Embed Size (px)

Citation preview

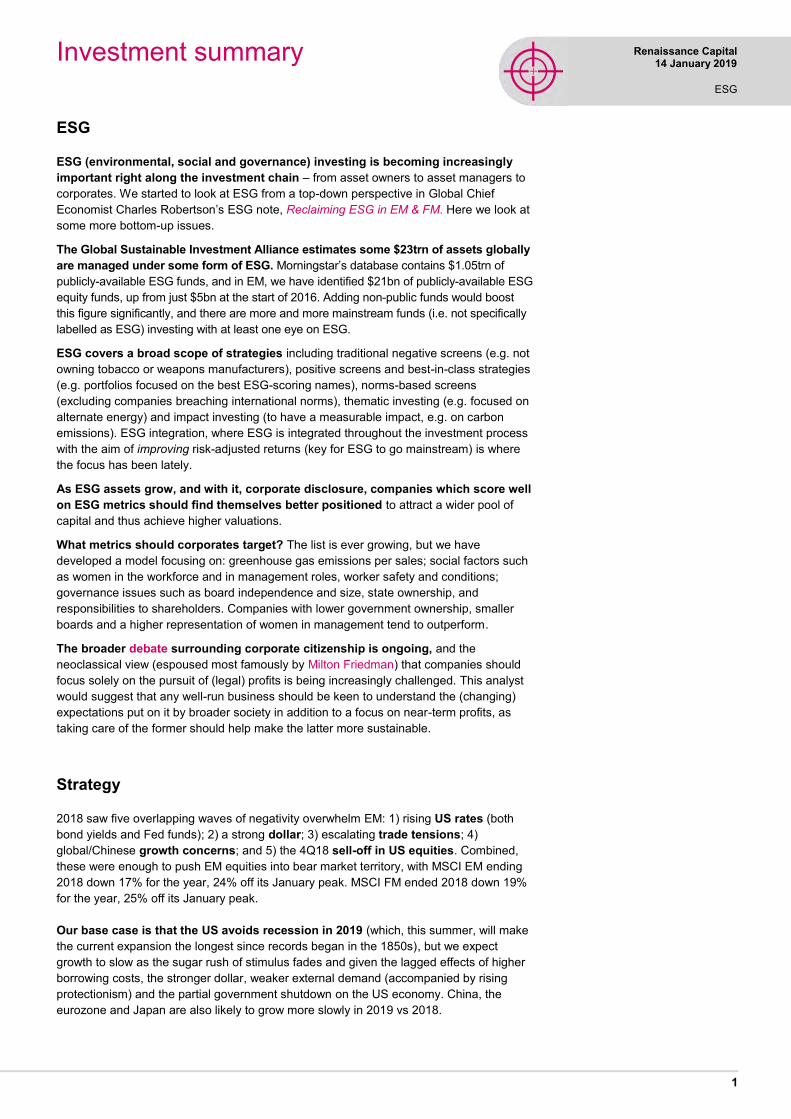

ESG

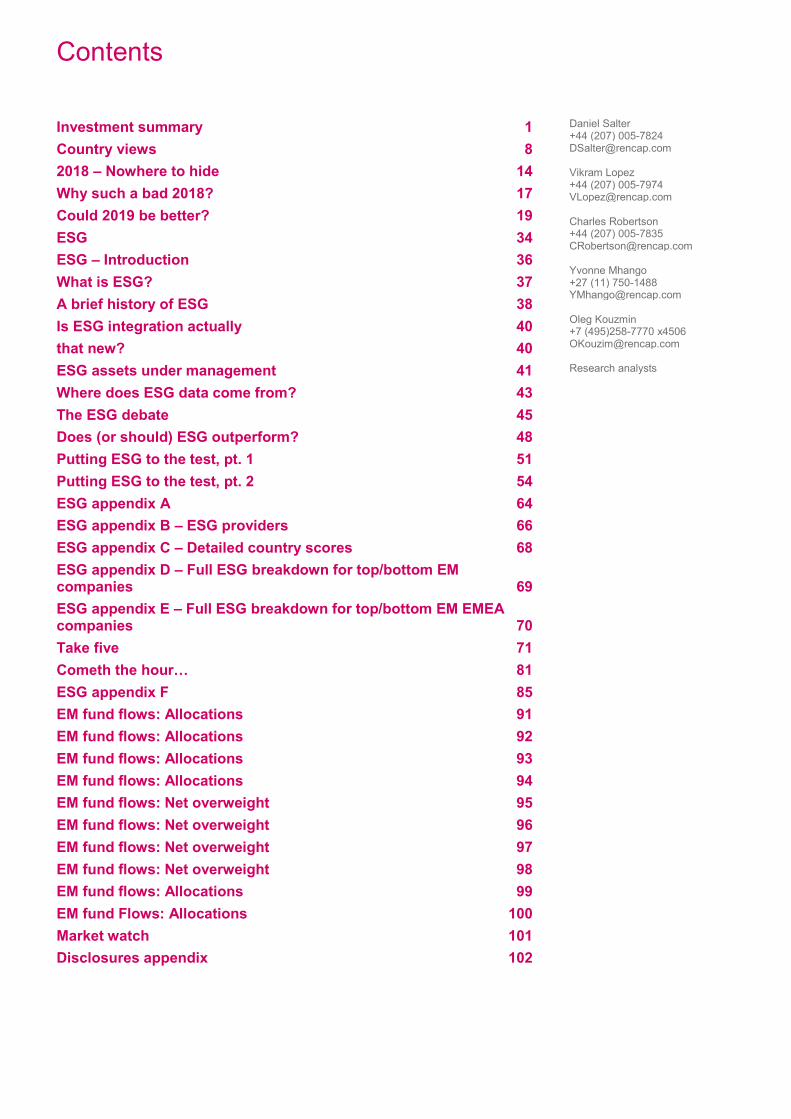

Investment summary 1 Country views 8

2018 – Nowhere to hide 14

Why such a bad 2018? 17

Could 2019 be better? 19

ESG 34

ESG – Introduction 36

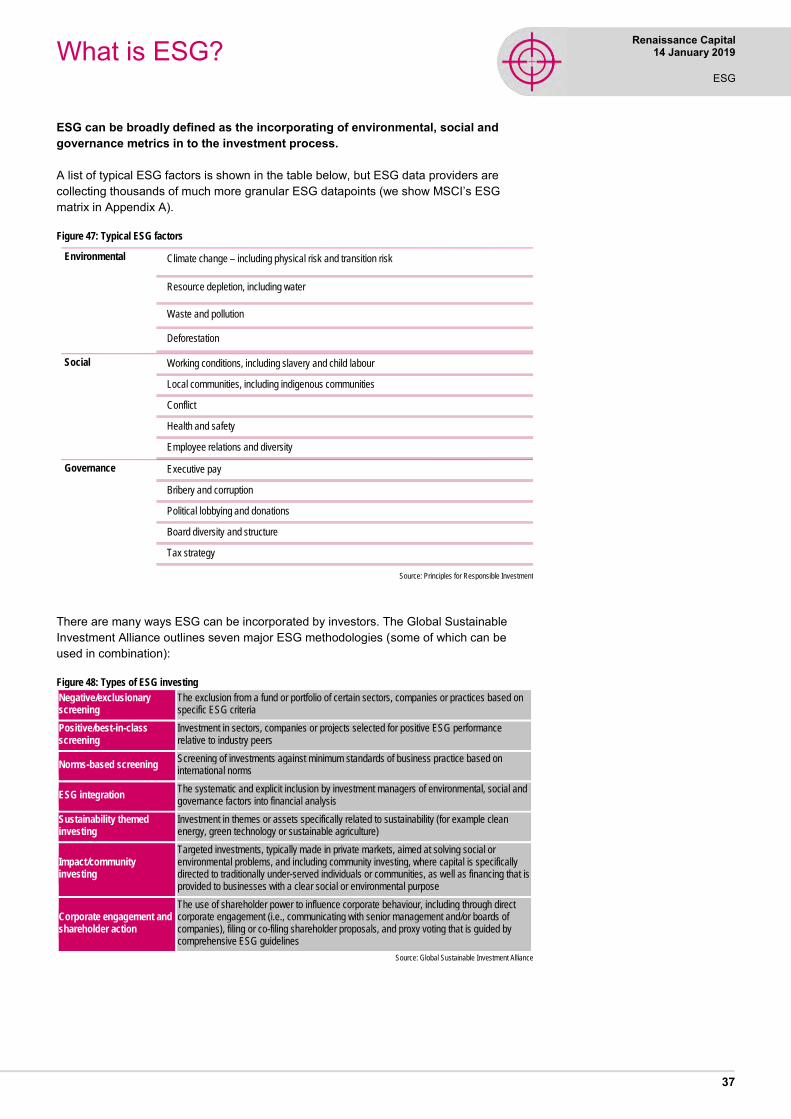

What is ESG? 37

A brief history of ESG 38

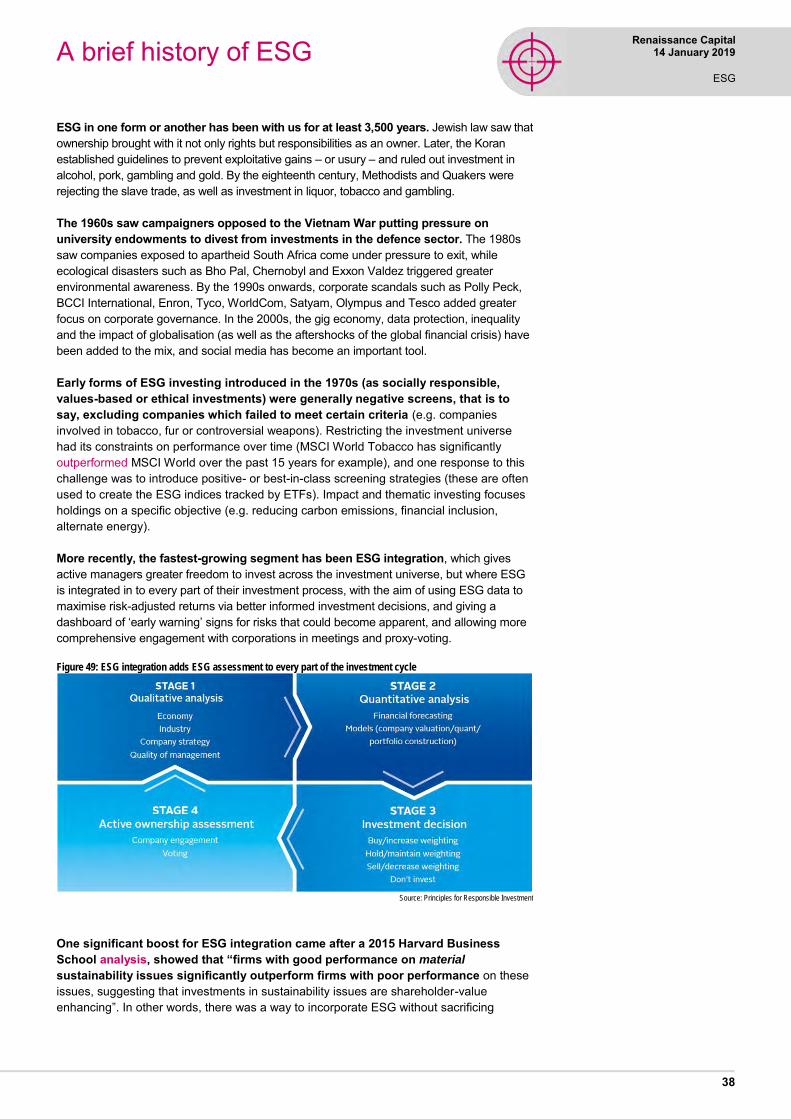

Is ESG integration actually 40

that new? 40

ESG assets under management 41

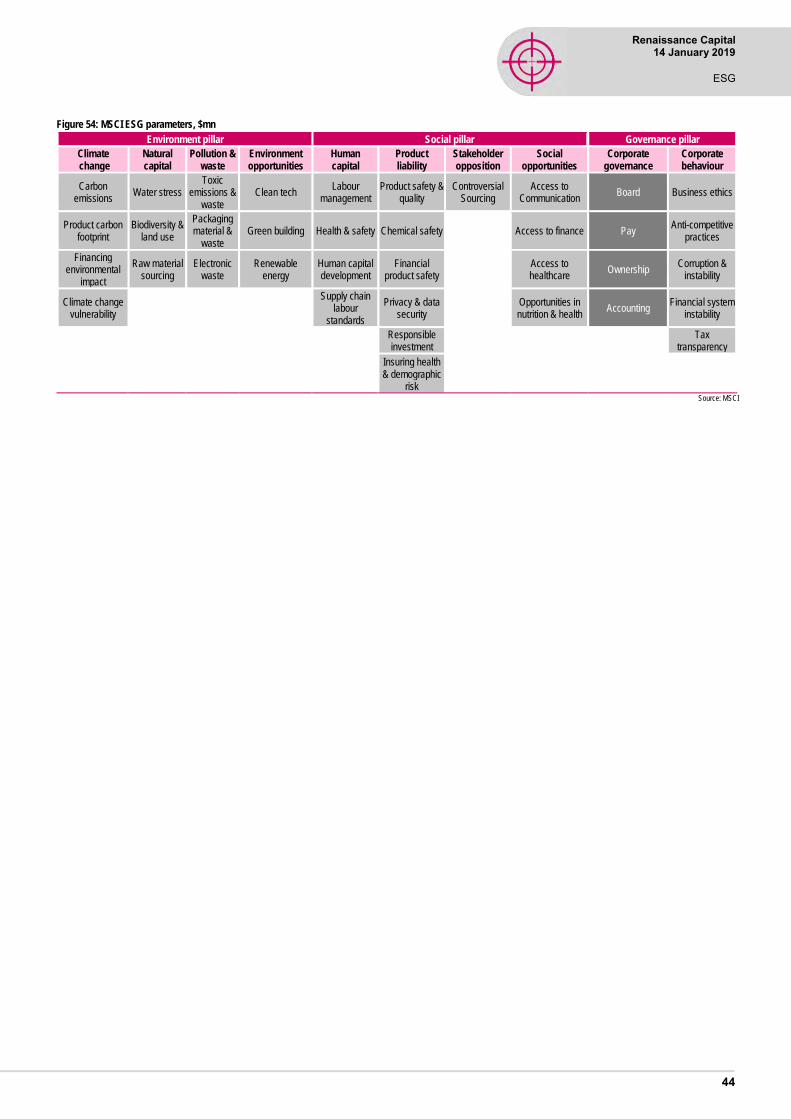

Where does ESG data come from? 43

The ESG debate 45

Does (or should) ESG outperform? 48

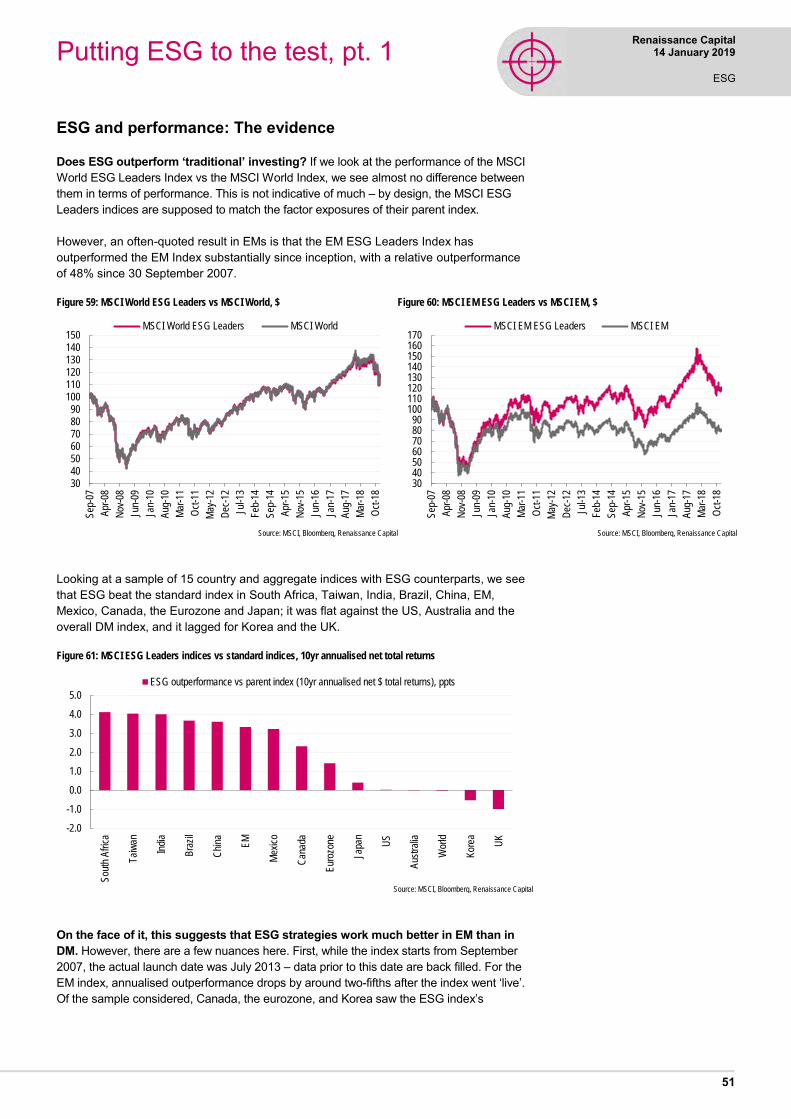

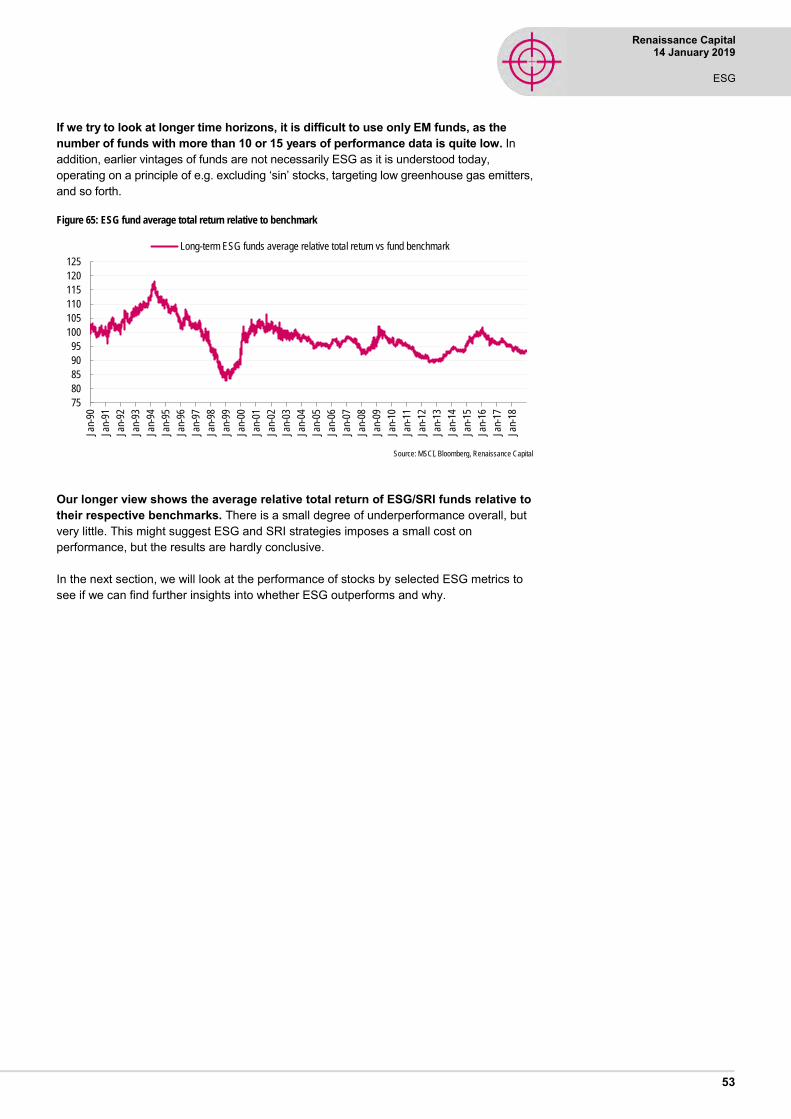

Putting ESG to the test, pt. 1 51

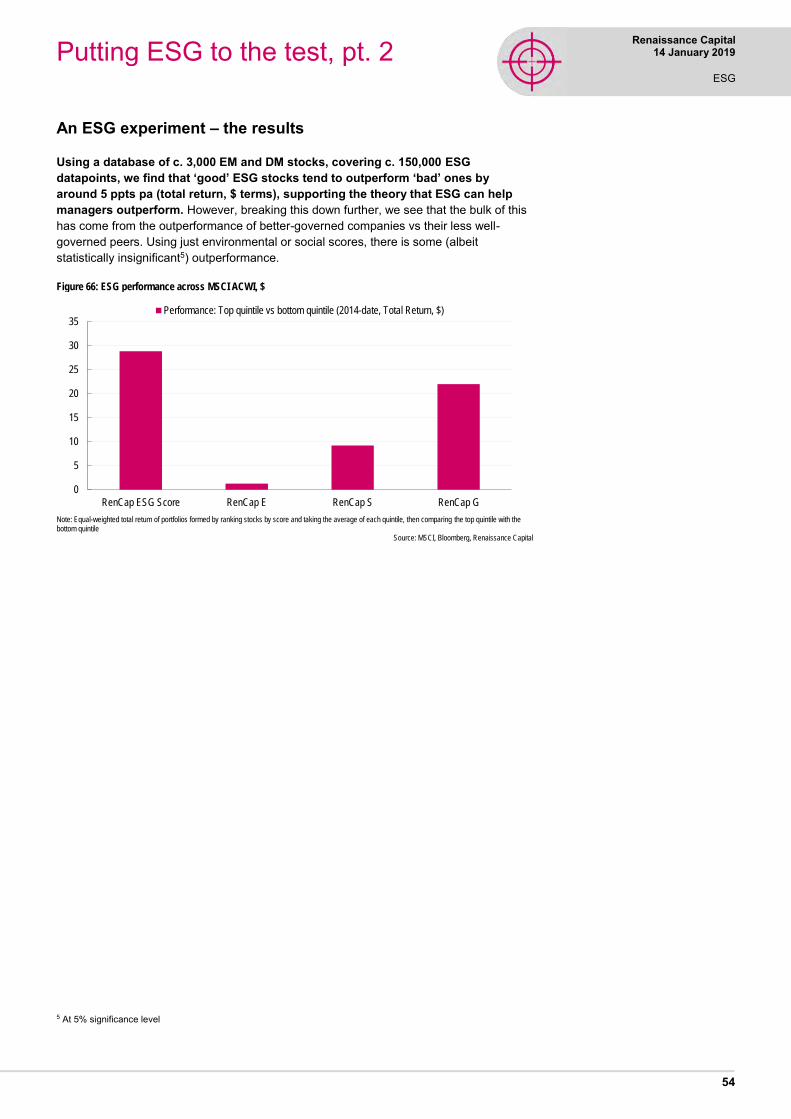

Putting ESG to the test, pt. 2 54

ESG appendix A 64

ESG appendix B – ESG providers 66

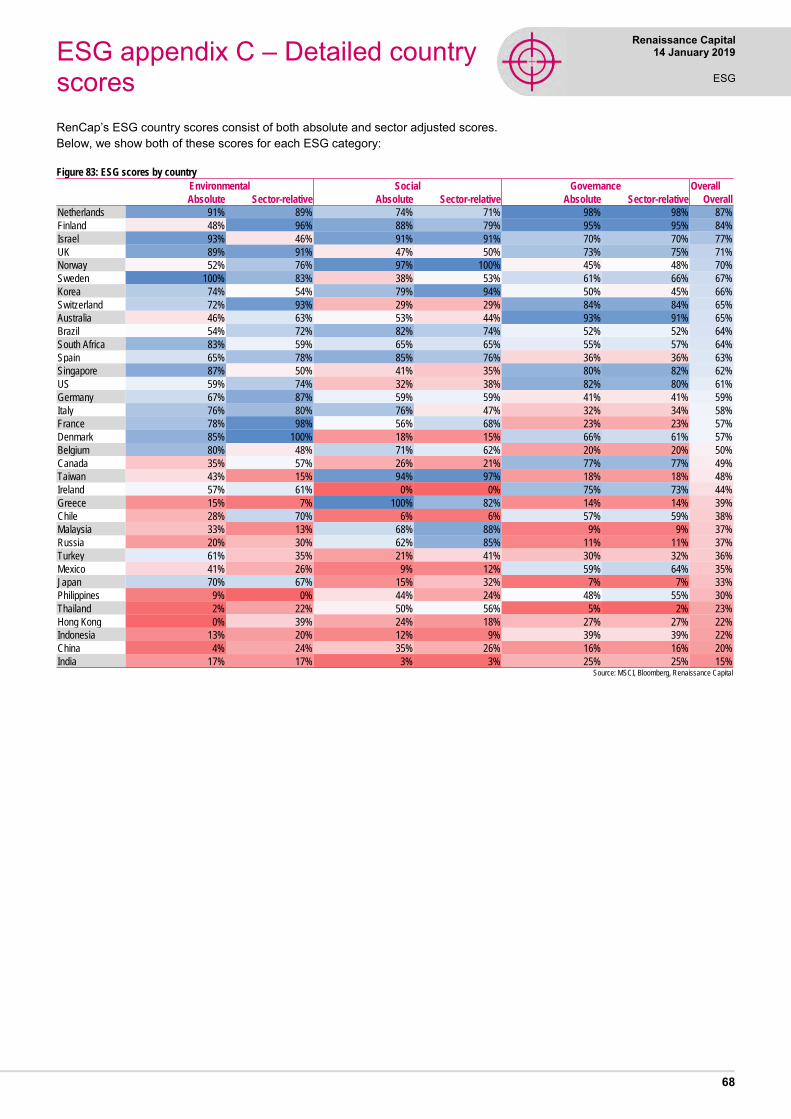

ESG appendix C – Detailed country scores 68

ESG appendix D – Full ESG breakdown for top/bottom EM companies 69

ESG appendix E – Full ESG breakdown for top/bottom EM EMEA companies 70

Take five 71

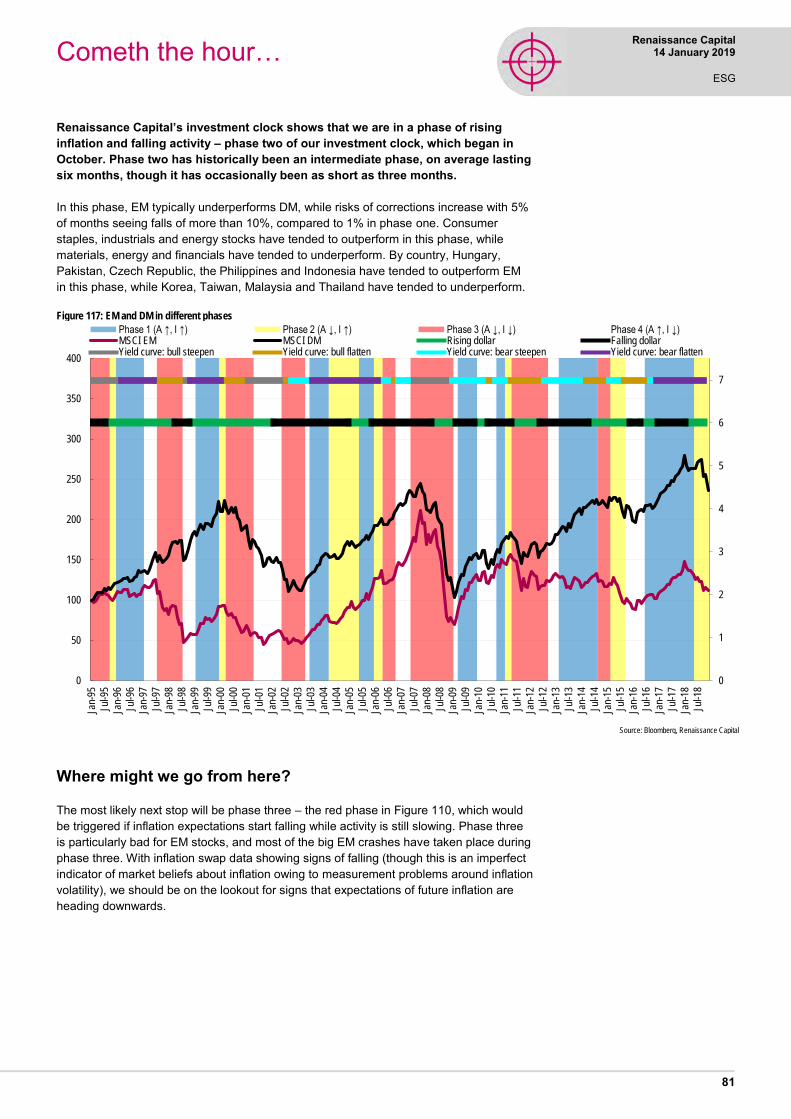

Cometh the hour… 81

ESG appendix F 85

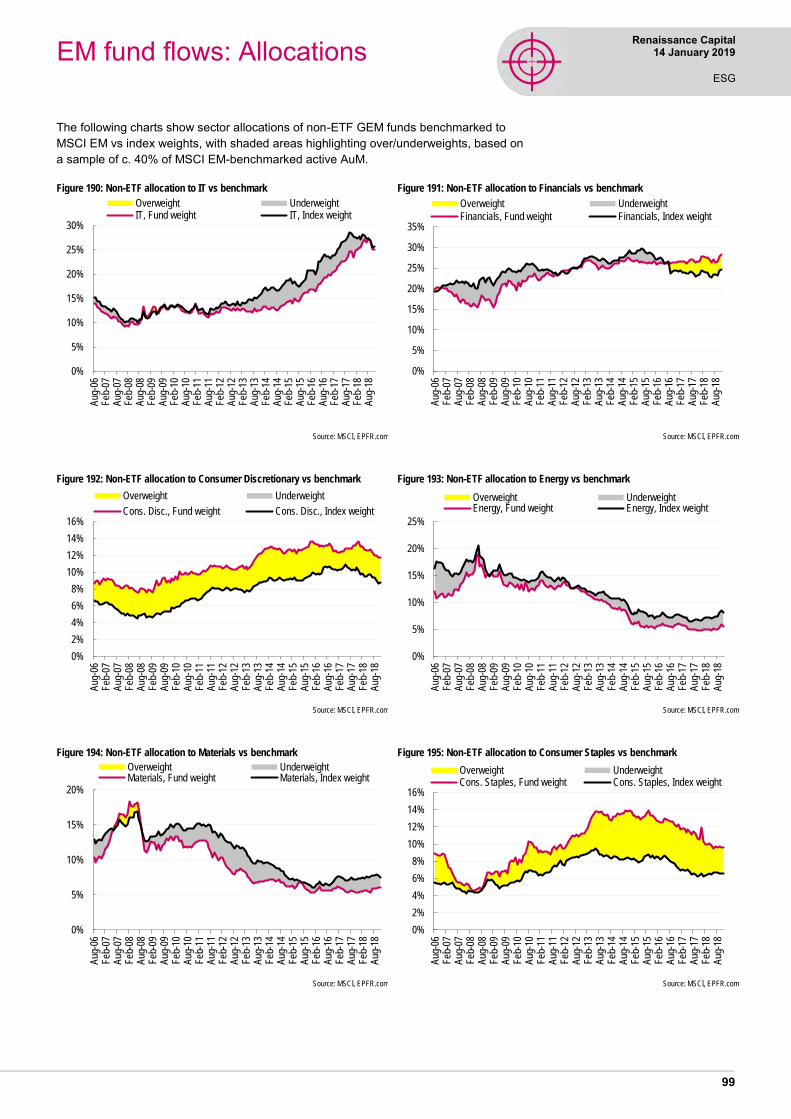

EM fund flows: Allocations 91

EM fund flows: Allocations 92

EM fund flows: Allocations 93

EM fund flows: Allocations 94

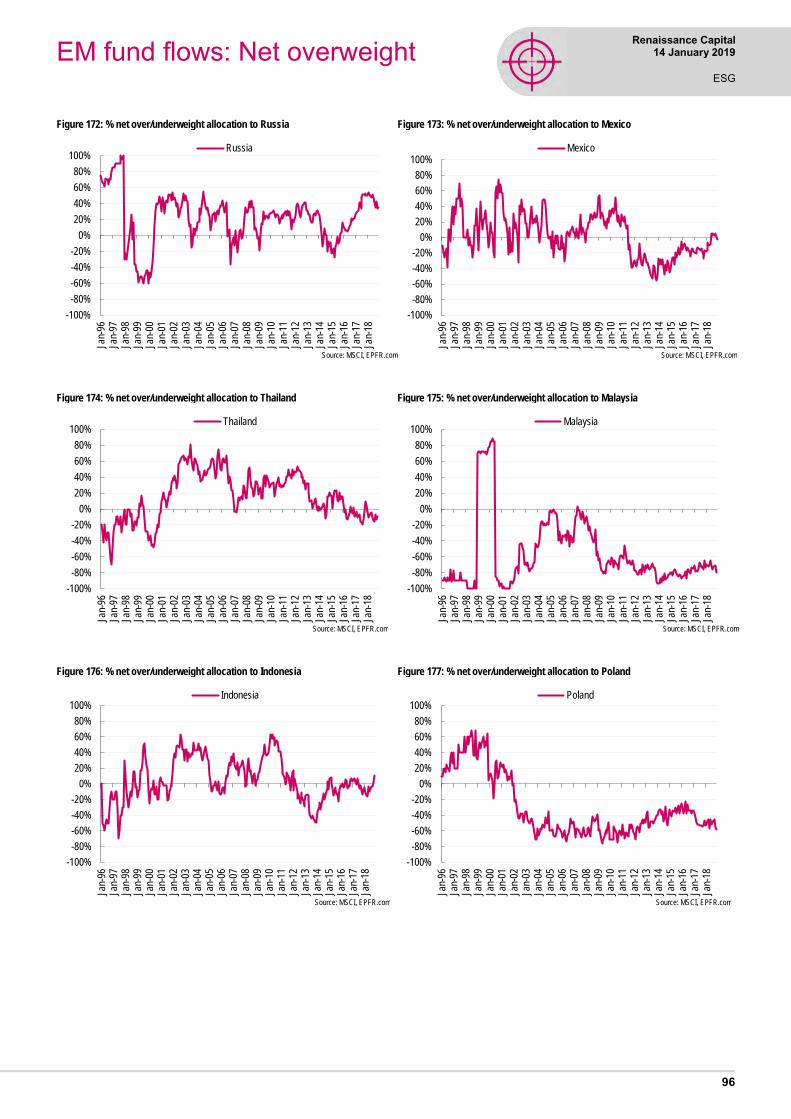

EM fund flows: Net overweight 95

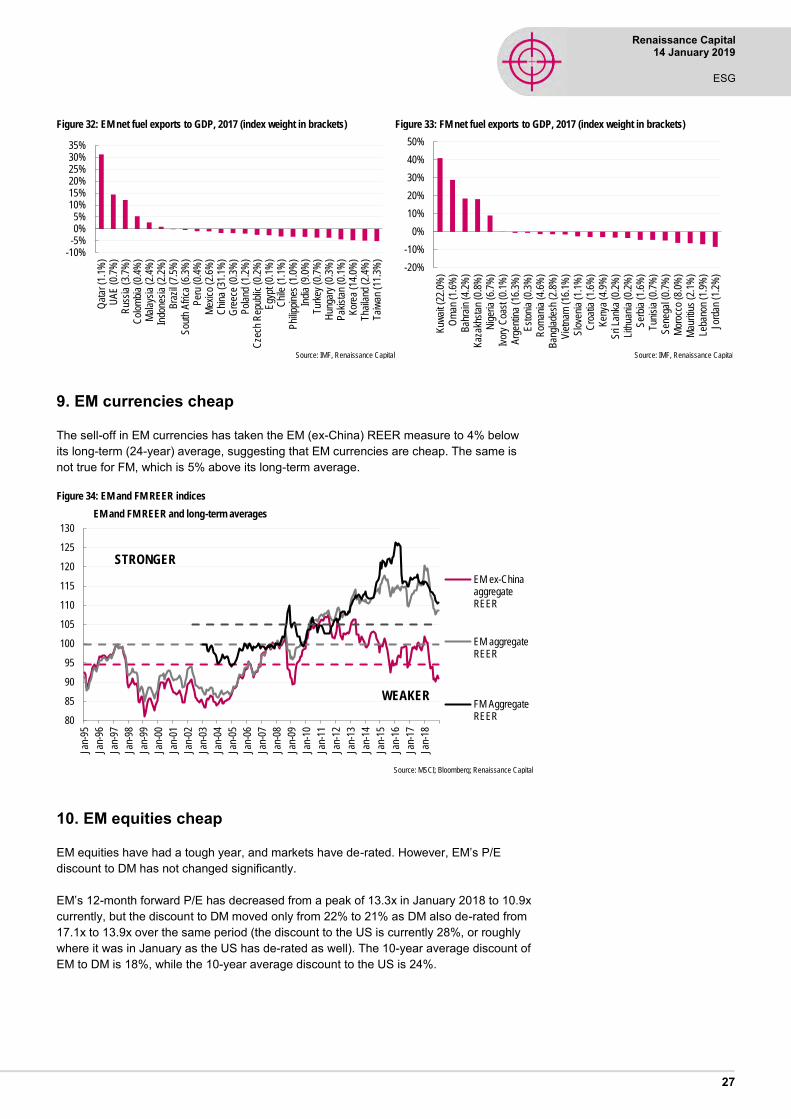

EM fund flows: Net overweight 96

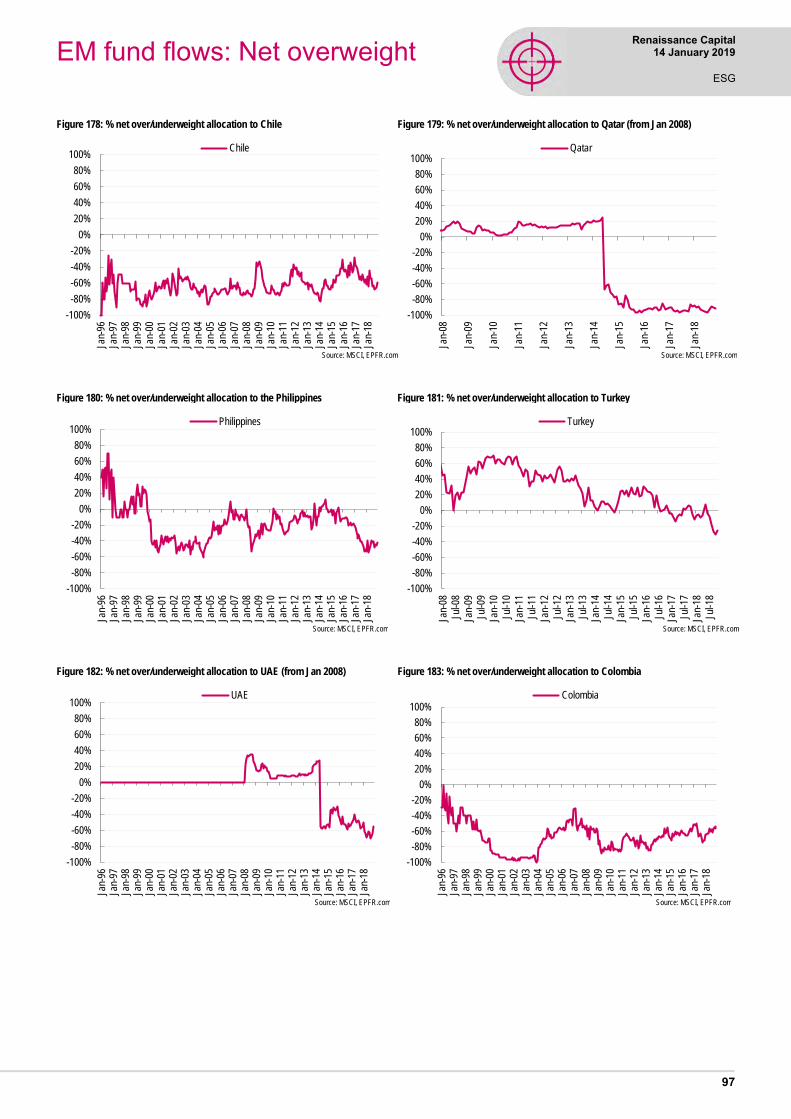

EM fund flows: Net overweight 97

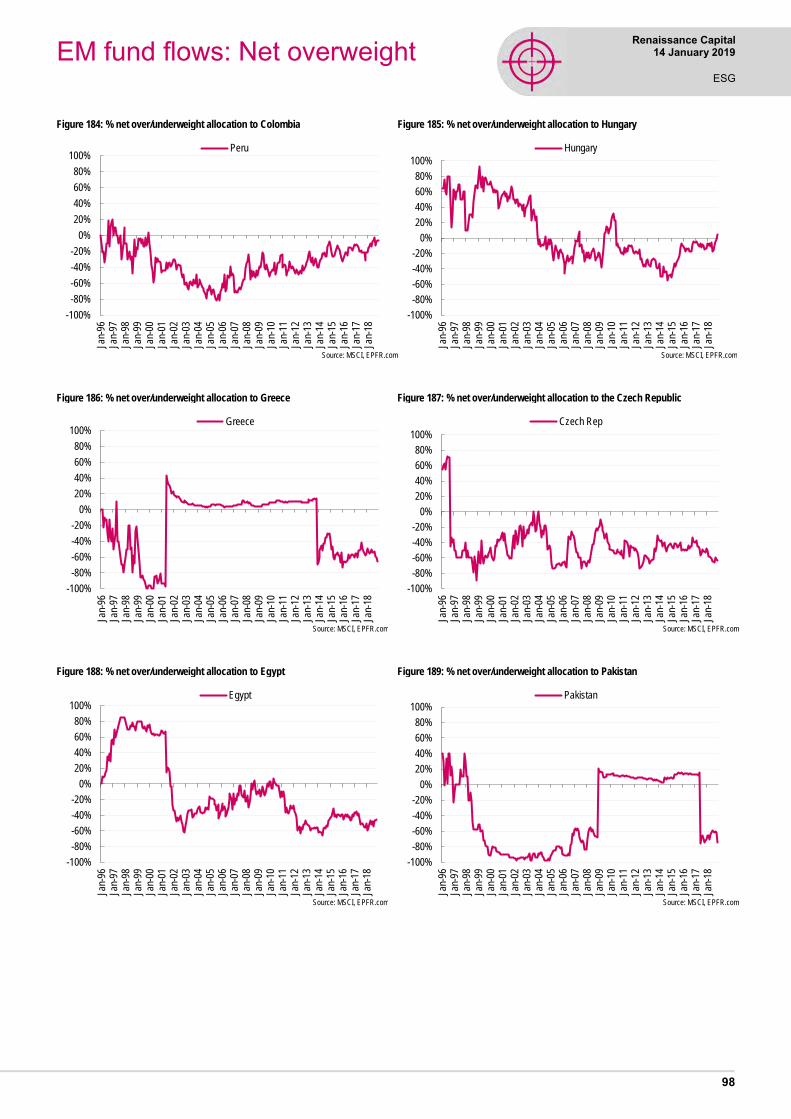

EM fund flows: Net overweight 98

EM fund flows: Allocations 99

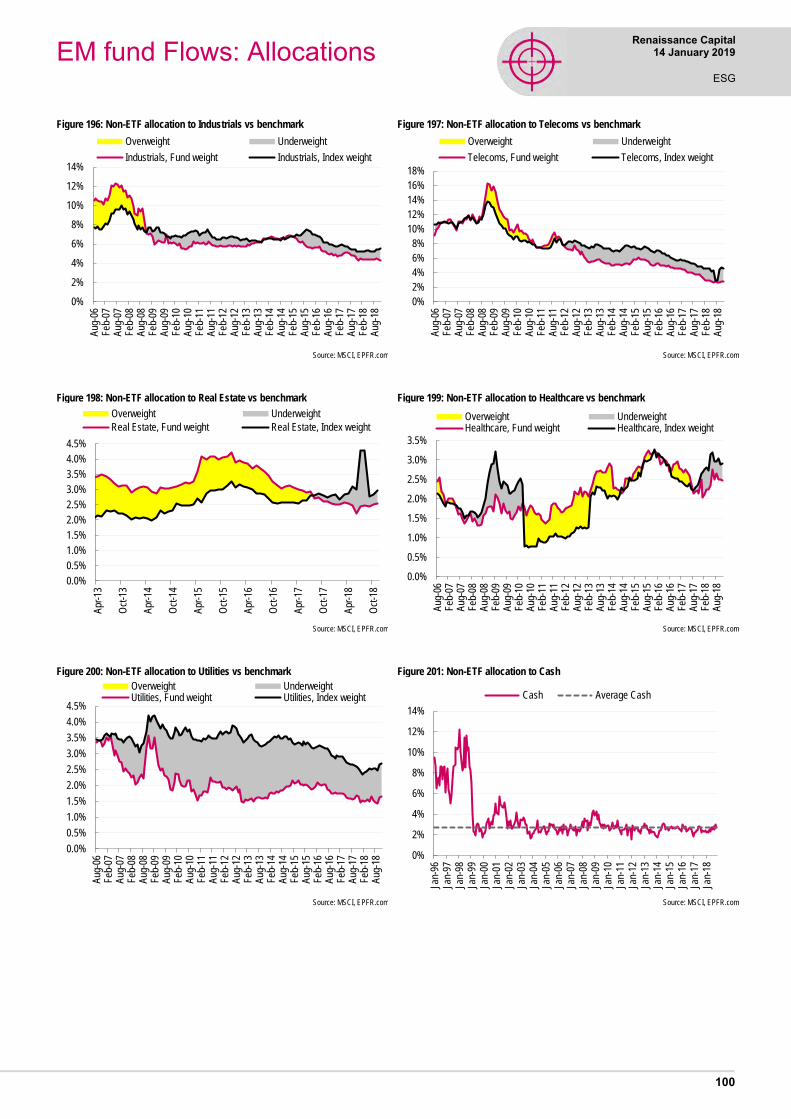

EM fund Flows: Allocations 100

Market watch 101

Disclosures appendix 102

Contents

Daniel Salter +44 (207) 005-7824 [email protected] Vikram Lopez +44 (207) 005-7974 [email protected] Charles Robertson +44 (207) 005-7835 [email protected] Yvonne Mhango +27 (11) 750-1488 [email protected] Oleg Kouzmin +7 (495)258-7770 x4506 [email protected] Research analysts

1

Renaissance Capital 14 January 2019

ESG

ESG

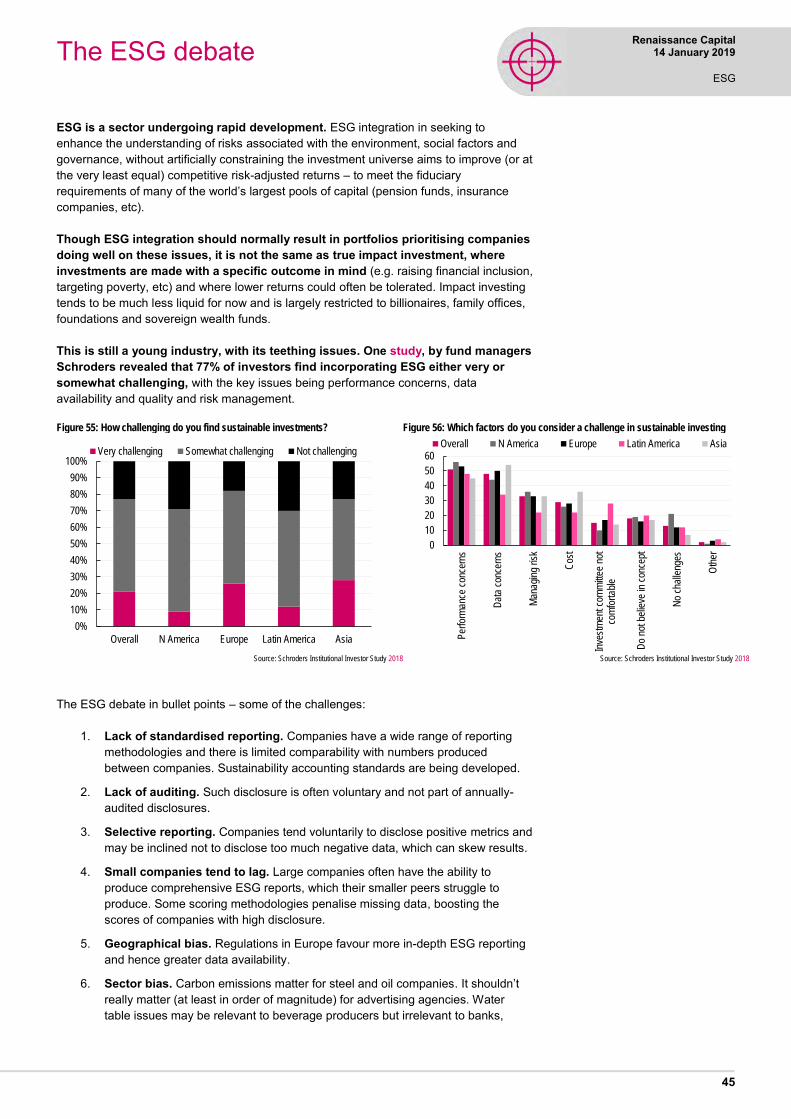

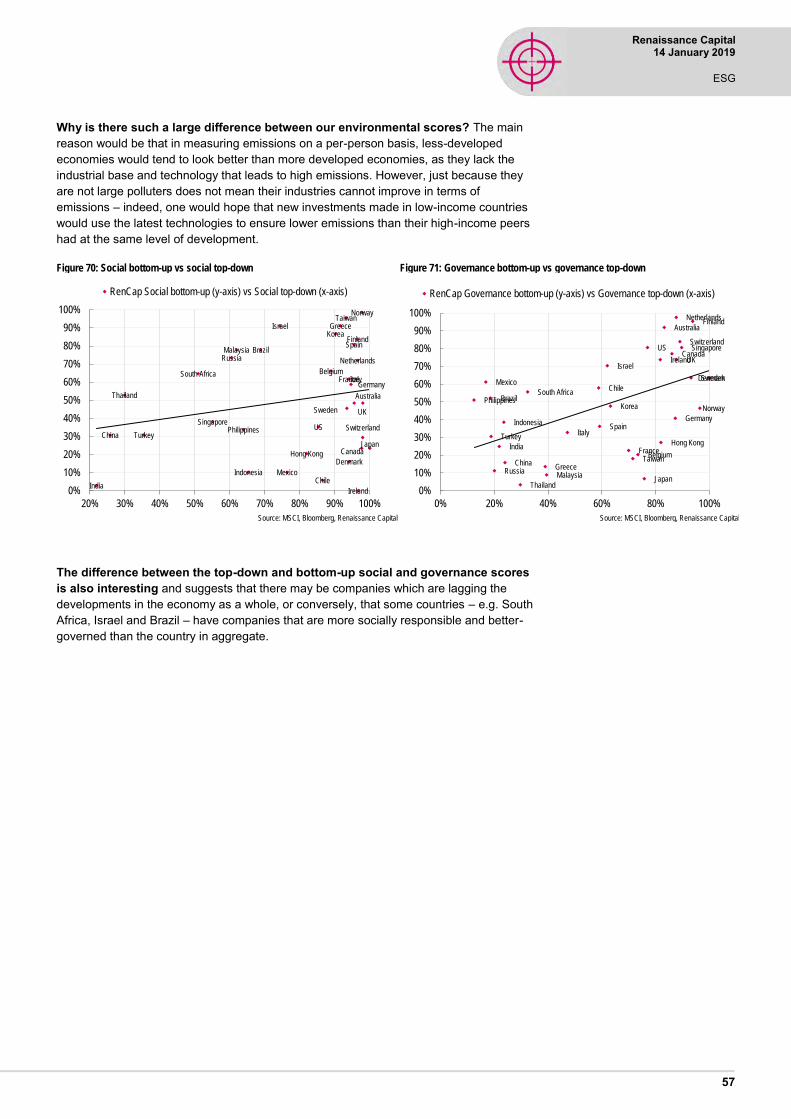

ESG (environmental, social and governance) investing is becoming increasingly important right along the investment chain – from asset owners to asset managers to corporates. We started to look at ESG from a top-down perspective in Global Chief Economist Charles Robertson’s ESG note, Reclaiming ESG in EM & FM. Here we look at some more bottom-up issues.

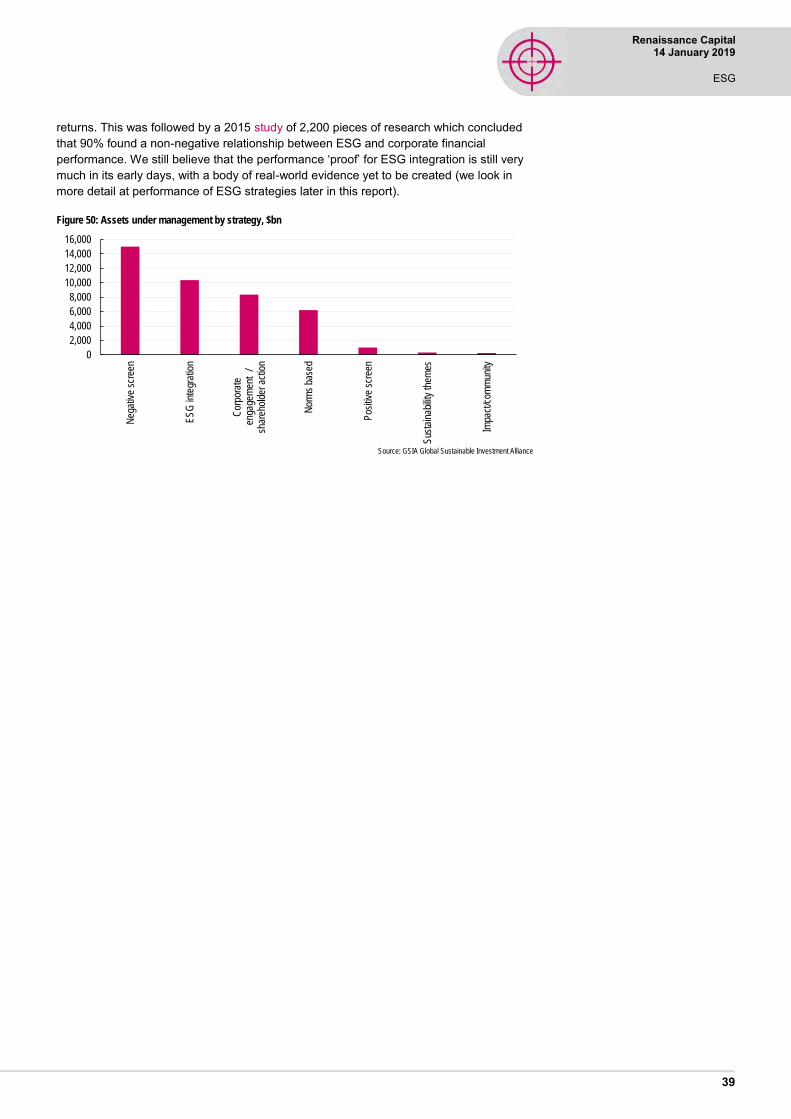

The Global Sustainable Investment Alliance estimates some $23trn of assets globally are managed under some form of ESG. Morningstar’s database contains $1.05trn of publicly-available ESG funds, and in EM, we have identified $21bn of publicly-available ESG equity funds, up from just $5bn at the start of 2016. Adding non-public funds would boost this figure significantly, and there are more and more mainstream funds (i.e. not specifically labelled as ESG) investing with at least one eye on ESG.

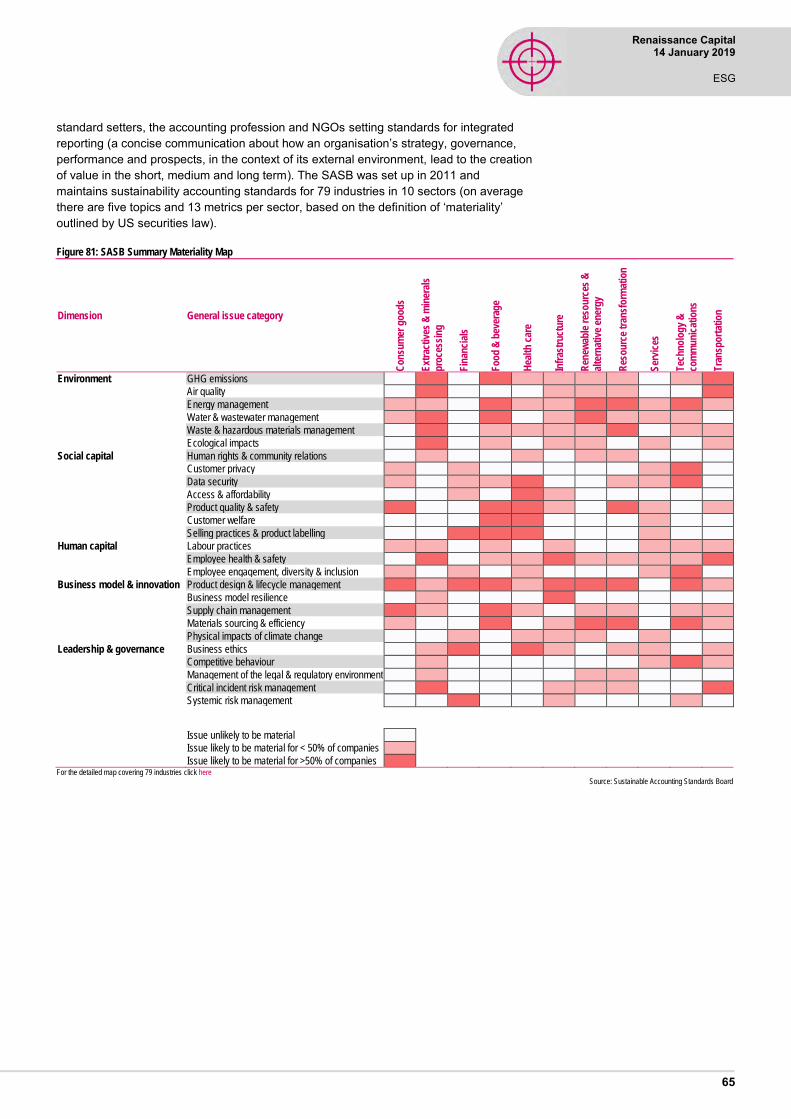

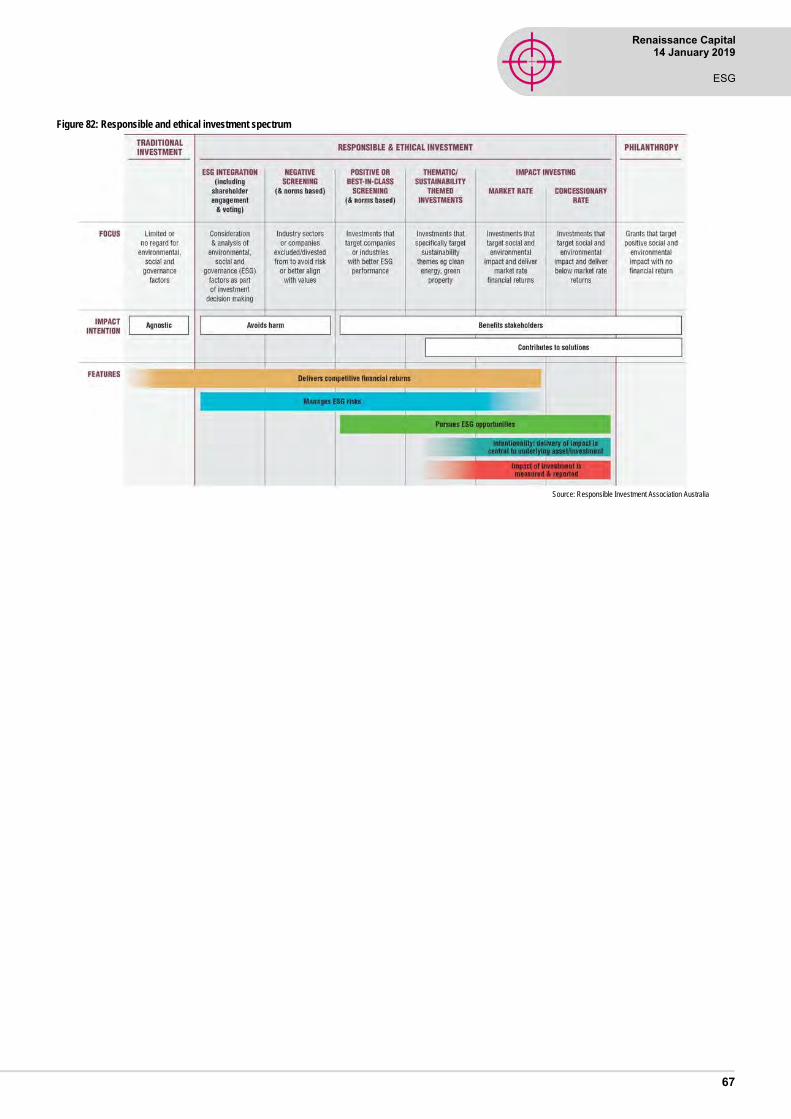

ESG covers a broad scope of strategies including traditional negative screens (e.g. not owning tobacco or weapons manufacturers), positive screens and best-in-class strategies (e.g. portfolios focused on the best ESG-scoring names), norms-based screens (excluding companies breaching international norms), thematic investing (e.g. focused on alternate energy) and impact investing (to have a measurable impact, e.g. on carbon emissions). ESG integration, where ESG is integrated throughout the investment process with the aim of improving risk-adjusted returns (key for ESG to go mainstream) is where the focus has been lately.

As ESG assets grow, and with it, corporate disclosure, companies which score well on ESG metrics should find themselves better positioned to attract a wider pool of capital and thus achieve higher valuations.

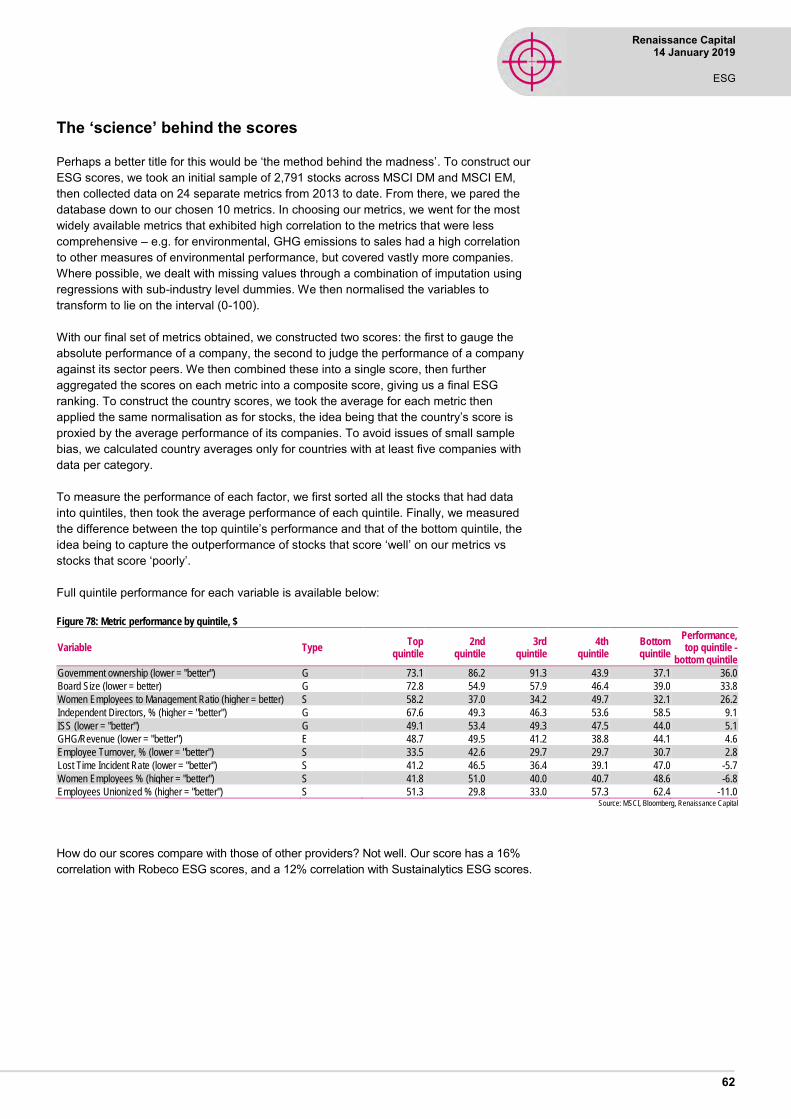

What metrics should corporates target? The list is ever growing, but we have developed a model focusing on: greenhouse gas emissions per sales; social factors such as women in the workforce and in management roles, worker safety and conditions; governance issues such as board independence and size, state ownership, and responsibilities to shareholders. Companies with lower government ownership, smaller boards and a higher representation of women in management tend to outperform.

The broader debate surrounding corporate citizenship is ongoing, and the neoclassical view (espoused most famously by Milton Friedman) that companies should focus solely on the pursuit of (legal) profits is being increasingly challenged. This analyst would suggest that any well-run business should be keen to understand the (changing) expectations put on it by broader society in addition to a focus on near-term profits, as taking care of the former should help make the latter more sustainable.

Strategy

2018 saw five overlapping waves of negativity overwhelm EM: 1) rising US rates (both bond yields and Fed funds); 2) a strong dollar; 3) escalating trade tensions; 4) global/Chinese growth concerns; and 5) the 4Q18 sell-off in US equities. Combined, these were enough to push EM equities into bear market territory, with MSCI EM ending 2018 down 17% for the year, 24% off its January peak. MSCI FM ended 2018 down 19% for the year, 25% off its January peak.

Our base case is that the US avoids recession in 2019 (which, this summer, will make the current expansion the longest since records began in the 1850s), but we expect growth to slow as the sugar rush of stimulus fades and given the lagged effects of higher borrowing costs, the stronger dollar, weaker external demand (accompanied by rising protectionism) and the partial government shutdown on the US economy. China, the eurozone and Japan are also likely to grow more slowly in 2019 vs 2018.

Investment summary

2

Renaissance Capital 14 January 2019

ESG

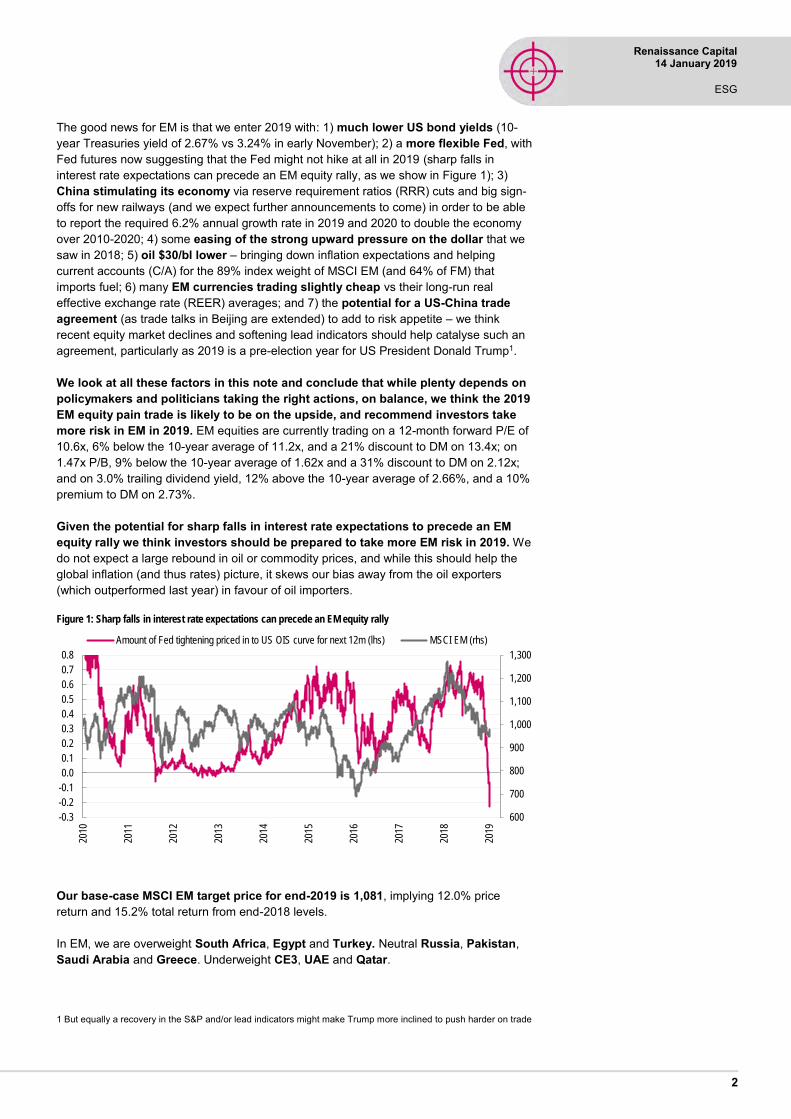

The good news for EM is that we enter 2019 with: 1) much lower US bond yields (10-year Treasuries yield of 2.67% vs 3.24% in early November); 2) a more flexible Fed, with Fed futures now suggesting that the Fed might not hike at all in 2019 (sharp falls in interest rate expectations can precede an EM equity rally, as we show in Figure 1); 3) China stimulating its economy via reserve requirement ratios (RRR) cuts and big sign-offs for new railways (and we expect further announcements to come) in order to be able to report the required 6.2% annual growth rate in 2019 and 2020 to double the economy over 2010-2020; 4) some easing of the strong upward pressure on the dollar that we saw in 2018; 5) oil $30/bl lower – bringing down inflation expectations and helping current accounts (C/A) for the 89% index weight of MSCI EM (and 64% of FM) that imports fuel; 6) many EM currencies trading slightly cheap vs their long-run real effective exchange rate (REER) averages; and 7) the potential for a US-China trade agreement (as trade talks in Beijing are extended) to add to risk appetite – we think recent equity market declines and softening lead indicators should help catalyse such an agreement, particularly as 2019 is a pre-election year for US President Donald Trump1.

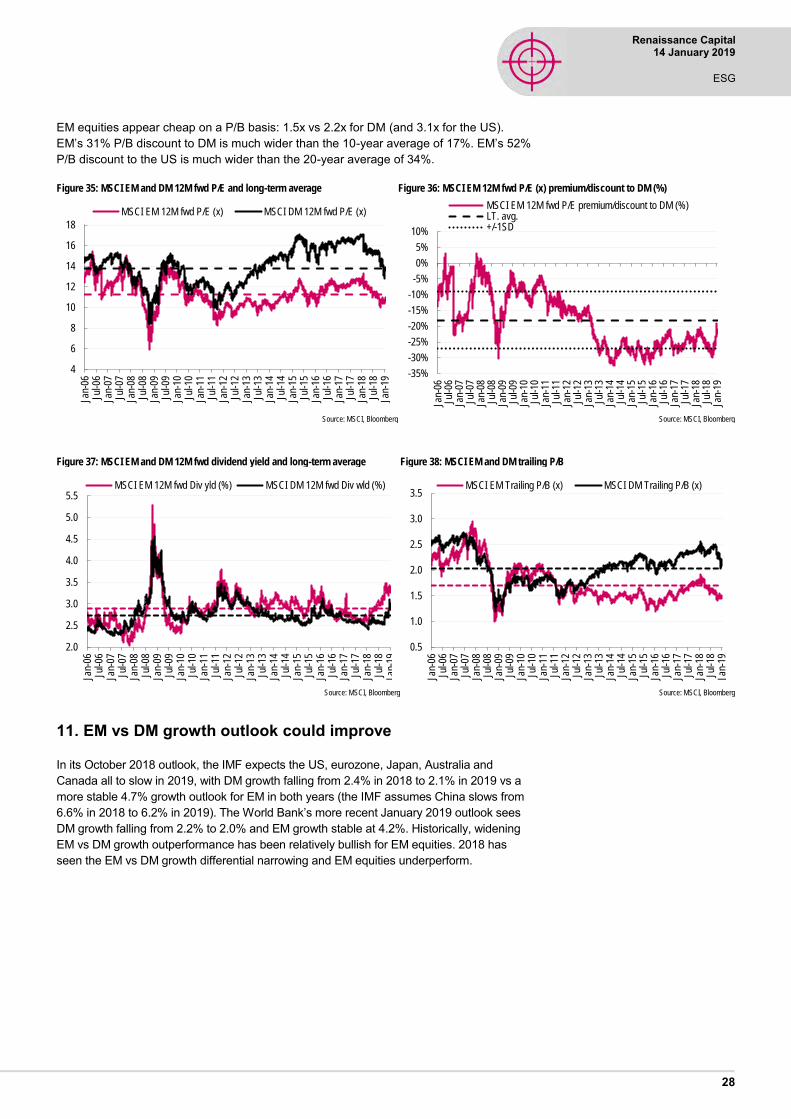

We look at all these factors in this note and conclude that while plenty depends on policymakers and politicians taking the right actions, on balance, we think the 2019 EM equity pain trade is likely to be on the upside, and recommend investors take more risk in EM in 2019. EM equities are currently trading on a 12-month forward P/E of 10.6x, 6% below the 10-year average of 11.2x, and a 21% discount to DM on 13.4x; on 1.47x P/B, 9% below the 10-year average of 1.62x and a 31% discount to DM on 2.12x; and on 3.0% trailing dividend yield, 12% above the 10-year average of 2.66%, and a 10% premium to DM on 2.73%.

Given the potential for sharp falls in interest rate expectations to precede an EM equity rally we think investors should be prepared to take more EM risk in 2019. We do not expect a large rebound in oil or commodity prices, and while this should help the global inflation (and thus rates) picture, it skews our bias away from the oil exporters (which outperformed last year) in favour of oil importers.

Figure 1: Sharp falls in interest rate expectations can precede an EM equity rally

Source: Bloomberg, Renaissance Capital

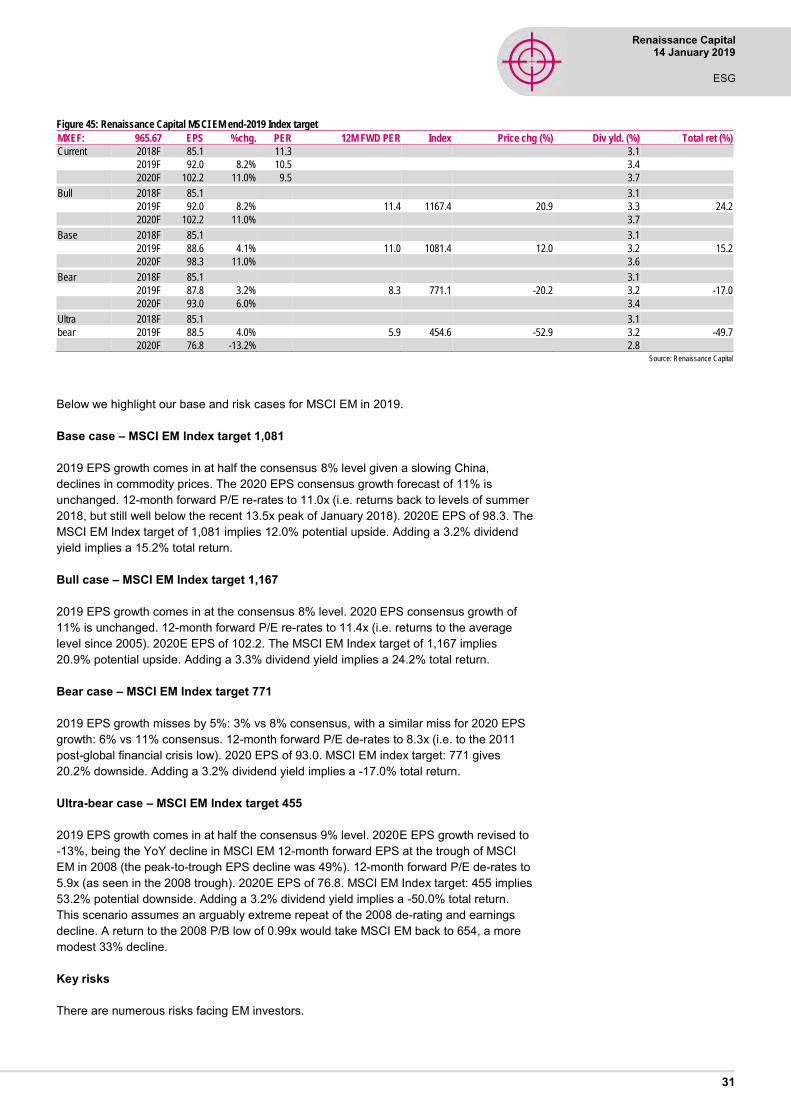

Our base-case MSCI EM target price for end-2019 is 1,081, implying 12.0% price return and 15.2% total return from end-2018 levels.

In EM, we are overweight South Africa, Egypt and Turkey. Neutral Russia, Pakistan, Saudi Arabia and Greece. Underweight CE3, UAE and Qatar.

1 But equally a recovery in the S&P and/or lead indicators might make Trump more inclined to push harder on trade

600

700

800

900

1,000

1,100

1,200

1,300

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

Amount of Fed tightening priced in to US OIS curve for next 12m (lhs) MSCI EM (rhs)

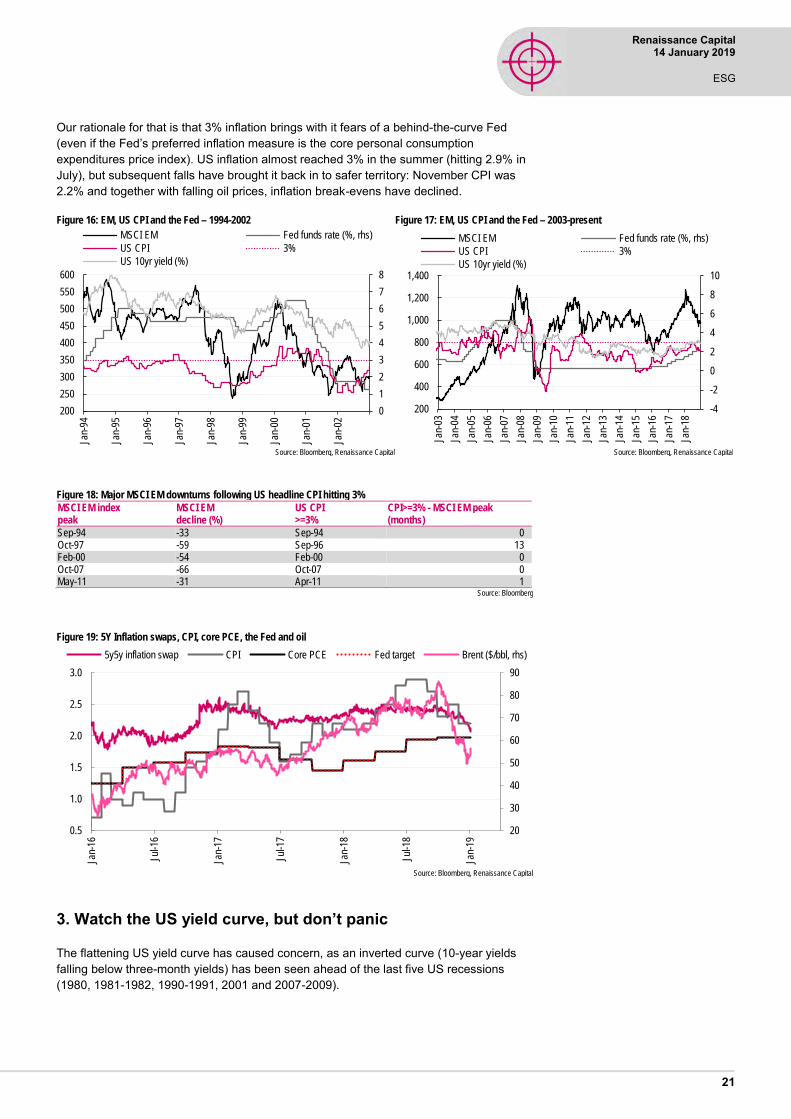

3

Renaissance Capital 14 January 2019

ESG

In FM, we are overweight Vietnam, Kazakhstan, Georgia, Argentina and Egypt. Neutral Romania, Kenya, Nigeria, Sri Lanka and Morocco. Underweight Bangladesh and Kuwait.

Our five-factor asset allocation model looks for countries with improving growth, faster bank lending, cheap currencies, scope for credit ratings to be upgraded and/or rate cuts (see page 69).

Emerging Markets

In EM, we are overweight South Africa, Egypt and Turkey. Neutral Russia, Pakistan, Saudi Arabia and Greece. Underweight CE3, UAE and Qatar.

Overweight

For the first time in recent years, our model is suggesting investors take a look at South Africa. The market was the fourth-worst performer in MSCI EM in 2018 as optimism over Cyril Ramaphosa’s presidency diminished in light of the lacklustre economy (and as index heavyweight Naspers sold off). It may be that the pre-election rhetoric remains tricky, but we don’t expect South Africa’s credit rating to be downgraded pre-election, and the economy should rebound gradually in 2019, and we expect bank lending to accelerate. We still see the ZAR as cheap on an REER basis and see the currency-rebound since the September-lows combined with the decline in oil prices as taking pressure off the South African Reserve Bank (SARB) to raise rates. We expect the market to look through populist pre-election statements, and see scope for a Ramaphosa 2.0 pre-election rally on the back of polls pointing to fading support for the Democratic Alliance (DA) and Economic Freedom Fighters (EFF) and a sizeable potential majority for the Africa National Congress (ANC), thus delivering a platform for the president to pursue reform. Coincidence or not, but the MSCI South Africa has had positive dollar returns in each of the last five election years going back to 1994.

Egyptian equities sold off sharply in 2018: the MSCI Egypt Investible Markets Index (which we tend to use in preference to the overly narrow, three constituent MSCI Egypt Index) closed the year 29% off its April peak and down 17% over the year as investors pushed out their rate cut forecasts from 2018 to 2019 given persistent inflation. The IMF expects the economy to accelerate in 2019, and for the C/A deficit to fall sub-2.5%. The decline in oil prices should help the story in 2019, and inflation has already fallen from 17.7% in October to 12.0% in December 2018. We see headline inflation in a 12-14% range from January to May 2019, before plunging to 8% by October 2019 (food price base effects) then picking back up to 11-13% until June 2020 (before falling back into single digits after the last subsidy removal falls out of the numbers in mid-2020). This means the Central Bank of Egypt (CBE): 1) should not need to hike interest rates now (we believe the CBE is forward looking); and 2) can start considering rate cuts in mid-2019. The currency is still cheap on our REER model, but inflation is eroding the undervaluation, and we hope the authorities will prioritise introducing greater exchange rate flexibility before the EGP reaches fair value (around end-2019) and then starts to get overvalued.

Turkey announced a record C/A surplus in October, and November’s was a fourth month of surplus – confirming: 1) how cheap the TRY has become (the cheapest in EM on our REER measure); and 2) the extent of the domestic slowdown (new passenger car sales, for example, were down 43% YoY in November). We expect the government to support the banking sector if required. In 2019, we expect growth of just 0.8%, but see upside risks to this (consensus and the IMF are more bearish). An environment of fewer Fed hikes and lower oil would benefit Turkey and allow rates to fall faster from the current 24%

4

Renaissance Capital 14 January 2019

ESG

level. One risk for the market could be economic populism ahead of March’s local elections, including renewed pressure on the central bank to cut rates. The shifting of VW production capacity from Central Europe to Turkey we see as demonstrating Turkey’s ability to gain manufacturing investment given full employment and poor demographics in Central Europe. Turkey was the worst-performing market in MSCI EM in 2018, down 43.6%. The market has de-rated by 30% vs its long-run average 12-month forward P/E: 6.3x v 8.9x (making Turkey the second-cheapest market in EM after Russia).

Neutral

Pakistan is starting to look interesting to us. The currency is now cheap on our REER model, and Pakistan was the second worst-performing market in MSCI EM in 2018, down 37.8%. Though IMF negotiations are complex, we expect them to continue – and an agreement would increase our enthusiasm for the market: the market is trading on a 12-month forward P/E of 7x down from a 2017 peak of 11.5x as FM investors have sold down and EM investors failed to engage.

Our lacklustre outlook on oil leads us to downgrade oil exporters.

Russia we take back to neutral. The equity market was the fourth-best performer in EMEA last year (declining just 5.6%) as Russia was seen as resilient to higher US rates and trade wars. Russia has strong valuation support, companies are paying higher dividends and the geopolitical backdrop has helped catalyse economic reforms designed to make the economy bullet-proof. However, we see headwinds to the consumer story in 2019 given the increase in VAT and higher inflation/rates. The lower oil price is not positive, but is not destabilising in our opinion given the flexible exchange rate, low oil-price breakeven and external deleveraging – our long-term regression suggests the market is currently pricing in $61/bl oil, and is thus trading around fair value. However, with Brent at $60/bl, well below the Bloomberg consensus of $70/bl, downgrades to consensus earnings may be necessary. On a relative basis, given our expectation of no major rebound in oil, we would expect Russia to lag an EM recovery in 2019. We still find it a challenge to find marginal investors given EM investors are already overweight Russia, and the risk of further sanctions on Russia in 2019 is likely to deter crossover investors – even if the momentum of new sanctions appears to have slowed (e.g. potential Congressional sanctions on US investors buying newly issued sovereign debt appear to have been pushed back).

Saudi Arabia we also cut to neutral. The oil price drop takes oil below Saudi Arabia’s fiscal breakeven of $83/bl in 2018 ($73/bl in 2019) according to the IMF, hampering the authorities’ ability to stimulate the economy. MSCI Saudi Arabia was up 15.1% in 2018, which would have made it the second-best performer in MSCI EM had it already been included in the index (inclusion is due in two tranches in May and August 2019) on the back of fiscal stimulus, ahead of the MSCI EM index inclusion, and with the authorities reportedly using government-linked funds to help support the market. We would trim into strength in the run-up to MSCI inclusion at these levels.

Greece scores well on our top-down screen. But this was the case in both 2017 and 2018 and in both years MSCI Greece underperformed MSCI EM. We have to concede that our model can’t capture the nuances of Greece’s banks, but with Greece having underperformed EM for five years in a row, at some point we should expect a rebound: 2019 will be a third consecutive year of growth for the Greek economy. Legislative elections due by October could be a potential trigger, given the lead enjoyed by New Democracy over Syriza in opinion polls.

5

Renaissance Capital 14 January 2019

ESG

Underweight

GCC markets we have reduced our enthusiasm on given strong performance in 2018 – we had liked their pegged currencies, oil exposure, rebounding economies and the positive margin impact on the banks of higher rates. Qatar was the top-performing market in EM (up 23.9%) in 2018 and Saudi Arabia (up 15.1%) would have been the second if it was already included in the MSCI EM index. Kuwait (up 11.1%) was the top-performing market in MSCI FM. The oil price dip tempers our enthusiasm, and if the dollar rally fades or reverses, the defensiveness of pegged currencies could prove less valuable. We move from overweight to underweight in aggregate, given the strong 2018 performance, decline in oil prices and continued declines in Dubai property prices. We are underweight Qatar, UAE and Kuwait, and neutral Saudi Arabia, which we would trim into MSCI inclusion related strength.

CE3 ought to be a relative safe haven in a major sell-off given a lack of macro-imbalances and EU membership (indeed, the three CE3 countries all outperformed MSCI EM in 2018) but we would expect them to lag a rebound in EM given their exposure to slowing eurozone growth (and the auto sector) as well as relatively full valuations. Labour market shortages are leading to more rapid wage increases, underpinning the consumer story.

Frontier Markets

In FM, we are overweight Vietnam, Kazakhstan, Georgia, Argentina and Egypt. Neutral Romania, Kenya, Nigeria, Sri Lanka and Morocco. Underweight Bangladesh and Kuwait.

Overweight

Vietnam – The market has de-rated significantly, from a 12-month forward P/E of 24.9x in March to 15.7x. Planned increases in foreign investor limits could attract additional foreign interest, particularly as Argentina (currently 17% of MSCI FM) transitions from MSCI Frontier to MSCI EM in May. Vietnam could be a winner in offshoring of production from China seeking to reduce the C/A surplus with the US. A more stable CNY could ease pressure to weaken the VND.

Kazakhstan – Though oil has fallen, the equity market is very cheap (MSCI Kazakhstan trades on a 12-month forward P/E of just 5x). Volume growth in hydrocarbons provides underpin for the economy and together with stronger demographics provides a better growth story than Russia (without sanction risk). The reform agenda, such as floating the currency, progress on resolving bad loans in the banking sector, financial market reforms and much needed privatisations (given the narrow stock market) make Kazakhstan one of our favoured oil producers.

Georgia – Share price declines have brought Georgia’s highly profitable banks back to attractive valuations (c. 1.4x trailing book value). Seasonal weakness for the GEL is possible during the low season for tourism. The authorities are trying to de-risk the economy (e.g. keeping a lid on consumer credit) as part of their aim to achieve an investment-grade sovereign credit rating.

Argentina – After heavy losses in 1H (Argentina was by far the worst performing in MSCI Frontier in 2018, declining 51.7%), the market has flatlined as the government perseveres with its austerity programme. The central bank’s ultra-tight monetary policy has kept a lid on equities, with the market trading on a 12-month forward P/E of 10x vs a peak of 16x in October 2017, but progress on bringing down inflation expectations has allowed the central bank to remove the 60% floor for rates. Argentina now has the second-cheapest

6

Renaissance Capital 14 January 2019

ESG

currency on our REER model in EM (we use ‘shadow’ inflation data for Argentina). The finance ministry has been guiding for a return to growth in 1H19, which would be a positive for President Mauricio Macri heading into October’s elections, though political risks remain.

Egypt – see above

Neutral

Romania – We had been worried about the economy overheating. We’re less worried about this now, as the economy has slowed and the government seems keen to bring the budget deficit sub-3% of GDP. Good for bonds, but less so for equities given the new bank and other sectoral taxes. Romania’s minimum wage has grown at the fastest rate in the EU over the past decade and is converging with Hungarian levels, which suggests that industrial competitiveness could be at threat.

Sri Lanka – The political crisis that prompted Moody’s, S&P and Fitch to cut the country’s credit rating appears to have been resolved peacefully for now with President Maithripala Sirisena reinstating Prime Minister Ranil Wickremesinghe, this could help equity markets provided political tensions do not return. Early elections are possible in 2019.

Kenya – The decline in the oil price is a positive for Kenya, for both inflation and the C/A deficit. The debate on the rate cap is ongoing, but provides growth optionality for the banks which already generate high RoEs and have de-rated from an average 12-month forward P/B of 1.6x for the three largest banks in April to 1.2x currently for 18% return on equity. Much depends on the government’s ability to cut the budget deficit without overly penalising the corporate sector.

Nigeria – With a lower oil price and the NGN already trading above fair value on our REER model, the concern is that the Nigerian story becomes increasingly reliant on foreign flows. The growth recovery is lacklustre, with real GDP growth likely to lag working age population growth in 2019 (for a fifth year), resulting in a recessionary economic backdrop. The 16 February general election needs to pass for us to become more certain on the 2019 equity market story, and we’d like to see greater flexibility for the naira. Cheap valuations in the banks suggest maintaining some exposure though.

Morocco – Under-owned by foreign investors, with a currency trading in line with its long-run REER, low interest rates and a stock market closely held by local pension funds we see Morocco as a long-term industrialisation beneficiary in North Africa. However, on a 12-month forward P/E of 17.5x we fail to find value.

Underweight

Bangladesh – Bangladesh has the most expensive currency in Frontier on our REER model (though the strengthening INR may help ease devaluation pressure). Although the market has de-rated from a 12-month forward P/E of 17x in January 2018 to 14x, the market is still expensive vs 9x for MSCI FM, given limited transparency of many companies. Though the election seems to have passed relatively peacefully, tightening of bank loan to deposit ratio targets post-election could slow bank lending and/or the economy. A potential longer-term beneficiary of Asian firms reallocating low wage production from China.

Kuwait – As with other GCC countries, our lower oil price outlook diminishes our enthusiasm. The market has been the top performer in MSCI Frontier over 2018, up 11.1%, with low foreign ownership and pegged currency keeping the market defensive. We expect Kuwait to underperform a more positive EM/FM backdrop, particularly if oil

7

Renaissance Capital 14 January 2019

ESG

stays subdued and given friction between the legislature and executive. As a large market, Kuwait might find itself a beneficiary of Frontier funds reallocating out of Argentina (currently 17% of MSCI Frontier) as it transitions from MSCI Frontier to MSCI EM. Kuwait itself is under review by MSCI for a potential transition to EM in 2020.

Renaissance Capital 14 January 2019

ESG

8

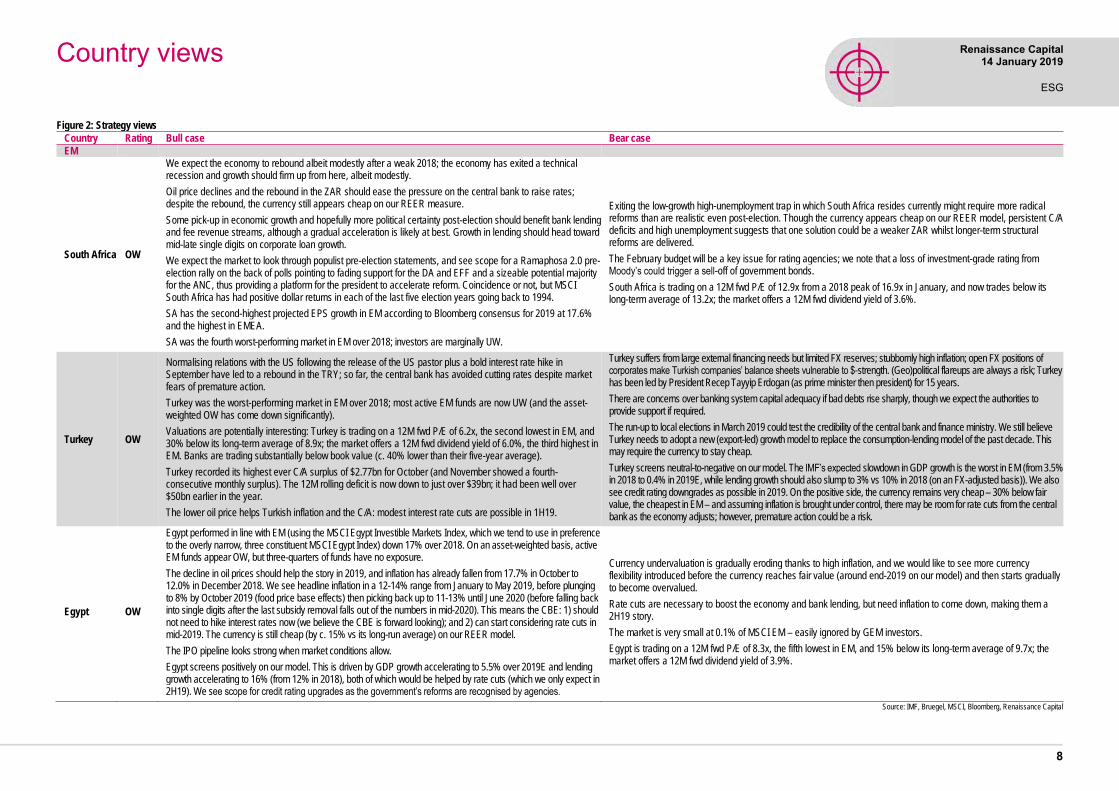

Figure 2: Strategy views

Country Rating Bull case Bear case

EM

South Africa OW

We expect the economy to rebound albeit modestly after a weak 2018; the economy has exited a technical recession and growth should firm up from here, albeit modestly.

Oil price declines and the rebound in the ZAR should ease the pressure on the central bank to raise rates; despite the rebound, the currency still appears cheap on our REER measure.

Some pick-up in economic growth and hopefully more political certainty post-election should benefit bank lending and fee revenue streams, although a gradual acceleration is likely at best. Growth in lending should head toward mid-late single digits on corporate loan growth.

We expect the market to look through populist pre-election statements, and see scope for a Ramaphosa 2.0 pre-election rally on the back of polls pointing to fading support for the DA and EFF and a sizeable potential majority for the ANC, thus providing a platform for the president to accelerate reform. Coincidence or not, but MSCI South Africa has had positive dollar returns in each of the last five election years going back to 1994.

SA has the second-highest projected EPS growth in EM according to Bloomberg consensus for 2019 at 17.6% and the highest in EMEA.

SA was the fourth worst-performing market in EM over 2018; investors are marginally UW.

Exiting the low-growth high-unemployment trap in which South Africa resides currently might require more radical reforms than are realistic even post-election. Though the currency appears cheap on our REER model, persistent C/A deficits and high unemployment suggests that one solution could be a weaker ZAR whilst longer-term structural reforms are delivered.

The February budget will be a key issue for rating agencies; we note that a loss of investment-grade rating from Moody’s could trigger a sell-off of government bonds.

South Africa is trading on a 12M fwd P/E of 12.9x from a 2018 peak of 16.9x in January, and now trades below its long-term average of 13.2x; the market offers a 12M fwd dividend yield of 3.6%.

Turkey OW

Normalising relations with the US following the release of the US pastor plus a bold interest rate hike in September have led to a rebound in the TRY; so far, the central bank has avoided cutting rates despite market fears of premature action.

Turkey was the worst-performing market in EM over 2018; most active EM funds are now UW (and the asset-weighted OW has come down significantly).

Valuations are potentially interesting: Turkey is trading on a 12M fwd P/E of 6.2x, the second lowest in EM, and 30% below its long-term average of 8.9x; the market offers a 12M fwd dividend yield of 6.0%, the third highest in EM. Banks are trading substantially below book value (c. 40% lower than their five-year average).

Turkey recorded its highest ever C/A surplus of $2.77bn for October (and November showed a fourth-consecutive monthly surplus). The 12M rolling deficit is now down to just over $39bn; it had been well over $50bn earlier in the year.

The lower oil price helps Turkish inflation and the C/A: modest interest rate cuts are possible in 1H19.

Turkey suffers from large external financing needs but limited FX reserves; stubbornly high inflation; open FX positions of corporates make Turkish companies’ balance sheets vulnerable to $-strength. (Geo)political flareups are always a risk; Turkey has been led by President Recep Tayyip Erdogan (as prime minister then president) for 15 years.

There are concerns over banking system capital adequacy if bad debts rise sharply, though we expect the authorities to provide support if required.

The run-up to local elections in March 2019 could test the credibility of the central bank and finance ministry. We still believe Turkey needs to adopt a new (export-led) growth model to replace the consumption-lending model of the past decade. This may require the currency to stay cheap.

Turkey screens neutral-to-negative on our model. The IMF’s expected slowdown in GDP growth is the worst in EM (from 3.5% in 2018 to 0.4% in 2019E, while lending growth should also slump to 3% vs 10% in 2018 (on an FX-adjusted basis)). We also see credit rating downgrades as possible in 2019. On the positive side, the currency remains very cheap – 30% below fair value, the cheapest in EM – and assuming inflation is brought under control, there may be room for rate cuts from the central bank as the economy adjusts; however, premature action could be a risk.

Egypt OW

Egypt performed in line with EM (using the MSCI Egypt Investible Markets Index, which we tend to use in preference to the overly narrow, three constituent MSCI Egypt Index) down 17% over 2018. On an asset-weighted basis, active EM funds appear OW, but three-quarters of funds have no exposure.

The decline in oil prices should help the story in 2019, and inflation has already fallen from 17.7% in October to 12.0% in December 2018. We see headline inflation in a 12-14% range from January to May 2019, before plunging to 8% by October 2019 (food price base effects) then picking back up to 11-13% until June 2020 (before falling back into single digits after the last subsidy removal falls out of the numbers in mid-2020). This means the CBE: 1) should not need to hike interest rates now (we believe the CBE is forward looking); and 2) can start considering rate cuts in mid-2019. The currency is still cheap (by c. 15% vs its long-run average) on our REER model.

The IPO pipeline looks strong when market conditions allow.

Egypt screens positively on our model. This is driven by GDP growth accelerating to 5.5% over 2019E and lending growth accelerating to 16% (from 12% in 2018), both of which would be helped by rate cuts (which we only expect in 2H19). We see scope for credit rating upgrades as the government’s reforms are recognised by agencies.

Currency undervaluation is gradually eroding thanks to high inflation, and we would like to see more currency flexibility introduced before the currency reaches fair value (around end-2019 on our model) and then starts gradually to become overvalued.

Rate cuts are necessary to boost the economy and bank lending, but need inflation to come down, making them a 2H19 story.

The market is very small at 0.1% of MSCI EM – easily ignored by GEM investors.

Egypt is trading on a 12M fwd P/E of 8.3x, the fifth lowest in EM, and 15% below its long-term average of 9.7x; the market offers a 12M fwd dividend yield of 3.9%.

Source: IMF, Bruegel, MSCI, Bloomberg, Renaissance Capital

Country views

Renaissance Capital 14 January 2019

ESG

9

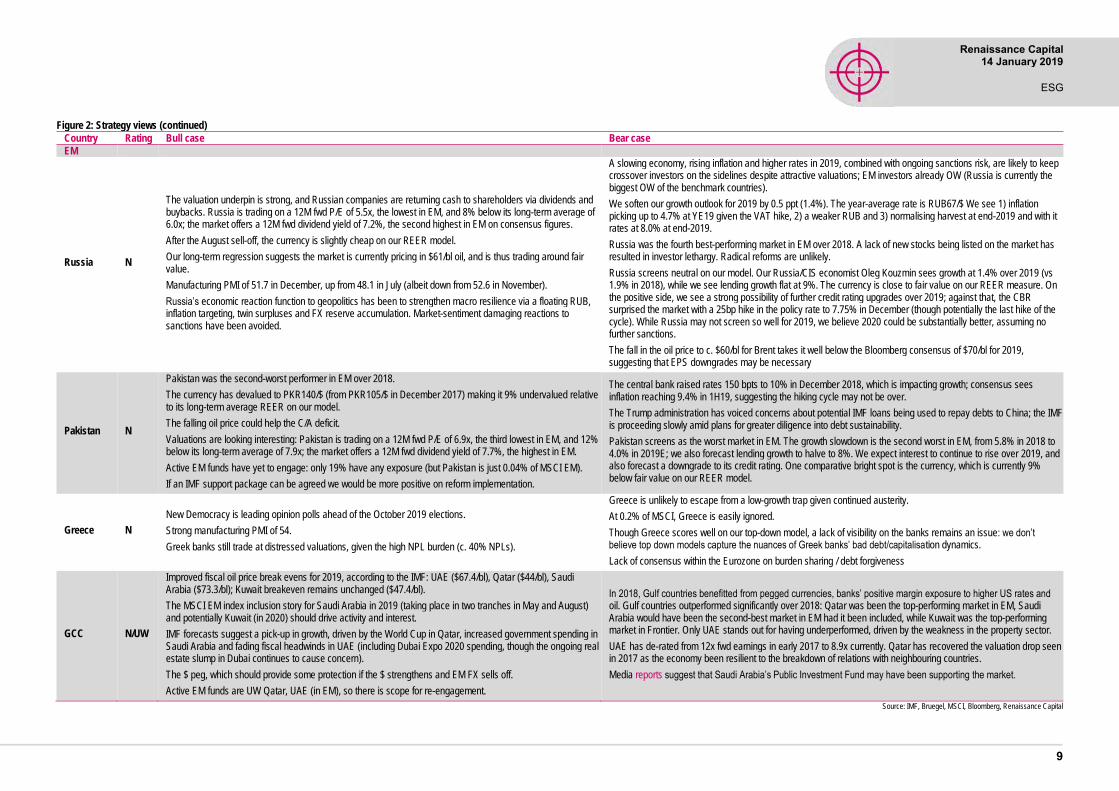

Figure 2: Strategy views (continued)

Country Rating Bull case Bear case

EM

Russia N

The valuation underpin is strong, and Russian companies are returning cash to shareholders via dividends and buybacks. Russia is trading on a 12M fwd P/E of 5.5x, the lowest in EM, and 8% below its long-term average of 6.0x; the market offers a 12M fwd dividend yield of 7.2%, the second highest in EM on consensus figures.

After the August sell-off, the currency is slightly cheap on our REER model.

Our long-term regression suggests the market is currently pricing in $61/bl oil, and is thus trading around fair value.

Manufacturing PMI of 51.7 in December, up from 48.1 in July (albeit down from 52.6 in November).

Russia’s economic reaction function to geopolitics has been to strengthen macro resilience via a floating RUB, inflation targeting, twin surpluses and FX reserve accumulation. Market-sentiment damaging reactions to sanctions have been avoided.

A slowing economy, rising inflation and higher rates in 2019, combined with ongoing sanctions risk, are likely to keep crossover investors on the sidelines despite attractive valuations; EM investors already OW (Russia is currently the biggest OW of the benchmark countries).

We soften our growth outlook for 2019 by 0.5 ppt (1.4%). The year-average rate is RUB67/$ We see 1) inflation picking up to 4.7% at YE19 given the VAT hike, 2) a weaker RUB and 3) normalising harvest at end-2019 and with it rates at 8.0% at end-2019.

Russia was the fourth best-performing market in EM over 2018. A lack of new stocks being listed on the market has resulted in investor lethargy. Radical reforms are unlikely.

Russia screens neutral on our model. Our Russia/CIS economist Oleg Kouzmin sees growth at 1.4% over 2019 (vs 1.9% in 2018), while we see lending growth flat at 9%. The currency is close to fair value on our REER measure. On the positive side, we see a strong possibility of further credit rating upgrades over 2019; against that, the CBR surprised the market with a 25bp hike in the policy rate to 7.75% in December (though potentially the last hike of the cycle). While Russia may not screen so well for 2019, we believe 2020 could be substantially better, assuming no further sanctions.

The fall in the oil price to c. $60/bl for Brent takes it well below the Bloomberg consensus of $70/bl for 2019, suggesting that EPS downgrades may be necessary

Pakistan N

Pakistan was the second-worst performer in EM over 2018.

The currency has devalued to PKR140/$ (from PKR105/$ in December 2017) making it 9% undervalued relative to its long-term average REER on our model.

The falling oil price could help the C/A deficit.

Valuations are looking interesting: Pakistan is trading on a 12M fwd P/E of 6.9x, the third lowest in EM, and 12% below its long-term average of 7.9x; the market offers a 12M fwd dividend yield of 7.7%, the highest in EM.

Active EM funds have yet to engage: only 19% have any exposure (but Pakistan is just 0.04% of MSCI EM).

If an IMF support package can be agreed we would be more positive on reform implementation.

The central bank raised rates 150 bpts to 10% in December 2018, which is impacting growth; consensus sees inflation reaching 9.4% in 1H19, suggesting the hiking cycle may not be over.

The Trump administration has voiced concerns about potential IMF loans being used to repay debts to China; the IMF is proceeding slowly amid plans for greater diligence into debt sustainability.

Pakistan screens as the worst market in EM. The growth slowdown is the second worst in EM, from 5.8% in 2018 to 4.0% in 2019E; we also forecast lending growth to halve to 8%. We expect interest to continue to rise over 2019, and also forecast a downgrade to its credit rating. One comparative bright spot is the currency, which is currently 9% below fair value on our REER model.

Greece N

New Democracy is leading opinion polls ahead of the October 2019 elections.

Strong manufacturing PMI of 54.

Greek banks still trade at distressed valuations, given the high NPL burden (c. 40% NPLs).

Greece is unlikely to escape from a low-growth trap given continued austerity.

At 0.2% of MSCI, Greece is easily ignored.

Though Greece scores well on our top-down model, a lack of visibility on the banks remains an issue: we don’t believe top down models capture the nuances of Greek banks’ bad debt/capitalisation dynamics.

Lack of consensus within the Eurozone on burden sharing / debt forgiveness

GCC N/UW

Improved fiscal oil price break evens for 2019, according to the IMF: UAE ($67.4/bl), Qatar ($44/bl), Saudi Arabia ($73.3/bl); Kuwait breakeven remains unchanged ($47.4/bl).

The MSCI EM index inclusion story for Saudi Arabia in 2019 (taking place in two tranches in May and August) and potentially Kuwait (in 2020) should drive activity and interest.

IMF forecasts suggest a pick-up in growth, driven by the World Cup in Qatar, increased government spending in Saudi Arabia and fading fiscal headwinds in UAE (including Dubai Expo 2020 spending, though the ongoing real estate slump in Dubai continues to cause concern).

The $ peg, which should provide some protection if the $ strengthens and EM FX sells off.

Active EM funds are UW Qatar, UAE (in EM), so there is scope for re-engagement.

In 2018, Gulf countries benefitted from pegged currencies, banks’ positive margin exposure to higher US rates and oil. Gulf countries outperformed significantly over 2018: Qatar was been the top-performing market in EM, Saudi Arabia would have been the second-best market in EM had it been included, while Kuwait was the top-performing market in Frontier. Only UAE stands out for having underperformed, driven by the weakness in the property sector.

UAE has de-rated from 12x fwd earnings in early 2017 to 8.9x currently. Qatar has recovered the valuation drop seen in 2017 as the economy been resilient to the breakdown of relations with neighbouring countries.

Media reports suggest that Saudi Arabia’s Public Investment Fund may have been supporting the market.

Source: IMF, Bruegel, MSCI, Bloomberg, Renaissance Capital

Renaissance Capital 14 January 2019

ESG

10

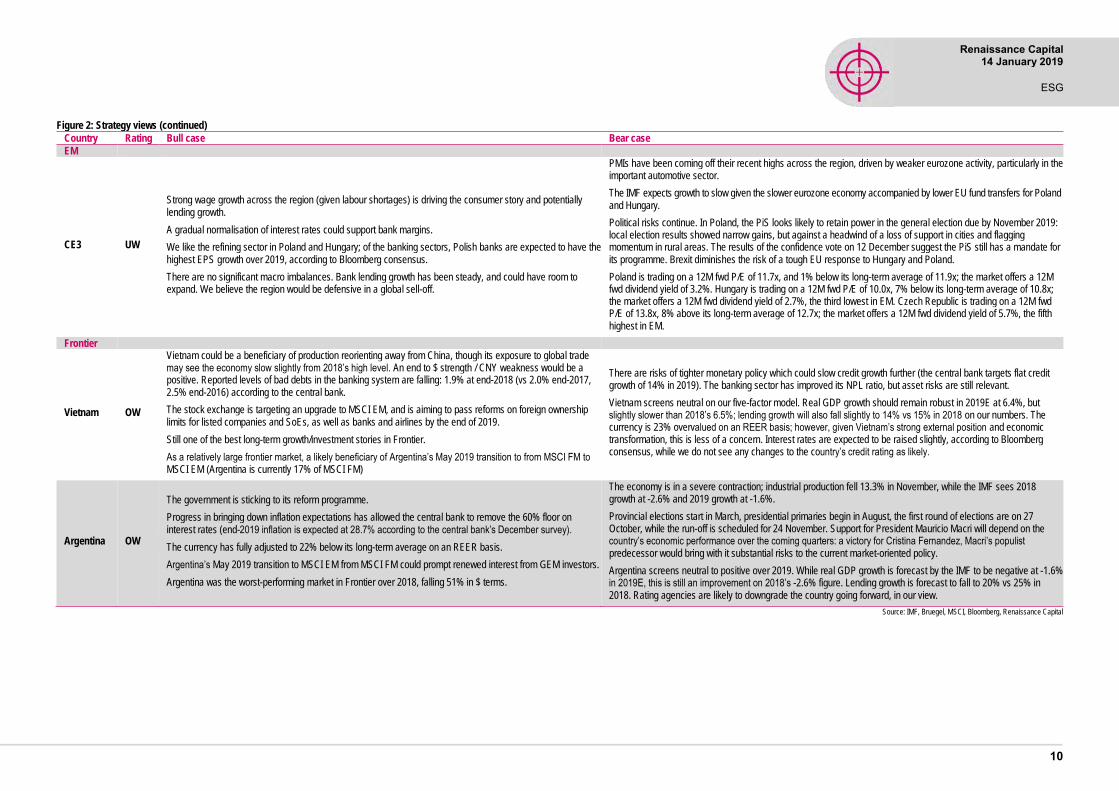

Figure 2: Strategy views (continued)

Country Rating Bull case Bear case

EM

CE3 UW

Strong wage growth across the region (given labour shortages) is driving the consumer story and potentially lending growth.

A gradual normalisation of interest rates could support bank margins.

We like the refining sector in Poland and Hungary; of the banking sectors, Polish banks are expected to have the highest EPS growth over 2019, according to Bloomberg consensus.

There are no significant macro imbalances. Bank lending growth has been steady, and could have room to expand. We believe the region would be defensive in a global sell-off.

PMIs have been coming off their recent highs across the region, driven by weaker eurozone activity, particularly in the important automotive sector.

The IMF expects growth to slow given the slower eurozone economy accompanied by lower EU fund transfers for Poland and Hungary.

Political risks continue. In Poland, the PiS looks likely to retain power in the general election due by November 2019: local election results showed narrow gains, but against a headwind of a loss of support in cities and flagging momentum in rural areas. The results of the confidence vote on 12 December suggest the PiS still has a mandate for its programme. Brexit diminishes the risk of a tough EU response to Hungary and Poland.

Poland is trading on a 12M fwd P/E of 11.7x, and 1% below its long-term average of 11.9x; the market offers a 12M fwd dividend yield of 3.2%. Hungary is trading on a 12M fwd P/E of 10.0x, 7% below its long-term average of 10.8x; the market offers a 12M fwd dividend yield of 2.7%, the third lowest in EM. Czech Republic is trading on a 12M fwd P/E of 13.8x, 8% above its long-term average of 12.7x; the market offers a 12M fwd dividend yield of 5.7%, the fifth highest in EM.

Frontier

Vietnam OW

Vietnam could be a beneficiary of production reorienting away from China, though its exposure to global trade may see the economy slow slightly from 2018’s high level. An end to $ strength / CNY weakness would be a positive. Reported levels of bad debts in the banking system are falling: 1.9% at end-2018 (vs 2.0% end-2017, 2.5% end-2016) according to the central bank.

The stock exchange is targeting an upgrade to MSCI EM, and is aiming to pass reforms on foreign ownership limits for listed companies and SoEs, as well as banks and airlines by the end of 2019.

Still one of the best long-term growth/investment stories in Frontier.

As a relatively large frontier market, a likely beneficiary of Argentina’s May 2019 transition to from MSCI FM to MSCI EM (Argentina is currently 17% of MSCI FM)

There are risks of tighter monetary policy which could slow credit growth further (the central bank targets flat credit growth of 14% in 2019). The banking sector has improved its NPL ratio, but asset risks are still relevant.

Vietnam screens neutral on our five-factor model. Real GDP growth should remain robust in 2019E at 6.4%, but slightly slower than 2018’s 6.5%; lending growth will also fall slightly to 14% vs 15% in 2018 on our numbers. The currency is 23% overvalued on an REER basis; however, given Vietnam’s strong external position and economic transformation, this is less of a concern. Interest rates are expected to be raised slightly, according to Bloomberg consensus, while we do not see any changes to the country’s credit rating as likely.

Argentina OW

The government is sticking to its reform programme.

Progress in bringing down inflation expectations has allowed the central bank to remove the 60% floor on interest rates (end-2019 inflation is expected at 28.7% according to the central bank’s December survey).

The currency has fully adjusted to 22% below its long-term average on an REER basis.

Argentina’s May 2019 transition to MSCI EM from MSCI FM could prompt renewed interest from GEM investors.

Argentina was the worst-performing market in Frontier over 2018, falling 51% in $ terms.

The economy is in a severe contraction; industrial production fell 13.3% in November, while the IMF sees 2018 growth at -2.6% and 2019 growth at -1.6%.

Provincial elections start in March, presidential primaries begin in August, the first round of elections are on 27 October, while the run-off is scheduled for 24 November. Support for President Mauricio Macri will depend on the country’s economic performance over the coming quarters: a victory for Cristina Fernandez, Macri’s populist predecessor would bring with it substantial risks to the current market-oriented policy.

Argentina screens neutral to positive over 2019. While real GDP growth is forecast by the IMF to be negative at -1.6% in 2019E, this is still an improvement on 2018’s -2.6% figure. Lending growth is forecast to fall to 20% vs 25% in 2018. Rating agencies are likely to downgrade the country going forward, in our view.

Source: IMF, Bruegel, MSCI, Bloomberg, Renaissance Capital

Renaissance Capital 14 January 2019

ESG

11

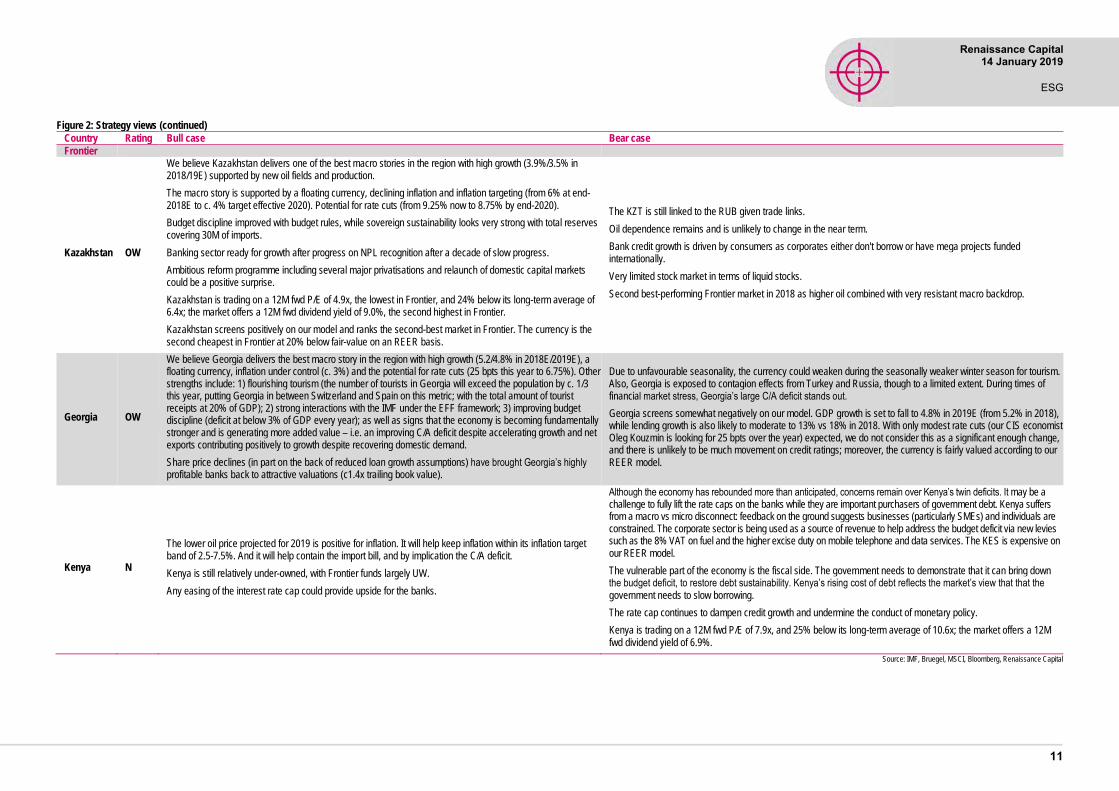

Figure 2: Strategy views (continued)

Country Rating Bull case Bear case

Frontier

Kazakhstan OW

We believe Kazakhstan delivers one of the best macro stories in the region with high growth (3.9%/3.5% in 2018/19E) supported by new oil fields and production.

The macro story is supported by a floating currency, declining inflation and inflation targeting (from 6% at end-2018E to c. 4% target effective 2020). Potential for rate cuts (from 9.25% now to 8.75% by end-2020).

Budget discipline improved with budget rules, while sovereign sustainability looks very strong with total reserves covering 30M of imports.

Banking sector ready for growth after progress on NPL recognition after a decade of slow progress.

Ambitious reform programme including several major privatisations and relaunch of domestic capital markets could be a positive surprise.

Kazakhstan is trading on a 12M fwd P/E of 4.9x, the lowest in Frontier, and 24% below its long-term average of 6.4x; the market offers a 12M fwd dividend yield of 9.0%, the second highest in Frontier.

Kazakhstan screens positively on our model and ranks the second-best market in Frontier. The currency is the second cheapest in Frontier at 20% below fair-value on an REER basis.

The KZT is still linked to the RUB given trade links.

Oil dependence remains and is unlikely to change in the near term.

Bank credit growth is driven by consumers as corporates either don't borrow or have mega projects funded internationally.

Very limited stock market in terms of liquid stocks.

Second best-performing Frontier market in 2018 as higher oil combined with very resistant macro backdrop.

Georgia OW

We believe Georgia delivers the best macro story in the region with high growth (5.2/4.8% in 2018E/2019E), a floating currency, inflation under control (c. 3%) and the potential for rate cuts (25 bpts this year to 6.75%). Other strengths include: 1) flourishing tourism (the number of tourists in Georgia will exceed the population by c. 1/3 this year, putting Georgia in between Switzerland and Spain on this metric; with the total amount of tourist receipts at 20% of GDP); 2) strong interactions with the IMF under the EFF framework; 3) improving budget discipline (deficit at below 3% of GDP every year); as well as signs that the economy is becoming fundamentally stronger and is generating more added value – i.e. an improving C/A deficit despite accelerating growth and net exports contributing positively to growth despite recovering domestic demand.

Share price declines (in part on the back of reduced loan growth assumptions) have brought Georgia’s highly profitable banks back to attractive valuations (c1.4x trailing book value).

Due to unfavourable seasonality, the currency could weaken during the seasonally weaker winter season for tourism. Also, Georgia is exposed to contagion effects from Turkey and Russia, though to a limited extent. During times of financial market stress, Georgia’s large C/A deficit stands out.

Georgia screens somewhat negatively on our model. GDP growth is set to fall to 4.8% in 2019E (from 5.2% in 2018), while lending growth is also likely to moderate to 13% vs 18% in 2018. With only modest rate cuts (our CIS economist Oleg Kouzmin is looking for 25 bpts over the year) expected, we do not consider this as a significant enough change, and there is unlikely to be much movement on credit ratings; moreover, the currency is fairly valued according to our REER model.

Kenya N

The lower oil price projected for 2019 is positive for inflation. It will help keep inflation within its inflation target band of 2.5-7.5%. And it will help contain the import bill, and by implication the C/A deficit.

Kenya is still relatively under-owned, with Frontier funds largely UW.

Any easing of the interest rate cap could provide upside for the banks.

Although the economy has rebounded more than anticipated, concerns remain over Kenya’s twin deficits. It may be a challenge to fully lift the rate caps on the banks while they are important purchasers of government debt. Kenya suffers from a macro vs micro disconnect: feedback on the ground suggests businesses (particularly SMEs) and individuals are constrained. The corporate sector is being used as a source of revenue to help address the budget deficit via new levies such as the 8% VAT on fuel and the higher excise duty on mobile telephone and data services. The KES is expensive on our REER model.

The vulnerable part of the economy is the fiscal side. The government needs to demonstrate that it can bring down the budget deficit, to restore debt sustainability. Kenya’s rising cost of debt reflects the market’s view that that the government needs to slow borrowing.

The rate cap continues to dampen credit growth and undermine the conduct of monetary policy.

Kenya is trading on a 12M fwd P/E of 7.9x, and 25% below its long-term average of 10.6x; the market offers a 12M fwd dividend yield of 6.9%.

Source: IMF, Bruegel, MSCI, Bloomberg, Renaissance Capital

Renaissance Capital 14 January 2019

ESG

12

Figure 2: Strategy views (continued)

Country Rating Bull case Bear case

Frontier

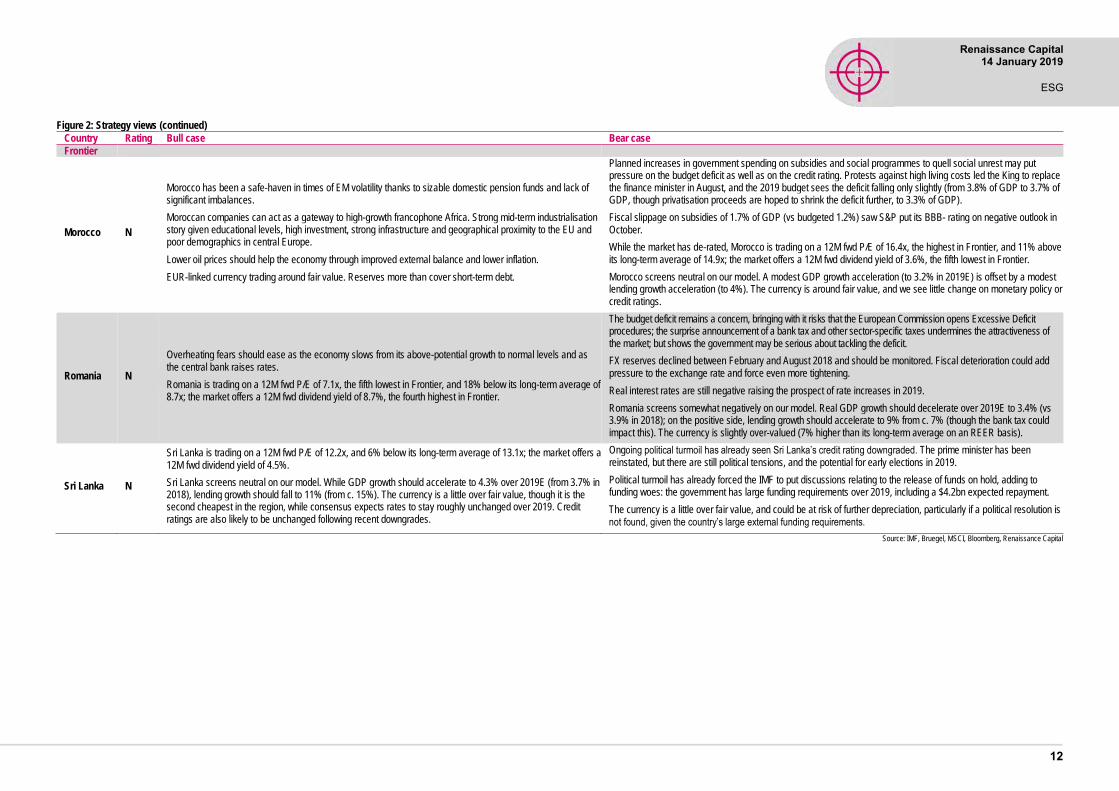

Morocco N

Morocco has been a safe-haven in times of EM volatility thanks to sizable domestic pension funds and lack of significant imbalances.

Moroccan companies can act as a gateway to high-growth francophone Africa. Strong mid-term industrialisation story given educational levels, high investment, strong infrastructure and geographical proximity to the EU and poor demographics in central Europe.

Lower oil prices should help the economy through improved external balance and lower inflation.

EUR-linked currency trading around fair value. Reserves more than cover short-term debt.

Planned increases in government spending on subsidies and social programmes to quell social unrest may put pressure on the budget deficit as well as on the credit rating. Protests against high living costs led the King to replace the finance minister in August, and the 2019 budget sees the deficit falling only slightly (from 3.8% of GDP to 3.7% of GDP, though privatisation proceeds are hoped to shrink the deficit further, to 3.3% of GDP).

Fiscal slippage on subsidies of 1.7% of GDP (vs budgeted 1.2%) saw S&P put its BBB- rating on negative outlook in October.

While the market has de-rated, Morocco is trading on a 12M fwd P/E of 16.4x, the highest in Frontier, and 11% above its long-term average of 14.9x; the market offers a 12M fwd dividend yield of 3.6%, the fifth lowest in Frontier.

Morocco screens neutral on our model. A modest GDP growth acceleration (to 3.2% in 2019E) is offset by a modest lending growth acceleration (to 4%). The currency is around fair value, and we see little change on monetary policy or credit ratings.

Romania N

Overheating fears should ease as the economy slows from its above-potential growth to normal levels and as the central bank raises rates.

Romania is trading on a 12M fwd P/E of 7.1x, the fifth lowest in Frontier, and 18% below its long-term average of 8.7x; the market offers a 12M fwd dividend yield of 8.7%, the fourth highest in Frontier.

The budget deficit remains a concern, bringing with it risks that the European Commission opens Excessive Deficit procedures; the surprise announcement of a bank tax and other sector-specific taxes undermines the attractiveness of the market; but shows the government may be serious about tackling the deficit.

FX reserves declined between February and August 2018 and should be monitored. Fiscal deterioration could add pressure to the exchange rate and force even more tightening.

Real interest rates are still negative raising the prospect of rate increases in 2019.

Romania screens somewhat negatively on our model. Real GDP growth should decelerate over 2019E to 3.4% (vs 3.9% in 2018); on the positive side, lending growth should accelerate to 9% from c. 7% (though the bank tax could impact this). The currency is slightly over-valued (7% higher than its long-term average on an REER basis).

Sri Lanka N

Sri Lanka is trading on a 12M fwd P/E of 12.2x, and 6% below its long-term average of 13.1x; the market offers a 12M fwd dividend yield of 4.5%.

Sri Lanka screens neutral on our model. While GDP growth should accelerate to 4.3% over 2019E (from 3.7% in 2018), lending growth should fall to 11% (from c. 15%). The currency is a little over fair value, though it is the second cheapest in the region, while consensus expects rates to stay roughly unchanged over 2019. Credit ratings are also likely to be unchanged following recent downgrades.

Ongoing political turmoil has already seen Sri Lanka’s credit rating downgraded. The prime minister has been reinstated, but there are still political tensions, and the potential for early elections in 2019.

Political turmoil has already forced the IMF to put discussions relating to the release of funds on hold, adding to funding woes: the government has large funding requirements over 2019, including a $4.2bn expected repayment.

The currency is a little over fair value, and could be at risk of further depreciation, particularly if a political resolution is not found, given the country’s large external funding requirements.

Source: IMF, Bruegel, MSCI, Bloomberg, Renaissance Capital

Renaissance Capital 14 January 2019

ESG

13

Figure 2: Strategy views (continued)

Country Rating Bull case Bear case

Frontier

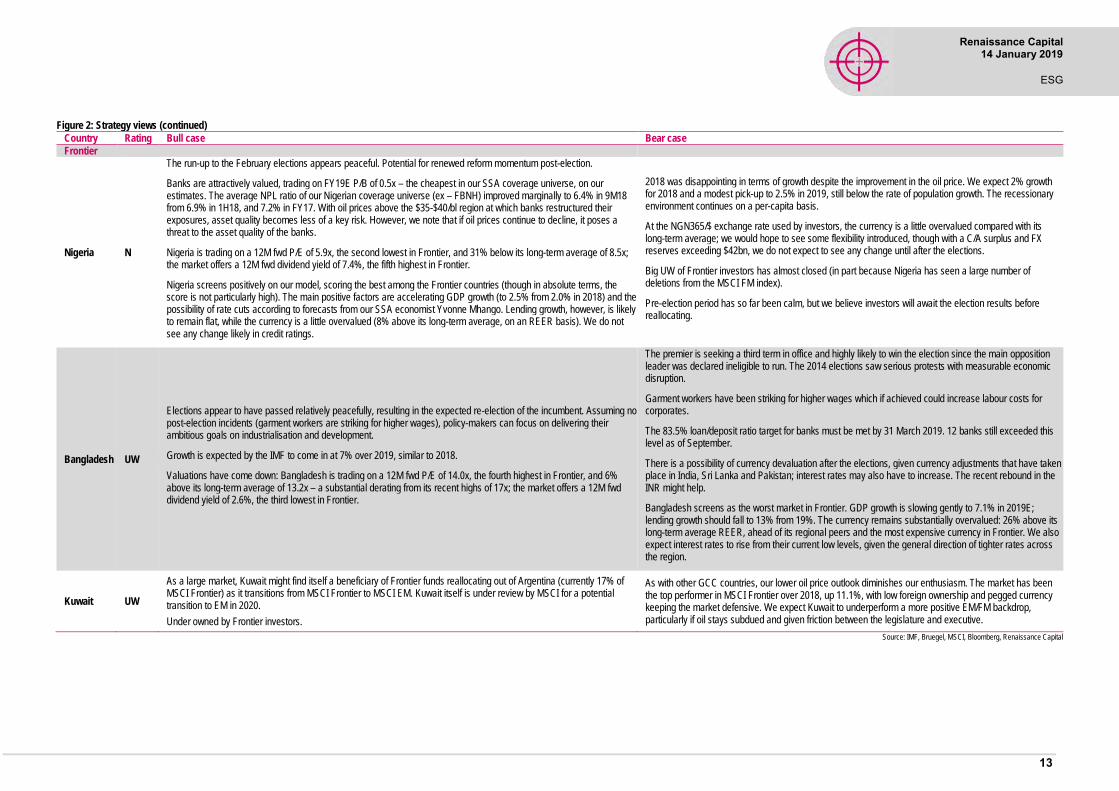

Nigeria N

The run-up to the February elections appears peaceful. Potential for renewed reform momentum post-election.

Banks are attractively valued, trading on FY19E P/B of 0.5x – the cheapest in our SSA coverage universe, on our estimates. The average NPL ratio of our Nigerian coverage universe (ex – FBNH) improved marginally to 6.4% in 9M18 from 6.9% in 1H18, and 7.2% in FY17. With oil prices above the $35-$40/bl region at which banks restructured their exposures, asset quality becomes less of a key risk. However, we note that if oil prices continue to decline, it poses a threat to the asset quality of the banks.

Nigeria is trading on a 12M fwd P/E of 5.9x, the second lowest in Frontier, and 31% below its long-term average of 8.5x; the market offers a 12M fwd dividend yield of 7.4%, the fifth highest in Frontier.

Nigeria screens positively on our model, scoring the best among the Frontier countries (though in absolute terms, the score is not particularly high). The main positive factors are accelerating GDP growth (to 2.5% from 2.0% in 2018) and the possibility of rate cuts according to forecasts from our SSA economist Yvonne Mhango. Lending growth, however, is likely to remain flat, while the currency is a little overvalued (8% above its long-term average, on an REER basis). We do not see any change likely in credit ratings.

2018 was disappointing in terms of growth despite the improvement in the oil price. We expect 2% growth for 2018 and a modest pick-up to 2.5% in 2019, still below the rate of population growth. The recessionary environment continues on a per-capita basis.

At the NGN365/$ exchange rate used by investors, the currency is a little overvalued compared with its long-term average; we would hope to see some flexibility introduced, though with a C/A surplus and FX reserves exceeding $42bn, we do not expect to see any change until after the elections.

Big UW of Frontier investors has almost closed (in part because Nigeria has seen a large number of deletions from the MSCI FM index).

Pre-election period has so far been calm, but we believe investors will await the election results before reallocating.

Bangladesh UW

Elections appear to have passed relatively peacefully, resulting in the expected re-election of the incumbent. Assuming no post-election incidents (garment workers are striking for higher wages), policy-makers can focus on delivering their ambitious goals on industrialisation and development.

Growth is expected by the IMF to come in at 7% over 2019, similar to 2018.

Valuations have come down: Bangladesh is trading on a 12M fwd P/E of 14.0x, the fourth highest in Frontier, and 6% above its long-term average of 13.2x – a substantial derating from its recent highs of 17x; the market offers a 12M fwd dividend yield of 2.6%, the third lowest in Frontier.

The premier is seeking a third term in office and highly likely to win the election since the main opposition leader was declared ineligible to run. The 2014 elections saw serious protests with measurable economic disruption.

Garment workers have been striking for higher wages which if achieved could increase labour costs for corporates.

The 83.5% loan/deposit ratio target for banks must be met by 31 March 2019. 12 banks still exceeded this level as of September.

There is a possibility of currency devaluation after the elections, given currency adjustments that have taken place in India, Sri Lanka and Pakistan; interest rates may also have to increase. The recent rebound in the INR might help.

Bangladesh screens as the worst market in Frontier. GDP growth is slowing gently to 7.1% in 2019E; lending growth should fall to 13% from 19%. The currency remains substantially overvalued: 26% above its long-term average REER, ahead of its regional peers and the most expensive currency in Frontier. We also expect interest rates to rise from their current low levels, given the general direction of tighter rates across the region.

Kuwait UW

As a large market, Kuwait might find itself a beneficiary of Frontier funds reallocating out of Argentina (currently 17% of MSCI Frontier) as it transitions from MSCI Frontier to MSCI EM. Kuwait itself is under review by MSCI for a potential transition to EM in 2020.

Under owned by Frontier investors.

As with other GCC countries, our lower oil price outlook diminishes our enthusiasm. The market has been the top performer in MSCI Frontier over 2018, up 11.1%, with low foreign ownership and pegged currency keeping the market defensive. We expect Kuwait to underperform a more positive EM/FM backdrop, particularly if oil stays subdued and given friction between the legislature and executive.

Source: IMF, Bruegel, MSCI, Bloomberg, Renaissance Capital

Renaissance Capital XX January 2019

ESG

Renaissance Capital 14 January 2019

ESG

14

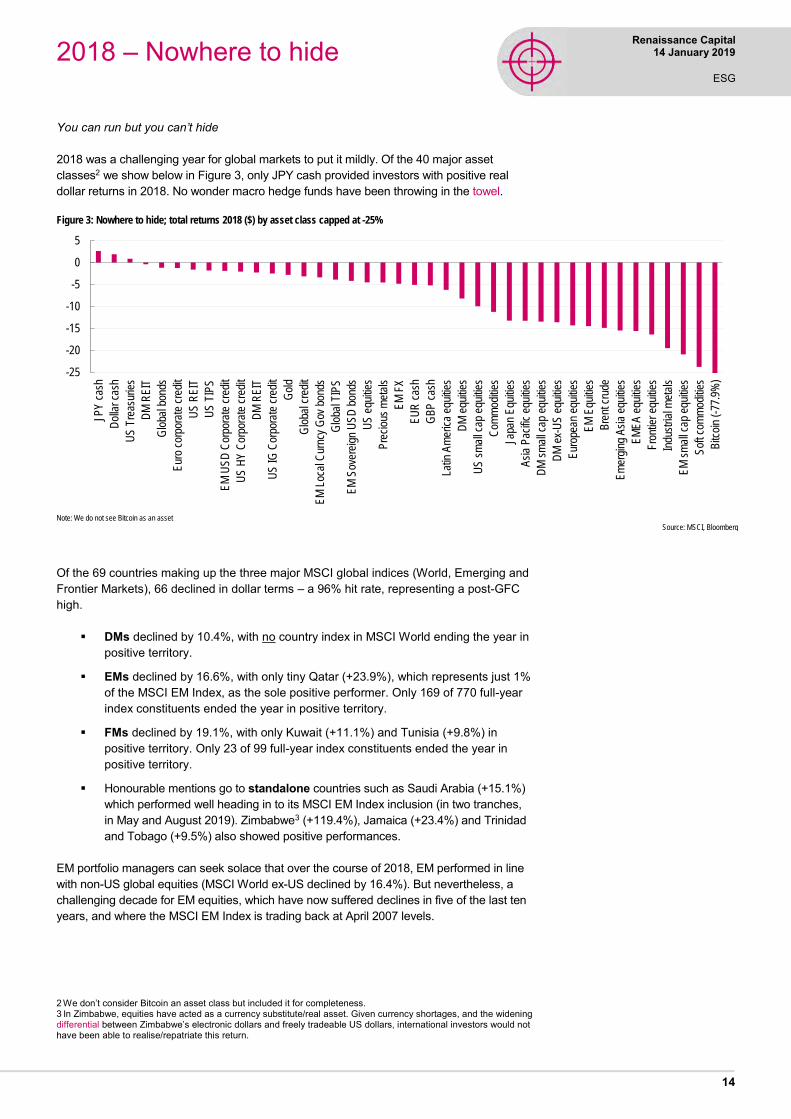

You can run but you can’t hide

2018 was a challenging year for global markets to put it mildly. Of the 40 major asset classes2 we show below in Figure 3, only JPY cash provided investors with positive real dollar returns in 2018. No wonder macro hedge funds have been throwing in the towel.

Figure 3: Nowhere to hide; total returns 2018 ($) by asset class capped at -25%

Note: We do not see Bitcoin as an asset

Source: MSCI, Bloomberg

Of the 69 countries making up the three major MSCI global indices (World, Emerging and Frontier Markets), 66 declined in dollar terms – a 96% hit rate, representing a post-GFC high.

▪ DMs declined by 10.4%, with no country index in MSCI World ending the year in positive territory.

▪ EMs declined by 16.6%, with only tiny Qatar (+23.9%), which represents just 1% of the MSCI EM Index, as the sole positive performer. Only 169 of 770 full-year index constituents ended the year in positive territory.

▪ FMs declined by 19.1%, with only Kuwait (+11.1%) and Tunisia (+9.8%) in positive territory. Only 23 of 99 full-year index constituents ended the year in positive territory.

▪ Honourable mentions go to standalone countries such as Saudi Arabia (+15.1%) which performed well heading in to its MSCI EM Index inclusion (in two tranches, in May and August 2019). Zimbabwe3 (+119.4%), Jamaica (+23.4%) and Trinidad and Tobago (+9.5%) also showed positive performances.

EM portfolio managers can seek solace that over the course of 2018, EM performed in line with non-US global equities (MSCI World ex-US declined by 16.4%). But nevertheless, a challenging decade for EM equities, which have now suffered declines in five of the last ten years, and where the MSCI EM Index is trading back at April 2007 levels.

2 We don’t consider Bitcoin an asset class but included it for completeness. 3 In Zimbabwe, equities have acted as a currency substitute/real asset. Given currency shortages, and the widening differential between Zimbabwe’s electronic dollars and freely tradeable US dollars, international investors would not have been able to realise/repatriate this return.

-25

-20

-15

-10

-5

0

5

JPY

cas

h

Dol

lar

cash

US

Tre

asur

ies

DM

RE

IT

Glo

bal b

onds

Eur

o co

rpor

ate

cred

it

US

RE

IT

US

TIP

S

EM

US

D C

orpo

rate

cre

dit

US

HY

Cor

pora

te c

redi

t

DM

RE

IT

US

IG C

orpo

rate

cre

dit

Gol

d

Glo

bal c

redi

t

EM

Loc

al C

urnc

y G

ov b

onds

Glo

bal T

IPS

EM

Sov

erei

gn U

SD

bon

ds

US

equ

ities

Pre

ciou

s m

etal

s

EM

FX

EU

R c

ash

GB

P c

ash

Latin

Am

eric

a eq

uitie

s

DM

equ

ities

US

sm

all c

ap e

quiti

es

Com

mod

ities

Japa

n E

quiti

es

Asi

a P

acifi

c eq

uitie

s

DM

sm

all c

ap e

quiti

es

DM

ex-

US

equ

ities

Eur

opea

n eq

uitie

s

EM

Equ

ities

Bre

nt c

rude

Em

ergi

ng A

sia

equi

ties

EM

EA

equ

ities

Fro

ntie

r eq

uitie

s

Indu

stria

l met

als

EM

sm

all c

ap e

quiti

es

Sof

t com

mod

ities

Bitc

oin

(-77

.9%

)

2018 – Nowhere to hide

Renaissance Capital XX January 2019

ESG

Renaissance Capital 14 January 2019

ESG

15

Figure 4: MSCI indices, $, rebased

Source: MSCI, Bloomberg

Figure 5: MSCI indices, $, rebased

Source: MSCI, Bloomberg

Figure 6: MSCI indices 2018, $ – DM

Source: Bloomberg, Renaissance Capital

Figure 7: MSCI indices 2018, $ – EM

Note: *Standalone index

Source: Bloomberg, Renaissance Capital

Figure 8: MSCI indices 2018, $ – FM

Note: *Standalone index

Source: Bloomberg, Renaissance Capital

Figure 9: MSCI indices 2018, $ – Sectors

Source: Bloomberg, Renaissance Capital

75

80

85

90

95

100

105

110

115

Jan-

18

Feb

-18

Mar

-18

Apr

-18

May

-18

Jun-

18

Jul-1

8

Aug

-18

Sep

-18

Oct

-18

Nov

-18

Dec

-18

Jan-

19

EM US World World ex-US

75

80

85

90

95

100

105

110

115

120

Jan-

18

Feb

-18

Mar

-18

Apr

-18

May

…

Jun-

18

Jul-1

8

Aug

-…

Sep

-…

Oct

-18

Nov

-…

Dec

-…

Jan-

19

EM Latin America Em Asia EMEA FM

-30%

-25%

-20%

-15%

-10%

-5%

0%

Fin

land

US

AIs

rael

New

Zea

land

Wor

ldH

ong

Kon

gS

witz

erla

ndN

orw

ayS

inga

pore

Por

tuga

lJa

pan

Fra

nce

Net

herla

nds

Aus

tral

iaS

wed

enD

enm

ark

Uni

ted

Kin

gdom

Spa

inC

anad

aIta

lyG

erm

any

Irel

and

Bel

gium

Aus

tria

-50%

-40%

-30%

-20%

-10%

0%

10%

20%

30%

Qat

arP

eru

Bra

zil

Rus

sia

Tha

iland

Cze

ch R

epub

licH

unga

ryIn

dia

Mal

aysi

aIn

done

sia

Tai

wan

UA

EC

olom

bia

Pol

and

Egy

ptE

MM

exic

oP

hilip

pine

sC

hina

Chi

leK

orea

Sou

th A

fric

aG

reec

eP

akis

tan

Tur

key

Sau

di A

rabi

a*

-60%-50%-40%-30%-20%-10%

0%10%20%30%

Kuw

ait

Tun

isia

Ser

bia

Slo

veni

aB

ahra

inR

oman

iaK

azak

hsta

nJo

rdan

Om

anM

oroc

coC

roat

iaLi

thua

nia

Vie

tnam

Sri

Lank

aK

enya

Ban

glad

esh

Est

onia

Leba

non

Nig

eria

FM

Mau

ritiu

sW

AE

MU

Arg

entin

a

Zim

babw

e* (

+11

9%)

Jam

aica

*T

rinid

ad &

Tob

ago*

Ukr

aine

*B

osni

a &

Her

zego

vina

*B

ulga

ria*

Pan

ama*

Bot

swan

a*

-50%

-40%

-30%

-20%

-10%

0%

10%

Hea

lthca

re

Util

ities IT

Con

s D

iscr

Rea

l Est

ate

Inde

x

Con

s S

tapl

es

Tel

ecom

s

Indu

stria

ls

Ene

rgy

Mat

eria

ls

Fin

anci

als

World EM FM

Renaissance Capital XX January 2019

ESG

Renaissance Capital 14 January 2019

ESG

16

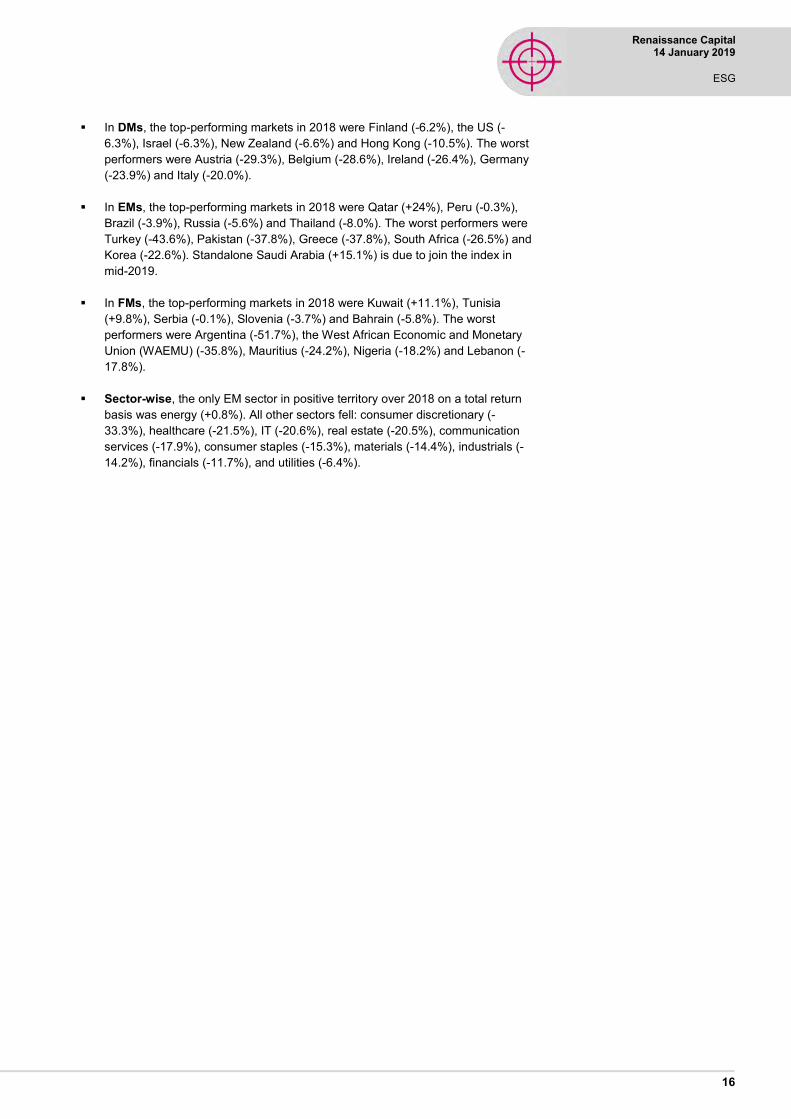

▪ In DMs, the top-performing markets in 2018 were Finland (-6.2%), the US (-6.3%), Israel (-6.3%), New Zealand (-6.6%) and Hong Kong (-10.5%). The worst performers were Austria (-29.3%), Belgium (-28.6%), Ireland (-26.4%), Germany (-23.9%) and Italy (-20.0%).

▪ In EMs, the top-performing markets in 2018 were Qatar (+24%), Peru (-0.3%), Brazil (-3.9%), Russia (-5.6%) and Thailand (-8.0%). The worst performers were Turkey (-43.6%), Pakistan (-37.8%), Greece (-37.8%), South Africa (-26.5%) and Korea (-22.6%). Standalone Saudi Arabia (+15.1%) is due to join the index in mid-2019.

▪ In FMs, the top-performing markets in 2018 were Kuwait (+11.1%), Tunisia (+9.8%), Serbia (-0.1%), Slovenia (-3.7%) and Bahrain (-5.8%). The worst performers were Argentina (-51.7%), the West African Economic and Monetary Union (WAEMU) (-35.8%), Mauritius (-24.2%), Nigeria (-18.2%) and Lebanon (-17.8%).

▪ Sector-wise, the only EM sector in positive territory over 2018 on a total return basis was energy (+0.8%). All other sectors fell: consumer discretionary (-33.3%), healthcare (-21.5%), IT (-20.6%), real estate (-20.5%), communication services (-17.9%), consumer staples (-15.3%), materials (-14.4%), industrials (-14.2%), financials (-11.7%), and utilities (-6.4%).

Renaissance Capital XX January 2019

ESG

Renaissance Capital 14 January 2019

ESG

17

The EM consensus has been wrongfooted for two years in a row.

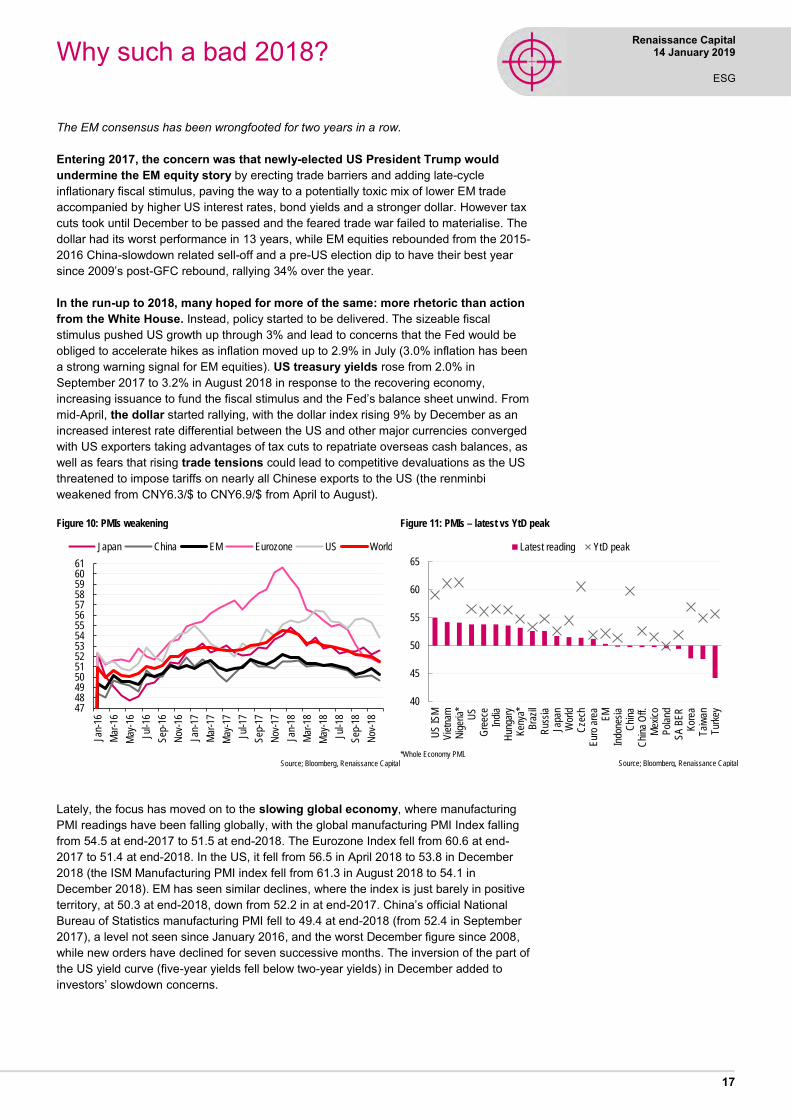

Entering 2017, the concern was that newly-elected US President Trump would undermine the EM equity story by erecting trade barriers and adding late-cycle inflationary fiscal stimulus, paving the way to a potentially toxic mix of lower EM trade accompanied by higher US interest rates, bond yields and a stronger dollar. However tax cuts took until December to be passed and the feared trade war failed to materialise. The dollar had its worst performance in 13 years, while EM equities rebounded from the 2015-2016 China-slowdown related sell-off and a pre-US election dip to have their best year since 2009’s post-GFC rebound, rallying 34% over the year.

In the run-up to 2018, many hoped for more of the same: more rhetoric than action from the White House. Instead, policy started to be delivered. The sizeable fiscal stimulus pushed US growth up through 3% and lead to concerns that the Fed would be obliged to accelerate hikes as inflation moved up to 2.9% in July (3.0% inflation has been a strong warning signal for EM equities). US treasury yields rose from 2.0% in September 2017 to 3.2% in August 2018 in response to the recovering economy, increasing issuance to fund the fiscal stimulus and the Fed’s balance sheet unwind. From mid-April, the dollar started rallying, with the dollar index rising 9% by December as an increased interest rate differential between the US and other major currencies converged with US exporters taking advantages of tax cuts to repatriate overseas cash balances, as well as fears that rising trade tensions could lead to competitive devaluations as the US threatened to impose tariffs on nearly all Chinese exports to the US (the renminbi weakened from CNY6.3/$ to CNY6.9/$ from April to August).

Figure 10: PMIs weakening

Source; Bloomberg, Renaissance Capital

Figure 11: PMIs – latest vs YtD peak

*Whole Economy PMI. Source; Bloomberg, Renaissance Capital

Lately, the focus has moved on to the slowing global economy, where manufacturing PMI readings have been falling globally, with the global manufacturing PMI Index falling from 54.5 at end-2017 to 51.5 at end-2018. The Eurozone Index fell from 60.6 at end-2017 to 51.4 at end-2018. In the US, it fell from 56.5 in April 2018 to 53.8 in December 2018 (the ISM Manufacturing PMI index fell from 61.3 in August 2018 to 54.1 in December 2018). EM has seen similar declines, where the index is just barely in positive territory, at 50.3 at end-2018, down from 52.2 in at end-2017. China’s official National Bureau of Statistics manufacturing PMI fell to 49.4 at end-2018 (from 52.4 in September 2017), a level not seen since January 2016, and the worst December figure since 2008, while new orders have declined for seven successive months. The inversion of the part of the US yield curve (five-year yields fell below two-year yields) in December added to investors’ slowdown concerns.

474849505152535455565758596061

Jan-

16

Mar

-16

May

-16

Jul-1

6

Sep

-16

Nov

-16

Jan-

17

Mar

-17

May

-17

Jul-1

7

Sep

-17

Nov

-17

Jan-

18

Mar

-18

May

-18

Jul-1

8

Sep

-18

Nov

-18

Japan China EM Eurozone US World

40

45

50

55

60

65

US

ISM

Vie

tnam

Nig

eria

*U

SG

reec

eIn

dia

Hun

gary

Ken

ya*

Bra

zil

Rus

sia

Japa

nW

orld

Cze

chE

uro

area EM

Indo

nesi

aC

hina

Chi

na O

ff.M

exic

oP

olan

dS

A B

ER

Kor

eaT

aiw

anT

urke

y

Latest reading YtD peak

Why such a bad 2018?

Renaissance Capital XX January 2019

ESG

Renaissance Capital 14 January 2019

ESG

18

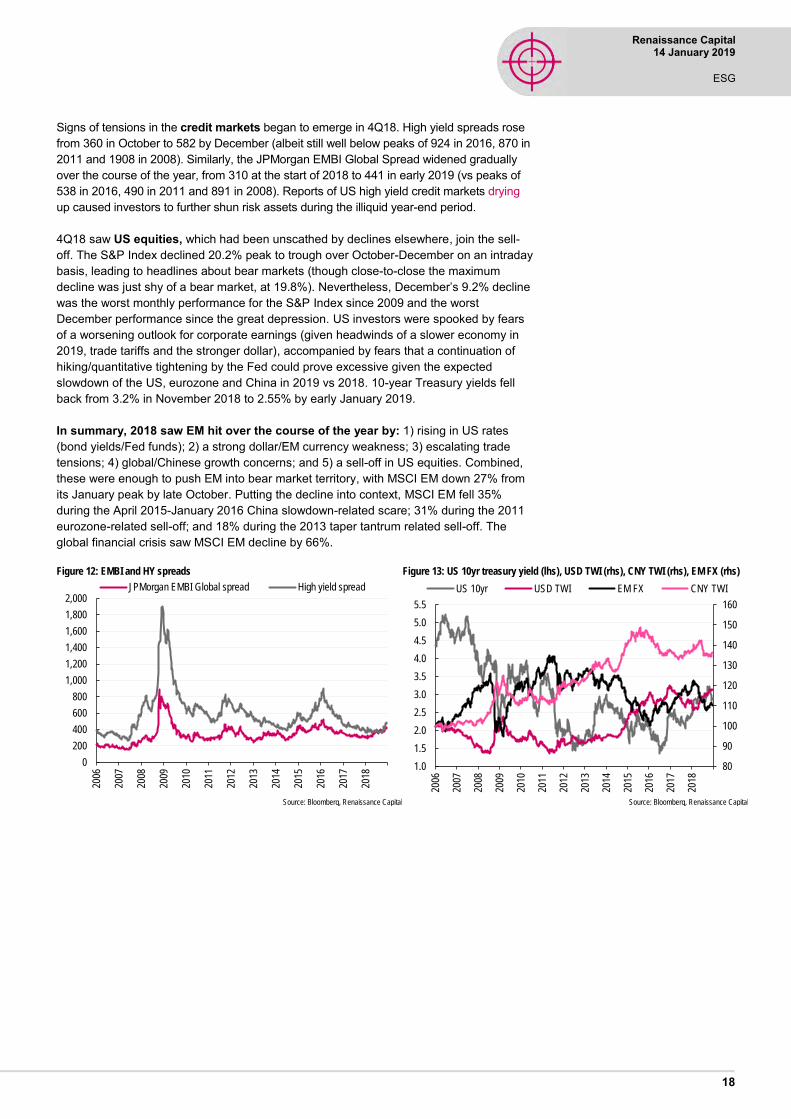

Signs of tensions in the credit markets began to emerge in 4Q18. High yield spreads rose from 360 in October to 582 by December (albeit still well below peaks of 924 in 2016, 870 in 2011 and 1908 in 2008). Similarly, the JPMorgan EMBI Global Spread widened gradually over the course of the year, from 310 at the start of 2018 to 441 in early 2019 (vs peaks of 538 in 2016, 490 in 2011 and 891 in 2008). Reports of US high yield credit markets drying up caused investors to further shun risk assets during the illiquid year-end period.

4Q18 saw US equities, which had been unscathed by declines elsewhere, join the sell-off. The S&P Index declined 20.2% peak to trough over October-December on an intraday basis, leading to headlines about bear markets (though close-to-close the maximum decline was just shy of a bear market, at 19.8%). Nevertheless, December’s 9.2% decline was the worst monthly performance for the S&P Index since 2009 and the worst December performance since the great depression. US investors were spooked by fears of a worsening outlook for corporate earnings (given headwinds of a slower economy in 2019, trade tariffs and the stronger dollar), accompanied by fears that a continuation of hiking/quantitative tightening by the Fed could prove excessive given the expected slowdown of the US, eurozone and China in 2019 vs 2018. 10-year Treasury yields fell back from 3.2% in November 2018 to 2.55% by early January 2019.

In summary, 2018 saw EM hit over the course of the year by: 1) rising in US rates (bond yields/Fed funds); 2) a strong dollar/EM currency weakness; 3) escalating trade tensions; 4) global/Chinese growth concerns; and 5) a sell-off in US equities. Combined, these were enough to push EM into bear market territory, with MSCI EM down 27% from its January peak by late October. Putting the decline into context, MSCI EM fell 35% during the April 2015-January 2016 China slowdown-related scare; 31% during the 2011 eurozone-related sell-off; and 18% during the 2013 taper tantrum related sell-off. The global financial crisis saw MSCI EM decline by 66%.

Figure 12: EMBI and HY spreads

Source: Bloomberg, Renaissance Capital

Figure 13: US 10yr treasury yield (lhs), USD TWI (rhs), CNY TWI (rhs), EM FX (rhs)

Source: Bloomberg, Renaissance Capital

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

JPMorgan EMBI Global spread High yield spread

80

90

100

110

120

130

140

150

160

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

US 10yr USD TWI EM FX CNY TWI

Renaissance Capital

XX January 2019

ESG

Renaissance Capital 14 January 2019

ESG

19

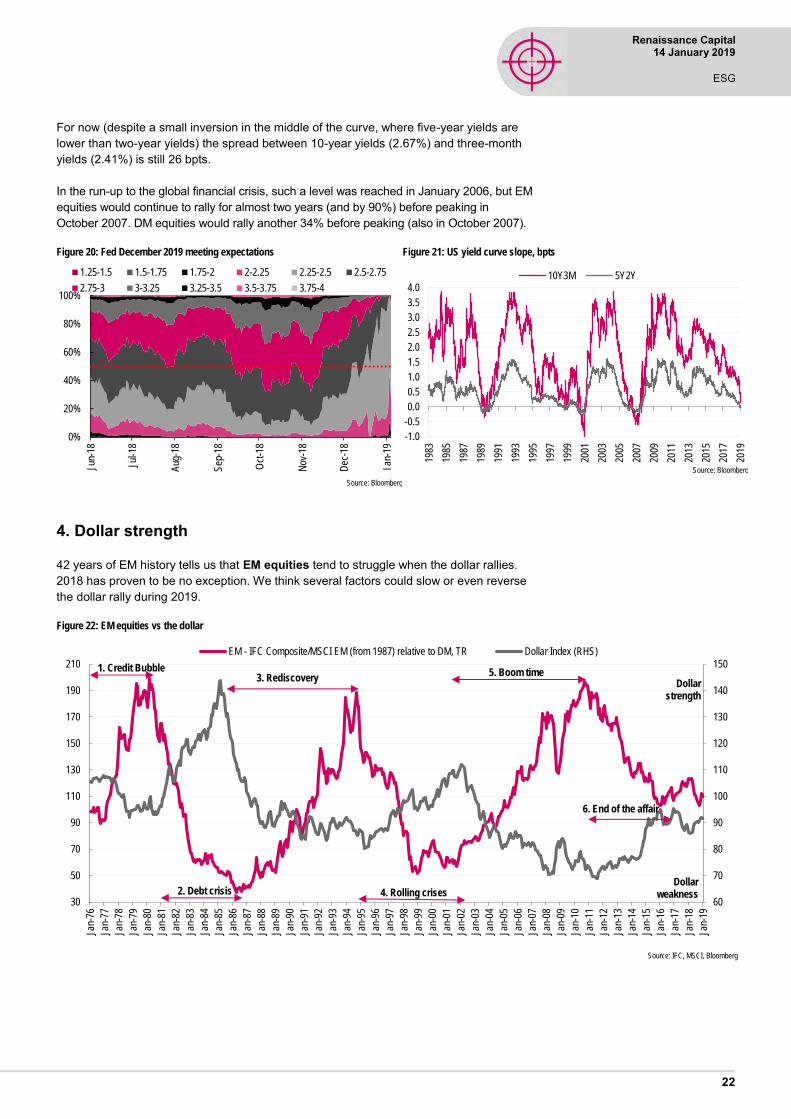

2018 saw five overlapping waves of negativity overwhelm EM: 1) rising US rates (bond yields and Fed funds); 2) a strong dollar; 3) escalating trade tensions; 4) global/Chinese growth concerns; and 5) the 4Q18 sell-off in US equities. Combined, these were enough to push EM equities into bear market territory, with MSCI EM closing 2018 down 17% for the year, 24% off its January peak. The bad news for bottom-up investors is that top-down themes are again likely to dominate in 2019. The good – and little noticed – news is that EM equities bottomed in (and have started to outperform DM since) early October.

Our base case is that the US avoids recession in 2019 (which this summer will make the current expansion the longest since records began in the 1850s), but that growth slows as the sugar rush of stimulus fades and given the lagged effects of higher borrowing costs, the stronger dollar, weaker external demand (accompanied by rising protectionism) and the partial US government shutdown.

The positive story for EM is that we enter 2019 with: 1) much lower US bond yields (10-year Treasuries yield of 2.67 vs 3.24 in early November); 2) the Fed indicating greater flexibility, with Fed futures now suggesting that the Fed might not hike at all in 2019 (sharp falls in interest rate expectations can precede an EM equity rally, see Figure 14); 3) China stimulating its economy via RRR cuts and big sign-offs for new railways (with more stimulus likely to be unveiled during 1H19) in order to report the required 6.2%annual growth rate in 2019 and 2020 to double the economy over 2010-2020; 4) some easing of the strong upwards dollar pressure of 2018; 5) oil $30/bl lower – bringing down inflation expectations and helping C/As for the 89% index weight of MSCI EM (and 64% of FM) that imports oil; 6) many EM currencies trading slightly cheap vs their long-run REER averages; and 7) the potential for a US-China trade agreement to add to risk appetite – we think recent equity market declines and softening lead indicators make such an agreement more likely, with President Trump in a pre-election year.

We examine these factors below and conclude that while plenty depends on policymakers and politicians taking the right actions, on balance, we think the 2019 EM equity pain trade is likely to be on the upside, and recommend investors take more risk in EM in 2019. But couldn’t 2019 just be a continuation of 2018’s poor performance? Yes, if financial market declines become a self-fulfilling prophecy and bring with them the next global recession, we can expect further declines.

1. The Fed and US bond yields

Trump’s $1.5trn of tax cuts helped push US growth above 3% during 2Q-3Q18. Democrat control of the House of Representatives makes a repeat fiscal stimulus unlikely, and the sugar rush for the economy should fade over the course of 2019. Together with the lagged effects of higher borrowing costs, the stronger dollar and weaker external demand (accompanied by rising protectionism) and the partial US government shutdown, the US economy should slow in 2019 vs 2018. A slower economy accompanied by the recent $30/bl decline in oil prices should in turn help keep inflationary pressure under control despite the tightening labour market (five-year inflation swaps have been coming down with the oil price, see Figure 19).

December’s ’dovish hike’ by the Fed (a 25-bpt hike, accompanied by a shift down in the dot plot for 2019 from three 25-bpt hikes to two) was perceived by the market as offering insufficient flexibility, and triggered sharp falls in US equities in December. January saw Fed Chairman Jerome Powell clarify that “there is no pre-set path for policy” and that the Fed is “prepared to shift economic policy and shift it significantly”, with flexibility including both the path of interest rates and the size of the Fed’s balance sheet size; several other senior Federal Reserve policymakers have counselled a wait-and-see approach to rates.

Could 2019 be better?

Renaissance Capital XX January 2019

ESG

Renaissance Capital 14 January 2019

ESG

20

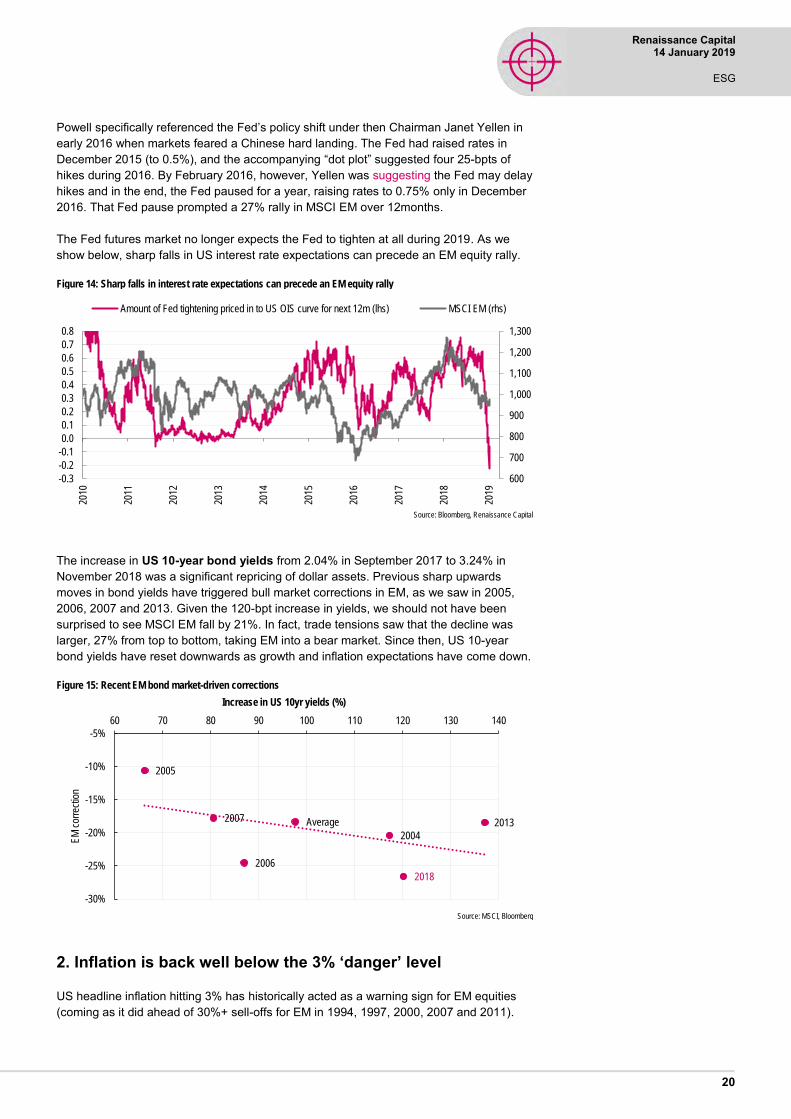

Powell specifically referenced the Fed’s policy shift under then Chairman Janet Yellen in early 2016 when markets feared a Chinese hard landing. The Fed had raised rates in December 2015 (to 0.5%), and the accompanying “dot plot” suggested four 25-bpts of hikes during 2016. By February 2016, however, Yellen was suggesting the Fed may delay hikes and in the end, the Fed paused for a year, raising rates to 0.75% only in December 2016. That Fed pause prompted a 27% rally in MSCI EM over 12months.

The Fed futures market no longer expects the Fed to tighten at all during 2019. As we show below, sharp falls in US interest rate expectations can precede an EM equity rally.

Figure 14: Sharp falls in interest rate expectations can precede an EM equity rally

Source: Bloomberg, Renaissance Capital

The increase in US 10-year bond yields from 2.04% in September 2017 to 3.24% in November 2018 was a significant repricing of dollar assets. Previous sharp upwards moves in bond yields have triggered bull market corrections in EM, as we saw in 2005, 2006, 2007 and 2013. Given the 120-bpt increase in yields, we should not have been surprised to see MSCI EM fall by 21%. In fact, trade tensions saw that the decline was larger, 27% from top to bottom, taking EM into a bear market. Since then, US 10-year bond yields have reset downwards as growth and inflation expectations have come down.

Figure 15: Recent EM bond market-driven corrections

Source: MSCI, Bloomberg

2. Inflation is back well below the 3% ‘danger’ level

US headline inflation hitting 3% has historically acted as a warning sign for EM equities (coming as it did ahead of 30%+ sell-offs for EM in 1994, 1997, 2000, 2007 and 2011).

600

700

800

900

1,000

1,100

1,200

1,300

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

2010

2011

2012

2013

2014

2015