Embed Size (px)

Citation preview

Competition Links and Stock Returns

Assaf Eisdorfer1 Kenneth Froot2 Gideon Ozik3 Ronnie Sadka4

1University of Connecticut2Harvard Business School

3EDHEC4Boston College

Oct 2019

1

Motivation

The information content of corporate financial statements has been explored for many years

The common objective of these studies:• To assess what investors can learn about a certain company

from the information embedded in its financial statements

Our study:• What we can learn about a company from the point of view

of its competitors

A firm being aimed at earns high returns:• Indicates attractive business opportunities?• Presents risk of business disruption?

2

How to measure competition?

Competition section in 10-K filings

Check which firms are being pointed at – strong competitors

• Technological challenges

• But not all mentions are created equally!

• A mention by a major competitor should count more than a mention by a minor competitor

Competition status should be evaluated simultaneously across all firms

• Implement a Google PageRank-type algorithm

3

Measuring competition Measuring a given firm’s competition strength from the

competition-link system across all firms

Firm A 10-K

Competition:

Firm B

Firm B 10-K

Competition:

Firm C

Firm C 10-K

Competition:

Firm A

Firm B

4

Measuring a given firm’s competition strength from the competition-link system across all firms

Firm A 10-K

Competition:

Firm B

Firm B 10-K

Competition:

Firm C

Firm C 10-K

Competition:

Firm A

Firm B

Measuring competition

• 𝐶𝐶𝐶𝐶 𝐴𝐴 = 1−𝑑𝑑𝑁𝑁

+ 𝑑𝑑 × 𝐶𝐶𝐶𝐶(𝐶𝐶)2

• 𝐶𝐶𝐶𝐶 𝐵𝐵 = 1−𝑑𝑑𝑁𝑁

+ 𝑑𝑑 × 𝐶𝐶𝐶𝐶 𝐴𝐴 + 𝐶𝐶𝐶𝐶(𝐶𝐶)2

• 𝐶𝐶𝐶𝐶 𝐶𝐶 = 1−𝑑𝑑𝑁𝑁

+ 𝑑𝑑 × 𝐶𝐶𝐶𝐶(𝐵𝐵)

5

Measuring a given firm’s competition strength from the competition-link system across all firms

Firm A 10-K

Competition:

Firm B

Firm B 10-K

Competition:

Firm C

Firm C 10-K

Competition:

Firm A

Firm B

Measuring competition

• 𝐶𝐶𝐶𝐶 𝐴𝐴 = 1−𝑑𝑑𝑁𝑁

+ 𝑑𝑑 × 𝐶𝐶𝐶𝐶(𝐶𝐶)2

• 𝐶𝐶𝐶𝐶 𝐵𝐵 = 1−𝑑𝑑𝑁𝑁

+ 𝑑𝑑 × 𝐶𝐶𝐶𝐶 𝐴𝐴 + 𝐶𝐶𝐶𝐶(𝐶𝐶)2

• 𝐶𝐶𝐶𝐶 𝐶𝐶 = 1−𝑑𝑑𝑁𝑁

+ 𝑑𝑑 × 𝐶𝐶𝐶𝐶(𝐵𝐵)

Assuming 0.7 damping factor:

• 𝐶𝐶𝐶𝐶 𝐴𝐴 = 0.2314• 𝐶𝐶𝐶𝐶 𝐵𝐵 = 0.3933• 𝐶𝐶𝐶𝐶 𝐶𝐶 = 0.3753

6

The C-Rank measure of competition

The C-Rank is not an independent assessment based on observed firm characteristics, such as firm size or product market share

Rather, it reflects the collective view of all companies on who the strong competitors in the market are

This feature can identify an element of a firm’s profile• We find high C-rank firms significantly outperform

Hypotheses:• Mispricing: High C-Rank signifies business opportunities; investors

do not understand/inattentive to information• Risk: High C-Rank signifies risk of business disruption; the risk

might be undiversifiable

7

Data

119,785 10-Ks filed by 11,304 firms over 1995-2017

68,952 reports (58%) include a competition section

# of firms in a single competition section ranges between zero (61% of the reports) to 35

69% of firms are not mentioned at all in other reports

Most mentions in a given year:IBM: 136 mentions in 1997Microsoft: 113 mentions in 1999

8

C-Rank properties

C-Ranks calculated each month using the most recent annual report of every firm over the past twelve months

Information sets:• Full sample; Cross sector; Within sector

C-Rank statistics (x100)

C-Rank correlated with size (~50%)• Orthogonalize in the cross-section each month• Also use non-parametric approach

9

Mean StDev Min p25 P50 p75 MaxC-Rank full sample 0.0191 0.0075 0.0169 0.0169 0.0169 0.0183 0.2333C-Rank cross-sector 0.0215 0.0073 0.0201 0.0201 0.0201 0.0201 0.2448C-Rank within-sector 0.2315 0.2330 0.0941 0.1156 0.1357 0.2321 3.5178

Returns of portfolios sorted by C-Rank

Each month sort stocks into five equal-size portfolios byC-Rank (orthogonalized to size)

Hold the portfolios for one month

low high1 2 3 4 5 5-1

Mean excess return (monthly) 0.77 0.87 0.80 0.97 1.70 0.93

(2.60) (2.40) (2.25) (2.55) (4.03) (3.76)

Alpha (monthly) -0.10 0.03 0.12 0.61 1.24 1.35(-1.62) (0.47) (1.04) (3.18) (7.23) (7.00)

10

Cross- and within-sector analysis

Separately recalculate C-Rank cross- and within-sector Each month sort stocks into five equal-size portfolios

Cross-sector C-Rank

low high

1 2 3 4 5 5-1

Mean excess return 0.80 0.87 0.93 0.90 1.61 0.81

(2.71) (2.39) (2.39) (2.42) (3.87) (2.87)

Alpha 0.00 0.00 0.15 0.44 1.30 1.30

(-0.03) (-0.01) (1.50) (2.56) (5.58) (5.22)

Within-sector C-Rank

low high

1 2 3 4 5 5-1

Mean excess return 0.96 0.93 0.97 1.33 0.94 -0.01

(1.98) (2.87) (3.06) (3.36) (2.98) (-0.04)

Alpha 0.59 0.17 0.25 0.70 0.18 -0.41

(3.71) (1.75) (2.34) (4.15) (1.36) (-1.98)

11

Fama-MacBeth regressions C-Rank full market C-Rank cross-sector C-Rank within-sector All firms Competitive firms All firms Competitive firms All firms Competitive firms Intercept 2.87 3.46 2.72 2.63 2.72 3.30

(4.88) (4.67) (4.62) (2.58) (4.80) (4.82) C-Rank 5.45 5.55 2.55 5.72 -0.09 2.13

(3.05) (2.13) (1.89) (1.80) (-0.02) (0.52) Log(size) -0.11 -0.15 -0.10 -0.11 -0.10 -0.14

(-3.21) (-3.51) (-2.94) (-1.79) (-3.05) (-3.73) Log(market-to-book) -0.03 0.03 -0.04 0.00 -0.03 0.06

(-0.75) (0.54) (-0.81) (-0.01) (-0.80) (0.98) Past return 0.56 0.48 0.53 0.31 0.54 0.50

(2.47) (1.41) (2.40) (0.82) (2.43) (1.50) Profitability 0.78 0.37 0.77 0.53 0.77 0.44

(3.72) (1.42) (3.61) (1.48) (3.72) (1.75) Investment -1.74 -1.25 -1.76 -1.42 -1.76 -1.31

(-4.85) (-2.54) (-4.84) (-1.79) (-4.92) (-2.75) Beta 0.00 0.01 -0.01 0.08 -0.01 0.02

(-0.02) (0.08) (-0.04) (0.39) (-0.05) (0.11) Idiosyncratic volatility -31.15 -22.59 -30.63 -16.15 -30.67 -20.39

(-6.30) (-3.88) (-6.15) (-1.63) (-6.11) (-3.59)

C-Rank also significant among high C-Rank firms Cross-sector rather than within-sector effect

12

Portfolio returns over time

13

0.00

1.00

2.00

3.00

4.00

5.00

1995

1996

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

Cumulative performance of C-Rank portfolio spreads

Portfolio excess return Portfolio 6-factor alpha

-0.04-0.02

00.020.040.060.08

0.10.120.140.16

1995

1996

1996

1997

1998

1999

2000

2001

2001

2002

2003

2004

2005

2006

2006

2007

2008

2009

2010

2011

2011

2012

2013

2014

2015

2016

2016

2017

Cumulative FMB regression coefficient of C-Rank

All firms Competitive firms

What have we shown so far?

High C-Rank firms outperform

Performance seems to stem from cross-sector competitors

The C-Rank effect appears monotonic, yet non-linear; exists also within high C-Rank firms

Robustness and persistence over time

14

Competing explanations Mispricing:

• Strong companies point to an undervalued business environment

Risk: • Being targeted by strong companies imposes risk—

underversifiable in periods of high cross-sector disruption

How can we identify explanation?• Test 1: Analyst coverage• Test 2: Changes in C-Rank• Test 3: C-Rank betas

15

Test 1, Analyst coverage

Analysts intensify information diffusion

16

Panel A. Analyst industry concentration

All firms

Firms with analyst

coverage Mean analyst industry concentration Low Mid High High-Low Full market 1.35 0.64 0.50 0.67 0.77 0.27 (7.00) (4.25) (2.99) (3.56) (3.05) (0.84) Cross sector 1.30 0.63 0.30 0.75 1.10 0.80 (5.22) (3.78) (1.69) (3.23) (3.48) (2.48) Within sector -0.41 -0.49 -0.31 -0.62 -0.49 -0.18 (-1.98) (-2.19) (-1.27) (-2.37) (-1.45) (-0.43)

Panel B. Joint analyst coverage

Competitive firms

Competitive with analyst

coverage

Competitive firms share analysts with their mentioning firms

No Yes Diff. Full market 0.55 0.50 0.61 -0.02 0.62 (3.36) (2.66) (2.23) (-0.05) (1.48) Cross sector 0.35 0.18 0.48 -0.14 0.61 (1.86) (0.85) (1.43) (-0.43) (1.64) Within sector 0.02 -0.26 -0.24 -0.13 -0.11 (0.10) (-1.09) (-0.78) (-0.46) (-0.38)

Test 2, Changes in C-Rank

17

-5.0%

-4.0%

-3.0%

-2.0%

-1.0%

0.0%

1.0%

2.0%

-12 -10 -8 -6 -4 -2 0 2 4 6 8 10 12 14 16 18 20 22 24

Months to change in C-Rank

C-Rank Portfolio Excess Return Spreads

Full market Cross-sector Within-sector

Increase in cross-sector C-Rank results in under-performance followed by long-run out-performance

Test 3, C-Rank beta

18

Compute firm C-Rank beta (36-month rolling)• Significant quintile return spread

(0.00)

(0.50)

(1.00)

(1.50)

(2.00)

(2.50)

(3.00)

(3.50)

(4.00)

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

1 2 3 4 5 5-1

T-st

atist

ic

Mon

thly

Ret

urn

C-Rank Beta Quintiles

Alpha T-stat

Test 3, Double sorts

19

Disentangling C-Rank level and beta using double sorts and building neutralized portfolio spreads

C-Rank beta does not explain C-Rank level

Results mostly consistent with mispricing rather than risk

C-Rank-beta return spread

C-Rank Singleneutral sort

Full sample 0.28 0.52[1.71] [2.47]

Cross sector 0.23 0.49[1.44] [2.15]

Within sector -0.25 -0.30[-1.14] [-1.14]

C-Rank return spread

C-Rank-Beta Singleneutral sort

Full sample 0.99 1.35[6.33] [7.00]

Cross sector 0.95 1.30[4.54] [5.22]

Within sector 0.12 -0.41[0.83] [-1.98]

The importance of the C-Rank features

The C-Rank measure has two unique features:

(1) A given firm’s competition is determined not only by its own financial statement but also by what other firms say about the given firm

(2) It gives more weight to the stronger firms (i.e. those that more firms mention them as competitors)

We show that both these features are important in capturing the competition strength and return predictability

20

C-Rank Feature 1: Own versus All

Event-time analysis: Buy-and-hold abnormal return of companies with under-and over-performing targeting firms

21

-3%-2%-1%0%1%2%3%4%5%6%

0 3 6 9 12 15 18 21 24

Months from portfolio formation

Cross-sector targeting firms

Targeting firms did well in the past year

Targeting firms did poorly in the past year

-3%

-1%

1%

3%

5%

0 3 6 9 12 15 18 21 24

Months from portfolio formation

Within-sector targeting firms

Targeting firms did well in the past year

Targeting firms did poorly in the past year

Outperforming cross-sector competition negatively impacts firm

C-Rank Feature 1: Own versus All – cont’d

22

-6%

-4%

-2%

0%

2%

4%

6%

0 3 6 9 12 15 18 21 24

Months from portfolio formation

Cross-sector mentioned firms

Mentioned firms did well in the past year

Mentioned firms did poorly in the past year

-6%-5%-4%-3%-2%-1%0%1%2%3%4%5%

0 3 6 9 12 15 18 21 24

Months from portfolio formation

Within-sector mentioned firms

Mentioned firms did well in the past year

Mentioned firms did poorly in the past year

Assess a firm’s competition using companies mentioned as competitors in that firm’s reports alone

Competition gauged from own firm reports behave differently

C-Rank Feature 2: Strong competitors

23

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

1.60%

C-Rank Number oftargeting firms

Mean size oftargeting firms

Sum size oftargeting firms

Quintile portfolio spreads

Excess return 6-factor alpha

C-Rank seems to outperform other measures

Conclusions

We implement a PageRank-type algorithm on 10-K filings to produce a dynamic measure of firm competitiveness (C-Rank)

A C-Rank portfolio spread yields an alpha of ~16% annually

Predictability is mainly cross-sector

Consistent with both risk and mispricing:• Seems mostly mispricing

24

THANK YOU!

25

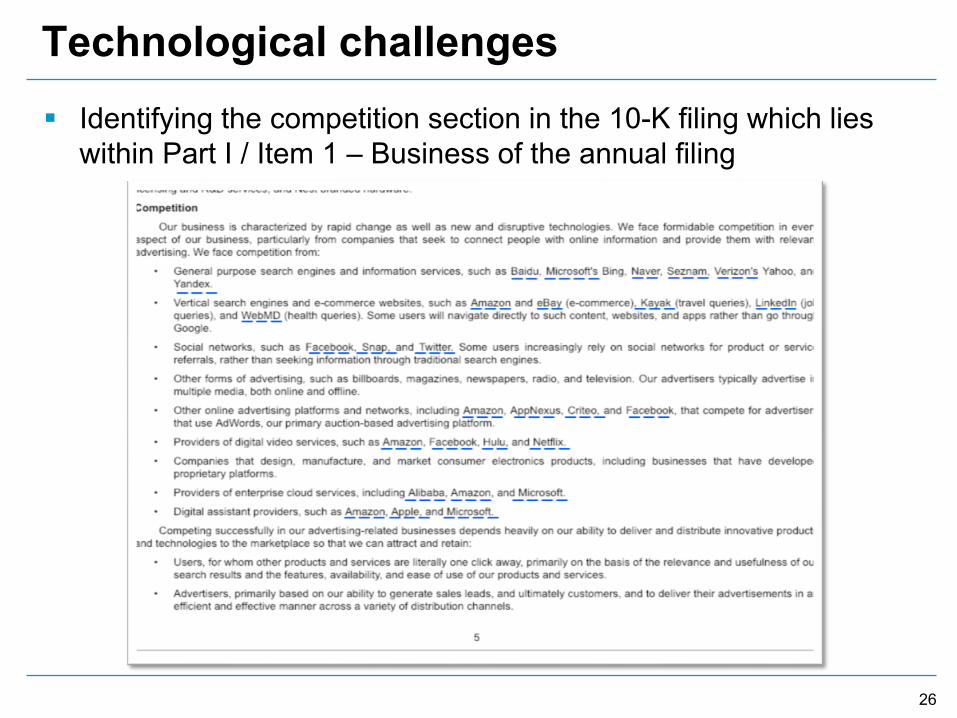

Technological challenges Identifying the competition section in the 10-K filing which lies

within Part I / Item 1 – Business of the annual filing

26

Technological challenges Example: entity extraction of the string “IBM” found in a competition section1. Google search of the

term: “IBM wiki”2. Identifying that the top

listed URL is the Wikipedia page of IBM

3. Accessing the Wikipedia page

4. Extracting ticker and other identifiers from the information box of the Wikipedia page

27

Technological challenges Identifying companies mentioned in the competition: Natural

Language Processing (NLP) methods + textual content analysis

28

Competition mentions in 10-Ks

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

0 1 2 3 4 5 6 7 8 9 10+

# of

repo

rts

# firms mentioned as competitors in a report

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

100,000

0 1 2 3 4 5 6 7 8 9 10+

# of

firm

-yea

rs

# reports in which a firm is mentioned as a competitor during a calendar year

29

C-Rank vs. firm size

Top competitors Largest firms Year 1st 2nd 3rd 4th 5th 1st 2nd 3rd 4th 5th 1995 IBM HPQ GE NIPNY ITC

GE T XOM KO MRK

1996 IBM MSFT HPQ WMT MSI

GE KO XOM INTC MSFT 1997 IBM MSFT HPQ LU JNJ

GE KO MSFT XOM MRK

1998 IBM MSFT HPQ LU MSI

MSFT GE INTC WMT XOM 1999 MSFT IBM LU HPQ MSI

MSFT GE CSCO WMT XOM

2000 MSFT IBM LU HPQ A

GE XOM PFE CSCO C 2001 IBM MSFT MSI SIEGY HPQ

GE MSFT XOM C WMT

2002 IBM MSFT HPQ CSCO GOOGL

MSFT GE XOM WMT PFE 2003 IBM MSFT CSCO WMT JNJ

GE MSFT XOM PFE C

2004 IBM MSFT WMT CSCO NVS

GE XOM MSFT C WMT 2005 IBM WMT MSFT A PFE

GE XOM MSFT C PG

2006 MSFT IBM WMT ELMG ABT

XOM GE MSFT C BAC 2007 IBM MSFT WMT GE GSK

XOM GE MSFT T PG

2008 MSFT WMT IBM GE A

XOM WMT PG MSFT GE 2009 IBM MSFT GE ELMG WMT

XOM MSFT WMT AAPL JNJ

2010 MSFT WMT GE IBM CSCO

XOM AAPL MSFT GE WMT 2011 MSFT IBM GE BAC ELMG

XOM AAPL MSFT IBM CVX

2012 MSFT GOOGL GE WMT IBM

AAPL XOM WMT MSFT GE 2013 GOOGL MSFT AAPL WMT IBM

AAPL XOM GOOGL MSFT GE

2014 GOOGL MSFT IBM FB WMT

AAPL XOM MSFT JNJ WFC 2015 GOOGL FB IBM MSFT MDT

AAPL MSFT XOM AMZN GE

2016 GOOGL FB PFE NVS MDT

AAPL MSFT XOM AMZN JNJ 2017 GOOGL NVS MDT FB PFE

AAPL MSFT AMZN FB JNJ

30

C-Rank correlations

Panel A. Full sample C-Rank full market C-Rank cross-sec C-Rank within-sec

Log(size) 0.568 0.410 0.239 Log(market-to-book) 0.019 0.008 -0.003 Past return 0.008 0.003 0.012 Profitability 0.080 0.051 0.072 Investment -0.018 -0.001 0.083 Beta 0.018 0.001 -0.109 Idiosyncratic volatility -0.107 -0.069 -0.137

Panel B. Competitive firms C-Rank full market C-Rank cross-sec C-Rank within-sec Log(size) 0.583 0.398 0.361 Log(market-to-book) 0.025 0.006 0.000 Past return 0.003 0.002 0.017 Profitability 0.121 0.063 0.127 Investment -0.039 -0.001 0.053 Beta -0.074 -0.081 -0.147 Idiosyncratic volatility -0.170 -0.112 -0.182

31

C-Rank correlations

Panel A. Full sample C-Rank full market C-Rank cross-sec C-Rank within-sec

Log(size) 0.568 0.410 0.239 Log(market-to-book) 0.019 0.008 -0.003 Past return 0.008 0.003 0.012 Profitability 0.080 0.051 0.072 Investment -0.018 -0.001 0.083 Beta 0.018 0.001 -0.109 Idiosyncratic volatility -0.107 -0.069 -0.137

Panel B. Competitive firms C-Rank full market C-Rank cross-sec C-Rank within-sec Log(size) 0.583 0.398 0.361 Log(market-to-book) 0.025 0.006 0.000 Past return 0.003 0.002 0.017 Profitability 0.121 0.063 0.127 Investment -0.039 -0.001 0.053 Beta -0.074 -0.081 -0.147 Idiosyncratic volatility -0.170 -0.112 -0.182

32

Controlling for stock characteristics Double-sort C-Rank portfolio means

6-factor alpha of the high-low C-Rank portfolios Full market Cross-sector Within-sector

Base results 1.35 1.30 -0.41 (7.00) (5.22) (-1.98)

Sorting characteristic

Size 1.07 0.77 -0.29 (8.42) (6.83) (-1.50)

Market-to-book 1.18 1.07 -0.45 (6.90) (4.92) (-2.23)

Past return 1.16 1.27 -0.11 (7.23) (5.96) (-0.64)

Profitability 1.31 1.30 -0.17 (7.74) (6.04) (-0.94)

Investment 1.31 1.34 -0.19 (7.10) (5.56) (-1.04)

Beta 1.13 1.19 0.00 (6.58) (4.96) (0.01)

Idiosyncratic volatility 1.19 1.27 0.04 (8.04) (6.58) (0.22)

33

Subsamples and long horizons 1-low C 2 3 4 5-high C high-low Full sample -0.10 0.03 0.12 0.61 1.24 1.35

(-1.62) (0.47) (1.04) (3.18) (7.23) (7.00) Panel A. Subsamples Excluding January -0.08 0.04 -0.08 0.03 0.72 0.80

(-1.25) (0.59) (-0.77) (0.21) (5.03) (5.01) Excluding Recessions -0.11 0.02 0.15 0.69 1.28 1.39

(-1.67) (0.29) (1.38) (3.58) (7.03) (6.74) 1995-2006 -0.18 0.12 0.35 0.98 1.78 1.96

(-1.75) (1.03) (1.86) (3.24) (6.04) (5.76) 2007-2017 -0.04 -0.06 -0.05 0.22 0.73 0.77

(-0.72) (-0.83) (-0.44) (0.96) (4.33) (4.48) Panel B. Longer investment horizons 3 months -0.10 0.05 0.21 0.64 1.13 1.23

(-1.57) (0.70) (1.88) (3.35) (6.95) (6.80) 6 months -0.09 0.08 0.25 0.68 1.06 1.15

(-1.35) (1.12) (2.19) (3.49) (6.83) (6.69) 12 months -0.05 0.06 0.29 0.71 0.96 1.01

(-0.80) (0.88) (2.40) (3.65) (6.66) (6.49) 18 months -0.03 0.08 0.32 0.71 0.88 0.91

(-0.38) (1.14) (2.60) (3.67) (6.28) (6.07)

34

Additional tests for risk

Test 1: Changes analysis

• If a large increase in a firm’s C-Rank indicates that the firm is under a bigger threat because more and stronger companies are pointing at it now, then the firm’s market value should react negatively

• Each month divide all companies that are recognized as competitors by other firms into five quintiles according to the change in C-Rank from the prior month

• Look at the difference between the average cumulative excess returns of the top and the bottom quintiles (the hedge portfolio) around the month of change

35

Additional tests for risk

Test 2: Sensitivity to targeting competitor’s performance

• The targeting risk explanation is based on the notion that when a company lists another company as a competitor in its 10-K, it intends to compete with that company, thereby increasing its risk

• Therefore, the market value of a company that is targeted by other firms will be negatively affected by the success of those firms

• Each month divide all firms into five equal-sized portfolios according to the average past 12-month returns of their targeting competitors. The average is value-weighted by the competitors’ C-Ranks. Hold the portfolios for 6 to 24 months

36

Additional tests for risk

All competitors Cross-sector competitors Within-sector competitors Holding period: 6m 12m 18m 24m 6m 12m 18m 24m 6m 12m 18m 24m

Mean excess return 0.07 -0.13 -0.23 -0.29 -0.22 -0.40 -0.41 -0.40 0.11 -0.05 -0.19 -0.21 (0.30) (-0.70) (-1.52) (-2.18) (-1.00) (-2.20) (-2.50) (-2.57) (0.42) (-0.24) (-1.08) (-1.44)

CAPM alpha 0.15 -0.07 -0.18 -0.25 -0.18 -0.37 -0.38 -0.38 0.19 0.01 -0.13 -0.17 (0.61) (-0.38) (-1.17) (-1.87) (-0.79) (-2.02) (-2.32) (-2.44) (0.72) (0.04) (-0.77) (-1.14)

3-factor alpha 0.14 -0.09 -0.20 -0.26 -0.20 -0.39 -0.40 -0.40 0.18 -0.01 -0.16 -0.18 (0.55) (-0.47) (-1.31) (-2.00) (-0.89) (-2.12) (-2.44) (-2.60) (0.67) (-0.05) (-0.90) (-1.26)

4-factor alpha 0.13 -0.12 -0.24 -0.29 -0.20 -0.39 -0.41 -0.40 0.18 -0.04 -0.19 -0.21 (0.54) (-0.60) (-1.52) (-2.18) (-0.86) (-2.14) (-2.46) (-2.56) (0.64) (-0.17) (-1.06) (-1.40)

5-factor alpha 0.22 -0.02 -0.16 -0.24 -0.14 -0.35 -0.38 -0.41 0.24 0.04 -0.12 -0.16 (0.85) (-0.09) (-0.98) (-1.75) (-0.59) (-1.87) (-2.24) (-2.58) (0.85) (0.19) (-0.64) (-1.04)

6-factor alpha 0.21 -0.04 -0.18 -0.26 -0.14 -0.36 -0.39 -0.41 0.23 0.02 -0.14 -0.17 (0.82) (-0.20) (-1.13) (-1.88) (-0.58) (-1.90) (-2.27) (-2.55) (0.82) (0.09) (-0.75) (-1.14)

Performance of hedge portfolio of high-minus-low targeting firms’ past returns

37

Additional tests for risk

All competitors Cross-sector competitors Within-sector competitors Holding period: 6m 12m 18m 24m 6m 12m 18m 24m 6m 12m 18m 24m

Mean excess return 0.07 -0.13 -0.23 -0.29 -0.22 -0.40 -0.41 -0.40 0.11 -0.05 -0.19 -0.21 (0.30) (-0.70) (-1.52) (-2.18) (-1.00) (-2.20) (-2.50) (-2.57) (0.42) (-0.24) (-1.08) (-1.44)

CAPM alpha 0.15 -0.07 -0.18 -0.25 -0.18 -0.37 -0.38 -0.38 0.19 0.01 -0.13 -0.17 (0.61) (-0.38) (-1.17) (-1.87) (-0.79) (-2.02) (-2.32) (-2.44) (0.72) (0.04) (-0.77) (-1.14)

3-factor alpha 0.14 -0.09 -0.20 -0.26 -0.20 -0.39 -0.40 -0.40 0.18 -0.01 -0.16 -0.18 (0.55) (-0.47) (-1.31) (-2.00) (-0.89) (-2.12) (-2.44) (-2.60) (0.67) (-0.05) (-0.90) (-1.26)

4-factor alpha 0.13 -0.12 -0.24 -0.29 -0.20 -0.39 -0.41 -0.40 0.18 -0.04 -0.19 -0.21 (0.54) (-0.60) (-1.52) (-2.18) (-0.86) (-2.14) (-2.46) (-2.56) (0.64) (-0.17) (-1.06) (-1.40)

5-factor alpha 0.22 -0.02 -0.16 -0.24 -0.14 -0.35 -0.38 -0.41 0.24 0.04 -0.12 -0.16 (0.85) (-0.09) (-0.98) (-1.75) (-0.59) (-1.87) (-2.24) (-2.58) (0.85) (0.19) (-0.64) (-1.04)

6-factor alpha 0.21 -0.04 -0.18 -0.26 -0.14 -0.36 -0.39 -0.41 0.23 0.02 -0.14 -0.17 (0.82) (-0.20) (-1.13) (-1.88) (-0.58) (-1.90) (-2.27) (-2.55) (0.82) (0.09) (-0.75) (-1.14)

Performance of hedge portfolio of high-minus-low targeting firms’ past returns

38

The importance of the C-Rank features

Testing feature 2:

• The key question: What is the marginal benefit of C-Rank over a simple counting of the number of targeting firms?

• Consider three simple algorithm-free alternative measures to C-Rank:

(1) Simple mention count (# of targeting firms)(2) Mean size of the targeting firms(3) Sum size of the targeting firms

• Replicate the portfolio sort analysis using the alternative measures

39