Embed Size (px)

DESCRIPTION

Commodities Report, Gold, Oil, Silver, USD, Grains

Citation preview

Paul Ebeling Commodities Report, Gold, Oil,

Silver, USD, Grains

24 March 2011

Red's Mid-week Report on Gold, Silver and Crude Oil + USD and Chicago Grains Charts by Omega Research 24 March 2011 Paul A. Ebeling, Jnr. www.livetradingnews.com The Overall Fundamentals Gold and Silver Gold futures on the COMEX Division of the New York Merc rose again Wednesday, as players remained concerned about developments in the MENA region, and the rally in energy prices intensified the fear of inflation. Global unrest moved the precious metals higher in a flight to safety. Apr Gold rallied for 0.7% to finish at 1438.00 oz, and May Sillver rose 2.5% to finish pit trade 37.19 oz. Silver traded to a new 31 yr high at 37.29, and Gold put in highs at 1441.20, just 4 pts short of its all time high. Crude Oil and Nat Gas US Crude Oil price Wednesday hit its highest mark since September 26, 2008, as US gasoline inventories dropped sharply last week and unrest in the MENA region weighted on the markets.

The US Energy Information Administration (EIA) said Wednesday, the gasoline stocks declined 5.32M bbls in the week ended March 18, surpassing an analyst forecast of a 1.8M bbl drop.

The gasoline stocks decline in the 1st 3 weeks in March was the most for the period since EIA started gathering weekly information in Y 1990. Gasoline demand over the past 4 weeks was 1.2% higher than a year earlier, the EIA said. And US is entering the Prime driving season, gasoline demand would increase in the next 90 days.

The unrest in the Middle East is still weighing the nervous players. In Libya, Western countries have started another round of air and missile strikes. In Yemen, the tension between the government and protesters got intensified. In Syria, violent protests spread to the Southern areas.

Light, Sweet Crude (WTI) for May delivery gained 78c to settle at 105.75 bbl on the New York Merc. In London, Brent Light Crude for May delivery last traded just above 115 bbl.

The US Dollar

The USD rose against major currencies in late New York trading Wednesday as Portugal' s austerity plan was rejected, and Great Britain cut its economic growth prospect in Y 2011 and Y 2012.

The vote comes just a day before a 2 day Summit of EU leaders which intends to discuss measures to boost economic co-ordination across the EuroZone.

The concerns over Portugal weighed on the Euro. The currency fell below 1.42% the USD in New York's trading session Wednesday.

The GBP fell against the "Greenback" Wednesday as Britain cut its economic growth forecasts.

The USD steadied vs. JPY between the range of 80. 80 and 81.00 in Wednesday's trading on player's cautions on further intervention and worries about radiation leaks from damaged Japanese nuclear power plants.

In late Tuesday trading, the USD bought 80.86 Yen, comparing with 80.91 late Monday, and the Euro fell to 1.4123 from 1. 4207.

The GBP fell to 1.6246 from 1.6382. The USD rose from 0.9032 to 0.9081 vs. the Swiss franc, and also rose to 0.9806 Canadian Dollars from 0.9793.

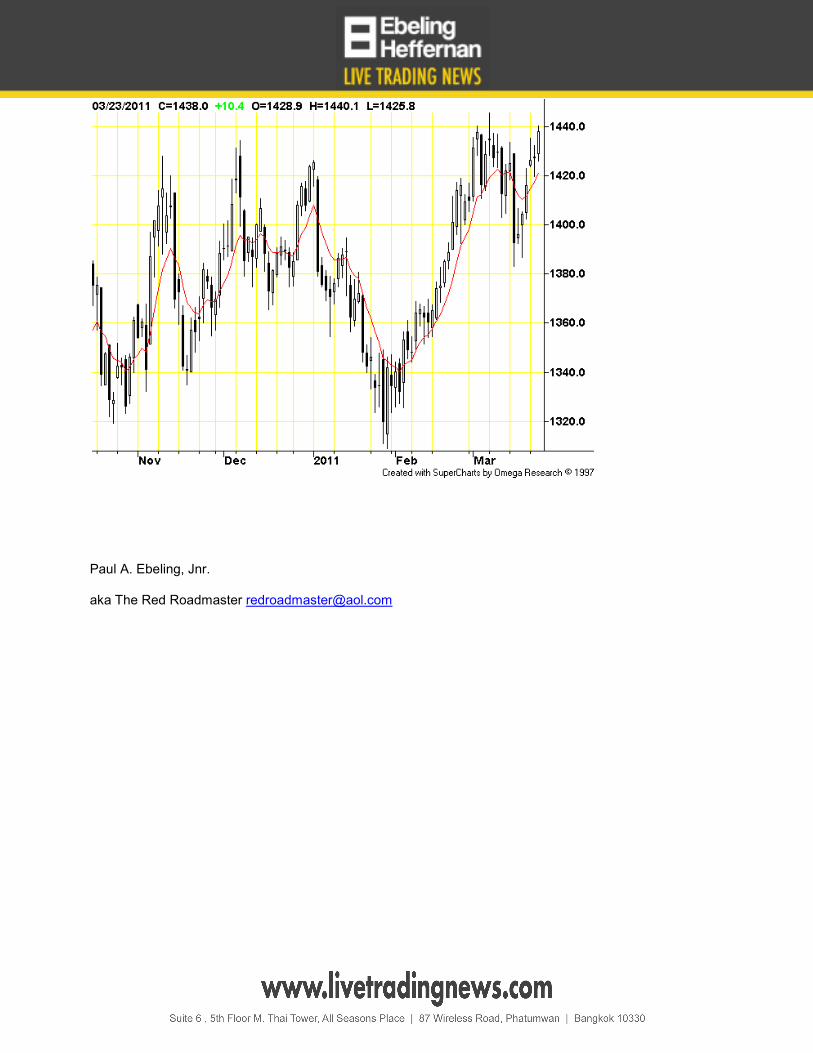

Chicago Grains

Chicago Grains contracted Wednesday, as a US government report indicated weak exports in the previous week. Besides, a firm USD and moisture weather in US also added a negative tone.

The most active Corn contract for May delivery fell 5.75c, or 0.84%, closing at 6.81 per bushel. May Wheat lost 8c, or 1.1%, to 7.1425 per bushel. May Soybean declined 14.25c, or 1%, to 13.5125 per bushel.

According to USDA's report, for the week from March 4 to 10, US sold a net of 146,800 metric tons of Soybeans to the World's importers for delivery in the marketing year F-Y 2010-2011, which was down 64% from the previous week and 59% from the average of the prior 4 weeks. The exports for the market Y 2011/2012 amounted to 27,700 metric tons.

Market traders attributed the weak exports to poor profit margins by China crushers and a shift to South America Soybeans by other end users.

Net exports of wheat totaled 858,800 metric tons for the week ended March 10, which is lower than expectation.

Some forecasters see moisture for the Western sections of the southern plains which have been the driest in the US Wheat growing area, and this helped spark a sharp sell off in the market

The Overall Technicals

Comex Gold (GC)

Gold is range bound at 1380.7/1445.7 and intra-day bias remains Neutral. Consolidations from 1445.7 may continue. But even in case of another decline, I expect strong support from 61.8% retracement at 1361.3 and bring on a rebound.

On the Upside: a clear decisive break of 1445.7 will confirm up-trend resumption for 100% projection of 1155.6 to 1432.5 from 1309.1 at 1480.2 next. But, a clear break of 1361.3 fibo mark will turn my focus back to 1309.1, the Key near term support, next.

The Big Picture: Gold is trading comfortably inside the long term rising channel from 681, the Y 2008 low, and there is no clear sign of reversal in here. Weekly MACD is supported by its trend line and Gold is regaining upside momentum. That said, I am staying Bullish as long as 1309.1 support holds, and I expect the current up-trend to target 1500, the Psych level, next. But, a clear break of 1309.1, Key support, will

indicate medium term Topping out, and should bring pull back to 1004.5/1227.5, the cluster support zone. Stay tuned...

Comex Silver (SI)

Silver closed higher Wednesday but the upside is limited below 36.74 resistance and the intra-day bias remains Neutral.

Consolidations from 36.47 might extend further. But, in case of another fall, I expect strong support from 31.52/69, 50% retracement of 26.30 to 36.74 at 31.52, to contain any downside and bring on a rebound.

On the Upside: a clear break of 36.74, the high, confirms the up-trend resumption for 100% projection of 17.735 to 31.275 from 26.3 at 39.84, which is close to 40 psych mark.

The Big Picture: long term up-trend in Silver is in progress, and is gaining momentum with weekly MACD back above Signal line. This rally will target 200% projection of 8.4 to 19.50 from 14.50 at 36.85 next, and will likely extend towards 261.8% projection at 43.71.

That being said, a clear break of 31.275, the Key resistance turned support, is needed to be the 1st signal of a reversal. Barring that, my medium term outlook is Bullish on Silver. Stay tuned...

Nymex Crude Oil (CL)

Crude Oil's rebound from 96.22 resumed after brief consolidations and intra-day bias is back on the upside for 106.95, Key resistance. A clear break there will confirm resumption of the rally and targets 100% projection of 64.23 to 92.58 from 83.85 at 112.20.

On the Downside: a break below 101.43 will bring on another decline to extend the consolidation from 106.95. But, any downside would be contained by 95.62 support, 50% retracement of 83.85 to 106.95 at 95.40, and bring on a resumption of the rise.

The Big Picture: the medium term rebound from 33.2 is in progress, and stronger rise should be seen towards 100% projection of 33.2 to 83.95 from 64.23 at 114.98. There is no change in my POV that this rally is the 2nd wave of the consolidation pattern from that started at 147.27, the Y 2008 high. So, I will start to look for reversal signal again above the 114.98 projection level. But, a break of 83.85, Key support, is needed to be the 1st sign of a medium term reversal, and break of 64.23 is needed to confirm that action. Barring that my outlook is Bullish on Crude Oil. Stay tuned...

Suite 53 Athenee Tower 63 Wireless Road, Lumpini, Pathumwan, Bangkok 10330 THAILAND

Tel: +66 2 126 8045

Fax: +66 2 126 8080

Mobile: +66 8 5997 0635

Email : [email protected]

New York

347 5th Avenue, Suite 1402-508 Ny, NY 10016

Tel: +1 646-403-9881

Fax: +1 646-403-8014

Singapore

3 Raffles Place #07-01 Bharat Building Singapore 048617

Tel: +65 6329 6408

Fax: +65 6329 9699

www.ebeling-heffernan.com www.livetradingnews.com www.paul-ebeling.com www.redroadmaster.com

Paul A. Ebeling, Jr. writes and publishes The Red Roadmaster’s Technical Report on the US Major Market

Indices, a weekly, highly-regarded financial market letter, read by opinion makers, business leaders and

organizations around the world. Ebeling has studied the global financial and stock markets since 1984,

following a successful business career that included investment banking, and market and business

analysis. He is a specialist in equities/commodities, and an accomplished chart reader who advises

technicians with regard to Major Indices Resistance/Support Levels. Paul Ebeling is a CO-Founder of

Ebeling Heffernan Asia’s fastest growing Advisory Firm and is a Senior Dark Pool FX, Equity and

Commodity Analyst at Heffernan Capital Management. www.heffcap.com

Disclaimer

Ebeling Heffernan (EH) distributes research and other information purchased and compiled from outside sources and analysts. This

report/release/advertisement is a commercial advertisement and is for general information purposes only. Do not base any investment decision

on information in this report/release/advertisement. EH is not a registered Investment Advisor or a member of any association for other

research providers. Under no circumstances is this report/release/advertisement to be used or considered as an offer to sell or a solicitation of

any offer to buy any security or other debt instruments, or any options, futures or other derivatives related to such securities herein. All

information herein is not intended to be used for investment advice. Price Targets are academic theory and should not be relied upon. The

majority of these profiled companies are highly risky OTC Bulletin Board or Pink Sheet companies. All readers of this information indemnify EH

from any liability for all accessed information. EH will not be responsible for updating any of its information in its report/release/advertisements.

EH advises recipients of all such data to be validated from the issuing company including all statistical information derived from SEC filings, from

data sources or financial information and data from the issuing company contained herein. The reader should seek professional financial advice,

verify all claims and do his/her own research and due diligence before investing in any securities mentioned. EH will not be liable to any person

or entity for the quality, accuracy, completeness, reliability or timeliness of information in this report/release/advertisement, or for any

direct, indirect, consequential, incidental, special or punitive damages that may arise out of the use of information, products or services from any

person or entity including but not limited to lost profits, loss of opportunities, trading losses, and damages that may result from any

incompleteness or inaccuracy in any of EH’s profiled companies. When paid in stock, EH its affiliates, directors, officers, outside sources, investor

awareness groups and employees may liquidate shares at any time or hold for investment purposes. Readers are advised to review SEC periodic

reports: Forms 10-Q, 10K, Form 8-K, insider reports, Forms 3, 4, 5 Schedule 13D, www.sec.gov.nasd.com, www.pinksheets.com, www.sec.gov

and www.finra.com. SPC is compliant with the Can Spam Act of 2003. Investing in micro cap and small cap securities is speculative and carries a

high degree of risk. Investors can lose their entire investment. The Private Securities Litigation Reform Act of 1995 provides investors a 'safe

harbor' in regard to forward-looking statements. EH cautions all investors that such forward-looking statements in this

report/release/advertisement are not guarantees of future performance. Investors should understand that statements regarding future

prospects may not be realized. This report/release/advertisement does not have regard to the specific investment objective, financial situation,

suitability, and the particular need of any specific person who may receive this report/release/advertisement. Investors should note that income

from such securities, if any, may fluctuate and that each security's price or value may rise or fall substantially. Accordingly, investors may receive

back less than originally invested, or lose their entire investment. Past performance is not indicative of future performance. The Company has

not paid compensation for this commercial advertisement. HCM. has written this commercial advertisement for EH.