Embed Size (px)

DESCRIPTION

Community Bankers of Iowa newsletter May 2015

Citation preview

OF

FIC

IAL

PU

BL

ICA

TIO

N O

F T

HE

CO

MM

UN

ITY

BA

NK

ER

S O

F I

OW

AM

AY

20

15

RECAP:Washington

Policy SummitPgs. 8-9

PeerConnection ForumPg. 4

NEW EVENT!

EffectiveLoan

Policy Pt. 1 Pgs. 10-13

REPUTATIONPg. 21

EnhancingYour Bank’s

2 COMMUNITY BANKER UPDATE | MAY 2015

Want To AttendA Webinar?

View a complete calendar andregister for CBI-sponsored webinarsand events at www.cbiaonline.org

or Call Us at 515.453.1495for more information.

hard work.dedication.strategy.

W W W. F I R S T B A N K E R S B A N C . C O M

888.726.2880

INVESTMENTS ARE NOT FDIC INSUREDNOT BANK GUARANTEED & MAY LOSE VALUE

FOR INSTITUTIONAL USE ONLY

GOVERNMENT & AGENCY BONDS MUNICIPAL BONDS | MORTGAGE BACKED SECURITIES

PUBLIC FINANCE | MUTUAL FUNDS/EQUITIES CORPORATE BONDS | MUNICIPAL BOND CREDIT REVIEW

BOND PORTFOLIO ACCOUNTING & ANALYSIS ASSET/LIABILITY MANAGEMENT

MAY 2015 WEBINAR LINE-UP

May 5 RevisedEscrowRulesEffectiveAugust1,2015

May 6 FromProspecttoCustomer:Skills&ToolsforSuccessfulBusinessDevelopment

May 7 DirectorSeries:Regulator&IndustryHotButtonsforDirectors

May 12 DutiesoftheBoardSecretary:Fundamentals,BestPractices&E-PackageDelivery

May 13 HomeEquity,HELOC&SecondLienRiskManagement, IncludingMaturingHELOCGuidance

May 14 IRASeries:IRADeathDistributions:BeneficiaryOptions&TaxConsequences

May 15 TheFFIEC’sNewAppendixJonOutsourcedTechnologyServices: RequiredActions,VendorManagement&BusinessContinuityExpectations

May 19 WireTransferCompliance:WhoisLiable?

May 20 You’retheNewHROfficer,NowWhat?

May 21 AdvancedACHSpecialistSeries:ACHDeathNotificationEntries(DNEs) &Reclamations:YourBank’sLiability

May 27 TheALLLinTroubledDebtRestructuring:Identifying&AccountingforImpairedLoans

May 28 HandlingDifficultCustomers:DealingwithIntimidation,Negativism&Anger

May 29 TestingLoanAuditProceduresforIntegratedDisclosureCompliance BeforetheAugust1,2015Deadline

COMMUNITY BANKER UPDATE | MAY 2015 3

In This Issue

May2015WebinarLineup.................. 2

FromtheEVP&CEO............................ 3

LOTUp&ComingBankerAward......... 4

PeerConnectionForum....................... 4

Best-of-the-BestCompetition.............. 5

44thAnnualConvention...................6-7

WashingtonPolicySummit...............8-9

DevelopmentandMaintenanceofanEffectiveLoanPolicy-Pt. 1......... 10-13

FromtheTop.......................................14

FinePoints..........................................15

RuralMainstreetSurvey.............. 16-18

Service-FocusedBranches................19

CBIMemberNews..............................20

EnhancingYourReputation...............21

TakeCreditProgram...........................22

Try Something NewThereisnodoubtthatcommunitybankingisfullofnewthingsthesedays…sadlymostlyjustnewregulations.Andwhilethosethingsmustbedealtwith,oneofthethingsthatisafocusofCBIistoprovidememberswithnewalternativesandactivitiestoimproveyourbank’sbottomline,learningandnetworking.Sodon’tjustfollowalongwiththesameoldthings,takealookatthebrandnewopportunitiesthatwehaveforyou.

ThebrandnewPeer Connection Forumprovidesyourfunctionalstafftheopportunitytomeettheirpeersfromacrossthestate,learnaboutleadership,thenbreakintointerestgroupstolearnandnetworkfromprofessionalandfellowattendeesabouttheirarea.Onedayonly.May28inAltoona.$135fortheentireday.

OurAnnual Management Conference and Convention in Okoboji, July 15-17.Thereareamanyofourmemberswhohavenotattendedourannualgatheringofcommunitybankersandtheirfamilies.Threedaysoflearning,nationallyknownspeakers,networkingandfun. If you haven’t attended this event in the past five years, you can attend THIS year for only $150! Comejoinus.

Bankingequipmentserviceisoftenanoverlookedpotentialareawhereopportunitiesexisttoimproveefficiencyandlowercosts.Multiplevendorsforvariouspiecesofequipmenteachwithauniqueserviceprovidermeansmoreadministrativetimespent.Anewconcept,availablefromCBI Endorsed Member Equips,bringsallofthisinformationtogetherinaneasytouseapplicationwithsingle-clickservicecalls.Andovertime,itcanreduceyourmaintenancecostsbyupto20%.MoreinformationisavailableontheCBIwebsite.

Comejoinyourfellowbankersatthe8th Annual CBI Golf Open on August 11atthe(thisisthenewpart!)HyperionFieldClubinJohnston.Putthatonyourcalendartodayandjointhenetworkofcommunitybankers.

JustastherelationshipofCBIwiththeICBAmakessurethatnewproactivechangesareadvocatedinWashingtonlikethe“PlanforProsperity”,soistheIowastaffofCBIdedicatedtomakingyourlifebetterbyaddingtotheoptionsyouhavetomakeyourbankgrowprosper.Theitemsaboveareonlyasampling.SogoaheadandTrySomethingNewfromCBI.

EVENTS CALENDARBest-of-the-Best CompetitionEntries Due.................................May 15

NEW! Peer Connection Forum...May 28

LOT Up & Coming Banker AwardNominations Due........................ June 5

PAC AuctionDonations Due.... June 12

Robert D. Dixon Founders’ AwardNominations Due...................... June 19

44th Management Conference &Annual Convention............... July 15-17

8th Annual Golf Tournament...Aug. 11

LOT Quarterly Meeting............ Aug. 20

Certified Community LenderCertification Renewal............... Aug. 20

Community Bankers for ComplianceFall Session......................Sep. 22 & 23

Community Banking SummitsFall Sessions........................Oct. 13-15

LOT Quarterly Meeting.............Nov. 19

Community Bankers of Iowa1603 22nd St, Suite 102West Des Moines, Iowa 50266Phone: 515.453.1495www.cbiaonline.org

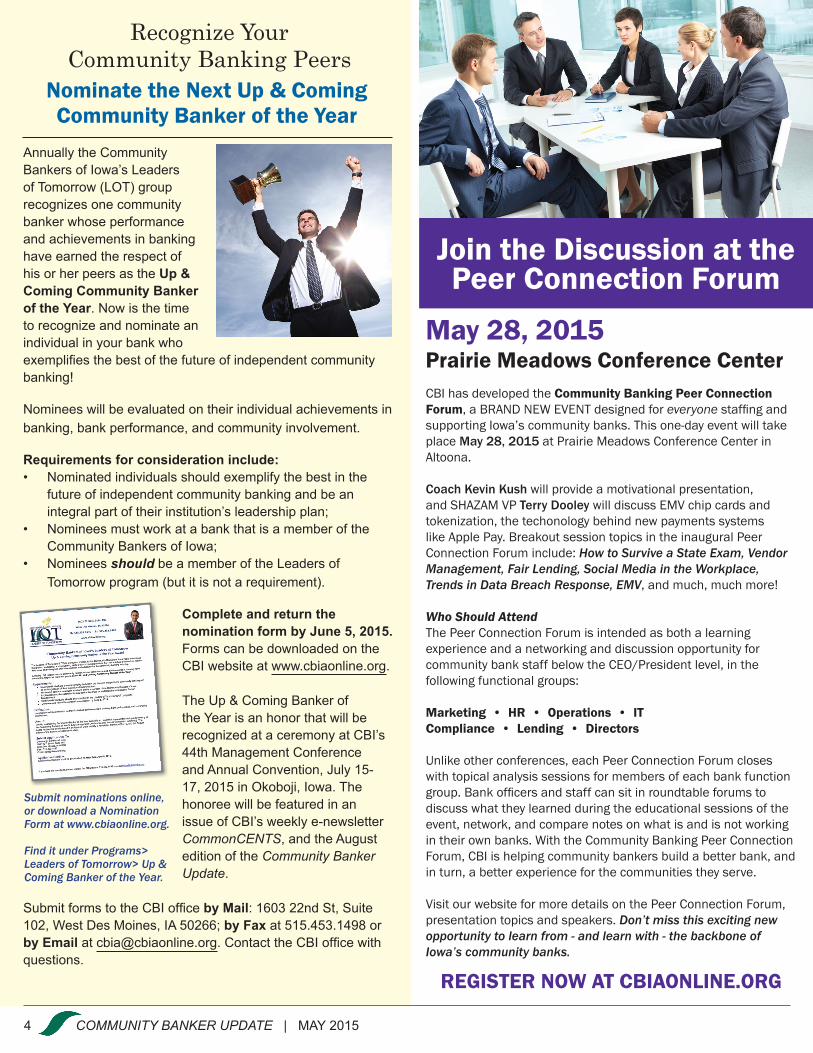

Annually the Community Bankers of Iowa’s Leaders of Tomorrow (LOT) group recognizes one community banker whose performance and achievements in banking have earned the respect of his or her peers as the Up & Coming Community Banker of the Year. Now is the time to recognize and nominate an individual in your bank who exemplifies the best of the future of independent community banking!

Nominees will be evaluated on their individual achievements in banking, bank performance, and community involvement.

Requirements for consideration include:• Nominated individuals should exemplify the best in the

future of independent community banking and be an integral part of their institution’s leadership plan;

• Nominees must work at a bank that is a member of the Community Bankers of Iowa;

• Nominees should be a member of the Leaders of Tomorrow program (but it is not a requirement).

Complete and return the nomination form by June 5, 2015. Forms can be downloaded on the CBI website at www.cbiaonline.org.

The Up & Coming Banker of the Year is an honor that will be recognized at a ceremony at CBI’s 44th Management Conference and Annual Convention, July 15-17, 2015 in Okoboji, Iowa. The honoree will be featured in an issue of CBI’s weekly e-newsletter CommonCENTS, and the August edition of the Community Banker Update.

Submit forms to the CBI office by Mail: 1603 22nd St, Suite 102, West Des Moines, IA 50266; by Fax at 515.453.1498 or by Email at [email protected]. Contact the CBI office with questions.

Recognize YourCommunity Banking Peers

Nominate the Next Up & Coming Community Banker of the Year

Submit nominations online, or download a Nomination Form at www.cbiaonline.org.

Find it under Programs> Leaders of Tomorrow> Up & Coming Banker of the Year.

Join the Discussion at the Peer Connection Forum

CBIhasdevelopedtheCommunity Banking Peer Connection Forum,aBRANDNEWEVENTdesignedforeveryonestaffingandsupportingIowa’scommunitybanks.Thisone-dayeventwilltakeplaceMay 28, 2015atPrairieMeadowsConferenceCenterinAltoona.

Coach Kevin Kushwillprovideamotivationalpresentation,andSHAZAMVPTerry DooleywilldiscussEMVchipcardsandtokenization,thetechonologybehindnewpaymentssystemslikeApplePay.BreakoutsessiontopicsintheinauguralPeerConnectionForuminclude:How to Survive a State Exam, Vendor Management, Fair Lending, Social Media in the Workplace, Trends in Data Breach Response, EMV,andmuch,muchmore!

Who Should AttendThePeerConnectionForumisintendedasbothalearningexperienceandanetworkinganddiscussionopportunityforcommunitybankstaffbelowtheCEO/Presidentlevel,inthefollowingfunctionalgroups:

Marketing•HR•Operations•ITCompliance • Lending • Directors

Unlikeotherconferences,eachPeerConnectionForumcloseswithtopicalanalysissessionsformembersofeachbankfunctiongroup.Bankofficersandstaffcansitinroundtableforumstodiscusswhattheylearnedduringtheeducationalsessionsoftheevent,network,andcomparenotesonwhatisandisnotworkingintheirownbanks.WiththeCommunityBankingPeerConnectionForum,CBIishelpingcommunitybankersbuildabetterbank,andinturn,abetterexperienceforthecommunitiestheyserve.

VisitourwebsiteformoredetailsonthePeerConnectionForum,presentationtopicsandspeakers.Don’t miss this exciting new opportunity to learn from - and learn with - the backbone of Iowa’s community banks.

REGISTER NOW AT CBIAONLINE.ORG

May 28, 2015Prairie Meadows Conference Center

4 COMMUNITY BANKER UPDATE | MAY 2015

COMMUNITY BANKER UPDATE | MAY 2015 5

CommunitybanksalloverIowacelebratedCommunityBankingMonthinAprilandspreadthe“MakingADifferenceOnMainStreet”messageintheircommunities.HowdidYOURbankparticipate?LetCBIknowandyourbankcouldwintheBest-of-the-BestTravelingTrophyandapizzapartyforstaff!

Andthat’snotall...yourbankalsogetsbraggingrights!ThewinningbankwillbeannouncedandhonoredattheKickoffReceptionduringour44th Annual ConventioninOkobojiinJuly,andwillalsobefeaturedintheAugusteditionofCommunity Banker UpdateandtheCommonCENTSnewsletter.

Toenter,sendusyourphotos,tweets,activitiesandwhateverelsetellsushowyourbankcelebratedCommunityBankingMonthinApril,alongwithacompleted2015CBIBest-of-the-BestCompetionentryform.All submissions are due to the CBI office by May 15, 2015.

Forinformation,entryformsandmore,visitwww.cbiaonline.organdcheckoutCommunityBankingMonthundertheEventsheader.

Community Banking Month Is Over!IT’S TIME TO ENTER COMMUNITY BANKERS OF IOWA’S2015 BEST-OF-THE-BEST COMPETITION!

Show us your photos, tweets, facebook posts,videos, pins...everything that tells us how your bank hosted Community Banking Month festivities!And remember...make sure to enter by May 15!

800.967.2645 | eojohnson.com

Secure IT and protecting customer information

matter toCedar Valley Bank & Trust.

What Matters?

“ Our board and bank leadership take IT security and our customer information very seriously. Having Locknet® as our IT partner is

the answer for our bank in addressing our IT needs. What I value most with Locknet® is knowing that our system is

being monitored 24/ 7 and that if something goes wrong it will be taken care of by experts.“ — Kim Frush, IT Officer – Cedar Valley Bank & Trust

• Budget predictability• Proactive instead of reactive IT• 1 – 3 – 5 year budgeting

• A solid foundation of security and efficiency

BUSINESS PROFILE:Cedar Valley Bank & Trust is a family owned full-service community bank with locations in La Porte City and Vinton, IA.

What matters most to your financial institution?

When security matters – Locknet®’s Keysuite™ fully managed IT services provides:

6 COMMUNITY BANKER UPDATE | MAY 2015

Join Us at CBI’s 44th Management Conference & Annual Convention

REGISTRATION IS NOW OPEN!

REGISTRATION IS NOW OPEN!CommunityBankersofIowa’s44thManagementConferenceandAnnualConventionrepresentstheimportanceofcommunitybanks’personalserviceandcommitmenttotheircustomersandthecommunitiestheyservewiththetheme,“Where Everybody Knows Your Name.”

TheConventionstrivestounitecommunitybankersthrougheducationfromnationallyrecognizedspeakers,accesstothelatestproductsandservices,andnumerousopportunitiesfornetworking,camaraderie,andtheexchangeofideaswithcommunitybankersstatewide.MeetupwitholdfriendsandnewattheKickoff Reception,onthelakeduringtheEleventh Annual Catch and Release Fishing Tournament,onthegolfcourseduringtheMixed Pair and Bankers’ Golf Tournaments,andattheGala and PAC Auction.

GuestspeakersthisyearincludeJim Olson,formerCIAoperative;motivationalspeakerChip Eichelberger;comedicsendoffspeakerJeff Havens;andICBAImmediatePastChairmanJohn Buhrmaster.Greatbreakoutsessionsarescheduledaswell,featuringafederalRegulators’ Panel,socialmedialessonsfromAnn ChenwithICBA,andtrendsindatabreachresponsewithDan KramerfromSHAZAM.

Join us at the family reunion during CBI’s 44th Management Conference and Annual Convention, July 15-17, 2015 in Okoboji, Iowa.Additionalinformationandregistrationisavailableonlineatwww.cbiaonline.org.Ifyouhaveanyquestionsabouttheconvention,pleasecalltheCBIofficeat515.453.1495.

July 15-17 2015

Check your snail mail!Get detailed info on events and more in the 44th Annual Convention brochure!

John Buhrmaster

ChipEichelberger

Dr. JamesOlson

JeffHavens

DanKramer

JamesLaPierre

AnnChen

JeffJensen

JimSchipper

44th Annual Convention Featured Speakers

Breakout Session Speakers: Regulators’ Panel

Breakout Session Speakers

COMMUNITY BANKER UPDATE | MAY 2015 7

bellbanks.com | Member FDIC

9933

Gary Keller [email protected]

Gene [email protected]

Call one of us for quick response, competitive rates and flexible underwriting.

We help you compete with the “big guys!”• Participation loans (commercial,

agricultural, construction, operating lines and term loans)

• Bank stock & ownership loans

• Bank building financing

• Business & personal loans for bankers

• Multi-family permanent financing

Partner with us for your participation and bank stock loan needs.

Community bankers will be honored during award presentations at the 44th Annual Convention’s Kickoff Reception.

Mingle and view new products and services at the convention’sGala / PAC Auction / Tradeshow event.

CBI PAC AuctionThurs. July 16, 2015

DonationsNeeded!

CBI’sLiveandSilentPACAuctionsarebeingheldduringour44thAnnualConvention.Weneeditemstobeauctioned!

Ifyou’dliketodonatecashoritemstobeauctioned,downloaddonationformsontheConventionpageatcbiaonline.organdreturnthemtotheCBIoffice,faxto515.453.1498,oremailtocbia@cbiaonline.org.Picturesofdonationsmayalsobeemailedtocbia@cbiaonline.org.Please return completed forms by June 12, 2015.

PleasebringalldonateditemstotheregistrationdeskinthelobbyoftheArrowwoodResortinOkoboji,Iowano later than Wednesday evening, July 15, 2015.

NotethattheCBIPACcannotacceptcorporatecontributions,anonymouscontributions,oracontributioninthenameoforonbehalfofanotherperson.

There’s plenty of entertainment for the familyat the convention’s outings and spouses-only events.

Learn about industry trends and get valuable informationduring the General Sessions of CBI’s 44th Annual Convention.

8 COMMUNITY BANKER UPDATE | MAY 2015

A group of community bankers from across Iowa joined community bankers from across the nation to spotlight community bank issues as part the Washington Policy Summit sponsored by ICBA, CBI’s national affiliate. The Summit spotlights the need for community bank regulatory relief, competitive parity and small business support.

After hearing speakers like Senate Banking Committee Chairman Richard Shelby of Alabama, Rep. Randy Neuberger, Chairman of the House Subcommittee on Financial Institutions and Consumer Credit and Governor Daniel Tarullo of the Federal Reserve, the bankers called on each of the Iowa representative offices to articulate the unique needs of community banks. There were also Agency Breakout Sessions featuring Martin Gruenberg, Chairman of the FDIC, Thomas Curry, Comptroller of the Currency, and Richard Cordray, Director of the FDIC.

Attending the Summit and representing the Iowa community banking industry were: Kris Ausborn, Iowa Trust & Savings Bank-Emmetsburg; Gus Barker, Community Bank of Oelwein; Rob Dixon, Citizens State Bank-Sheldon; Scott Dobesh-SHAZAM; Wade Gort, Premier Bank-Rock Valley; Kurt Henstorf, First Heritage Bank-Shenandoah; Dave Hibbs, ICBA

Midwest Regional Office-Urbandale; Don Hole, Community Bankers of Iowa; Brad Robson, First State Bank-Belmond; Marti Rodamaker, First Citizens National Bank-Mason City; Bob Steen, Bridge Community Bank-Mechanicsville; Charlie E. Walsh, Farmers & Merchants Bank-Burlington, and; Larry Winum, Glenwood State Bank-Glenwood.

2015 Washington Policy SummitBankers from Iowa Lobby in DC for Community Bank Issues

CBI members meet with US Senator Jodi Ernst (right)during the 2015 ICBA Washington Policy Summit.

Robb Nielsen (717) 369-0139 • [email protected]

www.protectmybank.com

• InformationSecurityAudit

• DesignedExclusivelyforBanks

• SimilarScope&ApproachasBankRegulators

• DeterminesAdequacyofSecurityControls

• FreeAccesstoanAutomatedRemediationTrackingTool

• VerifiesCompliancewithExistingBankPolicyandProcedures

• Savemoneybybundlingtheseservices

InformationSecurity Audit Bundle

• Penetration Test

• Vulnerability Assessment

• Social Engineering

Endorsed by:

The Iowa delegation attending the Washington PolicySummit pose on the steps of the nation’s Capitol building.

Iowa community bankers discuss the issues with US RepRod Blum (top, left) at the Washington Policy Summit.

COMMUNITY BANKER UPDATE | MAY 2015 9

Bank Architecture

& ConstructionPre-design

Master PlanningSite Development

ArchitectureProject Management

ConstructionPost-project SupportSecurity & Signage

TrustPersonalityExperienceIntegrityTeamwork

Steph Weiand (L) Suzanne Meyers (C) Jim Christensen (R)

112 W. Park Lane, Waterloo319-232-6554

US Reps David Loebsack (top photo, sixth from left) andDavid Young (lower photo, sixth from left) stand withCBI members at the 2015 Washington Policy Summit.

10 COMMUNITY BANKER UPDATE | FEBRUARY 2015

Loanportfoliostypicallyhavethelargestimpactontheoverallriskprofileandearningsperformance(interestincome,fees,provisions,andotherfactors)ofcommunitybanks.Theaverageloanportfoliorepresentsapproximately62.5percentoftotalconsolidatedassetsforbankingorganizationswithlessthan$1billionintotalassetsand64.9percentoftotalconsolidatedassetsforbankingorganizationswithlessthan$10billionintotalassets.1Inordertocontrolcreditrisk,itisimperativethatappropriateandeffectivepolicies,procedures,andpracticesaredevelopedandimplemented.Loanpoliciesshouldalignwiththemissionandobjectivesofthebank,aswellassupportsafeandsoundlendingactivity.Policiesandproceduresshouldserveasaframeworkforallmajorcreditdecisionsandactions,coverallmaterialaspectsofcreditrisk,andreflectthecomplexityoftheactivitiesinwhichabankengages.Policy DevelopmentWhileriskisinevitable,bankscanmitigatecreditriskthroughthedevelopmentofandadherencetoeffectiveloanpoliciesandprocedures.Awell-writtenanddescriptiveloanpolicyisthecornerstoneofasoundlendingfunction,andabank’sboardofdirectorsisultimatelyresponsibleforframingtheloanpoliciestoaddresstheinherentandresidualrisks(i.e.,thoserisksthatremainevenaftersoundinternalcontrolshavebeenimplemented)inthelendingbusinesslines.Oncethepolicyisformulated,seniormanagementisresponsibleforitsimplementationandongoingmonitoring,aswellasthemaintenanceofprocedurestoensuretheyareuptodateandrelevanttothecurrentriskprofile.Policy ObjectivesTheloanpolicyshouldclearlycommunicatethestrategicgoalsandobjectivesofthebank,aswellasdefinethetypesofloanexposuresacceptabletotheinstitution,loanapproval

authority,loanlimits,loanunderwritingcriteria,andseveralotherguidelines.Itisimportanttonotethatapolicydiffersfromproceduresinthatitsetsforththeplan,guidingprinciples,andframeworkfordecisions.Procedures,ontheotherhand,establishmethodsandstepstoperformtasks.Banksthatofferawidervarietyofloanproductsand/ormorecomplexproductsshouldconsiderdevelopingseparatepolicyandproceduremanualsforloanproducts.Policy ElementsOneplacetostartwhendeterminingwhichkeyelementsshouldbeincorporatedintotheloanpolicyiswiththeregulatoryagencies’examinationmanualsandpolicystatements.ThisarticlereliesprimarilyontheFederalReserve’sCommercialBankExaminationManual,2whichorganizesandformalizestheexaminationobjectivesandproceduresthatcommunicatesupervisoryguidancetobankexaminersonawiderangeoftopics.Althoughthisarticledoesnotprovideanall-inclusivelistingofelementsoneshouldfindinaloanpolicy,itdoesoutlineanddiscussthebasicelementsthatshouldbeincludedinageneralloanpolicy.Loanpolicieswilldiffersignificantlybetweenbanksbasedonthecomplexityoftheactivitiesinwhichtheyareinvolved;however,ageneralloanpolicyshouldincorporatecertainbasiclendingtenets.Consistentwiththelendingstrategy,theboardshouldidentifynotonlywhichtypesofloansarepermissibleandimpermissiblebutalsothetypesofloansthebankwillandwillnotunderwriteregardlessofpermissibility.Theboxtotherightoutlinessomeofthemorecommonloantypesfoundincommunitybanks.Loan TypesEachloantypelistedintheboxhasnumerousloanproductsubcategories.Communitybanksofferadiverserangeofloanproducts,andthislistisbynomeansall-inclusive.Afewoftheloantypeslisted,includinghomeequity3andcommercialandindustrial(C&I)lending,4havebeendiscussedinrecentlypublishedCommunityBankingConnectionsarticles.ArecentarticleintheFederalReserveBankofSt.Louis’sCentralBankeralsodiscusseslendingbycommunitybanksduringthefinancialcrisis.5Indeterminingpermissiblelendingactivity,theboardshouldaskanumberofquestionssuchasthefollowing:• Howcanwebetterservethecreditneedsofourcommunity?• Willourprimaryfocusberetaillending,commerciallending,

oramixofthetwo?• Whattypesofretailand/orcommercialloanswillweoffer?• Whatisourdesiredmixofloansincomparisonwithtotal

loansandtotalassets?

(Loan Policy continued on next page)

by James L. Adams, Supervising ExaminerFederal Reserve Bank of Philadelphia

EFFECTIVE LOAN POLICY - Pt. 1Development and Maintenance of an

Reprinted with permission of Community Banking Connections®

Copyright 2014 Federal Reserve System.

Read Part 2 of this article next month.

COMMUNITY BANKER UPDATE | MAY 2015 11

(Loan Policy continued from previous page)

• Doourlendingandcreditadministrationstaffmembershavetheappropriateskillsets?

Undesirableorimpermissiblelendingactivityshouldalsobeidentifiedwithintheloanpolicy.Thiswillensurethatmanagementandlendingstaffmembersdonotspendunduetimeorresourcescultivatingrelationshipsorpursuingloantypesthatarenotalignedwiththebank’sgoalsorstrategy.Undesirablelendingactivitycouldincludeactivitythatmayharmthereputationofthebankorforwhichtheexpectedreturnisnotcommensuratewiththelevelofrisk.Ifthelendingstaffmembersdonothavetheexpertisetounderwrite,service,ormonitorcertainloantypes,thebankshouldnotundertakesuchactivities.Thepolicyshouldalsostatethatengaginginthefinancingofillegalorillicitactivitiesisunacceptable.Policiesandproceduresneedtobecontinuallyevaluatedandupdated.Forexample,desirableandundesirableloantypesmaychangeasaresultofshiftingeconomicconditions,technology,andmarketdemographics,sopoliciesshouldbereevaluatedwhenevertheyarepresentedtotheboardforapproval.Loan Participations — Purchases and SalesTheloanpolicyshouldadequatelyaddressparticipations,bothpurchasesandsales.6Themostcommontypeofloanparticipationgenerallysharesprofitsandlossesonanequalbasis;therefore,relyingsolelyontheleadbanks’analysisandnotconductingindependent,thoroughanalysisisimprudent.Adequatefinancialanalysisandduediligencemustbeperformedpriortoenteringintoanyparticipations.Participations Purchased.Abankmaychoosetoenterintoparticipationsifitisunabletogeneratesufficientloandemandindependently.Inthiscase,partneringwithanotherstrongbankoperatinginahealthiermarketcouldhelpgenerateadditionalassetsandincome.Also,participationsmayhelptodiversifyriskamonglocalesorlendingtypes.Policiesshouldstresstheimportanceofprudentandindependentunderwriting,appropriatelegaldocumentation,andongoingmonitoringofloanparticipations.Participations Sold.Whenabankisunabletoadvancealoantoacustomerforthefullamountrequestedbecauseoflendinglimitsorforotherreasons,loanparticipationsmaybeanappropriatealternative.Insuchsituations,abankmayextendcreditto

acustomeruptotheinternalorlegallendinglimitandsellparticipationstocorrespondentbanksintheamountexceedingthelendinglimitorintheamountexceedingwhatthebankwishestoretain.Participationarrangementsshouldbeestablishedbeforethecreditisultimatelyapproved.Participationsshouldbedoneonanonrecoursebasis,andtheoriginatingandpurchasingbanksshouldshareintherisksandcontractualpaymentsonapro-ratabasis.Sellingorparticipatingoutportionsofloanstoaccommodatethecreditneedsofcustomerscanpromotegoodwillandmayenableabanktoretaincustomerswhomightotherwiseseekcreditelsewhere.7Ifmanagementparticipatesintheunderwritingofproductssimilartoloanparticipation(s),suchassyndications8and/orclubdeals,9theloanpolicyshouldappropriatelycoverthebasicelementsoftheseactivities(limits,underwritingrequirements,documentation,andsoforth).Foradditionalinformationregardingloanparticipations,bankersshouldconsulttheSecondQuarter2013issueofCommunityBankingConnections,whichfeaturedanarticlethatdiscussedseveralwaystostrengthenboardandseniormanagementoversightofloanparticipations.10Loan Portfolio Mix and LimitsThepolicyshouldalsoestablishthedesiredmixoftheloanportfolioandlimitsonindividualloantypes.Exposuremixandlimitsshouldbemonitoredonanongoingbasistoensurethattheyareappropriateandreasonable.Limitsshouldbedeterminedbasedonrisktolerancesandshouldbemeasuredincomparisonwithloans,assets,andtier1capitalplustheallowanceforloanandleaselosses(ALLL).Managementshouldcontinuallymonitorthedollarandpercentageexposuresofeachportfoliotoensurethebankmaintainsanappropriateriskprofilewithsufficientreturns.Whendeterminingrisktolerancesandlimits,portfoliostratificationisextremelyimportant.Stratificationorsegmentationoftheloanportfolioscanbeaccomplishedthroughnumerousvariables,dependingonthedesiredgranularity.Limitsestablishedbygeneralloantype(e.g.,commercialrealestate(CRE),C&I,andsmallbusiness)willprovideaverybroadportfoliooverview.UsingNorthAmericanIndustryClassificationSystem(NAICS)codeswillprovidegeneralindustryandsubindustrycategoriesthatshouldprovidegreatergranularityandinsightintotheportfoliocompositionandriskcharacteristics.Managementmayalsoconsiderstratifyingbyborrowerriskrating,collateraltype,loanofficer,orothervariables.Concentrationsofcreditandthelegallendinglimitarecloselylinkedtoportfoliomixandestablishedlimits;therefore,thesetopicsarecoveredwithinthissection.Concentrations of Credit.Concentrationsofcreditaredefinedasexposuretoanindustryorloantypeinexcessof25percentoftier1capitalplustheALLL.Concentrationsarenotnecessarilyindicativeofperformanceissuesandquiteoftenexistwithinportfolios.However,riskmanagementpracticesshouldbecommensuratewiththeriskprofileoftheconcentratedexposure.Bankswithconcentrationsinspecifictypesofloanswithcommoncharacteristics—forexample,commonindustriesand/orgeographicareas—canbenegativelyimpactedbyacatastrophiceventwithinthebusinessline,industry,orgeography.Therefore,banksneedtohavewell-establishedpoliciesandprocedures

(Loan Policy continued on next page)

LegalDisclaimer:TheanalysesandconclusionssetforthinthispublicationarethoseoftheauthorsanddonotnecessarilyindicateconcurrencebytheBoardofGovernors,theFederalReserveBanks,orthemembersoftheirstaffs.Althoughwestrivetomaketheinformationinthispublicationasaccurateaspossible,itismadeavailableforeducationalandinformationalpurposesonly.Accordingly,forpurposesofdeterminingcompliancewithanylegalrequirement,thestatementsandviewsexpressedinthispublicationdonotconstituteaninterpretationofanylaw,rule,orregulationbytheBoardorbytheofficialsoremployeesoftheFederalReserveSystem.

12 COMMUNITY BANKER UPDATE | MAY 2015

(Loan Policy continued from previous page)

thatstresstheidentificationofandtheprudentcontrolsoverconcentrations.Appropriateriskdiversificationthroughtheestablishmentofprudentconcentrationlimitsmayhelptominimizethepotentialnegativeimpactonearningsperformanceand/orcapitalshouldsuchaneventoccur.In2006,thefederalbankingregulatoryagenciesissuedguidanceonCREconcentrations.11Theguidanceaddressedtheagencies’observationthatCREconcentrationshadbeenrisingatmanyinstitutions,especiallyatsmall-to-medium-sizedinstitutions.Whilemostinstitutionshadsoundunderwritingpractices,theagenciesobservedthatsomeinstitutions’riskmanagementpracticesandcapitallevelshadnotevolvedwiththelevelandnatureoftheirCREconcentrations.Therefore,theagenciesissuedtheguidancetoremindinstitutionsthatstrongriskmanagementpracticesandappropriatelevelsofcapitalareimportantelementsofasoundCRElendingprogram,especiallywhenaninstitutionhasaCREconcentrationoraCRElendingstrategythatcouldleadtoaconcentration.Legal Lending Limit.Theloanpolicyshouldappropriatelyaddressthelegallendinglimit,whichistheaggregatemaximumdollaramountthatasinglebankcanlendtoagivenborrower.Becausethelegallendinglimitistiedtothebank’scapital,managementmustcalculateandmonitorthelegallendinglimitonanongoingbasis.State-charteredbanksmustcomplywiththelegallendinglimitsestablishedbythestatebankingsupervisoryagencieswithintheiroperatinglocation.StatememberbanksthataresupervisedbytheFederalReserveSystemmustalsocomplywiththelegallendinglimitregulationsoftheOfficeoftheComptrolleroftheCurrency.12Geographic AreaCommunitybanksaretypicallyestablishedtoservethelocalcommunitiesinwhichtheyoperate.Theloanpolicyshouldidentifythegeographicareainwhichanorganizationwilllendandthecircumstancesunderwhichcreditmaybeextendedoutsideofthatarea.Familiaritywiththegeographicareaprovidesinsightandsupportsmanagement’sabilitytocloselyandcontinuallymonitorborrowerperformance.Lendingoutsideofthelocalmarketcanhelptodiversifygeographicexposure,asexplainedintheloanparticipationsectionabove,butitcanalsoraiseconcernsaboutmanagement’sabilitytocloselymonitorprojectsandremaininformedaboutthelocaleconomy.Appropriatepoliciesandprocedurescoveringloanparticipationsandpotentialconcernswithout-of-arealendingwillhelpreduce,butnoteliminate,someoftheserisks.Structure of Lending FunctionThestructureofthelendingdepartmentorfunctionvarieswidelyamonginstitutions.Ideally,thelendingfunctionshouldhaveanappropriatesegregationofdutiesandindependenceintherolesthroughoutthedepartment.Managementmuststrivetomaintainsufficientcontrolsandsegregationofdutiesinalllendingfunctionstoavoidinappropriatecreditdecisionsand/orweakunderwritingprocesses.Theabilitytoseparatetheactivitiesoftheloangenerationfunctionfromthecreditunderwritingandanalysisfunctionhasnumerousbenefits.Unfortunately,thisisverydifficultandoftenunrealisticatsmallerbanks,wheretheseactivitiesareusuallycombined.Smallerbanksmaystrugglewithimplementingsuchcontrolsandstructurebecauseoftheirlimitedstaffandfinancialconstraints.

Lending AuthorityTheloanpolicyshouldalsoclearlydefinetheindividualsandloancommitteesthathavetheauthoritytoapproveloans.Dollarlimitsshouldbeestablishedforindividualsbynameorbyjobtitle,individualsactingtogether(dualormultipleindividuallendingauthority),loancommittees,andthelegallendinglimitauthority(boardorcommitteethereof).Individuallendingauthorityshouldbestructuredbyjobtitleandloanproduct,ensuringthatlendingdecisionsarebeingmadebyindividualswiththeappropriatecredentialsandexpertise.However,nobankshoulddelegateunlimitedlendingauthoritytooneoralimitednumberofindividuals.Beforeabankcanestablishlendingauthoritiesorlimits,theboardmustestablishtheapprovalhierarchyorstructure.Theboardisultimatelyresponsiblefortheaffairsoftheorganizationandmustdeterminetowhatdegreetheboardiswillingtodelegatelendingauthority.Theboardcoulddeterminethatitwillparticipatedirectly,establishacommitteeoftheboard,ordelegatetheauthoritytoaseniormanagementcommittee.InaccordancewiththeFederalReserveBoard’sRegulationO,theboardmustbeinvolvedintheultimatecreditdecisionwhenapprovingloanstoinsiders.ConclusionRegulatorsexpectcommunitybankstoestablishandmaintainpoliciesthatprovideaneffectiveframeworktomeasure,monitor,andcontrolcreditrisk.However,communitybankersdonotneedtostartwithablankslate.Informationonpolicydevelopmentandmaintenanceisreadilyavailableandeasilyaccessiblefromanumberofsources.Theregulatoryagencies’examinationmanualsandhandbooks,alongwithFederalReserveSupervisionandRegulationletters,provideguidanceandtimelyinformationonemergingissuesandregulatoryconcernsthatshouldbeincorporatedintotheloanpolicy.Inaddition,industryassociationsandprivateorganizationsprovideongoingtrainingandcurrentinformationoneffectivepolicydevelopment.Whiletheseresourcesmaybehelpfulandserveasasolidfoundationforacommunitybankloanpolicy,theimportanceoftailoringthepolicytothebankingorganizations’activitiescannotbeoverstressed.Althoughthisarticleaddressesbothwhatispermissibleandwhoisresponsibleinacomprehensivecommunitybankloanpolicy,itisbynomeansall-inclusive.Thenexttwoarticlesinthisserieswilldiscussadditionalelementsthatmaybeincorporatedintothepolicy,suchasunderwriting,appraisals,riskratings,pricing,anddocumentation;ongoingpolicyreviewandmaintenance;andoverallcompliancewiththeloanpolicy.Notes*Aloanpolicyshouldattempttospecifywhatispermissible,whoisresponsible,andhowactivitieswillbecontrolled,reportedon,andverified.Thisarticle,whichisthefirstofathree-partseriesthatcoverskeyelementsofasoundcommunitybankloanpolicy,anddiscussesthewhatandthewho.Thenexttwoarticleswillreviewthehow,touchingontopicssuchasunderwriting,appraisals,riskratings,pricing,anddocumentation,alongwithotherrelatedtopics,suchasloanreviewandpost-originationactivities.1FederalReservedataasofDecember31,2013.2SeeBoardofGovernorsoftheFederalReserveSystem,CommercialBankExaminationManual(CBEM),section2040.1,“LoanPortfolioManagement,”availableatwww.federalreserve.gov/boarddocs/supmanual/cbem/cbem.pdf.3SeeMichaelWebb,“HomeEquityLending:AHELOCHangoverHelper,”CommunityBankingConnections,SecondQuarter2013,availableatwww.cbcfrs.org/articles/2013/Q2/Home-Equity-Lending-A-HELOC-Hangover-Helper,and“HomeEquityLending:AHELOCHangoverHelper—Part2,”CommunityBankingConnections,FourthQuarter2013,availableatwww.cbcfrs.org/articles/2013/Q4/Home-Equity-Lending.4SeeCynthiaCourse,“SoundRiskManagementPracticesinCommunityBankC&ILending,”CommunityBankingConnections,FourthQuarter2012,availableat

(Loan Policy continued on next page)

COMMUNITY BANKER UPDATE | MAY 2015 13

© Copyright Employers Mutual Casualty Company 2014. All rights reserved.

Endorsed by your association.Recommended by your peers.

Home Office: Des Moines, IAwww.emcins.com CBSI is a subsidiary of

Community Bankers of Iowa

Make the EMC Choice® Financial Institution program your choice for the right insurance coverages, responsive service from a local company and competitive pricing. Count on EMC® and your independent insurance agent for protection that fits the unique needs of your community bank.

(Loan Policy continued from previous page) www.cbcfrs.org/articles/2012/Q4/Sound-Risk-Management-Practices-in-Community-Bank-CI-Lending.5SeeGaryS.CornerandAndrewP.Meyer,“CommunityBankLendingDuringtheFinancialCrisis,”FederalReserveBankofSt.LouisCentralBanker,Spring2013,availableatwww.stlouisfed.org/publications/cb/articles/?id=2342.6Aloanparticipationisasharingorsellingofownershipinterestsinaloanbetweentwoormorefinancialinstitutions.Normally,butnotalways,aleadbankoriginatestheloanandsellsownershipintereststooneormoreparticipatingbanks.Theleadbankretainsapartialinterestintheloan,holdsallloandocumentationinitsname,holdsalloriginaldocumentation,servicestheloan,anddealsdirectlywiththeborrowerforthebenefitofallparticipants.SeeCBEMsection2045.1,“LoanParticipations,theAgreementsandParticipants.”7SeeCBEM,section2040.1,“LoanPortfolioManagement.”8Asyndicationisaloanmadebytwoormorelenderscontractingdirectlywithaborrowerunderthesamecreditagreement.Eachlenderhasadirectlegalrelationshipwiththeborrowerandreceivesitsownpromissorynote(s)fromtheborrower.Typically,oneormorelenderswillalsotakeontheseparateroleofagentforthecreditfacilityandassumeresponsibilityforadministeringtheloansonbehalfofalllenders.Asyndicatedloandiffersfromaloanparticipationinthatthelendersinasyndicationparticipatejointlyintheoriginationandthelendingprocess.9Aclubdealisthesmallesttypeofsyndicatedloan,usuallyusedforloansbetween$25millionand$150million.Unliketheotherloantypes,theclubdealisanequaldenominationloaninwhichallpartieslendthesameamount;thearrangerputsinthesameamountasallotherlenders,andallpartiesequallysharetheloanfee.10SeeMichaelPoprik,“LoanParticipations:LessonsLearnedDuringaPeriodofEconomicMalaise,”CommunityBankingConnections,SecondQuarter2013,availableatwww.cbcfrs.org/articles/2013/Q2/Loan-Participations.11SeeSupervisionandRegulationletter07-1,“InteragencyGuidanceonConcentrationsinCommercialRealEstate,”anditsattachment,availableatwww.federalreserve.gov/boarddocs/srletters/2007/SR0701.htm.12See12CFRPart32,availableathttp://ow.ly/COXUD.

14 COMMUNITY BANKER UPDATE | MAY 2015

Community Bank ExcellenceWritten By: Jack Hartings, Chairman of ICBA

Neverstopstrivingforexcellence.ThatthoughtcomestomymindwhenIthinkoftop-performingcommunitybanks.Excellenceisbuiltintowhatcommunitybanksdoeveryday.Theydothisbyneversettlingforthestatusquoorthinkingthatwhatworkedlastyearwillworkthisyear.Theyareconstantlytryingtodobetterandensureexcellencebydemandingitineverythingtheydo.Becauseofthis,ourinstitutionsconstantlymonitorandmeasureourperformance.

Ascommunitybankers,however,wedon’tstopatthenumbers.Hard,empiricalperformancemeasures—suchasreturnonaverageassets,returnonaverageequityandefficiencyratios—areonlythebeginningwhenitcomestoanycommunitybank’ssuccess.Whilewearefor-profitbusinessesbalancingtheneedsofourcustomers,shareholdersandemployees,wealsohaveadirectstakeinthesuccessofourcustomersandcommunities,whichdependonuseveryday.

Forthesereasons,manyothercriticalbutlessquantifiablepiecesarepartofthepuzzleofsuccessandexcellenceforcommunitybanks.Thosefactorsinvolveintangibleslikehowwellwemaintainhighstaffinvolvementandmorale,sustainsuperiorcustomerservice,aswellassupporttheeconomicwell-beingofourcustomersandcommunities.Ourinstitutionsconstantlybalancethesedifferentprioritiesandalwaysstrivetofindwaystodobetterwhiledoingso.

Takeforinstancemycommunitybank,ThePeoplesBankCo.inColdwater,Ohio.Tomaintainahighlyefficientbank,wemakesurethatallmembersofourstaffareinvolvedincontinuallyimprovingourinstitution.Thismeansevery

processandpositionisconstantlyevaluatedtoseeifthere’sawaywecandothingsbetter.Canwemakeanindividualemployee’srolemoreproductive?Isthereawaytomakeataskmoreefficient,secureorconstructive?Ascommunitybankers,weallroutinelyaskourselvesthesequestionseveryday.Andfrommyexperience,communitybanksthatconsistentlyachievetheirgoalsengrainsuchacultureofrigorousexcellenceatalllevelsoftheirmanagementandstaff.

Whilethereisnosilverbulletformakingacommunitybankmoreefficient,therearealsomorethan1,000waysforacommunitybanktobesuccessful—andtodefinesuccessonitsownterms.

AboutaquarterofallcountiesintheUnitedStatesareservedonlybyasinglecommunitybankandnootherfinancialinstitution.Thenumberstoprofitablysupportaquick-buck,transaction-drivenbigbankdon’taddupinthosecounties—that’swhythemegabanksaren’tthere.Butthat’swherecommunitybanksstepupandmakeadifferencebyoperatingbalanced,efficient,resourcefulandconscientiousfinancialinstitutionsthatserveawiderangeofneeds.Ourcommunitybanksoperateforthelonghaulandthebestinterestsofallthepeopleweserve.Ofcourse,that’swhatmakescommunitybanksandcommunitybankersambassadorsoffinancialexcellence.

Enjoyreadingaboutthisyear’stop-performingmembercommunitybanksinthismonth’sissueofIndependentBanker,startingonpage20.Butrememberthateverycommunitybank,whetheritappearsonthisyear’slistsornot,isinherentlyabest-performingbankforitscommunity.Atitsheart,thatiswhatourgreat,marvelouslydiverseindustryistrulyabout.

JackHastingsisChairmanofICBA,andPresidentandCEOofThePeople’sBankinColdwater,Ohio.

“Our community banks operatefor the long haul and the best

interests of all the people we serve.”

TOPFrom the

COMMUNITY BANKER UPDATE | MAY 2015 15

AsanICBAmember,youknowaboutyournationaltradeassociation’ssimplebutpowerfulmission—abouthowitexclusivelyrepresentsandservesthenation’scommunitybanks.Uniqueamonganynationalfinancialtradeassociation,ICBA’smissionprovidesuswithasingularfocus.Whilewe’reonlyaboutcommunitybanking,we’realsoeverythingaboutcommunitybanking,too.Thismeansweworkashardtoadvancethefutureofcommunitybankingaswedotorepresentandserveourindustrytoday.

Simplyput,ICBAstriveseverydaytoensurethenation’scommunitybanksflourishineveryway.EnsuringcommunitybankscontinuetoflourishbothtodayandtomorrowisthemotivationandenergybehindCommunityBankerUniversity®,ICBA’snewcomprehensiveeducationprogramdevelopedexclusivelyforcommunitybanksandindividualcommunitybankersalike.It’sdesignedtostrengthenourindustry’sfuturebygivingallofthemoderneducationalresourcestothenextgenerationofcommunitybankingleaders.

Officiallylaunchedlastmonth,CommunityBankerUniversityisabroadbutflexibleeducationalplatformthatprovidespremierprofessionaldevelopmentopportunitiesforeverystageofacommunitybanker’scareer.Withlifelonglearningarealityforeveryoneinourhighlycompetitiveandever-evolvingindustry,ICBAhasforyearsofferedunparallelededucationalofferingstailoredtotheparticularneedsofcommunitybankers.ByestablishingCommunityBankerUniversity,however,ICBAhasbegunexpandingthescopeandaccessibilityofouronlineandclassroomofferingstoencourageongoingprofessionaldevelopmentthroughoutourindustry.What’snewincludesadditionalcoursesandaccreditedacademicopportunitiesinnewformatsfromnewprovidersforcurrentcommunitybankersaswellasfor

peopleseekingtojoinourindustry.Topursuethismissioninnewlyinnovativeandproductiveways,ICBAandCommunityBankerUniversityhaveaffiliatedwithtwocertifieduniversityprogramstobroadentheaccessibilityandvarietyofICBA’seducationalofferings.OneaffiliationwithCommunityBankerUniversityiswiththePaulW.BarretJr.SchoolofBankinginMemphis,Tenn.,whichoperatesathree-yeargraduatebankingprogram,includingacommerciallendingacademyandhumanresourcesmanagementprogram.TheBarretSchool’scurriculumcoversaboutallofthemajorfunctionsperformedinfinancialinstitutions.

ThesecondaffiliationiswithAthabascaUniversityinCalgary,Canada,whichspecializesinprovidingdistancelearningcourses,includingthoseassociatedwithitsfour-yearundergraduateandgraduatecommunitybankingdegrees.Theuniversity’scoursesalsoofferfocusedstudiesincommunitybankingbusinessmanagementandincommunitybankingmarketingandsales.

WhileICBA’slongstandingeducationalresources,includingourwell-establishedclassroomandonlinecourses,willremainavailablethroughCommunityBankerUniversity,knowthatICBA’soveralleducationalprogramisexpandingandadaptingdynamicallyandinnovatively.Byprovidingthebest,mostthoroughandmostaccessibleinstructiontoallowcommunitybankerstocontinuallyadvancetheirknowledgeandcareers,CommunityBankerUniversityisjustanotherwayICBAisensuringthatcommunitybankscontinuetoflourish.Discoverwhat’savailable,andwatchfornewdevelopmentsandopportunitiesthroughtheprogram.

Buildingthefuturealwaysstartswithtoday.Let’sstartbuildingyourcommunitybank’sfuture,andourindustry’sfuture,togethertoday.

Building Our FutureWrittenBy:CamdenFine,PresidentandCEOofICBA

“Building the futurealways starts with today.”

Following Mr. FineMore than 1,000 people are following Camden Fine’s tweets @Cam_Fine— are you? Visit www.twitter.com/cam_fine.

FINEPOINTS

16 COMMUNITY BANKER UPDATE | MAY 2015

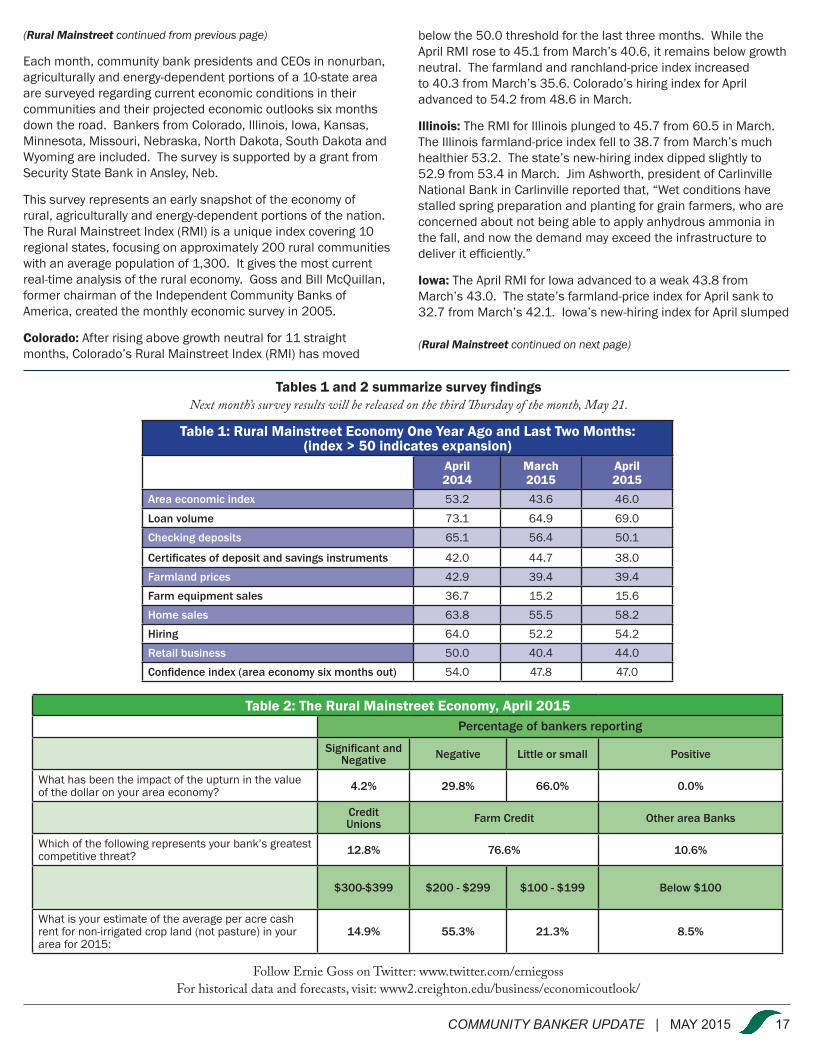

April Survey Results at a Glance:• TheRuralMainstreetIndexremainedbelowgrowthneutralfor

April,signalingpullbacksineconomicactivity.• Morethanone-thirdofbankersreportedthatthestrongdollar

ishavingnegativeimpactsontheirlocaleconomy.• Farmlandpricesdeclinedforthe17thstraightmonth.• Agricultureequipmentsaleswereveryweak,butupslightly

fromMarch’srecordlow.• Approximately75percentofbankCEOsreportedthatFarm

Creditrepresentedthegreatestcompetitivethreattotheiroperations.

OMAHA,Neb.–WhiletheCreightonUniversityRuralMainstreetIndexforAprilroseslightlyfromMarch’sweakreading,itremainsbelowgrowthneutral,accordingtothemonthlysurveyofbankCEOsinruralareasofa10-stateregiondependentonagricultureand/orenergy.

Overall:TheRuralMainstreetIndex(RMI),whichrangesbetween0and100,climbedto46.0inAprilfrom43.6inMarch.

“ThestrongerU.S.dollarcontinuestobeadragontheRuralMainstreeteconomy.Thismonthmorethanone-third,or34.0percentofthebankCEOsreportedthatthestrongU.S.dollarwashavinganegativeimpactontheirlocaleconomy.GainsintheU.S.dollarhavemadeU.S.goods,especiallyagriculturalandenergyproducts,lesscompetitivelypricedabroad,”saidErnieGoss,JackA.MacAllisterChairinRegionalEconomicsatCreightonUniversity’sHeiderCollegeofBusiness.

Farming and Ranching:Thefarmlandandranchland-priceindexforAprilsankto33.4fromMarch’sveryweak39.4.“Eventhoughcroppriceshavestabilized,demandforfarmlandwasweak,pullingagriculturallandpricesdownagain.Thisisthe17thstraightmonththeindexhasmovedbelowgrowthneutral,”saidGoss.

Eventhoughfarmlandpricescontinuetodecline,expectedcashrentsfornon-irrigatedagriculturallandcontinuedtorise.InJanuaryofthisyear,bankersestimatedthataverage2015cashrentswouldbe$214.Thismonthanaverageof$227wasrecorded.

AccordingtoToddDouglas,CEOofFirstNationalBankinPierre,S.D.,“WithGPS-basedyieldmapping,weareseeingsomeofthesmarteroperatorsstartingtofigureoutwhichlandismakingthemmoneyandwhichisnot.Sofarwhensomeonewalksawayfromsomepoorerground,therestillseemstobeagreaterfoolreadytostepupandrentit.”

TheAprilfarm-equipmentsalesindexincreasedtoafrail15.6fromMarch’srecordlowof15.2.Theindexhasbeenbelowgrowthneutralfor21straightmonths.“Withfarmincomeexpectedtodeclineforasecondstraightyear,farmershavebecomeverycautiousregardingthepurchaseofagriculturalequipment,”saidGoss.

Banking:TheAprilloan-volumeindexsoaredto69.0fromMarch’s64.9.Thechecking-depositindexsankto50.1fromMarch’s56.4,whiletheindexforcertificatesofdepositandothersavingsinstrumentsfellto38.0fromMarch’s44.7.

AccordingtoPeteHaddeland,CEOoftheFirstNationalBankinMahnomen,Minn,“Cashrentsarestartingtocomedown.MostofourFarmersarestillingoodshape,buttheyareborrowingmorethisyear.”

Thismonth,bankCEOswereaskedtoidentifythegreatestcompetitivethreatfor2015.Morethanthree-fourths,or76.6percent,ofthebankerssurveyednamedFarmCreditastheirchiefcompetitivethreat.Only10.6indicatedthatothercommercialbanksrepresentedtheirgreatestcompetitivethreat.“Overthelasttwoyears,thepercentageofbankersidentifyingcreditunionsastheirmajorcompetitorhasrisenfromnegligibleto12.8percentthismonth,”reportedGoss.

Hiring:Despiteweakercroppricesandpullbacksfrombusinesseswithclosetiestoagricultureandenergy,RuralMainstreetbusinessescontinuetoaddworkerstotheirpayrolls.TheAprilhiringindeximprovedtoasolid54.2fromMarch’s52.2.“Wehaveyettomeasureanysignificantdeclineinemploymentfortheenergysectorintheregionandforbusinesseslinkedtoagriculture.Iexpectthattochangeinthemonthsaheadaslowerenergyandagriculturalpricesworktheirwaythroughtheeconomy,”saidGoss.

Confidence:Theconfidenceindex,whichreflectsexpectationsfortheeconomysixmonthsout,dippedto47.0from47.8inMarch.“Thenegativetrendinfarmlandprices,agriculturalequipmentsales,andoilpriceshavenegativelyaffectedtheoutlookofRuralMainstreetbankCEOs,”reportedGoss.

Home and Retail Sales:TheAprilhome-salesindexclimbedto58.2fromMarch’s55.5.TheAprilretail-salesindexincreasedtoafrail44.0from40.4inMarch.“Muchlikeinurbanareas,retailsalesremainveryweakevenwiththereductioninfuelprices,”saidGoss.

(Rural Mainstreet continued on next page)

Main Street Economic Survey

C r e i g h t o nU N I V E R S I T Y

April Rural Mainstreet Index Remains Negative:Farmland Prices Decline Again

Ernie Goss

COMMUNITY BANKER UPDATE | MAY 2015 17

(Rural Mainstreet continued from previous page)

Eachmonth,communitybankpresidentsandCEOsinnonurban,agriculturallyandenergy-dependentportionsofa10-stateareaaresurveyedregardingcurrenteconomicconditionsintheircommunitiesandtheirprojectedeconomicoutlookssixmonthsdowntheroad.BankersfromColorado,Illinois,Iowa,Kansas,Minnesota,Missouri,Nebraska,NorthDakota,SouthDakotaandWyomingareincluded.ThesurveyissupportedbyagrantfromSecurityStateBankinAnsley,Neb.

Thissurveyrepresentsanearlysnapshotoftheeconomyofrural,agriculturallyandenergy-dependentportionsofthenation.TheRuralMainstreetIndex(RMI)isauniqueindexcovering10regionalstates,focusingonapproximately200ruralcommunitieswithanaveragepopulationof1,300.Itgivesthemostcurrentreal-timeanalysisoftheruraleconomy.GossandBillMcQuillan,formerchairmanoftheIndependentCommunityBanksofAmerica,createdthemonthlyeconomicsurveyin2005.

Colorado:Afterrisingabovegrowthneutralfor11straightmonths,Colorado’sRuralMainstreetIndex(RMI)hasmoved

belowthe50.0thresholdforthelastthreemonths.WhiletheAprilRMIroseto45.1fromMarch’s40.6,itremainsbelowgrowthneutral.Thefarmlandandranchland-priceindexincreasedto40.3fromMarch’s35.6.Colorado’shiringindexforApriladvancedto54.2from48.6inMarch.

Illinois:TheRMIforIllinoisplungedto45.7from60.5inMarch.TheIllinoisfarmland-priceindexfellto38.7fromMarch’smuchhealthier53.2.Thestate’snew-hiringindexdippedslightlyto52.9from53.4inMarch.JimAshworth,presidentofCarlinvilleNationalBankinCarlinvillereportedthat,“Wetconditionshavestalledspringpreparationandplantingforgrainfarmers,whoareconcernedaboutnotbeingabletoapplyanhydrousammoniainthefall,andnowthedemandmayexceedtheinfrastructuretodeliveritefficiently.”

Iowa:TheAprilRMIforIowaadvancedtoaweak43.8fromMarch’s43.0.Thestate’sfarmland-priceindexforAprilsankto32.7fromMarch’s42.1.Iowa’snew-hiringindexforAprilslumped

(Rural Mainstreet continued on next page)

Tables 1 and 2 summarize survey findingsNext month’s survey results will be released on the third Thursday of the month, May 21.

Table 1: Rural Mainstreet Economy One Year Ago and Last Two Months: (index > 50 indicates expansion)

April2014

March2015

April2015

Area economic index 53.2 43.6 46.0

Loan volume 73.1 64.9 69.0Checking deposits 65.1 56.4 50.1

Certificates of deposit and savings instruments 42.0 44.7 38.0Farmland prices 42.9 39.4 39.4Farm equipment sales 36.7 15.2 15.6Home sales 63.8 55.5 58.2Hiring 64.0 52.2 54.2Retail business 50.0 40.4 44.0Confidence index (area economy six months out) 54.0 47.8 47.0

Table 2: The Rural Mainstreet Economy, April 2015Percentage of bankers reporting

Significant and Negative Negative Little or small Positive

Whathasbeentheimpactoftheupturninthevalueofthedollaronyourareaeconomy? 4.2% 29.8% 66.0% 0.0%

Credit Unions Farm Credit Other area Banks

Whichofthefollowingrepresentsyourbank’sgreatestcompetitivethreat? 12.8% 76.6% 10.6%

$300-$399 $200 - $299 $100 - $199 Below $100

Whatisyourestimateoftheaverageperacrecashrentfornon-irrigatedcropland(notpasture)inyourareafor2015:

14.9% 55.3% 21.3% 8.5%

Follow Ernie Goss on Twitter: www.twitter.com/erniegossFor historical data and forecasts, visit: www2.creighton.edu/business/economicoutlook/

18 COMMUNITY BANKER UPDATE | MAY 2015

(Rural Mainstreet continued from previous page)

to48.2fromMarch’s53.8.JamesBrown,CEOofHardinCountySavingsBankinEldora,said,“Theaveragecashrentinourareaiscloseto$300.”

Kansas:TheKansasRMIforAprilclimbedtoatepid50.0fromMarch’s46.8.Thestate’sfarmland-priceindexforApriljumpedto59.1fromMarch’s57.1.Thenew-hiringindexforKansasclimbedto69.2from65.8inMarch.

Minnesota:TheAprilRMIforMinnesotajumpedto45.6fromMarch’s26.8.Minnesota’sfarmland-priceindeximprovedto36.1from33.2inMarch.Thenew-hiringindexforthestateexpandedto50.9fromMarch’s48.8.BrianNicklason,CEOofWoodlandBankinRemer,reported,“ThelocaleconomyappearsresilientdespiteseveralrecentannouncementsrelatedtotheminingindustryinnortheastMinnesota.JobLayoffsarebeingannouncedthatwilllikelyhavesomeimpactontheeconomyoverthenext12months.Thiscouldbeoffsetbyhiringinothersegmentsofthelocaleconomyand/oragoodsummertouristseason.”

Missouri:TheAprilRMIforMissourideclinedto39.2from39.4inMarch.Thefarmland-priceindexforAprilfellto15.5fromMarch’s16.3.Missouri’snew-hiringindexroseto34.4fromMarch’s33.2.

Nebraska:TheNebraskaRMIforAprilincreasedto46.2from43.3inMarch.Thestate’sfarmland-priceindexadvancedto40.3from33.3inMarch.Nebraska’snew-hiringindexgrewto54.2fromMarch’s51.3.

North Dakota:TheNorthDakotaRMIforAprilclimbedto46.6fromMarch’s45.4.Thefarmland-priceindexfellto48.3fromMarch’s51.3.NorthDakota’snew-hiringindexdecreasedto60.6fromMarch’ssankto61.2.

South Dakota:TheAprilRMIforSouthDakotaexpandedto45.0fromMarch’s41.7.Thefarmland-priceindexforAprildecreasedto33.3fromlastmonth’s35.3.SouthDakota’snew-hiringindexroseto48.7from45.8inFebruary.

Wyoming:TheAprilRMIforWyomingadvancedtoaweak43.6fromlastmonth’s41.9.TheAprilfarmlandandranchland-priceindexsankto31.6fromMarch’s34.1.Wyoming’snew-hiringindexdeclinedto47.2fromMarch’s47.4.

Please help save trees and cost by receiving Bankers Update in an electronic magazine format by inserting your email address below:

Please add the following names to the Bankers Update list so they will receive their own personal electronic copy each month:

Please FAX this entire page to CBI at 515-453-1498.

CBI and the forest thanks you.

COMMUNITY BANKER UPDATE | MAY 2015 19

Today,whenacustomerwalksintoabankbranch,they’reusuallynottheretodepositchecksormakeloanpayments—thoseare

taskstheycannowaccomplishfromanywhereusingmobiletechnologies.Rather,abranchvisitthesedaysentailssolvinganissuethatneedsahumandecision:openinganewaccountordiscussingsuchcomplexproductsasloansorfinancialplanning.

Withthatinmind,facilitiesmustalsoevolvefromtransaction-orientedlocationsintocustomer-centricservicecenters.Andbuildingservice-orientedbranchesrequiresafewspecificareasofinnovationthatprovidemanagersandfrontlineemployeesthetoolstheyneedtobemosteffective.Theideaisthatabank’stechnologyshouldempowerstafftoseecustomersthewaycustomersseethemselves.

Andarecentindustrystudyrevealsthatbankexecutivesunderstandtheimportanceofenhancingbranchoperationsthisyear.InCSI’sAnnualBankingPrioritiesStudy,44.6percentofrespondentsidentifiedbranchoptimizationasastrategicfocusfor2015.Thisstrategy,infact,isratedasthetopfocusareainthestudy,rankingaheadofothersuchimportantinitiativesasEMVpreparedness,mobilebankingadoptionandsocialmediaparticipation.Bankexecutivesclearlyseebranchtransformationkeytosuccessin2015andbeyond,sothequestionbecomeshowtogoaboutit.

Therearethreeprimaryareasthroughwhichbankscanfacilitateamoreservice-orientedbranch:

Customer-Centric ViewsFirst,institutionsshouldimplementtechsystemsthatenableacustomer-centricviewratherthananaccount-centricview.Customersseeonebank—theydon’trecognize,orevencare,whetherthecoresystem,Internetbanking,loanservicingsystemsandmobilebankingplatformsareseparate;theyjustwantaseamlessexperiencefromonetouchpointtothenext.Banksshouldusetoolsthatcan“journeymap”customerstogainacompletepictureoftheirexperienceacrossallinteractions.

Banksalsoshouldrecordandmonitorcustomerdatatohelpthemoptimizetheentirecustomerexperience,ratherthan

focusingonisolatedtouchpoints.Togaininsight,theymuststudybothstructureddata,liketransactiondata,aswellassuchunstructureddataascalllogs.

Strengthening Customer RelationshipsNextcomestheneedforsystemsthatcanautomatecustomerengagementforfrontlineemployees.PowerfulCRMprogramscancollectcustomerdatafromavarietyofplacesandprovideinformationtoemployeesonprofitability,recommendedproducts,transactionandaccounthistoryandcustomerserviceinteractions.

Bycreatingacompanywidetechfoundationthatisfocusedonthecustomer,bankscanincreasecollaborationacrossalllinesofbusinessandbuildacohesiveunderstandingofhowthevarioustouchpointsaffectthecustomerrelationship.Asaresult,theentirebankcancollectivelydeliveraconsistentlygreatexperiencethroughoutthecustomerlifecycle.

Branch MobilityFinally,banksshouldconsiderthephysicallayoutofthebranchandlookforwaystoincorporatetechnologythatallowsmoreflexibility.Inadditiontoprovidingmobiletechnologydirectlytotheconsumer,banksalsoshouldleveragetabletsandmobilesystemstoempoweremployeestomovethroughoutthebranchandworkwithcustomersinacomfortablesetting.Byunshacklingfrontlineemployeesfromthecounterordesk,theycaneducate,solveissuesandcollectdatathatisdirectlyenteredintothecoresystem,eliminatingroadblockstocentralizedinformation.

Ultimately,forbankstostandoutfromtheirrivals,theymustlookcloselyatthecustomerexperienceandensurethatthetechnologyismobileandflexible,andsupportsaservice-orientedculture.

Tim Kopischke is director of software engineering for CSI. In his role, he serves as chief architect of CSI’s cloud-based core system, and he leads research on emerging technologies and application development trends.

Written By: Tim Kopischke - Director of Software Engineering, Computer Services, Inc.

Take

StepsThree

to Service-Focused Branches in 2015

20 COMMUNITY BANKER UPDATE | MAY 2015

Emily Abbas,whojoinedBankersTrustCo.inSeptemberaschief

ofstaff,hasnowbeennamedchiefmarketingofficer.Shewillcontinuetoserveaschiefofstaff.Inthenewrole,Abbasischargedwithfurtheringthebank’sstrategicfocusoncustomers,communityandemployees,accordingtoarelease.

BeforejoiningBankersTrust,AbbasservedasexecutivedirectorofpublicrelationsatStrategicAmerica,andinvariousmarketingandcommunicationsleadershiprolesatGuideOneInsuranceandAviva.

“AsBankersTrustcontinuestogrow,wefeelitistherighttimetoelevateourmarketingpresenceandexpertise,”BankersTrustPresidentandCEOSukuRadiasaidintherelease.

CheckoutmoreaboutCBIAssociateMemberBankersTrustatwww.bankerstrust.com.

CSI Names Bill Crouch asBusiness Development Director

for the Midwest RegionComputerServices,Inc.(CSI),aproviderofend-to-endtechnologysolutionsthatempowerfinancialinstitutionstoremaincompetitive,

compliantandprofitable,ispleasedtoannouncethatBill CrouchhasjoinedtheorganizationasitsnewbusinessdevelopmentdirectorfortheMidwestregion.Inhisrole,BillwillassistfinancialinstitutionsinmakingstrategicITdecisionsrelatedtomanagedservicesandcloud-hostedtechnology.

BillcomestoCSIafter15years’experienceworkingontechnologyissuesinthecommunitybankspace.Morerecently,heconsultedwithorganizationsondatacenterenvironmentsandITsolutionsthataddressedenterprisewidesecurityandperformanceconcernsinthefinancialservicessector.Hisextensiveknowledgearoundprovidinglong-termITmanagedservicesinhighlyregulatedenvironmentsmakeshimavaluableresourceforcommunitybankslookingtodeployhostedtechnology.

“CSIgivesmeachancetoconsultwithcommunitybankersonthebestpossibleITapproaches,giventheirspecificsituation,toalleviatetheburdenofsecurityandregulatorycomplianceontheirstaff,”Billsays.“Ourgoalistoletbankersgetbacktowhattheydobest–beingbankers.”

ReachouttoBillinhisnewroleforyourinformationtechnologysolutionsat317-652-3579orbill.crouch@csiweb.com.

FormoreinformationaboutCBIEndorsedMemberCSI,visitwww.csiweb.com.

NewsfromCBIAffiliate&AssociateMembers

Abbas Named Chief Marketing Officerfor Bankers Trust

Emily Abbas has been named Bankers Trust’s new Chief Marketing Officer.

TheSHAZAMNetworktodayannouncedtheadditionofPatrick Dixtothecompany’smarketingteam.Hiredasaseniorpublicrelationsmanager,Dixbrings20yearsofpublicrelationsandwritingexperiencetothemember-ownedEFTnetwork.

PriortojoiningSHAZAM,Dixspentthemajorityofhiscareerasananchorofthe#1morningnewscastonWHO-HDinDesMoines.Duringhistenureatthestation,hecoveredfiveIowaCaucuscycles,cityandcountygovernmentandcountlessstoriesaboutIowaweatherincludingtwomajorfloods.

DixhasbeenrecognizedforoutstandingreportingwithawardsfromTheSocietyofProfessionalJournalists,TheWilliamRandolphHearstFoundationandtheMidwestBroadcastNewsAssociation.In2012,hebegandevelopingandteachingmediatrainingcourses.Theclassesfocusedonhownewsroomswork,howtogetstoriesonairandhowtodealwithmediainacrisissituation.AsPRmanageratSHAZAM,he’lloffersimilarservicestocommunityfinancialinstitutions.

TolearnmoreaboutthisCBIEndorsedMembervisitshazam.netandfollow@SHAZAMNetwork.

Patrick Dix Joins SHAZAM Network as PR Manager

COMMUNITY BANKER UPDATE | MAY 2015 21

Reputationisamongacommunitybank’slargestconcernsand,atthesametime,biggestadvantagesor,insomecases,disadvantages.The

mostsuccessfulcommunityfinancialinstitutionsacrosstheU.S.capitalizeontheirreputationaladvantagebycontinuallyexpandingtheirproductsandservicestoincreasemarketshare.Amongthebigreputationdrivers,productsandservicestogethermakeupthelargestfactorinthedevelopmentofbrandperceptionsbyabank’scustomers,accordingtoReputationInstitute’sanalysis.Fornoncustomers,governanceismostimportant,followedcloselybyproductsandservices.1

Oneoftenoverlookedreputationbuilderorrehabilitatoristooffercurrentandprospectivecustomersacompetitiveon-sitefinancialservicesprogram.Whilemanyinstitutionsseepositiveresultsfromin-houseinvestmentprograms,asignificantpercentageacrosstheU.S.havenotyetcapitalizedonthesereputationenhancing,revenuegeneratingofferings.

More Than A Reputation BoostBut,anon-siteinvestmentprogramsimplymakessenseforabank’sreputationmanagement.Customerslookupontheircommunitybankasatrustedadvisorwhogenuinelycaresabouttheirfinancialwellbeing.Addingfinancialservicestoabank’sportfolioprovidesmuchmoreconfidenceandtrustintheinstitutionandfurtherstheirstatureinthecommunitytheyserve.

Likewise,itincreasescustomerretention.Ifgiventheopportunity,customersarehighlylikelytopurchasein-houseinvestmentsonthebankpremisestheyalreadyrelyontodotheirfinancialbusinesswith.InacommunitybankstudyconductedbytheFederalReserveSystem,communitybankersindicatedthatprovidingall-encompassingfinancialservicesthatfurthertieacustomertoabankmakesitharderforthecustomertoleave.2

Yet,manybanksallowotherbignamefinancialservicescompetitorstoadvisetheirwould-becustomers,whichoftentimesresultsincrucialmissedopportunities,orworse,lossofbank-clientrelationshipsanddiminishingbankreputation.Inthesamestudy,participantssaidtheirlocalreputationandstrongcustomerrelationshipshelpthemdifferentiatetheirfinancialplanningandnontraditionalservicesfromtheircompetitors’.2

Focus on Your Reputation, Not LogisticsToabank’sadvantage,successfulthird-partyfinancialservicesfirmsareskilledattheset-upandmaintenanceofonsiteinvestmentprograms,allowingtheinstitutiontofullyreaptherevenueandreputationbenefitswithoutthehassleofadditionalprogramsupervision.Thesefirmsspecializeinandareresponsibleforsupervisingallinvestmentrelatedactivitiesonbankpremisesandprovidethebanksupportive,solidindustryexpertise.Moreover,thebestofthesefirmshelpbankspartnerwithalreadyestablishedlocaladvisorswithanequallypositivereputation,

furtherenhancingthebank’sstandinginthecommunity.Strongcomplianceprocessesandcontractualindemnificationalsominimizethebank’sriskandliabilitywhileraisingatrustingreputationamongthecommunitytheyserveasaleadingproviderofinvestmentservices.

Whiletheintricaciesofoperatingasuccessfulfinancialprogrammayinitiallyappearchallengingoroverwhelming,thetopbrokerdealersdedicatedtothecommunitybankchannelcontinuallyhonerepeatableblueprintsforsuccess,allowingbankstoprovidethesevaluableservicestotheircustomers,whilefocusingonsecuringareputablereputation.

Your Reputation In Today’s IndustryIt’sbeenmorethan30yearssinceregulatorsfirstgrantedbankstheabilitytoofferinvestmentstotheircustomers,makingitamatureindustrythathasstoodthetestoftime.Withunprecedentedneedfornoninterestincomeinthispost-Dodd-Frankera,it’snotsurprisingthatarecordnumberofinstitutionsaremoreandmorebeginningtocapitalizeontheirhard-earnedreputationsandexpandingtheirservicestoincludeinvestments.

Ifyourinstitutionhasnotconsideredaninvestmentprogram,orifyouhaveanunderperformingprogram,rethinkyouroptions.Investmentprogramsmanagedbysuccessfulthirdpartyexpertsareanuntappedopportunitytoeasilystrengthenyourrelationshipsandreputationallthewhileincreasingyourfinancialinstitution’snoninterestincome.

1. AmericanBanker.com2. Federal Reserve Community Bank Study

The Ease of Enhancing Your Bank’s Reputation

TheIowaFinanceAuthority(IFA)recentlyannouncedthateligiblefirst-timeIowahomebuyersmay

purchaseahomeandreducetheirfederalincometaxliabilitybyupto$2,000ayearforthelifeoftheirmortgage.Approximately400Iowahomebuyersareexpectedtobenefitfromtheprogram,whichisnowavailableforapprovednewpurchasesthroughanetworkofTakeCreditProgramParticipatingLendersthroughoutthestate.

Theprogramprovideseligiblehomebuyerswithataxcreditagainsttheirfederalincometaxliabilityeveryyearforthelifeoftheirmortgage,aslongasthehomeisusedastheirprimaryresidence,uptoamaximumof30years.

Theamountofthetaxcreditisbasedonapercentageofthehomeowner’smortgageinterest.Forthe2015TakeCreditProgram,thecreditrateissetat50%oftheannualinterestpaidonthemortgageloan,uptoamaximumof$2,000peryear.

Eligibility Eligibleapplicantsmustbefirst-timehomebuyer,purchaseahomeinaTargetedAreaorbeaneligiblemilitaryveteraninadditiontomeetingfederalincomelimitswhichvarybycounty.Thepurchasepriceofthehomepurchasedmaynotexceed

$250,000iflocatedinaNon-TargetedArea,or$305,000iflocatedinaTargetedArea.DetailedeligibilityinformationisavailableatIowaFinanceAuthority.gov/TakeCredit.

ProcessAfteraneligiblehomeownerhasreceivedawrittenNoticeofCommitmentfromIFAtheymaycloseonanapprovedmortgageloanwithanIFATakeCreditParticipatingLender.AfterclosingIFAwillissuethehomeowneramortgagecreditcertificate.Thehomeownerinturnmayapplythecreditagainsttheirfederalincometaxliabilityonanannualbasisforthelifeoftheirmortgage.ThecreditmaybeclaimedonIRSForm8396.

TheMortgagecreditcertificatesareavailableonafirst-comefirst-servebasisandtheprogramwillbeclosedforfurtherreservationsonceavailablefundinghasbeenexhausted.

Marketing materials ComplimentarysuppliesofTakeCreditprogrammarketingmaterialsareavailablebyrequest.Pleaseemailifafyi@iowa.gov.

Contact:Formoreinformationortoinquireabout

becomingaTakeCreditParticipatingLender:800-432-7230•IowaFinanceAuthority.gov/TakeCredit

Take CreditProgram

Iowa Finance Authority Announces Mortgage

Credit Certificate Program that will Allow First-Time Home Buyers to Reduce

Federal Tax Liability

CommonCENTS is a weekly e-newsletter that keeps you informed of current organization activities and community banking news, delivered to your email inbox every Friday.

Is everyone at your bank receiving CommonCENTS? If not, email CBI at [email protected] with a list of names and email addresses that you would like added to the recipient list.

If you would like to submit news and events from your bank for inclusion in the weekly e-newsletter, please contact Krissy Lee at [email protected].

Are you staying current on community banking news?

Get Some CommonCENTS

22 COMMUNITY BANKER UPDATE | MAY 2015