Embed Size (px)

Citation preview

Notified on 29th March,2016

Companies (Auditor’s Report) Order,2016

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 2

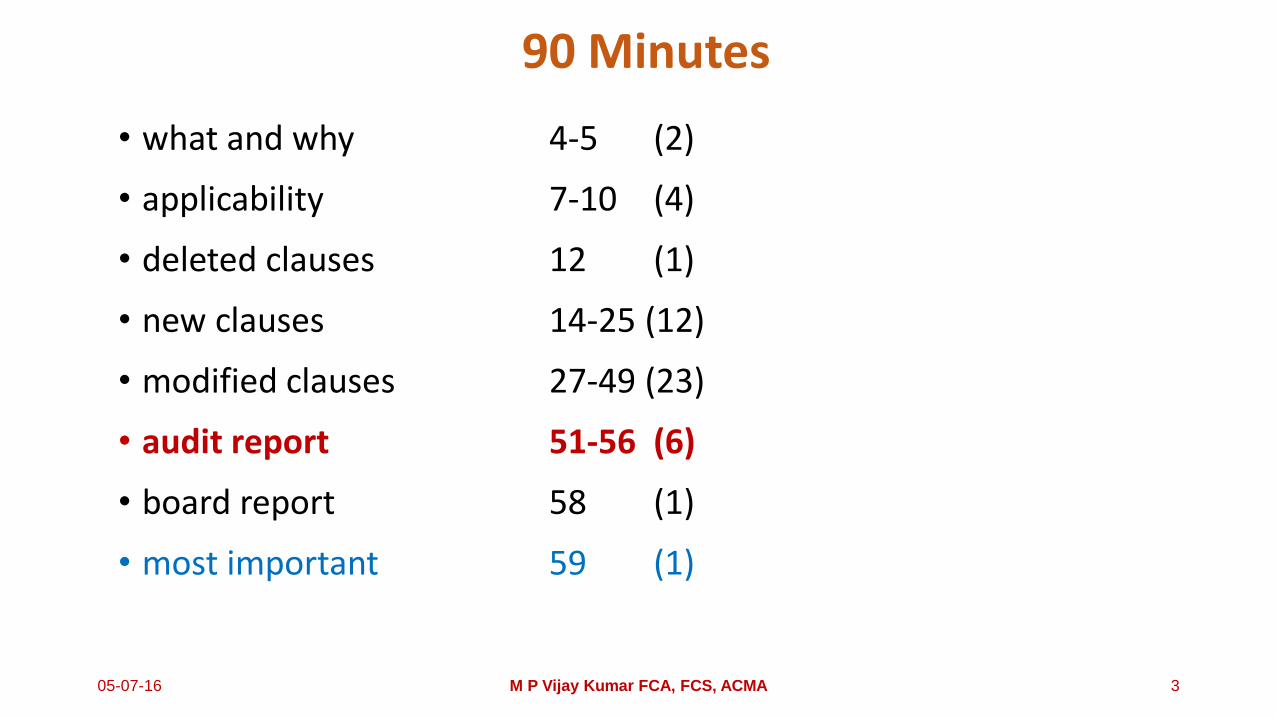

90 Minutes

• what and why 4-5 (2)

• applicability 7-10 (4)

• deleted clauses 12 (1)

• new clauses 14-25 (12)

• modified clauses 27-49 (23)

• audit report 51-56 (6)

• board report 58 (1)

• most important 59 (1)

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 3

what and why ?2 slides (4-5)

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 4

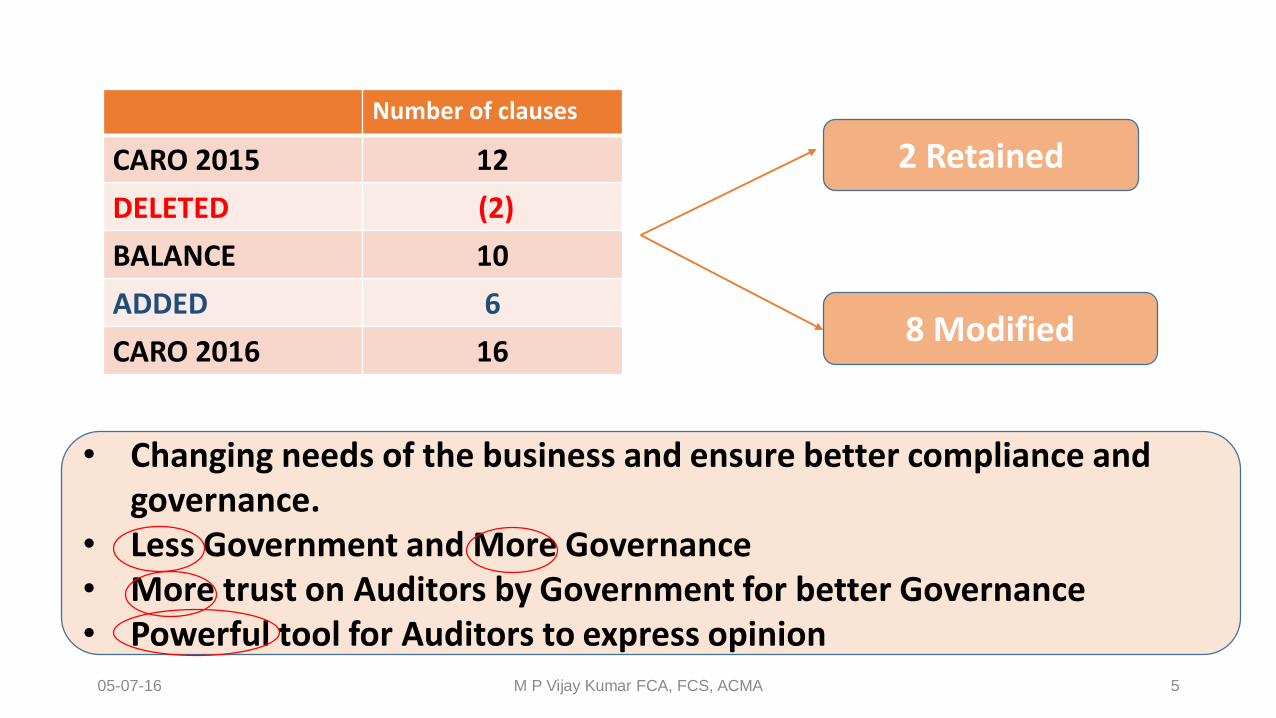

• Changing needs of the business and ensure better compliance and governance.

• Less Government and More Governance• More trust on Auditors by Government for better Governance• Powerful tool for Auditors to express opinion

2 Retained

8 Modified

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 5

Number of clauses

CARO 2015 12

DELETED (2)

BALANCE 10

ADDED 6

CARO 2016 16

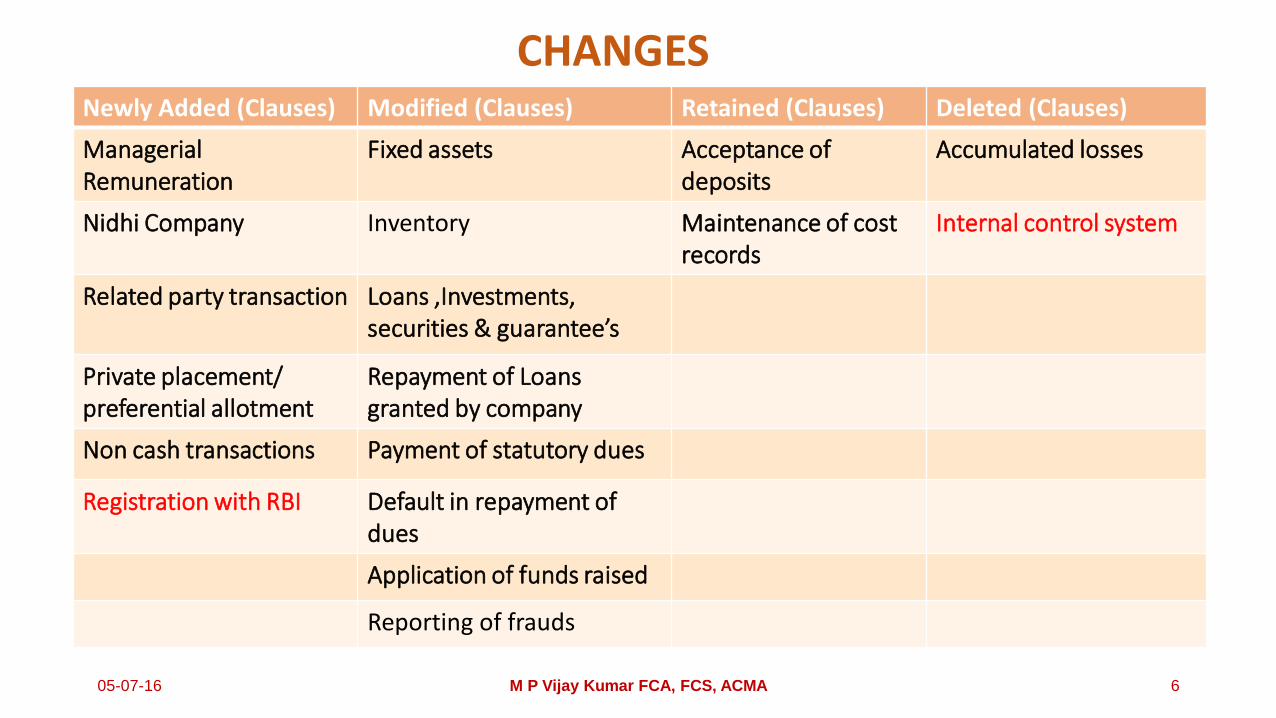

Newly Added (Clauses) Modified (Clauses) Retained (Clauses) Deleted (Clauses)

Managerial Remuneration

Fixed assets Acceptance of deposits

Accumulated losses

Nidhi Company Inventory Maintenance of cost records

Internal control system

Related party transaction Loans ,Investments, securities & guarantee’s

Private placement/ preferential allotment

Repayment of Loans granted by company

Non cash transactions Payment of statutory dues

Registration with RBI Default in repayment of dues

Application of funds raised

Reporting of frauds

CHANGES

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 6

applicability4 slides (7-10)

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 7

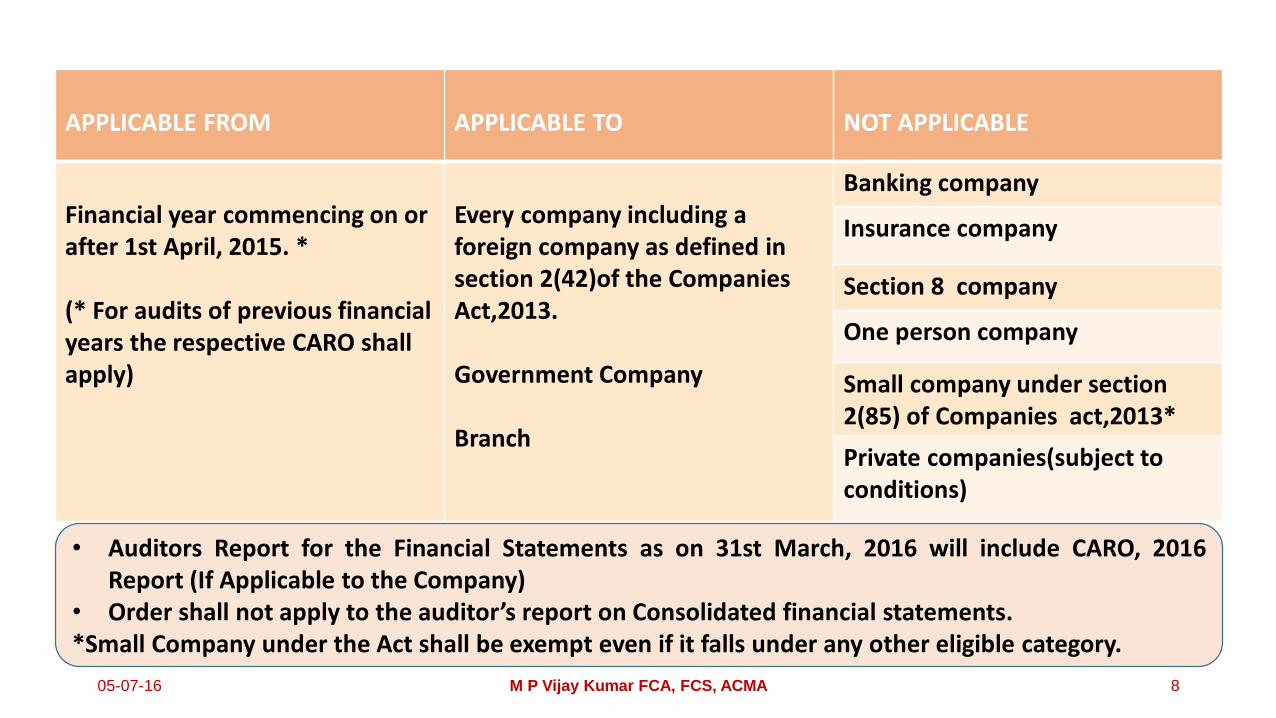

APPLICABLE FROM APPLICABLE TO NOT APPLICABLE

Financial year commencing on or after 1st April, 2015. *

(* For audits of previous financial years the respective CARO shall apply)

Every company including a foreign company as defined in section 2(42)of the Companies Act,2013.

Government Company

Branch

Banking company

Insurance company

Section 8 company

One person company

Small company under section 2(85) of Companies act,2013*

Private companies(subject to conditions)

• Auditors Report for the Financial Statements as on 31st March, 2016 will include CARO, 2016Report (If Applicable to the Company)

• Order shall not apply to the auditor’s report on Consolidated financial statements.*Small Company under the Act shall be exempt even if it falls under any other eligible category.

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 8

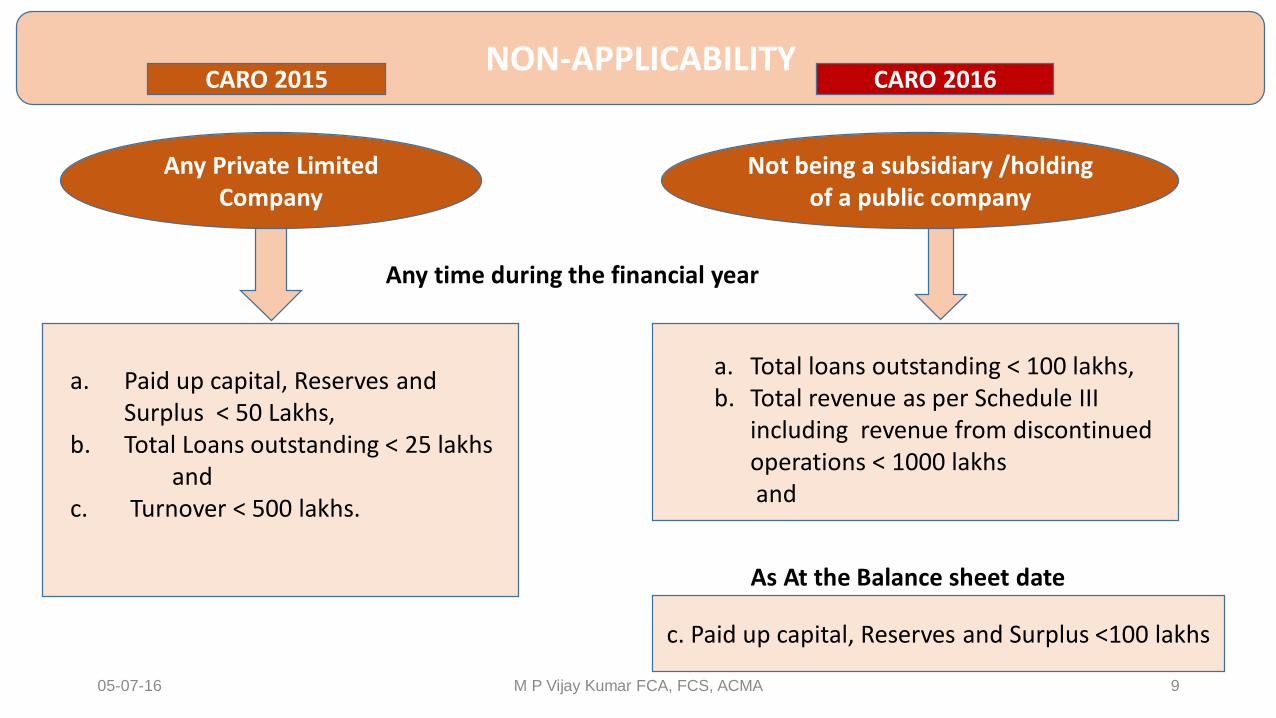

NON-APPLICABILITY

Any Private Limited Company

Not being a subsidiary /holding of a public company

Any time during the financial year

a. Paid up capital, Reserves and Surplus < 50 Lakhs,

b. Total Loans outstanding < 25 lakhsand

c. Turnover < 500 lakhs.

a. Total loans outstanding < 100 lakhs,b. Total revenue as per Schedule III

including revenue from discontinued operations < 1000 lakhsand

c. Paid up capital, Reserves and Surplus <100 lakhs

As At the Balance sheet date

CARO 2015 CARO 2016

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 9

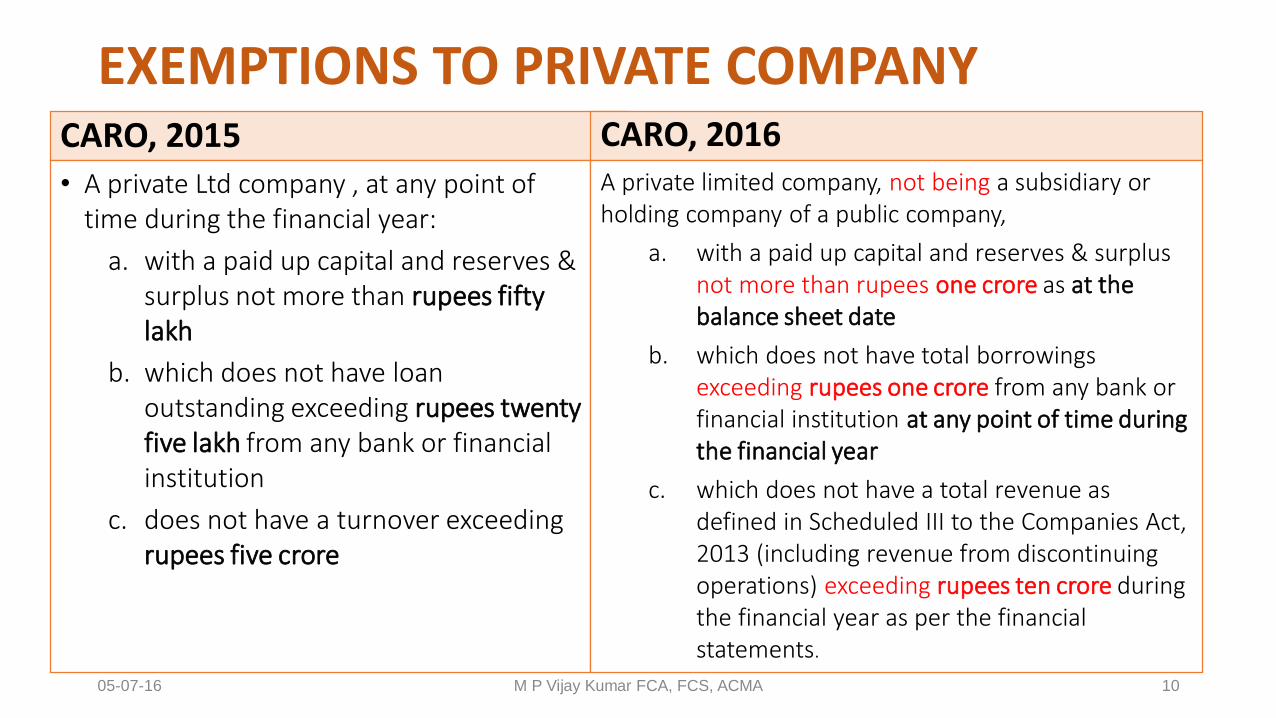

EXEMPTIONS TO PRIVATE COMPANY CARO, 2015• A private Ltd company , at any point of

time during the financial year:

a. with a paid up capital and reserves & surplus not more than rupees fifty lakh

b. which does not have loan outstanding exceeding rupees twenty five lakh from any bank or financial institution

c. does not have a turnover exceeding rupees five crore

CARO, 2016A private limited company, not being a subsidiary or holding company of a public company,

a. with a paid up capital and reserves & surplusnot more than rupees one crore as at the balance sheet date

b. which does not have total borrowings exceeding rupees one crore from any bank or financial institution at any point of time during the financial year

c. which does not have a total revenue as defined in Scheduled III to the Companies Act, 2013 (including revenue from discontinuing operations) exceeding rupees ten crore during the financial year as per the financial statements.

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 10

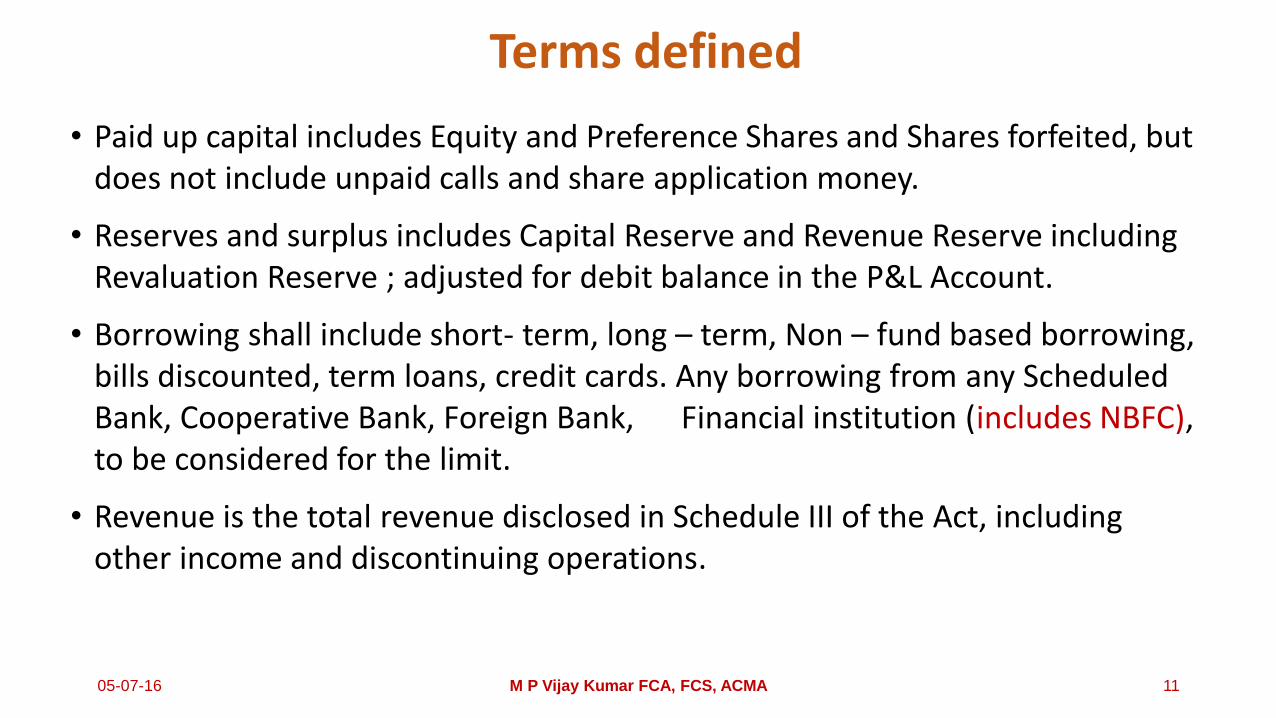

Terms defined

• Paid up capital includes Equity and Preference Shares and Shares forfeited, but does not include unpaid calls and share application money.

• Reserves and surplus includes Capital Reserve and Revenue Reserve including Revaluation Reserve ; adjusted for debit balance in the P&L Account.

• Borrowing shall include short- term, long – term, Non – fund based borrowing, bills discounted, term loans, credit cards. Any borrowing from any Scheduled Bank, Cooperative Bank, Foreign Bank, Financial institution (includes NBFC), to be considered for the limit.

• Revenue is the total revenue disclosed in Schedule III of the Act, including other income and discontinuing operations.

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 11

deleted clauses1 slide (12)

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 12

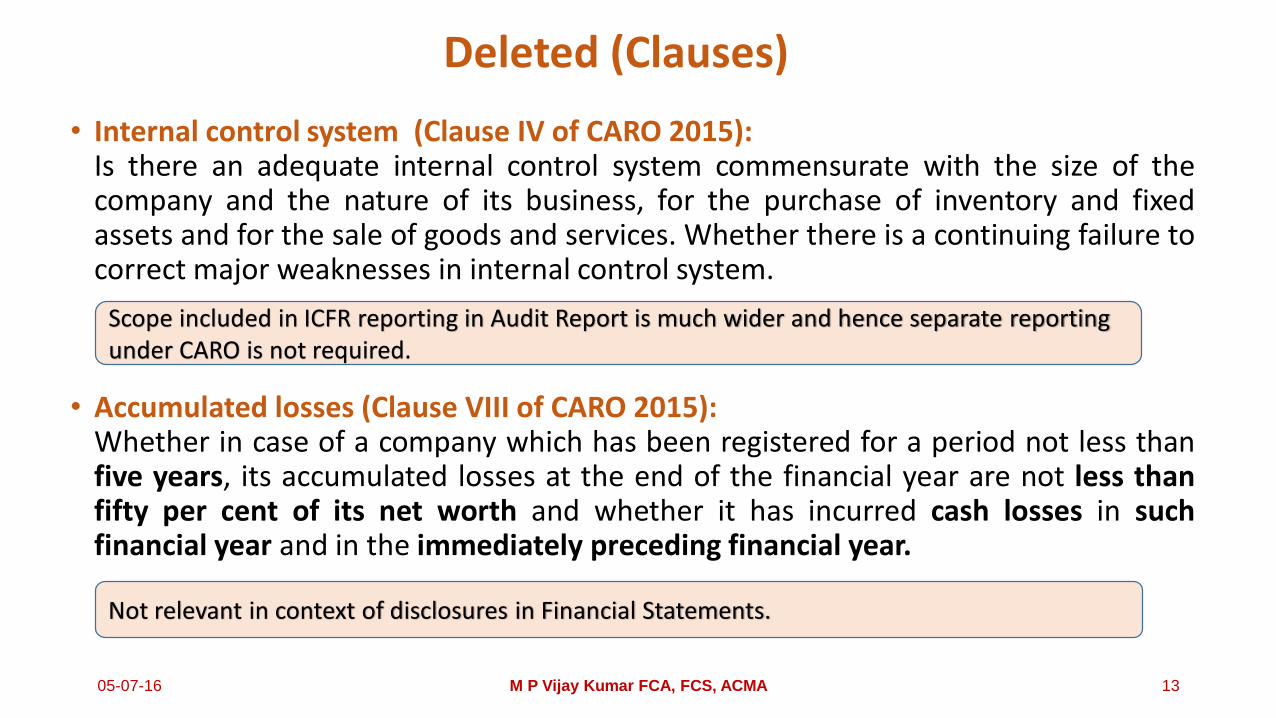

Deleted (Clauses)

• Internal control system (Clause IV of CARO 2015):Is there an adequate internal control system commensurate with the size of thecompany and the nature of its business, for the purchase of inventory and fixedassets and for the sale of goods and services. Whether there is a continuing failure tocorrect major weaknesses in internal control system.

• Accumulated losses (Clause VIII of CARO 2015):Whether in case of a company which has been registered for a period not less thanfive years, its accumulated losses at the end of the financial year are not less thanfifty per cent of its net worth and whether it has incurred cash losses in suchfinancial year and in the immediately preceding financial year.

Scope included in ICFR reporting in Audit Report is much wider and hence separate reporting under CARO is not required.

Not relevant in context of disclosures in Financial Statements.

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 13

new clauses12 slides (14-25)

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 14

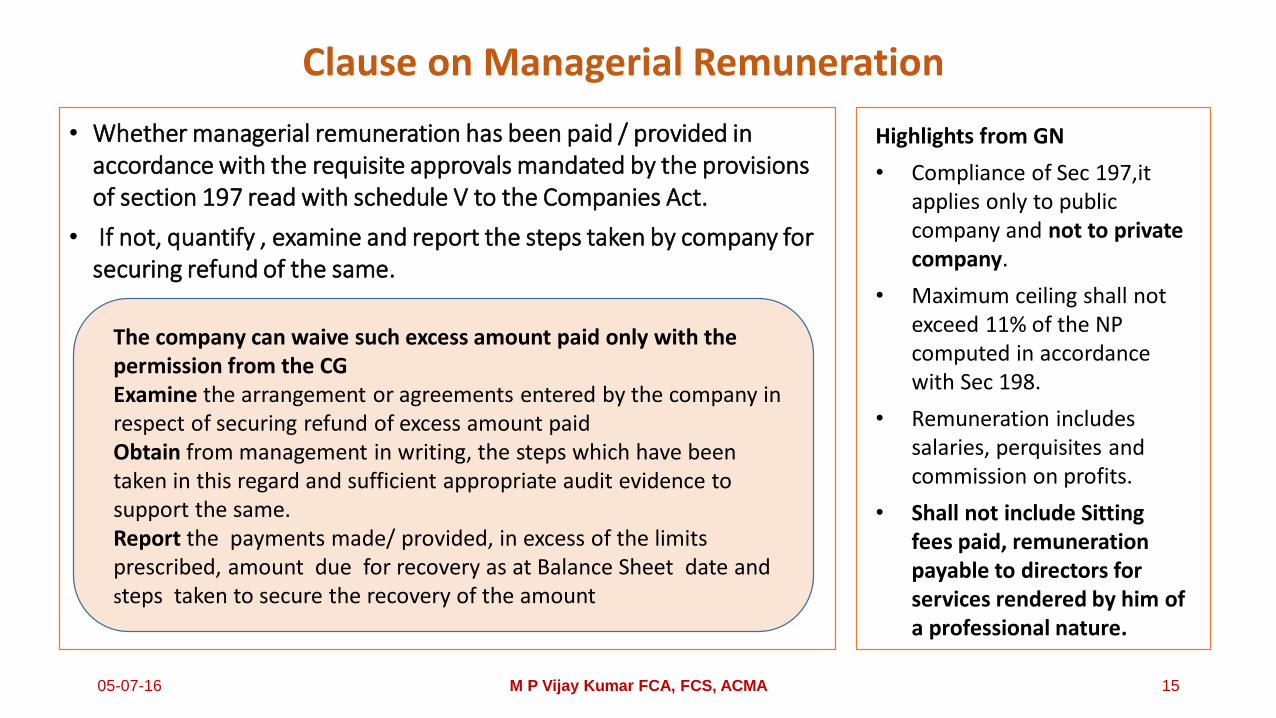

Clause on Managerial Remuneration

• Whether managerial remuneration has been paid / provided in accordance with the requisite approvals mandated by the provisions of section 197 read with schedule V to the Companies Act.

• If not, quantify , examine and report the steps taken by company for securing refund of the same.

Highlights from GN

• Compliance of Sec 197,it applies only to public company and not to private company.

• Maximum ceiling shall not exceed 11% of the NP computed in accordance with Sec 198.

• Remuneration includes salaries, perquisites and commission on profits.

• Shall not include Sitting fees paid, remuneration payable to directors for services rendered by him of a professional nature.

The company can waive such excess amount paid only with the permission from the CGExamine the arrangement or agreements entered by the company in respect of securing refund of excess amount paid Obtain from management in writing, the steps which have been taken in this regard and sufficient appropriate audit evidence to support the same.Report the payments made/ provided, in excess of the limits prescribed, amount due for recovery as at Balance Sheet date and steps taken to secure the recovery of the amount

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 15

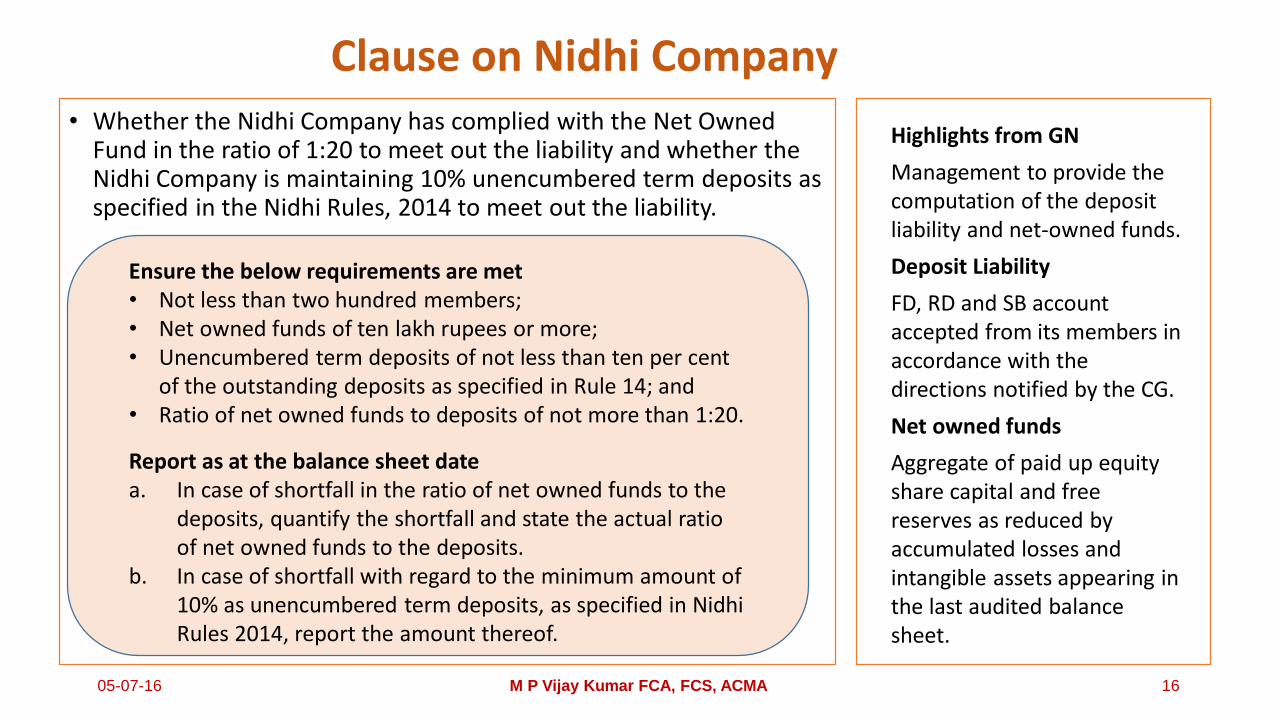

• Whether the Nidhi Company has complied with the Net Owned Fund in the ratio of 1:20 to meet out the liability and whether the Nidhi Company is maintaining 10% unencumbered term deposits as specified in the Nidhi Rules, 2014 to meet out the liability.

Highlights from GN

Management to provide the computation of the deposit liability and net-owned funds.

Deposit Liability

FD, RD and SB account accepted from its members in accordance with the directions notified by the CG.

Net owned funds

Aggregate of paid up equity share capital and free reserves as reduced by accumulated losses and intangible assets appearing in the last audited balance sheet.

Ensure the below requirements are met• Not less than two hundred members;• Net owned funds of ten lakh rupees or more;• Unencumbered term deposits of not less than ten per cent

of the outstanding deposits as specified in Rule 14; and• Ratio of net owned funds to deposits of not more than 1:20.

Report as at the balance sheet datea. In case of shortfall in the ratio of net owned funds to the

deposits, quantify the shortfall and state the actual ratio of net owned funds to the deposits.

b. In case of shortfall with regard to the minimum amount of 10% as unencumbered term deposits, as specified in Nidhi Rules 2014, report the amount thereof.

Clause on Nidhi Company

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 16

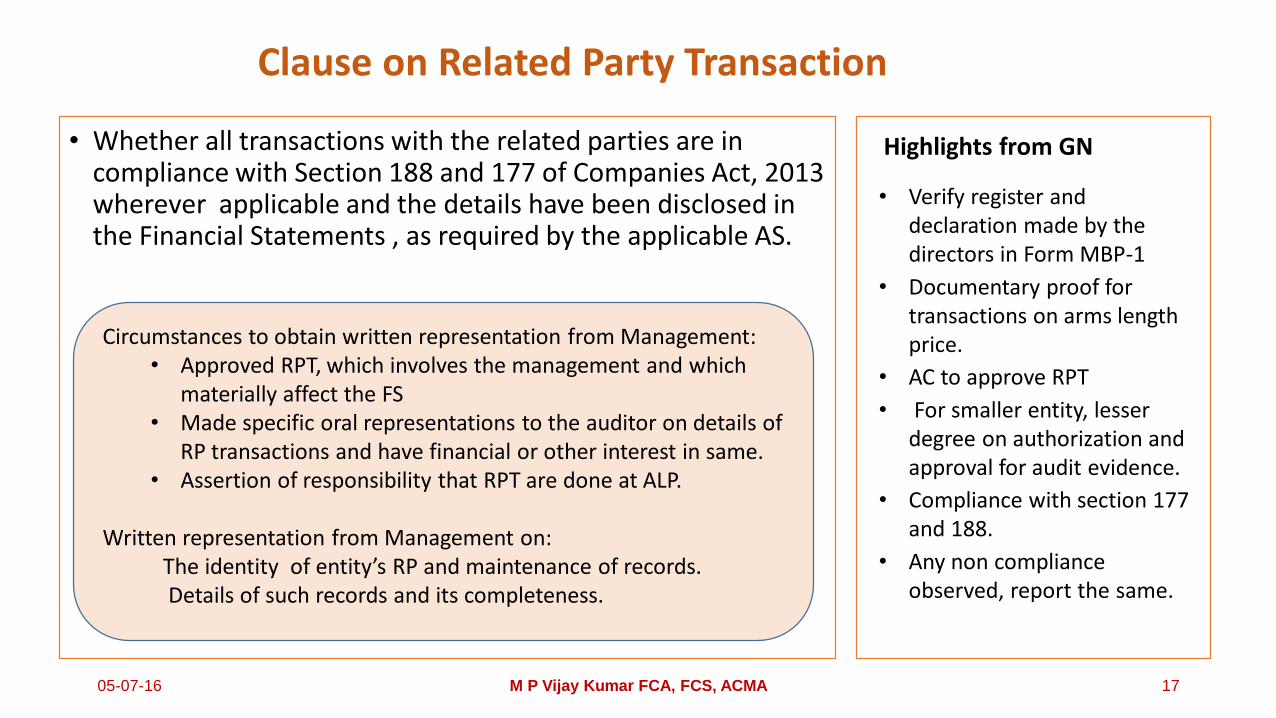

• Whether all transactions with the related parties are in compliance with Section 188 and 177 of Companies Act, 2013 wherever applicable and the details have been disclosed in the Financial Statements , as required by the applicable AS.

Highlights from GN

• Verify register and declaration made by the directors in Form MBP-1

• Documentary proof for transactions on arms length price.

• AC to approve RPT

• For smaller entity, lesser degree on authorization and approval for audit evidence.

• Compliance with section 177 and 188.

• Any non compliance observed, report the same.

Circumstances to obtain written representation from Management:• Approved RPT, which involves the management and which

materially affect the FS• Made specific oral representations to the auditor on details of

RP transactions and have financial or other interest in same. • Assertion of responsibility that RPT are done at ALP.

Written representation from Management on:The identity of entity’s RP and maintenance of records.Details of such records and its completeness.

Clause on Related Party Transaction

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 17

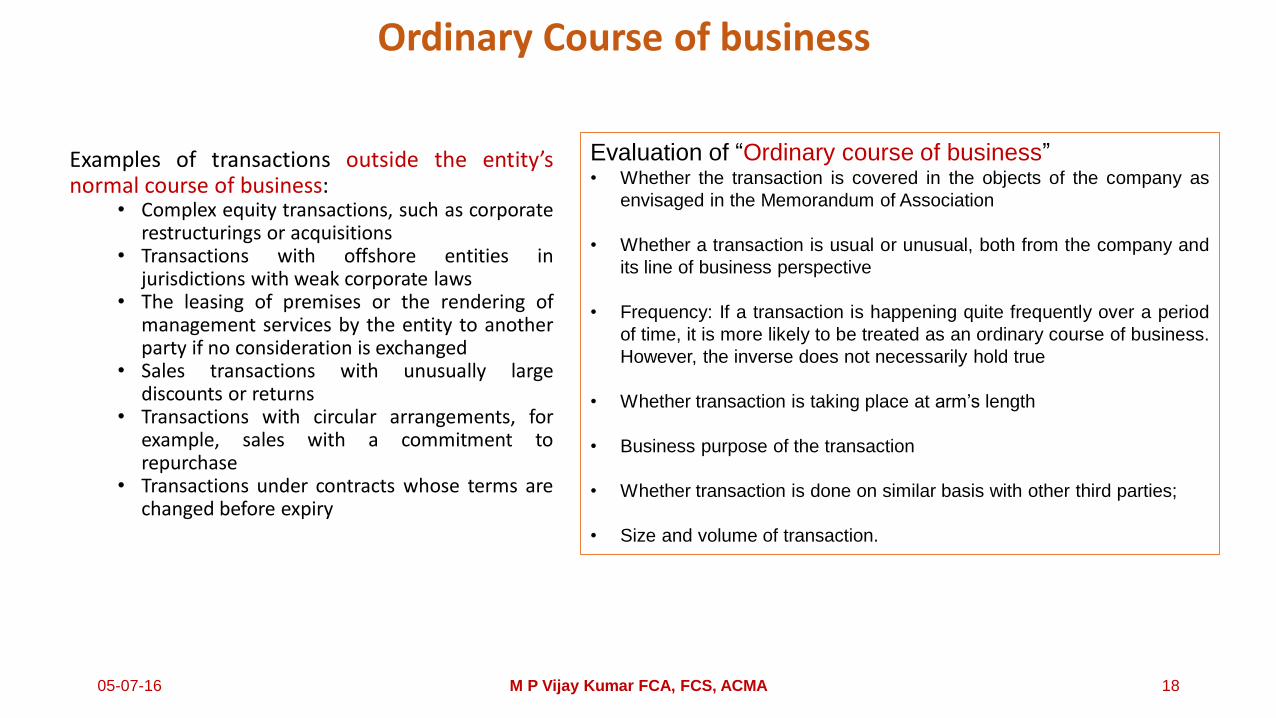

Ordinary Course of business

Examples of transactions outside the entity’snormal course of business:

• Complex equity transactions, such as corporaterestructurings or acquisitions

• Transactions with offshore entities injurisdictions with weak corporate laws

• The leasing of premises or the rendering ofmanagement services by the entity to anotherparty if no consideration is exchanged

• Sales transactions with unusually largediscounts or returns

• Transactions with circular arrangements, forexample, sales with a commitment torepurchase

• Transactions under contracts whose terms arechanged before expiry

Evaluation of “Ordinary course of business”• Whether the transaction is covered in the objects of the company as

envisaged in the Memorandum of Association

• Whether a transaction is usual or unusual, both from the company and

its line of business perspective

• Frequency: If a transaction is happening quite frequently over a period

of time, it is more likely to be treated as an ordinary course of business.

However, the inverse does not necessarily hold true

• Whether transaction is taking place at arm’s length

• Business purpose of the transaction

• Whether transaction is done on similar basis with other third parties;

• Size and volume of transaction.

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 18

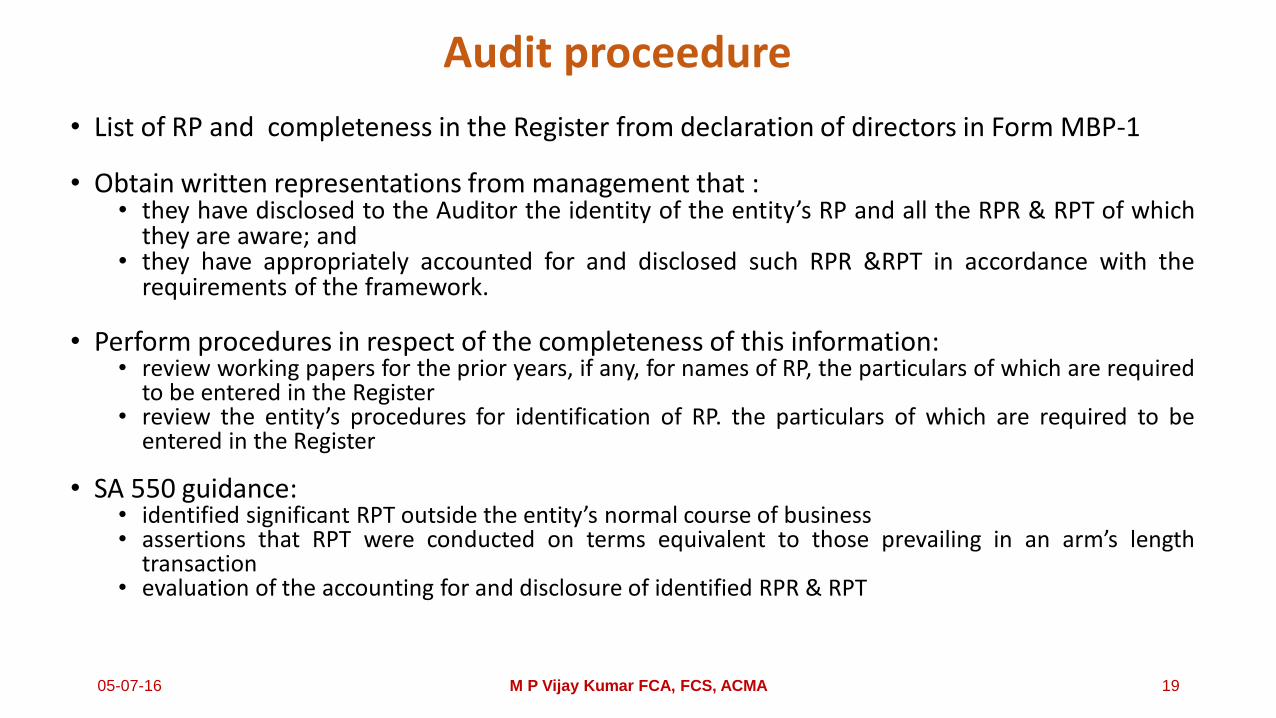

Audit proceedure

• List of RP and completeness in the Register from declaration of directors in Form MBP-1

• Obtain written representations from management that :• they have disclosed to the Auditor the identity of the entity’s RP and all the RPR & RPT of which

they are aware; and• they have appropriately accounted for and disclosed such RPR &RPT in accordance with the

requirements of the framework.

• Perform procedures in respect of the completeness of this information:• review working papers for the prior years, if any, for names of RP, the particulars of which are required

to be entered in the Register• review the entity’s procedures for identification of RP. the particulars of which are required to be

entered in the Register

• SA 550 guidance:• identified significant RPT outside the entity’s normal course of business• assertions that RPT were conducted on terms equivalent to those prevailing in an arm’s length

transaction• evaluation of the accounting for and disclosure of identified RPR & RPT

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 19

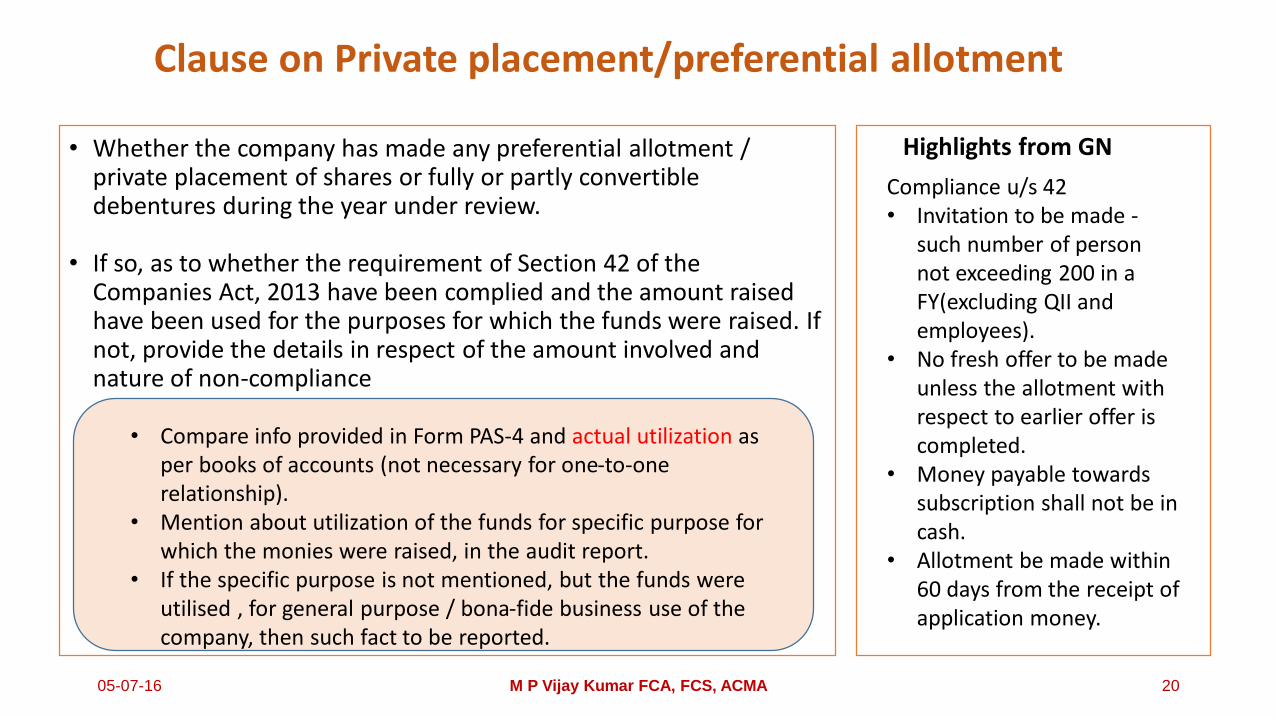

• Whether the company has made any preferential allotment / private placement of shares or fully or partly convertible debentures during the year under review.

• If so, as to whether the requirement of Section 42 of the Companies Act, 2013 have been complied and the amount raised have been used for the purposes for which the funds were raised. If not, provide the details in respect of the amount involved and nature of non-compliance

Highlights from GN

Compliance u/s 42 • Invitation to be made -

such number of person not exceeding 200 in a FY(excluding QII and employees).

• No fresh offer to be made unless the allotment with respect to earlier offer is completed.

• Money payable towards subscription shall not be in cash.

• Allotment be made within 60 days from the receipt of application money.

• Compare info provided in Form PAS-4 and actual utilization as per books of accounts (not necessary for one-to-one relationship).

• Mention about utilization of the funds for specific purpose for which the monies were raised, in the audit report.

• If the specific purpose is not mentioned, but the funds were utilised , for general purpose / bona-fide business use of the company, then such fact to be reported.

Clause on Private placement/preferential allotment

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 20

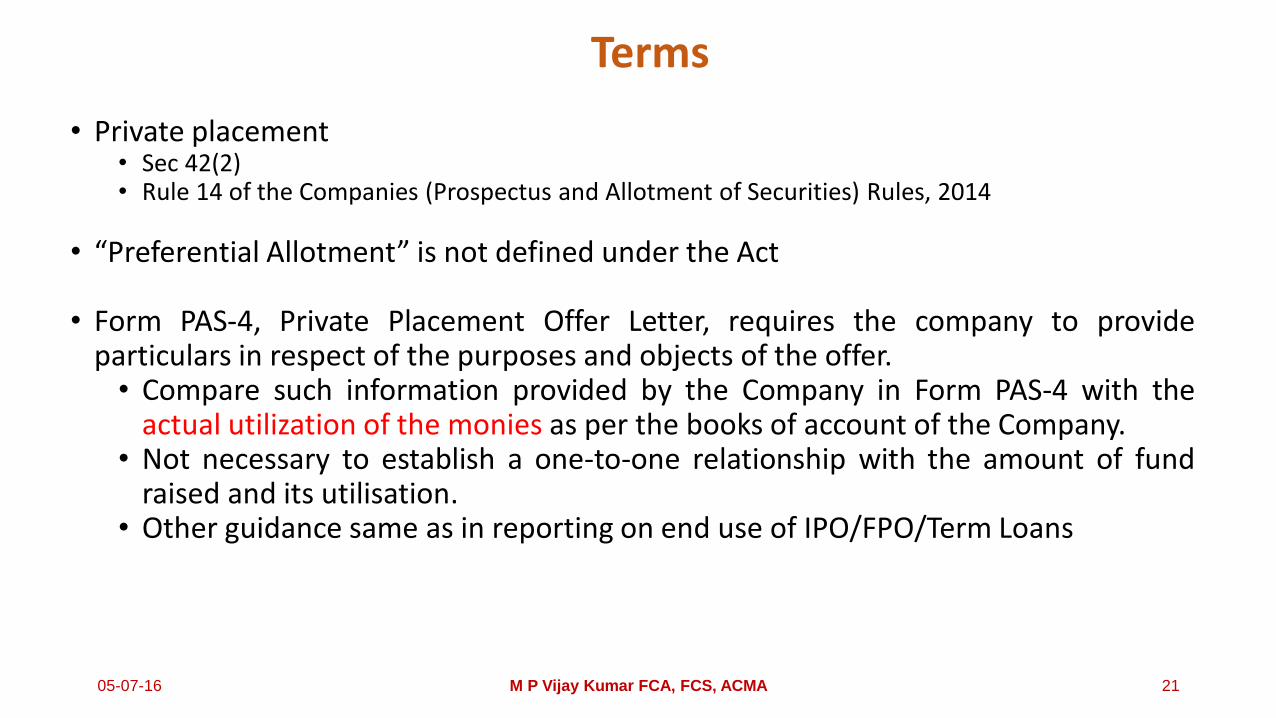

Terms

• Private placement • Sec 42(2)• Rule 14 of the Companies (Prospectus and Allotment of Securities) Rules, 2014

• “Preferential Allotment” is not defined under the Act

• Form PAS-4, Private Placement Offer Letter, requires the company to provideparticulars in respect of the purposes and objects of the offer.• Compare such information provided by the Company in Form PAS-4 with the

actual utilization of the monies as per the books of account of the Company.• Not necessary to establish a one-to-one relationship with the amount of fund

raised and its utilisation.• Other guidance same as in reporting on end use of IPO/FPO/Term Loans

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 21

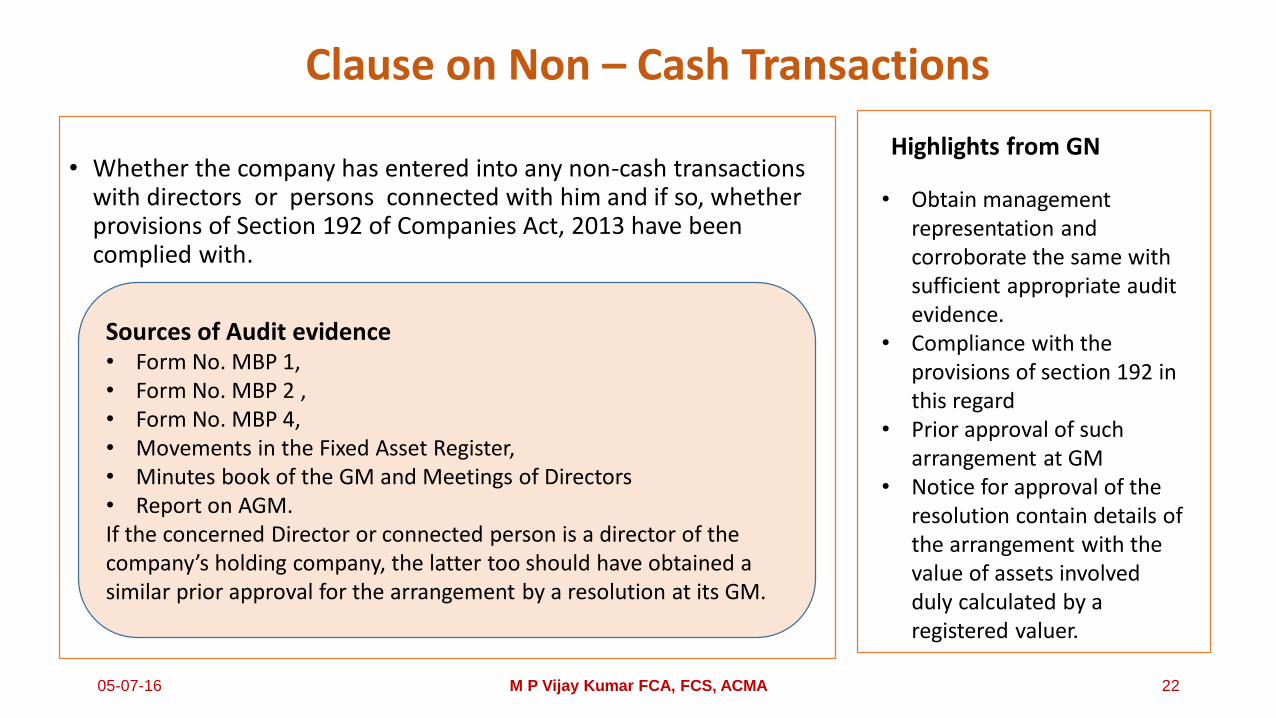

• Whether the company has entered into any non-cash transactions with directors or persons connected with him and if so, whether provisions of Section 192 of Companies Act, 2013 have been complied with.

Highlights from GN

• Obtain management representation and corroborate the same with sufficient appropriate audit evidence.

• Compliance with the provisions of section 192 in this regard

• Prior approval of such arrangement at GM

• Notice for approval of the resolution contain details of the arrangement with the value of assets involved duly calculated by a registered valuer.

Sources of Audit evidence• Form No. MBP 1,• Form No. MBP 2 ,• Form No. MBP 4,• Movements in the Fixed Asset Register, • Minutes book of the GM and Meetings of Directors • Report on AGM.If the concerned Director or connected person is a director of the company’s holding company, the latter too should have obtained a similar prior approval for the arrangement by a resolution at its GM.

Clause on Non – Cash Transactions

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 22

Terms

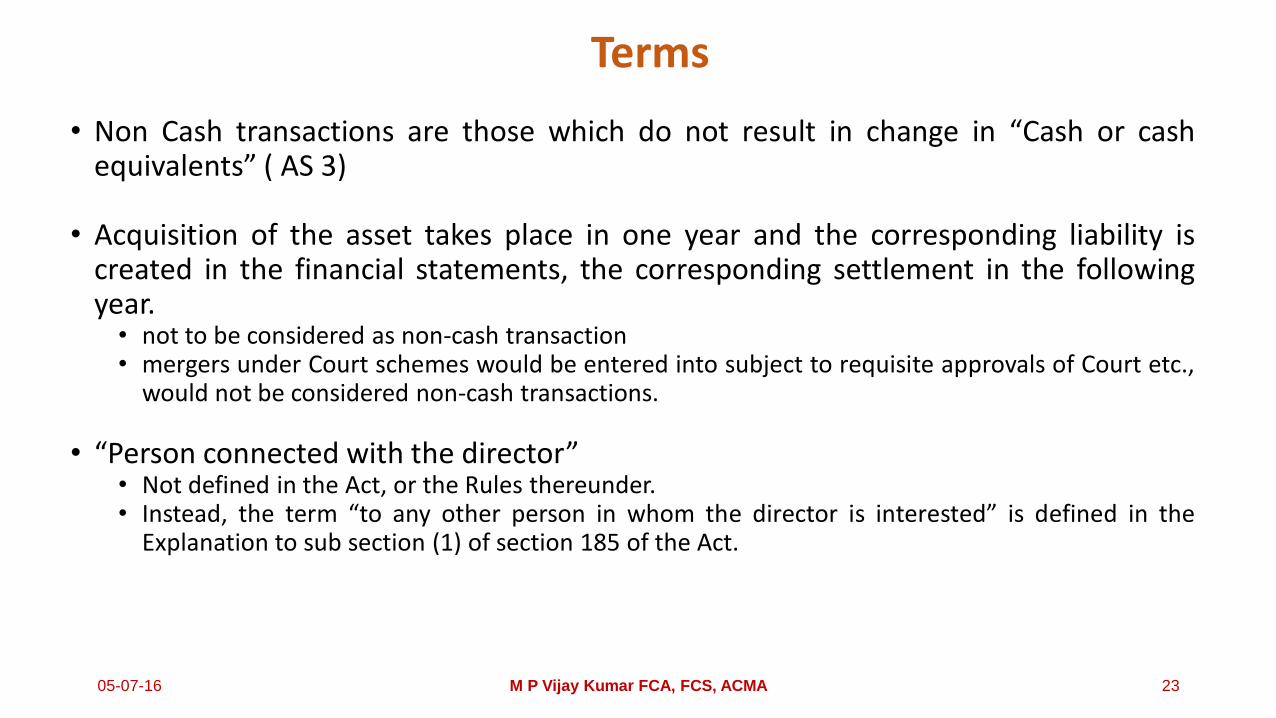

• Non Cash transactions are those which do not result in change in “Cash or cashequivalents” ( AS 3)

• Acquisition of the asset takes place in one year and the corresponding liability iscreated in the financial statements, the corresponding settlement in the followingyear.• not to be considered as non-cash transaction• mergers under Court schemes would be entered into subject to requisite approvals of Court etc.,

would not be considered non-cash transactions.

• “Person connected with the director”• Not defined in the Act, or the Rules thereunder.• Instead, the term “to any other person in whom the director is interested” is defined in the

Explanation to sub section (1) of section 185 of the Act.

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 23

Terms

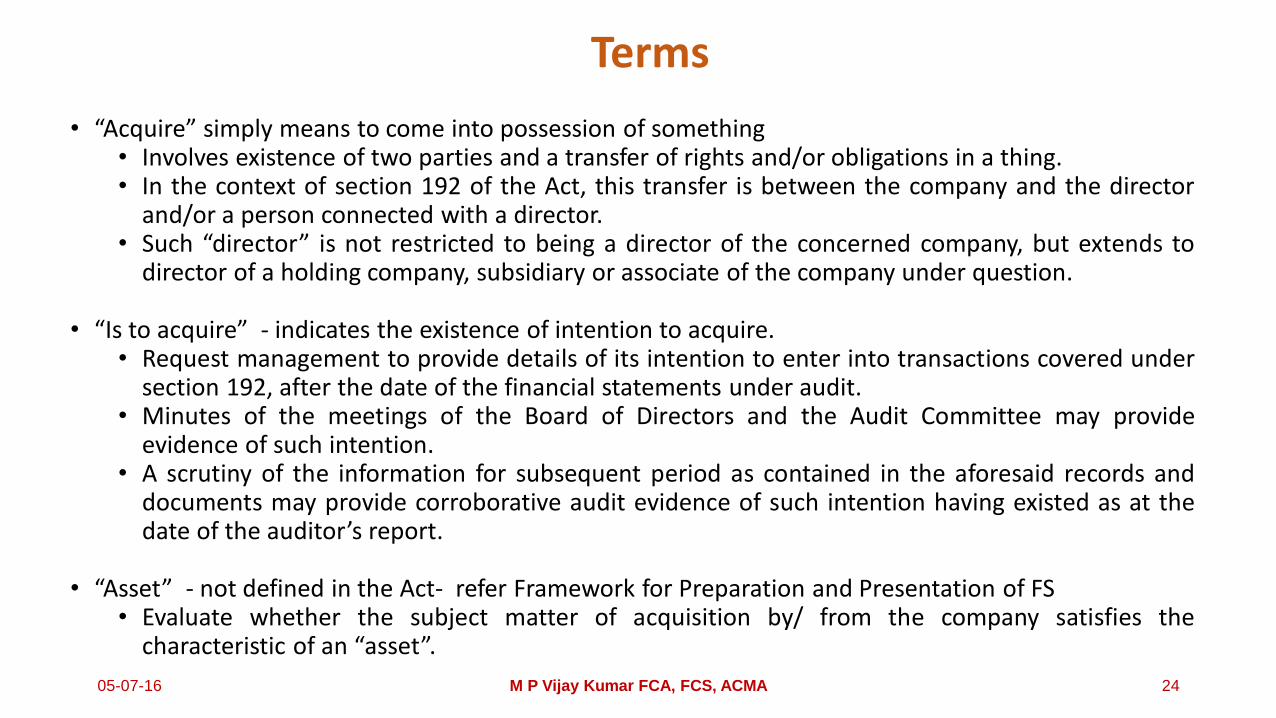

• “Acquire” simply means to come into possession of something• Involves existence of two parties and a transfer of rights and/or obligations in a thing.• In the context of section 192 of the Act, this transfer is between the company and the director

and/or a person connected with a director.• Such “director” is not restricted to being a director of the concerned company, but extends to

director of a holding company, subsidiary or associate of the company under question.

• “Is to acquire” - indicates the existence of intention to acquire.• Request management to provide details of its intention to enter into transactions covered under

section 192, after the date of the financial statements under audit.• Minutes of the meetings of the Board of Directors and the Audit Committee may provide

evidence of such intention.• A scrutiny of the information for subsequent period as contained in the aforesaid records and

documents may provide corroborative audit evidence of such intention having existed as at thedate of the auditor’s report.

• “Asset” - not defined in the Act- refer Framework for Preparation and Presentation of FS• Evaluate whether the subject matter of acquisition by/ from the company satisfies the

characteristic of an “asset”.

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 24

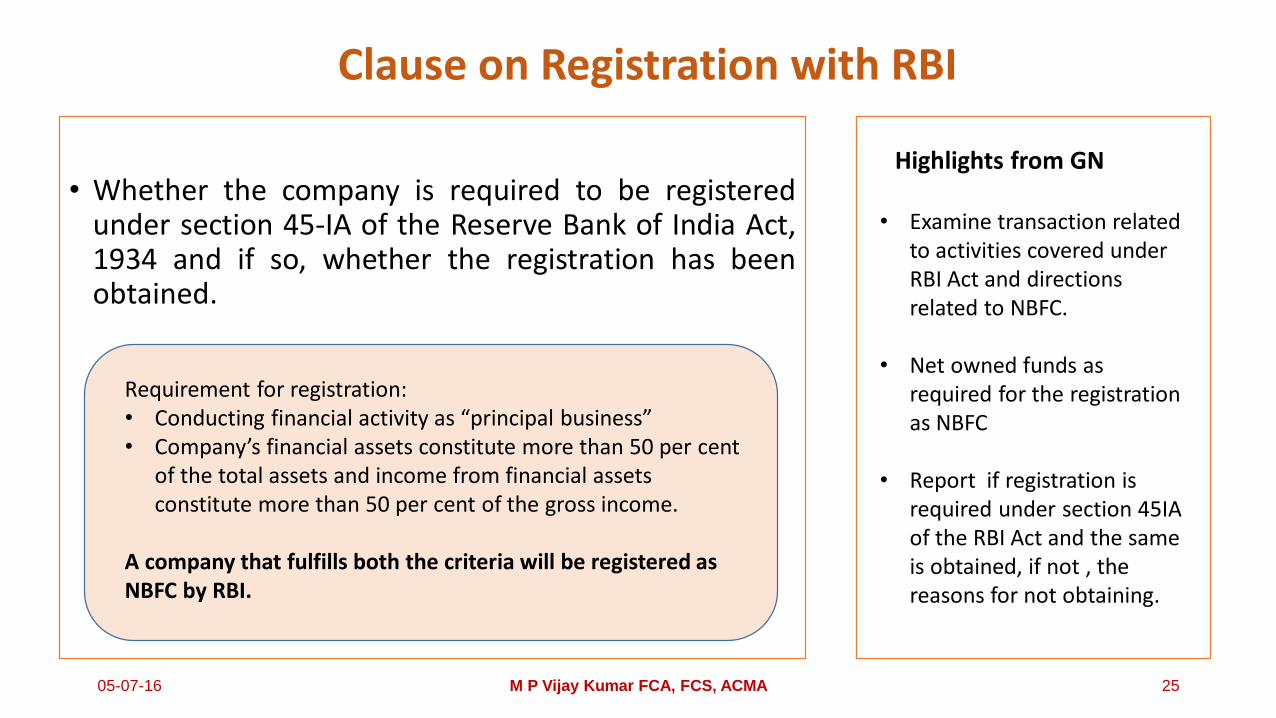

• Whether the company is required to be registeredunder section 45-IA of the Reserve Bank of India Act,1934 and if so, whether the registration has beenobtained.

Highlights from GN

• Examine transaction related to activities covered under RBI Act and directions related to NBFC.

• Net owned funds as required for the registration as NBFC

• Report if registration is required under section 45IA of the RBI Act and the same is obtained, if not , the reasons for not obtaining.

Requirement for registration:• Conducting financial activity as “principal business”• Company’s financial assets constitute more than 50 per cent

of the total assets and income from financial assets constitute more than 50 per cent of the gross income.

A company that fulfills both the criteria will be registered as NBFC by RBI.

Clause on Registration with RBI

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 25

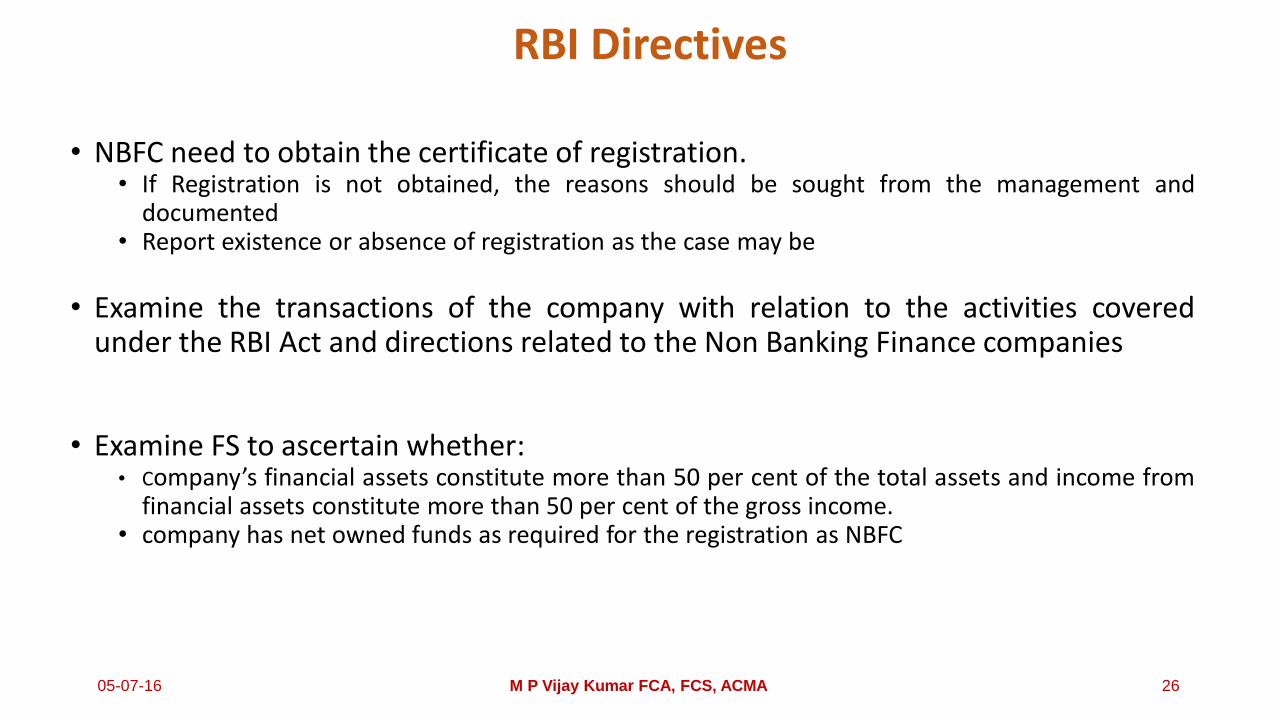

RBI Directives

• NBFC need to obtain the certificate of registration.• If Registration is not obtained, the reasons should be sought from the management and

documented• Report existence or absence of registration as the case may be

• Examine the transactions of the company with relation to the activities coveredunder the RBI Act and directions related to the Non Banking Finance companies

• Examine FS to ascertain whether:• Company’s financial assets constitute more than 50 per cent of the total assets and income from

financial assets constitute more than 50 per cent of the gross income.• company has net owned funds as required for the registration as NBFC

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 26

modified clauses17 slides (27-43)

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 27

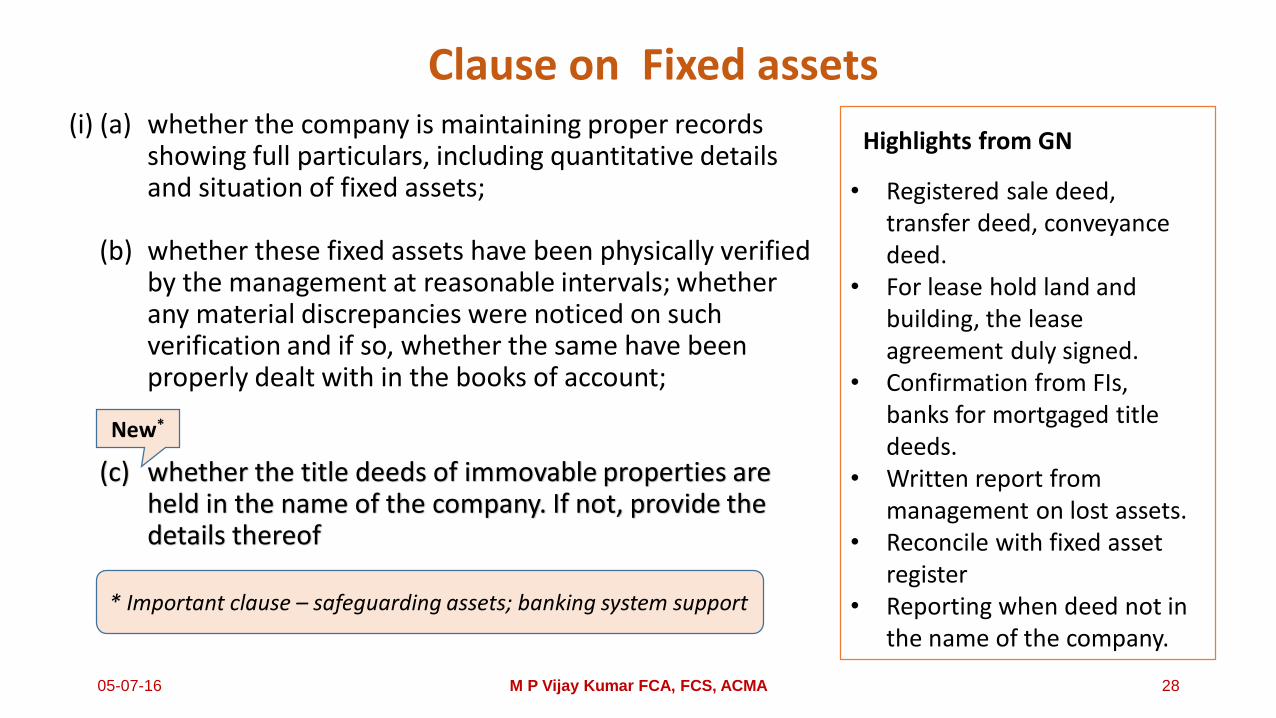

(i) (a) whether the company is maintaining proper records showing full particulars, including quantitative details and situation of fixed assets;

(b) whether these fixed assets have been physically verified by the management at reasonable intervals; whether any material discrepancies were noticed on such verification and if so, whether the same have been properly dealt with in the books of account;

(c) whether the title deeds of immovable properties are held in the name of the company. If not, provide the details thereof

• Registered sale deed, transfer deed, conveyance deed.

• For lease hold land and building, the lease agreement duly signed.

• Confirmation from FIs, banks for mortgaged title deeds.

• Written report from management on lost assets.

• Reconcile with fixed asset register

• Reporting when deed not in the name of the company.

Highlights from GN

New*

* Important clause – safeguarding assets; banking system support

Clause on Fixed assets

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 28

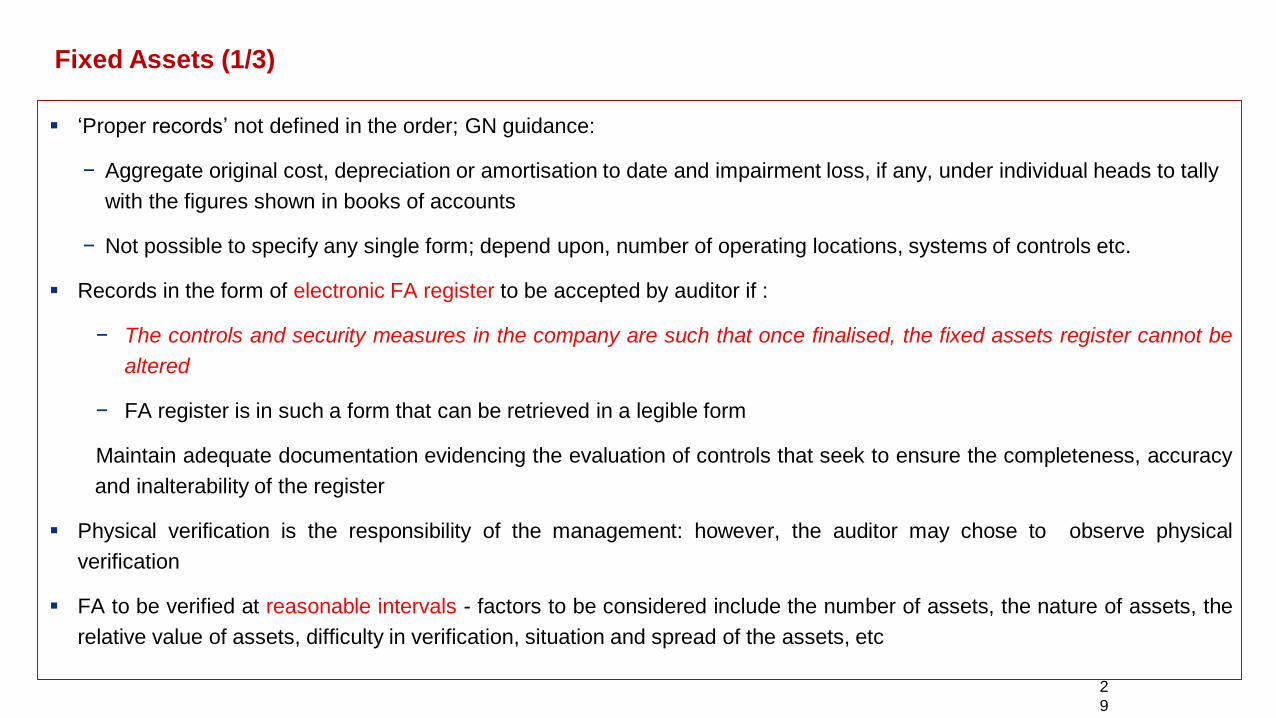

Fixed Assets (1/3)

‘Proper records’ not defined in the order; GN guidance:

− Aggregate original cost, depreciation or amortisation to date and impairment loss, if any, under individual heads to tally

with the figures shown in books of accounts

− Not possible to specify any single form; depend upon, number of operating locations, systems of controls etc.

Records in the form of electronic FA register to be accepted by auditor if :

− The controls and security measures in the company are such that once finalised, the fixed assets register cannot be

altered

− FA register is in such a form that can be retrieved in a legible form

Maintain adequate documentation evidencing the evaluation of controls that seek to ensure the completeness, accuracy

and inalterability of the register

Physical verification is the responsibility of the management: however, the auditor may chose to observe physical

verification

FA to be verified at reasonable intervals - factors to be considered include the number of assets, the nature of assets, the

relative value of assets, difficulty in verification, situation and spread of the assets, etc

2

9

Fixed Assets (2/3)

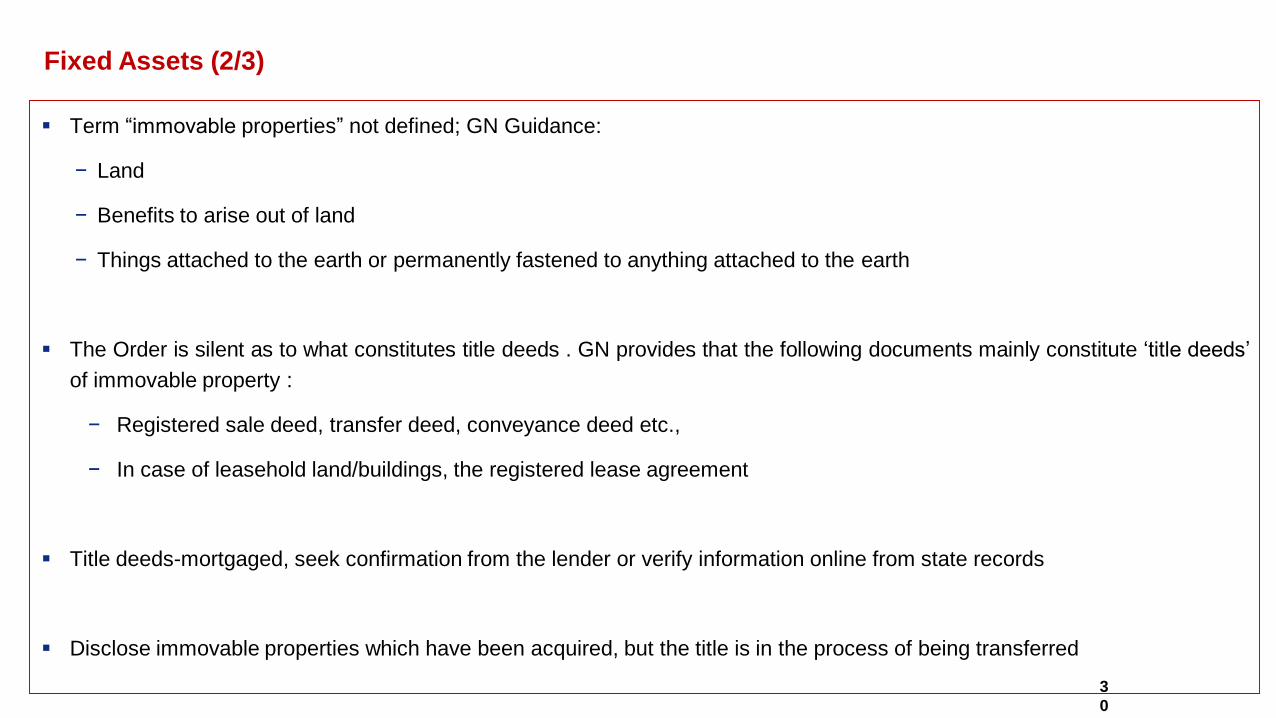

Term “immovable properties” not defined; GN Guidance:

− Land

− Benefits to arise out of land

− Things attached to the earth or permanently fastened to anything attached to the earth

The Order is silent as to what constitutes title deeds . GN provides that the following documents mainly constitute ‘title deeds’

of immovable property :

− Registered sale deed, transfer deed, conveyance deed etc.,

− In case of leasehold land/buildings, the registered lease agreement

Title deeds-mortgaged, seek confirmation from the lender or verify information online from state records

Disclose immovable properties which have been acquired, but the title is in the process of being transferred

3

0

Fixed Assets (3/3)

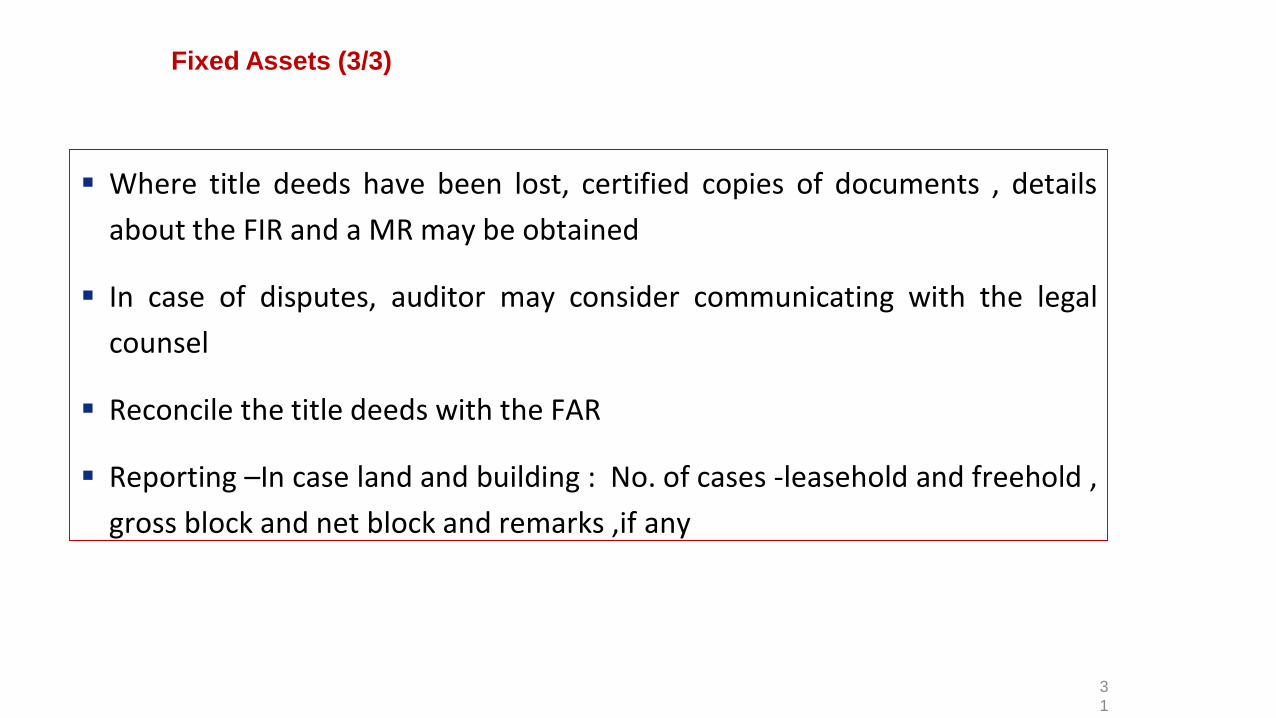

Where title deeds have been lost, certified copies of documents , details

about the FIR and a MR may be obtained

In case of disputes, auditor may consider communicating with the legal

counsel

Reconcile the title deeds with the FAR

Reporting –In case land and building : No. of cases -leasehold and freehold ,

gross block and net block and remarks ,if any

3

1

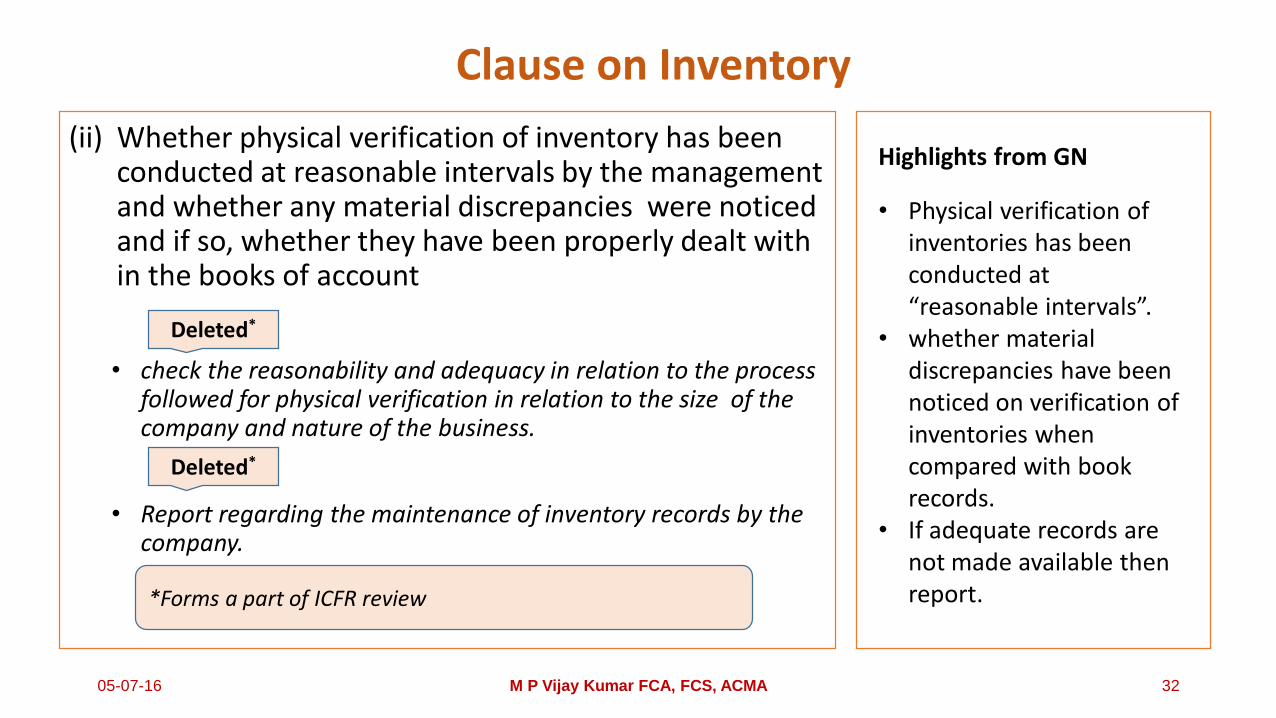

(ii) Whether physical verification of inventory has been conducted at reasonable intervals by the management and whether any material discrepancies were noticed and if so, whether they have been properly dealt with in the books of account

• check the reasonability and adequacy in relation to the process followed for physical verification in relation to the size of the company and nature of the business.

• Report regarding the maintenance of inventory records by the company.

Highlights from GN

• Physical verification of inventories has been conducted at “reasonable intervals”.

• whether material discrepancies have been noticed on verification of inventories when compared with book records.

• If adequate records are not made available then report.

Deleted*

*Forms a part of ICFR review

Deleted*

Clause on Inventory

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 32

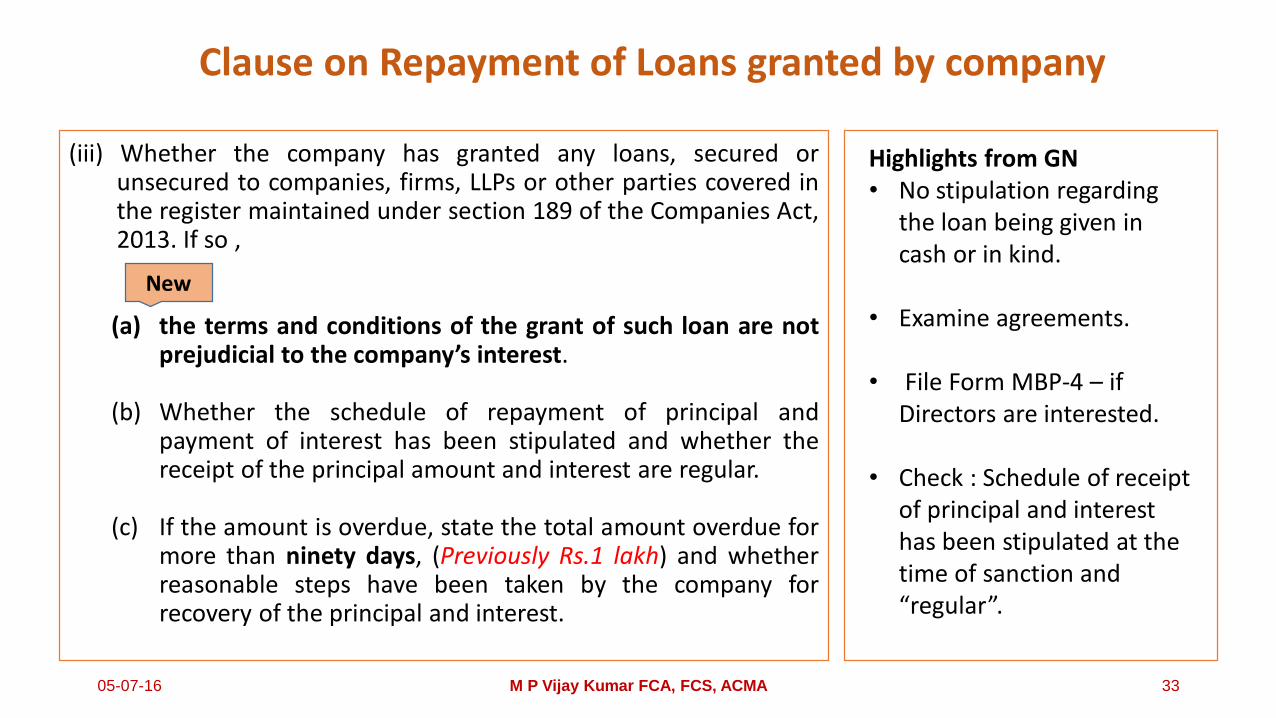

(iii) Whether the company has granted any loans, secured orunsecured to companies, firms, LLPs or other parties covered inthe register maintained under section 189 of the Companies Act,2013. If so ,

(a) the terms and conditions of the grant of such loan are notprejudicial to the company’s interest.

(b) Whether the schedule of repayment of principal andpayment of interest has been stipulated and whether thereceipt of the principal amount and interest are regular.

(c) If the amount is overdue, state the total amount overdue formore than ninety days, (Previously Rs.1 lakh) and whetherreasonable steps have been taken by the company forrecovery of the principal and interest.

Highlights from GN• No stipulation regarding

the loan being given in cash or in kind.

• Examine agreements.

• File Form MBP-4 – if Directors are interested.

• Check : Schedule of receipt of principal and interest has been stipulated at the time of sanction and “regular”.

New

Clause on Repayment of Loans granted by company

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 33

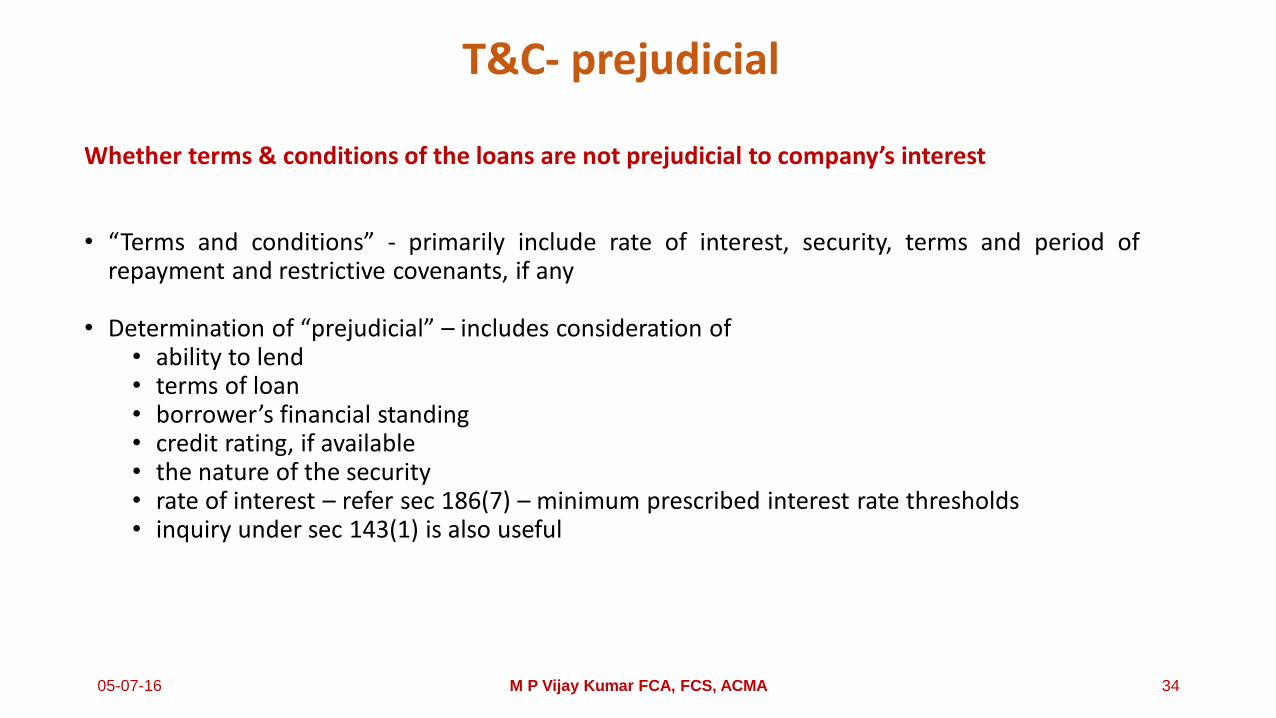

T&C- prejudicial

Whether terms & conditions of the loans are not prejudicial to company’s interest

• “Terms and conditions” - primarily include rate of interest, security, terms and period ofrepayment and restrictive covenants, if any

• Determination of “prejudicial” – includes consideration of• ability to lend• terms of loan• borrower’s financial standing• credit rating, if available• the nature of the security• rate of interest – refer sec 186(7) – minimum prescribed interest rate thresholds• inquiry under sec 143(1) is also useful

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 34

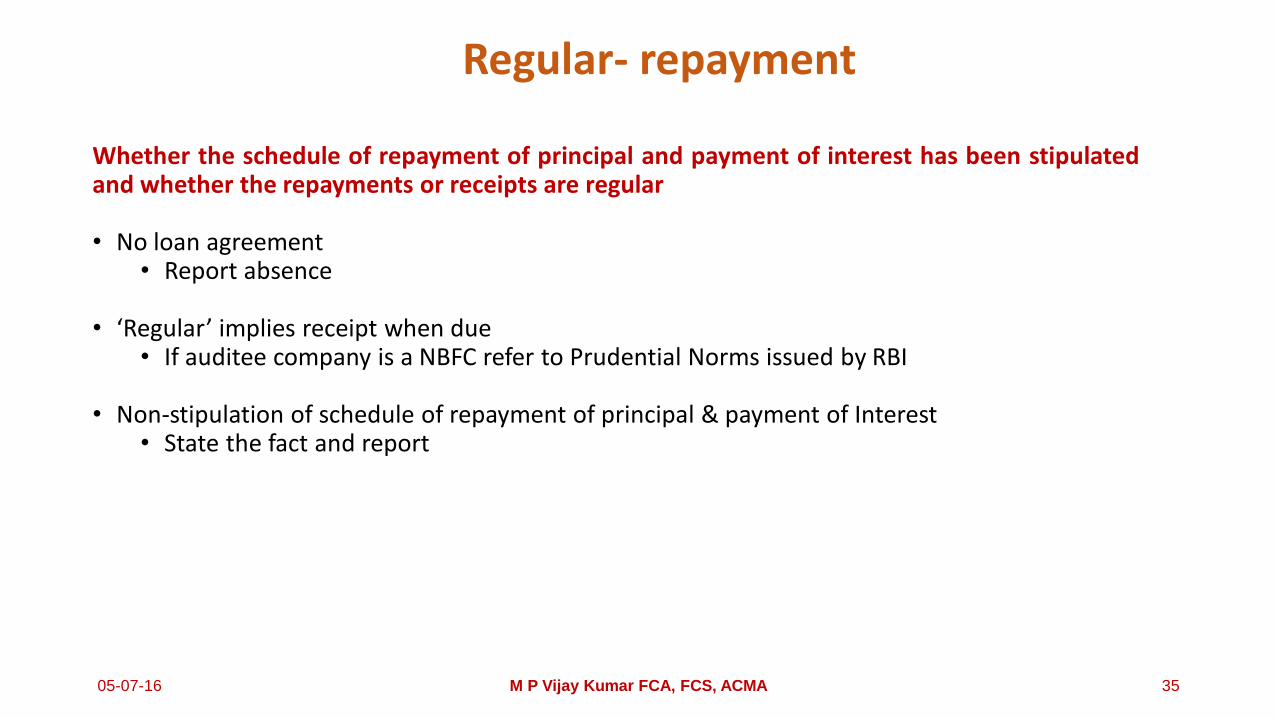

Regular- repayment

Whether the schedule of repayment of principal and payment of interest has been stipulatedand whether the repayments or receipts are regular

• No loan agreement• Report absence

• ‘Regular’ implies receipt when due• If auditee company is a NBFC refer to Prudential Norms issued by RBI

• Non-stipulation of schedule of repayment of principal & payment of Interest• State the fact and report

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 35

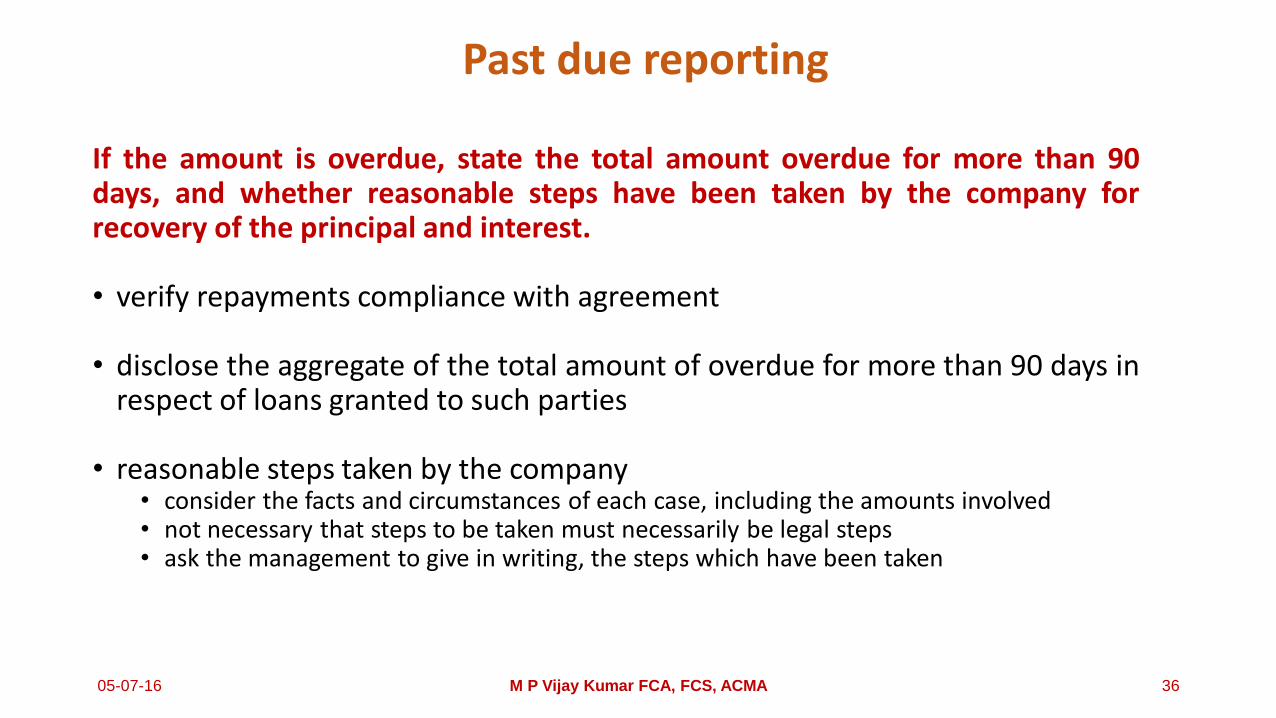

Past due reporting

If the amount is overdue, state the total amount overdue for more than 90days, and whether reasonable steps have been taken by the company forrecovery of the principal and interest.

• verify repayments compliance with agreement

• disclose the aggregate of the total amount of overdue for more than 90 days inrespect of loans granted to such parties

• reasonable steps taken by the company• consider the facts and circumstances of each case, including the amounts involved• not necessary that steps to be taken must necessarily be legal steps• ask the management to give in writing, the steps which have been taken

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 36

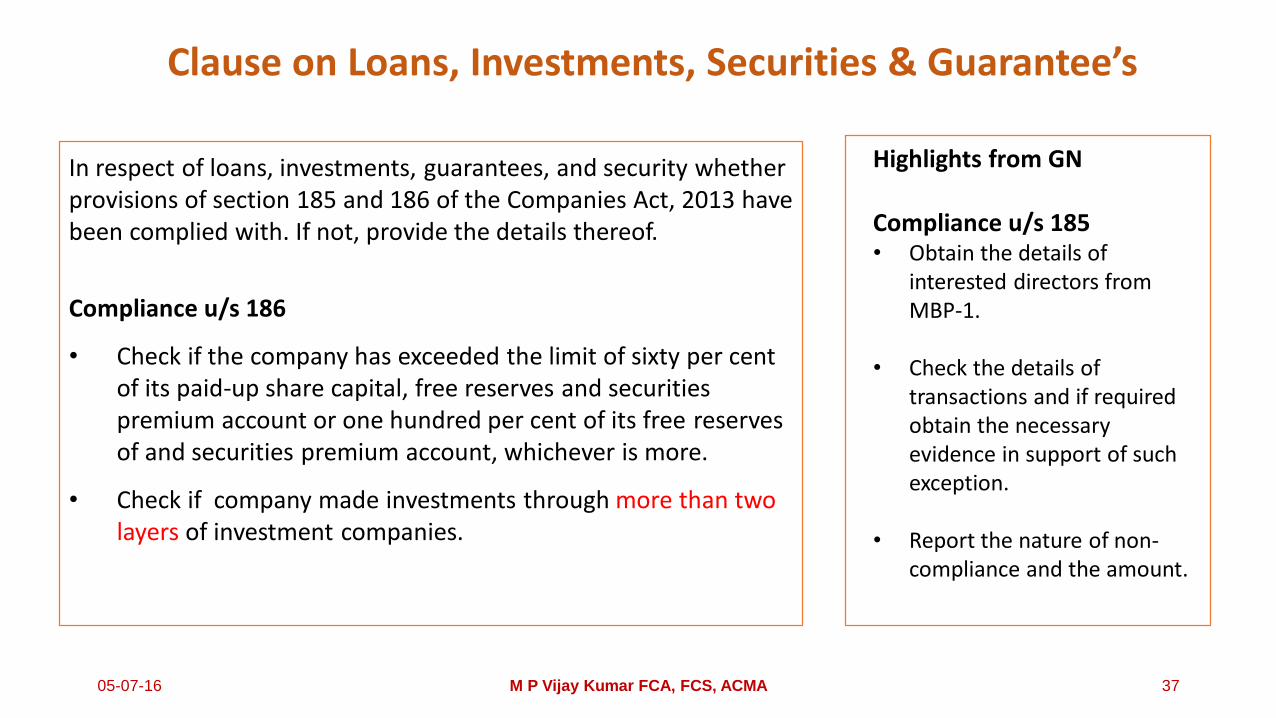

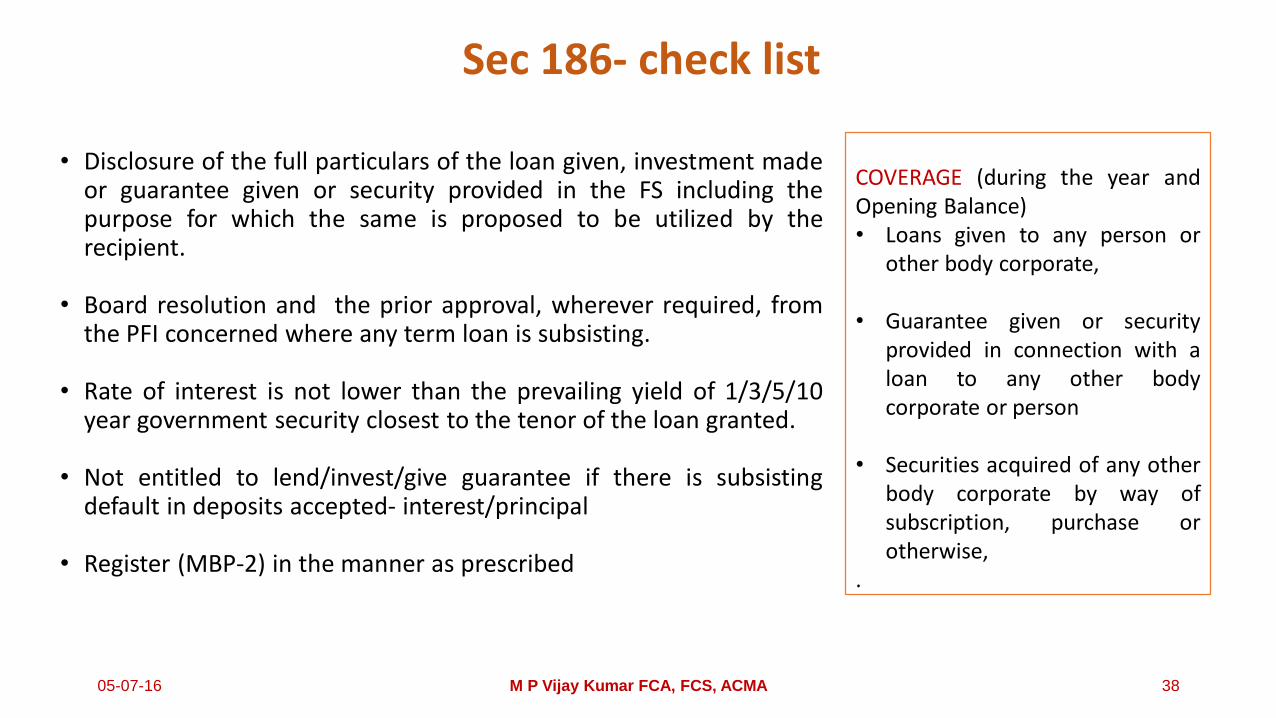

In respect of loans, investments, guarantees, and security whether provisions of section 185 and 186 of the Companies Act, 2013 have been complied with. If not, provide the details thereof.

Compliance u/s 186

• Check if the company has exceeded the limit of sixty per cent of its paid-up share capital, free reserves and securities premium account or one hundred per cent of its free reserves of and securities premium account, whichever is more.

• Check if company made investments through more than two layers of investment companies.

Highlights from GN

Compliance u/s 185• Obtain the details of

interested directors from MBP-1.

• Check the details of transactions and if required obtain the necessary evidence in support of such exception.

• Report the nature of non-compliance and the amount.

Clause on Loans, Investments, Securities & Guarantee’s

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 37

Sec 186- check list

• Disclosure of the full particulars of the loan given, investment madeor guarantee given or security provided in the FS including thepurpose for which the same is proposed to be utilized by therecipient.

• Board resolution and the prior approval, wherever required, fromthe PFI concerned where any term loan is subsisting.

• Rate of interest is not lower than the prevailing yield of 1/3/5/10year government security closest to the tenor of the loan granted.

• Not entitled to lend/invest/give guarantee if there is subsistingdefault in deposits accepted- interest/principal

• Register (MBP-2) in the manner as prescribed

COVERAGE (during the year andOpening Balance)• Loans given to any person or

other body corporate,

• Guarantee given or securityprovided in connection with aloan to any other bodycorporate or person

• Securities acquired of any otherbody corporate by way ofsubscription, purchase orotherwise,

.

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 38

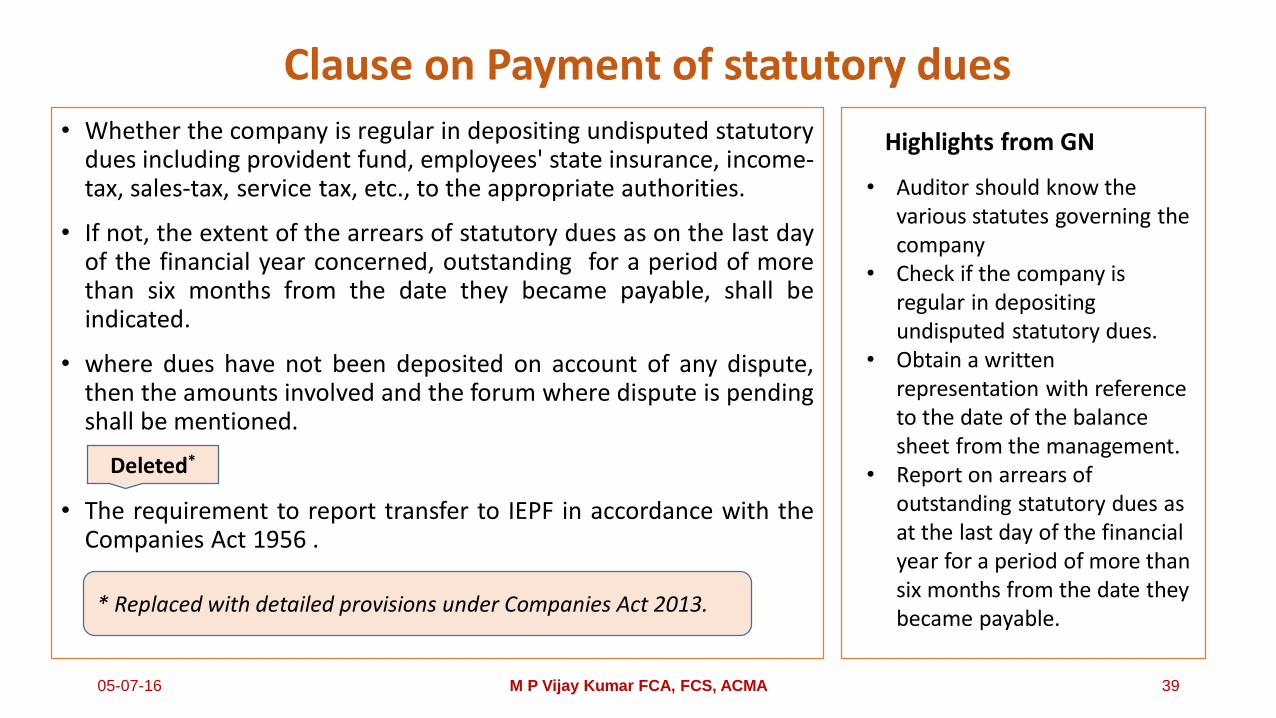

• Whether the company is regular in depositing undisputed statutorydues including provident fund, employees' state insurance, income-tax, sales-tax, service tax, etc., to the appropriate authorities.

• If not, the extent of the arrears of statutory dues as on the last dayof the financial year concerned, outstanding for a period of morethan six months from the date they became payable, shall beindicated.

• where dues have not been deposited on account of any dispute,then the amounts involved and the forum where dispute is pendingshall be mentioned.

• The requirement to report transfer to IEPF in accordance with theCompanies Act 1956 .

Highlights from GN

• Auditor should know the various statutes governing the company

• Check if the company is regular in depositing undisputed statutory dues.

• Obtain a written representation with reference to the date of the balance sheet from the management.

• Report on arrears of outstanding statutory dues as at the last day of the financial year for a period of more than six months from the date they became payable.

Deleted*

* Replaced with detailed provisions under Companies Act 2013.

Clause on Payment of statutory dues

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 39

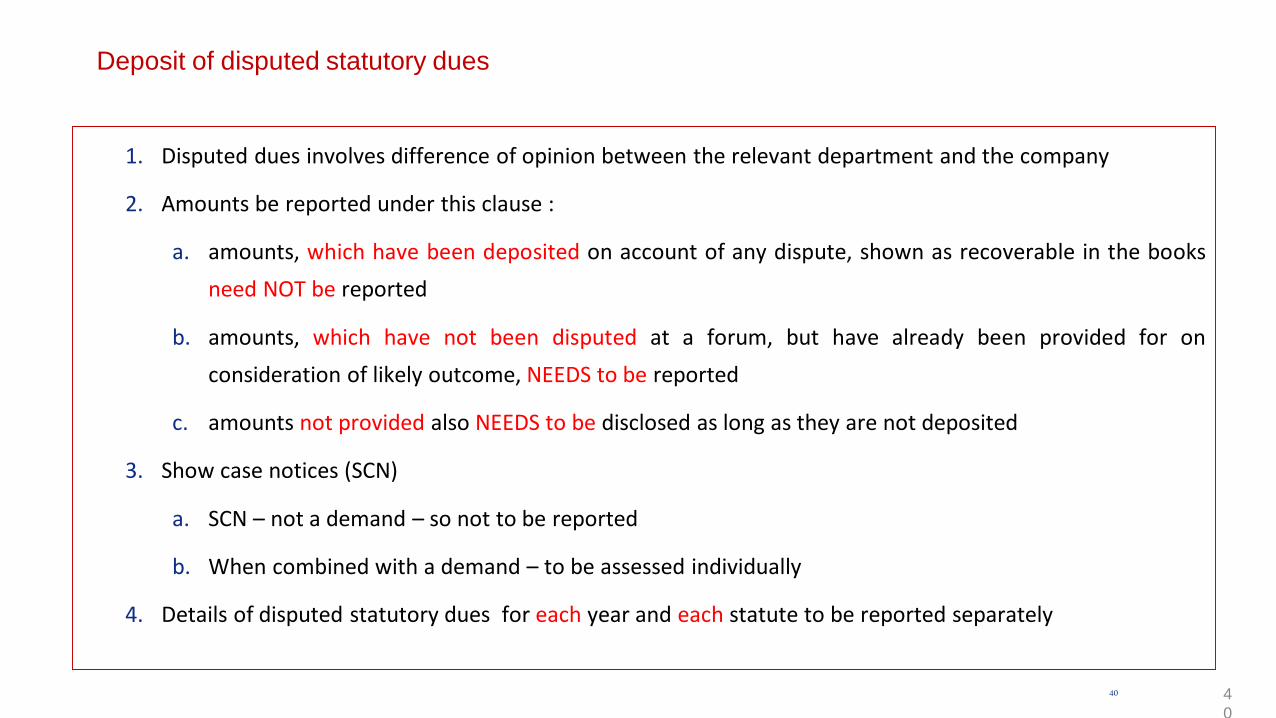

Deposit of disputed statutory dues

1. Disputed dues involves difference of opinion between the relevant department and the company

2. Amounts be reported under this clause :

a. amounts, which have been deposited on account of any dispute, shown as recoverable in the books

need NOT be reported

b. amounts, which have not been disputed at a forum, but have already been provided for on

consideration of likely outcome, NEEDS to be reported

c. amounts not provided also NEEDS to be disclosed as long as they are not deposited

3. Show case notices (SCN)

a. SCN – not a demand – so not to be reported

b. When combined with a demand – to be assessed individually

4. Details of disputed statutory dues for each year and each statute to be reported separately

40 4

0

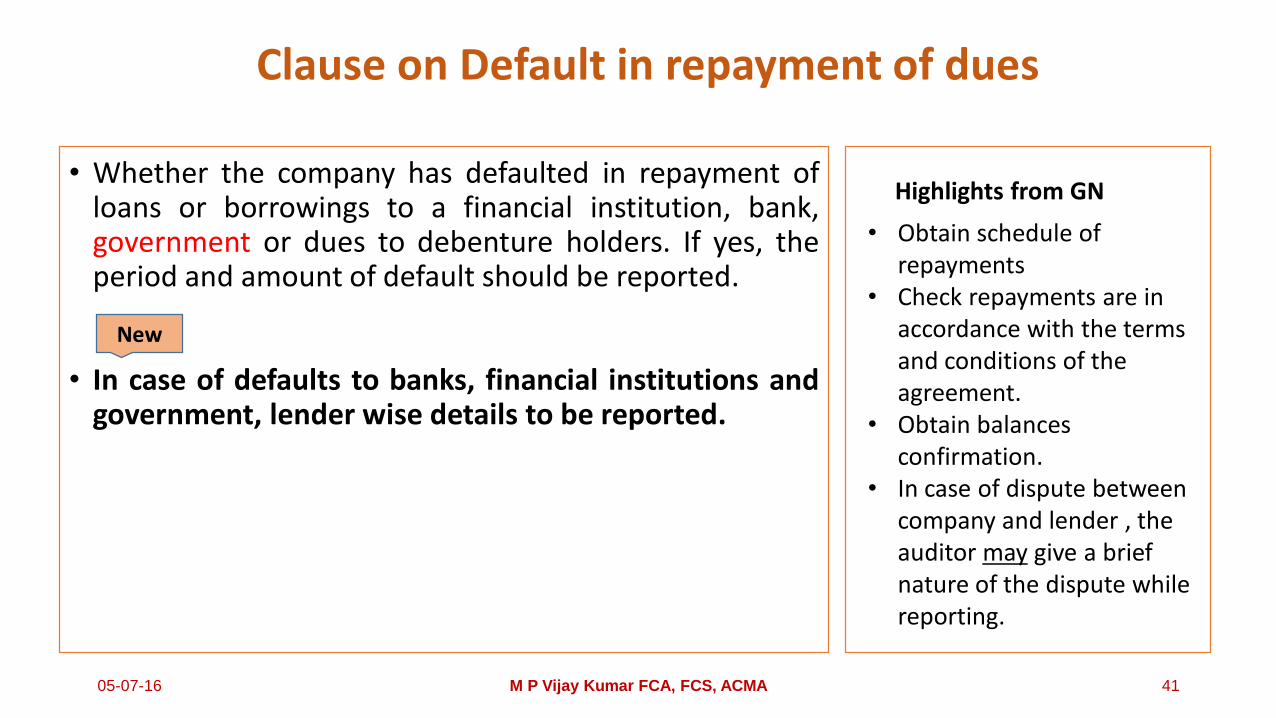

• Whether the company has defaulted in repayment ofloans or borrowings to a financial institution, bank,government or dues to debenture holders. If yes, theperiod and amount of default should be reported.

• In case of defaults to banks, financial institutions andgovernment, lender wise details to be reported.

Highlights from GN

• Obtain schedule of repayments

• Check repayments are in accordance with the terms and conditions of the agreement.

• Obtain balances confirmation.

• In case of dispute between company and lender , the auditor may give a brief nature of the dispute while reporting.

New

Clause on Default in repayment of dues

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 41

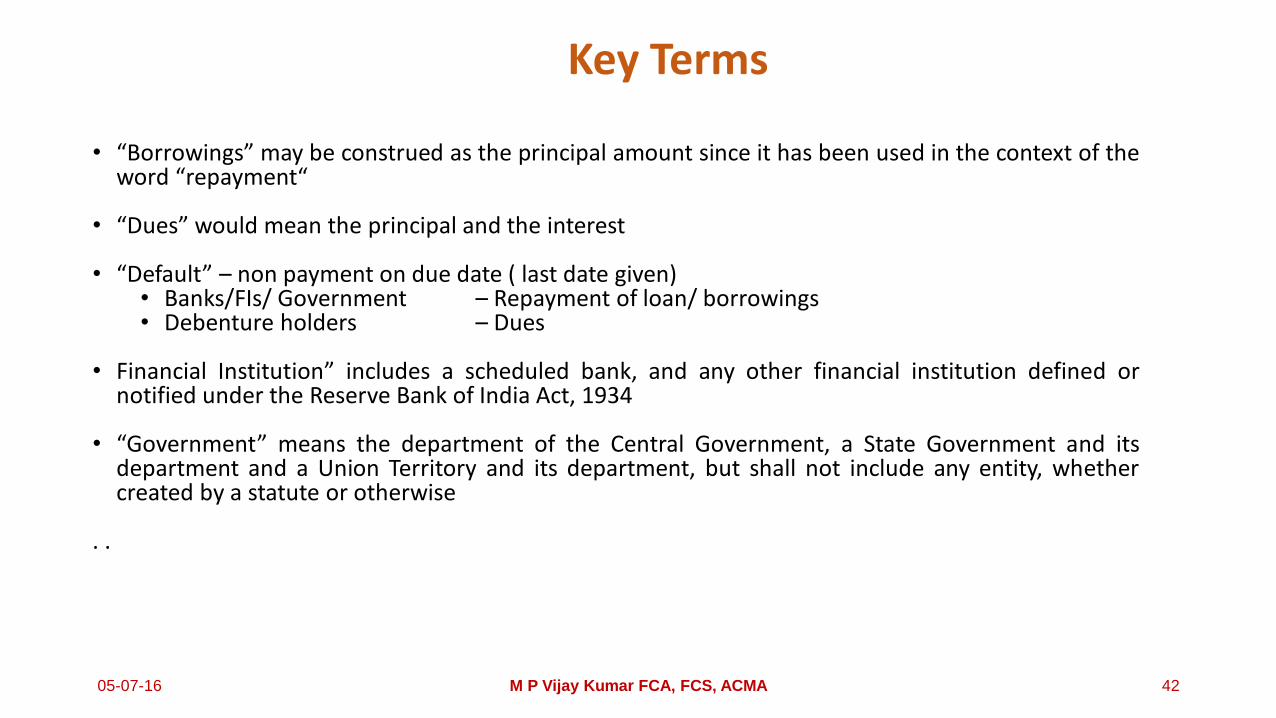

Key Terms

• “Borrowings” may be construed as the principal amount since it has been used in the context of theword “repayment“

• “Dues” would mean the principal and the interest

• “Default” – non payment on due date ( last date given)• Banks/FIs/ Government – Repayment of loan/ borrowings• Debenture holders – Dues

• Financial Institution” includes a scheduled bank, and any other financial institution defined ornotified under the Reserve Bank of India Act, 1934

• “Government” means the department of the Central Government, a State Government and itsdepartment and a Union Territory and its department, but shall not include any entity, whethercreated by a statute or otherwise

. .

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 42

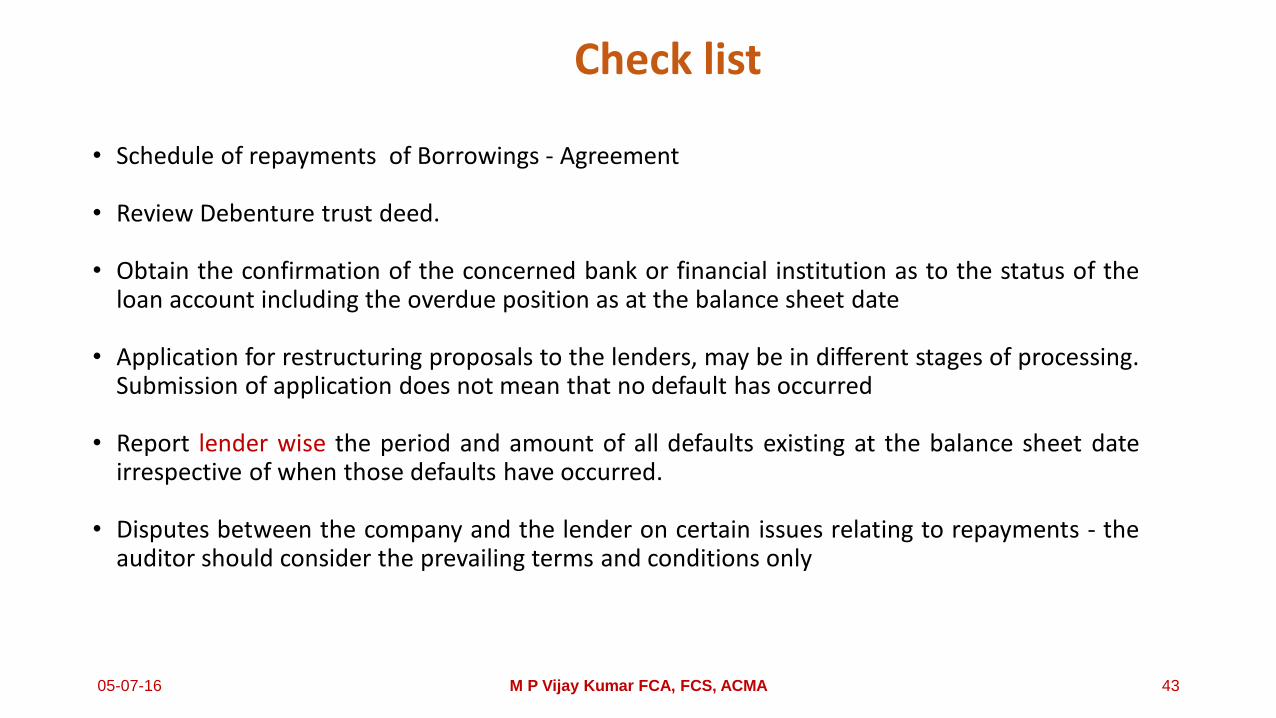

Check list

• Schedule of repayments of Borrowings - Agreement

• Review Debenture trust deed.

• Obtain the confirmation of the concerned bank or financial institution as to the status of theloan account including the overdue position as at the balance sheet date

• Application for restructuring proposals to the lenders, may be in different stages of processing.Submission of application does not mean that no default has occurred

• Report lender wise the period and amount of all defaults existing at the balance sheet dateirrespective of when those defaults have occurred.

• Disputes between the company and the lender on certain issues relating to repayments - theauditor should consider the prevailing terms and conditions only

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 43

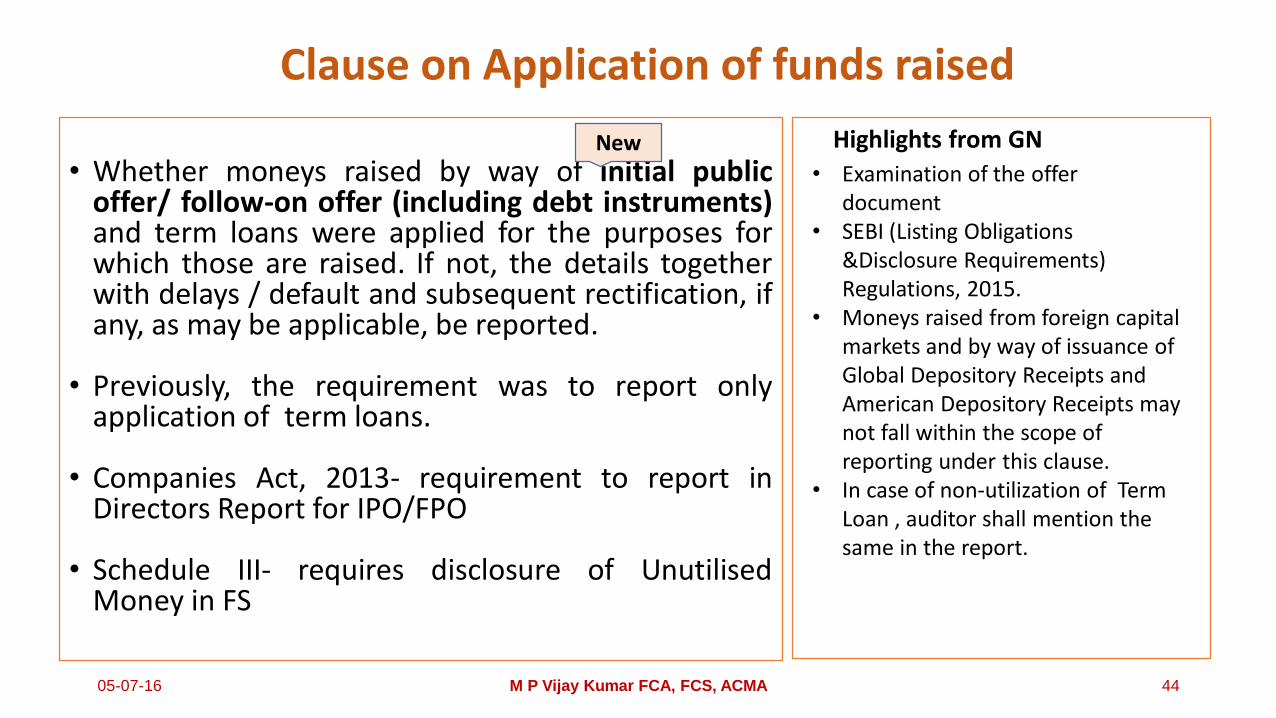

• Whether moneys raised by way of initial publicoffer/ follow-on offer (including debt instruments)and term loans were applied for the purposes forwhich those are raised. If not, the details togetherwith delays / default and subsequent rectification, ifany, as may be applicable, be reported.

• Previously, the requirement was to report onlyapplication of term loans.

• Companies Act, 2013- requirement to report inDirectors Report for IPO/FPO

• Schedule III- requires disclosure of UnutilisedMoney in FS

Highlights from GN

• Examination of the offer document

• SEBI (Listing Obligations &Disclosure Requirements) Regulations, 2015.

• Moneys raised from foreign capital markets and by way of issuance of Global Depository Receipts and American Depository Receipts may not fall within the scope of reporting under this clause.

• In case of non-utilization of Term Loan , auditor shall mention the same in the report.

Clause on Application of funds raised

New

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 44

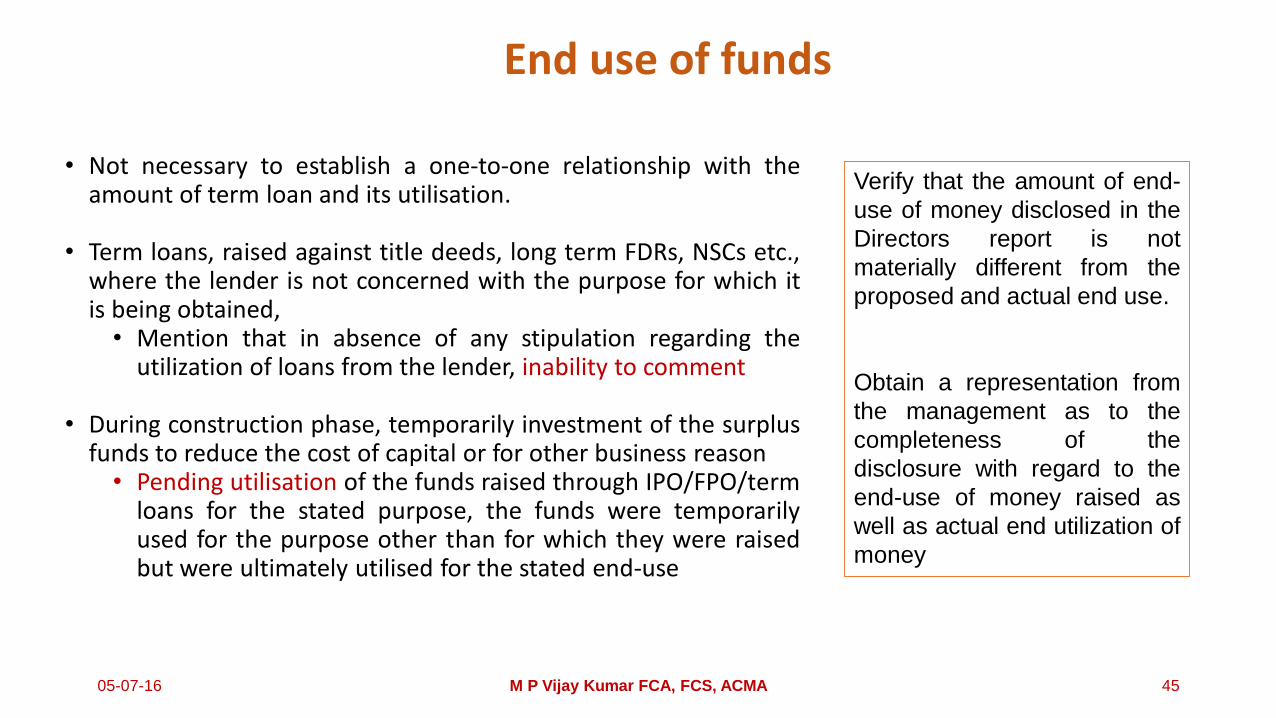

End use of funds

• Not necessary to establish a one-to-one relationship with theamount of term loan and its utilisation.

• Term loans, raised against title deeds, long term FDRs, NSCs etc.,where the lender is not concerned with the purpose for which itis being obtained,• Mention that in absence of any stipulation regarding the

utilization of loans from the lender, inability to comment

• During construction phase, temporarily investment of the surplusfunds to reduce the cost of capital or for other business reason• Pending utilisation of the funds raised through IPO/FPO/term

loans for the stated purpose, the funds were temporarilyused for the purpose other than for which they were raisedbut were ultimately utilised for the stated end-use

Verify that the amount of end-

use of money disclosed in the

Directors report is not

materially different from the

proposed and actual end use.

Obtain a representation from

the management as to the

completeness of the

disclosure with regard to the

end-use of money raised as

well as actual end utilization of

money

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 45

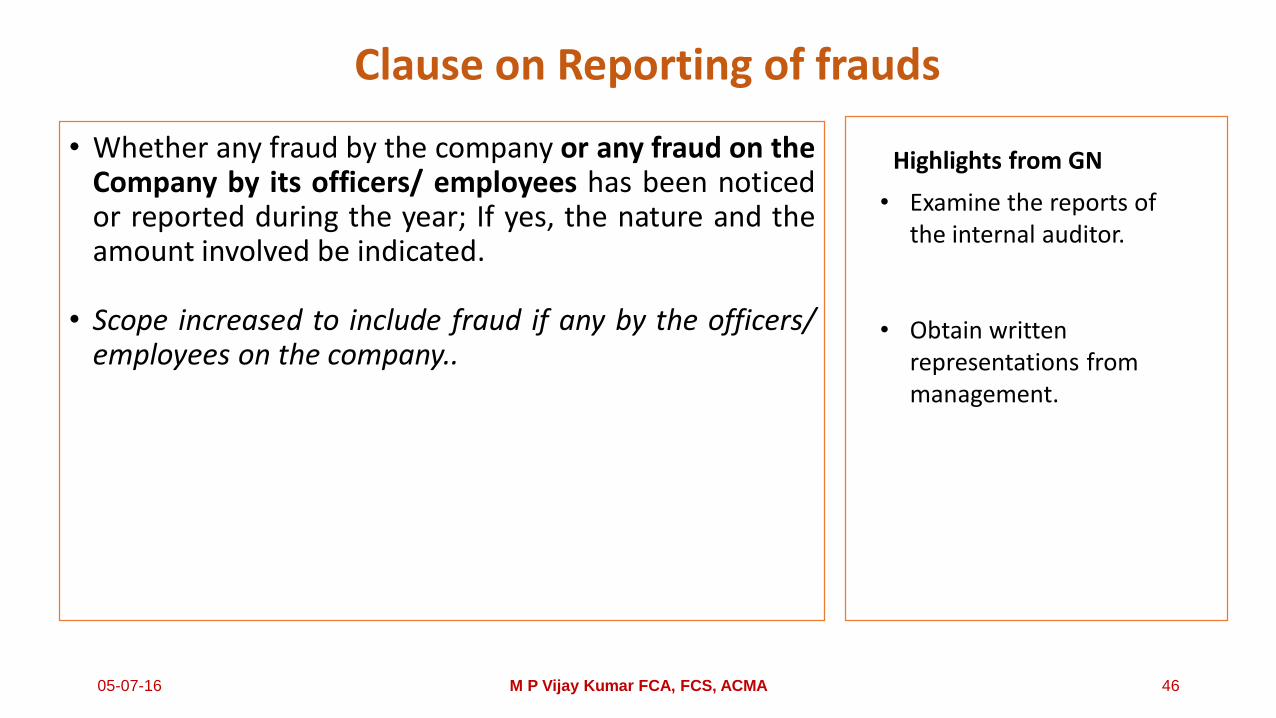

• Whether any fraud by the company or any fraud on theCompany by its officers/ employees has been noticedor reported during the year; If yes, the nature and theamount involved be indicated.

• Scope increased to include fraud if any by the officers/employees on the company..

Highlights from GN

• Examine the reports of the internal auditor.

• Obtain written representations from management.

Clause on Reporting of frauds

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 46

47

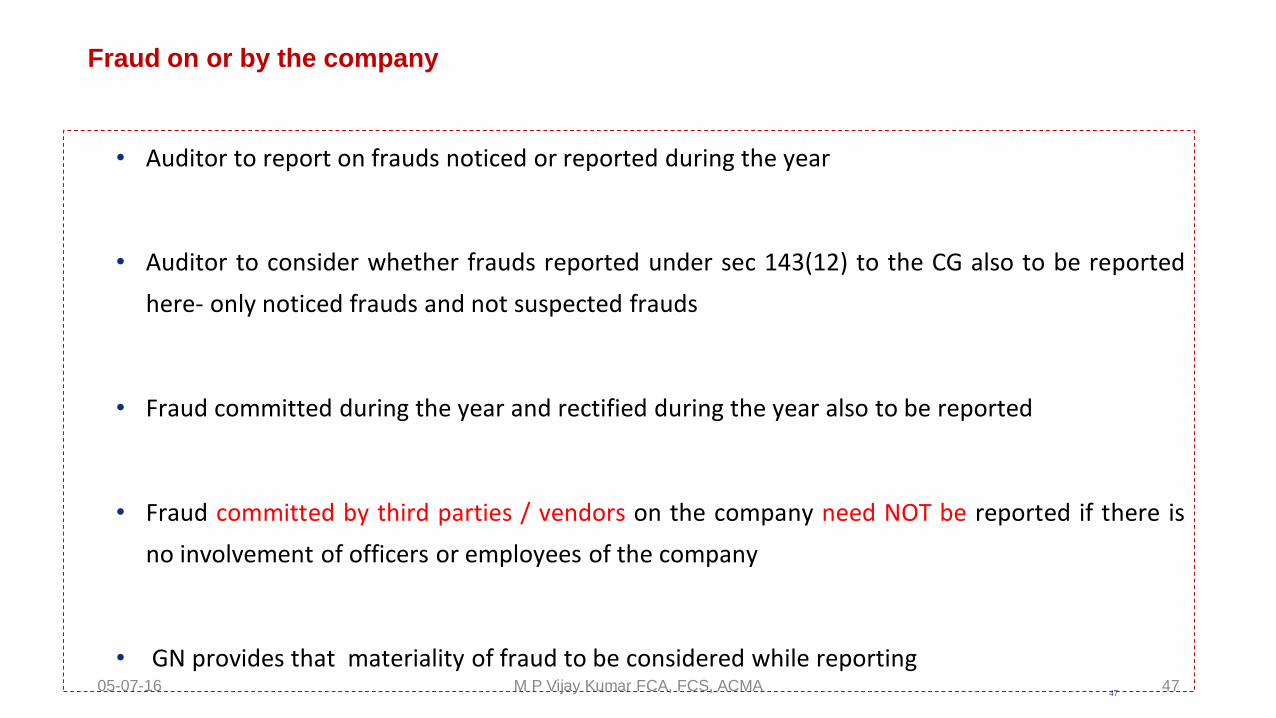

Fraud on or by the company

• Auditor to report on frauds noticed or reported during the year

• Auditor to consider whether frauds reported under sec 143(12) to the CG also to be reported

here- only noticed frauds and not suspected frauds

• Fraud committed during the year and rectified during the year also to be reported

• Fraud committed by third parties / vendors on the company need NOT be reported if there is

no involvement of officers or employees of the company

• GN provides that materiality of fraud to be considered while reporting05-07-16 M P Vijay Kumar FCA, FCS, ACMA 47

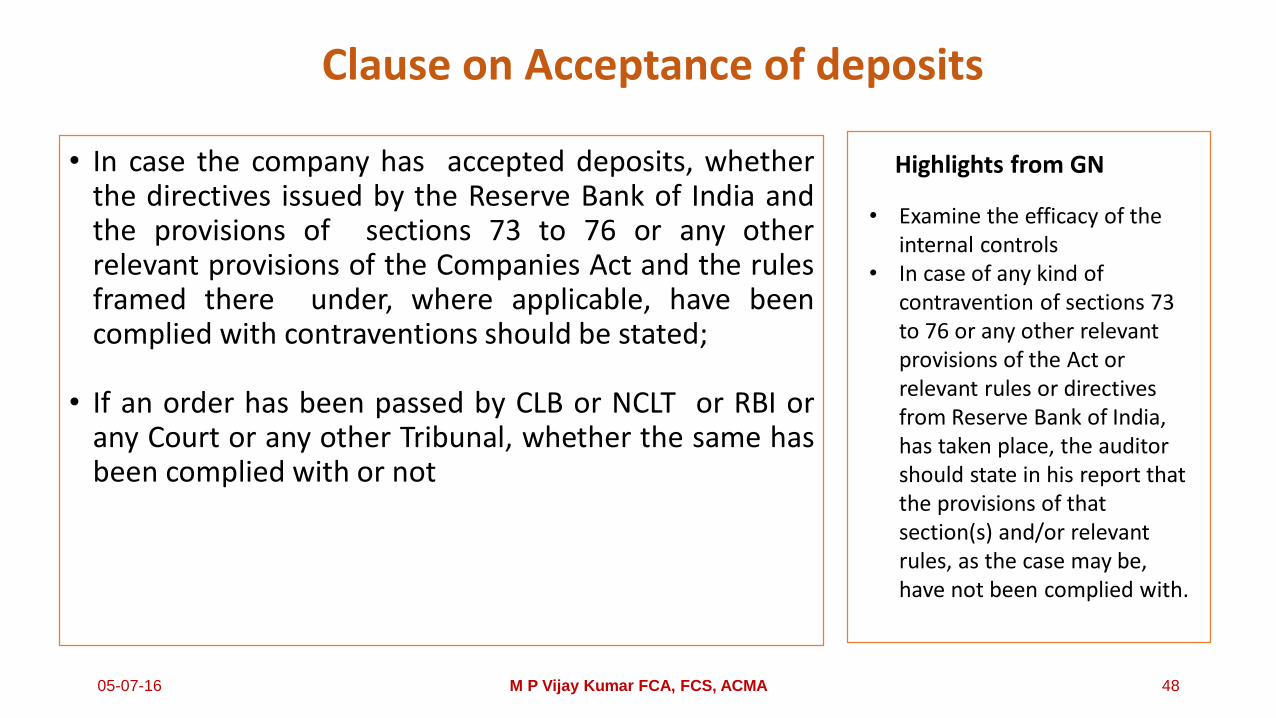

• In case the company has accepted deposits, whetherthe directives issued by the Reserve Bank of India andthe provisions of sections 73 to 76 or any otherrelevant provisions of the Companies Act and the rulesframed there under, where applicable, have beencomplied with contraventions should be stated;

• If an order has been passed by CLB or NCLT or RBI orany Court or any other Tribunal, whether the same hasbeen complied with or not

Highlights from GN

• Examine the efficacy of the internal controls

• In case of any kind of contravention of sections 73 to 76 or any other relevant provisions of the Act or relevant rules or directives from Reserve Bank of India, has taken place, the auditor should state in his report that the provisions of that section(s) and/or relevant rules, as the case may be, have not been complied with.

Clause on Acceptance of deposits

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 48

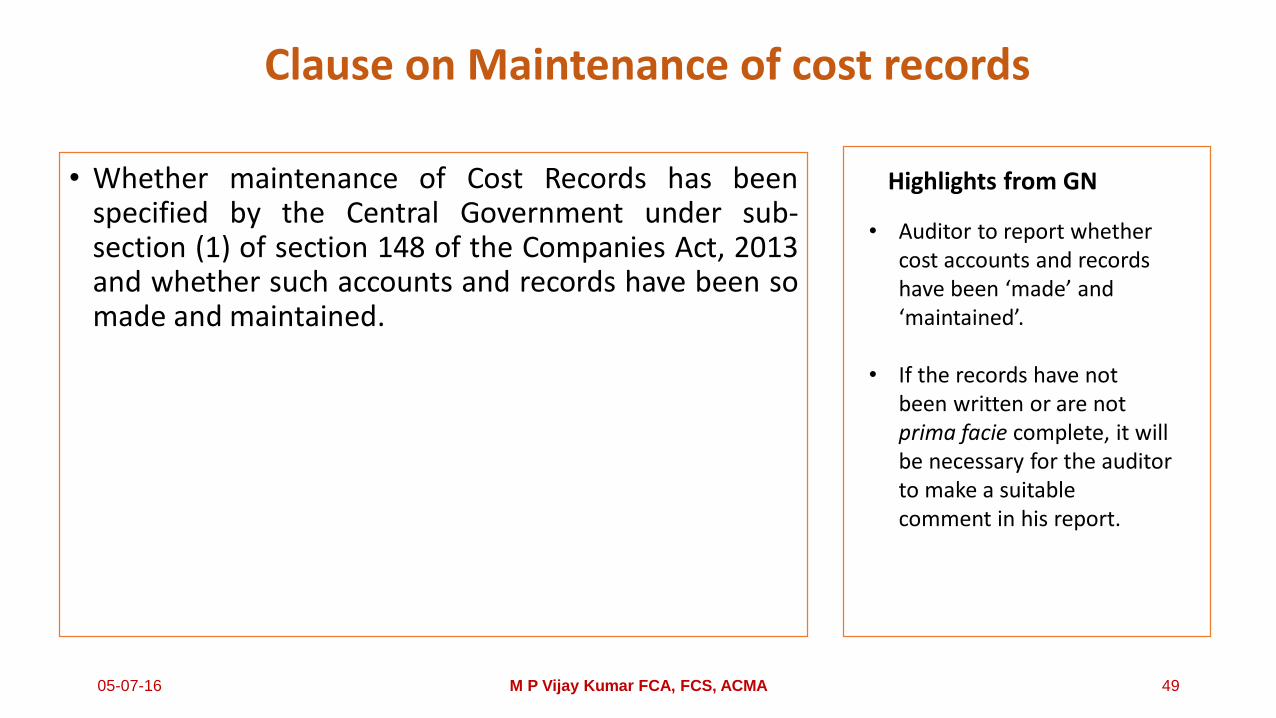

• Whether maintenance of Cost Records has beenspecified by the Central Government under sub-section (1) of section 148 of the Companies Act, 2013and whether such accounts and records have been somade and maintained.

Highlights from GN

• Auditor to report whether cost accounts and records have been ‘made’ and ‘maintained’.

• If the records have not been written or are not prima facie complete, it will be necessary for the auditor to make a suitable comment in his report.

Clause on Maintenance of cost records

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 49

audit report5 slides ( 45- 49)

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 50

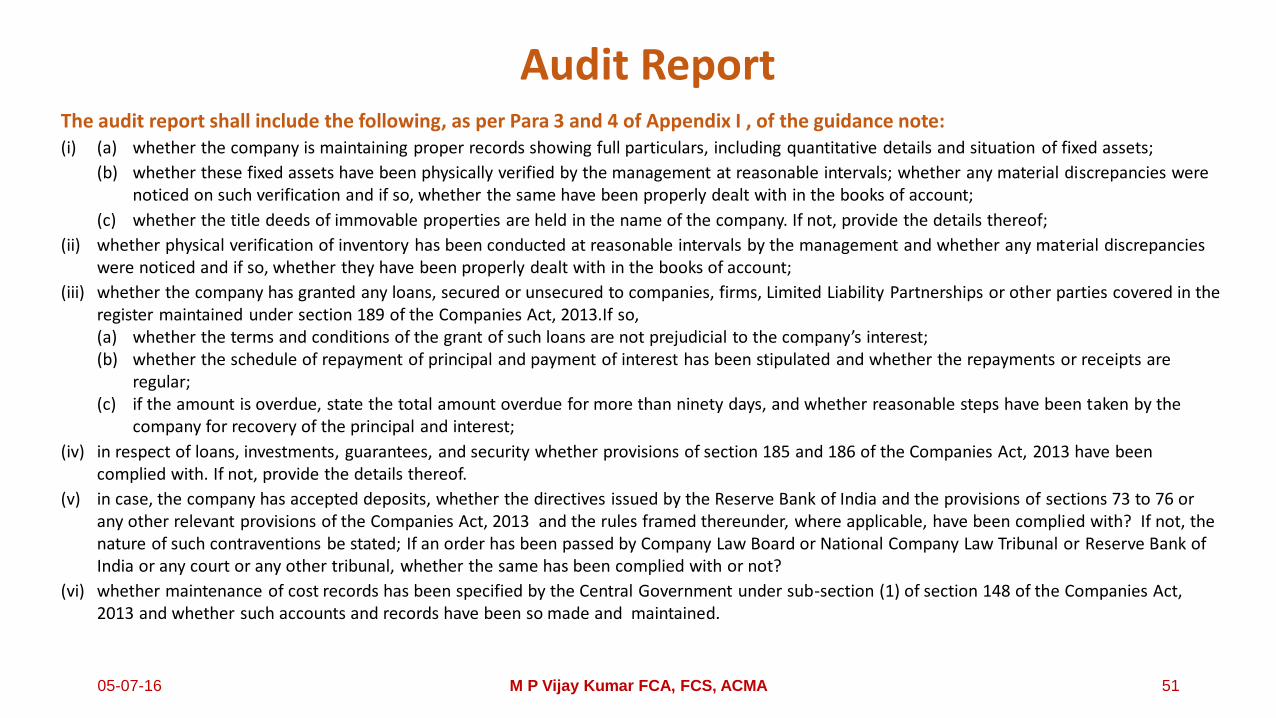

The audit report shall include the following, as per Para 3 and 4 of Appendix I , of the guidance note:(i) (a) whether the company is maintaining proper records showing full particulars, including quantitative details and situation of fixed assets;

(b) whether these fixed assets have been physically verified by the management at reasonable intervals; whether any material discrepancies were noticed on such verification and if so, whether the same have been properly dealt with in the books of account;

(c) whether the title deeds of immovable properties are held in the name of the company. If not, provide the details thereof;

(ii) whether physical verification of inventory has been conducted at reasonable intervals by the management and whether any material discrepancies were noticed and if so, whether they have been properly dealt with in the books of account;

(iii) whether the company has granted any loans, secured or unsecured to companies, firms, Limited Liability Partnerships or other parties covered in the register maintained under section 189 of the Companies Act, 2013.If so,(a) whether the terms and conditions of the grant of such loans are not prejudicial to the company’s interest;(b) whether the schedule of repayment of principal and payment of interest has been stipulated and whether the repayments or receipts are

regular;(c) if the amount is overdue, state the total amount overdue for more than ninety days, and whether reasonable steps have been taken by the

company for recovery of the principal and interest;

(iv) in respect of loans, investments, guarantees, and security whether provisions of section 185 and 186 of the Companies Act, 2013 have been complied with. If not, provide the details thereof.

(v) in case, the company has accepted deposits, whether the directives issued by the Reserve Bank of India and the provisions of sections 73 to 76 or any other relevant provisions of the Companies Act, 2013 and the rules framed thereunder, where applicable, have been complied with? If not, the nature of such contraventions be stated; If an order has been passed by Company Law Board or National Company Law Tribunal or Reserve Bank of India or any court or any other tribunal, whether the same has been complied with or not?

(vi) whether maintenance of cost records has been specified by the Central Government under sub-section (1) of section 148 of the Companies Act, 2013 and whether such accounts and records have been so made and maintained.

Audit Report

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 51

(vii) (a) whether the company is regular in depositing undisputed statutory dues including provident fund, employees' state insurance, income-tax, sales-tax, service tax, duty of customs, duty of excise, value added tax, cess and any other statutory dues to the appropriate authorities and if not, the extent of the arrears of outstanding statutory dues as on the last day of the financial year concerned for a period of more than six months from the date they became payable, shall be indicated;

(b) where dues of income tax or sales tax or service tax or duty of customs or duty of excise or value added tax have not been deposited on account of any dispute, then the amounts involved and the forum where dispute is pending shall be mentioned. (A mere representation to the concerned Department shall not be treated as a dispute).

(viii) whether the company has defaulted in repayment of loans or borrowing to a financial institution, bank, government or dues to debenture holders? If yes, the period and the amount of default to be reported (in case of defaults to banks, financial institutions, and government, lender wise details to be provided).

(ix) whether moneys raised by way of initial public offer or further public offer (including debt instruments) and term loans were applied for the purposes for which those are raised. If not, the details together with delays or default and subsequent rectification, if any, as may be applicable, be reported;

(x) whether any fraud by the company or any fraud on the Company by its officers or employees has been noticed or reported during the year; If yes, the nature and the amount involved is to be indicated;

(xi) whether managerial remuneration has been paid or provided in accordance with the requisite approvals mandated by the provisions of section 197 read with Schedule V to the Companies Act? If not, state the amount involved and steps taken by the company for securing refund of the same;

(xii) whether the Nidhi Company has complied with the Net Owned Funds to Deposits in the ratio of 1: 20 to meet out the liability and whether the NidhiCompany is maintaining ten per cent unencumbered term deposits as specified in the Nidhi Rules, 2014 to meet out the liability;

(xiii) whether all transactions with the related parties are in compliance with section 177 and 188 of Companies Act, 2013 where applicable and the details have been disclosed in the Financial Statements etc., as required by the applicable accounting standards;

(xiv) whether the company has made any preferential allotment or private placement of shares or fully or partly convertible debentures during the year under review and if so, as to whether the requirement of section 42 of the Companies Act, 2013 have been complied with and the amount raised have been used for the purposes for which the funds were raised. If not, provide the details in respect of the amount involved and nature of non-compliance;

(xv) whether the company has entered into any non-cash transactions with directors or persons connected with him and if so, whether the provisions of section 192 of Companies Act, 2013 have been complied with;

(xvi) whether the company is required to be registered under section 45-IA of the Reserve Bank of India Act, 1934 and if so, whether the registration has been obtained.

Audit Report

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 52

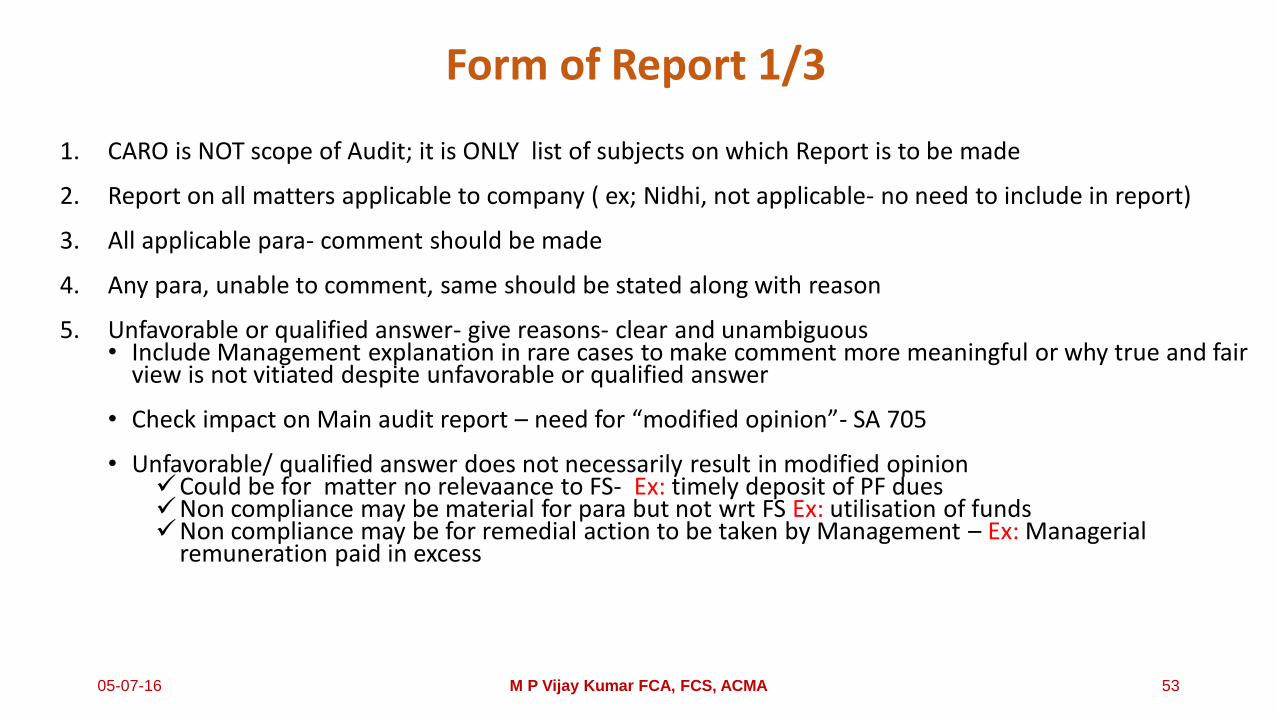

1. CARO is NOT scope of Audit; it is ONLY list of subjects on which Report is to be made

2. Report on all matters applicable to company ( ex; Nidhi, not applicable- no need to include in report)

3. All applicable para- comment should be made

4. Any para, unable to comment, same should be stated along with reason

5. Unfavorable or qualified answer- give reasons- clear and unambiguous• Include Management explanation in rare cases to make comment more meaningful or why true and fair

view is not vitiated despite unfavorable or qualified answer

• Check impact on Main audit report – need for “modified opinion”- SA 705

• Unfavorable/ qualified answer does not necessarily result in modified opinionCould be for matter no relevaance to FS- Ex: timely deposit of PF duesNon compliance may be material for para but not wrt FS Ex: utilisation of fundsNon compliance may be for remedial action to be taken by Management – Ex: Managerial

remuneration paid in excess

Form of Report 1/3

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 53

6. If comment on any para is adverse, Auditor to evaluate impact on “true and fair view”

7. Main audit report should have reference “ Further to our comments in the Annexure, we report that……..” , even if there are no unfavorable or qualified comment for any para

8. Most para require Opinion and not statement of facts - give either:• General preface- “In terms of information and explanation sought by us and given by

the company and the books and records examined by us in the normal course of audit and to the best of our knowledge and belief, we state that…..”

• Individual comments preface – “ in our opinion and according to the information and explanations given to us during the course of audit……..”

9. Audit covers CARO – hence instances of Information sought, not received, mention same and evaluate impact on main audit report.

10. Audit Checklist – Appendix IV of GN

Form of Report 2/3

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 54

11. Period of compliance• through out the year ; not balance sheet date or date of audit report• give weightage in forming opinion ( unfavorable/ qualified) to status on balance sheet date/ date of

report- ex; FA Records• most items- existence during the year is important to come to conclusion on matters of control

12. CARO – comments, should be done in compliance with SA

13. If any item is not complied, but Auditor choses not to make adverse comment, due to immateriality, record reason in WP

14. Audit planning for CARO –• request management for information on record• SA 230- see everything in writing• maintain record of explanation• have a check list

11. Working papers are LIFE• Evidence of examination to arrive at basis of opinion • Evidence of having given congizance to information/ explanation by company and that opinion is

not arbitrary• Evidence that information was full and complete, to arrive at the opinion• Evidence that auditor did not rely only on information/explanation by company, but he has

subjected the same to reasonable tests toe verify accuracy and explanation

Form of Report 3/3

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 55

11. Working papers are LIFE

• Evidence of examination to arrive at basis of opinion

• Evidence of having given congizance to information/ explanation by company and that opinion is not arbitrary

• Evidence that information was full and complete, to arrive at the opinion

• Evidence that auditor did not rely only on information/explanation by company, but he has subjected the same to reasonable tests to verify accuracy and explanation

Form of Report 3/3

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 56

board report1 slide ( 51)

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 57

1. Board to give full information and explanation for every unfavorable commentor qualification in the Board report

2. Auditors report comprises items of statement of facts and items requiringopinion – Circulate draft audit report to Board, to ensure no inconsistency onfacts

3. Directors and Auditors may have genuine difference of opinion on same factsin some cases.

1. Each entitled to their view2. Difference in view is not regarded as reflection on auditors opinion

Board Report

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 58

DISCLAIMER

The views of the Author presented here are his personal views and not those of AASB or ICAI. Members are requested to go through the

Relevant Guidance Note for Complete Information.

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 59

05-07-16 M P Vijay Kumar FCA, FCS, ACMA 60