Embed Size (px)

Citation preview

COMPONENT PRICING IN CANOLA: Weighing the Options

Prepared For: SaskCanola

Principal Authors: Tyler Bjornson, Christina Patterson and Shannon Schlecht

February 7, 2016

1 | P a g e

Table of Contents

Executive Summary ....................................................................................................................................... 3

Scope of the Project ...................................................................................................................................... 5

Introduction .................................................................................................................................................. 6

Section 1: Market Factors ............................................................................................................................. 7

Nature of Global Business in Canola ......................................................................................................... 7

Substitutes and the International Vegetable Oil Market .......................................................................... 7

Structure of International Purchase Contracts ....................................................................................... 11

Structure of Crushing Industry ................................................................................................................ 12

Structure of Grain Elevator Business ...................................................................................................... 13

Pricing Factors – Freight vs. Oil Content Premium ................................................................................. 14

Discounts & Premiums ............................................................................................................................ 15

Section 2: Production Factors ..................................................................................................................... 16

Overview ................................................................................................................................................. 16

North-South Oil Content Observations ................................................................................................... 20

Varieties .................................................................................................................................................. 22

Environment ........................................................................................................................................... 25

Agronomic Practices ............................................................................................................................... 26

Section 3: Implementation Issues ............................................................................................................... 28

Sampling/Testing .................................................................................................................................... 28

Storage/Segregation ............................................................................................................................... 28

Basis ........................................................................................................................................................ 29

Industry Views ......................................................................................................................................... 30

Producer Groups ................................................................................................................................. 30

Section 4: International Experience ............................................................................................................ 32

Australia .................................................................................................................................................. 33

Premium/Discount Schedule .............................................................................................................. 34

Environment........................................................................................................................................ 34

Results ................................................................................................................................................. 34

European Union ...................................................................................................................................... 35

Premium and Discount Schedule ........................................................................................................ 37

Testing ................................................................................................................................................. 38

Results ................................................................................................................................................. 38

2 | P a g e

United States ........................................................................................................................................... 38

Premium and Discount Schedule ........................................................................................................ 39

Results ................................................................................................................................................. 39

Other oilseeds in the international marketplace .................................................................................... 40

Section 5: Modelling Factors ....................................................................................................................... 42

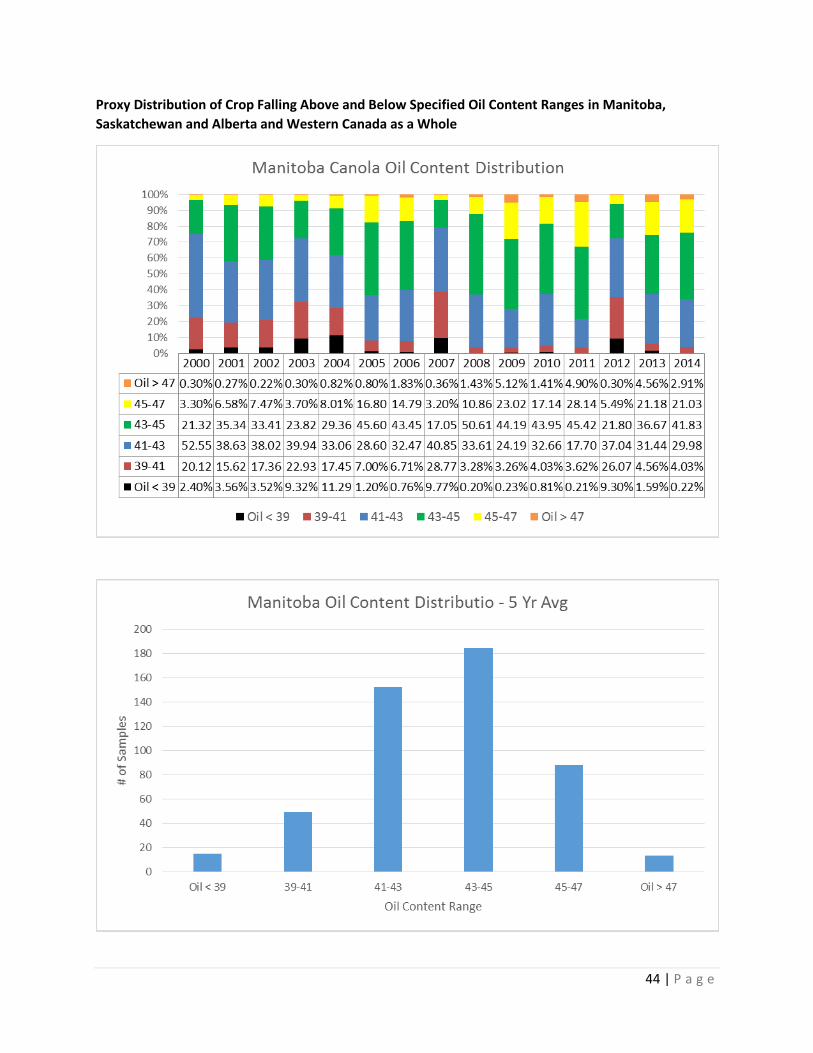

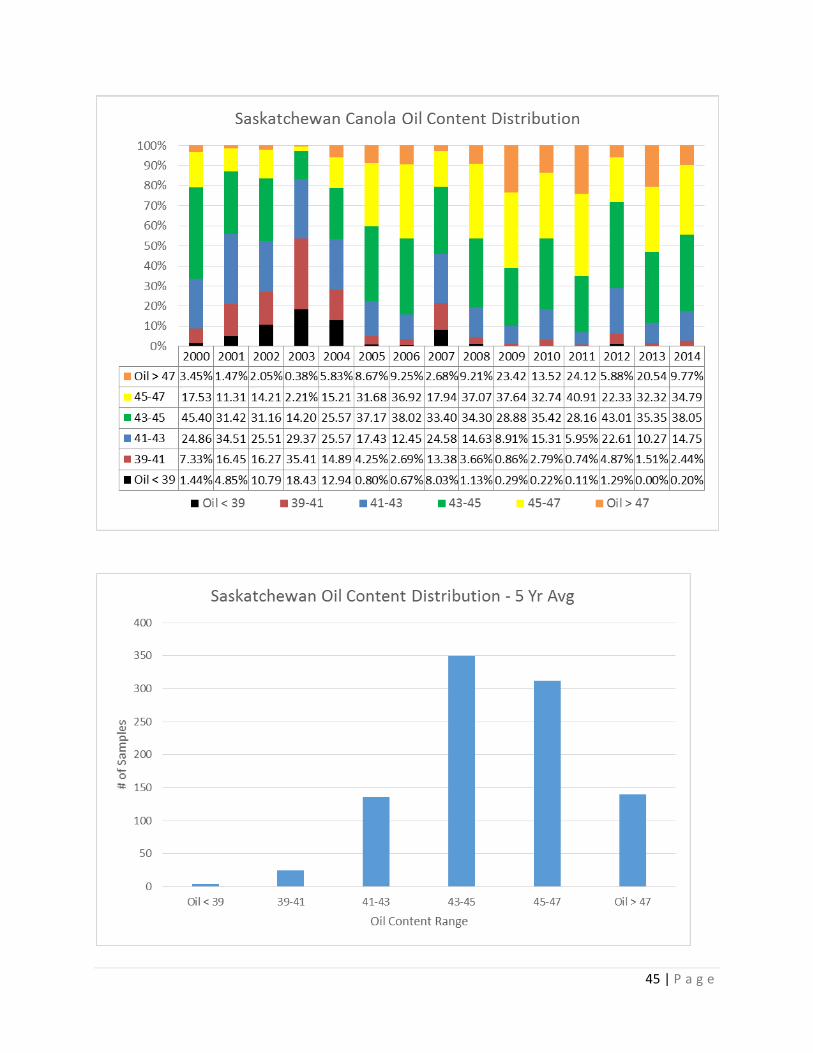

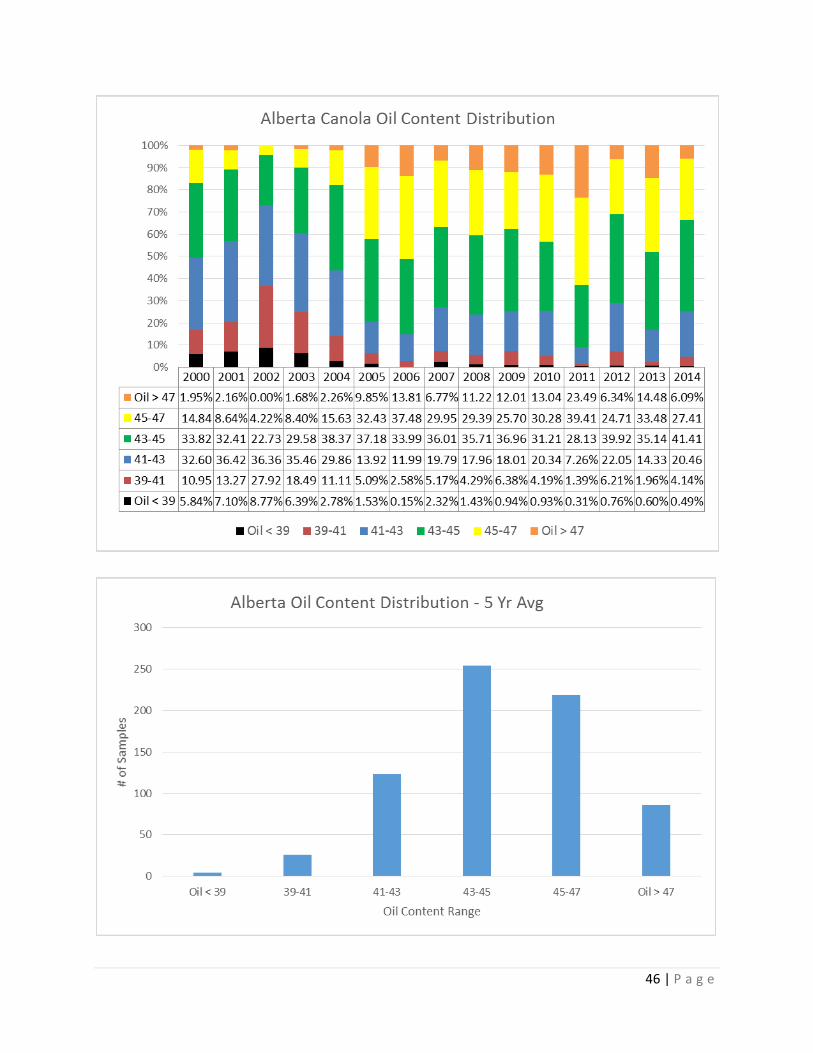

Oil Content Distribution .......................................................................................................................... 42

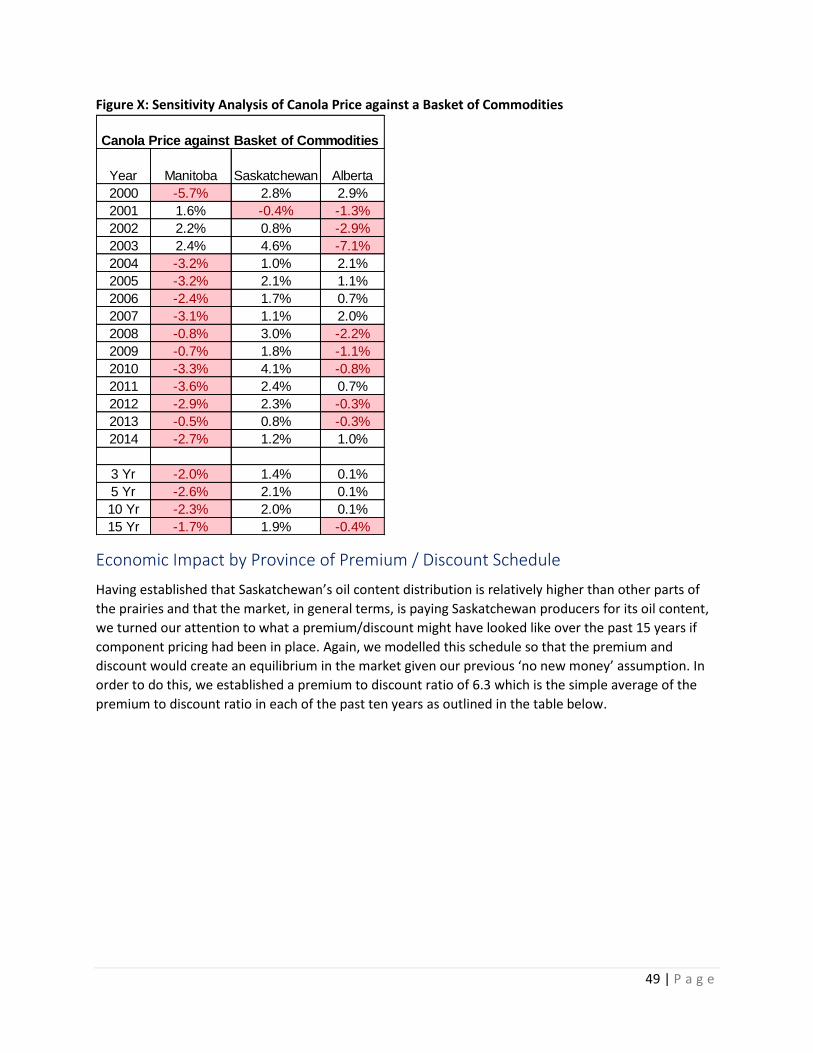

Sensitivity Analysis of Canola Prices Vs. Basket of Commodities ........................................................... 48

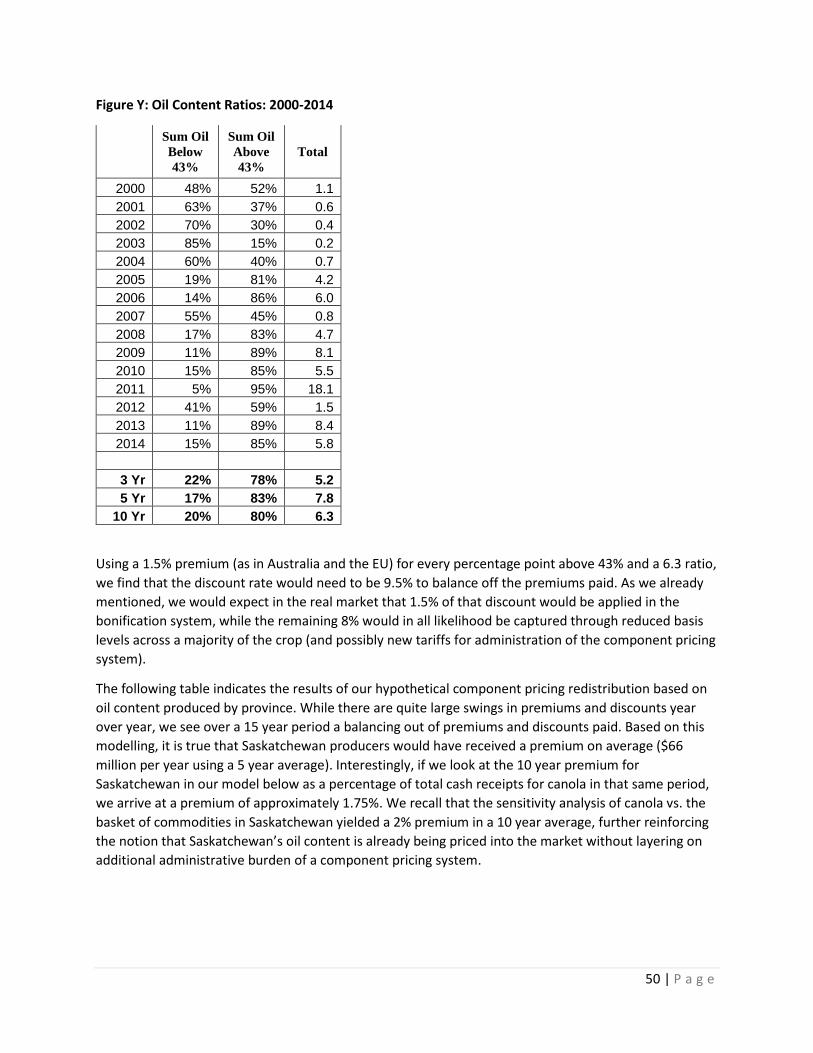

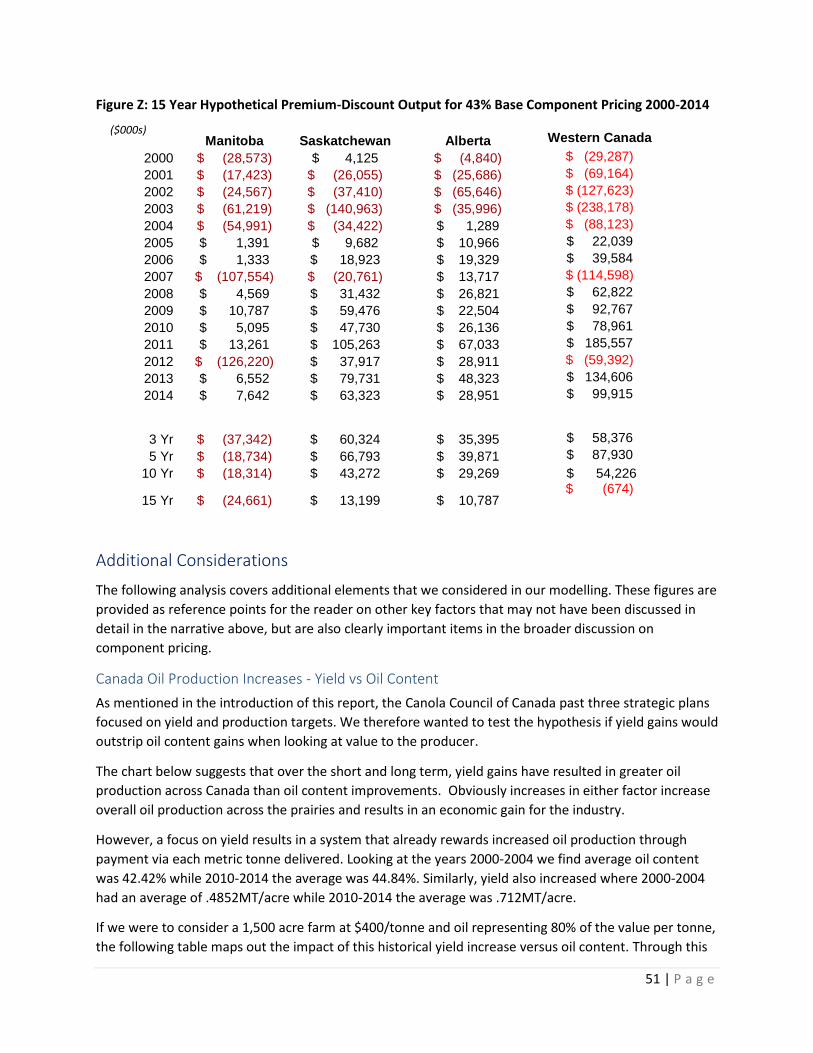

Economic Impact by Province of Premium / Discount Schedule ............................................................ 49

Additional Considerations ....................................................................................................................... 51

Canada Oil Production Increases - Yield vs Oil Content ...................................................................... 51

Value of Oil Content by Province ........................................................................................................ 52

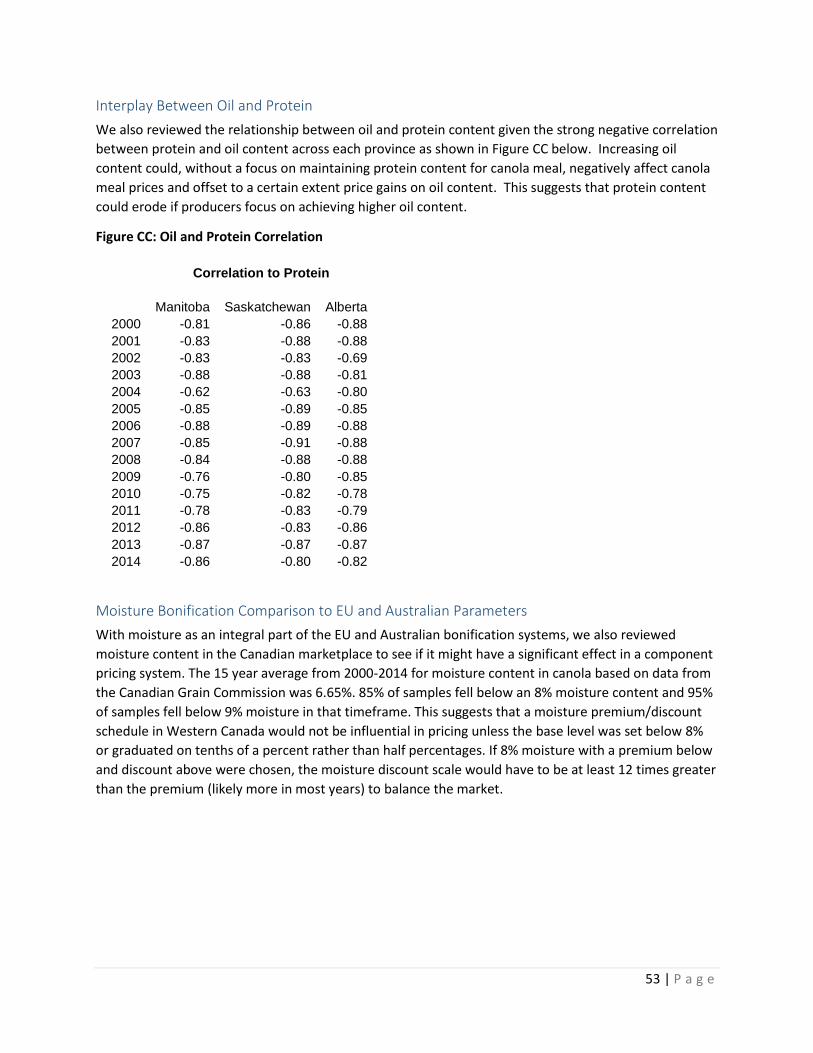

Interplay Between Oil and Protein...................................................................................................... 53

Moisture Bonification Comparison to EU and Australian Parameters ............................................... 53

Section 6: Conclusion & Recommendations ............................................................................................... 54

Recommendations .................................................................................................................................. 56

APPENDIX A – Questionnaire ...................................................................................................................... 57

Industry Questionnaire for SaskCanola Component Pricing Project ...................................................... 57

APPENDIX B – Overview of Interviewee Backgrounds ................................................................................ 60

APPENDIX C – Select Bibliography .............................................................................................................. 61

3 | P a g e

Executive Summary

This report provides an analysis and evaluation of moving the Canadian canola industry to a component

pricing system with a focus on oil content. The study considers whether component pricing would

create new value for the canola industry and whether it would result in a net benefit to the sector at

large and specifically to Saskatchewan canola producers. Market factors, production factors, relevant

international experience, implementation matters and statistical modelling are all reviewed as part of

this assessment.

The research and analysis in this report looks at global market factors such as canola’s substitutability,

the potential for product differentiation in the eyes of customers, canola’s shape and share of the

international vegetable oil market, the structure of demand from domestic buyers and importing

countries, the nature of international contracts in canola and competition from other producing

countries. It finds that canola in the international market carries the attributes of a bulk commodity

market and the need for high volume and efficient execution to drive value. Based on this assessment

and corroborated by extensive interviews, it determines that it would be unlikely that Canadian traders

would be able to extract additional value (i.e., beyond what is already captured today) for canola

sourced through a component pricing mechanism where premiums (or discounts) would have been paid

for higher (lower) oil content product.

Also assessed are the domestic market factors that similarly influence how and why buyers of farm gate

canola in the Western Canadian landscape act. It discusses the limitations and opportunities for

domestic buyers which in turn impacts the value that producers ultimately receive for their canola. The

report surmises that most buyers are driven by asset utilization and efficiency as well as freight costs vs.

opportunity. Regarding the latter, the study concludes that freight cost alone would be a significant

inhibitor to long haul procurement beyond natural catchment areas for local facilities in order to capture

high oil content opportunities.

It also reviews comparable markets namely the European Union (EU) and Australia which already use

component based pricing or ‘bonification’ systems. The study evaluates the relative success the system

has had at creating benefit or adding cost for the industry in those instances and draws lessons learned

which could be relevant to the Canadian context.

The report discusses production factors that could influence oil content in Western Canadian production

and concludes that environment and genetics are the major variables. In relation to varieties, it

highlights the jump in oil content roughly a decade ago corresponding to the introduction of new

genetics which may in large part be responsible for a relative narrowing of oil content distribution year

over year and between regions. Overall, it notes that producers have relatively few tools to directly

control oil content and as such, argues that this will balance out ‘good’ and ‘bad’ years and the

premiums or discounts that would come with them in a component pricing model.

Implementation matters are considered, including costs to administer component pricing, testing,

segregation costs among other issues. The study determines that while certain items may not be as

contentious as some actors suggest (e.g., testing), there will be costs to administering a bonification

model and these would be borne by the value chain without being able to pass them on to final

4 | P a g e

customers. Producers should be wary of adding costs into the system that could in part end up being

factored into the farm gate price.

Through a sensitivity analysis of canola pricing versus a basket of commodities, the report also finds that

Saskatchewan producers under the current system are already rewarded for higher oil content. If a

component pricing system were put into place, we anticipate that buyers would simply adjust basis

levels to accurately reflect local and international market expectations yielding the same profit result for

producers either inside or outside a bonification system.

Finally, the study considers a range of statistical information to aid analysis of a hypothetical oil content

pricing system and its potential impact on Saskatchewan canola producers. Data was gathered to model

different scenarios based on historical quality information, most notably the variance in oil content and

the distribution of oil content levels across the three main producing provinces. The model attempts to

illustrate the possible consequences for different production areas and its producers under a

component pricing system based on oil content.

In this it finds that the proportion of canola with oil content above 43% in Saskatchewan compared to

content below 43% is such that either punishing discounts would have to be in place to balance the

market or offsetting reductions in basis levels would need to occur to pay for the premium schedule

given that no new value is being created in the international market through the introduction of a

component pricing system in Canada. Overall it finds that while Saskatchewan producers may benefit

slightly from an oil content premium over time, it pales in comparison to the value driven by increased

canola yield on farm.

In a time when the canola industry is striving for continued higher production and greater yields, the

implementation of a system that focuses on oil content as a major pricing component may send the

wrong signal to producers and seed developers, add costs to administer the system that cannot be

recouped from customers, be a distraction and potential loadstone for unnecessary debate and friction

within the value chain, and would clearly create winners and losers among producers themselves.

The report finds that Saskatchewan canola producers have other opportunities to assess on a semi-

regular basis to determine if farmers are being paid the full value for their canola, and outlines

recommendations for SaskCanola to determine if its members are being fairly compensated through the

marketplace.

5 | P a g e

Scope of the Project

Component pricing of canola based on oil content is an issue that has been raised by some producers

across Western Canada. With the increasing oil content over the last number of years, especially in

Saskatchewan, some producers believe they are not being fully compensated when they sell their canola

with a higher oil content.

Like so many issues in the industry, there is no consensus on component pricing either between

producers or among various segments in the value chain. Historically, canola produced in Alberta had

the highest average oil content, while that produced in Manitoba has the lowest, with Saskatchewan

falling the middle. As such, the Alberta Canola Producers Commission has been vocal in its support of

component pricing whereas the Manitoba Canola Growers Association does not support a move to

component pricing.

Component pricing is not a unique concept. Premiums have been paid for higher protein content in

wheat for many years, so farmers wonder why something similar cannot be done for canola.

Other jurisdictions have implemented component pricing for canola. In Australia, the original goal of

moving to component pricing was to encourage the production of a consistent, higher quality product.

Across the Atlantic, the European market has had a bonification system in place for many years,

although it too has its own distinct characteristics that need to be taken into account when used as a

point of reference for this study.

Last year, SaskCanola invested in a study on canola crush margins and basis and are now looking to build

on that information by further researching the benefits and drawbacks of a potential component pricing

model for canola based on oil content.

Through investigative research and supply chain outreach, both in Canada and other jurisdictions, New

West Public Affairs will address the key factors in this report on whether or not it would be beneficial for

Saskatchewan producers to advocate for component pricing.

New West has engaged in significant online research, acquired considerable data from both government

and industry sources, and conducted phone interviews with canola handlers, exporters, processors and

their industry association representatives. The project is divided into six sections. Section 1 covers

market factors, Section 2 explores production factors, Section 3 discusses international experience with

component pricing in canola, Section 4 looks at implementation considerations, and Section 5 reviews

scenarios and information drawn from original modelling completed by New West for this project.

Finally, Section 6 provides conclusions and recommendations on component pricing for SaskCanola’s

consideration.

6 | P a g e

Introduction

Canada’s canola industry is a major success for the entire crop sector value chain. Since its inception in

the late 1970’s, canola is now second only to wheat in Canadian crop production volumes, but number

one in overall value to producers accounting for one quarter of all farm cash receipts1. Canada is by far

the largest exporter of canola at 74% of the world’s trade in this product. A significant domestic

crushing industry has also followed this success with roughly half of total canola production now going

to local value added processing facilities, and a major portion of that also undergoing further refining

within many of these plants. By adding in the major investments and assets required to refine,

companies have signaled their commitment to supply from Canada as the finished product is now

market ready for sale to end consumers (versus simply crushing for crude oil then transporting to a

refinery closer to market for the final processing steps.) In addition, the largest global research and

development investments in canola are being made in Canada, the only major crop to see this happen.

Alongside the incredible rise of this crop has come a relatively unique model of cooperation among

segments of the value chain, which includes considerable financial support from producers. There can

be challenges when competitors and members of the supply chain are brought around the same table,

however a lot of success of the canola industry can be attributed to everyone in the value chain

participating in the Canola Council of Canada. This includes work on production practices and

monitoring, market development research and promotion activities, regulatory improvements and

policy development particularly in the area of international trade and market access. Perhaps most

importantly, the value chain also cooperates extensively in the development and implementation of a

broad sector strategy to increase value of the sector to all of its participants. In the early 2000s this took

the form of a strategy calling on increased volumes in order to become more relevant to the global

vegetable oil complex and less risky from a supply perspective for potential end use customers to make

the switch to canola. The value chain is now on its third such strategy, going from a seed volume target

of 7 million tonnes by 2007 to its current overarching goal of achieving 26 million tonnes and 52 bushels

per acre by 2025.

1 Canola Council of Canada: http://www.canolacouncil.org/markets-stats/industry-overview/

7 | P a g e

Section 1: Market Factors

Nature of Global Business in Canola

This backdrop is relevant to the current study for several reasons. Firstly, even with a tripling of bulk

seed production volumes over two decades, canola’s overall share of the global vegetable oil market is

still smaller by comparison to the consumption of palm oil and soybean oil (See Figure A). In other

words, the canola oil market is from an international perspective still relatively illiquid in the eyes of

major global customers. This is particularly evident when one looks at the export market versus

production as we discuss further below.

Secondly, canola pricing internationally is still very much tied to the international market and pricing of

soybean oil, meaning canola is a bulk commodity product in the global market albeit with certain health

and functional attributes which do command a typical higher price over soybean oil. Nevertheless,

substitutes (e.g., soybean oil, sunflower oil, combination of oils and/or processes, etc.) are readily

available for most end use applications meaning global canola oil prices cannot pull too far away from

other vegetable oil pricing at the risk of being substituted. There are applications and varieties with

distinct quality characteristics that will command a significant premium because of the relative inability

of the end user to reasonably substitute, but these circumstances are few and the vast majority of global

canola production and usage does not fit this category. In the case of high oleic canola oil, both soybean

and sunflower have high oleic options which will temper premium pricing for this product.

Thirdly, the value chain as a whole continues to agree that bulk seed volume and production targets are

still the most relevant metrics to drive value for all participants and not other factors (e.g., increasing

quality characteristics, increasing oil content, etc.). In other words, the top line goal is still volume as a

whole, of which oil content is only one factor.

Fourthly, all segments of the value chain need to be aware of the impact of their actions on the broader

industry. Considering the extraordinary collaboration to date in the sector and the need for all

participants to be reasonably compensated for their part, strategies that are ‘win-lose’ between

segments are bound to be very contentious with the possibility of significant unintended repercussions.

This is not to say that fighting for one’s own is not proper, but rather that one needs to be mindful that

the market will naturally aim to redistribute profits in a balanced manner along the value chain. After

all, if significantly higher profits are available in one segment than another, one should expect to see

much more vertical integration or cross segment investing in response.

Substitutes and the International Vegetable Oil Market

In reviewing the possible benefits or drawbacks of a component pricing system it is worthwhile to

consider in slightly more detail the nature of the international vegetable oil market and the

substitutability among oil options.

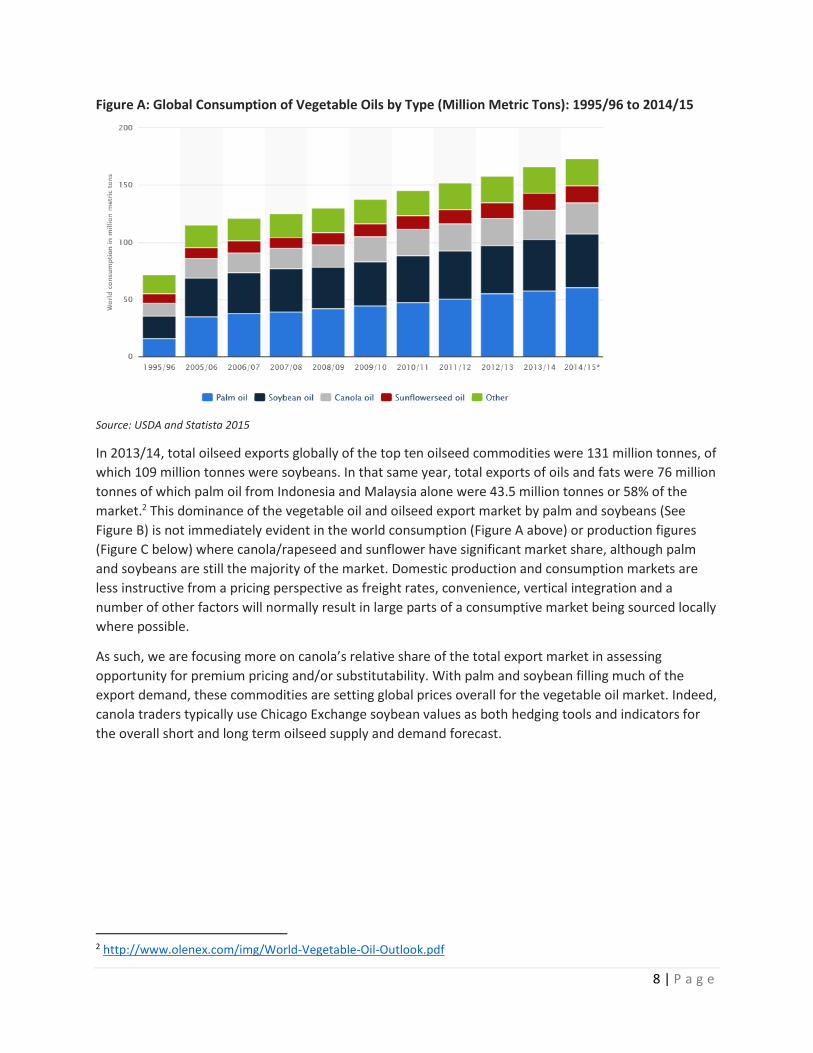

Consumption of canola oil globally is quite common and represents a significant amount of the global

disappearance seen in Figure A below. That being said, this chart also demonstrates that the majority of

growth in global consumption is happening in palm and soybean oil, although the past two years has

seen a bump in canola.

8 | P a g e

Figure A: Global Consumption of Vegetable Oils by Type (Million Metric Tons): 1995/96 to 2014/15

Source: USDA and Statista 2015

In 2013/14, total oilseed exports globally of the top ten oilseed commodities were 131 million tonnes, of

which 109 million tonnes were soybeans. In that same year, total exports of oils and fats were 76 million

tonnes of which palm oil from Indonesia and Malaysia alone were 43.5 million tonnes or 58% of the

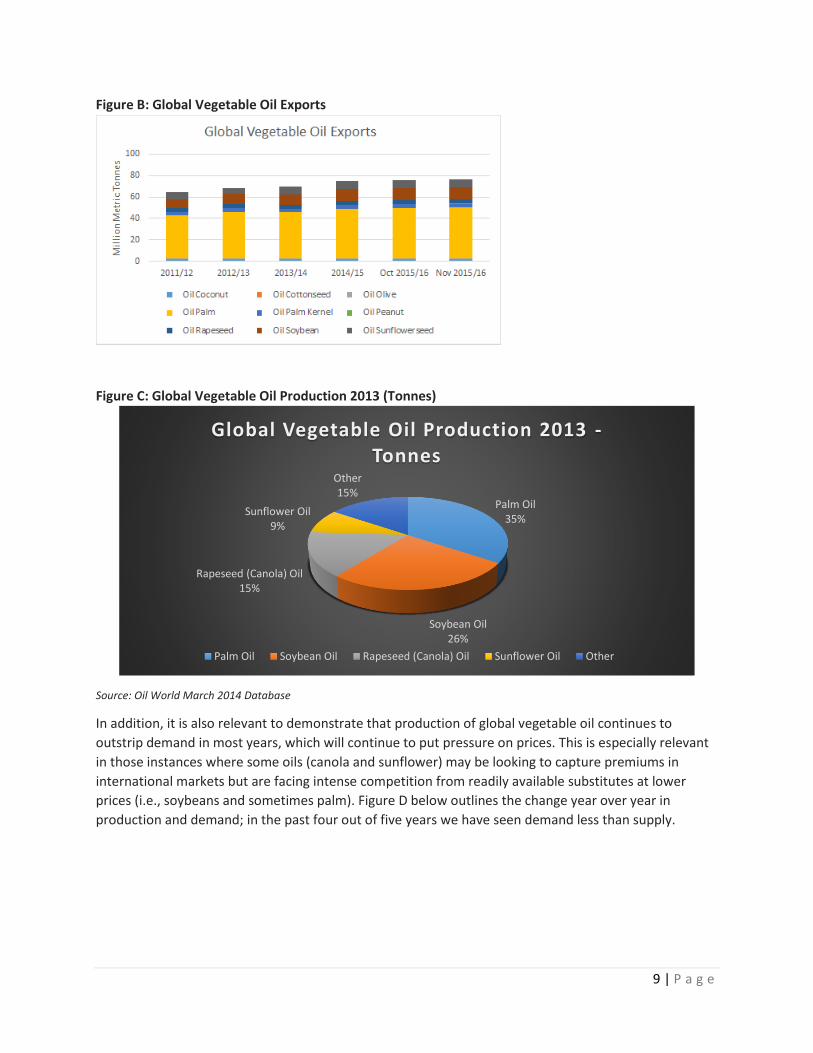

market.2 This dominance of the vegetable oil and oilseed export market by palm and soybeans (See

Figure B) is not immediately evident in the world consumption (Figure A above) or production figures

(Figure C below) where canola/rapeseed and sunflower have significant market share, although palm

and soybeans are still the majority of the market. Domestic production and consumption markets are

less instructive from a pricing perspective as freight rates, convenience, vertical integration and a

number of other factors will normally result in large parts of a consumptive market being sourced locally

where possible.

As such, we are focusing more on canola’s relative share of the total export market in assessing

opportunity for premium pricing and/or substitutability. With palm and soybean filling much of the

export demand, these commodities are setting global prices overall for the vegetable oil market. Indeed,

canola traders typically use Chicago Exchange soybean values as both hedging tools and indicators for

the overall short and long term oilseed supply and demand forecast.

2 http://www.olenex.com/img/World-Vegetable-Oil-Outlook.pdf

9 | P a g e

Figure B: Global Vegetable Oil Exports

Figure C: Global Vegetable Oil Production 2013 (Tonnes)

Source: Oil World March 2014 Database

In addition, it is also relevant to demonstrate that production of global vegetable oil continues to

outstrip demand in most years, which will continue to put pressure on prices. This is especially relevant

in those instances where some oils (canola and sunflower) may be looking to capture premiums in

international markets but are facing intense competition from readily available substitutes at lower

prices (i.e., soybeans and sometimes palm). Figure D below outlines the change year over year in

production and demand; in the past four out of five years we have seen demand less than supply.

Palm Oil35%

Soybean Oil26%

Rapeseed (Canola) Oil15%

Sunflower Oil9%

Other15%

Global Vegetable Oil Production 2013 -Tonnes

Palm Oil Soybean Oil Rapeseed (Canola) Oil Sunflower Oil Other

10 | P a g e

Figure D: 17 Oils & Fats: Global Production and Demand; Change From Year Ago (Million Tonnes)

Source: http://www.olenex.com/img/World-Vegetable-Oil-Outlook.pdf

Importers are also continuously looking at the natural competition between producing regions with

price sensitive customers often sourcing from numerous origins driving further price competition

between them. This analysis would automatically factor in concepts such as freight, oil content,

moisture and dockage among other criteria. This is certainly the case for major customers like China and

Mexico who routinely buy from other origins, but can also include less price sensitive import markets

like Japan. Furthermore, in price sensitive import markets customers are keeping a keen eye on the

spread between canola seed and/or oil pricing and that of substitute products and will move quickly to

alternative oils if the gap moves beyond its normal range. This means that Canadian exports must

continuously adjust its pricing to stay competitive with other origins and are unlikely to retain any

premium for oil content where other origins are able to deliver a similar range in oil content. Overall

export/import supply and demand factors are much more likely to drive pricing than oil content in this

current market structure.

Another factor worth considering in the analysis on the potential for premiums in the export market is

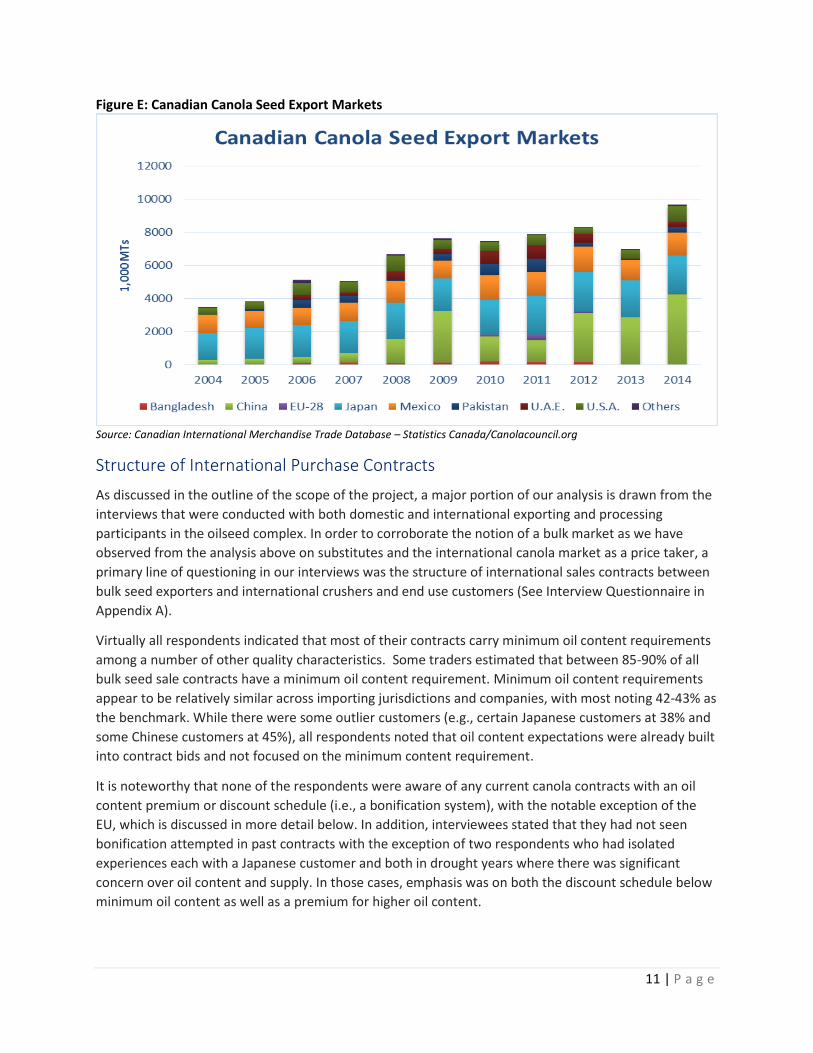

the relative concentration of demand for canola oil among a small number of markets. Unlike wheat, the

lion’s share of canola seed and oil exports are focused on the 5 markets of Canada, the United States,

Japan, China and Mexico. As can be seen in Figure E below, other significant markets include UAE,

Pakistan, Bangladesh and the EU, with demand for canola imports dropping off dramatically to countries

beyond these key market. In contrast, various wheat classes, varieties and qualities are sold by Canada

alone to over 70 countries, many with specific end uses in mind and most recognizing the value of the

high quality wheat grown in Canada in relation to several flagship wheat classes such as CWRS and

CWAD. Concentration of market (both supply and demand), by its nature, tends to be less inelastic from

a pricing perspective than a more diversified market. This means that year over year transactions and

relationships are likely to be less volatile in canola than in a commodity like wheat, including with

respect to price premium or discount scenarios.

11 | P a g e

Figure E: Canadian Canola Seed Export Markets

Source: Canadian International Merchandise Trade Database – Statistics Canada/Canolacouncil.org

Structure of International Purchase Contracts

As discussed in the outline of the scope of the project, a major portion of our analysis is drawn from the

interviews that were conducted with both domestic and international exporting and processing

participants in the oilseed complex. In order to corroborate the notion of a bulk market as we have

observed from the analysis above on substitutes and the international canola market as a price taker, a

primary line of questioning in our interviews was the structure of international sales contracts between

bulk seed exporters and international crushers and end use customers (See Interview Questionnaire in

Appendix A).

Virtually all respondents indicated that most of their contracts carry minimum oil content requirements

among a number of other quality characteristics. Some traders estimated that between 85-90% of all

bulk seed sale contracts have a minimum oil content requirement. Minimum oil content requirements

appear to be relatively similar across importing jurisdictions and companies, with most noting 42-43% as

the benchmark. While there were some outlier customers (e.g., certain Japanese customers at 38% and

some Chinese customers at 45%), all respondents noted that oil content expectations were already built

into contract bids and not focused on the minimum content requirement.

It is noteworthy that none of the respondents were aware of any current canola contracts with an oil

content premium or discount schedule (i.e., a bonification system), with the notable exception of the

EU, which is discussed in more detail below. In addition, interviewees stated that they had not seen

bonification attempted in past contracts with the exception of two respondents who had isolated

experiences each with a Japanese customer and both in drought years where there was significant

concern over oil content and supply. In those cases, emphasis was on both the discount schedule below

minimum oil content as well as a premium for higher oil content.

12 | P a g e

All of this points to the international canola seed market demonstrating the characteristics of a bulk

commodity market with relatively few opportunities for differentiated or premium product categories

for bulk seed exports or domestic use. This is in direct contrast to the wheat market which is a highly

differentiated marketplace and numerous opportunities to extract further value from end use

customers with the segregation of various wheat classes, varieties and qualities within them

demonstrating specific functional characteristics and end use customer willingness to pay for them3. In

other words, canola seed from an end use perspective is fairly homogenous by comparison to wheat

where value chain participants are paying for components in a more direct fashion.

We have made the argument that canola is an international price taker with direct substitutes that keep

its price within a typical spread of other oil options and that canola is a relatively undifferentiated (i.e.,

bulk) commodity. We have also highlighted that international purchase contracts do not reflect any

opportunity for a premium schedule for high oil content in and of itself. Therefore, one must then look

at the possible implications for the redistribution of current values in the supply chain if a component

pricing system were implemented in Western Canada.

Structure of Crushing Industry

Canada currently has 14 crushing plants with 11 located in Western Canada. Combined they have the

capacity to crush 10 million tonnes of canola seed per year. In 2014/15, Canada crushed 7.3 million

tonnes of a total canola production of 15.5 million tonnes (See Figure F below) or 47% of total

production. As we have already described, local processing demand almost always represents the

highest price opportunity for producers given the captive nature of crushing facility supply to the

immediate draw area and the relative expense of overland freight costs to supply from outside of that

draw area. Several interviewees noted that crusher bids typically outpace elevator bids, with one

commentator indicating this occurs 8 years out of 10. All crusher respondents agreed that oil content

was a major component of value to crushers in their profitability. When asked what each percent of oil

content above the average meant to them given sunk costs of the crush operation, all indicated this was

heavily dependent on the crush margin and that the opportunity fluctuated significantly. Respondents

noted that the value of oil content, as one factor among many, was shown in the cash basis they were

paying local producers. While they agreed this was not completely transparent, it was from their

perspective an important element in the cash price. Several interviewees said that differences in cash

bids between competitors in a given region can often fluctuate between $10-30/tonne. This is reflective

of different companies having unique margin structures, efficiencies, sales, contract requirements, etc.

The fact that many of these elements are not transparent to some degree drives competition. Where

elements of cost are publicized (e.g., tariff fees for certain activities), the bid range for that service

between competitors tends to narrow significantly. Many interviewees were of the view that this would

happen in the case of published premium/discount schedules, and many of the international

respondents noted that bid ranges in bonification systems were narrower than other regions. In our

view a fully transparent oil premium/discount schedule would result in a narrowing of the competitive

bid range which we argue is not in producers’ favour.

3 http://www.agr.gc.ca/eng/industry-markets-and-trade/statistics-and-market-information/by-product-sector/crops/crops-market-information-canadian-industry/market-outlook-report/wheat-sector-profile-part-one-overview-november-2010/?id=1378843495280

13 | P a g e

Figure F: Canola Crushing Volumes in Canada 2003/04-2014/15

Source: http://www.canolacouncil.org/markets-stats/statistics/historic-canola-crush/

A number of the crush plants in Canada are not located in high oil content producing areas. This does, in

part, indicate that oil content while important is not a dominant driver for crush profitability or location

of facilities. Some interviewees raised the issue of certain companies only having one or a small number

of facilities in the country, and as a result, monitoring for oil content was moot from their perspective as

freight rates alone were an ultimate disincentive for them to procure over long distances. This leads to

the belief and practice of “what we get at the plant is what is in the area” as opposed to a proactive plan

to monitor and secure high oil content product. We would argue that this alone is strong evidence that

high oil content would not be a major driver for further producer value. If it was we should have seen in

the market by now a significant increase in grain buying by crushers outside their normal draw area if it

was lucrative to them. Saskatchewan producers in several ways are in a fortunate position since 4 of the

largest crush plants are located in the province in the major canola growing region (5 if you count the

border facility at Lloydminster). These facilities are massive demand draws willing to pay higher values

typically over other competitors, and reflecting the higher oil content of Northern Saskatchewan

production in their bids.

Structure of Grain Elevator Business

Western Canada has an extensive grain elevator network located predominantly on major railway lines.

This network aims to move as much product as possible through each of these facilities, with many

operational improvements being geared towards efficient loading and unloading of product to remove

costs from the system. This drive for efficiency is the hallmark of a bulk commodity enterprise, where

companies want as little cost as possible when moving the most grain possible through their assets. This

also implies that grain elevator companies must also be price competitive in the countryside in order to

purchase from producers. In this way, canola has a distinct advantage over wheat in that grain elevators

do not require extra storage and elevation assets in order to handle multiple varieties and qualities like

with wheat. These efficiencies do translate back to producers, as most elevators would much prefer to

handle canola over wheat given the additional costs and management required for the latter.

Previously we discussed the importance of capturing local production for a crushing facility. While there

is typically a stronger demand signal from crushers, this is in part due to the significant competition

coming from local grain elevators who also need to acquire volume. This may be particularly true of high

oil content areas given elevator blending strategies at port in order to meet minimum oil content

requirements in contracts. In short, grain companies must procure a sizeable amount of high oil content

canola in order to meet, for example, contracts with high oil content requirements in the 44-45% range.

This means that grain elevators cannot ignore oil content in their cash bids. Indeed, interviewees noted

14 | P a g e

that they would move into high oil content areas and “pay up” in their bids in order to secure this

product much like a local crusher would. This allows them to ultimately meet contracts with high

percentage requirements, as well as blend with lower oil content product from other regions in order to

hit the minimum criteria for those contracts with average percentage oil content (e.g., 42-43%). The

difference in basis levels across Western Canada are therefore already reflective of oil content, among

other factors.

As a result, the question of “am I getting compensated for the oil content of my product” appears to be

too narrow given the many factors at play in pricing. From a producer perspective, the more important

question is “do I have enough competition for my canola in my growing region to ensure I am getting

the full value for my product”. Some interviewees noted that the vast majority (certainly 95%+) of

producers would have at least 3 or 4 bids to consider in their growing area, with numerous places having

as many as 7 or 8 bids. The more bids available to an individual producer, the more likely that the

market will efficiently arbitrage any potential value for increased oil content in a producer’s canola.

Much like crushing facilities, elevators are also fixed assets with a relatively inflexible procurement

radius given the margin dampening effects of trucking freight for longer distance procurement. While

some companies have an elevator footprint that covers 150km draw radius’ across all Western Canadian

producing regions, that does not imply that a company does not require all of its facilities to move as

much volume as possible. That is to say, companies cannot afford to have assets that are not turning,

and as such, will acquire the crop produced in an elevator draw region to the best of its ability. As one

respondent indicated, “we want to move the whole crop and we will take the good along with the bad.”

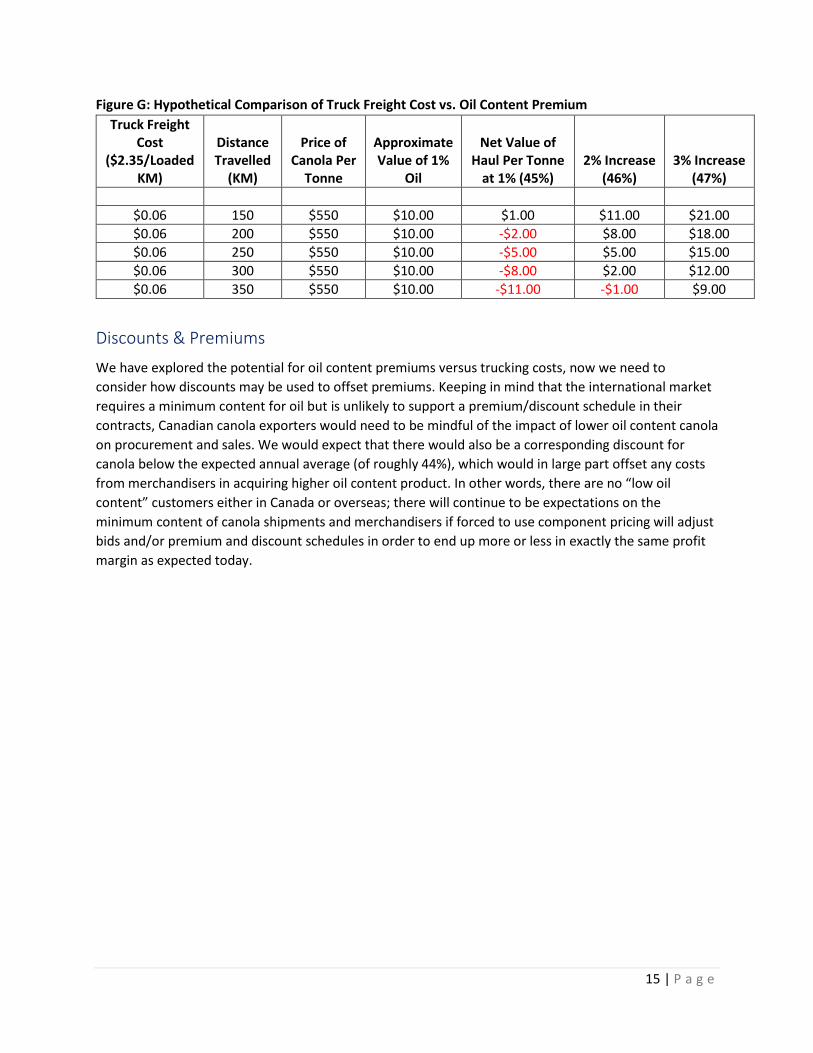

Pricing Factors – Freight vs. Oil Content Premium

The idea that freight rates discourage longer distance buying can be seen in the current average truck

freight costs versus a potential premium for oil content. If we were to use current truck freight rates of

approximately $0.06 per loaded kilometer, a 300 km haul (double a draw distance) would cost on

average $18/tonne. By contrast a 1% bump in canola oil content over 44% at $550/tonne for canola

seed (based on average per tonne value in 2014/15) with 80% of the value on average being in the oil

content, means there is roughly a $10/tonne premium for the additional percentage. Even if we were to

double the percentage (i.e., $20/tonne), it would still not be attractive to compensate a grain buyer to

take the extraordinary action of procuring well beyond the natural draw area of a facility. Figure G

below sets out a table contrasting different distances and values. This simple calculation does not take

into account all of the other potential costs that would need to be borne to procure the seed (samples,

tests, extra storage space, extra time to handle, etc.), not to mention longer term costs such as

additional wear and tear on roads, among others. These would also be figured into estimates in some

fashion, meaning that the hypothetical values for each percent increase net payback are very aggressive

in this table. To arrive at a more realistic number, it would need to be adjusted downwards to account

for these other costs that would be charged as an additional tariff and/or reflected in a lower basis

before a premium is added on top.

15 | P a g e

Figure G: Hypothetical Comparison of Truck Freight Cost vs. Oil Content Premium

Truck Freight Cost

($2.35/Loaded KM)

Distance Travelled

(KM)

Price of Canola Per

Tonne

Approximate Value of 1%

Oil

Net Value of Haul Per Tonne

at 1% (45%) 2% Increase

(46%) 3% Increase

(47%)

$0.06 150 $550 $10.00 $1.00 $11.00 $21.00

$0.06 200 $550 $10.00 -$2.00 $8.00 $18.00

$0.06 250 $550 $10.00 -$5.00 $5.00 $15.00

$0.06 300 $550 $10.00 -$8.00 $2.00 $12.00

$0.06 350 $550 $10.00 -$11.00 -$1.00 $9.00

Discounts & Premiums

We have explored the potential for oil content premiums versus trucking costs, now we need to

consider how discounts may be used to offset premiums. Keeping in mind that the international market

requires a minimum content for oil but is unlikely to support a premium/discount schedule in their

contracts, Canadian canola exporters would need to be mindful of the impact of lower oil content canola

on procurement and sales. We would expect that there would also be a corresponding discount for

canola below the expected annual average (of roughly 44%), which would in large part offset any costs

from merchandisers in acquiring higher oil content product. In other words, there are no “low oil

content” customers either in Canada or overseas; there will continue to be expectations on the

minimum content of canola shipments and merchandisers if forced to use component pricing will adjust

bids and/or premium and discount schedules in order to end up more or less in exactly the same profit

margin as expected today.

16 | P a g e

Section 2: Production Factors

Overview

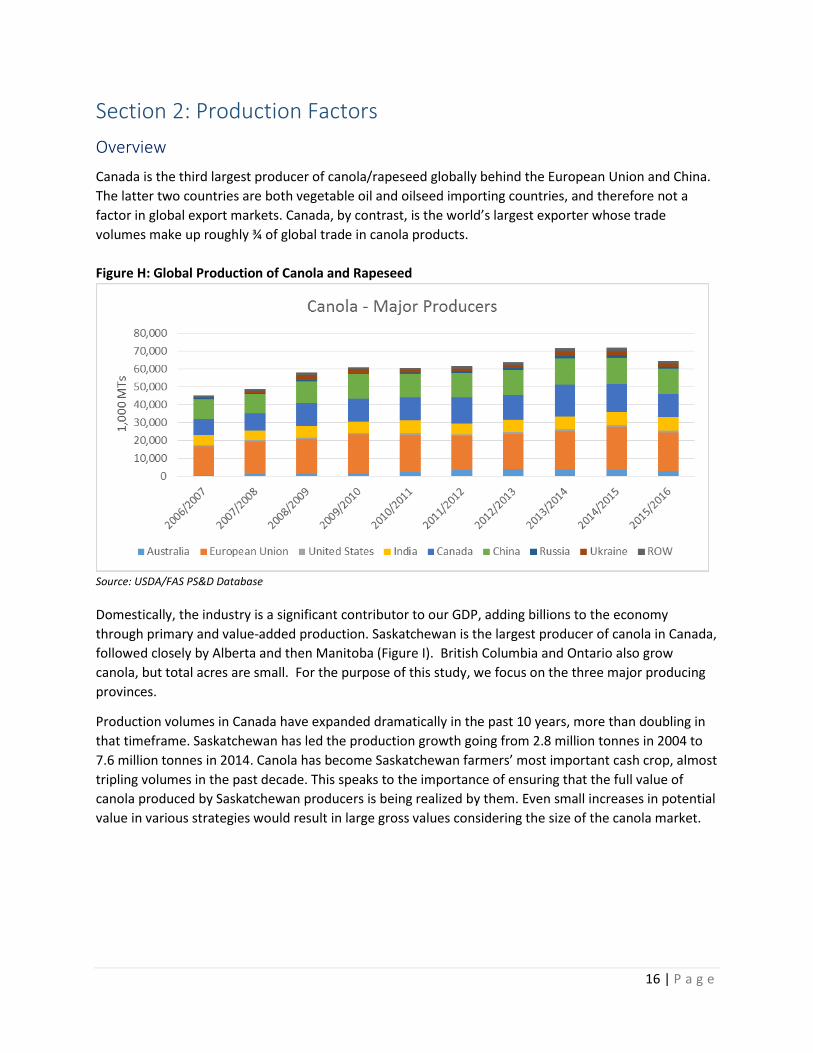

Canada is the third largest producer of canola/rapeseed globally behind the European Union and China.

The latter two countries are both vegetable oil and oilseed importing countries, and therefore not a

factor in global export markets. Canada, by contrast, is the world’s largest exporter whose trade

volumes make up roughly ¾ of global trade in canola products.

Figure H: Global Production of Canola and Rapeseed

Source: USDA/FAS PS&D Database

Domestically, the industry is a significant contributor to our GDP, adding billions to the economy

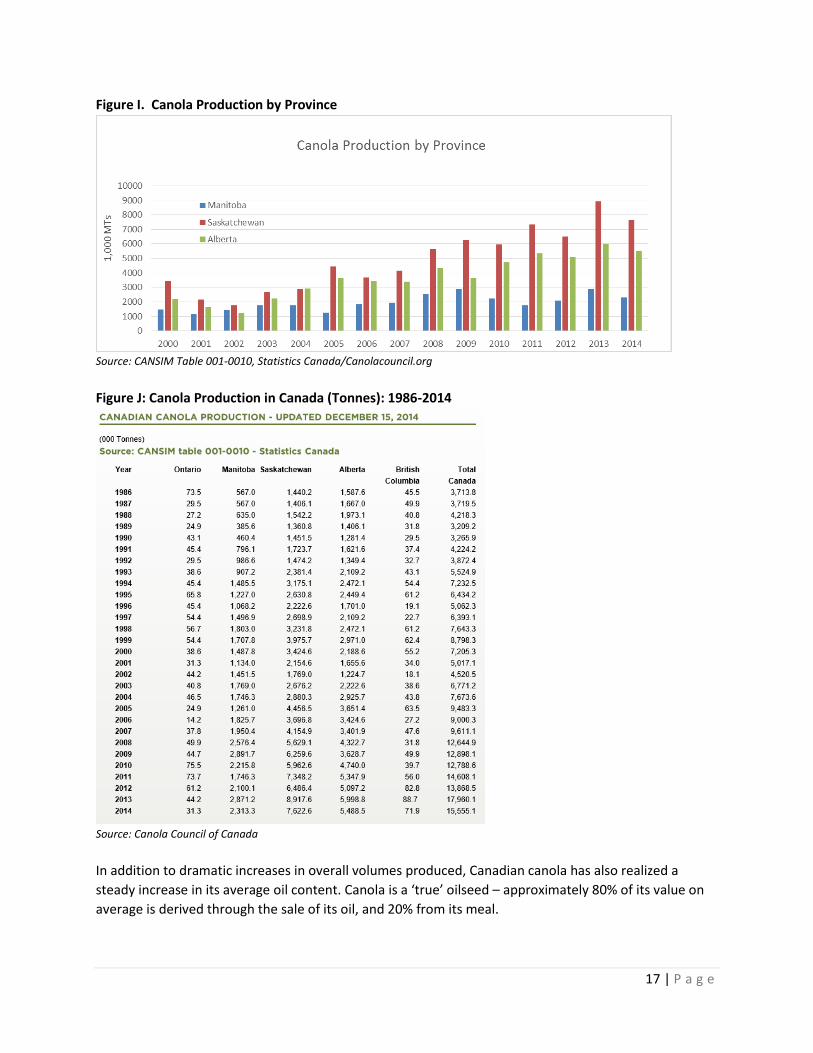

through primary and value-added production. Saskatchewan is the largest producer of canola in Canada,

followed closely by Alberta and then Manitoba (Figure I). British Columbia and Ontario also grow

canola, but total acres are small. For the purpose of this study, we focus on the three major producing

provinces.

Production volumes in Canada have expanded dramatically in the past 10 years, more than doubling in

that timeframe. Saskatchewan has led the production growth going from 2.8 million tonnes in 2004 to

7.6 million tonnes in 2014. Canola has become Saskatchewan farmers’ most important cash crop, almost

tripling volumes in the past decade. This speaks to the importance of ensuring that the full value of

canola produced by Saskatchewan producers is being realized by them. Even small increases in potential

value in various strategies would result in large gross values considering the size of the canola market.

17 | P a g e

Figure I. Canola Production by Province

Source: CANSIM Table 001-0010, Statistics Canada/Canolacouncil.org

Figure J: Canola Production in Canada (Tonnes): 1986-2014

Source: Canola Council of Canada

In addition to dramatic increases in overall volumes produced, Canadian canola has also realized a

steady increase in its average oil content. Canola is a ‘true’ oilseed – approximately 80% of its value on

average is derived through the sale of its oil, and 20% from its meal.

18 | P a g e

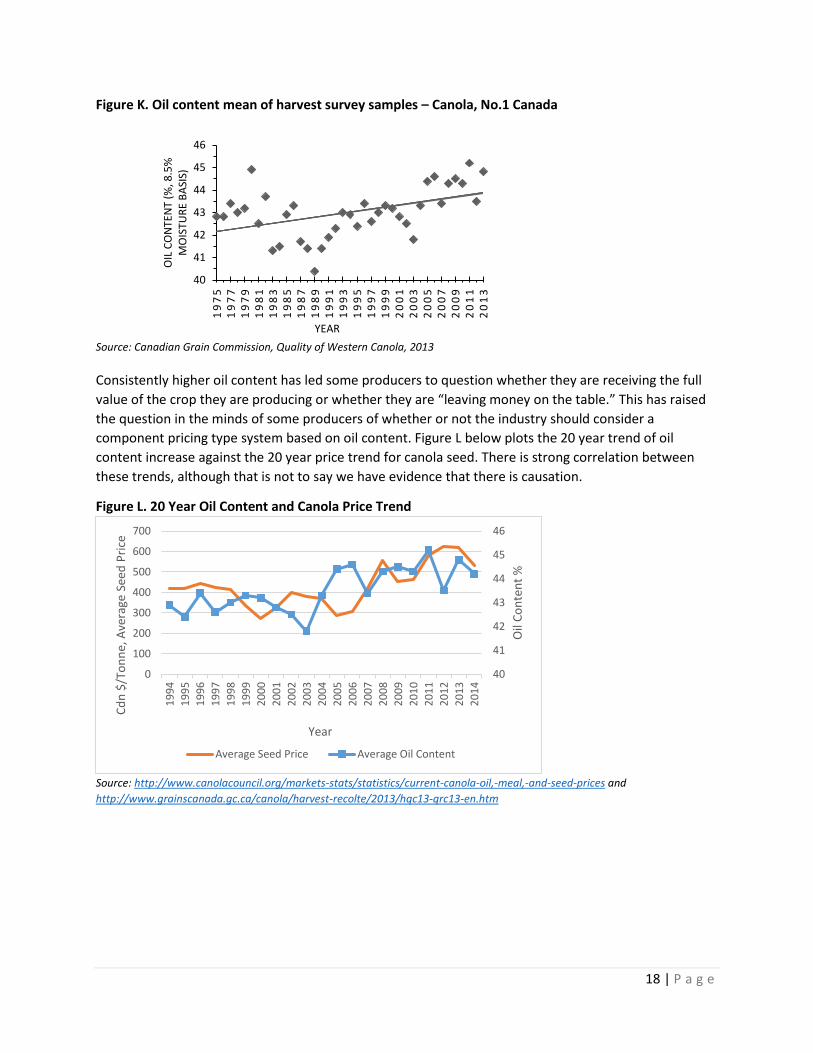

Figure K. Oil content mean of harvest survey samples – Canola, No.1 Canada

Source: Canadian Grain Commission, Quality of Western Canola, 2013

Consistently higher oil content has led some producers to question whether they are receiving the full

value of the crop they are producing or whether they are “leaving money on the table.” This has raised

the question in the minds of some producers of whether or not the industry should consider a

component pricing type system based on oil content. Figure L below plots the 20 year trend of oil

content increase against the 20 year price trend for canola seed. There is strong correlation between

these trends, although that is not to say we have evidence that there is causation.

Figure L. 20 Year Oil Content and Canola Price Trend

Source: http://www.canolacouncil.org/markets-stats/statistics/current-canola-oil,-meal,-and-seed-prices and

http://www.grainscanada.gc.ca/canola/harvest-recolte/2013/hqc13-qrc13-en.htm

40

41

42

43

44

45

46

19

75

19

77

19

79

19

81

19

83

19

85

19

87

19

89

19

91

19

93

19

95

19

97

19

99

20

01

20

03

20

05

20

07

20

09

20

11

20

13

OIL

CO

NTE

NT

(%, 8

.5%

M

OIS

TUR

E B

ASI

S)

YEAR

40

41

42

43

44

45

46

0

100

200

300

400

500

600

700

19

94

19

95

19

96

19

97

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

Oil

Co

nte

nt

%

Cd

n $

/To

nn

e, A

vera

ge S

eed

Pri

ce

Year

Average Seed Price Average Oil Content

19 | P a g e

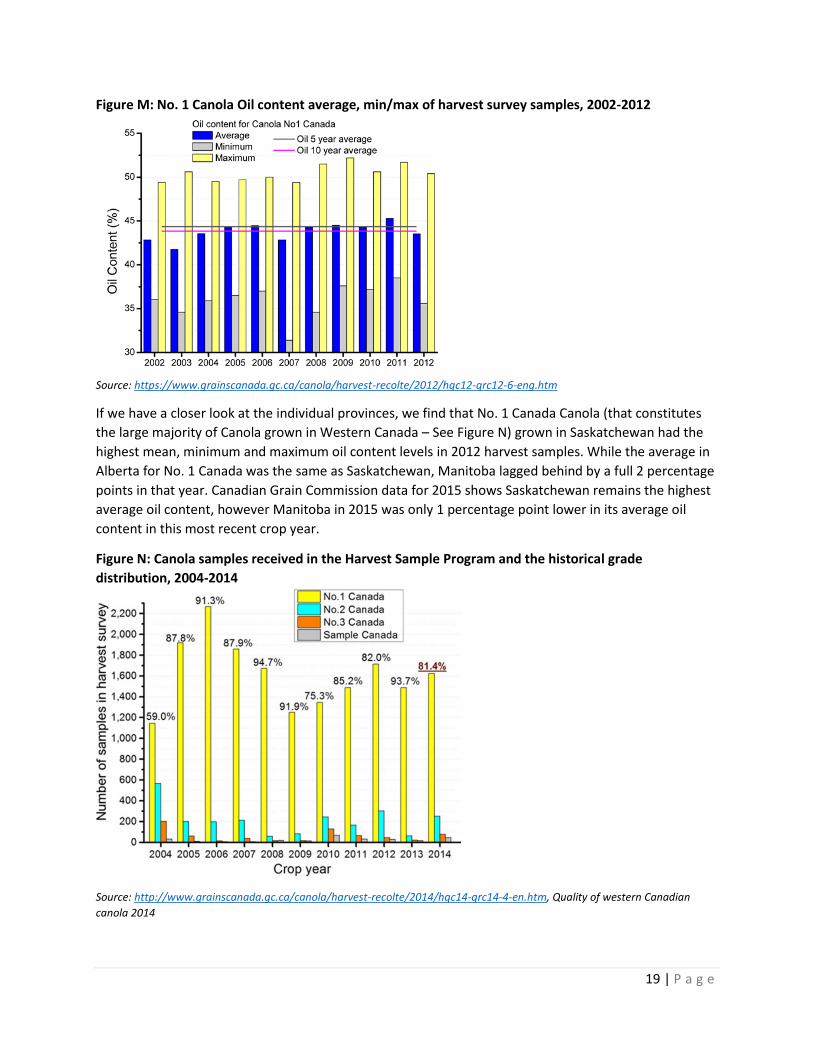

Figure M: No. 1 Canola Oil content average, min/max of harvest survey samples, 2002-2012

Source: https://www.grainscanada.gc.ca/canola/harvest-recolte/2012/hqc12-qrc12-6-eng.htm

If we have a closer look at the individual provinces, we find that No. 1 Canada Canola (that constitutes

the large majority of Canola grown in Western Canada – See Figure N) grown in Saskatchewan had the

highest mean, minimum and maximum oil content levels in 2012 harvest samples. While the average in

Alberta for No. 1 Canada was the same as Saskatchewan, Manitoba lagged behind by a full 2 percentage

points in that year. Canadian Grain Commission data for 2015 shows Saskatchewan remains the highest

average oil content, however Manitoba in 2015 was only 1 percentage point lower in its average oil

content in this most recent crop year.

Figure N: Canola samples received in the Harvest Sample Program and the historical grade

distribution, 2004-2014

Source: http://www.grainscanada.gc.ca/canola/harvest-recolte/2014/hqc14-qrc14-4-en.htm, Quality of western Canadian

canola 2014

20 | P a g e

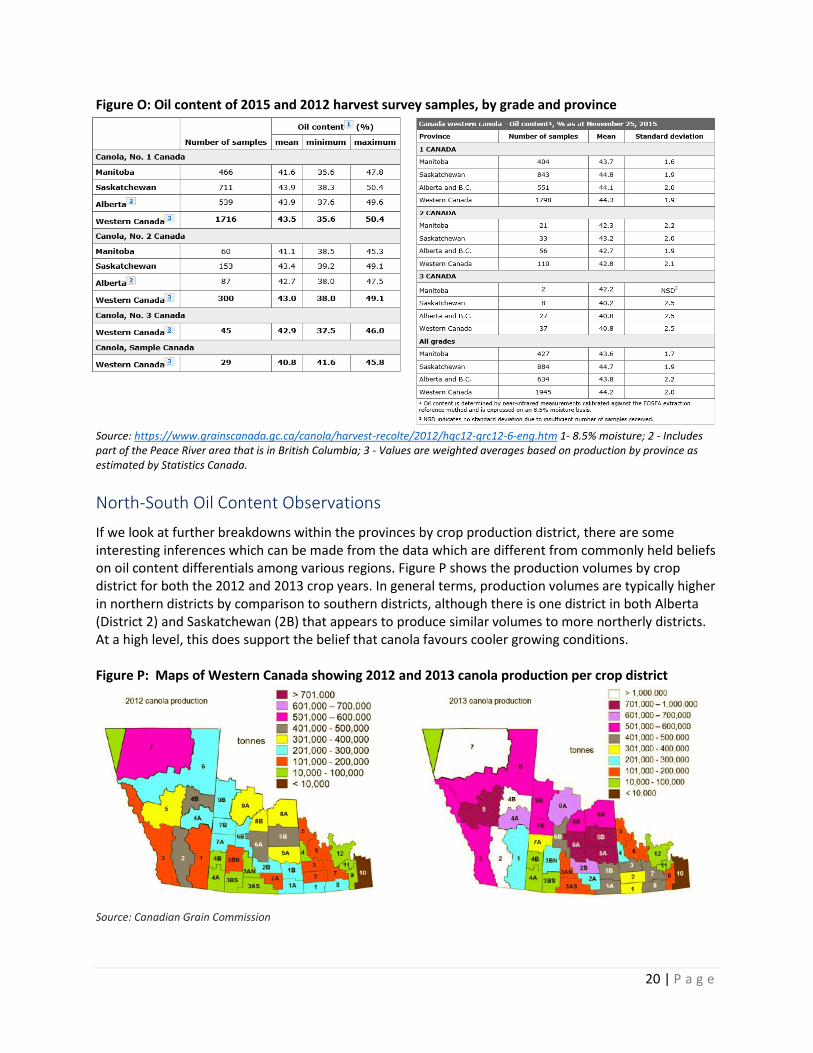

Figure O: Oil content of 2015 and 2012 harvest survey samples, by grade and province

Source: https://www.grainscanada.gc.ca/canola/harvest-recolte/2012/hqc12-qrc12-6-eng.htm 1- 8.5% moisture; 2 - Includes part of the Peace River area that is in British Columbia; 3 - Values are weighted averages based on production by province as estimated by Statistics Canada.

North-South Oil Content Observations

If we look at further breakdowns within the provinces by crop production district, there are some interesting inferences which can be made from the data which are different from commonly held beliefs on oil content differentials among various regions. Figure P shows the production volumes by crop district for both the 2012 and 2013 crop years. In general terms, production volumes are typically higher in northern districts by comparison to southern districts, although there is one district in both Alberta (District 2) and Saskatchewan (2B) that appears to produce similar volumes to more northerly districts. At a high level, this does support the belief that canola favours cooler growing conditions. Figure P: Maps of Western Canada showing 2012 and 2013 canola production per crop district

Source: Canadian Grain Commission

21 | P a g e

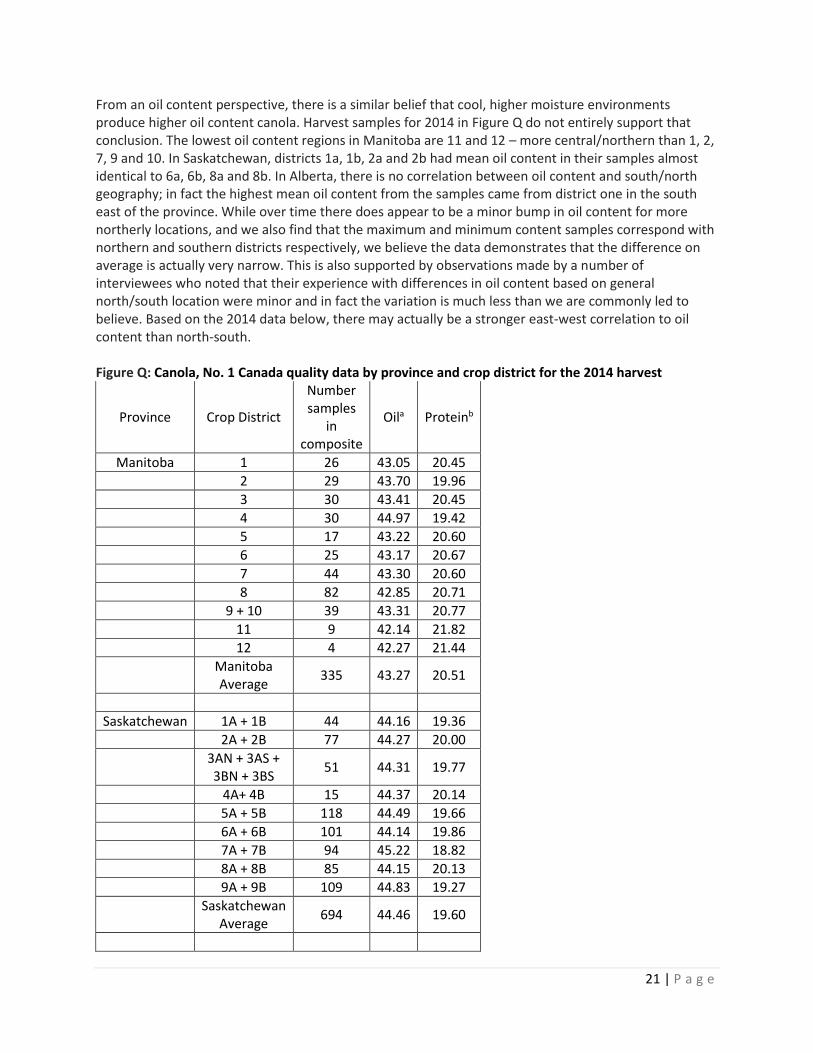

From an oil content perspective, there is a similar belief that cool, higher moisture environments produce higher oil content canola. Harvest samples for 2014 in Figure Q do not entirely support that conclusion. The lowest oil content regions in Manitoba are 11 and 12 – more central/northern than 1, 2, 7, 9 and 10. In Saskatchewan, districts 1a, 1b, 2a and 2b had mean oil content in their samples almost identical to 6a, 6b, 8a and 8b. In Alberta, there is no correlation between oil content and south/north geography; in fact the highest mean oil content from the samples came from district one in the south east of the province. While over time there does appear to be a minor bump in oil content for more northerly locations, and we also find that the maximum and minimum content samples correspond with northern and southern districts respectively, we believe the data demonstrates that the difference on average is actually very narrow. This is also supported by observations made by a number of interviewees who noted that their experience with differences in oil content based on general north/south location were minor and in fact the variation is much less than we are commonly led to believe. Based on the 2014 data below, there may actually be a stronger east-west correlation to oil content than north-south. Figure Q: Canola, No. 1 Canada quality data by province and crop district for the 2014 harvest

Province Crop District

Number samples

in composite

Oila Proteinb

Manitoba 1 26 43.05 20.45

2 29 43.70 19.96

3 30 43.41 20.45

4 30 44.97 19.42

5 17 43.22 20.60

6 25 43.17 20.67

7 44 43.30 20.60

8 82 42.85 20.71

9 + 10 39 43.31 20.77

11 9 42.14 21.82

12 4 42.27 21.44

Manitoba Average

335 43.27 20.51

Saskatchewan 1A + 1B 44 44.16 19.36

2A + 2B 77 44.27 20.00

3AN + 3AS + 3BN + 3BS

51 44.31 19.77

4A+ 4B 15 44.37 20.14

5A + 5B 118 44.49 19.66

6A + 6B 101 44.14 19.86

7A + 7B 94 45.22 18.82

8A + 8B 85 44.15 20.13

9A + 9B 109 44.83 19.27

Saskatchewan

Average 694 44.46 19.60

22 | P a g e

Alberta 1 20 44.63 20.16

2 74 44.09 20.52

3 28 43.97 20.87

4A + 4B 219 44.36 20.31

5 77 44.09 20.95

6 32 43.76 21.37

7 + Peace River B.C.

109 43.90 21.57

Alberta-Peace River Average

559 44.13 20.78

Western Canada Average

1588 44.16 20.15

a Oil content in % at 8.5% moisture b Protein content of the seed in % at 8.5% moisture, calculated with N x 6.25

Source: Canadian Grain Commission

Varieties

While we have no direct empirical data to support the following conclusion, we are of the view based on inferences from data on production volumes and oil content that more southerly districts have been significantly bolstered by the introduction of new varieties and improved agronomic practices. Many farmers have commented in the past couple of years on the stress tolerance of recent hybrid varieties that perform well in both high and extended heat and moisture scenarios. We infer this has had a similarly positive effect on oil content, where the data from 2014 above supports our view that these improvements have potentially compressed the oil content range between northern and southern districts. Several interviewees also commented on the resilience of new variety technology introduced in the past decade where they stated producer customers were able to produce strong canola crops in regions that 10 years ago Brassica Napus production would not have been considered.

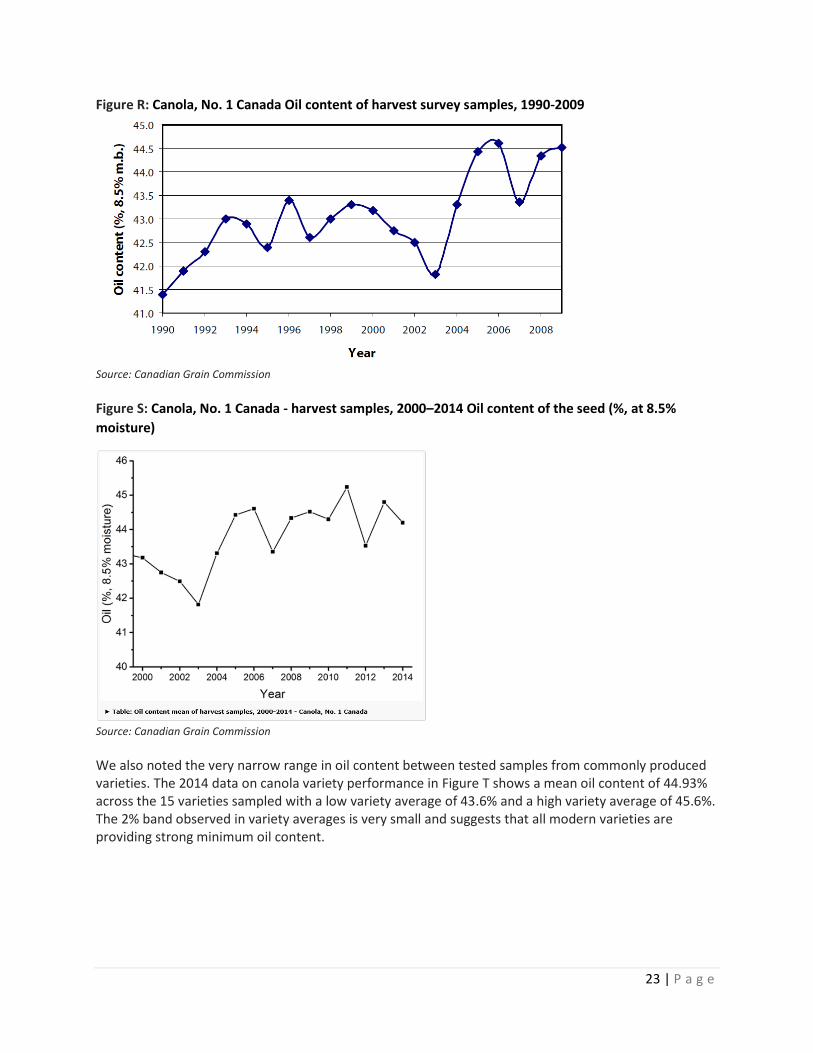

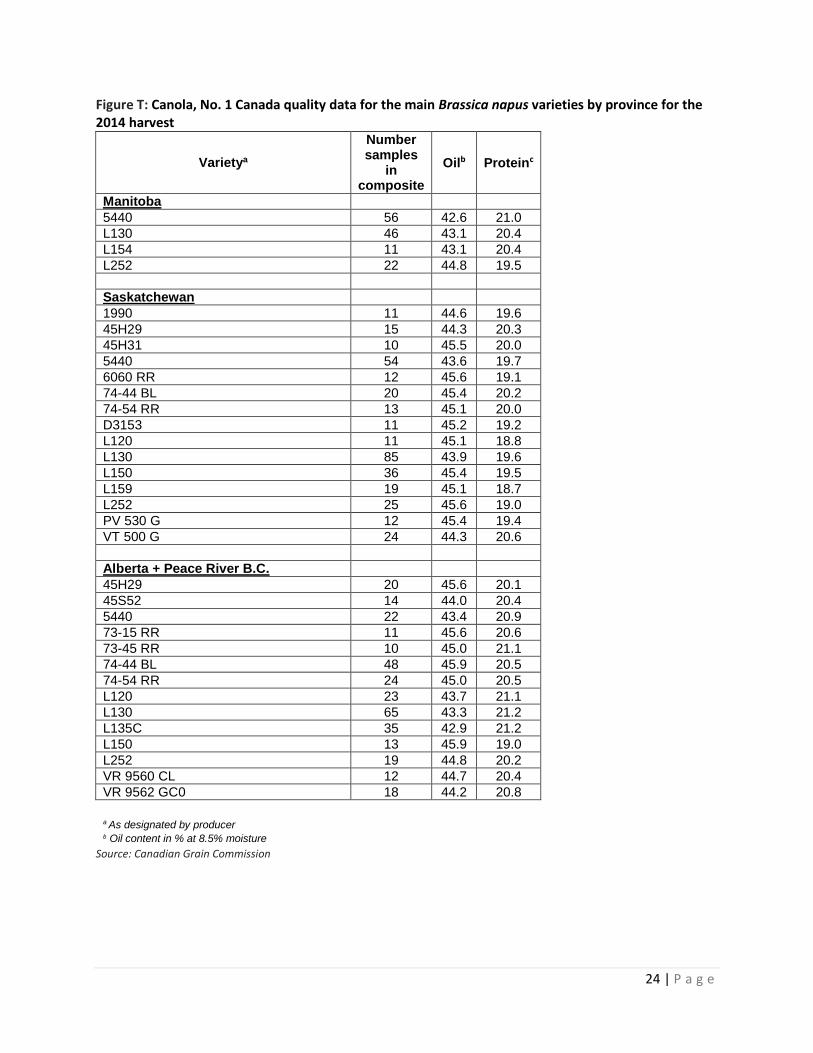

Looking back at more historical data (Figure R and S below), we see a dramatic shift in oil content from 2003/04 onwards (by comparison to 1990-2003) with more than a full percentage and a half in mean oil content gained from 2005-2009 in comparison to the prior 5 year period. The noticeable jump in oil content in a condensed timeframe coupled with steady oil content gains in future years suggests that an externality was introduced into canola production influencing this trend – new and improved varieties along with better agronomic practices.

23 | P a g e

Figure R: Canola, No. 1 Canada Oil content of harvest survey samples, 1990-2009

Source: Canadian Grain Commission

Figure S: Canola, No. 1 Canada - harvest samples, 2000–2014 Oil content of the seed (%, at 8.5%

moisture)

Source: Canadian Grain Commission

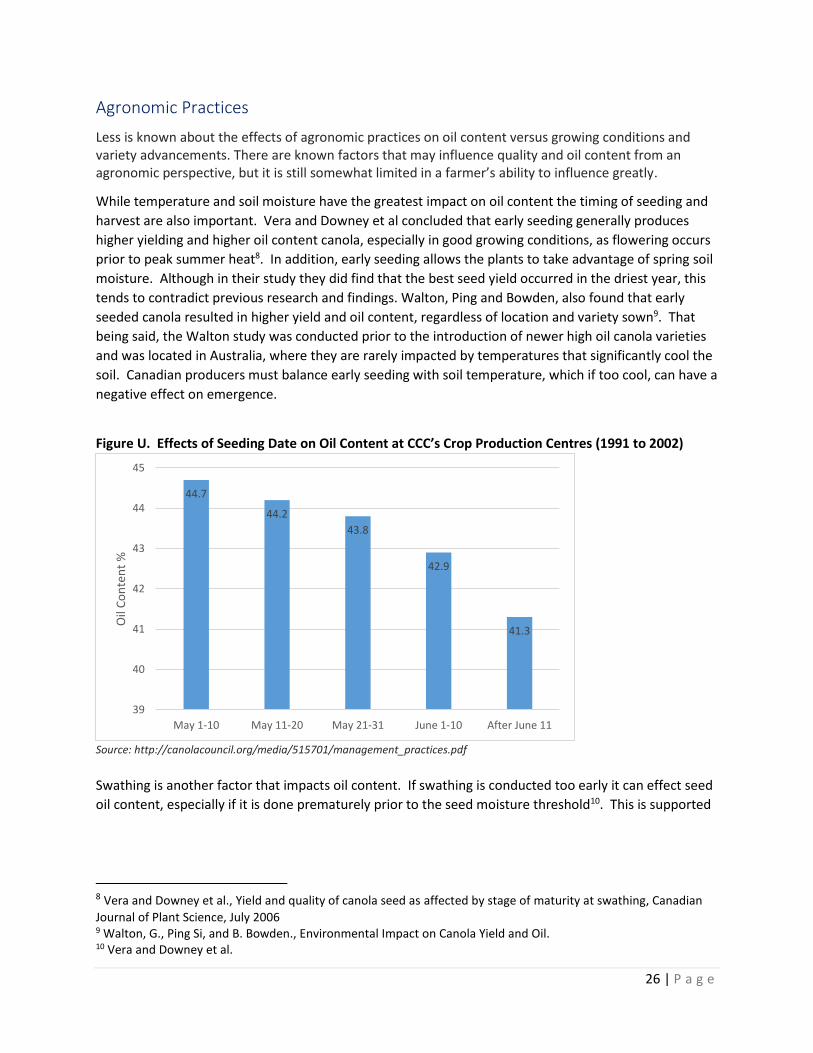

We also noted the very narrow range in oil content between tested samples from commonly produced varieties. The 2014 data on canola variety performance in Figure T shows a mean oil content of 44.93% across the 15 varieties sampled with a low variety average of 43.6% and a high variety average of 45.6%. The 2% band observed in variety averages is very small and suggests that all modern varieties are providing strong minimum oil content.

24 | P a g e

Figure T: Canola, No. 1 Canada quality data for the main Brassica napus varieties by province for the 2014 harvest

Varietya

Number samples

in composite

Oilb Proteinc

Manitoba

5440 56 42.6 21.0

L130 46 43.1 20.4

L154 11 43.1 20.4

L252 22 44.8 19.5

Saskatchewan

1990 11 44.6 19.6

45H29 15 44.3 20.3

45H31 10 45.5 20.0

5440 54 43.6 19.7

6060 RR 12 45.6 19.1

74-44 BL 20 45.4 20.2

74-54 RR 13 45.1 20.0

D3153 11 45.2 19.2

L120 11 45.1 18.8

L130 85 43.9 19.6

L150 36 45.4 19.5

L159 19 45.1 18.7

L252 25 45.6 19.0

PV 530 G 12 45.4 19.4

VT 500 G 24 44.3 20.6

Alberta + Peace River B.C.

45H29 20 45.6 20.1

45S52 14 44.0 20.4

5440 22 43.4 20.9

73-15 RR 11 45.6 20.6

73-45 RR 10 45.0 21.1

74-44 BL 48 45.9 20.5

74-54 RR 24 45.0 20.5

L120 23 43.7 21.1

L130 65 43.3 21.2

L135C 35 42.9 21.2

L150 13 45.9 19.0

L252 19 44.8 20.2

VR 9560 CL 12 44.7 20.4

VR 9562 GC0 18 44.2 20.8

a As designated by producer b Oil content in % at 8.5% moisture

Source: Canadian Grain Commission

25 | P a g e

Environment

Of the various factors discussed in this report, environmental conditions are likely to have the greatest

influence on oil content, even more so than genetics4. The two main environmental factors influencing

oil content are soil moisture and temperature. Prithchard et al studied the impact of environmental

variables on oil content and found that high rainfall and cooler temperatures allowed for a longer

maturation phase, which in turn allowed for longer oil accumulation in the seed, resulting in higher oil

content5.

Early seeding enables the plants to take advantage of spring moisture, but additional moisture following

flowering is also key. Walton, Ping and Bowden found a strong correlation between yield and oil content

and post-flowering rainfall. Their findings are similar to those of Jensen et al, who found that oil content

fell from 43.3% to 39.9% when comparing well-watered plants vs those under drought conditions6.

Walton, Ping and Bowden’s overall conclusion was that rainfall/moisture had greater impact on oil

content more so than temperature but they also found that temperature played a role.

High temperatures during development and maturation of the canola plant have also been shown to

negatively impact oil content. Sharp increases in temperature from flowering to maturity have been

shown to hasten maturity, thereby shortening the time for oil accumulation in the seed and lowering its

overall oil content7. The same study not only highlighted the impact of temperature on the overall oil

content, but also how it influenced the composition of the oil, with higher temperatures resulting in

higher linolenic acid and lower oleic acid.

Environmental stresses, especially after flowering has been shown to have a significant impact on

overall oil content. Canola producers felt this first hand in 2003 when hot, dry temperatures, including

during the both the day and night, dropped the average oil content down to 41.8%. Cooler, wetter

weather the following growing year helped improve oil content average to 43.3%. Fluctuations in

environmental factors throughout the subsequent growing years continue to influence the average oil

content.

With environmental factors being a key variable in oil content, and taking into account the general

improvement in genetics to improve higher oil content canola even under stressful environmental

conditions, we find that producers have relatively few tools to directly influence oil content. This

conclusion is yet another aspect to keep in mind as producers weigh the options on whether or not

component pricing adds value at farm gate.

4 https://www.dekalb.ca/_uploads/documents/Agronomic_Information/CanolaArchive/what_affects_canola_oil.pdf 5 Prithchard, F.M., Eagles, H.A., Norton, R.M., Salisbury, P.A., and M. Nicolas. Environmental Effects on Seed Composition of Victorian Canola. 6 Jensen, C.R., Mogensen, V. O., Mortensen, G., Fieldsend, J.K., Milford, G.F.I., Andersen, M.N. and Thage. J.H., (1996). Seed glucosinolate, oil and protein contents of field grown rape (Brassica napus) affected by soil drying and evaporative demand. Field Crop Research. 47, 93-105 7 Fayyaz-ul-Hassan, Hakoomat Ali, Mumtaz Akhtar Cheema, and Abdul Manaf. Effects of Environmental variation on canola content and fatty acid composition of canola cultivars.

26 | P a g e

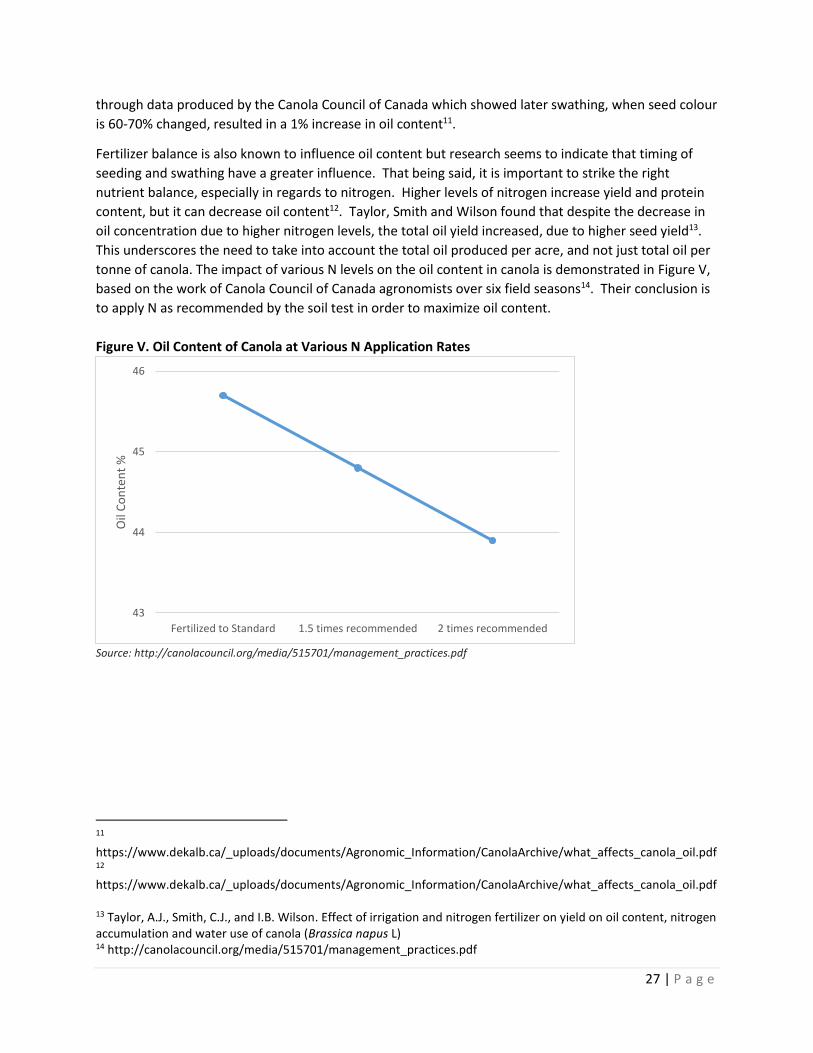

Agronomic Practices

Less is known about the effects of agronomic practices on oil content versus growing conditions and variety advancements. There are known factors that may influence quality and oil content from an agronomic perspective, but it is still somewhat limited in a farmer’s ability to influence greatly.

While temperature and soil moisture have the greatest impact on oil content the timing of seeding and

harvest are also important. Vera and Downey et al concluded that early seeding generally produces

higher yielding and higher oil content canola, especially in good growing conditions, as flowering occurs

prior to peak summer heat8. In addition, early seeding allows the plants to take advantage of spring soil

moisture. Although in their study they did find that the best seed yield occurred in the driest year, this

tends to contradict previous research and findings. Walton, Ping and Bowden, also found that early

seeded canola resulted in higher yield and oil content, regardless of location and variety sown9. That

being said, the Walton study was conducted prior to the introduction of newer high oil canola varieties

and was located in Australia, where they are rarely impacted by temperatures that significantly cool the

soil. Canadian producers must balance early seeding with soil temperature, which if too cool, can have a

negative effect on emergence.

Figure U. Effects of Seeding Date on Oil Content at CCC’s Crop Production Centres (1991 to 2002)

Source: http://canolacouncil.org/media/515701/management_practices.pdf

Swathing is another factor that impacts oil content. If swathing is conducted too early it can effect seed

oil content, especially if it is done prematurely prior to the seed moisture threshold10. This is supported

8 Vera and Downey et al., Yield and quality of canola seed as affected by stage of maturity at swathing, Canadian

Journal of Plant Science, July 2006 9 Walton, G., Ping Si, and B. Bowden., Environmental Impact on Canola Yield and Oil. 10 Vera and Downey et al.

44.7

44.2

43.8

42.9

41.3

39

40

41

42

43

44

45

May 1-10 May 11-20 May 21-31 June 1-10 After June 11

Oil

Co

nte

nt

%

27 | P a g e

through data produced by the Canola Council of Canada which showed later swathing, when seed colour

is 60-70% changed, resulted in a 1% increase in oil content11.

Fertilizer balance is also known to influence oil content but research seems to indicate that timing of

seeding and swathing have a greater influence. That being said, it is important to strike the right

nutrient balance, especially in regards to nitrogen. Higher levels of nitrogen increase yield and protein

content, but it can decrease oil content12. Taylor, Smith and Wilson found that despite the decrease in

oil concentration due to higher nitrogen levels, the total oil yield increased, due to higher seed yield13.

This underscores the need to take into account the total oil produced per acre, and not just total oil per

tonne of canola. The impact of various N levels on the oil content in canola is demonstrated in Figure V,

based on the work of Canola Council of Canada agronomists over six field seasons14. Their conclusion is

to apply N as recommended by the soil test in order to maximize oil content.

Figure V. Oil Content of Canola at Various N Application Rates

Source: http://canolacouncil.org/media/515701/management_practices.pdf

11 https://www.dekalb.ca/_uploads/documents/Agronomic_Information/CanolaArchive/what_affects_canola_oil.pdf 12 https://www.dekalb.ca/_uploads/documents/Agronomic_Information/CanolaArchive/what_affects_canola_oil.pdf 13 Taylor, A.J., Smith, C.J., and I.B. Wilson. Effect of irrigation and nitrogen fertilizer on yield on oil content, nitrogen accumulation and water use of canola (Brassica napus L) 14 http://canolacouncil.org/media/515701/management_practices.pdf

43

44

45

46

Fertilized to Standard 1.5 times recommended 2 times recommended

Oil

Co

nte

nt

%

28 | P a g e

Section 3: Implementation Issues

Sampling/Testing

Moving to component pricing would likely require industry investment in equipment for testing and

administration. Given the size and volume of canola and other grains moving through the Canadian

system, the test required to determine the oil content would need to be a “driveway” test, able to be

administered accurately and in minimal time as the grain is being delivered.

The Australian driveway test uses a near-infrared (NIR) system that takes a very short time on clean seed

and measures protein, oil and moisture. Producers are paid on the basis of the NIR at the time of

delivery. Each of the grain handlers will either use the NIR supplier (FOSS) supplied calibrations or

develop their own. The Australian Oilseeds Federation (AOF) ensures the accuracy of NIR through a

“test check” or “ring test” program which is applied to all participating labs. The variation rate of the

testing is very low (an average variation of 0.39 of one percent across the 15 participating labs as of the

July 2015 report) and reported monthly on the AOF website15. Test results are rarely disputed.

The Canadian Grain Commission (CGC) has also considered rapid methods of testing oil content,

including 3 Near-infrared (NIR) spectrometers, two Fourier Transform (FT-NIR) systems, Pulse nuclear

magnetic resonance (NMR) and an ultrapycnometer. They found oil content could be quickly

determined, but controls were necessary to ensure consistency between techniques and parameters.16

Any move to component pricing would require guidelines that emphasize consistent standards. The

testing equipment tested by the CGC was the DICKEY-john filter which costs $16,000-$20,000 and the

FOSS6500 NIR which is priced at $80,00017.

There are also a number of elevators and crushers conducting driveway tests currently for oil content in

canola. Based on the numerous interviews conducted, these tests are done by exporters in particular to

understand if rail cars delivered to port from various regions can meet the minimum oil content

specification from buyers and if not, a basic means to blend at port with higher content canola to meet

the contract terms. While these tests are not tied to pricing per se, we infer from this activity that tests

are relatively accurate and companies comfortable with the results.

Given the lack of dispute of driveway testing in the Australia and the EU, we do not think this would be

an issue in Canada either. However, significant costs would likely be added to the system for testing

equipment, training and infrastructure needed for every delivery point which would undoubtedly make

its way back into either pricing or potentially additional fees. Producers should be aware that a portion

of these costs would likely be borne by them.

Storage/Segregation

Storage both on farm and off of higher oil canola requires slightly different storage parameters than

lower oil canola in order to prevent spoilage. While other factors like moisture content and

temperature play an important role in the safe storage of canola, it has been found that the higher the

15 Australian Oilseeds Federation. Test Check Program. http://www.australianoilseeds.com/Technical_Info/test_check_program 16 Canadian Grain Commission: Measurement of Oil Content by Rapid Analytical Technique 17 Veronique J. Barthet, Programs Manager Oilseeds, Grain Research Laboratory, CGC

29 | P a g e

oil content, the less dry matter there is, making it more prone to spoilage than lower oil canola. Sun,

Jian et al, found that higher oil canola, under the same storage conditions and following the guidelines

recommended by the Canadian Grain Commission for low oil canola, had the same or shorter safe

storage times.18 They also determined that higher oil canola needed to be stored with lower moisture

content than lower oil canola. For every 1% higher oil content, a decrease in the safe moisture level by

0.1% was required19. For example, canola with 48% oil should be stored at 0.5% lower moisture than

canola with 43% oil20. In addition, Sun, Jian et al found that higher oil canola had a lower thermal

conductivity than lower oil canola, thereby taking longer to dissipate heat and cool down, and increasing

the risk of spoilage. Based on these findings it would be safe to assume that higher oil canola would

require more hands on management time than lower oil canola if storage is required for any length of

time.

In order to try and capture more value from the higher oil canola, additional storage facilities may need

to be added to segregate it from the lower oil content. Investing in additional storage for segregation

was not seen as cost recoverable from end use customers for all of the companies interviewed, meaning

that the value chain would either need to bear these costs if it implemented a component pricing

system, or simply not engage in segregation despite adoption of a premium-discount schedule.

Basis

While many producers are looking to create value with a component pricing system, industry feedback

indicates that basis level would adjust for the competitive nature of the canola market and bring it back

into equilibrium to where competition among buyers sits. So if oil content was added in as a factor, we

expect the basis will adjust to these new fixed elements. In other words no additional money or value

will be added to system despite a premium or discount being paid.

As previously noted, there is very little if any opportunity to capture a premium from the export market

for segregating product. If a component pricing system were put into place, it would be expected that

grain handlers would adjust the basis to compensate for the premiums paid to the producers given their

inability to pass these costs on to customers. As such, there would be very little net benefit to the

producer, as no extra value would be added to the system.

The canola market is highly competitive. Grain handlers and crush facilities routinely bid up the basis (or

lower it) to secure the product they want. Moving to a component pricing system would see the spread

between competitive basis levels narrow since the market was fixing a major factor that is a variable

today. By reducing the wider range in basis that one typically sees in the market today, we anticipate

that less opportunity would exist for producers to capitalize on variability in company approaches to

pricing in a less fixed environment.

18 Sun, K., Jian, F., Jayas, D.S., and N.D.G White. Quality changes in high and low oil content canola during storage: Part 1 – Safe storage time under constant temperatures. 19 Mills, J.T. and M. Hartman. Storage of Canola. http://www1.agric.gov.ab.ca/$department/deptdocs.nsf/all/crop1301#seed 20 Mills, J.T. and M. Hartman. Storage of Canola. http://www1.agric.gov.ab.ca/$department/deptdocs.nsf/all/crop1301#seed

30 | P a g e

Industry Views

Producer Groups

The Alberta Canola Producers Commission supports component pricing of canola seed as in their view it

provides for “the efficient transmission of end user demand signals.”21 The Manitoba Canola Growers

Association see the issue differently. As lower average oil content producers, the organization opposes

buying on oil content. However, the most important consideration for Manitoba producers is the

baseline as they expect the higher the baseline, the greater the negative impact on Manitoba producers.

The Canadian Canola Growers Association has yet to take an official position on the issue, though they

have investigated it a number of times. The lack of consensus among provincial canola producer

organizations has in large part made it difficult to pursue the matter further.

The difference in average oil contents in combination with producers’ inability to significantly influence

oil content puts Manitoba producers at a disadvantage compared to those in Saskatchewan and Alberta

when considering a system that would both reward and discount producers based on oil content.

Without the ability to directly and proactively manage oil content, the premium-discount schedule is

arbitrary although we would expect over time that some variables, such as land price, would being to

price in this variation if the difference in oil content among provinces or regions were to increase

further.

Exporters

Canola is generally exported as bulk product and as such there is very little willingness by our export

markets to pay a premium for a bulk commodity, regardless of whether it has high oil content. As well,

Canada’s export markets are generally price takers, again, making it difficult to extract a premium from

them. Australian exporters have found it challenging to extract additional value from their export

markets. Given that Australian and Canadian grain handlers export to shared markets, Canadian grain

handlers may face the same challenge, unable to draw additional value for higher oil canola.

While canola prices reflect the global market, most buyers buy based on previous experiences, paying

on price rather than on bonification. The price paid is based on an assumed oil yield stipulated in their

contracts, adjusting their bids in future contracts if necessary. If the grain handlers are unable to secure

a premium for canola from the export markets, this could be reflected by lowering the basis in order to

mitigate their losses.

Crushers

All crusher respondents indicated that crush profitability is heavily dependent on the availability and

quality of the canola seed within their catchment area. This was especially noteworthy for crusher

interviewees as there are far fewer crush plants in Western Canada than elevators, meaning there is

much less opportunity to be selective about what region to buy canola from if it were profitable to truck

longer distances.

Most interviewees said they were highly unlikely to have dedicated ‘runs’ for high oil content canola, as

the cost and time to separate high from low oil content would not result in increased profitability. Some

remarked that they had limited trials in the past on offering premiums/discounts for higher oil content,

21 ACPC official position

31 | P a g e

but in the end these pilot projects were abandoned as they had simply increased administrative and

operating costs with no payback for the industry. Most crushers felt that a bonification system would

likely result in increased costs if implemented across Western Canada that would need to be passed

through to producers because there was no apparent value being created through the segregation.

The industry consensus was component pricing increases costs in handling canola for no additional

value, and complicates a relatively simple marketing system. Most industry interviewees felt

bonification would undermine some of the key advantages the Canadian canola industry currently

enjoys which makes it a profitable commodity for producers and industry alike.

32 | P a g e

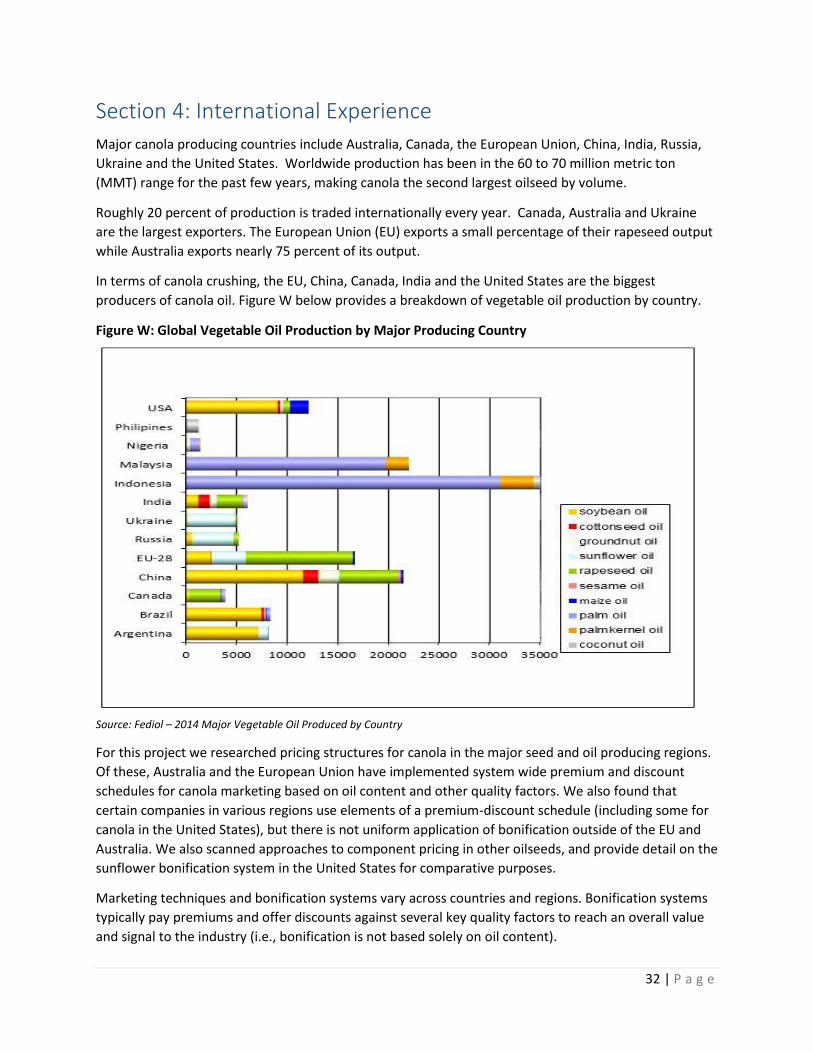

Section 4: International Experience

Major canola producing countries include Australia, Canada, the European Union, China, India, Russia,

Ukraine and the United States. Worldwide production has been in the 60 to 70 million metric ton

(MMT) range for the past few years, making canola the second largest oilseed by volume.

Roughly 20 percent of production is traded internationally every year. Canada, Australia and Ukraine

are the largest exporters. The European Union (EU) exports a small percentage of their rapeseed output

while Australia exports nearly 75 percent of its output.

In terms of canola crushing, the EU, China, Canada, India and the United States are the biggest

producers of canola oil. Figure W below provides a breakdown of vegetable oil production by country.

Figure W: Global Vegetable Oil Production by Major Producing Country

Source: Fediol – 2014 Major Vegetable Oil Produced by Country

For this project we researched pricing structures for canola in the major seed and oil producing regions.

Of these, Australia and the European Union have implemented system wide premium and discount

schedules for canola marketing based on oil content and other quality factors. We also found that

certain companies in various regions use elements of a premium-discount schedule (including some for

canola in the United States), but there is not uniform application of bonification outside of the EU and

Australia. We also scanned approaches to component pricing in other oilseeds, and provide detail on the

sunflower bonification system in the United States for comparative purposes.

Marketing techniques and bonification systems vary across countries and regions. Bonification systems

typically pay premiums and offer discounts against several key quality factors to reach an overall value

and signal to the industry (i.e., bonification is not based solely on oil content).

33 | P a g e

While the summary below of bonification systems in Australia, the EU and the United States is

instructive, there are a number of factors which complicate simple comparisons. Standards and

baselines for different quality criteria are diverse and typically shaped to fit the production realities of

the region in question. Translating this experience to the Canadian market may or may not be relevant,