Embed Size (px)

Citation preview

Completing the Accounting Cycle for a Service Business: Closing Entries and the Post-Closing Trial Balance

© Paradigm Publishing, Inc. 1

Chapter 5

1. Explain the purpose of the closing process.

2. Journalize and post closing entries.

3. Prepare a post-closing trial balance.

© Paradigm Publishing, Inc. 2

Learning Objectives

© Paradigm Publishing, Inc. 3

Explain the purpose of the closing process

Learning Objective 1

Temporary AccountsTemporary Accounts

Revenue and expense accounts and the Revenue and expense accounts and the owner’s owner’s drawing accountdrawing account

Used to show changes in owner’s equity Used to show changes in owner’s equity during a during a single accounting periodsingle accounting period

Closing ProcessClosing Process: The process of transferring the : The process of transferring the balances of the temporary accounts to the owner’s balances of the temporary accounts to the owner’s capital accountcapital account

Closing EntriesClosing Entries: Entries necessary to accomplish : Entries necessary to accomplish the closing processthe closing process

© Paradigm Publishing, Inc. 4

1.1. To reduce the balance of temporary owner’s To reduce the balance of temporary owner’s equity accounts to zero and thus make the equity accounts to zero and thus make the accounts ready for entries in the next accounting accounts ready for entries in the next accounting period.period.

2.2. To update the balance of the owner’s capital To update the balance of the owner’s capital account.account.

© Paradigm Publishing, Inc. 5

© Paradigm Publishing, Inc. 6

Journalize and post closing entries

Learning Objective 2

1.1. Close the balance of each revenue account to the Close the balance of each revenue account to the Income Summary account.Income Summary account.

2.2. Close the balance of each expense account to Close the balance of each expense account to Income Summary.Income Summary.

3.3. Close the balance of Income Summary to the Close the balance of Income Summary to the owner’s capital account.owner’s capital account.

4.4. Close the balance of the owner’s drawing account Close the balance of the owner’s drawing account directly to the owner’s capital account.directly to the owner’s capital account.

© Paradigm Publishing, Inc. 7

A clearing account used to summarize the balances A clearing account used to summarize the balances of revenue and expense accountsof revenue and expense accounts

Used only at the end of an accounting periodUsed only at the end of an accounting period

Opened and closed during the closing processOpened and closed during the closing process

Does not have a normal balance as do other Does not have a normal balance as do other accountsaccounts

Will never appear on the financial statementsWill never appear on the financial statements

© Paradigm Publishing, Inc. 8

© Paradigm Publishing, Inc. 9

Quick Check

The balance in the Income Summary account The balance in the Income Summary account

a.a. appears on the income statement.appears on the income statement.

b.b. appears on the balance sheet.appears on the balance sheet.

c.c. appears on the income statement and the appears on the income statement and the statement of owner’s equity.statement of owner’s equity.

d.d. does not appear on any financial statement.does not appear on any financial statement.

e.e. appears on the balance sheet and the statement appears on the balance sheet and the statement of owner’s equity.of owner’s equity.

We’ll use the numbers on the work sheet to We’ll use the numbers on the work sheet to demonstrate the closing entries.demonstrate the closing entries.

© Paradigm Publishing, Inc. 10

© Paradigm Publishing, Inc. 11

To close an account, we must make an entry that To close an account, we must make an entry that will reduce the balance of the account the zero.will reduce the balance of the account the zero.

Thus, a revenue account must be debited for the Thus, a revenue account must be debited for the amount of its credit balance.amount of its credit balance.

The credit will be to the Income Summary account.The credit will be to the Income Summary account.

© Paradigm Publishing, Inc. 12

© Paradigm Publishing, Inc. 13

Quick Check

When closing a revenue account, theWhen closing a revenue account, the

a.a. revenue account is credited for its balance.revenue account is credited for its balance.

b.b. owner’s capital account is credited for the balance owner’s capital account is credited for the balance of the revenue account.of the revenue account.

c.c. owner’s drawing account is credited for the balance owner’s drawing account is credited for the balance of the revenue account.of the revenue account.

d.d. Income Summary account is credited for the Income Summary account is credited for the balance of the revenue account.balance of the revenue account.

e.e. Income Summary account is debited for the Income Summary account is debited for the balance of the revenue account.balance of the revenue account.

An expense account An expense account must be credited for must be credited for the amount of its debit the amount of its debit balance.balance.

The debit will be to the The debit will be to the Income Summary Income Summary account.account.

© Paradigm Publishing, Inc. 14

© Paradigm Publishing, Inc. 15

Quick Check

When closing an expense account theWhen closing an expense account the

a.a. expense account is credited for its balance.expense account is credited for its balance.

b.b. owner’s capital account is credited for the balance owner’s capital account is credited for the balance of the expense account.of the expense account.

c.c. owner’s drawing account is credited for the owner’s drawing account is credited for the balance of the expense account.balance of the expense account.

d.d. Income Summary account is credited for the Income Summary account is credited for the balance of the expense account.balance of the expense account.

e.e. owner’s capital account is debited for the balance owner’s capital account is debited for the balance of the expense account.of the expense account.

Compute the balance in the Income Summary account.Compute the balance in the Income Summary account.

The balance in the Income Summary account will The balance in the Income Summary account will always reflect the amount of net income or net loss.always reflect the amount of net income or net loss.

Assuming a net income, it is transferred to the credit Assuming a net income, it is transferred to the credit side of the owner’s capital account.side of the owner’s capital account.

© Paradigm Publishing, Inc. 16

The Income Summary account is debited for its The Income Summary account is debited for its balance to close it.balance to close it.

© Paradigm Publishing, Inc. 17

© Paradigm Publishing, Inc. 18

Quick Check

When closing the Income Summary account, When closing the Income Summary account, assuming a net income theassuming a net income the

a.a. Income Summary account is credited for its Income Summary account is credited for its balance.balance.

b.b. owner’s capital account is credited for the amount owner’s capital account is credited for the amount of the net income.of the net income.

c.c. owner’s capital account is debited for the amount of owner’s capital account is debited for the amount of the net income.the net income.

d.d. owner’s drawing account is credited for the amount owner’s drawing account is credited for the amount of the net income.of the net income.

e.e. owner’s drawing account is debited for the amount owner’s drawing account is debited for the amount of the net income.of the net income.

The balance of the owner’s drawing account does not The balance of the owner’s drawing account does not enter into the determination of net income or net enter into the determination of net income or net loss.loss.

Therefore, the drawing account is not closed to the Therefore, the drawing account is not closed to the Income Summary account.Income Summary account.

Instead, it is closing directly into the owner’s capital Instead, it is closing directly into the owner’s capital account.account.

The drawing account has a debit balance and is The drawing account has a debit balance and is credited to close it.credited to close it.

© Paradigm Publishing, Inc. 19

The owner’s capital account is debited since drawing The owner’s capital account is debited since drawing decreases the owner’s capital.decreases the owner’s capital.

© Paradigm Publishing, Inc. 20

© Paradigm Publishing, Inc. 21

Quick Check

When closing the owner’s drawing account, theWhen closing the owner’s drawing account, the

a.a. owner’s capital account is debited for the amount owner’s capital account is debited for the amount of net income.of net income.

b.b. owner’s capital account is credited for the balance owner’s capital account is credited for the balance of the owner’s drawing account.of the owner’s drawing account.

c.c. owner’s drawing account is credited for its owner’s drawing account is credited for its balance.balance.

d.d. Income Summary account is credited for the Income Summary account is credited for the balance of the owner’s drawing account.balance of the owner’s drawing account.

e.e. Income Summary account is debited for the Income Summary account is debited for the balance of the owner’s drawing account.balance of the owner’s drawing account.

The balance in the owner’s capital account after all The balance in the owner’s capital account after all closing entries have been prepared will be the updated closing entries have been prepared will be the updated balance appearing on the balance sheet and the post-balance appearing on the balance sheet and the post-closing balance.closing balance.

© Paradigm Publishing, Inc. 22

© Paradigm Publishing, Inc. 23

Quick Check

The owner’s capital account isThe owner’s capital account is

a.a. increased by the balance in the owner’s drawing increased by the balance in the owner’s drawing account.account.

b.b. increased by the amount of net loss.increased by the amount of net loss.

c.c. decreased by the balance in the owner’s drawing decreased by the balance in the owner’s drawing account.account.

d.d. closed at the end of each accounting period.closed at the end of each accounting period.

e.e. decreased by the amount of net income.decreased by the amount of net income.

Temporary AccountsTemporary Accounts

All revenue accountsAll revenue accounts

All expense accountsAll expense accounts

All drawing accountsAll drawing accounts

Close at the end of the accounting periodClose at the end of the accounting period

© Paradigm Publishing, Inc. 24

© Paradigm Publishing, Inc. 25

Permanent AccountsPermanent Accounts

All balance sheet accountsAll balance sheet accounts

Do not close at the end of the accounting periodDo not close at the end of the accounting period

© Paradigm Publishing, Inc. 26

© Paradigm Publishing, Inc. 27

Quick Check

Select the correct statement:Select the correct statement:

a.a. Revenues, assets, and expenses are permanent Revenues, assets, and expenses are permanent accounts.accounts.

b.b. Liabilities and the owner’s capital account are Liabilities and the owner’s capital account are temporary accounts.temporary accounts.

c.c. Revenues, expenses, and the owner’s drawing Revenues, expenses, and the owner’s drawing account are temporary accounts.account are temporary accounts.

d.d. Assets, liabilities, and the owner’s drawing account Assets, liabilities, and the owner’s drawing account are temporary accounts.are temporary accounts.

e.e. Expenses and liabilities are permanent accounts.Expenses and liabilities are permanent accounts.

© Paradigm Publishing, Inc. 28

Example

Assume the Service Revenue account has an ending balance of $3,000.Prepare the closing entry.

© Paradigm Publishing, Inc. 29

General Journal

Date Account Title P.R. Debit Credit

20X1Dec.

31 Service Revenue 3,000

Income Summary 3,000

Example

Assume Salaries Expense has an ending balance of $1,200.Prepare the closing entry.

© Paradigm Publishing, Inc. 30

General Journal

Date Account Title P.R. Debit Credit

20X1Dec.

31 Income Summary 1,200

Salaries Expense 1,200

Example

Assume net income for the current period is $1,800 for June Delugas Interiors.Prepare the closing entry.

© Paradigm Publishing, Inc. 31

General Journal

Date Account Title P.R. Debit Credit

20X1Dec.

31 Income Summary 1,800

June Delugas, Capital 1,800

Example

Assume June Delugas, Drawing, has an ending balance of $500.Prepare the closing entry.

© Paradigm Publishing, Inc. 32

General Journal

Date Account Title P.R. Debit Credit

20X1Dec.

31 June Delugas, Capital 500

June Delugas, Drawing 500

1.1. Close the balance of revenue accounts to Income Close the balance of revenue accounts to Income Summary.Summary.

2.2. Close the balance of expense accounts to Income Close the balance of expense accounts to Income Summary.Summary.

3.3. Close the balance of Income Summary to the Close the balance of Income Summary to the owner’s capital account.owner’s capital account.

4.4. Close the balance of the owner’s drawing account Close the balance of the owner’s drawing account to the owner’s capital account.to the owner’s capital account.

© Paradigm Publishing, Inc. 33

© Paradigm Publishing, Inc. 34

Review Quiz 5-1

Close the temporary accounts. Close the temporary accounts.

© Paradigm Publishing, Inc. 35

© Paradigm Publishing, Inc. 36

Review Quiz 5-1

The closing entries are journalized.The closing entries are journalized.

© Paradigm Publishing, Inc. 37

Review Quiz 5-1

© Paradigm Publishing, Inc. 38

Review Quiz 5-1

After closing entries have been journalized, the next After closing entries have been journalized, the next step in the accounting cycle is to post these entries step in the accounting cycle is to post these entries from the general ledger to the general journalfrom the general ledger to the general journal

After posting has occurredAfter posting has occurred

The permanent accounts will have up-to-date The permanent accounts will have up-to-date balancesbalances

The temporary accounts will have zero balancesThe temporary accounts will have zero balances

© Paradigm Publishing, Inc. 39

Review Quiz 5-2

T-Account BalancesT-Account Balances

© Paradigm Publishing, Inc. 40

Review Quiz 5-2

The temporary accounts are journalized.The temporary accounts are journalized.

© Paradigm Publishing, Inc. 41

© Paradigm Publishing, Inc. 42

Prepare a post-closing trial balance

Learning Objective 3

The final step in the accounting cycleThe final step in the accounting cycle

Ensures the ledger will be in balance at the start of Ensures the ledger will be in balance at the start of the next account periodthe next account period

Only permanent accounts appear on the post-Only permanent accounts appear on the post-closing trial balance, since the balances of all closing trial balance, since the balances of all temporary accounts have been reduced to zerotemporary accounts have been reduced to zero

© Paradigm Publishing, Inc. 43

© Paradigm Publishing, Inc. 44

© Paradigm Publishing, Inc. 45

Quick Check

Select the correct statement:Select the correct statement:

a.a. The post-closing trial balance will list revenues The post-closing trial balance will list revenues and assets.and assets.

b.b. The post-closing trial balance will list assets and The post-closing trial balance will list assets and the owner’s capital account.the owner’s capital account.

c.c. The post-closing trial balance will list expenses The post-closing trial balance will list expenses and assets.and assets.

d.d. The post-closing trial balance will list the owner’s The post-closing trial balance will list the owner’s drawing account and the owner’s capital account.drawing account and the owner’s capital account.

e.e. The post-closing trial balance will list expenses, The post-closing trial balance will list expenses, revenues, and liabilities.revenues, and liabilities.

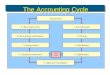

1.1. Analyze transactions from source Analyze transactions from source documentsdocuments

2.2. Record transactions in a journalRecord transactions in a journal

3.3. Post from the journal to the ledgerPost from the journal to the ledger

4.4. Prepare a trial balance of the ledgerPrepare a trial balance of the ledger

© Paradigm Publishing, Inc. 46

During the accounting period

5.5. Determine needed adjustmentsDetermine needed adjustments

6.6. Prepare a work sheetPrepare a work sheet

7.7. Prepare financial statements from a Prepare financial statements from a completed work sheetcompleted work sheet

8.8. Journalize and post adjusting entriesJournalize and post adjusting entries

9.9. Journalize and post closing entriesJournalize and post closing entries

10.10.Prepare a post-closing trial balancePrepare a post-closing trial balance© Paradigm Publishing, Inc. 47

At the end of the accounting period

Any period of time covering the complete Any period of time covering the complete accounting cycle, from the analysis of transactions accounting cycle, from the analysis of transactions to the post-closing trial balance.to the post-closing trial balance.

A fiscal period consisting of 12 consecutive months A fiscal period consisting of 12 consecutive months is a fiscal year.is a fiscal year.

A fiscal year does not necessarily coincide with the A fiscal year does not necessarily coincide with the calendar year.calendar year.

A fiscal year ending at a business’s lowest point of A fiscal year ending at a business’s lowest point of activity is referred to as a activity is referred to as a natural business yearnatural business year..

© Paradigm Publishing, Inc. 48

Accrual Basis of AccountingAccrual Basis of Accounting

The basis of accounting that requires that revenue is The basis of accounting that requires that revenue is recorded when earned, no matter when cash is recorded when earned, no matter when cash is received, and that expenses are recorded when received, and that expenses are recorded when incurred, no matter when cash is paid.incurred, no matter when cash is paid.

Cash Basis of AccountingCash Basis of Accounting

The basis of accounting where revenue is recorded The basis of accounting where revenue is recorded only when cash is received, and expenses are only when cash is received, and expenses are recorded only when cash is paid.recorded only when cash is paid.

The cash basis of accounting is not in accordance The cash basis of accounting is not in accordance with GAAP.with GAAP.

© Paradigm Publishing, Inc. 49

© Paradigm Publishing, Inc. 50

Focus on Ethics

© Paradigm Publishing, Inc. 51

What pressures might lead executives to try to illegally manipulate a company’s earnings?

Refer to the Focus on Ethics box on pages 191-Refer to the Focus on Ethics box on pages 191-192 in your text.192 in your text.

© Paradigm Publishing, Inc. 52

Steps in the Steps in the Accounting Cycle Accounting Cycle for a Service for a Service BusinessBusiness

Joining the Pieces