Embed Size (px)

Citation preview

31

Comparative tables

Organisation

I Financing

II Health care

III Sickness – Cash benefits

IV Maternity

V Invalidity

VI Old-Age

VII Survivors

VIII Employment injuries and occupational diseases

IX Family benefits

X Unemployment

XI Guaranteeing sufficient resources

Appendix: Long-term care

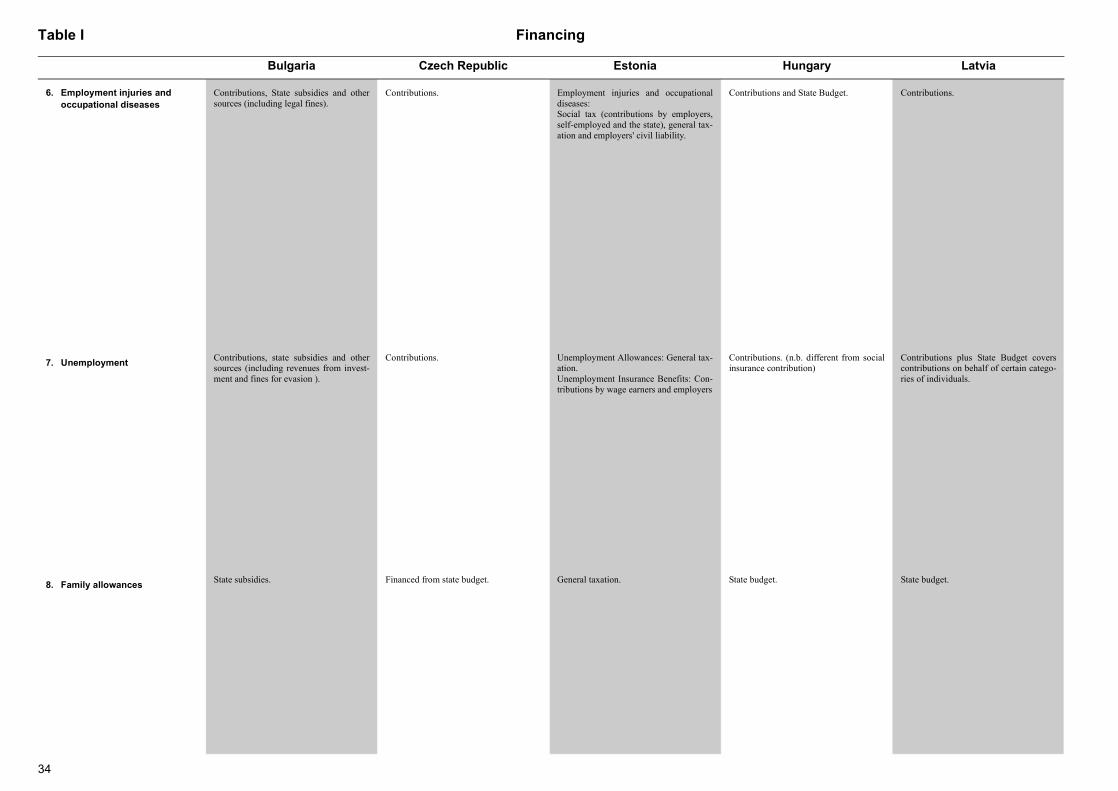

Table I Financing

3

Hungary Latvia

ons and State Budget. Ear marked part of personal income tax;subsidy from State Budget; patient co-payments.

ons and State Budget. Contributions.

et. No special scheme.

ons and State Budget. Contributions/State budget.

ar: Contribution and State

illar: Contributions (insurance

Contributions plus State Budget coverscontributions on behalf of certain catego-ries of individuals.

2

Bulgaria Czech Republic Estonia

Financing principle1. Sickness and maternity:

health care

Obligatory and voluntary health insur-ance contributions, state budget, privatehealth assurances and subscriptions(including revenues from legal fines forevasion).

(In fact the inclusion of health care underSickness and Maternity cannot possiblybe made. Health care includes health pro-motion and public health; outpatienthealth care (primary and specialised);impatient care. Health insured people inBulgaria are entitled to benefits from allthese types of health care. Services fromthe scope of emergency, blood transfu-sion, state sanitary control, etc. are paidthrough state budget.)

Contributions, state pays contributions onbehalf of certain categories of non-eco-nomically active individuals.

Social tax (contributions by employers,self-employed and the state).

Contributi

2. Sickness and maternity: Cash benefits

Contributions, state subsidies and othersources (including revenues from invest-ment and legal fines for evasion).

Contributions. Social tax (contributions by employers,self-employed and the state).

Contributi

3. Long-term care No special scheme. Financed from state budget. General taxation and local taxes. State Budg

4. Invalidity Contributions, state subsidies and othersources, including revenue from invest-ment, fines for evasion and the Govern-ment run Fund on Rehabilitation andSocial Integration of Handicapped (Фондза рехабилитация и социалнаинтеграция на инвалиди [Fond rehabili-tatzia i sotsialna integratzia na invalidi]).

Contributions. Pension for Incapacity to Work: Socialtax (contributions by employers, self-employed and the state).Pension supplements and National Pen-sion: General taxation.

Contributi

5. Old-age, survivors Contributions and State subsidies. Contributions. Old age pension: Social tax (contributionsby employers, self-employed and thestate).Pension supplements and National Pen-sion: General taxation.

First pillBudget.Second pfee)

Table I

33

Slovenia

ness and maternity: contributions forth insurance.

Financing principle1. Sickness and maternity:

health care

ness: See "Health Care" above.ernity cash benefits: special contribu- and State subsidy.

2. Sickness and maternity:Cash benefits

pecial scheme. 3. Long-term care

tributions and State guarantee for allfits.

4. Invalidity

tributions and State guarantee for allfits.

5. Old-age, survivors

Financing

Lithuania Poland Romania Slovakia

Contributions (earmarked taxes) and Statebudget.

Contributions and State subsidies. Contributions; State Budget; local budget;The Social Security Fund for Health(Fondul Asigurarilor Sociale de Sana-tate); the incomes of the special sanitaryunits and of the Ministry of Health andFamily (Ministerul Sanatatii si Familiei),which are constituted as extra budgetarysources at their disposal.

Contributions plus state subsidy. Sickheal

Contributions. Continued payment of sal-aries and wages by employer.

Contributions and State subsidies. • Contributions (sickness);• Budget of the state social insurance

(maternity).

Contributions plus state subsidy. SickMattion

No special scheme. Financed by themunicipalities as a part of health care orsocial services.

No special scheme. Contributions and State budget. Contributions plus state subsidy. No s

Contributions and State budget Contributions and State subsidies. • Local budgets; • State Budget covers deficit.

Contributions plus state subsidy. Conbene

Contributions. Contributions and State subsidies. Contributions. Contributions plus state subsidy. Conbene

Table I Financing

3

ons and State Budget. Contributions.

ons. (n.b. different from socialcontribution)

Contributions plus State Budget coverscontributions on behalf of certain catego-ries of individuals.

et. State budget.

Hungary Latvia

4

6. Employment injuries and occupational diseases

Contributions, State subsidies and othersources (including legal fines).

Contributions. Employment injuries and occupationaldiseases: Social tax (contributions by employers,self-employed and the state), general tax-ation and employers' civil liability.

Contributi

7. Unemployment Contributions, state subsidies and othersources (including revenues from invest-ment and fines for evasion ).

Contributions. Unemployment Allowances: General tax-ation.Unemployment Insurance Benefits: Con-tributions by wage earners and employers

Contributiinsurance

8. Family allowances State subsidies. Financed from state budget. General taxation. State budg

Bulgaria Czech Republic Estonia

Table I

35

tributions and State guarantee for allfits.

6. Employment injuries and occupational diseases

tributions and State subsidy. 7. Unemployment

e budget. 8. Family allowances

Slovenia

Financing

Contributions (since January 1, 2000,employer (for these risks before January1, 2000)).

Contributions and State subsidies. Contributions. Contributions. Conbene

Contributions. Contributions and State subsidies. Contributions. Contributions plus state subsidy. Con

State budget Financed entirely by the State. State budget (100%).Exception: guaranteeing minimumresources: State Budget (80%); revenueof local budgets of the territorial adminis-trative units (20%).

State Budget. Stat

Lithuania Poland Romania Slovakia

Table I Financing

3

survivors and invalidity:

ar: Pension Insurance Fundiztosítási Alap)er:e contributes only to this sys-f gross earningse contributes to both [state andstems): 2% of gross earnings 18% of the gross earnings

illar: Private Insurance Fundsond pillar covers only old age

type of survivor’s pension.)er: 6% of gross earnings No (compulsory) contribution

oth pillars):er: maximum 6490 HUF peray (2 368 850 HUF per calen-

No ceiling.

nal Health Insurance Fundbiztosítási Alap):

er: 3% of gross earnings 11% of gross earnings

er: No ceiling. No ceiling.

Global social insurance rate for sickness,maternity, invalidity, old-age, survivors,unemployment, employment injuries andoccupational diseases:• Wage earners who are covered by all

types of social insurance: wage earner: 9% gross earnings;employer: 26.09% gross earnings; total:35.09% gross earnings.

• Wage earners over state pensionableage and/or invalids of category one andtwo (insured for old age, survivors,sickness, maternity, employment inju-ries and occupational diseases):wage earner: 7.32% gross earnings;employer: 21.24% gross earnings; total:28.56% gross earnings.

• self-employed persons (insured for oldage, survivors, sickness, maternity andinvalidity): total: 32.27% gross earn-ings.

• self-employed persons over state pen-sionable age and/or invalids of categoryone and two (insured for old age, survi-vors, maternity and sickness): total:28.47% gross earnings.

• physical person who is carrying outmanagement of real estate and is regis-tered as a tax payer for the incomegained from the economic activity(insured for old age, survivors and inva-lidity): total: 30,86% gross earnings.

• permanent residents of Latviaemployed in Latvia by a foreign taxpayer (insured for sickness, maternity,invalidity, old-age, survivors, unem-ployment): wage earner: 35.00% ofgross earnings.

• permanent residents of Latvia over statepensionable age and/or invalids of cate-gory one and two and who areemployed in Latvia by a foreign taxpayer (insured for sickness, maternity,old age, survivors):wage earner: 28.47% of gross earnings.

• persons who are not permanent resi-dents of Latvia but who stay there for183 calendar days or more per tax yearand are employed by a foreign taxpayer (insured for old age, survivors,sickness, maternity and invalidity):wage earner: 8.52% gross earnings.

Hungary Latvia

6

Contributions of insured and employers Rates and ceiling1. Global contributions for

several branches

Contributions are calculated over grossmonthly earnings of employed anddeclared earnings of self-employed. In2002 the declared monthly income has tobe not less than 170 leva and up to a ceil-ing of 850 leva.

The general contribution rate for OldAge, Invalidity and Survivors accountsfor a 29% share in the proportion 75:25between the employer and wage earners,but this shall be gradually adjusted until itreaches 50/50 in 2007. The state pays theentire contribution for civil servants andmilitary officers; the self-employed (i.e.liberal professionals, craftsmen, soleentrepreneurs, shareholders, farmers etc.)pay the full amount of the contribution.

Insured persons are divided into 3 groupsaccording to the job conditions: • those employed by a contract for the

3rd (the most common) category oflabour;

• those employed by a contract for the2nd category of labour (operating underharmful work conditions);

• those employed by a contract for the 1stcategory of labour (the most harmfuland risky conditions of work).

The employers pay 3% higher generalcontribution rate for the 2nd and 1st cate-gory, as well as for the military servants.Next to this, all persons employed at theconditions of 2nd and 1st category partici-pate in the complementary professionalpension insurance (see “Other specialcontributions”) and this contribution ispaid entirely by the employer.

Basic Obligatory Pension Insurance (zák-ladní povinný systém důchodovéhopojištění)(covers old age, survivor's and invaliditypensions).

Wage earners: 6,5% gross earnings.Ceiling: none.Employers: 19,5% gross earnings.Ceiling: none.Total: 26%.

Self-employed: 26% declared earnings.Earnings ceiling: 486,000 CZK per year.

Employers:General rate of social tax 33% gross pay-roll, of which:• 13% health care and sickness insurance• 20% pension insurance.No ceiling.Wage earners:None

I. Old age,

First pill(NyugdíjbWage earna) (if he/shtem): 8% ob) (if he/shprivate] syEmployer:

Second p(Note: Secand some Wage earnEmployer:

Ceiling (bWage earncalendar ddar year)Employer:

II. Natio(EgészségRates: Wage earnEmployer:Ceiling:Wage earnEmployer:

Bulgaria Czech Republic Estonia

Table I

37

verall contribution. Contributions of insured and employers Rates and ceiling1. Global contributions for

several branches

Slovenia

Financing

Old age, invalidity and survivors pen-sions:• employers: 22.5% of gross wages of

wage earners• wage earners: 2.5% of gross wage• self-employed persons: 50% of the

basic pension and 15% of declaredincome subject to income tax. Ifdeclared income per year is lower than3 times official insured income, only50% of basic pension is obligatory.

• self-employed working by licence andfarmers: 50% of basic pension

• economically weak farmers: 20% of thebasic pension

Declared yearly income of self-employedpersons above 60 times official insuredincome is not subject of contributions.

No overall contribution. Sickness benefits in cash, maternity bene-fits in cash, old age pension, employmentinjury benefits, invalidity pension, andsurvivors’ pension are paid from thesocial insurance Fund (Bugetul Asigurar-ilor Sociale de Stat), funded through thecontributions paid by the employers (rep-resenting the main source of incomes ofthis system).

The contribution rates differ dependingon the working conditions of the insuredperson (35%, 40%, 45%). The contribu-tion rates are compulsory and apply to thegross income earned by the wage earner,thus to the total wage bill of eachemployer, out of which certain incomecategories are excepted.

In the case of the domestic personnelemployed by natural persons in order totake care of old persons, disabled andchildren, the social insurance contributionrate represents 15% of the gross wagereceived, but which cannot be lower thanthe gross economy-wide minimum wage.

Within the social security legislation threework groups can be distinguished accord-ing to the risks of the work performed:• Group 1, which concerns persons per-

forming most hazardous work like min-ing activities. The contribution for thisgroup is 45%;

• Group 2, which concerns persons per-forming hazardous work, like construc-tion work. The contribution for thisgroup is 40%;

• Group 3, concerning persons perform-ing normal work activities. The contri-bution for this group is 35%.

The monthly basis for the calculation ofthe individual social security contribu-tion cannot exceed 3 times the averagemonthly gross salary per economy.

Assessment Base:• wage earner: monthly gross earnings;• employer: total gross monthly payroll;• self-employed: 50% of average

monthly taxable income over previousyear.

If the self-employed is paying flat-rateincome tax, the assessment base is the fol-lowing:– one sixth of the flat-rate income tax

(minimum 4000 SKK per month) forpension (invalidity, old-age and survi-vors) insurance and sickness and mater-nity (cash benefits) insurance;

– voluntarily determined sum (minimum4000 SKK per month, if he/she has anincome below 500 000 SKK per year,5000 SKK per month, if he/she has anincome from 500 001 SKK to1 000 000 SKK per year, 6000 SKK permonth, if he/she has an income from1 000 001 SKK to 1 500 000 SKK peryear) to health insurance;

– voluntarily determined sum (minimum3000 SKK per month) to unemploy-ment insurance.

Invalidity, Old-Age and Survivors:Contribution as a percentage of theAssessment Base:• wage earner: 6,4%;• employer: 21,6% (5,3% for disabled

wage earners );• self-employed: 28%. Self-employed: If the taxable incomeover the previous year is below100 000 SKK, the participation is volun-tary. This sum will be valorized on 1 Julyof each calendar year from the year 2002on 10%.

Assessment Base Ceiling: minimum4000 SKK per month, maximum32 000 SKK per month. For disabled per-sons the minimum Assessment Base islower (3000 SKK in case of partial inva-lidity or juvenile wage earner over the ageof 16 years or 2000 SKK in case of totalinvalidity or juvenile wage earner underthe age of 16 years).

No o

Lithuania Poland Romania Slovakia

Table I Financing

3

Permanent residents aged 15 years andover, who are not subject to compulsorysocial insurance may join to state socialinsurance voluntarily. Persons who havenot already been granted an old age pen-sion may join the state pension insurancevoluntarily. The contribution basis isdeclared by the voluntarily insured them-selves. The volunteer contribution rate isthe same rate as for pension insurance –27.10% of gross earnings.Spouses of self-employed persons whoare not subject to compulsory socialinsurance may join the pension insurance,disability insurance, maternity and sick-ness insurance voluntarily if they havenot reached pensionable age. The volun-teer contribution rate is the sum of therates for pension insurance, disabilityinsurance, maternity and sickness insur-ance – 33.10% of gross earnings.Gross average insurance contributionsearnings are calculated from the insuredperson’s insurance contributions earningsfor the period of six calendar months ter-minating two calendar months precedingthe month of the insurance case.Earnings ceiling: maximum amount ofearnings subject to contributions is17 300 LVL per year, the minimum forself-employed persons is 480 LVL peryear and the minimum for voluntarilyinsured persons is 960 LVL per year.

Hungary Latvia

8

Bulgaria Czech Republic Estonia

Table I

39

Slovenia

Financing

Lithuania Poland Romania Slovakia

Table I Financing

4

bal contributions for severalabove. (Note: Mainly the

s 11% contribution covers this

Ear marked part of personal income tax,state subsidy and patient co-payments(see Chapter II Health Care).

bal contributions for severalabove. (Note: Mainly the wage% contribution covers this ben-

Included in "Global contributions for sev-eral branches" above: wage earner andemployer contributions for this branchamount to 2.24% of gross earnings (wageearners insured for all risks).

Hungary Latvia

0

2. Sickness and maternity: health care

(See subscript under "Financing princi-ple: 1. Sickness and maternity: healthcare" above.)

• employers: in 2002 4,5% gross earn-ings;

• wage earners: in 2002 1,5% gross earn-ings.

The state is covering the contributions forthe civil servants and pensioners and theProfessional Qualification and Unem-ployment. All self-employed are paying6% of their gross earnings. Someemployed members are paying in addition5% from their personal contribution forevery uninsured family member.

Wage earners: 4,5% gross earnings(obligatory). Ceiling: none.Employers: 9,0% gross earnings (obliga-tory). Ceiling: none.Total: 13,5%.

Self-employed: 13,5%. Ceiling: none.

Included in the general rate of social tax. No ceiling.

See "Globranches" employer’benefit.)

3. Sickness and maternity:Cash benefits

The contribution is 3% of the gross earn-ings, shared in proportion 75:25 betweenthe employer and wage earner, but thisshall be gradually adjusted until it reaches50/50 in 2007.

Wage earners: 1,1% gross earnings(obligatory). Ceiling: none.Employers: 3,3% gross earnings (obliga-tory). Ceiling: none.Total: 4,4%.Self-employed: 4,4% (voluntary). max. basis: 486,000 CZK yearly.

The assessment base for self-employedpersons in contributory schemes isdeclared earnings, which may not be lessthan 35% of the average monthly incomeor half the amount of the minimum wage.

Included in the general rate of social tax. No ceiling.

See "Globranches" earner’s 3efits.)

Bulgaria Czech Republic Estonia

Table I

41

tributions for all health insurancets for wage earners and self-employedons (excluding employment injuries):age earners: 6,36% of gross earningsr sickness benefit);ployers: 6,56% of gross earnings (orkness benefit);

lf-employed: 12,92% of insuranceting base;rmers: 6,36% of insurance ratingse.

ceiling for contributions forloyed, ceiling for self-employed anders.tribution for health services, thend of travel expenses, funeralnses and death grants for unem-ed persons and pensioners: 5,96% offit.eiling.

2. Sickness and maternity: health care

ness: shared contribution for health and cash benefits.ernity cash benefits:age earners: 0,1% of gross earnings;

ployers: 0,1% of gross earnings;lf-employed persons: 0,2% of insur-ce rating base;rmers: 0,2% of insurance rating base.tribution for sickness cash benefit,ral expenses and death benefits foremployed persons and farmers (ifred for pension and disability): 1,15%surance rating base.

3. Sickness and maternity:Cash benefits

Slovenia

Financing

• employers: 3% of gross earnings • wage earners: 0% of wage, but 30% of

personal income tax is directed intohealth insurance as a contribution.

• self-employed members of partner-ships and owners of personal enter-prises: 30% of personal income tax isdirected into health insurance as a con-tribution (in any case not less than 1/12of official yearly State contribution onbehalf of specific individuals who areaccording to the law “insured by theState” )

• self-employed working by licence: 30%of the cost of licence is directed intohealth insurance as a contribution. Min-imal contribution is 5% of official mini-mal wage.

• farmers and their family membersemployed in the farm: 3.5% of officialminimal wage.

• personal (small) land users and theirfamily members: 1.5% of official mini-mal wage

• other: 10% of average wage in thecountry.

No ceilings on contributions.

• insured persons: 7,75% of all earnings;• employers: none.

Ceiling: none.

The employers pay 7% of the gross earn-ings.The wage earners pay 7% of their grossincome.

For pensioners, unemployed, peoplereceiving support allowance and for thoseemployed in terms of a civil convention,the health insurance contribution is 7% oftwo time the national gross minimumwage.

The following categories of people arenon-contributory health insurance hold-ers:a) people who serve their military term;b) people on sick leave, or on sick leavegranted to attend the sick child aged lessthan 6 years;c) people who are imprisoned or are keptin preventive custody;d) people who are members of a familybenefiting from social assistance, accord-ing to bill no. 67/1995 regarding socialassistance.

The health insurance contribution due forthe persons mentioned above shall befunded as follows:a) by the State Budget - for those men-tioned above, subpar. a) c) and d):b) by the state social security budget - forthe persons mentioned above, subpar. b).

Contribution as a percentage of theAssessment Base (for Assessment Basesee "Global contributions for severalbranches" above):• wage earner: 4%;• employer: 10% (2,6% for disabled

wage earners);• self-employed: 14% (6,3% if disabled).

Assessment Base Ceiling: minimum3000 SKK (71 EUR) per month, maxi-mum 32 000 SKK per month. The mini-mum Assessment Base for disabled andjuvenile persons is lower (2250 SKK incase of partial invalidity or juvenile wageearner over the age of 16 years or1500 SKK in case of total invalidity orjuvenile wage earner under the age of 16years per month).

Conrighpers• w

(o• em

sic• se

ra• fa

baNo empfarmConrefuexpeploybeneNo c

• employer: 3% of gross earnings• wage earner: 0.5%No ceilings on contributions

• insured persons: 2,45% of all earnings;• employers: none.

Ceiling: none.

See "Global contributions for severalbranches" above.

Contribution as a percentage of theAssessment Base (for Assessment Basesee "Global contributions for severalbranches" above):• wage earner: 1,4%;• employer: 3,4% (1,1% for disabled

wage earner);• self -employed: 4,8%.Self-employed: the participation is volun-tary if the taxable income over the previ-ous year is below 100 000 SKK.

Assessment Base Ceiling: minimum4000 SKK (95 EUR) per month, maxi-mum 32 000 SKK (762 EUR) per month.For disabled persons the minimumassessment base is lower (3000 in case ofpartial immobility or juvenile wageearner over the age of 16 or 2000 SKK incase of total invalidity or juvenile wageearner under the age of 16) per month.

SickcareMat• w• em• se

an• faConfuneself-insuof in

Lithuania Poland Romania Slovakia

Table I Financing

4

et d, and operated under social system)

No special scheme.

bal contributions for severalabove.

Included in "Global contributions for sev-eral branches" above: wage earner and employer contributionsfor this branch amount to 3.76% of grossearnings (wage earners insured for allrisks).

bal contributions for severalabove

Included in "Global contributions for sev-eral branches" above: wage earner and employer contributionsfor this branch amount to 27.10% of grossearnings (wage earners insured for allrisks).From contributions of persons insured forold-age in the 2nd tier pension scheme(see Chapter VI Old-age), 10 % (to bephased in by 2010; 2% on 01.01.2002)are transferred to the 2nd tier.

o specific contribution, thesee financed partly by the HealthFund and partly by the PensionFund. (See "Global contribu-

everal branches" above.)

Included in "Global contributions for sev-eral branches" above: employer contributions for this branchamount to 0.09% of gross earnings (wageearners insured for all risks).

Hungary Latvia

2

4. Long-term care No special scheme. Tax financed. No special scheme. State Budg(Tax baseassistance

5. Invalidity See "Global contributions for severalbranches" above.

Basic Obligatory Pension Insurance: see"Global contributions for severalbranches" above.

Pension for incapacity for work: includedin the general rate of social tax. No ceiling.

See "Globranches"

6. Old-age, survivors See "Global contributions for severalbranches" above.

Basic Obligatory Pension Insurance: see"Global contributions for severalbranches" above.

Old age pension: included in the generalrate of social tax. No ceiling.

See "Globranches"

7. Employment injuries and occupational diseases

0,7% contribution rate over the grossearning, paid by the employer only.

Insurance contribution varies accordingto risk (between 0,2 and 1,2% of grossearnings) paid by the employer.

No special insurance, risks are coveredunder health care, sickness and invalidity.No ceiling.

There is nbenefits arInsurance Insurance tions for s

Bulgaria Czech Republic Estonia

Table I

43

pecial scheme. 4. Long-term care

uded in pension and invalidity insur- and health insurance contributions.

5. Invalidity

tributions for old age, survivors andlidity pensions and related benefitsurvivors, invalidity related and unre- to work and social benefits for

red persons:age earner: 15,50% gross wage;

ployer: 8,85% gross wage;lf-employed: 24,35% of insuranceting base (7 categories related to thevel of profit of the self-employed);rmers, if they do not exceed income

its: 15,50% of insurance rating base;ceiling for employed; ceiling for self-loyed.

6. Old-age, survivors

porary incapacity: contribution forloyment injuries and occupationalases: ployers: 0,53% of gross wage;

lf-employed persons: 0,53% of grossage;rmers (if insured for pensions): 0,53% gross wage.

g-term incapacity: see "Global contri-ons for several branches" above.

7. Employment injuries and occupational diseases

Slovenia

Financing

No special scheme, financed as part ofhealth care or social services.

No special scheme. No special scheme. Included in the health care contribution. No s

See "Global contributions for severalbranches" above.

• insured persons: 6,5% of all earnings;• employers: 6,5% of all earnings.

Ceiling: 30 times the projected nationalaverage wage as set out in the budget. Theceiling applies to the total contribution ofemployers and insured persons.

See "Global contributions for severalbranches" above.

See "Global contributions for severalbranches" above.

Inclance

See "Global contributions for severalbranches" above.

• Survivors: see “5. Invalidity” above.Survivors’ insurance contribution isshared together with invalidity insur-ance contribution

• Old-age: - insured persons: 9,76% of all earnings;- employers: 9,76% of all earnings.

Ceiling: 30 times the projected nationalaverage wage as set out in the StateBudget Act. The ceiling applies to thetotal contribution of employers andinsured persons.

See "Global contributions for severalbranches" above.

See "Global contribution for severalbranches" above.

Coninvafor slatedinsu• w• em• se

rale

• falim

No emp

• employer: 1% of gross earnings• wage earner: 0 %No ceilings on contributions.

• insured persons: none;• employers: 1,62% of gross earnings.

Ceiling: none.

• Temporary incapacity (incapacitatetemporara): financed by the employerand state social security budget.

• Permanent incapacity (incapacitatepermanenta): the same rules as forinvalidity.

No ceiling.

Employer's contributions of between0,2% and 1,2% of the Assessment Base(according to the degree of risk).

Temempdise• em• se

w• fa

of

Lonbuti

Lithuania Poland Romania Slovakia

Table I Financing

4

arket Fund (Munkaerőpiaci

ner: 1.5% of gross earningst pensioner, invalidity pen-workers’ compensation benefi- contribution) 3% of gross earnings

one.

Included in "Global contributions for sev-eral branches" above: wage earner and employer contributionsfor this branch amount to 1.90% of grossearnings (wage earners insured for allrisks).

et. No special contributions.

enefit contribution: are obliged to pay as contribu-ird of the sickness benefit dis-any insured person during thehich the person is incapable of

undergoing treatment in a hos-c).

No special scheme.

scheme. No special scheme.

scheme. No special scheme.

Hungary Latvia

4

8. Unemployment 4% gross earnings (total), the ratio ofemployer's to wage earner's contributionis currently 75:25 but this shall be gradu-ally adjusted until it reaches 50:50 in2007.

State employment policy:Wage earners: 0,4% gross earnings.Employers: 3,2 % gross earnings.Total: 3,6% gross earnings.Self-employed: 3,6% declared earnings.

Unemployment insurance contribution:• insured persons:

1% gross earnings• employers:

0.5% gross earnings

Labour MAlap)Rates:Wage ear(retiremensioner or ciaries: noEmployer:

Ceiling: N

9. Family allowances No special scheme. Tax financed. No special scheme State Budg

Other special contributions1. Sickness and maternity

• Fines for evasion;• Fees for administrative services;• Interest and revenues from investment.

No special scheme. No special scheme Sickness bEmployerstion one thbursed to period in wwork or ispital (clini

2. Long-term care No special scheme. No special scheme. No special scheme No special

3. Invalidity • Fines for evasion;• Fees for administrative services;• Interest and revenues from investment.

No special scheme. No special scheme No special

Bulgaria Czech Republic Estonia

Table I

45

tributions:age earners: 0,14% gross wage;

ployers: 0,06% gross wage.eiling.

8. Unemployment

pecial scheme. 9. Family allowances

pecial scheme. Other special contributions1. Sickness and maternity

pecial scheme. 2. Long-term care

pecial scheme. 3. Invalidity

Slovenia

Financing

• employer: 1.5% of gross earnings • wage earner: 0 %No ceilings on contributions.

• insured persons: none;• employers: 2,45% of earnings.

Ceiling: none.

• Employers: 5% of gross earnings. • Insured persons: 1% of the gross salary.

No ceiling.

Contributions as a percentage of theAssessment Base (for Assessment Basesee "Global contributions for severalbranches" above):• wage earner: 1%;• employer: 2,75% (0,9% for all wage

earners, if more than 25% of total workforce is disabled);

• self-employed persons: 3%.

Assessment Base Ceiling: minimum3000 SKK (71 EUR) per month, maxi-mum 24 000 SKK (560 EUR) per month.For disabled persons the minimumassessment base is lower (2250 SKK incase of partial invalidity or juvenile wageearner over age 16 or 1500 SKK in caseof total invalidity or juvenile wage earnerunder age 16 per month).

Con• w• emNo c

No special scheme. No special scheme. No special scheme. No special scheme. No s

No special scheme. No special scheme. Health care: subsidies from alcohol andtobacco tax.

No special scheme. No s

No special scheme. No special scheme. No special scheme. No special scheme. No s

No special scheme. No special scheme. No special scheme. No special scheme. No s

Lithuania Poland Romania Slovakia

Table I Financing

4

scheme. No special scheme.

in supplementary activities tevékenység): entrepreneurialployed activities performed bynsioners or surviving spouses

he retirement age must pay 5%rnings towards the expenses ofnt injuries and occupationalcial security services.

No special scheme.

scheme. No special scheme.

scheme. No special scheme.

Hungary Latvia

6

4. Old-age and survivors Compulsory complementary pensioninsurance (second pillar), which com-bines professional and universal insur-ance, both financed on capitalizationprinciple and run by private pension com-panies under the supervision of the StateInsurance Supervision Agency(Държавна агенция заздравноосигурителен надзор [Dazjavnaagentsija za zdravnoosiguritelen nad-zor]).

Other revenues:• Fines for evasion;• Fees for administrative services;

Interest and revenues from investment.

No special scheme. No special scheme No special

5. Employment injuries and occupational diseases

• Reimbursement from employers equalto the amount of benefits paid in case ofemployment injury related to the trau-matic damages;

• Fines for evasion;• Fees for administrative services;• Interest and revenues from investment.

No special scheme. No special scheme Engaged (kiegészítőor self-emold-age pereaching tof gross eaemploymedisease so

6. Unemployment • Fines for evasion;• Fees for administrative services;• Interest and revenues from investment.

No special scheme. No special scheme No special

7. Family allowances No special scheme. No special scheme. No special scheme No special

Bulgaria Czech Republic Estonia

Table I

47

pecial scheme. 4. Old-age and survivors

pulsory supplementary pensionrance for insured persons performingk particularly hard or harmful toth, and work that cannot be per-ed after a certain age. Contributions by the employer.

5. Employment injuries and occupational diseases

pecial scheme. 6. Unemployment

pecial scheme. 7. Family allowances

Slovenia

Financing

No special scheme. No special scheme. No special scheme. Contributions taken from supplementarypensions sum depends on "benefit plan"of the supplementary insurance agency.

No s

No special scheme. No special scheme. No special scheme. No special scheme. Cominsuworhealformpaid

No special scheme. No special scheme. No special scheme. Guarantee (Security) Fund: covers unpaidwages in case of employer insolvency,financed mainly from employer's contri-butions (0,25% from the AssessmentBase of all wage earners).

No s

No special scheme. No special scheme. Family benefits: subsidies from taxationon gambling.

No special scheme. No s

Lithuania Poland Romania Slovakia

Table I Financing

4

ontribution to the Nationalurance Fund:m (HUF 4500 /month) paid byloyer (if the wage earner hasen one employment relation- lump-sum must be paid onlyhis/her main employer) or the salary paid by the employere self-employed person), if the not covered under the generaltion scheme

No special scheme.

et guarantees deficit. Financed by state budget (28.40% of per-sonal income tax revenues).

et guarantees deficit. No participation of public authorities

Hungary Latvia

8

8. Other contributions or deductions not allocated to a particular branch

State subsidies for covering the deficit ofthe social insurance budget, donations ofprivate persons.

No special scheme. No special scheme Health cHealth Ins• lump-su

the empmore thship, theonce by

• 11% of (or by thsalary iscontribu

Public Authorities' participation1. Sickness and maternity:

Benefits in kind

Payment of a fixed contribution for speci-fied categories of persons (e.g. civil serv-ants, military personnel), and all costs forspecific services (e.g. financing measuresfor reduction of health risks, provision ofprosthetics, etc.).

Social tax paid by state on behalf of somecategories of non-active persons:• non-working spouses of diplomats and

public servants serving in foreign mis-sions

• working-age carer of a disabled personreceiving the Caregivers Benefit

• disabled persons working in a company,non-profit association or foundationincluded in the list established by theMinister of Social Affairs

• recipients of state unemploymentallowance or unemployment insurancebenefit

• persons raising a child up to 3 years ofage and receiving the Childcare Allow-ance

• non-working parents in a family withthree or more children at least 3 yearsof age and receiving the ChildcareAllowance

Ambulance services financed from gen-eral taxation.

State Budg

2. Sickness and maternity: Cash benefits

Payment of all contributions for civilservants, e.g. sick-pay for the first 3 days.

State pays contributions on behalf of non-economically active people.• pensioners,• dependent children,• students at secondary school or univer-

sity,• job seekers registered at a Labour

Office,• those on military or civilian service,• persons caring for a child up to the age

of 4 years, • persons caring for a close incapacitated

relative, etc.This contribution amounts to 13,5% of aMonthly Assessment Base (= 3250 CZK).

Social tax paid by state on behalf of somecategories of non-active persons. Forindication of categories see Sickness andMaternity: Benefits In-kind’ above.

State Budg

Bulgaria Czech Republic Estonia

Table I

49

pecial scheme. 8. Other contributions or deductions not allocated to a particular branch

e pays for:ntributions on behalf of certainoups of insured persons (e.g. recipi-ts of non-contributory unemploymentsh benefit, social assistance, invalid- assistance, as well as war veteransd military personnel performing civilrvice);alth care of military personnel, refu-es, prisoners etc.;blic health institutions (state andcal communities) and public healthogrammes;llection of blood, organs and tissuesr transplantation;ergency health care for uninsured

rsons.al authorities pay for citizens of Slov- residing in local community in Slov- who are not insured under anying of compulsory insurance.

Public Authorities' participation1. Sickness and maternity:

Benefits in kind

ate makes contributions on behalf ofrtain groups of insured persons (e.g.cipients of non-contributory unem-oyment benefit, social assistance andvalidity assistance, as well as war vet-ans and military personnel perform-g civil service).ate finances bulk of maternity bene-s from State budget (92% stateancing and 8% contributions).

ate makes contributions for employ-ent injuries and occupational diseasesr certain groups of insured persons.g. prisoners not working full-time,scue teams and some other organisedtions, if not insured on another basesc.).

2. Sickness and maternity: Cash benefits

Slovenia

Financing

No special scheme. No special scheme. No special scheme. No s

Partial participation in financing (contri-butions are made by the state on behalf ofspecific individuals who are according tothe law “insured by the State” (like pen-sioners, children, etc.)

Some medical services are financeddirectly from the State Budget or by thelocal authorities (for example organ trans-plantation, heart operations, treatment ofTurner's syndrome, treatment abroad).

State Budget covers deficit. State subsidy to cover deficit. State alsopays contributions into the health insur-ance system on behalf of:• children;• students;• pensioners;• unemployed persons not in receipt of

unemployment benefit; • women on maternity leave;• persons caring for disabled persons; • recipients of social assistance benefit; • soldiers during basic (compulsory) mil-

itary service, persons during civil serv-ice instead of basic military service;

• prisoners.The amount of contribution is 14% of anAssessment Base of 2750 SKK in theyear 2002. The National Labour Office(public body) pays contributions onbehalf of recipients of unemploymentbenefit at 14% of an Assessment Base of2700 SKK.

Stat• co

grencaityanse

• hege

• pulopr

• cofo

• empe

Loceniaeniahead

State subsidy to cover deficit. Deficits covered by the State Budget. State Budget covers deficit. State subsidy to cover deficit. The Statealso pays contributions on behalf of stu-dents and unemployed persons who arenot in receipt of unemployment benefit. In the year 2002 the amount of contribu-tion is 4,8 % from 45 % of an AssessmentBase of 5000 SKK. The National LabourOffice (public body) pays contributionson behalf of recipients of unemploymentbenefit at 4,8% of an Assessment Base of2700 SKK (130 SKK - 3 EUR permonth).

• Stcereplinerin

• Stfitfin

• Stmfo(ereacet

Lithuania Poland Romania Slovakia

Table I Financing

5

rom State Budget. No special scheme.

et guarantees deficit. Financed by state budget

Hungary Latvia

0

3. Long-term Care Not applicable. No public authority participation. Financed by the state from general taxa-tion and by local authorities.

Financed f

4. Invalidity Payment of contribution on behalf of civilservants and financing of non-contribu-tory benefits.

Tax financed. Pension for Incapacity to Work: social taxpaid by state on behalf of some categoriesof non-active persons: • non-working spouses of diplomats and

public servants serving in foreign mis-sions

• working-age carer of a disabled personreceiving the Caregivers Benefit

• disabled persons working in a company,non-profit association or foundationincluded in the list established by theMinister of Social Affairs

• army conscripts• persons raising a child up to 3 years of

age and receiving the Childcare Allow-ance

• non-working parents in a family withthree or more children at least 3 yearsof age and receiving the ChildcareAllowance

National Pension: financed from generaltaxation.Allowances for disabled children and spe-cial non-contributory social benefits forthe disabled are financed from generaltaxation.

State Budg

Bulgaria Czech Republic Estonia

Table I

51

e covers institutional care for severelybled children, elderly and disabledons who do not have sufficient bene-and income to cover expenses of insti-nal care.

3. Long-term Care

further, Old-age, survivors. 4. Invalidity

Slovenia

Financing

No special scheme financed as part ofhealth and social services.

No special scheme. State Budget covers deficit. State subsidy for home care service, forpersonal assistance, for purchasing andmaintaining medical equipment.

Statdisapersfits tutio

State subsidy to cover deficit. Also partialparticipation in financing. (contributionsare made by the state on behalf of specificindividuals).

Deficits covered by the State Budget. State Budget covers deficit and pays ben-efits (pensions) for war veterans, invalidsand war widows.

State subsidy to cover deficit. The Statealso pays contributions on behalf of:• university students;• parents of young or disabled children;• disabled persons;• unemployed persons who are not in

receipt of unemployment benefit;• soldiers during basic (compulsory) mil-

itary service, persons during civil serv-ice instead of basic military service.

The amount of contribution is 28% of anAssessment Base of 5000 SKK in theyear 2002. The National Labour Office(public body) pays contributions onbehalf of recipients of unemploymentbenefit at 28% of an Assessment Base of2700 SKK.

See

Lithuania Poland Romania Slovakia

Table I Financing

5

: State Budget guarantees for

illar: No direct contributionc authorities.

The State Budget pays compulsory con-tributions of 10 LVL per month on behalfof:• active military conscripts,• individuals taking care of a child under

1.5 years of age, • individuals whose spouse is on diplo-

matic or consular duty abroad and whoare residing in the relevant foreigncountry.

The state social insurance special budgetcovers the compulsory contributions onbehalf of:• recipients of unemployment benefit:

20% of unemployment benefit,• unemployed disabled persons: the rate

is 20% from 50% of the national aver-age insurance contribution earnings ofthe previous year or 20% of the insur-ance indemnity for the loss of capacityfor work,

• recipients of maternity or sickness ben-efit: 20% of sickness or maternity bene-fit.

et guarantees deficit. No participation of public authorities.

easures: Partial direct contribu-public authorities. asures: Partial direct contribu-

public authorities

The State Budget pays compulsory con-tributions of 0.95 LVL per month onbehalf of:• active military conscripts;• those caring for a child under 1.5 years

of age.

The state social insurance special budgetpays the compulsory contribution onbehalf of the recipients of sickness bene-fits amounting to 1.90% of the sicknessbenefit

Hungary Latvia

2

5. Old-age, survivors Payment of contributions on behalf ofcivil servants and financing of non-con-tributory benefits.

No public authority participation. Old Age Pension: social tax paid by stateon behalf of some categories of non-active persons (categories indicated underInvalidity).National Pension: financed from generaltaxation.Pension supplements for civil servants,victims of political repression and warveterans are financed from general taxa-tion.

First pillardeficit.Second pfrom publi

6. Employment injuries and occupational diseases

Payment of contributions on behalf ofcivil servants.

No public authority participation. Social tax paid by state on behalf of somecategories of non-active persons. Forindication of categories see Sickness andMaternity: Benefits In-kind’ above.National Pension: financed from generaltaxation.State takes over employers' civil liabilityto pay compensation in cases of insol-vency and liquidation.

State Budg

7. Unemployment Payment of contributions on behalf ofcivil servants.

No public authority participation. Unemployment allowances financed bythe state from general taxation.

Passive mtion from Active metion from

Bulgaria Czech Republic Estonia

Table I

53

e finances matters defined by the law: a rule insurance benefits of a socialture, included in insurance scheme;nsions for some categories of self-ployed not covered under previous

surance legislation; tirement under more favourable con-tions for police, army personnel, warterans, victims of war and members parliament;e minimum pension, state pensiond pension support for those who havet sufficient sources for basic subsist-ce within their family;ecial pensions assigned to excep-nal cultural and other distinctive per-ns; e deficit of the Pension and Invaliditysurance Institute.

5. Old-age, survivors

mporary incapacity: see "Sickness"ove.ng-term incapacity: see "Invalidity"ove.

6. Employment injuries and occupational diseases

e finances bulk of unemploymentfits from State budget (approxi-

ely 10% contributions and 90% statencing).

7. Unemployment

Slovenia

Financing

State subsidy to cover deficit. Also partialparticipation in financing. (contributionsare made by the state on behalf of specificindividuals).

Deficits covered by the State Budget. State Budget covers deficit. See “Invalidity” above. Stat• as

na• pe

emin

• rediveof

• thannoen

• sptioso

• thIn

State subsidy to cover deficit. Financial support for those effected byemployer's bankruptcy (employer had topay benefits to those who sufferedemployment injuries or occupational dis-eases before January 1, 2000)

Deficits covered by the State Budget. State Budget covers deficit. No participation of public authorities. • Teab

• Loab

State subsidy to cover deficit. Deficits covered by the State Budget. State Budget covers deficit. State subsidy to cover deficit. Statbenematfina

Lithuania Poland Romania Slovakia

Table I Financing

5

nanced from State Budget. Financed entirely by state.

scheme. Financed by municipalities.

u Go. Pay As You Go.

: Pay As You Go.lar: Funding system.

Old-age: 1st tier – Pay As You Go; 2nd tier– fundedSurvivors: Pay As You Go.

u Go. Pay As You Go.

Hungary Latvia

4

8. Family allowances Financed entirely by the state. No public authority participation. Financed entirely by the state from gen-eral taxation.

Entirely fi

9. General non-contributory minimum

State financed by both the central budgetand local revenues, disbursed to individu-als by the local authorities.

Financed by state budget. Financed by the state from general taxa-tion and by local authorities.

No special

Financing systems for long-term benefits:1. Invalidity

Pay As You Go. Pay as you go. Pay As You Go. Pay As Yo

2. Old-age, survivors • Basic compulsory scheme: Pays AsYou Go;

• Compulsory supplementary privatescheme: funded.

Pay as you go. Pay As You Go. First pillarSecond pil

3. Employment injuries and occupational diseases

Pay As You Go. Pay as you go. Pay As You Go. Pay As Yo

Bulgaria Czech Republic Estonia

Table I

55

nced entirely from State budget. 8. Family allowances

imum income for social assistancepients (individuals and families)nced by the State budget.

9. General non-contributory minimum

As You Go. Financing systems for long-term benefits:1. Invalidity

As You Go. 2. Old-age, survivors

As You Go. 3. Employment injuries and occupational diseases

Slovenia

Financing

Family allowances are paid from StateBudget.

Entirely financed by State Budget. • State Budget;• Local budgets of territorial administra-

tive units.

Financed entirely by the State Budget. Fina

See Chapter XI"Guaranteeing sufficientresources".

No general minimum. • State budget;• Local budgets.

Financed entirely by the State Budget. Minrecifina

Pay As You Go. Pay As You Go. Pay As You Go. Pay As You Go. Pay

Pay As You Go. • Survivors: Pay As You Go.• Old Age:- 1st pillar: Pay As You Go:- 2nd pillar: Funded.

Pay As You Go. Pay As You Go. Pay

Pay As You Go. Pay As You Go. Pay As You Go. Pay As You Go. Pay

Lithuania Poland Romania Slovakia

![[FA] MIB-13-0354-iFinancing-4 panels application …...I hereby consent that the Bank may classify me as a recalcitrant account holder and/or suspend, recall or terminate my account(s)](https://img.pdfslide.us/doc/110x75/5e44a7fc0a362654884f92a2/fa-mib-13-0354-ifinancing-4-panels-application-i-hereby-consent-that-the-bank.jpg)