Embed Size (px)

Citation preview

West Midlands Pension Fund

Compliance Manualand Summary OperatingProcedures

October 2015

2 COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015

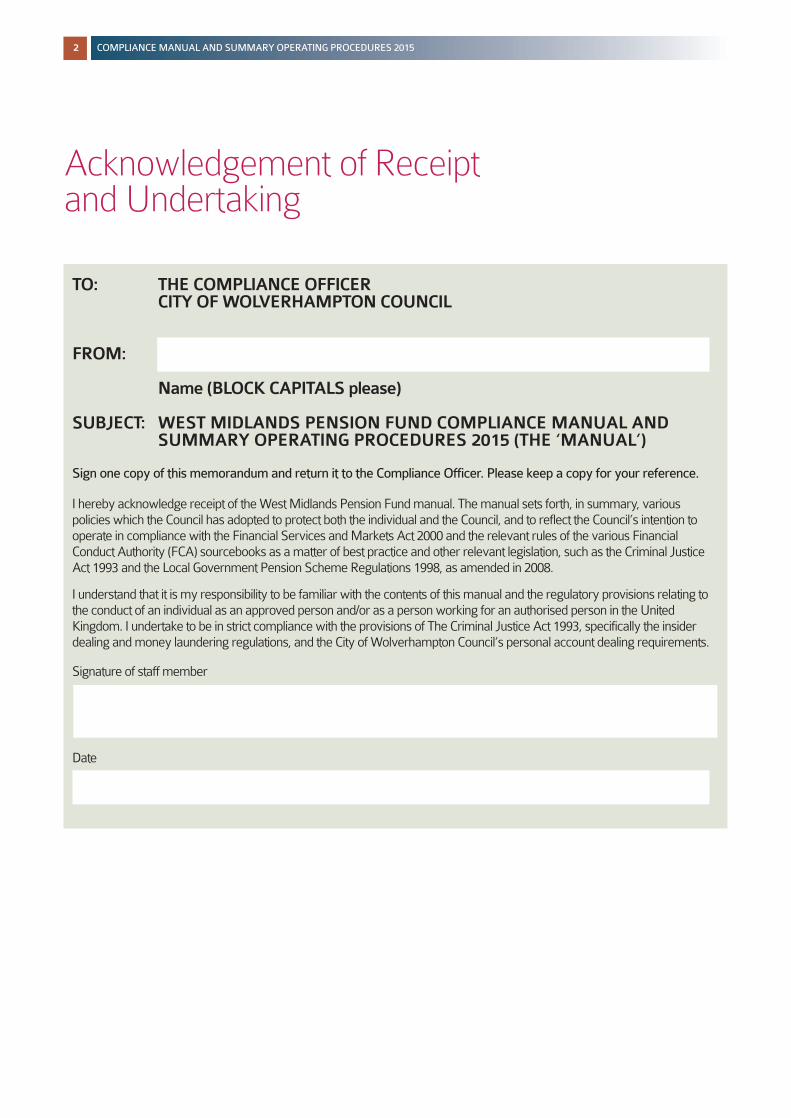

Acknowledgement of Receipt and Undertaking

TO: THE COMPLIANCE OFFICERCITY OF WOLVERHAMPTON COUNCIL

FROM:

Name (BLOCK CAPITALS please)

SUBJECT: WEST MIDLANDS PENSION FUND COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015 (THE ‘MANUAL’)

Sign one copy of this memorandum and return it to the Compliance Officer. Please keep a copy for your reference.

I hereby acknowledge receipt of the West Midlands Pension Fund manual. The manual sets forth, in summary, various policies which the Council has adopted to protect both the individual and the Council, and to reflect the Council’s intention tooperate in compliance with the Financial Services and Markets Act 2000 and the relevant rules of the various Financial Conduct Authority (FCA) sourcebooks as a matter of best practice and other relevant legislation, such as the Criminal JusticeAct 1993 and the Local Government Pension Scheme Regulations 1998, as amended in 2008.

I understand that it is my responsibility to be familiar with the contents of this manual and the regulatory provisions relating tothe conduct of an individual as an approved person and/or as a person working for an authorised person in the United Kingdom. I undertake to be in strict compliance with the provisions of The Criminal Justice Act 1993, specifically the insiderdealing and money laundering regulations, and the City of Wolverhampton Council’s personal account dealing requirements.

Signature of staff member

Date

Acknowledgement of Receipt and Undertaking 2

1 Introduction 41.1 Business Overview 41.2 Financial Service and Market Act 2000 81.3 FCA Statement of Principles 91.4 Statements of Principles and Code of Practice 10

for Approved Persons1.5 Meetings and Correspondence with Regulators 111.6 Compliance 121.7 Code of Market Conduct 131.8 Money Laundering 161.9 High Level Standards for Firms and Individuals 161.10 Impact of Markets in Financial Instruments 17

Directive (‘MiFID’) on the Council1.11 Impact of the Capital Requirements 17

Directive (‘CRD’)

2 Investments and Finance 192.1 Preface 192.2 Client Communications General Advertising 19

Requirements2.3 Charges 202.4 Suitability 202.5 Churning and Switching 212.6 Use of Dealing Commissions 222.7 Best Execution 232.8 Timely Execution 232.9 Trade Recording 242.10 Aggregation and Allocation 252.11 Periodic Information 252.12 Safekeeping Of Assets 262.13 Outsourcing Arrangement 282.14 External Fund Managers 282.15 Disclosure and Transparency Rules 292.16 Staff Fitness and Propriety 312.17 Training and Competence 312.18 Compliance Monitoring 322.19 Transaction Reporting 32

3 General 333.1 Conflicts of Interest 333.2 Personal Dealing Rules 343.3 Inducements 353.4 Bribery Act 2010 36

Principle 1 – Proportionate Procedures 36Principle 2 – Top-level Commitment 36Principle 3 – Risk Assessment 37Principle 4 – Due Diligence 37Principle 5 – Communication and Training 37Principle 6 – Monitoring & Review 37

3.5 Money Laundering – Procedures 373.6 Record Keeping 403.7 Rule and Procedure Breaches 403.8 Data Protection 413.9 Business Continuity 413.10 Compliants 42

Appendix A Dealing Limits 44

Appendix B Specific Approval 45

Appendix C Lending Limits 46

Appendix D LGPS (Management & Investment 47of Funds) Regulations 2009 – 1 April 2013

1) Citation, commencement and application 482) General definitions 483) Definition of ‘investment’ 484) Management of pension fund 495) Power to borrow 506) Separate bank account 507) Definition of ‘investment manager’ 518) Choice of investment managers 519) Terms of appointment of investment managers 5110) Review of investment manager’s performance 5211) Investment policy and investment of 52

pension fund money12) Statement of investment principles 5213) Investments under section 11(1) of the 53

Trustee Investments Act 196114) Restrictions on investments 5315) Requirements for increased limits 5316) Use of fund money by an 53

administering authority17) Revocations 54

Appendix E LGPS (Management & Investment of 58Funds) Regulations 2009 – 1 January 2010

1) Citation and commencement 592) General definitions 593) Definition of ‘investment’ 604) Management of pension fund 615) Definition of ‘investment manager’ 716) Choice of investment managers 717) Terms of appointment of investment managers 718) Review of investment manager's performance 729) Use and Investment of pension fund money 729a) Statement of investment principles 7210) Investments under s.11 of the Trustee 73

Investments Act 1961.11) Restrictions on investments 7311a) Requirements for increased limits 7312) Use of fund money by an 74

administering authority13) Consequential amendments and revocations 75

Appendix F Staff Declaration 80

COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015 3

Contents

4 COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015

1 Introduction

1.1 Business Overview

The City of Wolverhampton Council (the ‘authority’) is an administering authority of the Local Government PensionScheme (LGPS) and is responsible for administering the West Midlands Pension Fund (‘WMPF’) and the West MidlandsIntegrated Transport Authority Pension Fund (‘WMITA PensionFund’), known collectively as the ‘Fund’. Therefore, not only does it manage its own investments, it also carries out investment and other services for and on behalf of WMITA Pension Fund.

The investment services carried out by the authority for WMITAPension Fund fall within the remit of the Financial Services Act2012, the Act created the regulatory organisation, the Financial Conduct Authority (FCA). Although the authority is not regulatedby the FCA, it has decided to follow the rules of the FCA as amatter of best practice.

This manual needs to be read in conjunction with the Fund’s Employee Code of Conduct. It is acknowledged that there is a degree of overlap between the code and this manual but, takentogether, they create a structure within which employees canfeel secure that they are performing their jobs appropriately andthat the Fund is properly exercising its responsibilities.

1.1.1 Purpose of this ManualThis manual sets out the procedures that the City of Wolverhampton Council has decided to voluntarily observe asmanagers of an occupational pension scheme (OPS), called theWest Midlands Pension Fund. The following procedures arebased upon those of the FCA.

In addition to voluntarily complying with FCA rules as a matter of best practice, we are required to comply with the Local Government Pension Scheme Regulations 1995 as amendedand altered by subsequent regulation, which set out the mechanics of how the scheme should be run by us as an administering authority. These regulations are not considered indetail in this manual; however, the section governing powers ofinvestment is included in section two, in order to make this acomplete guide to the regulatory requirements of the InvestmentDivision of the WMPF. Also Appendix D includes the LGPS(Management & Investment of Funds) Regulations 2009 whichcame into force on 1 January 2010.

This manual provides an overview of compliance matters relevant to the authority as a whole, rather than to the regulationof all particular areas of investment business. Employees shouldbe familiar not only with these general principles, proceduresand rules but also with those applicable to their particular area of business. It is intended to outline the general principles of regulation and to highlight some of the more critical aspects ofthese requirements, from the employee's perspective.

It is not possible in a manual of this kind to cover all matters or to anticipate all the requirements which may arise in new or developing areas of Fund administration, so it will be necessaryto supplement and amend the manual from time to time. This willbe achieved through the issue of amendments and practicenotes.

1.1.2 ScopeThis manual is applicable in its entirety to all members of the investment or related divisions of the administering authority.Other members or employees of the administering authoritymust read the following sections of the manual:

Section 1 Introduction in its entirety; andSection 3 General rules, subsections:• Conflicts of interest• Personal dealing rules• Inducements• Bribery Act 2010• Money laundering – procedures• Record keeping• Rule and procedure breaches• Data protection• Business continuity, and• Complaints.

If you are in doubt whether you are a member of the investmentor related divisions, or whether any part of this manual is applicable to your role or activities, please contact the Compliance and Risk Team.

1.1.3 Your ResponsibilityAs an employee or member of the administering authority, it isyour responsibility to read these procedures, observing themboth in spirit as well as the letter, and to act with high standardsof honesty and fairness. Failure to do so constitutes a seriousbreach of duty and could result in dismissal.

If you do not understand how these procedures apply to you, orwhat action you should take in any circumstances, you should consult the Compliance and Risk Team. Ignorance or misunderstanding of these procedures will not be accepted as an excuse for failing to comply with them.

1.1.4 Notification of Breaches If, in any circumstances, you think you cannot fully comply withthese procedures or if you have for any reason failed to observeany of these procedures, you should immediately notify theCompliance and Risk Team who will advise on what steps totake.

1.1.5 Written Compliance Procedures To ensure that employees act in accordance with their own andthe Fund’s relevant responsibilities under the principles, the Fund is required to draw up written compliance procedures. This manual forms part of the Fund’s written compliance procedures. Further guidance on the obligations of staff is givenin the code of conduct issued to each member of staff.

1.1.6 Co-operation With Enquiries, Inspections, etc. Employees must fully co-operate with any inspection. Upon request they will make themselves available to any inspectionteam, produce any inspection team documents, files, computerdata and other material in their possession, power or control;give access to any inspection team to all premises at all times (including access to computer facilities, files or systems) and permit any inspection team to copy documents or other materialor remove copies; to answer truthfully, fully and promptly allquestions put to them by any member of an inspection team.Employees must take all steps within their power to ensure thatno record or file shall be amended or destroyed if it may be relevant to any matter which is currently the subject of a disciplinary enquiry, formal inspection or other process, reference or appeal.

1.1.7 Co-operation With a Customer Under the principles, the Fund’s employees must allow WMITAto inspect, either personally or through an agent, any record ofmatters relating exclusively to WMITA within seven days of receiving a request. If there is any doubt whether to allowWMITA to inspect a record, for example where that record doesnot relate exclusively to WMITA, the Compliance and Risk Teamshould be asked for further guidance.

It is the additional duty of the Chief Financial Reporting Officer,Strategic Director of Pensions, senior managers and managersto ensure that there is full compliance in every activity undertaken, whether or not it is part of the administering authority's business, which is in voluntary compliance with FCA rules.

1.1.8 Key PersonnelThe following is a list of key personnel with responsibilities for avariety of functions:

OfficersAssistant Director Finance: Mark TaylorChief Legal Officer: Kevin O’KeefeStrategic Director of Pensions: Geik DreverHead of Governance: Rachel HoweAssistant Director (Investments): Mark ChalonerAssistant Director (Actuarial & Pensions): Rachel Brothwood

Designated OfficersCompliance Officer: Mark TaylorMoney Laundering Reporting Officer: Mark TaylorTraining and Competence Officer: Geik Drever

1.1.9 Governance ArrangementsThe Fund’s governance arrangements have four elements:

1) Pensions Committeea) To discharge the functions of the administering authority

for the application of the Local Government Pension Scheme regulations in the West Midlands.

b) To put in place and monitor the arrangements for the administration of contributions and payments of benefits as required by the regulations, and the proper management and investment of monies held for the purpose of paying benefits.

c) To determine and review the provision of resources made available for the discharge of the function of administering authority.

2) Pensions BoardThe local Pensions Board assists the Pensions Committeewith the good governance of the scheme ensuring the Fund’s adherence to legislation, statutory codes of practice and guidance.

Consisting of five employer and five member representativestogether with two City of Wolverhampton councillors, theboard ensures the good performance of the Fund through theScheme Advisory Board’s benchmarking criteria.

COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015 5

6 COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015

3) Advisors and OfficersThe Fund’s principal advisors are as follows:

a) High level advice on general management from the Managing Director of the City of Wolverhampton Council.

b) Legal and general administrative advice and management from the Chief Legal Officer of the City of Wolverhampton Council who is also the monitoring officer for the City of Wolverhampton Council.

c) Financial and technical advice from the Strategic Director of Pensions who is the lead senior support officer and has direct responsibility for the in-house management.

d) The Strategic Director of Pensions is the senior full-time officer who provides technical advice to members and officers, as well as implementing the investment strategy through a team of professionally qualified staff and external managers.

e) Senior pension administration staff are responsible for pension’s administration and communications.

f) Assistant Director Finance of the City of Wolverhampton Council is the Section 151 officer of the City of Wolverhampton Council and that responsibility applies to the Fund.

4) Investment Advisory Sub-CommitteeThe Investment Advisory Sub-Committee has oversight of the implementation of the management arrangements andcomprises representatives from the seven district councilsand two local trade unions. The Committee meet at least fourtimes a year.

1.1.11 Organisation ChartThe WMPF structure is shown on the next page.

7CO

MP

LIA

NCE

MA

NU

AL

AN

D S

UM

MA

RY

OP

ERA

TIN

G P

RO

CED

UR

ES20

15

CFO

SECT

ION

151

O

FFIC

ER

(HEA

D O

F FI

NA

NCE

PR

OFE

SS

ION

)

Mar

k Ta

ylor

Fund

Acc

ount

ant

Rizw

an D

hana

ni

Acc

ount

ant

Erik

Bag

nall

Acc

ount

ing/

Inve

stm

ent

Adm

inis

trat

ion

Offi

cer

Vaca

ntPa

van

Bai

ns

Jam

es B

est

Ric

hard

Coo

kson

Pam

Law

Jatin

der R

aulia

Bev

erle

y To

mbs

Kally

Vird

ee

Acc

ount

ing/

Inve

stm

ent

Ass

ista

nt

Mar

cus

Perr

y

Cler

ical

Ass

ista

nt

Stew

art B

runs

don

HEA

D O

F G

OV

ER

NA

NCE

Rac

hel H

owe

HEA

D O

F FI

NA

NCE

Dav

id K

ane

AS

SIS

TAN

T D

IRECT

OR

(IN

VES

TMEN

TS)

Mar

k Ch

alon

er

Com

plia

nce

and

Ris

k M

anag

er

Emm

a B

land

Com

plia

nce

and

Ris

k O

ffice

r

Jen

Dug

mor

e

Com

mun

icat

ions

Offi

cer

Vaca

nt

Even

ts C

o-or

dina

tor

Vic

toria

Ben

nett

Gra

phic

s/M

arke

ting

Offi

cer

Step

hen

Leve

sley

Res

pons

ible

Inve

stm

ent O

ffice

r

Lean

ne C

lem

ents

Trus

tee

Man

agem

ent O

ffice

r

Jane

Haz

eldi

ne

Port

folio

Man

ager

x 5

Dav

id E

vans

Mar

k H

odge

sM

ike

Har

dwic

kVa

cant

Jas

Sidh

u

Ass

istan

t Inv

estm

ent A

naly

st x

4

Vic

toria

Cla

rkA

nn-M

arie

Pat

ters

onLi

ssa

Nic

hols

Ann

e R

usse

ll

Ass

ista

nt P

ortfo

lio M

anag

er x

3

Tom

Pow

ell

Jam

es S

olom

onVa

cant

Inve

stm

ent S

uppo

rt O

ffice

r x 3

Pava

n B

ains

Tany

a N

olan

Vaca

nt

Bus

ines

s D

evel

opm

ent O

ffice

r

Lisa

Dav

is

Bus

ines

s Su

ppor

t Offi

cer

Hea

ther

Cla

rke-

Trev

is

Bus

ines

s Su

ppor

t Offi

cer

Rut

h G

ould

PA to

the

Stra

tegi

c D

irect

or

Suni

ta G

odda

rd-P

atel

Tech

nica

l Tra

inin

g O

ffice

r x 2

Jas

Bho

gal

Mik

e H

ollin

gsw

orth

STR

ATE

GIC

DIR

ECT

OR

OF

PEN

SIO

NS

Gei

k D

reve

r

Gov

erna

nce

Inve

stm

ents

Fina

nce

8 COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015

1.2 Financial Service and Markets Act 2000

The Financial Services and Markets Act 2000 (‘FSMA’ asamended by the Financial Services Act 2012) is the underlyingprimary legislation which provided for the formation of the FCAand the establishment of its powers.

FSMA provides particular scope for the FCA’s enforcementpowers in respect of the Code of Market Conduct (see section1.6 below), contained within the Market Conduct Sourcebookelement of the FCA Handbook. The FCA is able to levy penaltiesagainst individuals or firms who breach the code through insiderdealing or attempted market manipulation. FSMA also enablesthe FCA to apply to the High Court for disgorgement or restitutionorders.

Part 1a of the Financial Services Act 2012 sets out three overallstatutory objectives which the FCA needs to achieve. These influence the FCA’s approach to regulation from policy to the detailed rule setting level.

The three objectives are:

a) the consumer protection objective: securing the appropriatedegree of protection for consumers;

b) the integrity objective: protecting and enhancing the integrityof the UK financial system; and

c) the competition objective: promoting effective competition inthe interest of consumers.

1.2.1 FCA RegulationAs the administering authority of the Fund, the Council’s mainbusiness area is discretionary investment management.

This activity is normally regulated by the FCA. The administeringauthority manages a local authority pension fund which is regulated by the Local Government Pension Fund Regulations1995, and as such does not require authorisation by the FCA. If the administering authority was regulated by FCA, it wouldhave to comply with:

a) The FCA Handbook of rules and guidance;

b) any limitations or requirements imposed on it by the FCA; and

c) the overall provisions of FSMA.

1.2.2 AuthorisationThe FSMA is the primary legislation in relation to investmentbusiness in the UK and provides that any person who carries ondesignated investment business without either authorisation orexemption will be guilty of an offence and will be liable to criminal and civil proceedings.

Investment activities carried out by the administering authority in relation to regulated investments, which are subject to the Financial Services and Markets Act; include arranging deals inand managing regulated investments.

The Financial Services and Markets Act requires companiessuch as the administering authority to be authorised so as to ensure that only people who are fit and proper carry on investment business within the UK.

However, the administering authority manages a local authoritypension fund which is regulated under the Local GovernmentPension Fund Regulations 1995, and as such does not requireauthorisation by the FCA.

The administering authority manages the Fund internally in conjunction with the use of external managers.

COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015 9

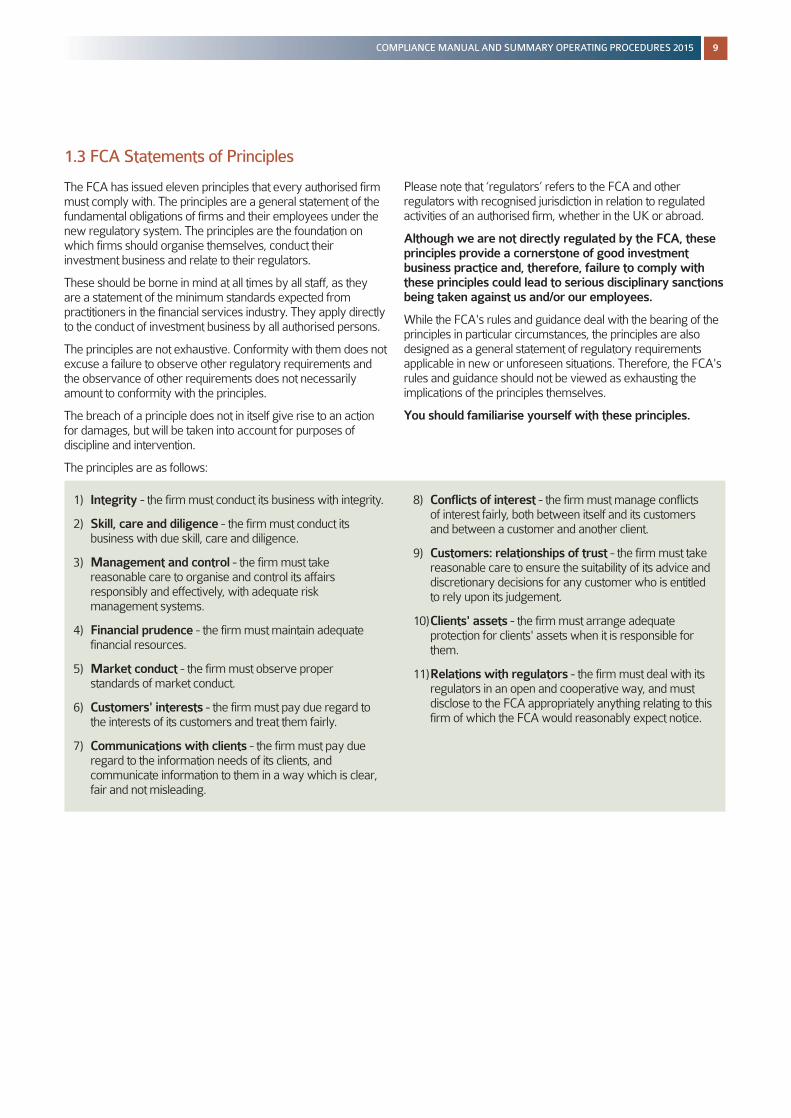

1.3 FCA Statements of Principles

The FCA has issued eleven principles that every authorised firmmust comply with. The principles are a general statement of thefundamental obligations of firms and their employees under thenew regulatory system. The principles are the foundation onwhich firms should organise themselves, conduct their investment business and relate to their regulators.

These should be borne in mind at all times by all staff, as they are a statement of the minimum standards expected from practitioners in the financial services industry. They apply directlyto the conduct of investment business by all authorised persons.

The principles are not exhaustive. Conformity with them does notexcuse a failure to observe other regulatory requirements andthe observance of other requirements does not necessarilyamount to conformity with the principles.

The breach of a principle does not in itself give rise to an actionfor damages, but will be taken into account for purposes of discipline and intervention.

The principles are as follows:

Please note that ‘regulators’ refers to the FCA and other regulators with recognised jurisdiction in relation to regulated activities of an authorised firm, whether in the UK or abroad.

Although we are not directly regulated by the FCA, these principles provide a cornerstone of good investment business practice and, therefore, failure to comply withthese principles could lead to serious disciplinary sanctionsbeing taken against us and/or our employees.

While the FCA's rules and guidance deal with the bearing of theprinciples in particular circumstances, the principles are also designed as a general statement of regulatory requirements applicable in new or unforeseen situations. Therefore, the FCA'srules and guidance should not be viewed as exhausting the implications of the principles themselves.

You should familiarise yourself with these principles.

1) Integrity - the firm must conduct its business with integrity.

2) Skill, care and diligence - the firm must conduct its business with due skill, care and diligence.

3) Management and control - the firm must take reasonable care to organise and control its affairs responsibly and effectively, with adequate risk management systems.

4) Financial prudence - the firm must maintain adequate financial resources.

5) Market conduct - the firm must observe proper standards of market conduct.

6) Customers' interests - the firm must pay due regard tothe interests of its customers and treat them fairly.

7) Communications with clients - the firm must pay due regard to the information needs of its clients, and communicate information to them in a way which is clear,fair and not misleading.

8) Conflicts of interest - the firm must manage conflicts of interest fairly, both between itself and its customers and between a customer and another client.

9) Customers: relationships of trust - the firm must takereasonable care to ensure the suitability of its advice anddiscretionary decisions for any customer who is entitled to rely upon its judgement.

10)Clients' assets - the firm must arrange adequate protection for clients' assets when it is responsible for them.

11)Relations with regulators - the firm must deal with itsregulators in an open and cooperative way, and must disclose to the FCA appropriately anything relating to thisfirm of which the FCA would reasonably expect notice.

1.4 Statements of Principles and Code of Practice for Approved Persons

In relation to individuals, underpinning all of the FCA’s regulationsfor approved persons are the seven principles set out in theStatements of Principles and Code of Practice for Approved Persons included in the FCA Handbook. The first four principlesapply to all approved persons while the remaining three apply tothose individuals performing significant influence functions (controlled functions 1 to 12B, 28 and 29 as set out within chapter 10 of the FCA’s supervision manual).

They are as follows:

• An approved person must act with integrity in carrying outtheir controlled function.

• An approved person must act with due skill, care and diligence in carrying out their controlled function.

• An approved person must observe proper standards ofmarket conduct in carrying out their controlled function.

• An approved person must deal with the FCA and other regulators in an open and co-operative way and must disclose appropriately any information of which the FCAwould reasonably expect notice.

• An approved person performing a significant influence function must take reasonable steps to ensure that the regulated business of the firm for which they are responsible in their controlled function is organised so that it can be controlled effectively.

• An approved person performing a significant influence function must exercise due skill, care and diligence in managing the business of that firm for which they are responsible in their controlled function.

• An approved person performing a significant influence function must take reasonable steps to ensure that the business of that firm for which they are responsible in their controlled function complies with the regulatory requirements imposed on that business.

The FCA has issued a Code of Conduct for Approved Personswhich sets out descriptions of conduct which, in the opinion ofthe FCA, do not comply with the statements of principle and, incertain cases, factors which, in the opinion of the FCA, are to betaken into account in determining whether or not an approvedperson’s conduct complies with one of the statements of principle.

1.4.1 Senior Managers’ Regime The FCA published Consultation Paper CP 14/13 - Strengtheningaccountability in banking: a new regulatory framework for individuals respectively in July 2014. This outlined the view thatbehaviour and culture within banks played a major role in the2008-09 financial crisis and in conduct scandals such as paymentprotection insurance (PPI) misselling and the attempted manipulation of LIBOR.

The FCA believes that holding individuals to account is a keycomponent of effective regulation. In this consultation, the regulator is proposing changes to the way individuals working for UK banks, building societies, credit unions and PRA-designated investment firms (collectively referred tothroughout the consultation paper (CP) as ‘relevant firms’) are assessed and held accountable for the roles they perform.The proposals reflect the recommendations of the ParliamentaryCommission on Banking Standards (‘PCBS’) and implementchanges required by amendments which the Financial Services(Banking Reform) Act 2013 (the ‘Act’) made to the FinancialServices and Markets Act 2000 (FSMA).

These changes are significant and include:

• a new ‘Senior Managers Regime’ (SMR) for individuals who are subject to regulatory approval, which will requirefirms to allocate a range of responsibilities to these individuals and to regularly vet their fitness and propriety.This will focus accountability on a narrower number of senior individuals in a firm than the current ‘Approved Persons Regime’ (‘APR’);

• a ‘Certification Regime’ which will require relevant firms toassess the fitness and propriety of certain employees whocould pose a risk of significant harm to the firm or any of its customers; and

• a new set of ‘conduct rules’.

A final policy statement and final rules will be published by theregulators, following which this manual, the code and relevantpolicies and procedures will be updated. Please contact theCompliance and Risk Team if you have any questions on the new ‘Senior Managers Regime’.

10 COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015

COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015 11

1.5 Meetings and Correspondence with Regulators

FCA Principle 11 - Relations with regulators - states that the "firmmust deal with its regulators in an open and co-operative way,and must disclose to the FCA appropriately anything relating tothe firm of which the FCA would reasonably expect notice".

The FCA specifically requires that the firm must take reasonablesteps to ensure that all information it gives to the FCA is factually accurate, complete and, in the case of estimates andjudgements, fairly and properly based after appropriate enquiries have been made by the firm.

As the firm must also have adequate systems and internal controls in place to conduct its business in an orderly manner, it is imperative that any dealings or communication with any ofthe firm's regulators must also be carried out in an orderly andconsistent manner.

Although we are not regulated by the FCA, other 'regulators'may make enquiries of us such as the National Audit Office,Local Government Office, The Pensions Regulator and the Pensions Ombudsman.

As such, all employees are subject to the following procedures:

• All communications in respect of any queries or investigation by a regulatory body must be referred immediately to the Compliance Officer.

• Any employee contacted by a regulatory body should take down brief details of the nature of the communicationand state that they will refer the matter to the ComplianceOfficer.

• Any requests for information or co-operation from a regulatory body must be referred to the Compliance Officer before any communication is forwarded. It will be responsibility of the Compliance and Risk Team for co-ordinating any request for information.

• Any request for information or cooperation from the police, the Department of Trade and Industry or any otherprosecuting authority must be immediately referred to the Compliance and Risk Team. The Compliance and Risk Team will co-ordinate any response with other departments. Occasionally, a regulatory body or the police may state that on no account may an employeespeak to anyone else in respect of an enquiry. Regardless of any attempt to impose such a prohibition, employeesmust immediately inform the relevant Compliance Officerbefore agreeing to provide any information or document.

• No employee should attend a meeting or interview with a regulatory body without informing and receiving permission from the Compliance and Risk Team. The Compliance and Risk Team will co-ordinate such meetings and retains the right to attend any such meeting or interview at its discretion.

It is vital that the firm has a co-ordinated and consistent approachto dealing with any regulators.

Always contact your Compliance Officer immediately upon receiving any communication from a regulator.

12 COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015

1.6 Compliance

1.6.1 Compliance OfficerThe administering authority must ensure that it takes reasonablesteps to establish and maintain compliance procedures, includingthe appointment of a Compliance Officer of appropriate statusand experience.

The Compliance Officer has responsibility for overseeing the administering authority's compliance procedures including responsibility for ensuring that any necessary records are kept.Responsibility for compliance also rests with line managementand employees themselves. All matters contravening the administering authority's internal compliance controls should be referred to him or her.

You should also speak to him or her in the first instance, if youhave any queries about how these procedures apply to you. In the absence of the Compliance Officer, you should consult amember of the Fund’s Compliance and Risk Team.

The Compliance Officer and the Compliance and Risk Team areavailable to assist employees to conduct business in accordancewith the relevant rules and regulations. Employees should not attempt to resolve difficult or unfamiliar questions alone.

When in doubt on a matter of interpretation or on the propriety ofa particular course of action or if uncertainty arises as to whetherwe are authorised to conduct a certain type of business, theyshould consult the designated Compliance Officer or a memberof the Compliance and Risk Team. A list of these individuals is detailed below:

The administering authority's Compliance Officer is Mark Taylor.

The Compliance Officer reports to the Pensions Committee.

1.6.2 Compliance and Risk TeamAll members of the Compliance and Risk Team assist the Compliance Officer.

The Compliance and Risk Team will assist, co-operate with, andmonitor the activities of all investment activities, and will submitregular reports on areas covered, including but not limited tobreaches of any kind, and identifying any needs for additionaltraining in any aspect of the administering authority's business.

The Compliance and Risk Team will be provided with adequateresources with regards to staff and finance to fulfil their role.

1.6.3 Responsibility for ComplianceThe Pensions Committee of the administering authority is ultimately responsible for the administering authority’s compliance. This is recognised by a regular review of compliance activities at Pensions Committee meetings:

The regular review of compliance activities includes but is notlimited to:

• reviewing the annual report and statement of accounts to ensure its compliance with legal and regulatory requirements;

• reviewing controls procedures relating to all significant operational risks;

• ensuring the independence of the compliance function;

• receiving a written report from the Compliance and RiskTeam, covering the general state of compliance within theadministering authority; and

• receiving a quarterly, written report on the programme of inspections and any findings or other matters likely to involve the reputation of the administering authority and/orrisk of significant compliance breach.

COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015 13

1.7 Code of Market Conduct

1.7.1 Market Conduct RulesThe Code of Market Conduct is part of the Market ConductSourcebook (‘MAR’) within the FCA Handbook. MAR was updated in July 2005 as part of the UK’s implementation of theMarket Abuse Directive, introduced through legislation acrossEurope to further advance the process of financial integrationand harmonisation.

The code itself establishes a regime for determining ‘marketabuse’, based upon the behaviour which a ‘regular user’ (‘a reasonable person who deals on that market in investmentsof the kind in question’) would regard as behaviour falling belowreasonably expected standards for that market.

The remit of the market abuse regime extends to qualifying investments (equities, debt and derivatives, including commodityderivatives) traded on prescribed markets (recognised investment exchanges in the UK).

The code outlines seven potential offences which are deemed toconstitute ‘market abuse’. These are:

1) Insider DealingThe abuse of insider dealing outlined by FCA rules should beconsidered in conjunction with the criminal penalty laid out by theCriminal Justice Act 93 (detailed in section 1.6.1). The followingfour types of behaviour are listed as being considered by theFCA to fall within the insider dealing definition of market abuse:

• Dealing on the basis of inside information which is not trading information;

• Front running/pre-positioning - that is, a transaction for aperson’s own benefit, on the basis of and ahead of an order which he is to carry out with or for another (in respect of which information concerning the order is inside information), which takes advantage of the anticipated impact of the order on the market price;

• In the context of a takeover, an offer or potential offeror entering into a transaction in a qualifying investment, on the basis of inside information concerning the proposed bid, that provides merely an economic exposure to movements in the price of the target company’s shares (for example, a spread bet on the target company’s shareprice); and

• In the context of a takeover, a person who acts for the offeror or potential offeror dealing for his own benefit in a qualifying investment or related investment on the basis of information concerning the proposed bid which is insideinformation.

2) Improper DisclosureThe FCA defines improper disclosure as being either of the following behaviour:

• Disclosure of inside information by the director of an issuer to another in a social context; and

• Selective briefing of analysts by directors of issuers or others who are persons discharging managerial responsibilities.

3) Misuse of InformationMAR describes the following as being behaviour that amounts toa misuse of information:

• Dealing or arranging deals in qualifying investments basedon relevant information, which is not generally available and relates to matters which a regular user would reasonably expect to be disclosed to users of the particularprescribed market, but which does not amount to marketabuse (insider dealing) (whether because the dealing relates to a qualifying investment to which section 118(2)does not apply or because the relevant information is not inside information); and

• A director giving relevant information, which is not generally available and relates to matters which a regularuser would reasonably expect to be disclosed to users of the particular prescribed market, to another otherwise thanin the proper course of the exercise of his employment orduties, in a way which does not amount to market abuse(improper disclosure) (whether because the relevant information is not inside information or for some other reason).

4) Manipulating TransactionsThe manipulation of transactions is defined as being the effectingof transactions which “give, or are likely to give, a false or misleading impression as to the supply of, or demand for, or asto the price of one or more qualifying investments; or secure theprice of one or more such investments at an abnormal or artificial level”. Behaviour that would fall within this definition issplit into that which could be viewed as giving a ‘false and misleading impression’, and that which could be deemed to beprice positioning. Examples of each are provided within the FCAHandbook, and the Compliance Officer should be consulted ifyou have any uncertainties, or require further clarification.

14 COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015

5) Manipulating DevicesThe FCA has included the following as examples of marketabuse through the manipulation of devices:

• Taking advantage of occasional or regular access to the traditional or electronic media by voicing an opinion about a qualifying investment (or indirectly about its issuer) while having previously taken positions on that qualifying investment and profiting subsequently from the impact ofthe opinions voiced on the price of that instrument, withouthaving simultaneously disclosed that conflict of interest tothe public in a proper and effective way;

• A transaction or series of transactions that are designed toconceal the ownership of a qualifying investment, so thatdisclosure requirements are circumvented by the holding of the qualifying investment in the name of a colluding party, such that disclosures are misleading in respect of the true underlying holding. These transactions are oftenstructured so that market risk remains with the seller. This does not include nominee holdings;

• Pump and dump - that is, taking a long position in a qualifying investment and then disseminating misleadingpositive information about the qualifying investment with aview to increasing its price; and

• Trash and cash - that is, taking a short position in a qualifyinginvestment and then disseminating misleading negative in-formation about the qualifying investment, with a view todriving down its price.

6) DisseminationThe abuse of dissemination is defined by the FCA as being behaviour which includes:

• knowingly or recklessly spreading false or misleading information about a qualifying investment through themedia, including in particular through a regulatory information service or similar information channel; and

• undertaking a course of conduct in order to give a false ormisleading impression about a qualifying investment.

7) Misleading Behaviour and DistortionThis type of market abuse is defined as being “likely to give aregular user of the market a false or misleading impression as to the supply of, demand for or price or value of, qualifying investments or would be, or would be likely to be, regarded by a regular user of the market as behaviour that would distort, orwould be likely to distort, the market in such an investment”.

At the same time, it is also “likely to be regarded by a regularuser of the market as a failure on the part of the person concerned to observe the standard of behaviour reasonably expected of a person in his position in relation to the market”.

Examples given by the FCA include:

• the movement of physical commodity stocks, which might create a misleading impression as to the supply of, or demand for, or price or value of, a commodity or the deliverable into a commodity futures contract; and

• the movement of an empty cargo ship, which might create a false or misleading impression as to the supply of, or thedemand for, or the price or value of a commodity or the deliverable into a commodity futures contract.

As can be clearly seen, the offences are wide ranging and theunderlying legislation has taken away the potential safe harboursof, for example, adherence to general market practice or recognised investment exchange (‘RIE’) rules.

Compliance with RIE rules will, however, be given ‘appropriateweight’ as part of the evaluation of potentially abusive transactions. In contrast, compliance with the Takeover Code andthe FCA price stabilising rules give an automatic safe harbour.

The administering authority and its employees should be particularly aware of potential offences as it should be noted that there is no need to prove intent as part of the evidence forabusive behaviour; ie, unintentional, accidental, abusive behaviour is still an offence. There is also a specific penalty in respect of requiring or encouraging a person to engage in behaviour which would amount to market abuse. If in doubt, you should consult the Compliance Officer.

If you are in any way unsure as to what might constitute marketabuse, you should contact the Compliance and Risk Team immediately.

1.7.2 Insider Dealing – The Criminal Justice Act 1993No employee of the administering authority or any closely connected person, who is in possession of 'inside information',may:

• deal in any 'price-affected' securities,

• encourage another person to deal in any 'price-affected' securities, or

• disclose the 'inside information' to another person (except in the proper performance of the function of his employment).

If the Fund or an individual is made an insider, neither the Fundnor the individual may trade in the security. Additionally, the individual should notify the Strategic Director of Pensions, theHead of Investments and the Compliance and Risk Manager.

Please note that 'securities' is very widely defined to include allequity, fixed income, derivative (including OTC) and commodityproducts.

COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015 15

A brief guide as to what constitutes ‘unpublished price-sensitiveinformation’ is contained in the following section of this chapter.When in doubt, employees must seek guidance from the Compliance and Risk Team.

Unpublished Price - Sensitive InformationPart V of the Criminal Justice Act 1993 states that unpublishedprice-sensitive 'inside information', is information which:

a) relates to particular securities or to a particular issuer or issuers of securities and not to securities or to issuers of securities generally,

b) is specific or precise,

c) has not been made 'public', and

d) if it were made 'public' would be likely to have a significant effect on the price or value of any securities.

Please note that although the inside information may be held inrespect of one security, other securities – eg, in the same sector– may be 'price-affected'.

'Price-affected securities' are those where the 'inside information', if made public, would be likely to have a significant effect on the price or value of the securities.

A person has information as an insider if:

a) it is, and they know that it is, inside information; and

b) they have it, and know that they have it, from an insidesource.

A person has information from an inside source if:

a) they have it through being a director, employee or shareholder of an issuer of securities; or

b) they have it through having access to the information byvirtue of their employment office or profession; or

c) the direct or indirect source of their information is a personwho falls within (a) above.

Information is made 'public' if:

a) it is published in accordance with the rules of a regulated market for the purpose of informing investors and their professional advisers;

b) it is contained in records which by virtue of any enactment areopen to inspection by the public;

c) it can be readily acquired by those likely to deal in any securities:

i) to which the information relates, or

ii) of an issuer to which the information relates; or

d) it is derived from information which has been made public. Information may be treated as made 'public' if or eventhough:

i) it can be acquired only by persons exercising diligence or expertise; or

ii) it is communicated to a section of the public and not to the public at large; or

iii) it can be acquired only by observation; or

iv)it is communicated only on payment of a fee; or

v) it is published only outside the UK.

In plain terms, therefore, the information must be:

• Unpublished: not available to the general public. It is sufficient that the information can be legitimately and readily obtained by any member of the public who wants it, eg, through a TOPIC screen.

• Price-sensitive: as well as being unavailable to the generalpublic the information must be of a nature which could, ifpublished, make a material difference to the market value of the securities.

If in any doubt as to whether information is unpublished andprice sensitive, seek guidance from the Compliance and RiskTeam.

16 COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015

1.8 Money Laundering

A summary of the key provisions of the Money Laundering Regulations 2007, the Joint Money Laundering Steering GroupGuidance (December 2007), the FCA Senior ManagementArrangements, Systems and Controls (SYSC) Sourcebook andthe administering authority’s own money laundering proceduresare included in Section 3.3 of this manual.

1.9 High Level Standards for Firms and Individuals

The following sections are drawn from the section of the FCA Handbook in High Level Standards on Senior ManagementArrangements, Systems and Controls (‘SYSC’).

1.9.1 Apportionment of ResponsibilitiesA firm must take reasonable care to maintain a clear and appropriate apportionment of significant responsibilities amongits directors and senior managers in such a way that:

a) it is clear who has which of those responsibilities; and

b) the business and affairs of the firm can be adequately monitored and controlled by the directors, relevant seniormanagers and the governing body of the firm.

(SYSC 2.1.1R)

1.9.2 RequirementA firm must appropriately allocate to one or more individuals, inaccordance with SYSC 2.1.4R, the functions of:

a) dealing with the apportionment of responsibilities under SYSC 2.1.1R; and

b) overseeing the establishment and maintenance of systemsand controls under SYSC 3.1.1R. (SYSC 2.1.3R)

1.9.3 SYSC 2.1.4R Table: Allocation of Functions (see SYSC 2.1.3R)

1.9.4 Recording the ApportionmentA firm must make a record of the arrangements it has made to satisfy SYSC 2.1.1R (apportionment) and SYSC 2.1.3R (allocation) and take reasonable care to keep this up to date.

This record must be retained for six years from the date onwhich it was superseded by a more up-to-date record. (SYSC 2.2.1R)

1.9.5 Systems and ControlsA firm must take reasonable care to establish and maintain suchsystems and controls as are appropriate to its business (SYSC3.1.1R).

The FCA provides no definitive guidance on what are appropriate systems and controls. FCA has indicated that some of the factors which will be of relevance are:

a) the nature, scale and complexity of the business;

b) the diversity of operations;

c) the volume and size of operations; and

d) the degree of risk involved.

The firm will have to demonstrate that it has made a proper assessment of these factors. There is, however, from the focusadopted in the Senior Management Arrangements, Systems and Controls Rules, a clear indication of the main areas that FCAexpects to be both covered by systems and controls (SYSC 3.2)and adequately documented.

3) Allocation to one or more individuals selected from this column is compulsory if there is no allocation to an individual in column 2, but is otherwise optional and additional:

The firm’s and its group’s directors and seniormanagers

1) Firm type 2) Allocation of both functions must be to the following individual, if any (see note):

Any other firm 1) the firm’s managing director (and all of themjointly, if more than one); or

2) a director or senior manager responsible for the overall management of:a) the group; orb) a group division within which some or all of

the firm’s regulated activities fall.

COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015 17

1.9.6 Senior Management Arrangements, Systems andControls Rules Coverage Relevant systems and controls are:

a) adequacy of management information;

b) business continuity;

c) clarity of reporting lines and delegation in the organisation;

d) documentation of business strategy;

e) maintenance of records;

f) adequacy of compliance reporting and monitoring;

g) systems and controls in relation to financial crime and money laundering;

h) suitability of remuneration policy;

i) recruitment and oversight of employees and agents;

j) Cabinet (Resources) panel and internal audit;

k) performance of risk assessment;

l) documentation and control of outsourcing relationships; and

m)management and disclosure of conflicts of interest.

1.10 Impact of the Markets in Financial Instruments Directive (‘MiFID’) on the Council

The MiFID is a Europe-wide directive, intended to further promote a single European market for wholesale and retailtransactions in financial instruments. The MiFID provides theframework for the establishment of a more level playing field inrespect of investment firms in Europe. It paves the way, potentially, for less local protectionism, more effective and wideruse of passporting of services, and the initiation of cross-borderpassporting of clearing and settlement services to create a moreunified capital market structure in Europe.

The MiFID was implemented in the UK on 1 November 2007with a number of significant changes to the FCA Handbook rulesand guidance. Some of the key provisions have been set outbelow.

1.10.1 Suitability and AppropriatenessThere is an increased onus on firms to demonstrate that theyhave satisfactorily assessed the ability of professional and retailcustomers to undertake transactions from the financial and trading track record of firms and individuals, including sources of available income, and their professional or educational background. The assessment of suitability depends on the client’sinvestment objectives and time horizon for investments, as wellas his knowledge and understanding of the particular productswhich the investment firm is intending to sell to him. While thereare relaxations for execution only business, this can only be

undertaken for the client if the investments concerned are non-complex (eg, non-financial derivative financial instruments),the service is initiated by the client (which appears to precludeanything other than very generalised marketing to potential customers), and the client is informed that certain protections donot apply.

1.10.2 Pre- and Post-Trade TransparencyRegulated markets have to make public all bid and offer pricesthat are advertised through their systems. Regulated marketshave to publish the price volume and time of transactions thathave taken place under their systems. They must make the details of these transactions public as close to real-time as possible. All types of trading in shares, whether on regulatedmarkets, multilateral trade facilities (‘MTFs’) or over-the-counterare subject to post-trade transparency obligations.

All investment firms trading outside a regulated market areobliged to make public the number of shares and the price of alltransactions, as well as where they took place. For retail clients,and for trades under “customary retail size”, firms are specificallyforbidden from trading at anything other than their firm quotewith clients, so price improvement is effectively forbidden. Thereis no restriction on the frequency with which the quote can beupdated. Currently nearly all trades (on-exchange and upstairstrades) are reported via recognised exchanges like the LondonStock Exchange. The MiFID allows firms conducting OTC tradesmore freedom in publication (eg, via the firm’s website).

1.10.3 Best ExecutionUnder the MiFID, investment firms need to adhere to a numberof new requirements, including ensuring that they obtain the bestpossible result for clients, as well as having an ‘order executionpolicy’ in place to allow this to be achieved. The ‘best possible result’ now includes, for non-private clients, a number of otherfactors beyond the execution price including costs, speed, likelihood of execution and settlement, size, nature or any otherconsideration relevant to the execution of an order.

1.11 Impact of the Capital Requirements Directive (‘CRD’)

The new Basel Accord was implemented within the EuropeanUnion via the Capital Requirements Directive (‘CRD’). The original Basel Accord, introduced with the intention ofstrengthening the soundness and stability of the internationalbanking system through the higher capital ratios that it required,was agreed in 1988 by the Basel Committee on Banking Supervision.

The CRD, which came into force on 1 January 2007, is a revision of the previous framework which introduced a modern, risk-sensitive prudential framework for credit institutions and investment firms across the EU, and was developed in line withthe revised Basel framework.

18 COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015

The CRD framework consists of four main components:

a) It contains an explicit measure for operational risk and includes more risk sensitive weightings against credit risk.

b) It reflects improvements in firms’ risk management practices,for example, by the introduction of an internal ratings basedapproach that allows firms to rely to a certain extent on theirown estimates of credit risk.

c) It provides incentives for firms to improve their risk management practices, with more risk sensitive risk areas as firms adopt more sophisticated approaches to risk management.

d) The new framework leaves the overall level of capital held byfirms collectively broadly unchanged.

The revised adequacy framework further ensures that the financial resources held by a firm are in line with the risk associated with the business profile and control environmentwithin the firm. Capital resources therefore consist of three ‘pillars’. Pillar 1 sets out the minimum capital requirements firms will have to meet for credit, market and operational risk.

Under pillar 2, firms and supervisors have to take a view onwhether a firm should hold additional capital against risks notcovered in pillar 1. The aim of pillar 3 is to improve market discipline by requiring firms to publish details of their risks, capital and risk management.

COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015 19

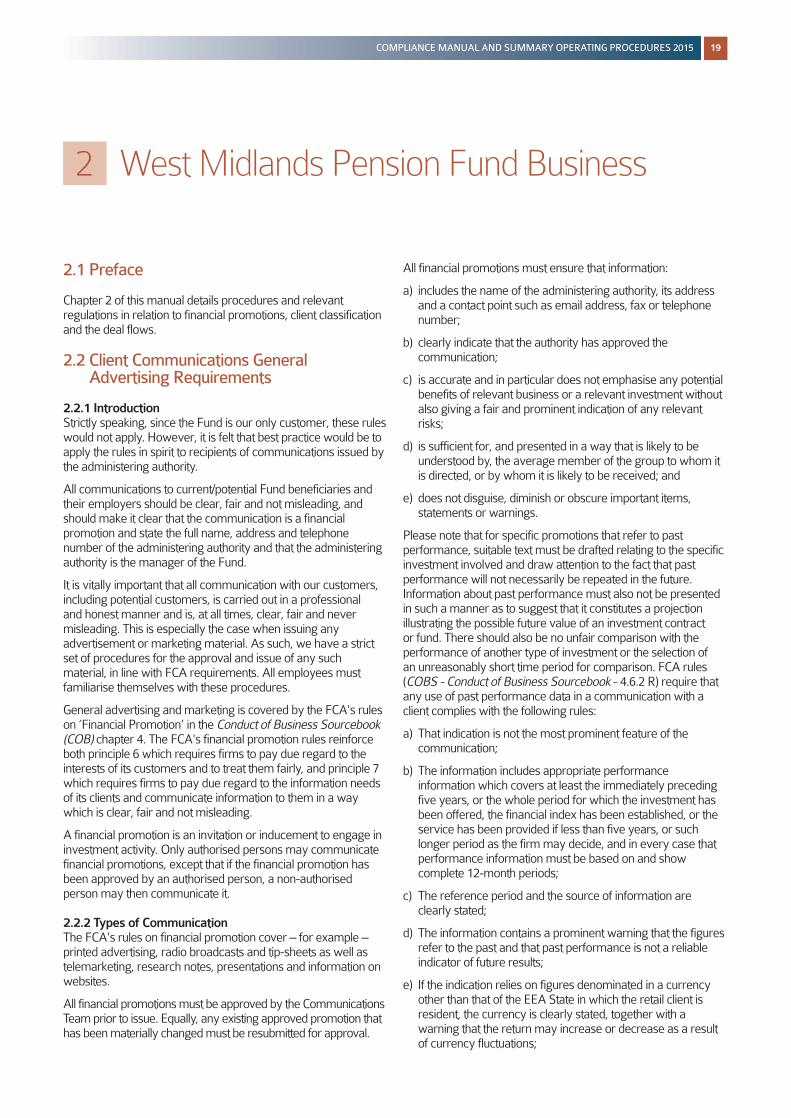

2 West Midlands Pension Fund Business

2.1 Preface

Chapter 2 of this manual details procedures and relevant regulations in relation to financial promotions, client classificationand the deal flows.

2.2 Client Communications General Advertising Requirements

2.2.1 IntroductionStrictly speaking, since the Fund is our only customer, these ruleswould not apply. However, it is felt that best practice would be toapply the rules in spirit to recipients of communications issued bythe administering authority.

All communications to current/potential Fund beneficiaries andtheir employers should be clear, fair and not misleading, andshould make it clear that the communication is a financial promotion and state the full name, address and telephone number of the administering authority and that the administeringauthority is the manager of the Fund.

It is vitally important that all communication with our customers,including potential customers, is carried out in a professional and honest manner and is, at all times, clear, fair and never misleading. This is especially the case when issuing any advertisement or marketing material. As such, we have a strictset of procedures for the approval and issue of any such material, in line with FCA requirements. All employees must familiarise themselves with these procedures.

General advertising and marketing is covered by the FCA's ruleson ‘Financial Promotion’ in the Conduct of Business Sourcebook(COB) chapter 4. The FCA's financial promotion rules reinforceboth principle 6 which requires firms to pay due regard to the interests of its customers and to treat them fairly, and principle 7which requires firms to pay due regard to the information needsof its clients and communicate information to them in a waywhich is clear, fair and not misleading.

A financial promotion is an invitation or inducement to engage ininvestment activity. Only authorised persons may communicatefinancial promotions, except that if the financial promotion hasbeen approved by an authorised person, a non-authorised person may then communicate it.

2.2.2 Types of CommunicationThe FCA's rules on financial promotion cover – for example – printed advertising, radio broadcasts and tip-sheets as well astelemarketing, research notes, presentations and information onwebsites.

All financial promotions must be approved by the CommunicationsTeam prior to issue. Equally, any existing approved promotion thathas been materially changed must be resubmitted for approval.

All financial promotions must ensure that information:

a) includes the name of the administering authority, its addressand a contact point such as email address, fax or telephonenumber;

b) clearly indicate that the authority has approved the communication;

c) is accurate and in particular does not emphasise any potentialbenefits of relevant business or a relevant investment withoutalso giving a fair and prominent indication of any relevantrisks;

d) is sufficient for, and presented in a way that is likely to be understood by, the average member of the group to whom itis directed, or by whom it is likely to be received; and

e) does not disguise, diminish or obscure important items, statements or warnings.

Please note that for specific promotions that refer to past performance, suitable text must be drafted relating to the specificinvestment involved and draw attention to the fact that past performance will not necessarily be repeated in the future. Information about past performance must also not be presentedin such a manner as to suggest that it constitutes a projection illustrating the possible future value of an investment contract or fund. There should also be no unfair comparison with the performance of another type of investment or the selection of an unreasonably short time period for comparison. FCA rules(COBS - Conduct of Business Sourcebook - 4.6.2 R) require thatany use of past performance data in a communication with aclient complies with the following rules:

a) That indication is not the most prominent feature of the communication;

b) The information includes appropriate performance information which covers at least the immediately precedingfive years, or the whole period for which the investment hasbeen offered, the financial index has been established, or theservice has been provided if less than five years, or suchlonger period as the firm may decide, and in every case thatperformance information must be based on and show complete 12-month periods;

c) The reference period and the source of information areclearly stated;

d) The information contains a prominent warning that the figuresrefer to the past and that past performance is not a reliable indicator of future results;

e) If the indication relies on figures denominated in a currencyother than that of the EEA State in which the retail client is resident, the currency is clearly stated, together with a warning that the return may increase or decrease as a resultof currency fluctuations;

20 COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015

f) If the indication is based on gross performance, the effect ofcommissions, fees or other charges are disclosed.

2.3 Charges

Before providing fund management services, we should disclosethe basis or amount of our charges and the nature or amount ofany other remuneration receivable by us and attributable to ourservices. Best practice would seem to be to apply this rule to potential beneficiaries and employers, even though they are notcustomers, since it is reasonable that contributors to a Fundshould know how the Fund is charged.

Therefore, when approaching potential employers/Fund beneficiaries, it should be explained to them that:

a) the Fund is charged for management services on a cost basis;

b) the remuneration of the fund managers is in accordance with the local authority's pay structure; and

c) the charges of external managers are a negotiated percentage of total funds managed by them.

Reasonable ChargesOur charges (and those of external managers) to the Fund mustnot be unreasonable in the circumstances. In order to complywith this, the following should be adhered to:

a) In-house charges to the Fund should always be actual costsincurred.

b) External managers either invoice the administering authority,or deduct charges at source, quarterly or half-yearly. Theircharges should be verified.

Most costs (including fund managers' charges) are met directlyfrom the Fund's bank account. The only exceptions are overheads (eg, for the building and salaries) which are initiallypaid out of the administering authority's account, and a proportion recharged to the Fund (except salaries of Fund employees which are recharged 100%) in accordance withagreed service levels.

The Strategic Director of Pensions should ensure that therecharges are reasonable.

2.4 Suitability

In deciding to effect any transaction for the Fund, we must havereasonable grounds for believing that such a transaction is suitable for the Fund's purpose having regard to the powers and provisions of the Local Government Pension Scheme Regulations 1995 and also we ensure that our external fundmanagers abide by this.

The aim of the Fund is to provide for past, present and futureemployees' pensions. As such the Fund is required to provide acombination of income and capital growth. It is vital that no unnecessary risks are taken with the assets of the Fund. Any investments, which are contrary to this policy, would automatically be regarded as unsuitable.

In assessing suitability of a particular transaction the appropriateinvestment manager must have regard to the following:

a) The powers and provisions contained in the Local Government Pension Scheme Regulations 1995 and asamended (see later);

b) The Fund’s Statement of Investment Principles, Funding Strategy Statement, Investment Strategy Statement and quarterly Tactical Asset Allocation Review;

c) The future marketability of the investment;

d) The risk involved in the investment. The level of risk is a relative term as it depends as much upon the amount of funds allocated to a particular type of investment and thespread of such allocations as the risk inherent in the investment itself;

e) His/her own skill and knowledge in that particular type of investment. (To facilitate this, the Strategic Director of Pensions is responsible for notifying each manager of the limits and scope of his/her discretion concerning such investments. If unsure as to the limit of his/her authorityhe/she should see the Strategic Director of Pensions immediately.) Details of the limits can be found in Appendix A.

A list of investment areas requiring specific approval from theStrategic Director of Pensions is found in Appendix B.

As a general principle, decisions as to whether an investment issuitable are based on independent research and reports received, and potentially require approval from the Strategic Director of Pensions. For each portfolio, this includes consideration of the following factors:

Quoted EquitiesThe Portfolio Manager's interpretation and knowledge of themarket gained from reliable sources and awareness of topics ofdiscussion among brokers generally, including the following:

a) Advice and research from one or more of the Fund's approved brokers that a particular transaction is recommended as suitable in the light of the Fund's policies;

b) Experience and reliability of a broker's analyst when assessing the reliability of broker's suggestions;

c) Existing/desired portfolio construction;

d) Data sources such as Bloomberg;

e) Political, economic and stock market conditions.

Fixed interest

a) Yields and prices, as shown by electronic market informationservices;

b) Research received and brokers' advice;

COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015 21

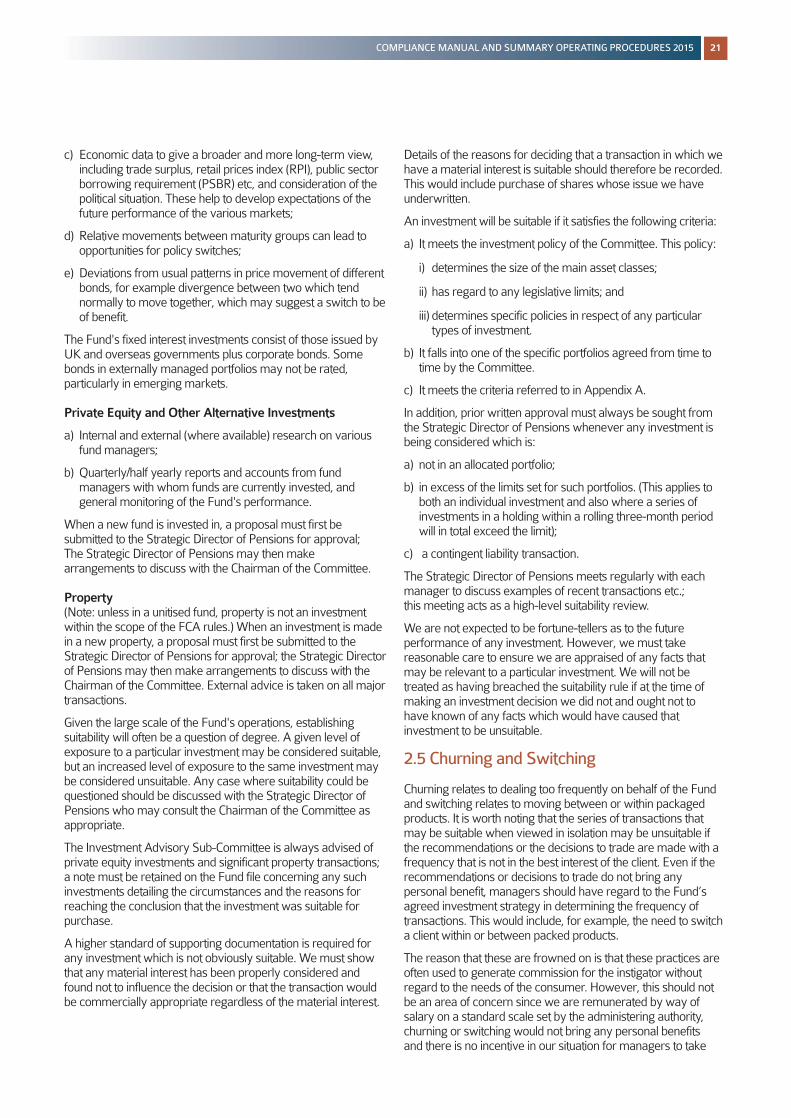

c) Economic data to give a broader and more long-term view,including trade surplus, retail prices index (RPI), public sectorborrowing requirement (PSBR) etc, and consideration of thepolitical situation. These help to develop expectations of the future performance of the various markets;

d) Relative movements between maturity groups can lead to opportunities for policy switches;

e) Deviations from usual patterns in price movement of differentbonds, for example divergence between two which tend normally to move together, which may suggest a switch to beof benefit.

The Fund's fixed interest investments consist of those issued byUK and overseas governments plus corporate bonds. Somebonds in externally managed portfolios may not be rated, particularly in emerging markets.

Private Equity and Other Alternative Investments

a) Internal and external (where available) research on variousfund managers;

b) Quarterly/half yearly reports and accounts from fund managers with whom funds are currently invested, and general monitoring of the Fund's performance.

When a new fund is invested in, a proposal must first be submitted to the Strategic Director of Pensions for approval; The Strategic Director of Pensions may then make arrangements to discuss with the Chairman of the Committee.

Property(Note: unless in a unitised fund, property is not an investmentwithin the scope of the FCA rules.) When an investment is madein a new property, a proposal must first be submitted to theStrategic Director of Pensions for approval; the Strategic Directorof Pensions may then make arrangements to discuss with theChairman of the Committee. External advice is taken on all majortransactions.

Given the large scale of the Fund's operations, establishing suitability will often be a question of degree. A given level of exposure to a particular investment may be considered suitable,but an increased level of exposure to the same investment maybe considered unsuitable. Any case where suitability could bequestioned should be discussed with the Strategic Director ofPensions who may consult the Chairman of the Committee asappropriate.

The Investment Advisory Sub-Committee is always advised ofprivate equity investments and significant property transactions;a note must be retained on the Fund file concerning any such investments detailing the circumstances and the reasons forreaching the conclusion that the investment was suitable for purchase.

A higher standard of supporting documentation is required forany investment which is not obviously suitable. We must showthat any material interest has been properly considered andfound not to influence the decision or that the transaction wouldbe commercially appropriate regardless of the material interest.

Details of the reasons for deciding that a transaction in which wehave a material interest is suitable should therefore be recorded.This would include purchase of shares whose issue we have underwritten.

An investment will be suitable if it satisfies the following criteria:

a) It meets the investment policy of the Committee. This policy:

i) determines the size of the main asset classes;

ii) has regard to any legislative limits; and

iii) determines specific policies in respect of any particular types of investment.

b) It falls into one of the specific portfolios agreed from time totime by the Committee.

c) It meets the criteria referred to in Appendix A.

In addition, prior written approval must always be sought fromthe Strategic Director of Pensions whenever any investment isbeing considered which is:

a) not in an allocated portfolio;

b) in excess of the limits set for such portfolios. (This applies toboth an individual investment and also where a series of investments in a holding within a rolling three-month periodwill in total exceed the limit);

c) a contingent liability transaction.

The Strategic Director of Pensions meets regularly with eachmanager to discuss examples of recent transactions etc.; this meeting acts as a high-level suitability review.

We are not expected to be fortune-tellers as to the future performance of any investment. However, we must take reasonable care to ensure we are appraised of any facts thatmay be relevant to a particular investment. We will not betreated as having breached the suitability rule if at the time ofmaking an investment decision we did not and ought not to have known of any facts which would have caused that investment to be unsuitable.

2.5 Churning and Switching

Churning relates to dealing too frequently on behalf of the Fundand switching relates to moving between or within packagedproducts. It is worth noting that the series of transactions thatmay be suitable when viewed in isolation may be unsuitable ifthe recommendations or the decisions to trade are made with afrequency that is not in the best interest of the client. Even if therecommendations or decisions to trade do not bring any personal benefit, managers should have regard to the Fund’sagreed investment strategy in determining the frequency oftransactions. This would include, for example, the need to switcha client within or between packed products.

The reason that these are frowned on is that these practices areoften used to generate commission for the instigator without regard to the needs of the consumer. However, this should notbe an area of concern since we are remunerated by way ofsalary on a standard scale set by the administering authority,churning or switching would not bring any personal benefits and there is no incentive in our situation for managers to take

22 COMPLIANCE MANUAL AND SUMMARY OPERATING PROCEDURES 2015

any decision that is not in the Fund's interest. At all times, managers should never the less be mindful of any conflicts of interest. Please see section 3.3 of this manual for further guidance on conflicts of interest.

2.6 Use of Dealing Commissions

The FCA rules on the use of dealing commissions (COBS 11.6)builds on the guidance on the acceptance of inducements bymanagers, and it’s dealt with further in section 3.2 of this manual.Managers should ensure that they comply with both this sectionand the rules on inducements at section 3.2.

The rules on the use of dealing commissions apply to a firm that acts as an investment manager when it executes customerorders that relate to:

a) shares; and

b) to the extent that they relate to shares:

i) warrants;

ii) certificates representing certain securities;

iii) options; and

iv)rights to or interests in investments of the nature referred to in (i) and (iii).

Use of Dealing Commission to Purchase Goods or Services A manager must not accept any goods or services in addition tothe execution of its customers’ orders if it:

a) executes its customer orders through a broker or another person;

b) passes on the broker’s or other person’s charges to its customers; and

c) is offered that good or service in return for the chargesreferred to in (b).

The prohibition above does not apply where:

a) the investment manager has reasonable grounds to be satisfied that the good or service received in return for thecharges in (b) above will reasonably assist the investmentmanager in the provision of its services to its customers, onwhose behalf the relevant customer orders are being executed;

b) the investment manager's receipt of that good or service inreturn for the charges in (b) above does not, and is not likelyto, impair compliance with the duty of the investment manager to act in the best interests of its customers; and

c) that good or service either:

i) is directly related to the execution of trades on behalf of the investment manager's customers; or

ii) amounts to the provision of substantive research.

An example of a good or service relating to the execution oftrades that the FCA does not regard as meeting the requirementsof the rule on use of dealing commission is post trade analytics.These would not meet the evidential criteria for a good or serviceto be directly related to the execution of trades.

Examples of goods or services that relate to the provision of research that the FCA does not regard as meeting the requirements of the rule on use of dealing commission includeprice feeds or historical price data that have not been analysed or manipulated in order to present the investment manager withmeaningful conclusions. These would not meet the evidential criteria for a good or service to amount to the provision of substantive research.

A manager intending to pass on to its customer or the Fund anycharges should always have regard to their duties under the customer or Fund’s best interest.

Disclosure and Record KeepingManagers that enter into arrangements involving dealing commissions must make adequate prior disclosure to customersand the Fund concerning the receipt of goods or services that directly relate to the execution of trades or amount to the provision of substantive research. This prior disclosure shouldform part of the summary form disclosure under the rule on inducements.

If a manager enters into arrangements in accordance with therule on use of dealing commission, he must in a timely mannermake adequate periodic disclosure to the relevant customers orthe Fund of the arrangements entered into.

Adequate prior and periodic disclosure must include details of thegoods or services that directly relate to the execution of tradesand, wherever appropriate, separately identify the details of thegoods or services that are an attributable amount to the provisionof substantive research.

In assessing the adequacy of prior and periodic disclosuresmade, the FCA will have regard to the extent to which the investment manager adopts disclosure standards developed by industry associations such as the Investment ManagementAssociation, the National Association of Pension Funds and theAssociation for Financial Markets in Europe.

Disclosure should be made at least once a year and a record ofeach prior and periodic disclosure to customers and the Fundmust be maintained for at least five years from the date on whichit is provided.

Detailed rules on the use of dealing commission can be found atCOBS 11.6 of the FCA Handbook. If a manager is in any doubtwhether or not a good or service can be accepted they shouldcontact the Compliance and Risk Team.