Embed Size (px)

Citation preview

12 September 2017

Colombo, Sri Lanka

Proprietary and Confidential

Complement to Traditional Banking:

Facilitating Access and Inclusion

Mondato in Brief

Page 2

❖ Mondato is a boutique consultancy specializing in strategic, commercial and operational support across the DFC ecosystem

❖ Born from years of experience in the telecommunications, technology and finance industries; we understand DFC pain points, and have designed our solutions to address these

❖ We cater to companies across the globe, from pre-revenue start-ups to large multi-nationals; we also support public sector entities, whether national, multilateral or NGO

❖ Also publish an original Mondato Insight weekly, and convene Mondato Summit Asia annually

12 September 2017

DFC can be likened to an expanding, exploding star

Page 3

Spiking demand for new payment and other financial service options:

• $100Bn+ fintech funding over four years (e.g., AI, IoT, Insure/Wealth/Reg Tech, machine learning, mobile wallets, payments, APIs)

• Strong emphasis on mobile and online technologies

• Bevy of local/int’l and non-bank and players (social, search, retail, network, telco)

• New applications and consumers driving demand

• Regulatory / Gov’t engagement, and emphasis on financial inclusion

• Disruption to fiat currency from cryptocurrencies

12 September 2017

Developed mobile money / agent banking study for ADB

Page 4

The study was commissioned by ADB to consider areasfor improvements to promote and enhance paymentsystems, digital finance, and e-money services inBangladesh, Nepal and Sri Lanka.

Digital payments and broader digital financial services arean evolving and complex domain that do not always haveclearly delineated boundaries or universal terminology.

This report focuses on the supply side of services beyondbank branches via agents and mobile devices for under-served populations. These services are generally definedas mobile money and agent banking.

12 September 2017

Presentation provides global contextualization

Page 5

Sri Lanka has a leading banking sector in the region, though seeks to increase account usage

• Gov’t controlling stake in largest banks brings stability, and as allowed for good core infrastructure

• Smaller banks less successful, though some mid-sized entities have mixed success with niche offerings

• Remains very much a cash-based economy, though OTC popularity hints at significant latent demand

Targeted value propositions provide an opportunity to increase perceived value by end-users

• Opportunity for banks to leverage 3rd party services to expand range of offerings w/ limited investment

• Banks provide regulatory compliance / systems for linked accounts used in higher-value transactions

• Payment services providers (PSPs) and mobile network operators (MNOs) integrators of 3rd parties

Opportunity to consider how global trends might be applied in addressing local requirements

• An array of vertical and advanced financial services use cases launched globally using MM rails

• Likewise, regulators are looking to facilitate digitization of economic activity as a driver of growth

• Experimentation with emerging fintech e.g., blockchain and cryptocurrencies to leapfrog market gaps

Relatively solid connectivity, banking infrastructure and digital adoption offers unique opportunity

12 September 2017

Page 6

Increasing Uncertainty and Disruption

Global Contextualization of Financial Inclusion

Sector is Reinventing Itself

Considerations for Sri Lanka

12 September 2017

Cryptocurrency, just a few years old, illustrative of volatility

Page 7

• ~700 cryptocurrencies with market capitalization

• Top 100 cryptocurrency market cap of ~ $146 billion

• Volatility can be extreme ( 10-20%+ weekly change)

• Bitcoin recently again hit record highs, but for how long

• Bitcoin has greatest overall market cap at ~ $70 billion

• CaliphCoin was recently lowest at ~$110 (circulation of 87k)

613 Currencies in this range

Market Capitalization Splits of Cryptocurrencies

Sources: Mondato analysis, CoinMarketCap; note, market cap was $80 billion in July

12 September 2017

Established channels at risk of disruption with digitization

Page 8Sources: Mondato analysis, eMarketer

-1%

1%

3%

5%

7%

9%

11%

13%

15%

$0

$1

$2

$3

$4

$5

2015 2016 2017 2018 2019 2020

An

nu

al e

Co

mm

erce

$Tr

illio

n

As

% o

f G

lob

al R

etai

l

* Excludes travel and event tickets

Some forecasts expect eCommerce to almost triple in the coming years

• Asia Pacific expected to drive growth as it reaches $1 trillion annually

• One constraint for developing markets is payments and logistics

• Financial inclusion a first step for both merchants and consumers

• Traditional businesses need to evolve or risk being left behind

• Payment gateways facilitate cross-border sales opportunities

• Still, however, often requires both parties to be linked to bank accounts

12 September 2017

Mobile money taking the lead in many developing markets

Page 9

30%

43%

63%

67%

75%

82%

Europe & Central Asia

Middle East & N. Africa

East Asia & Pacific

Latin America

South Asia

Sub-Saharan Africa

Significant share of developing markets have live mobile money deployments

(End of 2016)

Registered Accounts(3-yr CAGR)

Active(3-yr CAGR)

% Active

277 M (34%) 100 M (28%) 36%

164 M (55%) 40 M (47%) 25%

23 M (34%) 11 M (54%) 47%

37 M (13%) 7 M (24%) 19%

44 M (6%) 14 M (77%) 32%

10 M (74%) 1 M (113%) 13%

Source: Mondato analysis, GSMA

Strong growth in registered and active accounts despite number of markets being relatively constant in recent years

12 September 2017

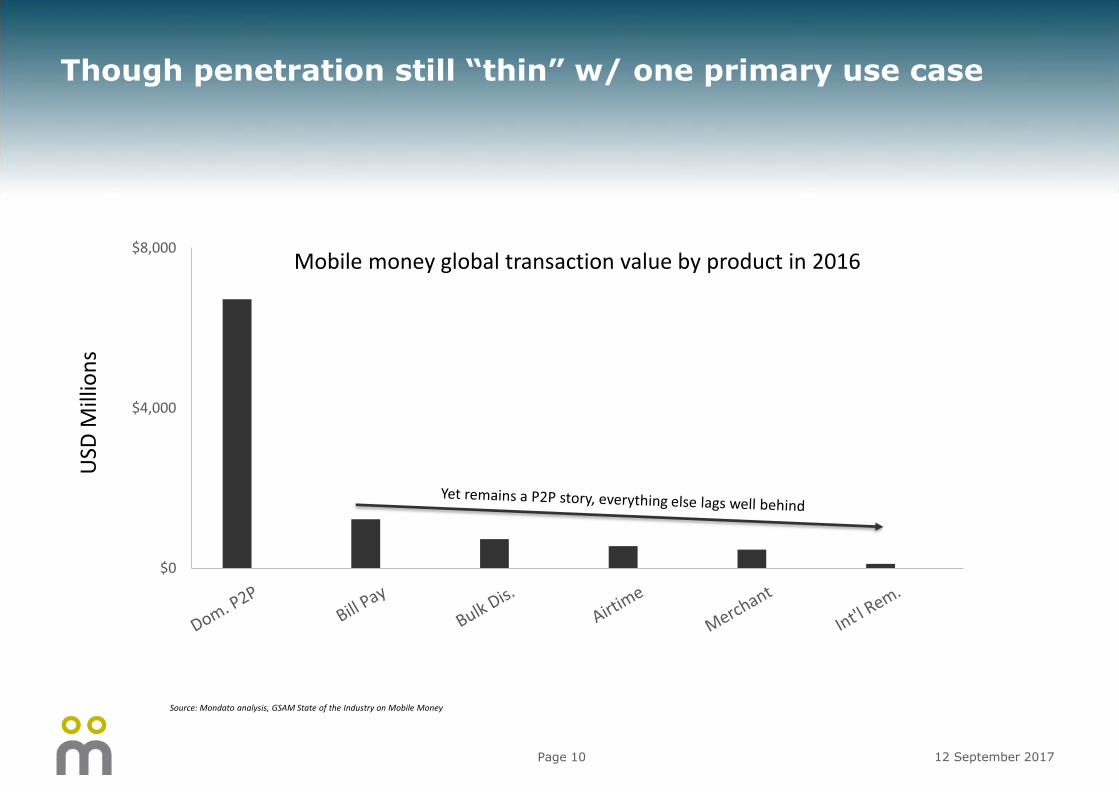

Though penetration still “thin” w/ one primary use case

Page 10

$0

$4,000

$8,000Mobile money global transaction value by product in 2016

Source: Mondato analysis, GSAM State of the Industry on Mobile Money

USD

Mill

ion

s

12 September 2017

Recent research validates regional preference for cash

Page 11 12 September 2017

Source: “Digital Payments: Thinking beyond Transactions,” PayPal, August 2017, conducted with 4,000 participants in China, India, Hong Kong, Singapore, Thailand, Philippines and Indonesia

Observations

• Consumers and merchants often aware of digital payments, due to such offerings have been available across Emerging Asia for many years

• Yet ex China, cash remains preferred mode of payment, despite ever rising Internet and smartphone penetration

• Compare with Europe; for example, cash transactions made 2% of value of all payments made in Sweden in 2015

• Education, simplicity, and safety / privacy potential bottlenecks

• PayPal contends innovation, rewards, advocates, and connectivity as opps

Most Often Used Payment Methods in Asia

China the galloping outlier; Singapore taking note

Page 12 12 September 2017

Some beggars in China now exhibit QR codes

• In a report by the International Business Times, Chinese digital marketing firm China Channel claims that many beggars they encountered in Beijing "are actually being paid by local businesses and startups to promote QR codes and entice passersby to scan them."

Sources: http://www.asiaone.com/china/no-loose-change-beggars-china-now-accepting-

mobile-payments, Aug 25, 2017; http://www.channelnewsasia.com/news/singapore/national-

day-message-pm-lee-highlights-3-longer-term-issues-9103714, Aug 8, 2017

• During Aug 8 National Day message, Prime Minister Lee Hsien Loong highlighted three issues: Pre-school, war on diabetes and goal of making Singapore a Smart Nation

• He pointed out country has a natural advantage: It is a highly connected and digitally literate society, but must do better on going cashless… “We must learn from them, catch up and get ahead.”

Singapore PM makes Smart Nation a priority

Cash still king in Sri Lanka, but markers of evolution evident

Page 13 12 September 2017

Source: Daily FT, September 11, 2017

• According to Visa Sri Lanka and Maldives Country Manager, Anthony Watson:

• Last year, payment volume on Visa credit cards increased 23%, while Visa debit cards were up 21%

• Overall number of credit and debit cards in the market is estimated at around 17 million

• “Personal consumption expenditure on electronic payments remains at a very low level of 4.2%, which indicates there is still considerable room for growth;” in Asia Pacific it is 45%

• Industry studies have shown the cost of handling cash to be between 1% and 3% of a country’s GDP

Consider a few key initiatives, while mindful of convergence[Illustrative of major trends, and non-exhaustive]

Page 14

Initiative Description and Distinctions Indicative Considerations

Mobile banking Digital channel for account services typically through smartphone app, occasionally USSD

While less hype about omni-channel, how to prioritize branch efficiencies and engagement?

Digital Wallets Not necessarily specific to a device (e.g., in-app purchases) to be seamless across touchpoints

How to automate payments beyond digital channels, e.g., counterless checkouts? Is it something that might be seen more as closed-loop proprietary systems (e.g. retailers)?

Mobile Wallets Makes the phone the vehicle for processing payments, and bring functionality to a device

What role for payments tied to physical devices, or even cards, given digitization?

Mobile Money / eMoney Electronic storage and transfer of value linked to a mobile rather than account or mWallet

How will MM need to transform beyond USSD in the world of smartphones and apps?

OTC* and mPOS Agent banking, and can be either formal or illicit, where 3rd parties transact for their clients

What is the tradeoff in convenience and costs to the end-user (e.g., for illiterate poor)?

Cryptocurrencies** Digital money using cryptography which to date has been independent of central banks

How can organizations experiment with real applications in validating opportunities?

*Over-the-counter **somewhat parallel to a few other categories 12 September 2017

Page 15

Increasing Uncertainty and Disruption

Global Contextualization of Financial Inclusion

Sector is Reinventing Itself

Considerations for Sri Lanka

12 September 2017

% Increase between Findex waves

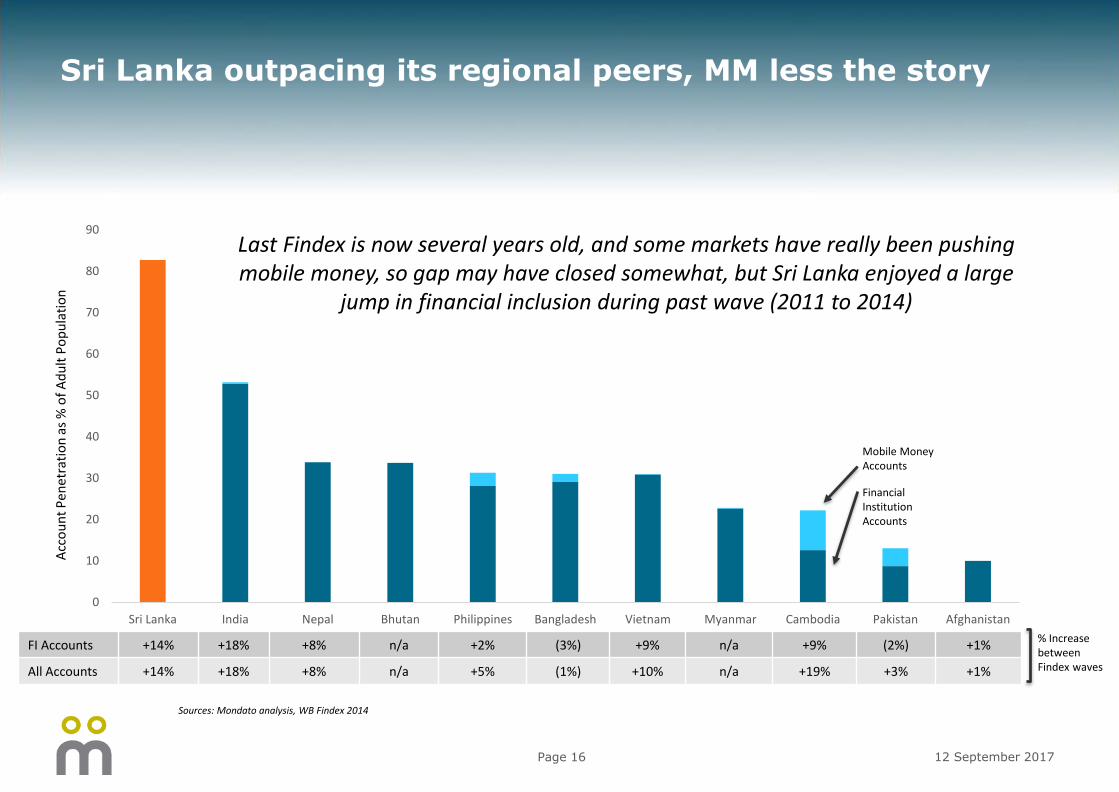

Sri Lanka outpacing its regional peers, MM less the story

Page 16

0

10

20

30

40

50

60

70

80

90

Sri Lanka India Nepal Bhutan Philippines Bangladesh Vietnam Myanmar Cambodia Pakistan Afghanistan

FI Accounts +14% +18% +8% n/a +2% (3%) +9% n/a +9% (2%) +1%

All Accounts +14% +18% +8% n/a +5% (1%) +10% n/a +19% +3% +1%

Last Findex is now several years old, and some markets have really been pushing mobile money, so gap may have closed somewhat, but Sri Lanka enjoyed a large

jump in financial inclusion during past wave (2011 to 2014)

Acc

ou

nt

Pen

etra

tio

n a

s %

of

Ad

ult

Po

pu

lati

on

Financial Institution Accounts

Mobile Money Accounts

Sources: Mondato analysis, WB Findex 2014

12 September 2017

Wide penetration, but need to translate into active usage

Page 17

India

Sri Lanka

BangladeshBhutan

PakistanAfghanistan

MyanmarCambodiaVietnam

0

10

20

30

40

50

60

70

80

90

100

Overall Male Female Age 25+ <=Primary Edu. >=Secondary Edu. Rural Wealthiest 60% Poorest 40%

Acc

ou

nt

Pen

etra

tio

n a

s %

of

Ad

ult

Po

pu

lati

on

Lack of active account usage remains an issue, however, given account fees, dissatisfaction with customer service, and general lack of financial education; OTC fills this gap for many payments

Sources: Mondato analysis, WB Findex 2014* For example, we know India has had a more significant increasing in mobile money since the last survey which would not be included here

Nepal

Account Penetration by Segment, Sri Lanka vs. Regional Markets

12 September 2017

MM potentially plays bigger role in a layered proposition

Mobile Banking Mobile Money

Additive to existing bank channels and services, yet compliance remains costly, but much better customer engagement in personalizing products for specific needs

Transformative as a “lite” bank account or stored value for providers to reach a new, previously un-addressable customer base (agent banking need not rely on mobile phones), and offers a key “on-ramp” for those that may find formal channels and account intimidating, and potentially provides rails over which more advanced products can be offered by 3rd parties

Agent Banking

Page 18 12 September 2017

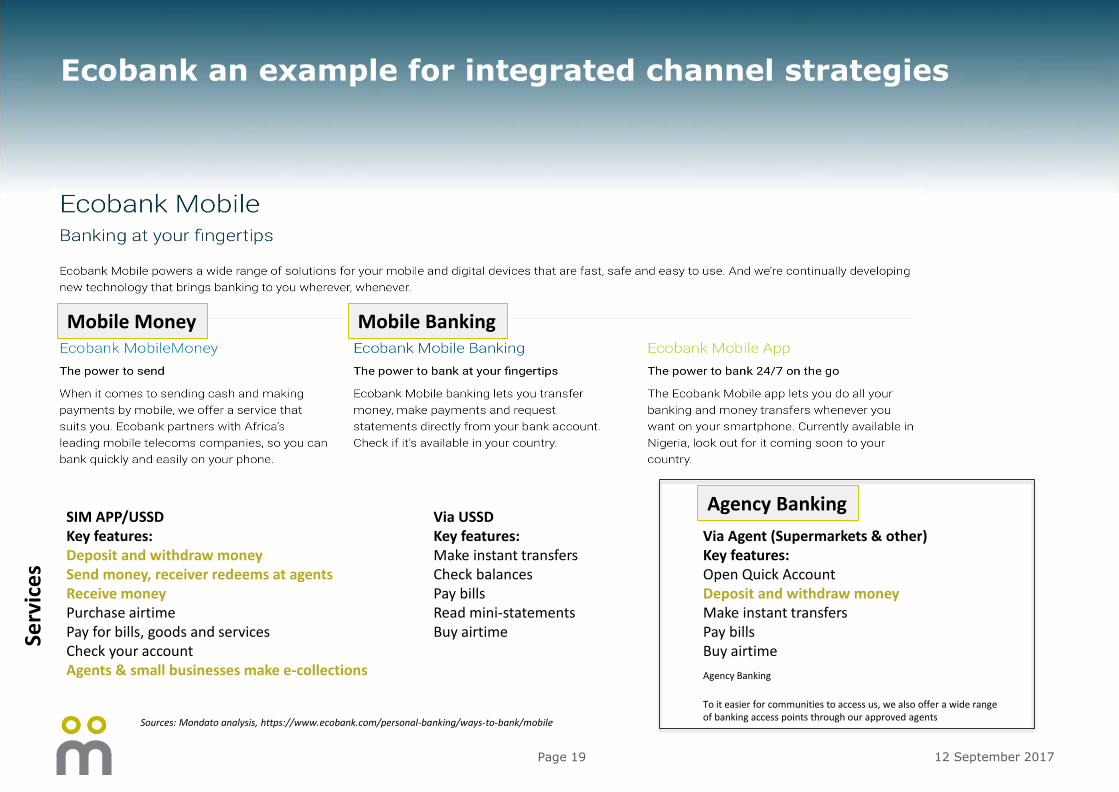

Ecobank an example for integrated channel strategies

Page 19

Sources: Mondato analysis, https://www.ecobank.com/personal-banking/ways-to-bank/mobile

SIM APP/USSDKey features:Deposit and withdraw moneySend money, receiver redeems at agentsReceive moneyPurchase airtimePay for bills, goods and servicesCheck your accountAgents & small businesses make e-collections

Via USSDKey features:Make instant transfersCheck balancesPay billsRead mini-statementsBuy airtime

Mobile BankingMobile Money

Serv

ice

s

Via Agent (Supermarkets & other)Key features:Open Quick AccountDeposit and withdraw moneyMake instant transfersPay billsBuy airtime

Agency Banking

Agency Banking

To it easier for communities to access us, we also offer a wide range of banking access points through our approved agents

12 September 2017

SA struggled repeatedly, MNOs finally abandoned efforts

Page 20 12 September 2017

Two broad pathways in balancing formal vs. informal

Page 21

Revert back at some point in future as sector matures / achieves critical

mass?

Intricately Managed Interventions

Get Out of the Way

• Regulatory mandates such as branch coverage, fees & charges

• Detailed licensing defined by product(s), each w/ distinct rules

• Mandating of competitive dynamics (e.g., levels of interoperability)

• Converged licensing beyond types of entities, instead use risk tiers

• Macro-stability uses core banking for trust accounts / collateral

• Focus on anti-competitive behavior (e.g., MNOs restricting access)

Either need to actively engage at many levels, or peel back regulations based on willingness to push the risk-reward frontier

12 September 2017

Page 22

Increasing Uncertainty and Disruption

Global Contextualization of Financial Inclusion

Sector is Reinventing Itself

Considerations for Sri Lanka

12 September 2017

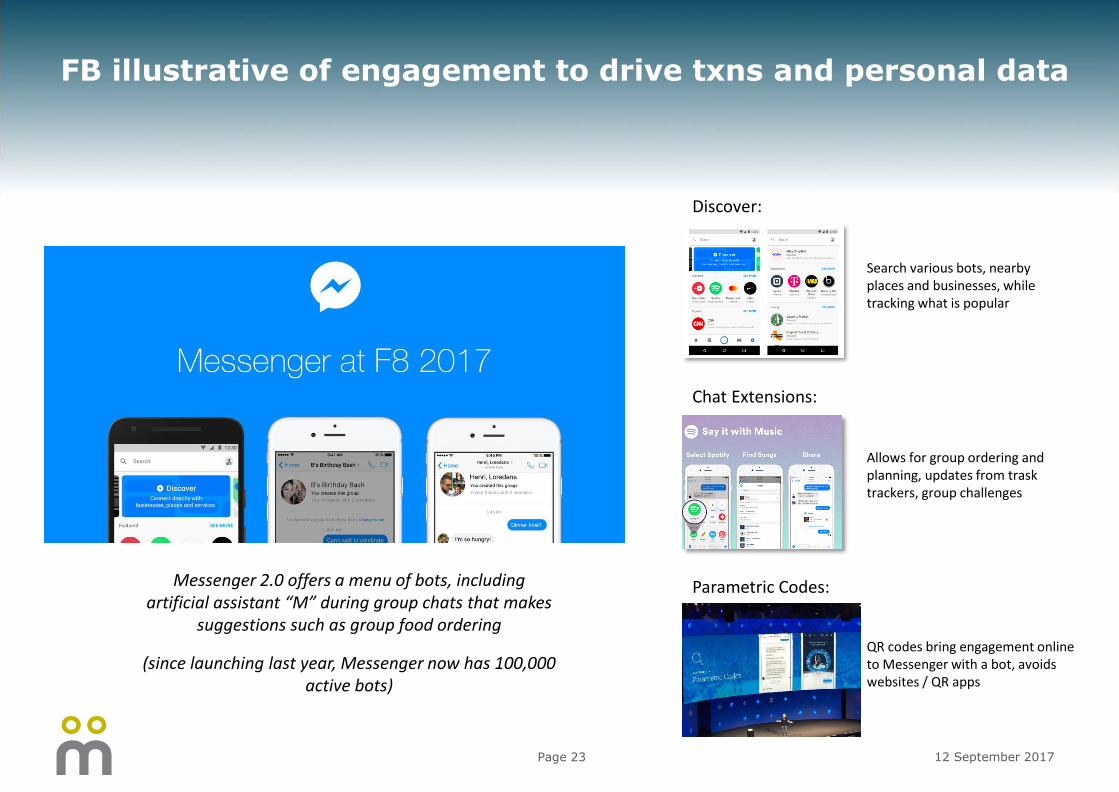

FB illustrative of engagement to drive txns and personal data

Page 23

Messenger 2.0 offers a menu of bots, including artificial assistant “M” during group chats that makes

suggestions such as group food ordering

(since launching last year, Messenger now has 100,000 active bots)

Discover:

Search various bots, nearby places and businesses, while tracking what is popular

Chat Extensions:

Parametric Codes:

Allows for group ordering and planning, updates from trasktrackers, group challenges

QR codes bring engagement online to Messenger with a bot, avoids websites / QR apps

12 September 2017

May portend global consolidation, e.g., PSPs from China

Page 24

UnionPay, 43%

Visa, 21%

MasterCard, 16%

Others, 20%

14 billion cards globally in 2016

Cards by Network

UnionPay only became the largest scheme in 2010, and has since achieved global leadership through its

domestic market. Competition at home has it looking overseas to expand upon the paltry 1% of its cards

issued internationally

• Even if the market may be somewhat cut off for certain services, difficult to ignore its scale

• Winners in that market tend to be positioned for int’l expansion given scale and network effects

• Alipay and WeChat are two prime examples, with both on acquisition sprees abroad

• Global players may target larger markets first, with roll-outs elsewhere not as well supported

• Balance immediacy of niche providers vs. risk of ending up left behind with legacy systems

• Risks such that it is even becoming difficult in some parts of China to even use cash these days

12 September 2017

And blockchain shows power of distributed networks

Page 25

The breakthrough behind Bitcoin, blockchain verifies transactions by comparing records across nodes such that it cannot be corrupted unless half the network is breached, allowing for irreversible transfers of value

Has Already Driven Experimentation by a Diverse Range of Stakeholders

Financial Institutions Disintermediation“Decentralized Autonomous

Organizations”

Complex software comprising smart contracts which basically automate business plans absent bureaucracy and management

Startups using original use case of cryptocurrencies to avoid txn costs of formal banking rails, including FX

fees and spreads

Incumbents are forming consortiums to experiment with

substitutes for traditional systems and compliance

Some initial growing pains as a premium on computing power to process transactions has meant slower processing times and higher transaction fees illustrating uncertainties that lie ahead

12 September 2017

Note: Perhaps a sign of stakes going up, Ripple, R3, two distributed ledger startups, currently embroiled in legal battle over crypto contract dispute

Page 26

Market dynamics that have been conducive to date for MM(Illustrative and non-exhaustive)

No unnecessary restrictions in regard to cross-border payments such as amount limits, onerous licensing and costs

A competitive, dynamic and interoperable environment, permitting several actors, including, non-Financial Institutions, to issue e-Money

Risk-proportional initial and ongoing capital requirements, relative to the risks of the e-Money business; safeguarded customer funds

Risk-proportional tiered KYC for both agents and users across different types of providers and for different services

Diverse type of players allowed to be agents for Cash-In and Cash-Out operations to extend the distribution network

Complementary Services

Macro Proportionality

Capillarization

Global Marketplace

Streamlined Adoption

12 September 2017

No set formula, increasing bifurcation of winners and losers

Page 27

Avoiding Launchpad Failure

Seeking Escape Velocity

Illustrative Examples: Philippines, Tanzania

Current Situation: Competing platforms have achieved significant penetration, though some fragmentation, as focus shift towards interoperability in moving beyond the initial use cases

Going Forward: Still standalone ventures reliant on the “rocket fuel” of controlling MNOs to bring new propositions, and now need to consider opening platforms for 3rd party VAS innovation

Illustrative Examples: Albania, South Africa

Current Situation: M-Pesa invested significant resources in markets, in some cases multiple time, yet the propositions failed to get off the ground, with services suspended in these markets

Going Forward: While significant under-banked populations, operators considering what they can offer beyond agent networks, or even what role to play, or whether others are better placed

Increasingly a split between markets which are taking off, yet now looking to see how to boost the next phase of growth, and others for which success remains elusive regardless of amount of resources or number of attempts

Incr

easi

ng

Bif

urc

atio

n o

f W

inn

ers

and

Lo

sers

12 September 2017

Ecosystem view: new players may rise up to fill canopy gaps

Page 28

Gaps may occasionally appear offering opportunities for others

to grow into larger spaces

• Reshuffling of the deck chairs with sectors converging

• New configuration may be required for the digital economy

• The long promised transition is seemingly now gaining speed

• Some players are achieving significant scale, others specializing

• Potentially a second inflection point, a new phase of disruption

Retail Payments Logistics

Traditionally quite distinct:

Stylized, Illustrative Example

eCommerce and payments:

Sometimes scaled & spun off:

Platforms for ecosystems:

Mix of fragmentation, reintegration and scale over past years:

12 September 2017

Page 29

Increasing Uncertainty and Disruption

Global Contextualization of Financial Inclusion

Sector is Reinventing Itself

Considerations for Sri Lanka

12 September 2017

Getting pieces in place for a next phase of growth

Page 30

Good foundational infrastructure for financial services

Reasoned approach to rules supports innovation

Targeted propositions may increase digital commerce

Launch infrastructure is in place, rocket is being hoisted into position, yet several phases yet to successfully navigate in order to reach orbit

12 September 2017

Stable banking sector, consider alternative channels

Page 31

Payment Systems MM & Agents Regulation

Potential Focus Areas

Distribution efficiencies beyond physical branches

Fintech lacking, loss of expertise to int’l hubs

Strongly Bank led, savings dictate available capital

Colocation could be better for uptime & services*

Metro / access fiber for enterprise virtualization

Considerations

Universal service policies: 2G coverage, 3G/4G access

Grants, accelerators, outreach to retain entrepreneurs

Capital markets initiatives to access additional capital

Transition from vertically integrated to DC specialists

PPP initiatives to spread costs / risk for more fiber

12 September 2017

*First Tier 3 facility was recently opened by Dialogue, but opportunities for independent facilities with dedicated focus on facilities management and hosted enterprise services

Leverage tiered strategy for products and distribution

Page 32

Potential Challenges

Limited financial education for greater inclusion

Less incentive for MNOs to directly drive usage

Bank-led agent banking only recently launched

Agent network rural coverage could be improved

USSD menus are not always very intuitive

Nascent ecosystem for 3rd party VAS

Lack of trust in SMS-based digital payments

Considerations

Traditional mechanisms (e.g., linked cards) for uptake

Super agent managed services extend network reach

Non-merchant agents for more specialized outreach

Agent liquidity rules to facilitate bulk disbursements

Extension of KYC limits for a greater range of services

App-based offerings for engagement and transparency

Payment Systems MM & Agents Regulation

12 September 2017

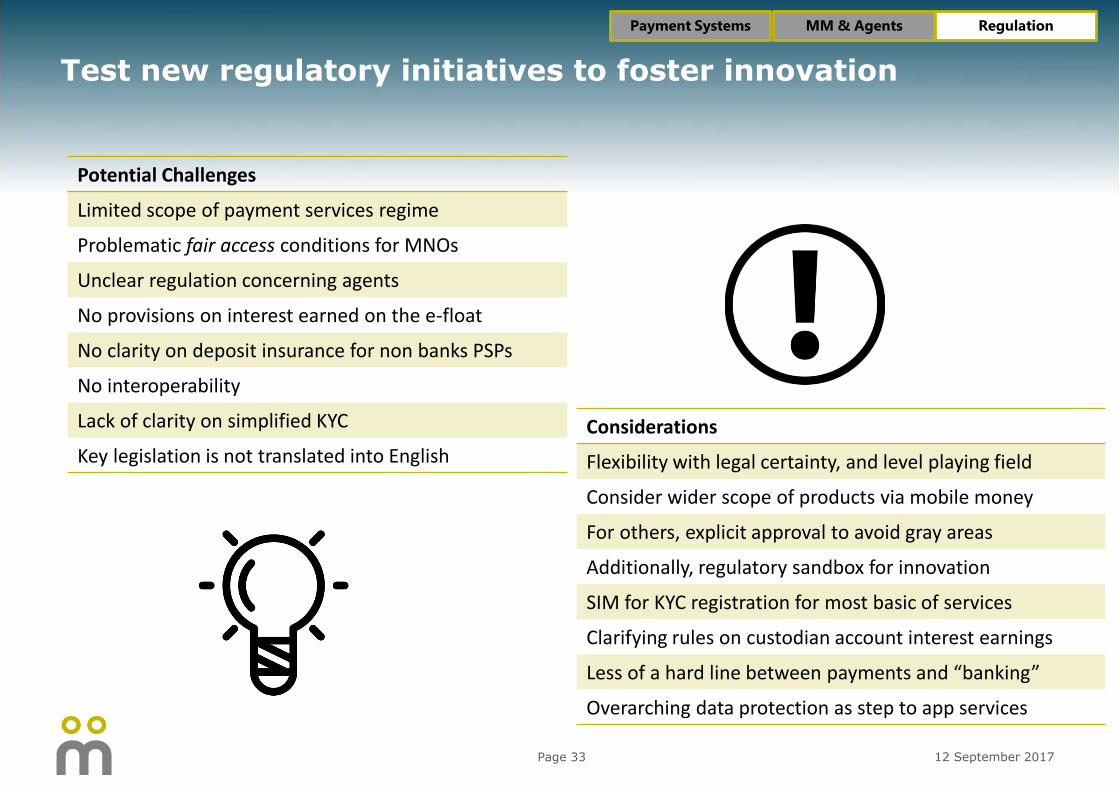

Test new regulatory initiatives to foster innovation

Page 33

Potential Challenges

Limited scope of payment services regime

Problematic fair access conditions for MNOs

Unclear regulation concerning agents

No provisions on interest earned on the e-float

No clarity on deposit insurance for non banks PSPs

No interoperability

Lack of clarity on simplified KYC

Key legislation is not translated into English

Considerations

Flexibility with legal certainty, and level playing field

Consider wider scope of products via mobile money

For others, explicit approval to avoid gray areas

Additionally, regulatory sandbox for innovation

SIM for KYC registration for most basic of services

Clarifying rules on custodian account interest earnings

Less of a hard line between payments and “banking”

Overarching data protection as step to app services

Payment Systems MM & Agents Regulation

12 September 2017

Concluding observations in getting balance right in Sri Lanka

Page 34

Focus Areas Global Insights Considerations for Sri Lanka

Alternative Channels MNOs have shown greatest ability to invest, though independent PSPs have occasionally succeeded in more restrictive markets

Agent / platform interoperability should be a longer-term objective, but risk is forcing this either too soon (no incentive to invest) or late (entrenched interests make change more difficult)

Robust Ecosystem Outside of Zimbabwe, which is somewhat unique given past banking crises, few incumbents succeed through closed networks of building their own comprehensive portfolio of offerings

New revenue models may be required within the MNO mobile money consortiums, because the current problem is the free-rider issue which acts as disincentive to invest in a service which may benefit competitors

Future Evolution Vast majority of success stories have been MNO-led models where regulations were limited and banks took a back seat given their primary focus on wealthy individuals and enterprise

While true that MNO-led has been most successful to date, it is still early days, and Sri Lanka may provide a unique situation where MNO-bank partnerships offer significant synergies to leverage accounts / drive usage

12 September 2017

Potentially greater prospects for competing bank-MNO alliances than seen elsewhere

ABOUT MONDATO LLC

Mondato is a boutique management consultancy specializing in the provision of strategic, commercial and operational

support across the digital finance and commerce (DFC) ecosystem.

Established in 2008 on a foundation of years of experience in the telecommunications, technology and financial sectors,

Mondato possesses a unique understanding of the fast evolving, ever expanding DFC space; we understand the players’

pain points, and have designed our solutions to address them. Mondato’s portfolio of strategic and tactical offerings target

MNOs, banks, retailers, vendors, regulators, DFIs, and others interested in implementing, investing in, or encouraging the

development of DFC, whether as a pure play or as part of a broader proposition.

Mondato Summits offer clarity amid a chaotic and constantly changing industry. From defining a strong value proposition

and forging strategic partnerships to sourcing technology efficiently and ensuring compliant service delivery, Mondato

Summits take on the most pressing issues in DFC today, and do so in an intelligent, substantive, and actionable manner.

Headquartered in Washington, DC, Mondato works around the globe with a cadre of highly-trained experts, who have

executed high-stakes projects for private and public sector organizations operating in DFC and adjacent spheres.

CONTACT US

Mondato LLC 4201 Connecticut Ave. NW, Suite 600, Washington, DC 20008, USA

Tel: +1-202-803-8704 / Fax: +1-202-459-9512 / www.mondato.com

25 July 2017