Embed Size (px)

Citation preview

BrianWilliamson

Nextgenerationcommunications&thelevelplayingfield–whatshouldbedone?

June2016

[1]

Acknowledgement&DisclaimerThisisanindependentreportfundedbyCCIA.

Theopinionsofferedhereinarepurelythoseoftheauthor.TheydonotnecessarilyrepresenttheviewsofCCIA,noracorporateviewofCommunicationsChambers.

AbouttheAuthorBrianWilliamsonisaPartneratCommunicationChambersandhasextensivepolicyandstrategyexperienceinrelationtoapplications,networksandradiospectrum.Hehasworkedonthebenefitsof,andpolicyinrelationto,mobileappsandtheinternet.

[2]

Contents1. ExecutiveSummary...............................................................................................................................3

2. Towardsanextgenerationcommunicationsmarket.............................................................5Broadbandgoesmainstream 5Rapidadoptionofnextgenerationcommunications 5Transitiontonextgenerationbroadband 6Pricecompetition&tariffrebalancing 6Innovationandnewfeatures 7Unbundlingofnetworks,apps&devices 8Openmessaginginitiatives 9Integrationofmessagingintootherapplications 9Messagingasaplatform 9Whatnext? 10Conclusion 10

3. Isthereafree-riderproblem?........................................................................................................12Nextgenerationnetworks&communicationsarecomplements 12Poor performance by some operators is not due to next generationcommunications 12Therehasnotbeenavaluetransferfromnetworkstoapplications 13Datagrowthissustainable 15Messagingappprovidershaveinvestedinconnectivity 16Conclusion 17

4. Alevelplayingfield–butwhichfield&whatlevel?............................................................18Frameworkforanalysis 18Issuebyissueanalysis 20Fromspecifictogeneral 25Policyimplications 26Conclusion 29

5. Nextgenerationcommunications-helpingcompletethesinglemarket....................30

[3]

1. ExecutiveSummaryThispaperarguesthatthefocusofsectorspecificexantetelecomsregulationshouldbenarrowedtoaccessbottleneckswithfreedomtoinnovateandcompeteforallinthecommunicationsappsmarket,thatthetermthe‘levelplayingfield’hasnopracticalapplicationandthatnextgenerationcommunicationsappsareevolvingrapidly.

Some have argued that next generation communications apps(including voice, messaging, video and other forms ofcommunication)freerideonnetworksandbenefitfromregulatoryasymmetries. We address these questions, concluding that nextgenerationcommunicationsappsdonotfreeride,ingeneraldonotbenefit from regulatory asymmetries and suffer some competitivedisadvantagesduetoalackofverticalintegration.

Next generation communications,far from free riding, stimulateswillingness to pay for nextgeneration networks. The userbenefitsaresubstantial,anditisnota zero-sum game, with networkoperators who adapt seeingrevenuegrowth.

Apps including Skype, WhatsApp,iMessage, Google Hangouts andFacebook Messenger includefeatures such as no cross-bordercharges, interoperability acrossnetworks includingWi-Fi, presence, group chat, video calling andphotosharing.

Next generation communications apps also help those withdisabilitiestocommunicateusingsignlanguageandtexttospeech.TheyhelptobreakdownlanguagebarrierswithlivevoicetranslationinSkypeanda“Taptotranslate”featureinAndroid;andareseeingadoptionbyenterprise,particularlySMEs.

Regarding the level playing field, legacy communications enjoyadvantages over next generation communications apps includingaccess tomanagednetworkcapacityand2Gcoverage, integrationwith the default calling “app”, numbering based interoperability,emergencycallingandbundlingundercontracts.Theseadvantagesstem from vertical integration and standards. We are, however,neitherproposingthattheseadvantagesberemovednorextendedtoothers.

Avirtuouscirclecontributingtodigitalsinglemarketgoals

Smartdevices

Nextgeneration

communicationsapps(pan-European)

Nextgenerationnetworks

[4]

Ontheotherhand,a rangeofsector-specific regulationapplies tolegacy services which does not apply to next generationcommunications. However, such regulation is not in generalapplicable to next generation communications for the followingreasons.

Anobligationmaybeneutralbutnextgenerationcommunicationsmay not fallwithin its scope. Fees for licenced spectrum apply toanyone holding licenced spectrum, which next generationcommunication app providers in general do not. Other examplesincludeprovisionsrelatingtocontractsandnumberportability.

Therationaleforagivenregulatoryobligationmaynotapplytonextgenerationcommunications.Obligationsthatapplytoaccessandnotappsfallwithinthiscategory,includingaspectsofuniversalservice.

Problems in relation to market power may be unique to legacyservices. These include call termination and roaming, neither ofwhichariseinrelationtonextgenerationcommunications.However,to theextent thatnextgeneration communicationsapps competewithlegacyservices,therationaleforsomeregulationmayfallaway.

The balance of costs and benefits of an obligation may differ.Emergencycalling isanexample.Whilst inprinciple itmight seemlogical to extend this obligation to all communication services thecostsofdoingso,andtheriskofconsumerconfusionandthereforeharm,raiseseriousdoubtsregardingextension.

Consideringtheabove,alevelplayingfieldintermsofregulationisnotahelpfulgeneralguidingprincipleforpolicy.AsNERAnotedinapaperforGSMA,afunctionality-basedapproachtoregulationshouldrecognise that “differences in technology may require differentregulatorytreatmenttoachieveacommonobjective.”

There are no clean lines between apps in general andcommunicationsapps.Communicationshasbeenincorporatedintoa wide range of apps such as games, social networks includingLinkedInande-commerceincludinge-Bay.Communicationsapps,forexampleWeChat,arealsobecomingplatformsforotherapps.

Thevibrancyofnextgenerationcommunicationsisdowntofreedomto innovate. Extension of regulation to next generationcommunications would chill European innovation in thedevelopmentanduseofrapidlyevolvingapps.Instead,anobjectiveand problem driven approach to regulation should be adopted.Ratherthanextendingexanteregulationtothebroadermessagingenvironment,andbyextensionappsingeneral,thefocusofexanteregulationshouldbenarrowedtonetworkaccessbottlenecks.

[5]

2. Towardsanextgenerationcommunicationsmarket

Fourbroadshiftsareunderwayinthecommunicationsmarket:

• A shift to broadband, which isalmostcomplete

• Smart device adoption which ismainstreaming mobilebroadband and promises to liftinternetadoption

• Apps (including communicationsapps)have taken-off -drivenbyinnovative features, smartdevices,appstoresandwirelessnetworks

• A transition to next generationaccess - 4G, 5G, improvedWi-Fiandmore fibre - drivenbyappsincludingmessaging.

Broadbandgoesmainstream

Broadbandaccessandtheinternetopenedupthepotentialfornextgenerationcommunicationsapplications.Duringthedecadeto2014,fixed broadband adoption rose from 15% to just over 70% ofhouseholds in Europe. By 2015 individual smartphone adoptionexceeded household broadband adoption, and a number ofhouseholdsweresmartphoneonly.

Rapidadoptionofnextgenerationcommunications

Skype,aEuropeanstart-upfoundedin2003,startedasaPCandfixedbroadband application. By 2013 Skype had international voiceminutesequaltoalmost40%oftheentireconventionalinternationaltelecom market.1 Skype subsequently offered video calling andotherservices.

Coupledwiththeadventofappsstoresfrom2008,thesmartphonephenomenonhaspropelledinnovationandgrowthintheappmarketand innextgenerationcommunications.2 Forexample,WhatsApppassedthe500millionand1billionusermilestonesinApril2014andFebruary 2016 respectively3; whilst by 2016 FacebookMessenger

1WSJ,Skype’sIncredibleRise,inOneImage,January2015.2Williamson,ChanandWood,Apolicytoolkitfortheappeconomy-whereonlinemeetsoffline,March2016.3WhatsApp,Onebillion,February2016.

Figure1:Avirtuouscirclecontributingtodigitalsinglemarketgoals

Smartdevices

Nextgeneration

communicationsapps(pan-European)

Nextgenerationnetworks

[6]

andWhatsAppcarried60billionmessagesaday,threetimesmorethanSMS.4

Smartphoneadoptioncontinuestogrowandisexpectedtoconvergewithmobileadoptionby2020.5Coupledwithongoinginnovationinrelation to next generation communications apps, andimprovementsintheperformanceandavailabilityof4GandWi-Fi,thiswillcontinuetopropelgrowthinmessagingapps.

Transitiontonextgenerationbroadband

Fixednetworksareundergoingaprogressiveupgrade with fibre closer to, or to, thepremise (or mobile site) and higher speedtechnologies over copper including VDSL,G.FastandcableDOCSIS3/3.1.

Mobile networks are undergoing aprogressive upgrade aswell with improvedcoverage,highercapacityandmoreefficientand capable technologies including 4G(Figure2)andtheprospectof5G.

Innovation and investment in nextgeneration access networks is driven byconsumer use of rich applications including next generationcommunicationsapplications (legacyvoiceandtextdonotrequiresuchinvestmentsincetheyoperateoverbasicfixedaccessand2Gmobile networks). Improved 4G coverage will stimulate furtheradoptionanduseofnextgenerationcommunications.

Pricecompetition&tariffrebalancing

Somehavearguedthatgrowthinnextgenerationcommunicationshas been driven largely by arbitrage, the opportunity to undercutexistingtelecomsservicetariffstructures.Forexample,theOECD:7

“VoIP largely exists because it exploits arbitrageopportunities. If itwere a cheaperway todeliver callswewould expect mobile networks to have adopted itthemselves.”

4TheVerge,MessengerandWhatsAppprocess60billionmessagesaday,threetimesmorethanSMS,April2016.5Asymco,WhenwilltheEuropeanUnionFivereachsmartphonesaturation?,2013.6EuropeanCommission,DigitalAgendaScoreboard[accessed17April2016]7OECD,WorkingPartyNo.2onCompetitionandRegulation,June2011.

Figure2:Mobile4Gavailability(%households)6

0102030405060708090100

2011 2012 2013 2014 2015

[7]

Networksare,ofcourse,adopting internetprotocolwith telecomsundergoinga transition to “All-IP”8. VoIP is alsoaboutmore thanarbitrage,andnextgenerationcommunicationsisaboutmuchmorethanVoIP.

At least initially, the price differential between next generationcommunications and legacy telecoms services contributed to thegrowth of the former. The differential was most pronounced inrelationtocrossbordercommunicationandroaming.

In these areas next generation communications introducedcompetitionwhere it wasweakest, helped alignmessaging priceswith incremental costs (close to zero) and contributed to thecompletionofthedigitalsinglemarketinEurope.

Telecoms operators have, over time, rebalanced their tariffstructures towardsaccessanddataandaway fromvoiceandSMS(withanumberofmobileplansincludingunlimitedvoiceandSMS).

Innovationandnewfeatures

Rapid innovation continues in relation to next generationcommunicationsapps.ConventionalstandardsbasedvoiceandSMShavefailedtokeeppace(themobileindustryis,however,promotingrich communication services (RCS) and Google have announcedsupportforRCSinAndroid9).

Examples of innovation and features provided by next generationcommunicationsappsinclude:

• Newmessaging features including group calling and chat,presence,videocalling,videoandphotosharing.

• Extensions beyond communication including locationsharingandsendingandreceivingmoney.

• Theuseofformsofidentityotherthanatelephonenumbercanbeconvenientandpreserveprivacy,forexample,whenmessagingwithinaplatformsuchaseBay.

• TheabilitytocommunicateoverarangeofdevicesincludingPCs, tablets, games consoles and music players withoutaccesstovoiceandSMSservices;andoveravarietyofformsofconnectivityincludingfixed,cellularandWi-Fi.

• Accessibility features including Apple ‘Voice Over’ (an OSlevel feature) which describes what is on the screen,

8LightReading,DTCompletesAll-IPMoveinCroatia,2015.http://www.lightreading.com/ethernet-ip/new-ip/dt-completes-all-ip-move-in-croatia/d/d-id/7196169GSMA,Globaloperators,GoogleandtheGSMAalignbehindadoptionofrichcommunicationsservices,February2016.

[8]

Facebook‘automaticalternativetext’10whichusesartificialintelligence toprovideabasicdescriptionofwhat is in animage, andGoogle Hangouts Captionswhich provides livevoicetranscription.Videoalsofacilitatessignlanguage.11

• Language translation of text and voice with live voicetranslation in Skype Translator and a cross-app “Tap totranslate”featureinAndroid.12

• Developmentof features, including collaboration, financialservice data compliance exports and security, tailored toenterpriseuse.13

• FireChatutilisesmeshnetworking to supportmessaging inthe absence ofWi-Fi or cellular coverage. ‘FireChat alerts’allows emergency services to send alerts even if cellularserviceisnotavailable.14

TheabovedevelopmentshaverequiredR&Dandinvestmentbynextgeneration communications providers. The consumer andenterprisebenefitsaresubstantial.

Unbundlingofnetworks,apps&devices

The rise of network independent applications including nextgenerationcommunicationsisaformof“unbundling”,thoughasarulenextgenerationcommunicationsappshaveco-existedalongsidelegacyvoiceandSMS (with theexceptionofuseondevicesotherthanmobilephonessuchastablets,musicplayersetc).

FreedomPop,amobile“phone”serviceoriginatingintheUSandnowavailable in the UK, operates as an MVNO.15 FreedomPop take“unbundling” further, offering free data connectivity and amessagingappwhichoperatesoveradataconnection,ratherthansupportforthestandardpre-installedcallingapp.

Next generation communications may therefore pave the way tobusinessmodelsthatdonotinvolveverticalintegrationorbundlingofmessaging, devices andnetworks. Thesedevelopments raise aquestionovertheclaimthatlegacyservicesaredisadvantaged,sincethey are typically integrated by default into devices and networkserviceofferstotheexclusionofothercompetingservices,whereasnextgenerationcommunicationsisnot.

10Facebook,UsingArtificialIntelligencetoHelpBlindPeople‘See’Facebook,April2016.11Quartz,AstartupfromIsraelhasaccidentallycreated“WhatsAppforthedeaf”,April2015.12Googleblog,Translatewhereyouneedit:inanyapp,offline,andwhereveryouseeChinese,May2016.13TheEconomist,TheSlackgeneration-Howworkplacemessagingcouldreplaceothermissives,May2016.14TheVerge,Thisappletsrescueworkerssendofflinealertswhendisasterstrikes,May2016.15http://uk.freedompop.com/uk?experience=organic.default

[9]

Openmessaginginitiatives

Next generation communications have developed rapidly viaindividual appswhich competewith another, and seek to identifyunmetnichesinthemarket. It isuptodeveloperstodecidewhatplatformstheysupport,sonotallappsareavailableonallplatforms.

Anopensourceinitiative,OpenWebRTC,isbringingnextgenerationcommunications support to browsers on a cross platform basis.16ChromeandFirefoxsupportWebRTC,andsupportisindevelopmentforWebKit – theopen-sourcewebbrowser engineusedbyAppleSafariandotherbrowsers.17

There is also an Ericsson initiative,18 in collaborationwithGoogle,thatallowsmobileoperatorsto'connect'tomultipleinternetbasedplayerstodelivernewservicestousers.Theservicestrivestobridgethegapbetweenoperatornetworksandinternetbasedapplications,potentiallyincludingnextgenerationcommunicationsservices.

Integrationofmessagingintootherapplications

Messaging has also expanded well beyond standalone messagingapplicationsandisembeddedintomanyotherapplicationsincludinggames, e-commerce platforms, peer-to-peer transportation andaccommodation services, business collaboration platforms, socialnetworks including LinkedIn and even baby monitors. Nextgeneration communications have enabled this extension sincemessaging is just another internet based application that can beaddedandintegratedintootherapplications.

Messagingasaplatform

Notonlydootherapplicationscomewithmessaging,butmessagingapplicationsarebecomingplatformsforotherapplications.

WeChat is an example of a messaging app with a developedecosystemofadditionalservices.19Byearly2015,WeChathad549millionmonthly active users. Alongwith its basic communicationfeatures,WeChatusersinChinacanaccessanarrayofservicesvia“appswithinanapp”. The lightweightappsonWeChatarecalled“officialaccounts”andtherearewellover10millionoftheseontheplatform.Thecornerstoneofthismodelispayments.

16http://www.openwebrtc.org17https://webkit.org/status/#specification-webrtc18Ericsson,Ericssonlaunches"OTTCloudConnect"serviceformobileoperators,February2016.19JeanPaulSimon,Howtocatchaunicorn,2016.

[10]

Facebookhave also set out an ambition to turnMessenger into adiverse platform.20 Messaging is a basic and familiar form ofinteraction that, coupledwithmachine intelligence, can provide anew formsofuser interfaceandaplatform forappsdevelopmentand integration. FacebookMessenger is now a platform for otherservices,includingUber.21

Whatnext?

We can observe current innovation, including use of messagingacross applications and efforts to turn messaging apps intoplatforms.Beyondthat,wearenotsure.Asoneobserverputit:22

“Thecoreissueacrossallofthis,Ithink,ishowmuchisstilltotally unsettled. We spent 20 years in which themainstreaminternetexperiencewasawebbrowser,mouseandkeyboard,andoveradecadeinwhichGooglewastheway you navigated. Smartphones ended all that, but wehaven'tsettledonanewmodel,andtheideawe'llallrevertback to the comfortable, simplemodel of theweb seemsincreasinglyremote.Evenwithinmessaging,themodelisstillinflux.Iwroteaboveaboutthesearchfornewpsychologies,buttherearedeeperarchitecturalquestionsthananonymityor filters, which you can see in SnapChat's disappearingmessagesorMeerkatandPeriscope'suseoflive.Whatwillthenextblow-upmodelbe - synchronousornot?One toone or one to many? Feed based or thread-based?Algorithmic filter or endless stream? Rich client or richmessage?Runtimeordeeplinks?”

Whatisclearisthatweshouldletinnovation,whichhasdeliveredsomuch already, continue. It is also clear that this is not theenvironmentsectorspecificexantetelecommunicationsregulationwasdesignedtoaddress.Ratherthanextendingexanteregulationto the broadermessaging environment, and by extension apps ingeneral,weshouldnarrowthefocusofexanteregulationtonetworkaccessbottlenecks.

Conclusion

Next generation communications continue to innovate and grow,even where legacy services are now free as part of a bundle.

20Wired,FacebookMessenger:insideZuckerberg'sappforeverything,October2015.21Facebook,MessengerPlatformatF8,April2016.22BenedictEvans,Messagingandmobileplatforms,March2015.

[11]

Innovation,ratherthanarbitrage,istheunderlyingdriverofgrowthinnextgenerationcommunications.

Next generation communications are also increasingly integratedinto other applications, and is itself becoming a platform forapplications.Therearenocleanlinesbetweenappsingeneralandmessaging.

TheEUelectroniccommunications frameworkshouldbeamendedto support continued innovation and the complementarydevelopmentofnetworksandapplications, an issue considered indetailinSection4.

[12]

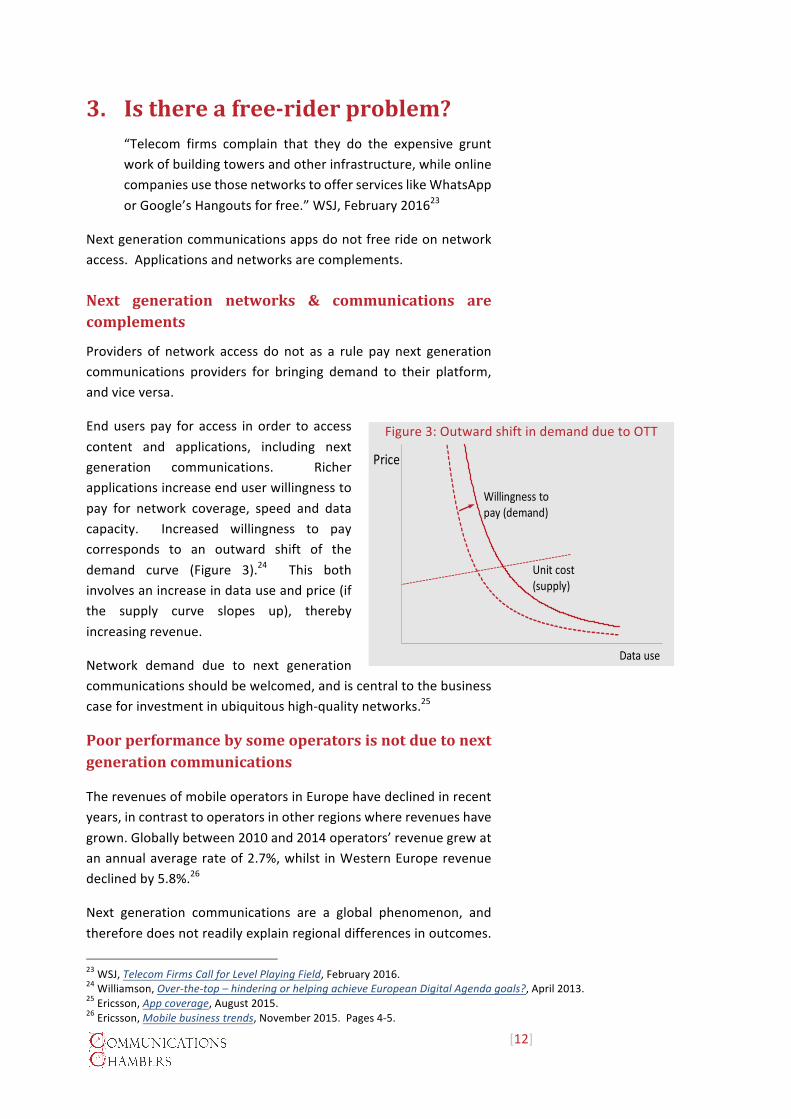

3. Isthereafree-riderproblem?“Telecom firms complain that they do the expensive gruntworkofbuildingtowersandotherinfrastructure,whileonlinecompaniesusethosenetworkstoofferserviceslikeWhatsApporGoogle’sHangoutsforfree.”WSJ,February201623

Nextgenerationcommunicationsappsdonotfreerideonnetworkaccess.Applicationsandnetworksarecomplements.

Next generation networks & communications arecomplements

Providers of network access do not as a rule pay next generationcommunications providers for bringing demand to their platform,andviceversa.

Enduserspay for access inorder to accesscontent and applications, including nextgeneration communications. Richerapplicationsincreaseenduserwillingnesstopay for network coverage, speed and datacapacity. Increased willingness to paycorresponds to an outward shift of thedemand curve (Figure 3).24 This bothinvolvesanincreaseindatauseandprice(ifthe supply curve slopes up), therebyincreasingrevenue.

Network demand due to next generationcommunicationsshouldbewelcomed,andiscentraltothebusinesscaseforinvestmentinubiquitoushigh-qualitynetworks.25

Poorperformancebysomeoperatorsisnotduetonextgenerationcommunications

TherevenuesofmobileoperatorsinEuropehavedeclinedinrecentyears,incontrasttooperatorsinotherregionswhererevenueshavegrown.Globallybetween2010and2014operators’revenuegrewatanannualaveragerateof2.7%,whilst inWesternEuroperevenuedeclinedby5.8%.26

Next generation communications are a global phenomenon, andthereforedoesnotreadilyexplainregionaldifferencesinoutcomes.

23WSJ,TelecomFirmsCallforLevelPlayingField,February2016.24Williamson,Over-the-top–hinderingorhelpingachieveEuropeanDigitalAgendagoals?,April2013.25Ericsson,Appcoverage,August2015.26Ericsson,Mobilebusinesstrends,November2015.Pages4-5.

Figure3:OutwardshiftindemandduetoOTT

Price

Datause

Willingnesstopay(demand)

Unit cost(supply)

[13]

Indeed, to the extent that next generation communications hasdriven smartphone adoption and data growth, it is likely to havecontributed to revenue growth for those operators who haveadapted.Globallymobiledatarevenuegrewatanannualaveragerateof34percentbetween2010and2014,drivenbydemandforaccesstoapplicationsonthemove.

Factors depressing revenue growth in Europe may include thedelayed release of spectrum and 4G deployment (which offersimproved service quality coupled with lower unit costs) and thefinancialcrisisandrecession,whichhasbeendeepandprolongedinEurope. AstudybyIDATEforEricssonandQualcommalsoarguedthat policy is insufficiently focused on long-term investment inEurope.27

Operators’ results suggest a turnaroundmaynowbeunderway inEurope. Vodafone reported for Q4 2015 that eight out of 13Europeanmarketswerebacktogrowth.28Vodafonenotedthattheimprovement “reflects a combination of our commercialperformanceandstrongdatausage”.

Therehasnotbeenavaluetransfer fromnetworkstoapplications

In addition to theargument thatnext generation communicationsfree rides on networks it has been argued that the value chain is‘broken’, that value has been transferred from networks toapplicationsprovidersandthatafundamentalchangeisrequiredtoreturnthetelecommunicationsindustrytohealth.

Theregionaldifferencesinoutcomesfornetworkoperatorsraiseanimmediatequestionregardingthishypothesis,namelyifitweretruesurely it would be true globally? Yet network operators in othermarkets have weathered the transition to next generationcommunications.

We have witnessed value creation in relation to messaging,measured in terms of market valuations and consumer use andbenefits. Butthisdoesnotimplyatransferofvaluefromnetworkoperators to applications providers.29 Rather, overall value hasgrown.

27WhitepaperbasedonIDATEstudy,Mobileoperators’investments-Europeneedsapro-investmentmobileregulatoryframework,November2015.28Vodafone, Tradingupdateforthethreemonthsended31December2015,February2016.29Feasey,Confusion,denialandanger:thetelecomsindustryandtheinternet,2013.

[14]

Amoreconvincingexplanationisthattheinternetisnotazerosumgame,ratherinnovationinrelationtocommunicationshascreatedvalueforprovidersandconsumers;andfornetworkoperatorswhohaveadaptedtothechangingmarket.Ericsson,incollaborationwithEY,analysedtheperformanceofmarketleadingnetworkoperatorsandconcludedthat:30

“Withvoice revenuesunderpressureandmobiledatausesoaring, operators have been forced to evolve both theirnetworksandtheirbusinessmodels.Somehavebeenmoresuccessful than others – we call these operatorsFrontrunners. Between 2010 and 2014, Frontrunnersenjoyed a 9.6% CAGR while competitors in their marketsachievedonly2.7%.”

Ericsson noted that frontrunners “…do not regard OTT players asthreats, but instead generally leverage their offerings.” AnotherstudybyIDATEconsideredtheimpactofVoIPandinstantmessagingontraditionalserviceprovidersandconcludedthat,overall:31

“…there appears to be a small net benefit: losses to SMSrevenueshavebeenbalancedbyoverallincreasesinrevenuefrom data-tariffs -- driven by demand for services such asVOIPandinstantmessaging.”

AstudybyATKearneyfortheGSMAfoundthataccessrevenueshadgrowngloballyatarateof14%perannumbetween2008and2015:32

“ConnectivityrevenuegrewfromEUR199billionin2008toEUR508billionin2015,butthisrepresentsasmallershareoftheofthetotalinternetvaluechain,decliningfrom18percentto17percent…”

Some operators have expressed similar views. Hiroyasu Asami ofNTTDOCOMOnotedthat:33

“Of course the services that OTT players supply oftencompetewiththeservicesofferedbynetworkoperators.Ontheonehand,competitionaddsuservaluebecauseservicestend to improve as a result of the rivalry between serviceproviders,butitalsoleadstoaddedvalueacrosstheboardifeachcompetitorpursuesareasinwhichtheyexcel.”

30Ericsson,GrowthCodes,May2015.31IDATE,VOIPandinstantmessaginghavenotharmedEUtelcos,2015.32GSMA,NewGSMAStudyDescribestheChangingEconomicsoftheDigitalEcosystem,May2016.33EricssonBusinessReview,Drivingserviceevolutionintheageofsmartphones,2013.

[15]

WhilsttheCEOofUKoperatorEEnotedthat:34

“…thegrowthofmobile-messagingserviceslikeWhatsAppwasn’t a threat to his business as the sector’s growth isdrivenbydata-hungryconsumers.”

Datagrowthissustainable

Metcalfe (co-inventor of Ethernet) predicted in 1996 that theinternet would collapse due to traffic growth.35 It did not. Thereason it didn’t collapse is that computing and networkingtechnologyhaveseencontinuedinnovationwhichhaskeptthecostof accommodating ever higher levels of traffic relatively constant(thepriceperGBcarriedhasfallendramatically).36

Innovation continues to increase the capacity of fibre links;whilstspectrum,sitesincludingsmallcellsandnewstandards(5Gvs.4Gvs.3G)increasethecapacityofmobilenetworks.Verizonnotedthatthetransitionto4Goffereda4-5-foldreductioninunitcostsandthat5Gwilldeliverasimilarreduction,forarelativelymodestinvestment:37

“keepinmindthat5Gisnotareplacementtechnologyof4G,sothisisnotacapital-intensiveoverlaytothe4Gnetwork.Itreallyisallabouthigh-speedvideodeliveryoverawirelessnetworkinavery,veryefficientway.Youshouldthinkabout5G,againlikewedidwithLTE,whereyouseethose4to5incremental cost decreases when delivering that video.That'ssimilartowhatwewillseeinthe5Genvironment.”

Indeed, continued technical progress coupled with slower trafficgrowth,wouldseenetworkcostsandrevenuesdecline:38

“…intheabsenceofdemandgrowthinducedbylowerpricesandanoutwardshift inthedatademandcurve–decliningunit costs would result in a revenue contraction for themobile industry. Thedemand stimulus fromgrowth in theuseofapplicationsoffsetstheimpactofdecliningunitcostsdue to spectrum efficiency, utilisation and increasedspectrumavailability.”Page7

34WallStreetJournal,WhatsAppIsKillingSMS,butThat’sOK,EE’sCEOSays,February2014.35JohnMacMullen,Bobgetshisjustdesserts....,April1997.36Kenny,Aretrafficchargesneededtoavertacomingcapexcatastrophe?AreviewoftheATKearneypaperAViableFutureModelfortheInternet,August2011.37Verizon,1Q2016QuarterEarnings–Transcript,April2016.38WilliamsonandWood,TheSpectrumCrunchisDead,LongLiveSpectrumDemand,2015

[16]

Networkoperatorshavefacedchallenges,buttheserelateprimarilytothe2007recessionandregulation,ratherthantrafficgrowth.AsWIKnoted:39

“Overall, we feel that the current data continue todemonstrate that traffic growth is not a root causeof thechallengesthatnetworkoperatorsface.”Page1

Datagrowth,drivenbyuserwillingnesstopaytoaccessappsandbyfallingnetworkunitcostsdrivenbyinnovation,issustainable.

Messagingappprovidershaveinvestedinconnectivity

Next generation communications providers have made targetedinvestments in infrastructure including servers and networkinfrastructure.40 The aim is not to do what others are doingefficiently,buttolowercostsandextendaccesswherethemarketmaynotfullymeetdemand.

Agap,whichnextgenerationcommunicationsprovidersareseekingto fill by developing and sharing new technologies, is to extendaccesstothosewhocurrentlydonothaveaccess.Whilstthefocusis primarily on developing country markets, the innovation andinvestment efforts illustrate that next generation communicationsprovidersarenotaversetoinvestinginrelationtoaccess.

Microsofthaveinvestedinaffordableaccess41,GooglehaveinvestedinfibretothepremiseintheUSanddevelopedballoonbasedaccess(Google Project Loon42), whilst Facebook have announced acollaborationwithEutelsattolaunchasatellite,43areexperimentingwith providing access via solar powered drones,44 are developingopensourcenetworkingstandards45andhaveannouncedinitiativestoextendmobilewirelessaccessanddevelopahighspeedwirelesslast mile fibre substitute.46 Microsoft and Facebook have alsoannouncedaninvestmentina160Tbpstransatlanticfibrelink.47InQ12016Facebookinvested$1,343bninR&D,25%ofrevenue,withhundredsofmillionsplannedforR&Donconnectivity.48

39WIK,TheeconomicimpactofInternettrafficgrowthonnetworkoperators,October2014.40AnalysysMason,Investmentinnetworks,facilitiesandequipmentbycontentandapplicationproviders,September2014.41https://www.microsoft.com/en-us/affordable-access-initiative/home42http://www.google.com/loon/43https://www.facebook.com/zuck/posts/1010240767586506144https://info.internet.org/en/story/connectivity-lab/45LightReading,DT:TelcosMustEscapeVendorPrison,May2016.46https://code.facebook.com/posts/1072680049445290/introducing-facebook-s-new-terrestrial-connectivity-systems-terragraph-and-project-aries/47MicrosoftandFacebooktobuildsubseacableacrossAtlantic,May2016.48https://www.facebook.com/zuck/posts/10102777889538891

[17]

Conclusion

Nextgenerationcommunicationsdonotfree-rideonaccess;justasnetwork access providers do not free-ride on next generationcommunications.Accessandapplicationsarecomplements.Richerapplications drive demand and willingness to pay for enhancednetworkaccess,whilstimprovedaccesscoverageandqualityenablesgreaterusemessagingandotherapplications.Thereisnofreeriderproblem.

[18]

4. Alevelplayingfield–butwhichfield&whatlevel?“Stagecoach companies were unhappy in the late 19thcentury, justasdisrupted taxi companiesare today. Legacyplayers will claim they are facing unfair competition fromplayers that are not abiding by the same rules.” Jean PaulSimon,2016,Page6049

Thepolicyanalysisinthissectiondoesnotstartfromtheideathatregulationshouldnecessarilybethesamefor‘equivalent’services,orthatalevelplayingfield(withvariouspossibleinterpretations)isadesirablepersegoal.Rather,ittacklestheunderlyingquestionofwhat specific policy and regulation, if any, of communicationsservicesisappropriate.

Inthefollowingaframeworkforanalysisissetout,specificareasofregulationareconsideredandgeneralconclusionsaredrawn.

Frameworkforanalysis

Tennenhouse and Gillett (2014) discuss making innovation theprimarypolicygoal.50Theydiscusshow,towardstheendofthe20thcenturycompetitionsupplanteduniversalvoiceastheprimarygoalof communications policy. The paper argues that policy makersshould now pursue an innovation-first approach and undertake a‘backtobasics’processof:

• “Identifyingrulesthatarebarrierstoinnovation• Clarifyingtheoriginalpublicinterestvaluesservedbylegacy

policies, and determining which values remain relevanttoday

• Leveragingtechnologytohelpaddresstoday’sconcerns.”

This basic approach appears well suited to addressing the policyquestionsraisedbynextgenerationcommunications.

NERA(2016),inapaperonbehalfoftheGSMA,developtheideaoffunctionality-basedregulation.51Thepaperstartswithfourpremisessummarisedbelow:

“I:Whilemarkets are generally themost effectiveway tofosterinnovationandconsumerwelfare,theydonotalwaysdeliver optimal outcomes. If market conduct is harming

49JeanPaulSimon,HowtoCatchaUnicorn,2016.50TennenhouseandGillett,Whataboutinnovation?,InterMEDIA,Volume42(1),Spring2014.51NERA,Anewregulatoryframeworkforthedigitalecosystem,2016.Pages8-9.

[19]

consumerwelfareandregulatoryinterventionwouldcreateanetbenefit,thenregulationsshouldbedesignedtoachievethegreatestpossiblebenefitatthelowestpossiblecost.

II: Policy should be functionality-based, rather thanstructure- or technology-based. By this we mean thatregulatorypolicyshouldbedesignedtoachievethedesiredobjective (e.g., protecting privacy, promoting universaladoption, providing incentive for investment andinnovation) in the most efficient way, regardless of thetechnology,industrystructure,orlegacyregulatoryregime.

III: Information technology markets are characterised bydynamic competition, meaning that companies largelycompete through innovation, rather than price. Thiscompetition leads to rapid changes in markets andtechnologies, so regulation must be flexible enough toaccommodate thesechangeswhile creating the regulatorycertainty and predictability that companies need to takerisks.

IV:Thesesweepingchanges in thedigitalecosystemmeanthat even when the goals for regulatory policies andinstitutionsremainunchanged,itisnecessarytorethinkhowto achieve these goals from the ground up.We thereforepropose that policymakers take a bottom-up approach toregulatoryreformdiscussions,whichwillencouragethemtoconsider entirely new approaches—and be willing, whereappropriate,tojettisonoldones.”

TheNERApaperlists(Table2,page29)sector-specificregulationofcommunicationsproviders,andtheclaimeddisparity intreatment,acrossregulatoryissuesincludingeconomicregulationofpricesandentry, consumer protection, competition regulation, privacy anddata protection, security and law enforcement, and taxation.However, theNERApaper (page 32) also notes that functionality-based regulation may require different regulatory treatment ofservicesprovidedviadifferentmeans:

“Functionality-based regulation is related to policy criterialike technological neutrality or ‘same service, same rules’,butgoesbeyondthem.First,itistechnology-agnosticratherthan technology-neutral, since it calls for all technologicalmeansforachievingthedesiredobjectivetobeexamined,but does not demand that each technology be regulatedidentically. Indeed, a functionality-based approachrecognises that differences in technology may require

[20]

different regulatory treatment to achieve a commonobjective.”

BothTennenhouseandGillett(2014)andNERA(2016)pointtotheneedforanobjectiveandproblemdrivenapproachtopolicy,andtothe need to maximize scope for innovation in relation to marketoutcomes and delivery of public policy goals. In what follows,specific regulatory issues relating to legacy and next generationcommunicationsareconsideredwiththeseprinciplesinmind.

Issuebyissueanalysis

InteroperabilityLegacyvoiceandSMSmessagingappsareinteroperableinthesensethat anyone with a telephone number can, in principle, contactanyone else with a telephone number (in practice the ability todiscoversomeone’sphonenumberandthecostofcallingortextingthemmayconstraintheextentofinteroperability).Thisispossiblebecausethetelephonenetworks,byusingacommonsetofuniqueidentifiers, become one network. So, while interoperable amongthemselves, they cannot necessarily interoperate with messagingservices.

It has been argued that next generation communications serviceslackinteroperability,thoughwhatisproposedisunclear.Compellinginteroperabilitywithothernextgenerationandlegacyservicesmaysimply not be practical or desirable. DG Competition consideredinteroperabilityinrelationtotheFacebookacquisitionofWhatsAppandconcludedthat:52

“…technical integration betweenWhatsApp and Facebook[including Facebook Messenger] is unlikely to be asstraightforwardfromatechnicalperspectiveaspresentedbythirdparties.”Paragraph139

Within technology markets there is a constant search for thecombination of closed versus interoperable elements whichmaximises innovation and benefits.53 Open innovation andinteroperability may be in tension, after all next generationcommunications has innovated far faster than legacy standardsbasedservices.ViberfounderTalmonMarcoexpressedthistensionasfollows:54

52DGCompetition,CaseNoCOMP/M.7217-FACEBOOK/WHATSAPP,October2014.53AutoritédelaconcurrenceandCMA,Theeconomicsofopenandclosedsystems,December2014.54TheVerge,Alonetogether:willonemessagingapprulethemall?,May2013.

[21]

“Youcanchoosetointeroperateorinnovate;youcannotdobothatthesametime."

In addition, legacy services lack interoperability across otherdimensions where next generation communications apps areinteroperable(Figure4).

Figure4:Nextgenerationversuslegacyserviceinteroperability

Voice SMS Skype WhatsApp

Phonenumberinteroperability(bydefault) ü ü x x

Deviceinteroperabilitye.g.PC,tablet,mobile x x ü ü

Networkinteroperability(Wi-Fi,cellular&fixed)† x x ü ü

†SomemobiledevicesandnetworkssupportWi-Fibasedcalling

Finally, consumers achieve effective interoperability by havingmultipleappsontheirdevice(multi-homing),viaoperatingsystemfunctionality that aggregates messages (for example, via thenotifications screen in iOS) and via access to a common set ofcontactsinformation.

SwitchingandnumberportabilityThe transfer of numbers from one service provider to another isregulatedtoreduceswitchingbarriersforconsumers.

Such requirements can be expected to continue, given theuniqueness of numbers, and the fact that consumers cannotassociatemultiplenumberswithagivendevice/SIMcard.

In contrast to legacy services, consumers using next generationcommunications servicesdonotneed to switchproviderandporttheir means of identity, but can adopt multiple services (multi-homing)andusemultipleformsofidentity.

Somehavearguedthatconsumersmayneverthelessfacebarriersin“switching” next generation communications provider. DGCompetition considered switching in relation to the FacebookacquisitionofWhatsAppandfound,initsmarketinvestigation,thattherearenosignificantcostspreventingconsumersfromswitchingbetween different apps.55 The Commission gave the followingreasonsforthisconclusion:

“First, all consumer communications apps are offered forfree or at a very low price. Second, all consumer

55DGCompetition,CaseNoCOMP/M.7217-FACEBOOK/WHATSAPP,October2014.

[22]

communications apps are easily downloadable onsmartphonesandcancoexistonthesamehandsetwithouttaking much capacity. Third, once consumercommunications apps are installed on a device, users canpass from one to another in no-time. Fourth, consumercommunicationsappsarenormallycharacterisedbysimpleuserinterfacessothatlearningcostsofswitchingtoanewappareminimalforconsumers.Fifth,informationaboutnewappsiseasilyaccessiblegiventheeverincreasingnumberofreviewsofconsumercommunicationsappsonappstores.”Paragraph109

“…theCommissionhasnot foundanyevidence suggestingthat data portability issues would constitute a significantbarrier to consumers' switching in the case of consumercommunicationsapps.”Paragraph113

SwitchingandcontractsTelecoms contracts, applying to both broadband access and voiceservices, are subject to specific provisions to support competitionandprotectconsumers.Sincenextgenerationcommunicationsappsarenotingeneralsubjecttocontractsthatbindtheusertoaspecifictermorspend,sectorspecificregulationofcontactsisunlikelytobeapplicable.

SpectrumfeesandcoverageobligationsSpectrum fees and associated obligations are not restricted totelecoms network operators, but apply to anyone acquiring orholdinglicencedspectrumsubjecttofeesorobligations.

Nextgenerationcommunicationserviceprovidershavenot,asarule,soughttopurchaseorholdlicencedspectrum.Assuch,theydonotpayfees. This isnotdiscriminatory. Feesshouldhoweveronlybeappliedtotheextentthattheypromoteoptimalspectrumuse.56

UniversalserviceUniversal service requirements apply to broadband, voice andfacsimile. Existing requirements relate to access to underlyinginfrastructureinordertoaccessservices;andtotheaffordabilityofaccessandservices.

Next generation communications have contributed greatly toaffordability, and access obligations are not relevant to nextgeneration communications. The current approach is notdiscriminatory.

56Williamson,MarksandYiShen,Annuallicencefees-youcannothaveyourcakeandeatit,January2014.

[23]

Universal service should, however, be re-examined in light of anumberofdevelopments,inparticular:

• The shift from the household (at a fixed location) to theindividual(anywhere)astheprimaryunitofconsumption.

• AshiftfromfundingviacrosssubsidyorindustrylevytoStateAid funding for non-commercial extension of high speedbroadband.

• The growing relative importance of a demand-side ratherthansupplyside-gap.Broadbandcoverageisnearuniversal,whereasaround100millionadultsinEuropedonotusetheinternet.

The outcome of such a re-examination will depend on the policyobjectives. Arguably,givenmarketdevelopmentsandthegoalsoftheDigitalSingleMarketstrategy,thefocusofpolicyshouldbeon:

• Broadbandaccessandinternetuse;ratherthantelephony,facsimileandservicessuchascallboxes.

• Mobile data availability and use, given shifts in behaviourandintheecosystemofapplications.

Further,futurepolicyinitiativesshouldbetechnologyagnosticandpublicly funded. This would increase transparency, reduceinefficiency resulting from sector specific levies or cross subsidy57,fosterinnovationandcompetitioninprovision.

Inconclusion,universalservicerequirementsshouldbemodernised,simplified and publicly funded; and are not applicable to nextgenerationcommunications.

Voiceorigination,terminationandroamingWholesale calls (and in a few cases SMS) are subject toeconomicregulationofpriceswherecompetitionisjudgedinsufficient.Suchregulation applies to fixed call origination (in somemarkets), callterminationandinternationalroaming.

Totheextentthat fixed-mobilecompetitionandcompetitionfromnext generation communications acts as a constraint on pricing(absentregulation),regulationshouldberemoved.58Whilstthereisacaseforreducingoreliminatingexistingwholesalepriceregulation

57AccordingtotheDiamondMirrleesresulttaxesofinputsisinefficientcomparedtogeneraltaxationofincomeandconsumption.https://assets.aeaweb.org/assets/production/journals/aer/top20/61.1.8-27.pdf58Theremovalofvoiceoriginationfromthelistofrelevantmarketsin2014wasastepinthisdirection.Others,forexample,theNordicRegulatorsGroup,havequestionedwhetherregulationofcallterminationwillremainrelevant“Asmoreandmoretrafficismadeupofdata,theneedtomaintainthetraditionalregulationonvoiceterminationratesisbecominglessrelevant,andmayeven,withinaforeseeablefuture,createmarketinefficiencies.”NordicRegulatorsGroup,TheDigitalSingleMarketStrategy,August2015.

[24]

of callsandSMS, it isnotdiscriminatorybetweennextgenerationandlegacymessagingservices.

InformationgatheringIt has also been suggested by BEREC that information gatheringpowersbeextendedbeyondlegacyservices.However,ifthefocusofregulationisaccess,theninformationregardingapplicationsisnotrelevant.

Informationregardingconsumeruseofapplicationsmighthoweverbe of value, for example, in assessing future bandwidth demand.Such informationwouldneed tobebasedon statedand revealedconsumer preferences and bottom-up demand estimates, ratherthanformalinformationrequeststoapplicationproviders.

BundlingBundling of services, including broadband, messaging and videocouldpotentiallymakeswitchingmoredifficultforconsumers.Nextgeneration communications tend to counteract the impact ofbundlingbyallowingconsumerstopickandmixtheapplicationstheywant.

EmergencycallsandtheriskofconsumerconfusionEmergency calling requirements relate to the use of telephonenumbers,andarelinkedtorequirementsinrelationtothelocationofcallers.

Whilst thestatusquoaroseforhistoricalreasons,therearesoundgroundsformaintaininganarrowfocusintermsofemergencycallrequirements:

• It isessentialthatthepublichaveaclearunderstandingofhowtheycancontacttheemergencyservicestoensurethathelpisobtainedpromptly.

• Not all the devices and networks that support nextgeneration communications would allow location to bedetermined, for example, an iPod touch does not havecellularserviceorGPS.Inaddition,itisthenetworkratherthan the app that has access to the location informationrequiredbyemergencyservices.

• Emergency calling is provided over dedicated switchedcapacity,ratherthanthepublicinternet.Amanagedserviceis required which offers a high degree of reliability;somethingthe ‘bestefforts’modelof internetapplicationsdoesnotprovide.

[25]

• Accommodatingawiderrangeofapplicationswouldimposeadditional costs on the emergency services and on thosedevelopingnextgenerationcommunicationsapps.

Maintaininganarrowfocus in termsof themeansof reachingtheemergencyservices,andtheuniversalityofemergencynumber112,appearssound.Extendingtherequirementtoapplicationswould,inpractice,fallshortofallformsofcommunications.

This would likely result in consumer confusion and delays incontacting the emergency services given the ubiquity ofcommunicationsinapplicationssuchasgamesincludingAngrybirdsand Minecraft; e-commerce including eBay; and social networksincluding LinkedIn. It would likely prove impossible to draw, andcommunicate, a clear and unambiguous distinction in terms ofemergencyservicesupportbeyondlegacyvoice(andperhapsSMS).

DataprotectionandinterceptionWith the adoption of the General Data Protection Regulationoverlappingprovisionsinthee-PrivacyDirectiveshouldberemoved.

Inrelationtointerception,thecostsandbenefitsoflegalinterceptof stored communications differ from those involved in providingaccesstoencryptedcommunications.59

The question of interception highlights the importance ofconsideringthecostsandbenefitsofregulationindifferentcontextsrather thansimplyassumingthat thesameruleshouldnecessarilyapplyacrosstheboard.

Fromspecifictogeneral

Theaboveanalysisof specific regulatory requirementsapplying totelecomsservicespointstoanumberofgeneralconclusions,buttheidea of a level playing field for regulation does not emerge as anoverridingprinciple.

AnobligationmaybeneutralbutnextgenerationcommunicationsmaynotfallwithinitsscopeFees for licenced spectrum apply to anyone holding licencedspectrum, which next generation communications providers ingeneral do not. Other examples include provisions relating tocontractsandnumberportability.

59TheEconomist,Internetsecurity-Whenbackdoorsbackfire,January2016.Abelsonetal,KeysUnderDoormats:Mandatinginsecuritybyrequiringgovernmentaccesstoalldataandcommunications,July2015.

[26]

TherationaleforagivenregulatoryobligationmaynotapplytonextgenerationcommunicationsObligations that apply to network access and not applications fallwithin this category, including aspects of universal serviceobligations.

Problems in relation to market power may be unique to legacyservicesTheseincludecallterminationandroaming,neitherofwhichariseinrelationtonextgenerationcommunications.However,totheextentthatnextgenerationcommunicationscompeteswithlegacyservices,the rationale for economic regulation of legacy services may fallaway.

ThebalanceofcostsandbenefitsofanobligationmaydifferEmergencycallingisanexample. Whilst inprincipleitmightseemlogical to extend this obligation to all communication services thecostsofdoingso (for theemergencyservicesandnextgenerationcommunicationsproviders),andtheriskofconsumerconfusionandthereforeharm,raiseseriousdoubtsregardingextension.

Policyimplications

Defining a general boundary between next generation & legacyservicesdoesnotappearhelpfulThequestionofhowtodefineelectroniccommunicationsservices(ECS), in light of next generation communications, has receivedattention (for example, byBEREC,whichdidnot agreea commonposition60).

One proposed approach that has been proposed is to considerwhether consumers view next generation communications assubstitutesforECS.WhilstthisquestionisrelevanttothequestionofwhetherpricecontrolsrelatingtoECSshouldberemoved,itdoesnot help clarify the applicability of other regulation currentlyapplyingtoECS.

Anotherapproach suggestedby some is to considerwhethernextgenerationcommunicationsappscanmakeand/orreceivecallstoatelephone number. However, whilst this may relate to numberportabilityprovisions, itdoesn’tclarifyotherquestions. Further, ifuseofnumberingisadecidingfactorintermsofwhetherarangeofregulatory obligations apply to next generation communications,

60BEREC,ReportonOTTservices,January2016.

[27]

next generation communications providers may remove usefulfunctionality.

Focussing electronic communications regulation on accessinfrastructureappearsdesirableAnalternativetoattemptingtofinessetheboundaryofECSandnextgeneration communications would be to narrow the definition ofelectroniccommunicationstonetworkaccess.Thiswouldsharpenthefocusofexanteregulators,andleavelegacyandnextgenerationcommunication applications regulation to general competition,consumerprotectionanddataprotectionlaw.

CERREhaveproposedthatelectroniccommunicationsregulationbefocusedonaccessratherthanservices:61

“Serviceswhichconsistintheaccessto,andtheconveyanceofsignalson,electroniccommunicationsnetworks.”

WIKmadeasimilarsuggestion“ConsiderreducingthescopeoftheEUFrameworkforelectroniccommunicationstoconnectivity.”62

Other specificobligations couldapply independentof this change,forexample,inrelationtoradiospectrumandtelephonenumbers.RoamingregulationiscoveredbyEuropeanregulationwithroamingsurcharges eliminated by June 2017. Obligations in relation toemergencycallingwouldalsoneedtobemaintained.

Alevelplayingfieldforcompetitiondiffersfromapplyingthesameregulation,andneithermaybefeasibleordesirableAs NERA (2016) note, appropriate regulationmay depend on themeans of service delivery (even where consumers would notnecessarilyseetheservicesasdistinct).Platformsmayalsoregulatemarkets,therebyshiftingtheappropriatebalancebetweenselfandexternally imposedregulation. AsCohenandSundararajan (2015)noted:63

“…platformsshouldnotbeviewedasentitiestoberegulatedbut rather as actors that are a key part of the regulatoryframework…For non-intermediated peer-to-peer exchangein the past, the primary solution to market failure wasintervention by a government agency. But today, theexistence of third-party platforms that mediate exchangefundamentallyalterswhatthemarketiscapableofprovidingon its own, and it creates a new institution capable of

61CERRE,Anintegratedframeworkfordigitalnetworksandservices,2016.Page22.62WIK,Over-the-Topplayers(OTTs),December2015.63MaryCohenandArunSundararajan,Self-RegulationandInnovationinthePeer-to-PeerSharingEconomy,UniversityofChicagoLawReview,Feb2015.

[28]

affectingwhatMichaelFoucaultreferredtoasthe“conductofconduct.”

The concept of same regulation for same service is therefore notuniversally applicable, nor desirable, as a guiding principle. Apossiblevariationwouldbetorequirethesamelevelofconsumerprotection, allowing for self-regulation. However, legacy servicesmaynotbeabletomatchthelevelofconsumerprotectionaffordedvia self-regulation utilising information technology and data. AsJoshuaGans(2015)putit:64

“Uber and Airbnb are in fact some of themost regulatedecosystemsintheworld.Theyhavemassiveregulationsthatwouldmakeanywould-bebureaucratproud.Theproblemisessentially thatwehaveacompatibility issuebetweenthepublicandprivateregulations…”

Another conception of the level playing field is that it relates tocompetitive neutrality. Whilst it is desirable not to distortcompetition,acompletelylevelplayingfieldmaynotbefeasible,inparticulargivenintegrationoflegacyservices.

Legacy communication services and next generationcommunications may have competitive advantages anddisadvantages,notallofwhichcan(orperhapsshould)beremoved.Whilstithasbeenarguedthatlegacyservicesaredisadvantagedbyexisting regulation, they also enjoy advantages compared to nextgenerationcommunications,inparticularlegacyservices:

• Enjoydedicatednetworkcapacityandprioritycomparedtoservicesprovidedoverthepublicinternet.

• Areabletoutilisemoreextensive2Gcoveragecomparedto3Gand4Gdatacoverage.

• Are integratedwith the default “Phone” and “Messaging”appsonsmartphones,andcannotbereplaced.

• Provideaccesstoanyonewithanumberandintegrationtothetheemergencyservices.

Application of the level playing field concept as an overarchingprinciple would therefore require removal of those advantagesenjoyedbylegacyservices.LegacyservicesmightalsoberequiredtobesupportedonacrossnetworkbasisincludingWi-Fi,topreventconsumerlock-intocellularservice.

64FTC,WorkshopTranscript-The“Sharing”Economy:IssuesFacingPlatforms,Participants,andRegulators,June2015.Page25.

[29]

Whilst removing some of the existing regulatory constraints onlegacy service providers may be justified, application of the levelplaying field as an overarching principle might also require newregulation of legacy services to overcome advantages stemmingfromverticalintegration.

Doingso,however,wouldnotnecessarilybeinconsumers’interestsasintegrationcansimplifyandimproveservices.Tobeclear,wearenotnecessaryadvocatingsuchaction,butsimplyillustratingreductioadabsurdumthatalevelplayingfieldisneitherstraightforward,nornecessarilydesirableasanoverridingpolicygoal.

Conclusion

Alevelplayingfieldforcompetitionmaybedesirablebutmaynotbeachievable in practice (for example, legacy messaging hasadvantages stemming from vertical integration) and would notnecessarilyinvolvethesameregulationacrossservices.

The scope of the electronic communications framework shouldideally be narrowed to network access, with nearly all issues inrelation to legacy and next generation communications appsaddressed via general competition, consumer protection anddataprotectionlaw.

Anobjectiveandproblemdrivenapproachtoregulationshouldbeadopted, and would be likely to leave some asymmetries ofregulation where the costs of equalisation exceed the benefits.Removing unnecessary restrictions on innovation and competitionwhereverpossibleisdesirable.

[30]

5. Nextgenerationcommunications-helpingcompletethesinglemarket

TheDigitalSingleMarketinitiativeaimstocontributetogrowthandjobs,basedonthreepillars:

1) Access:TheDigitalSingleMarketstrategywantstoallowbetteraccessforconsumersandbusinesstoonlinegoodsandservicesacross Europe. This will remove the key differences betweenonlineandofflineworlds,tobreakdownbarrierstocross-borderonlineactivity.

2) Environment:TheDigitalSingleMarketaimstocreatetherightenvironmentandconditionsfordigitalnetworksandservicestoflourish by providing high-speed, secure and trustworthyinfrastructures and services supported by the right regulatoryconditions.

3) Economy & Society: The Digital Single Market Strategy willmaximisethegrowthpotentialoftheEuropeanDigitalEconomyand of its society, so that every European can enjoy its fullbenefit.

Innovation and growth in relation to next generationcommunicationsiscontributingtotheabovegoalsinseveralways:

• In contrast to legacy voice and SMS services, which areprovided on a national basis, next generationcommunicationsservicesarepan-Europeanbydefault.

• Nextgeneration communications reduce languagebarriersby combining speech, video and text; with some appssupportingtranslation.

• Next generation communications stimulate demand formoreubiquitousdataaccess;whilstvideoandphotosharingsimulatedemandforfasterhigher-capacitynetworks.

European citizens and enterprises (in particular SMEs) havebenefitedfromnextgenerationcommunications. Nextgenerationcommunications focussedontheenterprisemarket, suchasSlack,HipChat, Symphony and Skype for Business, are now also beenadoptedbyenterprises.

These developments will facilitate cross border collaboration anddevelopment of the single market. To support the role of nextgeneration communications in breaking down barriers to cross-border communication, it is important that the country of originprincipleappliesandthatinnovationisallowedtoflourish.