Embed Size (px)

Citation preview

Michael S Haigh Managing Director, Head of Commodities Research

Phone: +212 278 6020

Important Notice: The circumstances in which this publication has been produced are such that it is not appropriate to characterise it as independent

investment research as referred to in MiFID and that it should be treated as a marketing communication even if it contains a research recommendation. This

publication is also not subject to any prohibition on dealing ahead of the dissemination of investment research. However, SG is required to have policies to

manage the conflicts which may arise in the production of its research, including preventing dealing ahead of investment research.

March 2017

TOP DOWN AND BOTTOM UP IN COMMODITIES

Michael Haigh – MD / Head of Commodity Research 2

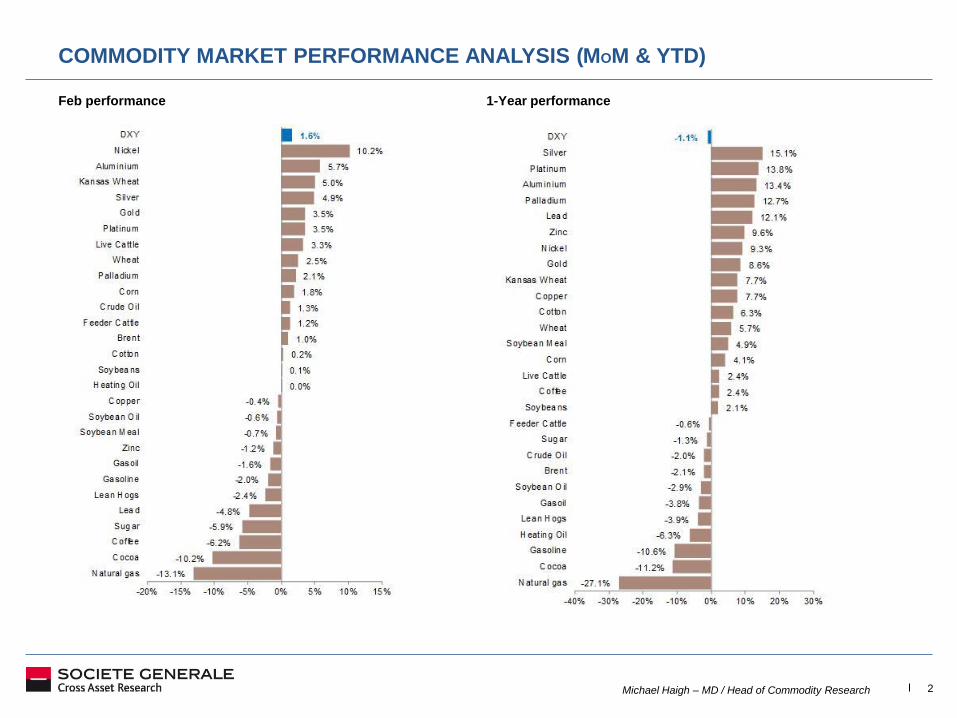

COMMODITY MARKET PERFORMANCE ANALYSIS (MOM & YTD)

Feb performance 1-Year performance

Michael Haigh – MD / Head of Commodity Research 3

OVERVIEW

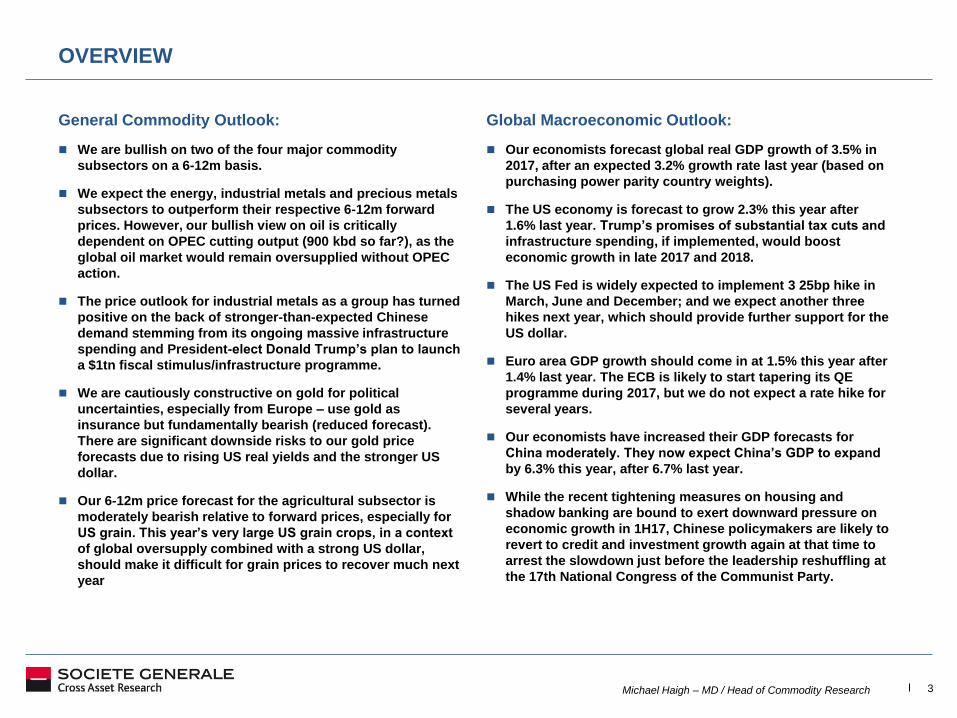

General Commodity Outlook:

We are bullish on two of the four major commodity

subsectors on a 6-12m basis.

We expect the energy, industrial metals and precious metals

subsectors to outperform their respective 6-12m forward

prices. However, our bullish view on oil is critically

dependent on OPEC cutting output (900 kbd so far?), as the

global oil market would remain oversupplied without OPEC

action.

The price outlook for industrial metals as a group has turned

positive on the back of stronger-than-expected Chinese

demand stemming from its ongoing massive infrastructure

spending and President-elect Donald Trump’s plan to launch

a $1tn fiscal stimulus/infrastructure programme.

We are cautiously constructive on gold for political

uncertainties, especially from Europe – use gold as

insurance but fundamentally bearish (reduced forecast).

There are significant downside risks to our gold price

forecasts due to rising US real yields and the stronger US

dollar.

Our 6-12m price forecast for the agricultural subsector is

moderately bearish relative to forward prices, especially for

US grain. This year’s very large US grain crops, in a context

of global oversupply combined with a strong US dollar,

should make it difficult for grain prices to recover much next

year

Global Macroeconomic Outlook:

Our economists forecast global real GDP growth of 3.5% in

2017, after an expected 3.2% growth rate last year (based on

purchasing power parity country weights).

The US economy is forecast to grow 2.3% this year after

1.6% last year. Trump’s promises of substantial tax cuts and

infrastructure spending, if implemented, would boost

economic growth in late 2017 and 2018.

The US Fed is widely expected to implement 3 25bp hike in

March, June and December; and we expect another three

hikes next year, which should provide further support for the

US dollar.

Euro area GDP growth should come in at 1.5% this year after

1.4% last year. The ECB is likely to start tapering its QE

programme during 2017, but we do not expect a rate hike for

several years.

Our economists have increased their GDP forecasts for

China moderately. They now expect China’s GDP to expand

by 6.3% this year, after 6.7% last year.

While the recent tightening measures on housing and

shadow banking are bound to exert downward pressure on

economic growth in 1H17, Chinese policymakers are likely to

revert to credit and investment growth again at that time to

arrest the slowdown just before the leadership reshuffling at

the 17th National Congress of the Communist Party.

Michael Haigh – MD / Head of Commodity Research 4

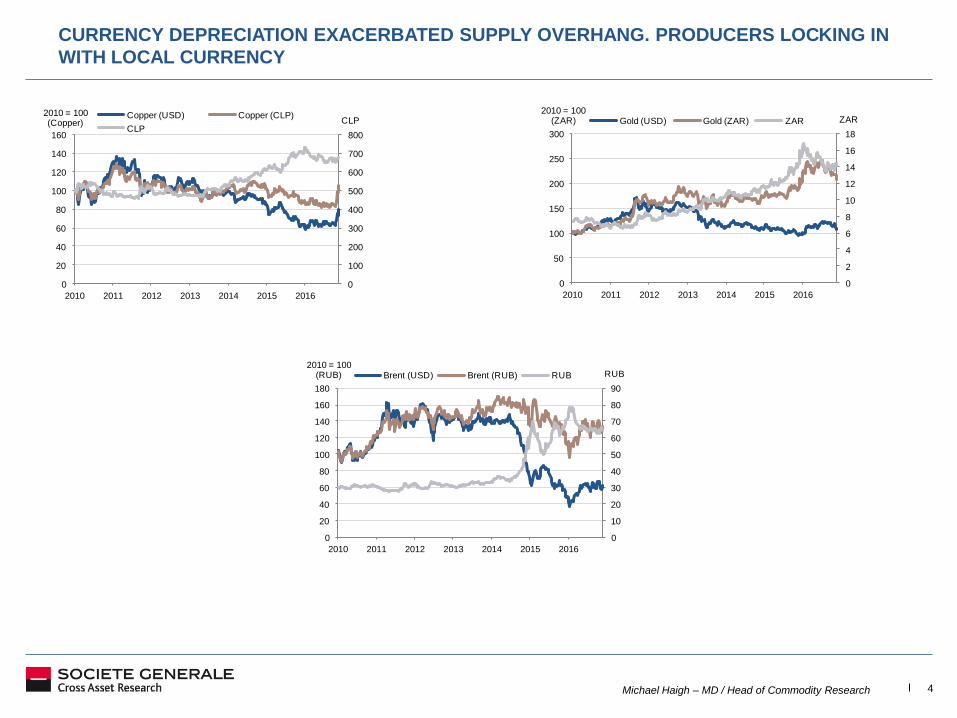

CURRENCY DEPRECIATION EXACERBATED SUPPLY OVERHANG. PRODUCERS LOCKING IN

WITH LOCAL CURRENCY

0

100

200

300

400

500

600

700

800

0

20

40

60

80

100

120

140

160

2010 2011 2012 2013 2014 2015 2016

CLP2010 = 100(Copper)

Copper (USD) Copper (CLP)

CLP

0

2

4

6

8

10

12

14

16

18

0

50

100

150

200

250

300

2010 2011 2012 2013 2014 2015 2016

ZAR2010 = 100

(ZAR) Gold (USD) Gold (ZAR) ZAR

0

10

20

30

40

50

60

70

80

90

0

20

40

60

80

100

120

140

160

180

2010 2011 2012 2013 2014 2015 2016

RUB2010 = 100

(RUB) Brent (USD) Brent (RUB) RUB

Michael Haigh – MD / Head of Commodity Research 5

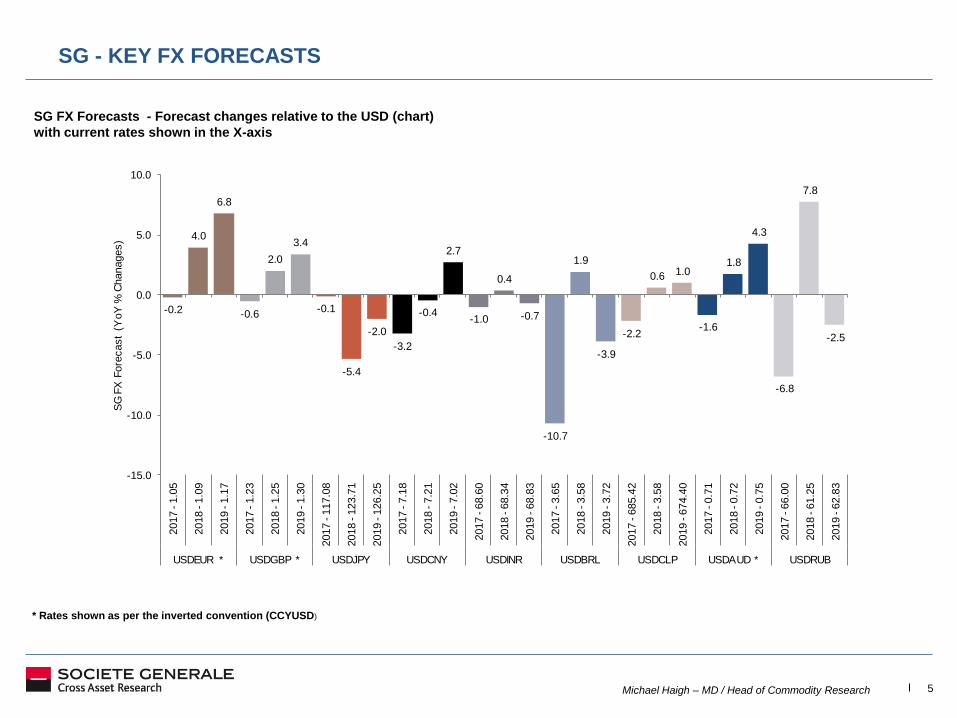

SG - KEY FX FORECASTS

SG FX Forecasts - Forecast changes relative to the USD (chart)

with current rates shown in the X-axis

* Rates shown as per the inverted convention (CCYUSD)

-0.2

4.0

6.8

-0.6

2.0

3.4

-0.1

-5.4

-2.0

-3.2

-0.4

2.7

-1.0

0.4

-0.7

-10.7

1.9

-3.9

-2.2

0.6 1.0

-1.6

1.8

4.3

-6.8

7.8

-2.5

-15.0

-10.0

-5.0

0.0

5.0

10.02017 -

1.0

5

2018 -

1.0

9

2019 -

1.1

7

2017 -

1.2

3

2018 -

1.2

5

2019 -

1.3

0

2017 -

117.0

8

2018 -

123.7

1

2019 -

126.2

5

2017 -

7.1

8

2018 -

7.2

1

2019 -

7.0

2

2017 -

68.6

0

2018 -

68.3

4

2019 -

68.8

3

2017 -

3.6

5

2018 -

3.5

8

2019 -

3.7

2

2017 -

685.4

2

2018 -

3.5

8

2019 -

674.4

0

2017 -

0.7

1

2018 -

0.7

2

2019 -

0.7

5

2017 -

66.0

0

2018 -

61.2

5

2019 -

62.8

3

USDEUR * USDGBP * USDJPY USDCNY USDINR USDBRL USDCLP USDAUD * USDRUB

SG

FX

Fore

cast

(YoY

% C

hanages)

Michael Haigh – MD / Head of Commodity Research 6

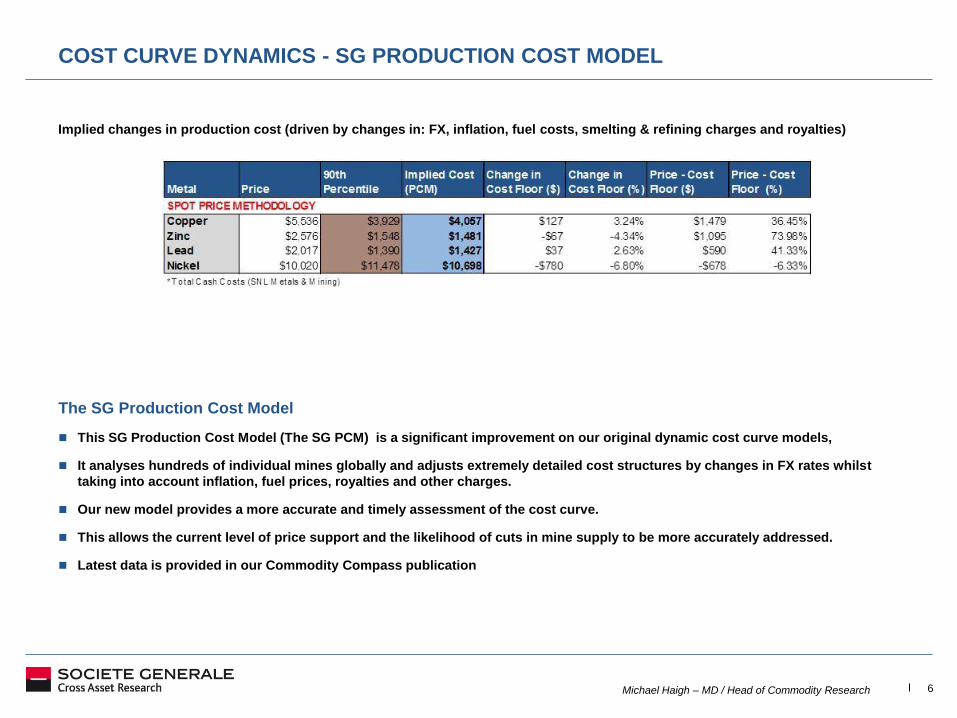

COST CURVE DYNAMICS - SG PRODUCTION COST MODEL

Implied changes in production cost (driven by changes in: FX, inflation, fuel costs, smelting & refining charges and royalties)

The SG Production Cost Model

This SG Production Cost Model (The SG PCM) is a significant improvement on our original dynamic cost curve models,

It analyses hundreds of individual mines globally and adjusts extremely detailed cost structures by changes in FX rates whilst

taking into account inflation, fuel prices, royalties and other charges.

Our new model provides a more accurate and timely assessment of the cost curve.

This allows the current level of price support and the likelihood of cuts in mine supply to be more accurately addressed.

Latest data is provided in our Commodity Compass publication

Michael Haigh – MD / Head of Commodity Research 7

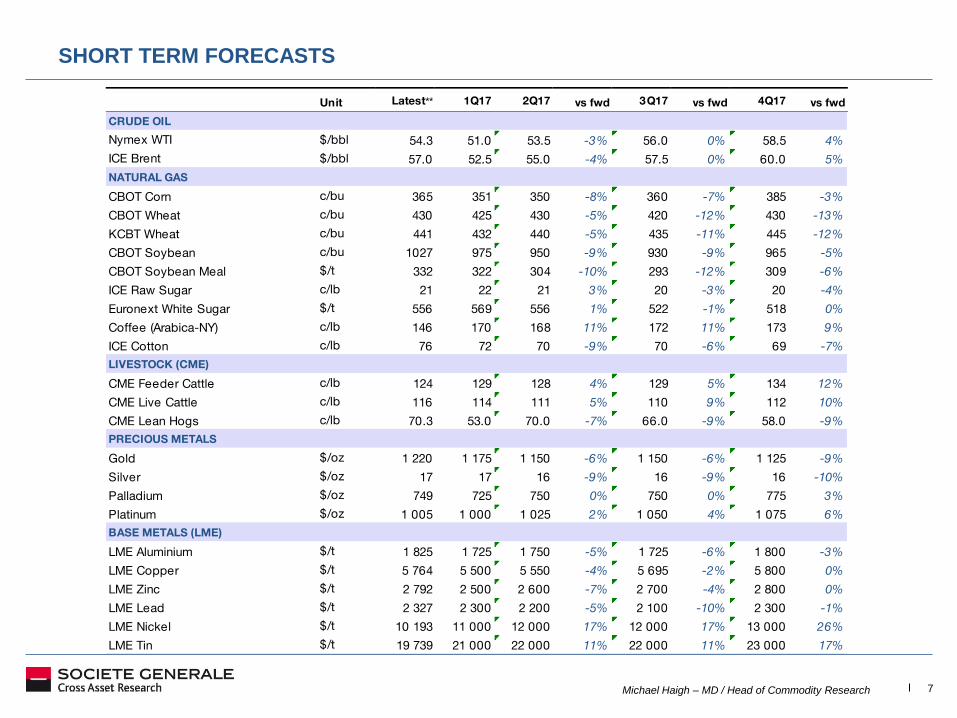

SHORT TERM FORECASTS

Unit Latest** 1Q17 2Q17 vs fwd 3Q17 vs fwd 4Q17 vs fwd

CRUDE OIL

Nymex WTI $/bbl 54.3 51.0 53.5 -3% 56.0 0% 58.5 4%

ICE Brent $/bbl 57.0 52.5 55.0 -4% 57.5 0% 60.0 5%

NATURAL GAS

CBOT Corn c/bu 365 351 350 -8% 360 -7% 385 -3%

CBOT Wheat c/bu 430 425 430 -5% 420 -12% 430 -13%

KCBT Wheat c/bu 441 432 440 -5% 435 -11% 445 -12%

CBOT Soybean c/bu 1027 975 950 -9% 930 -9% 965 -5%

CBOT Soybean Meal $/t 332 322 304 -10% 293 -12% 309 -6%

ICE Raw Sugar c/lb 21 22 21 3% 20 -3% 20 -4%

Euronext White Sugar $/t 556 569 556 1% 522 -1% 518 0%

Coffee (Arabica-NY) c/lb 146 170 168 11% 172 11% 173 9%

ICE Cotton c/lb 76 72 70 -9% 70 -6% 69 -7%

LIVESTOCK (CME)

CME Feeder Cattle c/lb 124 129 128 4% 129 5% 134 12%

CME Live Cattle c/lb 116 114 111 5% 110 9% 112 10%

CME Lean Hogs c/lb 70.3 53.0 70.0 -7% 66.0 -9% 58.0 -9%

PRECIOUS METALS

Gold $/oz 1 220 1 175 1 150 -6% 1 150 -6% 1 125 -9%

Silver $/oz 17 17 16 -9% 16 -9% 16 -10%

Palladium $/oz 749 725 750 0% 750 0% 775 3%

Platinum $/oz 1 005 1 000 1 025 2% 1 050 4% 1 075 6%

BASE METALS (LME)

LME Aluminium $/t 1 825 1 725 1 750 -5% 1 725 -6% 1 800 -3%

LME Copper $/t 5 764 5 500 5 550 -4% 5 695 -2% 5 800 0%

LME Zinc $/t 2 792 2 500 2 600 -7% 2 700 -4% 2 800 0%

LME Lead $/t 2 327 2 300 2 200 -5% 2 100 -10% 2 300 -1%

LME Nickel $/t 10 193 11 000 12 000 17% 12 000 17% 13 000 26%

LME Tin $/t 19 739 21 000 22 000 11% 22 000 11% 23 000 17%

Michael Haigh – MD / Head of Commodity Research 8

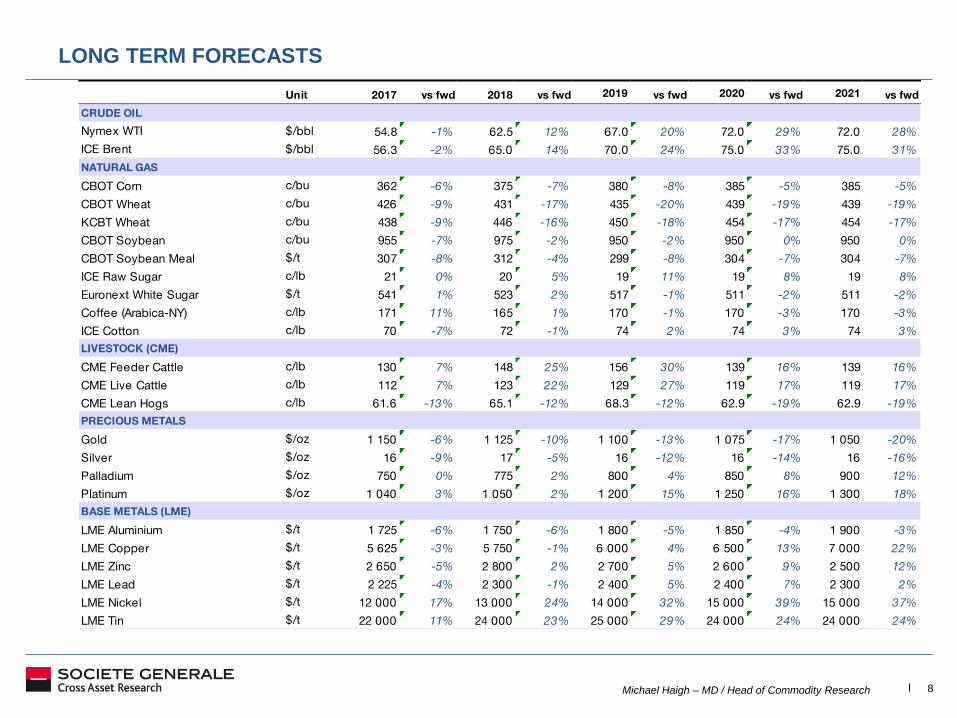

LONG TERM FORECASTS

Unit 2017 vs fwd 2018 vs fwd 2019 vs fwd 2020 vs fwd 2021 vs fwd

CRUDE OIL

Nymex WTI $/bbl 54.8 -1% 62.5 12% 67.0 20% 72.0 29% 72.0 28%

ICE Brent $/bbl 56.3 -2% 65.0 14% 70.0 24% 75.0 33% 75.0 31%

NATURAL GAS

CBOT Corn c/bu 362 -6% 375 -7% 380 -8% 385 -5% 385 -5%

CBOT Wheat c/bu 426 -9% 431 -17% 435 -20% 439 -19% 439 -19%

KCBT Wheat c/bu 438 -9% 446 -16% 450 -18% 454 -17% 454 -17%

CBOT Soybean c/bu 955 -7% 975 -2% 950 -2% 950 0% 950 0%

CBOT Soybean Meal $/t 307 -8% 312 -4% 299 -8% 304 -7% 304 -7%

ICE Raw Sugar c/lb 21 0% 20 5% 19 11% 19 8% 19 8%

Euronext White Sugar $/t 541 1% 523 2% 517 -1% 511 -2% 511 -2%

Coffee (Arabica-NY) c/lb 171 11% 165 1% 170 -1% 170 -3% 170 -3%

ICE Cotton c/lb 70 -7% 72 -1% 74 2% 74 3% 74 3%

LIVESTOCK (CME)

CME Feeder Cattle c/lb 130 7% 148 25% 156 30% 139 16% 139 16%

CME Live Cattle c/lb 112 7% 123 22% 129 27% 119 17% 119 17%

CME Lean Hogs c/lb 61.6 -13% 65.1 -12% 68.3 -12% 62.9 -19% 62.9 -19%

PRECIOUS METALS

Gold $/oz 1 150 -6% 1 125 -10% 1 100 -13% 1 075 -17% 1 050 -20%

Silver $/oz 16 -9% 17 -5% 16 -12% 16 -14% 16 -16%

Palladium $/oz 750 0% 775 2% 800 4% 850 8% 900 12%

Platinum $/oz 1 040 3% 1 050 2% 1 200 15% 1 250 16% 1 300 18%

BASE METALS (LME)

LME Aluminium $/t 1 725 -6% 1 750 -6% 1 800 -5% 1 850 -4% 1 900 -3%

LME Copper $/t 5 625 -3% 5 750 -1% 6 000 4% 6 500 13% 7 000 22%

LME Zinc $/t 2 650 -5% 2 800 2% 2 700 5% 2 600 9% 2 500 12%

LME Lead $/t 2 225 -4% 2 300 -1% 2 400 5% 2 400 7% 2 300 2%

LME Nickel $/t 12 000 17% 13 000 24% 14 000 32% 15 000 39% 15 000 37%

LME Tin $/t 22 000 11% 24 000 23% 25 000 29% 24 000 24% 24 000 24%

Michael Haigh – MD / Head of Commodity Research 9

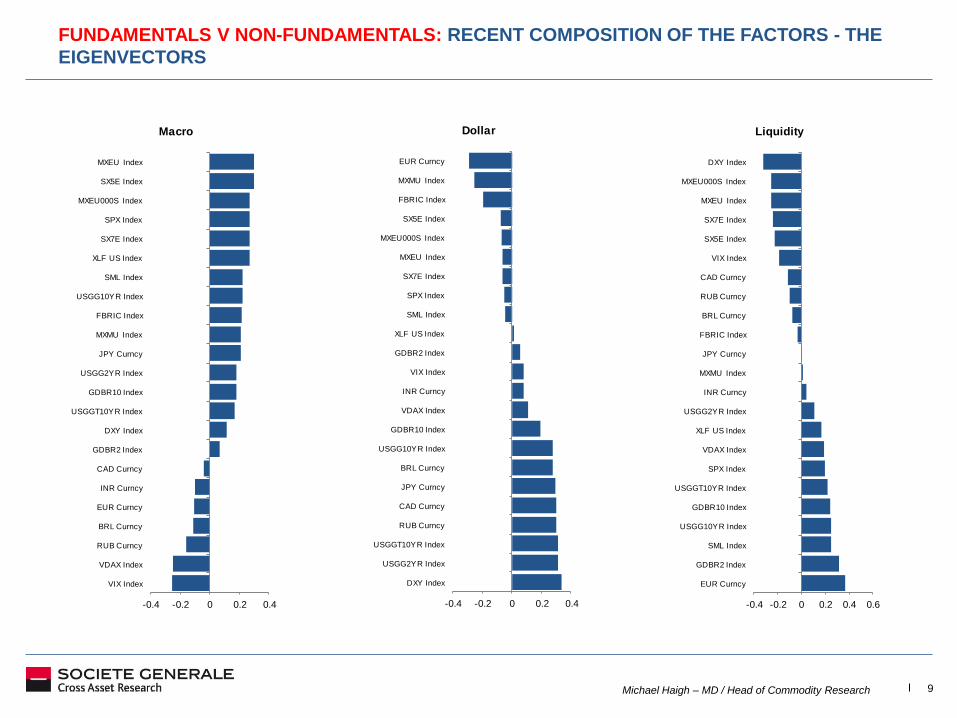

FUNDAMENTALS V NON-FUNDAMENTALS: RECENT COMPOSITION OF THE FACTORS - THE

EIGENVECTORS

-0.4 -0.2 0 0.2 0.4

VIX Index

VDAX Index

RUB Curncy

BRL Curncy

EUR Curncy

INR Curncy

CAD Curncy

GDBR2 Index

DXY Index

USGGT10YR Index

GDBR10 Index

USGG2YR Index

JPY Curncy

MXMU Index

FBRIC Index

USGG10YR Index

SML Index

XLF US Index

SX7E Index

SPX Index

MXEU000S Index

SX5E Index

MXEU Index

Macro

-0.4 -0.2 0 0.2 0.4

DXY Index

USGG2YR Index

USGGT10YR Index

RUB Curncy

CAD Curncy

JPY Curncy

BRL Curncy

USGG10YR Index

GDBR10 Index

VDAX Index

INR Curncy

VIX Index

GDBR2 Index

XLF US Index

SML Index

SPX Index

SX7E Index

MXEU Index

MXEU000S Index

SX5E Index

FBRIC Index

MXMU Index

EUR Curncy

Dollar

-0.4 -0.2 0 0.2 0.4 0.6

EUR Curncy

GDBR2 Index

SML Index

USGG10YR Index

GDBR10 Index

USGGT10YR Index

SPX Index

VDAX Index

XLF US Index

USGG2YR Index

INR Curncy

MXMU Index

JPY Curncy

FBRIC Index

BRL Curncy

RUB Curncy

CAD Curncy

VIX Index

SX5E Index

SX7E Index

MXEU Index

MXEU000S Index

DXY Index

Liquidity

Michael Haigh – MD / Head of Commodity Research 10

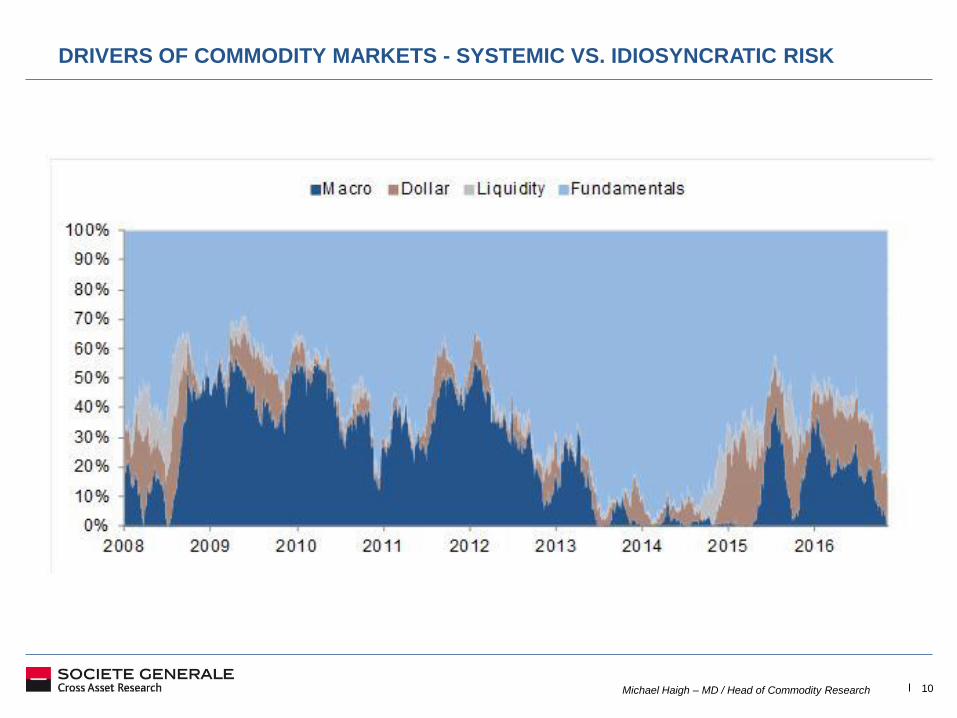

DRIVERS OF COMMODITY MARKETS - SYSTEMIC VS. IDIOSYNCRATIC RISK

Michael Haigh – MD / Head of Commodity Research 11

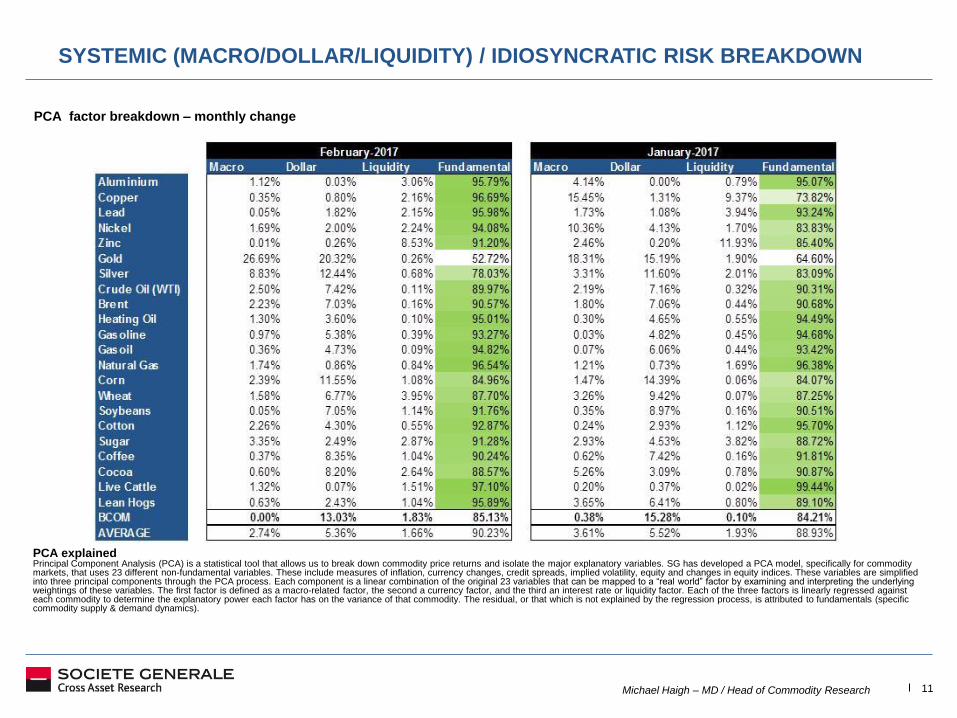

SYSTEMIC (MACRO/DOLLAR/LIQUIDITY) / IDIOSYNCRATIC RISK BREAKDOWN

PCA factor breakdown – monthly change

PCA explained Principal Component Analysis (PCA) is a statistical tool that allows us to break down commodity price returns and isolate the major explanatory variables. SG has developed a PCA model, specifically for commodity markets, that uses 23 different non-fundamental variables. These include measures of inflation, currency changes, credit spreads, implied volatility, equity and changes in equity indices. These variables are simplified into three principal components through the PCA process. Each component is a linear combination of the original 23 variables that can be mapped to a “real world” factor by examining and interpreting the underlying weightings of these variables. The first factor is defined as a macro-related factor, the second a currency factor, and the third an interest rate or liquidity factor. Each of the three factors is linearly regressed against each commodity to determine the explanatory power each factor has on the variance of that commodity. The residual, or that which is not explained by the regression process, is attributed to fundamentals (specific commodity supply & demand dynamics).

Michael Haigh – MD / Head of Commodity Research 12

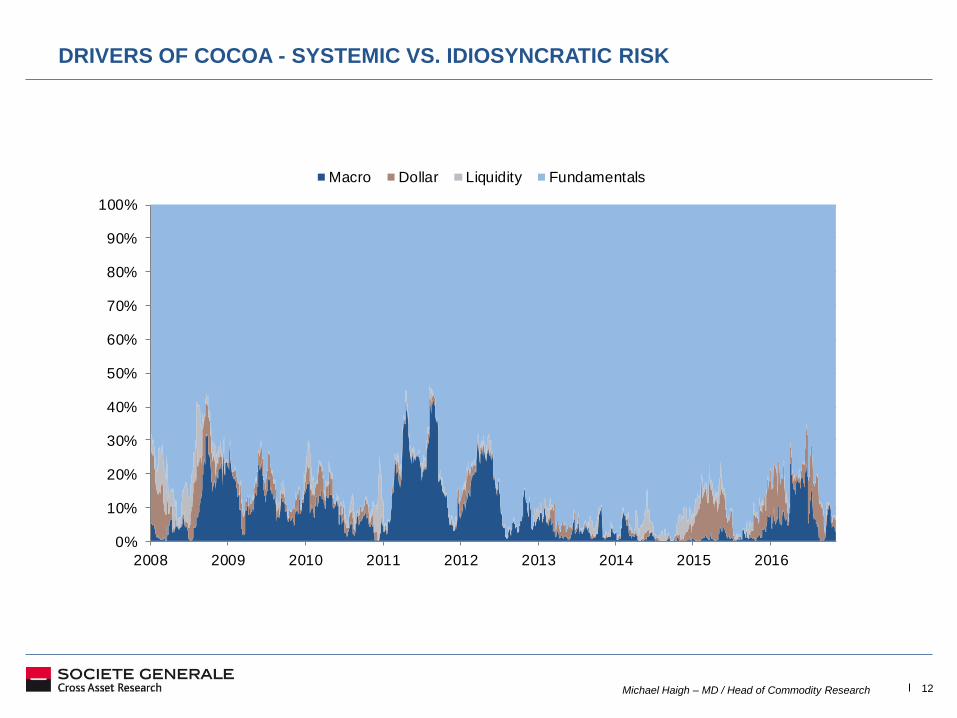

DRIVERS OF COCOA - SYSTEMIC VS. IDIOSYNCRATIC RISK

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012 2013 2014 2015 2016

Macro Dollar Liquidity Fundamentals

Michael Haigh – MD / Head of Commodity Research 13

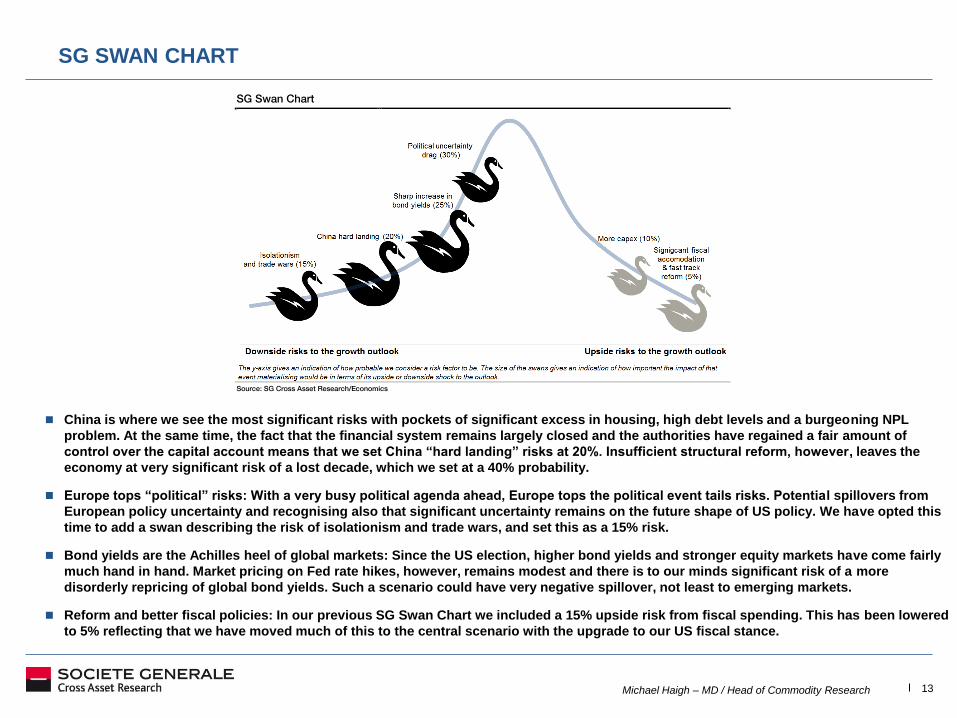

SG SWAN CHART

SG Swan Chart

Source: SG Cross Asset Research/Economics

China is where we see the most significant risks with pockets of significant excess in housing, high debt levels and a burgeoning NPL

problem. At the same time, the fact that the financial system remains largely closed and the authorities have regained a fair amount of

control over the capital account means that we set China “hard landing” risks at 20%. Insufficient structural reform, however, leaves the

economy at very significant risk of a lost decade, which we set at a 40% probability.

Europe tops “political” risks: With a very busy political agenda ahead, Europe tops the political event tails risks. Potential spillovers from

European policy uncertainty and recognising also that significant uncertainty remains on the future shape of US policy. We have opted this

time to add a swan describing the risk of isolationism and trade wars, and set this as a 15% risk.

Bond yields are the Achilles heel of global markets: Since the US election, higher bond yields and stronger equity markets have come fairly

much hand in hand. Market pricing on Fed rate hikes, however, remains modest and there is to our minds significant risk of a more

disorderly repricing of global bond yields. Such a scenario could have very negative spillover, not least to emerging markets.

Reform and better fiscal policies: In our previous SG Swan Chart we included a 15% upside risk from fiscal spending. This has been lowered

to 5% reflecting that we have moved much of this to the central scenario with the upgrade to our US fiscal stance.

Michael Haigh – MD / Head of Commodity Research 14

CL

NG

HO

XB

C

W

KW

S

GC

SI

HG

SB

CT

KC

CC

LC

LH

CL

NG

HO

XB

C

W

KW

S

GC

SI

HG

SB

CT

KC

CC

LC

LH

0%

25%

50%

75%

100%

-100% -75% -50% -25% 0% 25% 50% 75% 100%

Price %

of

Price R

ange

Short MM % Range Long MM % Range

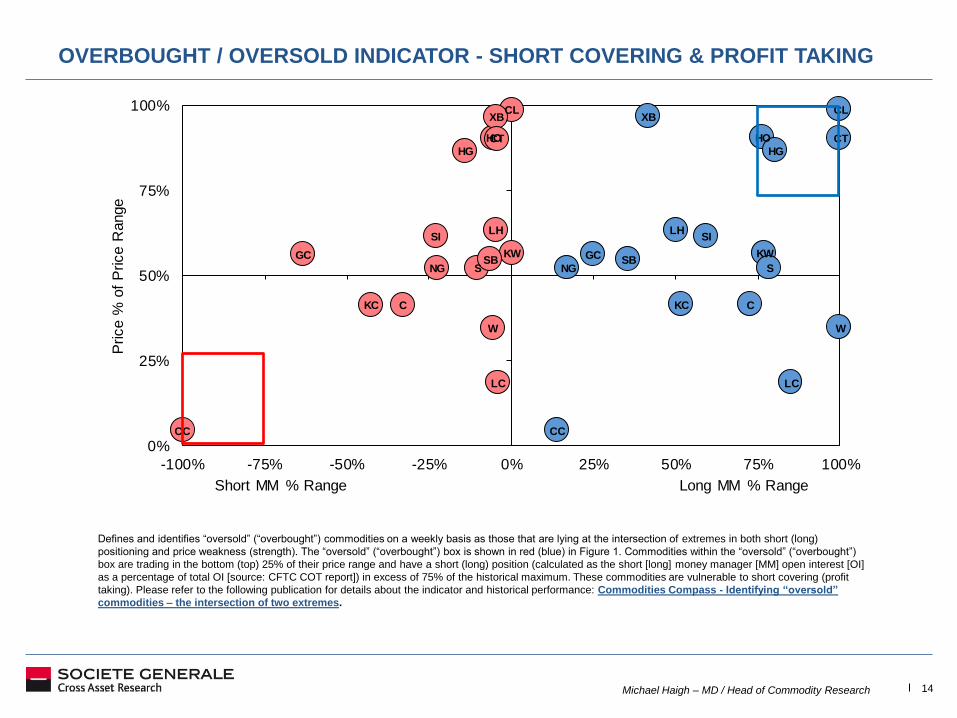

OVERBOUGHT / OVERSOLD INDICATOR - SHORT COVERING & PROFIT TAKING

Defines and identifies “oversold” (“overbought”) commodities on a weekly basis as those that are lying at the intersection of extremes in both short (long)

positioning and price weakness (strength). The “oversold” (“overbought”) box is shown in red (blue) in Figure 1. Commodities within the “oversold” (“overbought”)

box are trading in the bottom (top) 25% of their price range and have a short (long) position (calculated as the short [long] money manager [MM] open interest [OI]

as a percentage of total OI [source: CFTC COT report]) in excess of 75% of the historical maximum. These commodities are vulnerable to short covering (profit

taking). Please refer to the following publication for details about the indicator and historical performance: Commodities Compass - Identifying “oversold”

commodities – the intersection of two extremes.

Michael Haigh – MD / Head of Commodity Research 15

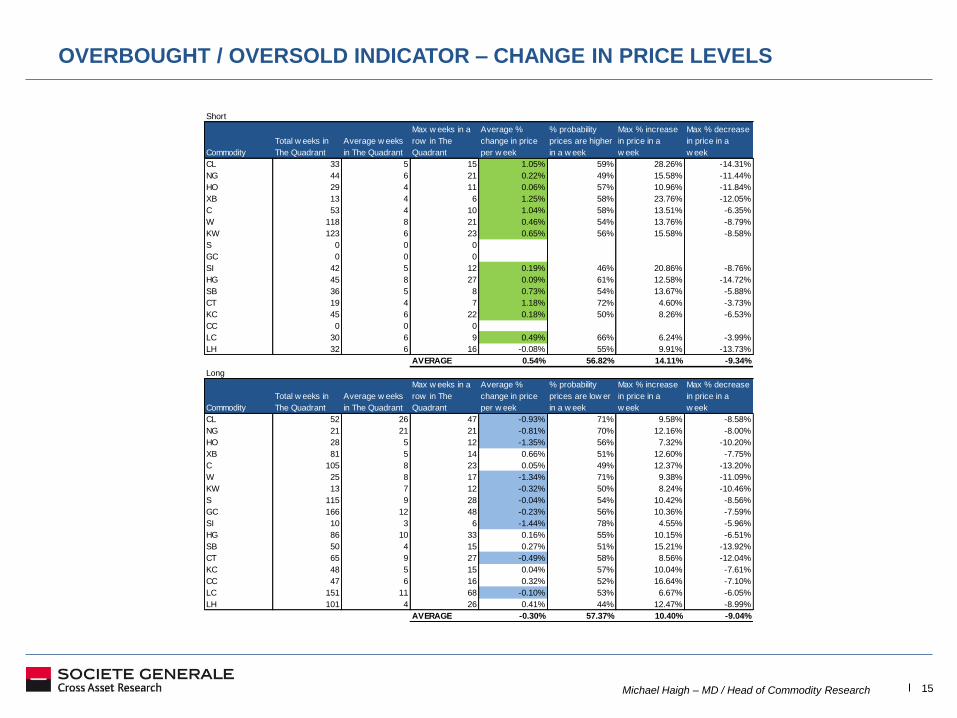

OVERBOUGHT / OVERSOLD INDICATOR – CHANGE IN PRICE LEVELS

Short

Commodity

Total w eeks in

The Quadrant

Average w eeks

in The Quadrant

Max w eeks in a

row in The

Quadrant

Average %

change in price

per w eek

% probability

prices are higher

in a w eek

Max % increase

in price in a

w eek

Max % decrease

in price in a

w eek

CL 33 5 15 1.05% 59% 28.26% -14.31%

NG 44 6 21 0.22% 49% 15.58% -11.44%

HO 29 4 11 0.06% 57% 10.96% -11.84%

XB 13 4 6 1.25% 58% 23.76% -12.05%

C 53 4 10 1.04% 58% 13.51% -6.35%

W 118 8 21 0.46% 54% 13.76% -8.79%

KW 123 6 23 0.65% 56% 15.58% -8.58%

S 0 0 0

GC 0 0 0

SI 42 5 12 0.19% 46% 20.86% -8.76%

HG 45 8 27 0.09% 61% 12.58% -14.72%

SB 36 5 8 0.73% 54% 13.67% -5.88%

CT 19 4 7 1.18% 72% 4.60% -3.73%

KC 45 6 22 0.18% 50% 8.26% -6.53%

CC 0 0 0

LC 30 6 9 0.49% 66% 6.24% -3.99%

LH 32 6 16 -0.08% 55% 9.91% -13.73%

AVERAGE 0.54% 56.82% 14.11% -9.34%

Long

Commodity

Total w eeks in

The Quadrant

Average w eeks

in The Quadrant

Max w eeks in a

row in The

Quadrant

Average %

change in price

per w eek

% probability

prices are low er

in a w eek

Max % increase

in price in a

w eek

Max % decrease

in price in a

w eek

CL 52 26 47 -0.93% 71% 9.58% -8.58%

NG 21 21 21 -0.81% 70% 12.16% -8.00%

HO 28 5 12 -1.35% 56% 7.32% -10.20%

XB 81 5 14 0.66% 51% 12.60% -7.75%

C 105 8 23 0.05% 49% 12.37% -13.20%

W 25 8 17 -1.34% 71% 9.38% -11.09%

KW 13 7 12 -0.32% 50% 8.24% -10.46%

S 115 9 28 -0.04% 54% 10.42% -8.56%

GC 166 12 48 -0.23% 56% 10.36% -7.59%

SI 10 3 6 -1.44% 78% 4.55% -5.96%

HG 86 10 33 0.16% 55% 10.15% -6.51%

SB 50 4 15 0.27% 51% 15.21% -13.92%

CT 65 9 27 -0.49% 58% 8.56% -12.04%

KC 48 5 15 0.04% 57% 10.04% -7.61%

CC 47 6 16 0.32% 52% 16.64% -7.10%

LC 151 11 68 -0.10% 53% 6.67% -6.05%

LH 101 4 26 0.41% 44% 12.47% -8.99%

AVERAGE -0.30% 57.37% 10.40% -9.04%

Michael Haigh – MD / Head of Commodity Research 16

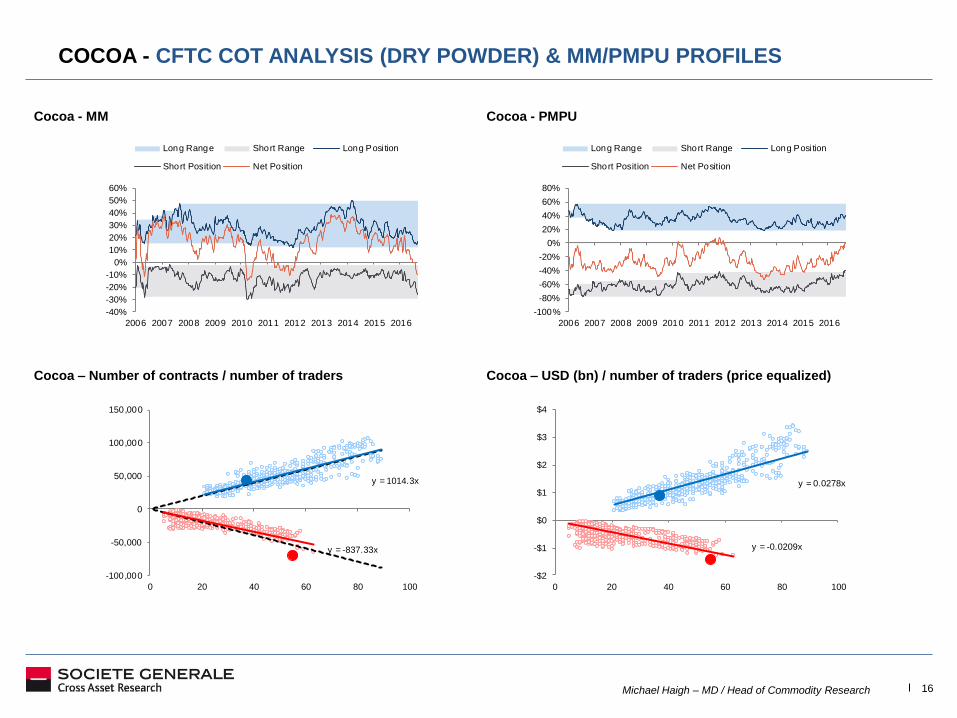

COCOA - CFTC COT ANALYSIS (DRY POWDER) & MM/PMPU PROFILES

Cocoa - MM Cocoa - PMPU

Cocoa – Number of contracts / number of traders Cocoa – USD (bn) / number of traders (price equalized)

y = 1014.3x

y = -837.33x

-100,000

-50,000

0

50,000

100,000

150,000

0 20 40 60 80 100

y = 0.0278x

y = -0.0209x

-$2

-$1

$0

$1

$2

$3

$4

0 20 40 60 80 100

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Long Range Short Range Long Posi tion

Short Position Net Position

-100%

-80%

-60%

-40%

-20%

0%

20%

40%

60%

80%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Long Range Short Range Long Posi tion

Short Position Net Position

Michael Haigh – MD / Head of Commodity Research 17

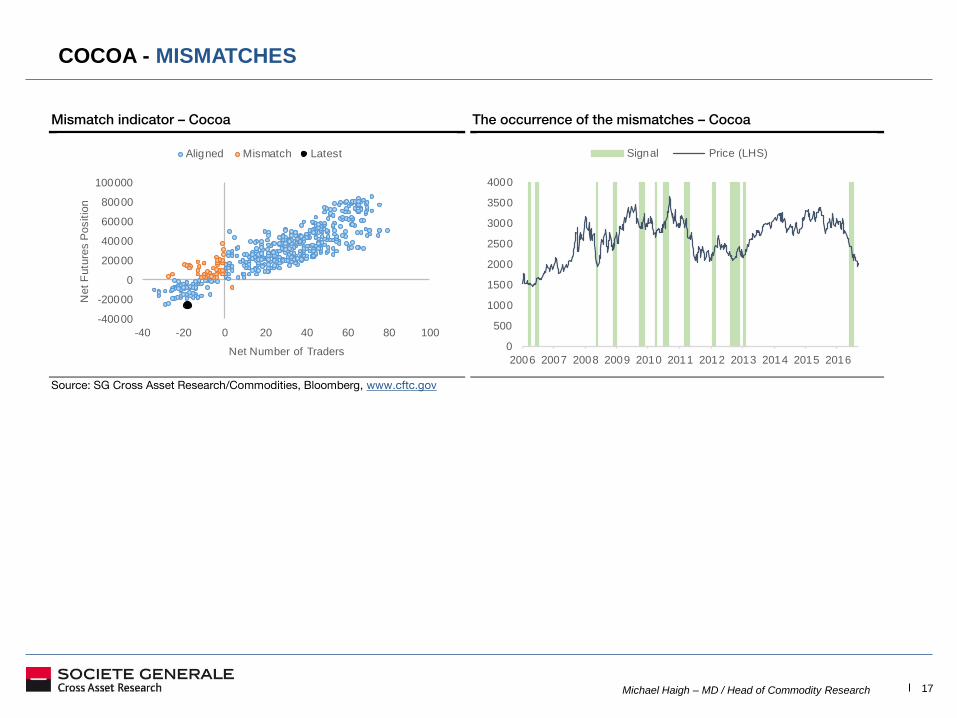

COCOA - MISMATCHES

Mismatch indicator – Cocoa The occurrence of the mismatches – Cocoa

Source: SG Cross Asset Research/Commodities, Bloomberg, www.cftc.gov

-40000

-20000

0

20000

40000

60000

80000

100000

-40 -20 0 20 40 60 80 100

Net

Futu

res

Pos

itio

n

Net Number of Traders

Aligned Mismatch Latest

0

500

1000

1500

2000

2500

3000

3500

4000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Signal Price (LHS)

Michael Haigh – MD / Head of Commodity Research 18

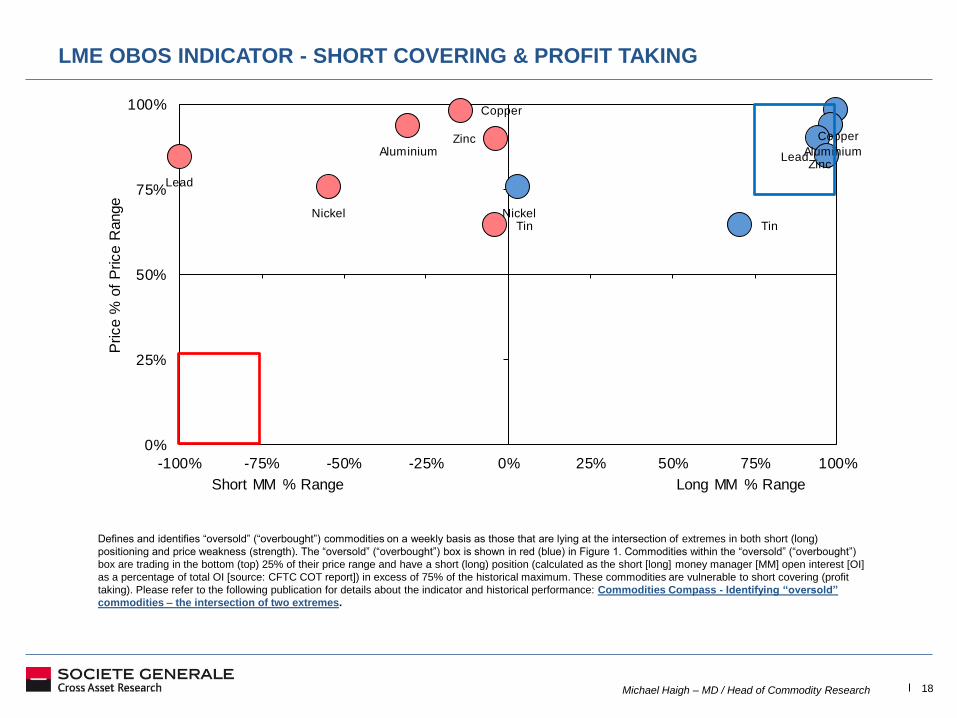

Copper

AluminiumZinc

Lead

NickelTin

Copper

AluminiumZinc

Lead

NickelTin

0%

25%

50%

75%

100%

-100% -75% -50% -25% 0% 25% 50% 75% 100%

Price %

of

Price R

ange

Short MM % Range Long MM % Range

LME OBOS INDICATOR - SHORT COVERING & PROFIT TAKING

Defines and identifies “oversold” (“overbought”) commodities on a weekly basis as those that are lying at the intersection of extremes in both short (long)

positioning and price weakness (strength). The “oversold” (“overbought”) box is shown in red (blue) in Figure 1. Commodities within the “oversold” (“overbought”)

box are trading in the bottom (top) 25% of their price range and have a short (long) position (calculated as the short [long] money manager [MM] open interest [OI]

as a percentage of total OI [source: CFTC COT report]) in excess of 75% of the historical maximum. These commodities are vulnerable to short covering (profit

taking). Please refer to the following publication for details about the indicator and historical performance: Commodities Compass - Identifying “oversold”

commodities – the intersection of two extremes.

Michael Haigh – MD / Head of Commodity Research 19

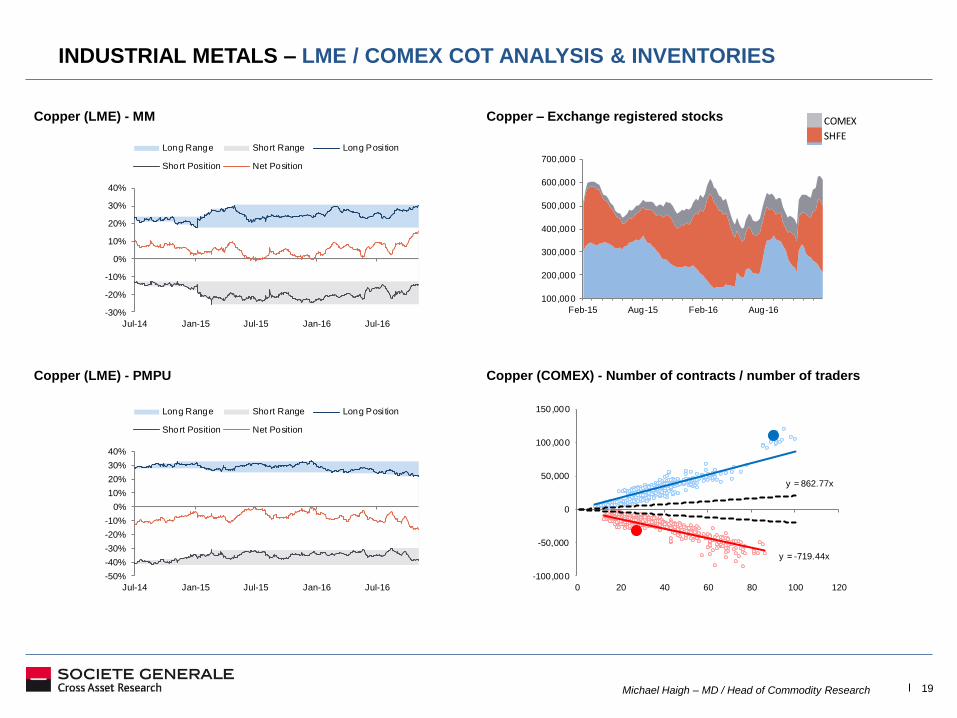

INDUSTRIAL METALS – LME / COMEX COT ANALYSIS & INVENTORIES

Copper (LME) - MM Copper – Exchange registered stocks

Copper (LME) - PMPU Copper (COMEX) - Number of contracts / number of traders

-30%

-20%

-10%

0%

10%

20%

30%

40%

Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

Long Range Short Range Long Posi tion

Short Position Net Position

y = 862.77x

y = -719.44x

-100,000

-50,000

0

50,000

100,000

150,000

0 20 40 60 80 100 120

COMEX

SHFE

LME

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

Jul-14 Jan-15 Jul-15 Jan-16 Jul-16

Long Range Short Range Long Posi tion

Short Position Net Position

100,000

200,000

300,000

400,000

500,000

600,000

700,000

Feb-15 Aug-15 Feb-16 Aug-16

Michael Haigh – MD / Head of Commodity Research 20

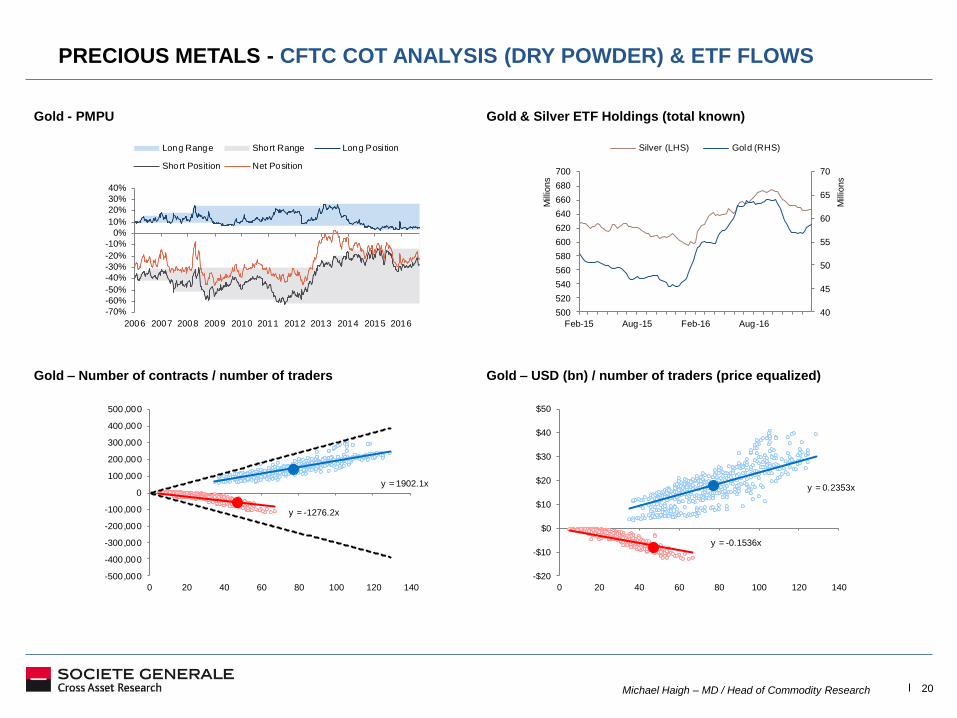

PRECIOUS METALS - CFTC COT ANALYSIS (DRY POWDER) & ETF FLOWS

Gold - PMPU Gold & Silver ETF Holdings (total known)

Gold – Number of contracts / number of traders Gold – USD (bn) / number of traders (price equalized)

y = 1902.1x

y = -1276.2x

-500,000

-400,000

-300,000

-200,000

-100,000

0

100,000

200,000

300,000

400,000

500,000

0 20 40 60 80 100 120 140

y = 0.2353x

y = -0.1536x

-$20

-$10

$0

$10

$20

$30

$40

$50

0 20 40 60 80 100 120 140

-70%

-60%

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

40%

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Long Range Short Range Long Posi tion

Short Position Net Position

40

45

50

55

60

65

70

500

520

540

560

580

600

620

640

660

680

700

Feb-15 Aug-15 Feb-16 Aug-16

Mill

ions

Mill

ions

Silver (LHS) Gold (RHS)

Michael Haigh – MD / Head of Commodity Research 21

COMMODITY SENTIMENT & BEHAVIOURAL ANALYSIS

-100%

-75%

-50%

-25%

0%

25%

50%

75%

100%

2009 2010 2010 2011 2011 2012 2012 2013 2013 2014 2014 2015 2015 2016 2016

Commodity Sentiment - 4 week MA

57

87 84

44

63

25

60

84 80

5465

38

7762 58

46

90 94

6454

9

37

-68

-26

-53-44

-15-29 -26 -26 -31 -25

-53

-16

-47

-17 -13 -10

-27 -23-33

-10 -6

-55-80

-60

-40

-20

0

20

40

60

80

100

120

CB

OT

Wh

ea

t

CB

OT

Soybean

CB

OT

Corn

CB

OT

Soy. oil

CB

OT

Soy. m

eal

CM

E F

. c

attle

CM

E L

ea

n h

og

s

CM

E L

ive

ca

ttle

NY

M C

rud

e o

il

NY

M G

aso

line

NY

M N

G

NY

M H

eati

ng

oil

CM

X G

old

CM

X S

ilve

r

CM

X P

latin

um

CM

X P

alla

diu

m

CM

X C

op

pe

r

ICE

Co

tto

n

ICE

Coffee

ICE

Su

gar

ICE

FC

OJ

ICE

Coc

oa

-60

-10

40

90

140

-200,000

-100,000

0

100,000

200,000

300,000

400,000

500,000

600,000

CB

OT

Wh

eat

CB

OT

So

yb

ea

n

CB

OT

Co

rn

CB

OT

Soy. oil

CB

OT

So

y. m

ea

l

CM

E F

. cattle

CM

E L

ean

hog

s

CM

E L

ive

ca

ttle

NY

M C

rud

e o

il

NY

M G

aso

line

NY

M N

G

NY

M H

eati

ng

oil

CM

X G

old

CM

X S

ilve

r

CM

X P

latin

um

CM

X P

alla

diu

m

CM

X C

opper

ICE

Cotton

ICE

Co

ffe

e

ICE

Su

gar

ICE

FC

OJ

ICE

Co

co

a

-4

3

-20

-15

-10

-5

0

5

10

15

20

CB

OT

Wh

eat

CB

OT

So

yb

ea

n

CB

OT

Co

rn

CB

OT

Soy. oil

CB

OT

Soy. m

eal

CM

E F

. c

attle

CM

E L

ea

n h

og

s

CM

E L

ive c

attle

NY

M C

rud

e o

il

NY

M G

aso

line

NY

M N

G

NY

M H

eati

ng

oil

CM

X G

old

CM

X S

ilve

r

CM

X P

latin

um

CM

X P

alla

diu

m

CM

X C

op

pe

r

ICE

Co

tto

n

ICE

Coffee

ICE

Su

gar

ICE

FC

OJ

ICE

Co

co

a

Mismatch – Potential change in direction? Traders Position vs. Actual Position (MM)

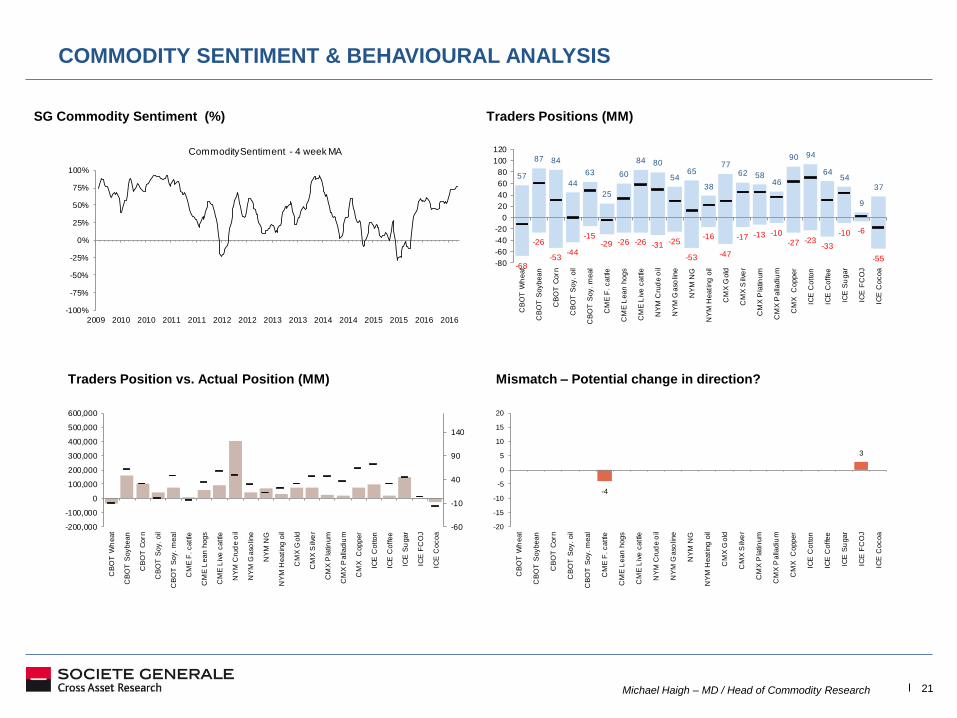

SG Commodity Sentiment (%) Traders Positions (MM)

Michael Haigh – MD / Head of Commodity Research 22

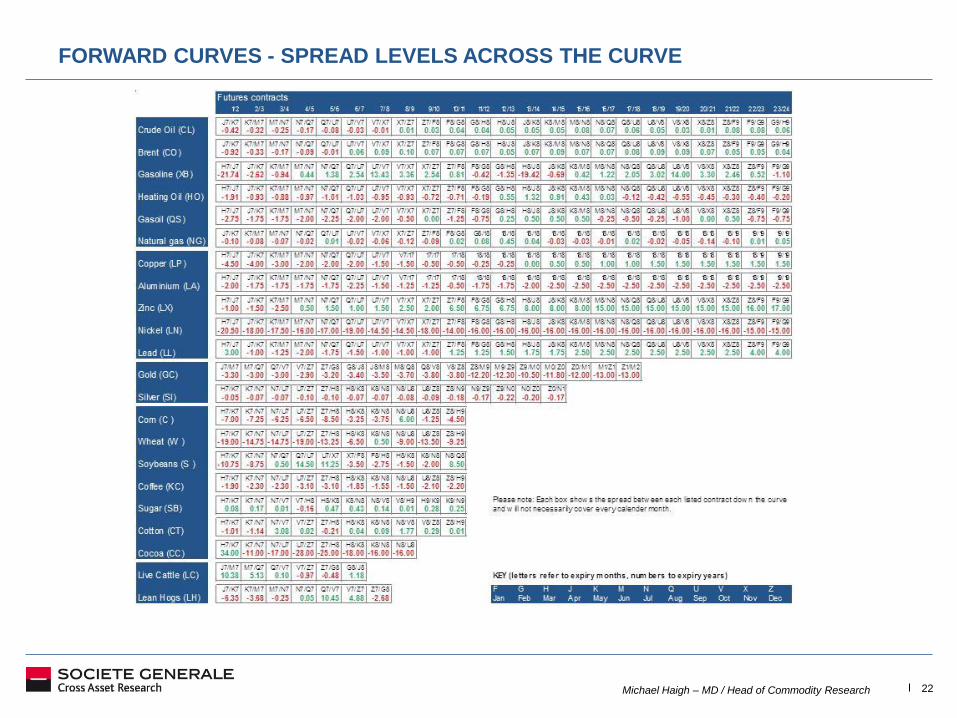

FORWARD CURVES - SPREAD LEVELS ACROSS THE CURVE

Michael Haigh – MD / Head of Commodity Research 23

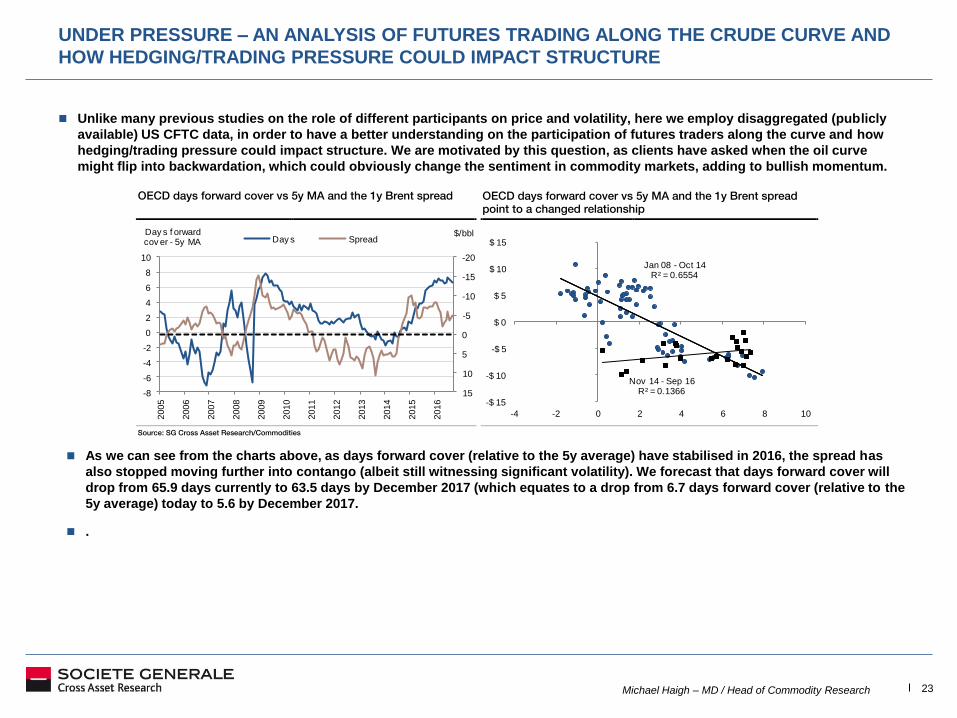

UNDER PRESSURE – AN ANALYSIS OF FUTURES TRADING ALONG THE CRUDE CURVE AND

HOW HEDGING/TRADING PRESSURE COULD IMPACT STRUCTURE

Unlike many previous studies on the role of different participants on price and volatility, here we employ disaggregated (publicly

available) US CFTC data, in order to have a better understanding on the participation of futures traders along the curve and how

hedging/trading pressure could impact structure. We are motivated by this question, as clients have asked when the oil curve

might flip into backwardation, which could obviously change the sentiment in commodity markets, adding to bullish momentum.

OECD days forward cover vs 5y MA and the 1y Brent spread OECD days forward cover vs 5y MA and the 1y Brent spread

point to a changed relationship

Source: SG Cross Asset Research/Commodities

-20

-15

-10

-5

0

5

10

15-8

-6

-4

-2

0

2

4

6

8

10

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

$/bblDay s f orward cov er - 5y MA Day s Spread

Jan 08 - Oct 14R² = 0.6554

Nov 14 - Sep 16R² = 0.1366

-$ 15

-$ 10

-$ 5

$ 0

$ 5

$ 10

$ 15

-4 -2 0 2 4 6 8 10

As we can see from the charts above, as days forward cover (relative to the 5y average) have stabilised in 2016, the spread has

also stopped moving further into contango (albeit still witnessing significant volatility). We forecast that days forward cover will

drop from 65.9 days currently to 63.5 days by December 2017 (which equates to a drop from 6.7 days forward cover (relative to the

5y average) today to 5.6 by December 2017.

.

Michael Haigh – MD / Head of Commodity Research 24

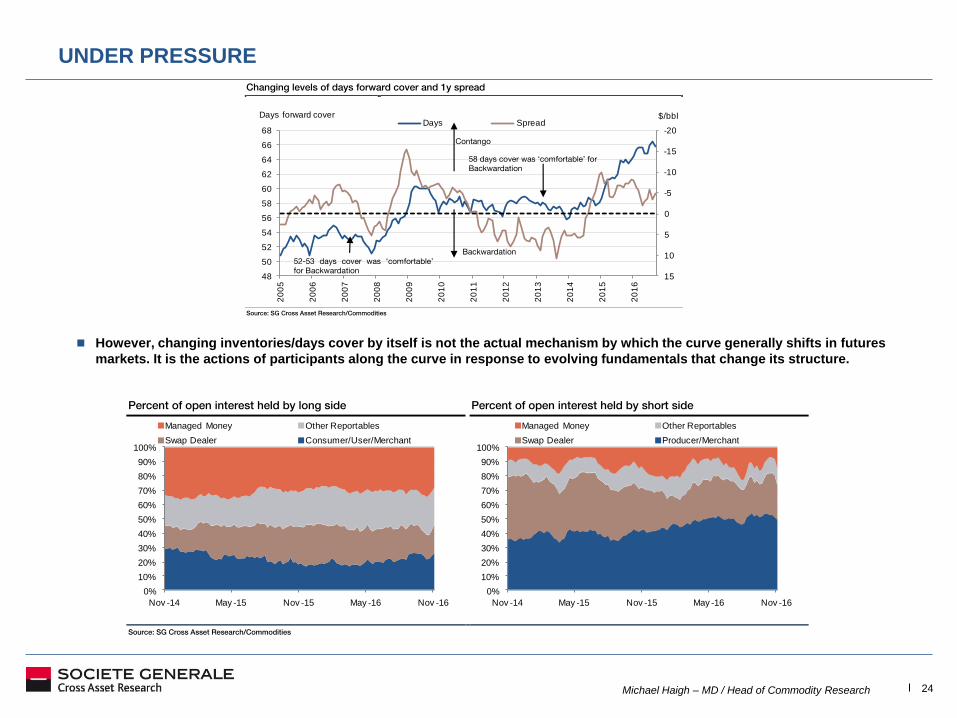

UNDER PRESSURE

However, changing inventories/days cover by itself is not the actual mechanism by which the curve generally shifts in futures

markets. It is the actions of participants along the curve in response to evolving fundamentals that change its structure.

Changing levels of days forward cover and 1y spread

Source: SG Cross Asset Research/Commodities

-20

-15

-10

-5

0

5

10

1548

50

52

54

56

58

60

62

64

66

68

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

$/bblDays forward cover Days Spread

Contango

Backwardation

52-53 days cover was ‘comfortable’

for Backwardation

58 days cover was ‘comfortable’ for

Backwardation

Percent of open interest held by long side Percent of open interest held by short side

Source: SG Cross Asset Research/Commodities

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Nov -14 May -15 Nov -15 May -16 Nov -16

Managed Money Other Reportables

Swap Dealer Consumer/User/Merchant

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Nov -14 May -15 Nov -15 May -16 Nov -16

Managed Money Other Reportables

Swap Dealer Producer/Merchant

Michael Haigh – MD / Head of Commodity Research 25

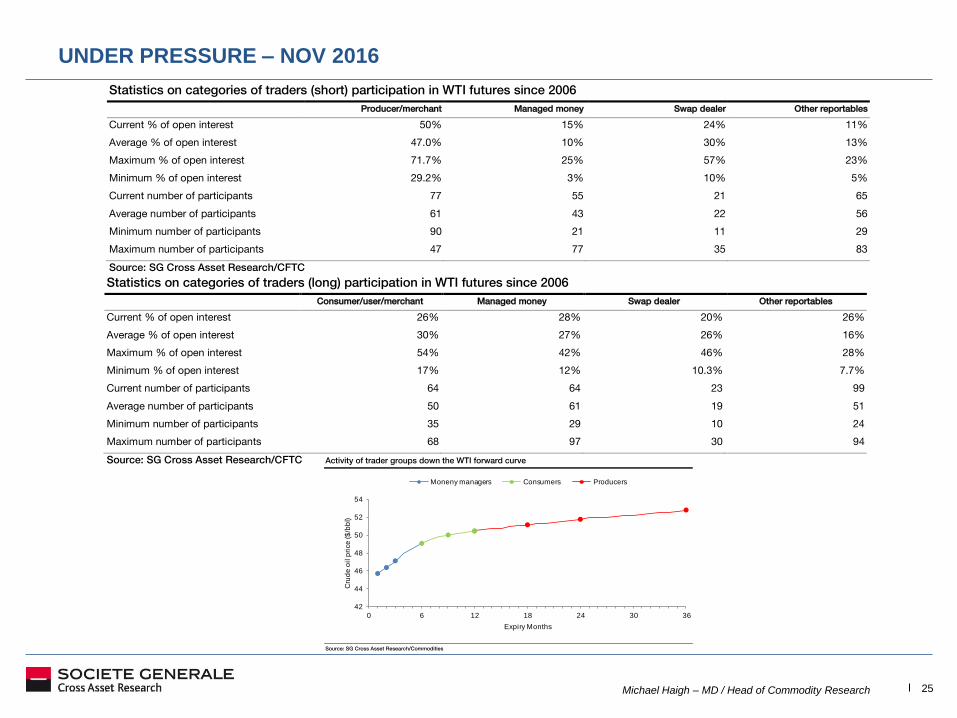

UNDER PRESSURE – NOV 2016

Statistics on categories of traders (short) participation in WTI futures since 2006

Producer/merchant Managed money Swap dealer Other reportables

Current % of open interest 50% 15% 24% 11%

Average % of open interest 47.0% 10% 30% 13%

Maximum % of open interest 71.7% 25% 57% 23%

Minimum % of open interest 29.2% 3% 10% 5%

Current number of participants 77 55 21 65

Average number of participants 61 43 22 56

Minimum number of participants 90 21 11 29

Maximum number of participants 47 77 35 83

Source: SG Cross Asset Research/CFTC

Statistics on categories of traders (long) participation in WTI futures since 2006

Consumer/user/merchant Managed money Swap dealer Other reportables

Current % of open interest 26% 28% 20% 26%

Average % of open interest 30% 27% 26% 16%

Maximum % of open interest 54% 42% 46% 28%

Minimum % of open interest 17% 12% 10.3% 7.7%

Current number of participants 64 64 23 99

Average number of participants 50 61 19 51

Minimum number of participants 35 29 10 24

Maximum number of participants 68 97 30 94

Source: SG Cross Asset Research/CFTC Activity of trader groups down the WTI forward curve

Source: SG Cross Asset Research/Commodities

42

44

46

48

50

52

54

0 6 12 18 24 30 36

Cru

de

oil

pri

ce

($

/bb

l)

Expiry Months

Moneny managers Consumers Producers

Michael Haigh – MD / Head of Commodity Research 26

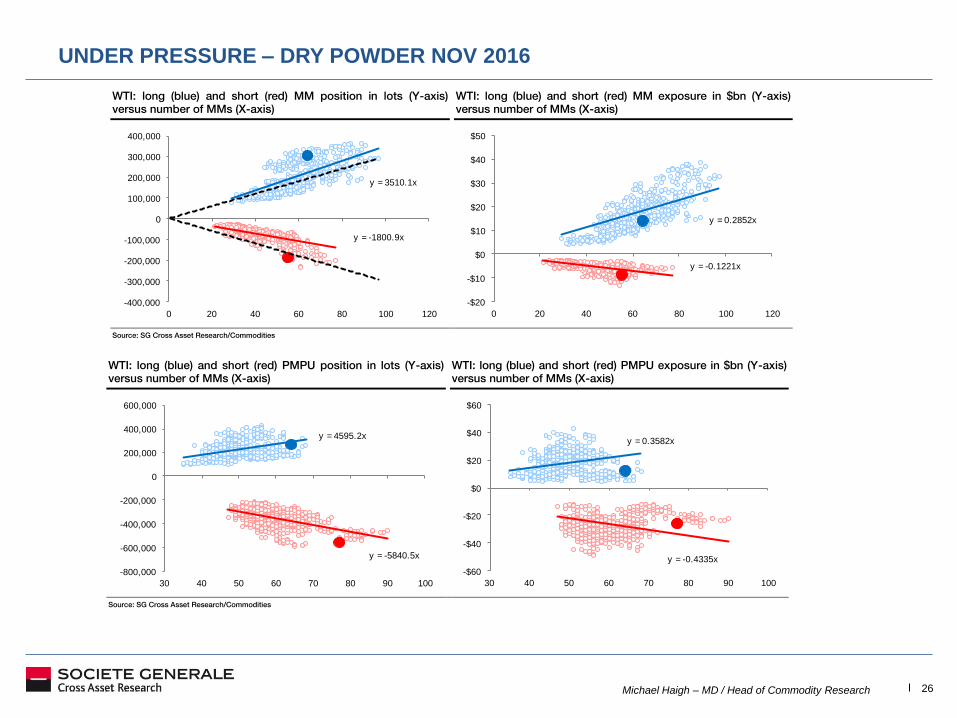

UNDER PRESSURE – DRY POWDER NOV 2016

WTI: long (blue) and short (red) MM position in lots (Y-axis)

versus number of MMs (X-axis)

WTI: long (blue) and short (red) MM exposure in $bn (Y-axis)

versus number of MMs (X-axis)

Source: SG Cross Asset Research/Commodities

y = 3510.1x

y = -1800.9x

-400,000

-300,000

-200,000

-100,000

0

100,000

200,000

300,000

400,000

0 20 40 60 80 100 120

y = 0.2852x

y = -0.1221x

-$20

-$10

$0

$10

$20

$30

$40

$50

0 20 40 60 80 100 120

WTI: long (blue) and short (red) PMPU position in lots (Y-axis)

versus number of MMs (X-axis)

WTI: long (blue) and short (red) PMPU exposure in $bn (Y-axis)

versus number of MMs (X-axis)

Source: SG Cross Asset Research/Commodities

y = 4595.2x

y = -5840.5x

-800,000

-600,000

-400,000

-200,000

0

200,000

400,000

600,000

30 40 50 60 70 80 90 100

y = 0.3582x

y = -0.4335x

-$60

-$40

-$20

$0

$20

$40

$60

30 40 50 60 70 80 90 100

Michael Haigh – MD / Head of Commodity Research 27

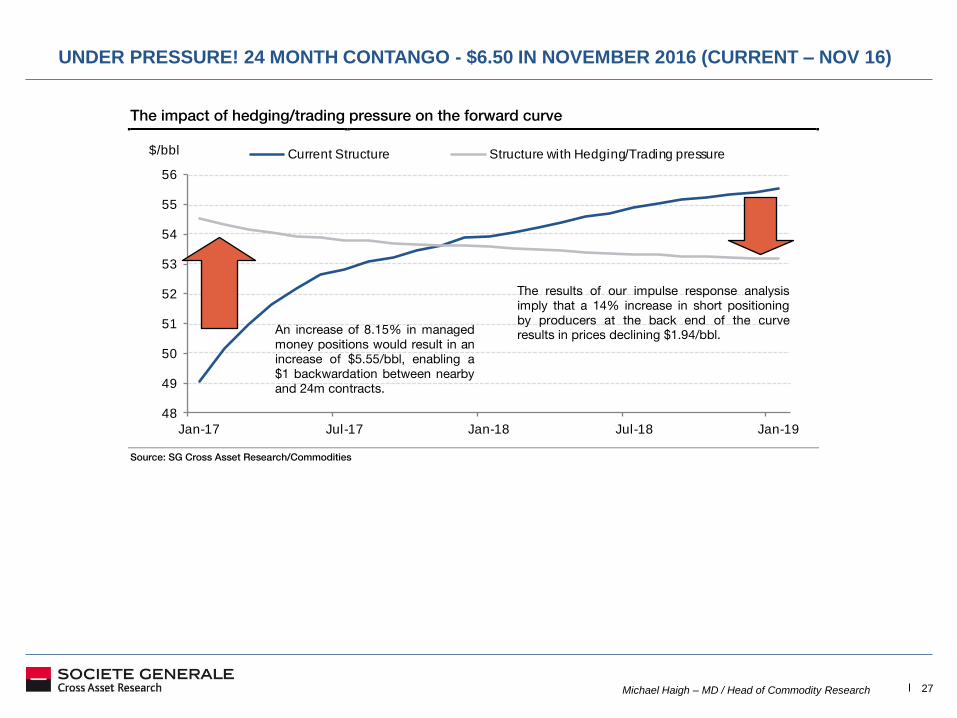

UNDER PRESSURE! 24 MONTH CONTANGO - $6.50 IN NOVEMBER 2016 (CURRENT – NOV 16)

The impact of hedging/trading pressure on the forward curve

Source: SG Cross Asset Research/Commodities

48

49

50

51

52

53

54

55

56

Jan-17 Jul-17 Jan-18 Jul-18 Jan-19

$/bbl Current Structure Structure with Hedging/Trading pressure

The results of our impulse response analysis

imply that a 14% increase in short positioning

by producers at the back end of the curve

results in prices declining $1.94/bbl. An increase of 8.15% in managed

money positions would result in an

increase of $5.55/bbl, enabling a

$1 backwardation between nearby

and 24m contracts.

Michael Haigh – MD / Head of Commodity Research 28

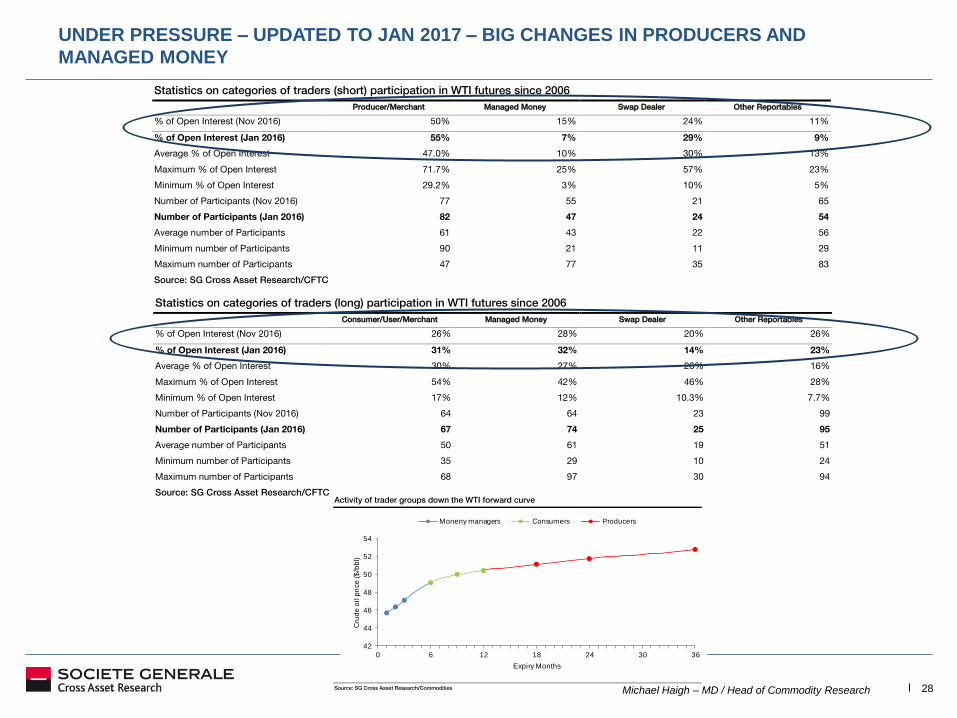

UNDER PRESSURE – UPDATED TO JAN 2017 – BIG CHANGES IN PRODUCERS AND

MANAGED MONEY

Activity of trader groups down the WTI forward curve

Source: SG Cross Asset Research/Commodities

42

44

46

48

50

52

54

0 6 12 18 24 30 36

Cru

de

oil

pri

ce

($

/bb

l)

Expiry Months

Moneny managers Consumers Producers

Statistics on categories of traders (long) participation in WTI futures since 2006

Consumer/User/Merchant Managed Money Swap Dealer Other Reportables

% of Open Interest (Nov 2016) 26% 28% 20% 26%

% of Open Interest (Jan 2016) 31% 32% 14% 23%

Average % of Open Interest 30% 27% 26% 16%

Maximum % of Open Interest 54% 42% 46% 28%

Minimum % of Open Interest 17% 12% 10.3% 7.7%

Number of Participants (Nov 2016) 64 64 23 99

Number of Participants (Jan 2016) 67 74 25 95

Average number of Participants 50 61 19 51

Minimum number of Participants 35 29 10 24

Maximum number of Participants 68 97 30 94

Source: SG Cross Asset Research/CFTC

Statistics on categories of traders (short) participation in WTI futures since 2006

Producer/Merchant Managed Money Swap Dealer Other Reportables

% of Open Interest (Nov 2016) 50% 15% 24% 11%

% of Open Interest (Jan 2016) 55% 7% 29% 9%

Average % of Open Interest 47.0% 10% 30% 13%

Maximum % of Open Interest 71.7% 25% 57% 23%

Minimum % of Open Interest 29.2% 3% 10% 5%

Number of Participants (Nov 2016) 77 55 21 65

Number of Participants (Jan 2016) 82 47 24 54

Average number of Participants 61 43 22 56

Minimum number of Participants 90 21 11 29

Maximum number of Participants 47 77 35 83

Source: SG Cross Asset Research/CFTC

Michael Haigh – MD / Head of Commodity Research 29

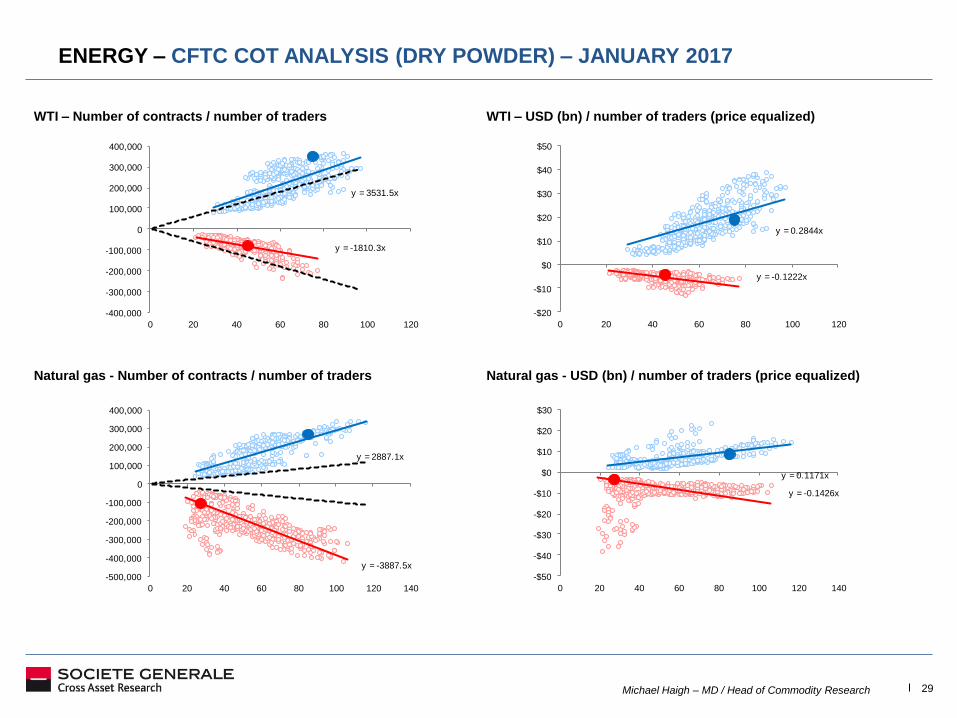

ENERGY – CFTC COT ANALYSIS (DRY POWDER) – JANUARY 2017

WTI – Number of contracts / number of traders WTI – USD (bn) / number of traders (price equalized)

Natural gas - Number of contracts / number of traders Natural gas - USD (bn) / number of traders (price equalized)

y = 3531.5x

y = -1810.3x

-400,000

-300,000

-200,000

-100,000

0

100,000

200,000

300,000

400,000

0 20 40 60 80 100 120

y = 0.2844x

y = -0.1222x

-$20

-$10

$0

$10

$20

$30

$40

$50

0 20 40 60 80 100 120

y = 2887.1x

y = -3887.5x

-500,000

-400,000

-300,000

-200,000

-100,000

0

100,000

200,000

300,000

400,000

0 20 40 60 80 100 120 140

y = 0.1171x

y = -0.1426x

-$50

-$40

-$30

-$20

-$10

$0

$10

$20

$30

0 20 40 60 80 100 120 140

Michael Haigh – MD / Head of Commodity Research 30

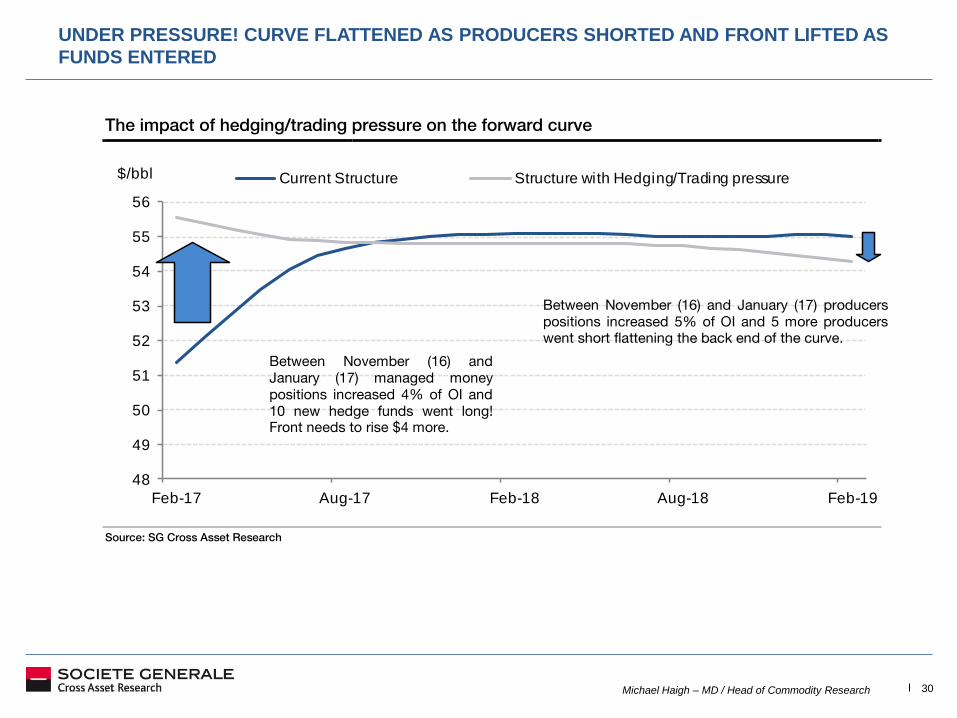

UNDER PRESSURE! CURVE FLATTENED AS PRODUCERS SHORTED AND FRONT LIFTED AS

FUNDS ENTERED

The impact of hedging/trading pressure on the forward curve

Source: SG Cross Asset Research

48

49

50

51

52

53

54

55

56

Feb-17 Aug-17 Feb-18 Aug-18 Feb-19

$/bbl Current Structure Structure with Hedging/Trading pressure

Between November (16) and January (17) producers

positions increased 5% of OI and 5 more producers

went short flattening the back end of the curve.

Between November (16) and

January (17) managed money

positions increased 4% of OI and

10 new hedge funds went long! Front needs to rise $4 more.

Michael Haigh – MD / Head of Commodity Research 31

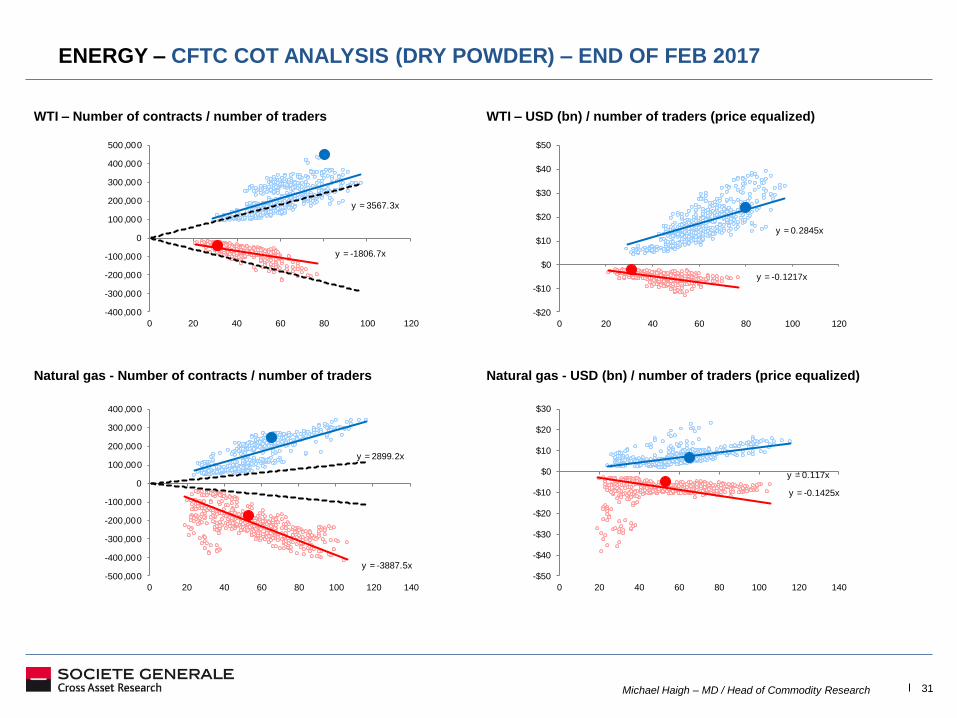

ENERGY – CFTC COT ANALYSIS (DRY POWDER) – END OF FEB 2017

WTI – Number of contracts / number of traders WTI – USD (bn) / number of traders (price equalized)

Natural gas - Number of contracts / number of traders Natural gas - USD (bn) / number of traders (price equalized)

y = 3567.3x

y = -1806.7x

-400,000

-300,000

-200,000

-100,000

0

100,000

200,000

300,000

400,000

500,000

0 20 40 60 80 100 120

y = 0.2845x

y = -0.1217x

-$20

-$10

$0

$10

$20

$30

$40

$50

0 20 40 60 80 100 120

y = 2899.2x

y = -3887.5x

-500,000

-400,000

-300,000

-200,000

-100,000

0

100,000

200,000

300,000

400,000

0 20 40 60 80 100 120 140

y = 0.117x

y = -0.1425x

-$50

-$40

-$30

-$20

-$10

$0

$10

$20

$30

0 20 40 60 80 100 120 140

Michael Haigh – MD / Head of Commodity Research 32 Michael Haigh- MD / Head of Commodity Research

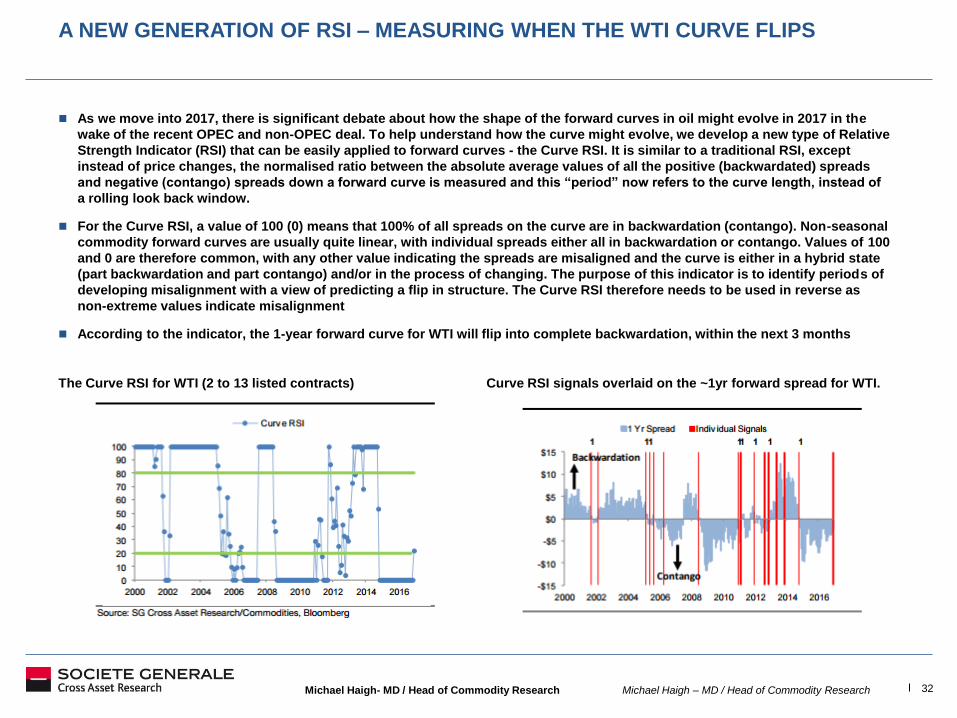

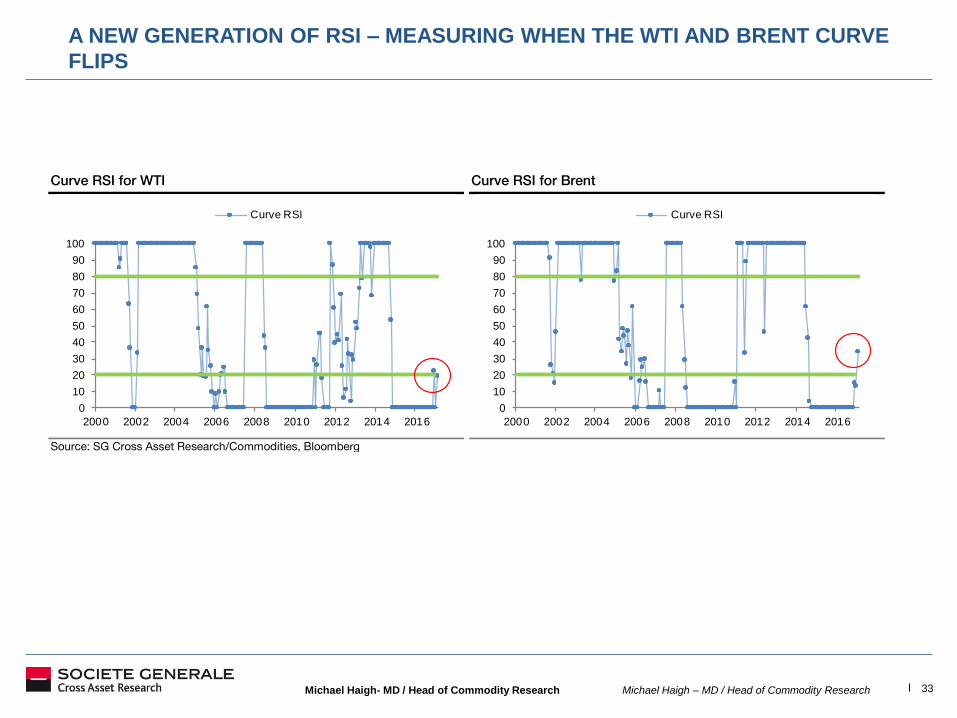

A NEW GENERATION OF RSI – MEASURING WHEN THE WTI CURVE FLIPS

As we move into 2017, there is significant debate about how the shape of the forward curves in oil might evolve in 2017 in the

wake of the recent OPEC and non-OPEC deal. To help understand how the curve might evolve, we develop a new type of Relative

Strength Indicator (RSI) that can be easily applied to forward curves - the Curve RSI. It is similar to a traditional RSI, except

instead of price changes, the normalised ratio between the absolute average values of all the positive (backwardated) spreads

and negative (contango) spreads down a forward curve is measured and this “period” now refers to the curve length, instead of

a rolling look back window.

For the Curve RSI, a value of 100 (0) means that 100% of all spreads on the curve are in backwardation (contango). Non-seasonal

commodity forward curves are usually quite linear, with individual spreads either all in backwardation or contango. Values of 100

and 0 are therefore common, with any other value indicating the spreads are misaligned and the curve is either in a hybrid state

(part backwardation and part contango) and/or in the process of changing. The purpose of this indicator is to identify periods of

developing misalignment with a view of predicting a flip in structure. The Curve RSI therefore needs to be used in reverse as

non-extreme values indicate misalignment

According to the indicator, the 1-year forward curve for WTI will flip into complete backwardation, within the next 3 months

The Curve RSI for WTI (2 to 13 listed contracts) Curve RSI signals overlaid on the ~1yr forward spread for WTI.

Michael Haigh – MD / Head of Commodity Research 33 Michael Haigh- MD / Head of Commodity Research

A NEW GENERATION OF RSI – MEASURING WHEN THE WTI AND BRENT CURVE

FLIPS

Curve RSI for WTI Curve RSI for Brent

Source: SG Cross Asset Research/Commodities, Bloomberg

0

10

20

30

40

50

60

70

80

90

100

2000 2002 2004 2006 2008 2010 2012 2014 2016

Curve RSI

0

10

20

30

40

50

60

70

80

90

100

2000 2002 2004 2006 2008 2010 2012 2014 2016

Curve RSI

Michael Haigh – MD / Head of Commodity Research 34

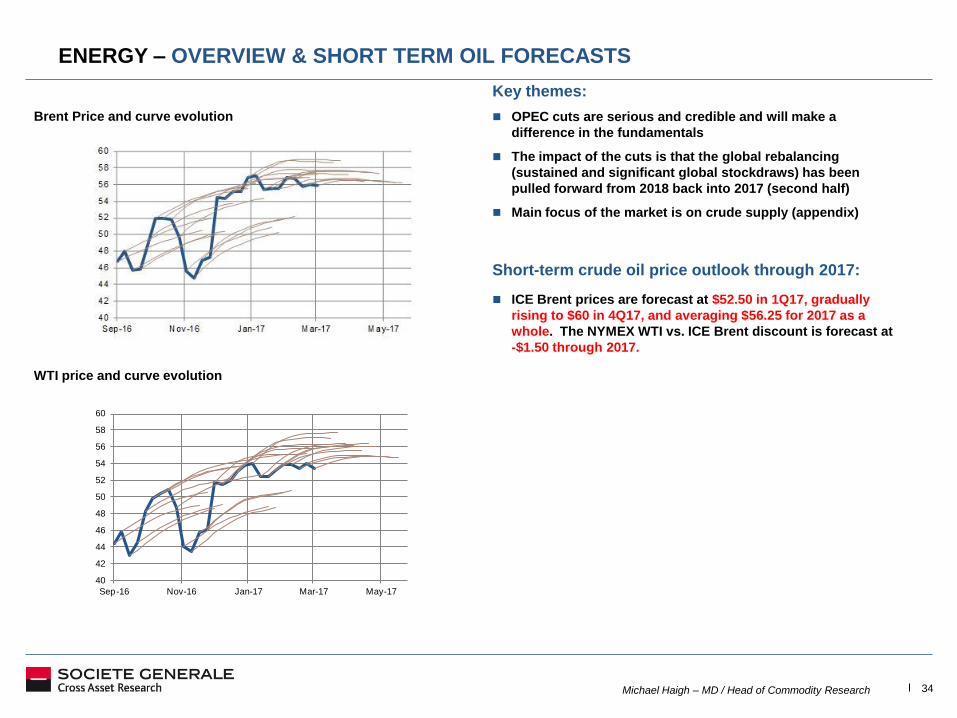

ENERGY – OVERVIEW & SHORT TERM OIL FORECASTS

Key themes:

OPEC cuts are serious and credible and will make a

difference in the fundamentals

The impact of the cuts is that the global rebalancing

(sustained and significant global stockdraws) has been

pulled forward from 2018 back into 2017 (second half)

Main focus of the market is on crude supply (appendix)

Short-term crude oil price outlook through 2017:

ICE Brent prices are forecast at $52.50 in 1Q17, gradually

rising to $60 in 4Q17, and averaging $56.25 for 2017 as a

whole. The NYMEX WTI vs. ICE Brent discount is forecast at

-$1.50 through 2017.

Brent Price and curve evolution

WTI price and curve evolution

40

42

44

46

48

50

52

54

56

58

60

Sep-16 Nov-16 Jan-17 Mar-17 May-17

Michael Haigh – MD / Head of Commodity Research 35

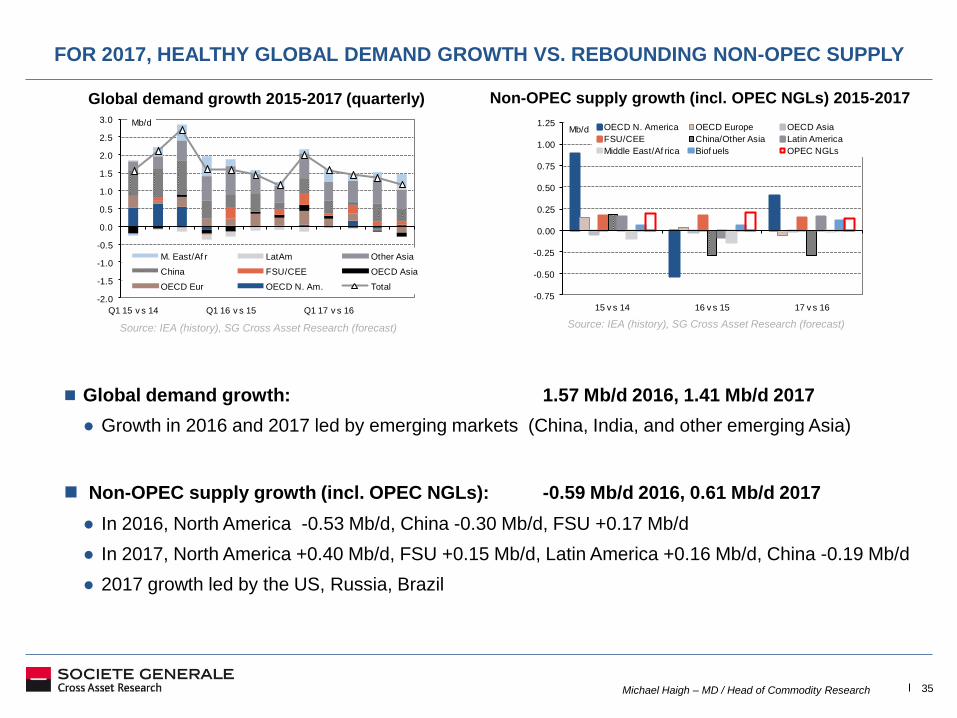

Global demand growth: 1.57 Mb/d 2016, 1.41 Mb/d 2017

● Growth in 2016 and 2017 led by emerging markets (China, India, and other emerging Asia)

Non-OPEC supply growth (incl. OPEC NGLs): -0.59 Mb/d 2016, 0.61 Mb/d 2017

● In 2016, North America -0.53 Mb/d, China -0.30 Mb/d, FSU +0.17 Mb/d

● In 2017, North America +0.40 Mb/d, FSU +0.15 Mb/d, Latin America +0.16 Mb/d, China -0.19 Mb/d

● 2017 growth led by the US, Russia, Brazil

Global demand growth 2015-2017 (quarterly)

Non-OPEC supply growth (incl. OPEC NGLs) 2015-2017

FOR 2017, HEALTHY GLOBAL DEMAND GROWTH VS. REBOUNDING NON-OPEC SUPPLY

Source: IEA (history), SG Cross Asset Research (forecast) Source: IEA (history), SG Cross Asset Research (forecast)

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Q1 15 v s 14 Q1 16 v s 15 Q1 17 v s 16

Mb/d

M. East/Af r LatAm Other Asia

China FSU/CEE OECD Asia

OECD Eur OECD N. Am. Total-0.75

-0.50

-0.25

0.00

0.25

0.50

0.75

1.00

1.25

15 v s 14 16 v s 15 17 v s 16

Mb/d OECD N. America OECD Europe OECD Asia

FSU/CEE China/Other Asia Latin America

Middle East/Af rica Biof uels OPEC NGLs

Michael Haigh – MD / Head of Commodity Research 36

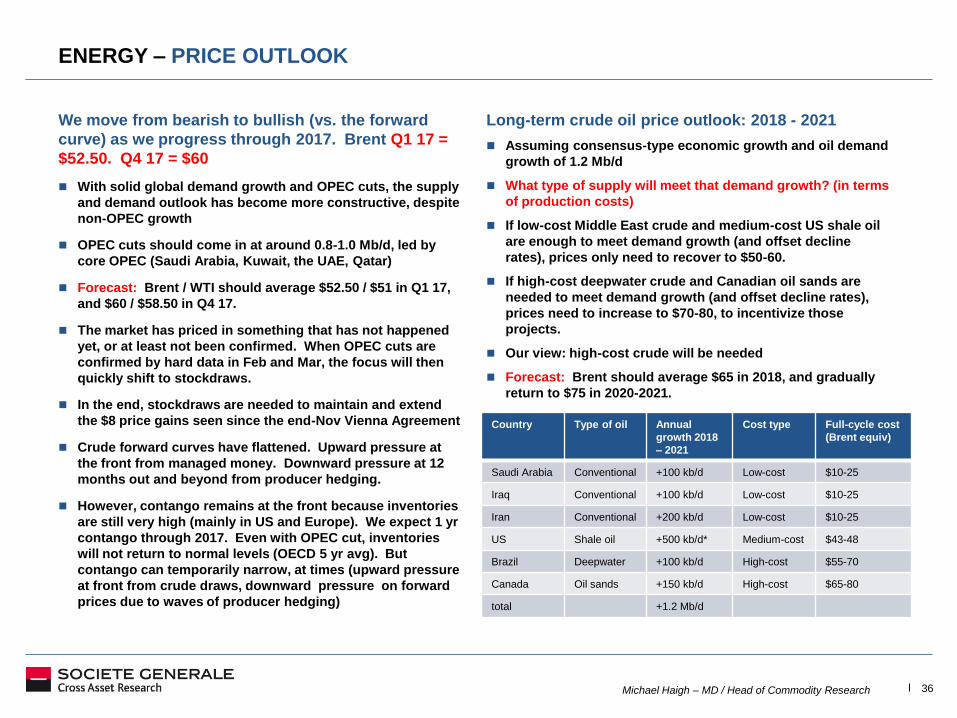

ENERGY – PRICE OUTLOOK

We move from bearish to bullish (vs. the forward

curve) as we progress through 2017. Brent Q1 17 =

$52.50. Q4 17 = $60

With solid global demand growth and OPEC cuts, the supply

and demand outlook has become more constructive, despite

non-OPEC growth

OPEC cuts should come in at around 0.8-1.0 Mb/d, led by

core OPEC (Saudi Arabia, Kuwait, the UAE, Qatar)

Forecast: Brent / WTI should average $52.50 / $51 in Q1 17,

and $60 / $58.50 in Q4 17.

The market has priced in something that has not happened

yet, or at least not been confirmed. When OPEC cuts are

confirmed by hard data in Feb and Mar, the focus will then

quickly shift to stockdraws.

In the end, stockdraws are needed to maintain and extend

the $8 price gains seen since the end-Nov Vienna Agreement

Crude forward curves have flattened. Upward pressure at

the front from managed money. Downward pressure at 12

months out and beyond from producer hedging.

However, contango remains at the front because inventories

are still very high (mainly in US and Europe). We expect 1 yr

contango through 2017. Even with OPEC cut, inventories

will not return to normal levels (OECD 5 yr avg). But

contango can temporarily narrow, at times (upward pressure

at front from crude draws, downward pressure on forward

prices due to waves of producer hedging)

Long-term crude oil price outlook: 2018 - 2021

Assuming consensus-type economic growth and oil demand

growth of 1.2 Mb/d

What type of supply will meet that demand growth? (in terms

of production costs)

If low-cost Middle East crude and medium-cost US shale oil

are enough to meet demand growth (and offset decline

rates), prices only need to recover to $50-60.

If high-cost deepwater crude and Canadian oil sands are

needed to meet demand growth (and offset decline rates),

prices need to increase to $70-80, to incentivize those

projects.

Our view: high-cost crude will be needed

Forecast: Brent should average $65 in 2018, and gradually

return to $75 in 2020-2021.

Country Type of oil Annual

growth 2018

– 2021

Cost type Full-cycle cost

(Brent equiv)

Saudi Arabia Conventional +100 kb/d Low-cost $10-25

Iraq Conventional +100 kb/d Low-cost $10-25

Iran Conventional +200 kb/d Low-cost $10-25

US Shale oil +500 kb/d* Medium-cost $43-48

Brazil Deepwater +100 kb/d High-cost $55-70

Canada Oil sands +150 kb/d High-cost $65-80

total +1.2 Mb/d

Michael Haigh – MD / Head of Commodity Research 37

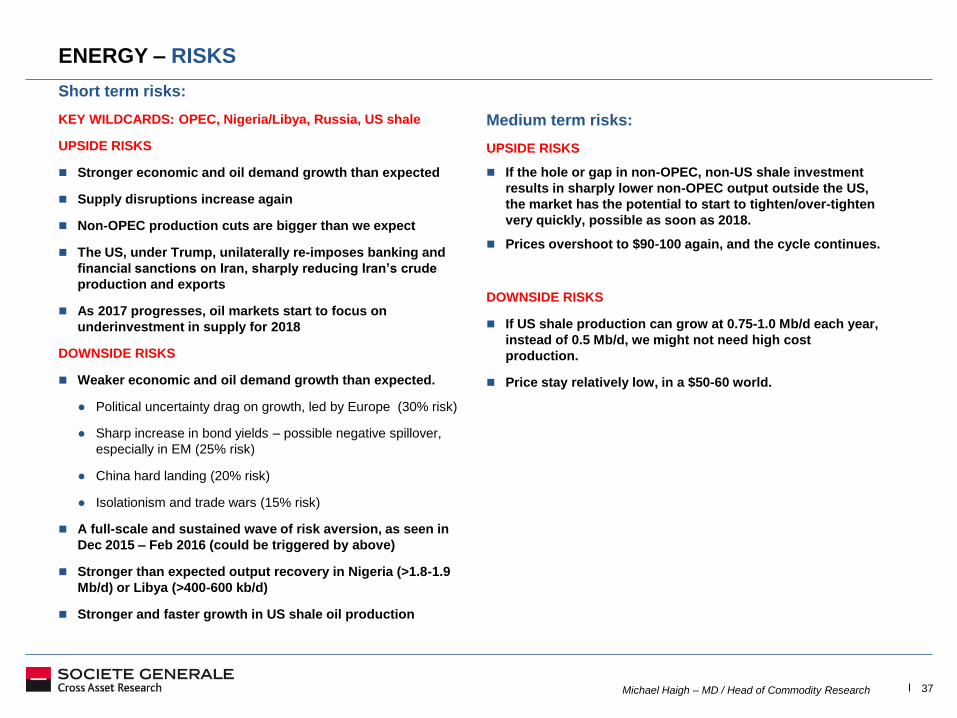

ENERGY – RISKS

Short term risks:

KEY WILDCARDS: OPEC, Nigeria/Libya, Russia, US shale

UPSIDE RISKS

Stronger economic and oil demand growth than expected

Supply disruptions increase again

Non-OPEC production cuts are bigger than we expect

The US, under Trump, unilaterally re-imposes banking and

financial sanctions on Iran, sharply reducing Iran’s crude

production and exports

As 2017 progresses, oil markets start to focus on

underinvestment in supply for 2018

DOWNSIDE RISKS

Weaker economic and oil demand growth than expected.

● Political uncertainty drag on growth, led by Europe (30% risk)

● Sharp increase in bond yields – possible negative spillover,

especially in EM (25% risk)

● China hard landing (20% risk)

● Isolationism and trade wars (15% risk)

A full-scale and sustained wave of risk aversion, as seen in

Dec 2015 – Feb 2016 (could be triggered by above)

Stronger than expected output recovery in Nigeria (>1.8-1.9

Mb/d) or Libya (>400-600 kb/d)

Stronger and faster growth in US shale oil production

Medium term risks:

UPSIDE RISKS

If the hole or gap in non-OPEC, non-US shale investment

results in sharply lower non-OPEC output outside the US,

the market has the potential to start to tighten/over-tighten

very quickly, possible as soon as 2018.

Prices overshoot to $90-100 again, and the cycle continues.

DOWNSIDE RISKS

If US shale production can grow at 0.75-1.0 Mb/d each year,

instead of 0.5 Mb/d, we might not need high cost

production.

Price stay relatively low, in a $50-60 world.

Michael Haigh – MD / Head of Commodity Research 38

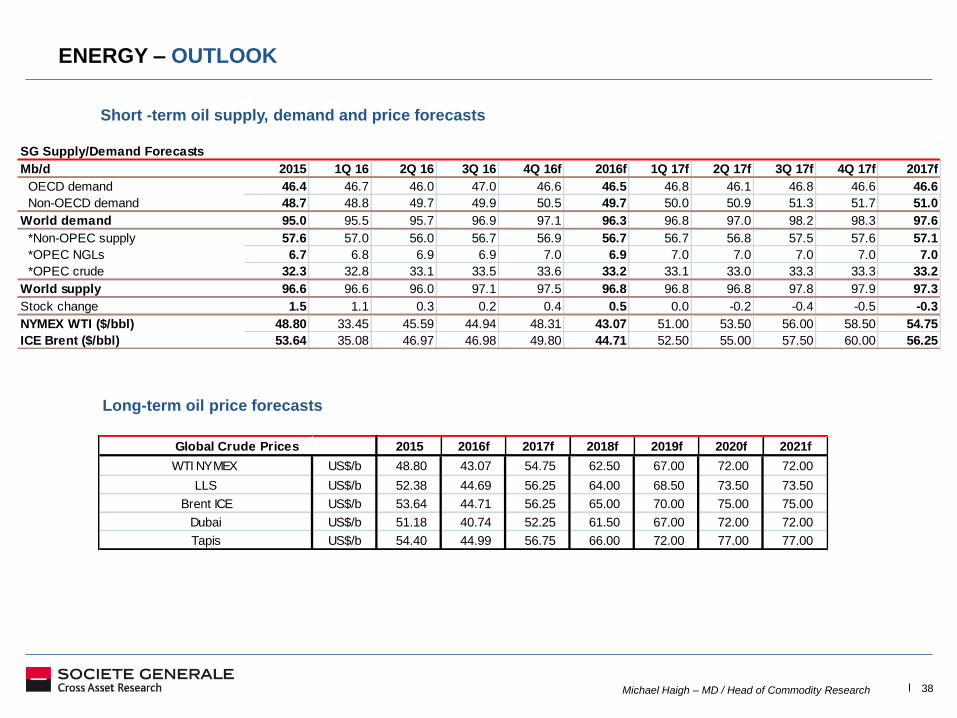

ENERGY – OUTLOOK

SG Supply/Demand Forecasts

Mb/d 2015 1Q 16 2Q 16 3Q 16 4Q 16f 2016f 1Q 17f 2Q 17f 3Q 17f 4Q 17f 2017f

OECD demand 46.4 46.7 46.0 47.0 46.6 46.5 46.8 46.1 46.8 46.6 46.6

Non-OECD demand 48.7 48.8 49.7 49.9 50.5 49.7 50.0 50.9 51.3 51.7 51.0

World demand 95.0 95.5 95.7 96.9 97.1 96.3 96.8 97.0 98.2 98.3 97.6

*Non-OPEC supply 57.6 57.0 56.0 56.7 56.9 56.7 56.7 56.8 57.5 57.6 57.1

*OPEC NGLs 6.7 6.8 6.9 6.9 7.0 6.9 7.0 7.0 7.0 7.0 7.0

*OPEC crude 32.3 32.8 33.1 33.5 33.6 33.2 33.1 33.0 33.3 33.3 33.2

World supply 96.6 96.6 96.0 97.1 97.5 96.8 96.8 96.8 97.8 97.9 97.3

Stock change 1.5 1.1 0.3 0.2 0.4 0.5 0.0 -0.2 -0.4 -0.5 -0.3

NYMEX WTI ($/bbl) 48.80 33.45 45.59 44.94 48.31 43.07 51.00 53.50 56.00 58.50 54.75

ICE Brent ($/bbl) 53.64 35.08 46.97 46.98 49.80 44.71 52.50 55.00 57.50 60.00 56.25

2015 2016f 2017f 2018f 2019f 2020f 2021f

WTI NYMEX US$/b 48.80 43.07 54.75 62.50 67.00 72.00 72.00

LLS US$/b 52.38 44.69 56.25 64.00 68.50 73.50 73.50

Brent ICE US$/b 53.64 44.71 56.25 65.00 70.00 75.00 75.00

Dubai US$/b 51.18 40.74 52.25 61.50 67.00 72.00 72.00

Tapis US$/b 54.40 44.99 56.75 66.00 72.00 77.00 77.00

Global Crude Prices

Short -term oil supply, demand and price forecasts

Long-term oil price forecasts

Michael Haigh – MD / Head of Commodity Research 39

TRUMP AND OIL: REPUBLICAN PROPOSAL FOR BORDER TAX ADJUSTMENT

The proposal by Republican Speaker of the House Paul Ryan is from August 2016. Politics is quite complicated and

traditional conservative Republicans – the source of the proposal – do not appear to be in agreement with Trump on

this issue. There is no draft legislation currently. Long process – hypothetically would not become law before 2018.

But the odds are against it. For oil: the main impact would be that the cost of crude imported in to the US would be

increased by 20% relative to domestic crude (20% comes from the new corporate tax rate).

SHORT RUN IMPACT

A global (Brent) crude price of $50 would become $60. WTI immediately jumps to parity with Brent, because US

producers would charge US refiners the same price that the refiners would have to pay for competing crude. Prices

across the entire global crude and products complex would increase.

ADJUSTMENTS

US producers would benefit and invest more. US refiners would suffer domestically (with differences by region). In

a $50-60 world, retail gasoline prices estimated to increase by $0.30-0.36/gallon. Hypothetically, US refiners would

adapt by investing to run more light sweet domestic / less med/hvy sour imported crude. However, this is key,

refinery cycle is 5 years or more. Cannot adapt fast and still needs sour imports.

LONG RUN IMPACT

US production growth would be strong in any case. The US needs to import less and less crude IF refiners could

adapt to using more sweet. In addition, with the same or lower global demand (higher prices), something has got to

give. Brent drops to a discount against WTI, and investment and production in other crudes suffers. Bottom line:

US production growth “crowds out” more expensive crude elsewhere.

However, the reality is refiners cycle and shale cycle is very different (many years versus few months). As oil prices

jump, US shale increases and gets exported (export restrictions lifted in Dec 2015) and global oil prices get pushed

further down. WTI, export prices and Brent prices (etc) go down. US production also crowds out more expensive oil

production in this case too. We are back to the same world as before Nov 2014 (where large scale global oversupply

led by US puts higher cost projects at risk).

Michael Haigh – MD / Head of Commodity Research 40 Michael Haigh- MD / Head of Commodity Research

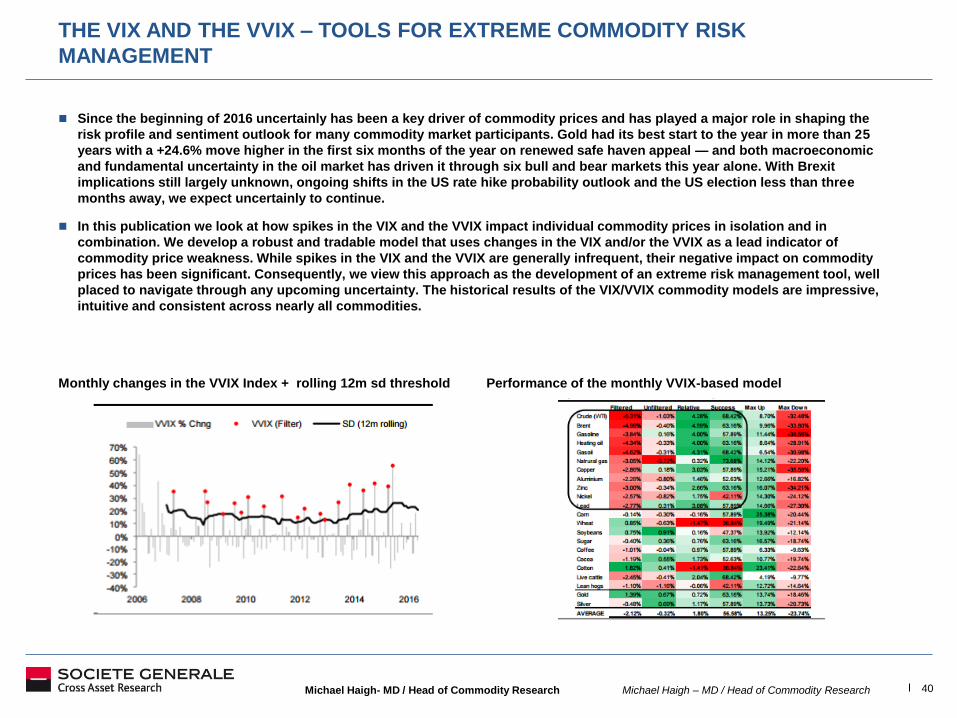

THE VIX AND THE VVIX – TOOLS FOR EXTREME COMMODITY RISK

MANAGEMENT

Since the beginning of 2016 uncertainly has been a key driver of commodity prices and has played a major role in shaping the

risk profile and sentiment outlook for many commodity market participants. Gold had its best start to the year in more than 25

years with a +24.6% move higher in the first six months of the year on renewed safe haven appeal — and both macroeconomic

and fundamental uncertainty in the oil market has driven it through six bull and bear markets this year alone. With Brexit

implications still largely unknown, ongoing shifts in the US rate hike probability outlook and the US election less than three

months away, we expect uncertainly to continue.

In this publication we look at how spikes in the VIX and the VVIX impact individual commodity prices in isolation and in

combination. We develop a robust and tradable model that uses changes in the VIX and/or the VVIX as a lead indicator of

commodity price weakness. While spikes in the VIX and the VVIX are generally infrequent, their negative impact on commodity

prices has been significant. Consequently, we view this approach as the development of an extreme risk management tool, well

placed to navigate through any upcoming uncertainty. The historical results of the VIX/VVIX commodity models are impressive,

intuitive and consistent across nearly all commodities.

Monthly changes in the VVIX Index + rolling 12m sd threshold Performance of the monthly VVIX-based model

Michael Haigh – MD / Head of Commodity Research 41

APPENDIX - DISCLAIMER

ANALYST CERTIFICATION

Each author of this research report listed on the cover hereby certifies that the views expressed in the research report accurately reflect his or her personal views, including views about subject securities or issuers mentioned in the report, if any. No part of his or her compensation was, is or will be related, directly or indirectly to the specific recommendations or views expressed in this report.

The analyst(s) who author research are employed by SG and its affiliates in locations, including but not limited to, Paris, London, New York, Hong Kong, Tokyo, Bangalore, Madrid, Milan, Warsaw and Moscow.

CONFLICTS OF INTEREST

This research contains the views, opinions and recommendations of Société Générale (SG) credit research analysts and/or strategists. To the extent that this research contains trade ideas based on macro views of economic market conditions or relative value, it may differ from the fundamental credit opinions and recommendations contained in credit sector or company research reports and from the views and opinions of other departments of SG and its affiliates. Credit research analysts and/or strategists routinely consult with SG sales and trading desk personnel regarding market information including, but not limited to, pricing, spread levels and trading activity of a specific fixed income security or financial instrument, sector or other asset class. Trading desks may trade, or have traded, as principal on the basis of the research analyst(s) views and reports. In addition, research analysts receive compensation based, in part, on the quality and accuracy of their analysis, client feedback, trading desk and firm revenues and competitive factors. As a general matter, SG and/or its affiliates normally make a market and trade as principal in fixed income securities discussed in research reports.

IMPORTANT DISCLAIMER: The information herein is not intended to be an offer to buy or sell, or a solicitation of an offer to buy or sell, any securities and has been obtained from, or is based upon, sources believed to be reliable but is not guaranteed as to accuracy or completeness. Material contained in this report satisfies the regulatory provisions concerning independent investment research as defined in MiFID. Information concerning conflicts of interest and SG’s management of such conflicts is contained in the SG’s Policies for Managing Conflicts of Interests in Connection with Investment Research which is available at https://www.sgresearch.com/Content/Compliance/Compliance.aspx SG does, from time to time, deal, trade in, profit from, hold, act as market-makers or advisers, brokers or bankers in relation to the securities, or derivatives thereof, of persons, firms or entities mentioned in this document and may be represented on the board of such persons, firms or entities. SG does, from time to time, act as a principal trader in equities or debt securities that may be referred to in this report and may hold equity or debt securities positions. Employees of SG, or individuals connected to them, may from time to time have a position in or hold any of the investments or related investments mentioned in this document. SG is under no obligation to disclose or take account of this document when advising or dealing with or on behalf of customers. The views of SG reflected in this document may change without notice. In addition, SG may issue other reports that are inconsistent with, and reach different conclusions from, the information presented in this report and is under no obligation to ensure that such other reports are brought to the attention of any recipient of this report. To the maximum extent possible at law, SG does not accept any liability whatsoever arising from the use of the material or information contained herein. This research document is not intended for use by or targeted to retail customers. Should a retail customer obtain a copy of this report he/she should not base his/her investment decisions solely on the basis of this document and must seek independent financial advice.

The financial instruments discussed in this report may not be suitable for all investors and investors must make their own informed decisions and seek their own advice regarding the appropriateness of investing in financial instruments or implementing strategies discussed herein. The value of securities and financial instruments is subject to currency exchange rate fluctuation that may have a positive or negative effect on the price of such securities or financial instruments, and investors in securities such as ADRs effectively assume this risk. SG does not provide any tax advice. Past performance is not necessarily a guide to future performance. Estimates of future performance are based on assumptions that may not be realized. Investments in general, and derivatives in particular, involve numerous risks, including, among others, market, counterparty default and liquidity risk. Trading in options involves additional risks and is not suitable for all investors. An option may become worthless by its expiration date, as it is a depreciating asset. Option ownership could result in significant loss or gain, especially for options of unhedged positions. Prior to buying or selling an option, investors must review the "Characteristics and Risks of Standardized Options" at http://www.optionsclearing.com/about/publications/character-risks.jsp. or from your SG representative. Analysis of option trading strategies does not consider the cost of commissions. Supporting documentation for options trading strategies is available upon request.

.

Michael Haigh – MD / Head of Commodity Research 42

APPENDIX – DISCLAIMER (CONT’D)

Notice to French Investors: This publication is issued in France by or through Société Générale ("SG") which is authorised and supervised by the Autorité de Contrôle Prudentiel et de Résolution (ACPR) and regulated by the Autorité des Marchés Financiers (AMF).

Notice to U.K. Investors: Société Générale is a French credit institution (bank) authorised by the Autorité de Contrôle Prudentiel (the French Prudential Control Authority) and the Prudential Regulation Authority and subject to limited regulation by the Financial Conduct Authority and Prudential Regulation Authority. Details about the extent of our authorisation and regulation by the Prudential Regulation Authority, and regulation by the Financial Conduct Authority are available from us on request.

Notice to Swiss Investors: This document is provided in Switzerland by or through Société Générale Paris, Zürich Branch, and is provided only to qualified investors as defined in article 10 of the Swiss Collective Investment Scheme Act (“CISA”) and related provisions of the Collective Investment Scheme Ordinance and in strict compliance with applicable Swiss law and regulations. The products mentioned in this document may not be suitable for all types of investors. This document is based on the Directives on the Independence of Financial Research issued by the Swiss Bankers Association (SBA) in January 2008.

Notice to Polish Investors: This document has been issued in Poland by Societe Generale S.A. Oddzial w Polsce (“the Branch”) with its registered office in Warsaw (Poland) at 111 Marszałkowska St. The Branch is supervised by the Polish Financial Supervision Authority and the French ”Autorité de Contrôle Prudentiel”. This report is addressed to financial institutions only, as defined in the Act on trading in financial instruments. The Branch certifies that this document has been elaborated with due dilligence and care.

Notice to U.S. Investors: For purposes of SEC Rule 15a-6, SG Americas Securities LLC (“SGAS”) takes responsibility for this research report. This report is intended for institutional investors only. Any U.S. person wishing to discuss this report or effect transactions in any security discussed herein should do so with or through SGAS, a broker-dealer registered with the SEC and a member of FINRA, with its registered address at 245 Park Avenue, New York, NY, 10167. (212)-278-6000.

Notice to Canadian Investors: This document is for information purposes only and is intended for use by Permitted Clients, as defined under National Instrument 31-103, Accredited Investors, as defined under National Instrument 45-106, Accredited Counterparties as defined under the Derivatives Act (Québec) and "Qualified Parties" as defined under the ASC, BCSC, SFSC and NBSC Orders

Notice to Singapore Investors: This document is provided in Singapore by or through Société Générale ("SG"), Singapore Branch and is provided only to accredited investors, expert investors and institutional investors, as defined in Section 4A of the Securities and Futures Act, Cap. 289. Recipients of this document are to contact Société Générale, Singapore Branch in respect of any matters arising from, or in connection with, the document. If you are an accredited investor or expert investor, please be informed that in SG's dealings with you, SG is relying on the following exemptions to the Financial Advisers Act, Cap. 110 (“FAA”): (1) the exemption in Regulation 33 of the Financial Advisers Regulations (“FAR”), which exempts SG from complying with Section 25 of the FAA on disclosure of product information to clients; (2) the exemption set out in Regulation 34 of the FAR, which exempts SG from complying with Section 27 of the FAA on recommendations; and (3) the exemption set out in Regulation 35 of the FAR, which exempts SG from complying with Section 36 of the FAA on disclosure of certain interests in securities.

Notice to Hong Kong Investors: This report is distributed in Hong Kong by Société Générale, Hong Kong Branch which is licensed by the Securities and Futures Commission of Hong Kong under the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong) ("SFO"). This document does not constitute a solicitation or an offer of securities or an invitation to the public within the meaning of the SFO. This report is to be circulated only to "professional investors" as defined in the SFO.

Notice to Japanese Investors: This publication is distributed in Japan by Societe Generale Securities (North Pacific) Ltd., Tokyo Branch, which is regulated by the Financial Services Agency of Japan. This document is intended only for the Specified Investors, as defined by the Financial Instruments and Exchange Law in Japan and only for those people to whom it is sent directly by Societe Generale Securities (North Pacific) Ltd., Tokyo Branch, and under no circumstances should it be forwarded to any third party. The products mentioned in this report may not be eligible for sale in Japan and they may not be suitable for all types of investors.

Notice to Korean Investors: This report is distributed in Korea by SG Securities Korea Co., Ltd which is regulated by the Financial Supervisory Service and the Financial Services Commission.

Notice to Australian Investors: Societe Generale is exempt from the requirement to hold an Australian financial services licence (AFSL) under the Corporations Act 2001 (Cth) in respect of financial services, in reliance on ASIC Class Order 03/8240, a copy of which may be obtained at the web site of the Australian Securities and Investments Commission, http://www.asic.gov.au. The class order exempts financial services providers with a limited connection to Australia from the requirement to hold an AFSL where they provide financial services only to wholesale clients in Australia on certain conditions. Financial services provided by Societe Generale may be regulated under foreign laws and regulatory requirements, which are different from the laws applying in Australia.

http://www.sgcib.com. Copyright: The Société Générale Group 2014. All rights reserved.

This publication may not be reproduced or redistributed in whole in part without the prior consent of SG or its affiliates.