Embed Size (px)

DESCRIPTION

The report describes the requirements Interim Financial Statements and finally includes compliance analysis of interim financial statements of selected companies.

Citation preview

AbstractAn interim financial report is intended to provide an update of the last annual report. IAS 34 is

based on the presumption that interim financial statements are essentially an extension of

the previous annual financial statements to which anyone who reads the entity’s interim

report will also have access. An entity is required to apply the same accounting policies

in its interim financial report as in its immediately preceding annual financial statements.

This report includes the disclosure requirements for interim financial statements as per IAS 34.

This report includes the compliance analysis of interim financial statements of selected 4

companies with IAS 34. Two of them are from manufacturing sector, 1 from textile sector and

the other from fuel and power sector. The financial statements have been analyzed on the basis

of a check list consisting of significant disclosures requirements. We have found that the

financial statements did not include some useful requirements outlined in IAS 34. The financial

statements could have been more useful to the users in decision making if they include these

disclosures.

1.0 IntroductionInterim financial statements are financial reports covering a period of less than a financial year.

An interim statement is used to convey the performance of a company before the end of the year.

Unlike annual statements, interim statements do not have to be audited. Interim statements

increase communication between companies and the public, and provide investors with up-to-

date information between annual reporting periods. Therefore few of the notes to the annual

financial statements are repeated or updated in the interim report. Instead, the interim

notes include primarily an explanation of the events and changes that are significant to an

understanding of the changes in financial position and performance of the entity since the end of

the last annual reporting period. An entity that presents interim financial statements can choose

either to prepare them in the format of a complete set of financial statements or in the format a

set of condensed financial statements. IAS 34 Interim Financial Reporting also does not mandate

which entities are required to publish interim financial statements, how frequently they should

be produced or how soon interim reports should be released after each reporting date. The

standard however encourages, specifically, publicly traded entities to provide interim financial

reports at least as of the end of the first half of their financial year, not later than 60 days after the

interim reporting date.

In this report the interim financial statements of first two quarter of selected 4 companies have

been analyzed and compared to the disclosure requirements set by IAS 34. The companies are

ACI Limited, Agricultural Marketing Co. Ltd, Khulna Power Company Ltd and Apex Spinning

& Knitting Mills Limited.

2.0 Definition of Interim Financial StatementsInterim period is a financial reporting period shorter than a full financial year (most typically a

quarter or half-year). Interim financial report is a financial report that contains either a complete

or condensed set of financial statements for an interim period. Interim financial statements cover

information prepared and presented in accordance with an applicable financial reporting

framework that comprises either a complete or condensed set of financial statements covering a

period or periods less than one full year or covering a 12-month period ending on a date other

than the entity's fiscal year end. The International Accounting Standards Board (IASB) suggests

certain standards to be followed for interim statements. These include a series of condensed

statements covering the company's financial position, income, cash flows and changes in equity

along with notes of explanation. The IASB also suggests that companies should follow the same

guidelines in their interim statements as they use in preparing their annual reports, including

using the same accounting methods.

Important characteristics of interim financial statements are:

cover a financial reporting period shorter than a full financial year

apply the same accounting policies as in its immediately preceding annual financial

statements

IFRS does not require the preparation of interim financial statements.

required by Securities regulators, stock exchanges or other stake holders

notes include primarily an explanation of the events and changes that are

significant to an understanding of the changes in financial position and performance of

the entity since the end of the last annual reporting period

3.0 Minimum content and period of an interim financial reportThe minimum components specified for an interim financial report are: [IAS 34.8]

a condensed balance sheet (statement of financial position)

either (a) a condensed statement of comprehensive income or (b) a condensed statement

of comprehensive income and a condensed income statement

a condensed statement of changes in equity

a condensed statement of cash flows

selected explanatory notes

If a complete set of financial statements is published in the interim report, those financial

statements should be in full compliance with IFRSs. If the financial statements are condensed,

they should include, at a minimum, each of the headings and sub-totals included in the most

recent annual financial statements and the explanatory notes required by IAS 34. Additional line-

items or notes should be included if their omission would make the interim financial information

misleading. If the annual financial statements were consolidated (group) statements, the interim

statements should be group statements as well. The periods to be covered by the interim

financial statements are as follows:

balance sheet (statement of financial position) as of the end of the current interim period

and a comparative balance sheet as of the end of the immediately preceding financial

year

statement of comprehensive income (and income statement, if presented) for the current

interim period and cumulatively for the current financial year to date, with comparative

statements for the comparable interim periods (current and year-to-date) of the

immediately preceding financial year

statement of changes in equity cumulatively for the current financial year to date, with a

comparative statement for the comparable year-to-date period of the immediately

preceding financial year

statement of cash flows cumulatively for the current financial year to date, with a

comparative statement for the comparable year-to-date period of the immediately

preceding financial year

If the company's business is highly seasonal, IAS 34 encourages disclosure of financial

information for the latest 12 months, and comparative information for the prior 12-month period,

in addition to the interim period financial statements. [IAS 34.21]

4.0 Required note disclosuresThe explanatory notes required are designed to provide an explanation of events and transactions

that are significant to an understanding of the changes in financial position and performance of

the entity since the last annual reporting date. IAS 34 states a presumption that anyone who reads

an entity's interim report will also have access to its most recent annual report. Consequently,

IAS 34 avoids repeating annual disclosures in interim condensed reports.

4.1 Significant events and transactionsA reporting entity, as a consequence, only provides explanatory notes that are material to

an understanding of the current interim period. Disclosures that are available from the most

recent annual statements are not duplicated in the interim financial statements. The information

in the notes is normally presented on a financial year to date basis (i.e. they cover the period

from the beginning of the financial year until the end of the interim period). IAS 34

provides a list of examples that, if material would require disclosures. These are:

Write-down of inventories to net realisable value and the reversal of such a write-down

Recognition of a loss from the impairment of financial assets, property, plant and

equipment, intangible assets, or other assets, and the reversal of such an impairment loss

Reversal of any provisions for the costs of restructuring

Acquisitions and disposals of items of property, plant and equipment

Commitments for the purchase of property, plant and equipment

Litigation settlements

Corrections of prior period errors

Changes in the business or economic circumstances that affect the fair value of

the entity’s financial assets and financial liabilities, whether those assets or

liabilities are recognised at fair value or amortised cost

Loan default or breach of a loan agreement that has not been remedied on or before the

end of the reporting period

Related party transactions

Transfers between levels of the fair value hierarchy used in measuring the fair

value of financial instruments

Changes in the classification of financial assets as a result of a change in the purpose or

use of those assets

Changes in contingent liabilities or contingent assets.

For events or transactions that are considered to be significant to an understanding

of the interim financial statements, an explanation of the transaction is required

together with an update of the relevant information which was included in most recent

annual financial statements

4.2 Other required disclosuresThe information set out in IAS 34, if not disclosed elsewhere in the interim condensed

consolidated financial statements, is required:

A statement that the same accounting policies and methods of computation are

followed in the interim financial statements as compared with the most recent

annual financial statements or, if those policies or methods have been changed, a

description of the nature and effect of the change

Explanatory comments about the seasonality or cyclicality of interim operations

The nature and amount of items affecting assets, liabilities, equity, net income or

cash flows that are unusual because of their nature, size or incidence

The nature and amount of changes in estimates of amounts reported in prior interim

periods of the current financial year or changes in estimates of amounts reported in prior

financial years

Issues, repurchases and repayments of debt and equity securities

Events after the interim period that have not been reflected in the financial

statements for the interim period

The effect of changes in the composition of the entity during the interim period, including

business combinations, obtaining or losing control of subsidiaries and long-term

investments, restructurings, and discontinued operations. In the case of business

combinations, the entity shall disclose the information required by IFRS 3 Business

Combinations. The applicable disclosures for business combinations during the

interim period are defined in IFRS 3. Disclosures regarding business combinations

in prior years that result in adjustments in the current interim period are defined in

IFRS 3.

Dividends paid (aggregate or per share) separately for ordinary shares and other shares

The following segment information (disclosure of segment information is required

in an entity’s interim financial report only if IFRS 8 Operating Segments requires

that entity to disclose segment information in its annual financial statements):

Revenues from external customers, if included in the measure of segment profit or

loss reviewed by the chief operating decision maker or otherwise regularly

provided to the chief operating decision maker

Intersegment revenues, if included in the measure of segment profit or loss

reviewed by the chief operating decision maker or otherwise regularly provided

to the chief operating decision maker

A measure of segment profit or loss

Total assets for which there has been a material change from the amount

disclosed in the last annual financial statements

A description of differences from the last annual financial statements in the

basis of segmentation or in the basis of measurement of segment profit or loss

A reconciliation of the total of the reportable segments’ measures of profit or loss to

the entity’s profit or loss before tax expense (tax income) and discontinued

operations. However, if an entity allocates to reportable segments items such as

tax expense (tax income), the entity may reconcile the total of the segments’

measures of profit or loss to profit or loss after those items.

4.3 Other Important Issues

Accounting policies

The same accounting policies should be applied for interim reporting as are applied in the entity's

annual financial statements, except for accounting policy changes made after the date of the most

recent annual financial statements that are to be reflected in the next annual financial statements.

A key provision of IAS 34 is that an entity should use the same accounting policy throughout a

single financial year. If a decision is made to change a policy mid-year, the change is

implemented retrospectively, and previously reported interim data is restated. [IAS 34.43]

Measurement

Measurements for interim reporting purposes should be made on a year-to-date basis, so that the

frequency of the entity's reporting does not affect the measurement of its annual results. Several

important measurement points:

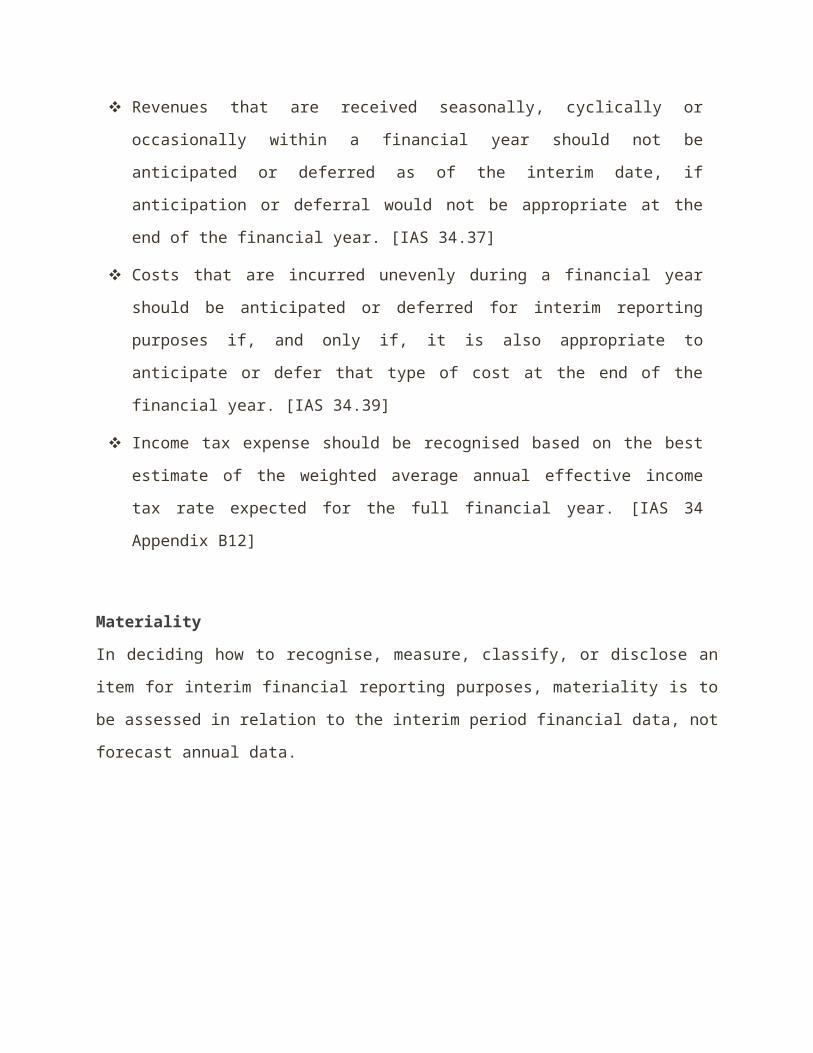

Revenues that are received seasonally, cyclically or occasionally within a financial year

should not be anticipated or deferred as of the interim date, if anticipation or deferral

would not be appropriate at the end of the financial year. [IAS 34.37]

Costs that are incurred unevenly during a financial year should be anticipated or deferred

for interim reporting purposes if, and only if, it is also appropriate to anticipate or defer

that type of cost at the end of the financial year. [IAS 34.39]

Income tax expense should be recognised based on the best estimate of the weighted

average annual effective income tax rate expected for the full financial year. [IAS 34

Appendix B12]

Materiality

In deciding how to recognise, measure, classify, or disclose an item for interim financial

reporting purposes, materiality is to be assessed in relation to the interim period financial data,

not forecast annual data.

5.0 Compliance Analysis of selected financial statements with IAS 34The interim financial statements should follow the requirements mentioned in IAS 34 and should

include certain note disclosures. In this report the compliance of the interim financial statements

with IAS 34 has been analyzed in respect of following points:

Significant Requirements or Note Disclosures for Interim Financial Statements

A statement that entity’s interim financial report is in compliance with IAS 34

Inclusion of at least each of the headings and subtotals that were included in their

most recent annual financial statements

Comparative information should be presented in the interim financial statements unless

the current period is the entity’s first period of operations.

The interim statement of financial position is required to include comparative

information i.e. the information of the current interim period and the comparable

interim periods

Inclusion of income and expenses of the current interim period and the

comparable interim periods in the interim Statement of comprehensive income

Inclusion of cash flows of the current interim period and the comparable

interim periods in the interim Statement of cash flows

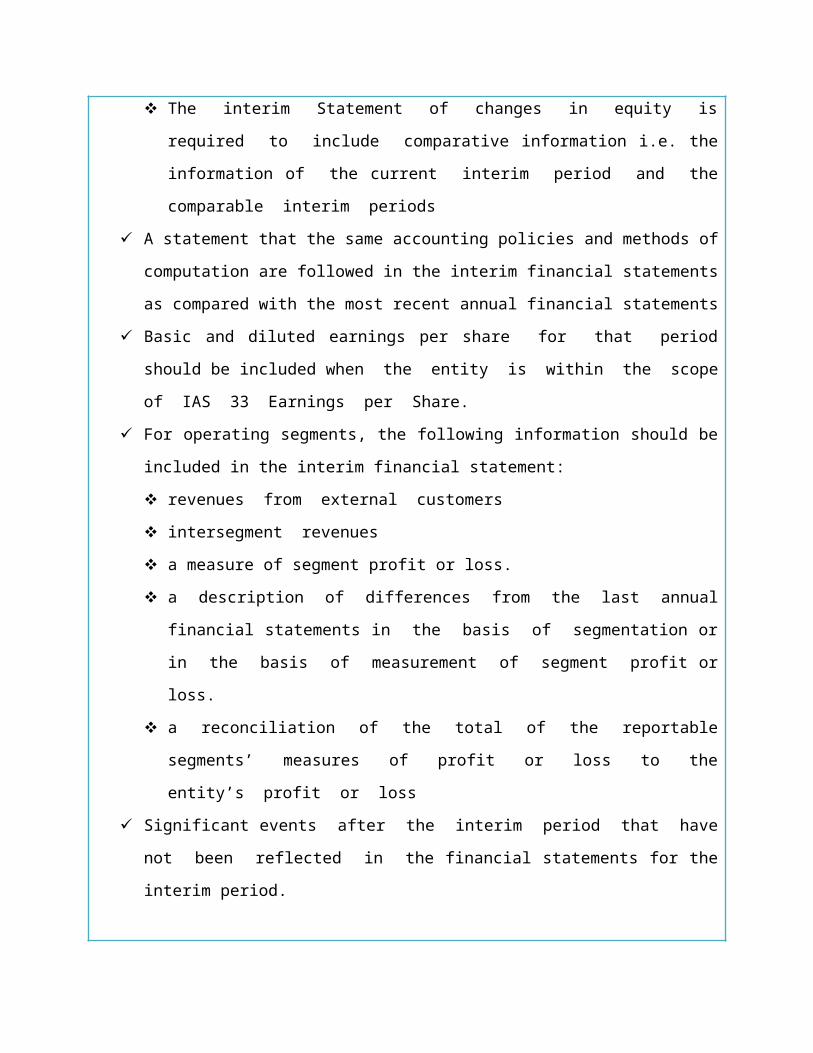

The interim Statement of changes in equity is required to include comparative

information i.e. the information of the current interim period and the comparable

interim periods

A statement that the same accounting policies and methods of computation are followed

in the interim financial statements as compared with the most recent annual financial

statements

Basic and diluted earnings per share for that period should be included when the

entity is within the scope of IAS 33 Earnings per Share.

For operating segments, the following information should be included in the interim

financial statement:

revenues from external customers

intersegment revenues

a measure of segment profit or loss.

a description of differences from the last annual financial statements in the basis of

segmentation or in the basis of measurement of segment profit or loss.

a reconciliation of the total of the reportable segments’ measures of profit or

loss to the entity’s profit or loss

Significant events after the interim period that have not been reflected in the

financial statements for the interim period.

In this report, interim financial statements of 4 companies have been analyzed to have an idea of

reporting in the real financial statements and to determine whether they have been prepared in

compliance with IAS 34. Interim financial statements of first two quarters have been taken into

consideration in this report. Interim financial statements of the following companies have been

considered:

a) ACI Limited

b) Agricultural Marketing Co. Ltd.

c) Khulna Power Company Ltd

d) Apex Spinning & Knitting Mills Limited.

Analysis of the interim financial statements of the above mentioned companies has been

discussed in the next sections.

5.1 ACI Limited

The two following interim financial statements of ACI Limited have been considered:

1. Interim Financial Statements of 1st Quarter Ended at 31st March, 2013

2. Interim Financial Statements of half year/quarter ended 30th June, 2013

The unaudited financial statements include the Statement of Financial Position, Statement of

Comprehensive Income, Statement of Cash Flow, Statement of Changes in Equity and selected

explanatory notes. Financial Statements also include consolidated statements. We have found the

following compliance and inconsistencies in the financial statements:

Compliances Inconsistencies

A statement that entity’s interim

financial report is in compliance with

the applicable accounting policies

Inclusion of at least each of the

headings and subtotals that were

included in their most recent annual

financial statements

Comparative information presented in

the interim financial statements unless

the current period is the entity’s first

period of operations.

Basic earnings per share for the

period

For operating segments:

revenues from external customers

intersegment revenues

a measure of segment profit or loss.

There is no statement that the same

accounting policies and methods of

computation are followed in the interim

financial statements as compared with

the most recent annual financial

statements

There is no disclosure regarding

significant events after the interim

period that have not been reflected

in the financial statements for the

interim period.

No Disclosure about the treatment of

tax

No Disclosure regarding related party

transactions

For operating segments, there is no

reconciliation of the total of the

reportable segments’ measures of

profit or loss to the entity’s profit

or loss

5.2 Agricultural Marketing Co. Limited (Pran)

Interim financial statements of the 1st quarter covering a period of July, 2013 to September, 2013

have been analyzed for determining whether they have been prepared in compliance with IAS

34. The unaudited financial statements include the Balance Sheet, Income Statement, Cash Flow

Statement, Statement of Changes in Equity and selected explanatory notes.

We have found the following compliance and inconsistencies in the financial statements:

Compliances Inconsistencies

Inclusion of at least each of the

headings and subtotals that were

included in their most recent annual

financial statements

Comparative information presented in

the interim financial statements unless

the current period is the entity’s first

period of operations.

Basic and diluted earnings per share

for the period

Disclosure about the treatment of tax

There is no statement that the same

accounting policies and methods of

computation are followed in the interim

financial statements as compared with

the most recent annual financial

statements

A statement that entity’s interim

financial report is in compliance with

the applicable accounting policies

There is no disclosure regarding

significant events after the interim

period that have not been reflected

in the financial statements for the

interim period.

No Disclosure regarding related party

transactions

No disclosure regarding operating

segments

5.3 Khulna Power Company Ltd

The two following interim financial statements of Khulna Power Company Ltd have been

considered:

1. Interim Financial Statements of 1st Quarter Ended 31st March, 2013

2. Interim Financial Statements of half year/quarter ended 30th June, 2013

The unaudited financial statements include the Statement of Financial Position, Statement of

Comprehensive Income, Statement of Cash Flow, Statement of Changes in Equity and selected

explanatory notes. Financial Statements also include consolidated statements.

We have found the following compliance and inconsistencies in the financial statements:

Compliances Inconsistencies

A statement that entity’s interim

financial report is in compliance with

the applicable accounting policies

A statement that the same accounting

policies and methods of computation

are followed in the interim financial

statements as compared with the most

recent annual financial statements

Inclusion of at least each of the

headings and subtotals that were

included in their most recent annual

financial statements

Comparative information in the interim

financial statements

Basic earnings per share for that

period

There is no disclosure regarding

significant events after the interim

period that have not been reflected

in the financial statements for the

interim period.

No Disclosure regarding related party

transactions

5.4 Apex Spinning & Knitting Mills Limited

The two following interim financial statements of Khulna Power Company Ltd have been

considered:

1. Interim Financial Statements of 1st Quarter 30th June, 2013

2. Interim Financial Statements of half year/quarter ended 30th September, 2013

The unaudited financial statements include the Statement of Financial Position, Statement of

Comprehensive Income, Statement of Cash Flow, Statement of Changes in Equity and selected

explanatory notes. Financial Statements also include consolidated statements. We have found the

following compliance and inconsistencies in the financial statements:

Compliances Inconsistency

Inclusion of at least each of the

headings and subtotals that were

included in their most recent

annual financial statements

Comparative information

presented in the interim financial

statements unless the current

period is the entity’s first period of

operations.

Basic earnings per share for the

period

No statement that entity’s interim financial

report is in compliance with the applicable

accounting policies

There is no statement that the same

accounting policies and methods of

computation are followed in the interim

financial statements as compared with the

most recent annual financial statements

There is no disclosure regarding significant

events after the interim period that have

not been reflected in the financial

statements for the interim period.

No Disclosure about the treatment of tax

No Disclosure regarding related party

transactions

No Disclosure regarding operating segment

6.0 FindingsInterim financial report is a financial report that contains either a complete or condensed set of

financial statements for an interim period. IFRS does not require the preparation of interim

financial statements. The standard however encourages, specifically, publicly traded entities to

provide interim financial reports at least as of the end of the first half of their financial year, not

later than 60 days after the interim reporting date. The interim financial statements should follow

the requirements mentioned in IAS 34 and should include certain note disclosures. In this report,

interim financial statements of 4 companies have been analyzed to identify their compliance with

IAS 34. After analyzing these interim financial statements, we have found that there are some

inconsistencies in the statements. Overall findings have been shown in the given table:

Requirements ACI

Limited

AMCL (Pran)

Khulna Power Company Ltd

Apex Spinning & Knitting Mills Ltd.

A statement that entity’s interim financial report

is in compliance with IAS 34

Inclusion of at least each of the headings and

subtotals that were included in their most

recent annual financial statements

Comparative information in the financial

statements

A statement that the same accounting policies

and methods of computation are followed as

compared with the most recent annual financial

statements

Basic earnings per share

Disclosures regarding operating segments

Disclosures regarding Significant events after

the interim period

Disclosures regarding treatment of tax

Disclosure regarding related party transactions

All of the financial statements didn’t follow the following:

A statement that the same accounting policies and methods of computation are followed

as compared with the most recent annual financial statements

Disclosures regarding Significant events after the interim period

Disclosure regarding related party transactions

All of the financial statements have followed the following:

Inclusion of at least each of the headings and subtotals that were included in their

most recent annual financial statements

Comparative information in the financial statements

Basic earnings per share

Though the financial statements didn’t include some important disclosures, they have followed

significant requirements set by IAS 34. The financial statements could have been more useful to

the users if they include them. But they are not so significant that their omission could lead to

influence the judgment of the users.

7.0 ConclusionAn interim statement is used to convey the performance of a company before the end of the year.

This report can increase communication between companies and the public, and provide

investors with up-to-date information between annual reporting periods. An entity is required

to apply the same accounting policies in its interim financial report as in its immediately

preceding annual financial statements. This report includes few of the notes to the annual

financial statements are repeated or updated in the interim report. Instead, the interim

notes include primarily an explanation of the events and changes that are significant to an

understanding of the changes in financial position and performance of the entity since the end of

the last annual reporting period. This report includes the compliance analysis of interim financial

statements of selected 4 companies with IAS 34. The financial statements include most of the

disclosures which can influence the decisions of users in making economic decisions.

ReferencesACI Ltd, 1st Quarter Ended Report

ACI Ltd, Half Yearly Report

Agricultural Marketing Co. Limited, 1st Quarter Report

Apex Spinning & Knitting Mills Limited, 1st Quarter Ended Report

Apex Spinning & Knitting Mills Limited, Half Yearly Report

Khulna Power Company Ltd, 1st Quarter Report

Khulna Power Company Ltd, Half Yearly Report

![[2011]Consolidated Interim Financial Statements](https://img.pdfslide.us/doc/110x75/5695d4801a28ab9b02a1aa9a/2011consolidated-interim-financial-statements.jpg)

![[2012]Consolidated Interim Financial Statements](https://img.pdfslide.us/doc/110x75/55cf9a69550346d033a19aa5/2012consolidated-interim-financial-statements.jpg)