Embed Size (px)

Citation preview

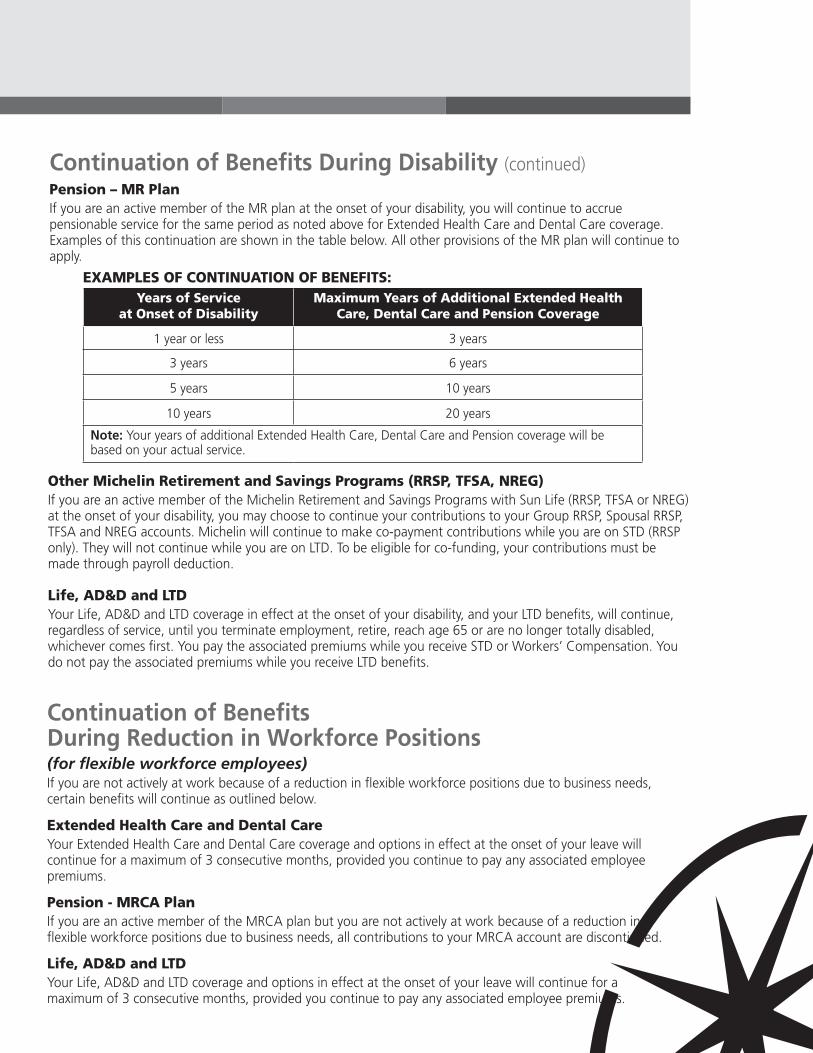

Compensation & Benefits

Our Benefits

GuideMichelin North America (Canada) Inc.

Ver-

siOn

3.0

January 2015

| 1 |

This guide is intended for employees of Michelin North America (Canada) Inc. (the “Company”) excluding any person who is represented by a union.

unless otherwise noted, benefits and programs are available to all employees in all provinces.

Please keep in mind that no one, including any personnel from any benefit carriers or their call centres or any Michelin personnel, is authorized to provide you with personal advice. They can clarify or provide information, but they cannot provide you with advice. No one can advise which benefit plan or option is best for you.

Where plan choices are available, you are responsible for choosing which benefits are best for you and making your own decisions. Michelin is not responsible for any plan choices or decisions you make. Everyone’s personal needs are different. You are responsible for providing Sun Life with the required forms.

This guide summarizes certain plans and policies for ease of understanding. If there is any error, misunderstanding or conflict, official plan texts and policies govern. The Company retains the right, for any reason, at any time and from time to time, to amend, discontinue, introduce or otherwise change policies and benefits applicable to employees and retirees. Certain benefit and pension plans, amendments or options may be subject to approval of regulatory authorities. You will be provided with information regarding these changes as required.

Your facility Personnel Department should be notified immediately in writing of any changes to your personal information (name, address, telephone number, marital status, etc.). Inaccurate information could seriously affect your benefits.

Important!

| 2 |

| 3 |

introductionPurpose of this Guide ................................................................................................................. 5Additional Resources .................................................................................................................... 5

Benefits at a Glance Michelin Health & Welfare Choice Plan ....................................................................................... 7Michelin Retirement and Saving Program ................................................................................... 10Additional Michelin Benefits, Programs and Services ................................................................. 11Benefit Plan Financial Arrangement Clarification ....................................................................... 12

Michelin Health & Welfare Choice PlanOverview ............................................................................................................................. 13

Extended Health Care and Dental Care Plans ............................................................................ 15Health Spending Account (HSA) ............................................................................................. 16Your Assure Drug Card ............................................................................................................ 16Emergency Travel Assistance/Medi-Passport ............................................................................. 16Life and Accidental Death and Dismemberment Coverage ....................................................... 17Long Term Disability ................................................................................................................ 17MHWC Tax Facts ...................................................................................................................... 17

Michelin retirement and savings ProgramOverview ............................................................................................................................. 18

Michelin Retirement Contribution Account (MRCA) Plan .......................................................... 18

Michelin Retirement (MR) Plan ................................................................................................. 20

Pension Plan Information for MR/MRCA Members ................................................................... 20

Michelin Group Registered Retirement Savings Plan (RRSP) ....................................................... 21

Michelin Tax Free Savings Account (TFSA) ................................................................................. 22

Michelin Non Registered Account (NREG) ................................................................................. 23

“My Investment Advice” .......................................................................................................... 23

New Michelin Retirement Planner .............................................................................................. 23

Your Michelin Retirement Plans “To Do” List ............................................................................ 24

Michelin Retirement Plans Tax Facts .......................................................................................... 24

Table of Contents

| 4 |

Table of Contents

additional Michelin Benefits, Programs and servicesBusiness Travel Accident Insurance ............................................................................................ 25Canada Savings Bonds .............................................................................................................. 27Educational Reimbursement ...................................................................................................... 28Employee Tire Program (ETPX) ................................................................................................... 30Employee Tire Purchase Program (ETPP) .................................................................................... 30Michelin Employee Life Services (MELS) .................................................................................... 32Michelin Canada BASE Award Program .................................................................................... 33Purchase of Company Products ................................................................................................ 33Service Award Program ............................................................................................................ 33

Leaves of absence ............................................................................................................ 34• Holidays and Vacations ...................................................................................................... 34• Bereavement Leave ............................................................................................................ 37• Birth/Adoption Leave .......................................................................................................... 37• Compassionate Care or Family Medical Leave (Nova Scotia) ................................................ 38• Jury Duty Leave or Subpoenaed Witness Leave ................................................................... 38• Leave for Family Obligations (Quebec) ................................................................................ 38• Marriage/Civil Union Leave ................................................................................................. 38• Maternity/Pregnancy Leave ................................................................................................. 39• Parental Leave .................................................................................................................... 40• Sickness of a Family Member (Quebec) ............................................................................... 41• Sick Leave (Nova Scotia) ..................................................................................................... 41• Short Term Disability .......................................................................................................... 41• Workers’ Compensation .................................................................................................... 44• Continuation of benefits during disability .......................................................................... 45 • Continuation of benefits during reduction in workforce positions ...................................... 45

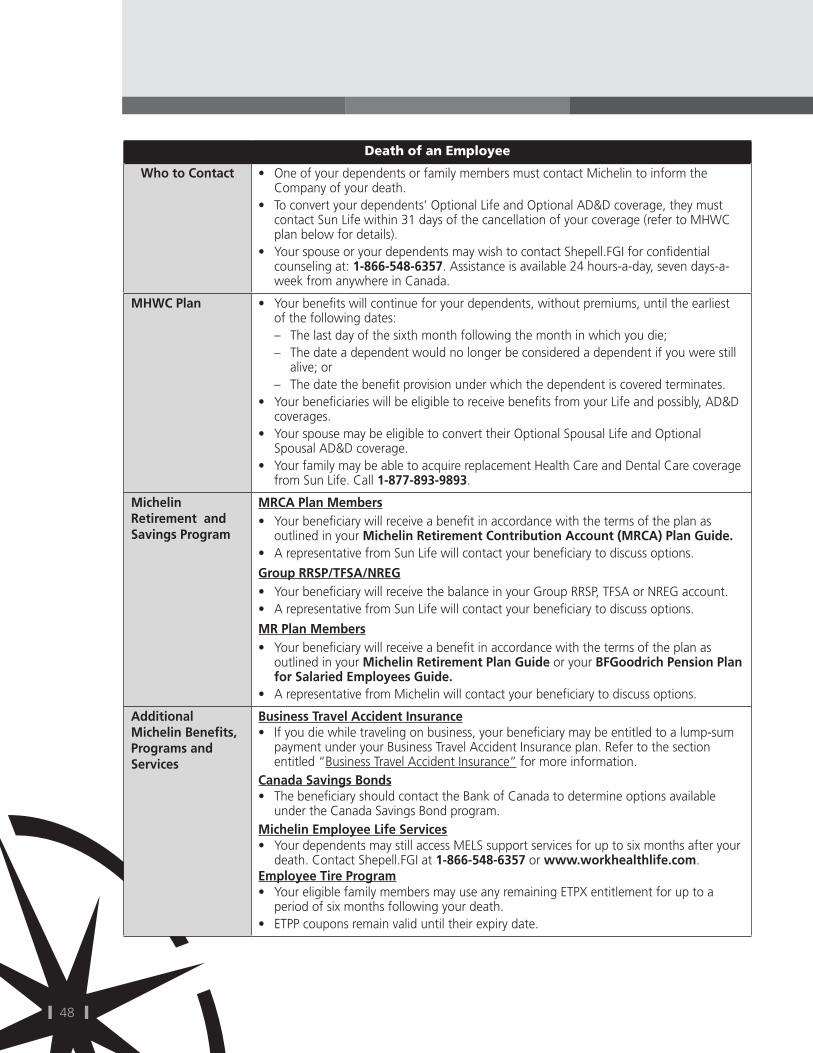

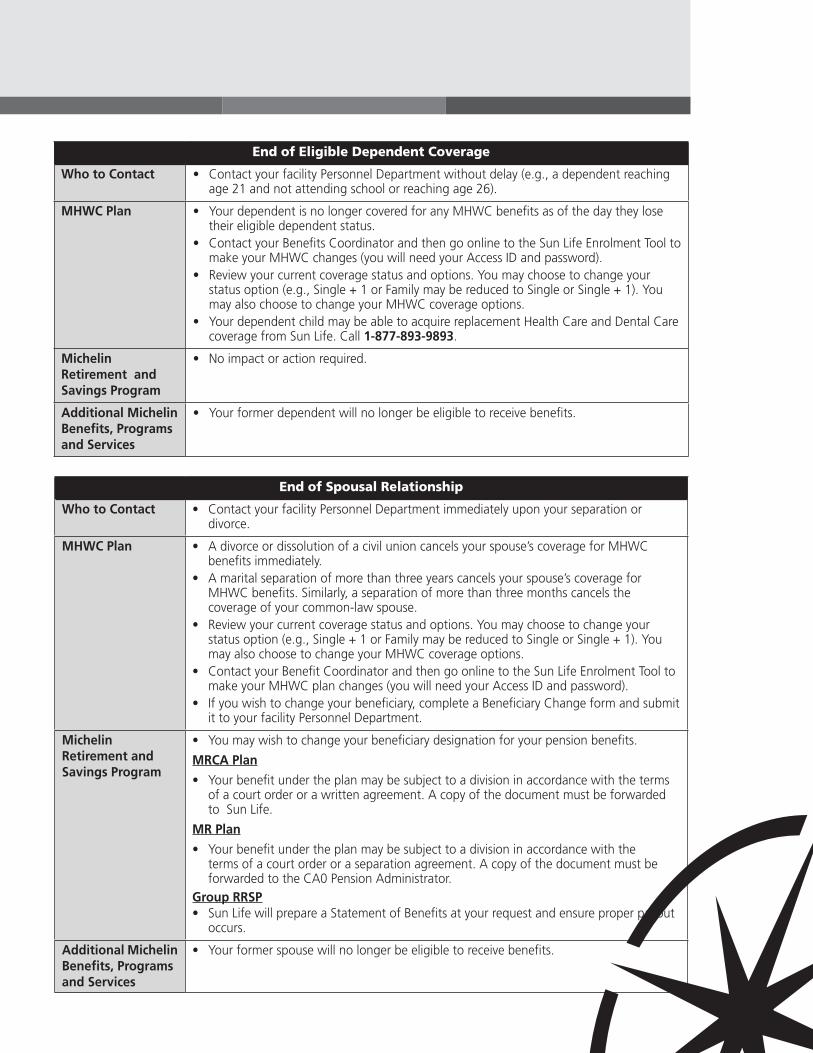

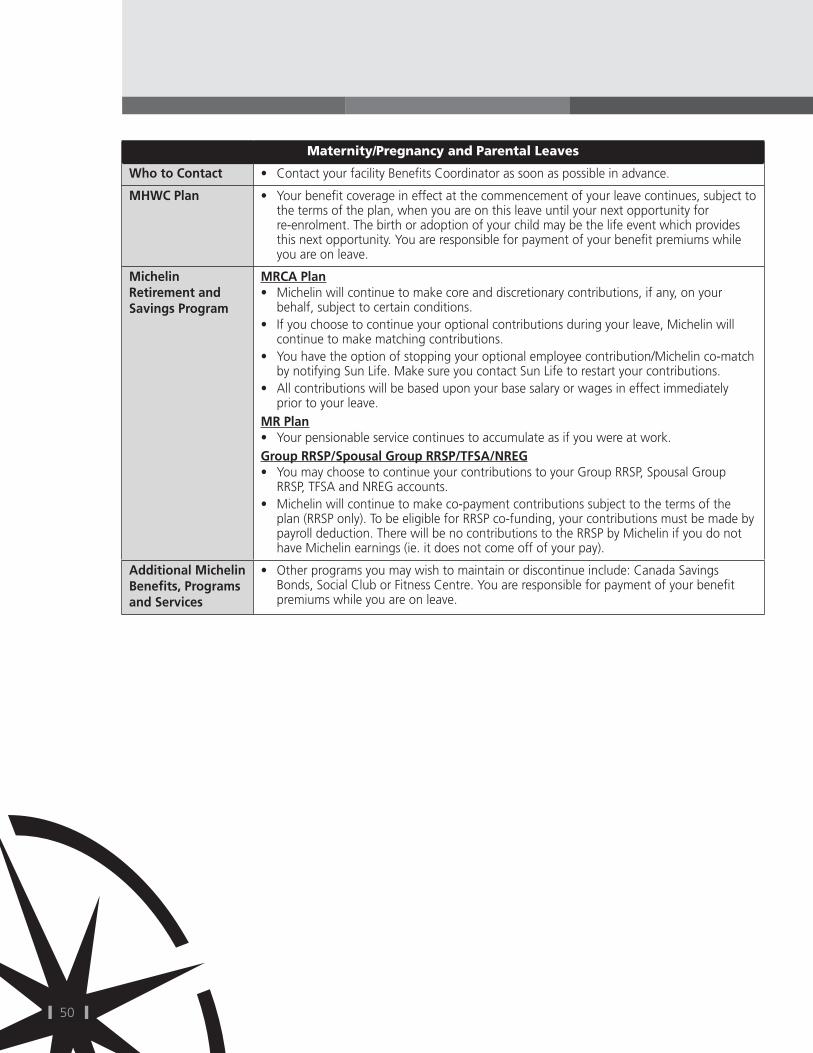

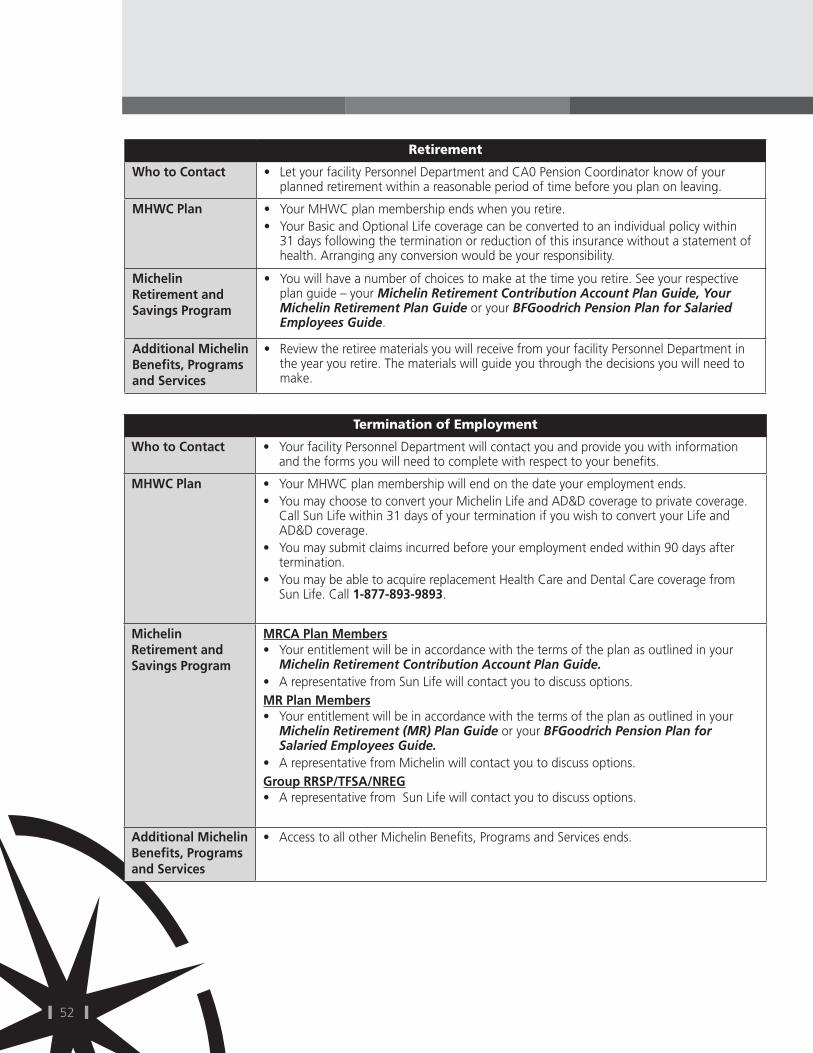

When your Circumstances Change• Birth or Adoption of a Child ............................................................................................... 46• Commencement of Spousal Relationship ............................................................................ 47• Death of a Dependent ........................................................................................................ 47• Death of an Employee ........................................................................................................ 48• End of Eligible Dependent Coverage .................................................................................. 49• End of Spousal Relationship ............................................................................................... 49• Maternity/Pregnancy and Parental Leaves ........................................................................... 50• STD, LTD, Non-Occupational Illness and Workers’ Compensation ........................................ 51• Retirement ......................................................................................................................... 52• Termination of Employment ............................................................................................... 52

| 5 |

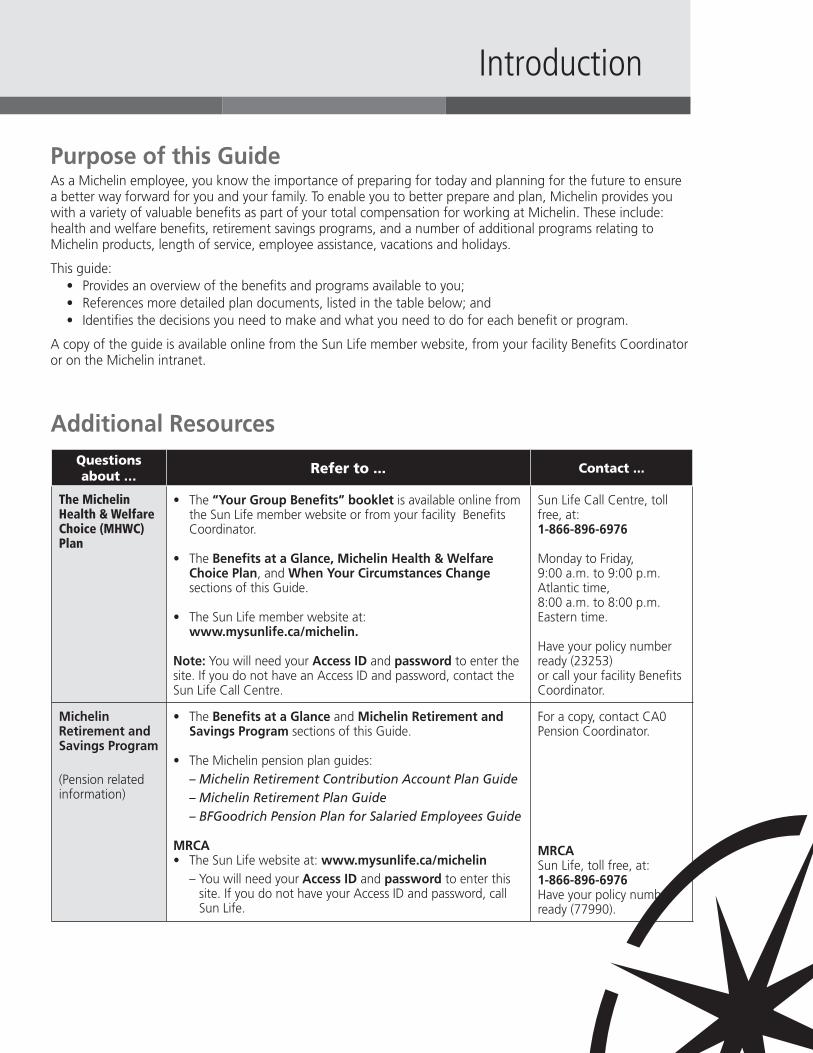

additional resourcesQuestions about … Refer to ... Contact ...

The Michelin Health & Welfare Choice (MHWC) Plan

• The “your Group Benefits” booklet is available online from the Sun Life member website or from your facility Benefits Coordinator.

• The Benefits at a Glance, Michelin Health & Welfare Choice Plan, and When your Circumstances Change sections of this Guide.

• The Sun Life member website at: www.mysunlife.ca/michelin.

note: You will need your access iD and password to enter the site. If you do not have an Access ID and password, contact the Sun Life Call Centre.

Sun Life Call Centre, toll free, at: 1-866-896-6976

Monday to Friday, 9:00 a.m. to 9:00 p.m. Atlantic time, 8:00 a.m. to 8:00 p.m. Eastern time.

Have your policy number ready (23253)or call your facility Benefits Coordinator.

Michelin retirement and savings Program

(Pension related information)

• The Benefits at a Glance and Michelin retirement and savings Program sections of this Guide.

• The Michelin pension plan guides: – Michelin Retirement Contribution Account Plan Guide – Michelin Retirement Plan Guide – BFGoodrich Pension Plan for Salaried Employees Guide

MrCa• The Sun Life website at: www.mysunlife.ca/michelin

– You will need your access iD and password to enter this site. If you do not have your Access ID and password, call Sun Life.

For a copy, contact CA0 Pension Coordinator.

MrCaSun Life, toll free, at:1-866-896-6976Have your policy number ready (77990).

Purpose of this GuideAs a Michelin employee, you know the importance of preparing for today and planning for the future to ensure a better way forward for you and your family. To enable you to better prepare and plan, Michelin provides you with a variety of valuable benefits as part of your total compensation for working at Michelin. These include: health and welfare benefits, retirement savings programs, and a number of additional programs relating to Michelin products, length of service, employee assistance, vacations and holidays.

This guide:• Provides an overview of the benefits and programs available to you;• References more detailed plan documents, listed in the table below; and • Identifies the decisions you need to make and what you need to do for each benefit or program.

A copy of the guide is available online from the Sun Life member website, from your facility Benefits Coordinator or on the Michelin intranet.

Introduction

| 6 |

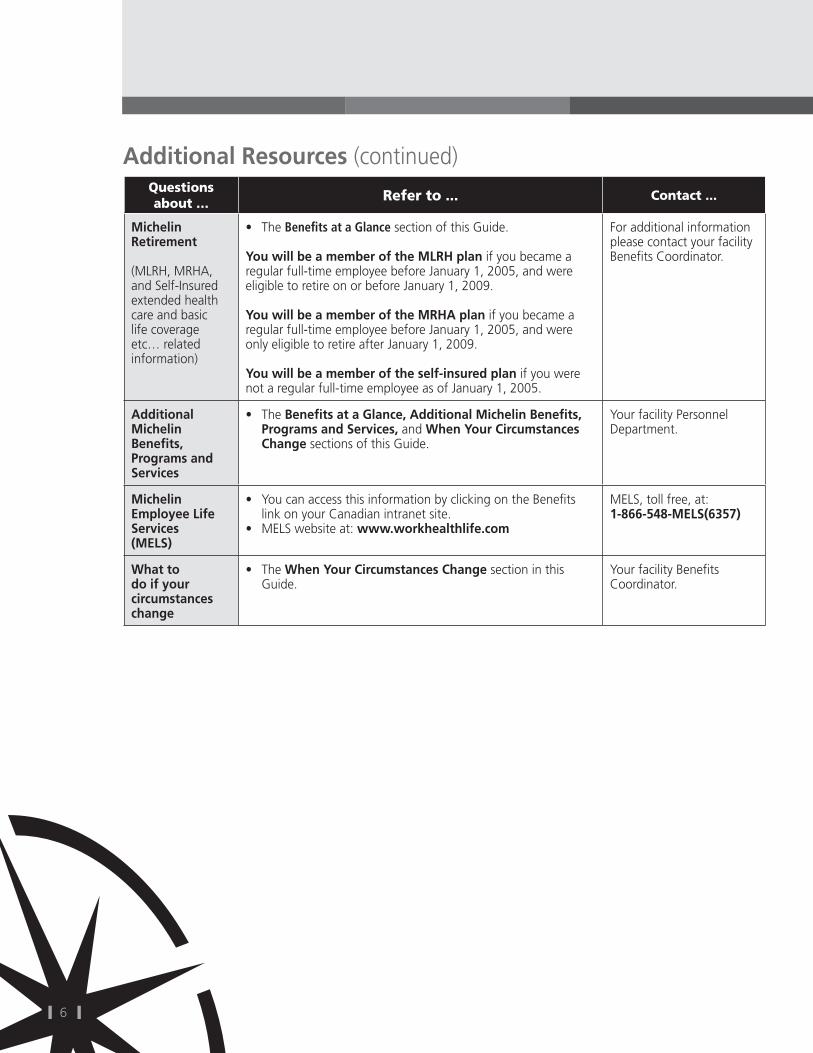

additional resources (continued)Questions about … Refer to ... Contact ...

Michelin retirement

(MLRH, MRHA, and Self-Insured extended health care and basic life coverage etc… related information)

• The Benefits at a Glance section of this Guide.

you will be a member of the MLrH plan if you became a regular full-time employee before January 1, 2005, and were eligible to retire on or before January 1, 2009.

you will be a member of the MrHa plan if you became a regular full-time employee before January 1, 2005, and were only eligible to retire after January 1, 2009.

you will be a member of the self-insured plan if you were not a regular full-time employee as of January 1, 2005.

For additional information please contact your facility Benefits Coordinator.

additional Michelin Benefits, Programs and services

• The Benefits at a Glance, additional Michelin Benefits, Programs and services, and When your Circumstances Change sections of this Guide.

Your facility Personnel Department.

Michelin employee Life services (MeLs)

• You can access this information by clicking on the Benefits link on your Canadian intranet site.

• MELS website at: www.workhealthlife.com

MELS, toll free, at: 1-866-548-MeLs(6357)

What to do if your circumstances change

• The When your Circumstances Change section in this Guide.

Your facility Benefits Coordinator.

| 7 |

Benefits at a Glance

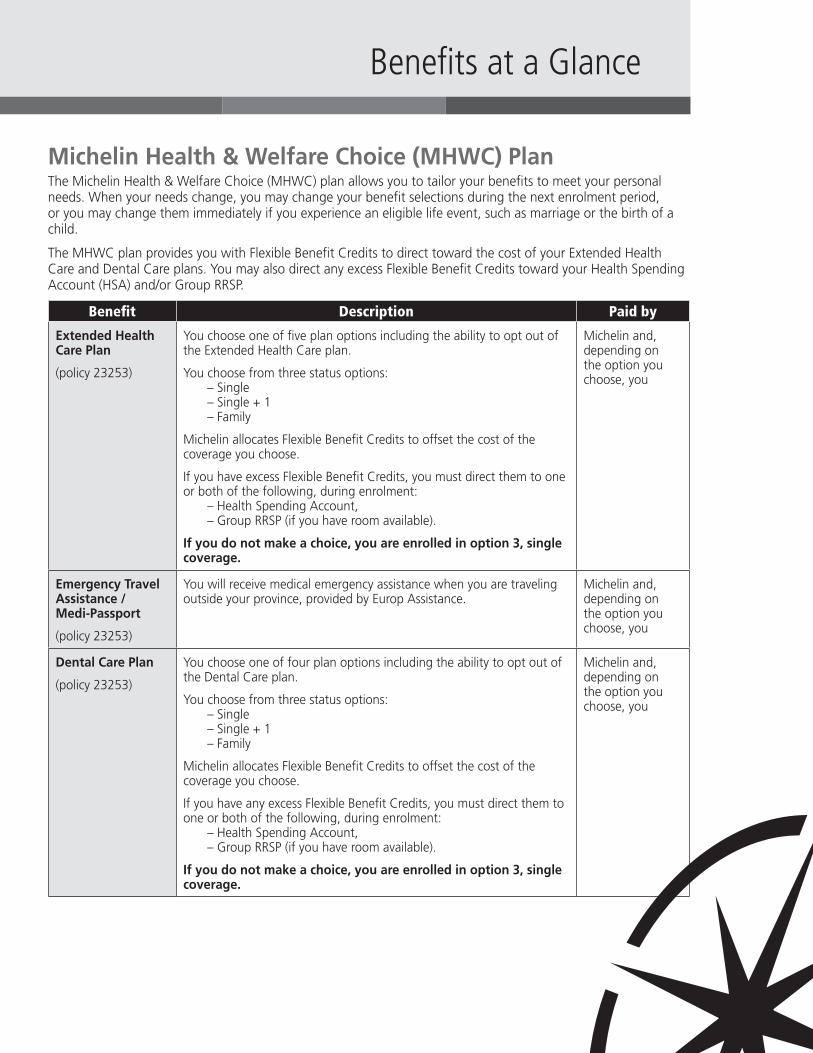

Michelin Health & Welfare Choice (MHWC) PlanThe Michelin Health & Welfare Choice (MHWC) plan allows you to tailor your benefits to meet your personal needs. When your needs change, you may change your benefit selections during the next enrolment period, or you may change them immediately if you experience an eligible life event, such as marriage or the birth of a child.

The MHWC plan provides you with Flexible Benefit Credits to direct toward the cost of your Extended Health Care and Dental Care plans. You may also direct any excess Flexible Benefit Credits toward your Health Spending Account (HSA) and/or Group RRSP.

Benefit Description Paid by

extended Health Care Plan

(policy 23253)

You choose one of five plan options including the ability to opt out of the Extended Health Care plan.

You choose from three status options: – Single – Single + 1 – Family

Michelin allocates Flexible Benefit Credits to offset the cost of the coverage you choose.

If you have excess Flexible Benefit Credits, you must direct them to one or both of the following, during enrolment:

– Health Spending Account, – Group RRSP (if you have room available).

if you do not make a choice, you are enrolled in option 3, single coverage.

Michelin and, depending on the option you choose, you

emergency Travel assistance / Medi-Passport

(policy 23253)

You will receive medical emergency assistance when you are traveling outside your province, provided by Europ Assistance.

Michelin and, depending on the option you choose, you

Dental Care Plan

(policy 23253)

You choose one of four plan options including the ability to opt out of the Dental Care plan.

You choose from three status options: – Single – Single + 1 – Family

Michelin allocates Flexible Benefit Credits to offset the cost of the coverage you choose.

If you have any excess Flexible Benefit Credits, you must direct them to one or both of the following, during enrolment:

– Health Spending Account, – Group RRSP (if you have room available).

if you do not make a choice, you are enrolled in option 3, single coverage.

Michelin and, depending on the option you choose, you

| 8 |

Michelin Health & Welfare Choice (MHWC) Plan (continued)

Benefit Description Paid by

Health spending account (Hsa)

(policy 23253)

The MHWC plan includes a Health Spending Account (HSA). The number of Flexible Benefit Credits you have will depend on the Extended Health Care and Dental Care plan options you choose. You may direct any excess Flexible Benefit Credits to your HSA and/or Group RRSP.

You may use your HSA to pay for eligible expenses not covered by the MHWC plan, the provincial health care plan or another private plan.

Michelin, if excess Flexible Benefit Credits are available

Basic Life Coverage

(policy 45053)

Coverage equal to 2 times your annual basic earnings rounded to the next higher $1,000.

Michelin

Optional Life Coverage

(policy 45053)

1, 2, 3, 4 or 5 times your annual basic earnings, rounded to the next higher $1,000 subject to approval of statement of Health by sun Life.

You

Optional spousal Life Coverage

(policy 45053)

Up to $250,000 of coverage subject to approval of statement of Health by sun Life.

You

Optional Child Life Coverage

(policy 45053)

Up to $20,000 for each child. You

accidental Death and Dismemberment (aD&D) Coverage

(policy 45053)

Coverage equal to 2 times your annual basic earnings rounded to the next higher $1,000.

Michelin

Optional aD&D Coverage

(policy 45053)

1, 2, 3, 4 or 5 times your annual basic earnings, rounded to the next higher $1,000.

You

Optional spousal aD&D Coverage

(policy 45053)

Up to $250,000 of coverage. You

Optional Child aD&D Coverage

(policy 45053)

Up to $20,000 for each child. You

Long Term Disability

(policy 45053)

You choose one of four options. Coverage provides an income based on a percentage of your monthly basic earnings in the event of disability. You pay the premiums through payroll deductions. As a result, you do not pay income tax on any LTD benefits you may receive. if you do not make a choice, coverage defaults to option 3.

You

| 9 |

Michelin Health & Welfare Choice (MHWC) Plan (continued)

Benefit Description Paid by

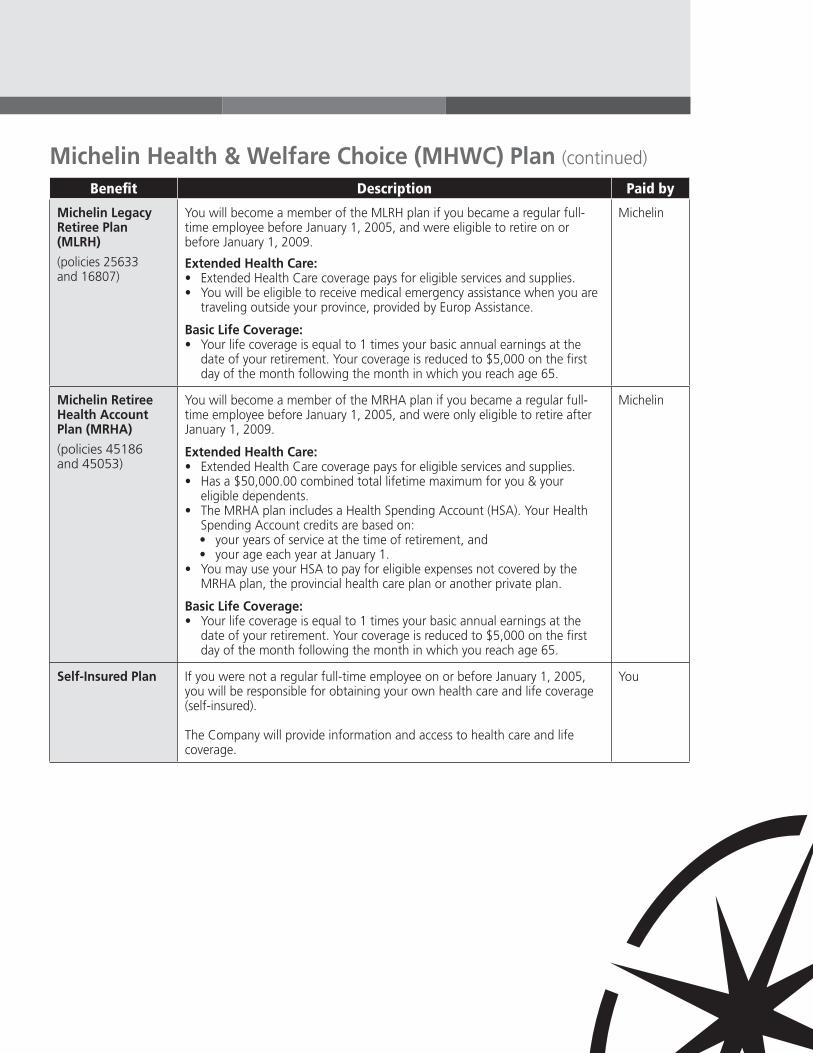

Michelin Legacy retiree Plan (MLrH)

(policies 25633 and 16807)

You will become a member of the MLRH plan if you became a regular full-time employee before January 1, 2005, and were eligible to retire on or before January 1, 2009.

extended Health Care:• Extended Health Care coverage pays for eligible services and supplies. • You will be eligible to receive medical emergency assistance when you are

traveling outside your province, provided by Europ Assistance.

Basic Life Coverage:• Your life coverage is equal to 1 times your basic annual earnings at the

date of your retirement. Your coverage is reduced to $5,000 on the first day of the month following the month in which you reach age 65.

Michelin

Michelin retiree Health account Plan (MrHa)

(policies 45186 and 45053)

You will become a member of the MRHA plan if you became a regular full-time employee before January 1, 2005, and were only eligible to retire after January 1, 2009.

extended Health Care:• Extended Health Care coverage pays for eligible services and supplies. • Has a $50,000.00 combined total lifetime maximum for you & your

eligible dependents.• The MRHA plan includes a Health Spending Account (HSA). Your Health

Spending Account credits are based on:• your years of service at the time of retirement, and• your age each year at January 1.

• You may use your HSA to pay for eligible expenses not covered by the MRHA plan, the provincial health care plan or another private plan.

Basic Life Coverage:• Your life coverage is equal to 1 times your basic annual earnings at the

date of your retirement. Your coverage is reduced to $5,000 on the first day of the month following the month in which you reach age 65.

Michelin

self-insured Plan If you were not a regular full-time employee on or before January 1, 2005, you will be responsible for obtaining your own health care and life coverage (self-insured).

The Company will provide information and access to health care and life coverage.

You

| 10 |

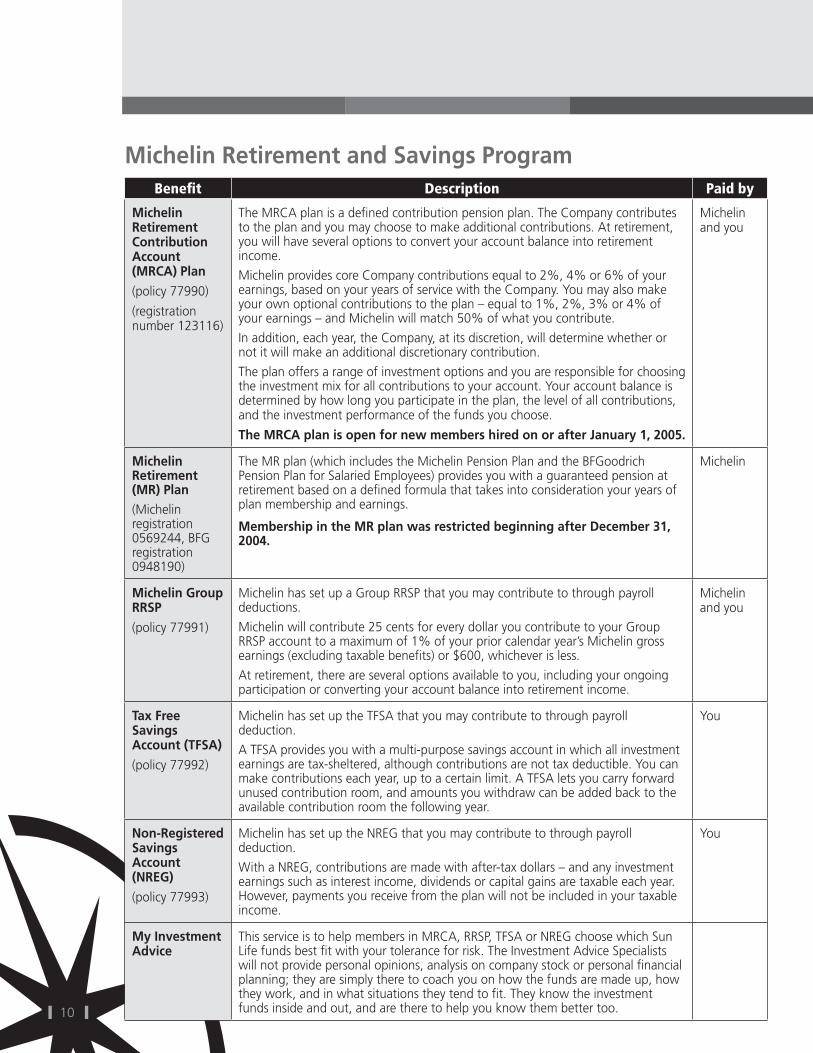

Michelin retirement and savings ProgramBenefit Description Paid by

Michelin retirement Contribution account (MrCa) Plan

(policy 77990)

(registration number 123116)

The MRCA plan is a defined contribution pension plan. The Company contributes to the plan and you may choose to make additional contributions. At retirement, you will have several options to convert your account balance into retirement income.

Michelin provides core Company contributions equal to 2%, 4% or 6% of your earnings, based on your years of service with the Company. You may also make your own optional contributions to the plan – equal to 1%, 2%, 3% or 4% of your earnings – and Michelin will match 50% of what you contribute.

In addition, each year, the Company, at its discretion, will determine whether or not it will make an additional discretionary contribution.

The plan offers a range of investment options and you are responsible for choosing the investment mix for all contributions to your account. Your account balance is determined by how long you participate in the plan, the level of all contributions, and the investment performance of the funds you choose.

The MrCa plan is open for new members hired on or after January 1, 2005.

Michelin and you

Michelin retirement (Mr) Plan

(Michelin registration 0569244, BFG registration 0948190)

The MR plan (which includes the Michelin Pension Plan and the BFGoodrich Pension Plan for Salaried Employees) provides you with a guaranteed pension at retirement based on a defined formula that takes into consideration your years of plan membership and earnings.

Membership in the Mr plan was restricted beginning after December 31, 2004.

Michelin

Michelin Group rrsP

(policy 77991)

Michelin has set up a Group RRSP that you may contribute to through payroll deductions.

Michelin will contribute 25 cents for every dollar you contribute to your Group RRSP account to a maximum of 1% of your prior calendar year’s Michelin gross earnings (excluding taxable benefits) or $600, whichever is less.

At retirement, there are several options available to you, including your ongoing participation or converting your account balance into retirement income.

Michelin and you

Tax Free savings account (TFsa)

(policy 77992)

Michelin has set up the TFSA that you may contribute to through payroll deduction.

A TFSA provides you with a multi-purpose savings account in which all investment earnings are tax-sheltered, although contributions are not tax deductible. You can make contributions each year, up to a certain limit. A TFSA lets you carry forward unused contribution room, and amounts you withdraw can be added back to the available contribution room the following year.

You

non-registered savings account (nreG)

(policy 77993)

Michelin has set up the NREG that you may contribute to through payroll deduction.

With a NREG, contributions are made with after-tax dollars – and any investment earnings such as interest income, dividends or capital gains are taxable each year. However, payments you receive from the plan will not be included in your taxable income.

You

My investment advice

This service is to help members in MRCA, RRSP, TFSA or NREG choose which Sun Life funds best fit with your tolerance for risk. The Investment Advice Specialists will not provide personal opinions, analysis on company stock or personal financial planning; they are simply there to coach you on how the funds are made up, how they work, and in what situations they tend to fit. They know the investment funds inside and out, and are there to help you know them better too.

| 11 |

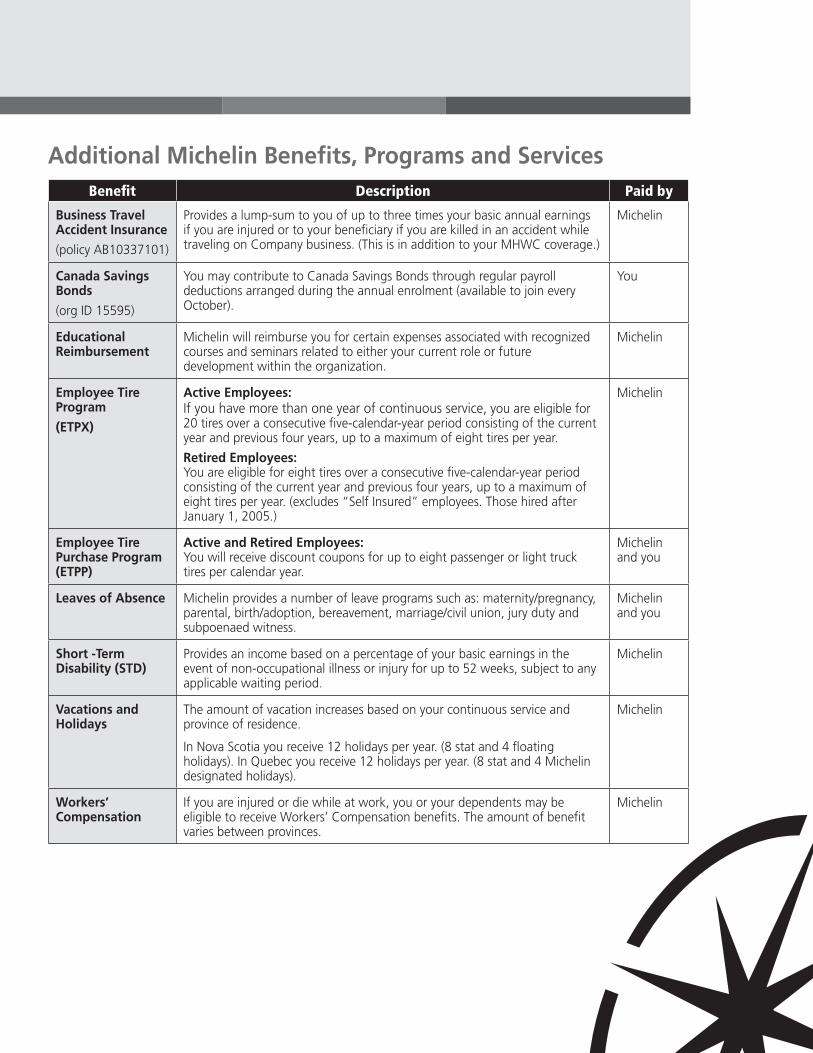

additional Michelin Benefits, Programs and servicesBenefit Description Paid by

Business Travel accident insurance

(policy AB10337101)

Provides a lump-sum to you of up to three times your basic annual earnings if you are injured or to your beneficiary if you are killed in an accident while traveling on Company business. (This is in addition to your MHWC coverage.)

Michelin

Canada savings Bonds

(org ID 15595)

You may contribute to Canada Savings Bonds through regular payroll deductions arranged during the annual enrolment (available to join every October).

You

educational reimbursement

Michelin will reimburse you for certain expenses associated with recognized courses and seminars related to either your current role or future development within the organization.

Michelin

employee Tire Program

(eTPX)

active employees:If you have more than one year of continuous service, you are eligible for 20 tires over a consecutive five-calendar-year period consisting of the current year and previous four years, up to a maximum of eight tires per year.

retired employees:You are eligible for eight tires over a consecutive five-calendar-year period consisting of the current year and previous four years, up to a maximum of eight tires per year. (excludes “Self Insured” employees. Those hired after January 1, 2005.)

Michelin

employee Tire Purchase Program (eTPP)

active and retired employees: You will receive discount coupons for up to eight passenger or light truck tires per calendar year.

Michelin and you

Leaves of absence Michelin provides a number of leave programs such as: maternity/pregnancy, parental, birth/adoption, bereavement, marriage/civil union, jury duty and subpoenaed witness.

Michelin and you

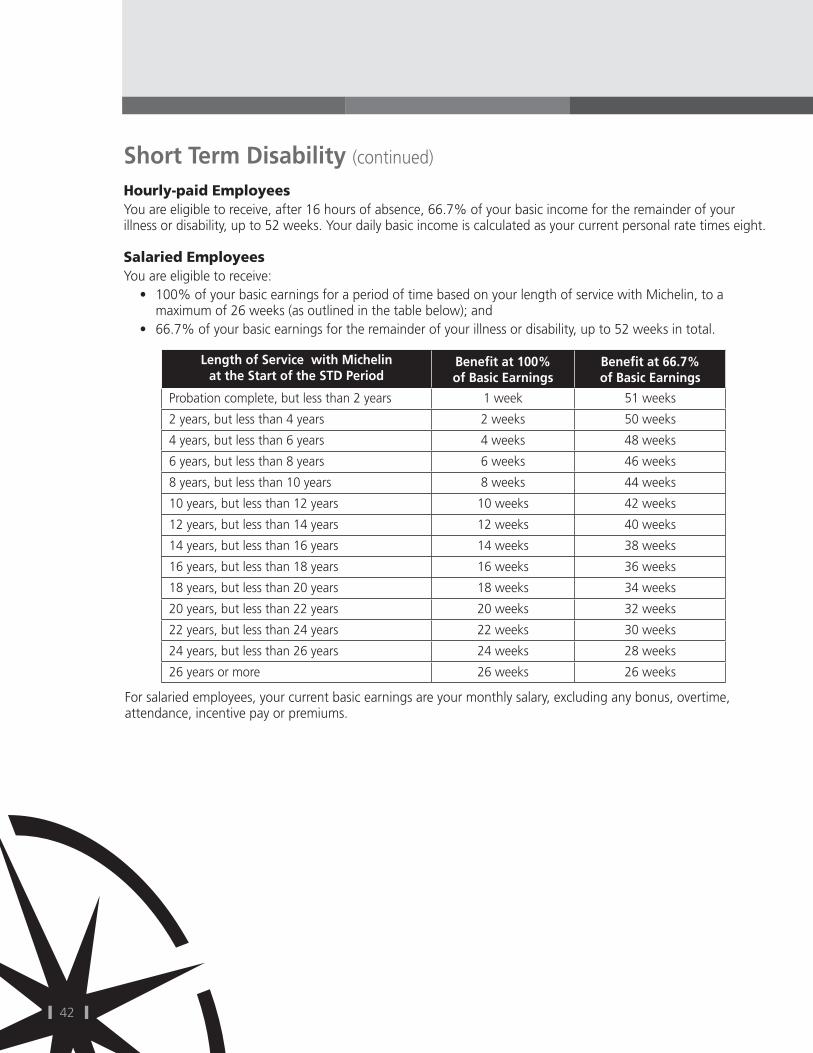

short -Term Disability (sTD)

Provides an income based on a percentage of your basic earnings in the event of non-occupational illness or injury for up to 52 weeks, subject to any applicable waiting period.

Michelin

Vacations and Holidays

The amount of vacation increases based on your continuous service and province of residence.

In Nova Scotia you receive 12 holidays per year. (8 stat and 4 floating holidays). In Quebec you receive 12 holidays per year. (8 stat and 4 Michelin designated holidays).

Michelin

Workers’ Compensation

If you are injured or die while at work, you or your dependents may be eligible to receive Workers’ Compensation benefits. The amount of benefit varies between provinces.

Michelin

| 12 |

Benefit Description Paid by

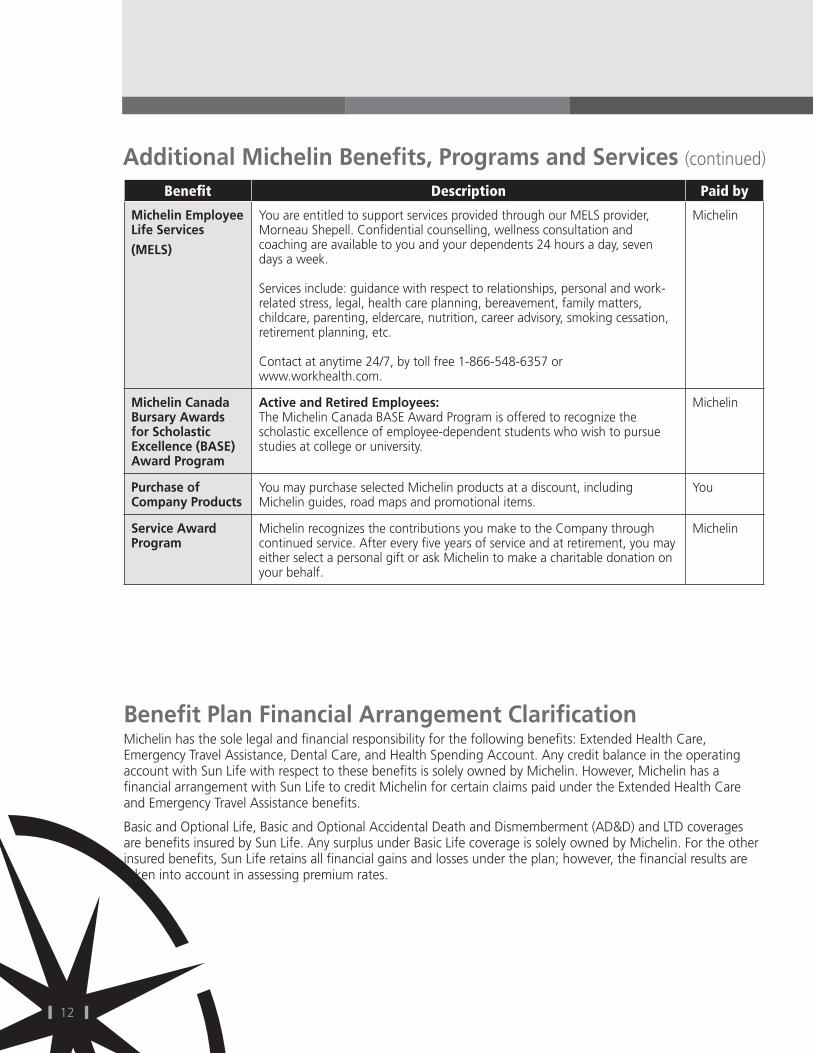

Michelin employee Life services

(MeLs)

You are entitled to support services provided through our MELS provider, Morneau Shepell. Confidential counselling, wellness consultation and coaching are available to you and your dependents 24 hours a day, seven days a week.

Services include: guidance with respect to relationships, personal and work-related stress, legal, health care planning, bereavement, family matters, childcare, parenting, eldercare, nutrition, career advisory, smoking cessation, retirement planning, etc.

Contact at anytime 24/7, by toll free 1-866-548-6357 or www.workhealth.com.

Michelin

Michelin Canada Bursary awards for scholastic excellence (Base) award Program

active and retired employees: The Michelin Canada BASE Award Program is offered to recognize the scholastic excellence of employee-dependent students who wish to pursue studies at college or university.

Michelin

Purchase of Company Products

You may purchase selected Michelin products at a discount, including Michelin guides, road maps and promotional items.

You

service award Program

Michelin recognizes the contributions you make to the Company through continued service. After every five years of service and at retirement, you may either select a personal gift or ask Michelin to make a charitable donation on your behalf.

Michelin

additional Michelin Benefits, Programs and services (continued)

Benefit Plan Financial arrangement ClarificationMichelin has the sole legal and financial responsibility for the following benefits: Extended Health Care, Emergency Travel Assistance, Dental Care, and Health Spending Account. Any credit balance in the operating account with Sun Life with respect to these benefits is solely owned by Michelin. However, Michelin has a financial arrangement with Sun Life to credit Michelin for certain claims paid under the Extended Health Care and Emergency Travel Assistance benefits.

Basic and Optional Life, Basic and Optional Accidental Death and Dismemberment (AD&D) and LTD coverages are benefits insured by Sun Life. Any surplus under Basic Life coverage is solely owned by Michelin. For the other insured benefits, Sun Life retains all financial gains and losses under the plan; however, the financial results are taken into account in assessing premium rates.

| 13 |

Michelin Health & Welfare Choice (MHWC) Plan

OverviewThe Michelin Health & Welfare Choice (MHWC) plan is all about choosing benefits that work for you. The plan provides you with a number of valuable benefits, including: Extended Health Care, Dental Care, Life, Accidental Death and Dismemberment and Long Term Disability coverage. However, instead of issuing a standard set of benefits to everyone, the MHWC plan provides different options which you can adjust to meet your changing needs and those of your family.

You will find details on each of the Michelin Health and Welfare Choice benefits in your MHWC ”your Group Benefits” booklet, including: benefit coverage, limitations, terms and conditions, as well as when to make a claim.

EligibilityYou can join the Michelin Health & Welfare Choice plan at the beginning of the month following your successful completion of 90 days of active employment, or upon acceptance as an established employee. When you join the plan, your eligible dependents may also be covered under you. Eligible dependents include your spouse and any dependent children.

Who Qualifies as Your Dependent?Your spouse qualifies as a dependent if he or she is:

• Married to you or is in a formal union recognized by law with you; or• Living with you in a spousal relationship and has been doing so for at least one year.

Your child qualifies as a dependent if he or she is your or your spouse’s natural oradopted unmarried child, who is:

• Under age 21;• Under age 26 and in full-time attendance at an accredited educational institution; or• Age 21 or over and living with a physical or mental disability that prevents self support.

For complete definitions of spouse and dependent child, please see your MHWC ”your Group Benefits” booklet.

EnrolmentWhen you become eligible for the MHWC plan, you will be asked to make choices and enrol online. You will find the enrolment tool on the Sun Life member website at: www.mysunlife.ca/michelin. You will need your Access ID and password to enter this site.

If you do not have or do not remember your Access ID and/or password, please follow the instructions online, otherwise call the Sun Life Call Centre at 1-866-896-6976 and they will provide you with your existing Access ID and a temporary password.

It is your responsibility to ensure your personal and dependent information and benefit choices are correct on the enrolment tool. If your information is incorrect:

• Your benefit coverage may be void; • You may incur incorrect payroll deductions; and/or • You may be required to refund any incorrect claim payments.

There is no opportunity for retroactive premium adjustments for employees who over-pay premiums because they failed to keep their records current. if your information is incorrect, contact your facility Benefits Coordinator immediately.

| 14 |

Your benefit choices are valid throughout the benefit year, which runs from the period of January 1 to December 31. Each fall, you will have the opportunity to review your benefit choices and make adjustments for the upcoming benefit year (this is subject to any change restrictions relating to a benefit). For example, some Dental Care and Long Term Disability benefits require you to remain in that choice for two years before changing options. For more information on limitations for changing your benefits, please see your MHWC ”your Group Benefits” booklet.

You can also make changes during the benefit year if you experience certain eligible life events. These are:• Marriage or any other formal union recognized by law or common-law; • Birth or adoption of a child;• Divorce or legal separation;• Change in a spouse’s benefits coverage;• Child becomes eligible or ceases to be eligible under this or another plan; and• Death of a dependent.

You may also make benefit choice changes under the following circumstances:• Dependent reaching age 26 and in full-time attendance at an accredited educational institution and causing

a status change to Single or Single + 1;• Dependent reaching age 21 and causing a status change to Single or Single + 1.

| 15 |

extended Health Care and Dental Care PlansYou choose one of five plan options including the ability to opt out of the Extended Health and Dental Care plans.

You choose from three status options (Single, Single + 1, Family). Michelin allocates Flexible Benefit Credits to offset the cost of the coverage you choose. If you have any excess Flexible Benefit Credits, you must direct them to your Health Spending Account or your Michelin Group RRSP (if you have room available). How the plan works is summarized in the diagram below.

Keep in mind that employees pay only a fraction of the total cost of providing Extended Health Care and Dental Care benefits. While employees share in the cost of Extended Health Care and Dental Care premiums, Michelin pays significantly more.

Extended Health Care Plan

Michelin Flexible Benefit Credits

Employee Price Tag of the Extended Health Care option you choose

option 1 (opt out) option 3option 2 option 4 option 5

Status: single single + 1 family

Employee premiums through payroll

deduction

Michelin pays premiums on your behalf

If the employee price tag is greater than the Flexible Benefit Credits you receive, you will pay the difference

through payroll deductions.

You choose the available plan option and status

that best meets your needs.

Each option has a price tag.

Refer to your MHWC plan booklet

for details on each option.

You use your Michelin Flexible Benefit Credits to pay for the option

you choose.

minus

Dental Care Plan

Michelin Flexible Benefit Credits

Employee Price Tag of the Dental Care option

you choose

option 1 (opt out) option 3option 2 option 4

Status: single single + 1 family

Health Spending Account

Group RRSP

You allocate any excess Flexible Benefit Credits to your Health Spending Account or Group RRSP or both.

minus

| 16 |

Health spending account (Hsa) The MHWC plan includes a Health Spending Account (HSA). You may use your HSA to pay for eligible expenses not covered by the MHWC plan, your provincial health care plan or another private plan. The MHWC “your Group Benefits” booklet contains an extensive list of eligible Extended Health Care and Dental Care expenses under the HSA. You can also contact the Sun Life Call Centre at 1-866-896-6976 to confirm whether an expense is eligible.

The amount of credits you have in your HSA depends on the Extended Health Care plan and Dental Care plan options you choose. Excess Flexible Benefit Credits for the upcoming year may be directed to your HSA and/or your Group RRSP (if you have room available) during the enrolment period each year.

You may also use your HSA to pay for eligible expenses incurred by other family members, such as a parent or sibling, who are financially dependent on you as defined by the Canada Revenue Agency. You may seek reimbursement for expenses incurred by anyone who is listed as a dependent on your income tax return.

You can claim many but not all HSA expenses online to receive faster reimbursement. Any unused credits in your HSA can be carried over until December 31 of the following year.

note: Canada Revenue Agency rules dictate that any unused credits must be forfeited after two years.

A Tax-Effective BenefitThe dollars that are reimbursed from the Health Spending Account (HSA) are not taxable to you if you live outside of Quebec. As well, you will have the opportunity to use your HSA balance to pay for expenses you currently pay out of your own pocket.

your assure Drug Card Depending on the Extended Health Care option you choose, you as well as your spouse and any eligible dependent are entitled to an Assure drug card.

Your Assure drug card contains information for your pharmacist, including contract information for you and your dependents.

You can use your drug card anywhere in Canada, providing the pharmacy is connected to the Telus system. Telus is Canada’s largest pharmacy benefit management provider. When you use your card, you do not have to pay the full amount and wait for reimbursement. If you forget to use your card, you will need to pay the pharmacy the full amount and submit a claim to Sun Life for reimbursement.

You, your spouse and your eligible dependents can use the drug card to cover prescription drug costs.

You may print additional drug cards from the Sun Life member website at: www.mysunlife.ca/michelin.

If you, your spouse and/or eligible dependents are covered under another plan and wish to coordinate your benefits, you can use your drug card to pay the primary and/or the secondary amount.

note: You must advise the pharmacist of both plans in order for the online claims system to work. Refer also to the website or “your Group Benefits” booklet.

emergency Travel assistance/Medi-Passport If you are faced with a medical emergency when traveling for business or pleasure outside of the province where you live, Michelin provides Emergency Travel Assistance benefits. The benefit, called Europ Assistance, supplements the emergency portion of your Extended Health Care coverage. It provides on-the-spot medical assistance and covers transportation, meals and accommodation, and expenses to return home, if required. For more information on this benefit, as well as terms and conditions, see your MHWC “your Group Benefits” booklet.

Print your Travel Card from the Sun Life member website at: www.mysunlife.ca/michelin. It contains your contract and member ID numbers as well as important contact information.

| 17 |

Life and accidental Death and Dismemberment CoverageThe Michelin Health & Welfare Choice plan provides you with a basic level of Life and Accidental Death and Dismemberment (AD&D) coverage. You may then add to these benefits by choosing optional coverage. Optional coverage is paid for through payroll deductions. You will find more details on these options in your MHWC “your Group Benefits” booklet.

You have 31 days to submit a completed Statement of Health form from the date you elect and/or increase Optional Life or Optional Spousal Life coverage. Forms received after 31 days will not be accepted by Sun Life and your coverage summary will indicate the new or additional coverage as declined.

Long Term Disability (LTD)There are four Long Term Disability (LTD) options. You choose the option that best meets your needs. For more information, see your MHWC “your Group Benefits” booklet.

MHWC Tax FactsBenefit Tax Facts

extended Health Care Michelin-paid premiums are considered taxable income in Quebec only. You do not pay income tax on any benefit received.

Dental Care Michelin-paid premiums are considered taxable income in Quebec only. You do not pay income tax on any benefit received.

Health spending account (Hsa)

The dollars that are reimbursed from the HSA are considered taxable income only if you live in Quebec.

Basic Life Michelin-paid premiums are considered taxable income. Because you pay tax on the premium, your beneficiaries do not pay tax on the benefit.

Optional Life Coverage

(Employee, Spouse, Child)

You pay your Optional Life premiums with after-tax income; therefore, you do not pay tax on any Optional Life benefits you or a beneficiary may receive.

accidental Death and Dismemberment (aD&D)

Michelin-paid premiums are considered taxable income in Quebec only. You do not pay income tax on any benefit received.

Optional accidental Death and Dismemberment

(Employee, Spouse, Child)

You pay your optional AD&D premiums with after-tax income; therefore, you do not pay tax on any optional AD&D benefits you or a beneficiary may receive.

Long Term Disability (LTD) You pay your LTD premiums with after-tax income; therefore, you do not pay tax on any LTD benefits you may receive.

| 18 |

OverviewCareful financial planning can make your retirement years both enjoyable and secure. There are three primary sources that will contribute toward an adequate retirement income:

• Government plans;• Employer pension plans; and • Personal savings (e.g., RRSPs, bank accounts and other savings).

Michelin offers its employees several ways of preparing for retirement:• Company registered pension plans – the Michelin Retirement Contribution Account (MRCA) plan or

the Michelin Retirement (MR) plan. Membership in the MR plan was restricted beginning after December 31, 2004. Both the Michelin Pension Plan and the BFGoodrich Pension Plan for Salaried Employees are considered the MR plan;

• The Michelin Group RRSP – a registered savings plan with Michelin co-funding;• Tax Free Savings Account (TFSA); and• Non Registered Savings Account (NREG).

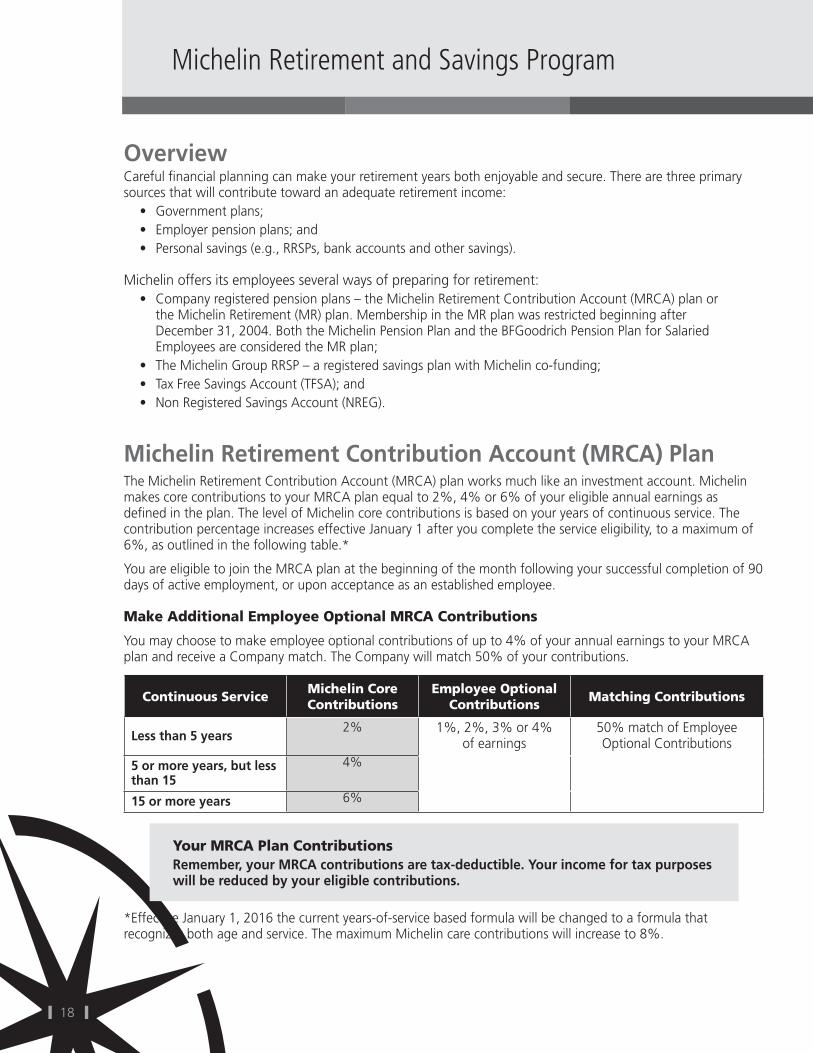

Michelin retirement Contribution account (MrCa) Plan The Michelin Retirement Contribution Account (MRCA) plan works much like an investment account. Michelin makes core contributions to your MRCA plan equal to 2%, 4% or 6% of your eligible annual earnings as defined in the plan. The level of Michelin core contributions is based on your years of continuous service. The contribution percentage increases effective January 1 after you complete the service eligibility, to a maximum of 6%, as outlined in the following table.*

You are eligible to join the MRCA plan at the beginning of the month following your successful completion of 90 days of active employment, or upon acceptance as an established employee.

Make Additional Employee Optional MRCA Contributions

You may choose to make employee optional contributions of up to 4% of your annual earnings to your MRCA plan and receive a Company match. The Company will match 50% of your contributions.

Continuous ServiceMichelin Core Contributions

Employee Optional Contributions

Matching Contributions

Less than 5 years2% 1%, 2%, 3% or 4%

of earnings50% match of Employee Optional Contributions

5 or more years, but less than 15

4%

15 or more years 6%

Your MRCA Plan Contributionsremember, your MrCa contributions are tax-deductible. your income for tax purposes will be reduced by your eligible contributions.

*Effective January 1, 2016 the current years-of-service based formula will be changed to a formula that recognizes both age and service. The maximum Michelin care contributions will increase to 8%.

Michelin Retirement and Savings Program

| 19 |

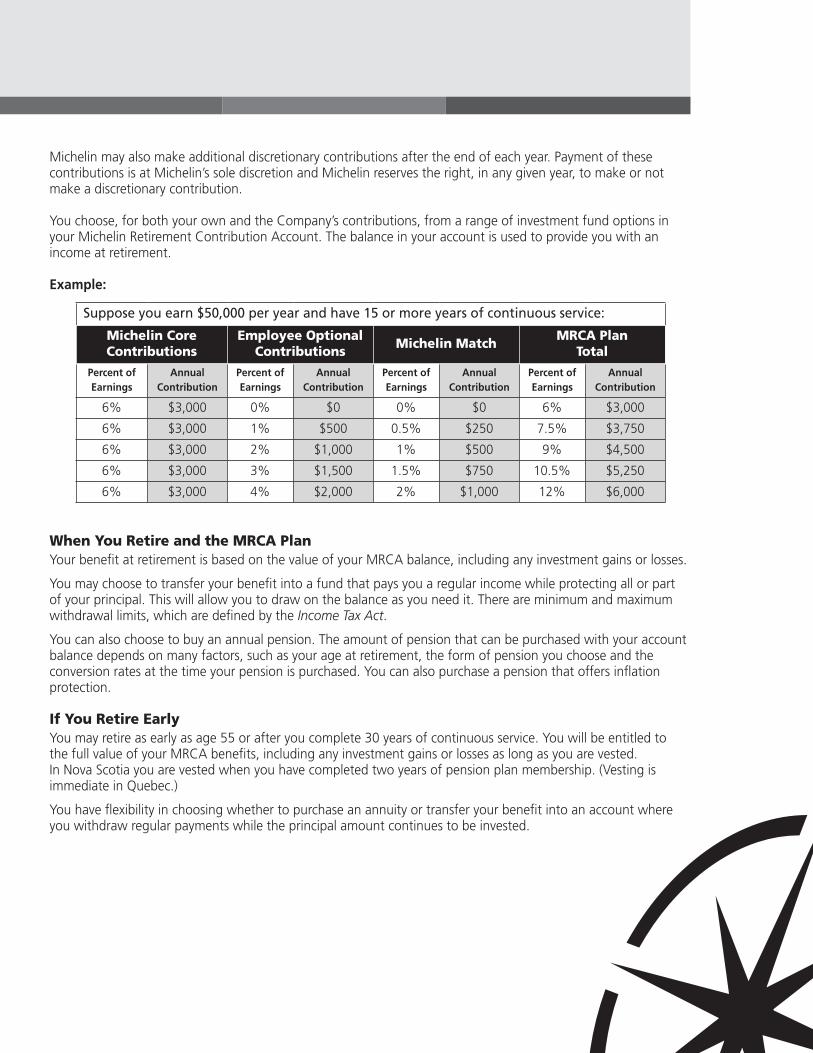

Michelin may also make additional discretionary contributions after the end of each year. Payment of these contributions is at Michelin’s sole discretion and Michelin reserves the right, in any given year, to make or not make a discretionary contribution.

You choose, for both your own and the Company’s contributions, from a range of investment fund options in your Michelin Retirement Contribution Account. The balance in your account is used to provide you with an income at retirement.

example:

Suppose you earn $50,000 per year and have 15 or more years of continuous service:

Michelin Core Contributions

Employee Optional Contributions

Michelin MatchMRCA Plan

Total

Percent of earnings

annual Contribution

Percent of earnings

annual Contribution

Percent of earnings

annual Contribution

Percent of earnings

annual Contribution

6% $3,000 0% $0 0% $0 6% $3,000

6% $3,000 1% $500 0.5% $250 7.5% $3,750

6% $3,000 2% $1,000 1% $500 9% $4,500

6% $3,000 3% $1,500 1.5% $750 10.5% $5,250

6% $3,000 4% $2,000 2% $1,000 12% $6,000

When You Retire and the MRCA PlanYour benefit at retirement is based on the value of your MRCA balance, including any investment gains or losses.

You may choose to transfer your benefit into a fund that pays you a regular income while protecting all or part of your principal. This will allow you to draw on the balance as you need it. There are minimum and maximum withdrawal limits, which are defined by the Income Tax Act.

You can also choose to buy an annual pension. The amount of pension that can be purchased with your account balance depends on many factors, such as your age at retirement, the form of pension you choose and the conversion rates at the time your pension is purchased. You can also purchase a pension that offers inflation protection.

If You Retire EarlyYou may retire as early as age 55 or after you complete 30 years of continuous service. You will be entitled to the full value of your MRCA benefits, including any investment gains or losses as long as you are vested. In Nova Scotia you are vested when you have completed two years of pension plan membership. (Vesting is immediate in Quebec.)

You have flexibility in choosing whether to purchase an annuity or transfer your benefit into an account where you withdraw regular payments while the principal amount continues to be invested.

| 20 |

Michelin retirement (Mr) Plan(Membership in the MR plan was restricted beginning after December 31, 2004)* Your Michelin Retirement (MR) Plan (which includes the Michelin Pension Plan and the BFGoodrich Pension Plan for Salaried Employees) provides you with a guaranteed pension at retirement based on a defined formula which takes into consideration your years of plan membership and earnings. Your earnings in the formula grow over time, as your earnings increase, and your final pension is based on your highest average annual earnings for 60 consecutive calendar months of pensionable service.

You are not required, nor are you permitted, to make contributions to your MR plan. When contributions are required, the Company makes the contributions to the plan that, combined with investment earnings, are sufficient to pay for the benefits accrued by all plan members.

Your MR plan provides you with a benefit according to a defined formula, based on your service and earnings as defined in your plan – the Michelin Pension Plan or the BFGoodrich Pension Plan for Salaried Employees. For details on the formula used to determine your pension benefits, refer to your Michelin Retirement Plan Guide or your BFGoodrich Pension Plan for Salaried Employees Guide.

When You Retire and the MR PlanIn addition to the benefit provided by the MR plan formula (either the Michelin Pension Plan or the BFGoodrich Pension Plan), the MR plan provides partial inflation protection by increasing the benefit each year based on a formula related to the Consumer Price Index. (BFG members: This partial inflation protection is available for benefits earned after January 1, 1994.) If you are at least age 55 when you retire, partial inflation protection will begin on the following January 1. If you retire before age 55, partial inflation protection will begin on the January 1 after you reach age 65.

If You Retire EarlyYou may retire as early as age 55 or when you have completed 30 years of continuous service. Your early retirement pension will be reduced based on the provisions in your MR plan because your pension will be paid over a longer period of time than if you had retired at age 65.

Of particular note is the bridge benefit for employees with 30 years of continuous service (or at age 55 for portions of service for BFG plan members). This benefit pays an extra pension benefit from your early retirement date to age 65. The bridge benefit is not subject to partial inflation protection.

*Effective January 1, 2016, the defined benefit provisions of the MR plan will be frozen. All active MR members will move to a new defined contribution provision of the MR plan.

Pension Plan information for Mr/MrCa MembersThis section pertains to MR pension plan members who chose to join the MRCA pension plan effective January 1, 2006. Effective January 1, 2016, the above noted changes will apply.

For Pension Service Before January 1, 2006• The value of your pension, for pensionable service before January 1, 2006, will remain in your MR plan.• At retirement, termination of service or death, your benefit for pension service before January 1, 2006,

will be paid from your MR plan. Your pensionable service will be frozen at its December 31, 2005, level. However, your benefit from your MR plan will be calculated using your highest average annual earnings, as defined in the plan, at the date the benefit becomes payable (on retirement, termination of service or death).

• Under your MR plan:– Your service for early retirement eligibility includes your service under both your MR and the MRCA

plans.– Your service in the MRCA plan will also count in determining your eligibility for the bridge benefit.

• Your service in the MRCA plan will not be included in the MR benefit calculation.

| 21 |

For Pension Service On and After January 1, 2006• Michelin contributes company contributions on your behalf as defined in the plan. You may, but are not

required to, make employee optional contributions.• You choose from a range of investment funds for your contributions and Michelin’s contributions. You are

responsible for ongoing investment choices. • Your service in the MRCA plan will count in determining your eligibility for the bridge benefit under your

MR plan. Your service for early retirement eligibility includes your service under the MR plan and MRCA plan.

• At retirement or termination of service, you will be entitled to your vested MRCA plan balance, made up of contributions from January 1, 2006, adjusted by any investment gains or losses. If you die before retiring, your vested MRCA balance will be transferred to your spouse, beneficiary or estate.

Michelin Group registered retirement savings Plan (rrsP)Michelin encourages employees to supplement their retirement savings by regular investment in a tax-sheltered RRSP. The Michelin Group Registered Retirement Savings Plan (Group RRSP) is designed to assist you in your savings efforts by allowing you to make contributions through payroll deductions.

EligibilityYou may participate in the plan at the beginning of the month following your successful completion of 90 days of active employment or upon acceptance as an established employee. You may open a personal Group RRSP account, and/or a spousal Group RRSP account. Enrol online at www.mysunlife.ca/michelin; this requires your Access ID and password, call Sun Life for assistance.

ContributionsYou may make contributions to the plan via payroll deductions, providing you have RRSP room available. You may also make lump-sum contributions to your account, as well as transfers from another registered plan. For more information, contact the Sun Life call center.

Michelin Contributions – Co-fundingEach calendar year Michelin will contribute 25 cents for each dollar you contribute to your Group RRSP account (employee or spousal) to the lesser of:

• 1% of your prior year Michelin gross earnings (excluding taxable benefits);• $600.00; or• 20% of the RRSP room arising from Michelin gross earnings.

Co-funding contributions:• are made only on contributions made through payroll deductions;• only arise from prior year Michelin Canada earnings;• are not included in your pensionable earnings or vacation gross earnings;• are taxable income, but the tax effect may be offset by the corresponding tax reduction available on each

contribution as it is made; and• are vested immediately, which means you “own” the contributions as soon as they are made to your

account and you can invest them in the same way as you would invest your own contributions.

| 22 |

Investment AllocationYou may invest in several types of investment funds. More information about these funds and how to choose your investments (as well as other details about the plan) may be found in the employee information package available from Sun Life, or at the Sun Life member website www.mysunlife.ca/michelin.

Your contributions will be invested according to the most recent direction you provided to Sun Life. if no instructions for investment are on file, the funds will be deposited into the plan’s default fund, currently the sun Life Financial Granite segregated Fund closest to, but without exceeding your 65th birthday.

You may change the investment direction for either current holdings or future contributions at any time through Sun Life. You can transfer money between investments at any time. There is no charge for the transfers unless you make a transfer into a fund followed by a transfer out of the same fund within 30 calendar days (called short-term trading – see the Sun Life member website for more information).

Plan AdministratorThe Group RRSP is administered by Sun Life and is registered under Group plan number 77991. Your individual account number under the plan is your employee number.

Michelin Tax Free savings account (TFsa)The TFSA allows you to choose from the same funds that are available through your Michelin Retirement and Savings Program. Contributions are not tax-deductible. Save for short-term goals or build additional retirement savings by contributing up to $5,000 per year (indexed annually to inflation and rounded to the nearest $500). And here’s what else is really great about it:

You’re never too old for a TFSA. As long as you’re 18 or older and a Canadian resident, you can save with a TFSA and you won’t be forced to take your money out at retirement age.

Take money out and replace it later. If you make a withdrawal from your account, you can re-contribute that money later without being taxed. The amount you withdraw gets added to what you’re allowed to contribute for the next year.

Know your money is always available to you. There is no waiting period for you to use the money in your account.

a TFsa offers:• A flexible savings account within your existing group plan;• Tax-free investment growth;• Unlimited tax-free withdrawals;*• The ability to carry forward unused contribution room;• Withdrawal amounts added to the available contribution room in the following year; and• Lifetime contributions with no requirement to withdraw at a certain age.

*Note: Your most recent Notice of Assessment from Canada Revenue Agency contains your personal limit information. While withdrawals from the TFSA are not subject to tax, fees for withdrawals are applicable. You have one free withdrawal per year, and a $25 fee will apply to each subsequent withdrawal or transfer. To take advantage of this free withdrawal, you must contact our Customer Care Centre at 1-866-896-6976.

| 23 |

Michelin non-registered savings account (nreG)The Non-Registered savings account allows you to choose from the same funds that are available through your Michelin Retirement and Savings Program. Contributions are not tax-deductible. You pay tax annually on any investment earnings that occur while the funds are in the account.

a nreG offers:• A flexible savings account within your existing group plan,• Lifetime contributions with no requirement to withdraw at a certain age;• There is no maximum yearly contribution, you may contribute any amount; and• Unlimited tax-free withdrawals.*

* A $25 fee will apply to each withdrawal made. Co-Funding Employer contributions do not apply to the NREG.

“My investment advice”You may not know how to make the investment choices that are right for you. You want to feel comfortable with your investment decisions and you want to make sure you’re getting all you can out of your plan.

Sound familiar? A lot of us feel this way. As a group plan member you don’t need a background in investing to make sound decisions. That’s because your plan offers you my investment advice from Sun Life Financial.

This is a one-on-one personalized service from fully licensed specialists – all Investment Advice Specialists are licensed in their home province and have non-resident life licenses for all other provinces and territories. Their annual license renewal process requires continued education, and all specialists have completed a Canadian Securities Course (CSC) or Investment Funds Institute of Canada (IFIC) designation

You can call Sun Life Financial’s Customer Care Centre 1-866-896-6976 from 9:30 a.m. to 5:30 p.m. ET, each business day for personal, unbiased, one-on-one advice from an Investment Advice Specialist. Each call starts with determining your risk tolerance. So, if you haven’t already done so, you can complete the investment risk Profiler questionnaire on your own before calling, or complete it with the help of the Investment Advice Specialist while on the phone.

Once you and the Investment Advice Specialist know your risk tolerance, the specialist will work with you to pick the investments offered under your plan that are most appropriate for you based on your particular situation. That includes:

• reviewing your risk tolerance and how that might fit particular asset mixes;• reviewing your plan’s investment options;• providing advice on which funds fit your profile and situation; and• completing any transactions over the phone, with your consent.

new Michelin retirement PlannerTo further help you plan for your future, in early 2014, we introduced a personalized retirement planner.

The Michelin Retirement Planner will help you determine and mange your retirement savings. It is pre-populated with your personal information (earnings, date of birth, pension plan data) and allows you to project what your retirement benefits would be at the age you chose. You can make assumptions about your future contributions, salary as well as project any savings you may have in personal registered investments, such as registered retirement savings.

The projected values in the retirement Planner are estimates designed to assist you with planning your retirement income. While this program is based on current and future Michelin provisions as well as your personal data and government legislation, the official plan documents supersede any information or projection shown in the retirement planner. Any estimates shown cannot be construed as a warranty or guarantee of any pension payment. For members of the Michelin Retirement (MR) Plan, an accurate estimate of your Defined Benefit components will be provided from Aon Hewitt, our pension administrator, when you request Michelin retirement estimates.

Go to: https://www.ebo.aon.ca/clients/Michelin/login.asp

If you have misplaced your PIN or have difficulty logging in, contact your Pension Coordinator at 1-877-311-7367.

| 24 |

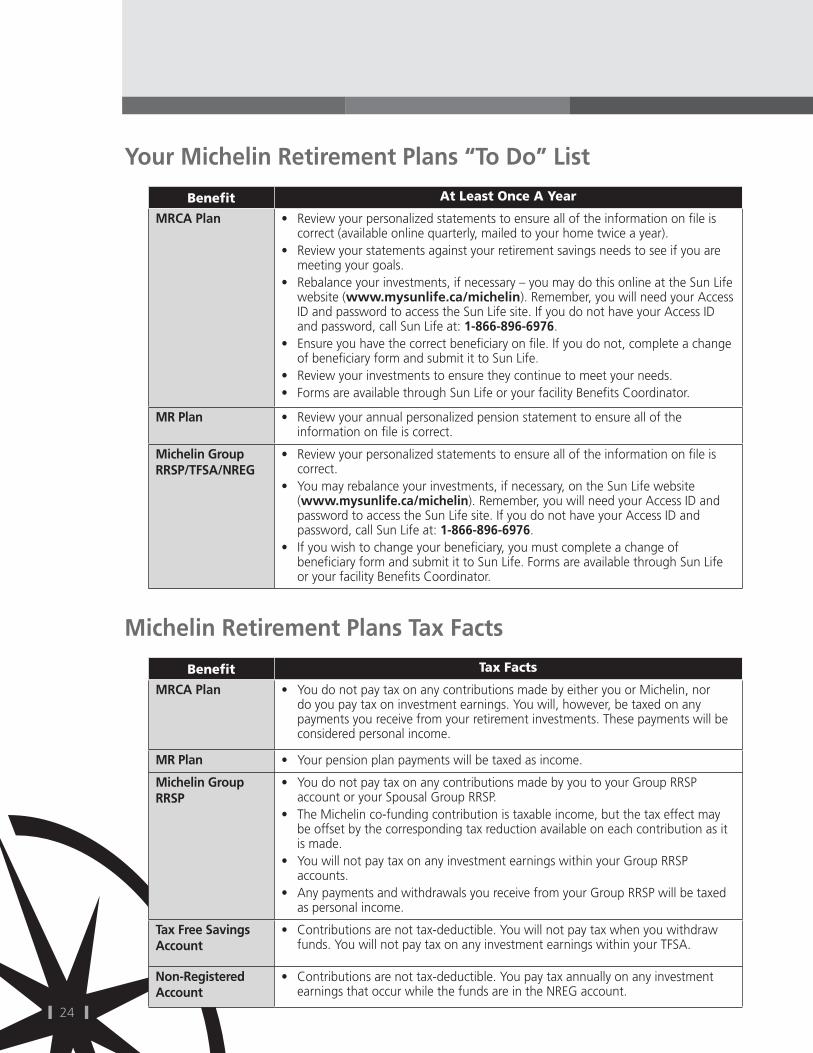

your Michelin retirement Plans “To Do” List

Benefit At Least Once A Year

MrCa Plan • Review your personalized statements to ensure all of the information on file is correct (available online quarterly, mailed to your home twice a year).

• Review your statements against your retirement savings needs to see if you are meeting your goals.

• Rebalance your investments, if necessary – you may do this online at the Sun Life website (www.mysunlife.ca/michelin). Remember, you will need your Access ID and password to access the Sun Life site. If you do not have your Access ID and password, call Sun Life at: 1-866-896-6976.

• Ensure you have the correct beneficiary on file. If you do not, complete a change of beneficiary form and submit it to Sun Life.

• Review your investments to ensure they continue to meet your needs.• Forms are available through Sun Life or your facility Benefits Coordinator.

Mr Plan • Review your annual personalized pension statement to ensure all of the information on file is correct.

Michelin Group rrsP/TFsa/nreG

• Review your personalized statements to ensure all of the information on file is correct.

• You may rebalance your investments, if necessary, on the Sun Life website (www.mysunlife.ca/michelin). Remember, you will need your Access ID and password to access the Sun Life site. If you do not have your Access ID and password, call Sun Life at: 1-866-896-6976.

• If you wish to change your beneficiary, you must complete a change of beneficiary form and submit it to Sun Life. Forms are available through Sun Life or your facility Benefits Coordinator.

Michelin retirement Plans Tax Facts

Benefit Tax Facts

MrCa Plan • You do not pay tax on any contributions made by either you or Michelin, nor do you pay tax on investment earnings. You will, however, be taxed on any payments you receive from your retirement investments. These payments will be considered personal income.

Mr Plan • Your pension plan payments will be taxed as income.

Michelin Group rrsP

• You do not pay tax on any contributions made by you to your Group RRSP account or your Spousal Group RRSP.

• The Michelin co-funding contribution is taxable income, but the tax effect may be offset by the corresponding tax reduction available on each contribution as it is made.

• You will not pay tax on any investment earnings within your Group RRSP accounts.

• Any payments and withdrawals you receive from your Group RRSP will be taxed as personal income.

Tax Free savings account

• Contributions are not tax-deductible. You will not pay tax when you withdraw funds. You will not pay tax on any investment earnings within your TFSA.

non-registered account

• Contributions are not tax-deductible. You pay tax annually on any investment earnings that occur while the funds are in the NREG account.

| 25 |

Additional Michelin Benefits, Programs and Services

Business Travel accident insuranceMichelin provides all of its employees with additional accident insurance in addition to your existing Michelin Health & Welfare Choice insurance coverage when traveling on business for the Company.

This plan will provide your beneficiary with a lump-sum benefit if an accident causes your death. Unless you have specified otherwise, the beneficiary you have designated for your Company-paid life insurance coverage is also the recipient of any Business Travel Accident Insurance. If you lose your sight, hearing, speech or limbs as a result of an accident while traveling on business for the Company, you will receive a benefit based on the degree of your loss.

The plan is underwritten by ACE INA Life Insurance, policy number AB10337101. Michelin pays 100% of the premiums associated with this insurance.

When You Are CoveredThis plan provides you with 24-hour coverage during a business trip. If you choose to take a personal side trip while traveling on business, you will continue to be covered, both seven days immediately prior to or following an authorized business trip.

Your CoverageYour coverage is equal to three times your basic annual earnings rounded up to the next highest thousand dollars (if not already a multiple thereof) to a maximum of $500,000.

If you die as a result of an accident while traveling on business for the Company, your beneficiary will receive a lump-sum payment of your amount of insurance.

This insurance also provides repatriation, rehabilitation, family transportation, spousal occupational training, home alteration and vehicle modification, and seat belt benefits under certain conditions and limitations.

| 26 |

Loss means, with regard to:

a) Hand or foot, actual severance through or above the wrist or ankle joint;

b) Arm or leg, actual severance through or above the elbow or knee joint;

c) Thumb and index finger, actual severance through or above the first phalange;

d) Fingers, actual severance through or above the first phalange of all four fingers of the same hand;

e) Toes, actual severance of both phalanges of all toes of the same foot;

f) Sight, total and irrecoverable loss of sight;

g) Speech, total and irrecoverable loss of speech which does not allow audible communication in any degree;

h) Hearing, total and irrecoverable loss of hearing which cannot be corrected by any hearing aid or device; or

i) Paralysis of limbs, complete and irrecoverable paralysis of such limbs.

Loss of use means the total and irrecoverable loss of function of an arm, hand, or leg provided such loss of function is continuous for 12 consecutive months and such loss of function is thereafter determined on evidence satisfactory to the insurer to be permanent.

Loss ScheduleWhen an injury results in any of the following losses within one year after the date of the accident, the benefit payable will be based on the table below:

Nature of LossAmount of

Coverage Paid

Loss of life 100%

Loss of both hands or both feet 100%

Loss of entire sight of both eyes 100%

Loss of one hand and one foot 100%

Loss of one hand and entire sight of one eye 100%

Loss of one foot and entire sight of one eye 100%

Loss of speech and hearing in both ears 100%

Loss of use of both arms or both hands or both feet

100%

Loss of thumb and index finger of same hand 1/3 of 100%

Loss of four fingers of same hand 1/3 of 100%

Loss of all toes of same foot 1/8 of 100%

Loss of one arm or one leg 3/4 of 100%

Loss of use of one arm or one leg 3/4 of 100%

Loss of one hand or one foot 2/3 of 100%

Loss of entire sight of one eye 2/3 of 100%

Loss of use of one hand or one foot 2/3 of 100%

Loss of speech or hearing in both ears 2/3 of 100%

Loss of hearing in one ear 1/4 of 100%

Paralysis of both upper and lower limbs (quadriplegia)

200%

Paralysis of both lower limbs (paraplegia) 200%

Total paralysis of upper and lower limbs of one side of the body (hemiplegia)

200%

| 27 |

LimitationsThe total amount payable under the Business Travel Policy for losses resulting from one accident will be $5,000,000. If the amount otherwise payable exceeds that, the amount paid to each employee involved in the same accident will be reduced on a pro-rata basis based on each insured person’s coverage (ie. If there are multiple employees in one accident, the maximum payout for that one accident is 5,000,000).

ExclusionsThis policy does not cover any loss resulting from:

a) Commuting between home and home plant/office or work area;b) Intentionally self-inflicted injuries, suicide or attempt thereat, while sane or insane;c) Declared or undeclared war or any act thereof;d) While serving on full-time active duty in the Armed Forces of any country or international authority;e) Injury resulting from an accident which occurs while you are on, boarding or alighting from an aircraft

engaged in one or more of the following activities:i. While being used for any test or experimental purpose; orii. While the insured person is operating, learning to operate or serving as a member of the crew

thereof; oriii. While being operated by or for or under the direction of any military authority, other than

transport type aircraft operated by the Canadian Armed Forces Air Transport Command or the similar air transport service of any other country; or

iv. With the exception of aircraft owned or leased by Michelin North America, any such aircraft or device which is owned or leased by or on behalf of Michelin Canada or any subsidiary or affiliate of Michelin Canada, or by an insured person or any member of his/her household; or

v. While being used for acrobatic flying as defined by the Department of Transport; orvi. While being operated where a special permit or waiver from the Department of Transport is

required even though granted, other than a permit waiver issued because of the territory to be flown over or landed upon; or

vii. While being used for crop dusting or spraying, seeding, fire fighting, sky writing, pipeline inspection, power line inspection, aerial photography, exploration, racing, endurance test, or exhibition stunt flying.

Canada savings BondsFrom October 1st to November 1st, you are able to go online at work or at home to purchase a bond for you or for someone else.

www.mybonds.gc.ca – You can also make changes to your existing Canada Savings Bond (CSB) contribution.

If you do not want to change anything to your current bonds, there’s nothing you need to do!

Call 902-753-1016 for further details.

| 28 |

educational reimbursementIf you take educational programs outside of regular working hours, you may be eligible for reimbursement for some or all of your expenses under Michelin’s Educational Reimbursement Policy. The Company will reimburse you for certain educational expenses you incur when taking recognized courses and seminars relating to your current role or future development within the organization. More detailed information on this program is available in personnel policies and can be obtained from your facility Personnel Department.

The following types of courses and degree programs are typically approved for reimbursement:• Technical disciplines, such as electrical and mechanical engineering and technology, chemistry and physics,

electronics, and other areas that routinely relate to Michelin business; and• Administrative disciplines, including: business administration, accounting, information technology,

economics and finance.

Degree programs in the humanities and social sciences are typically not approved for reimbursement.

If you would like to apply for educational reimbursement, at least six to eight weeks before you need to register for the course you should:

• Discuss your education objective with your supervisor or manager, who will help determine whether the course curriculum is directly related to your job or to your career with Michelin;

• If you are considering a university degree, you should also discuss the degree program with your Area Personnel Manager, who will help determine whether the degree and school meet Michelin’s criteria for approval; and

• Complete an application for educational reimbursement form, available from your facility Personnel Department.

If you are unable to complete a course due to transfer within the Company, you will be reimbursed for the full amount of eligible costs incurred up to the date of your transfer. However, if you withdraw from a course, voluntarily leave Michelin or are involuntarily terminated, you will not be reimbursed for any outstanding expenses.

employee Tire Program (eTPX)The Employee Tire Program (ETPX) gives you the opportunity to obtain Michelin, BFGoodrich and Uniroyal tires, if they are available, at no cost, other than government tax. Under the program, you may receive a total of 20 tires over a consecutive five-calendar-year period consisting of the current year and previous four years, up to a maximum of eight tires per year.

EligibilityIf you have more than one year of continuous service, the Company will provide you with new passenger or light truck tires for vehicle(s) that are registered in your name or the name of your spouse or dependent as defined in the MHWC Eligibility section of this Guide.

Remember, any tires acquired for your dependents are counted as part of your entitlement. If you die while employed by Michelin, your family will continue to be eligible for tires for up to six months after your death.

The TiresCertain sizes and tread designs may not be available or applicable. Your facility Personnel Department can confirm the range of sizes available under this program. Motorcycle tires are also available under limited circumstances. Any tires you order must be in accordance with the Bennett Garfield or the Marketing and Sales Technical Staff guides for the vehicle on which the tires are to be mounted. You are not obligated to use a designated dealer for the installation of your tires.

| 29 |

You Pay Tax on Your TiresBoth the provincial and federal governments consider ETPX tires as a taxable benefit. To calculate the tax payable, a standard value per tire has been set for all ETPX tires. You will pay:

• Income tax on the tires, according to your personal income tax rate; • Goods and Services Tax (GST) or Harmonized Sales Tax (HST); and• Provincial sales tax, based on the tax rate in your province.

These taxes will be deducted from your pay when you request the ETPX form. You may choose to have the taxes deducted over one or two pay periods (default is two pay periods if not indicated by you), following the date on which your ETPX form was issued. You will also be responsible for costs associated with mounting and balancing your ETPX tires, as well as disposing of or recycling your previous tires.

Your ResponsibilitiesWhen you apply for ETPX tires, they become your property. Therefore, it is your responsibility to:

• Determine when tires should be replaced due to wear. note: Your ETPX tires are covered by a manufacturer’s warranty, and you may visit any participating dealer for an adjustment under the terms of the warranty policy;

• Replace your tires at your own cost or by using your ETPP coupons (see employee Tire Purchase Program section in this Guide) or by using the ETPX program; and

• Keep all forms issued to you in a safe place. Forms issued to you will not be replaced.

The Company accepts no liability whatsoever for any injury, loss or damage to any person or property occurring with respect to a vehicle fitted with ETPX tires.

To Participate in the ETPX Program• Obtain the appropriate form from your facility Personnel Department. Marketing and Sales employees can

contact at: 1-877-661-8473; or by email at: employee-canada, eTPP-eTPX-nM04505• When your form is complete and authorized by your facility Personnel Department, contact a designated

dealer to order your tires. You can obtain a list of designated dealers in your area from your facility Personnel Department; and

• If you have questions about tire fitment, ask your designated dealer.

note: Tires from the ETPX program are strictly for your own personal use or that of your spouse or eligible dependent. You, your spouse, or your eligible dependent may not use the tires at any time for remuneration. These tires are not to be put on business vehicles.

| 30 |

employee Tire Purchase Program (eTPP)Under the Employee Tire Purchase Program (ETPP), you and your family (including your spouse, parents, grandparents, children, brothers, sisters, and in-laws) have the opportunity to purchase Michelin, BFGoodrich and Uniroyal tires for your own personal use at a discounted rate. You are eligible to participate in this program from your first date of hire.

How ETPP WorksYour facility Personnel Department will provide you with eight ETPP discount coupons per year, which are valid only for the calendar year in which you receive them. These coupons entitle you to a discount off of the:

• Base price for first choice tires; or• Adjusted price of any tire eligible for replacement under a Michelin warranty program regardless of the

original method of purchase (ETPX, ETPP or retail) of the tire being replaced.

note: Certain sizes and tread designs may not be available or applicable. Your facility Personnel Department can confirm the range of sizes available under this program.

Any tires you order must be in accordance with the Bennett Garfield or the Marketing and Sales Technical Staff guides for the vehicle on which the tires are to be mounted.

Your ResponsibilitiesWhen you apply for ETPP tires, they become your property. Therefore, it is your responsibility to:

• Ensure these coupons are only used by you or an eligible member of your family as described above;• Determine when tires should be replaced due to wear.

note: Your ETPP tires are covered by a manufacturer’s warranty and you may visit any participating dealer for an adjustment under the terms of the warranty policy. You may use additional ETPP coupons toward adjustment replacement cost;

• Replace your tires at your own cost, by using ETPP coupons or by using the ETPX program; and• Keep your coupons in a safe place. Coupons issued to you will not be replaced.

The Company accepts no liability whatsoever for any injury, loss or damage to any person or property occurring with respect to a vehicle fitted with ETPP tires.

note: All financial arrangements are between you and the designated dealer.

To Take Advantage of the ETPP Benefit• If you have not already received your coupons for the year, pick them up from your facility Personnel

Department, along with a list of designated dealers;• Contact a designated dealer to order your tires; • The dealer will inform you of the availability and size of your tires;• When the tires are available, provide the dealer with your coupons and remaining cost on the tires.

The dealer will provide you with your tires and the warranty booklet; and• If you have questions about tire fitment, ask your designated dealer.

nOTe: • You are not obligated to use a designated dealer for the installation of your tires;• You pay provincial sales tax and GST/HST on the tires you receive; and• If you die while employed at Michelin, any remaining ETPP coupons may be used by your eligible family

members until the expiry date of the coupons.

note: Tires from the eTPP program are exclusively for your own personal use or for the use of eligible family members. eTPP coupons may not be sold or given to anyone else. These are not for use on business vehicles.

| 31 |