Embed Size (px)

Citation preview

BERMUDA AND CAYMAN - REGISTRATION AND LEASING OF AIRCRAFT – A COMPARISON

Page 2 of 19

Foreword

This guide has been prepared for the assistance of those who are considering the

registration of aircraft in Bermuda or the Cayman Islands and to provide a

comparison of the registration requirements, process and costs in these two

jurisdictions.

We do not attempt to cover these subjects in detail but rather aim to deal in broad

terms with the matters of significance.

Before proceeding with any matter discussed herein, persons are advised to consult

with their legal, tax and other professional advisers in their respective jurisdictions.

This Memorandum has been prepared on the basis of the law and practice as at the

date referred to below. All fees referred to herein are correct at the time of publication

and are subject to further review.

Conyers Dill & Pearman

February 2013

Page 3 of 19

TABLE OF CONTENTS

1. GENERAL OVERVIEW

1.1 Benefits of Registration in Bermuda or Cayman

1.2 Tax Neutrality

2. OPERATIONAL OVERSIGHT

2.1 Air Navigation (Overseas Territories) Order 2007

2.2 Article 83 bis

2.3 Cape Town Convention

3. COMPARISONS

Page 4 of 19

1. GENERAL OVERVIEW

1.1 Benefits of Registration in Bermuda or Cayman

Both Bermuda and the Cayman Islands offer the aircraft industry a commercially

flexible and adaptable approach from stable economic and political jurisdictions.

Whether in Bermuda or Cayman, owners and operators enjoy an administration that

is rated as a Category 1 Aviation Regulatory Authority by the US Federal Aviation

Administration. The authorities in both jurisdictions are prepared to accept more

than one internationally recognised set of airworthiness requirements, various flight

crew licences for validation and a “low‐profile” registration mark which some

operators consider of value when operating in areas of the world which may be

subject to certain security risks or political instability. The Bermuda registration

marks “VP‐B” and “VQ‐B” and the Cayman Islands registration mark “VP‐C” are

seen as neutral marks as opposed to major European marks or the American marks.

Further, owners and operators have expressed satisfaction with the responsiveness of

the applicable aviation authorities in Bermuda and Cayman in dealing with their

enquiries and requirements. This is made possible by the absence of the degree of

administrative bureaucracy encountered in some other major jurisdictions. For

example, some jurisdictions may impose requirements that an aircraft registered in

that jurisdiction must be based and primarily used in that jurisdiction. Aircraft

registration in either Bermuda or Cayman are not subject to any such requirements

and aircraft registered in either jurisdiction may be operated anywhere in the world

(excluding war zones and similar areas).

1.2 Tax Neutrality

On an aircraft finance transaction, it is generally imperative that there is no tax

leakage in the deal. With the increasing size of recent transactions, even a small

number of basis points of tax can amount to a large overall tax charge. In both

Bermuda and Cayman, however, there is no corporation or other tax on any company

carrying on business in or outside Bermuda or Cayman. For further information, see

the chart below.

Page 5 of 19

2. OPERATIONAL OVERSIGHT

2.1 Air Navigation (Overseas Territories) Order 2007

Both Bermuda and Cayman are Overseas Territories of the United Kingdom and, as

such, the legislative framework relating to the registration of aircraft emanates from

the United Kingdom pursuant to the provisions of the Air Navigation (Overseas

Territories) Order 2007 (the “Order”). Air Safety Support International (“ASSI”), a

wholly owned subsidiary company of the Civil Aviation Authority of the United

Kingdom, acts as the oversight regulatory body of the Overseas Territories of the

United Kingdom in relation to aviation matters.

The Bermuda Department of Civil Aviation (the “BDCA”) implemented Article 85 of

the Order as of 1 November 2009, requiring the operators of all aircraft who fall

within the provisions of such Article (whether categorised as private or commercial)

to comply with the safety and other requirements set out in Article 85. The BDCA

brought in enforcement of Article 85 in advance of the deadline imposed by the

International Civil Aviation Organisation (“ICAO”).

The Civil Aviation Authority of the Cayman Islands (ʺCAACIʺ) has also implemented

Article 85 of the Order by requiring operators of aircraft on the Cayman Islands

Registry to achieve compliance by 1 January 2011.

Aircraft approved under Article 85 are deemed to be operating at a higher safety

level. In certain circumstances this can allow operators of both commercial and

private aircraft to negotiate a reduction in their annual aircraft insurance with their

insurance companies.

2.2 Article 83 bis

Article 83 bis is an amendment to the Convention on Civil Aviation signed in Chicago

on 7 December 1944 (the “Convention”). The amendment authorises Contracting

States (as defined in the Convention) to make bilateral transfers of safety oversight

responsibilities relating to the lease, charter, and interchange of aircraft. Typically,

the State of Registry of an aircraft transfers the responsibilities to the state in which

the aircraft is to be based (“State of Operator”). Article 83 bis guarantees that bilateral

agreements for transfers of oversight responsibilities are recognised by all states

signatory to ICAO pursuant to the Convention. In this way, certain functions and

Page 6 of 19

duties normally carried out by a State of Registry are transferred, under strict

guidelines, to the State of Operator. The aim of this highly successful operational

initiative is to ensure on the spot safety oversight and allow for greater efficiencies at

both the government and operator level.

Bermuda currently has agreements with:

Russian, Minister of Transport,

Austrian, Austro Control,

Republic of Uzbekistan, Flight Safety Oversight, and

Republic of Azerbaijan, State Concern.

Cayman currently has an agreement with:

The General Authority of Civil Aviation of Saudi Arabia.

2.3 Cape Town Convention

Once widely in force, the Cape Town Convention on International Interests in Mobile

Equipment (the “Cape Town Convention”) and the related Aircraft Equipment

Protocol (the “Protocol”) will facilitate the cross‐border financing and leasing of,

amongst other aviation assets, aircraft engines. There will be an ability to register

international interests in such assets. Until such time, owners and financiers alike will

look to traditional methods of control over the use of their asset. They will use a full

range of backstops, both legal and practical, to ensure their valuable security is

available in an expected and acceptable location at the time enforcement and

repossession is being contemplated.

While the United Kingdom (and hence Bermuda and Cayman) is, as yet, not a

signatory to the Protocol, registration of a registrable international interest or interests

may be possible where an aircraft owned by a Bermuda or a Cayman special purpose

vehicle (“SPV”) structure has a certain connection to a jurisdiction which is a

signatory. In these circumstances, the appropriate office of Conyers Dill & Pearman

will be able to arrange for a third party registration service in regards to the relevant

equipment.

Page 7 of 19

Certain provisions of the Cape Town Convention have been given domestic effect in

the Cayman Islands by virtue of the Cape Town Convention Law 2009 (the “Law”).

The primary benefits of the new Law are the certainty created by the International

Registry and the clarity brought to matters of international enforcement. The Law

gives recognition in the Cayman Islands to the registered rights in the internet‐based

International Registry of mobile assets created under the Cape Town Convention and

sets out legal remedies for defaults in financing arrangements. The Law also

addresses jurisdictional issues and specifies the effects of international interests

against third parties.

3. COMPARISON

BERMUDA CAYMAN

1. GENERAL

Regulatory

Authority

The Bermuda Department of Civil

Aviation (“BDCA”). The Bermuda

Register has been in existence since 1931.

Private and commercial aircraft

registrations are accepted by the BDCA.

The Civil Aviation Authority of the

Cayman Islands (the “CAACI”). The

Cayman Islands Register has been in

existence since 1976.

The CAACI will register aircraft that are

based overseas and operated in the

private category, provided such aircraft

are above a MTOW of 5700 Kg, except

turbojet aircraft or helicopters based on

Cayman Islands registered yachts. The

CAACI will also register aircraft based

overseas and operated for commercial

air transport when there is an Article 83

bis agreement in place with the State of

Operator.

Number of

Aircraft

545 ‐ 179 private aircraft and 366

commercial aircraft.

173 ‐ 154 private aircraft and 19

commercial aircraft.

Page 8 of 19

BERMUDA CAYMAN

Registered

Registration Mark(s)

VP‐B or VQ‐B followed by two letters

assigned to the specific aircraft.

VP‐C followed by two letters assigned to

the specific aircraft.

Persons

entitled to

Register

Current Bermuda Government policy

stipulates that an application to register

an aircraft will normally only be

accepted from a person residing in

Bermuda or a body incorporated in

Bermuda and having its registered office

in Bermuda.

In practice the registrant will most often

be a Bermuda exempted company which

holds a legal or beneficial interest by

way of ownership in the aircraft.

In addition, if an aircraft is chartered by

demise (leased) to a Bermuda company,

registration in the name of the charterer

during the period of the charter may be

permitted, whether or not an unqualified

person is entitled as owner to a legal or

beneficial interest in the aircraft.

Persons wishing to register an aircraft in

the ʺPrivate Categoryʺ in the Cayman

Islands must first prove eligibility in

accordance with Article 4 (2) & (3) of the

Order. The following persons and no

others shall be qualified to hold a legal

or beneficial interest by way of

ownership in an aircraft registered in the

Territory or a share therein:

(a) The Crown in right of Her Majesty’s

Government in the United Kingdom

or the Government of the Cayman

Islands ;

(b) Commonwealth citizens*;

(c) British protected persons*;

(d) Bodies incorporated in some part of

the Commonwealth and having their

principal place of business in any

part of the Commonwealth.

*As defined in the British Nationality

Act 1981.

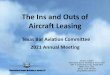

Registration

Process

On 1 February 2008, the BDCA

implemented the Aircraft Information

and Records System (“AIRS”). AIRS is

essentially an electronic filing and record

keeping system to be used by authorised

The registration process may be initiated

by completing and submitting all of the

relevant application forms to the CAACI

for the approval of the Director General

of Civil Aviation (“DGCA”). The

Page 9 of 19

BERMUDA CAYMAN

persons during the initial registration of

the aircraft and to renew certificates and

licences while an aircraft remains

registered in Bermuda. The initial

application for “approval in principle” in

relation to a proposed registration must

now be submitted by “authorised and

certified users” which includes certain

personnel of Bermuda law firms.

If a formal approval in principle has

been granted by the Director of Civil

Aviation via AIRS, formal application for

full registration may be made. Full

particulars of the application procedure

are provided in the Department of

Aviation’s “Bermuda Register of Aircraft

and Flight Crew – General Information

Brief”, copies of which may be obtained

from the Director of Civil Aviation upon

request or at website www.dca.gov.bm

application forms must be accompanied

by the following items:

(a) applicant company’s certificate of

incorporation or comparable

document;

(b) a list of authorised company

signatories with a signature sample

of each;

(c) a general description of the

company’s activities, geographical

areas and main base of aircraft

operations; and

(d) a statement which states that the

aircraft will only be operated within

the definition of “Private Category”.

Private Category is defined as being

“any purpose other than public

transport or aerial work”, and

therefore, excludes aircraft used for

the purposes of “hire and reward”.

Full particulars of the application

process and procedure are provided by

the CAACI. Copies of the application

documentation may be obtained from

the CAACI upon request or at the

CAACI’s website

www.caacayman.com

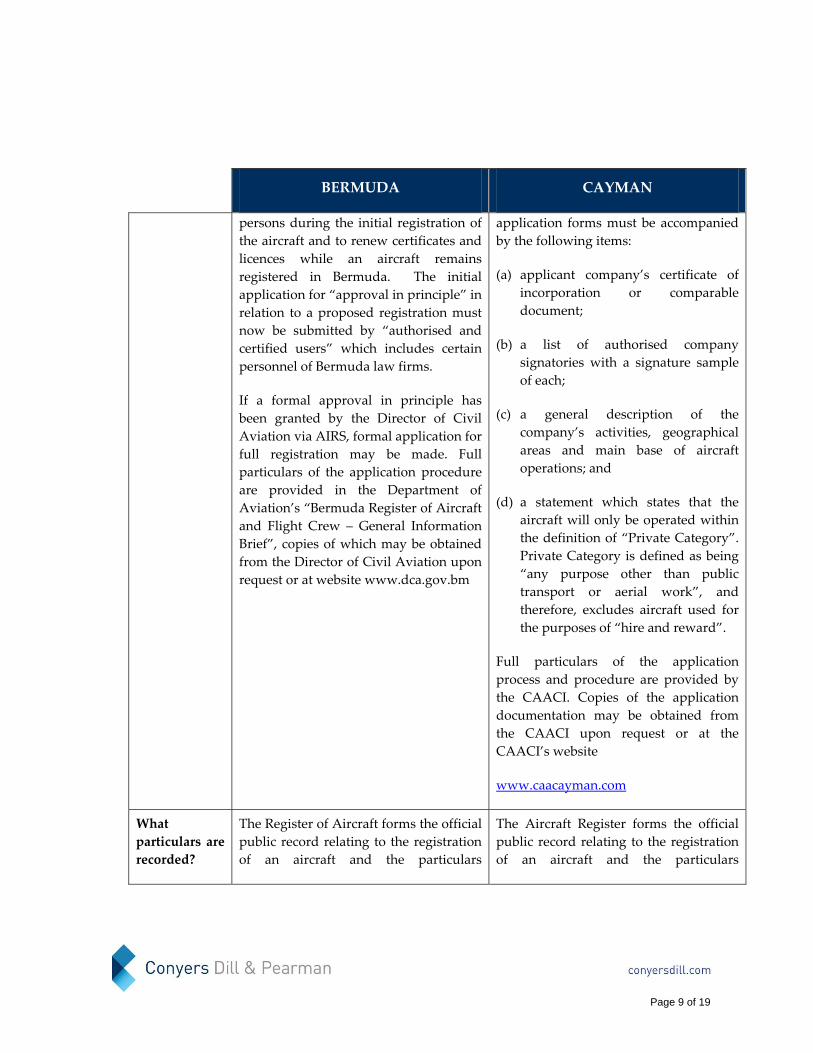

What

particulars are

recorded?

The Register of Aircraft forms the official

public record relating to the registration

of an aircraft and the particulars

The Aircraft Register forms the official

public record relating to the registration

of an aircraft and the particulars

Page 10 of 19

BERMUDA CAYMAN

recorded in it are the only details which

are publicly available. All other records

related to the owner, aircraft, etc are

treated as confidential.

The Register of Aircraft will include the

following particulars:

(a) the registration certificate number;

(b) the aircraft’s nationality mark and

the registration mark assigned to it;

(c) the name of the constructor of the

aircraft and its designation;

(d) the aircraft serial number;

(e) the name and address of every

person who is entitled to a legal

interest in the aircraft or a share in it,

or, in the case of an aircraft which is

the subject of a charter by demise,

the name and address of the

charterer by demise; and in the case

of an aircraft registered pursuant to

the exemptions relating to legal or

beneficial ownership held by an

unqualified person who is resident

in Bermuda, an indication that it is

so registered; and

(f) relevant dates such as of registration,

change of ownership, cancellation of

registration.

On registration, the Director of Civil

Aviation will furnish to the person in

recorded in it are the only details which

are publicly available. All other records

related to the owner, aircraft, etc are

treated as confidential.

The Aircraft Register will include the

following particulars:

(a) the registration certificate number;

(b) the aircraft’s nationality mark and

the registration mark assigned to it;

(c) the name of the manufacturer of the

aircraft and its designation;

(d) the aircraft serial number;

(e) the name and address and

nationality of the registered owner

of the aircraft;

(f) whether the aircraft is owned or

chartered; and

(g) relevant dates such as of registration, change of ownership, cancellation of

registration.

On registration, the DGCA will furnish

to the registered owner of the aircraft a

Certificate of Registration. This will

include the particulars detailed above.

Page 11 of 19

BERMUDA CAYMAN

whose name that aircraft is registered a

Certificate of Registration. This will

include the particulars detailed above.

Radio

Licensing

The Class Six Radio Licence is issued by

the Bermuda Government Department

of Telecommunications. This will be

issued upon receipt of a copy of the

aircraft’s Certificate of Registration from

the BDCA.

This licence is issued by the Cayman

Islands Government, Information and

Communications Technology Authority

(ICTA).

Is there a

register of

aircraft

leases?

No register of aircraft leases is

maintained in Bermuda. Neither the

BDCA nor Bermuda law require that

leases take any particular form and it is

not required that leases relating to

aircraft registered in Bermuda be

governed by Bermuda law. There is no

concept of “perfection” of the status of a

lease under Bermuda law.

No register of aircraft leases is

maintained in the Cayman Islands. An

aircraft lease can be noted on the

relevant Aircraft Register.

2. COSTS OF AIRCRAFT REGISTRATION

Certificate of

Airworthiness

Annual fees for the issue of the

Certificate of Airworthiness are

calculated as follows, where the

maximum total weight:

(a) does not exceed 5700 kg US$5000

(b) for aircraft exceeding 5,700 kgs but not exceeding 30,000kg US$5000

plus US$175 per 500 kgs or part

thereof exceeding 5,700 kgs up to a

maximum of US$13,500

(c) for aircraft exceeding 30,000 kgs but

The applicants for initial certificates of

airworthiness are required to pay:

(a) for the investigation required by the CAACI in the case of any aircraft in

respect of each 500 kg., or part

thereof, of the maximum weight, a

charge of US$244; and

(b) for the issue of the certificate in any case in respect of complete year of

validity applied for in respect of the

certificate, a charge of US$366.

Page 12 of 19

BERMUDA CAYMAN

not exceeding 100,000 kgs US$13,500

plus US$145 per 500 kgs or part

thereof exceeding 30,000 kgs up to a

maximum of US$33,000

(d) for aircraft exceeding 100,000 kgs but not exceeding 200,000 kgs US$33,000

plus US$135 per 500 kgs or part

thereof exceeding 100,000 kgs up to a

maximum of US$60,000

(e) for aircraft exceeding 200,000 kgs but not exceeding 300,000 kgs US$60,000

plus US$130 per 500 kgs or part

thereof exceeding 200,000 kgs up to a

maximum of US$86,000

for aircraft exceeding 300,000 kgs

US$86,000 plus US$125 per 500 kgs or

part thereof exceeding 300,000 kgs

The applicants for renewal of certificates

of airworthiness are required to pay in

respect of each complete year of validity

applied for the cost of any investigation

required by the CAACI plus in respect of

the certificate where the maximum total

weight:

(a) does not exceed 2,730 kg US$1,220;

(b) for aircraft exceeding 2,730 kg but not exceeding 5,700 kg US$2,440;

(c) for aircraft exceeding 5,700 kg but not exceeding 34,000 kg US$2,440

plus US$183 per 500 kg or part

thereof exceeding 5,700 kg up to a

maximum of US$12,196;

(d) for aircraft exceeding 34,000 kg but not exceeding 68,000 kg US$12,196

plus US$171 per 500 kg or part

thereof exceeding 34,000 kg up to a

maximum of US$23,171;

(e) for aircraft exceeding 68,000 kg but not exceeding 91,000 kg US$23,171

plus US$159 per 500 kgs or part

thereof exceeding 68,000 kg up to a

maximum of US$29,269;

(f) for aircraft exceeding 91,000 kg but

not exceeding 182,000 kg US$29,269

plus US$153 per 500 kgs or part

thereof exceeding 91,000 kg up to a

maximum of US$56,098;

(g) for aircraft exceeding 182,000 kg but

Page 13 of 19

BERMUDA CAYMAN

not exceeding 273,000 kg US$56,098

plus US$147 per 500 kgs or part

thereof exceeding 182,000 kg up to a

maximum of US$80,488; and

for aircraft exceeding 273,000 kg

US$80,488 plus US$141 per 500 kg or

part thereof exceeding 273,000 kg.

Certificate of

Registration

None The fee payable for Registration of an

aircraft and issue of the relevant

certificate is US$610.

Certificate of

Approval for

Radio

Installation

Initial Issue: None

Renewal or amendment: None

The applicant shall pay for the

investigations required by the CAACI

for the approval or any subsequent

modification a charge of an amount

equal to the actual cost of making the

investigation plus a charge of US$366.

Aircraft Radio

Licence Fee

Initial Application: US$310.00

Renewal: US$260.00

Upon making an application for the

grant or renewal of a licence payable to

ICTA of the Cayman Islands:

Initial Application: US$120.

Renewal: US$120.

Licences for

Flight Crew –

Private Pilot’s

Licence

Initial Issue: US$120

Renewal: US$75

Upon making an application for the

grant or renewal of a licence to act as a

flight crew member, the applicant shall

pay:

(a) for a Certificate of Validation of a foreign licence –

(i) in relation to a specific aircraft

Page 14 of 19

BERMUDA CAYMAN

registration, a fee of US$305; and

(ii) where no specific aircraft

registration is stipulated, a fee of

US$1,220; and

(b) for a General Certificate of

Validation of a foreign licence

associated with a commercial air

transport operation or an aircraft

manufacturer, a fee of US$2,440 per

group of twenty licences or less.

Commercial

Pilot’s Licence

Initial Issue: US$240

Renewal: US$120

Not applicable.

Airline

Transport

Pilot’s Licence

Initial Issue: US$240

Renewal: US$120

Not applicable.

3. REGISTRATION OF SECURITY INTERESTS OVER AIRCRAFT

Aircraft

Mortgages

The BDCA maintains a Register of

Aircraft Mortgages and a Register of

Aircraft Engine Mortgages. The

Mortgaging of Aircraft and Aircraft

Engines Act 1999 and related regulations

have been in place since 1 July 1999.

Under this legislation, a Register of

Aircraft Mortgages and a Register of

Aircraft Engine Mortgages is maintained

to assist in the registration of security

interests in both aircraft and aircraft

engines (with certain minimum thrust or

horsepower levels) and owned by or

otherwise in the lawful possession of a

Cayman Islands law contain regulations

for the mortgaging of aircraft, which in

part state ʺan aircraft registered in the

Cayman Islands register or such an

aircraft together with any store of spare

parts for that aircraft may be made

security for a loan or other valuable

considerationʺ. Applications to enter a

mortgage in the Register may be made to

the CAACI by or on behalf of the

mortgagee using the prescribed forms

and must be accompanied by a certified

true copy of the mortgage and the

Page 15 of 19

BERMUDA CAYMAN

company incorporated in Bermuda.

Fees relating to the filing of mortgages

are presently set on a sliding scale up to

a maximum of US$800.

Note that a mortgage to be registered in

Bermuda is not required to be governed

by Bermuda law.

appropriate fee:

(i) where the sum secured by the

mortgage does not exceed

US$6,097,561, a charge of

US$1,525;

(ii) where the sum secured by the

mortgage does not exceed

US$12,195,122, a charge of

US$3,049;

(iii) where the sum secured by the

mortgage does not exceed

US$24,390,244, a charge of

US$4,574; and

(iv) where the sum secured by the

mortgage exceeds

US$24,390,244, a charge of

US$6,098.

Note that a mortgage to be registered in

the Cayman Islands is not required to be

governed by Cayman Islands law.

Priority

Notices

The priority of a mortgage can be fixed

by acceptance of a priority notice by the

BDCA pursuant to which the priority of

a yet to be executed mortgage can be

fixed for a 14 day renewable period. A

filing fee of US$80 is applicable to such a

notice.

A notice of intention to make an

application to enter a contemplated

mortgage of an aircraft in the Register,

otherwise known as a ʺpriority noticeʺ

may also be entered in the Register and

will hold a validity period of 14 days.

The fee applicable for filing a priority

notice is US$305.

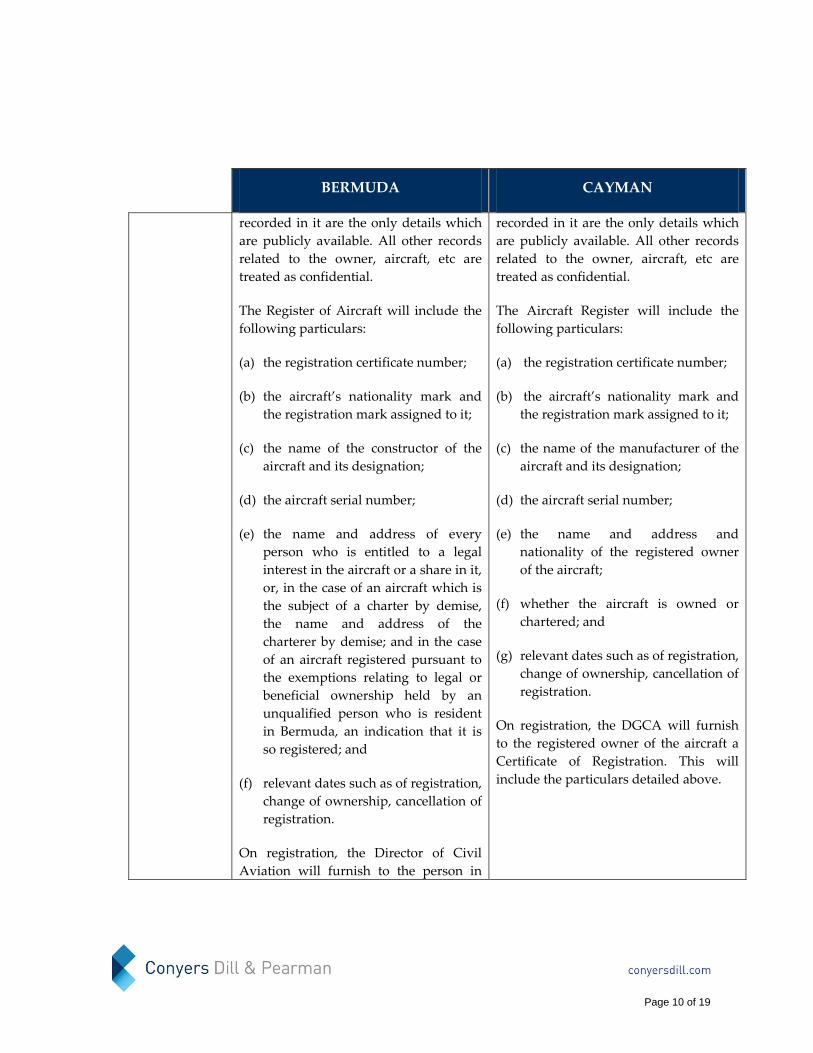

Other security Any aircraft registered in Bermuda or

any interest therein registerable under

Any aircraft registered in the Cayman

Islands which is subject to any interest

Page 16 of 19

BERMUDA CAYMAN

interests the Mortgage Act must be registered

thereunder. If security is taken over the

shares of the Bermuda company

incorporated for purposes of owning or

leasing the aircraft, such share charge

may be registered under the Companies

Act 1981 of Bermuda with the Registrar

of Companies for priority purposes. A

fee of US$557 applies to any such filing.

therein registerable under the

Mortgaging of Aircraft Regulations

(1979) must be registered thereunder. If

security is taken over the shares of a

Cayman Islands company incorporated

for purposes of owning or leasing the

aircraft, such share mortgage or charge is

not required to be registered with any

public authority of the Cayman Islands.

A Cayman Islands company granting a

mortgage or charge of its assets must

record the same in its Register of

Mortgages and Charges maintained at its

Registered Office.

4. COMPANY FEES

Incorporation

fee

Approximately US$6,000 (automatically

includes a tax exemption undertaking to

2036)

Approximately US$3,540 (plus US$1,830

if a tax exemption undertaking is

required).

Annual

service fee

US$6,930 (for a sole shareholder

company)

US$2,780 to provide registered office

services.

Annual

Government

Fee

US$1,995 (for a company with a share

capital of US$12,000 or less)

These fees range from US$732 for

companies with up to US$50,000 in

authorized capital to US$3,010 for

companies with over $2 million in

capitalization.

Can a special

purpose

vehicle be

used to

register

Yes. Bermuda plays an important role in

the creation of asset holding entities and,

increasingly, the use of exempted

company special purpose vehicles

coupled with a purpose trust in export

credit financings. The enactment of the

Yes. Cayman exempted companies are

commonly incorporated as special

purpose vehicles (“SPVs”) to play a

particular role within a financing or

leasing transaction. The rationale for

introducing the SPV into the structure

Page 17 of 19

BERMUDA CAYMAN

aircraft? Trusts (Special Provisions) Act 1989 in

Bermuda enabled the creation of trusts

for a broad range of non‐charitable

purposes (“purpose trusts”), and since

that time the practice of establishing

purpose trusts has become increasingly

common in Bermuda. This structure

avoids potential conflicts that can arise

when a charitable trust structure is used

and where one of the objects of the trust

is to maximise returns for certain named

charitable beneficiaries and to make

appropriate distributions.

will depend upon financing and leasing

regulations in the jurisdictions of the

participant airlines, lessors or sub‐lessors

and therefore the SPV’s role in each

structure will be tailored to fit the

particular transaction.

The SPV is usually structured as an

orphan company with the shares held in

trust for either a charitable purpose, or

for the benefit of the transaction itself (an

innovation of the Special Trusts

(Alternative Regime) Law, 1997 (“STAR

trust”).

5. TAXATION

Taxation ‐

general

There is presently no Bermuda income

or profits tax, withholding tax, capital

gains tax, capital transfer tax, estate duty

or inheritance tax payable by a Bermuda

company or its shareholders, other than

shareholders ordinarily resident in

Bermuda.

A Bermuda exempted company may

apply for and receive from the Minister

of Finance of Bermuda under the

Exempted Undertakings Tax Protection

Act 1966, an assurance that in the event

of there being enacted in Bermuda any

legislation imposing tax computed on

profits or income, or computed on any

capital assets, gain or appreciation, or

any tax in the nature of estate duty or

inheritance tax, such tax shall not be

applicable to the company or to any of

Cayman has no corporation tax, income

tax, capital gains tax, inheritance tax, gift

tax, wealth tax, or any other tax

applicable to a company conducting off‐

shore business. All exempted companies

are entitled to receive from the

government a “Tax Exemption

Undertaking” exempting them from any

possible future Cayman taxes enacted to

be levied on profits, income, gains or

appreciations, or tax in the nature of

estate duty or inheritance tax applicable

to the company or its operations or to

shares, debentures or other obligations

of the company for a period of twenty

years. Ordinary non‐resident companies

are not entitled to receive the Tax

Exemption Undertaking.

Page 18 of 19

BERMUDA CAYMAN

its operations or to the shares,

debentures or other obligations of the

company except insofar as such tax

applies to persons ordinarily resident in

Bermuda and holding such shares,

debentures or other obligations of the

company or any land leased or let to the

company. In accordance with the

relevant legislation, such assurances are

presently granted until the year 2036.

Stamp duty Stamp duties are not presently levied by

the Bermuda government on documents

to which an exempted Bermuda

company is party other than if the

subject property is located in Bermuda.

Stamp duty only arises in Cayman

where the relevant instrument is

executed in or physically brought into

Cayman (usually for enforcement

purposes) and is subject to a maximum

of US$600.

For further information please contact Julie McLean or Jason Piney (with respect to

Bermuda transactions) or Kevin Butler or Olivaire Watler (with respect to Cayman

Islands transactions) as set out below.

CONYERS DILL & PEARMAN LIMITED

Clarendon House

Church Street

Hamilton HM 11

Bermuda

Tel: 441 295 1422

Fax: 441 292 4720

E‐mail: [email protected]

CONYERS DILL & PEARMAN Boundary Hall, 2nd Floor, Cricket Square

PO Box 2681, Grand Cayman KY1‐1111,

Cayman Islands

Tel: +1 (345) 945 3901

Fax: +1 (345) 945 3902

E‐mail: [email protected]

Page 19 of 19

This publication is not a substitute for legal advice nor is it a legal opinion. It deals in broad

terms only and is intended merely to provide a brief overview and give general information.

About Conyers Dill & Pearman

Founded in 1928, Conyers Dill & Pearman is a world‐class legal services firm advising

on the laws of Bermuda, the British Virgin Islands, the Cayman Islands and

Mauritius. With a global network that includes 140 lawyers spanning eight offices

worldwide, Conyers provides responsive, sophisticated, solution‐driven legal advice

to clients seeking specialised expertise on corporate, company and commercial,

litigation, restructuring and insolvency, and trust and private client matters. Conyers

is affiliated with the Codan group of companies, which provide a range of trust,

corporate, secretarial, accounting and management services.

www.conyersdill.com

![The Outlook for Aircraft Leasing - General Electric Outlook for Aircraft Leasing Henry Hubschman ... Company press releases, ... Hubschman_ SG Cowen_ 8Feb_handout.ppt [Read-Only]](https://img.pdfslide.us/doc/110x75/5ac3d7427f8b9a5c558c42f6/the-outlook-for-aircraft-leasing-general-electric-outlook-for-aircraft-leasing.jpg)