Embed Size (px)

Citation preview

COMMODITY RISK MANAGEMENT FOR INDIAN BANKS

Introduction

Agriculture commodities business is generally perceived as a high volume and low margin business and

is often accompanied by moderate to high level of price volatility. Farming activities (at pre-and post-

production stage) serve a classic example, wherein economic returns are highly vulnerable to

production risks, market risks and environmental/institutional risks.

Given the forward and backward linkages of agriculture to various sectors in the economy, different

risks experienced by primary agricultural producers get transmitted to the operations of input suppliers,

to entities involved in the commodity value chain and ultimately to the consumer. Spill over effects of

these risks get magnified due to the increasing integration of our domestic economy with the global

ecosystem.

Exposure of Banks to Commodities

1As banks are mandated to maintain an adequate credit flow to the agriculture sector and the value

chain participants (VCPs), the banking industry has direct or indirect exposures to firms having high

linkages with commodities and hence commodity prices.

In fact, agricultural financing forms a prime source of exposure to commodities for banks. Banks are

required to lend 18% of their (Adjusted) Net Bank Credit to agriculture and allied sector under the

'priority sector lending'(PSL).

They are required to deploy 13.5% of their non-food credit towards direct agricultural lending and 4.5%

towards indirect agricultural lending. According to RBI the total outstanding to agriculture and allied

activities under priority sector lending as on February 21, 2014, is Rs 651.1 thousand crore. This is an

increase of 13.1% as compared with the increase of 15.9% in February 2013 (Appendix II).

However, agriculture / commodity lending has not been a preferred choice for banks in India, as it is

susceptible to lower repayment rates or at times defaults. This makes it necessary for banks to find 2

cost-effective ways of mitigating these risks, even if the loan is collateralized or asset-backed.

Moreover given that for any bank customers, the volatility in physical market prices is the biggest risk, it

becomes extremely important for banks to monitor commodity price fluctuations. Understanding

factors which influence demand and supply of a commodity, its prices and its value chain will help banks

to avoid the problem of adverse selection and moral hazard. This in turn enable them manage their risks

efficiently and offer more innovative financing products (Refer to 'Road Ahead' section in the

subsequent paragraphs).

Refer to Appendix I for activities falling under direct and indirect lending to agriculture & allied sector.

In conventional lending, collateral is used to mitigate risks to the lender. However, collateral management requires technical know-how and special expertise as there could be issues related to the quality of the underlying which makes assaying and grading activities even more critical. Thus, ensuring the maintenance and periodic assessment of commodity collateral is often found difficult or outside the purview of banks' knowhow. Moreover, the credit advances to the agricultural sector is often marred by poor recovery; which exposes banks to the risk of liquidation of collateral at a price below the loan amount. Also, it is noteworthy that agri collateral is perishable and any quality degradation would mean liquidation of collateral at discounted market price.

1)

2)

Box 1: Warehouse Receipt Financing

Within value chain financing, warehouse receipt financing can be identified as an important source

of bank exposure to commodities. Warehouse Receipts are documents issued by warehouses to

depositors against the commodities deposited in the warehouses, for which the warehouse is the

bailee. Banks provide credit to farmers to finance their production, and to processors to finance

their inventories against structured warehouse receipts which provide secure collateral for banks

by assuring holders of the existence and quality conditions of agricultural inventories.

Warehouse receipt financing has its own set of risks. Banks are unable to verify credibility of the

warehouse owner and its managerial ability and also to evaluate quantity and quality of goods

stored in warehouses. Further, there is doubt regarding longevity of goods, as agricultural

commodities are prone to deterioration in quality, if stored over a longer period. Hence, in case of

default, if banks want to sell the pledged goods, they are not able to realise the (accurate) value

due to the deterioration in the quality of the goods.

Given the high risk associated with this kind of lending, banks are reluctant to extend such credit

and tend to charge high rate of interest on such loans. This has affected the deployment of rural

finance making banks fall short of meeting their lending targets. Some reports state that

performance of banks in meeting these sub-targets reveals that meeting the Direct Agriculture

sub-target has consistently proven to be a challenge for the banking system, with a 25% shortfall 3

in achievement against the stipulated target .

Government of India formulated WDRA 2007 to enable negotiability of Warehouse Receipt and 4thus forming the base for higher credit flow to the agriculture sector in the country.

http://www.ifmr.co.in/blog/2014/01/27/the-adjusted-psl-mechanism-for-priority-sector-lending-by-banks/

http://www.wdra.nic.in/

3)

4)

Mitigating Commodity Risks and Role of Commodity Derivatives Exchange

Formal Framework for Commodity Risk Management

Banks generally have their own risk management department for identification, measurement and

mitigation of commodity risks. They also have a formal enterprise risk management framework in

compliance with RBI guidelines. However, few banks have a separate formal risk management

framework/policy or procedure in place for identification, reporting, measurement, monitoring and

mitigation of commodity price risk.

Banks have internal limits for their lending exposure. These limits are generally calculated on the basis

of the sector or balance sheet of the borrower. Only rarely are the limits set commodity-wise. This

makes banks more vulnerable to credit defaults arising out of failure to manage commodity risk.

Moreover, banks in India are not allowed to participate in the commodity futures market, which also

limits their capacity to hedge commodity-related risks.

The Banking Regulation Act of 1949 strictly prohibits banks (both domestic and foreign) from trading in

goods. Therefore they are not allowed to trade in commodity futures market. The Section 8 of Banking

Regulation Act clearly states that no bank shall “directly or indirectly deal in the buying or selling or

bartering of goods, except in connection with the realisation of security given to or held by it.”

However, banks are allowed to finance the commodity business and provide fund and non-fund-based

facilities to commodity traders to meet their working capital requirements. Banks also provide clearing

and settlement services for commodities derivatives transactions. In India, banks can also own a stake

in commodity exchanges.

Road Ahead

Given the facts that banks do not have any specific, formal risk management system at their disposal to

mitigate commodity related risks; there are regulatory restrictions on participation in commodity

futures market; and unresolved issues related to collateral management; and the question is how are

banks going to mitigate commodity risks?

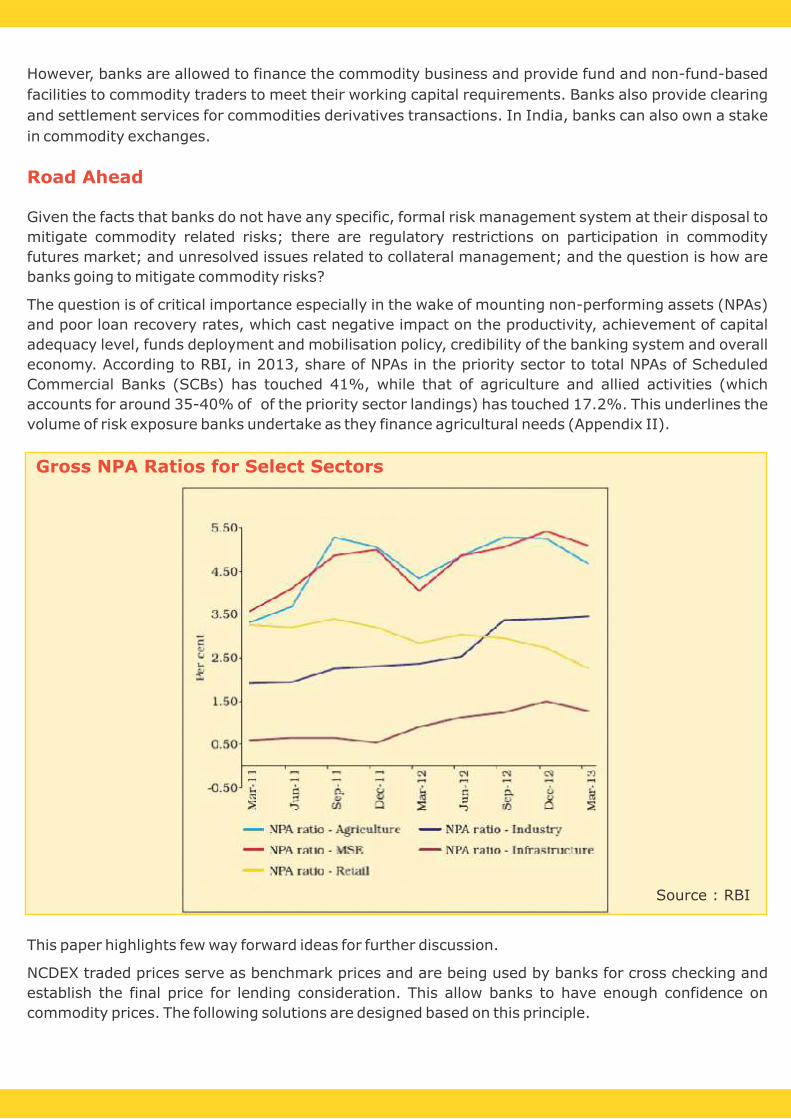

The question is of critical importance especially in the wake of mounting non-performing assets (NPAs)

and poor loan recovery rates, which cast negative impact on the productivity, achievement of capital

adequacy level, funds deployment and mobilisation policy, credibility of the banking system and overall

economy. According to RBI, in 2013, share of NPAs in the priority sector to total NPAs of Scheduled

Commercial Banks (SCBs) has touched 41%, while that of agriculture and allied activities (which

accounts for around 35-40% of of the priority sector landings) has touched 17.2%. This underlines the

volume of risk exposure banks undertake as they finance agricultural needs (Appendix II).

This paper highlights few way forward ideas for further discussion.

NCDEX traded prices serve as benchmark prices and are being used by banks for cross checking and

establish the final price for lending consideration. This allow banks to have enough confidence on

commodity prices. The following solutions are designed based on this principle.

Gross NPA Ratios for Select Sectors

Source : RBI

Solution 1 – The Banks provide advisory services to the clients operating in the commodity market and

help them build strategies to hedge their price risk on commodity futures exchanges, where there is

efficient price discovery and price risk management. A higher credit rating is given to entities that hedge

and report that on their balance sheet can be an additional requirement.

Solution 2 – Banks to act as Professional Clearing Members for Future as well as spot exchange

transactions. The number of members in both the platform is large which provides them with a business

opportunity as well. The spot exchange has 900 members and adds around 300 members every year.

On future exchange there are approximately 800 members.

Solution 3 – For meeting their obligation towards PSL banks can take advantage of goods deposited as

collateral in the Exchange ecosystem.

a. To address issues related to warehouse receipts, warehouse approval, and collateral

management, NCDEX through its spot exchange NSPOT (NCDEX Spot Exchange) has developed

a e-pledge platform which brings depositors, warehouse service providers and banks under one

umbrella. The risk of warehouse quality and management is addressed by stringent approval

norms and processes for empanelling a warehouse service provider. The risk of quality

deterioration in the underlying pledged commodity is reduced, as it is deposited onto the

approved warehouse which assays them on the basis of contract specifications. The empanelled

warehouse service provider guarantees the quality, safety and insurance of the deposited

commodities.

Thus, the foremost advantage for banks using the e-pledge platform is increased transparency,

as it enables online tracking and traceability of pledged lots. In event of a loan default by the

borrower, the bank can invoke the pledge, confiscate the pledged commodity and sell it through

the NSPOT that e- auction which ensures better price because of wider participation.

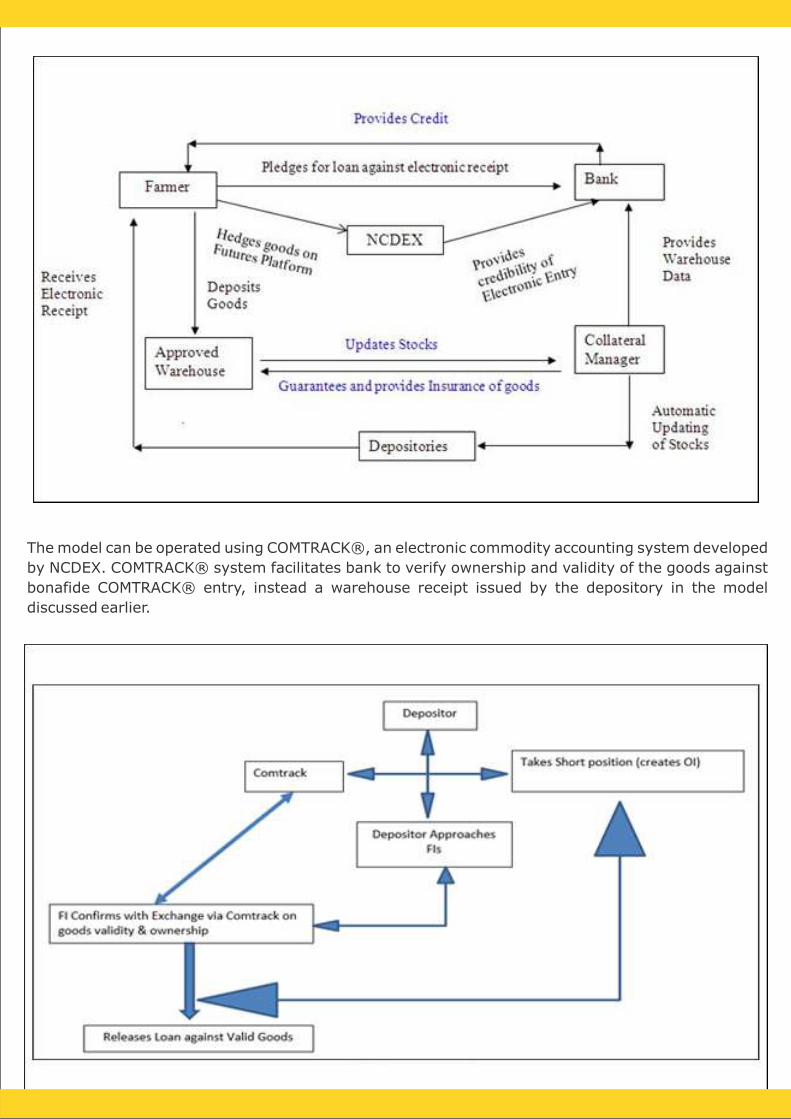

b. The system can be further refined by making a commodity-backed financing a more of a

market-linked product. A model can be built up aligning inventory finance to commodity

derivative exchange.

Functioning of the Model:

A farmer/trader/processor pledges his produce in the Exchange approved warehouse. A collateral

management company provides guarantee for quality and quantity and insurance for the goods

pledged, thus, covering the warehouse risk.

Books a short contract in that commodity on the Exchange and thus locks in his receivables for

future.

Since warehouses are electronically connected, information about the goods deposited

automatically gets updated on real-time basis and collateral management company issues a

dematerialised warehouse receipt to the farmer where he has deposited his produce.

The Loan seeker approaches bank for loan pledging the warehouse receipt.

The Exchange provides the credibility of warehouse receipt to the bank by confirming the details

about short position booked by the farmer and ownership of the goods, while the collateral

management company provides electronically updated information of the warehoused goods to

the bank.

Bank provides loans against the warehouse receipt after taking into account the interest burden

for financing, margins, mark-to-market (MTM) provisions of the exchange and warehouse

charges, till the expiry date of the contract

1.

2.

3.

4.

5.

6.

The model can be operated using COMTRACK®, an electronic commodity accounting system developed

by NCDEX. COMTRACK® system facilitates bank to verify ownership and validity of the goods against

bonafide COMTRACK® entry, instead a warehouse receipt issued by the depository in the model

discussed earlier.

The system of inventory finance along with hedging on the commodity exchange thus turns out to

be a win-win situation for farmer/ depositor as well as for banks (Refer to Appendix III for a case

study on Sugar Industry).

For a farmer, the system can help smoothening income flow by providing liquidity at times when

cash flows dry out. Availing of the facility simply extends his already existing price exposure

beyond the harvest season, providing him with a readily available cash flow and a potential upside.

Moreover, he can avail credit at favourable terms and conditions. He can get higher loan amount

(with less haircut) against the hedged collateral.

For banks, though the risk lies with them after lending against warehouse receipt or bonafide

COMTRACK® entry, the, since the commodity is hedged on the Exchange, thus covering credit

risk. Even if the depositor defaults, bank can sell the commodity Exchange and realise the value.

Additionally, the system can reduce some of the administrative hassles (maintaining KYC records)

for banks and save on heavy investments of time and manpower required for performing risk

assessment exercise.

Report of the Working Group on Risk Management in Agriculture - The Eleventh Five Year Plan

(2007-2012), Planning Commission, Govt. of India states

“Futures trading platforms can be used to provide effective risk-cover to farmers, on both the price

and volume ends and further between future and spot prices, in a seamless manner. While,

commodity exchanges may not be a panacea for all risk related issues of the farmers, their

platforms can be effectively harnessed, to deliver effective results, along with other risk mitigation

measures such as contract farming, product diversification, market development, etc.”

Smooth and efficient functioning of the model can be ensured adhering to the following conditions:

Short position taken in the future contracts

The term loan /margin funding will be depend on validity of goods – shorter period can be the

case for margin funding

Goods pledged will be locked in Comtrack during the term of loan

Hedged position against which loan has been issued will be locked and can't be squared off

MTM account will be locked with exchange; however, he will have to bring in pay in amount

depending upon the margin requirement

FMC regulations will be amended to the extent that banks can access information on the

hedge position of the pledgee on daily basis

WDRA 2007 will be modified to accept electronic entry as bona fide to be stock statement

against which lending and margin funding can be done

5RBI Working Group report (2005) recognizes the fact banks lending to agriculture commodities

are exposed to Price volatility and commodity derivatives platform can mitigate such risks to a

certain extent. The WG also observed that “while dealing in commodity futures, banks are in

effect, dealing in financial instruments and hence, trading in commodity derivatives may be

treated as permissible. To remove any lingering doubt, banks could be prohibited from giving or

taking physical delivery.”

For the Exchange, the system might help enhance the liquidity, especially in mid and far month

contracts depending on the maturity periods of credit.

Finally, there is a business opportunity for banks in reaching out to the major value chain

participants in the commodity sector. This will not only help them mitigate their own commodity

risk but also help them connect with small suppliers, especially farmers. This will go a long towards

financial inclusion, thereby empowering and enabling people to participate more effectively in the

economy.

http://www.prsindia.org/uploads/media/1167471035/bill67_2007010167_Report_ofRBI_working_group_on_warehouse_receipts_and_commodity_futures.pdf5)

Appendix I: Description of the Categories under Priority Sector

1.1. Direct Agriculture

Loans to individual farmers [including Self Help Groups (SHGs) or Joint Liability Groups (JLGs), i.e.

groups of individual farmers, provided banks maintain disaggregated data on such loans] engaged

in Agriculture and Allied Activities, viz., dairy, fishery, animal husbandry, poultry, bee-keeping and

sericulture (up to cocoon stage).

Loans to others [such as corporates, partnership firms and institutions] for Agriculture and Allied

Activities (dairy, fishery, piggery, poultry, bee-keeping, etc.) up to an aggregate limit of Rs 2 crore

per borrower for the following purposes:

Short-term loans for raising crops, i.e. for crop loans.This will include traditional/non-

traditional plantations, horticulture and allied activities.

Medium & long-term loans for agriculture and allied activities (e.g. purchase of agricultural

implements and machinery, loans for irrigation and other developmental activities

undertaken in the farm and development loans for allied activities).

Loans for pre-harvest and post-harvest activities viz. spraying, weeding, harvesting, sorting,

grading and transporting of their own farm produce.

Loans to farmers up to Rs 50 lakh against pledge / hypothecation of agricultural

produce (including warehouse receipts) for a period not exceeding 12 months,

irrespective of whether the farmers were given crop loans for raising the produce or not.

Loans to small and marginal farmers for purchase of land for agricultural purposes.

Loans to distressed farmers indebted to non-institutional lenders, against appropriate

collateral.

Export credit for exporting their own farm produce.

(i)

(ii)

(iii)

(iv)

(v)

(vi)

(vii)

1.2. Indirect agriculture

1.2.1. Loans to corporates, partnership firms and institutions engaged in Agriculture and Allied

Activities [dairy, fishery, animal husbandry, poultry, bee-keeping and sericulture (up to cocoon

stage)]

If the aggregate loan limit per borrower is more than Rs. 2 crore in respect of eligible advances

under direct agriculture, the entire loan should be treated as indirect finance to agriculture

Short-term loans for raising crops, i.e. for crop loans. This will include traditional/non-

traditional plantations, horticulture and allied activities.

Medium & long-term loans for agriculture and allied activities (e.g. purchase of agricultural

implements and machinery, loans for irrigation and other developmental activities

undertaken in the farm, and development loans for allied activities).

Loans for pre-harvest and post-harvest activities such as spraying, weeding, harvesting,

grading and sorting.

Loans up to Rs 50 lakh against pledge / hypothecation of agricultural produce

(including warehouse receipts) for a period not exceeding 12 months, irrespective

of whether the farmers were given crop loans for raising the produce or not.

Export credit to corporates, partnership firms and institutions for exporting their own farm

produce.

Loans up to Rs 5 crore to Producer Companies set up exclusively by only small and marginal

farmers under Part IXA of Companies Act, 1956 for agricultural and allied activities.

(i)

(ii)

(iii)

(iv)

(v)

(vi)

1.2.2. Other indirect agriculture loans

Loans up to Rs 5 crore per borrower to dealers / sellers of fertilizers, pesticides, seeds, cattle

feed, poultry feed, agricultural implements and other inputs.

Loans for setting up of Agri-clinics and Agribusiness Centres.

Loans to Custom Service Units managed by individuals, institutions or organisations who

maintain a fleet of tractors, bulldozers, well-boring equipment, threshers, combines, etc.,

and undertake farm work for farmers on contract basis.

Loans for construction and running of storage facilities (warehouse, market yards, godowns

and silos), including cold storage units designed to store agriculture produce/products,

irrespective of their location.

(i)

(ii)

(iii)

(iv)

Appendix II:

gAug

Priority Sector Lending

4. Constituent items may not add up to the total due to rounding off.

Source: Based on off-site returns (domestic).

Appendix III: Hedging in Sugar Futures by VCPs – A Risk Mitigation Opportunity for Banks

Sugar remains one of the most volatile of all the commodities, given pronounced cyclicality in the

production of sugar cane as well as in sugar on one hand and increasing demand for sugar from

food and energy segments on the other. Being regarded as an essential commodity, regulatory

policies (vis-a-vis pricing, distribution and trade of sugar) over the years have been geared

towards protecting the interest of cane growers, sugar manufacturers and domestic consumers.

However, they have rendered fixed sugar cane prices disconnected from the relatively market-

based sugar prices, thus, leaving room for fluctuations in sugar prices arising due to demand-

supply mismatch in the domestic as well as international market.

6Very high volatility in sugar prices poses significant downside risks to its value chain participants;

to the extent of affecting their credit re-payment ability. This, in turn, raises the probability of

credit defaults, weakening the balance sheets of financial institutions involved in extending credit 7

facilities to the sugar industry VCPs . For instance, as on March 31, 2012, SBI had fund based

exposures of Rs 8580.72 crore to Sugar industry (28% of total industry); of which around 0.5%

has turned into NPA.

Hedging (partially/fully) their risks on the futures platform facilitate sugar industry VCPs lock in

their margins insulating themselves from the impact of adverse movements in sugar prices and

can, indirectly, help banks manage their credit risks.

Our study (based on the historical data sourced from CMIE) to analyse the benefits of trading in

sugar futures to sugar industry VCPs revealed that a confectionary manufacturer, who uses sugar

as one of the major raw materials, can reduce his expense on sugar purchase by trading in sugar

futures (Box 2).

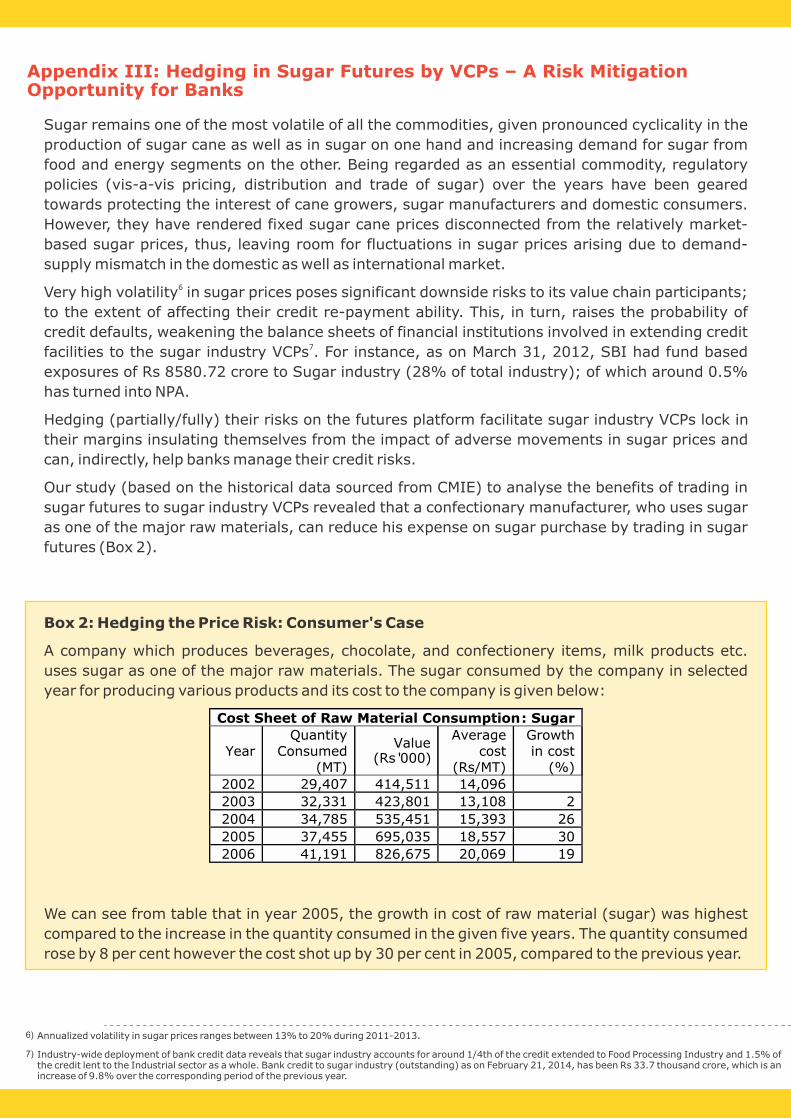

Box 2: Hedging the Price Risk: Consumer's Case

A company which produces beverages, chocolate, and confectionery items, milk products etc.

uses sugar as one of the major raw materials. The sugar consumed by the company in selected

year for producing various products and its cost to the company is given below:

We can see from table that in year 2005, the growth in cost of raw material (sugar) was highest

compared to the increase in the quantity consumed in the given five years. The quantity consumed

rose by 8 per cent however the cost shot up by 30 per cent in 2005, compared to the previous year.

Annualized volatility in sugar prices ranges between 13% to 20% during 2011-2013.

Industry-wide deployment of bank credit data reveals that sugar industry accounts for around 1/4th of the credit extended to Food Processing Industry and 1.5% of the credit lent to the Industrial sector as a whole. Bank credit to sugar industry (outstanding) as on February 21, 2014, has been Rs 33.7 thousand crore, which is an increase of 9.8% over the corresponding period of the previous year.

6)

7)

It was noticed that futures contracts in sugar had indicated upward movement in prices in 2005.

When the futures price of sugar was higher compared to the last year's average cost, the company

could have hedged a part of its requirement on the futures platform. If the company would have

hedged a part of the total quantity consumed in that year, the savings on the part of raw material

cost from the hedged output would have been as followed:

If the company would have hedged some part of its total sugar requirement, it might have saved

on the cost of raw material (6.2%) and bank's credit risk exposure could have been mitigated to

the same extent. The company had the option of taking delivery of the commodity or if the variety

of sugar used is different from the traded commodity specifications, it could have squared off the

position at higher prices. The gain on futures platform could have been utilized while buying

required variety of sugar from the spot market.

Disclaimer

NCDEX does not represent or guarantee the accuracy or completeness of the Information even though NCDEX has taken efforts to ensure that the information provided as part of this report is as accurate as possible at the time of inclusion in the report.

NCDEX shall not be liable for any changes, including without limitation direct or indirect, special, incidental or consequential damages, losses or expenses that may arise on account of such investment decisions based on this report.