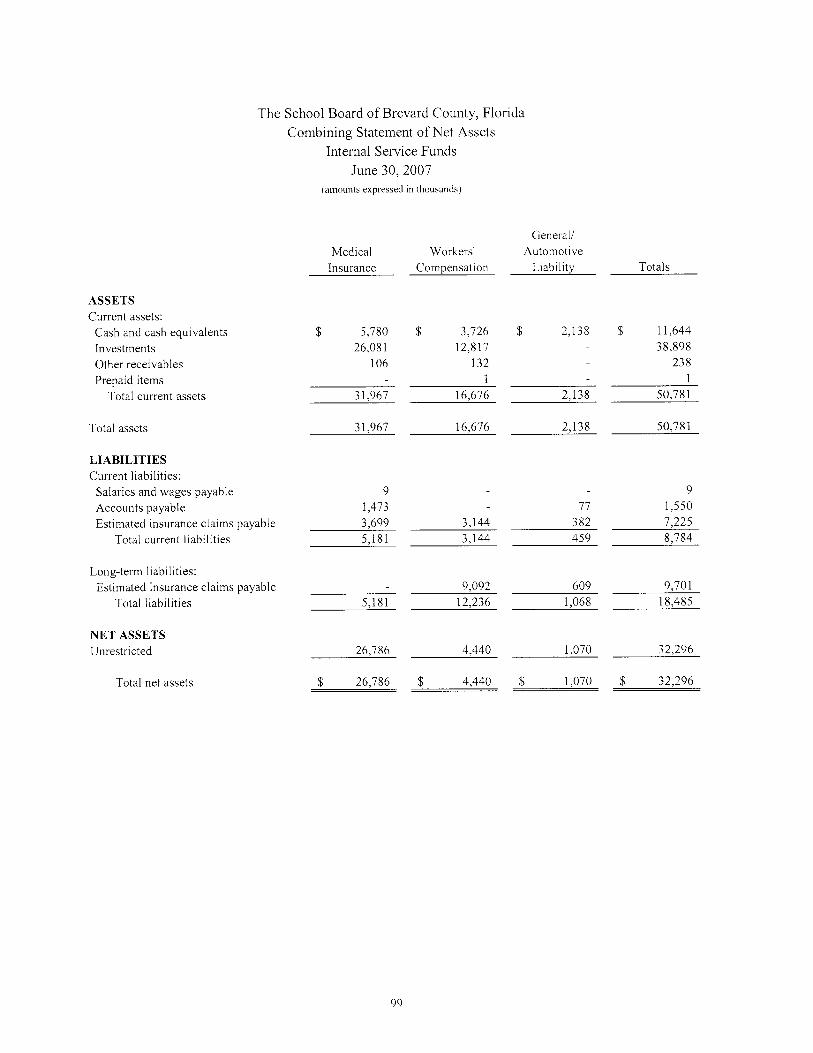

Risk and Benefits Management - Due to the exposure for financial losses associated with the District’s operations, the School Board of Brevard County continues to maintain a comprehensive Risk Management program. The District self-insures its program for Workers’ Compensation (to a maximum payment of $500,000 per claim) and General Liability and Auto Liability (to the maximum allowable under the State’s Sovereign Immunity Caps), and employs a third-party administrator to perform the claims administration for the self-insured exposures. The other risks such as property losses, boiler and machinery losses, school leaders error’s and omission claims, police officer death exposure, catastrophic student athletic injuries, and excess workers’ compensation exposure are protected using various commercial insurance policies.

The District uses multiple third-party administrators to administer its various employee health plans. All medical benefit plans are self-insured to maximize effective cost controls and to ensure adequate services are available to employees.

Retirement Plans - District employees participate in the Florida Retirement System, a multiple-employer, noncontributory, cost-sharing public employee retirement system. Generally, a member’s retirement pension benefit vests after six years of service and members are eligible for normal retirement benefits at age 62 with six years of service or at any age with thirty years of service.

xii

OTHER INFORMATION

Student Performance - Brevard County students continue to perform very favorably compared to other students in Florida. Brevard students exceeded the state average in reading and math at all grade levels tested by the 2007 Florida Comprehensive Assessment Test (FCAT). The FCAT measures student progress toward mastery of the benchmarks of the Sunshine State Standards for all Florida public school students in grades 3 through 10. Brevard students had averages that ranged from 11 to 22 points higher than the State average in reading. Brevard students had math scores that ranged from 12 to 27 points above the state average. Out of the 67 school districts in Florida, Brevard students had the highest average score in the State in 5th grade science, 6th grade math, 6th grade reading, and 11th grade science. District average scale scores place Brevard in the top seven districts in Florida on eighteen of the twenty-two data points measured on FCAT.

Audit Committee - The School Board has created an Audit Committee, which acts as an advisory committee to the Board. The purpose of the Audit Committee is to assist the District’s management team in maintaining a high level of accountability and fiscal responsibility to the School Board and its citizenry. The Audit Committee is intended to serve in an advisory capacity, and, as such, provides advice to the School Board, as well as guidance and assistance to implement any changes brought forward through the audit process. The Audit Committee is composed of: the Chairperson of the School Board, the Superintendent, one Area Superintendent, and five Board-appointed community members. The Superintendent, Board Chair and the Area Superintendent serve as ex-officio members. The Audit Committee meets on a quarterly basis, and at least once per year presents a public report to the School Board regarding its progress and findings.

INDEPENDENT AUDIT

Section 11.45, Florida Statutes, requires an annual audit by independent certified pubic accountants. The Office of the Auditor General for the State of Florida conducted the audit for the fiscal year ended June 30, 2007. In addition to meeting the requirements set forth in State statutes, the audit also was designed to meet the requirements of the Federal Single Audit Act of 1996 and related OMB Circular A-133, Audits of States, Local Governments and Non-Profit Organizations. The auditor’s report on the basic financial statements is included in the Financial Section of this report.

REPORTING ACHIEVEMENTS

The Government Finance Officers Association of the United States and Canada (GFOA) awarded the Certificate of Achievement for Excellence in Financial Reporting to The School Board of Brevard County for its comprehensive annual financial report for the fiscal year ended June 30, 2006. In order to be awarded a

xiii

Certificate of Achievement, a government must publish an easily readable and efficiently organized comprehensive annual financial report. This report must satisfy both generally accepted accounting principles and applicable legal requirements. A Certificate of Achievement is valid for a period of one year only.

The School Board of Brevard County also received the Association of School Business Officials (ASBO) International Certificate of Excellence in Financial Reporting for the Comprehensive Annual Financial Report for the fiscal year ended June 30, 2006. This award, valid for one year, certifies that the report substantially conforms to the principles and standards of financial reporting as recommended and adopted by the Association of School Business Officials International.

We believe that our current comprehensive annual financial report continues to meet the Certificate of Achievement Program and the Certificate of Excellence Program requirements, and we are submitting it to both the GFOA and ASBO, to determine its eligibility to receive these prestigious awards.

ACKNOWLEDGEMENT

The preparation of this report could not have been accomplished without the efficient and dedicated services of the entire staff of Financial Services, particularly Accounting Services, and of all the other departments, which provided assistance and support throughout the preparation of this report.

In closing, we would like to thank the members of the School Board for their leadership and support in planning and conducting the financial operations of the District.

Respectfully submitted,

Richard A. DiPatri, Ed.D. Superintendent of Schools

Judy R. Preston Associate Superintendent of Financial Services

xiv

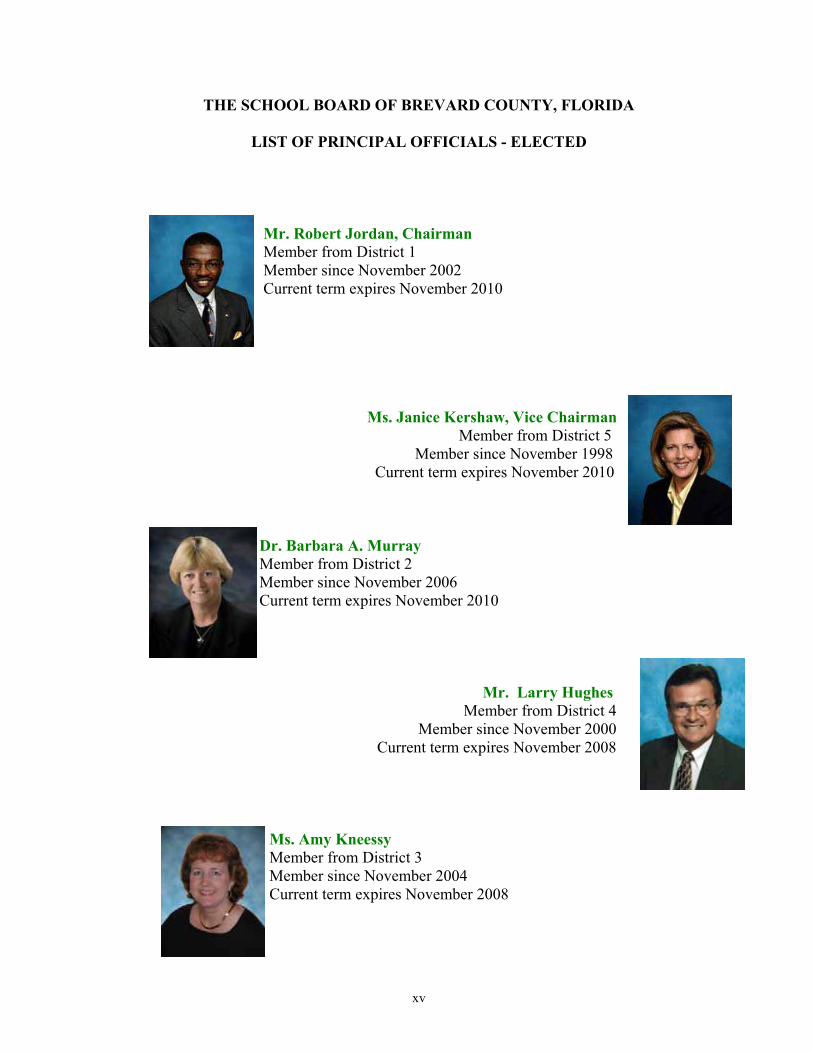

THE SCHOOL BOARD OF BREVARD COUNTY, FLORIDA

LIST OF PRINCIPAL OFFICIALS - ELECTED

Mr. Robert Jordan, Chairman Member from District 1Member since November 2002 Current term expires November 2010

Ms. Janice Kershaw, Vice Chairman Member from District 5 Member since November 1998 Current term expires November 2010

Dr. Barbara A. Murray Member from District 2 Member since November 2006 Current term expires November 2010

Mr. Larry Hughes Member from District 4

Member since November 2000 Current term expires November 2008

Ms. Amy KneessyMember from District 3 Member since November 2004 Current term expires November 2008

xv

xvi

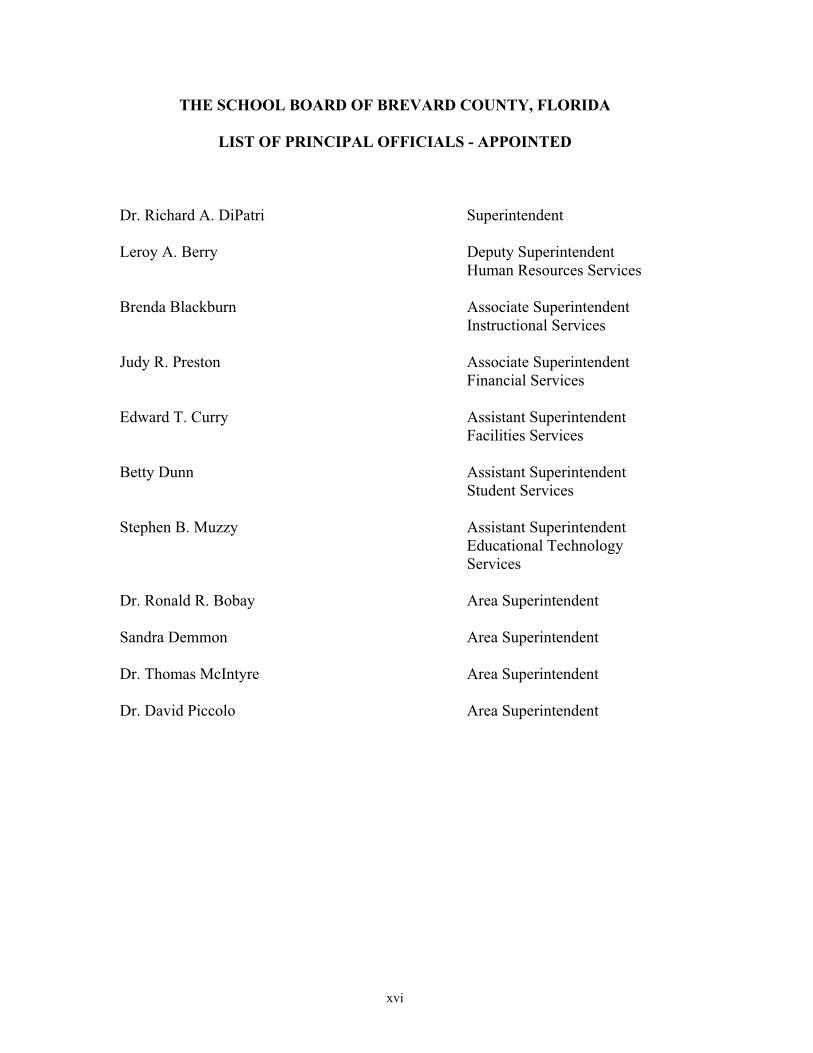

THE SCHOOL BOARD OF BREVARD COUNTY, FLORIDA

LIST OF PRINCIPAL OFFICIALS - APPOINTED

Dr. Richard A. DiPatri Superintendent

Leroy A. Berry Deputy Superintendent Human Resources Services

Brenda Blackburn Associate Superintendent Instructional Services

Judy R. Preston Associate Superintendent Financial Services

Edward T. Curry Assistant Superintendent Facilities Services

Betty Dunn Assistant Superintendent Student Services

Stephen B. Muzzy Assistant Superintendent Educational Technology Services

Dr. Ronald R. Bobay Area Superintendent

Sandra Demmon Area Superintendent

Dr. Thomas McIntyre Area Superintendent

Dr. David Piccolo Area Superintendent

Financial Section

AUDITOR GENERAL

STATE OF FLORIDA

G74 Claude Pepper Building 111 West Madison Street

Tallahassee, Florida 32399-1450 DAVID W. MARTIN, CPA AUDITOR GENERAL

850/488-5534/SC 278-5534 Fax: 488-6975/SC 278-6975

The President of the Senate, the Speaker of the House of Representatives, and the Legislative Auditing Committee

INDEPENDENT AUDITOR'S REPORT ON FINANCIAL STATEMENTS

We have audited the accompanying financial statements of the governmental activities, the business-type

activities, the aggregate discretely presented component units, each major fund, and the aggregate remaining fund

information of the Brevard County District School Board as of and for the fiscal year ended June 30, 2007, which

collectively comprise the District’s basic financial statements as listed in the table of contents. These financial

statements are the responsibility of the District’s management. Our responsibility is to express opinions on these

financial statements based on our audit. We did not audit the financial statements of the aggregate discretely

presented component units. Those financial statements were audited by other auditors whose reports have been

provided to us, and our opinion, insofar as it relates to the amounts included for the aggregate discretely

presented component units, is based on the reports of the other auditors.

Except as discussed in the following paragraphs, we conducted our audit in accordance with auditing standards

generally accepted in the United States of America and the standards applicable to financial audits contained in

Government Auditing Standards issued by the Comptroller General of the United States. Those standards require

that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free

of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and

disclosures in the financial statements. An audit also includes assessing the accounting principles used and

significant estimates made by management, as well as evaluating the overall financial statement presentation. We

believe that our audit, and the reports of the other auditors, provide a reasonable basis for our opinions.

Accounting principles generally accepted in the United States provide criteria for including component units in an

organization’s financial statements. The District has identified 13 entities which meet the requirements for

inclusion as component units, including 12 charter schools. As discussed in Note 1, the financial statements do

not include the financial data for four charter schools. Pursuant to Section 1002.33(g), Florida Statutes, the

District is required to otherwise provide for audits of its charter schools. However, Note 1 further indicates that

Page 1

the charters for three of these charter schools were not subsequently renewed and that audits were, therefore, not

provided by those charter schools. Accordingly, our audit did not extend to these four charter schools.

In our opinion, based on the reports of the other auditors, and except for the effects of such adjustments on the

aggregate discretely presented component units, as might have been determined to be necessary for inclusion of

the financial data of the remaining component units, the financial statements referred to above present fairly, in all

material respects, the financial position of the remaining aggregate discretely presented component units for the

Brevard County District School Board as of June 30, 2007, and the respective changes in financial position

thereof for the year then ended in conformity with accounting principles generally accepted in the United States

of America.

In addition, in our opinion, the financial statements referred to above present fairly, in all material respects, the

respective financial position of the governmental activities, the business-type activities, each major fund, and the

aggregate remaining fund information, of the Brevard County District School Board as of June 30, 2007, and the

respective changes in financial position, and where applicable, cash flows thereof and the respective budgetary

comparison for the General Fund for the year then ended in conformity with accounting principles generally

accepted in the United States of America.

In accordance with Government Auditing Standards, we have also issued a report on our consideration of the Brevard

County District School Board's internal control over financial reporting and on our tests of its compliance with

certain provisions of laws, administrative rules, regulations, contracts, and grant agreements and other matters

included under the heading INDEPENDENT AUDITOR'S REPORT ON INTERNAL CONTROL

OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON

AN AUDIT OF THE FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH

GOVERNMENT AUDITING STANDARDS. The purpose of that report is to describe the scope of our

testing of internal control over financial reporting and compliance and the results of that testing, and not to

provide an opinion on the internal control over financial reporting or on compliance. That report is an integral

part of an audit performed in accordance with Government Auditing Standards and should be considered in assessing

the results of our audit.

The Management’s Discussion and Analysis (pages 7 through 16) is not a required part of the basic financial

statements but is supplementary information required by accounting principles generally accepted in the United

States of America. We have applied certain limited procedures, which consisted principally of inquiries of

management regarding the methods of measurement and presentation of the required supplementary information.

However, we did not audit the information and express no opinion thereon.

Our audit was conducted for the purpose of forming opinions on the financial statements that collectively

comprise the Brevard County District School Board’s basic financial statements. The introductory section, the

combining and individual fund financial statements and budgetary schedules, and the statistical section listed in

Page 2

the accompanying table of contents are presented for purposes of additional analysis and are not a required part

of the basic financial statements. Additionally, the accompanying Schedule of Expenditures of Federal Awards is

presented for purposes of additional analysis as required by the United States Office of Management and Budget’s

Circular A-133, Audits of States, Local Governments, and Non-Profit Organizations, and is not a required part of the basic

financial statements. The combining and individual fund financial statements and related budgetary schedules

(pages 74 through 112) and the Schedule of Expenditures of Federal Awards (page 167) have been subjected to

the auditing procedures applied in the audit of the basic financial statements and, in our opinion, are fairly stated,

in all material respects, in relation to the basic financial statements taken as a whole. The introductory section

(pages i through xix) and the statistical section (pages 117 through 155) have not been subjected to the auditing

procedures applied in the audit of the basic financial statements and, accordingly, we express no opinion on them.

Respectfully submitted,

David W. Martin, CPA January 25, 2008

Page 3

THE FUTUREOF FLORIDA'SSPACE COAST

MANAGEMENT’S DISCUSSION AND ANALYSIS

The Management of the School Board of Brevard County, Florida’s (the District) has prepared the following discussion and analysis to provide an overview of the District’s financial activities for the fiscal year ended June 30, 2007. The information contained in the Management’s Discussion and Analysis (MD&A) is intended to highlight significant transactions, events, and conditions and should be considered in conjunction with the District’s financial statements and the notes to the financial statements, found on pages 19 through 69.

FINANCIAL HIGHLIGHTS

Key financial highlights for the 2006-07 fiscal year are as follows:

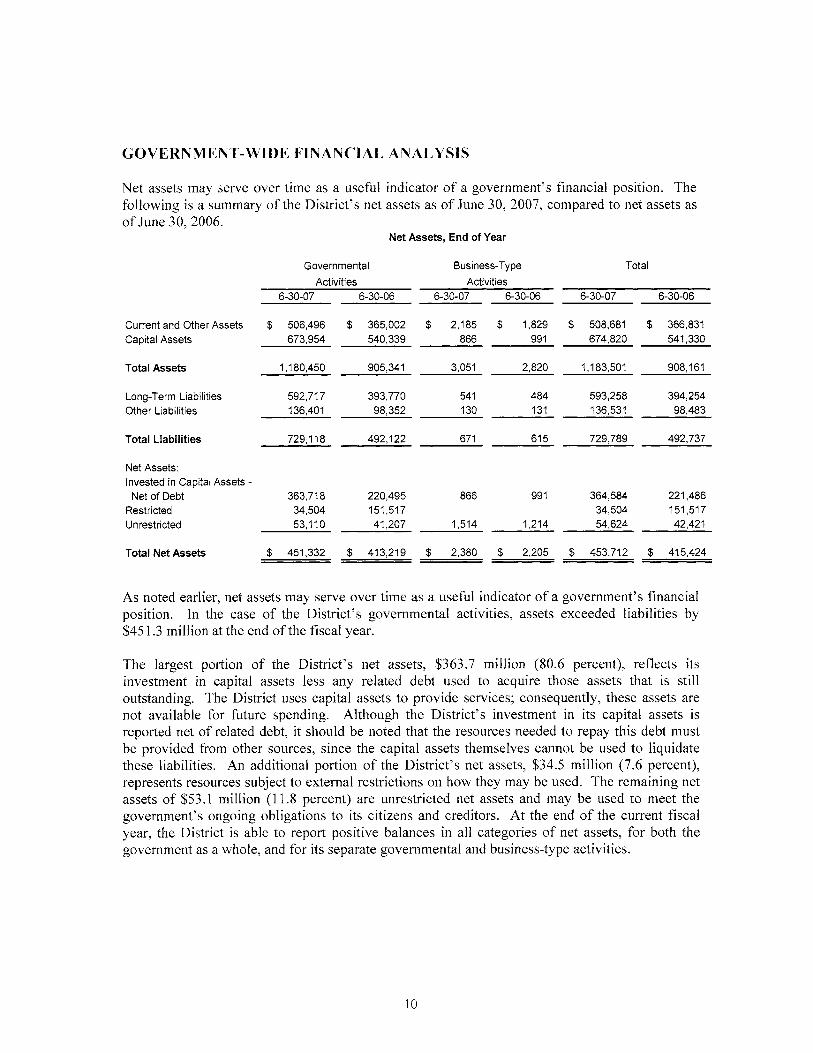

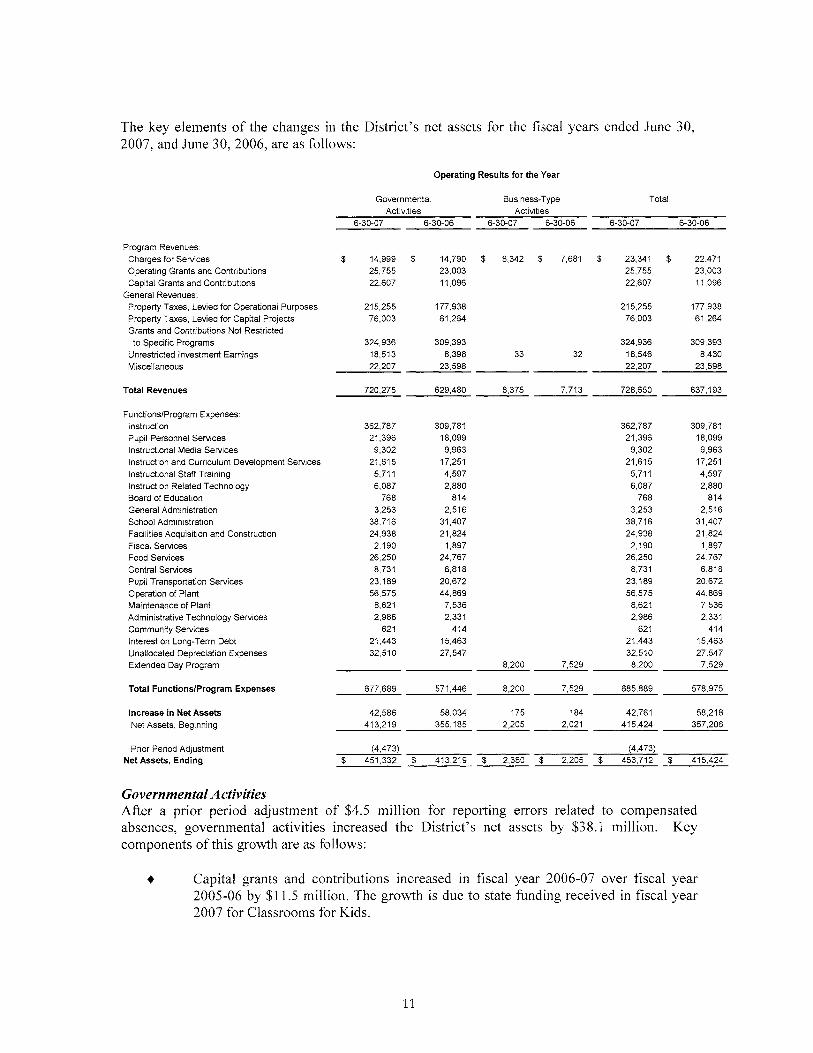

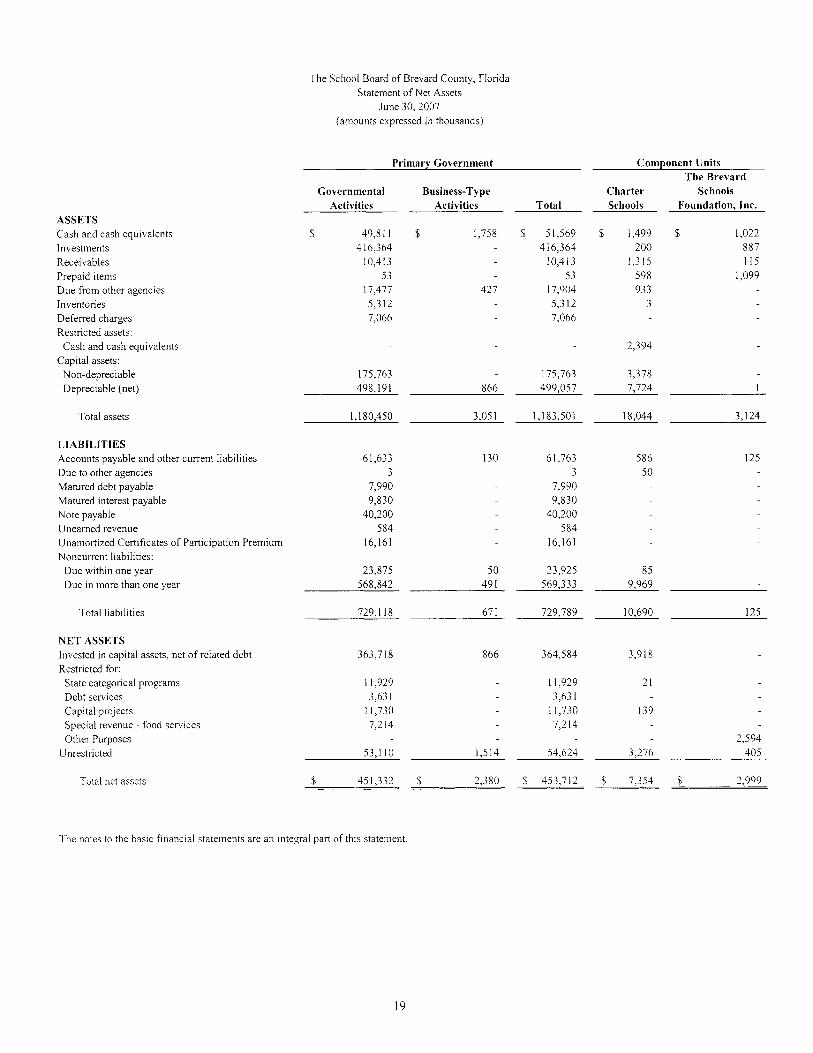

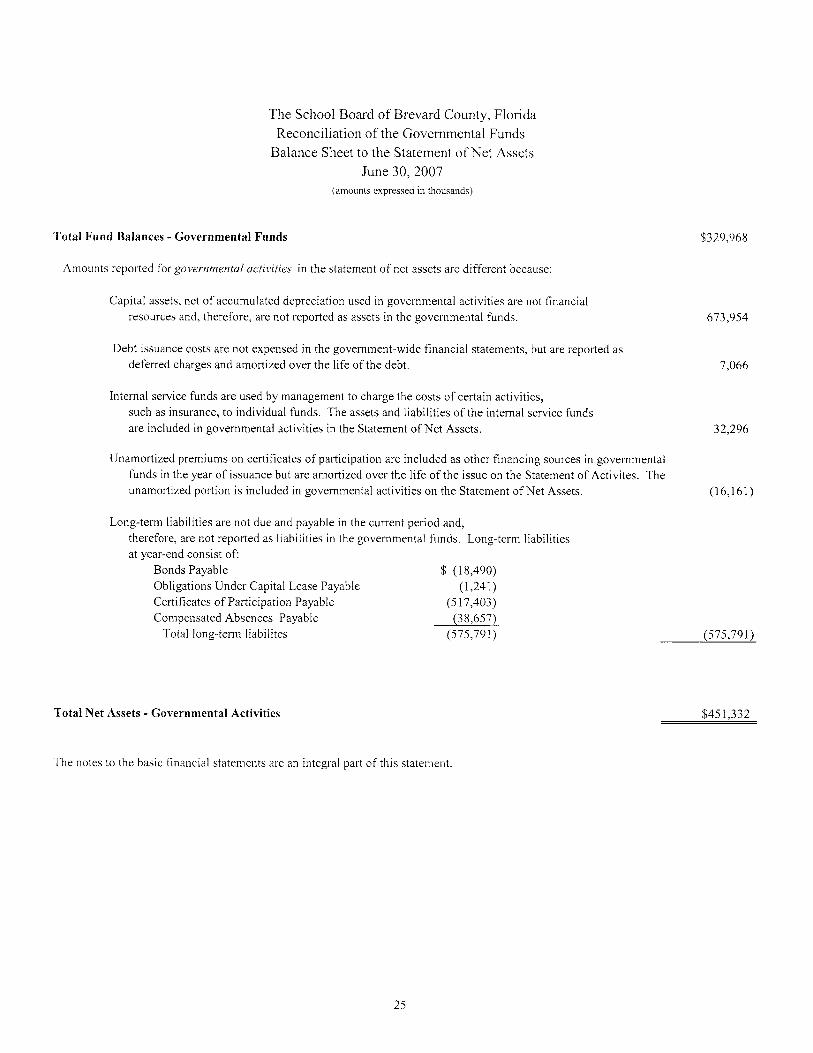

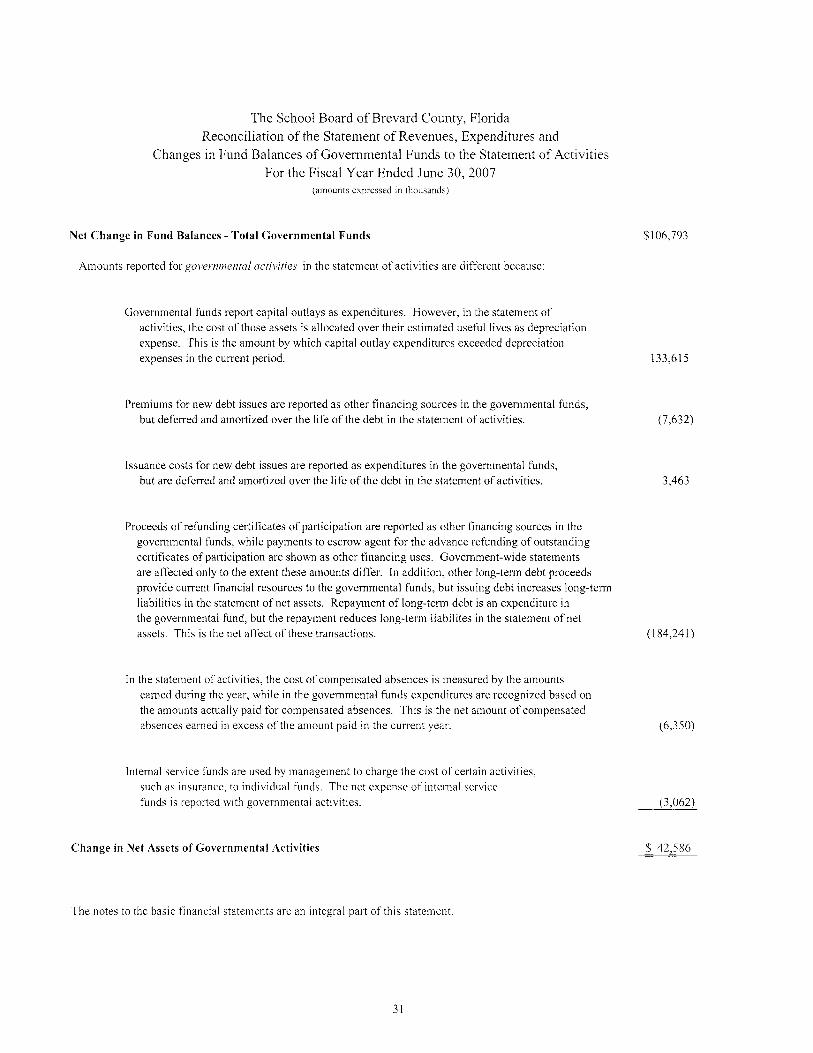

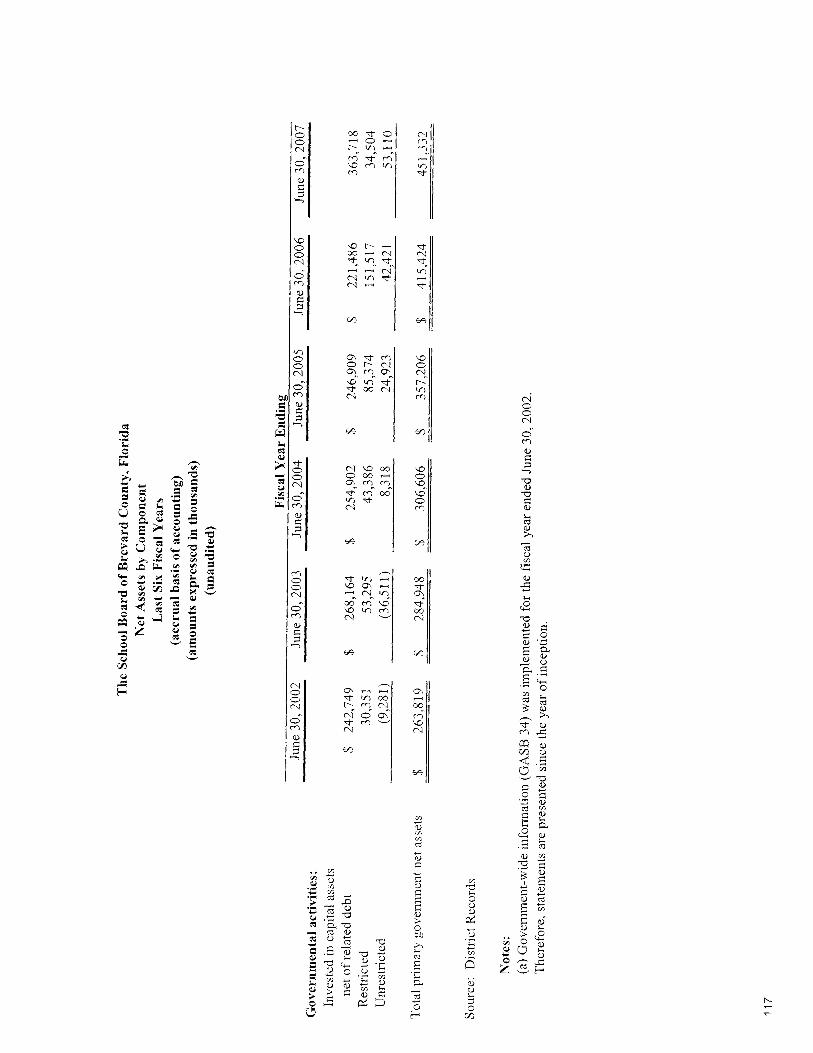

� The assets of the District exceeded its liabilities for the governmental activities, at June 30, 2007, by $451.3 million. Of this amount, $363.7 million represents investments in capital assets (net of related debt) and $87.6 million represents restricted and unrestricted net assets of $34.5 million and $53.1 million, respectively.

� The District’s total net assets for governmental activities increased by $42.6 million, or 10.4 percent.

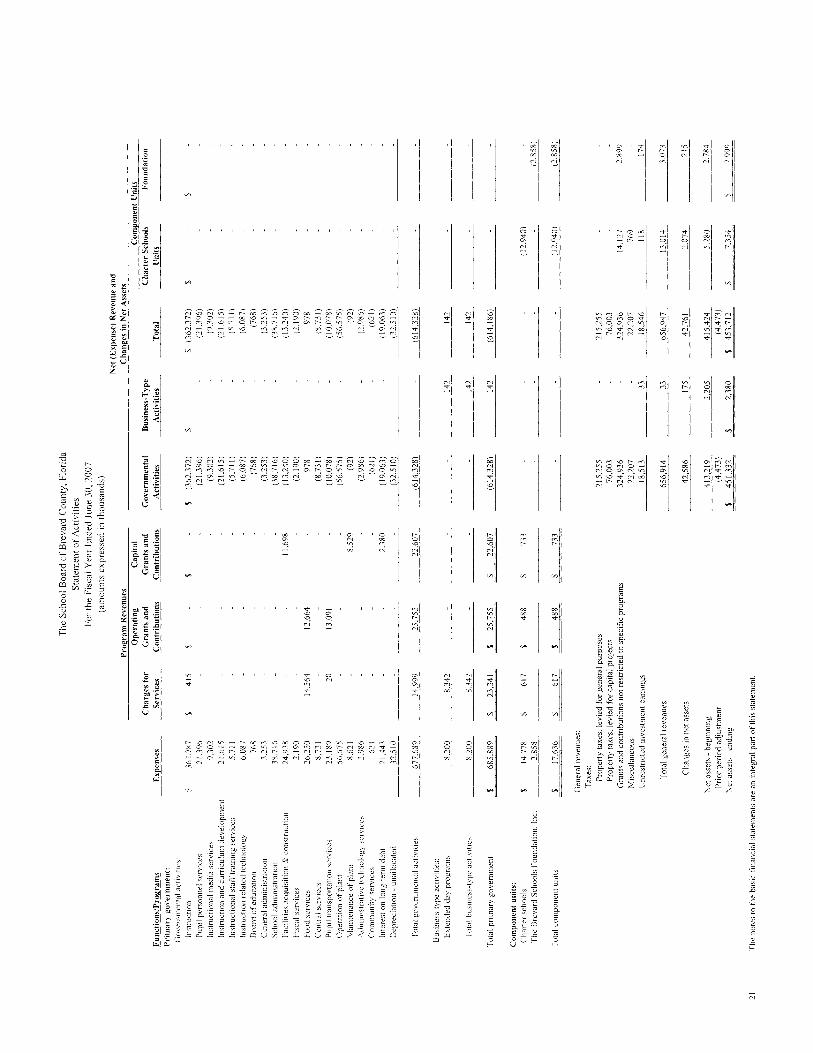

� Program revenues for governmental activities accounted for $63.4 million, or 8.8 percent of total revenues, and general revenues accounted for $656.9 million, or 91.2 percent.

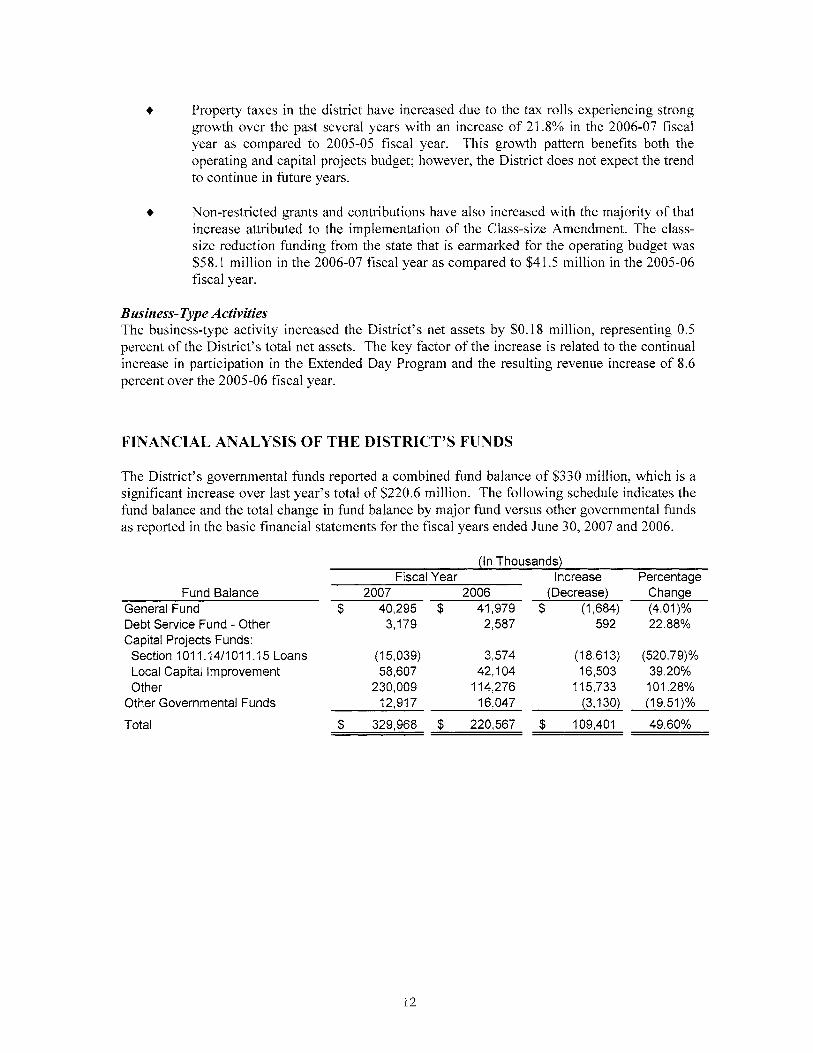

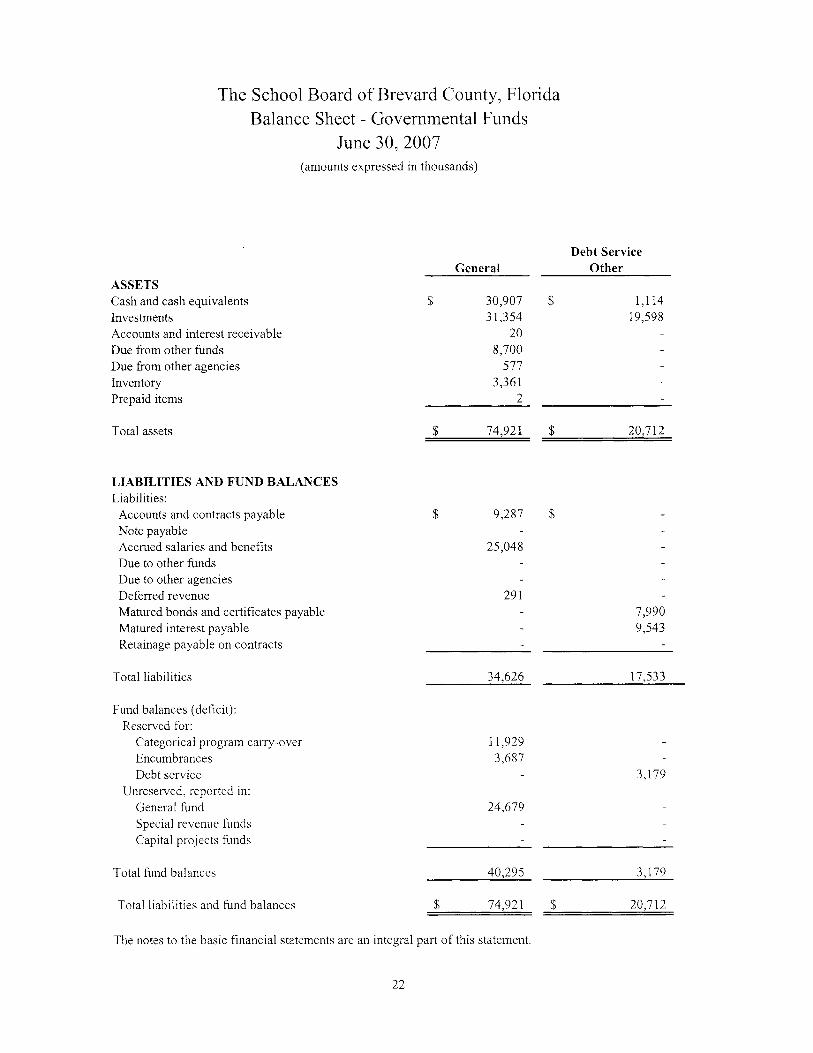

� The governmental funds reported combined fund balances of $330 million, an increase of $106.8 million in comparison to the prior fiscal year.

� At the end of the fiscal year, the unreserved fund balance for the General Fund was $24.7 million, or 4.7 percent of the General Fund revenues.

OVERVIEW OF THE FINANCIAL STATEMENTS

The basic financial statements consist of three components:

� Government-wide financial statements.

� Fund financial statements.

� Notes to financial statements

Government-Wide Financial StatementsThe government-wide financial statements provide both short-term and long-term information about the District’s overall financial condition in a manner similar to those of a private-sector business. The statements include a statement of net assets and a statement of activities that are designed to provide consolidated financial information about the governmental and business-type activities of the primary government presented on the accrual basis of accounting. The statement of net assets provides information about the government’s financial position, its assets and liabilities, using an economic resources measurement focus. The difference between the assets and liabilities, the net assets, is a measure of the financial health of the District. The statement of activities presents information about the change in the District’s net assets, the results of operations, during the fiscal year. An increase or decrease in net assets is an indication of whether the District’s financial health is improving or deteriorating.

7

The government-wide statements present the District’s activities in three categories:

� Governmental activities – This represents most of the District’s services, including its educational programs: basic, vocational, adult, and exceptional education. Support functions such as transportation and administration are also included. Local property taxes and the State’s education finance program provide most of the resources that support these activities.

� Business-type activities – The District charges fees to cover the cost of certain services it provides. These activities are for its Extended Day Care Program.

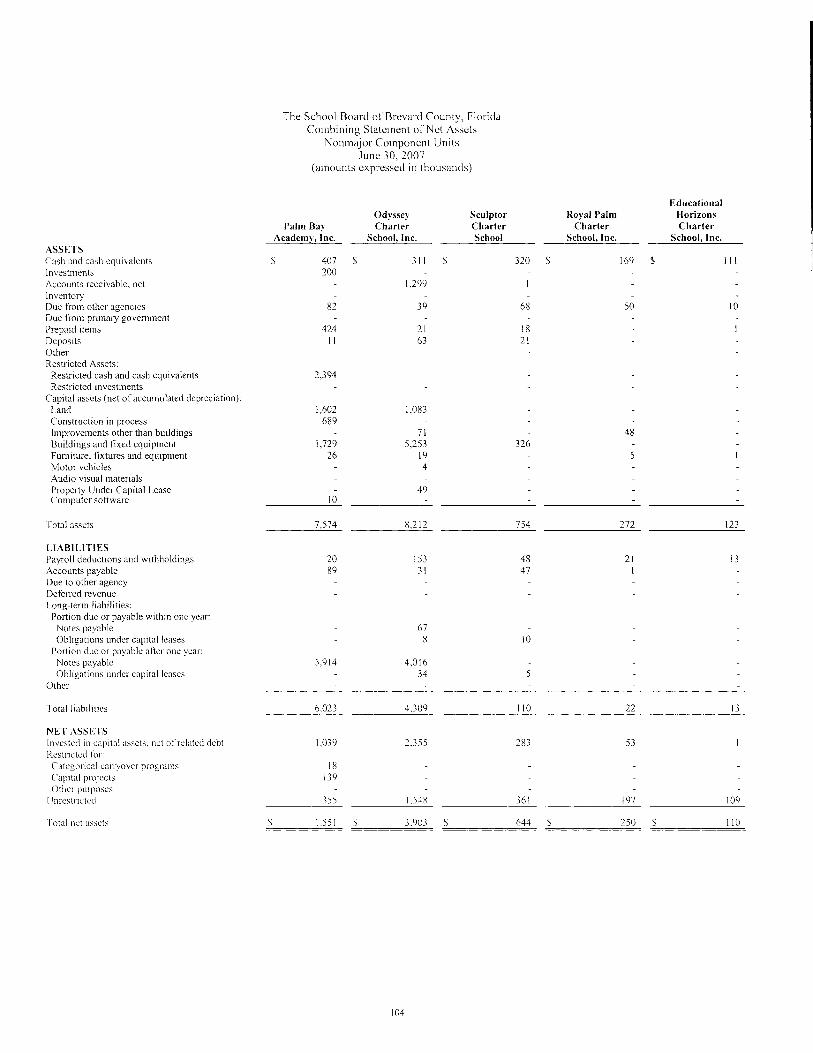

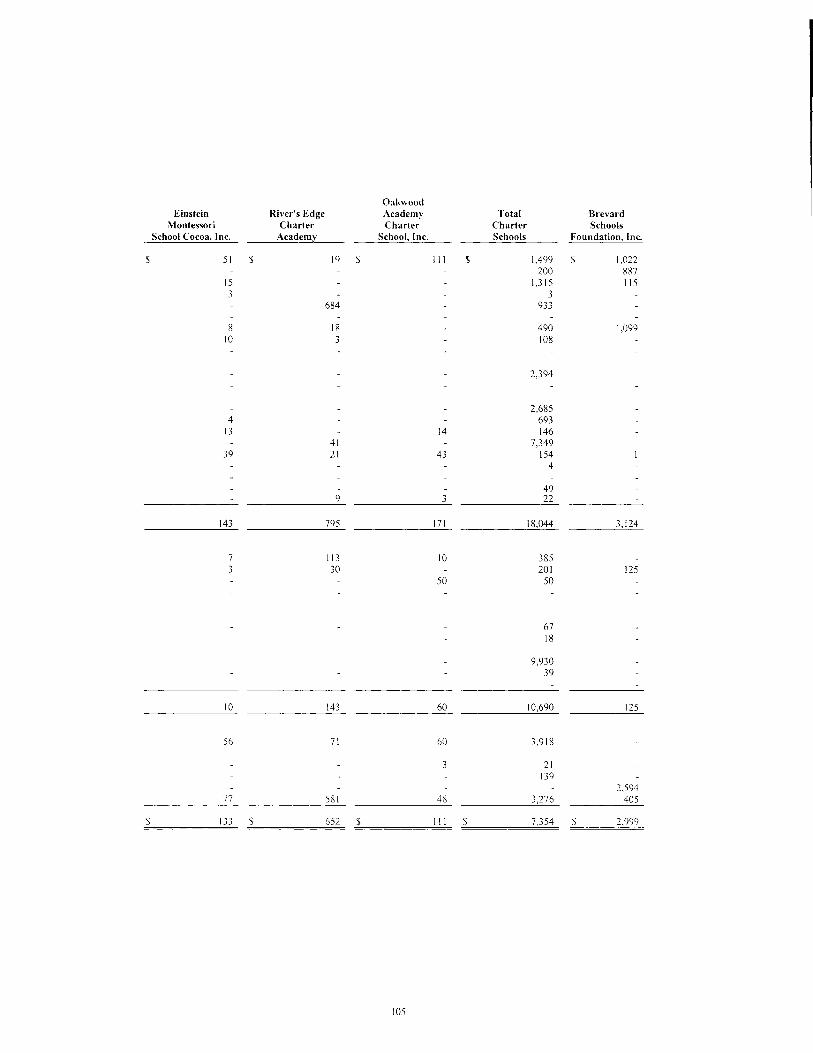

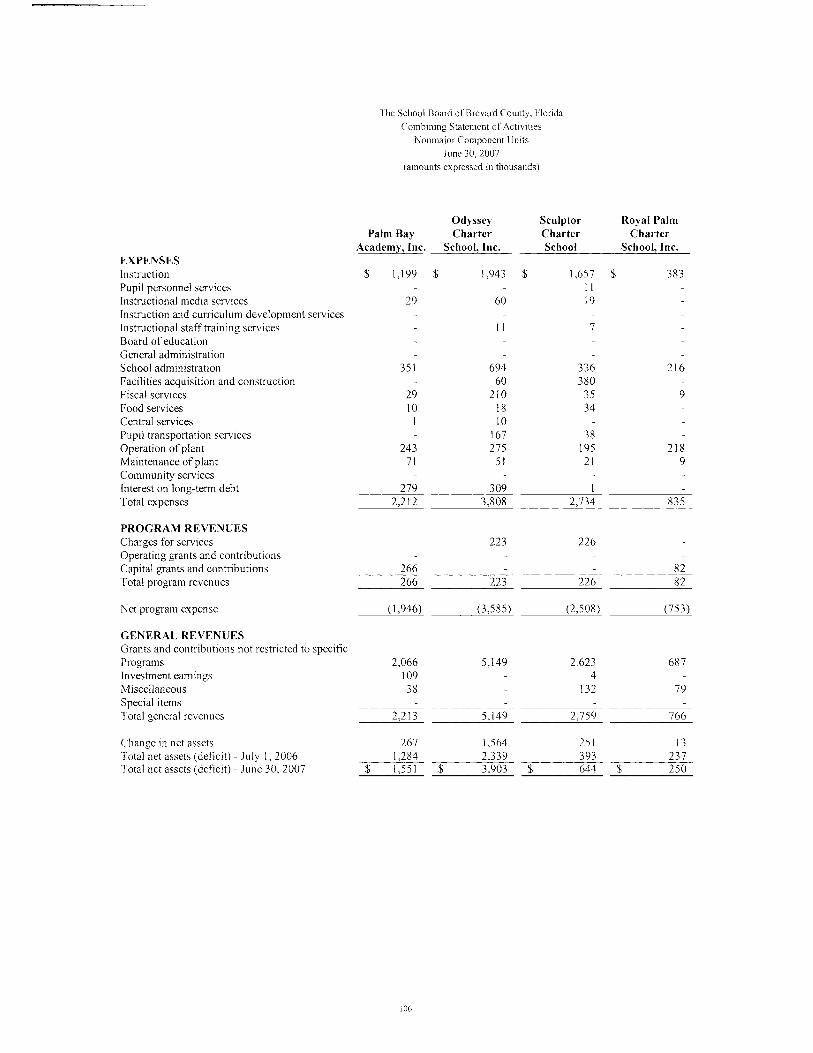

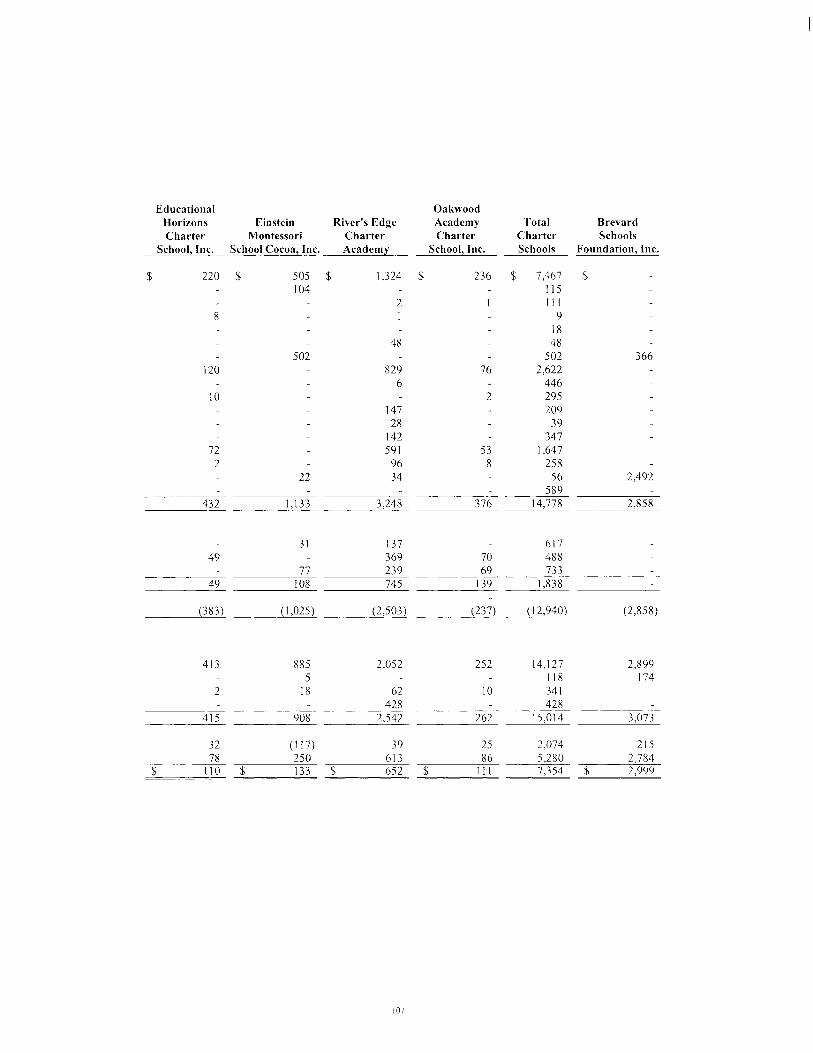

� Component units – The District has identified thirteen separate legal entities which meet the criteria to be included as a component unit, including twelve charter schools and the Brevard Schools Foundation. This report includes nine of those component units, including eight charter schools and Brevard Schools Foundation. Although legally separate organizations, the component units are included in this report because they meet the criteria for inclusion provided by generally accepted accounting principles. Financial information for these component units is reported separately from the financial information presented for the primary government. Additional information regarding the four charter schools that are not included, can be found in the notes to the financial statements.

The Brevard County School Board Leasing Corporation, although a legally separate entity, was formed to facilitate financing for the acquisition of facilities and equipment for the District. Due to the substantive economic relationship between the District and the Leasing Corporation, the Leasing Corporation has been included as an integral part of the primary government.

Fund Financial Statements Fund financial statements are one of the components of the basic financial statements. A fund is a grouping of related accounts that is used to maintain control over resources that have been segregated for specific activities or objectives. The District uses fund accounting to ensure and demonstrate compliance with finance-related legal requirements and prudent fiscal management. Certain funds are established by law while others are created by legal agreements, such as bond covenants. Fund financial statements provide more detailed information about the District’s financial activities, focusing on its most significant or “major” funds rather than fund types. This is in contrast to the entity-wide perspective contained in the government-wide statements. All of the District’s funds may be classified within one of three broad categories as discussed below. Governmental Funds Most of the District’s activities are reported in governmental funds, which focus on how money flows into and out of those funds and the balances left at year-end available for spending in future periods. These funds are reported using an accounting method called modified accrual accounting, which measures cash and other financial assets that can readily be converted to cash. The governmental fund statements provide a detailed short-term view of the District’s general government operations and the basic services it provides. Governmental fund information helps the reader determine whether there are more or less financial resources available to spend in the near future to finance the District’s programs. The relationship (or differences) between governmental activities (reported in the Statement of Net Assets and the Statement of Activities) and governmental funds is reconciled in the basic financial statements.

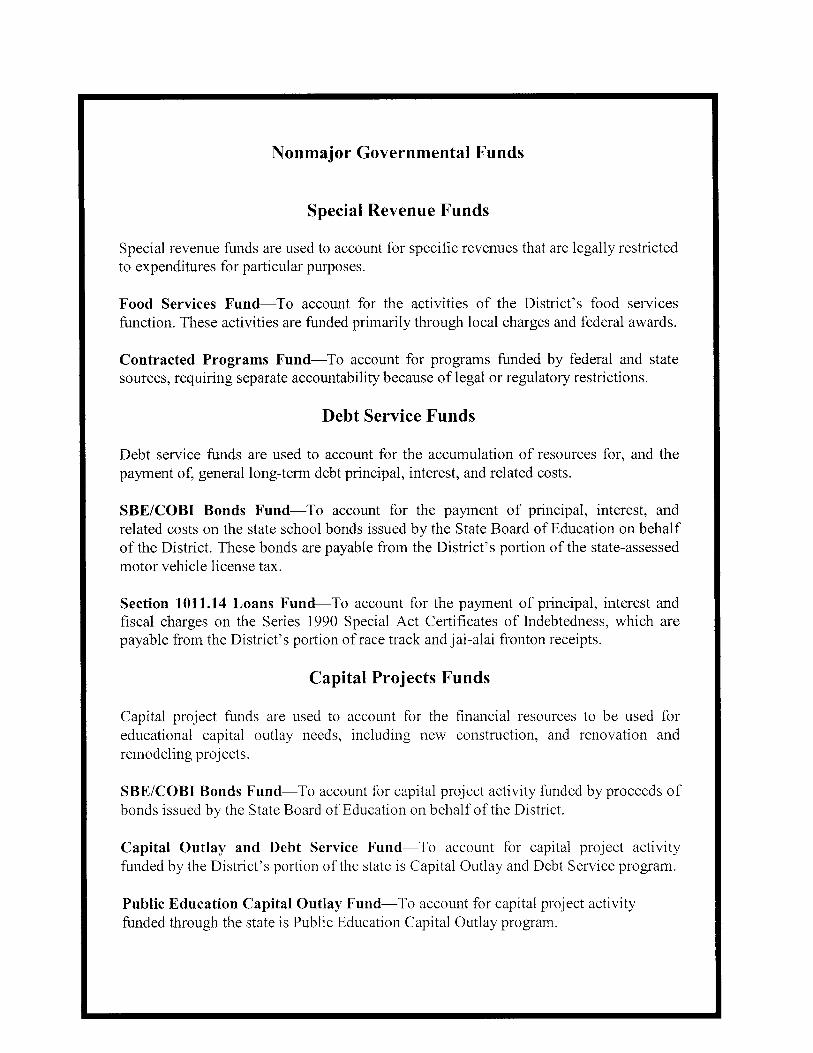

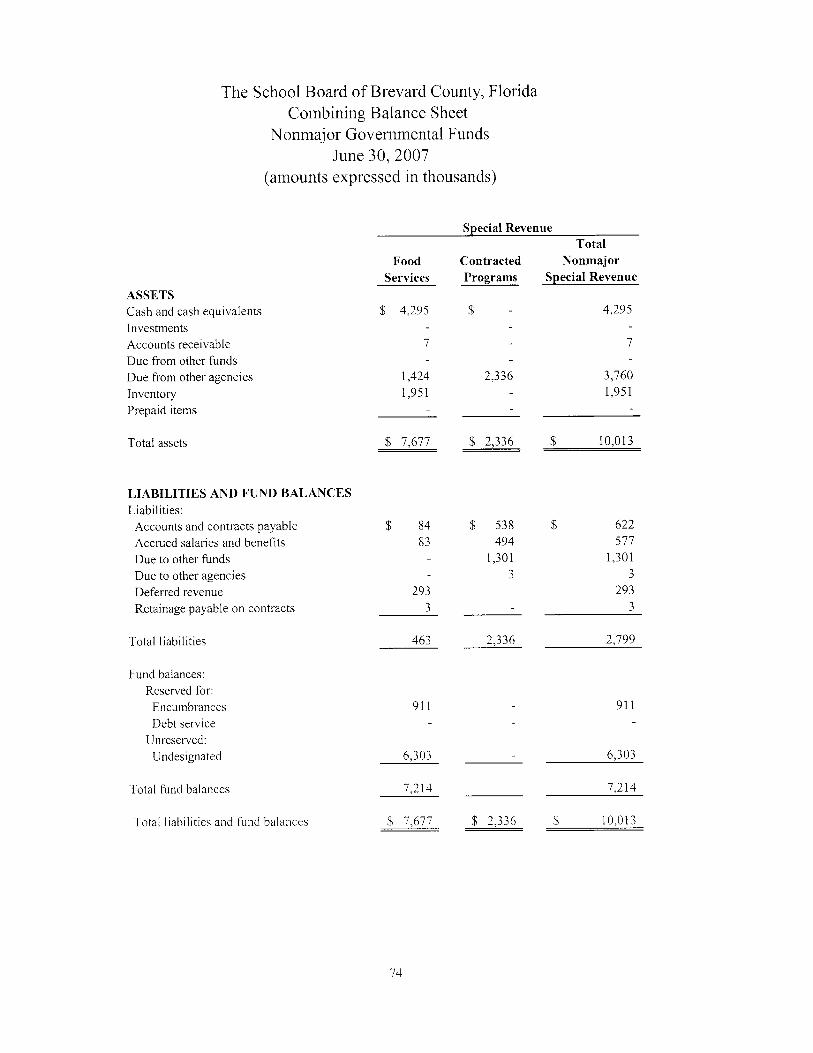

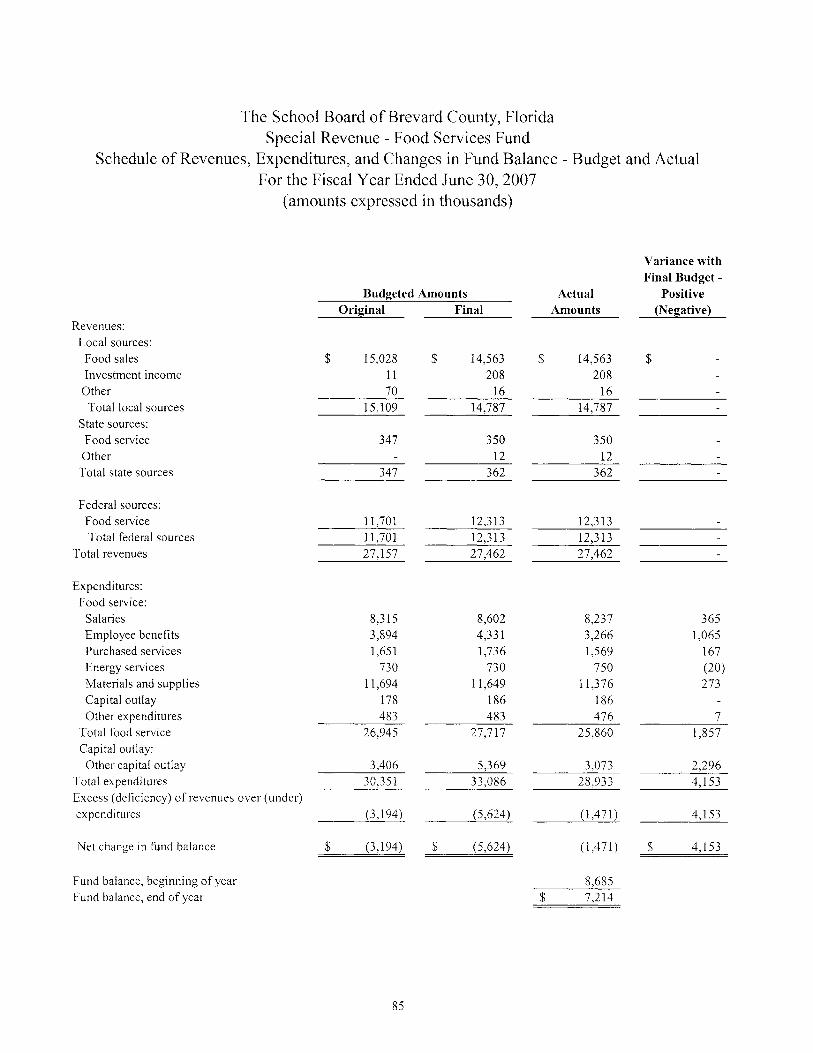

The District has several governmental funds: the General Fund, Debt Service Funds, Special Revenue Funds (including the School Food Services Program) and the Capital Projects Funds.

8

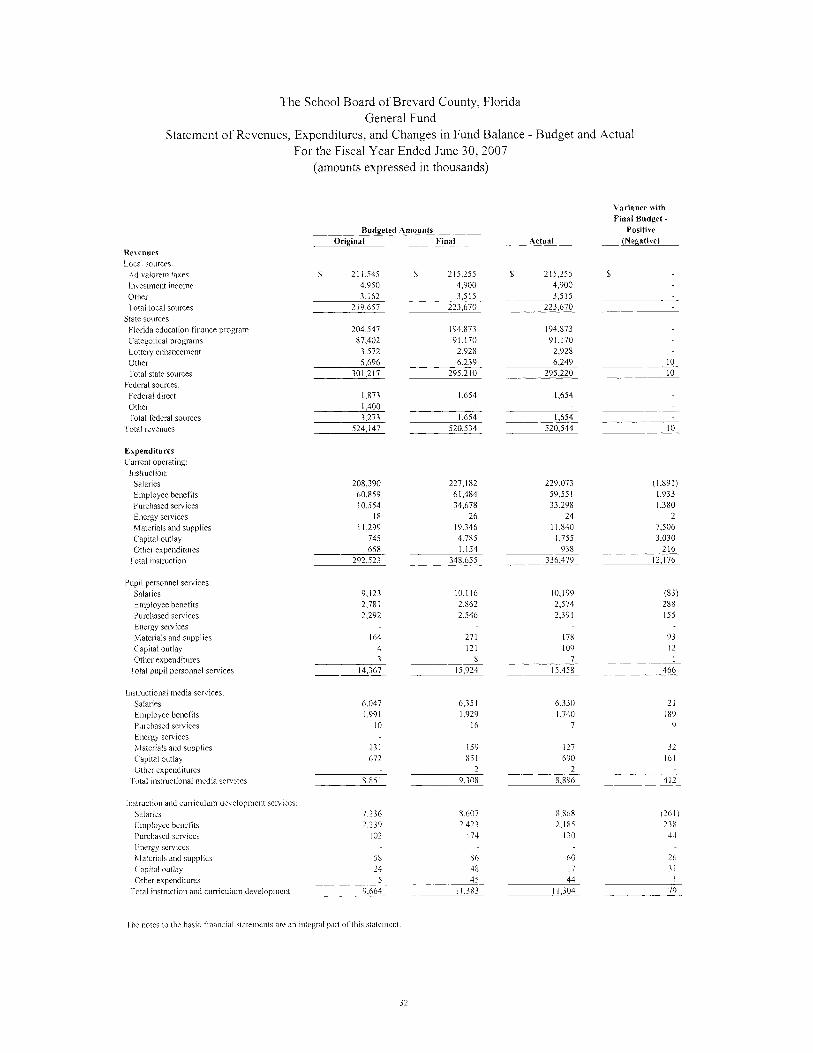

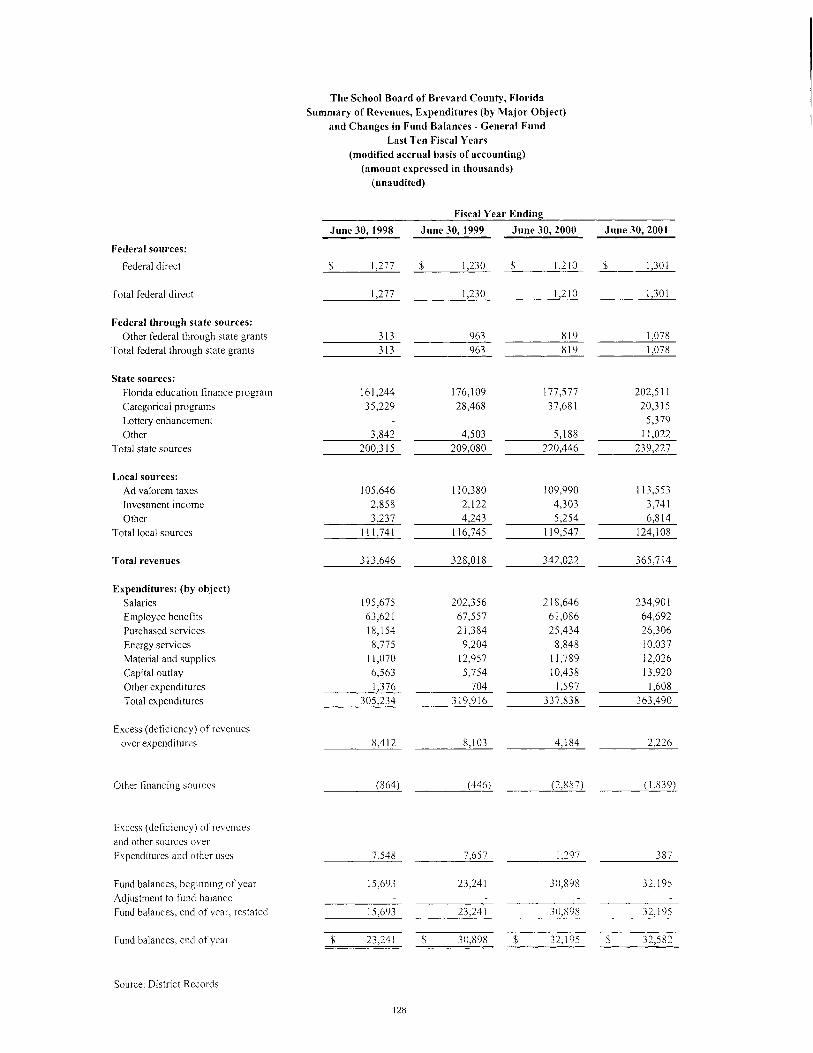

General FundThe District’s general fund balance increased due mainly to increases in state revenue for both the state mandated class-size requirements, but also the increase due to student population growth. The tables and data that follow illustrate the financial activities and balance of the general fund.

(In Thousands)Fiscal Year Increase Percentage

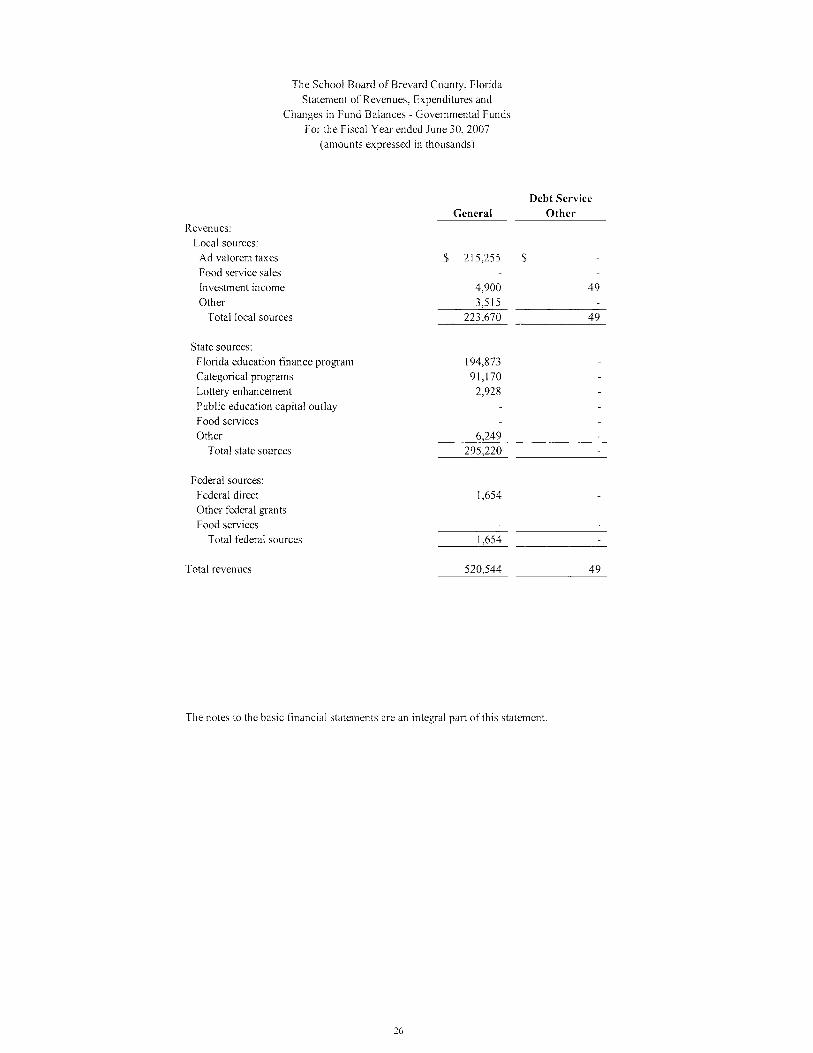

Revenues 2007 2006 (Decrease) ChangeTaxes 215,255$ 177,938$ 37,317$ 20.97%Interest Earnings 4,900 4,490 410 9.13%State Revenues 295,220 278,672 16,548 5.94%Other Revenues 5,169 6,835 (1,666) (24.37)%

Total 520,544$ 467,935$ 52,609$ 11.24%

The property tax revenue is up $37.3 million due to growth. The District anticipates tax collections will increase slightly in 2007-08 fiscal year, compared to the 2006-07 fiscal year with a 4.1 percent increase in the tax rolls and will remain rather flat in the next few years.

Interest earnings increased 9.13 percent over the prior year as the interest rate environment continued to improve, particularly in the short term investment arena.

State revenues are up $16.5 million for the fiscal year ended June 30, 2007. This increase is due mainly to fiscal year 2006-07 increase in class-size reduction funding. This revenue is to be utilized in meeting the requirements of the constitutional amendment requiring only a certain number of students at each grade level.

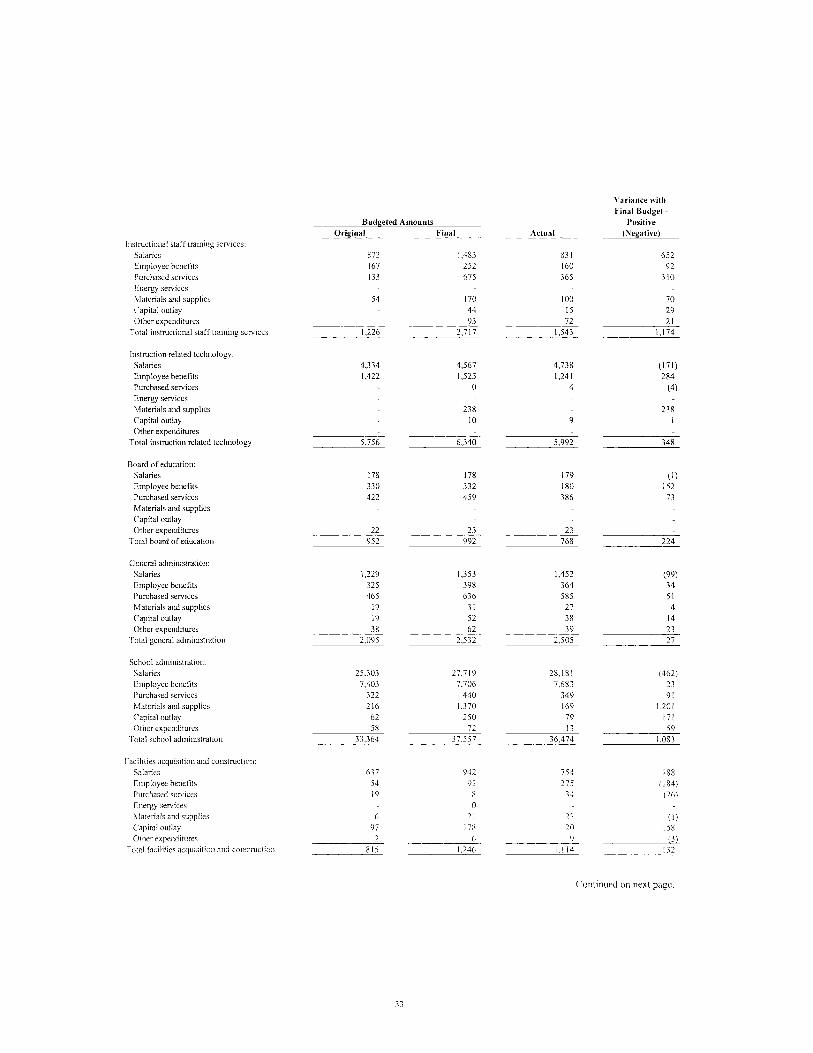

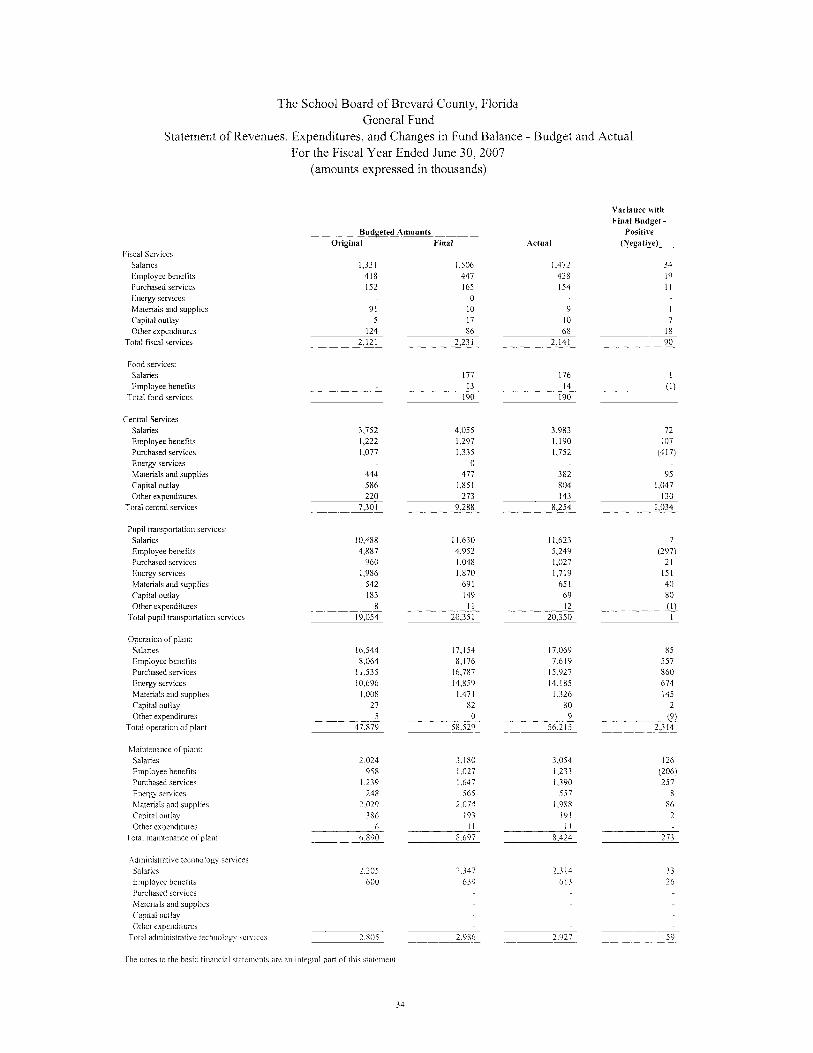

As the table below illustrates, the largest portions of general fund expenditures are for salaries and fringe benefits. The District is a service entity and as such is labor intensive.

(In Thousands)Fiscal Year Increase Percentage

Expenditures by Objects 2007 2006 (Decrease) ChangeSalaries 330,595$ 300,039$ 30,556$ 10.18%Employee Benefits 92,349 89,255 3,094 3.47%Purchased Services 57,798 40,453 17,345 42.88%Energy Services 16,485 15,104 1,381 9.14%Materials & Supplies 16,905 14,830 2,075 13.99%Capital Outlay 9,621 7,006 2,615 37.33%Other 2,220 2,469 (249) (10.09)%

Total 525,973$ 469,156$ 56,817$ 12.11%

13

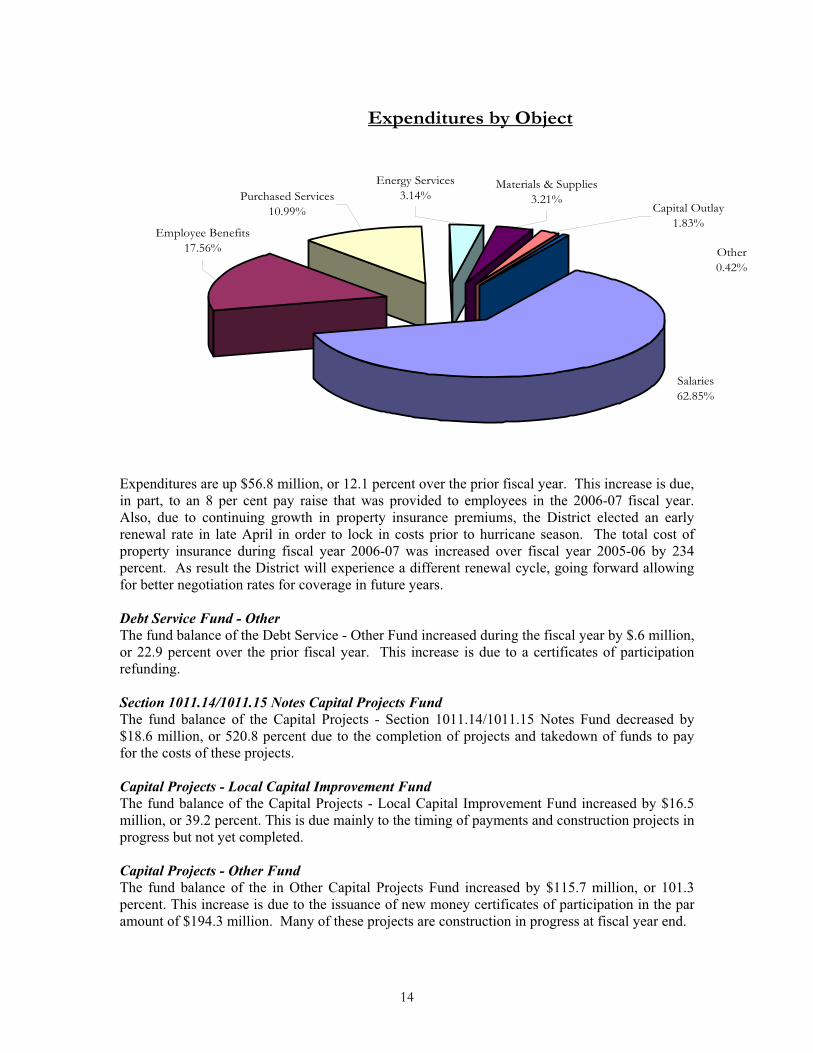

Expenditures by Object

Salaries62.85%

Materials & Supplies3.21%

Energy Services3.14%

Employee Benefits17.56%

Capital Outlay1.83%

Purchased Services10.99%

Other0.42%

Expenditures are up $56.8 million, or 12.1 percent over the prior fiscal year. This increase is due, in part, to an 8 per cent pay raise that was provided to employees in the 2006-07 fiscal year. Also, due to continuing growth in property insurance premiums, the District elected an early renewal rate in late April in order to lock in costs prior to hurricane season. The total cost of property insurance during fiscal year 2006-07 was increased over fiscal year 2005-06 by 234 percent. As result the District will experience a different renewal cycle, going forward allowing for better negotiation rates for coverage in future years.

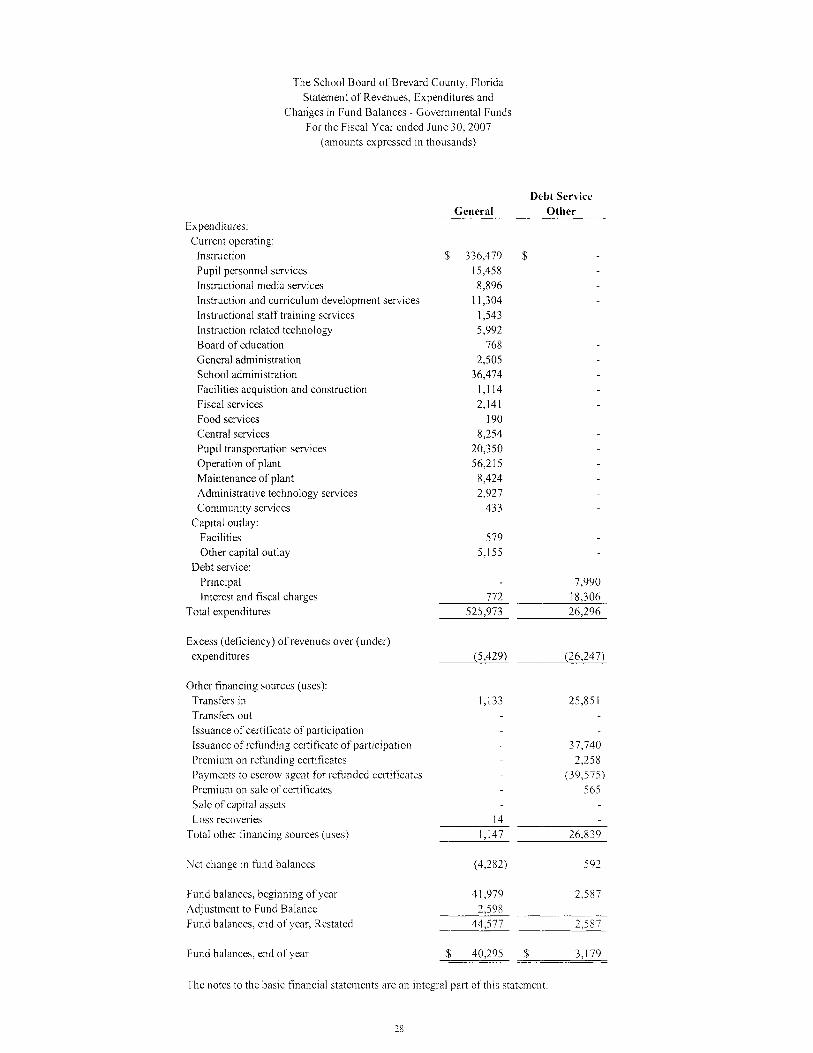

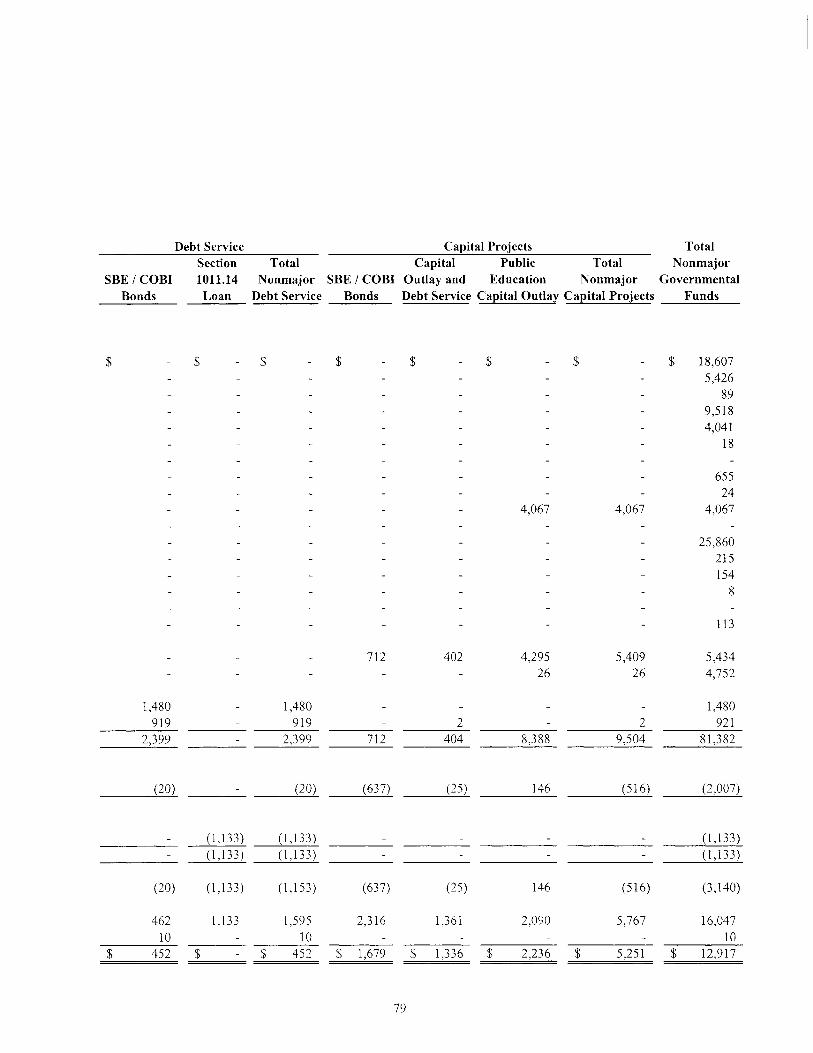

Debt Service Fund - Other The fund balance of the Debt Service - Other Fund increased during the fiscal year by $.6 million, or 22.9 percent over the prior fiscal year. This increase is due to a certificates of participation refunding.

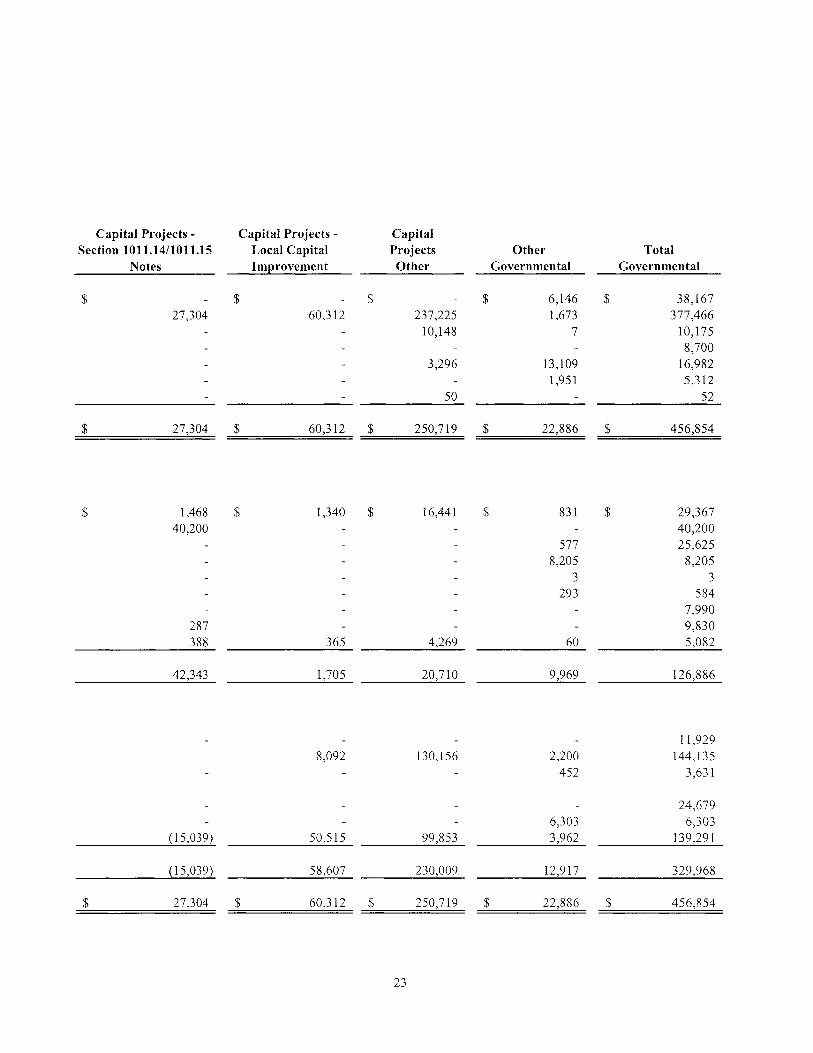

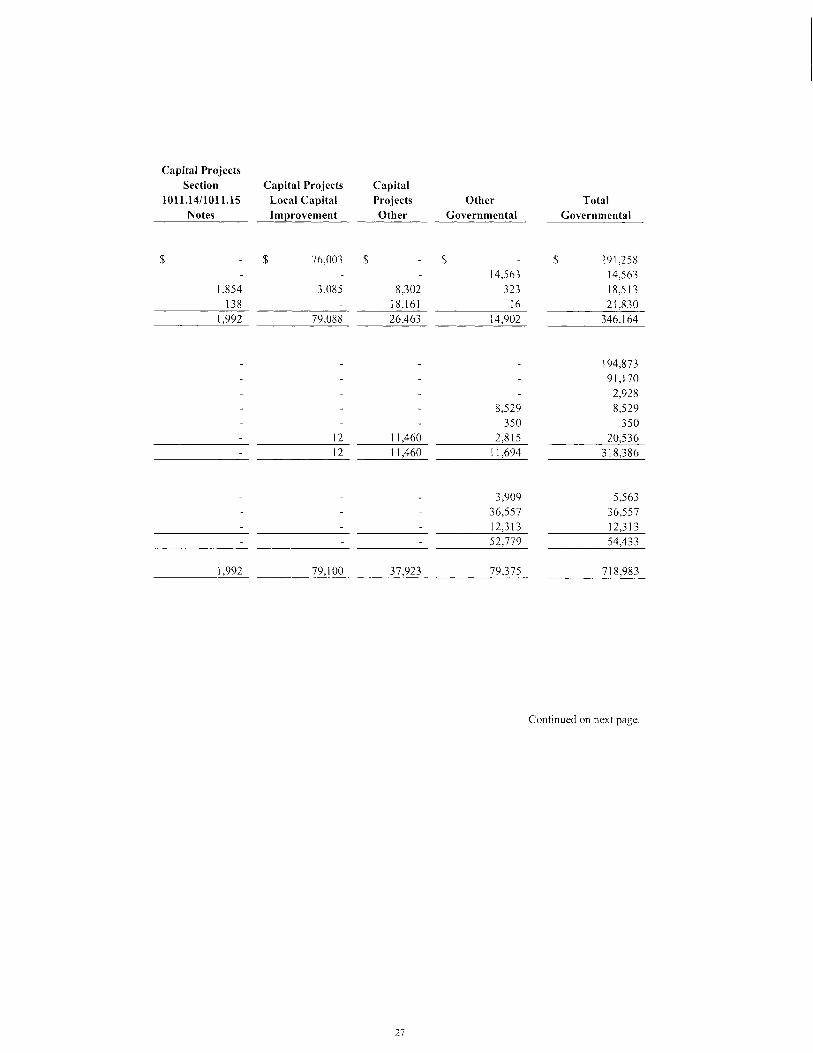

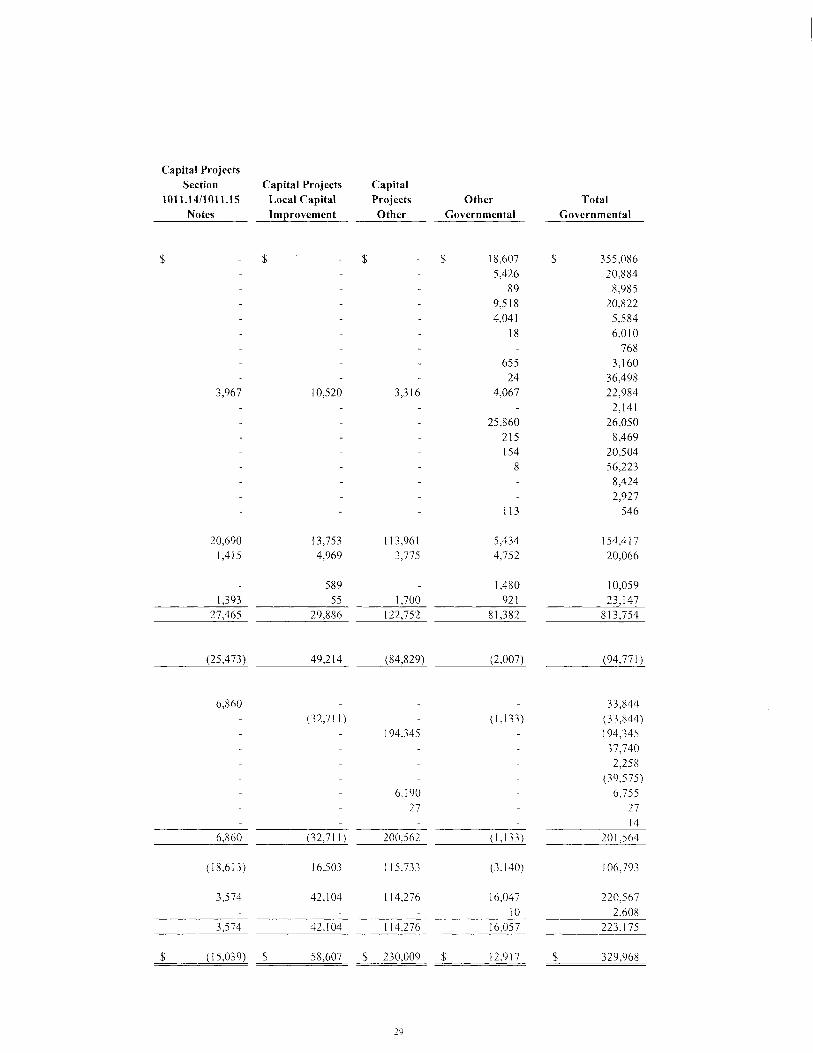

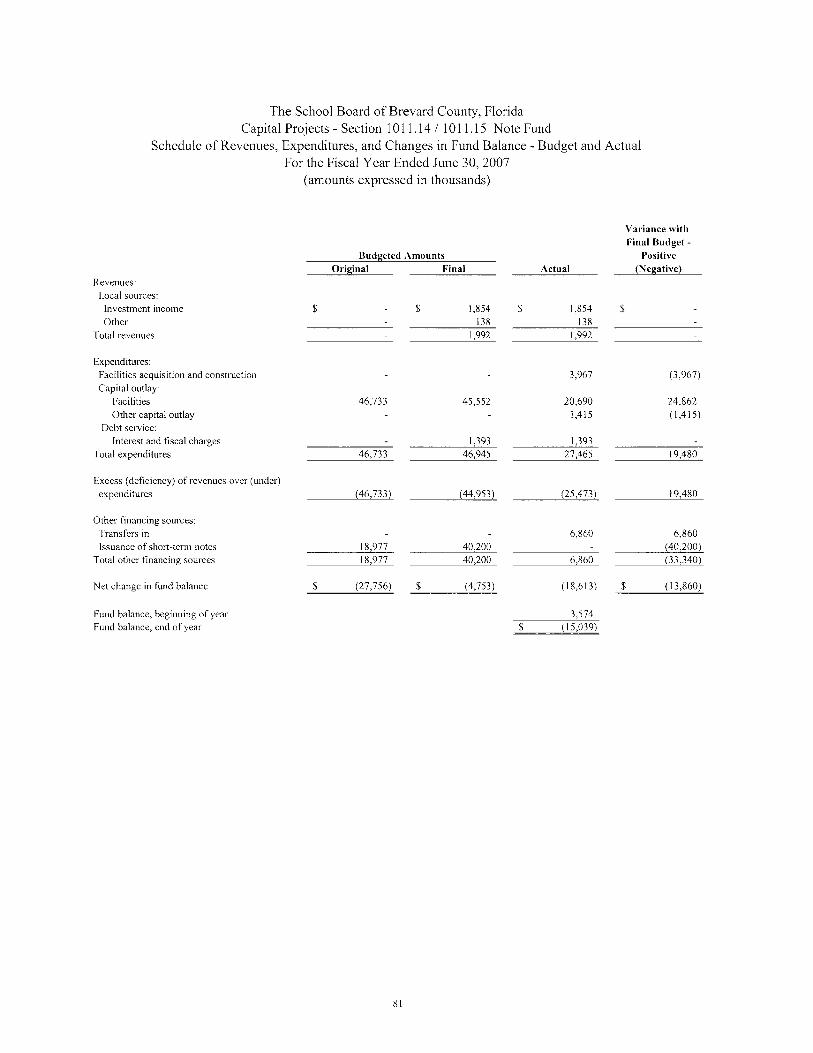

Section 1011.14/1011.15 Notes Capital Projects Fund The fund balance of the Capital Projects - Section 1011.14/1011.15 Notes Fund decreased by $18.6 million, or 520.8 percent due to the completion of projects and takedown of funds to pay for the costs of these projects.

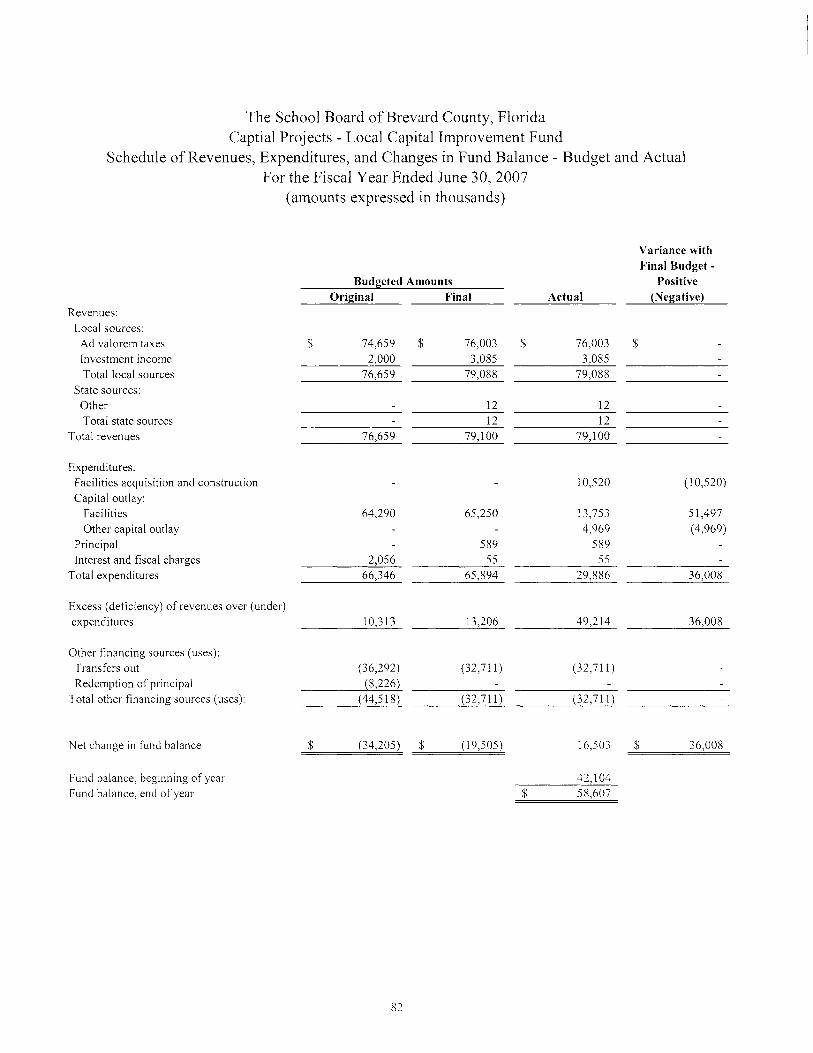

Capital Projects - Local Capital Improvement Fund The fund balance of the Capital Projects - Local Capital Improvement Fund increased by $16.5 million, or 39.2 percent. This is due mainly to the timing of payments and construction projects in progress but not yet completed.

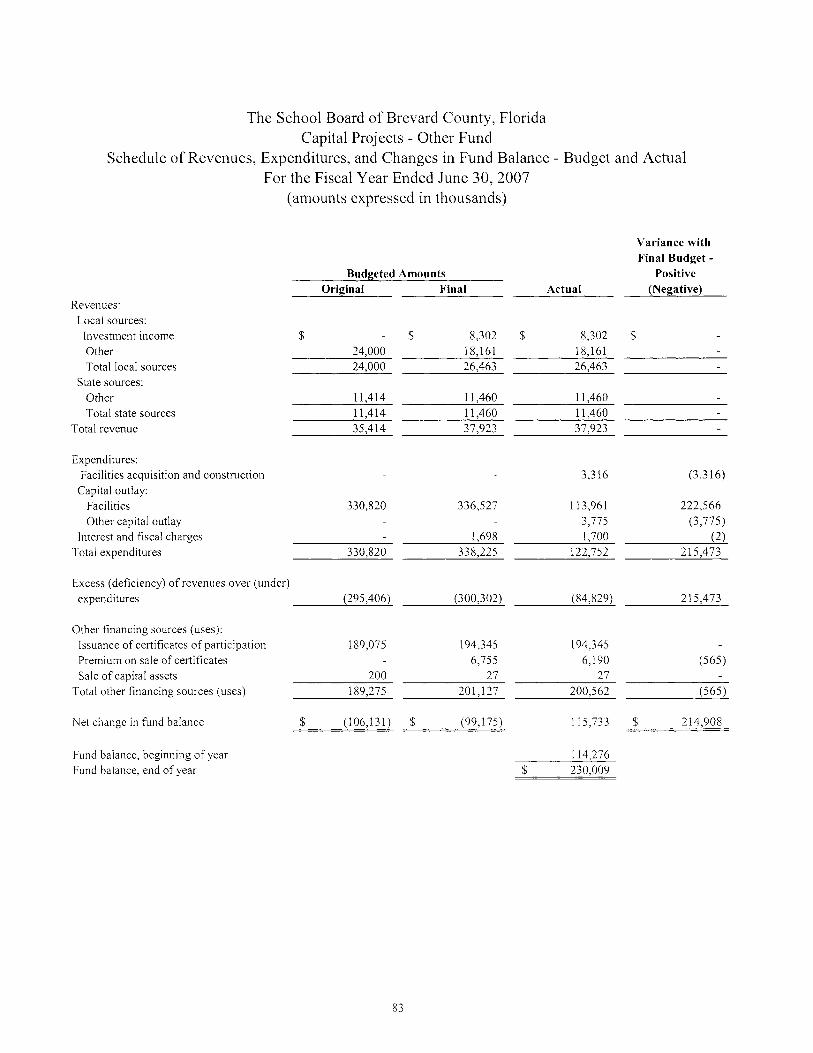

Capital Projects - Other Fund The fund balance of the in Other Capital Projects Fund increased by $115.7 million, or 101.3 percent. This increase is due to the issuance of new money certificates of participation in the par amount of $194.3 million. Many of these projects are construction in progress at fiscal year end.

14

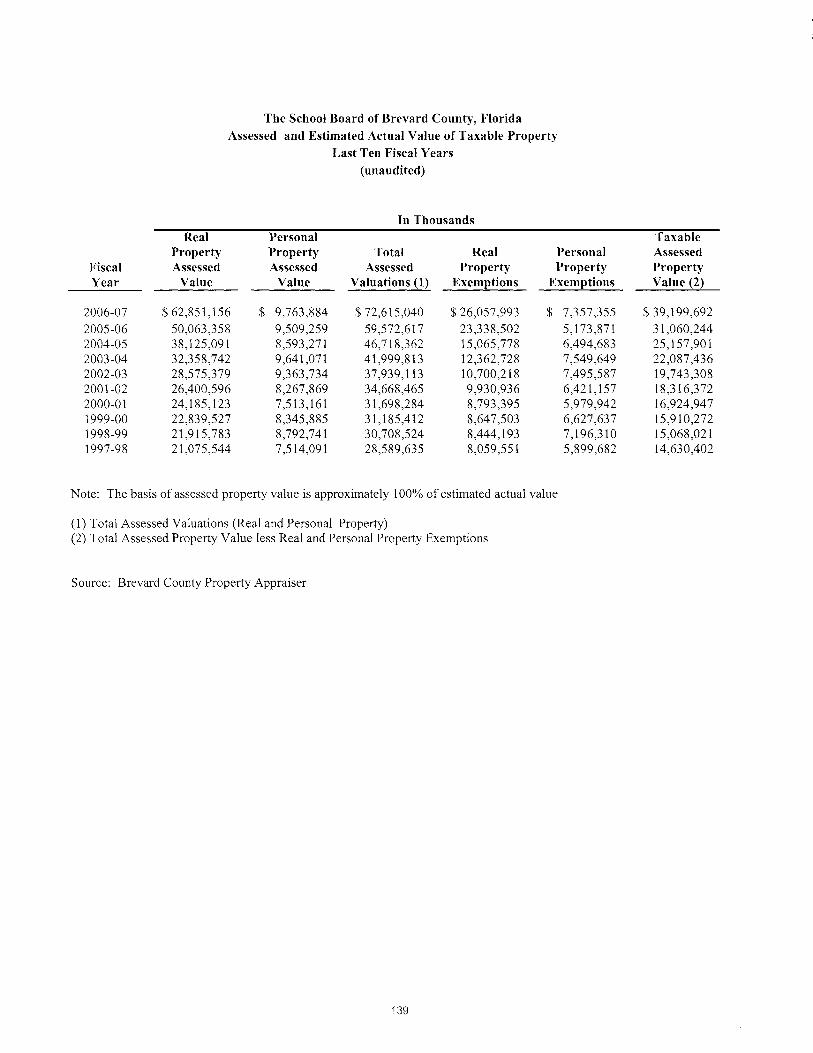

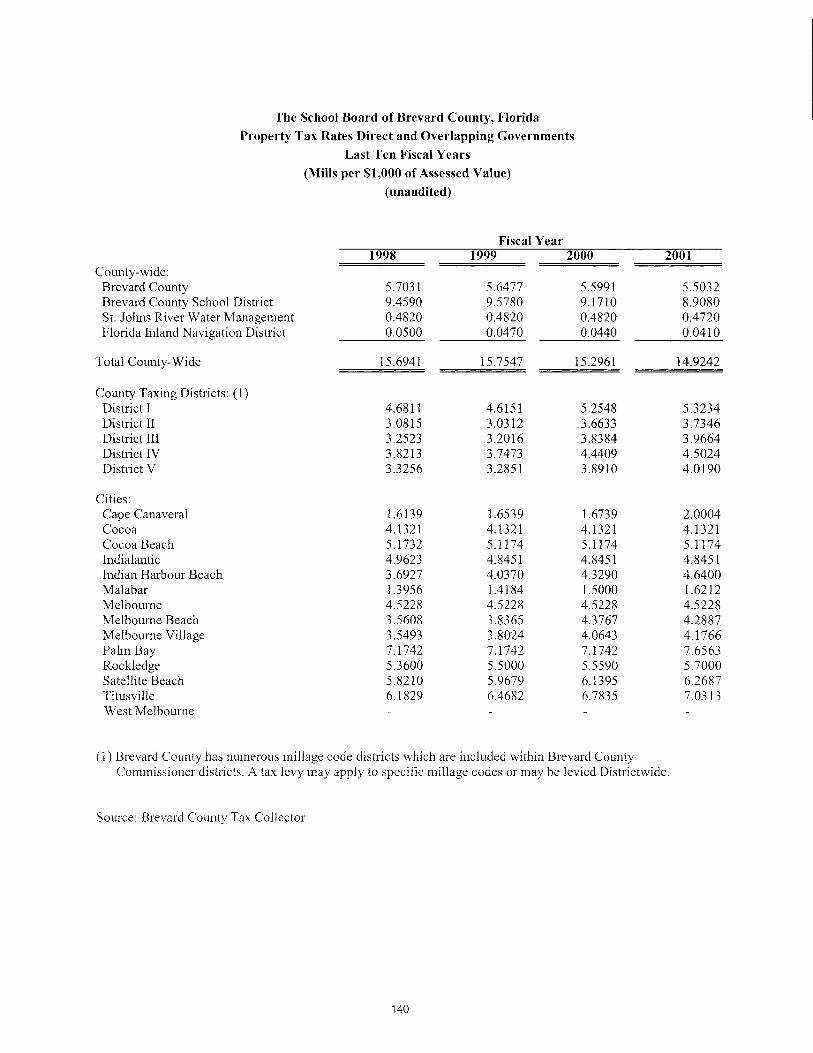

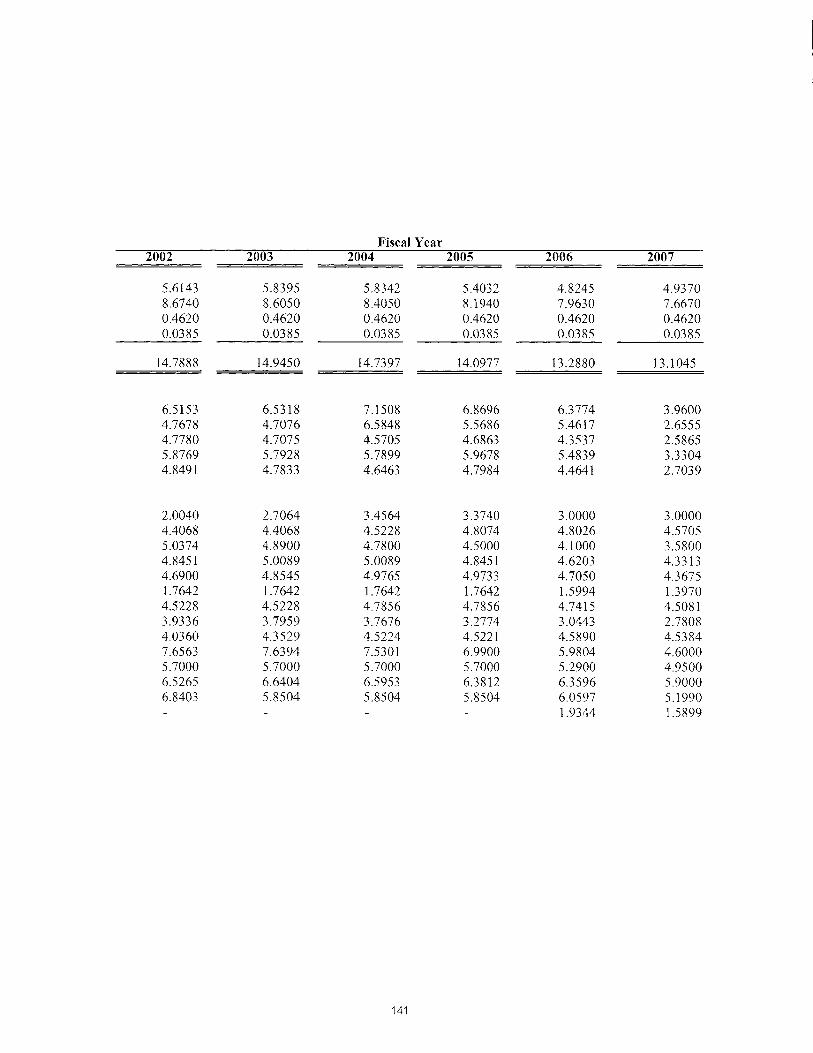

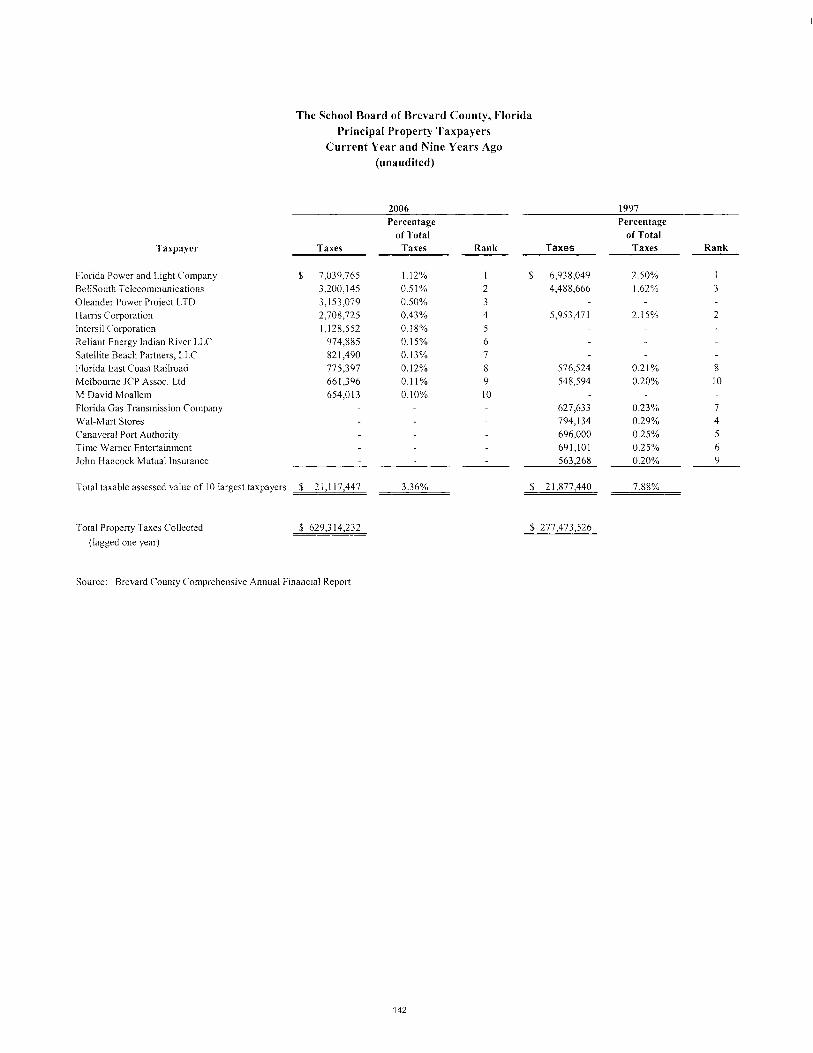

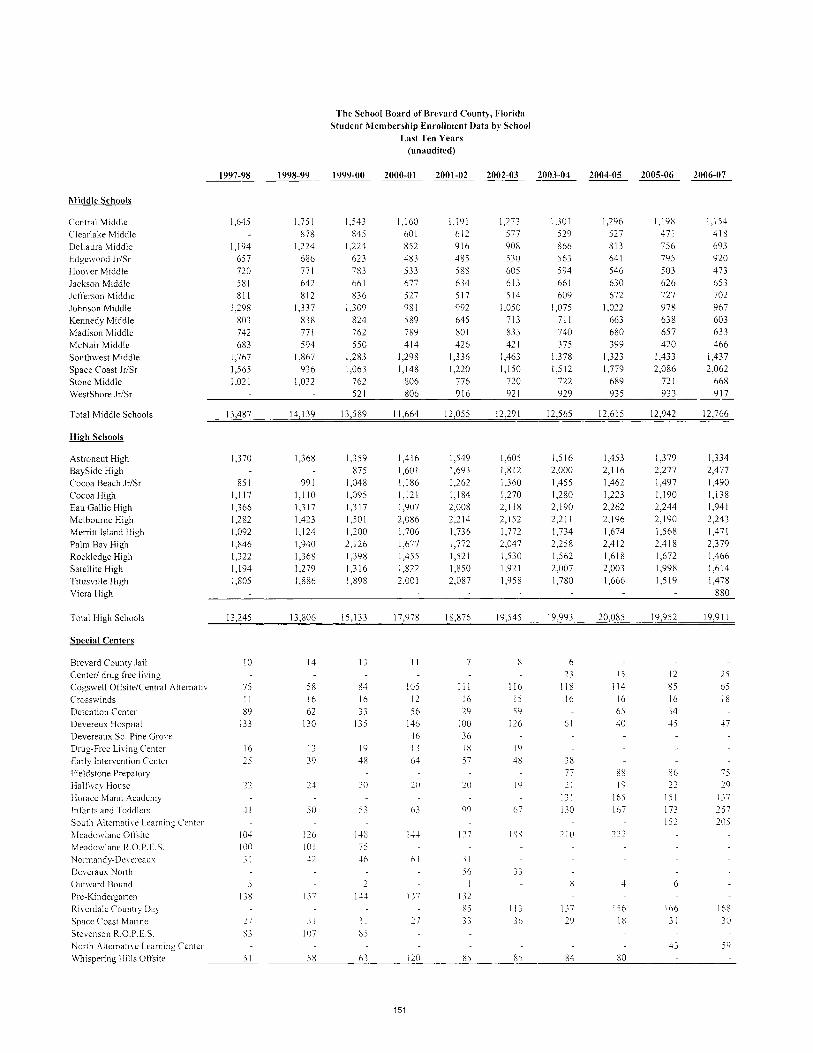

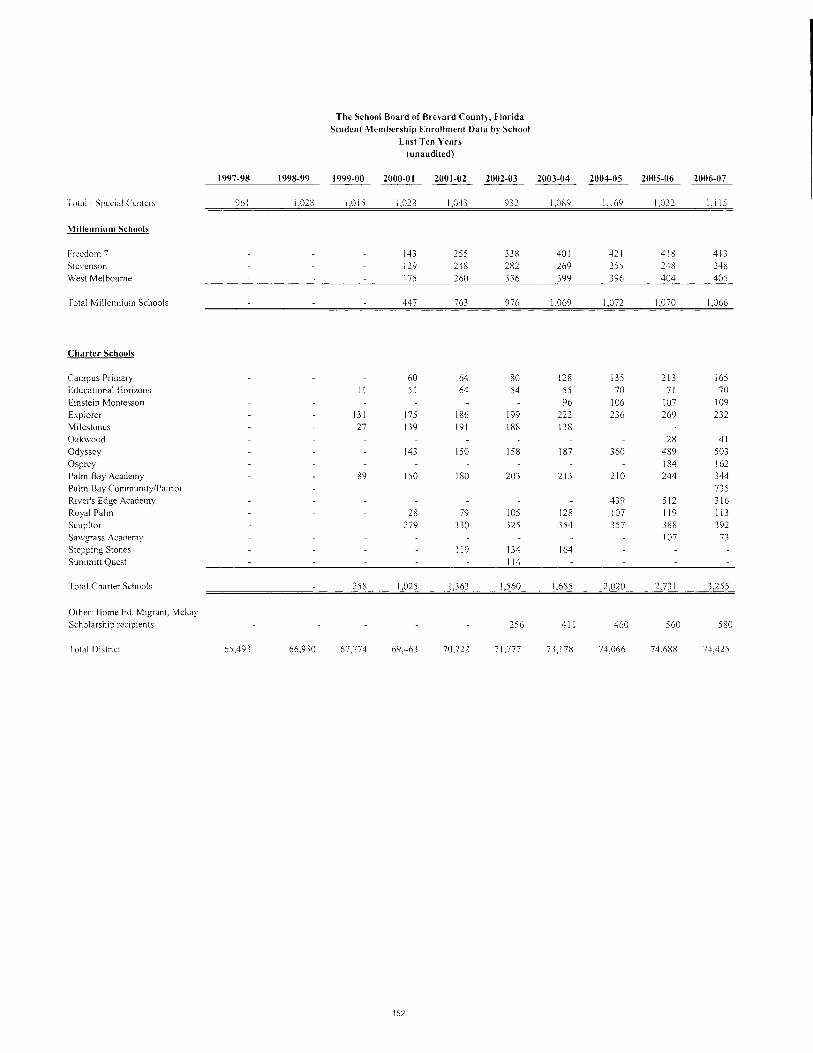

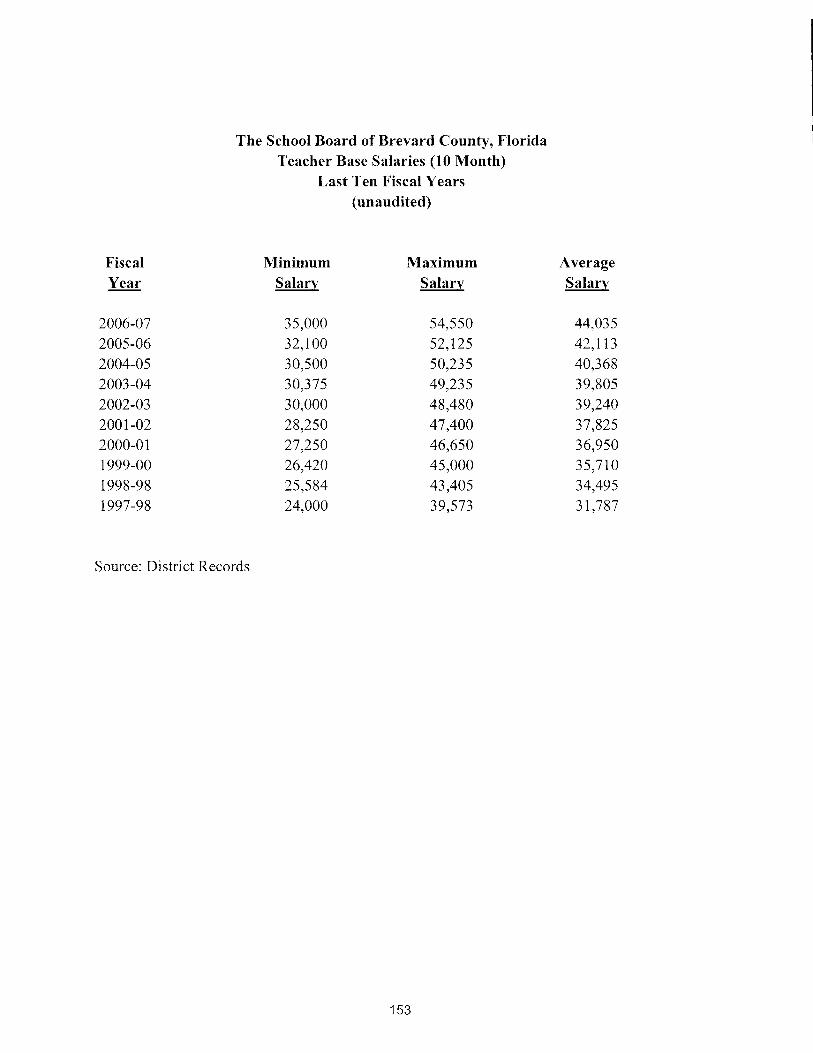

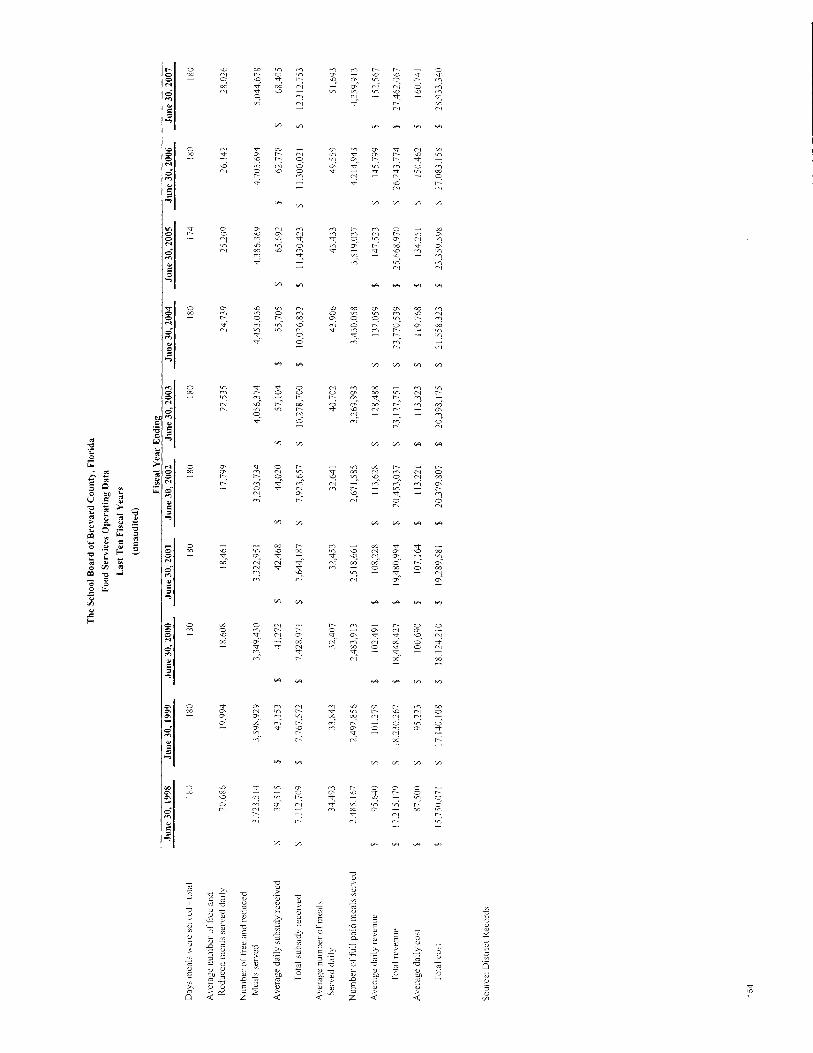

Statistical Section

Single Audit Section

Page 159

FEDERAL REPORTS AND SCHEDULES

INDEPENDENT AUDITOR’S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON AN AUDIT OF THE FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

INDEPENDENT AUDITOR’S REPORT ON COMPLIANCE WITH REQUIREMENTS APPLICABLE TO EACH MAJOR FEDERAL PROGRAM AND ON INTERNAL CONTROL OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDS

SCHEDULE OF FINDINGS AND QUESTIONED COSTS

SUMMARY SCHEDULE OF PRIOR AUDIT FINDINGS – FEDERAL AWARDS

Page 160

This page intentionally left blank.

Page 161

AUDITOR GENERAL

STATE OF FLORIDA G74 Claude Pepper Building

111 West Madison Street Tallahassee, Florida 32399-1450

The President of the Senate, the Speaker of the House of Representatives, and the Legislative Auditing Committee

INDEPENDENT AUDITOR'S REPORT ON INTERNAL CONTROL OVER FINANCIAL REPORTING AND ON COMPLIANCE AND OTHER MATTERS BASED ON

AN AUDIT OF THE FINANCIAL STATEMENTS PERFORMED IN ACCORDANCE WITH GOVERNMENT AUDITING STANDARDS

We have audited the financial statements of the governmental activities, the business-type activities, the

aggregate discretely presented component units, each major fund, and the aggregate remaining fund

information of the Brevard County District School Board as of and for the fiscal year ended June 30, 2007,

which collectively comprise the District’s basic financial statements, and have issued our report thereon

included under the heading INDEPENDENT AUDITOR'S REPORT ON FINANCIAL

STATEMENTS. Our report on the basic financial statements was modified to include a reference to other

auditors and to address the District’s exclusion of the four component units from the aggregate discretely

presented component units. We conducted our audit in accordance with auditing standards generally

accepted in the United States of America and the standards applicable to financial audits contained in

Government Auditing Standards issued by the Comptroller General of the United States. Except for the four

charter schools noted above, other auditors audited the financial statements of the aggregate discretely

presented component units, as described in our report on the Brevard County District School Board’s

financial statements. This report does not include the results of the other auditors’ testing of internal control

over financial reporting or compliance and other matters that are reported on separately by those auditors.

Internal Control Over Financial Reporting

In planning and performing our audit, we considered the District's internal control over financial reporting

as a basis for designing our auditing procedures for the purpose of expressing our opinions on the financial

statements, but not for the purpose of expressing an opinion on the effectiveness of the District’s internal

control over financial reporting. Accordingly, we do not express an opinion on the effectiveness of the

District’s internal control over financial reporting.

DAVID W. MARTIN, CPA AUDITOR GENERAL

850/488-5534/SC 278-5534 Fax: 488-6975/SC 278-6975

Page 162

A control deficiency exists when the design or operation of a control does not allow management or

employees, in the normal course of performing their assigned functions, to prevent or detect misstatements

on a timely basis. A significant deficiency is a control deficiency, or combination of control deficiencies, that

adversely affects the District's ability to initiate, authorize, record, process, or report financial data reliably in

accordance with generally accepted accounting principles such that there is more than a remote likelihood

that a misstatement of the District’s financial statements that is more than inconsequential will not be

prevented or detected by the District’s internal control. We consider the deficiencies described in the

FINDINGS AND RECOMMENDATIONS section of this audit report, Finding Nos. 1 through 6, to be

significant deficiencies in internal control over financial reporting.

A material weakness is a significant deficiency, or combination of significant deficiencies, that results in more

than a remote likelihood that a material misstatement of the financial statements will not be prevented or

detected by the District’s internal control.

Our consideration of internal control over financial reporting was for the limited purpose described in the

first paragraph of this section and would not necessarily disclose all deficiencies in internal control that might

be significant deficiencies and, accordingly, would not necessarily disclose all significant deficiencies that are

also considered to be material weaknesses. However, we believe that none of the significant deficiencies

described above is a material weakness.

Compliance and Other Matters

As part of obtaining reasonable assurance about whether the District’s financial statements are free of

material misstatement, we performed tests of its compliance with certain provisions of laws, administrative

rules, regulations, contracts, and grant agreements, noncompliance with which could have a direct and

material effect on the determination of financial statement amounts. However, providing an opinion on

compliance with those provisions was not an objective of our audit and, accordingly, we do not express such

an opinion. The results of our tests disclosed no instances of noncompliance or other matters that are

required to be reported under Government Auditing Standards.

Also, we noted certain additional matters which are not material to the basic financial statements which are

discussed in the FINDINGS AND RECOMMENDATIONS section of this audit report.

The District’s response to the findings identified in our audit is described in the accompanying

MANAGEMENT RESPONSE. We did not audit the District’s response and, accordingly, we express no

opinion on it.

Page 163

This report is intended for the information of the Legislative Auditing Committee, members of the Florida

Senate and the Florida House of Representatives, Federal and other granting agencies, and applicable

management. Copies of this report are available pursuant to Section 11.45(4), Florida Statutes, and its

distribution is not limited.

Respectfully submitted,

David W. Martin, CPA January 25, 2008

Page 164

This page intentionally left blank.

Page 165

AUDITOR GENERAL

STATE OF FLORIDA

G74 Claude Pepper Building 111 West Madison Street

Tallahassee, Florida 32399-1450 The President of the Senate, the Speaker of the House of Representatives, and the Legislative Auditing Committee

INDEPENDENT AUDITOR'S REPORT ON AUDIT OF COMPLIANCE WITH REQUIREMENTS APPLICABLE TO EACH MAJOR FEDERAL PROGRAM

AND ON INTERNAL CONTROL OVER COMPLIANCE IN ACCORDANCE WITH OMB CIRCULAR A-133

Compliance

We have audited the District's compliance with the types of compliance requirements described in the

United States Office of Management and Budget's (OMB) Circular A-133 Compliance Supplement that are

applicable to each of its major Federal programs for the fiscal year ended June 30, 2007. The District’s major

Federal programs are identified in the SUMMARY OF AUDITOR’S RESULTS section of the

accompanying SCHEDULE OF FINDINGS AND QUESTIONED COSTS. Compliance with the

requirements of laws, regulations, contracts, and grants applicable to each of the District’s major Federal

programs is the responsibility of District management. Our responsibility is to express an opinion on the

District’s compliance based on our audit.

We conducted our audit of compliance in accordance with auditing standards generally accepted in the

United States of America; the standards applicable to financial audits contained in Government Auditing

Standards, issued by the Comptroller General of the United States; and the OMB’s Circular A-133, Audits of

States, Local Governments, and Non-Profit Organizations. Those standards and OMB Circular A-133 require that

we plan and perform the audit to obtain reasonable assurance about whether noncompliance with the types

of compliance requirements referred to above that could have a direct and material effect on a major Federal

program occurred. An audit includes examining, on a test basis, evidence about the District’s compliance

with those requirements and performing such other procedures as we considered necessary in the

circumstances. We believe that our audit provides a reasonable basis for our opinion. Our audit does not

provide a legal determination of the District's compliance with those requirements.

DAVID W. MARTIN, CPA AUDITOR GENERAL

850/488-5534/SC 278-5534 Fax: 488-6975/SC 278-6975

Page 166

In our opinion, the District complied, in all material respects, with the requirements referred to above that

are applicable to each of its major Federal programs for the year ended June 30, 2007.

Internal Control Over Compliance

District management is responsible for establishing and maintaining effective internal control over

compliance with requirements of laws, regulations, contracts, and grants applicable to Federal programs. In

planning and performing our audit, we considered the District’s internal control over compliance with the

requirements that could have a direct and material effect on a major Federal program in order to determine

our auditing procedures for the purpose of expressing our opinion on compliance, but not for the purpose

of expressing an opinion on the effectiveness of internal control over compliance. Accordingly, we do not

express an opinion on the effectiveness of the District’s internal control over compliance.

A control deficiency in the District’s internal control over compliance exists when the design or operation of

a control does not allow management or employees, in the normal course of performing their assigned

functions, to prevent or detect noncompliance with a type of compliance requirement of a Federal program

on a timely basis. A significant deficiency is a control deficiency, or combination of control deficiencies, that

adversely affects the District’s ability to administer a Federal program such that there is more than a remote

likelihood that noncompliance with a type of compliance requirement of a Federal program that is more than

inconsequential will not be prevented or detected by the District’s internal control.

A material weakness is a significant deficiency, or combination of significant deficiencies, that results in more

than a remote likelihood that material noncompliance with a type of compliance requirement of a Federal

program will not be prevented or detected by the District’s internal control.

Our consideration of internal control over compliance was for the limited purpose described in the first

paragraph of this section and would not necessarily identify all deficiencies in internal control that might be

significant deficiencies or material weaknesses. We did not identify any deficiencies in internal control over

compliance that we consider to be material weaknesses, as defined above.

This report is intended for the information of the Legislative Auditing Committee, members of the Florida

Senate and the Florida House of Representatives, Federal and other granting agencies, and applicable

management. Copies of this report are available pursuant to Section 11.45(4), Florida Statutes, and its

distribution is not limited.

Respectfully submitted,

David W. Martin, CPA January 25, 2008

Page 167

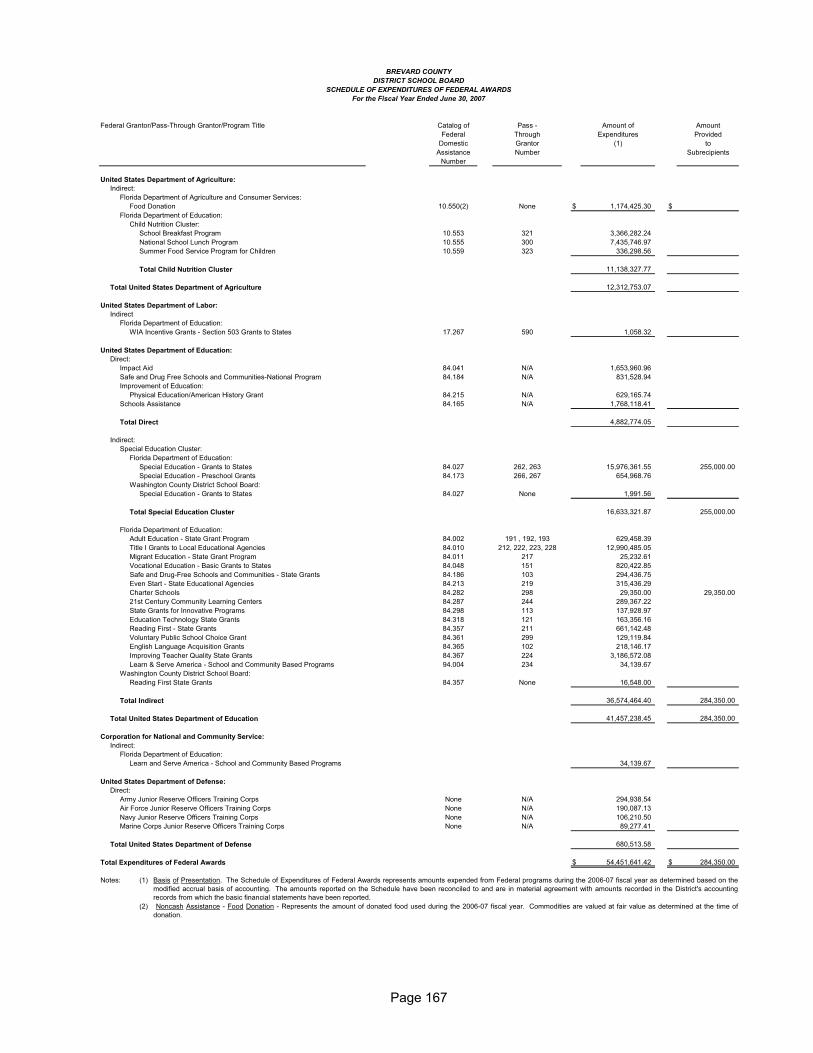

BREVARD COUNTYDISTRICT SCHOOL BOARD

SCHEDULE OF EXPENDITURES OF FEDERAL AWARDSFor the Fiscal Year Ended June 30, 2007

Federal Grantor/Pass-Through Grantor/Program Title Catalog of Pass - Amount of AmountFederal Through Expenditures Provided

Domestic Grantor (1) toAssistance Number Subrecipients

Number

United States Department of Agriculture:Indirect:

Florida Department of Agriculture and Consumer Services:Food Donation 10.550(2) None $ 1,174,425.30 $

Florida Department of Education:Child Nutrition Cluster:

School Breakfast Program 10.553 321 3,366,282.24 National School Lunch Program 10.555 300 7,435,746.97 Summer Food Service Program for Children 10.559 323 336,298.56

Total Child Nutrition Cluster 11,138,327.77

Total United States Department of Agriculture 12,312,753.07

United States Department of Labor:Indirect

Florida Department of Education:WIA Incentive Grants - Section 503 Grants to States 17.267 590 1,058.32

United States Department of Education:Direct:

Impact Aid 84.041 N/A 1,653,960.96 Safe and Drug Free Schools and Communities-National Program 84.184 N/A 831,528.94 Improvement of Education:

Physical Education/American History Grant 84.215 N/A 629,165.74 Schools Assistance 84.165 N/A 1,768,118.41

Total Direct 4,882,774.05

Indirect:Special Education Cluster:

Florida Department of Education:Special Education - Grants to States 84.027 262, 263 15,976,361.55 255,000.00 Special Education - Preschool Grants 84.173 266, 267 654,968.76

Washington County District School Board:Special Education - Grants to States 84.027 None 1,991.56

Total Special Education Cluster 16,633,321.87 255,000.00

Florida Department of Education:Adult Education - State Grant Program 84.002 191 , 192, 193 629,458.39 Title I Grants to Local Educational Agencies 84.010 212, 222, 223, 228 12,990,485.05 Migrant Education - State Grant Program 84.011 217 25,232.61 Vocational Education - Basic Grants to States 84.048 151 820,422.85 Safe and Drug-Free Schools and Communities - State Grants 84.186 103 294,436.75 Even Start - State Educational Agencies 84.213 219 315,436.29 Charter Schools 84.282 298 29,350.00 29,350.00 21st Century Community Learning Centers 84.287 244 289,367.22 State Grants for Innovative Programs 84.298 113 137,928.97 Education Technology State Grants 84.318 121 163,356.16 Reading First - State Grants 84.357 211 661,142.48 Voluntary Public School Choice Grant 84.361 299 129,119.84 English Language Acquisition Grants 84.365 102 218,146.17 Improving Teacher Quality State Grants 84.367 224 3,186,572.08 Learn & Serve America - School and Community Based Programs 94.004 234 34,139.67

Washington County District School Board:Reading First State Grants 84.357 None 16,548.00

Total Indirect 36,574,464.40 284,350.00

Total United States Department of Education 41,457,238.45 284,350.00

Corporation for National and Community Service:Indirect:

Florida Department of Education:Learn and Serve America - School and Community Based Programs 34,139.67

United States Department of Defense:Direct:

Army Junior Reserve Officers Training Corps None N/A 294,938.54 Air Force Junior Reserve Officers Training Corps None N/A 190,087.13 Navy Junior Reserve Officers Training Corps None N/A 106,210.50 Marine Corps Junior Reserve Officers Training Corps None N/A 89,277.41

Total United States Department of Defense 680,513.58

Total Expenditures of Federal Awards $ 54,451,641.42 $ 284,350.00

Notes: (1)

(2)

Basis of Presentation. The Schedule of Expenditures of Federal Awards represents amounts expended from Federal programs during the 2006-07 fiscal year as determined based on themodified accrual basis of accounting. The amounts reported on the Schedule have been reconciled to and are in material agreement with amounts recorded in the District's accountingrecords from which the basic financial statements have been reported.Noncash Assistance - Food Donation - Represents the amount of donated food used during the 2006-07 fiscal year. Commodities are valued at fair value as determined at the time of

donation.

Page 168

BREVARD COUNTY

DISTRICT SCHOOL BOARD SCHEDULE OF FINDINGS AND QUESTIONED COSTS

FOR THE FISCAL YEAR ENDED JUNE 30, 2007

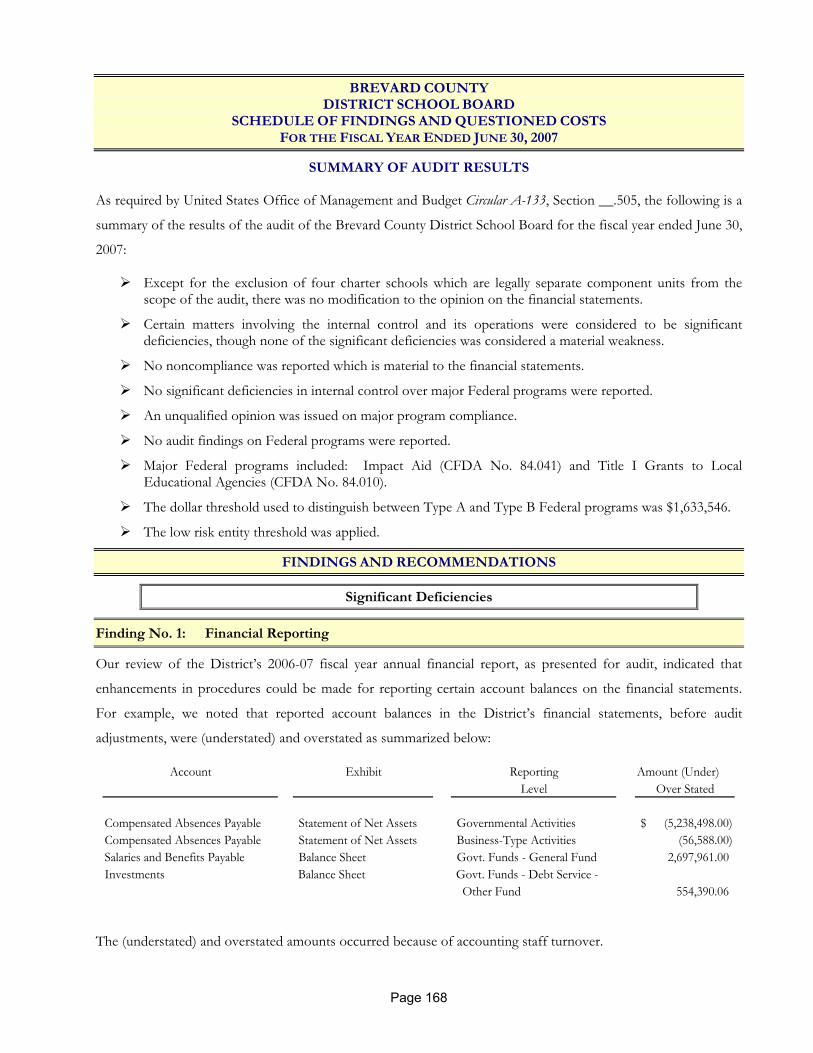

SUMMARY OF AUDIT RESULTS

As required by United States Office of Management and Budget Circular A-133, Section __.505, the following is a

summary of the results of the audit of the Brevard County District School Board for the fiscal year ended June 30,

2007: