Embed Size (px)

Citation preview

Making buildings better

Combined solar and HP systems

respond to policy goals and can

appeal to end user

Krystyna Dawson

Business manager WMI

May 2017

2 Making buildings better BSRIA ©

Agenda

• Sales of hydronic heat pumps in Europe and the shift towards DHW HPs

• Decarbonised electricity is both: advantage and obstacle for HPs • Combined solar and HP systems can help reduce CO2 emissions in existing

homes

• Support needed to maintain the value proposition of combined systems in the long term

• Technology development and policy making need to meet with end user acceptance to propel heat pumps to the main stream

3 Making buildings better BSRIA ©

Heat pumps historic growth in Europe

3

8%

52%

-10% -7%

8%

5% 8% 9% 8% 7%

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

0

100,000

200,000

300,000

400,000

500,000

600,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

HP yearly sales Market growth

units % growth

Source: BSRIA based on data from 21 European countries

Sales of hydronic heat pumps Europe, units, 2006 – 2016 CAGR

2006 -16

8%

CAGR

2010 -16

9%

4 Making buildings better BSRIA ©

Legislative push meets consumer resistance

European Legislation

National Building Regulations

Incentive programs

5 Making buildings better BSRIA ©

Uneven growth in energy prices

0

1

2

3

4

5

6

7

8

2004 2011 2014 2015 2016

EEG Umlage value

CSPE value

€cent /

kWh

Electricity price between 2006 and 2016

Up 47% Up 41%

Special tax on electricity in Germany and France

(Germany)

(France)

Gas price between 2006 and 2016

Up 10% Up 3%

6 Making buildings better BSRIA ©

Increasing energy prices impact HP sales

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

0

20

40

60

80

100

120

140

160

180

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016e

HP sales Germany HP sales France Spark Germany Spark France

‘000 units Spark, unit

Sales of hydronic heat pumps in Germany and France

against the electricity / gas price ratio, units, 2006 – 2016

Source: BSRIA based on data from 21 European countries

Spark = ratio between the price of electricity and gas for residential end user

7 Making buildings better BSRIA ©

Slow progression of heating HPs

units

CAGR

26%

CAGR

2%

Growth of hydronic HPs in Europe and share of DHP Heat Pumps, 2009 - 2016

0

100,000

200,000

300,000

400,000

500,000

600,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Other HP DHW HP

10%

63%

France

Germany

Italy

Slovenia

Poland

Switzerland

Others

2016 split by countries

Source: BSRIA based on data from 21 European countries

8 Making buildings better BSRIA ©

Installations in new buildings dominate today

44%

56%

New build Existing buildings

65%

35%

2016 2009

Share of HP installations in New and Exiting buildings in Europe

Source: BSRIA based on data from 21 European countries

9 Making buildings better BSRIA ©

Decarbonised electricity gives HP advantage

0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0

1,000

2,000

3,000

4,000

5,000

6,000

existing dwelling with HP inGermany

existing dwelling with HP inFrance

existing dwelling with gas CB

Kg CO2emissions per year standard emission factor 2012

Kg CO2/year tCO2/MWhe

Level of CO2 emissions for households fitted with either A/W heat pump

or gas condensing boiler in Germany and France

Source: BSRIA

10 Making buildings better BSRIA ©

Combined HP and PV installation lowers the energy

cost for consumer

€ / year

987

1271

825

1363

503

839

0 200 400 600 800 1000 1200 1400 1600

France

Germany

Air/Water HP + PV Air/Water HP Gas condensing boiler

Yearly energy cost for a dwelling with Air to Water HP stand alone and

combined with PV system (existing dwellings, € / year )

Source: BSRIA

11 Making buildings better BSRIA ©

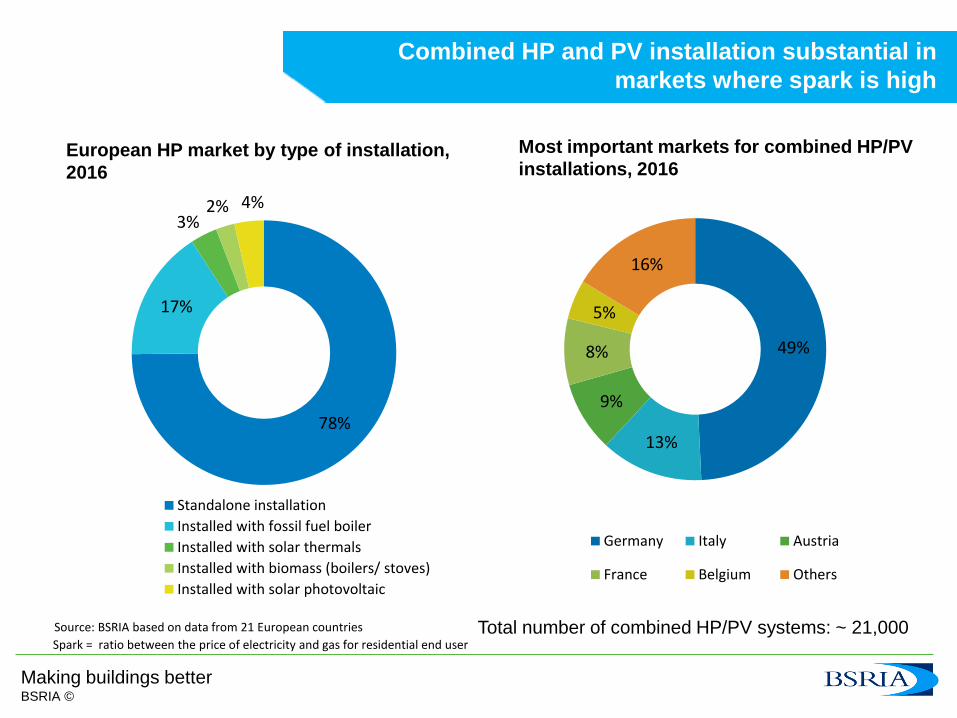

Combined HP and PV installation substantial in

markets where spark is high

European HP market by type of installation,

2016

78%

17%

3% 2% 4%

Standalone installation

Installed with fossil fuel boiler

Installed with solar thermals

Installed with biomass (boilers/ stoves)

Installed with solar photovoltaic

Most important markets for combined HP/PV

installations, 2016

49%

13%

9%

8%

5%

16%

Germany Italy Austria

France Belgium Others

Total number of combined HP/PV systems: ~ 21,000 Source: BSRIA based on data from 21 European countries

Spark = ratio between the price of electricity and gas for residential end user

12 Making buildings better BSRIA ©

Reinforced value proposition is needed for the

future

Projected energy cost for a dwelling with heat pump in relation to electricity price and FiT*

GERMANY

0510152025303540

- 200 400 600 800

1,000 1,200 1,400 1,600

2012 2016 2020e

PV FiT/KW price of electricty energy cost with GCB

energy cost with HP energy cost with HP & PV

* FiT = feed-in-tariff

HP COP 3.5

Own use of generated electricity; 35%

HP + PV (50% own use)

Energy cost

€/year FiT / electricity price

€cent / kWh

Electricity price CAGR: 2.6%

Gas price CAGR: 1.2%*

Source: BSRIA based on data from 21 European countries

13 Making buildings better BSRIA ©

Long term market drivers for Heat Pumps

Building regulations . . .

Energy efficiency regulations for products . . .

PV & storage market development . . .

Smart grid development. . .

Mostly related to new build might open up to

renovation

Requirements are becoming tighter

Storage batteries needed to support own consumption

Slow but ongoing with HPs being already used in smaller

networks

2010 2015 2020 2030

timeline

market size

Source: BSRIA

14 Making buildings better BSRIA ©

Summary and questions

• Heat pumps are growing but need stronger value proposition for end user to become real mainstream

o Is it enough to rejoice on growth of domestic hot water heat pumps only?

• Combined HP and solar installations are attractive as low energy cost system and as a low carbon solution

o Is it enough to relay on legislation and government fiscal incentives to develop this market further?

• Increased self consumption will support progress of combined HP/PV systems

o Is it possible to match consumer interests with those of energy providers?

15 Making buildings better BSRIA ©

Thank you

Krystyna Dawson Business Manager – BSRIA WMI Worldwide Market Intelligence

Old Bracknell Lane West, Bracknell, Berkshire RG12 7AH

D : +44 (0)1344 465638 F : +44 (0)1344 465626 M : +44 (0)7990 595836 E : [email protected]

W : www.bsria.co.uk

More information at www.bsria.co.uk/market-intelligence