Embed Size (px)

Citation preview

Commissioning a Major Copper MineCommissioning a Major Copper Mine

Cautionary Language and Forward Looking StatementsCautionary Language and Forward Looking StatementsThis press release contains �forward-looking statements�, which are subject to various risks and uncertainties that could cause actual results and future events to differ materially from those expressed or implied by such statements. Investors are cautioned that such statements are not guarantees of future performance and results. Risks and uncertainties about the Company's business are more fully discussed in the Company�s disclosure documents filed from time to time with the Canadian and Australian securities authorities. Technical information in this release is summarized or extracted from the ��Technical Report on the Lumwana Copper Project, North West Province, Republic of Zambia�� dated June 2008 (the ��Technical Report��), prepared by Michael Davis, Process Manager, Ausenco Ltd. (��Ausenco��), Ross Bertinshaw, Principal of Golder Associates Pty Ltd. (��Golder��), Andrew Daley, Director, of Investor Resources Finance Pty Ltd(��IRF��), Daniel Guibal, Corporate Consultant, SRK Consulting (Australasia) Pty Ltd and Robert Hanbury, Associate Director, of Knight Piésold Pty Ltd. (��Knight Piésold��), each of whom is a ��QualiÞed Person�� in accordance with National Instrument 43-101 �Standards of Disclosure for Mineral Projects.The economic analysis of Lumwana in the Technical Report is based on a �Base Case� model (11-year mine life) which excludes Inferred Resources that are considered not to be defined in sufficient detail to have the economic considerations applied to them that would enable them to be categorized as Mineral Reserves. There is no certainty that the economic performance proposed in the economic analysis following depletion of the Mineral Reserves will be achieved. A �Development Scenario� is also discussed in the Technical Report that provides details of the 37-year mine life development plan. See the Technical Report for further details. Readers are cautioned not to rely solely on the summary of such information contained in this presentation, but should read the Technical Report which is posted on Equinox�s website (www.equinoxminerals.com www.sedar.com) and filed on SEDAR ( ) and any future amendments to such report. Readers are also directed to the cautionary notices and disclaimers contained herein. All currency in this presentation is U.S. dollars unless otherwise stated.

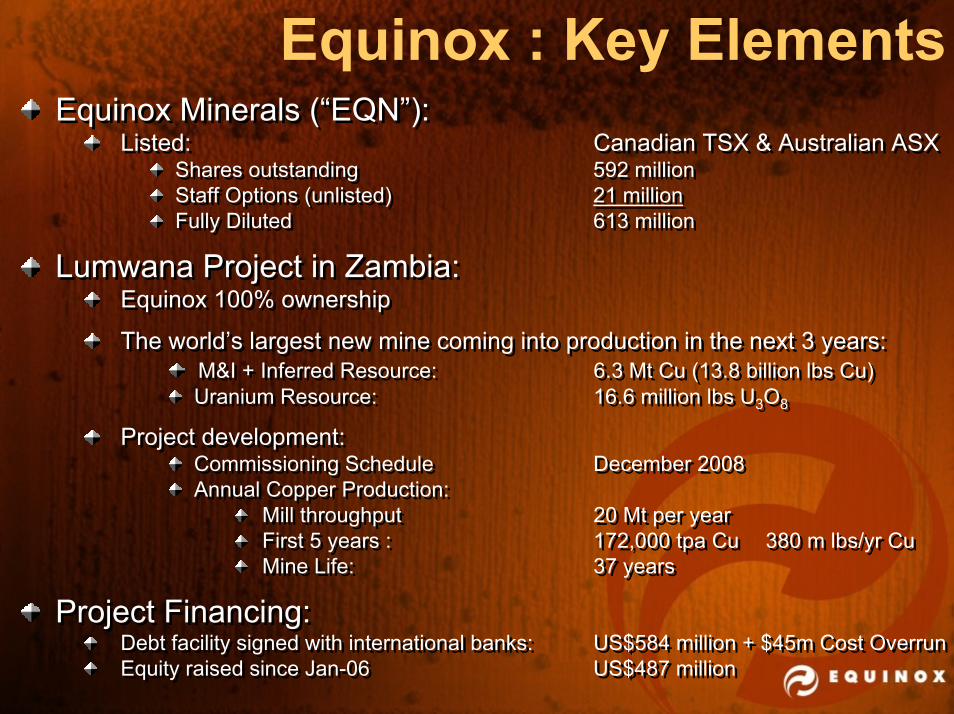

Equinox Minerals (�EQN�):Listed: Canadian TSX & Australian ASX

Shares outstanding 592 millionStaff Options (unlisted) 21 millionFully Diluted 613 million

Lumwana Project in Zambia:Equinox 100% ownership

The world�s largest new mine coming into production in the next 3 years:M&I + Inferred Resource: 6.3 Mt Cu (13.8 billion lbs Cu)Uranium Resource: 16.6 million lbs U3O8

Project development:Commissioning Schedule December 2008Annual Copper Production:

Mill throughput 20 Mt per yearFirst 5 years : 172,000 tpa Cu 380 m lbs/yr CuMine Life: 37 years

Project Financing:Debt facility signed with international banks: US$584 million + $45m Cost OverrunEquity raised since Jan-06 US$487 million

Equinox Minerals (�EQN�):Listed: Canadian TSX & Australian ASX

Shares outstanding 592 millionStaff Options (unlisted) 21 millionFully Diluted 613 million

Lumwana Project in Zambia:Equinox 100% ownership

The world�s largest new mine coming into production in the next 3 years:M&I + Inferred Resource: 6.3 Mt Cu (13.8 billion lbs Cu)Uranium Resource: 16.6 million lbs U3O8

Project development:Commissioning Schedule December 2008Annual Copper Production:

Mill throughput 20 Mt per yearFirst 5 years : 172,000 tpa Cu 380 m lbs/yr CuMine Life: 37 years

Project Financing:Debt facility signed with international banks: US$584 million + $45m Cost OverrunEquity raised since Jan-06 US$487 million

Equinox : Key Elements

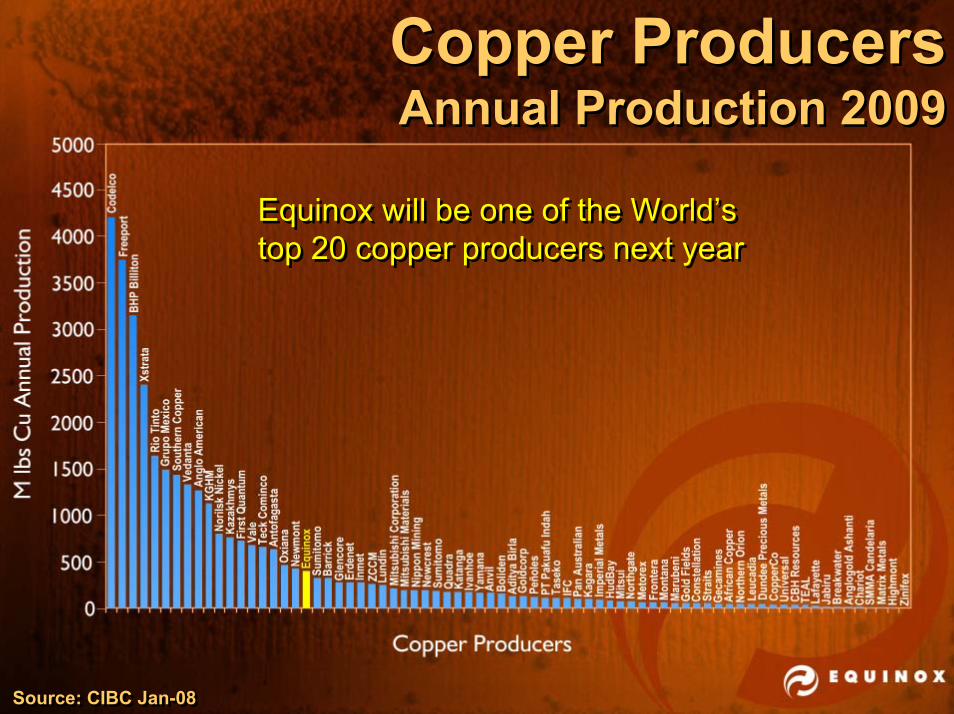

Copper ProducersAnnual Production 2009Copper ProducersAnnual Production 2009

Source: CIBC Jan-08Source: CIBC Jan-08

Equinox will be one of the World�s top 20 copper producers next yearEquinox will be one of the World�s top 20 copper producers next year

Global Copper Expansions2008 - 2009

Global Copper Expansions2008 - 2009

Source: GSJBWSource: GSJBW

Lumwana will be the largest new producer coming on-stream 2008-09

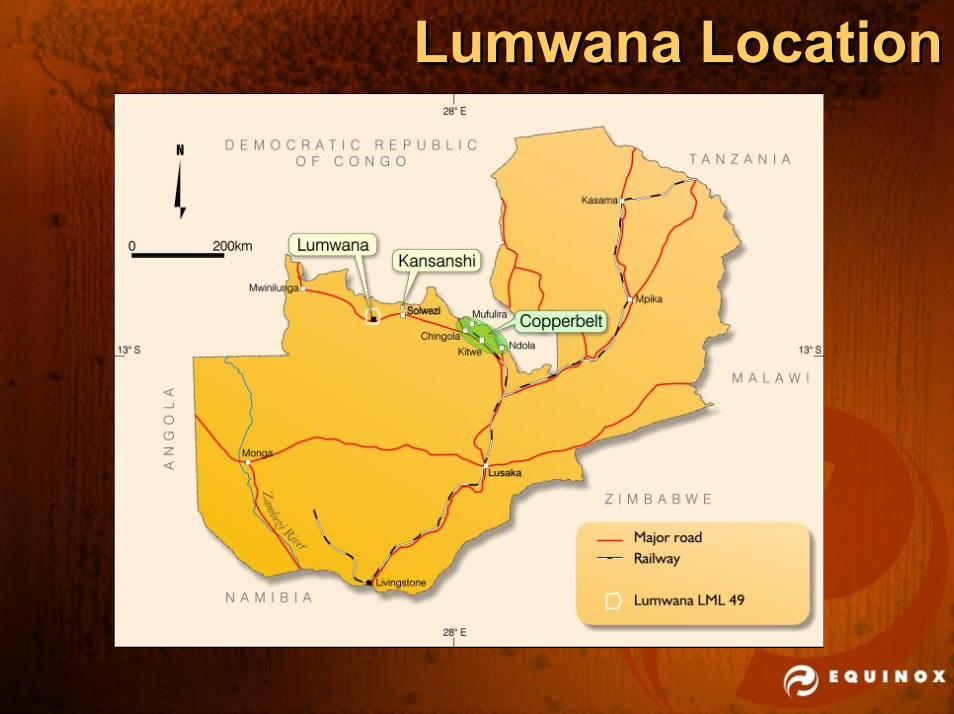

Lumwana LocationLumwana Location

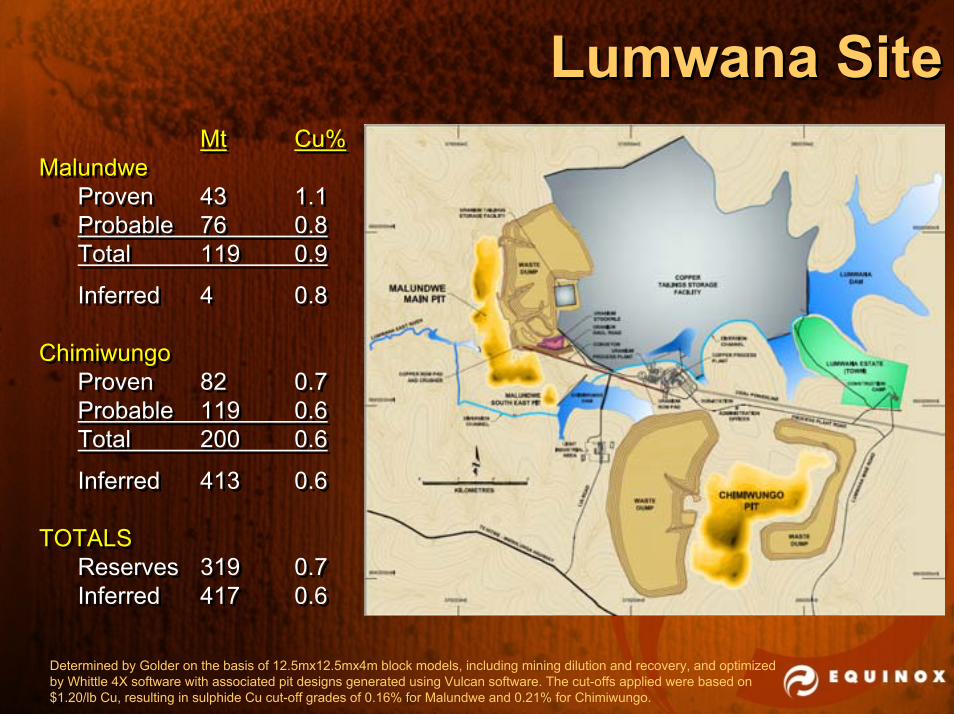

Lumwana SiteLumwana SiteMt Cu%

MalundweProven 43 1.1Probable 76 0.8Total 119 0.9

Inferred 4 0.8

ChimiwungoProven 82 0.7Probable 119 0.6Total 200 0.6

Inferred 413 0.6

TOTALSReserves 319 0.7Inferred 417 0.6

Mt Cu%Malundwe

Proven 43 1.1Probable 76 0.8Total 119 0.9

Inferred 4 0.8

ChimiwungoProven 82 0.7Probable 119 0.6Total 200 0.6

Inferred 413 0.6

TOTALSReserves 319 0.7Inferred 417 0.6

Determined by Golder on the basis of 12.5mx12.5mx4m block models, including mining dilution and recovery, and optimized by Whittle 4X software with associated pit designs generated using Vulcan software. The cut-offs applied were based on $1.20/lb Cu, resulting in sulphide Cu cut-off grades of 0.16% for Malundwe and 0.21% for Chimiwungo.

Simple Copper MetallurgySimple Copper MetallurgyComminution:

Very coarse sulphides

Ore is easy to crush + grind

Comminution:Very coarse sulphides

Ore is easy to crush + grind

Flotation:Ore floats easily and quickly

>95% recovery at coarse grind

Concentrate grades:Malundwe 41 - 45% CuChimiwungo 28 - 32% Cu

Flotation:Ore floats easily and quickly

>95% recovery at coarse grind

Concentrate grades:Malundwe 41 - 45% CuChimiwungo 28 - 32% Cu

Chambishi Smelter under constructionChambishi Smelter under construction

Smelting Contracts:All output for first 5 years

55% to CNMC/Yunnan

45% to Glencore/Mopani

5 year �Take & Pay�

TCRC/PP global benchmark

Smelting Contracts:All output for first 5 years

55% to CNMC/Yunnan

45% to Glencore/Mopani

5 year �Take & Pay�

TCRC/PP global benchmark

Uranium Reserves + ResourcesUranium Reserves + Resources

Uraninite occurs as high grade veins within copper mineralization

Primarily within 2 discrete zones at copper orebody hangingwall and footwall

Uranium to be selectively mined and stockpiled

Uraninite occurs as high grade veins within copper mineralization

Primarily within 2 discrete zones at copper orebody hangingwall and footwall

Uranium to be selectively mined and stockpiled

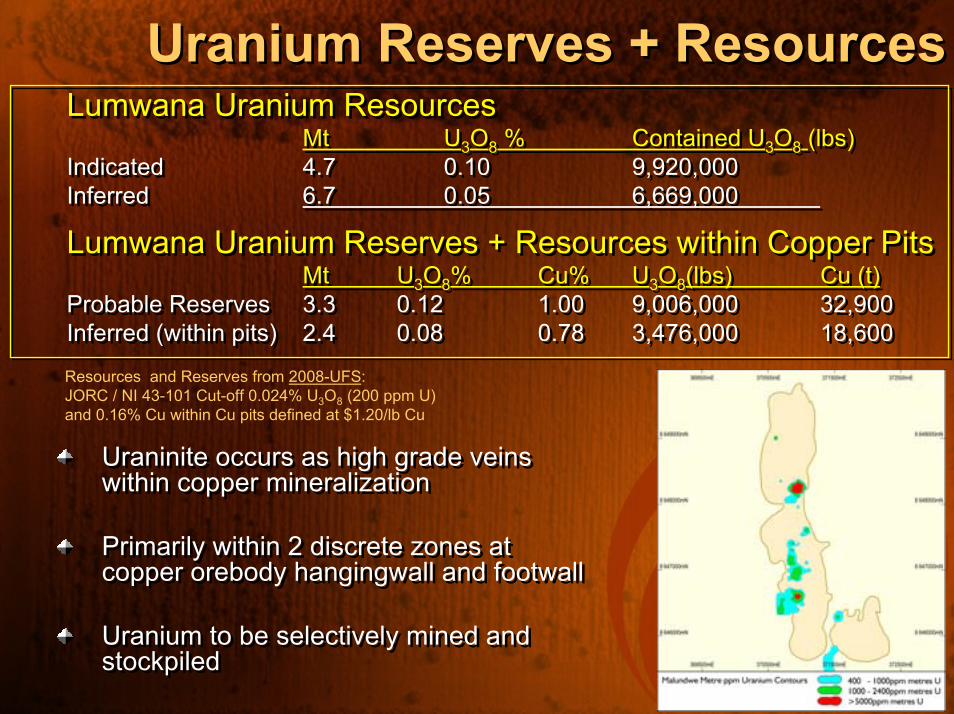

Lumwana Uranium ResourcesMt U3O8 % Contained U3O8 (lbs)

Indicated 4.7 0.10 9,920,000Inferred 6.7 0.05 6,669,000

Lumwana Uranium Reserves + Resources within Copper PitsMt U3O8% Cu% U3O8(lbs) Cu (t)

Probable Reserves 3.3 0.12 1.00 9,006,000 32,900Inferred (within pits) 2.4 0.08 0.78 3,476,000 18,600

Lumwana Uranium ResourcesMt U3O8 % Contained U3O8 (lbs)

Indicated 4.7 0.10 9,920,000Inferred 6.7 0.05 6,669,000

Lumwana Uranium Reserves + Resources within Copper PitsMt U3O8% Cu% U3O8(lbs) Cu (t)

Probable Reserves 3.3 0.12 1.00 9,006,000 32,900Inferred (within pits) 2.4 0.08 0.78 3,476,000 18,600

Resources and Reserves from 2008-UFS: JORC / NI 43-101 Cut-off 0.024% U3O8 (200 ppm U) and 0.16% Cu within Cu pits defined at $1.20/lb Cu

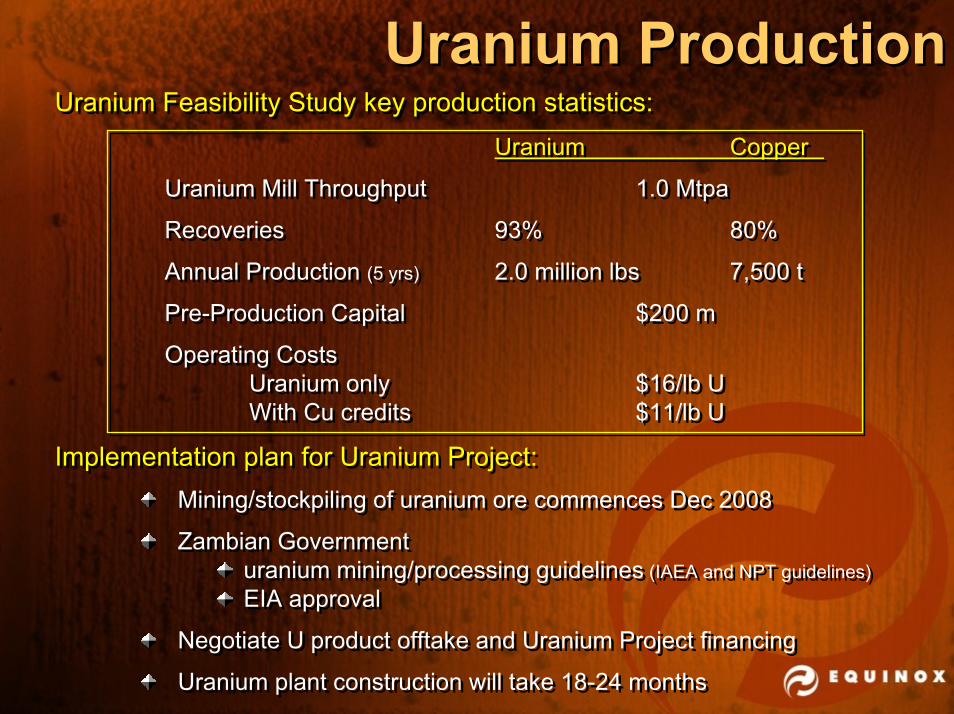

Uranium ProductionUranium ProductionUranium Copper

Uranium Mill Throughput 1.0 Mtpa

Recoveries 93% 80%

Annual Production (5 yrs) 2.0 million lbs 7,500 t

Pre-Production Capital $200 m

Operating CostsUranium only $16/lb UWith Cu credits $11/lb U

Uranium Copper

Uranium Mill Throughput 1.0 Mtpa

Recoveries 93% 80%

Annual Production (5 yrs) 2.0 million lbs 7,500 t

Pre-Production Capital $200 m

Operating CostsUranium only $16/lb UWith Cu credits $11/lb U

Uranium Feasibility Study key production statistics:Uranium Feasibility Study key production statistics:

Implementation plan for Uranium Project:Mining/stockpiling of uranium ore commences Dec 2008

Zambian Government uranium mining/processing guidelines (IAEA and NPT guidelines)EIA approval

Negotiate U product offtake and Uranium Project financing

Uranium plant construction will take 18-24 months

Implementation plan for Uranium Project:Mining/stockpiling of uranium ore commences Dec 2008

Zambian Government uranium mining/processing guidelines (IAEA and NPT guidelines)EIA approval

Negotiate U product offtake and Uranium Project financing

Uranium plant construction will take 18-24 months

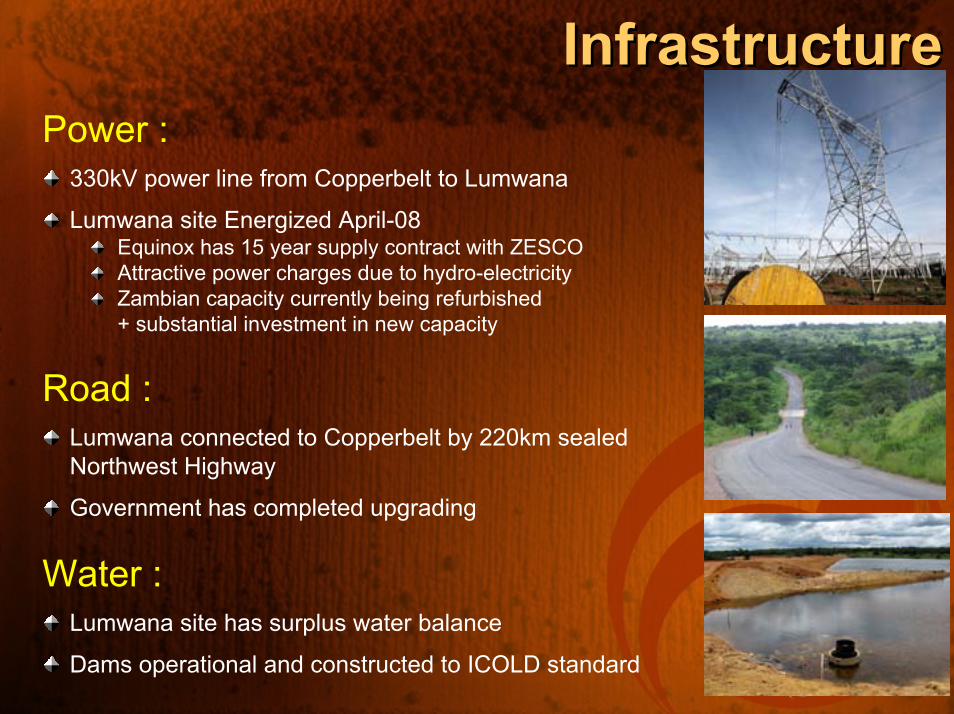

InfrastructureInfrastructurePower :

330kV power line from Copperbelt to Lumwana

Lumwana site Energized April-08Equinox has 15 year supply contract with ZESCOAttractive power charges due to hydro-electricityZambian capacity currently being refurbished + substantial investment in new capacity

Road :Lumwana connected to Copperbelt by 220km sealed Northwest Highway

Government has completed upgrading

Water :Lumwana site has surplus water balance

Dams operational and constructed to ICOLD standard

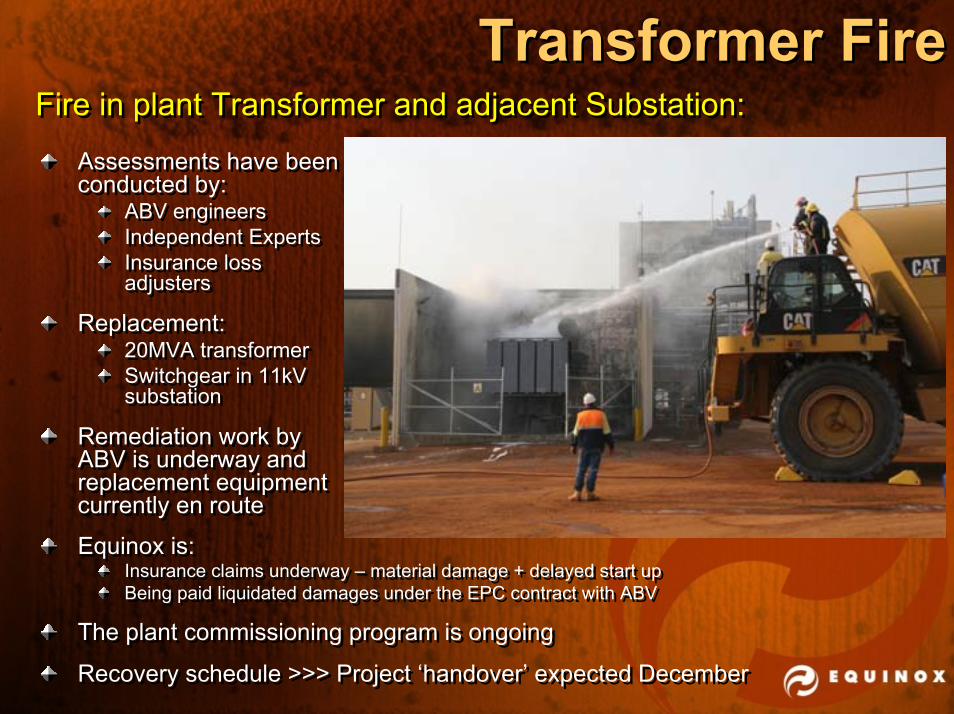

Transformer FireTransformer FireFire in plant Transformer and adjacent Substation:Fire in plant Transformer and adjacent Substation:

Assessments have been conducted by:

ABV engineersIndependent ExpertsInsurance loss adjusters

Replacement:20MVA transformerSwitchgear in 11kV substation

Remediation work by ABV is underway and replacement equipment currently en route

Assessments have been conducted by:

ABV engineersIndependent ExpertsInsurance loss adjusters

Replacement:20MVA transformerSwitchgear in 11kV substation

Remediation work by ABV is underway and replacement equipment currently en route

Equinox is:Insurance claims underway � material damage + delayed start upBeing paid liquidated damages under the EPC contract with ABV

The plant commissioning program is ongoing

Recovery schedule >>> Project �handover� expected December

Equinox is:Insurance claims underway � material damage + delayed start upBeing paid liquidated damages under the EPC contract with ABV

The plant commissioning program is ongoing

Recovery schedule >>> Project �handover� expected December

Transformer FireTransformer FireFire Incident rectification is now well advanced:Fire Incident rectification is now well advanced:

2nd Hand Transformer is now onsite ready for installation

New WEG Transformer currently en route from Brazil

3rd WEG Transformer on order

2nd Hand Transformer is now onsite ready for installation

New WEG Transformer currently en route from Brazil

3rd WEG Transformer on order

Replacement Switchgear is now being installed

Electrical �audit� underway to ensure that issues are rectified and unlikely to happen again

Replacement Switchgear is now being installed

Electrical �audit� underway to ensure that issues are rectified and unlikely to happen again

Mining FleetMining Fleet27 Hitachi Trucks (EH4500)

Hybrid diesel � electric with trolley assist:

200t weight240t load2,000 kW power

7 Hitachi Loaders (EX5500)3 diesel + 4 electric:

518t weight27 m3 bucket4,000 tph loading capacity

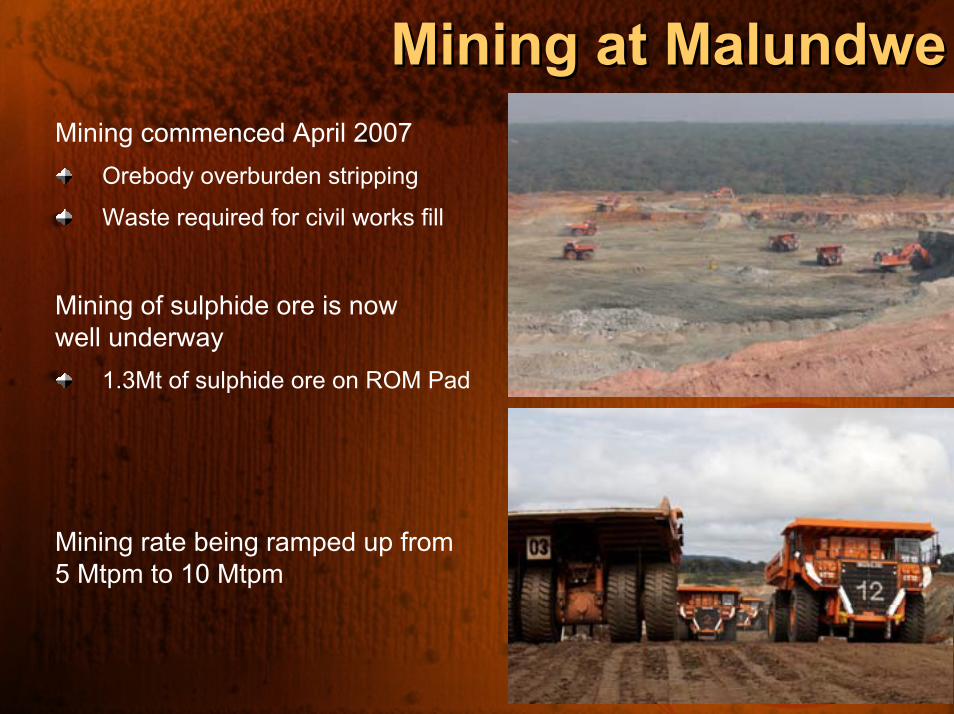

Mining at MalundweMining at Malundwe

Mining rate being ramped up from 5 Mtpm to 10 Mtpm

Mining commenced April 2007Orebody overburden stripping

Waste required for civil works fill

Mining of sulphide ore is now well underway

1.3Mt of sulphide ore on ROM Pad

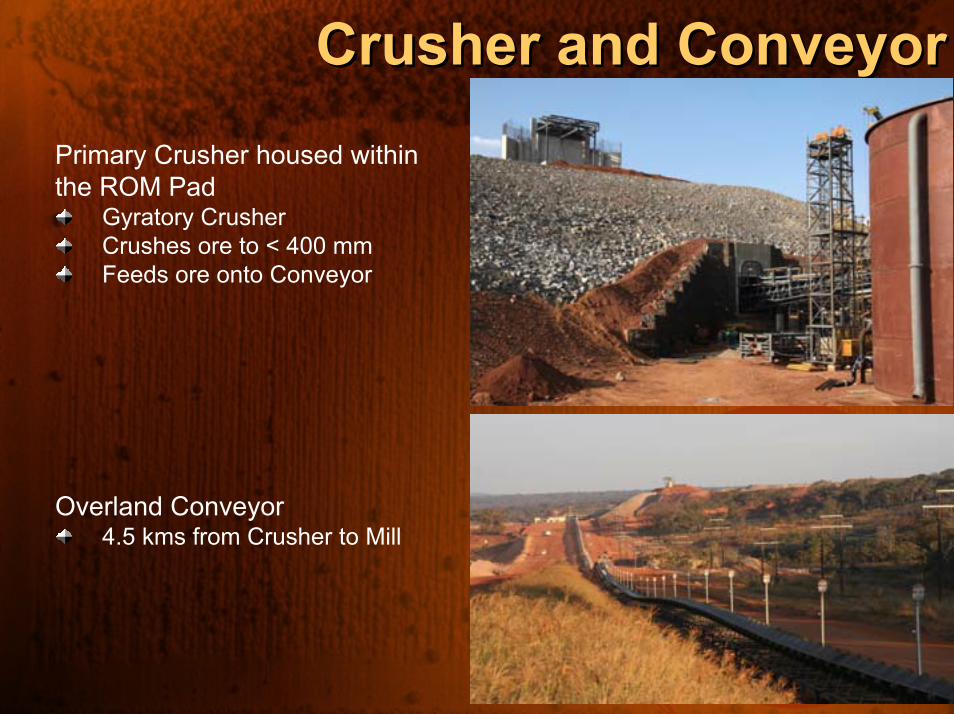

Crusher and ConveyorCrusher and ConveyorPrimary Crusher housed within the ROM Pad

Gyratory CrusherCrushes ore to < 400 mmFeeds ore onto Conveyor

Overland Conveyor4.5 kms from Crusher to Mill

SAG Mill CommissioningSAG Mill Commissioning

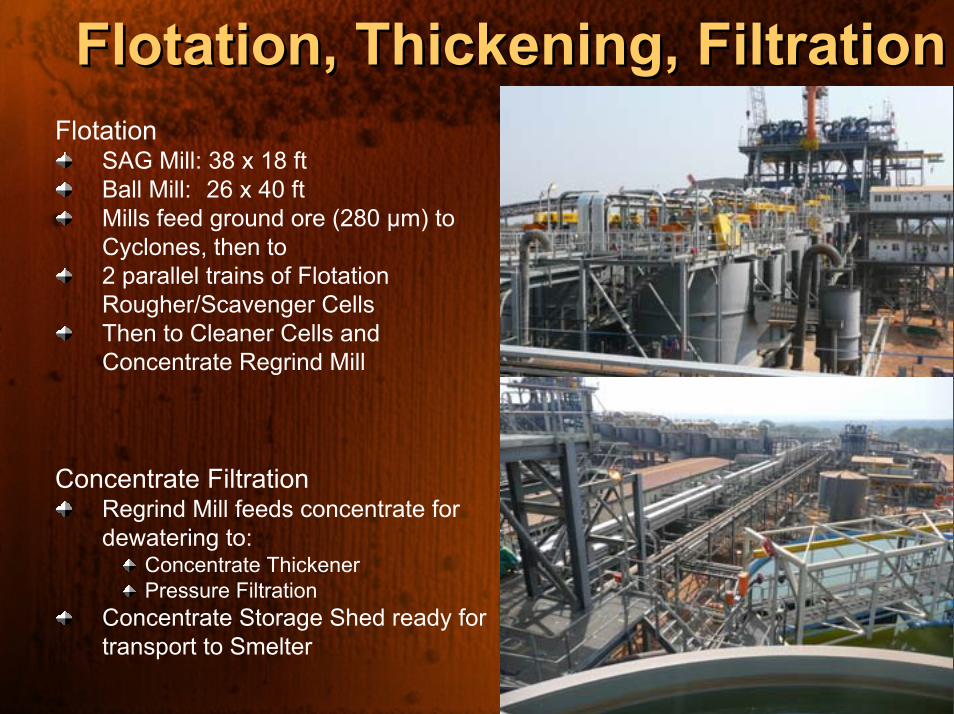

Flotation, Thickening, FiltrationFlotation, Thickening, FiltrationFlotation

SAG Mill: 38 x 18 ftBall Mill: 26 x 40 ftMills feed ground ore (280 µm) to Cyclones, then to2 parallel trains of Flotation Rougher/Scavenger CellsThen to Cleaner Cells and Concentrate Regrind Mill

Concentrate FiltrationRegrind Mill feeds concentrate for dewatering to:

Concentrate ThickenerPressure Filtration

Concentrate Storage Shed ready for transport to Smelter

Plant ConstructionPlant Construction

SAG, Ball Mill & Concentrator

Plant ConstructionPlant Construction

Commissioning well underway

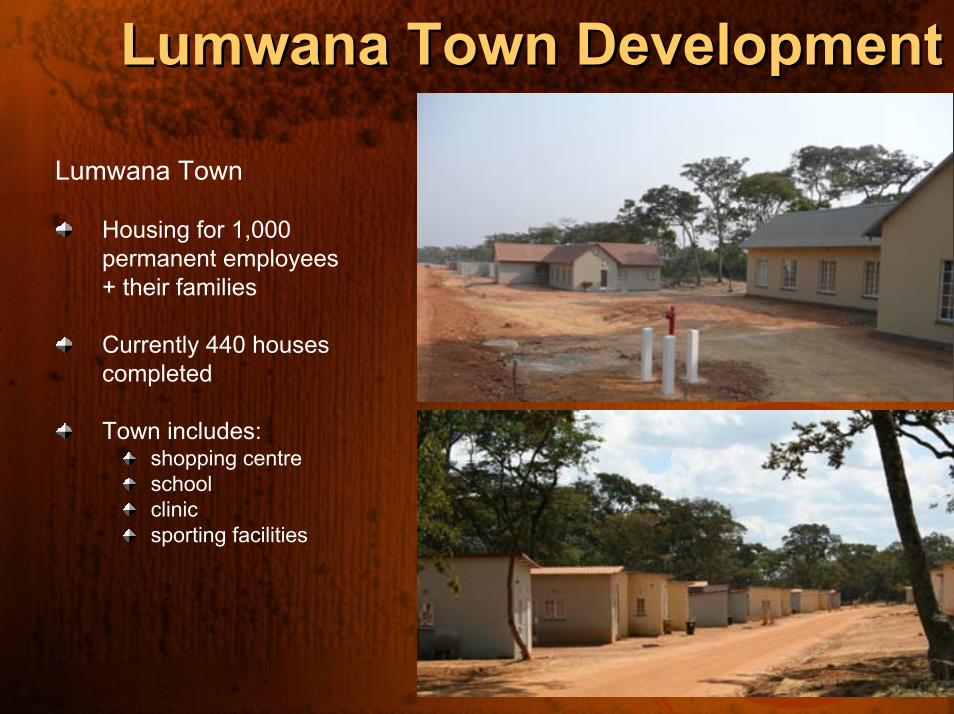

Lumwana Town DevelopmentLumwana Town Development

Lumwana Town

Housing for 1,000 permanent employees+ their families

Currently 440 houses completed

Town includes:shopping centreschoolclinicsporting facilities

Supporting Local CommunitiesSupporting Local CommunitiesEquinox fuelling local business development:

Small-Medium Business DevelopmentCrafts, textiles, sample bags tailoringCommunity market days

Commercial Agriculture/AquacultureFloriculture � Protea farmingVegetable farming and marketingJatropha plantations � bio diesel (JV with BP)Commercial fishery developed

Social Infrastructure/ LMC Trust FundConstruction for 6 local schools

30 classroom blocks 4 teachers houses

3 local clinics 2 women�s development centres1 Community Library

Local EmploymentEmployment for 1000 peopleEducation, scholarships, apprenticeships

ZambiaZambiaPolitics:

Stable, multi-party democracy

Equinox has a very constructive relationship with the Government

Unfortunate death of President Mwanawasa

Election 0n 30 October

English language + law

Modern Mining Act

Mining �culture�:1970�s: Zambia was the World�s largest Copper exporter

Mining provides 85% offoreign exchange

Politics:Stable, multi-party democracy

Equinox has a very constructive relationship with the Government

Unfortunate death of President Mwanawasa

Election 0n 30 October

English language + law

Modern Mining Act

Mining �culture�:1970�s: Zambia was the World�s largest Copper exporter

Mining provides 85% offoreign exchange

Zambia Tax IssuesZambia Tax IssuesHistory of Tax Concessions:

Implemented in mid-1990s � early-2000sCopper prices < $0.60/lb meant mines losing money � privatization process

But since Copper prices jumped in 2003:Operating mines have made massive profitsThis created the political imperative for �a better return to the Zambian people�

Tax Package introduced April 2008:30% Corporate Tax � 3% RoyaltyVariable Profits Tax � Windfall Profits Tax (Cu prices >$2.50/lb)Reduced capital write down � 25% per year

However, Equinox has a Development Agreement (�DA�)Legally binding DA signed in Dec 2005 (already high Copper prices)Lumwana is �greenfields� development � unlike other mines that acquired existing operations and infrastructureEquinox has not been making �windfall profits� � it has been investing $800mZambian Government recognises that Lumwana is different

The terms of the Equinox DA have been applied to date and the Government continues to do so

History of Tax Concessions:Implemented in mid-1990s � early-2000sCopper prices < $0.60/lb meant mines losing money � privatization process

But since Copper prices jumped in 2003:Operating mines have made massive profitsThis created the political imperative for �a better return to the Zambian people�

Tax Package introduced April 2008:30% Corporate Tax � 3% RoyaltyVariable Profits Tax � Windfall Profits Tax (Cu prices >$2.50/lb)Reduced capital write down � 25% per year

However, Equinox has a Development Agreement (�DA�)Legally binding DA signed in Dec 2005 (already high Copper prices)Lumwana is �greenfields� development � unlike other mines that acquired existing operations and infrastructureEquinox has not been making �windfall profits� � it has been investing $800mZambian Government recognises that Lumwana is different

The terms of the Equinox DA have been applied to date and the Government continues to do so

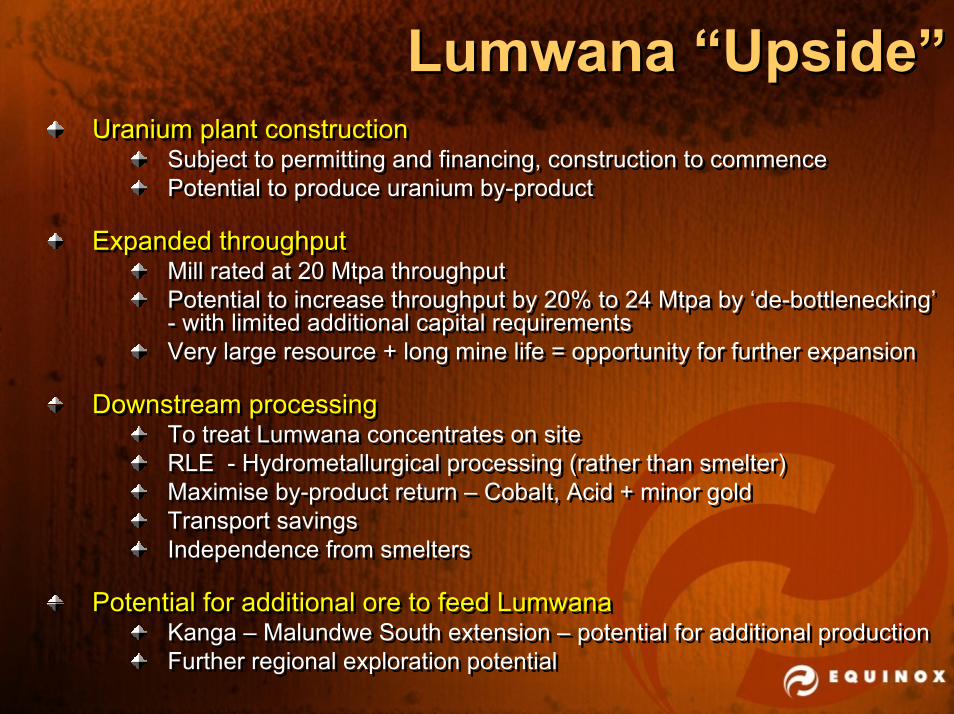

Lumwana �Upside�Lumwana �Upside�Uranium plant construction

Subject to permitting and financing, construction to commence Potential to produce uranium by-product

Expanded throughputMill rated at 20 Mtpa throughputPotential to increase throughput by 20% to 24 Mtpa by �de-bottlenecking�- with limited additional capital requirementsVery large resource + long mine life = opportunity for further expansion

Downstream processingTo treat Lumwana concentrates on siteRLE - Hydrometallurgical processing (rather than smelter)Maximise by-product return � Cobalt, Acid + minor goldTransport savingsIndependence from smelters

Potential for additional ore to feed LumwanaKanga � Malundwe South extension � potential for additional productionFurther regional exploration potential

Uranium plant constructionSubject to permitting and financing, construction to commence Potential to produce uranium by-product

Expanded throughputMill rated at 20 Mtpa throughputPotential to increase throughput by 20% to 24 Mtpa by �de-bottlenecking�- with limited additional capital requirementsVery large resource + long mine life = opportunity for further expansion

Downstream processingTo treat Lumwana concentrates on siteRLE - Hydrometallurgical processing (rather than smelter)Maximise by-product return � Cobalt, Acid + minor goldTransport savingsIndependence from smelters

Potential for additional ore to feed LumwanaKanga � Malundwe South extension � potential for additional productionFurther regional exploration potential

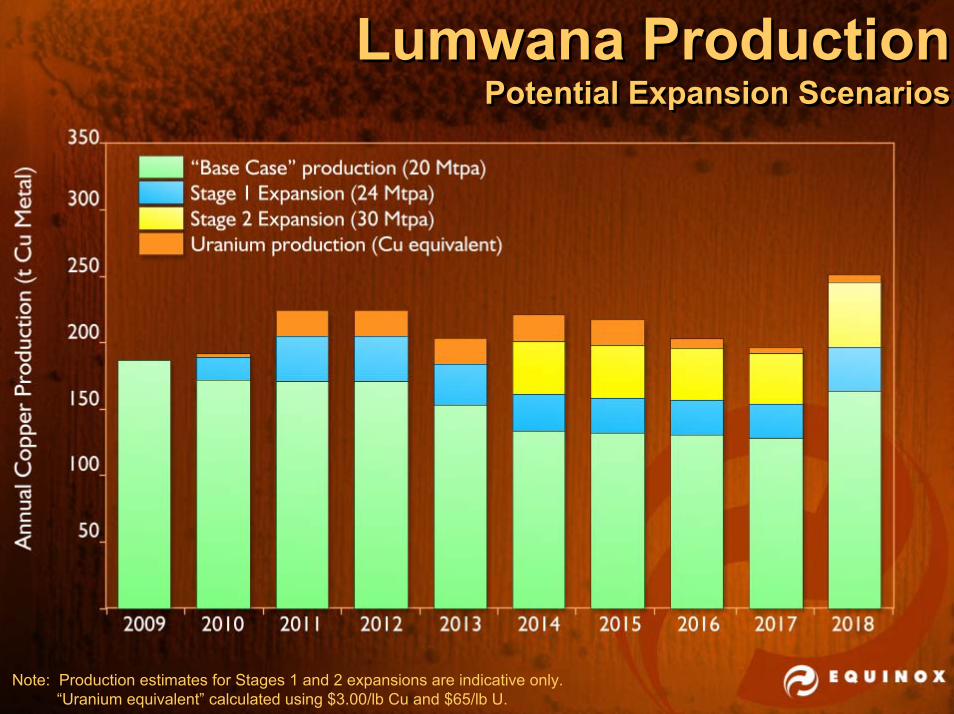

Lumwana ProductionPotential Expansion Scenarios

Lumwana ProductionPotential Expansion Scenarios

Note: Production estimates for Stages 1 and 2 expansions are indicative only.�Uranium equivalent� calculated using $3.00/lb Cu and $65/lb U.

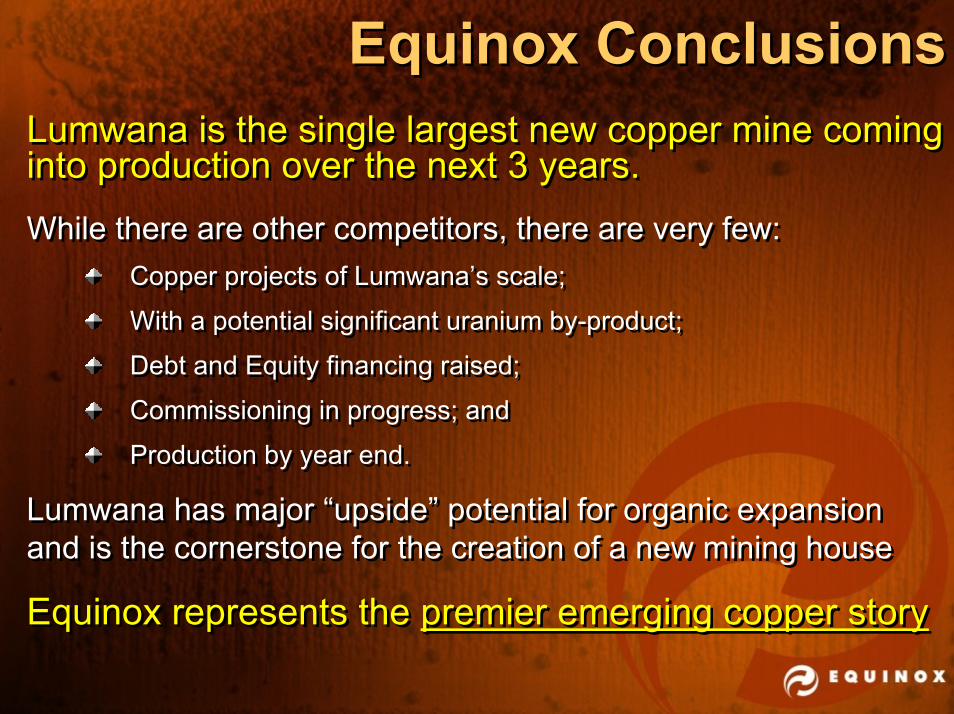

Equinox ConclusionsEquinox ConclusionsLumwana is the single largest new copper mine coming into production over the next 3 years.While there are other competitors, there are very few:

Copper projects of Lumwana�s scale;

With a potential significant uranium by-product;

Debt and Equity financing raised;

Commissioning in progress; and

Production by year end.

Lumwana has major �upside� potential for organic expansionand is the cornerstone for the creation of a new mining house

Equinox represents the premier emerging copper story

Lumwana is the single largest new copper mine coming into production over the next 3 years.While there are other competitors, there are very few:

Copper projects of Lumwana�s scale;

With a potential significant uranium by-product;

Debt and Equity financing raised;

Commissioning in progress; and

Production by year end.

Lumwana has major �upside� potential for organic expansionand is the cornerstone for the creation of a new mining house

Equinox represents the premier emerging copper story

![Rectified Financial Results for March 31, 2015 [Result]](https://img.pdfslide.us/doc/110x75/577cb42d1a28aba7118c566e/rectified-financial-results-for-march-31-2015-result.jpg)

![Rectified Financial Results for March 31, 2016 [Result]](https://img.pdfslide.us/doc/110x75/577c79551a28abe05492461b/rectified-financial-results-for-march-31-2016-result-577f241f289b8.jpg)