Embed Size (px)

Citation preview

00500/CF

Company introduction

Dr Carl Firth - Chairman & CEO

May 2017

00500/CF

Disclaimer

All materials and information set out herein are for reference only and whilst we make every effort to ensure accuracy and completeness, we cannot guarantee this. We make no recommendation as to the competence or suitability of persons or entities referenced herein (if any). Nothing herein constitutes an invitation or offer to invest in or deal in the securities of ASLAN. Anyone considering investment in ASLAN should refer to the information officially published the Taiwan Stock Exchange Market Observation System (MOPS).

All forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by this cautionary statement. Readers are cautioned not to place undue reliance on such forward-looking statements, which are inherently unreliable, and you should not rely on them. Any such forward-looking statement will have been based on ASLAN’s expectations, assumptions, estimates and projections about future events on the date(s) made. Actual outcomes are subject to numerous risks and uncertainties, many of which relate to factors beyond ASLAN’s control, that could cause them to differ materially from those expressed in a forward-looking statement. ASLAN has no obligation to update or otherwise revise any forward-looking statements to reflect the occurrence of unanticipated events or for any other reason.

2

00500/CF

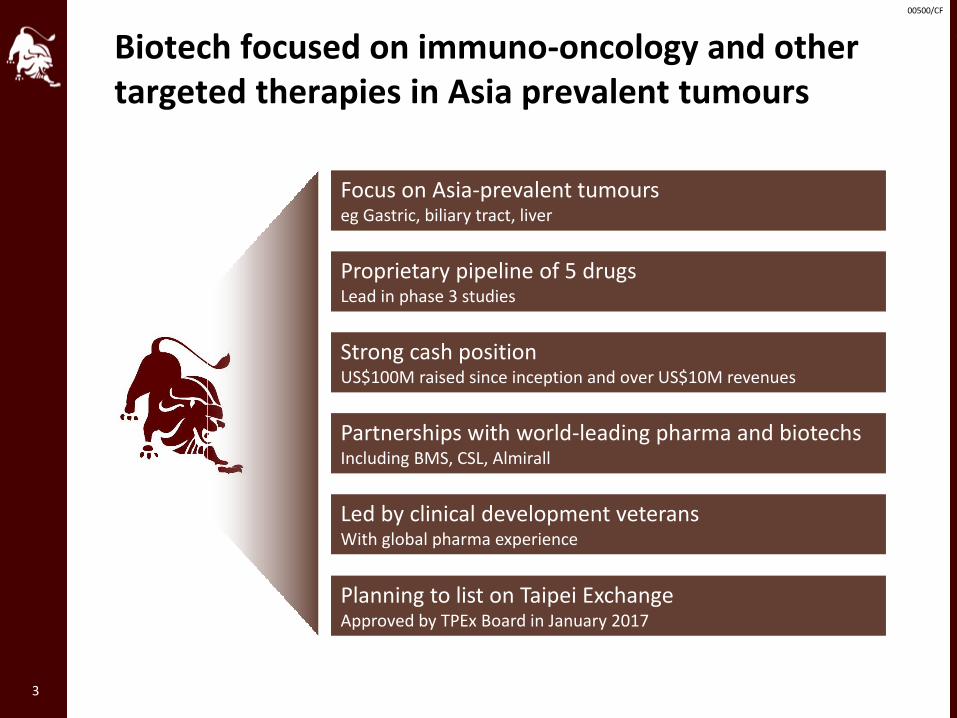

Biotech focused on immuno-oncology and other targeted therapies in Asia prevalent tumours

3

Focus on Asia-prevalent tumourseg Gastric, biliary tract, liver

Proprietary pipeline of 5 drugs Lead in phase 3 studies

Partnerships with world-leading pharma and biotechsIncluding BMS, CSL, Almirall

Led by clinical development veterans With global pharma experience

Strong cash positionUS$100M raised since inception and over US$10M revenues

Planning to list on Taipei ExchangeApproved by TPEx Board in January 2017

00500/CF

Company introduction

1. Company overview

2. Our portfolio

3. Financials

4. Comparable companies

5. Future milestones

4

00500/CF

1. COMPANY OVERVIEW

5

00500/CF

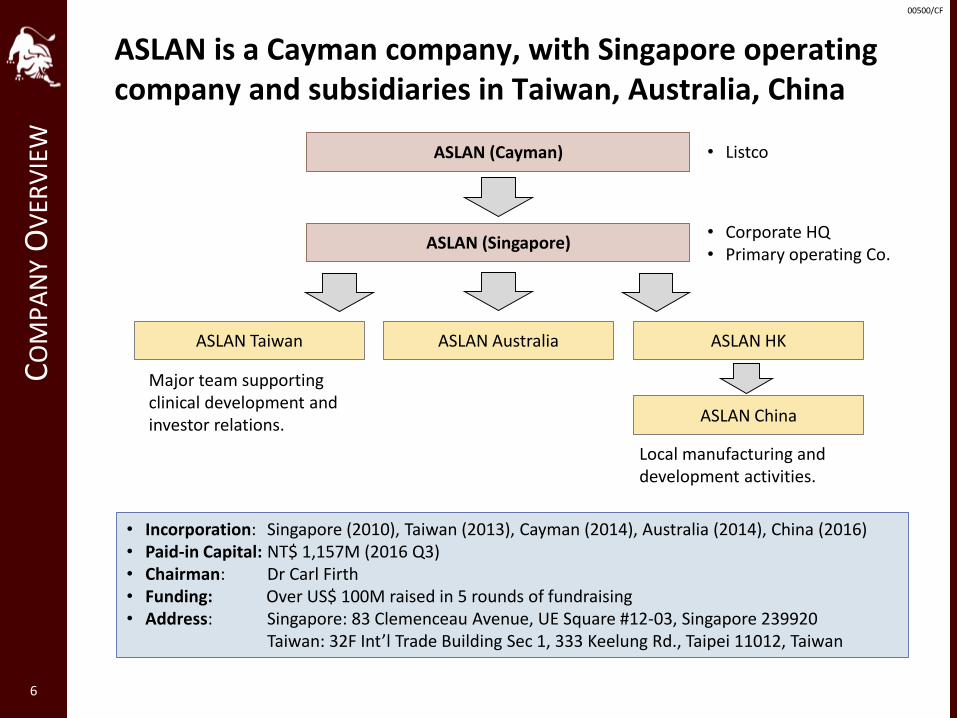

ASLAN is a Cayman company, with Singapore operating company and subsidiaries in Taiwan, Australia, China

6

ASLAN Taiwan

CO

MP

AN

YO

VER

VIE

W

ASLAN HK

ASLAN (Singapore)

Major team supporting clinical development and investor relations.

• Corporate HQ• Primary operating Co.

Local manufacturing and development activities.

ASLAN (Cayman) • Listco

ASLAN Australia

• Incorporation: Singapore (2010), Taiwan (2013), Cayman (2014), Australia (2014), China (2016)• Paid-in Capital: NT$ 1,157M (2016 Q3)• Chairman: Dr Carl Firth• Funding: Over US$ 100M raised in 5 rounds of fundraising• Address: Singapore: 83 Clemenceau Avenue, UE Square #12-03, Singapore 239920

Taiwan: 32F Int’l Trade Building Sec 1, 333 Keelung Rd., Taipei 11012, Taiwan

ASLAN China

00500/CF

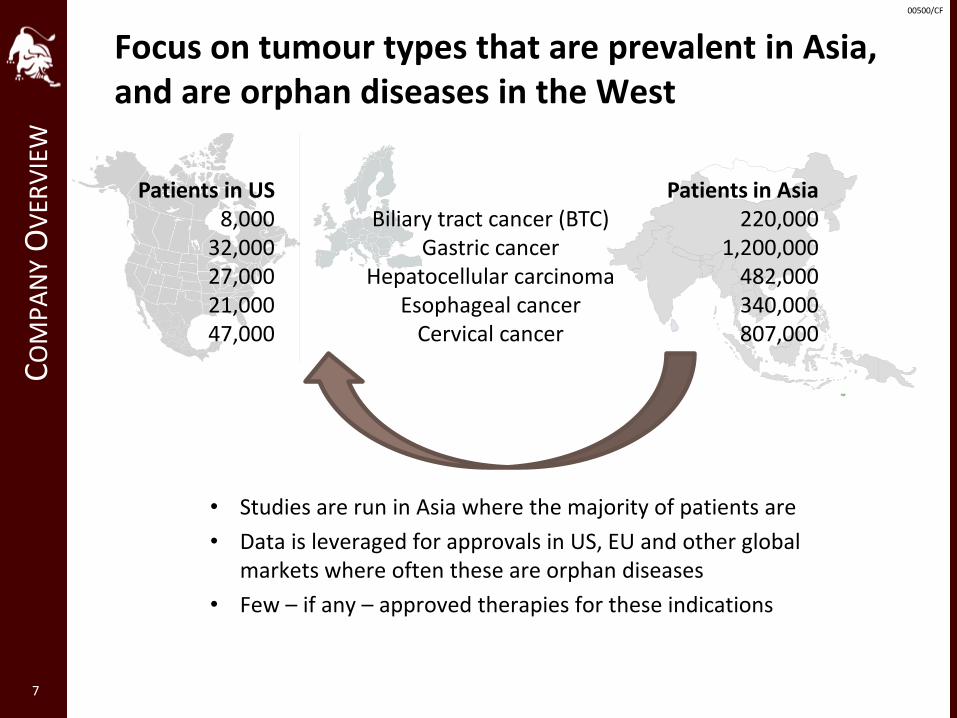

Focus on tumour types that are prevalent in Asia, and are orphan diseases in the West

CO

MP

AN

YO

VER

VIE

W

• Studies are run in Asia where the majority of patients are

• Data is leveraged for approvals in US, EU and other global markets where often these are orphan diseases

• Few – if any – approved therapies for these indications

7

Patients in US Patients in Asia8,000 Biliary tract cancer (BTC) 220,000

32,000 Gastric cancer 1,200,00027,000 Hepatocellular carcinoma 482,00021,000 Esophageal cancer 340,00047,000 Cervical cancer 807,000

00500/CF

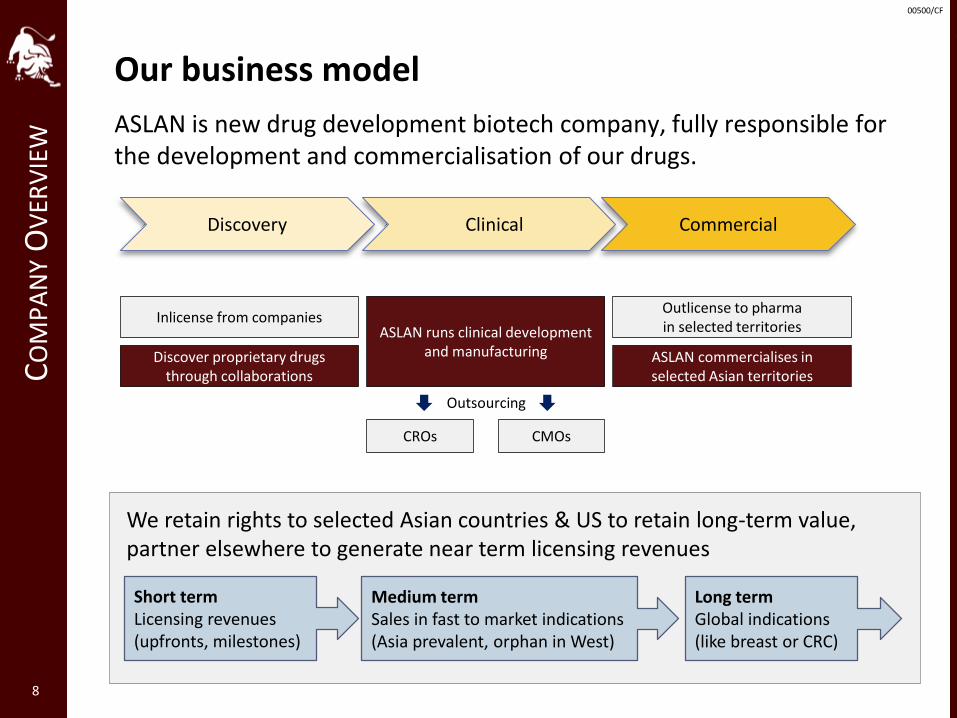

Our business modelC

OM

PA

NY

OV

ERV

IEW

ASLAN is new drug development biotech company, fully responsible for the development and commercialisation of our drugs.

8

We retain rights to selected Asian countries & US to retain long-term value, partner elsewhere to generate near term licensing revenues

Short termLicensing revenues (upfronts, milestones)

Medium termSales in fast to market indications (Asia prevalent, orphan in West)

Long termGlobal indications (like breast or CRC)

Discovery Clinical Commercial

Inlicense from companies

Discover proprietary drugs through collaborations

Outlicense to pharma in selected territories

ASLAN commercialises in selected Asian territories

ASLAN runs clinical development and manufacturing

CROs CMOs

Outsourcing

00500/CF

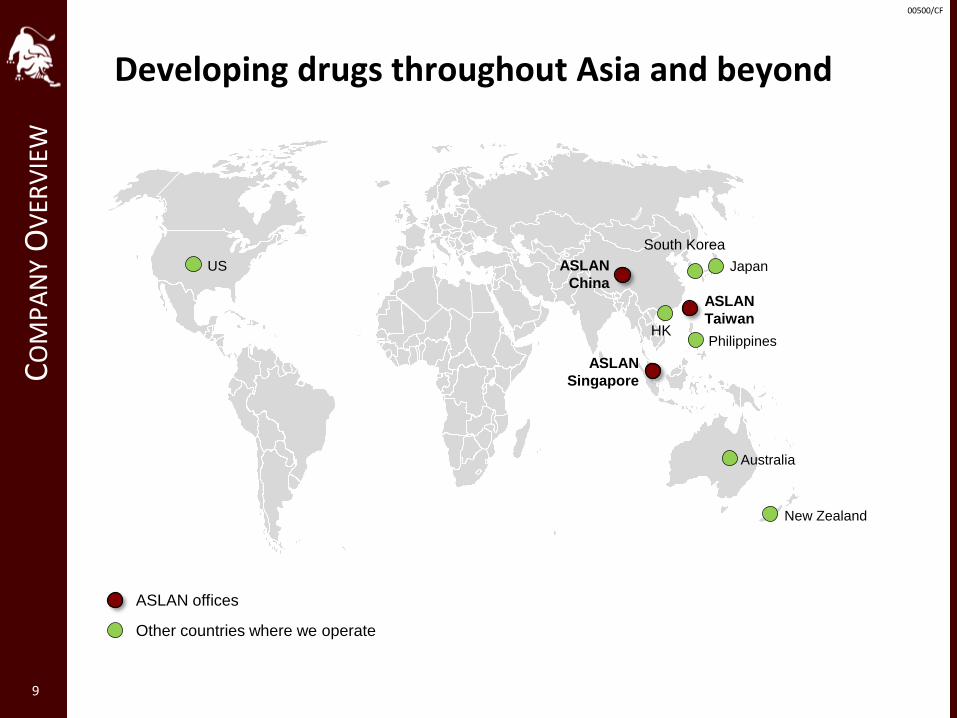

Developing drugs throughout Asia and beyondC

OM

PA

NY

OV

ERV

IEW

9

ASLAN offices

Other countries where we operate

ASLAN

Singapore

ASLAN

Taiwan

ASLAN

China

New Zealand

HK

South Korea

Japan

Philippines

US

Australia

00500/CF

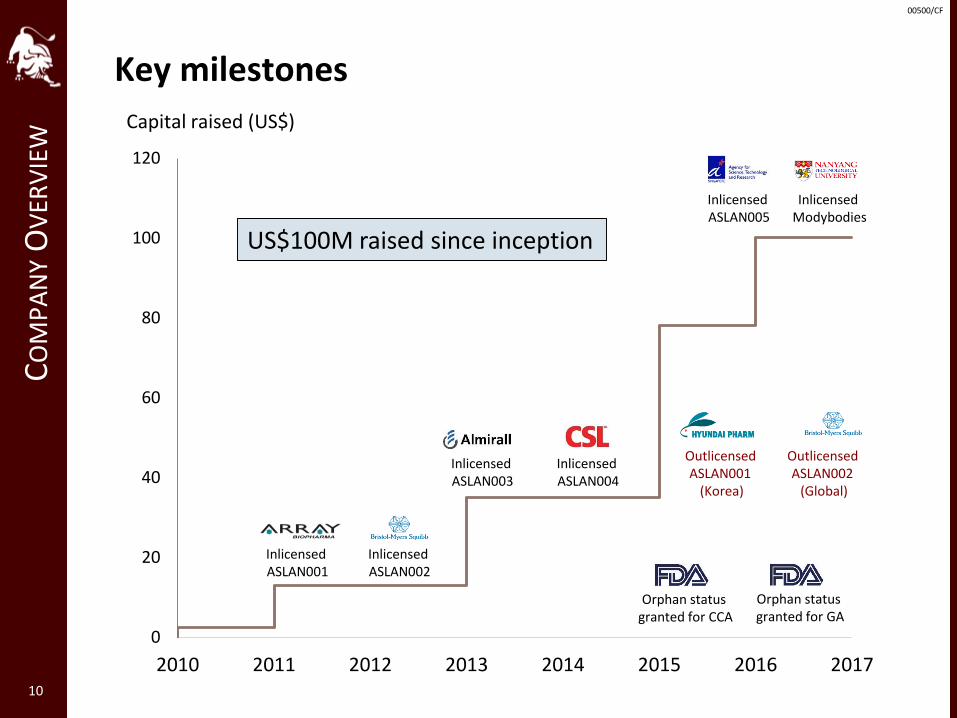

Key milestonesC

OM

PA

NY

OV

ERV

IEW

10

0

20

40

60

80

100

120

2010 2011 2012 2013 2014 2015 2016 2017

Capital raised (US$)

InlicensedASLAN001

InlicensedASLAN002

InlicensedASLAN003

InlicensedASLAN004

InlicensedASLAN005

InlicensedModybodies

OutlicensedASLAN001

(Korea)

OutlicensedASLAN002

(Global)

Orphan status granted for CCA

Orphan status granted for GA

US$100M raised since inception

00500/CF

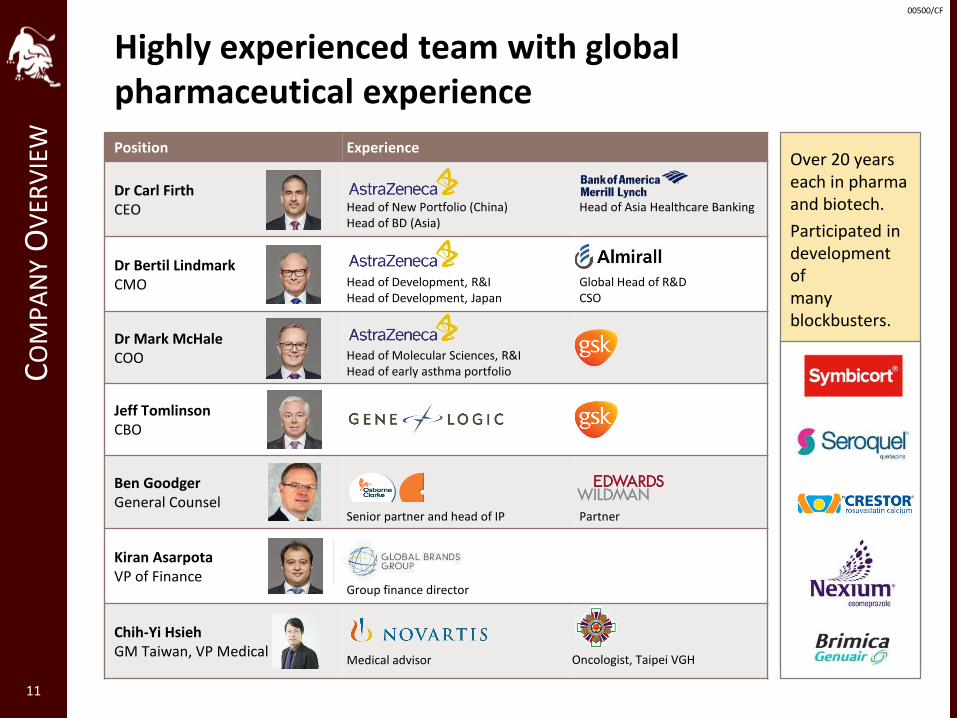

Over 20 years each in pharma and biotech.

Participated in development of many blockbusters.

Highly experienced team with global pharmaceutical experience

11

CO

MP

AN

YO

VER

VIE

W Position Experience

Dr Carl FirthCEO Head of New Portfolio (China)

Head of BD (Asia)Head of Asia Healthcare Banking

Dr Bertil LindmarkCMO Head of Development, R&I

Head of Development, JapanGlobal Head of R&DCSO

Dr Mark McHaleCOO Head of Molecular Sciences, R&I

Head of early asthma portfolio

Jeff TomlinsonCBO

Ben GoodgerGeneral Counsel

Senior partner and head of IP Partner

Kiran AsarpotaVP of Finance

Group finance director

Chih-Yi HsiehGM Taiwan, VP Medical

Medical advisor Oncologist, Taipei VGH

00500/CF

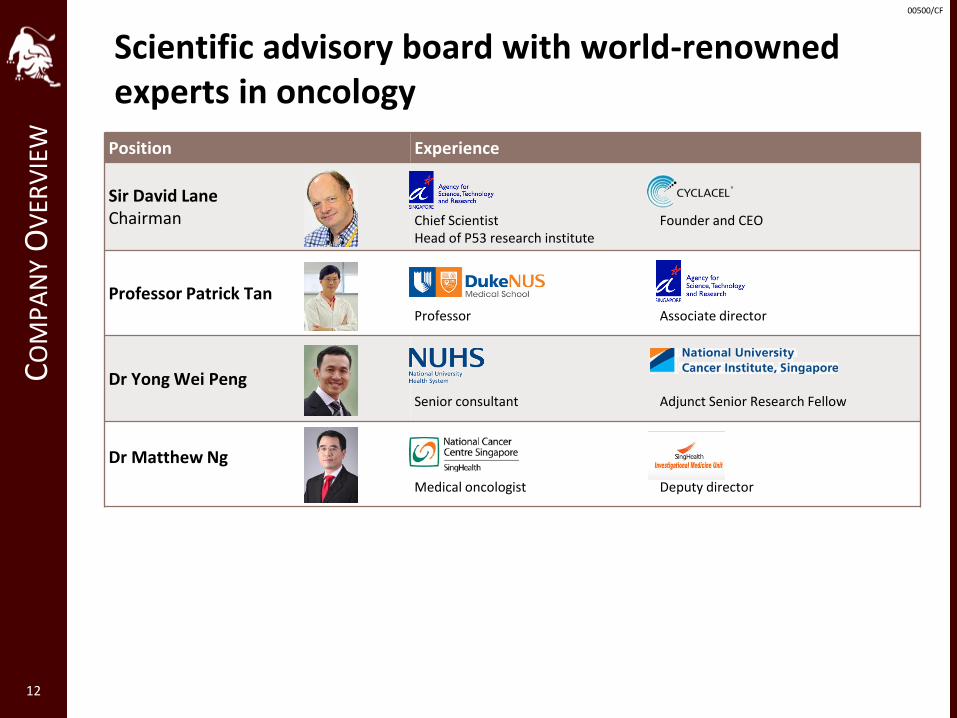

Scientific advisory board with world-renowned experts in oncology

12

CO

MP

AN

YO

VER

VIE

W Position Experience

Sir David LaneChairman Chief Scientist

Head of P53 research instituteFounder and CEO

Professor Patrick TanProfessor Associate director

Dr Yong Wei PengSenior consultant Adjunct Senior Research Fellow

Dr Matthew Ng

Medical oncologist Deputy director

00500/CF

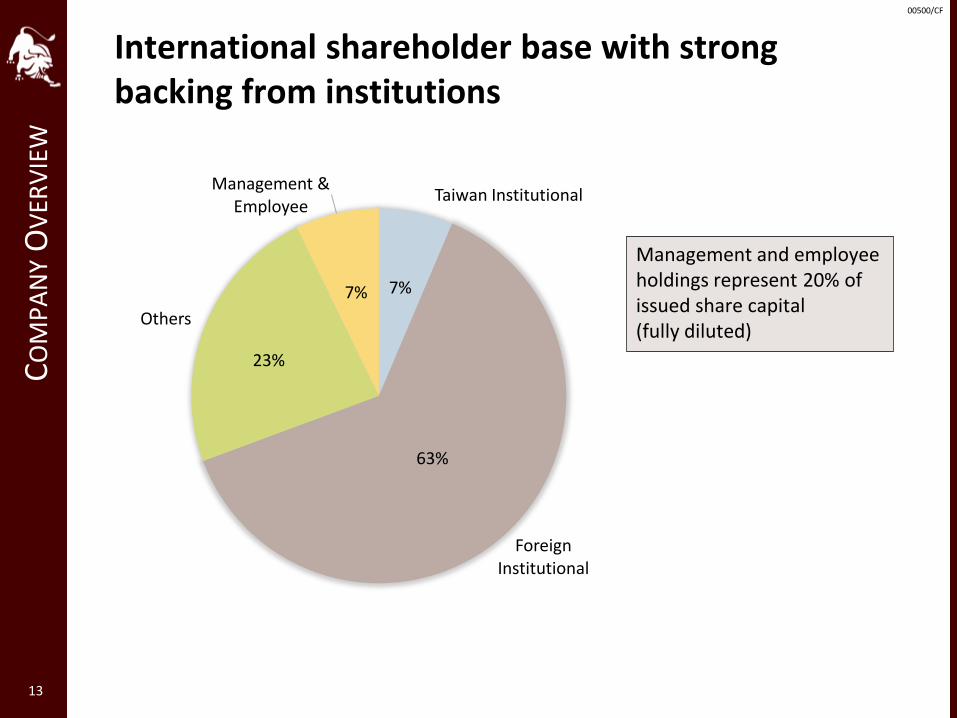

International shareholder base with strong backing from institutions

CO

MP

AN

YO

VER

VIE

W

Management and employee holdings represent 20% of issued share capital (fully diluted)

13

Taiwan Institutional

Foreign Institutional

Others

Management & Employee

63%

23%

7% 7%

00500/CF

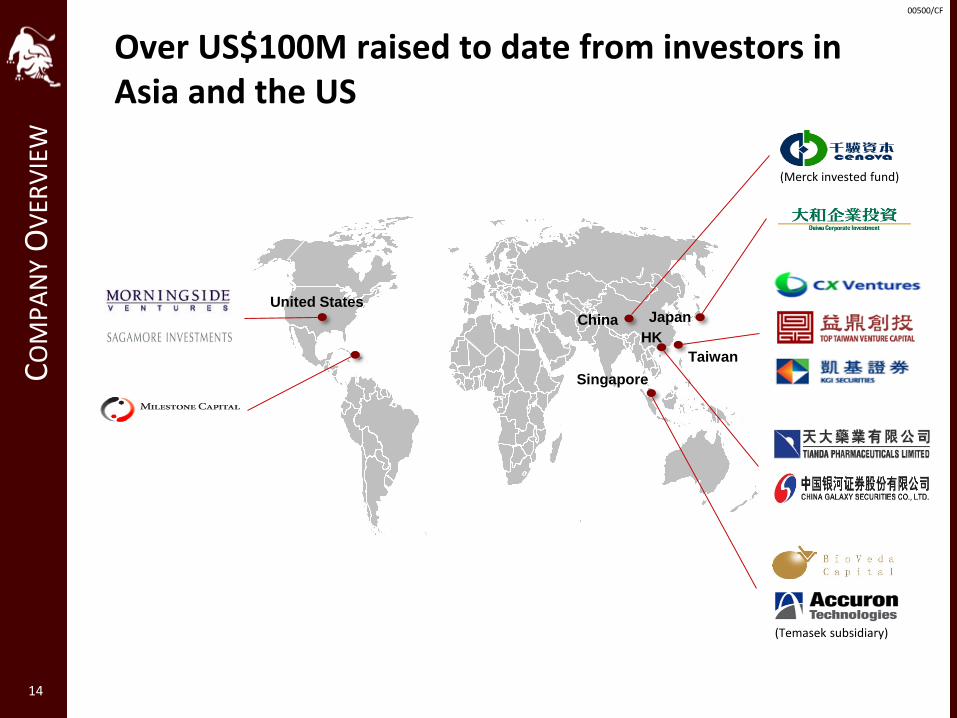

Over US$100M raised to date from investors in Asia and the US

CO

MP

AN

YO

VER

VIE

W

14

United StatesJapan

Singapore

Taiwan

HK

China

(Temasek subsidiary)

(Merck invested fund)

00500/CF

2. OUR PORTFOLIO

15

00500/CF

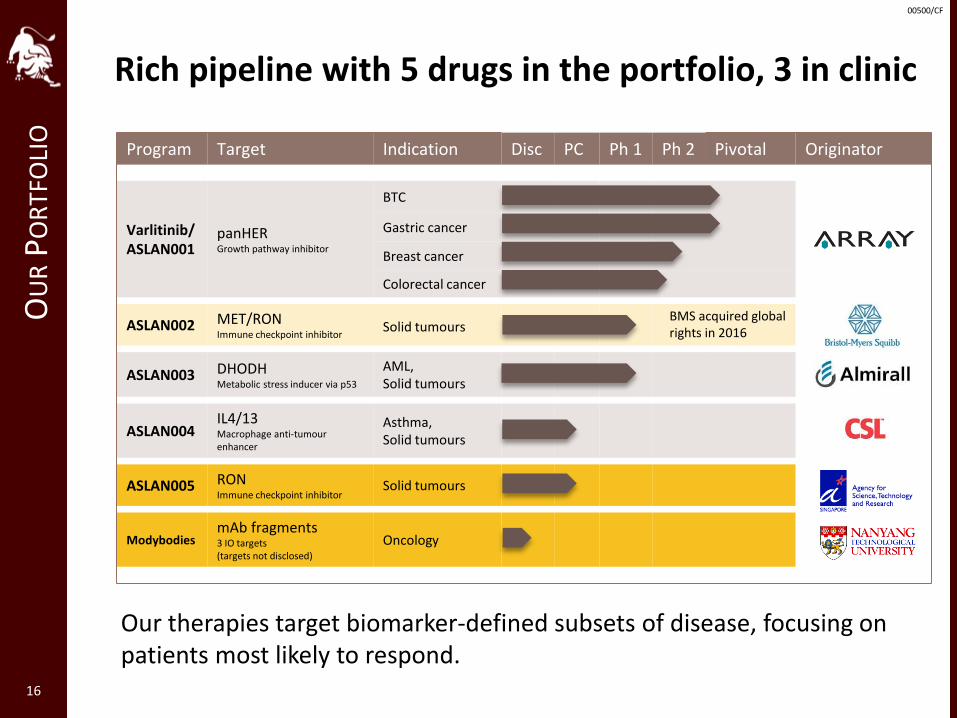

Rich pipeline with 5 drugs in the portfolio, 3 in clinic

16

Program Target Indication Disc PC Ph 1 Ph 2 Pivotal Originator

Varlitinib/ASLAN001

panHERGrowth pathway inhibitor

BTC

Gastric cancer

Breast cancer

Colorectal cancer

ASLAN002 MET/RONImmune checkpoint inhibitor

Solid tumours

ASLAN003 DHODHMetabolic stress inducer via p53

AML,Solid tumours

ASLAN004IL4/13Macrophage anti-tumour enhancer

Asthma, Solid tumours

ASLAN005 RONImmune checkpoint inhibitor

Solid tumours

ModybodiesmAb fragments3 IO targets(targets not disclosed)

Oncology

OU

RP

OR

TFO

LIO

BMS acquired global rights in 2016

Our therapies target biomarker-defined subsets of disease, focusing on patients most likely to respond.

00500/CF

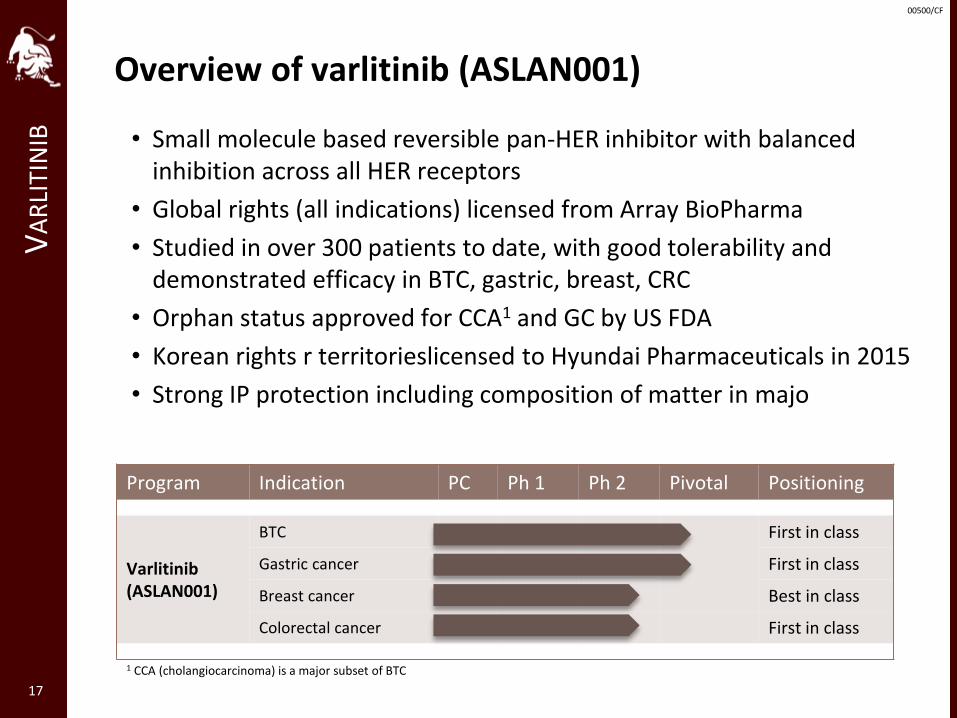

Overview of varlitinib (ASLAN001)V

AR

LITI

NIB • Small molecule based reversible pan-HER inhibitor with balanced

inhibition across all HER receptors

• Global rights (all indications) licensed from Array BioPharma

• Studied in over 300 patients to date, with good tolerability and demonstrated efficacy in BTC, gastric, breast, CRC

• Orphan status approved for CCA1 and GC by US FDA

• Korean rights r territorieslicensed to Hyundai Pharmaceuticals in 2015

• Strong IP protection including composition of matter in majo

17

Program Indication PC Ph 1 Ph 2 Pivotal Positioning

Varlitinib(ASLAN001)

BTC First in class

Gastric cancer First in class

Breast cancer Best in class

Colorectal cancer First in class

1 CCA (cholangiocarcinoma) is a major subset of BTC

00500/CF

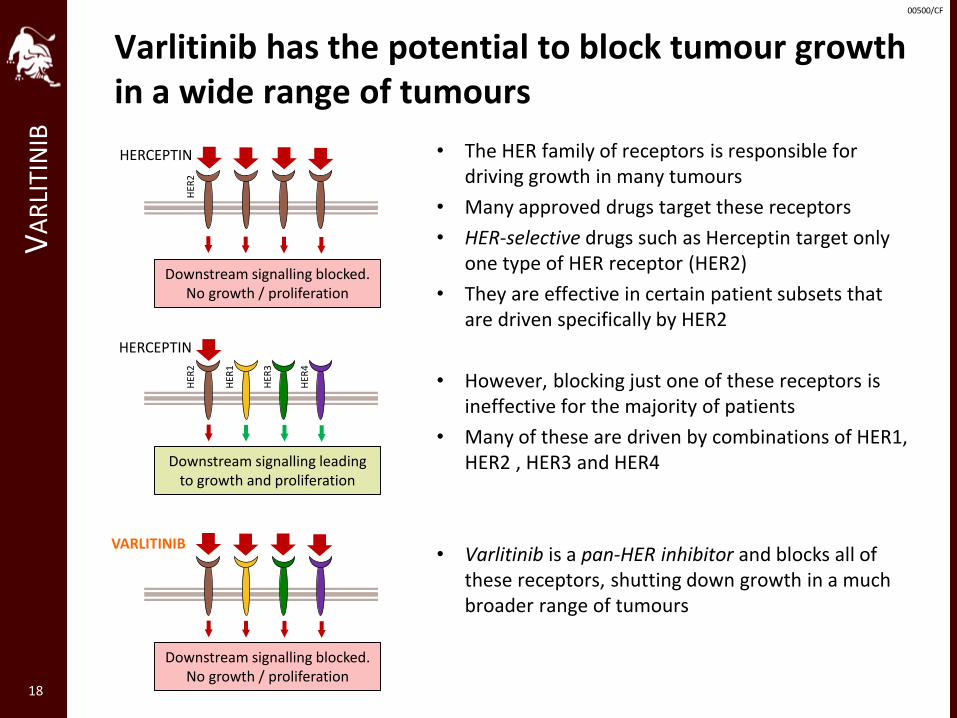

Varlitinib has the potential to block tumour growth in a wide range of tumours

VA

RLI

TIN

IB

• The HER family of receptors is responsible for driving growth in many tumours

• Many approved drugs target these receptors

• HER-selective drugs such as Herceptin target only one type of HER receptor (HER2)

• They are effective in certain patient subsets that are driven specifically by HER2

• However, blocking just one of these receptors is ineffective for the majority of patients

• Many of these are driven by combinations of HER1, HER2 , HER3 and HER4

• Varlitinib is a pan-HER inhibitor and blocks all of these receptors, shutting down growth in a much broader range of tumours

18

Downstream signalling leading to growth and proliferation

Downstream signalling blocked.No growth / proliferation

HERCEPTIN

HERCEPTIN

Downstream signalling blocked. No growth / proliferation

VARLITINIB

HER

2H

ER2

HER

1

HER

3

HER

4

00500/CF

-0%

-21%

-29%

-41%-47%

49%

33%

5%

-0%-4%

-11%-16%

-37%

-65%

-87%

12% 10% 10%

-4%-7%

-13%

-48%

-69%

29%

2% 0%

-4% -4%

-19%

-27%

(100%)

(80%)

(60%)

(40%)

(20%)

0%

20%

40%

60%

VA

RLI

TIN

IB

19

Max

imu

m t

um

ou

rsh

rin

kage

(%

)

GastricBTCColorectalOther

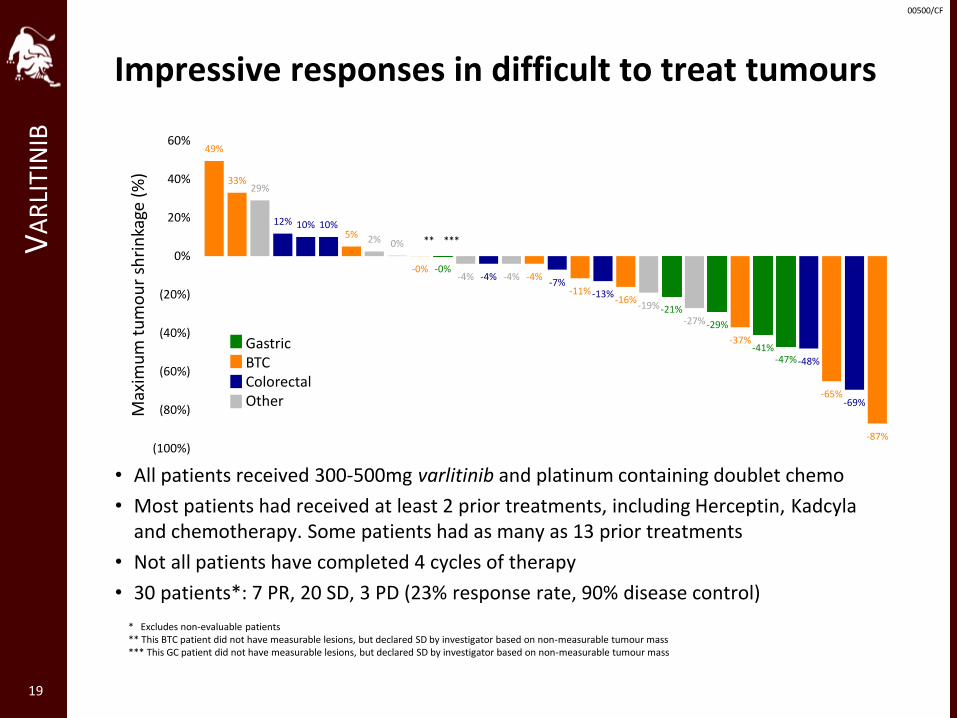

• All patients received 300-500mg varlitinib and platinum containing doublet chemo

• Most patients had received at least 2 prior treatments, including Herceptin, Kadcylaand chemotherapy. Some patients had as many as 13 prior treatments

• Not all patients have completed 4 cycles of therapy

• 30 patients*: 7 PR, 20 SD, 3 PD (23% response rate, 90% disease control)

* Excludes non-evaluable patients** This BTC patient did not have measurable lesions, but declared SD by investigator based on non-measurable tumour mass*** This GC patient did not have measurable lesions, but declared SD by investigator based on non-measurable tumour mass

** ***

Impressive responses in difficult to treat tumours

00500/CF

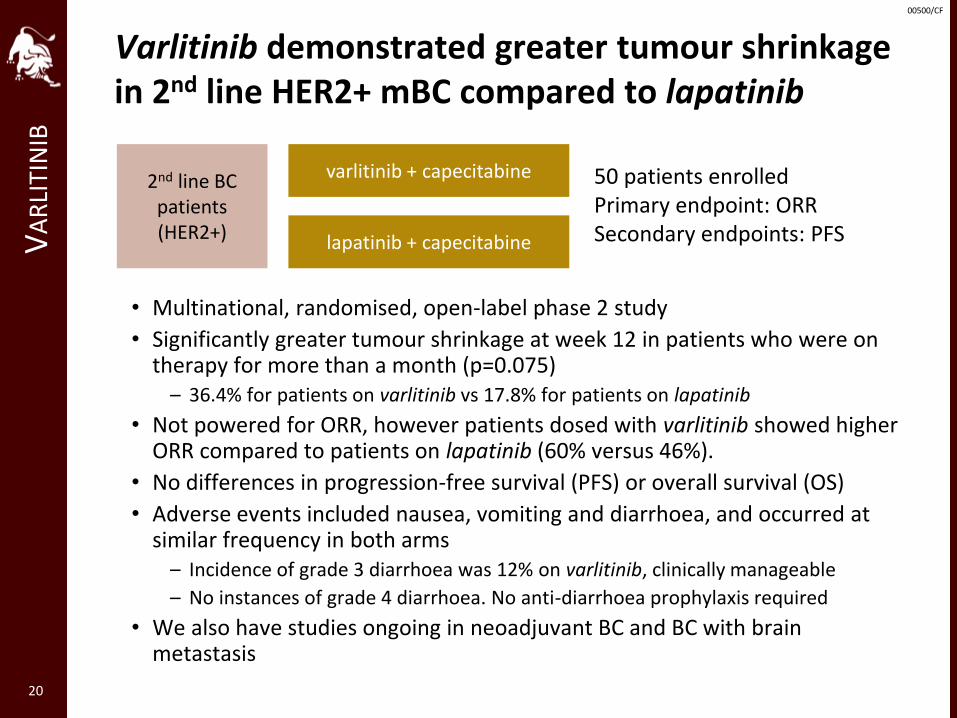

Varlitinib demonstrated greater tumour shrinkage in 2nd line HER2+ mBC compared to lapatinib

VA

RLI

TIN

IB

• Multinational, randomised, open-label phase 2 study

• Significantly greater tumour shrinkage at week 12 in patients who were on therapy for more than a month (p=0.075)

– 36.4% for patients on varlitinib vs 17.8% for patients on lapatinib

• Not powered for ORR, however patients dosed with varlitinib showed higher ORR compared to patients on lapatinib (60% versus 46%).

• No differences in progression-free survival (PFS) or overall survival (OS)

• Adverse events included nausea, vomiting and diarrhoea, and occurred at similar frequency in both arms

– Incidence of grade 3 diarrhoea was 12% on varlitinib, clinically manageable

– No instances of grade 4 diarrhoea. No anti-diarrhoea prophylaxis required

• We also have studies ongoing in neoadjuvant BC and BC with brain metastasis

20

2nd line BC patients(HER2+)

varlitinib + capecitabine

lapatinib + capecitabine

50 patients enrolledPrimary endpoint: ORRSecondary endpoints: PFS

00500/CF

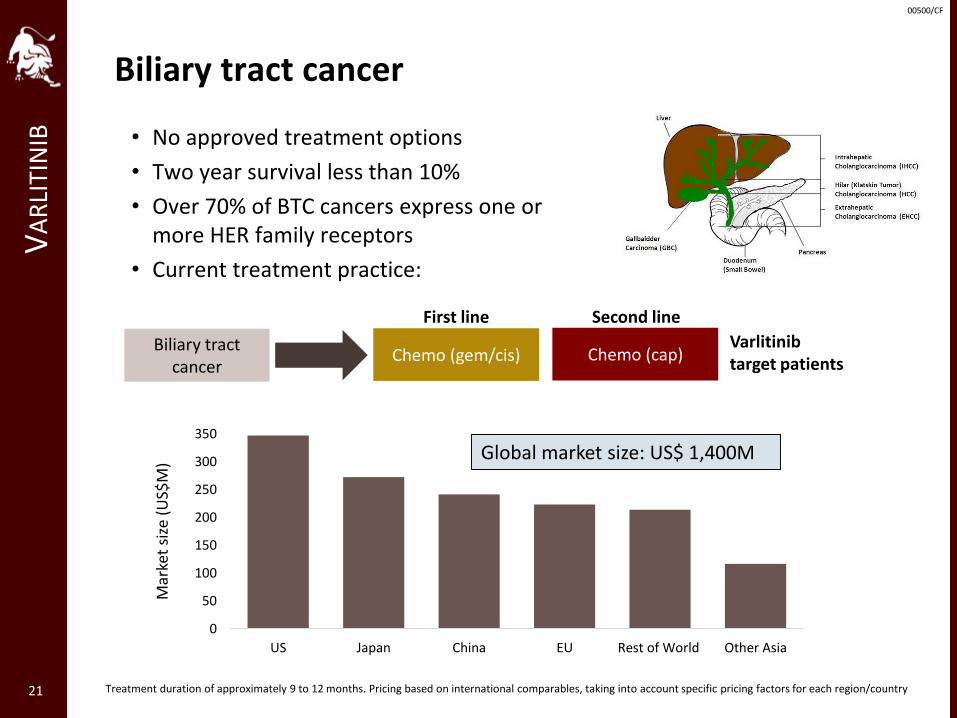

Biliary tract cancerV

AR

LITI

NIB • No approved treatment options

• Two year survival less than 10%

• Over 70% of BTC cancers express one or more HER family receptors

• Current treatment practice:

21

Biliary tractcancer

Chemo (gem/cis)

First line

Chemo (cap)

Second line

Varlitinib target patients

0

50

100

150

200

250

300

350

US Japan China EU Rest of World Other Asia

Mar

ket

size

(U

S$M

)

Treatment duration of approximately 9 to 12 months. Pricing based on international comparables, taking into account specific pricing factors for each region/country

Global market size: US$ 1,400M

00500/CF

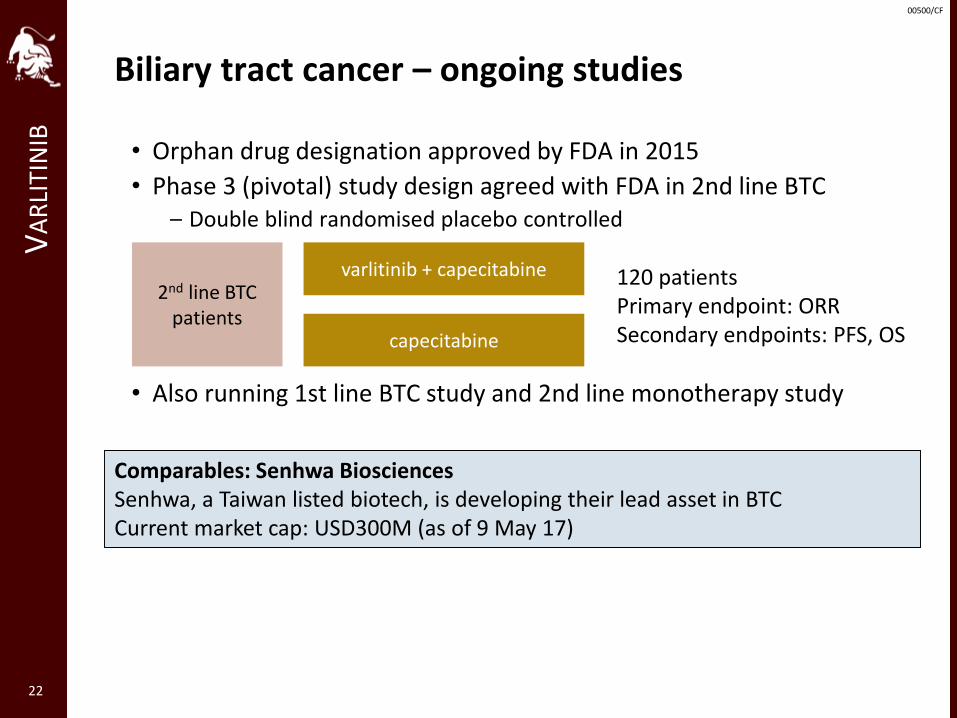

Biliary tract cancer – ongoing studiesV

AR

LITI

NIB

• Orphan drug designation approved by FDA in 2015

• Phase 3 (pivotal) study design agreed with FDA in 2nd line BTC– Double blind randomised placebo controlled

• Also running 1st line BTC study and 2nd line monotherapy study

22

2nd line BTC patients

varlitinib + capecitabine

capecitabine

120 patientsPrimary endpoint: ORRSecondary endpoints: PFS, OS

Comparables: Senhwa BiosciencesSenhwa, a Taiwan listed biotech, is developing their lead asset in BTCCurrent market cap: USD300M (as of 9 May 17)

00500/CF

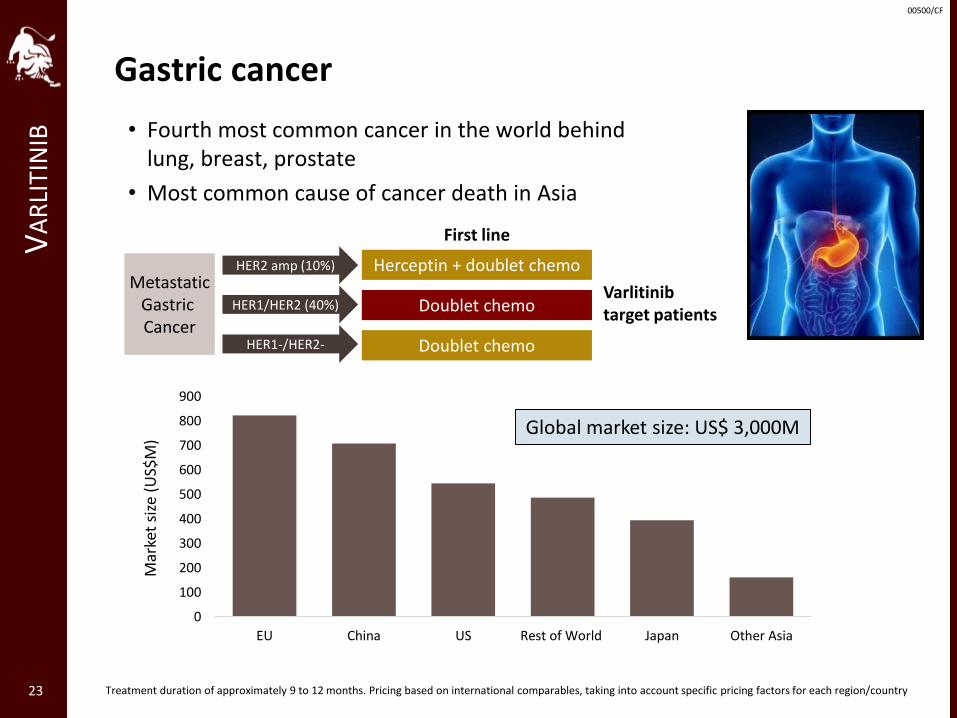

Gastric cancerV

AR

LITI

NIB • Fourth most common cancer in the world behind

lung, breast, prostate

• Most common cause of cancer death in Asia

23

MetastaticGastric Cancer

HER2 amp (10%) Herceptin + doublet chemo

Doublet chemo

Doublet chemo

Varlitinibtarget patients

First line

HER1/HER2 (40%)

HER1-/HER2-

0

100

200

300

400

500

600

700

800

900

EU China US Rest of World Japan Other Asia

Mar

ket

size

(U

S$M

)

Treatment duration of approximately 9 to 12 months. Pricing based on international comparables, taking into account specific pricing factors for each region/country

Global market size: US$ 3,000M

00500/CF

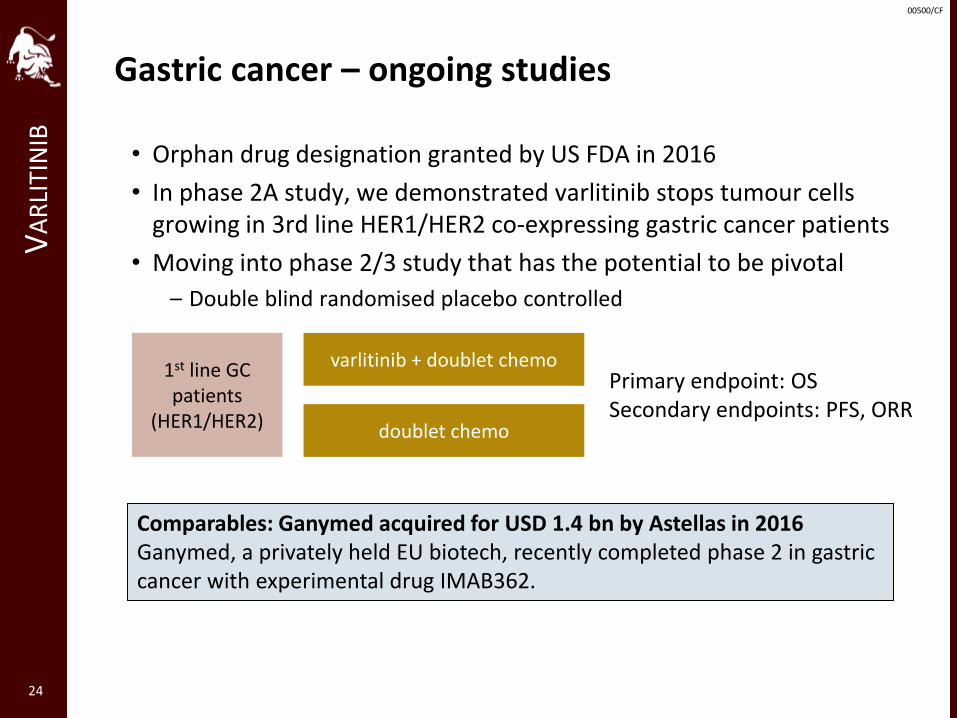

Gastric cancer – ongoing studiesV

AR

LITI

NIB

• Orphan drug designation granted by US FDA in 2016

• In phase 2A study, we demonstrated varlitinib stops tumour cells growing in 3rd line HER1/HER2 co-expressing gastric cancer patients

• Moving into phase 2/3 study that has the potential to be pivotal

– Double blind randomised placebo controlled

24

1st line GC patients

(HER1/HER2)

varlitinib + doublet chemo

doublet chemo

Primary endpoint: OSSecondary endpoints: PFS, ORR

Comparables: Ganymed acquired for USD 1.4 bn by Astellas in 2016Ganymed, a privately held EU biotech, recently completed phase 2 in gastric cancer with experimental drug IMAB362.

00500/CF

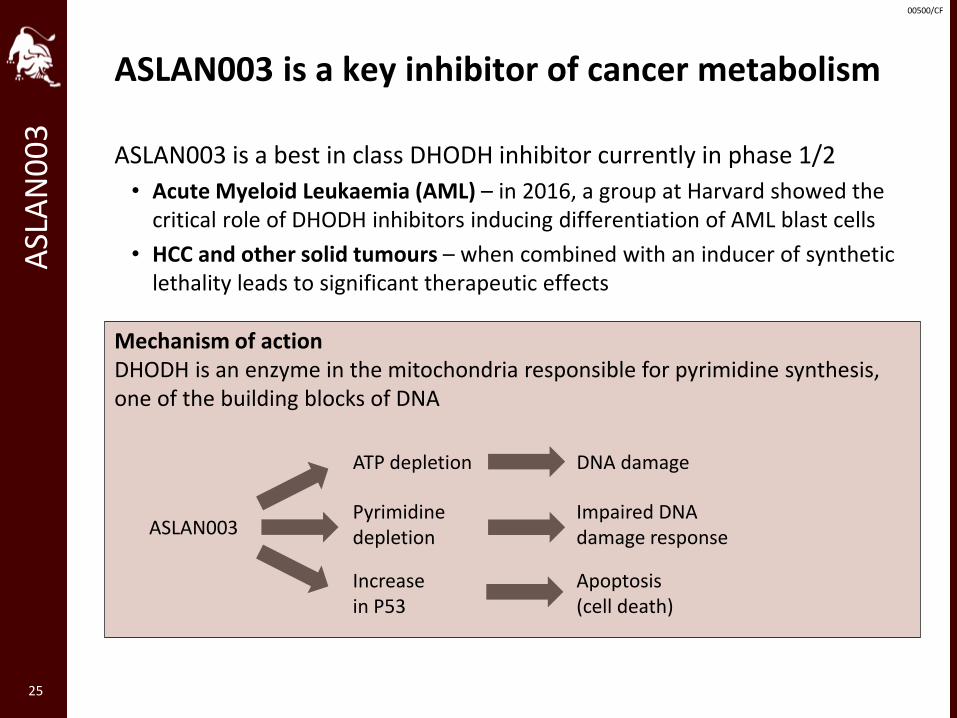

ASLAN003 is a key inhibitor of cancer metabolismA

SLA

N0

03

25

ASLAN003 is a best in class DHODH inhibitor currently in phase 1/2

• Acute Myeloid Leukaemia (AML) – in 2016, a group at Harvard showed the critical role of DHODH inhibitors inducing differentiation of AML blast cells

• HCC and other solid tumours – when combined with an inducer of synthetic lethality leads to significant therapeutic effects

Mechanism of actionDHODH is an enzyme in the mitochondria responsible for pyrimidine synthesis, one of the building blocks of DNA

ASLAN003

ATP depletion DNA damage

Pyrimidinedepletion

Impaired DNAdamage response

Increase in P53

Apoptosis(cell death)

00500/CF

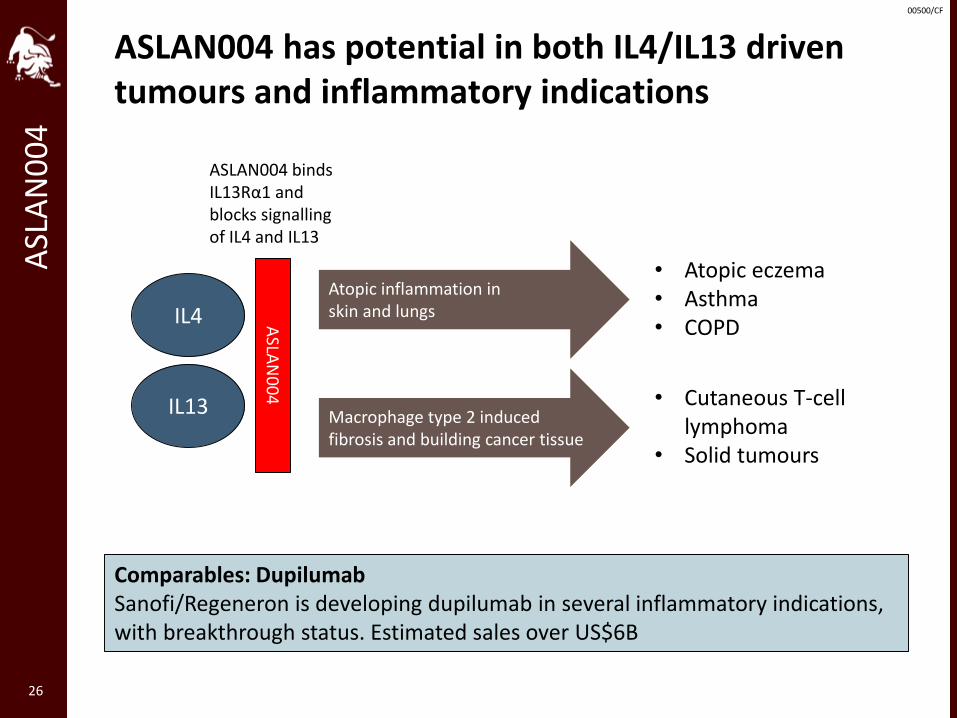

ASLAN004 has potential in both IL4/IL13 driven tumours and inflammatory indications

ASL

AN

00

4

26

IL4

IL13

ASLA

N0

04

ASLAN004 binds IL13Rα1 and blocks signalling of IL4 and IL13

Comparables: DupilumabSanofi/Regeneron is developing dupilumab in several inflammatory indications, with breakthrough status. Estimated sales over US$6B

Atopic inflammation in skin and lungs

Macrophage type 2 induced fibrosis and building cancer tissue

• Atopic eczema• Asthma• COPD

• Cutaneous T-cell lymphoma

• Solid tumours

00500/CF

ASL

AN

00

5

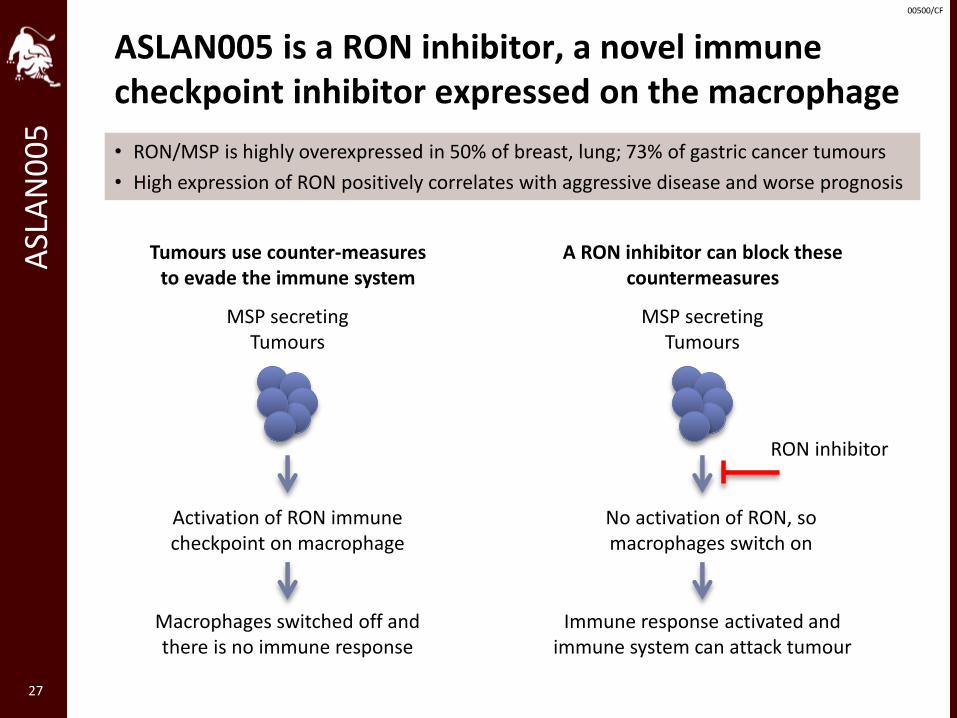

27

MSP secreting Tumours

Activation of RON immune checkpoint on macrophage

Macrophages switched off and there is no immune response

MSP secreting Tumours

No activation of RON, so macrophages switch on

Immune response activated and immune system can attack tumour

RON inhibitor

Tumours use counter-measures to evade the immune system

A RON inhibitor can block these countermeasures

• RON/MSP is highly overexpressed in 50% of breast, lung; 73% of gastric cancer tumours

• High expression of RON positively correlates with aggressive disease and worse prognosis

ASLAN005 is a RON inhibitor, a novel immune checkpoint inhibitor expressed on the macrophage

00500/CF

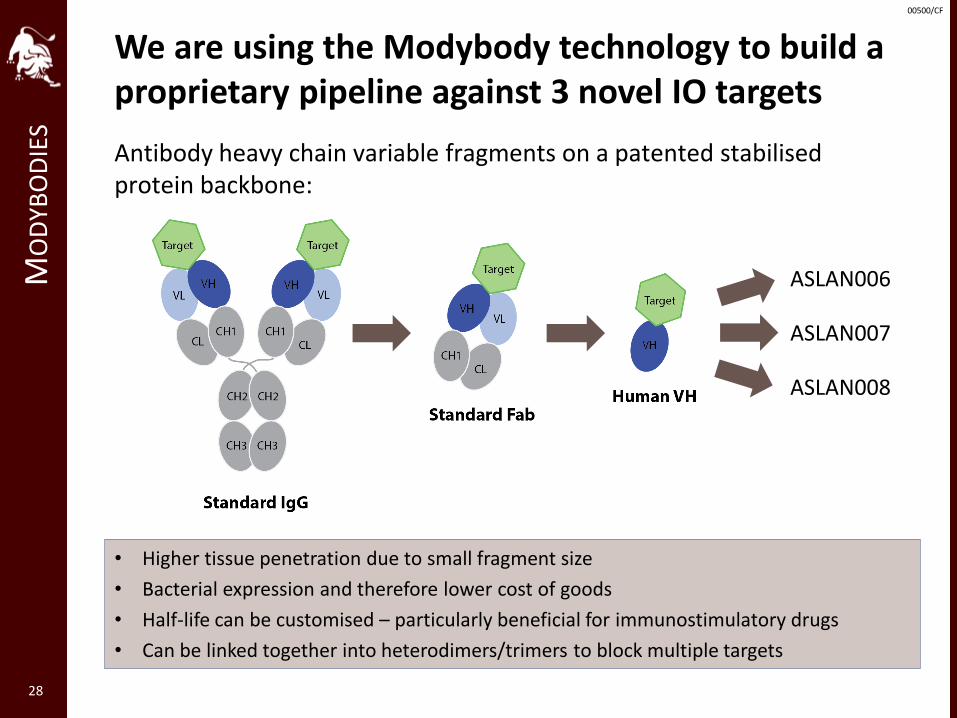

Antibody heavy chain variable fragments on a patented stabilisedprotein backbone:

28

MO

DYB

OD

IES

• Higher tissue penetration due to small fragment size

• Bacterial expression and therefore lower cost of goods

• Half-life can be customised – particularly beneficial for immunostimulatory drugs

• Can be linked together into heterodimers/trimers to block multiple targets

We are using the Modybody technology to build a proprietary pipeline against 3 novel IO targets

ASLAN006

ASLAN007

ASLAN008

00500/CF

3. FINANCIALS

29

00500/CF

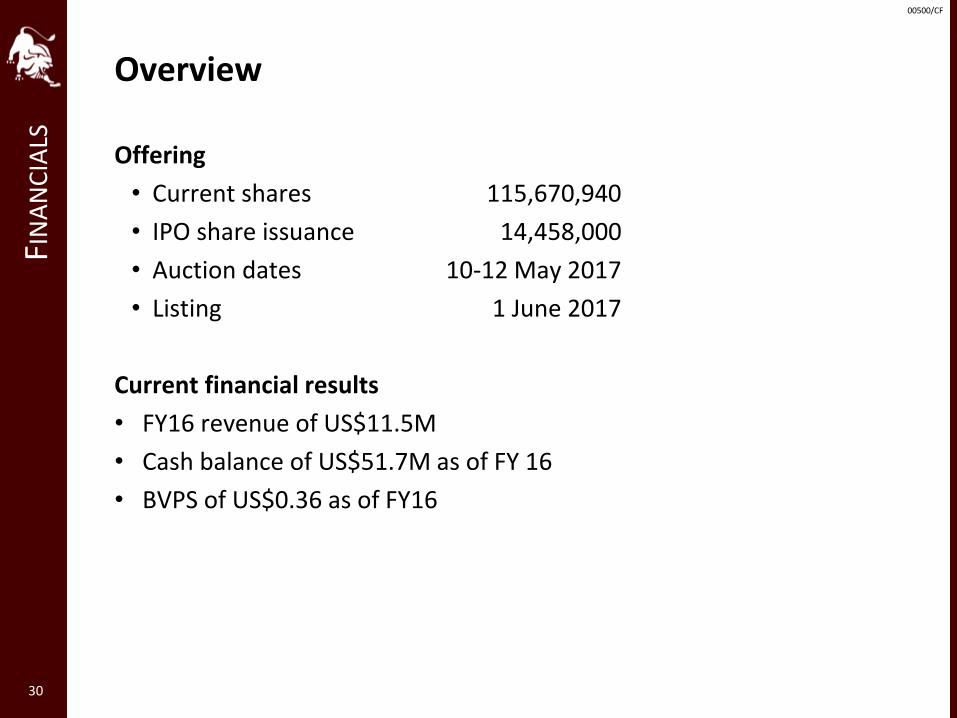

OverviewFI

NA

NC

IALS

Offering

• Current shares 115,670,940

• IPO share issuance 14,458,000

• Auction dates 10-12 May 2017

• Listing 1 June 2017

Current financial results

• FY16 revenue of US$11.5M

• Cash balance of US$51.7M as of FY 16

• BVPS of US$0.36 as of FY16

30

00500/CF

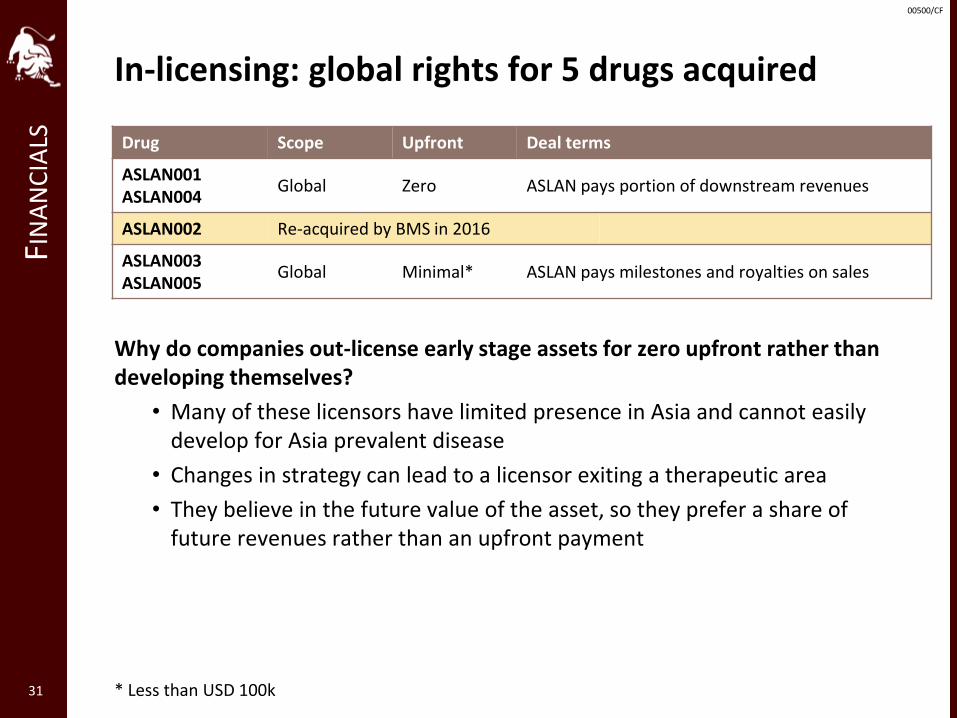

In-licensing: global rights for 5 drugs acquiredFI

NA

NC

IALS Drug Scope Upfront Deal terms

ASLAN001ASLAN004

Global Zero ASLAN pays portion of downstream revenues

ASLAN002 Re-acquired by BMS in 2016

ASLAN003ASLAN005

Global Minimal* ASLAN pays milestones and royalties on sales

31

Why do companies out-license early stage assets for zero upfront rather than developing themselves?

• Many of these licensors have limited presence in Asia and cannot easily develop for Asia prevalent disease

• Changes in strategy can lead to a licensor exiting a therapeutic area

• They believe in the future value of the asset, so they prefer a share of future revenues rather than an upfront payment

* Less than USD 100k

00500/CF

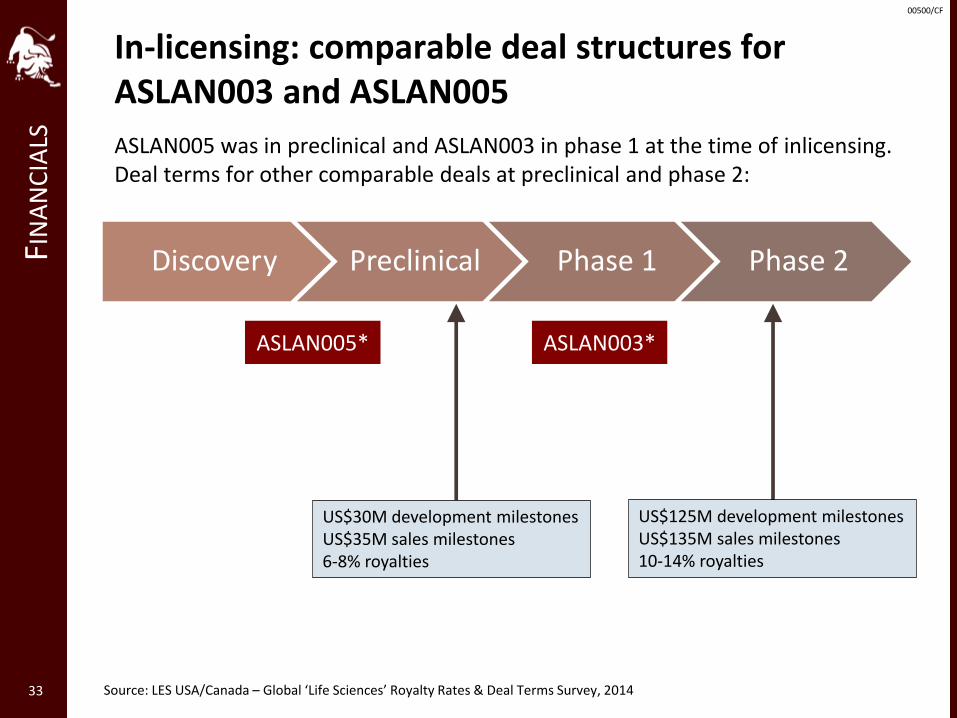

In-licensing: comparable deal structures for ASLAN001 and ASLAN004

FIN

AN

CIA

LS

32

Date Product Originator Licensor Revenue split Other terms

Jan 17 TAK935 50 : 50

May 13 ARRY380 50 : 50 Upfront of US$10M

Jan 17KTE-C19 andadditional products

60 : 40Upfront of US$40M,US$20M in initial funding for the JV

Jan 08 Mipomersen 70 : 30

Upfront of US$175M, US$150M investment

Will reach 50/50 on a slidingscale as annual revenues ramp up to US$2B

Nov 11 PRT062607 75 : 25Upfront of US$36M, US$9M investment

Deal terms for other comparable deals with revenue split:

00500/CF

In-licensing: comparable deal structures for ASLAN003 and ASLAN005

FIN

AN

CIA

LS ASLAN005 was in preclinical and ASLAN003 in phase 1 at the time of inlicensing. Deal terms for other comparable deals at preclinical and phase 2:

33 Source: LES USA/Canada – Global ‘Life Sciences’ Royalty Rates & Deal Terms Survey, 2014

Discovery Preclinical Phase 1 Phase 2

ASLAN005* ASLAN003*

US$30M development milestonesUS$35M sales milestones6-8% royalties

US$125M development milestonesUS$135M sales milestones10-14% royalties

00500/CF

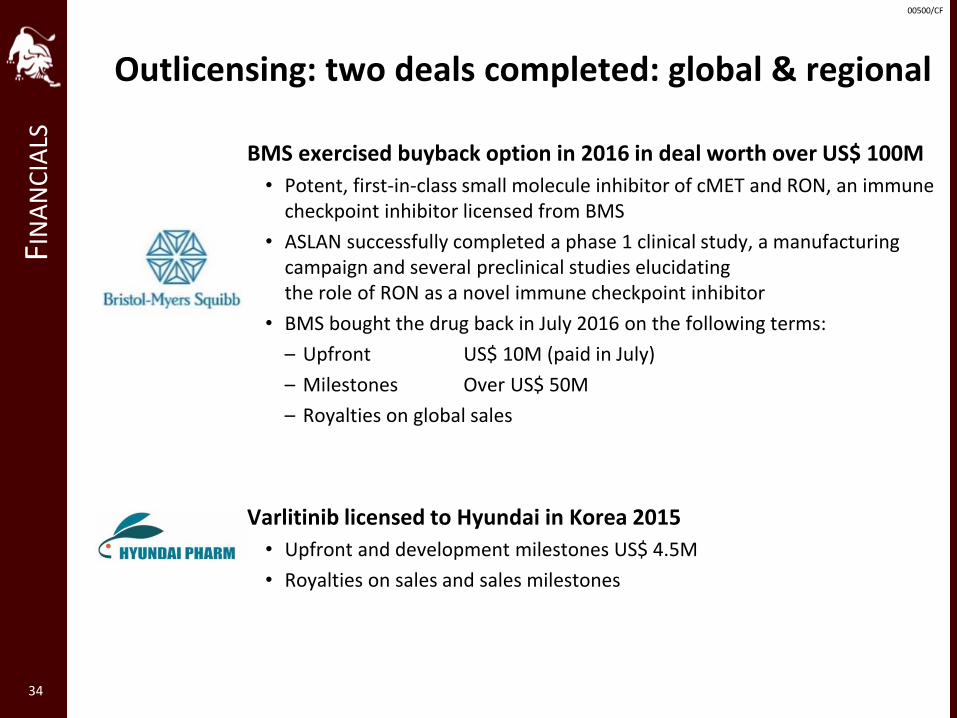

Outlicensing: two deals completed: global & regionalFI

NA

NC

IALS

34

BMS exercised buyback option in 2016 in deal worth over US$ 100M

• Potent, first-in-class small molecule inhibitor of cMET and RON, an immune checkpoint inhibitor licensed from BMS

• ASLAN successfully completed a phase 1 clinical study, a manufacturing campaign and several preclinical studies elucidating the role of RON as a novel immune checkpoint inhibitor

• BMS bought the drug back in July 2016 on the following terms:

– Upfront US$ 10M (paid in July)

– Milestones Over US$ 50M

– Royalties on global sales

Varlitinib licensed to Hyundai in Korea 2015

• Upfront and development milestones US$ 4.5M

• Royalties on sales and sales milestones

00500/CF

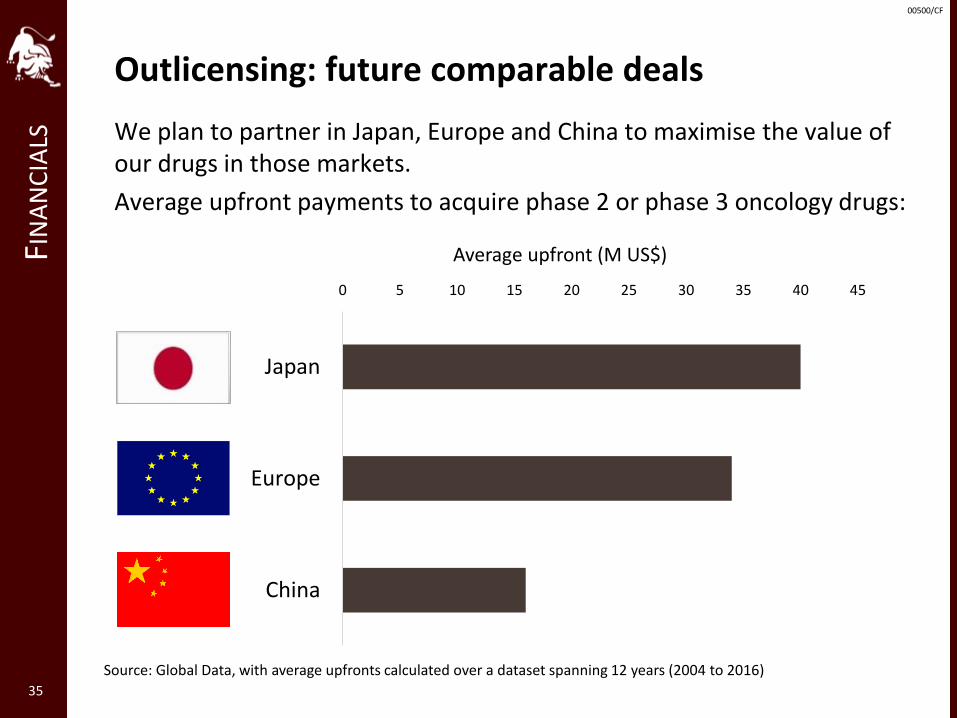

Outlicensing: future comparable dealsFI

NA

NC

IALS We plan to partner in Japan, Europe and China to maximise the value of

our drugs in those markets.

Average upfront payments to acquire phase 2 or phase 3 oncology drugs:

35

0 5 10 15 20 25 30 35 40 45

Japan

Europe

China

Average upfront (M US$)

Source: Global Data, with average upfronts calculated over a dataset spanning 12 years (2004 to 2016)

00500/CF

4. COMPARABLE COMPANIES

36

00500/CF

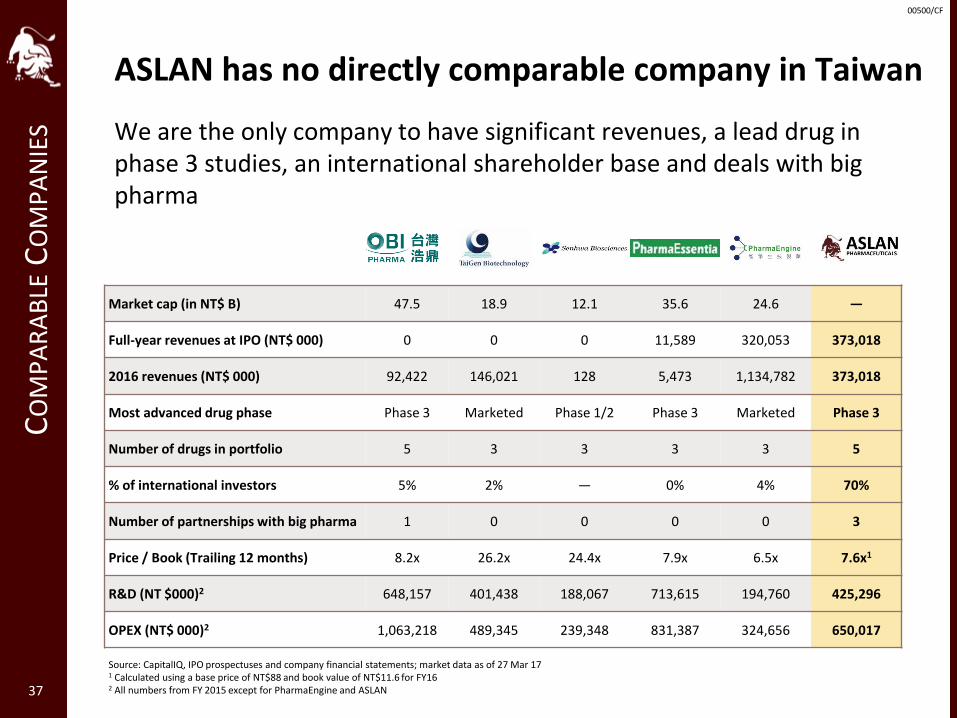

Market cap (in NT$ B) 47.5 18.9 12.1 35.6 24.6 —

Full-year revenues at IPO (NT$ 000) 0 0 0 11,589 320,053 373,018

2016 revenues (NT$ 000) 92,422 146,021 128 5,473 1,134,782 373,018

Most advanced drug phase Phase 3 Marketed Phase 1/2 Phase 3 Marketed Phase 3

Number of drugs in portfolio 5 3 3 3 3 5

% of international investors 5% 2% — 0% 4% 70%

Number of partnerships with big pharma 1 0 0 0 0 3

Price / Book (Trailing 12 months) 8.2x 26.2x 24.4x 7.9x 6.5x 7.6x1

R&D (NT $000)2 648,157 401,438 188,067 713,615 194,760 425,296

OPEX (NT$ 000)2 1,063,218 489,345 239,348 831,387 324,656 650,017

ASLAN has no directly comparable company in TaiwanC

OM

PA

RA

BLE

CO

MP

AN

IES We are the only company to have significant revenues, a lead drug in

phase 3 studies, an international shareholder base and deals with big pharma

37

Source: CapitalIQ, IPO prospectuses and company financial statements; market data as of 27 Mar 171 Calculated using a base price of NT$88 and book value of NT$11.6 for FY162 All numbers from FY 2015 except for PharmaEngine and ASLAN

00500/CF

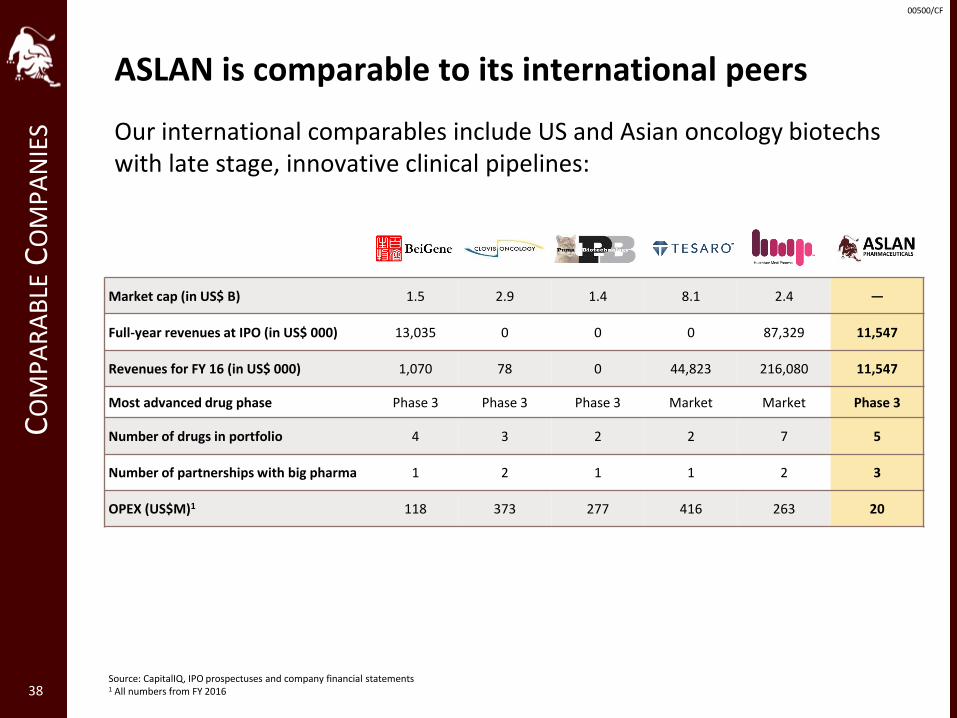

ASLAN is comparable to its international peersC

OM

PA

RA

BLE

CO

MP

AN

IES

38

Market cap (in US$ B) 1.5 2.9 1.4 8.1 2.4 —

Full-year revenues at IPO (in US$ 000) 13,035 0 0 0 87,329 11,547

Revenues for FY 16 (in US$ 000) 1,070 78 0 44,823 216,080 11,547

Most advanced drug phase Phase 3 Phase 3 Phase 3 Market Market Phase 3

Number of drugs in portfolio 4 3 2 2 7 5

Number of partnerships with big pharma 1 2 1 1 2 3

OPEX (US$M)1 118 373 277 416 263 20

Our international comparables include US and Asian oncology biotechswith late stage, innovative clinical pipelines:

Source: CapitalIQ, IPO prospectuses and company financial statements1 All numbers from FY 2016

00500/CF

5. FUTURE MILESTONES

39

00500/CF

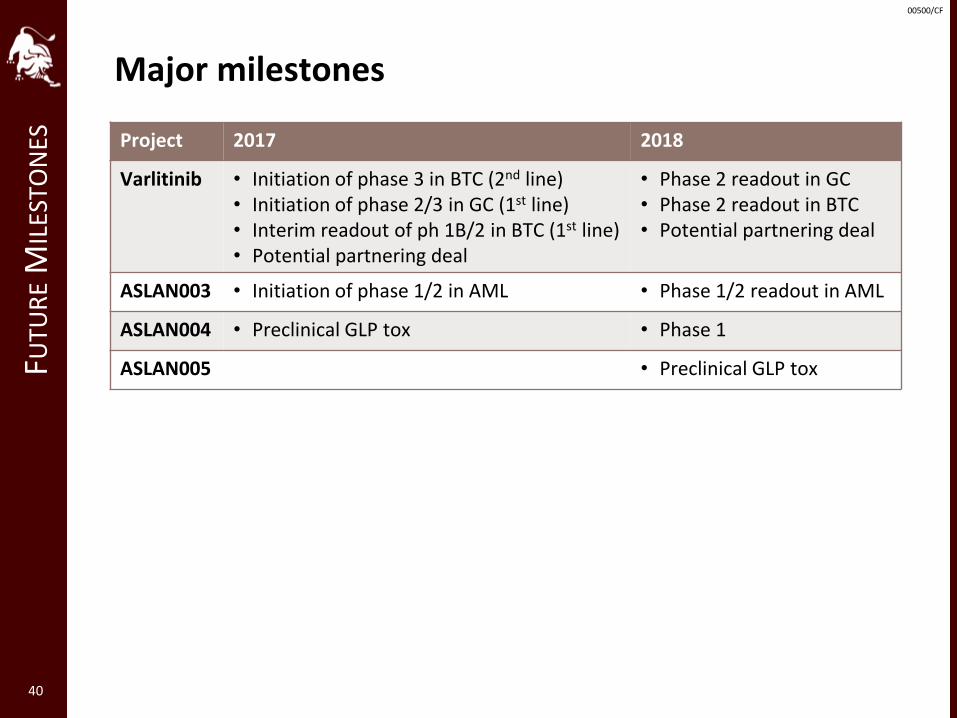

Major milestones

40

FUTU

RE

MIL

ESTO

NES Project 2017 2018

Varlitinib • Initiation of phase 3 in BTC (2nd line)• Initiation of phase 2/3 in GC (1st line)• Interim readout of ph 1B/2 in BTC (1st line)• Potential partnering deal

• Phase 2 readout in GC• Phase 2 readout in BTC• Potential partnering deal

ASLAN003 • Initiation of phase 1/2 in AML • Phase 1/2 readout in AML

ASLAN004 • Preclinical GLP tox • Phase 1

ASLAN005 • Preclinical GLP tox

00500/CF

SUM

MA

RY

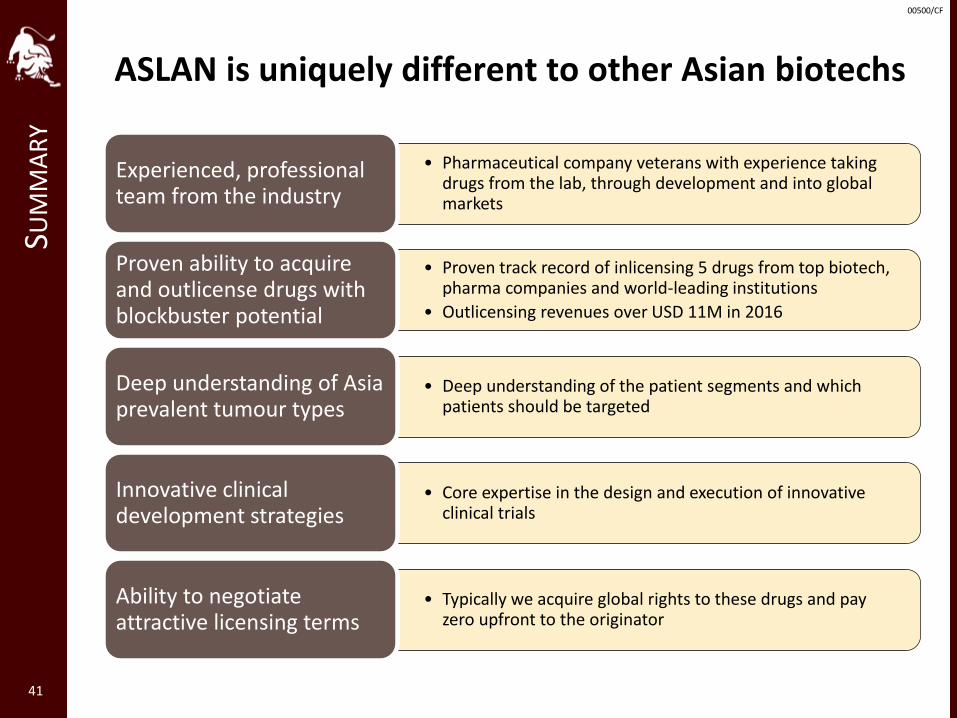

ASLAN is uniquely different to other Asian biotechs

41

• Pharmaceutical company veterans with experience taking drugs from the lab, through development and into global markets

Experienced, professional team from the industry

• Proven track record of inlicensing 5 drugs from top biotech, pharma companies and world-leading institutions

• Outlicensing revenues over USD 11M in 2016

Proven ability to acquire and outlicense drugs with blockbuster potential

• Deep understanding of the patient segments and which patients should be targeted

Deep understanding of Asia prevalent tumour types

• Core expertise in the design and execution of innovative clinical trials

Innovative clinical development strategies

• Typically we acquire global rights to these drugs and pay zero upfront to the originator

Ability to negotiate attractive licensing terms

00500/CF

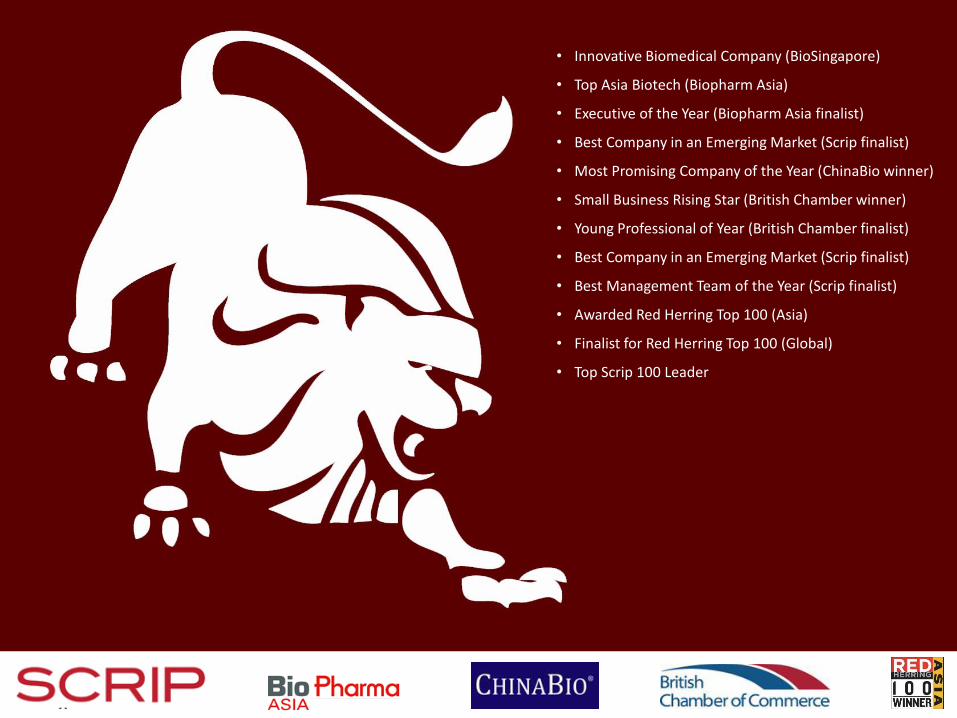

• Innovative Biomedical Company (BioSingapore)

• Top Asia Biotech (Biopharm Asia)

• Executive of the Year (Biopharm Asia finalist)

• Best Company in an Emerging Market (Scrip finalist)

• Most Promising Company of the Year (ChinaBio winner)

• Small Business Rising Star (British Chamber winner)

• Young Professional of Year (British Chamber finalist)

• Best Company in an Emerging Market (Scrip finalist)

• Best Management Team of the Year (Scrip finalist)

• Awarded Red Herring Top 100 (Asia)

• Finalist for Red Herring Top 100 (Global)

• Top Scrip 100 Leader

g

![[ ] BMN-ehealth presentat](https://img.pdfslide.us/doc/110x75/55d6f95bbb61eb98188b467a/-bmn-ehealth-presentat.jpg)