Embed Size (px)

Citation preview

224

VI. Comparative Value Chain and Economic

Analysis of the Metal Sector (Crown Cork) in

Ethiopia, Zambia, China and Vietnam

225

VI.1. Crown Cork (Bottle Caps) Products Analysis: Objectives

The purpose of the crown cork products analysis is to assess the current competitiveness

of the subsector and the main opportunities for maintaining and increasing

competitiveness in the future. To do this, a typical product (steel bottle caps) was

analyzed in the following manner:

Examine important issues and trends in the world metals and metal products

market;

Review the structures of the Ethiopian, Zambian, Chinese and Vietnamese metal

goods markets;

Assess the key features, strengths and weaknesses of the existing supply chains

for metal products in Ethiopia, Zambia, China and Vietnam;

Assess the overall economic efficiency of domestic crown cork production in

relation to world prices (as reflected by production prices in China and Vietnam)

using alternative cost projection scenarios to establish current and medium term

competitiveness;

Taking the economic efficiency result as a starting point, analyze the metal

products (crown cork) value chain to identify key strengths, weaknesses and

opportunities or needs for investment, expansion or contraction to maintain and

increase crown cork productivity and competitiveness at the business strategy and

business process levels; and

Provide possible policy options and recommendations to help stimulate growth

and improve competitiveness in the sector.

VI.2. Product Selection Method

Following a review of the first product screening in which 40 products were selected for

consideration for the value chain analysis and feasibility study, the World Bank (WB)

and Global Development Solutions (GDS)/HQ teams immediately agreed on seven out of

the ten products needed for the analysis. The seven products selected by the teams were

as follows:

1. Apparel:

a. Polo shirt; and

b. Underwear

2. Agribusiness:

a. Milk; and

b. Wheat milling

3. Leather:

a. High-end sheepskin loafers

4. Wood:

226

a. Windows/French windows and frames

5. Metal:

a. Padlocks.

To finalize the selection of the remaining products from the wood, metal and leather

sectors, based on the Africa Competitiveness: Phase 1.1 - Preliminary Product Screening

in Ethiopia report (July 2010), the WB and GDS/HQ teams chose six products as

potential candidates to be included in the list of the final ten products to be the target

products for the value chain analysis and feasibility study. The six products included the

following:

1. Wood products:

a. Wooden doors; and

b. Wooden chairs (not upholstered).

2. Leather products:

a. Leather golf gloves; and

b. Sports footwear of leather.

3. Metal products:

a. Metal doors, window-frame (security window frame); and

b. Aluminum doors and windows.

In order to screen the final six products, a product screening survey was developed which

revolved around six factors:

1. Whether these products are currently produced by companies with less than

50 employees;

2. If companies identified in #1 above can be set up with less than US$100,000

in investment capital;

3. The minimum level of skills and know-how required to produce the products;

4. Whether the products produced by the companies in #1 are being exported;

5. Whether products produced by companies in #1 are consolidated by brokers

or other intermediaries for exports; and

6. Whether companies identified in #1 can readily access raw material inputs in

the market to produce the products.

These questions were posed to the wood, metal and leather sector associations in both

China and Vietnam. Following interviews with sector associations, additional interviews

were conducted at the firm level to identify specifically the level of investments and

minimum level of technical skills required for an entrepreneur or existing SMEs to set up

a production operation. These questions were posed to existing operators in China and

Vietnam to identify whether:

227

Barriers to market entry, particularly from a financial and skills

requirement, were sufficiently low to allow entrepreneurs and SMEs in

Ethiopia to easily establish operations; and

These products are currently being produced by SMEs in China and

Vietnam, and are effectively being sold in local and export markets.

The product screening survey identified the following products as viable candidates to be

targeted for the value chain and feasibility analysis.

1. Wood product:

a. Wooden chairs (soft wood); and

b. Wooden door (semi-solid).

Although French windows and their frames made of wood had originally been

preselected for analysis, a decision was made to opt to analyze both wooden

chairs and wooden doors. This decision stemmed from the fact that French

windows require glass thus introducing an outside factor that could influence

the manufacturing of the final product. Wooden doors (without glass) and

wooden chairs (without upholstery) are more representative of wood

processing exclusively.

2. Leather products: Leather golf gloves or sports glove of comparable structure

and weight.

3. Metal products: Both the pre-selected products (security window frame; and

aluminum doors and windows) were screened out of the selection due to

various factors including high initial investment requirements. As a result,

further analyses of products identified during the preliminary product

screening were conducted. Interviews with metal sector associations and

enterprises currently operating in China and Vietnam, as well as interviews

with existing operators in the fabricated metal products sector in Ethiopia

identified crown corks (bottle caps) as a viable candidate to be targeted for

value chain analysis. Crown corks currently are produced in four of the five

countries (not in Tanzania), but Ethiopia continues to import substantial

volumes of this product, including imports from China. As a result, crown

corks have been chosen as the final fabricated metal product to be the focus of

a value chain analysis in the target countries.

228

VI.2.1. Respective Government Definitions of Small, Medium and

Large Enterprises in Ethiopia, Tanzania, Zambia, China and

Vietnam

Ethiopia: For Ethiopia, the classification of enterprises into small, medium and large

scale depends on a number of variables such as level of employment, turnover, capital

investment, production capacity, level of technology and subsector. Accordingly, the

following scales are referred to the classification of enterprises in the Ethiopian context

(Table 117).

Table 117: Company Size Classification Structure for Ethiopia

Small Scale Medium Scale Large Scale

Textile and Apparel 5-9 10 – 49 above 50

According to the Central

Statistics Agency (CSA)

Leather 2-10 21 – 50 above 51

Diary 2-10 21 – 50 above 51

Wheat 2-10 21 – 50 above 51

Wood Processing 2-10 21 – 50 above 51

Metal 2-10 21 – 50 above 51

According to Federal

Medium and Small

Enterprise Development

Agency (FeMSEDA)

Sub-sector Remark

Number of Employees

Source: Ethiopia CSA and FeMSEDA

Tanzania: For Tanzania, the classification of enterprises into small, medium and large

scale depends on a number of variables such as level of employment and capital

investment in machinery. The classification cuts across sectors and subsectors of the

economy. Accordingly, the following scales refer to the classification of enterprises in

the Tanzanian context (Table 118). Note that the small enterprise type is most

appropriate for all sectors studied in this analysis.

Table 118: Company Size Classification Structure for Tanzania

Category Employees

Capital Investment in Machinery

(TZS million) Remarks

Micro enterprise 1 - 4 Up to 5 Majority in the informal sector

Small enterprise 5 - 49 5 - 200 Most in the informal sector

Medium enterprise 50 - 99 200 - 800 Most in the formal sector

Large enterprise 100+ 800+ All in the formal sector Source: Tanzania Chamber of Commerce, Industry and Agriculture (TCCIA)

Zambia: Zambia classifies enterprises as micro, small, medium and large based on

several factors including number of employees, annual revenue and capital investment.

The capital investment category is further delineated by whether the firm is engaged in

manufacturing or if it is a trading/services firm. For microenterprises, the minimum

revenue and investment requirements are kept intentionally low in order to encourage

registration, although few microenterprises actually register.

229

Table 119: Company Size Classification Structure for Zambia

Classification Employees

Annual Revenue

(ZMK million)

Capital Investment for Manufacturing

Firms (ZMK million)

Capital Investment for Trading/ Services

Firms (ZMK million)

Micro < 10 < 20 < 10 < 10

Small 10 - 50 150 - 250 80 – 200 150

Medium 51-100 300 - 800 200 – 500 151 - 300

Large > 100 > 800 > 500 > 300

Source: Zambia Development Agency

China: The China government is challenged in defining sizes of firms. Temporary

definitions have been used for the past several years, and the government promised to

revise the standard in 2010. The definition from the National Bureau of Statistics of

China is complex. The definition was published in 2002 jointly by the Ministry of

Finance, National Bureau of Statistics of China, State Economic and Trade Commission

(no longer exists), and China Planning Commission, which has since split and exists as

the State Development and Planning Commission (SDPC) and the National Development

and Reform Commission (NDRC). A simplified presentation of the company size

classification is shown in Table 120. Note that the Industrial type is most appropriate for

all sectors studied in this analysis.

Table 120: Company Size Classification Structure for China

Type Index Unit Small Medium Large

Employee person Less than 300 300-2000 More than 2000

Revenue million RMB Less than 30 30-300 More than 300

Asset million RMB Less than 40 40-400 More than 400

Employee person Less than 600 600-3000 More than 3000

Revenue million RMB Less than 30 30-300 More than 300

Asset million RMB Less than 40 40-400 More than 400

Employee person Less than 100 100-200 More than 200

Revenue million RMB Less than 30 30-300 More than 300

Employee person Less than 100 100-500 More than 500

Revenue million RMB Less than 10 10-150 More than 150

Employee person Less than 500 500-3000 More than 3000

Revenue million RMB Less than 30 30-300 More than 300

Employee person Less than 400 400-1000 More than 1000

Revenue million RMB Less than 30 30-300 More than 300

Employee person Less than 400 400-800 More than 800

Revenue million RMB Less than 30 30-150 More than 150

Lodging and

Catering services

Industrial

Construction

Wholesale

Retail

Transportation

Post services

Source: National Bureau of Statistics of China

Vietnam: A small firm has less than 50 laborers, while a medium-size firm has 51-200

laborers. Within the small and medium-size classifications, there are some detailed

categories depending on the purpose of research and management. For instance, a firm

230

with less than 10 laborers is called a super small-size firm. Such a regulation is in line

with Social Insurance Law.104

VI.2.2. Product Technical Specifications

Following the identification of products to be targeted for the value chain and feasibility

analysis, a detailed technical profile of each product with an accompanying diagram or

photograph was complied and sent to the field teams to help ensure that product data

collection in the field focused on products with similar - if not identical - technical

specifications.

Table 121 below provides the product technical specifications for all ten products for

which product data are being collected.

Table 121: Product Technical Specifications

Material

Product WeightUnit of

measureUnit of measure

1 Golf gloves 85 - 141 grams Men's medium Sheepskin

Loafer 780 grams Heel Width Insole

Size US = 8 EU = 7 2.5 10 30

3 Padlock* 760 grams 7 7 NA* cm Brass

Thickness Diameter Height

0.24 31.9 6.6

Width Depth Height

45 45 75

Width Depth Height

80 4 210

Protein Lactose Ash Vitamins Fat content

3.5% 4.7% 0.8% B1, B2, C and D Full

Type (German) Type (French) Ash Protein Moisture

550 55 <0.65%approx.

11%<14.5%

9 Polo shirt 250 - 270 grams 100% cotton

10 Underwear 80 - 100 grams80% cotton/

20% spandex

* Overall height is 14 cm with a 2 cm shackle diameter

** The weight of the cover (plastic sole made from PVC) in the internal surface of the cap is 290 mg

Source: Global Development Solutions, LLC

Pine

Wheat or rice

Dimension

All purpose flour

cm

Refer to diagram

Weight

cm

mm

cm

tin free steel

(tfs)

Sheepskin

Pine

mg

kg

kg

liters

Refer to picture

Crown cork

(metal bottle

cap)**

Wooden chair

Wooden door

Milk

Milling

290

6.5

12

0.5

2

4

5

6

7

8

104

Information garnered from

http://laws.dongnai.gov.vn/1991_to_2000/2000/200004/200004280005_en/lawdocum

231

VI.3. Global Metal Products Market

The production of iron and steel ore and products based on these metals are the most

important items in the global metal products trade. As per the classification of the

International Trade Statistics of the International Trade Center, the most significant

products in this market segment are shown in Table 122 below.

Table 122: Iron and Steel Products and Articles of Iron or Steel

Iron and Steel Products Articles of Iron or Steel

1. Pig iron and spiegeleisen in pigs

2. Ferro-alloys

3. Ferrous products obtained by direct reduction

of iron ore (min. pure iron of 99.9 percent)

4. Ferrous waste and scrap; remelting scrap

ingots or iron or steel

5. Granules and powders of pig iron, spiegeleisen,

iron or steel

6. Iron and non-alloy steel in ingots or other

primary forms

7. Semi-finished products of iron/non-alloy steel

8. Flat-rolled products of iron/non-alloy steel

9. Bars and rods

10. Angles, shapes and sections of iron or non-

alloy steel

11. Wire of iron or non-alloy steel

12. Stainless steel in ingots/other primary forms

13. Flat-rolled products of stainless steel

14. Bars and rods, hot rolled in irregular wound

coils of stainless steel

15. Bars and rods of stainless steel, angles and

shapes

16. Wire of stainless steel

17. Alloy steel in ingots/other primary form

18. Flat-rolled products of other alloy

19. Bars and rods other alloy steel hollow drill bars

20. Wire of other alloy steel

1. Sheet piling, etc., of iron/steel

2. Rail, crossing pieces iron/steel

3. Tubes, pipes and hollow profiles of cast iron

4. Structures (roads, angles, plates)

5. Iron and steel reservoirs, tanks, vats (cap>300 l)

6. Iron or steel tanks, casks, drums, cans and boxes

7. Containers for compressed or liquefied gas

8. Iron or steel stranded wire, ropes, cables, etc.,

not electrically insulated

9. Iron and steel wire barbed twisted hoop, etc.

10. Cloth grill, netting and fencing of iron and steel

wire

11. Chain and parts thereof of iron or steel

12. Anchors, grapnels and parts thereof

13. Nails, staples and sim art, iron or steel

14. Iron or steel screws, bolts, nuts, coach-screws

15. Iron and steel sewing, knitting needles and sim

arts for hand use

16. Spring and leaves for springs

17. Iron or steel stoves, ranges, barbecues and semi

non-electrical apparatuses

18. Iron and steel radiators, air heaters and hot air

distributers

19. Iron or steel tables and household articles

20. Sanitary ware and parts thereof

21. Cast articles of iron or steel

22. Articles of iron or steel

Source: International Trade Center

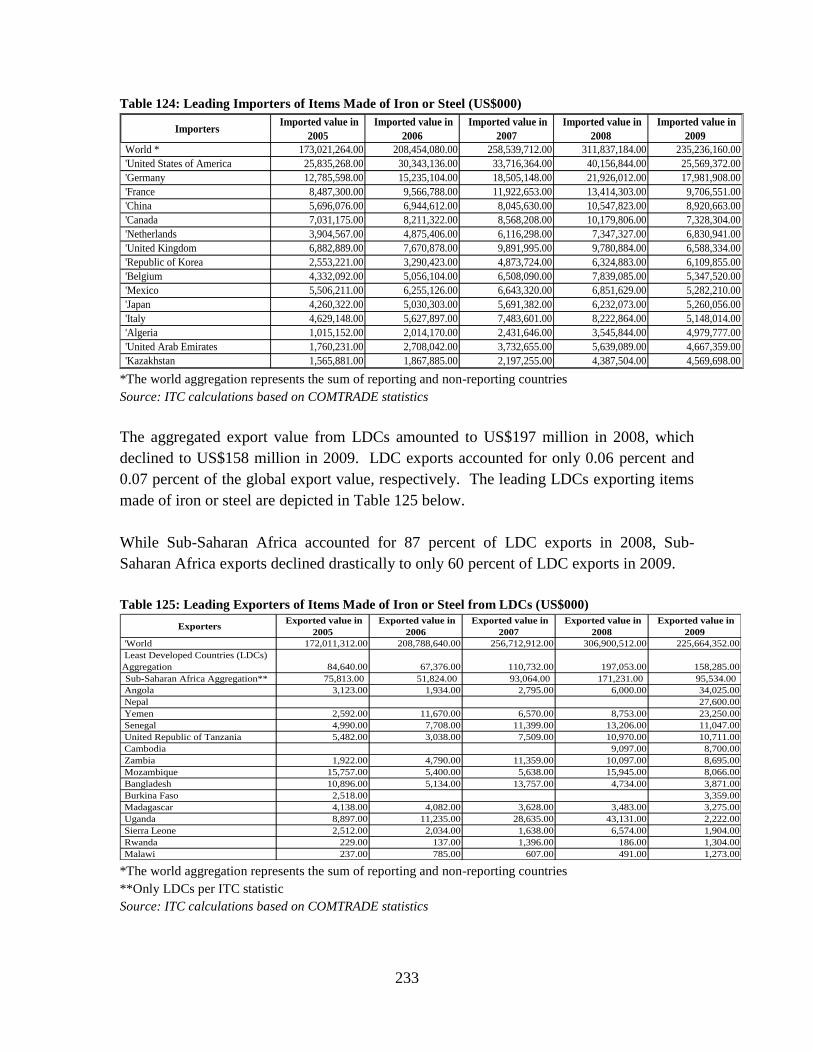

Market Trends: Global iron and steel exports attained the highest export value of

US$529 billion in 2008. Germany was the largest exporter, accounting for 7.6 percent of

the global export in 2008. Global exports experienced a sharp decline (by 47.6 percent)

in 2009 against 2008 due to the economic crisis and registered a substantially lower

export value of US$273 billion. Following Germany, major iron and steel exporters are

Japan, Republic of Korea, USA, Russian Federation, Belgium, China, France,

Netherlands and Ukraine.

232

With regard to import of iron and steel products, the global import value registered in

2008 was the highest, amounting to US$546 billion of which Germany accounted for 7.4

percent, followed by the Republic of Korea (6.5 percent). The leading importers in 2009

were China, Germany, Republic of Korea, Italy, USA, France, Turkey, Belgium,

Netherlands and India.

The aggregated export and import by LDCs in iron and steel accounted for only 0.12

percent and 1.13 percent of the global figures, respectively.

With respect to items made of iron or steel, the global export value in 2008 was US$307

billion, which suffered a 26.5 percent decline the following year to US$226 billion.

China was the leading exporter of items made of iron or steel and accounted for 15.8

percent of global exports in 2008 and 15 percent in 2009. The export values of the major

15 exporting countries are depicted in Table 123 below.

Table 123: Leading Exporters of Items Made of Iron or Steel (US$000)

Exporters Exported value in

2005

Exported value in

2006

Exported value in

2007

Exported value in

2008

Exported value in

2009

World * 172,011,312.00 208,788,640.00 256,712,912.00 306,900,512.00 225,664,352.00

'China 19,032,492.00 26,784,042.00 36,739,592.00 48,419,120.00 33,781,144.00

'Germany 21,490,444.00 26,056,732.00 31,238,204.00 35,632,184.00 28,304,016.00

'Italy 14,381,019.00 17,619,888.00 22,490,508.00 25,388,438.00 17,642,628.00

'United States of America 11,284,488.00 13,490,562.00 14,872,820.00 17,720,372.00 13,797,469.00

'Japan 9,411,485.00 11,033,798.00 12,097,593.00 13,727,355.00 10,524,204.00

'France 8,236,698.00 9,349,253.00 11,882,738.00 13,165,533.00 9,519,684.00

'Republic of Korea 4,425,868.00 5,875,965.00 7,017,940.00 9,062,526.00 8,022,113.00

'Netherlands 3,930,404.00 4,722,160.00 6,197,963.00 7,023,034.00 6,480,614.00

'United Kingdom 5,302,817.00 5,933,115.00 7,254,103.00 7,274,785.00 5,709,821.00

'Belgium 4,339,551.00 5,092,192.00 6,258,115.00 7,260,830.00 5,391,108.00

'Spain 4,406,745.00 4,856,903.00 6,444,109.00 7,759,928.00 5,311,791.00

'Czech Republic 4,056,744.00 4,635,045.00 5,982,851.00 7,365,110.00 4,882,103.00

'Austria 3,916,570.00 4,718,309.00 5,913,590.00 6,918,761.00 4,682,389.00

'Turkey 2,731,357.00 3,336,371.00 4,129,749.00 5,742,371.00 4,550,970.00 *The world aggregation represents the sum of reporting and non-reporting countries

Source: ITC calculations based on COMTRADE statistics

The global import value in items made of iron or steel in 2008 was US$312 billion,

which declined by 24.6 percent to US$235 billion in 2009. The USA is the major

importer, accounting for 12.9 percent and 10.9 percent in 2008 and 2009, respectively.

The import value of the top 15 countries is indicated in Table 124 below.

233

Table 124: Leading Importers of Items Made of Iron or Steel (US$000)

Importers Imported value in

2005

Imported value in

2006

Imported value in

2007

Imported value in

2008

Imported value in

2009

World * 173,021,264.00 208,454,080.00 258,539,712.00 311,837,184.00 235,236,160.00

'United States of America 25,835,268.00 30,343,136.00 33,716,364.00 40,156,844.00 25,569,372.00

'Germany 12,785,598.00 15,235,104.00 18,505,148.00 21,926,012.00 17,981,908.00

'France 8,487,300.00 9,566,788.00 11,922,653.00 13,414,303.00 9,706,551.00

'China 5,696,076.00 6,944,612.00 8,045,630.00 10,547,823.00 8,920,663.00

'Canada 7,031,175.00 8,211,322.00 8,568,208.00 10,179,806.00 7,328,304.00

'Netherlands 3,904,567.00 4,875,406.00 6,116,298.00 7,347,327.00 6,830,941.00

'United Kingdom 6,882,889.00 7,670,878.00 9,891,995.00 9,780,884.00 6,588,334.00

'Republic of Korea 2,553,221.00 3,290,423.00 4,873,724.00 6,324,883.00 6,109,855.00

'Belgium 4,332,092.00 5,056,104.00 6,508,090.00 7,839,085.00 5,347,520.00

'Mexico 5,506,211.00 6,255,126.00 6,643,320.00 6,851,629.00 5,282,210.00

'Japan 4,260,322.00 5,030,303.00 5,691,382.00 6,232,073.00 5,260,056.00

'Italy 4,629,148.00 5,627,897.00 7,483,601.00 8,222,864.00 5,148,014.00

'Algeria 1,015,152.00 2,014,170.00 2,431,646.00 3,545,844.00 4,979,777.00

'United Arab Emirates 1,760,231.00 2,708,042.00 3,732,655.00 5,639,089.00 4,667,359.00

'Kazakhstan 1,565,881.00 1,867,885.00 2,197,255.00 4,387,504.00 4,569,698.00 *The world aggregation represents the sum of reporting and non-reporting countries

Source: ITC calculations based on COMTRADE statistics

The aggregated export value from LDCs amounted to US$197 million in 2008, which

declined to US$158 million in 2009. LDC exports accounted for only 0.06 percent and

0.07 percent of the global export value, respectively. The leading LDCs exporting items

made of iron or steel are depicted in Table 125 below.

While Sub-Saharan Africa accounted for 87 percent of LDC exports in 2008, Sub-

Saharan Africa exports declined drastically to only 60 percent of LDC exports in 2009.

Table 125: Leading Exporters of Items Made of Iron or Steel from LDCs (US$000)

Exporters Exported value in

2005

Exported value in

2006

Exported value in

2007

Exported value in

2008

Exported value in

2009

'World 172,011,312.00 208,788,640.00 256,712,912.00 306,900,512.00 225,664,352.00

Least Developed Countries (LDCs)

Aggregation 84,640.00 67,376.00 110,732.00 197,053.00 158,285.00

Sub-Saharan Africa Aggregation** 75,813.00 51,824.00 93,064.00 171,231.00 95,534.00

Angola 3,123.00 1,934.00 2,795.00 6,000.00 34,025.00

Nepal 27,600.00

Yemen 2,592.00 11,670.00 6,570.00 8,753.00 23,250.00

Senegal 4,990.00 7,708.00 11,399.00 13,206.00 11,047.00

United Republic of Tanzania 5,482.00 3,038.00 7,509.00 10,970.00 10,711.00

Cambodia 9,097.00 8,700.00

Zambia 1,922.00 4,790.00 11,359.00 10,097.00 8,695.00

Mozambique 15,757.00 5,400.00 5,638.00 15,945.00 8,066.00

Bangladesh 10,896.00 5,134.00 13,757.00 4,734.00 3,871.00

Burkina Faso 2,518.00 3,359.00

Madagascar 4,138.00 4,082.00 3,628.00 3,483.00 3,275.00

Uganda 8,897.00 11,235.00 28,635.00 43,131.00 2,222.00

Sierra Leone 2,512.00 2,034.00 1,638.00 6,574.00 1,904.00

Rwanda 229.00 137.00 1,396.00 186.00 1,304.00

Malawi 237.00 785.00 607.00 491.00 1,273.00 *The world aggregation represents the sum of reporting and non-reporting countries

**Only LDCs per ITC statistic

Source: ITC calculations based on COMTRADE statistics

234

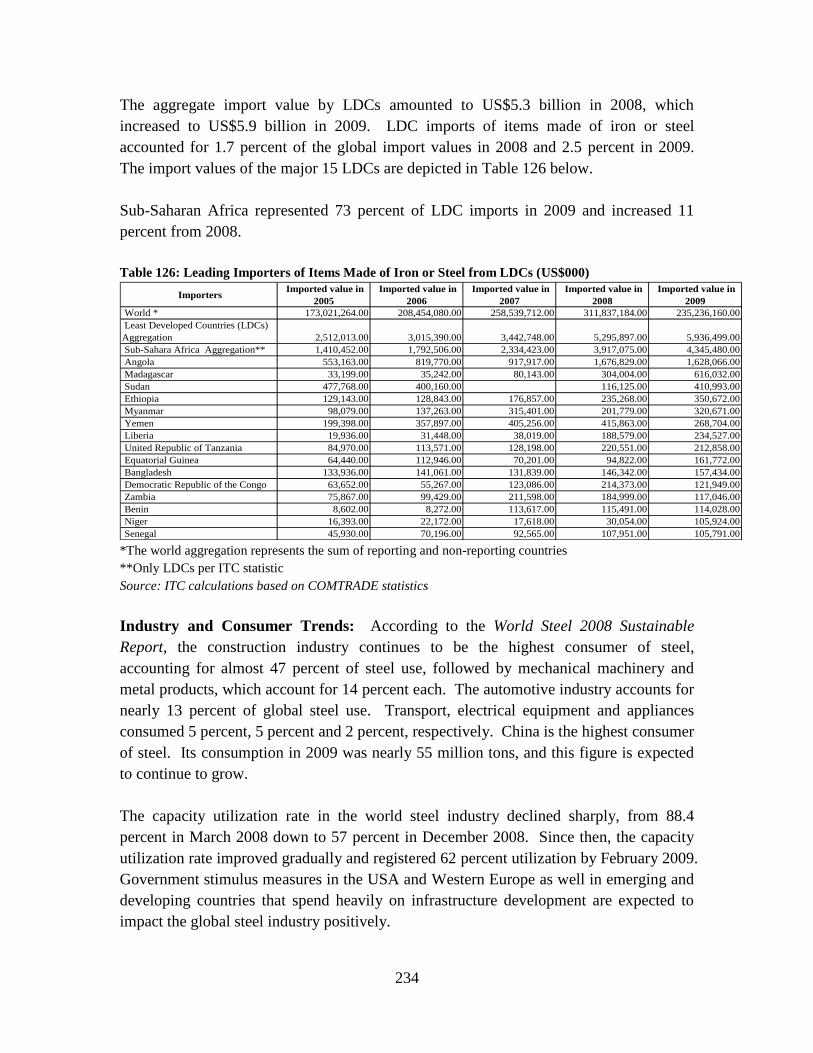

The aggregate import value by LDCs amounted to US$5.3 billion in 2008, which

increased to US$5.9 billion in 2009. LDC imports of items made of iron or steel

accounted for 1.7 percent of the global import values in 2008 and 2.5 percent in 2009.

The import values of the major 15 LDCs are depicted in Table 126 below.

Sub-Saharan Africa represented 73 percent of LDC imports in 2009 and increased 11

percent from 2008.

Table 126: Leading Importers of Items Made of Iron or Steel from LDCs (US$000)

Importers Imported value in

2005

Imported value in

2006

Imported value in

2007

Imported value in

2008

Imported value in

2009

World * 173,021,264.00 208,454,080.00 258,539,712.00 311,837,184.00 235,236,160.00

Least Developed Countries (LDCs)

Aggregation 2,512,013.00 3,015,390.00 3,442,748.00 5,295,897.00 5,936,499.00

Sub-Sahara Africa Aggregation** 1,410,452.00 1,792,506.00 2,334,423.00 3,917,075.00 4,345,480.00

Angola 553,163.00 819,770.00 917,917.00 1,676,829.00 1,628,066.00

Madagascar 33,199.00 35,242.00 80,143.00 304,004.00 616,032.00

Sudan 477,768.00 400,160.00 116,125.00 410,993.00

Ethiopia 129,143.00 128,843.00 176,857.00 235,268.00 350,672.00

Myanmar 98,079.00 137,263.00 315,401.00 201,779.00 320,671.00

Yemen 199,398.00 357,897.00 405,256.00 415,863.00 268,704.00

Liberia 19,936.00 31,448.00 38,019.00 188,579.00 234,527.00

United Republic of Tanzania 84,970.00 113,571.00 128,198.00 220,551.00 212,858.00

Equatorial Guinea 64,440.00 112,946.00 70,201.00 94,822.00 161,772.00

Bangladesh 133,936.00 141,061.00 131,839.00 146,342.00 157,434.00

Democratic Republic of the Congo 63,652.00 55,267.00 123,086.00 214,373.00 121,949.00

Zambia 75,867.00 99,429.00 211,598.00 184,999.00 117,046.00

Benin 8,602.00 8,272.00 113,617.00 115,491.00 114,028.00

Niger 16,393.00 22,172.00 17,618.00 30,054.00 105,924.00

Senegal 45,930.00 70,196.00 92,565.00 107,951.00 105,791.00 *The world aggregation represents the sum of reporting and non-reporting countries

**Only LDCs per ITC statistic

Source: ITC calculations based on COMTRADE statistics

Industry and Consumer Trends: According to the World Steel 2008 Sustainable

Report, the construction industry continues to be the highest consumer of steel,

accounting for almost 47 percent of steel use, followed by mechanical machinery and

metal products, which account for 14 percent each. The automotive industry accounts for

nearly 13 percent of global steel use. Transport, electrical equipment and appliances

consumed 5 percent, 5 percent and 2 percent, respectively. China is the highest consumer

of steel. Its consumption in 2009 was nearly 55 million tons, and this figure is expected

to continue to grow.

The capacity utilization rate in the world steel industry declined sharply, from 88.4

percent in March 2008 down to 57 percent in December 2008. Since then, the capacity

utilization rate improved gradually and registered 62 percent utilization by February 2009.

Government stimulus measures in the USA and Western Europe as well in emerging and

developing countries that spend heavily on infrastructure development are expected to

impact the global steel industry positively.

235

Supply and Demand: According to the World Steel Association (WSA), crude steel

production logged steady growth from 1950 to 1973 (growth rate of 5.8 percent) and

entered a stagnant period from 1974 to 2001 with an average growth rate of only 0.7

percent per annum. World steel production increased from 200 million tons in 1950 to

650 million tons in 1973 and gradually grew to about 800 million tons by 2001. World

crude steel production worldwide has experienced a boom since 2001, registering an

average growth rate of 8.4 percent and attained a total production of 1.33 billion tons in

2008.

Demand for steel is driven broadly by the level of socioeconomic development and the

living standards in a country. In this context, per capita consumption of steel is highest in

industrialized countries and is low in developing countries. A few examples are provided

in Table 127 below.

Table 127: Per Capita Consumption of Steel in Select Countries

Country Per Capita

Consumption in kg

Japan 574.6

USA 372.8

China 132.2

Kenya 65.0

Ethiopia 9.0

Source: Metal Industry Development Institute, Addis Ababa

VI.4. Comparative Sector Profile: Processed Metal Sector

Key Indicators: Employing nearly 3.6 million workers, and with over US$225 billion in

total production in 2009, China is the largest producer of processed metal in the world.

Of the over 24,000 companies operating in China‘s processed metal sector, half are

medium-size companies.

Vietnam, on the other hand, consumes 10.6 million metric tons annually, but over 40

percent of Vietnam‘s steel is imported. Only a fraction of the size of the Chinese market,

the metals sector in Vietnam employs slightly over 130,000 workers. Similar to China,

over 59 percent of the 3,762 firms operating in the sector in Vietnam are medium-size

firms.

In Ethiopia, fabricated metal products accounted for 4.6 percent of the country‘s

industrial production in 2009/10 and employed slightly more than 21,000 workers.

Unlike China and Vietnam, small-scale firms represent 98 percent of the 4,400 firms in

Ethiopia. In all three countries, male workers dominate the sector (73 percent to 91

percent).

236

Zambia is well known as one of the world‘s leading producers of copper. There is,

however, little value addition in terms of processed copper and, further, there is little steel

processing in the country. Reportedly only 43 companies are active in metal processing

in Zambia, with the majority (46.5 percent) being medium size (Table 128).

Table 128: Snapshot of Processed Metal Sectors in China, Vietnam and Ethiopia (2009)

Key Comparative Indicators China Vietnam Ethiopia Zambia

Total Import (US$1,000) 8,920,663 1,548,413 350,672 4,084

Total Export (US$1,000) 33,781,144 706,226 960 9,938

Companies Operating in the Sector 24,547 3,762 4,456 43

Small 20.0% 38.7% 97.0% 32.6%

Medium 50.0% 59.3% 1.6% 46.5%

Large 30.0% 2.0% 0.7% 20.9%

Est. No. of workers in the sector 3,561,638 130,436 21,054 2,360

Male 73.0% 74.0% 91.0% 85.0%

Female 27.0% 26.0% 9.0% 15.0% Source: Global Development Solutions, LLC; COMTRADE

Policy and Regulatory Environment: There is a wide array of tariffs in China covering

processed metal products, but of primary concern for this analysis are tariffs related to

iron sheets and products where the preferential rate for iron sheets is 7 percent and the

tariff rate (regular) for iron products is as high as 90 percent (preferential rate: 20

percent). In Vietnam, tariff rates (preferential) for base metals and metal parts relevant

for this analysis is approximately 27 percent. With this noted, the Common Effective

Preferential Tariff (CEPT) covers other products at an average rate of 2.3 percent.

In China, other taxes and levies relevant to the sector include a 25 percent income tax and

VAT of 17 percent (which is higher than in Vietnam where VAT is 10 percent, but VAT

reimbursements are generally immediate in China). In Vietnam, in addition to the VAT,

enterprises in the processed metal sector face a relatively high income tax (28 percent)

and export tax ranging up to 45 percent. Zambia income tax is high at 35 percent and

VAT is 16 percent. Regardless of raw material or finished goods, duties in Zambia are

25 percent. As Table 129 below indicates, enterprises in Ethiopia face a wide range of

taxes, starting with a VAT (15 percent) – for which refunds are either slow or non-

existent – and income tax ranging up to 35 percent.

237

Table 129: Comparative Policy and Regulatory Environment for the Processed Metal Sector

Iron sheets

(regular) 20%

Padlock, of base metal

(preferential) 27%

Import duties

(COMESA) 18% - 30% Iron ore 25%

Iron sheets

(preferential) 7%

Clasps and frames with

claps, incorporating locks

of base metal (preferential) 27% Customs duty 10% - 30% Iron sheets 25%

Iron product

(regular) 90%

Parts of padlocks and

Locks, of base metal

(Preferential) 27% Iron wire 25%

Iron product

(preferential) 20%

CEPT (over 40,773 fast and

normal track tariff rates)

Average

rate 2.3% Brass alloys 25%

Finished brass products 25%

Finished padlocks 25%

Finished crown cork 25%

VAT 17% VAT 10% VAT 15% VAT 16%

Income tax 25% Income tax 28% Income tax 0 - 35%, 30% Income tax 35%

Other tax 7% Other tax 0% Provident fund tax 10%

Business tax

55 ~ 155

US$ Salary tax 0 - 35%

Export tax 0% - 45% Excise tax 10% - 100%

License fee 1% - 2% Surtax 10%

Turnover tax 2%, 10%

Dividend tax 10%

Royalty tax 5%

Capital gains tax 30%:15%

Withholding tax 3%

Iron sheets 9%

Tax reduction for rural

enterprises

1/7th

reduction of

income tax

rate for 1st

five years

Iron product

5%, 9%,

13%

1 Tariffs

2Taxes and

Levies

3 Subsidies

China (import tariff) Vietnam Ethiopia Zambia

None None

Source: Global Development Solutions, LLC

Enterprises in the processed metal sector in China enjoy a subsidy of 9 percent for iron

sheets and subsidies ranging from 5 percent to 13 percent for iron products. In Zambia,

there are no specific subsidies for the sector but there is a general tax subsidy of 1 1/7th

reduction in income tax for the first five years of operation for rural enterprises. Neither

Vietnam nor Ethiopia enjoys such subsidies, although enterprises in Vietnam enjoy a

preferential rate for electricity and water.

VI.5. Sector Profile for the Processed Metal Sector in Ethiopia, China, and

Vietnam

VI.5.1. Sector Profile: Fabricated Metal Products - Ethiopia

The Ethiopian fabricated metal products sector accounted for 4.6 percent of the country‘s

industrial production in 2009/10. Key products for the year were iron sheets (1,768,355

tons), nails (17,036 tons), iron bars (16,258 tons), wires (2,847 tons), crown cork (1,563

tons), motor vehicle springs (712.2 tons), doors and window frames (42,938 m2) and

ovens/stoves (<100 tons).105

Total imports for the sector amounted to US$240.7 million

(269,101 tons) in 2009; this represented a 46 percent decrease in value and 43 percent

105

The Federal Democratic Republic of Ethiopia Central Statistical Agency, Report on Large and Medium

Scale Manufacturing and Electricity Industry Survey, December 2009, Addis Ababa.

238

less demand from 2008. Leading import partners are China, India, Turkey, Ukraine and

Kazakhstan. There are no fabricated metal exports registered from Ethiopia.

Current capacity of the 14 basic metal companies exceeds 1 million tons. A breakdown

of production by the 14 companies is shown in Table 130 below.

Table 130: Production by 14 Basic Metal Companies in Ethiopia

Item Billet

Reinforced

Bars

Hollow

Section

Corrugated

Sheet Wire Nails

Number of Producers 5 6 4 6 3 4 Source: JICA, Basic Metal and Engineering Industries Firm-Level Study

Eighty-five percent of Ethiopia‘s basic metal and engineering industry product (BMEI)

demand is met by imports. The Ministry of Finance and Economic Development‘s Plan

for Accelerated and Sustained Development to End Poverty II (PASDEP II) will likely

focus on the industry for import substitution. Targets include:

Gross production value in 2014/15 to be five times that of 2010/11;

Steel demand to grow 28 percent per annum until 2014/15: per capita steel

consumption grew from 12.1 kg in EFY 2002 to 34.72 kg in EFY 2007 (3 million

tons total); and

Within five years, demand for BMEI products by major industrial sectors is

expected to be met through local production.

The sector has attracted approximately US$30 million in foreign investment mainly from

India and Pakistan, which each established a steel factory in Ethiopia.

The sector supports 4,456 companies, of which 83.1 percent are informal. Total

employment is estimated to be 21,054 people, with 91 percent being male and 9 percent

female (Table 131).

Table 131: Employment Statistics for Ethiopia Fabricated Metals Sector

Company Size

Estimated Number

of Companies

% of Companies

by Size

Number of

Employees

Average Employees

per Company

Small 4,355 97.7% 15,301 4

Medium 70 1.6% 3,142 45

Large 31 0.7% 2,611 84

Subtotal 4,456 100.0% 21,054

Informal 3,701 83.1%

Formal 754 16.9%

State-owned enterprise 4 0.1% Source: Central Statistical Agency

239

The fabricated metals sector in Ethiopia has the following advantages:

A promising site exists in West Ethiopia, with 22 million tons of ore with high

content of pentoxide vanadium (V2O5) and titanium oxide (TiO2), which increases

value;

Long experience in manufacturing basic metal products;

Availability of manpower commensurate with prevailing technology with the

exception of a few disciplines;

The existence of engineering factories with substantial hardware;

Good experience in structure, tanks, truck body and trailer manufacturing; and

Presence of institutional infrastructure for quality, standardization and services

(QSAE).

Disadvantages are:

High investment requirement for most industries in the metal sector;

Steel industry depends heavily on raw material import; and

Shortage of supply of spare parts.

VI.5.1.1 Supply Chain and Institutional Support Structure: Metal - Ethiopia

Figure 42: Ethiopian Metal Sector Market and Institutional Support Structure Ethiopian Metal Sector Market and Institutional Support Structure

Market structure Institutional Support structure

Old/ Post consumer

metal scraps

- Ministry of Finance

Metal Scrap

Collectors/Dealers

Basic Metal Processing Mfs

Imported

metal ore

Metal Engineering Industry

FDI

LE SMEs

Local Market

- Ministry of Trade and Industry (MOTI)

- Ministry of Finance (MoF)

- Quality & Standard Authority of Ethiopia

(QSAE)

- Ministry of Justice (MOJ)

- Ministry of Capacity Building (MCB)

- Ethiopian Society of Mechanical

Engineers (ESME)

Notes: FDI – Foreign Direct Investment Enterprises; LE – Large enterprises; SMEs – Small and Medium enterprises

Second Hand

metal Products

Imported

fabricated

metal products

Imported

basic metal

products

Local Enterprises

Scrap Collectors: Most of scrap

collectors and dealers are informal

individuals and groups

Basic Metal Processing Mfs:

FDI: 2

Large: 10

Engineering Industry

Small: 4,355

Medium: 70

Large: 19

New/

Industrial

metal scrap

Scrap generators: The main venues of

scrap sourcing are insurance industries

(stocking and selling vehicles and

machines when condemned as total

loss) and service industries like

(Anbessa City Bus, Ethiopian Road

Authority).

Local Industries

LE

Source: Global Development Solutions, LLC

240

VI.5.2. Sector Profile: Fabricated Metal Products - Zambia

Zambia‘s economy has always been dependent on its metal mining industry, dominated

by copper mining, which accounts for about 10 percent of Zambia‘s Gross Domestic

Product (down from 40 percent in 1965) and 90 percent of export revenues. Zambia‘s

industrial sector has long lacked growth, and so has the contribution of the metal and

engineering sector to the national output. The decline in the output levels in Zambia is

also reflected in the reduction of contribution of the industrial sector to GDP from 18.5

percent in 1980 to 10.9 percent in 2008. The situation in the manufacturing sector

decline has been exacerbated by the liquidation of most companies in the mid-1990s,

which resulted in deindustrialization.106

The Zambian metal products subsector has continually only accounted for less than 1

percent of the GDP and only about 1.6 percent of manufacturing output.107

The country‘s

recorded trade deficit of US$108,351,244 in 2009 is on all processed metals.108

Zambia

both imports and exports metal products. According to the Zambia Development Agency,

the major exported items include copper rods, copper wire, power cables, nuts and bolts,

mill balls, aluminum wire, carbon brushes and switch gears.109

The major export

destinations are South Africa, Switzerland, Hong Kong, India, Tanzania, Congo and

Zimbabwe. Padlocks are not produced in Zambia, but the country re-exports a small

number of the imported padlocks (less than 0.5 percent) primarily to Democratic

Republic of Congo. Table 132 shows the export data for all processed metal products for

the period 2007 to 2009.

Table 132: Zambia Metal Sector Exports110

Category 2007 2008 2009

All Processed Metal Products

Volume - Units (kg) 12,854,333 1,369,768 1,726,197

Value (US$) 7,621,779 3,445,798 9,937,652

Crown Cork

Volume - Units (kg) 167,699 17 74,403

Value (US$) 482,833 1,803 175,227

Padlocks

Volume - Units (kg) 352 481 327

Value (US$) 8,734 8,955 7,941 Source: Central Statistical Office/UN COMTRADE

106

Central Statistical Office, Zambia 107

Central Statistical Office, Zambia; Ministry of Commerce Trade and Industry 108

COMSTATS 109

Zambia Development Agency 110

Although this data were reported by both the Central Statistical Office, Zambia and by UN

COMTRADE, nobody was able to provide explanation regarding the variability in values from year to

year.

241

The major sources of imports are China, South Africa, Zimbabwe, Tanzania and Hong

Kong. Table 133 shows the import data for the sector for the period 2007 to 2009.

Table 133: Zambia Metal Sector Imports

Category 2007 2008 2009

All Processed Metal Products

Volume - Units (kg) 1,966,305 2,535,351 1,638,757

Value (US$) 5,017,067 5,906,421 4,084,130

Crown Cork

Volume - Units (kg) 366 7,023 10,010

Value (US$) 440 24,342 40,511

Padlocks

Volume - Units (kg) 98,506 211,740 97,832

Value (US$) 151,927 525,571 303,114 Source: Central Statistical Office/UN COMTRADE

The sector has 43 registered companies and employs approximately 2,360 people. The

male:female ratio is estimated by industry specialists to be 85 percent:15 percent but no

official data is available.

Table 134: Employment Statistics for Zambia Fabricated Metals Sector

Est. no. of firms in the sector (2)

All Processed Metal

Products (Exludes

Ore) Padlocks Crown Cork

Ave no. of

employees

/firm

Small 14 - 0 25

Medium 20 - 0 60

Large 9 - 1 90

Subtotal 43 0 1 2,360

Informal NA 0 0

Formal NA 0 1

State-owned enterprise NA 0 0

Est. no. of workers employed by the sector

% Male 85

% Female 15 Source: Global Development Solutions, LLC; Zambia metals industry experts

Main Issues

Zambia has had a longstanding desire to capture additional economic returns through

value addition to its raw materials before exports. However, for the fabrication of metal

products, the viability of producing and selling these products on a significant scale is

constrained by a number of factors, both on the supply-side and the demand-side.

242

On the supply side, there is little competitive advantage from sourcing metal (copper)

inputs locally, since the price of copper is set by international commodity exchanges and

varies little throughout the world. For example, the only cost advantage that can be

maximized by a Zambian fabricator of copper is in the cost of shipping the cathode for a

fabricator in China. However, that savings is likely to be offset entirely by the Zambian

fabricator having to ship the same weight of (fabricated) copper to China where it will be

used to manufacture the final product. On the demand side, local and regional demand

for semi-manufactures is small due to a lack of an industrial and consumer goods

manufacturing base of any significant size. Additionally, Zambian competitiveness in

this industry on the international market outside Africa is likely to be hampered by

logistical difficulties in servicing these markets reliably.111

Being a landlocked country,

these logistical difficulties include long waiting times at border posts, poor transport

infrastructure and difficulties in accessing seaports. Additional difficulties arise due to

long distance to the major would-be importers.

111

Jobs and Prosperity: Building Zambia‘s Competitiveness (JPC)

243

VI.5.2.1 Supply Chain and Institutional Support Structure: Metal - Zambia

Figure 43: Zambian Metal Sector Market and Institutional Support Structure

Sources of scrap metal are disused mines and equipment. Other sources include waste from processing & engineering

industry.

- Ministry of Mining - Ministry of Commerce

and Industry - Chamber of Mines - Scrap Metal dealers

Association of Zambia - Zambia Development

Agency

- Ministry of Commerce and Industry

- Zambia Development Agency

- Manufacturers Association of Zambia

- Engineering Institution of Zambia

- Zambia Chamber of Commerce and Industry

- Export Board of Zambia - Development Bank of

Zambia

Institutional Support

Structure

Market

Structure Mineral Ore

Mining & Processing

Scrap Metal Dealers and Collectors

Local Enterprises

Basic Metal Processing

LE SME

Local Enterprises

Metal Engineering Industry

LE SME

Export Market

Local Market

Imported Fabricated

Metal Products

Major exports include copper rods, copper

wire, power cables, nuts & bolts, mill balls, aluminum wire, carbon brushes and

switchgear

Overall firm size for the industry: Small: 14 Medium: 20 Large 9

Imported Basic Metal

Products

Imported Metal/All

oys

Notes: i) FDI – Foreign Direct Investment; IS – Informal Sector

ii) Dash line (- - -) indicates a weak linkage, lack of organization, and area where

technical support is required to help strengthen linkages along the supply chain

Dotted arrow indicates scrap

metal from local companies that is recycled back into the supply chain

VI.5.3. Sector Profile: Fabricated Metal Products - China

China is the largest producer and exporter of metals and articles of metal in the world. In

the first six months of 2010, China produced 46 percent of the world‘s crude steel (570

million tons).112

Its output of nonferrous metals is equally strong. According to the

China Nonferrous Metals Industry Association, the output of ten types of nonferrous

metals from China exceeded 26 million tons in 2009 (up 3.99 percent year-on-year).

Refined copper output reached 4.11 million tons, primary aluminum 12.85 million tons,

lead 3.71 million tons, zinc 4.36 million tons, nickel 164,800 tons, tin 134,500 tons,

antimony 165,800 tons, magnesium 500,800 tons, and sponge titanium 61,500 tons.

In terms of exports, after a sharp increase in 2008, metals and articles of metal exports in

2009 decreased to US$115 billion. Almost 7 percent of base metal exports are in the

form of miscellaneous articles. Chinese exports of padlocks, locks, clasps with locks and

keys hover at around US$2 billion per year, making up approximately one-third of the

112

Japan Iron and Steel Federation

244

world trade in this category.113

Chinese exports of stoppers, caps and lids, including

crown corks, increased by 30 percent from 2007 to 2009; at US$130 million per year,

Chinese exports in this category constitute a little less than 40 percent of the world trade

in the category.114

Table 135: Exports of Base Metals and Their Products (Locks and Corks), China, 2007-2009

Total Exports (Value, US$ million) 2007 2008 2009

Base metals and articles of base metal, of which: 77,103$ 144,015$ 115,697$

Miscellaneous articles of base metal, of which: 8,226$ 8,782$ 7,416$

Padlocks, locks, clasps with locks, keys 1,966$ 2,124$ 1,872$

Stoppers, caps and lids, including crown corks 98$ 122$ 130$

Main countries/regions of destination Central Asia, Malaysia, Australia, Japan Source: UN Comtrade

There were nearly 25,000 firms in the metals and metal products industry in China in

2009. The sector employs 3.5 million people.115

Most firms (over 70 percent) are small

or medium-size firms with 100 to 150 employees per firm on average.

One of the world‘s richest countries in terms of resources, China is abundant in metals.

In addition, China has a good technological base and strong economic growth, suggesting

that the country is likely to remain the dominant player in the metals and metal products

113

UN Comtrade 114

UN Comtrade 115

China Statistical Yearbook Network

Tariff on Steel

Ethiopia‘s import tariffs on steel vary according to type of steel.

Tariff Rates for Imported Steel, 2010

Article Tariff rate on CIF value

wire < Ø 6 mm 20%

wire > Ø 6 mm 10%

Sheet metal 5% Source: Ethiopian Customs Agency

With regard to self-sufficiency in steel production, currently there is no basic metal industry that can

extract iron/steel from ore. So far existing engineering companies depend on imported articles of steel.

Recently, a large metals enterprise, Metal and Engineering Corporation (MaEC), has been established

and it is expected to build its capacity and capability to manufacture machinery and equipment for the

entire manufacturing sector. MaEC shall only import components that it cannot manufacture locally. It

may find it plausible to go into basic metal production in the long-run as demand for steel will increase

sharply in light of the rapid development taking place in the country.

245

industry in the near future. Some of the key challenges that are likely to be faced by the

industry relate to:

Ore access – notwithstanding their abundance, metal ores are located in

prohibitively rugged regions of the Chinese northwest. Recent exploration and

site development/modernization deals signed by Chinese metals companies with

multinational firms are illustrations of initiatives aimed at improving ore access in

China.

Energy costs – last year, metal producers in China were stripped of their access to

preferential power rates as utility companies began to address the demand and

supply imbalances with price as well as service interruption interventions. These

measures are expected to increase the price of metal raw materials along the

supply chain.

VI.5.3.1 Supply Chain and Institution Support Structure: Metal - China

Figure 44: Metal Products Market and Institutional Support Structure, China Metal Products Market and Institutional Support Structure, China

Market structure Institutional Support structure

i) FDI – Foreign Direct Investment Enterprises; LE – Large Enterprises; SME – Small and Medium Enterprises ii) Dashed line (- - -) indicates a week

linkage, lack of organization, and areas where technical support is required to help strengthen linkages along the supply chain

Mineral Ores/Mining

Metal Processing

Primary Processed

Metals/Alloys Hardware (Locks,

Corks, etc) FDI LE SME

Local Market Export Market

- Ministry of Land And Resources

- China Iron and Steel Association

o China Metallurgical Construction Association

o China Metallurgical Mining Enterprises Association o China Special Steel Enterprises Association

o China Refractory Materials Industry Association

o China Coking Industry Association

o China Ferroalloy Industry Association o China Structural Steel Association

o China Carbon Industry Association

o Chinese Form-Work Association

o China Scrap Steel Application Association o Metallurgical Planning & Research Institute

o Metallurgical Information & Standardization Research Institute

o Metallurgical Economic Development Research Center

o Metallurgical Information Research Center Metallurgical Human Resources Development Center

o Metallurgical Education Resources Development Center

o Metallurgical Science and Technology Development Center

o Metallurgical Legal Affairs Center o Metallurgical Industry Finance Service Center

o Metallurgical Construction and Quota Center

o Metallurgical Project Quality Supervision Center

o Chinese Society for Metals o Chinese Society for Rare Earth

o Chinese Society for Metallurgical Education

o Metallurgical Council of China Council for the Promotion of International

Trade

- China National Hardware Association

o Tool Hardware Branch Kitchen Apparatus and Stainless Steel

o Building Hardware Branch Lock Branch

o Daily-use Hardware Branch Zipper Branch o Cooking Utensils Branch Shower-bath Products Branch

o Hoods Branch Gas Appliance Branch

FDI LE

Source: Global Development Solutions, LLC

VI.5.4. Sector Profile: Metal – Vietnam

According to the Southeast Asian Iron and Steel Institute (SEAISI), the apparent steel

consumption of total steel products in Vietnam reached approximately 10.6 million

246

metric tons in 2009, just behind Thailand (10.7 million metric tons), and Taiwan (11.7

million metric tons). Over 40 percent of the steel consumed in the country is imported.

(According to the Vietnam Steel Association, the country imported more than 200,000

tons of finished steel products during the first half of 2010.) In addition, Vietnam

imports 94 percent of its metalworking equipment and mechanical products, with only 6

percent of demand met by local manufacturers. Similarly, as industrial production in

Vietnam grows at a pace of 19 percent per year, imports of modern technology continue

to increase at an annual rate of 30 percent.

On the production of raw material, the first cold rolling mill began operating in Vietnam

in 2005, and its rolling capacity is as little as 400,000 tons. As of 2007, there were more

than ten 100 percent privately owned or foreign-invested firms operating in the long

product rolling business. Vietnam continues to be a major importer of low and medium

grade steel products from Japan and also imports even lower grade from Russia, Ukraine

and China, which suggests that the high-grade steel market continues to be limited.

Demand for high-grade hot coil and cold rolled sheets to manufacture mechanical

products such as motorcycles continues to be high, but demand for other high-grade

products such as heavy plates used for large scale industrial production such as

shipbuilding and galvanized steel for automotive production continues to be low.

Despite a period of decline in steel prices earlier in 2010, steel consumption continued to

be slow and producers were suffering from high interest rates. Recently, the declining

price trend reversed and in response to an increase in the price of steel ingots, the

domestic steel price increased in July by VND600,000 – VND700,000 per ton to VND14

– 14.5 million (US$736 - US$762).

Thanks to an increase in price of steel ingots, following a period of decline, the domestic

steel price increased in July by VND600,000 to VND700,000 per ton to VND14 – 14.5

million (US$736 to US$762). Despite the decline in prices, steel consumption continues

to be slow and producers are suffering from high interest rates.

The fabricated metal products sector currently employs approximately 130,436 workers

across 3,762 enterprises (Table 136).

Table 136: Enterprises in the Fabricated Metal Products Sector in Vietnam (2010)

Size Categories No. of Enterprises percent of Total Size of Employees

Small 1,457 38.7 percent < 10

Medium 2,229 59.3 percent 10 – 200

Large 76 2.0 percent >300

Total 3,762 100 percent

Source: Global Development Solutions, LLC

247

Male workers dominate the labor force in the fabricated metal products sector and

represent approximately 74 percent of the workforce.

According to the Ministry of Industry and Trade, as many as 65 steel projects (7 FDI

projects and 58 domestic and joint venture projects) are currently in the pipeline with an

aggregate yearly design capacity of more than 100,000 tons spread across 30 provinces in

the country. In this context, the Ministry has asked cities and provinces to stop granting

new investment licenses to steel projects and revise existing contracts as supply continues

to outstrip demand in the country.

Last year, the industry met 54 percent of the country‘s total demand for steel ingot, and

40 percent of cold steel and 100 percent of building steel demand, but by 2015, it is

estimated that Vietnam will require 15 million tons of steel.

VI.5.4.1 Supply Chain and Institutional Support Structure: Metal - Vietnam

Figure 45: Vietnam’s Iron Ore-to-Steel Market and Institutional Support Structure Vietnam’s Iron ore -to- Steel Market and Institutional Support Structure

Iron ore, scrap steel

Imported

steel scrap

Casting Mfs.

Imported

billet & slabs

Rolling Mills

No. of exploited iron mines: 38

Reserves: 956.415 mil. tons

Long Flat

Export market Domestic market

- Ministry of Industry and Trade (MOIT)

- Vietnam National Coal and Mineral

Industries Group

- Department of Geology and Minerals

of Vietnam

- Ministry of Industry and Trade (MOIT)

- Vietnam Steel Association (VSA)

- Ministry of Planning and

Investment (MPI)

- Local governments

- National Research Institute of

Mechanical Engineering (Narime)

Billets: 11 (MS)

Slabs: 0

Long: 60 (LS: 3; MS: 20; SS: 37) /

Capacity: 6.5mil. tons

Flat: 4 (L/MS) / Capacity: 1,1mil.

tons

Imported flats

(80%)

Notes: i) LS: Large scale; MS: Medium scale; small scale

ii) Dash line (- - -) indicates a week linkage, lack of organization, and areas where technical support is required

to help strengthen linkages along the supply chain

Source: Global Development Solutions, LLC

248

VI.6. Economic Efficiency and Competitiveness in Metal Processing – Crown

Corks

VI.6.1. Ethiopia: Crown Cork

The aim of this section is to establish the basic economics of a representative metal

products activity, crown corks (bottle tops), and its competitiveness vis-à-vis imports.

The comparison with imports is justified because Ethiopia is a net importer of crown

corks, as it is with most metal products. The analysis provides a complement to the VCA

by establishing whether the domestic industry is, can become, or can remain competitive.

The VCA itself looks in more detail at the strategic and business process opportunities for

cost reduction, upgrading, expansion and investment at each production stage over the

next five years.

Only one firm produces crown corks in Ethiopia, and although the VCA survey shows it

is operating at close to full capacity, its cost of production is high, its wastage rates are

high, its labor productivity is low and it is operating with very old equipment. In the case

of crown corks, the survey reveals Vietnam to be a higher productivity, lower cost

production location than China (although the surveyed firms in Vietnam do not appear to

be exporting yet). Ethiopia is importing crown corks, and the price data collected for the

survey indicate a wide range of prices: CIF Djibouti of US$0.0043 to US$0.0110 per

piece.

The average unit economic cost of the Ethiopian producer (calculated by omitting import

tariffs and VAT and estimating an annual capital charge) is approximately $0.0058/piece,

and of this 73 percent is composed of directly imported inputs largely of steel (Table 137).

Production appears profitable, however, since the average selling price of approximately

$0.008/piece is high in comparison with domestic prices in China and Vietnam.

Table 137: Ethiopia Crown Cork: Average Unit Economic Cost

Average

Cost/Piece

Revenue 5729938.0 0.0080

Costs

Imported Inputs 3056040.0 0.0042

Domestic Inputs 0 0

Packaging 129388.8 0.0002

Labor 103316.4 0.0001

Electricity 69065.8 9.59E-05

Water/Fuel 266341.6 0.0004

Laboratory Testing 49642.0 6.89E-05

249

Professional Services 25016.4 3.47E-05

R and M 126935.5 0.0002

Admin 271655.8 0.0004

Capital Cost 97818.7 0.00014

Total Cost 4195221.0 0.0058

Average Unit Cost 0.0058

Source: Global Development Solutions, LLC

The level of Ethiopian production efficiency will depend on what CIF price is used as a

comparison against domestic productions costs. Given the high wastage rates and old

equipment, product quality is likely to be low, which implies that the lower end of the

range of CIF prices is the most appropriate price comparison. Note, however, that this

low CIF price of US$0.0043 is very close to the bottom end of the range of domestic

prices reported for Vietnam. At this CIF price, domestic production in Ethiopia is highly

economically inefficient. Total costs of foreign exchange (allowing for indirect foreign

exchange effects) are greater than the saving of foreign exchange derived if output is

valued at US$0.0043/piece. The net foreign exchange effect is thus negative, creating a

negative DRC indicating significant economic inefficiency (see Table 138 below). This

implies that imported materials are in total being converted into products of lower value

than the cost of the materials themselves (due to the high wastage and inefficient

equipment).

However, the result is very sensitive to the assumed CIF price, and the switching value

price at which the DRC ratio becomes 1.0 is approximately $0.00583 (or approximately

35 percent above the bottom of the current range of CIF prices). In other words, if a CIF

price 35 percent higher is assumed, the production of crown corks becomes competitive.

Table 138: Ethiopia Crown Cork: Economic Efficiency 2010

CIF Price 0.0043

Costs

Imported Inputs 3056040.0

Domestic Inputs

Packaging 129388.8

Labor 103316.4

Electricity Local 34532.9

Electricity: Foreign 34532.9

Fuel: Local 159805.0

Fuel: Import 106536.6

Laboratory Testing 49642.0

Professional Services 25016.4

R and M 126935.5

Admin 271655.8

250

Capital Cost: Local 36339.6

Capital Cost: Import 61479.0

Total 4195221.0

Foreign Exchange

Savings 3096000.0

Direct Use 3056040.0

Indirect Use 202548.6

Net -162588.0

Domestic Resources 936632.3

DRC -5.76

Source: Global Development Solutions, LLC

As with the previous products discussed, two ways in which the economic efficiency of

crown corks could improve are a) better productivity, and b) a realignment of real

exchange rates. Accordingly, as with other products, the assumption is to increase

(double) labor productivity, and then examine how far the Dong or RMB would need to

appreciate in order to render Ethiopian production competitive (i.e., the switching value

of the currencies).

The projections for 2015 with an exchange rate appreciation scenario are complicated

because Vietnam, not China, is the marginal product supply source, but none of the

imports required for local production come from Vietnam. Thus in the calculations for

2015, any projected real appreciation of the Dong has no impact on import costs of

Ethiopian production. Labor is a very small element in total cost (2.5 percent), and even

if labor productivity (pieces per person day) doubles in Ethiopia by 2015, which would

bring it to the average level reported for China in the VCA survey but still below the

level for Vietnam, it would have only a very marginal impact on overall efficiency.

Table 139 gives the DRC result for 2015 assuming a) a doubling of labor productivity,

and b) the real appreciation of the Dong required to make Ethiopian domestic production

competitive assuming an import price of $0.0043/piece remains constant in real terms. It

also shows the new switching value CIF price with higher labor productivity and a

constant real value of the Dong.

Table 139: Summary DRC Results for 2015 Different Scenarios Summary

Assumptions

Doubling labor

productivity, constant real

Dong

Switching value for real

appreciation of Dong

with a doubling of labor

productivity

Switching value for real

CIF price with a doubling

of labor productivity and

constant real Dong

DRC Ratio DRC = -5.44 34 percent appreciation

DRC=1.0

$0.00575/piece

DRC = 1.0

251

Level of

Competitiveness

HIGHLY

INEFFICIENT

MARGINALLY

EFFICIENT

MARGINALLY

EFFICIENT

Source: Global Development Solutions, LLC

Production will remain highly inefficient in 2015 with a doubling of labor productivity

alone. By 2015, on these assumptions a 34 percent real appreciation of the Dong would

also be required to make domestic production competitive with imports from Vietnam. A

real adjustment of this size is very unlikely to occur. At a constant real value of the Dong,

and with the assumed doubling of labor productivity, the effective import price would

need to rise to $0.00575/piece, about 33 percent higher than that currently prevailing.

Based on the above results, current production of crown corks in Ethiopia is

economically uncompetitive, with little prospect for medium term competitiveness

through higher real levels of prices from competing economies like Vietnam and China.

Complete re-equipment to increase productivity through lower material wastage and

lower production costs looks to be the main possibility of producing domestically without

the need for protection.

VI.6.2. Zambia: Crown Cork

The aim of this section is to establish the basic economics of a metal product and its

competitiveness in Zambia. We analyze metal crown corks, which are in significant local

demand as an input into the beverage industry. The VCA looks in detail at the strategic

and business process opportunities for cost reduction, upgrading, expansion and

investment at each production stage, while as in the other cases, the DRC analysis

complements the VCA by establishing whether the industry can be competitive, the

ground that it has to cover to become competitive or, alternatively, how well it can

maintain competitiveness.

The DRC cost adjustment methodology is based on a separate methodological annex –

‗The Methodology for Efficiency and Competitiveness Analysis.‘

In Zambia, crown corks are produced locally and run a positive trade balance, denoting a

product that is exportable at the margin, and where the reference price for the DRC

analysis would therefore be the FOB price. An existing production unit in Zambia has

been taken for this analysis. Average unit economic cost is calculated using firm-level

financial data from the VCA survey adjusted to economic values as follows:

Import tariffs are removed from the value of imported inputs;

VAT is removed from the value of domestic items;

252

An annual capital charge is estimated based on the application of a capital

recovery factor for 12 percent over 10 years to the replacement value of assets;

Overhead costs are allocated to crown cork on the basis of their share in total firm

revenue; and

To allow for indirect foreign exchange content, it is assumed that 80 percent of

fuel and electricity cost is for foreign exchange.116

Table 140: DRC Analysis: Crown Corks – Zambia (US$)

Output (pcs p.a.)

477,440,000

Revenue p.a.

$3,247,800.0

Cost Financial Economic Per kg

Imported

PVC compound (liner) 350000.00 301724.14 0.00063

Tin-free steel 1575997.00 1358618.10 0.00285

Printing inks/varnish/lacquers 126000.00 96183.21 0.00020

Domestic

Printing inks/varnish/lacquers 171509.90 147853.36 0.00031

Cartons 74136.65 74136.65 0.00016

Poly bags/Wrap 6326.33 6326.33 0.00001

Salary/wage for primary output 126810.97 126810.97 0.00027

Electricity 84251.97 84251.97 0.00018

Fuel 25163.77 25163.77 0.00005

Testing equipment 68.85 68.85 0.00000

Safety equipment 1.06 0.00 0.00000

Lab supplies 68.85 68.85 0.00000

Prof services 19254.66 19254.66 0.00004

R and M 42594.00 42594.00 0.00009

Admin 377952.59 377952.59 0.00079

Capital charge 135540.31 135540.31 0.00028

Total cost 2796547.73

Average unit cost 0.00586

Source: Global Development Solutions, LLC

As shown in Table 140, the average unit cost per piece is US$0.00586, which is very

similar to the average unit cost found for Ethiopia of US$0.00583. The domestic selling

price for this firm is reported as US$0.0077, which is a little below the selling price in

Ethiopia. Unlike the Ethiopian firm surveyed, the Zambian firm reports the export of

around 25 percent of its output to the Congo at an FOB price of US$0.0068. No

116

This is an assumption but given the relatively small share of fuel in total cost the results are not sensitive

to it.

253

competing imports are reported into Zambia.117

In the Ethiopian case, Vietnam was a

more competitive exporter than China, but import prices varied widely with quality and

scale of purchase.

Zambia is selling to the Congo at a price that is higher than the bottom of the CIF range

reported for Ethiopia. However, these exports indicate an ability to compete in the

regional market, probably due to transport and marketing advantages relative to China

and Vietnam. Using the FOB price as a measure of value for the product gives a DRC of

0.68, indicating it is competitive, as it can be produced at a cost well below the regional

market export price (Table 141).

Table 141: DRC Estimate: Crown Corks - Zambia (US$)

FOB price 0.0068

Import content

Fuel 0.80

Electricity 0.80

Foreign exchange output 3246592.00

Imported inputs 1756525.45

Indirect imports 87532.59

Net foreign exchange 1402533.96

Domestic resources 952489.70

DRC 0.68

Source: Global Development Solutions, LLC

Medium term Outlook - 2015

Crown cork production currently is competitive in the regional market (e.g., Congo).

Productivity is relatively high under good management, with very low wastage and

absenteeism rates. Production is, however, highly import-intensive with imported steel

nearly 50 percent of total cost, so that any significant adverse relative price shift for steel

on the world market could undermine future competitiveness. If there were a RMB/ZMK

exchange rate realignment by 2015 that saw an appreciation of the Chinese currency, this

would strengthen Zambia‘s competitive position in the medium term, although there

almost certainly would need to be re-equipment of the Zambian plant to ensure adequate

productivity levels are maintained. There is, however, no presumption that unit labor

costs (and the RER) will shift in Zambia relative to China in the medium term.

117

Indian supplies have been quoted as low as US$5.25 per 1000 caps, but no imports have been made.

This is probably because of long standing agreements between the crown cork company and the bottlers,

and partly because demand for corks is highly price inelastic (since they are such a small component of

total cost).

254

VI.7. Value Chain Analysis: Crown Cork (Bottle Caps) 118

The cost of producing crown cork (bottle caps) in Ethiopia is estimated to be about

US$6.60 per 1,000 pieces. In contrast, the same quality caps cost approximately

US$5.66 per 1,000 pieces in Zambia, US$5.28 per 1,000 pieces in China and US$5.01 in

Vietnam. In Ethiopia, crown corks were produced using imported tin-free steel at a

delivered price of US$1,414/ton. In Vietnam, locally available tin-free steel is used at a

price of approximately US$1,360/ton. In China, however, where tin-free steel is readily

available, the delivered price of tin-free steel at the factory gate is approximately

US$1,106/ton. The delivered price in Zambia is highest among the four countries at

US$1,610/ton, largely due to transport logistics.

Key Characteristics: Raw materials account for more than 85 percent of the overall

value chain for the production of bottle caps. The primary raw material (tin-free steel)

accounts for a large portion of the value chain in Ethiopia, Zambia and Vietnam (65

percent, 58 percent and 72 percent, respectively), while in China, however, given the low

price of locally available tin-free steel, it only accounts for 42 percent of the overall value

chain.

The distribution of resources across the value chain is somewhat similar for all countries.

Excluding the primary raw material, the seal making and sealing stage of the production

accounts for 14 percent to 30 percent of the value chain, of which more than 78 percent is

comprised of consumables such as PVC compound and bonding chemicals.

For enterprises in Ethiopia and China, coating and printing is the third largest segment of

the value chain and accounts for 9 percent to 17 percent of the overall value chain. Here

again, consumables account for more than 78 percent of the inputs for this segment of the

value chain. In Vietnam, however, cutting and shaping was the third largest segment of

the value chain, accounting for approximately 5.4 percent of the overall value chain. In

Zambia, coating and painting is the second highest cost contributor to the value chain

(16.8 percent). This is attributed to the high cost of consumables but also the fact that the

technology in Zambia requires LPG (liquid petroleum gas) to run the printing operation

(which adds nearly 19 percent to the coating and painting cost component). The reliance

upon LPG can cause a problem with operations. The LPG is sourced from South Africa

and if it is not available for any reason, as was the case for a week in January 2011, the

printing operations cannot be executed and the line has to shut down.

118

Value chain diagrams in this section reflect actual data from export oriented best practice firms.

255

Figure 46: Crown Cork Value Chain Diagram, Ethiopia

Crown Cork Addis Ababa Ethiopia Unit production cost 6.60 $ (per 1,000) Price of Imported Tin-Free Steel $/ton 1,414 $ Skilled:Unskilled Worker Ratio 1:1.02

Raw material Coating & Painting

Cutting and Shaping

Seal Making & Sealing Packing Admin

65.0% 8.6% 0.8% 17.1% 3.3% 5.2%

Tin-free steel 100.0% Raw material 78.2% Raw material 78.2% Labor 4.0% Labor 1.5% Electricity 4.3% Fuel/oil/ water 17.4%

R & M 11.6% R & M 1.6% Raw material 5.61 $ 85.1% Labor 0.11 $ 1.6%

Packing material 0.21 $ 3.1% Global Development Solutions, LLC

256

Figure 47: Crown Cork Value Chain Diagram, Zambia

Crown Cork Ndola Zambia Unit production cost 5.66 (per 1,000) 0.005661 $ Price of Imported Tin-Free Steel $/ton 1,610 Skilled:Unskilled Worker Ratio 2.8:1

Raw material Coating & Painting

Cutting and Shaping

Seal Making & Sealing Packing Admin

58.3% 16.8% 2.6% 14.4% 3.4% 4.5%

Tin-free steel 100.0% Raw material 65.5% Raw material 89.9%

Fuel/oil/LPG 18.8% Labor 8.5% Labor 8.1% R&M 0.9%

R&M 4.0%