Embed Size (px)

Citation preview

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

COMPARATIVE ASSESSMENT OF COMPARATIVE ASSESSMENT OF ENERGY OPTIONS AND ENERGY OPTIONS AND

STRATEGIES UNTIL 2025STRATEGIES UNTIL 2025OVERVIEW AND RESULTSOVERVIEW AND RESULTS

Analysis Conducted by a Team of Analysts from:Analysis Conducted by a Team of Analysts from:

SENERSENERUNAMUNAM

CONAECONAEIMPIMPIIEIIEINEINE

PEMEXPEMEXCFECFE

Work Sponsored byWork Sponsored byIAEA, USDOSIAEA, USDOS

Presented at SENER on February 28, 2003Presented at SENER on February 28, 2003

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

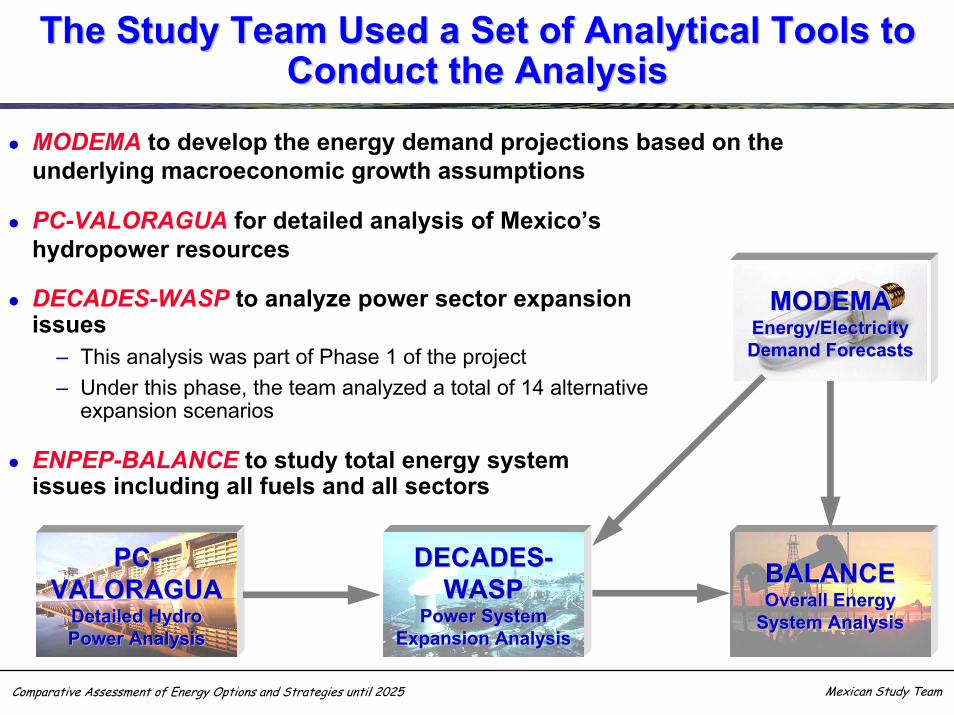

The Study Team Used a Set of Analytical Tools to The Study Team Used a Set of Analytical Tools to Conduct the AnalysisConduct the Analysis

MODEMAMODEMAEnergy/ElectricityEnergy/ElectricityDemand ForecastsDemand Forecasts

MODEMA to develop the energy demand projections based on the underlying macroeconomic growth assumptions

PCPC--VALORAGUAVALORAGUA

Detailed HydroDetailed HydroPower AnalysisPower Analysis

PC-VALORAGUA for detailed analysis of Mexico’shydropower resources

DECADESDECADES--WASPWASP

Power SystemPower SystemExpansion AnalysisExpansion Analysis

DECADES-WASP to analyze power sector expansionissues

– This analysis was part of Phase 1 of the project– Under this phase, the team analyzed a total of 14 alternative

expansion scenarios

BALANCEBALANCEOverall EnergyOverall Energy

System AnalysisSystem Analysis

ENPEP-BALANCE to study total energy systemissues including all fuels and all sectors

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

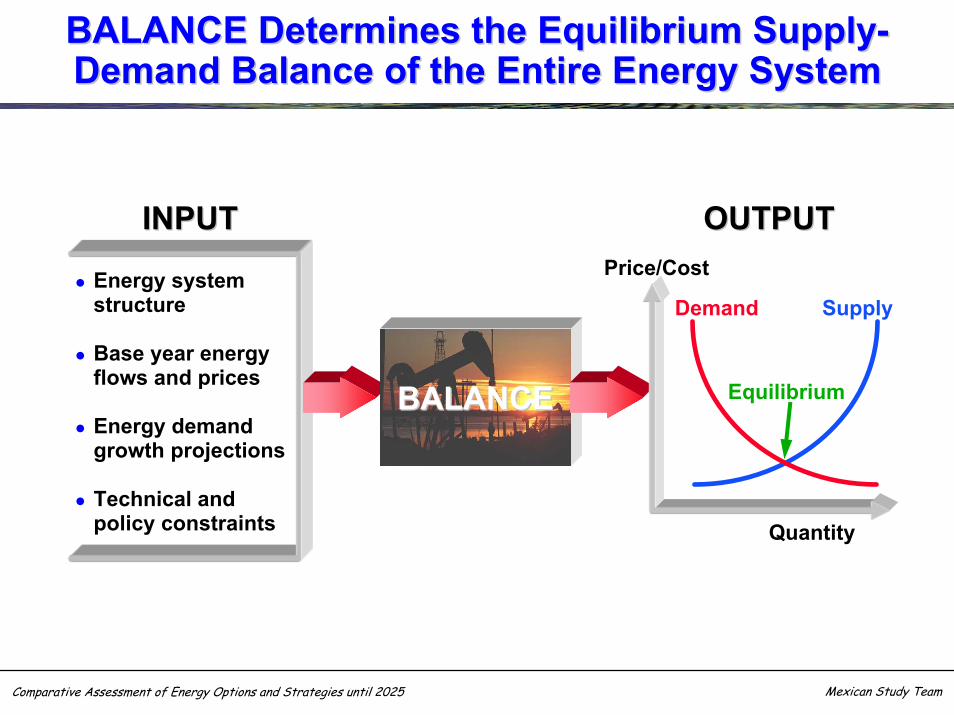

INPUTINPUT

Energy systemstructure

Base year energyflows and prices

Energy demandgrowth projections

Technical andpolicy constraints

BALANCEBALANCE

SupplyDemand

Equilibrium

OUTPUTOUTPUT

Quantity

Price/Cost

BALANCE Determines the Equilibrium SupplyBALANCE Determines the Equilibrium Supply--Demand Balance of the Entire Energy SystemDemand Balance of the Entire Energy System

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

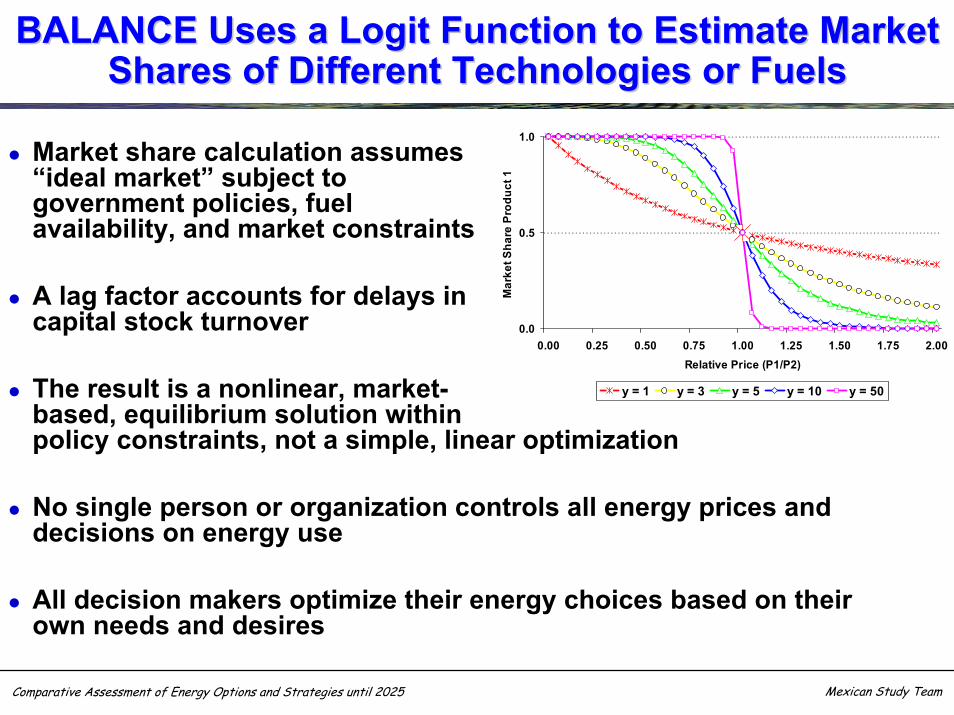

BALANCE Uses a BALANCE Uses a LogitLogit Function to Estimate Market Function to Estimate Market Shares of Different Technologies or FuelsShares of Different Technologies or Fuels

Market share calculation assumes“ideal market” subject togovernment policies, fuelavailability, and market constraints

A lag factor accounts for delays incapital stock turnover

The result is a nonlinear, market-based, equilibrium solution withinpolicy constraints, not a simple, linear optimization

No single person or organization controls all energy prices and decisions on energy use

All decision makers optimize their energy choices based on theirown needs and desires

0.0

0.5

1.0

0.00 0.25 0.50 0.75 1.00 1.25 1.50 1.75 2.00Relative Price (P1/P2)

Mar

ket S

hare

Pro

duct

1

y = 1 y = 3 y = 5 y = 10 y = 50

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

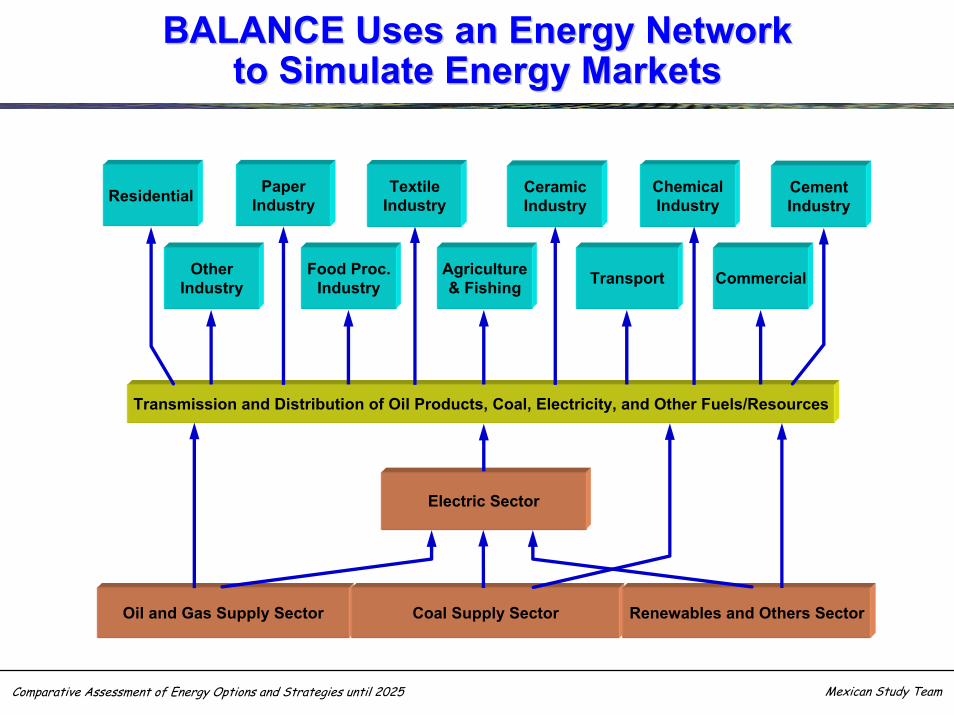

BALANCE Uses an Energy NetworkBALANCE Uses an Energy Networkto Simulate Energy Marketsto Simulate Energy Markets

Transmission and Distribution of Oil Products, Coal, Electricity, and Other Fuels/Resources

Residential PaperIndustry

OtherIndustry

Food Proc.Industry

Agriculture& Fishing Transport Commercial

CementIndustry

ChemicalIndustry

CeramicIndustry

TextileIndustry

Electric Sector

Oil and Gas Supply Sector Coal Supply Sector Renewables and Others Sector

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

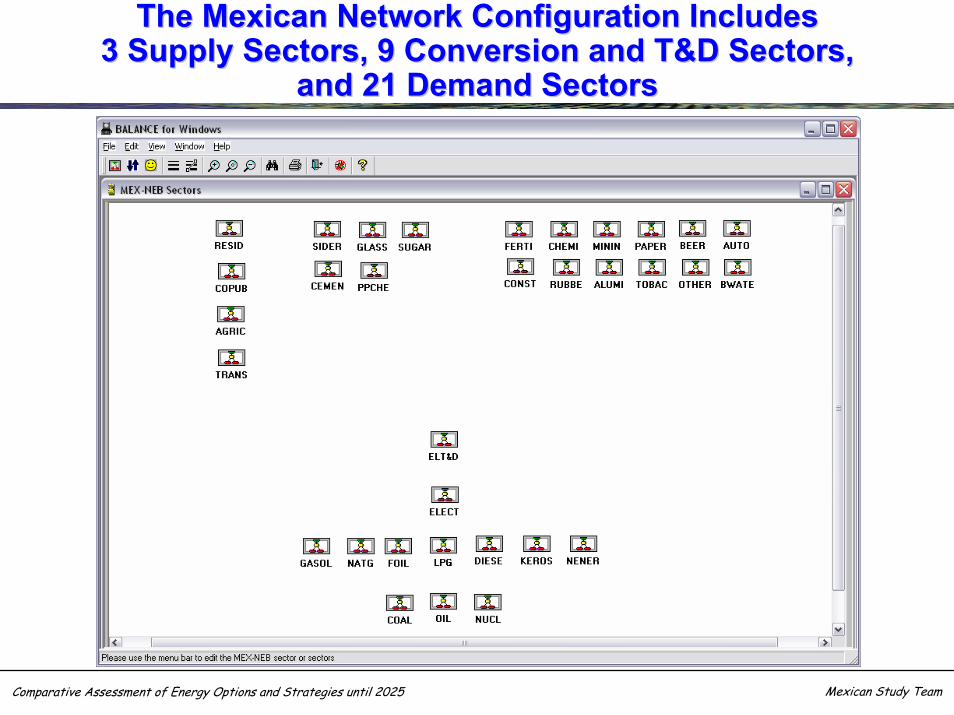

The Mexican Network Configuration IncludesThe Mexican Network Configuration Includes3 Supply Sectors, 9 Conversion and T&D Sectors,3 Supply Sectors, 9 Conversion and T&D Sectors,

and 21 Demand Sectorsand 21 Demand Sectors

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

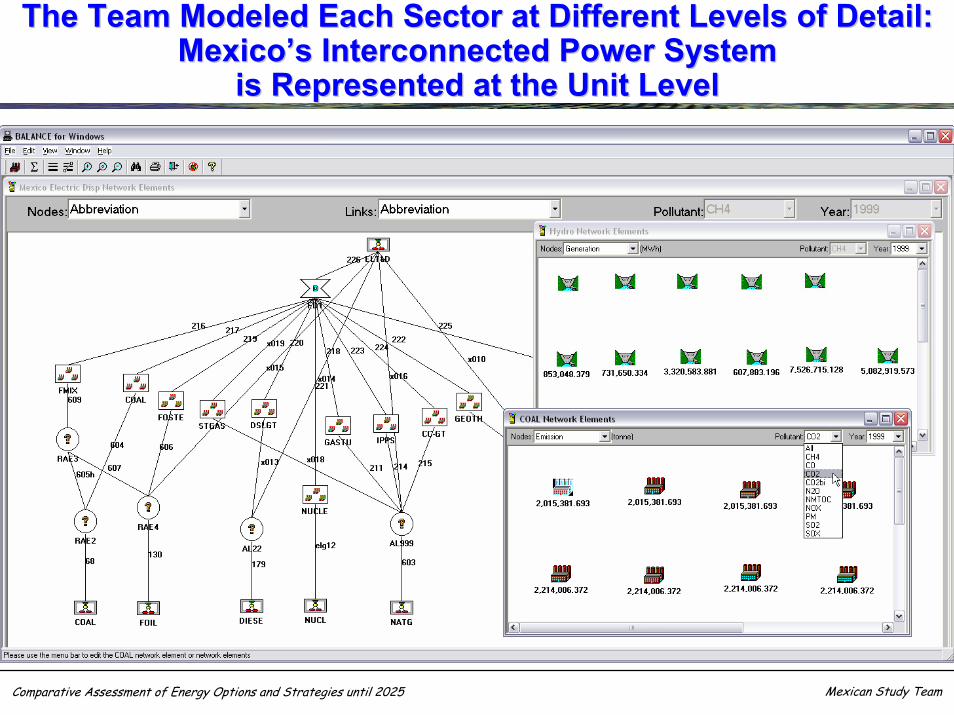

The Team Modeled Each Sector at Different Levels of Detail: The Team Modeled Each Sector at Different Levels of Detail: MexicoMexico’’s Interconnected Power Systems Interconnected Power System

is Represented at the Unit Levelis Represented at the Unit Level

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

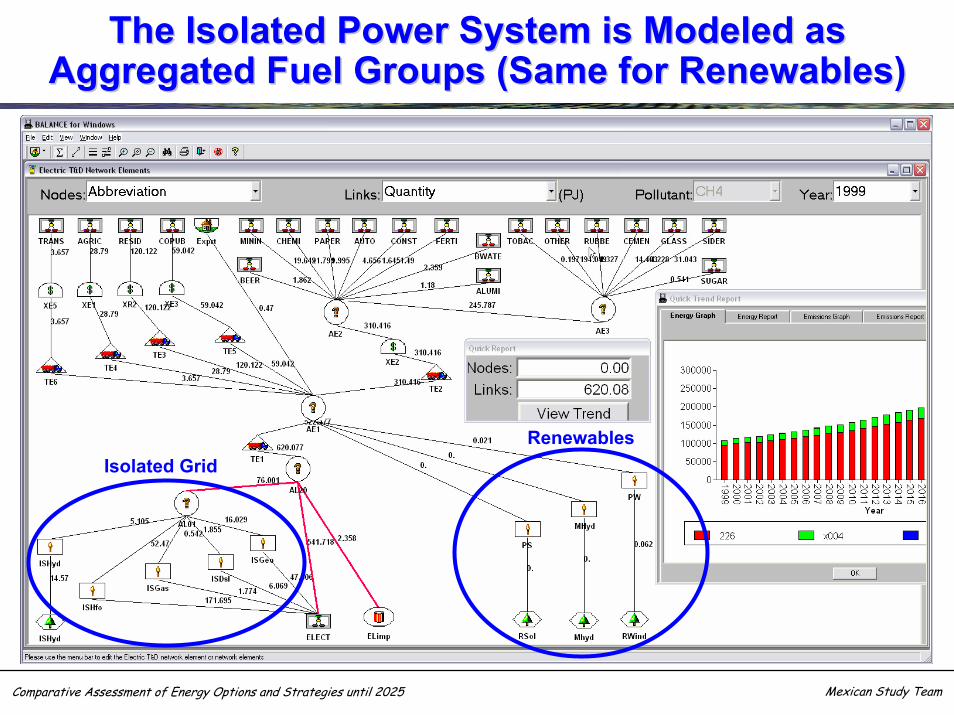

The Isolated Power System is Modeled asThe Isolated Power System is Modeled asAggregated Fuel Groups (Same for Renewables)Aggregated Fuel Groups (Same for Renewables)

Isolated GridRenewables

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

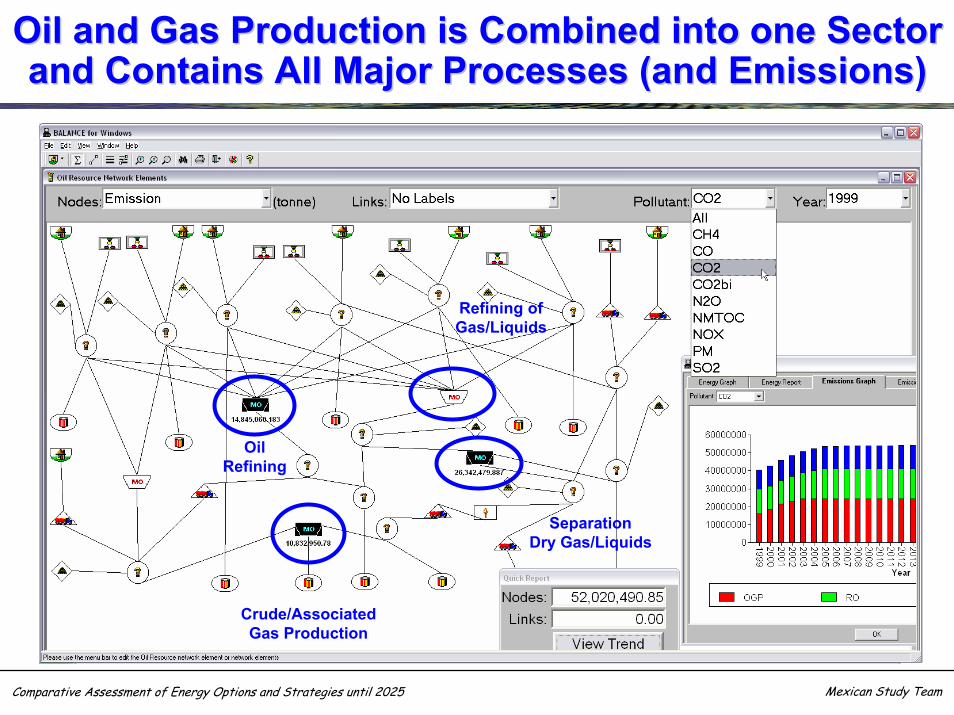

Oil and Gas Production is Combined into one Sector Oil and Gas Production is Combined into one Sector and Contains All Major Processes (and Emissions) and Contains All Major Processes (and Emissions)

OilRefining

Crude/AssociatedGas Production

SeparationDry Gas/Liquids

Refining ofGas/Liquids

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

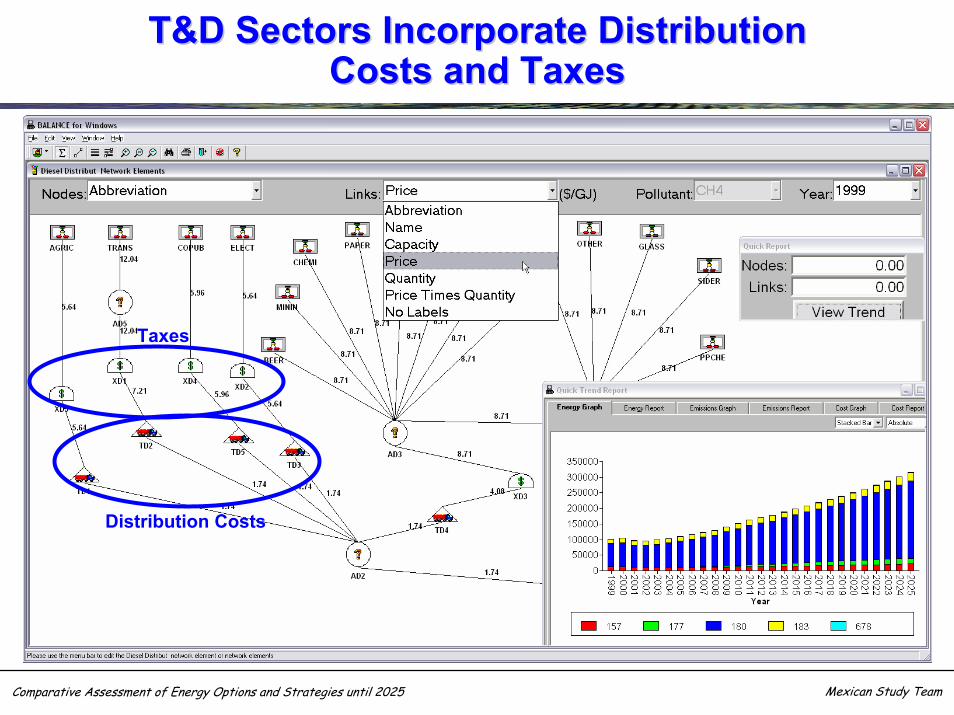

T&D Sectors Incorporate DistributionT&D Sectors Incorporate DistributionCosts and TaxesCosts and Taxes

Taxes

Distribution Costs

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

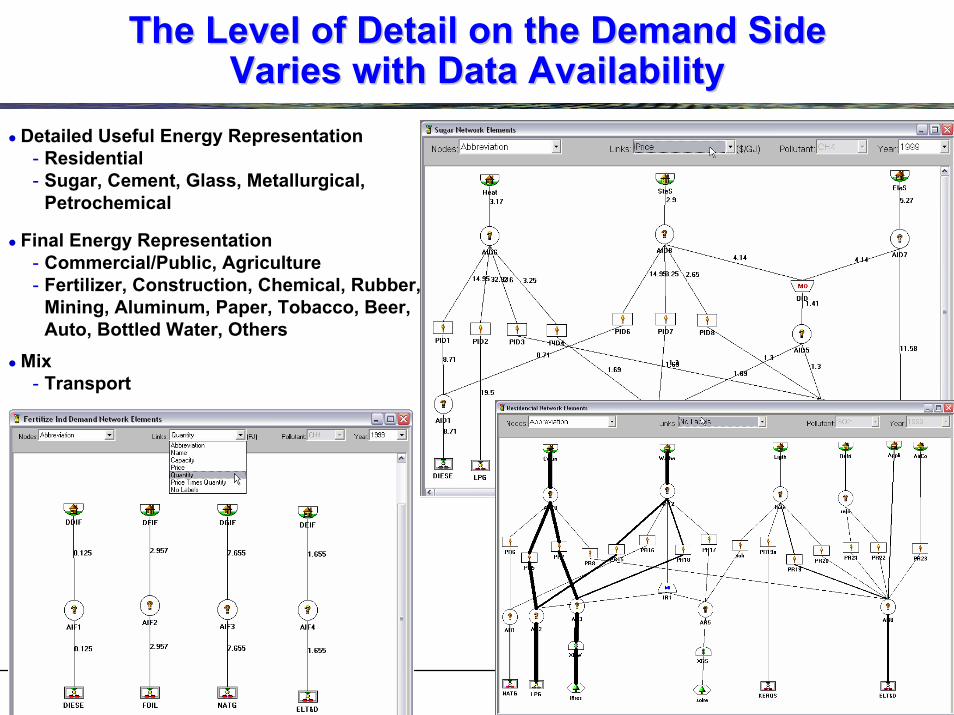

The Level of Detail on the Demand SideThe Level of Detail on the Demand SideVaries with Data AvailabilityVaries with Data Availability

Detailed Useful Energy Representation- Residential- Sugar, Cement, Glass, Metallurgical,

Petrochemical

Final Energy Representation- Commercial/Public, Agriculture- Fertilizer, Construction, Chemical, Rubber,

Mining, Aluminum, Paper, Tobacco, Beer,Auto, Bottled Water, Others

Mix- Transport

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

Data Availability and Data QualityData Availability and Data Quality

Supply side information is extensive, well documented, and of good quality– Power sector information available from CFE

Generation and fuel consumption data from annual report “Informe de Operacion”Unit characteristics directly from CFE’s Investment Planning and Expansion Analysis Departments

– Oil and gas sectorNational energy balance “Balance Nacional de Energia 2001”; price statistics from SENER/IEAAnnual forecasts for different products: “Prospectiva Gas Natural”, “Prospectiva LPG”, “Prospectiva Petroliferos”Cost data less reliable; some information available from PEMEX

– Other supply sectorsNational energy balance from SENERInformation from UNAM

Demand side information is more limited– Detailed industrial energy data available for 5 branches (UNAM and SENER)– Information for residential, transport, commercial/public, and agriculture came from IMP, INE,

and CONAE– No cost data available; used information from international literature– SENER is in the process of collecting regional demand data

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

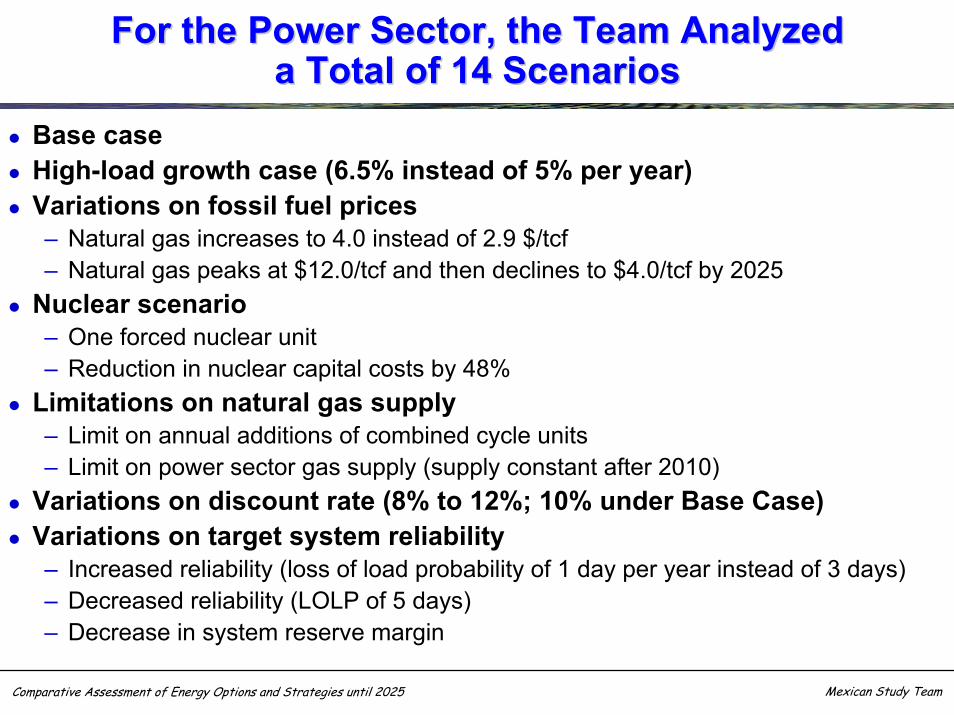

For the Power Sector, the Team AnalyzedFor the Power Sector, the Team Analyzeda Total of 14 Scenariosa Total of 14 Scenarios

Base caseHigh-load growth case (6.5% instead of 5% per year)Variations on fossil fuel prices– Natural gas increases to 4.0 instead of 2.9 $/tcf– Natural gas peaks at $12.0/tcf and then declines to $4.0/tcf by 2025

Nuclear scenario– One forced nuclear unit– Reduction in nuclear capital costs by 48%

Limitations on natural gas supply– Limit on annual additions of combined cycle units– Limit on power sector gas supply (supply constant after 2010)

Variations on discount rate (8% to 12%; 10% under Base Case)Variations on target system reliability– Increased reliability (loss of load probability of 1 day per year instead of 3 days)– Decreased reliability (LOLP of 5 days)– Decrease in system reserve margin

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

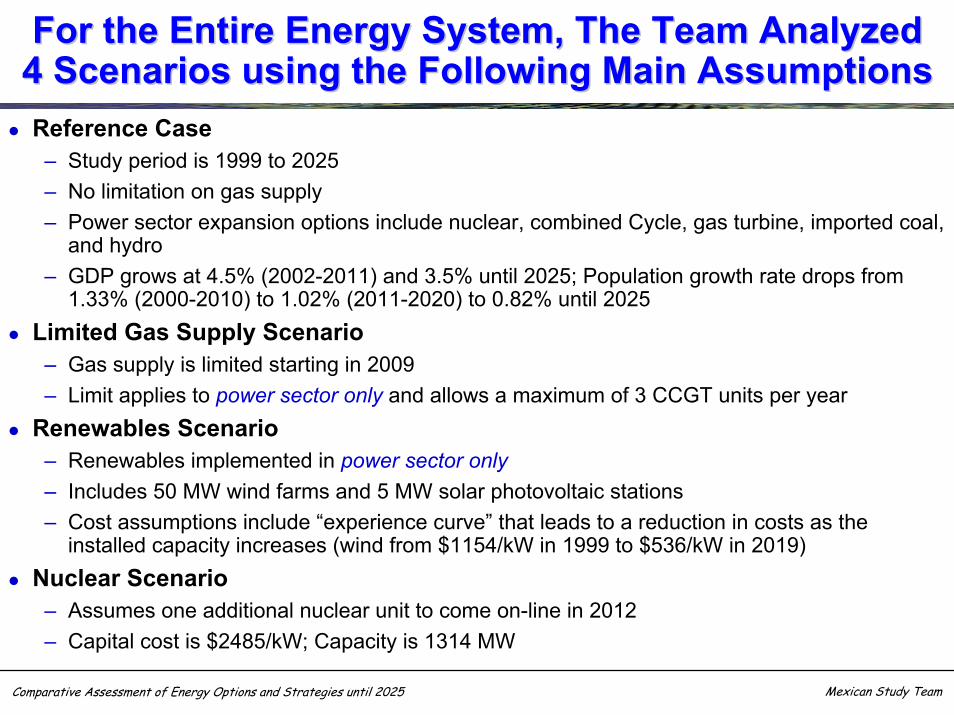

For the Entire Energy System, The Team AnalyzedFor the Entire Energy System, The Team Analyzed4 Scenarios using the Following Main Assumptions4 Scenarios using the Following Main AssumptionsReference Case

– Study period is 1999 to 2025– No limitation on gas supply– Power sector expansion options include nuclear, combined Cycle, gas turbine, imported coal,

and hydro– GDP grows at 4.5% (2002-2011) and 3.5% until 2025; Population growth rate drops from

1.33% (2000-2010) to 1.02% (2011-2020) to 0.82% until 2025Limited Gas Supply Scenario

– Gas supply is limited starting in 2009– Limit applies to power sector only and allows a maximum of 3 CCGT units per year

Renewables Scenario– Renewables implemented in power sector only– Includes 50 MW wind farms and 5 MW solar photovoltaic stations– Cost assumptions include “experience curve” that leads to a reduction in costs as the

installed capacity increases (wind from $1154/kW in 1999 to $536/kW in 2019)Nuclear Scenario

– Assumes one additional nuclear unit to come on-line in 2012– Capital cost is $2485/kW; Capacity is 1314 MW

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

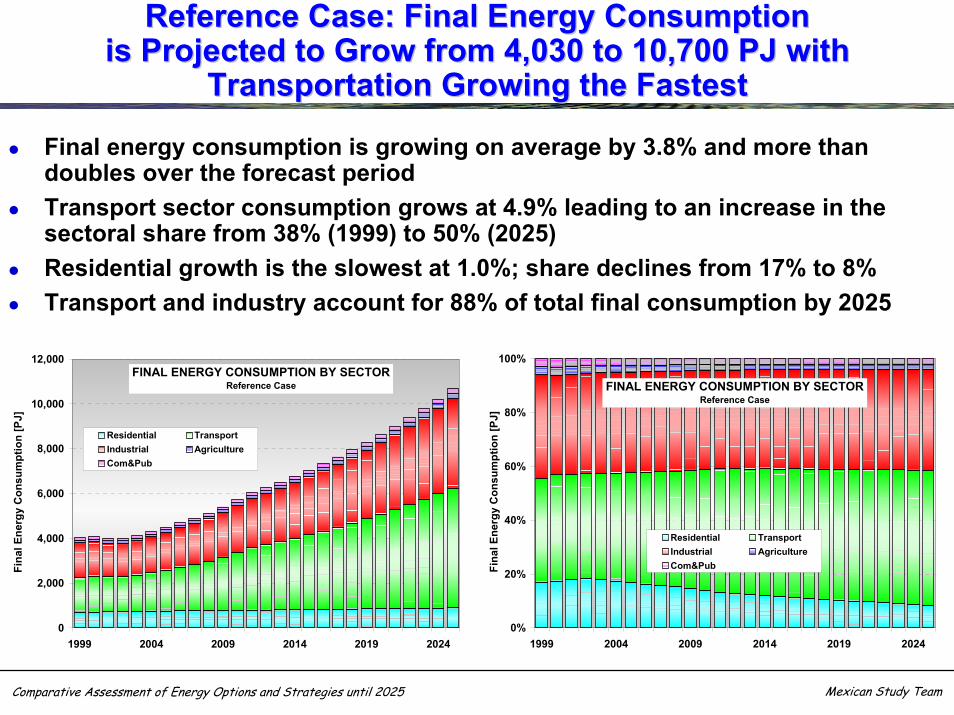

Reference Case: Final Energy ConsumptionReference Case: Final Energy Consumptionis Projected to Grow from 4,030 to 10,700 PJ with is Projected to Grow from 4,030 to 10,700 PJ with

Transportation Growing the FastestTransportation Growing the Fastest

Final energy consumption is growing on average by 3.8% and more than doubles over the forecast periodTransport sector consumption grows at 4.9% leading to an increase in the sectoral share from 38% (1999) to 50% (2025)Residential growth is the slowest at 1.0%; share declines from 17% to 8%Transport and industry account for 88% of total final consumption by 2025

0

2,000

4,000

6,000

8,000

10,000

12,000

1999 2004 2009 2014 2019 2024

Fina

l Ene

rgy

Con

sum

ptio

n [P

J]

Residential TransportIndustrial AgricultureCom&Pub

FINAL ENERGY CONSUMPTION BY SECTORReference Case

0%

20%

40%

60%

80%

100%

1999 2004 2009 2014 2019 2024

Fina

l Ene

rgy

Con

sum

ptio

n [P

J]

Residential TransportIndustrial AgricultureCom&Pub

FINAL ENERGY CONSUMPTION BY SECTORReference Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

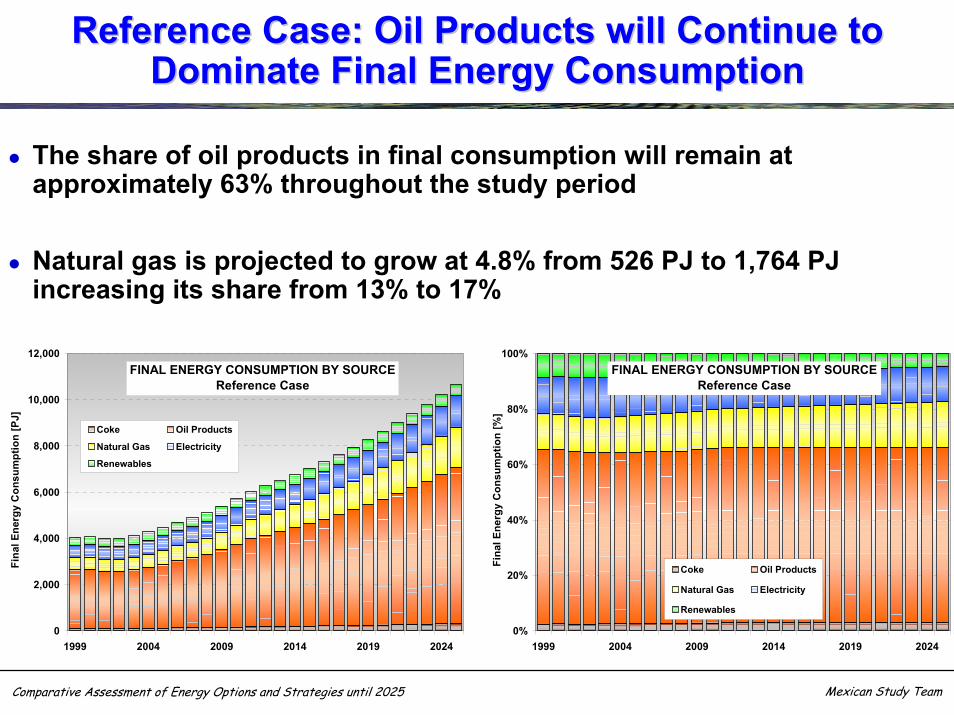

Reference Case: Oil Products will Continue to Reference Case: Oil Products will Continue to Dominate Final Energy ConsumptionDominate Final Energy Consumption

The share of oil products in final consumption will remain at approximately 63% throughout the study period

Natural gas is projected to grow at 4.8% from 526 PJ to 1,764 PJincreasing its share from 13% to 17%

0

2,000

4,000

6,000

8,000

10,000

12,000

1999 2004 2009 2014 2019 2024

Fina

l Ene

rgy

Con

sum

ptio

n [P

J]

Coke Oil Products

Natural Gas Electricity

Renewables

FINAL ENERGY CONSUMPTION BY SOURCEReference Case

0%

20%

40%

60%

80%

100%

1999 2004 2009 2014 2019 2024

Fina

l Ene

rgy

Con

sum

ptio

n [%

]

Coke Oil Products

Natural Gas Electricity

Renewables

FINAL ENERGY CONSUMPTION BY SOURCEReference Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

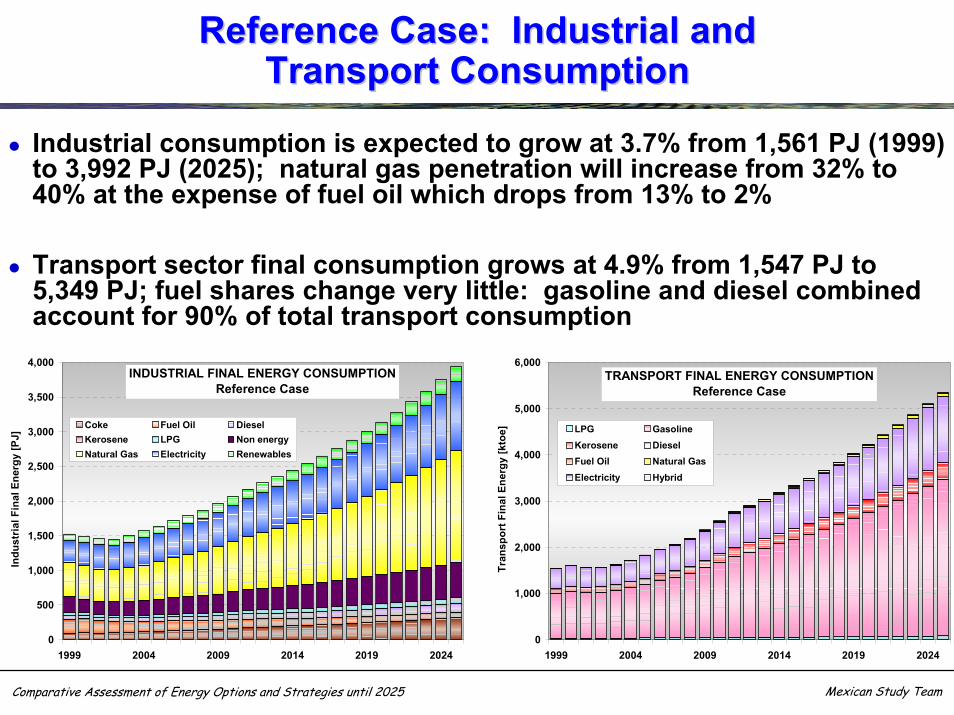

Reference Case: Industrial andReference Case: Industrial andTransport ConsumptionTransport Consumption

Industrial consumption is expected to grow at 3.7% from 1,561 PJ (1999) to 3,992 PJ (2025); natural gas penetration will increase from 32% to 40% at the expense of fuel oil which drops from 13% to 2%

Transport sector final consumption grows at 4.9% from 1,547 PJ to 5,349 PJ; fuel shares change very little: gasoline and diesel combined account for 90% of total transport consumption

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

1999 2004 2009 2014 2019 2024

Indu

stria

l Fin

al E

nerg

y [P

J]

Coke Fuel Oil DieselKerosene LPG Non energyNatural Gas Electricity Renewables

INDUSTRIAL FINAL ENERGY CONSUMPTIONReference Case

0

1,000

2,000

3,000

4,000

5,000

6,000

1999 2004 2009 2014 2019 2024

Tran

spor

t Fin

al E

nerg

y [k

toe] LPG Gasoline

Kerosene DieselFuel Oil Natural GasElectricity Hybrid

TRANSPORT FINAL ENERGY CONSUMPTIONReference Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

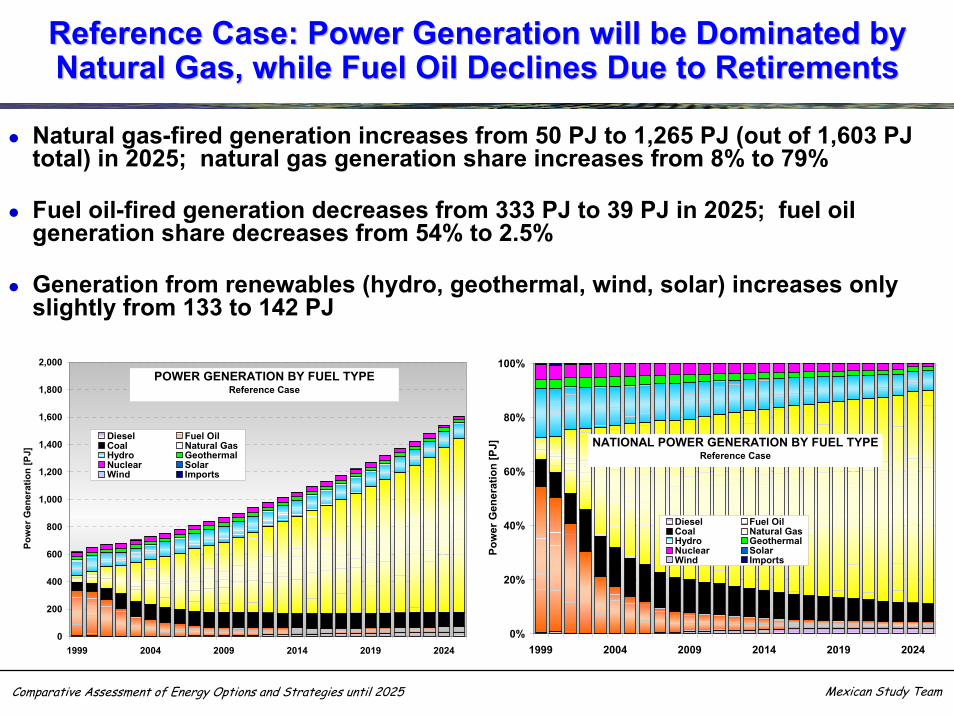

Reference Case: Power Generation will be Dominated by Reference Case: Power Generation will be Dominated by Natural Gas, while Fuel Oil Declines Due to RetirementsNatural Gas, while Fuel Oil Declines Due to Retirements

Natural gas-fired generation increases from 50 PJ to 1,265 PJ (out of 1,603 PJ total) in 2025; natural gas generation share increases from 8% to 79%

Fuel oil-fired generation decreases from 333 PJ to 39 PJ in 2025; fuel oil generation share decreases from 54% to 2.5%

Generation from renewables (hydro, geothermal, wind, solar) increases only slightly from 133 to 142 PJ

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1999 2004 2009 2014 2019 2024

Pow

er G

ener

atio

n [P

J]

Diesel Fuel OilCoal Natural GasHydro GeothermalNuclear SolarWind Imports

POWER GENERATION BY FUEL TYPEReference Case

0%

20%

40%

60%

80%

100%

1999 2004 2009 2014 2019 2024

Pow

er G

ener

atio

n [P

J]

Diesel Fuel OilCoal Natural GasHydro GeothermalNuclear SolarWind Imports

NATIONAL POWER GENERATION BY FUEL TYPEReference Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

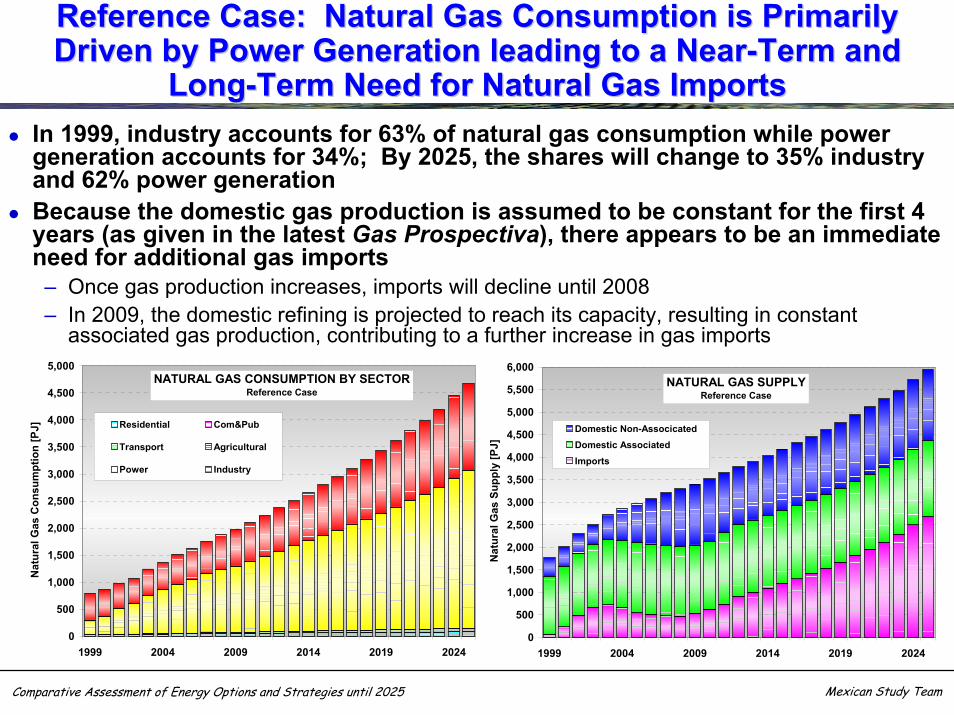

Reference Case: Natural Gas Consumption is Primarily Reference Case: Natural Gas Consumption is Primarily Driven by Power Generation leading to a NearDriven by Power Generation leading to a Near--Term and Term and

LongLong--Term Need for Natural Gas ImportsTerm Need for Natural Gas ImportsIn 1999, industry accounts for 63% of natural gas consumption while power generation accounts for 34%; By 2025, the shares will change to 35% industry and 62% power generationBecause the domestic gas production is assumed to be constant for the first 4 years (as given in the latest Gas Prospectiva), there appears to be an immediate need for additional gas imports

– Once gas production increases, imports will decline until 2008– In 2009, the domestic refining is projected to reach its capacity, resulting in constant

associated gas production, contributing to a further increase in gas imports

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1999 2004 2009 2014 2019 2024

Nat

ural

Gas

Con

sum

ptio

n [P

J] Residential Com&Pub

Transport Agricultural

Power Industry

NATURAL GAS CONSUMPTION BY SECTORReference Case

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

5,500

6,000

1999 2004 2009 2014 2019 2024

Nat

ural

Gas

Sup

ply

[PJ]

Domestic Non-AssocicatedDomestic AssociatedImports

NATURAL GAS SUPPLYReference Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

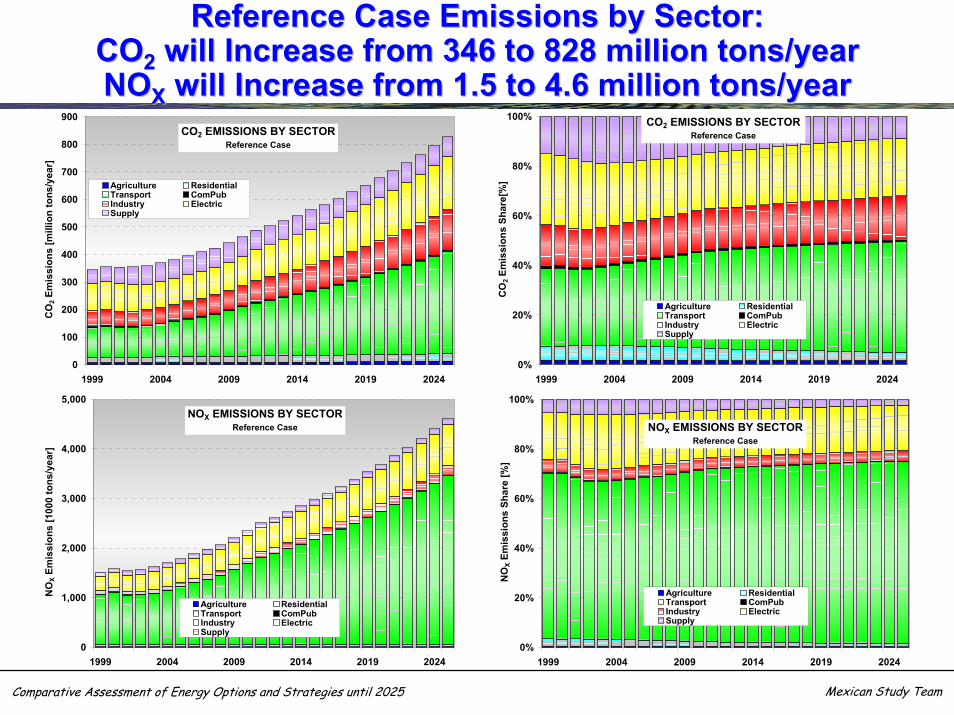

Reference Case Emissions by Sector:Reference Case Emissions by Sector:COCO22 will Increase from 346 to 828 million tons/yearwill Increase from 346 to 828 million tons/yearNONOXX will Increase from 1.5 to 4.6 million tons/yearwill Increase from 1.5 to 4.6 million tons/year

0%

20%

40%

60%

80%

100%

1999 2004 2009 2014 2019 2024

CO

2 Em

issi

ons

Shar

e[%

]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

CO2 EMISSIONS BY SECTORReference Case

0

100

200

300

400

500

600

700

800

900

1999 2004 2009 2014 2019 2024

CO

2 Em

issi

ons

[mill

ion

tons

/yea

r]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

CO2 EMISSIONS BY SECTORReference Case

0

1,000

2,000

3,000

4,000

5,000

1999 2004 2009 2014 2019 2024

NO

X Em

issi

ons

[100

0 to

ns/y

ear]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

NOX EMISSIONS BY SECTORReference Case

0%

20%

40%

60%

80%

100%

1999 2004 2009 2014 2019 2024

NO

X Em

issi

ons

Shar

e [%

]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

NOX EMISSIONS BY SECTORReference Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

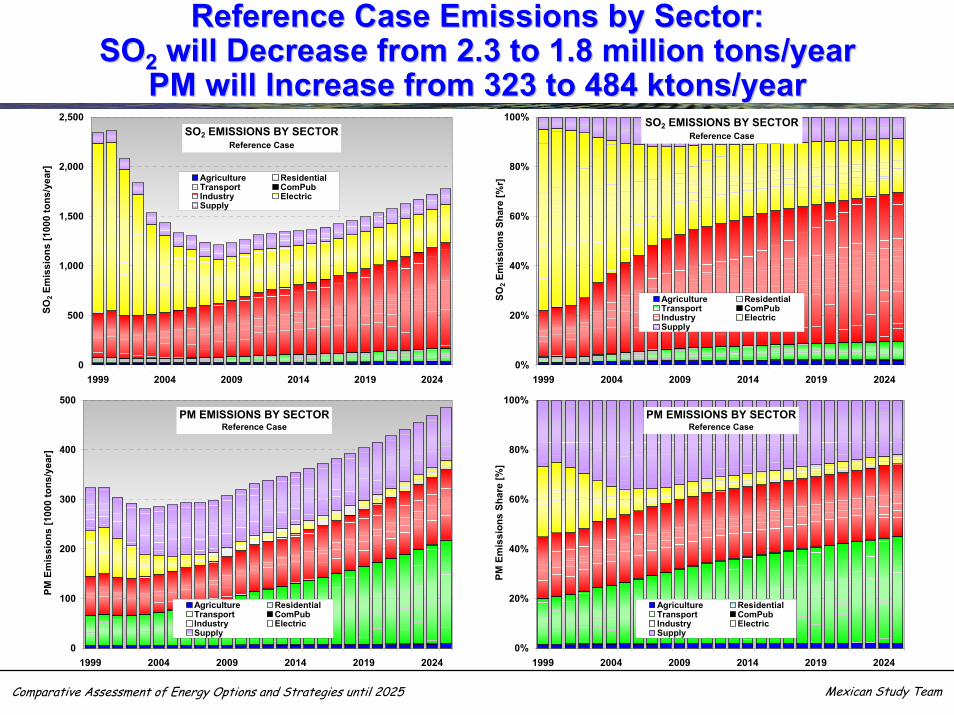

Reference Case Emissions by Sector:Reference Case Emissions by Sector:SOSO22 will Decrease from 2.3 to 1.8 million tons/yearwill Decrease from 2.3 to 1.8 million tons/year

PM will Increase from 323 to 484 ktons/yearPM will Increase from 323 to 484 ktons/year

0

500

1,000

1,500

2,000

2,500

1999 2004 2009 2014 2019 2024

SO2 E

mis

sion

s [1

000

tons

/yea

r]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

SO2 EMISSIONS BY SECTORReference Case

0%

20%

40%

60%

80%

100%

1999 2004 2009 2014 2019 2024

SO2 E

mis

sion

s Sh

are

[%r]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

SO2 EMISSIONS BY SECTORReference Case

0

100

200

300

400

500

1999 2004 2009 2014 2019 2024

PM E

mis

sion

s [1

000

tons

/yea

r]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

PM EMISSIONS BY SECTORReference Case

0%

20%

40%

60%

80%

100%

1999 2004 2009 2014 2019 2024

PM E

mis

sion

s Sh

are

[%]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

PM EMISSIONS BY SECTORReference Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

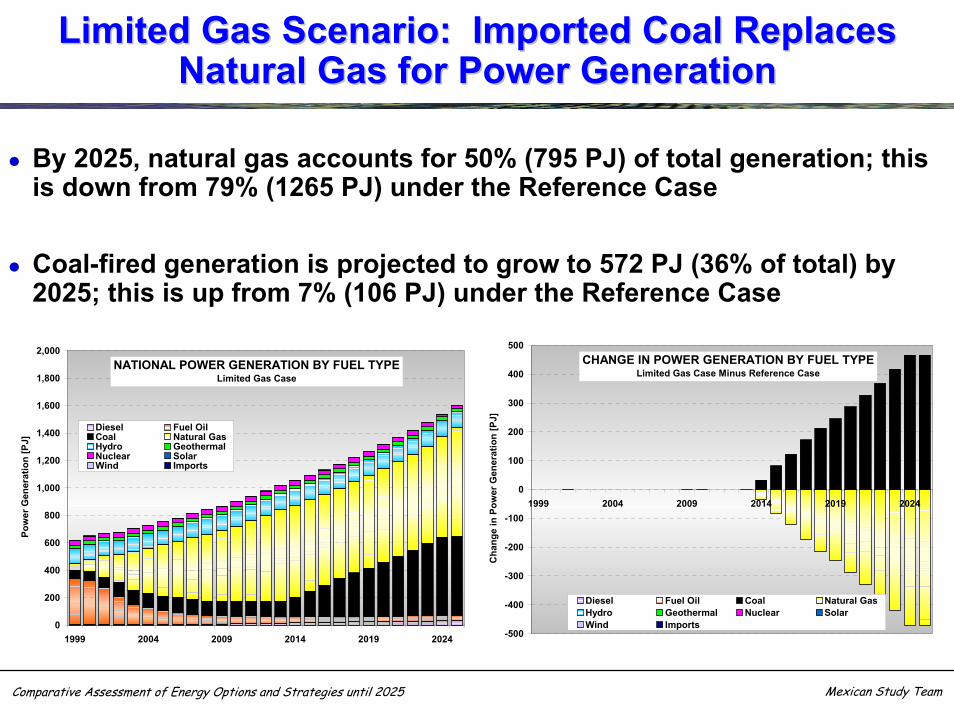

Limited Gas Scenario: Imported Coal Replaces Limited Gas Scenario: Imported Coal Replaces Natural Gas for Power Generation Natural Gas for Power Generation

By 2025, natural gas accounts for 50% (795 PJ) of total generation; this is down from 79% (1265 PJ) under the Reference Case

Coal-fired generation is projected to grow to 572 PJ (36% of total) by 2025; this is up from 7% (106 PJ) under the Reference Case

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1999 2004 2009 2014 2019 2024

Pow

er G

ener

atio

n [P

J]

Diesel Fuel OilCoal Natural GasHydro GeothermalNuclear SolarWind Imports

NATIONAL POWER GENERATION BY FUEL TYPELimited Gas Case

-500

-400

-300

-200

-100

0

100

200

300

400

500

1999 2004 2009 2014 2019 2024C

hang

e in

Pow

er G

ener

atio

n [P

J]

Diesel Fuel Oil Coal Natural GasHydro Geothermal Nuclear SolarWind Imports

CHANGE IN POWER GENERATION BY FUEL TYPELimited Gas Case Minus Reference Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

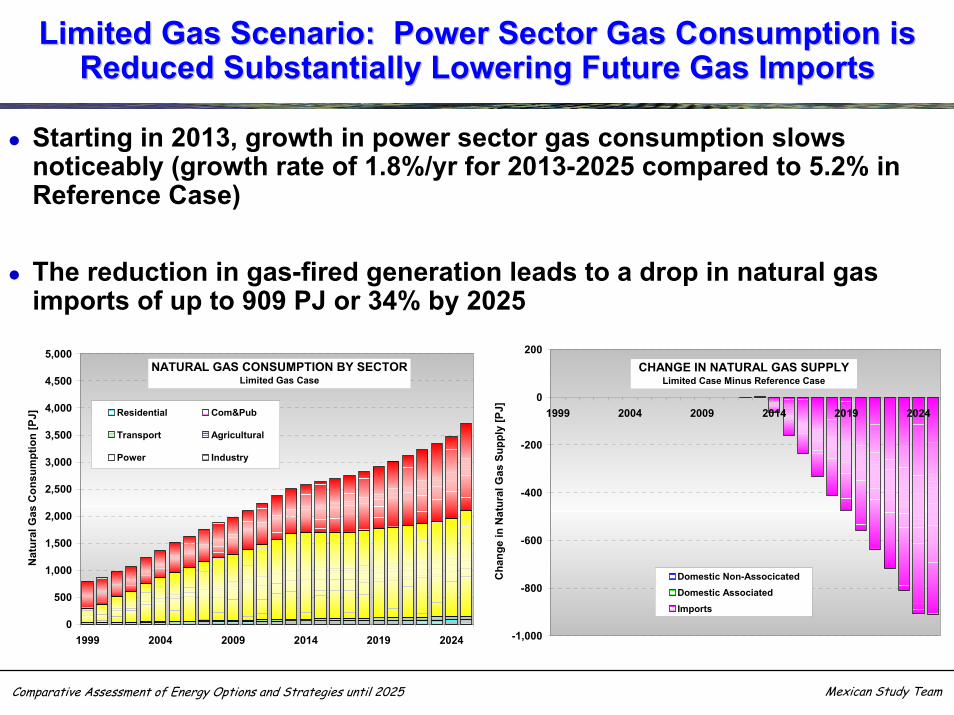

Limited Gas Scenario: Power Sector Gas Consumption is Limited Gas Scenario: Power Sector Gas Consumption is Reduced Substantially Lowering Future Gas ImportsReduced Substantially Lowering Future Gas Imports

Starting in 2013, growth in power sector gas consumption slows noticeably (growth rate of 1.8%/yr for 2013-2025 compared to 5.2% in Reference Case)

The reduction in gas-fired generation leads to a drop in natural gas imports of up to 909 PJ or 34% by 2025

-1,000

-800

-600

-400

-200

0

200

1999 2004 2009 2014 2019 2024

Cha

nge

in N

atur

al G

as S

uppl

y [P

J]

Domestic Non-AssocicatedDomestic AssociatedImports

CHANGE IN NATURAL GAS SUPPLYLimited Case Minus Reference Case

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

1999 2004 2009 2014 2019 2024

Nat

ural

Gas

Con

sum

ptio

n [P

J] Residential Com&Pub

Transport Agricultural

Power Industry

NATURAL GAS CONSUMPTION BY SECTORLimited Gas Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

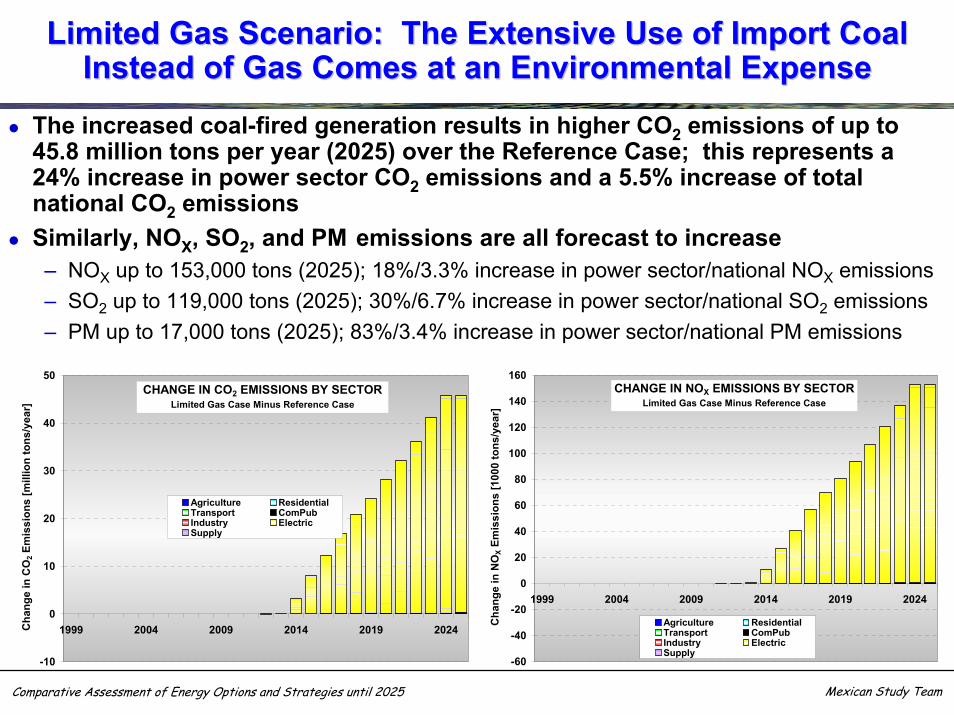

Limited Gas Scenario: The Extensive Use of Import Coal Limited Gas Scenario: The Extensive Use of Import Coal Instead of Gas Comes at an Environmental ExpenseInstead of Gas Comes at an Environmental Expense

The increased coal-fired generation results in higher CO2 emissions of up to 45.8 million tons per year (2025) over the Reference Case; this represents a 24% increase in power sector CO2 emissions and a 5.5% increase of total national CO2 emissionsSimilarly, NOX, SO2, and PM emissions are all forecast to increase

– NOX up to 153,000 tons (2025); 18%/3.3% increase in power sector/national NOX emissions– SO2 up to 119,000 tons (2025); 30%/6.7% increase in power sector/national SO2 emissions– PM up to 17,000 tons (2025); 83%/3.4% increase in power sector/national PM emissions

-10

0

10

20

30

40

50

1999 2004 2009 2014 2019 2024Cha

nge

in C

O2 E

mis

sion

s [m

illio

n to

ns/y

ear]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

CHANGE IN CO2 EMISSIONS BY SECTORLimited Gas Case Minus Reference Case

-60

-40

-20

0

20

40

60

80

100

120

140

160

1999 2004 2009 2014 2019 2024

Cha

nge

in N

OX

Emis

sion

s [1

000

tons

/yea

r]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

CHANGE IN NOX EMISSIONS BY SECTORLimited Gas Case Minus Reference Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

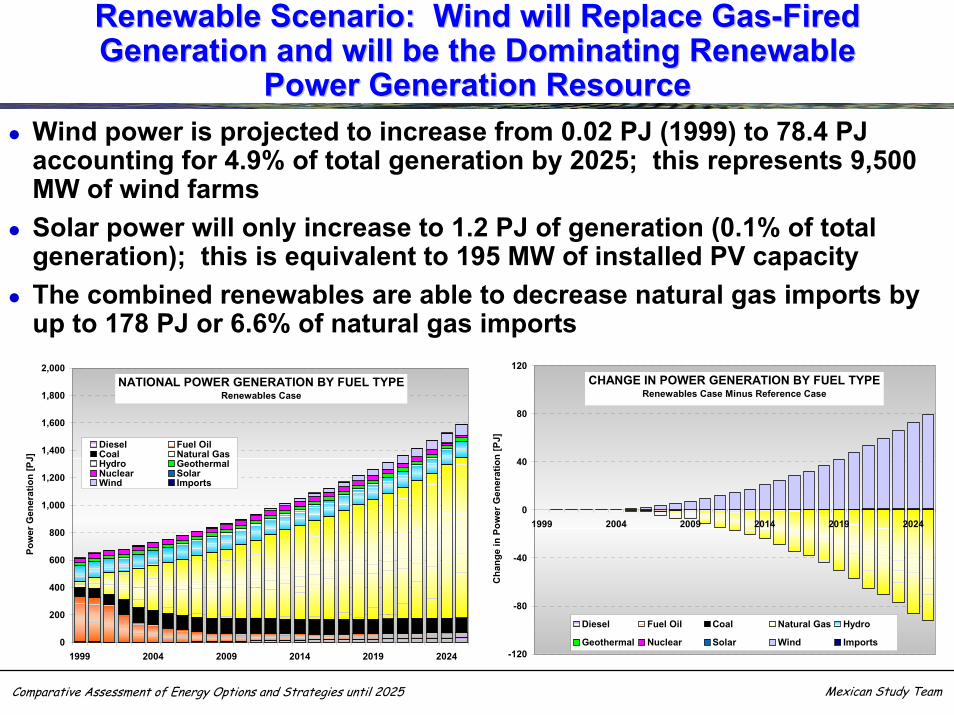

Renewable Scenario: Wind will Replace GasRenewable Scenario: Wind will Replace Gas--Fired Fired Generation and will be the Dominating RenewableGeneration and will be the Dominating Renewable

Power Generation ResourcePower Generation ResourceWind power is projected to increase from 0.02 PJ (1999) to 78.4 PJ accounting for 4.9% of total generation by 2025; this represents 9,500 MW of wind farmsSolar power will only increase to 1.2 PJ of generation (0.1% of total generation); this is equivalent to 195 MW of installed PV capacityThe combined renewables are able to decrease natural gas imports by up to 178 PJ or 6.6% of natural gas imports

-120

-80

-40

0

40

80

120

1999 2004 2009 2014 2019 2024

Cha

nge

in P

ower

Gen

erat

ion

[PJ]

Diesel Fuel Oil Coal Natural Gas Hydro

Geothermal Nuclear Solar Wind Imports

CHANGE IN POWER GENERATION BY FUEL TYPERenewables Case Minus Reference Case

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

1999 2004 2009 2014 2019 2024

Pow

er G

ener

atio

n [P

J]

Diesel Fuel OilCoal Natural GasHydro GeothermalNuclear SolarWind Imports

NATIONAL POWER GENERATION BY FUEL TYPERenewables Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

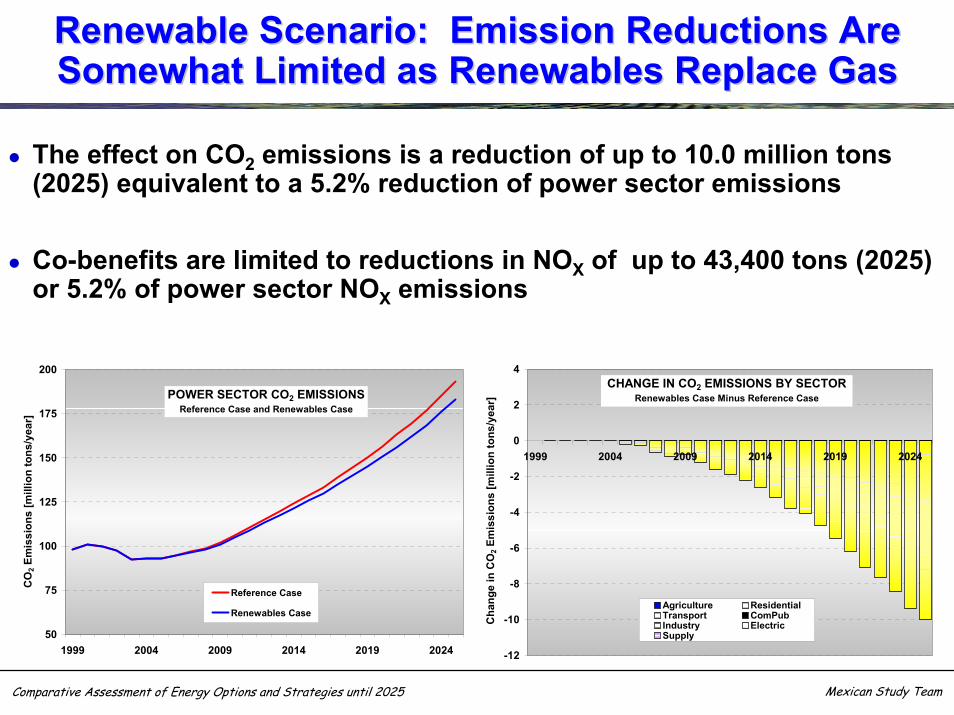

Renewable Scenario: Emission Reductions Are Renewable Scenario: Emission Reductions Are Somewhat Limited as Renewables Replace GasSomewhat Limited as Renewables Replace Gas

The effect on CO2 emissions is a reduction of up to 10.0 million tons (2025) equivalent to a 5.2% reduction of power sector emissions

Co-benefits are limited to reductions in NOX of up to 43,400 tons (2025) or 5.2% of power sector NOX emissions

-12

-10

-8

-6

-4

-2

0

2

4

1999 2004 2009 2014 2019 2024

Cha

nge

in C

O2 E

mis

sion

s [m

illio

n to

ns/y

ear]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

CHANGE IN CO2 EMISSIONS BY SECTORRenewables Case Minus Reference Case

50

75

100

125

150

175

200

1999 2004 2009 2014 2019 2024

CO

2 Em

issi

ons

[mill

ion

tons

/yea

r]

Reference Case

Renewables Case

POWER SECTOR CO2 EMISSIONSReference Case and Renewables Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

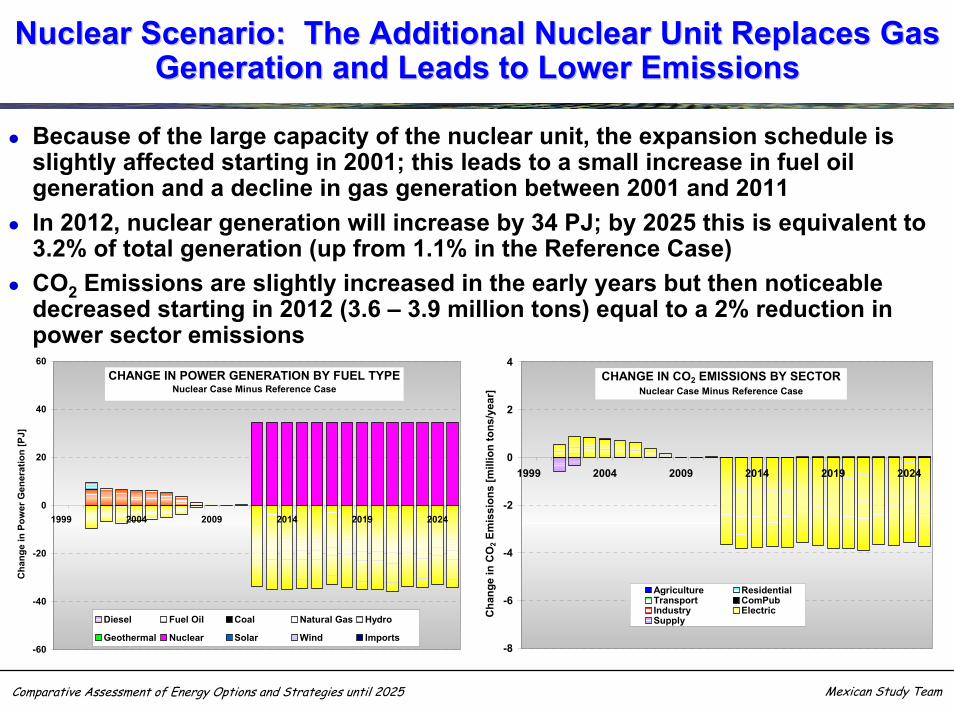

Nuclear Scenario: The Additional Nuclear Unit Replaces Gas Nuclear Scenario: The Additional Nuclear Unit Replaces Gas Generation and Leads to Lower EmissionsGeneration and Leads to Lower Emissions

Because of the large capacity of the nuclear unit, the expansion schedule is slightly affected starting in 2001; this leads to a small increase in fuel oil generation and a decline in gas generation between 2001 and 2011In 2012, nuclear generation will increase by 34 PJ; by 2025 this is equivalent to 3.2% of total generation (up from 1.1% in the Reference Case)CO2 Emissions are slightly increased in the early years but then noticeable decreased starting in 2012 (3.6 – 3.9 million tons) equal to a 2% reduction in power sector emissions

-60

-40

-20

0

20

40

60

1999 2004 2009 2014 2019 2024

Cha

nge

in P

ower

Gen

erat

ion

[PJ]

Diesel Fuel Oil Coal Natural Gas Hydro

Geothermal Nuclear Solar Wind Imports

CHANGE IN POWER GENERATION BY FUEL TYPENuclear Case Minus Reference Case

-8

-6

-4

-2

0

2

4

1999 2004 2009 2014 2019 2024C

hang

e in

CO

2 Em

issi

ons

[mill

ion

tons

/yea

r]

Agriculture ResidentialTransport ComPubIndustry ElectricSupply

CHANGE IN CO2 EMISSIONS BY SECTORNuclear Case Minus Reference Case

Comparative Assessment of Energy Options and Strategies until 2025 Mexican Study Team

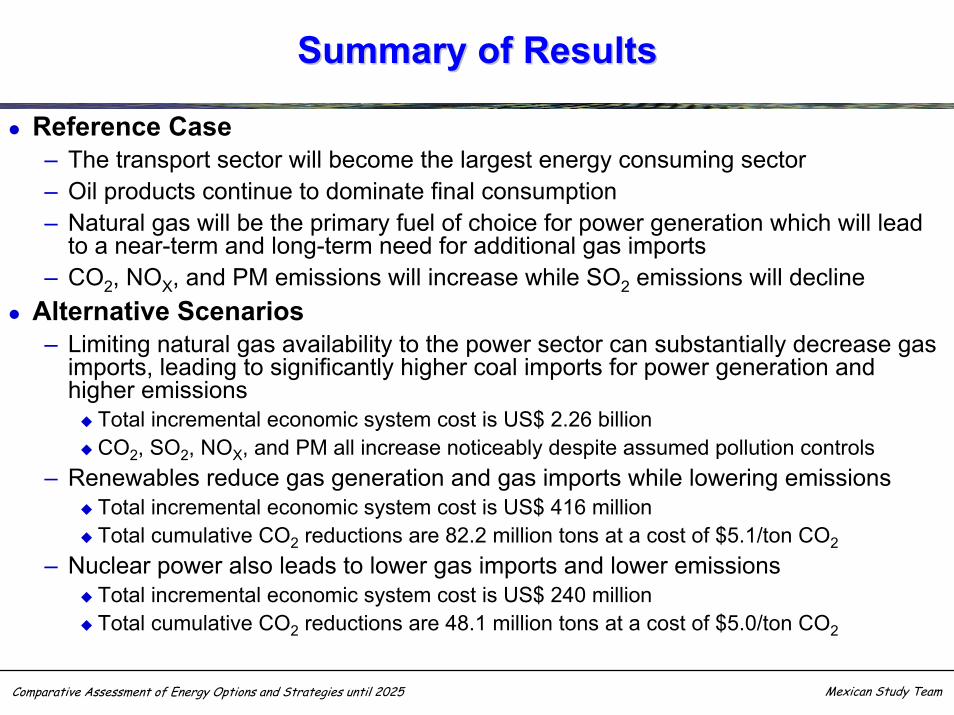

Summary of ResultsSummary of Results

Reference Case– The transport sector will become the largest energy consuming sector– Oil products continue to dominate final consumption– Natural gas will be the primary fuel of choice for power generation which will lead

to a near-term and long-term need for additional gas imports– CO2, NOX, and PM emissions will increase while SO2 emissions will decline

Alternative Scenarios– Limiting natural gas availability to the power sector can substantially decrease gas

imports, leading to significantly higher coal imports for power generation and higher emissions

Total incremental economic system cost is US$ 2.26 billionCO2, SO2, NOX, and PM all increase noticeably despite assumed pollution controls

– Renewables reduce gas generation and gas imports while lowering emissionsTotal incremental economic system cost is US$ 416 millionTotal cumulative CO2 reductions are 82.2 million tons at a cost of $5.1/ton CO2

– Nuclear power also leads to lower gas imports and lower emissionsTotal incremental economic system cost is US$ 240 millionTotal cumulative CO2 reductions are 48.1 million tons at a cost of $5.0/ton CO2