Embed Size (px)

Citation preview

8000 Towers Crescent Drive Suite 1200

Tysons Corner, Virginia 22182 703.442.1400

www.kippsdesanto.com

Commercial Aerospace Maintaining Altitude

Fall 2018

2

Commercial Aerospace Maintaining Altitude Fall 2018

Aerospace M&A Valuations and Activity Maintaining Altitude The aerospace industry is experiencing near record high valuations and increased deal volume in mergers and acquisitions (“M&A”) due to the favorable state of the current sector fundamentals. The four factors driving these developments are (i) robust demand, (ii) remarkable backlogs in commercial aerospace, (iii) accelerating production schedules, and (iv) pressure to consolidate to reduce costs and strengthen competitiveness. Therefore, aerospace company owners must consider the positive state of the M&A market as they weigh their alternatives on how to optimize the company’s competitive positioning and maximize value. Excellent Aerospace Industry Fundamentals First, the aerospace sector is experiencing an unprecedented expansion. Air traffic demand, defined as revenue passenger kilometers (“RPKs”), has steadily increased and the growth is accelerating. The chart below depicts demand over the past 13 years. After sprinting from 3.6 billion to 4.6 billion RPKs from 2004 to 2008, RPKs declined 1.2% during the Great Recession. The market quickly compensated for this decline. The sector returned to robust growth, experiencing a compounded annual growth rate (“CAGR”) of 6.8% from 2009 to 2017. Moreover, this CAGR has continued to accelerate over the past three years reaching 7.6% from 2014 to 2017. Strong demand has translated into sustainable growth.

Revenue Passenger Kilometers: Systemwide — Global

(billions)

As a result of these exceptional growth rates, it is not surprising that demand has led to record backlogs for Airbus and Boeing. At current production rates, the OEMs have eight years of backlog. The chart below illustrates the phenomenal backlog growth experienced by Boeing and Airbus from 2009 to 2014. Although Boeing experienced a slight decline in its backlog from 2009 to 2014, the combined backlog continued to expand from 2014 to 2017.

3,6133,934

4,2064,538 4,647 4,591

4,9585,271

5,5505,867

6,2196,679

7,1737,754

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

8,000

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

3

Commercial Aerospace Maintaining Altitude Fall 2018

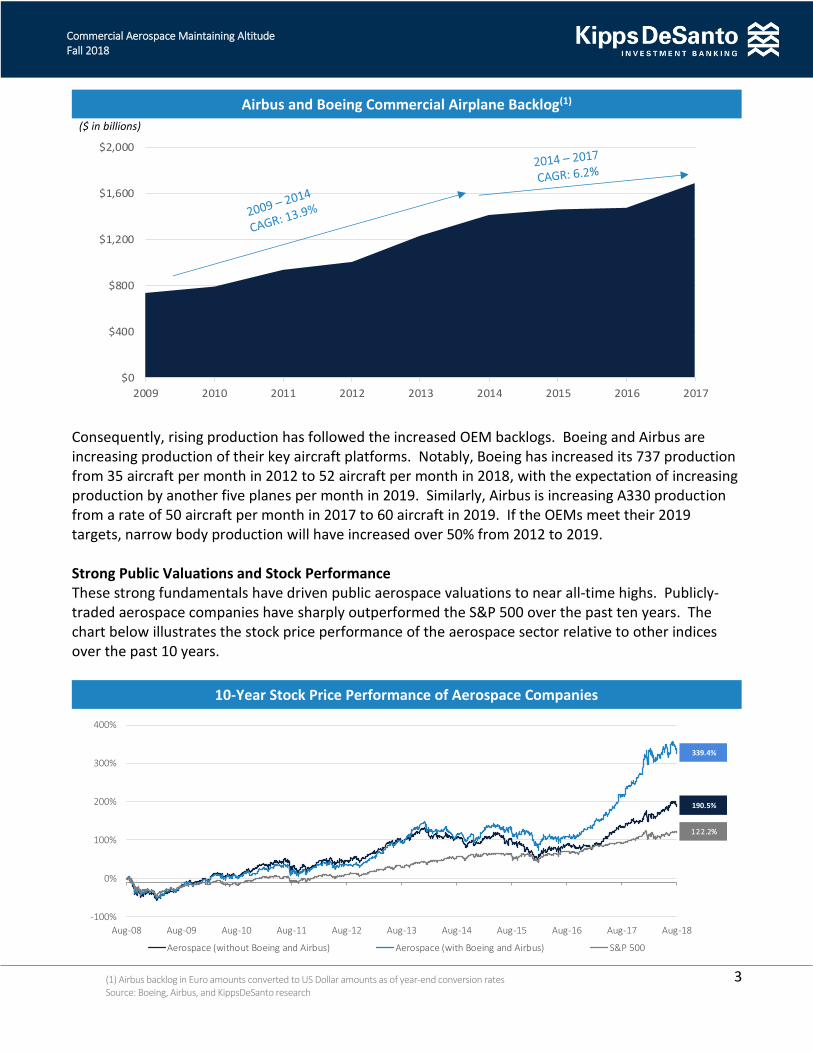

Airbus and Boeing Commercial Airplane Backlog(1)

($ in billions)

Consequently, rising production has followed the increased OEM backlogs. Boeing and Airbus are increasing production of their key aircraft platforms. Notably, Boeing has increased its 737 production from 35 aircraft per month in 2012 to 52 aircraft per month in 2018, with the expectation of increasing production by another five planes per month in 2019. Similarly, Airbus is increasing A330 production from a rate of 50 aircraft per month in 2017 to 60 aircraft in 2019. If the OEMs meet their 2019 targets, narrow body production will have increased over 50% from 2012 to 2019. Strong Public Valuations and Stock Performance These strong fundamentals have driven public aerospace valuations to near all-time highs. Publicly-traded aerospace companies have sharply outperformed the S&P 500 over the past ten years. The chart below illustrates the stock price performance of the aerospace sector relative to other indices over the past 10 years.

10-Year Stock Price Performance of Aerospace Companies

$0

$400

$800

$1,200

$1,600

$2,000

2009 2010 2011 2012 2013 2014 2015 2016 2017

339.4%

190.5%

122.2%

-100%

0%

100%

200%

300%

400%

Aug-08 Aug-09 Aug-10 Aug-11 Aug-12 Aug-13 Aug-14 Aug-15 Aug-16 Aug-17 Aug-18

Aerospace (without Boeing and Airbus) Aerospace (with Boeing and Airbus) S&P 500

(1) Airbus backlog in Euro amounts converted to US Dollar amounts as of year-end conversion rates Source: Boeing, Airbus, and KippsDeSanto research

4

Commercial Aerospace Maintaining Altitude Fall 2018

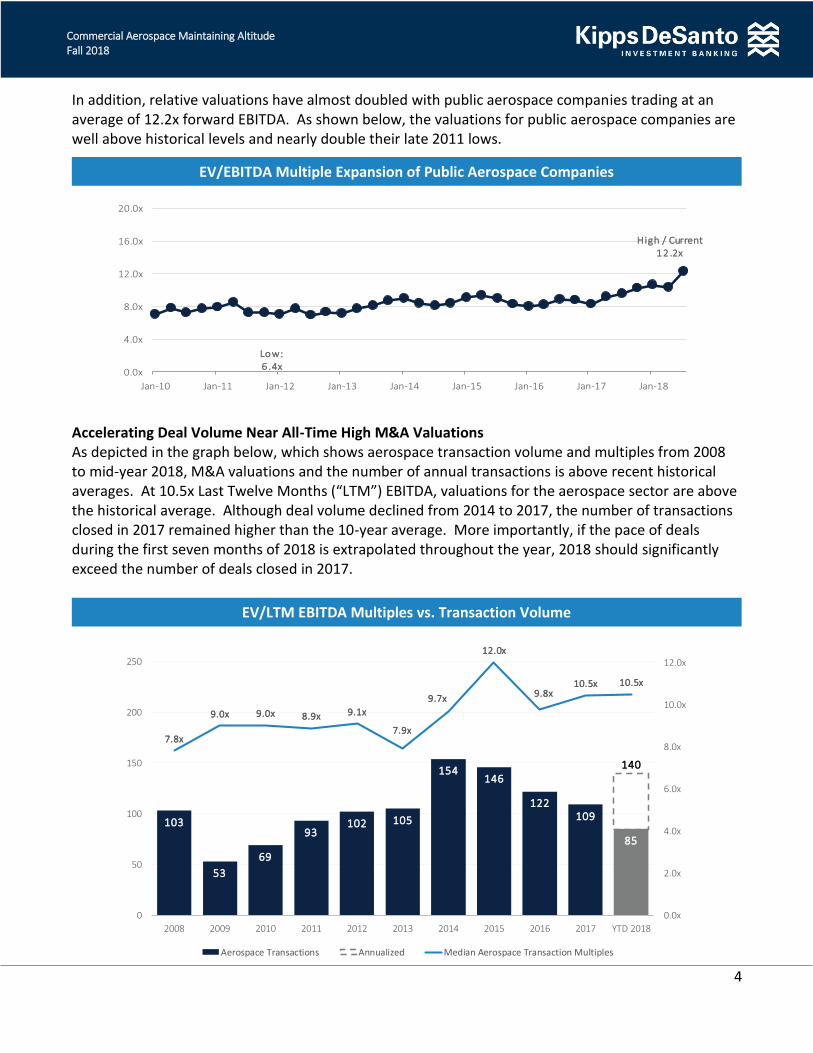

In addition, relative valuations have almost doubled with public aerospace companies trading at an average of 12.2x forward EBITDA. As shown below, the valuations for public aerospace companies are well above historical levels and nearly double their late 2011 lows.

EV/EBITDA Multiple Expansion of Public Aerospace Companies

Accelerating Deal Volume Near All-Time High M&A Valuations As depicted in the graph below, which shows aerospace transaction volume and multiples from 2008 to mid-year 2018, M&A valuations and the number of annual transactions is above recent historical averages. At 10.5x Last Twelve Months (“LTM”) EBITDA, valuations for the aerospace sector are above the historical average. Although deal volume declined from 2014 to 2017, the number of transactions closed in 2017 remained higher than the 10-year average. More importantly, if the pace of deals during the first seven months of 2018 is extrapolated throughout the year, 2018 should significantly exceed the number of deals closed in 2017.

EV/LTM EBITDA Multiples vs. Transaction Volume

Low:6 .4x

High / Current12.2x

0.0x

4.0x

8.0x

12.0x

16.0x

20.0x

Jan-10 Jan-11 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Jan-18

103

53

69

93102 105

154146

122109

85

140

7.8x

9.0x 9.0x 8.9x 9.1x

7.9x

9.7x

12.0x

9.8x10.5x 10.5x

0.0x

2.0x

4.0x

6.0x

8.0x

10.0x

12.0x

0

50

100

150

200

250

2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 YTD 2018

Aerospace Transactions Annualized Median Aerospace Transaction Multiples

5

Commercial Aerospace Maintaining Altitude Fall 2018

Transformative Deals are Re-Shaping the Market The leading aircraft OEMs and Tier I suppliers are significantly altering the competitive landscape. With the Embraer joint venture, Boeing expands its position within the narrow body aircraft category and becomes a leader within the regional jet market. Boeing also acquired KLX in May to expand its presence in supply chain management, building upon its acquisition of Aviall in 2006. The Airbus tie up with Bombardier regarding the C-Series was a catalyst for making the Boeing/Embraer joint venture a reality. Of course, Airbus gained control of the C-Series aircraft without making a cash investment. Furthermore, United Technologies Corporation (“UTC”), as well as Safran, are consolidating Tier I suppliers with the purchases of Rockwell Collins and Zodiac Aerospace, respectively. Also, Spirit Aerosystems is leading its own Tier I consolidation with the acquisition of ASCO. Essentially, the aerospace market is undergoing a critical transformation that emphasizes consolidation of the supplier base to eliminate unnecessary costs and enhance the long-term viability of each successor organization. The chart below highlights several of the most impactful deals over the past two years.

Select Recent Deals Greater than $500 million in Transaction Value

Date Announced Buyer Target EV ($M)

EV / EBITDA Rationale

July 2018 $4,750 NA

Footprint in regional jets

June 2018

$1,389 NA Aviation services

platform

May 2018

$540 NA Aviation sustainment

platform

May 2018

$650 NA Consolidate Tier I

supplier

May 2018 $4,159 14.7x

Expands supply chain management

March 2018

$12,332 9.3x Untapped potential

Sept 2017

$30,192 16.0x Consolidate Tier I

supplier

Jan 2017 $9,228 24.1x

Consolidate Tier I supplier

Oct 2016

$8,600 14.1x Consolidate Tier I

supplier

Vertex Aerospace

6

Commercial Aerospace Maintaining Altitude Fall 2018

Middle Market M&A Transactions are the Sweet Spot of Activity Although the large deals receive most of the headlines, the middle market continues to lead M&A deal volume. As the pie chart indicates, 95% of deals in the aerospace and defense sector are less than $500mm in transaction size. Consolidation of the Middle Market Includes Multiple Buy and Build Strategies The chart below highlights ten deals from the past several months of companies that are deploying a buy and build strategy in the aerospace market. Eight of the ten deals were financed by private equity groups and the deals range from metal processing and precision machining manufacturers to Maintenance, Repair and Overhaul (“MRO”) providers to aircraft interiors manufacturers. No matter the sub-sector within aerospace, there is a group of acquirers aiming to consolidate the market.

Select Recent Deals in the Middle Market

Date Announced Buyer Target Target Description

September 2018 Lynwood, CA

Provides metal finishing on parts up to 110 ft in length and 14 feet in

width / depth

July 2018

Provides proprietary aftermarket replacement components and complementary repair services

July 2018

Provides MRO services and supply chain management to fixed and

rotary-wing aircraft

July 2018

Provides metal alloy-based manufacturing services for the

A&D sector

July 2018

Manufactures aircraft interior products for the business jet

market

July 2018

Provides inventory management and aircraft components for

commercial aircraft and engines

July 2018

Provides manufacturing of titanium castings and machined aircraft

components

June 2018

Provides flight data recorders, ground support equipment, and

electronics manufacturing

May 2018

Provides manufacturing of precision machined parts from

metals for the aerospace industry

March 2018

Precision Aerospace Group provides complex parts and

assemblies for commercial A&D applications

2018 Transaction by Deal Size As of August 10, 2018

< $15M6%

$15M -$100M

81%

$100M -$500M

8%

> $500M5%

7

Commercial Aerospace Maintaining Altitude Fall 2018

Industry Participants are Actively Acquiring Aerospace Companies Private equity groups and their portfolio companies are actively acquiring aerospace and defense businesses – PE involvement represents almost 40% of deal activity in the aerospace market. In addition, many of these groups are serial acquirers with multiple platforms. Some of the most active PE firms in the sector include Acorn Growth Companies, AE Industrial Partners, Arlington Capital, and Liberty Hall Partners, while groups such as Blackstone, The Carlyle Group, GenNx360, JLL Partners, and Trive Capital also maintain a presence. In all, there are more than 100 PE firms with one or more portfolio companies focused in the aerospace market. However, strategics are not ready to be outdone by PE firms. In 2017, UTC acquired Rockwell Collins, itself among the more active acquirers of aerospace companies. The market has also witnessed European aerostructures companies, such as Sonaca and Aernnova, purchase U.S. platforms to expand their presence with Boeing. Furthermore, Transdigm has remained aggressive in the space, recently adding Skandia to its portfolio, as it continues to acquire approximately three companies annually. Other key acquirers in the sector include AAR Corp, CIRCOR, Curtiss Wright, Ducommun, HEICO, Heroux-Devtek, and L-3 Technologies. These strategic buyers actively utilize M&A as a way of acquiring new customers and capabilities, while also improving their relative importance within the supply chain. Decisionmakers are Optimistic About the Future The KippsDeSanto 2018 M&A Survey has several interesting findings regarding market optimism. Generally, respondents expressed a favorable sentiment about the U.S. economy, M&A activity in the commercial aerospace sector, and the stability and growth of the commercial aerospace market.

✓ 95% of respondents are optimistic about U.S. economic growth

✓ 98% expect aerospace M&A activity to remain the same as 2017 or increase by more than 5%

✓ 82% anticipate a stable or growing commercial aerospace market

o Remarkably, 5% of the respondents indicated that the commercial aerospace market is

no longer cyclical, noting; “Cycle? What Cycle? Cycles are dead.”

Not surprisingly, given record setting economic expansion, years-long backlog, and ramp-up in air traffic demand, respondents expressed a favorable perspective about commercial aerospace M&A. Current Market Conditions Afford Shareholders / Owners a Great Opportunity to Maximize Value In essence, the current market affords shareholders and owners a great opportunity to maximize value. As summarized above, fundamentals are excellent and have led to record valuations. The velocity of transactions has remained robust and recent indicators suggest this may accelerate. Consolidation amongst large Tier I suppliers is occurring at a quick pace and, in turn, putting more downward pressure on the supply base to consolidate. Consequently, middle market deals are the most active segment of the market and are supported by significant interest from both private equity firms and strategics alike. And, amongst strategic acquirers, both domestic and international buyers remain active. In summary, all M&A signals lead to positive trends for the aerospace industry. Authors: Warren Romine, Managing Director, KippsDeSanto & Co. Brian Tunney, Vice President, KippsDeSanto & Co. Alexia Marchetta, Associate, KippsDeSanto & Co.

8

Commercial Aerospace Maintaining Altitude Fall 2018

Select Recent KippsDeSanto & Co. Advised Transactions

9

Commercial Aerospace Maintaining Altitude Fall 2018

5

About KippsDeSanto & Co.

KippsDeSanto is an investment banking firm focused on delivering M&A and financing expertise. Our solutions are focused on the sectors we know – aerospace / defense and government technology solutions. We are recognized for our depth of industry experience, knowledge of sector-specific transaction drivers, and long-standing relationships with industry participants.

We welcome the opportunity to have a more detailed discussion of developments in our focus industries. For more information, please contact us:

Warren Romine Managing Director [email protected] Brian T. Tunney Vice President [email protected] Alexia N. Marchetta Associate [email protected]

Connect with KippsDeSanto:

The information and opinions in this newsletter were prepared by KippsDeSanto & Co. and the information herein is believed to be reliable and has been obtained from and based upon public sources believed to be reliable. KippsDeSanto & Co. makes no representation as to the accuracy or completeness of such information. Opinions, estimates, and analyses in this newsletter constitute the current judgment of the author as of the date of this newsletter. They do not necessarily reflect the opinions of KippsDeSanto & Co. and are subject to change without notice. This newsletter is meant to impart general knowledge about a sector or industry and is not expected to provide reasonably sufficient information upon which to make any investment decisions. KippsDeSanto & Co. is not affiliated with any of the companies identified in this newsletter. Unless otherwise described, the companies identified are also not affiliated with one another. This newsletter may contain information obtained from third parties. Reproduction and distribution of third party content in any form is prohibited except with the prior written permission of the related third party. Third party content providers do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. Third party content providers give no express or implied warranties, including, but not limited to, any warranties of merchantability or fitness for a purpose or use. Third party content providers shall not be liable for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequential damages, costs, expenses, legal fees, or losses (including lost income or profits and opportunity costs or losses caused by negligence) in connection with any use of their content, including ratings.

8000 Towers Crescent Drive Suite 1200

Tysons Corner, Virginia 22182 703.442.1400

www.kippsdesanto.com