Embed Size (px)

Citation preview

Commercial Association of REALTORS® Wisconsin

Tom McGeePresident & CEOICSC

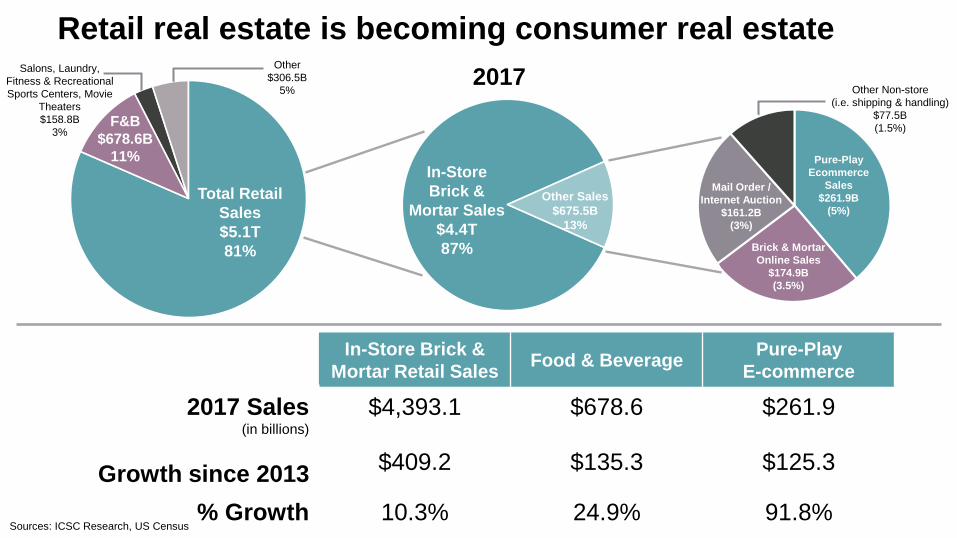

In-Store Brick &

Mortar Sales$4.4T87%

Other Sales$675.5B

13%

Brick & MortarOnline Sales

$174.9B(3.5%)

Pure-Play Ecommerce

Sales$261.9B

(5%)

Mail Order / Internet Auction

$161.2B(3%)

Other Non-store (i.e. shipping & handling)

$77.5B(1.5%)

Retail real estate is becoming consumer real estate

In-Store Brick & Mortar Retail Sales Food & Beverage Pure-Play

E-commerce

2017 Sales(in billions)

$4,393.1 $678.6 $261.9

Growth since 2013 $409.2 $135.3 $125.3

% Growth 10.3% 24.9% 91.8%

Salons, Laundry, Fitness & Recreational Sports Centers, Movie

Theaters$158.8B

3%

Total Retail Sales$5.1T81%

F&B$678.6B

11%

Other$306.5B

5%2017

Sources: ICSC Research, US Census

Technology Omnichannel E-Commerce Customer Engagement

Major global trends impacting our industry

Consumer Personalization

Demographics

Experience Value

Baby Boomers Millennials Urban Density

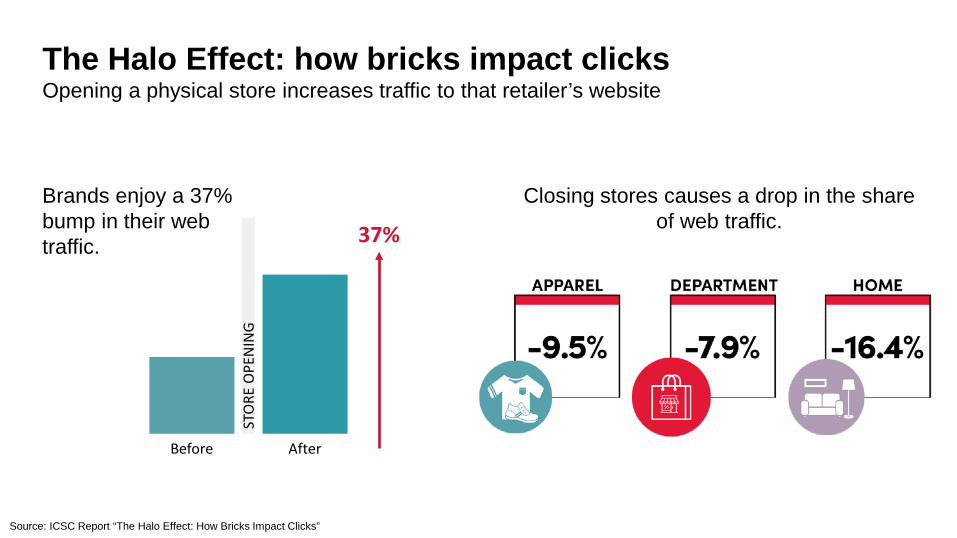

The Halo Effect: how bricks impact clicksOpening a physical store increases traffic to that retailer’s website

Source: ICSC Report “The Halo Effect: How Bricks Impact Clicks”

STO

RE O

PEN

ING

Before After

37%

Brands enjoy a 37% bump in their web traffic.

Closing stores causes a drop in the share of web traffic.

69%

31%Used for Store Expansion

Used for Other Expenses

Omnichannel is coming to lifeNearly 75% of multi-channel retailers are more profitable than their pureplay counterparts

Stated Purpose for Most Recent VC Funding RoundSurvey of VC-backed “evolved pureplay” retailers

Actual Stores

2016 2017 20225 25 100

Planned

Sources: L2: Death of Pureplay Retail

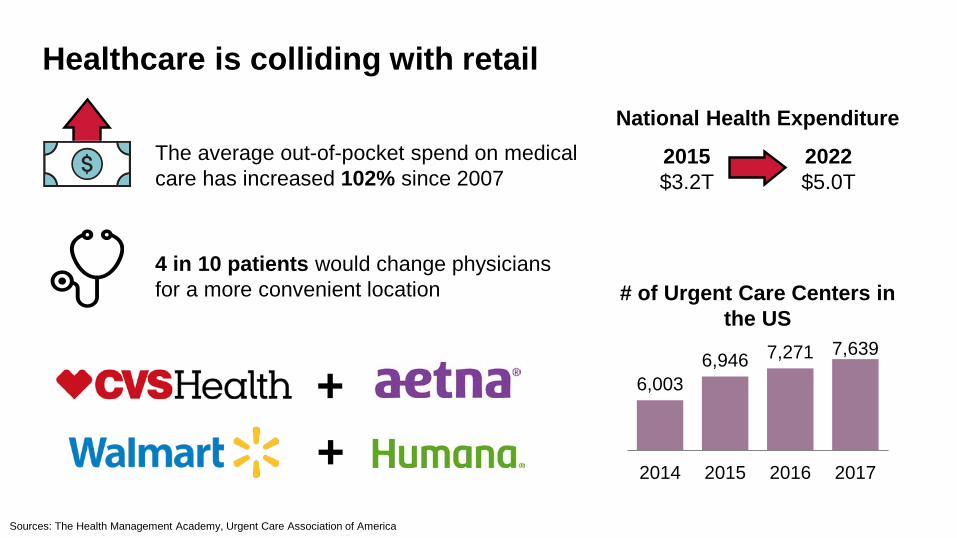

Healthcare is colliding with retail

Sources: The Health Management Academy, Urgent Care Association of America

# of Urgent Care Centers in the US

6,0036,946 7,271 7,639

2014 2015 2016 2017

4 in 10 patients would change physicians for a more convenient location

2015 2022$3.2T $5.0T

National Health ExpenditureThe average out-of-pocket spend on medical care has increased 102% since 2007

++

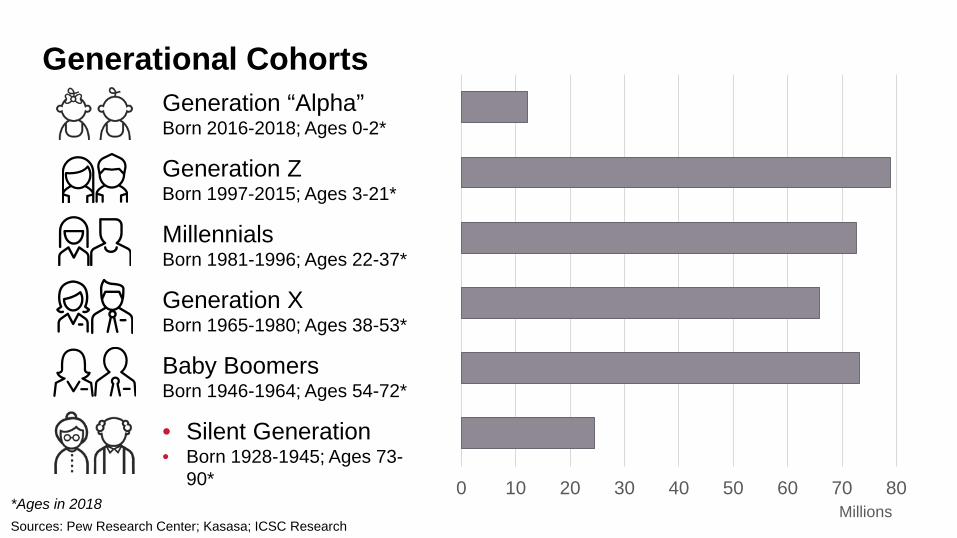

Generational Cohorts

• Silent Generation• Born 1928-1945; Ages 73-

90*

Sources: Pew Research Center; Kasasa; ICSC Research*Ages in 2018

Generation XBorn 1965-1980; Ages 38-53*

Baby Boomers Born 1946-1964; Ages 54-72*

Generation Z Born 1997-2015; Ages 3-21*

MillennialsBorn 1981-1996; Ages 22-37*

Generation “Alpha” Born 2016-2018; Ages 0-2*

0 10 20 30 40 50 60 70 80Millions

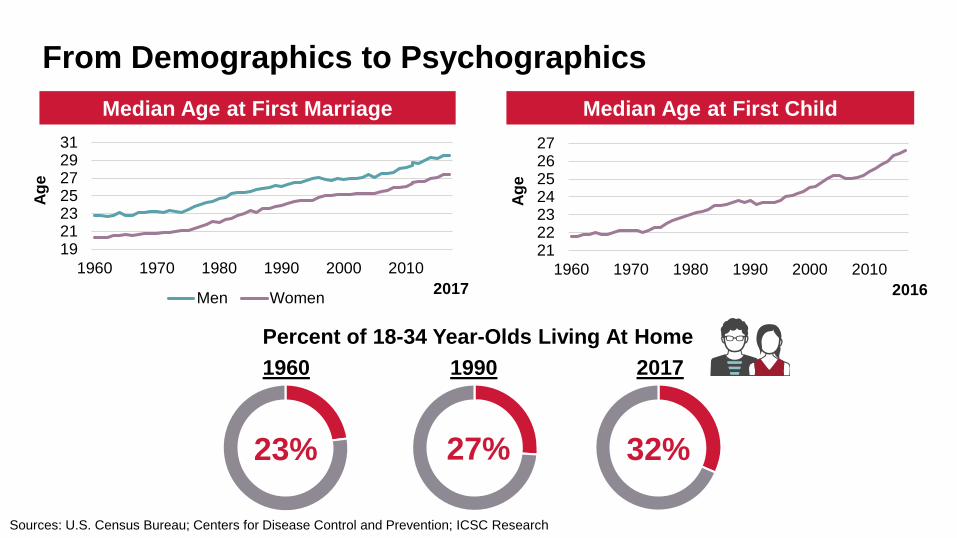

From Demographics to Psychographics

19212325272931

1960 1970 1980 1990 2000 2010

Age

Men Women 2017

Sources: U.S. Census Bureau; Centers for Disease Control and Prevention; ICSC Research

21222324252627

1960 1970 1980 1990 2000 2010

Age

2016

23%

Median Age at First Marriage

32%

1960 2017

27%

1990Percent of 18-34 Year-Olds Living At Home

Median Age at First Child

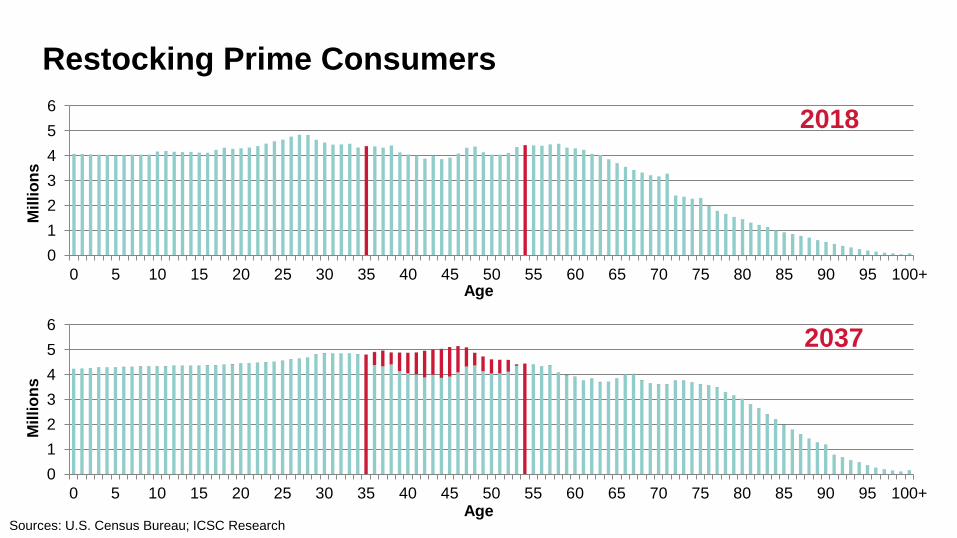

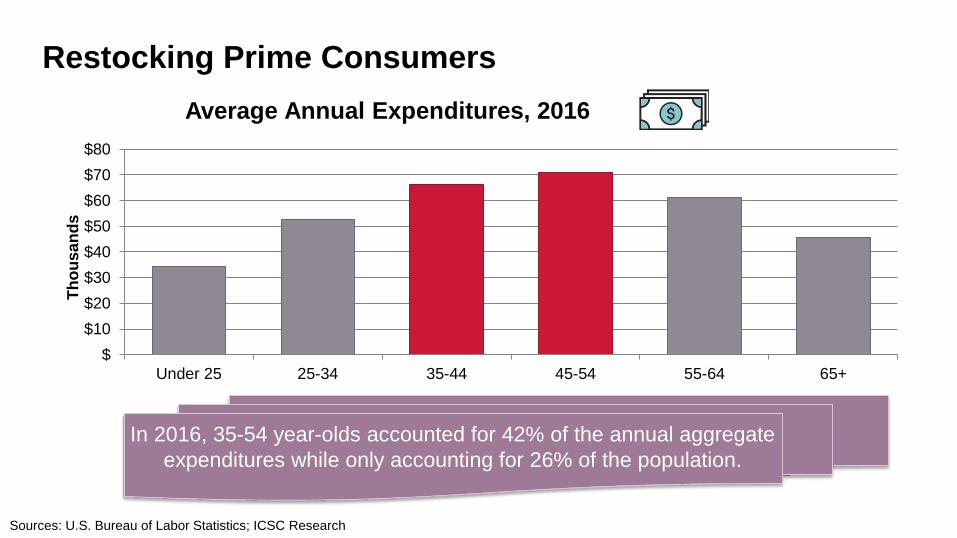

Restocking Prime Consumers

0123456

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100+

Mill

ions

2018

0123456

0 5 10 15 20 25 30 35 40 45 50 55 60 65 70 75 80 85 90 95 100+

Mill

ions

2037

Sources: U.S. Census Bureau; ICSC Research

Age

Age

Restocking Prime Consumers

$$10$20$30$40$50$60$70$80

Under 25 25-34 35-44 45-54 55-64 65+

Thou

sand

s

Average Annual Expenditures, 2016

Sources: U.S. Bureau of Labor Statistics; ICSC Research

In 2016, 35-54 year-olds accounted for 42% of the annual aggregate expenditures while only accounting for 26% of the population.

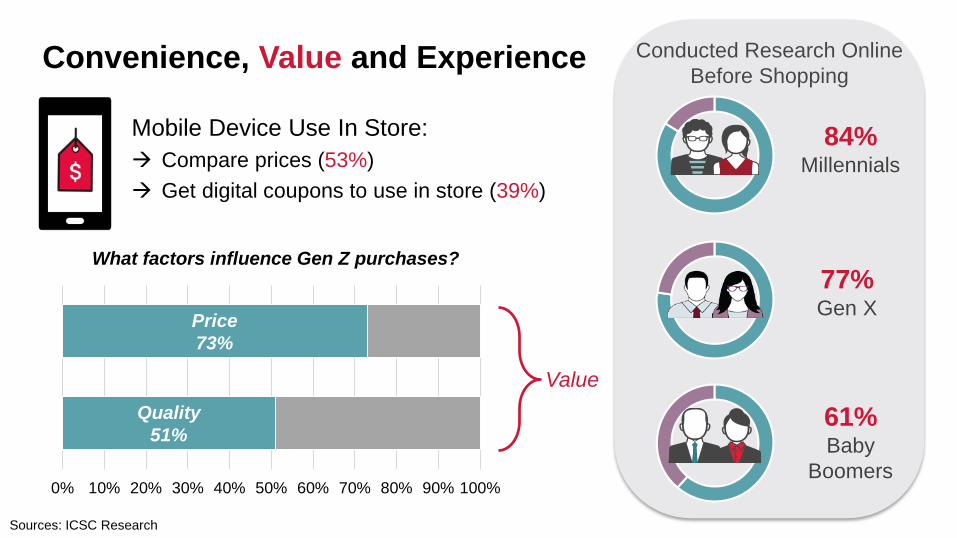

Convenience, Value and Experience

Sources: ICSC Research

Conducted Research Online Before Shopping

84%Millennials

77%Gen X

61%Baby

Boomers0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

What factors influence Gen Z purchases?

Quality51%

Price73%

Value

Mobile Device Use In Store: Compare prices (53%) Get digital coupons to use in store (39%)

37.3%35.3%

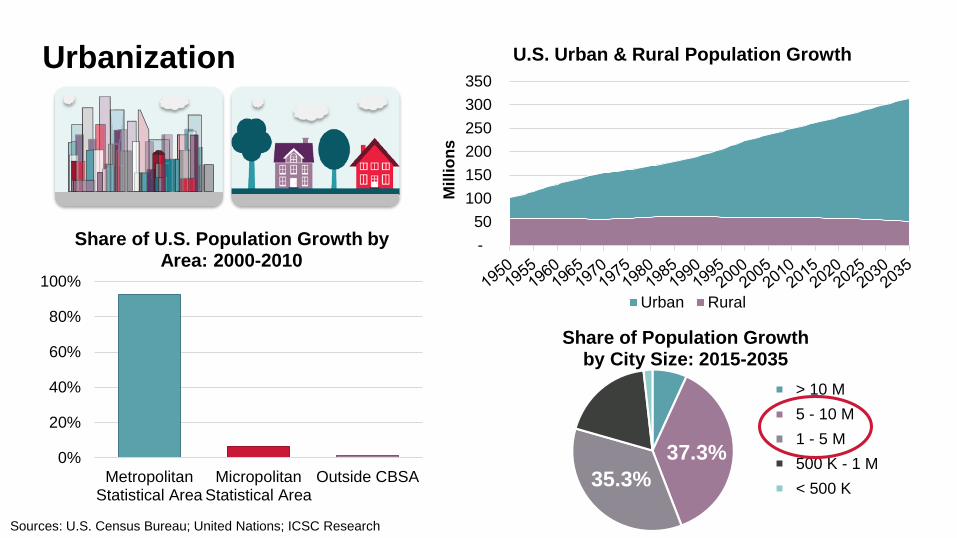

Share of Population Growth by City Size: 2015-2035

> 10 M 5 - 10 M 1 - 5 M 500 K - 1 M < 500 K

Urbanization

- 50

100 150 200 250 300 350

Mill

ions

U.S. Urban & Rural Population Growth

Urban Rural

0%

20%

40%

60%

80%

100%

MetropolitanStatistical Area

MicropolitanStatistical Area

Outside CBSA

Share of U.S. Population Growth by Area: 2000-2010

Sources: U.S. Census Bureau; United Nations; ICSC Research

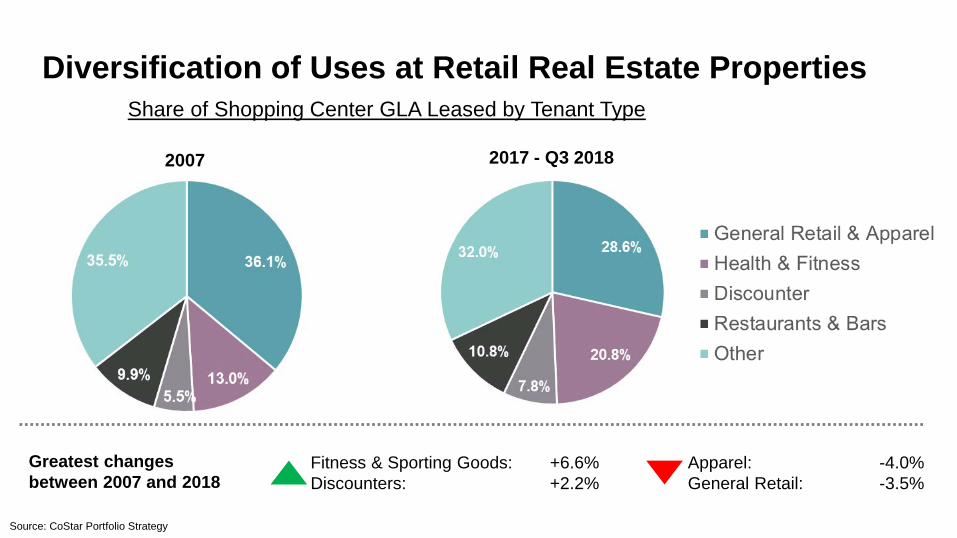

2007 2017 - Q3 2018

Share of Shopping Center GLA Leased by Tenant Type

Diversification of Uses at Retail Real Estate Properties

Source: CoStar Portfolio Strategy

Greatest changes between 2007 and 2018

Fitness & Sporting Goods: +6.6%Discounters: +2.2%

Apparel: -4.0% General Retail: -3.5%

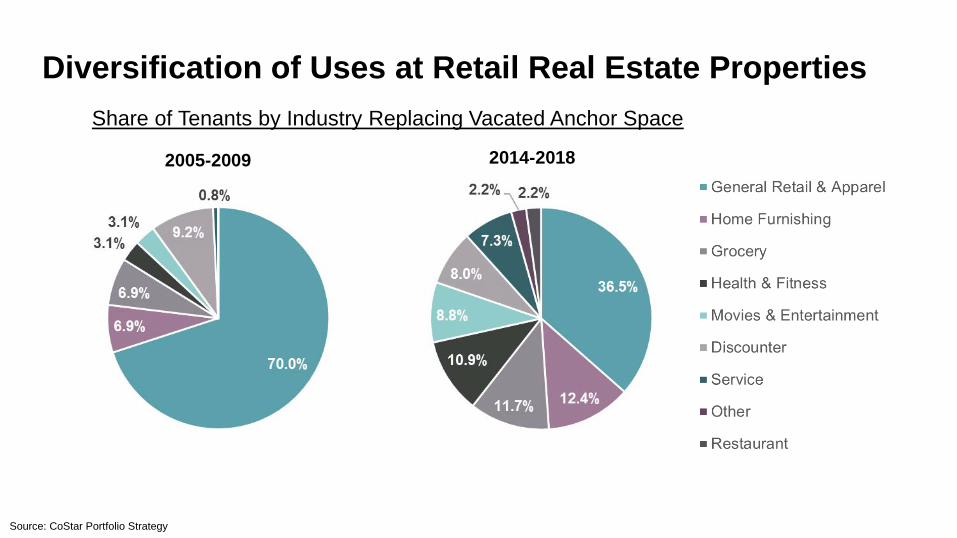

Share of Tenants by Industry Replacing Vacated Anchor Space

Diversification of Uses at Retail Real Estate Properties

2005-2009 2014-2018

Source: CoStar Portfolio Strategy

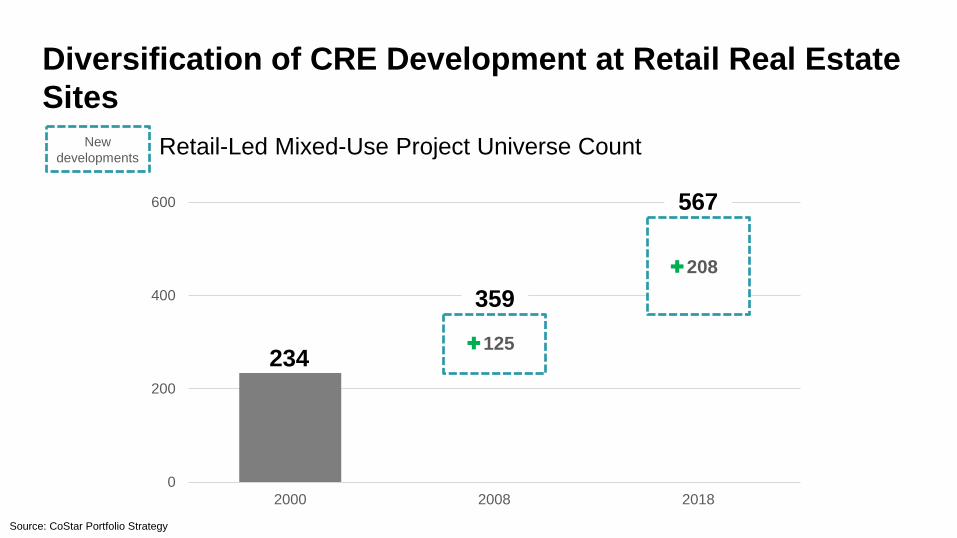

Diversification of CRE Development at Retail Real Estate Sites

0

200

400

600

2000 2008 2018

125

208

234

359

567

New developments

Source: CoStar Portfolio Strategy

Retail-Led Mixed-Use Project Universe Count

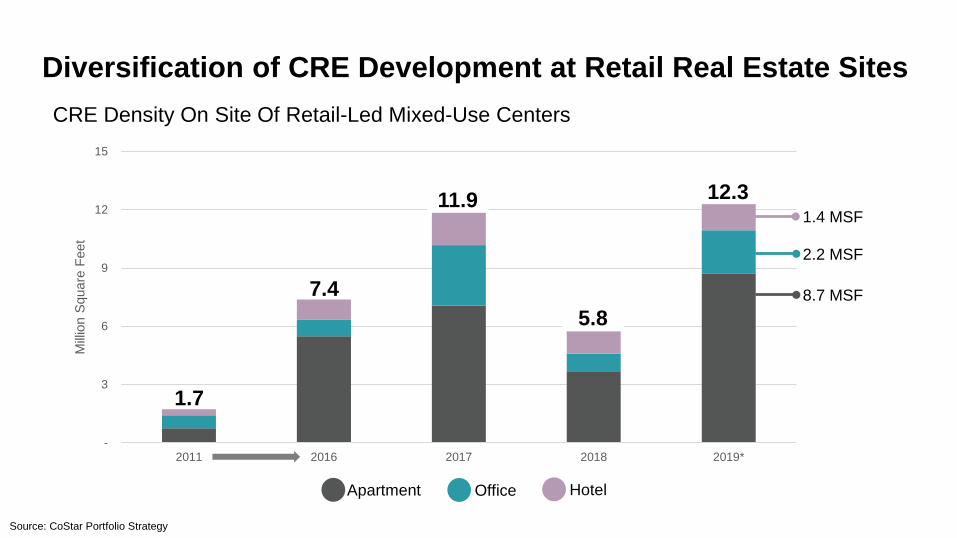

Diversification of CRE Development at Retail Real Estate Sites

Source: CoStar Portfolio Strategy

-

3

6

9

12

15

2011 2016 2017 2018 2019*

Milli

on S

quar

e Fe

et

CRE Density On Site Of Retail-Led Mixed-Use Centers

1.4 MSF

2.2 MSF

8.7 MSF

1.7

12.3

7.4

11.9

5.8

Apartment Office Hotel

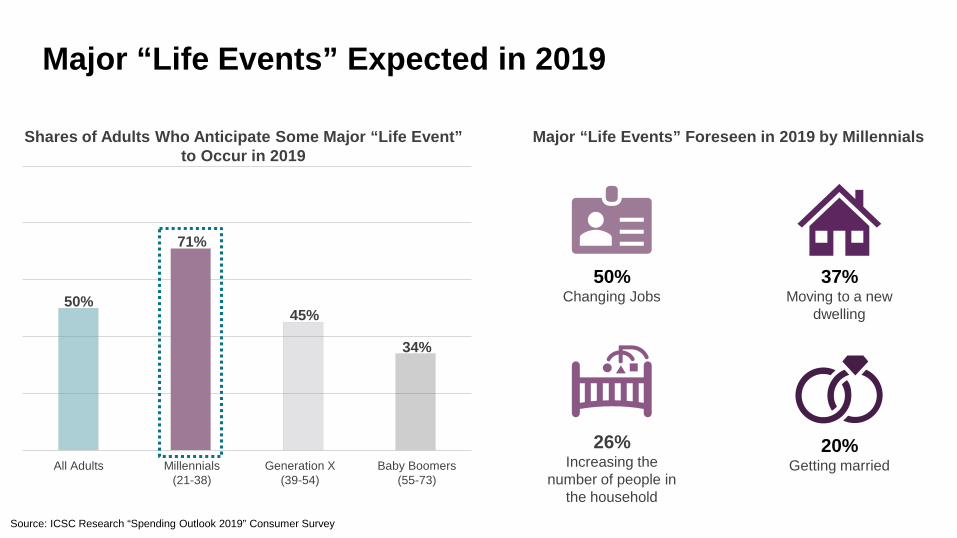

Major “Life Events” Expected in 2019

Shares of Adults Who Anticipate Some Major “Life Event” to Occur in 2019

Source: ICSC Research “Spending Outlook 2019” Consumer Survey

50%

71%

45%

34%

All Adults Millennials(21-38)

Generation X(39-54)

Baby Boomers(55-73)

Major “Life Events” Foreseen in 2019 by Millennials

50%Changing Jobs

37%Moving to a new

dwelling

26%Increasing the

number of people in the household

20%Getting married

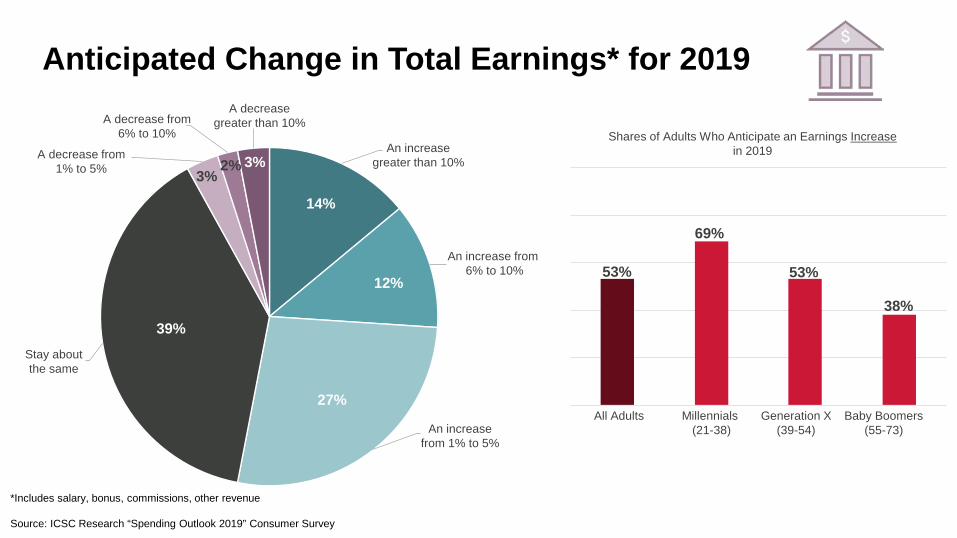

An increase grea 10%

An

An incre

me

rom 1% to 5%

decrease from 6% to 10%

10%

Anticipated Change in Total Earnings* for 2019A decrease

greater than 10%

An increase greater than 10%

An increase from6% to 10%

An increase from 1% to 5%

39%

A decrease from 1% to 5%

A decrease from 6% to 10%

14%

12%

27%

3%2% 3%

All Adults Millennials(21-38)

Generation X(39-54)

Baby Boomers (55-73)

53%

69%

53%

38%

Shares of Adults Who Anticipate an Earnings Increasein 2019

*Includes salary, bonus, commissions, other revenue

Source: ICSC Research “Spending Outlook 2019” Consumer Survey

Stay about the same

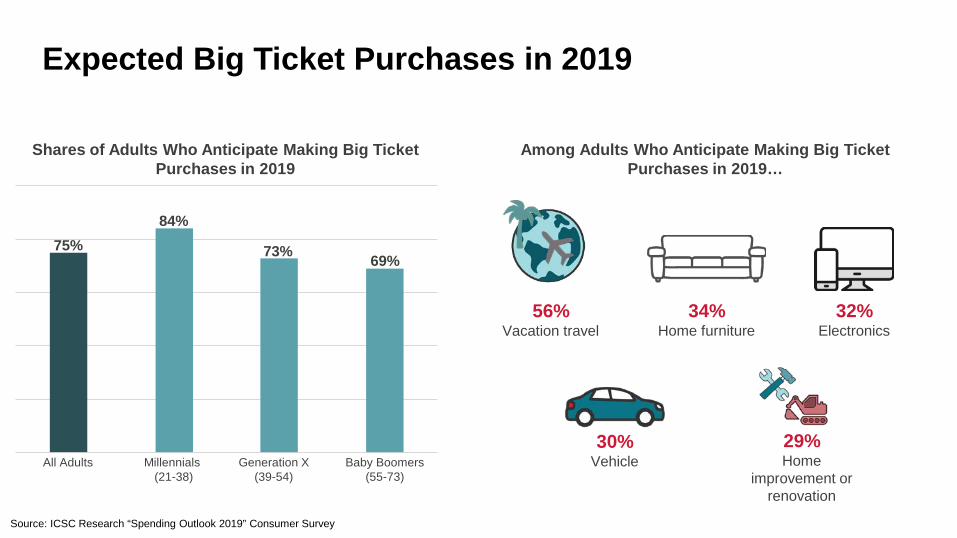

Expected Big Ticket Purchases in 2019

34%Home furniture

32%Electronics

30%Vehicle

29%Home

improvement or renovation

All Adults Millennials(21-38)

Generation X(39-54)

Baby Boomers (55-73)

75%84%

73% 69%

Shares of Adults Who Anticipate Making Big Ticket Purchases in 2019

Source: ICSC Research “Spending Outlook 2019” Consumer Survey

Among Adults Who Anticipate Making Big Ticket Purchases in 2019…

56%Vacation travel