Embed Size (px)

Citation preview

Competitive Strategy and the Wal-MartThreat: Positioning for Survival and SuccessJohn A. Parnell, University of North Carolina-Pembroke

Donald L. Lester, Middle Tennessee State University

No class of retailer has influenced the businesslandscape in recent years more than the big box,and no big boxer is more prominent than Wal-Mart. Big boxers like Wal-Mart not only applypressure to suppliers and alter the mix of shop-ping alternatives for consumers, but they alsogreatly influence the competitive behavior oftraditional retailers. The academic and businesspress has chronicled the wide-ranging effects ofthe mega-retailer over the past two decades(McCune, 1994; McGee and Peterson, 2000;Stone, 1993). Although there is growing evi-dence that Wal-Mart's hold on retail may beslipping, it remains a competitive nightmare formany of its competitors, particularly small rivalsin local markets (McWiltiams, 2()07a. 2007b).

A number of authors (e.g.. McGee andPeterson, 2000; Edid, 2005; Spector, 2005) havesuggested or inferred competitive responses forsmaller retailers when a big box like Wal-Martcomes to town. This paper builds on such workby providing a more comprehensive and theory-based analysis of strategic alternatives availableto retailers specifically facing a threat from Wal-Mart. Toward that end, the remainder of thepaper begins with an overview of the big boxphenomenon and a framework for understandinghow the big box influences the strategic land-scape. Three theory-based potential strategicresponses are evaluated, followed by conclu-sions and opportunities for further research.

Wal-Mart and the Big Box PhenomenonThe emergence of big box retailers in the UnitedStates has changed the retailing landscape con-siderably. The term "big box" typically refers todiscount retailers whose stores exceed 50.000square feet, with many as large as 200,000square feet. Big boxers usually implement alimited number of store designs across markets

and seek profits through high volume via lowmarkups. Their facades are standardized withlai"ge windowiess single-story buildings. Ampleparking is usually available, although customersmay be required to walk a considerabie distanceto enter the store.

Store traffic patterns spell the success of bigboxers, particularly in the United States. Duringthe la.st 15 years, the number of consumer tripsto the shopping mall has been cut in half, a trendthat has not always held true for malls anchoredby a big box like Wal-Mart or Target (Chittum,2005), In addition, a growing percentage ofAmerican teenagers have access to a credit card.Teens are making more and more purchasedecisions and are frequenting shopping mallsless and shopping more at big boxers, entertain-ment-oriented retailers, and online retailers(Barta. Martin, Frye, and Woods. 1999; Etter,2005; Raymond, 1999; Spector. 2005).

A big box store that operates primarily in aspecialized market may also be referred to as a"category killer." Toys "R" Us is widely refer-enced as the first category killer; others in theU.S, include Best Buy, Circuit City. Lowe's,Blockbuster, and Home Depot. From a strategicperspective, general merchandise big boxers andcategory killers are similar in a number of ways,with the primary distinction being the breadth ofthe product line (Spector, 2005). Wai-Mart, forexample, sells office supplies like Office Depot,electronics like Best Buy, and hardware likeHome Depot, but does not offer as wide a selec-tion as their specialized counterparts.

Wal-Mart is the perennial general merchan-dise big-box retailer in the United States, al-though rivals Costco and Target are alsoprominent examples. Wal-Mart boasts 23 milesof retail selling space in the U.S., where 70%of its approximately 5,500 stores are located.

14 SAM ADVANCED MANAGEMENT JOURNAL

Annual revenues for 2004 were slightly over$288 billion (Revell. 2005). making it numberone on the Fortune 500 ranking. By 2005, Wal-Mart had slipped to second place on the Fortune500 (McGirt, 2006) with revenues of $315billion, just behind Exxon Mobil. However, in2006 it regained the top spot as revenues ex-ceeded $350 billion (Useem. 2007), with itsheadcount nearing two million.

Because of its prominence and ability to trimcosts, Wal-Mart is often the brunt of criticismfrom politicians, activists, union leaders, andothers. Detractors, for example, contend thatWal-Mart's aggressive negotiating tactics ulti-mately annihilate U.S. manufacturing firms andsend American jobs overseas. Some charge thatthe mega-retailer seeks to render obsolete smallbusinesses in the communities in which it oper-ates (Edid, 2005: Quinn, 2000). Others citepositive influences, however, noting such factorsas job creation and the benefits of low prices(Etter, 2005; York, 2005). When Albertson's —the second largest grocer in the U.S. with 2,500stores — searched for a buyer in 2005, it wasanother reminder that Wal-Mart can destroysmaller competitors and have a staggering effecton the success of large retailers as well (Berman,Adamy and Sender. 2005). Besides Albertson's,a host of formerly successful discount chainstores were bankrupt by the late 1990s, includ-ing Heck's. Arlans, Federals, Ames, E.J. Kor-vette, Atlantic Mills, iind W.T. Grant (Camerius,2006).

Wal-Mart critic Arindrajit Dube suggests thatWal-Mart's relatively low wages resuit in anannual wage loss in the retail sector of almost $5billion. Hollywood producer Robert Greenwaldeven produced a movie about the giant retailer,"WAL-MART: The High Cost of Low Price,"chronicling the plight of an Ohio-based hard-ware store when Wal-Mart moved to town (York.2005). Indeed, the liberal segment of the U.S.has adopted Wal-Mart as its cause de jour withsuch a vengeance that one writer has labeledtheir obsession WMDS — Wal-Mart derange-ment syndrome (Goldberg. 2006). Senator JohnKerry (D. Mass.) has been quoted as saying thatWal-Mart is "disgraceful" and a symbol of"what's wrong with America" (Will, 2006b). Heis basing his remarks on Will's (2006b) claimthat Wal-Mart costs about 50 retail jobs forevery 100 jobs that it creates.

Critics are aghast at Wal-Mart's wages andlack of health care coverage, siding with unionsin their efforts to organize Wal-Mart workers.

They argue that Wal-Mart takes advantage ofAmerican blue-collar workers who, due todownsizing and outsourcing, cannot find viableemployment elsewhere. They also suggest thatmuch of the outsourcing can be blamed on Wal-Mart's coercive tactics in dealing with suppliersand costs. Through laws and ordinances, theunion push has even led several states and citiesto try to force Wal-Mart and other big-boxretailers to spend at least 8% of its payroll onhealth care or pay a minimum of $ 13 an hour tohourly employees (Novak, 2(X)6: Will. 2006a).When Wal-Mart announced its intention to moveinto inner city areas of Los Angeles, for ex-ample, voters rejected its effort (Kaplan. 2006),choosing instead to rely on small mom and popmerchants that some suggest have historicallyovercharged local residents who lack basictransportation.

Not all press has been negative, however. AsJason Furman of New York University notes,Wal-Mart's economic benefits cannot be ignoredas the retailer saves its customers an estimated$200 billion or more on food and other itemsevery year (Mallaby, 2005). As for health insur-ance, Wal-Mart offers 18 different plans lo itsemployees, with one having monthly premiumsas low as $11 (Will, 2()()6a). All togethei; over86% of Wal-Mart employees have some form ofhealth insurance, witb about half being insuredthrough the company. With over 1.3 millionworkers in the U.S., Wal-Mart accounted for13% of the country's productivity gains in thescondhalfofthe 1990s.

The competitive issue for the future is howconstrained Wal-Mart's domestic growth willbecome due to this class war being fostered bythe more liberal segment of U.S. society. Iflegislation takes hold on a widespread basis tolimit Wal-Mart's penetration of untapped U.S.markets, will that create opportunities for otherfirms to expand their operations to take up theslack?

The Big Box and the StrategicLandscapeTraditional economic theory suggests that therules governing firm success and failure tend toevolve over time as a result of the collectiveactivities of numerous competitors in an indus-try. This economic ideal is marked by free andopen competition and assumes that no singlefinn is able to rise head and shoulders above tbecrowded field and dominate the industry. Theproblem, bowever, is that all firms in an industry

SPRING 2008 15

are neither equally competifive nor equallylucky. In many cases, this results in one or morerising to prominence. Such is the case with bigboxers.

Industrial organization (10) economics em-phasizes the influence ofthe industry environ-ment on firms. The central tenet of industrialorganization Iheory is che notion that a firm mustadapt to influences in its industry to survive andprosper; thus, its financial pertbrmance is prima-rily detennined by the success of the industry inwhich it competes. Industries with favorablestructures offer the greatest opportunity for firmprofitability (Bain. 1968). Recent research hassupported the notion that industry factors tend toplay a dominant role in the performance of mostcompetitors, except for those that are the notableindustry leaders or losers (Hawawini,Subramanian, and Verdin. 2003).

The IO perspective assumes that a firm'sperfonnance and ultimate survival depend on itsability to adapt to industry forces over which ithas little or no control. According to 10, strate-gic managers should seek to understand thenature of the industry and formulate strategiesthat feed off the industry's characteristics. Be-cause 10 focuses on industry forces, otherfactors including strategies, resources, andcompetencies are assumed to be fairly similaramong competitors within a given industry.

If one firm deviates from the industry normand implements a new, successful strategy, otherfirms will attempt to rapidly mimic the higher-performing firm by purchasing the resources,competencies, or management talent that havemade the leading firm so profitable. Hence,although the 10 perspective emphasizes theindustry's influence on individual firms, it is alsopossible for firms to influence the strategy ofrivals, and in some cases even modify the struc-ture ofthe industry, albeit in a limited fashion(Barney. 1986; Seth and Thomas. 1994).

Perhaps the opposite of IO, the resource-basedview (RBV) considers performance to be afunction of a firm's ability to utilize its resources(Barney. 1986). Although environmental oppor-tunities and threats are important, a firm'sunique resources compo.se the key variables thatallow it to develop a distinctive competence(Lado. Boyd. and Wright, 1992) and enable il todistinguish itself from rivals and create competi-tive advantage. A firm's resources include all ofits tangible and intangible assets, such as capital,equipment, employees, knowledge, and informa-tion. An organization's resources are directly

linked to its capabilities, which can create valueand ultimately lead to profitability for the fimi.Hence, re source-based theory focuses primarilyon individual firms rather than on the competi-tive environment.

The increasing speed of business activity andthe notion of ephemeral competitive advantagehave prompted researchers to emphasize dy-namic strategy positioning models. This ap-proach does not refute the tenets of IO and theRBV per se, but challenges their static assump-tions in favor of strategies that are more flexibleand adaptive to changing market conditions.This is especially true in industries where suc-cess depends on a constant flow of new offerings(Bamett. 2006; Fiegenbaum and Thomas. 2004;Selsky, Goes, and Baburoglu. 2007).

The IO, resource-based, and dynamic strategicpositioning perspectives can be useful tools forunderstanding competitive behavior in industrieswhere big boxers thrive. Contrary to 10 assump-tions concerninfi the limited power of any sinfilefirm, however, hig boxers set — or at least influ-ence significantly — the competitive rules intheir industries. For example, big boxers shiftthe power relationship between retailer andproducer in favor of the retailer, a move that caneffectively reduce the level of differentiationamong producers. When a retailer becomes adominant player in ils industry, it begins tocontrol a large percentage of the output of manyof its suppliers. As a result, the retailer cansometimes exercise more influence on a prod-ucts position and image than the manufacturer.10 and strategic group models acknowledge onlyminimal influence on the part of a single com-petitor. Industry factors dictate critical successfactors, and even large flrms must adapt to them.In contrast, big boxers leverage their size andscope in such a way that rivals, suppliers, andbuyers must reorient their competitive strategiesaccordingly. As Hannaford (2005) relates, firmswith market dominance in the past would havecharged above-market prices, earning above-average returns for their oligopolistic position.Wal-Mart, however, charges below-marketprices, forcing suppliers who wish to take advan-tage of their vast market to keep their costs andprices low.

Consider the case of Wai-Man and Vlasicpickles. In 2003 Wai-Man priced a gallon ofVlasic pickles at $2.97, thereby selling agallon ofthe nation's top-.selling brand for lessthan most other retailers charged for a quan.The move was a good one for Wai-Man as it

16 SAM ADVANCED MANAGEMENT JOURNAL

strengthened the retailer's image as a delivererof value. Unfortunatety, the move underminedefforts Vlasic had made for years to establish itsposition as a producer synonymous with thepickle itself. If Vlasic had chosen not to sell toWal-Mart, the producer would have paid a greatprice in terms of market share. Ultimately,Vlasic had little choice but to allow Wal-Mart tosell its pickles in whatever way the retailer sawfit (Fishman, 2003).

Consider another case involving Wal-Martand Levi Strauss. In 2002, Levi and Wal-Martannounced that the retailer would begin sellingLevis in its stores. Levi had experienced declin-ing market share in the decades prior, closing58 manufacturing plants in the U.S. and out-sourcing 25% of its sewing between 1980 and1991. After rebuilding and posting a record $7.1billion in sales in 1996, Levi experienced sixyears of decline. The Wal-Mart deal was de-signed to revive the brand. The problem wasthat half the jeans sold in the U.S. in 2002 costless than $20 a pair, a year in which Levi soldnone for less than $30. Clearly Wal-Mart, thecountry's leading clothing retailer, would not beinterested in selling premium jeans at a premiumprice. Levi had to develop a fresh line of lessexpensive jeans for Wal-Mart, the Levi StraussSignature brand. As expected, Levi sales in-creased shortly after its new line of jeans wereintroduced in Wal-Mart (Fishman, 2003). Atleast some of the Wal-Mart sales cannibalizedthose of Levi's more profitable premium brandsin other outlets, however. In addition, the sale ofLevis at Wal-Maii tarnished the image of thecentury-and-a-half old American icon.

Big boxers adopt a resource-based perspectiveto a great extent, seeking to develop resourcesand competencies that cannot be readily dupli-cated by rivals. Although competitive strategiescan vary among big boxers, the general approachis based on four pillars:

Build economies of scale. Big boxers lowercosts by purchasing larger quantities. Theydistribute these products efficiently to a largenumber of stores strategically located to mini-mize transportation and related costs. Sheer sizerepresents the single greatest resource advantagepossessed by the big boxer.

Offer everyday low prices on most items.Leveraging scale economies, big boxers typi-cally offer prices that simply cannot be tnatchedby rivals. As a result, most competitors find itdifficuh to compete with the big boxers solelyon price.

Sell a wide variety of products. Selling lots ofproducts increases store traffic. A customer mayvisit the big box to purchase one or two prod-ucts, but will likely leave with more. Productlines for general merchandise big boxers likeWal-Mart are not as deep as they are at theirspecialized rivals. Only products that sell consid-erable volume are carried, fueling even greatereconomies of scale.

Offer a consi.stent, predictable shoppingexperience across time and locations. Econo-mies of scale and low prices are achieved whenall stores sell the same products. Predictabilityenables customers to plan their shopping tripsaccordingly.

The four-pronged strategy employed by thetypical big box like Wal-Mart can be lethal tocompetitors, but the approach is not without itsshortcomings and can be attacked effectively bysmaller retailers. Specific plans for addressingthe Wal-Mart threat are outlined in the followingsection.

Strategies for Confronting the Wal-MartThreatBig boxers reduce the relative size of otherwise"large" retailers. To effectively confront the bigbox threat, smaller, often sizable and establishedrivals must account for the influence of the bigboxer on the industry and formulate their strate-gies accordingly. Specifically, the first step inconfronting Wal-Mart is to understand thethreats it creates, as well as the opportunities itaffords traditional retailers. While the competi-tive threat posed by the entry of a Wal-Martstore into a locale previously dominated bytraditional and specialty retailers is substantial, itdoes not necessarily create a hopeless situationfor smaller rivals. Competitive strategy is aboutchoices, some of which are mutually exclusive.By its very nature, a big box like Wal-Martpossesses key competitive strengths and weak-nesses that should be understood before craftinga response.

Wal-Mart's strengths are forthright andwidely acknowledged. With its size and accessto capital, Wal-Mart can sustain even a low-performing store for the long term when movinginto a region, a luxury not afforded many small,family-based businesses. Distribution andsupply chain efficiencies enable the retailer tooffer exceptionally low prices that are difficultfor rivals to match. Its wide product assortment— especially in superstores where both grocer-ies and general merchandise are offered —

SPRING 2008 17

generates store traffic and suppons a one-stopshopping experience for the consumer. And. itscost-control-oriented corporate culture, whichincludes a reliance on low-cost, pan-time labor,keeps costs down.

Wa!-Man's business mode! has its shoncom-ings, however. Ofthe five primai-y dimensions toretailing — quality, service, convenience, selec-tion, and price — and Wai-Man wins only onprice and selection (Rigby and Haas. 2004).Since Wai-Man typically captures about 30% ofa Iocal market, 70% remains for its rivals, in-cluding local retailers, other big boxers, andsmaller-store chains. While Wai-Man is oftenreferenced as the "500-pound gorilla," maintain-ing such a stature is not easy. As a big boxseeking to secure maximum market share from abroad audience. Wal-Mart simply lacks the focusand resolve to battle competitors along theperiphery, thereby creating opportunities forretailers that can compete on quality, service,and convenience. The success enjoyed by fiim-ily-owned businesses such as Berlin Myers, Ji.,owner of a lumber company in Summerville.South Carolina, bearing the family name, sug-gests that superstores and other retailers cancoexist, often with the smaller outlets supple-menting what the large ones carry. The bigboxers typically do not compete directly withsmaller retailers unless they are attacked first(McCune, 1994).

Because of its reliance on distribution andsupply chain efficiencies. Wal-Mart retailers arechallenged to alter product assonments andtailor offerings to the specific needs of a region.In addition. Wai-Man's approach assumes thatprice is the primary factor consumers evaluatewhen choosing a retailer. While Wal-Mart is ableto offer high-demand products at low prices, itssheer size makes it difficult for associates todeliver exceptional customer service on a consis-tent basis, a key component in the consumershopping experience. Wai-Man's image asGoliath in a David versus Goliath battle can be aliability if consumers become sensitive to theplight of family-owned businesses defendingthemselves against the onslaught of a retailinvasion.

In general, Wai-Man's competitive responsestarget large general merchandise retailers orgrocers (e.g.. Home Depot, Best Buy, andKroger), not small niche-oriented specialtyretailers. As category killers fight more amongthemselves, their success is less connected withan ability to dwarf smaller retailers, than with an

ability to attack and defeat other category killers(Barta. Manin. et al, 1999). The sale of Toys-R-Us in 2OO.'i demonstrates the rise ofone categorykiller and its subsequent fall at the hands ofother big boxers.

The process of formulating a competitiveresponse to Wal-Mart can be a challenge tosmall retailers if their managers do not under-stand local demographics or how customersmake shopping decisions. The Wal-Mart threatis greatest for a retailer whose survival has beenhistorically based on a lack of competition, noton proflciency in meeting the needs of certaincustomers. Clearly, such businesses are not ina position to evaluate altemative strategic re-sponses to Wai-Man until they develop a clearunderstanding of their own resource advantagesand vulnerabilities.

Patience can be a vinue when battling a cat-egory killer like Wal-Miul. It is not unusual forthe new category killer to offer steep discountsand an abundance of helpful employees at theoutset, only to ease prices higher and eliminatesome of the extra help after some of the smallercompetitors will have been eliminated from thescene (Grantz and Mintz, 1998). Existing retail-ers often suffer the most during this initial timeperiod, but not always.

Wal-Mart's effects on other retailers are notuniversally negative. When a large generalmerchandiser like Wai-Man comes to town itoften increases the "pull factor," resulting in anoverall increase in sales revenue for the commu-nity as a whole. Total general merchandise salesfor the town may increase by as much as 50% ormore during the first year or two. but usuallybegin to decline after five years. Revenues fromsome stores, like those specializing in homefumishings. typically benefit from Wal-Mart'spresence. The effect on other outlets such asclothing stores is not as evident. Nonetheless,tax revenues from sales in the "Wai-Man town"generally outpace those in communities withouta Wai-Man, which is why effons to convincepoliticians to block entry into a community aregenerally ineffective (Stone, 1993).

Big boxers affect retailers within close prox-imity, with two imponant caveats. First, not allretailers are affected equally. Retailers withsimilar product lines may be affected moredirectly than those with altemative or comple-mentary product lines. Restaurants, for example,typically benefit from a big box locating nearbybecause ofthe increased traffic in the immediatearea.

18 SAM ADVANCED MANAGEMENT JOURNAL

Second, retailers Iocated miles away may beadversely affected when a new big box opens.Traffic patterns tnay shift as consumers locatedcloser to a traditional retailer decide to drive alonger distance to shop at the big box. Thiseffect is exacerbated when other retailers "clus-ter" around the big box, drawing even morepotential store traffic away from retailers inother locales.

Given Wal-Mart's array of resource strengthsand shortcomings, three strategic approachesmay be utilized vis-a-vis Wal-Mart. Porter's(1980) strategy typology serves as a usefulframework for illustrating the first two of thesealternatives, as elaix)rated below.

• Strategy 1: Focus-Low Costs

"We can beat Wc/Z-Mart at its own game as longas we fight on our own turf."According to the focus-low cost strategy, theretailer should compete on the basis of costs,hut not target the mass market. Online auctionfacilitator eBay is replete with microbusinessesselling a few products at rock-bottom prices. Inmany cases these sellers undercut the big boxersby marketing only a iimited number of productsto a highly defined end user. By minimizingoverhead, targeting specific buyers, and offeringconvenience — no trip to the store is required —these microbusinesses beat the big boxers attheir own game, but only on a very small pieceof turf. This approach mimics what Porter(1980) termed a focus-low cost strategy. Em-pirical research supports the effectiveness ofthisapproach among select small retailers, especiallythose that operate in hostile and intensely com-petitive environments (McGee and Rubach,1996/1997).

It is difficult for rivals to match thesuperstores on price because they typically lackthe volume to negotiate better deals from theirsuppliers. In some cases, however, a smallerretailer can emphasize a limited number of"products and achieve a substantial volume.Alternatively, a small retailer can join with thosein other communities to strengthen its bargain-ing power. Trade associations may be abie todirect small retailers to "co-ops" that are alreadyengaged in this process. Co-ops typically wel-come newcomers in an effort to drive volumeseven higher.

Interestingly, Wal-Mart prices are not alwaysthe lowest. One study reports that prices at thebig box are actually higher for approximately

one-third of their products compared with othermajor competitors in key U.S. markets (Craw-ford and Mathews. 2001). Astute competitorsmay be able to compete with WaKMart on pricewithin the boundaries of specific product linesand customer groups.

Aldi provides an example of a not-so-big boxthat competes effectively by employing a focus-low cost strategy. Aldi is an intemationai retailerthat offers a limited assortment of groceries andrelated items at the lowest possible prices. Func-tional operations are all focused on minimizingcosts, and efforts are targeted to consumers withlow-to-moderate incomes.

Aldi minimizes costs a number of ways. Mostproducts are private label, allowing Aldi tonegotiate rock-bottom prices from its suppliers.Stores are modest in size, much smaller thanthose of a typical chain grocer. Aldi only stockscommon food and reiated products, maximizinginventory turnover. The grocer does not acceptcredit cards, eliminating the 2-4% fee typicallycharged by banks to process the transaction.Customers bag their own groceries and musteither bring their own bags or purchase themfrom Aldi for a nominal charge. Aldi also takesan innovate approach to the use of its shoppingcarts in its U.S. stores. As in many Canadianstores, customers insert a quarter to unlock acart from the interlocked row of carts locatedoutside the store entrance. The quarter is re-turned when the cart is locked back into thegroup. As a result, no employee time is requiredto collect stray carts unless a customer is willingto forego the quarter by not returning the cart.

Like Aldi. rival chain Save-A-Lot has found away to compete successfully against Wal-Mart.The grocery store pursues locations in urbanareas rejected by Wal-Mart and offers pricescompetitive with the big box. Save-A-Lot gener-ates profits by opening small, cheap storescatering to households earning less than $35,000a year. Save-A-Lot stocks mostly its own brandof high-turnover goods to minimize costs andeschews pharmacies, bakeries, and baggers(Adamy, 2005).

Dollar General is an example of a generalmerchandiser that has adopted a focus—low coststrategy, coupled with an emphasis on customeraccess. Prices are kept to a minimum, althoughthey may not be as low as those at Wal-Mart forcommon items. Dollar General also offersdeeply discounted store-branded products. Thekey, however, is that unlike Wal-Mart, DollarGeneral positions its stores for easy access.

SPRING 2008 19

Customers can easily park, enter the store, andmake their purchases (Crawford and Mathews,2001).

• Strategy 2: Focus-Differentiation

"Wal-Mart simply cannot meet the needs of ourcustomers."One approach for successfully competingagainst a big box requires a recognition thatcosts must be kept under control, but that lowcosts — and low prices — cannot serve as aneffective basis for that competition. Retailersadopting a focus-differentiation strategy eschewprice competition and compete on the basis ofother factors such as quality, selection, conve-nience, and service. There is mounting evidencethai a number of Wal-Mart's smaller rivals areemploying this approach effectively against thebig box (McWilliams, 2007a).

Michael Porter's low cost-differentiationdichotomy illustrates the conundrum faced bymost businesses. Simply stated, differentiatingproducts or services requires resources, therebyraising one's cost position relative to others inan industry. On the other hand, a strong empha-sis on minimizing costs may limit the use ofadvertising, product development, and the like,all of which enable a firm to differentiate itsoutput. In the end, there is a tendency for lowcosts and differentiation to work against eachother. A business attempting both strategiessimultaneously can end up "stuck in the middle"(Porter, 1980) because implementing the combi-nation strategy is generally more difficult thanimplementing either the low-cost or the differen-tiation strategy alone.

In many cases, however, it is not necessary toabandon cost containment to pursue differentia-tion. The key point is this: Consumers may bewilling to pay a somewhat higher price for aproduct similar to one offered by the hig box ifthey believe that other factors — quality, conve-nience, location, service, favorable terms, etc. —compensate for the higher price. At some point,however, the perceived worth ofthe nonpricefactors may not be substantial enough to warrantthe higher price, or the price difference will betoo great for potential customers to afford. AsToby Kaye, owner of two computer stores inBaltimore put it, the smaller retailer does notneed to match prices, but they need to be "withinstriking distance" (McCune. 1994). The problemis that many small retailers do not consider whatthe market will bear when pricing their merchan-

dise. They may simply add a set percentage totheir costs instead of viewing pricing strategiesas a competitive weapon. One proven approachin the convenience store market segment is toprice commonly-purchased goods such as milkand bread at competitive prices but make itnecessary for customers to walk past dozens ofother products that are priced at a premium toget to those goods, hoping impulse buying willoccur.

Specialization can also be an excellent ap-proach to combating the big box. Stores likeWal-Mart are masters of breadth, not depth.Due to the smaller margins, big box stores areusually able to carry only high-demand products.Smaller retailers can carve out a niche by carry-ing related items or product lines that the bigboxers do not. Examples can be found through-out America's small towns in areas such ashardware, auto parts, and sporting goods.

Small retailers are also better equipped totailor their product and service lines to localtastes. Limited product line variations are com-mon among big boxers and are necessary toachieve economies of scale. In many lines ofbusiness, however, local tastes may differ sub-stantially from the generic approach, providingopportunities to rivals to fulfill these needs.Empirical research supports the effectiveness ofthis type of "focus" approach among select smallretailers, especially those that operate in hostileand intensely competitive environments (McGeeand Rubach, 1996/1997). Smaller retailers mayeven succeed by cooperating with their big boxrivals, not competing with them.

As the world's largest retailer, Wal-Mart is alightning rod for attention, negative publicity,and legal confrontations, resulting in almost5,000 lawsuit defenses in 2004 alone (Willing,2001). Simply stated, the volume of businesstransacted at a big box such as Wal-Mart canreadily take a toll on customer service. Hence,providing consistent service is always a chal-lenge, particularly at the big boxers where em-ployees may lack expertise in their respectivedepartments. Today's consumer is strapped fortime and more selective than in the past. Womenare spending less time shopping, and manyconsumers are shopping more on the Intemet(Barta, Martin, Frye, and Woods, 1999; Spector,2005).

Rigby and Haas (2004) suggest that com-peting with Wai-Man requires some retailersto segment their customer bases and "wow'the ones that matter. This can be done through

20 SAM ADVANCED MANAGEMENT JOURNAL

expanding signature categories, customizinglocal assortments, focusing on personal atten-tion, and raising loyalty benefits to customers.Consider the case of Dick's, a small grocerychain in the Midwest. Dick's culls names ofnewcomers and birth and wedding announce-ments from local newspapers. New arrivals andnewlyweds receive letters of congratulations andcoupons from Ihc nearest store. Follow-up lettersare sent to lure customers into stores on a consis-tent basis (Kawasaki, 1995).

The emphasis on service among grocers hasextended to the implementation of loyalty cards.A number of grocers have implemented loyaltyprograms to track purchase behavior and rewardrepeat customers. Given Wal-Mart's emphasison efficiency and low prices, the big box is notin a position to get to know individual customersand local buying patterns like other retailers maybe. Such programs have met with mixed results,however.

Department store Nordstrom's emphasizesexceptional service. The typical Nordstrom'sdepartment store carries 150,0(X) pairs of shoesof virtually every size and width, with an on-lineinventory of over 20 million pairs. The retaileralso provides shoe shines, spas for women, andeven a concierge service (Spector, 2001).

Although Wal-Mart's wages are competitive,they are not as high as many of their competi-tors. Competitors may be able to recruit innova-tive employees with above-market wages,providing them with opportunities to be morecreative in their work. Developing and empha-sizing distinctive competencies is critical, andhuman resources can be a key means of doing so(McGee and Peterson, 2000).

• Strategy 3: Value Orientation

"Wal-Mart might offer a htXX&v price, but weoffer a better value."Rather than focus solely on costs and prices ormeans of differentiation, a distinct approachseeks to blend the two into a superior valueproposition for the retailer. Such rivals competeon the basis of value by controlling costs vigor-ously whenever such costs do not directly andsignificantly enhance the attractiveness ofptod-ucts or .services. Value can be viewed as a formof differentiation, but it is distinguished by itsco-emphasis on cost leadership.

Value can be expressed as the ratio of per-ceived worth to price and can rise when theproduct or service's perceived worth increases or

its price decreases. In essence, Wal-Mart hastaken the simplest approach to create value,minimizing prices. Other formulas for creatingvalue exist, however, aithough they require adetailed understanding of consumer tastes andpreferences as they relate to a given retailer'sline of business.

Wal-Mart's one-size-fits-all approach pre-cludes it from exploring some of these alterna-tives in an efficient manner, especially at thelocal level. One way to improve one's valueproposition reiative to that of Wal-Mart is toadd relatively inexpensive features or serviceswhen they increase the perceived value of theoffering considerably, especially when Wal-Mart is not in a position to integrate a similarapproach. Delivery — whether free or for anominal charge — is a common example of ameans of enhancing perceived value, as areexpertise ;md repair, real services after a sale.

The value orientation strategy begins with anorganizational commitment lo quality productsor services, thereby differentiating a firm fromits competitors. Because customers may bedrawn to high quality, demand may rise, result-ing in a larger market share, providing econo-mies of scale that permit lower per-unit costs inpurchasing, manuf'acturing, fmancing. researchand development, and marketing. In this regard,a firm can seek to provide maximum value bydifferentiating products and services only to theextent that any associated cost hikes can bejustified by increases in overall value and bypursing cost reductions that result in minimal. Ifany, reductions in value.

Conceptually, this strategic approach may beviewed as a hybrid of the other two. although itis qualitatively different. Value-oriented retailersdo not merely seek a middle position betweenthe low-cost and differentiation strategies, anapproach Porter (1985) suggested can leavecompetitors stuck in the middle. Alternatively,such retailers consciously seek cost and pricepositions that may be nominally higher thanthose of big boxers like Wai-Mart, but alsoenhance their offerings so that additional value iscreated. Store managers can be trained to recog-nize pricing opportunities or vulnerabilities intheir individual markets. In addition, supplychains must be examined, labor deploymentmanaged, and overhead wastes eliminated if thisvalue orientation is to be viable (Rigby andHaas, 2004).

In a study of independent drugstores, McGeeand Peterson (2000) found that competitive

SPRING 2008 21

advantage could be achieved through ati imageof high-quality service. This perception of highquality by the customer is driven by an ability toact decisively, control retail programs related toprice, and overwhelm customers with service,particularly the handling of complaints. Theyreported thai these drugstores were successfultlirough the implementation of three compe-tency-based constructs and only one perfor-mance-based construct.

Arkansas-based grocer Harp's, for example,has grown to about 50 stores by maintainingcompetitive prices, but also emphasizing serviceand freshness. By maintaining price levels closeto those at Wal-Mart, Harp's is able to lurecustomers who are willing to pay a little morefor enhanced services and produce freshness.Harp's has discovered how to balance price andother competitive factors to produce value for itscustomer base.

ConclusionsThe Wal-Mart footprint has created numerouschallenges for competitors, particularly smallretailers whose managers are not well preparedwhen the big boxer opens a store nearby. In2006, Wal-Mart began to implement a low-cost/differentiation strategy, focusing at first on sixdemographic groups in the U.S. (Zimtnerman,2006). The decades-old layaway plan was dis-continued and a celebrity line of home decorfrom Colin Cowie was added (Kabel, 2006).Store upgrades include specialists in the area ofelectronics for consumers interested in those bigticket items, products targeting Hispanic shop-pers, more upscale merchandise for affluentconsumers such as those who shop at the Piano.Texas. Wal-Mart, and a better variety of productsthat appeal directly to the African-Americancommunity {Zimmemian, 2006). Early indica-tions of this attempt to attract upscale consumersto the supercenters are negative as It appears thestrategy is not taking hold (McWilliams. 2007b).

As if this wasn't daunting enough. Wal-Marthas embarked on a "green" strategy of environ-mental conservation and protection that not onlyincludes its stores but also the suppliers of itsproduct lines (Gunther, 2006). Early goals in-clude 25% increased vehicle efficiency, 30%reduction in energy consumed by stores, and a25% reduction in solid waste. Eventually, CEOLee Scott wants to get rid of chemicals in the airaround production facilities, smog in cities, andanything bad that is now going into a river(Gunther, 2006). The concept of going green

originated with Sam Walton's son, Rob, but waspropelled to fruition by two things: Wal-Marthas been fending off criticism for its environ-mental unfriendliness for years, costing it ap-proximately 8% of its former customers, and the"green" strategy might just save the firm moneyin the long run.

These challenges can be addressed success-fully, however, when retailers understand howtheir resource strengths and weaknesses comparewith those of the big boxer. Under certain situa-tions, a retailer may be successful by focusingon a market niche in conjunction with either lowcosts or differentiation, or by incorporating avalue orientation. Dynamic strategic positioningmodels can also be utilized to augment theseapproaches. By emphasizing flexibility andadaptability, a dynamic strategy approach canenable a small, nimble firm to respond to indus-try and environmental changes more rapidly thanbig boxers like Wal-Mart.

Although a number of published studies haveidentified various examples of retailers that havecompeted effectively with big boxers like Wal-Mart, no panacea has emerged. This paperprovides a number of examples as well, butintegrates them with three strategic approachesbuilt on existing theory. A focus—differentiationstrategy may be the most intuitively appealingfor many retailers. Indeed, this basic approachseems to be the strategy of choice for manyresearchers investigating the big box phenom-enon, although it is not optimal for all retailers.When a retailer combines this approach with aflexible, dynamic competitiveness perspective,such as the development of a network of suppli-ers that provide enough variety to rotate severalproduct-supported themes through the storeduring the year, providing a different look everyfew months, it can devise a strategy that a bigboxer cannot duplicate. However, Wal-Mart'srecent interest in smaller iind higher-end stores— if executed — might create a strategic re-sponse problem for smaller, higher-end competi-tors {McWilliams, 2007b).

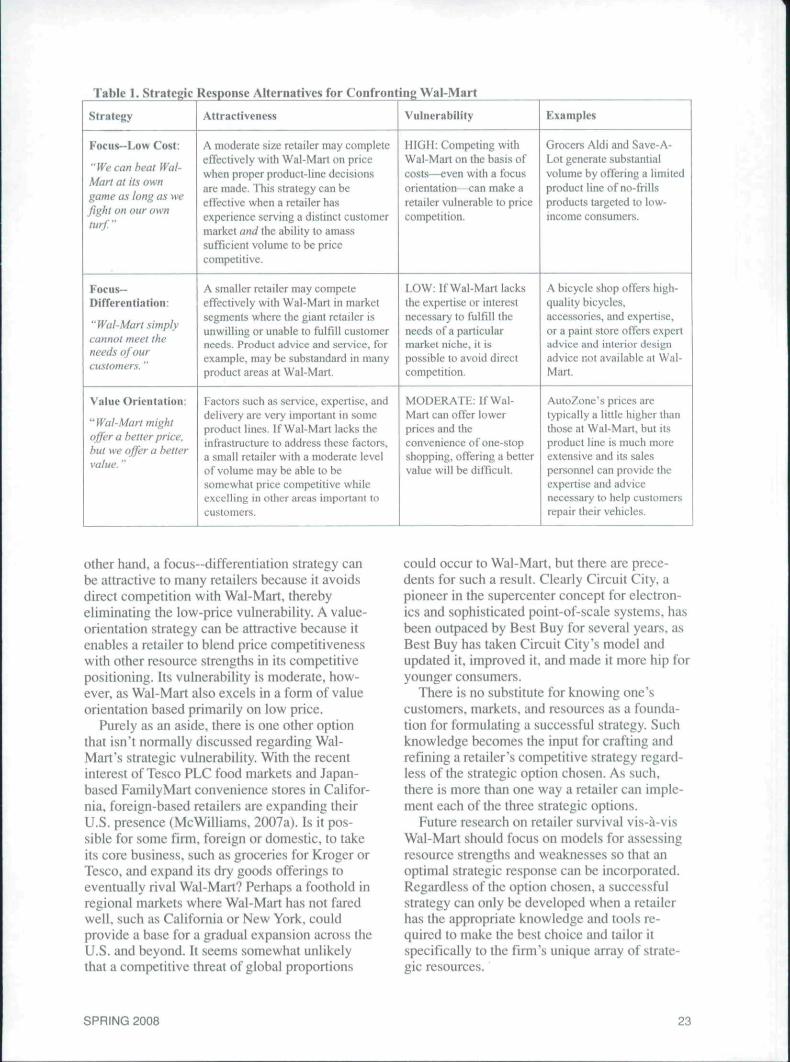

The most appropriate strategic approachdepends on the firm and its unique situation.Indeed, each strategy has its own strengths andvulnerabilities, as summarized in Table 1. Afocus—low cost strategy can be attractive be-cause it limits the areas in which a retailer mustcompete with Wal-Mart on price, but it is highlyvulnerable to a competitive response because itrelies on the very strategic dimension that is coreto the big boxer's success, low price. On the

22 SAM ADVANCED MANAGEMENT JOURNAL

Table 1. Strategic

Strategy

Focus-Low Cost:

"We can heat Wal-Mart at its owngame as long as wefight on our ownturf."

Focus-Differentiation:

"Wai-Marl simplycannot meet theneeds of ourcustomers."

Value Oricntatiou:

""Wal-Mart mightoffer a better price,iyui we offer a bettervalue."

Response Alternatives for Confronting Wal-Mart

Attractiveness

A moderate size retailer may completeeffectively with Wal-Mart on pricewhen proper product-line decisionsare made. Tliis strategy can beeffective when a retailer hasexperience serving a distinct customermarket and the ability to amasssufficient volume to be pricecompetitive.

A smaller retailer may competeefTectively with Wal-Mart in marketsegments where the giant retailer Isunwilling or unable to fulfill customerneeds. Prt>ducl advice and service, forexample, maybe substandard in manyproduct areas at Wal-Mart.

Factors such as service, expertise, anddelivery are very Important in someproduct lines. If Wal-Mart lacks theinfrastructure to address these factors,a small retailer with a moderate levelof volume may be able to besomewhat price competiiive whileexcelling in other areas important tocustomers.

Vulnerability

HIGH: Competing withWal-Mart on the basis ofcosts—even with a focusorientation—can make aretailer vulnerable to pricecompetition.

LOW: If Wal-Mart lacksthe expertise or interestnecessary to fulfill theneeds of a particularmarket niche, it ispossible to avoid directcompetition.

MODERATE: If Wal-Mart can offer lowerprices and theconvenience of one-stopshopping, offering a bettervalue will be ditficult.

Examples

Grocers Aldi and Save-A-Lot generate substantialvolume by offering a limitedproduct line of no-trillsproducts targeted to low-income consumers.

A bicycle shop oOers high-quality bicycles,accessories, and expertise,or a paint store offers expertadvice and interior designadvice not available at Wal-Mart.

AutoZone's prices aretypically a little higher thanthose at Wal-Mart, but itsproduct line is much moreextensive and its salespersonnel can provide theexpertise and advicenecessary to help customersrepair their vehicles.

Other hand, a focus—differentiation strategy canbe attractive to many retailers because it avoidsdirect competition with Wal-Mart, therebyeliminating the low-price vulnerability. A value-orientation strategy can be attractive because itenables a retailer to blend price competitivenesswith other resource strengths in its competitivepositioning. Its vulnerability is moderate, how-ever, as Wai-Mart also excels in a form of valueorientation based primarily on low price.

Purely as an aside, there is one other optionthat isn't nonnally discussed regarding Wal-Mart's strategic vulnerability. With the recentinterest of Tesco PLC food markets and Japan-based FamilyMart convenience stores in Califor-nia, foreign-based retailers are expanding theirU.S. presence (MeWilliams. 2007a). Is it pos-sible for some firm, foreign or domestic, to takeits core business, such as groceries for Kroger orTesco, and expand its dry goods offerings toeventually rival Wal-Mart? Perhaps a foothold inregional markets where Wal-Mart has not faredwell, such as California or New York, couldprovide a base for a gradual expansion across theU.S. and beyond. It seems somewhat unlikelythat a competitive threat of global proportions

could occur to Wal-Mart, but there are prece-dents for such a result. Clearly Circuit City, apioneer in the supercenter concept for electron-ics and sophisticated point-of-scale systems, hasbeen outpaced by Best Buy for several years, asBest Buy has taken Circuit City's model andupdated it, improved it. and made it more hip foryounger consumers.

There is no substitute for knowing one'scustomers, markets, and resources as a founda-tion for formulating a successful strategy. Suchknowledge becomes the input for crafting andrefinitig a retailer's competitive strategy regard-less of the strategic option chosen. As such,there is more than one way a retailer can imple-ment each of the three strategic options.

Future research on retailer survival vis-a-visWal-Mart should focus on models for assessingresource strengths and weaknesses so that anoptimal strategic response can be incorporated.Regardless of the option chosen, a successfuistrategy can only be developed when a retailerhas the appropriate knowledge and tools re-quired to make the best choice and tailor itspecifically to the firm's unique array of strate-gic resources.'

SPRING 2008 23

Dr. Parnell has published over 200 basic andapplied reseaich articles, presentations, andcases in strategic management and relatedareas. Dr. Lester has published works in numer-ous journals in the fields of strategic manage-ment, entrepreneurship. and organizationaltheory.

REFERENCESAdamy, J. (2005, August 30). To fmd growth, no-frills grocer

goes where other chains won't. Wall Street Journal, pp,A1.A8.

Bain, J.S. (1968). Industrial Organization. New York. Wiley.Barnett, M.L. (2006). Finding a working balance between

competitive and communal strategies. Journal of Manage-ment Studies. 4.i. 1753-1773.

Bamey, J.B. (1986). Strategic factor markets: Expectations,luck, and business strategy. Management Science. 42.1231-1241.

Barta. S.. Martin, J, Frye. J., and Woods, M.D. (1999). Trendsin retail trade. Stillwater. Oklahoma: Cooperative Exten-sion Service.

Berman. D.. Adamy. J.. and Sender. H. (2tX)5. March 16).Cerberus nears deal for Albertson 's. Wall Street Journal.A3, A15.

Camerius. J. (2006). Wal-Mart stores. Inc.: On becoming theworld's largest company. In T, Wheelen, and J.D. Hunger,Cases in Strategic Management and Business Policy. Up-per Saddle River, NJ: Pearson Prentice Hall. p. 18-1-18-21.

Chittum.R. (2005, March 1). Anchors away! Wall Street Jour-nal On-Line Edition.

Crawford. F. and Mathews. R. (2001). The myth of excel-lence. New York: Crown Business.

Edid. M. (2005). The Good, the bad. and Wal-Mart. Ithaca.NY: Cornell University Institute of Workplace Studies.

Etter, L. (2005. December). Gauging the Wal-Mart effect. WallStreet Journal. 3—4, p. A9.

Fiegenbaum. A., and Thomas, H. (2004). Strategic risk andcompetitive advantage: An integrative perspective. Euro-pean Management Review. 1(1). 84-95.

Fishman, C. (2003). The Wal-Mart you don't know. FastCompany, 77.68.

Grantz. R.B., and Mintz. N. (1998). Cities back from the edge.New York. Preservation Press.

Goldberg. J. (2006. August 25). Dems have bad case ofWMDS. The Commercial Appeal. AlO.

Gunther, M. (2006). The green machine. Fortune, 154(3). 42-57.

Hannaford, S. (2005). Both sides now. Harvard BusinessW*T/CM,83(3). 17.

Hawawini. G.. Subramanian, V., and Verdin. P. (2003). Isperformance driven by industry — or firm-specific fac-tors? A new look at the evidence. Strategic ManagementJournal. 24. 1-16.

Kabel. M. (2006, September 15). Wal-Mart ends layaway plan,adds celebrity decor line. USA Today, 9A.

Kaplan. E. A. (2006. August 25). Wal-Mart mouthpiece gagson his foot. The Commercial Appeal, AlO.

Kawasaki. G. (1995). How to drive yotir competition crazy.New York: Wesley Publishing.

Lado. A., Boyd, N., :ind Wright, P. (1992). A competency-based model of sustainable competitive advantage: Towarda conceptual integration. Journal of Management, IH( \),

77-91.Mallaby, S. (2005. November 29). Wal-Mart: A progressive

dream company, really. Fayetteville Ohsen>er, p. 11 A.McCune. J. C. (1994). Inthe shadow of Wal-Mart. Manaj?f-

ment Review. S3{\2), 10-16.McGee, J. E. and Peterson, M. (2000). Toward the develop-

ment of measures of distinctive competencies among smallindependent retailers. Journal of Small Business Manage-ment. Ml). 19-33.

McGee. J,E.. and Rubach, MJ. (1996/1997). Responding toincreased environmental hostility: A study of the com-petitive behavior or small retailers. Journal of AppliedBu.siness Research. IS{ 1). 83-94.

McGirt. E. (2006). A banner year. f>»-mHc. }53{1), 192-195.McWilliams. G. (2007a. October 3). Wal-Mart era wanes amid

shifts in retail. Wall Street Journal. ALMcWilliams, G. (2()O7b. August 17). Wal-Mart eyes smaller

and higher-end stores. Wall Street Journal, BI.Novak, R. (2006, September 18). Chicago mayor shows la-

bor lagging in Wal-Mart vote. Daily News Journal, B2.Porter. M.E. (1980). Competitive .strategy. New York: Free

Press.Quinn, B. (2000). How Wal-Mart is destroying America. Ber-

keley. CA..Ten Speed Press.Raymond. J. (1999. January). The millennial mind-set. Ameri-

can Demographics, 60-65.Revell, J. (2005). Up, up. and away. Fortune, /5/(8), 232-

236.Rigby. D., and Haas, D. (2004). Outsmarting Wal-Mart.

Harvard Business Review, S2( 12). 22-26.Selsky, J.W., Goes, J., and Baburoglu. O.N. (2007). Contrast-

ing perspectives of strategy making: Applications in'hyper'envimnments. Organization Studies. 28. 71-94,

Seth, A., and Thomas, H. (1994). Theories of the finn: Impli-cations for strategy Tsaearch. Journal of Management Stud-ies. 31. 165-191.

Spector, R. (2001). Lessons from the Nordstrom way. NewYork: Wiley and Sons.

Spector. R. (2005), Category killers. Boston, Harvard Busi-ness School Press.

Stone. K.E. (1993). Impact of the Wal-Mart phenomenon onrural communities. Increasing Understiuiding of PublicProblems and Policies, Chicago.

Useem. J, (2007). The big get bigger. Fortune, /55(8), 81 -84.Will. G. (2006a. January 19). Union's touch is felt in Wal-

Mart legislation. Daily News Journal. B2.Will. G. (2006b, September 15). Liberals can't handle deals

at Wal-Mart. Daily News Journal. B2.Willing. W. (2001, August 13). Lawsuits a volume business

at Wal-Mart. USAToday.com.York, B. (2(K)5. November 23). Panic in a small town. Na-

tional Review (on-line).

24 SAM ADVANCED MANAGEMENT JOURNAL