Embed Size (px)

Citation preview

COLLEGE SAVINGS MADE EASY.

2 | SCHOLARSHARE

START EARLY.

TINYCHANGES

CAN ADD UP.

Start small. Dream big.

INVITE FAMILY TO HELP.

CHANGE BENEFICIARIES

IF NEEDED.

USE FOR A VARIETY OF QUALIFIEDEXPENSES.

AUTOMATE YOUR

SAVINGS.

MOMENTUMBUILDS

OVER TIME.

Share More for Their Future 3

How ScholarShare Works 4

Tax Advantages 5

ScholarShare Is Flexible to Use 6

Investment Portfolios 8

Answers to Your Questions 12

Start Sharing Today 14

CALIFORNIA’S 529 COLLEGE SAVINGS PLAN | 3

A plan that puts higher education within reach.All parents want to give their child(ren) or another loved one a good education and

bright future. Higher education — whether at a four-year college, community college,

or technical school — offers students a chance to open their minds, develop their

talents, acquire knowledge and hone their skills for a fulfilling career. Higher education

also can translate into stronger earning power and steadier employment during the

course of one’s lifetime.

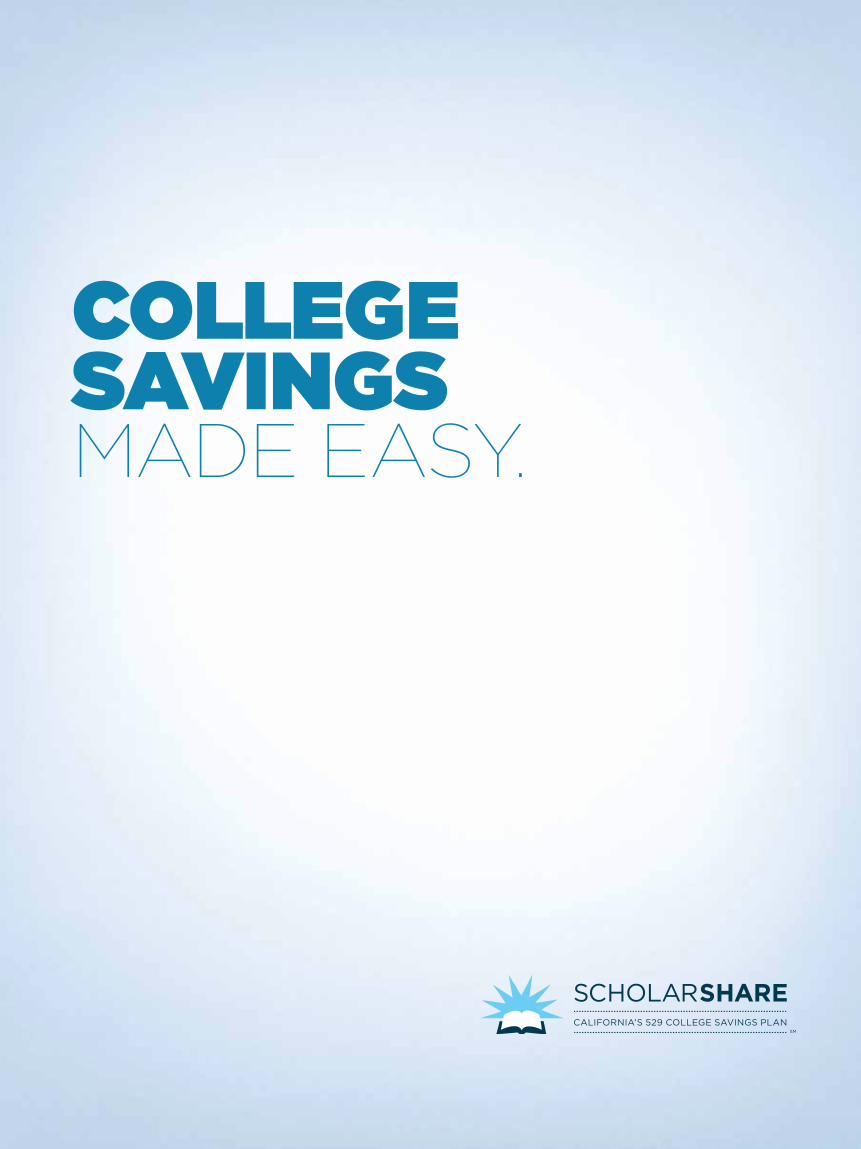

Start small. Start early.A person who goes to college typically earns more than a person who does not.

$89,960

$69,732

$35,256

$59,124

$41,496

$0 $50,000 $100,000

High SchoolDiploma

Bachelor’sDegree

AssociateDegree

Master’sDegree

ProfessionalDegrees

Source: “Earnings and unemployment rates by educational attainment,” Bureau of Labor Statistics. 2015, http://www.bls.gov/emp/ep_table_001.htm (March 15, 2016). (Note: Data are for persons age 25 and over. Earnings are for full-time wage and salary workers.

Planning is the key to achieving a college education. Planning for higher

education involves both academic and financial preparedness. There are

many excellent resources available to help you navigate the path toward

college, which can start as early as a few weeks after your child is born.

Helpful resources for families with children of all ages include:

californiacolleges.edu, FederalStudentAid.ed.gov and edpubs.ed.gov.

Start small. Dream big.Whether your child or loved one is a newborn or entering high school, ScholarShare, California’s 529 College Savings Plan, can help you achieve your college savings goals.

In 2016, college graduates in the United States completed their education

with an average debt of $37,172 (https://studentloanhero.com/student-loan-

debt-statistics-2016/). Starting a career with this amount of debt can limit

your loved ones’ retirement savings, delay their first home purchase or

even impact their ability to provide for their own families. ScholarShare

provides you with the ability to contribute to your family’s financial well-

being. While some may find the very thought of saving for higher

education overwhelming, you should remember that relatives, especially

grandparents, may want to contribute as well. You may also aim to fund

just a portion of your loved one’s education with the understanding that

every dollar invested is potentially one less dollar borrowed later. Your

loved one’s brighter future can start today.

GIVE THE GIFT OF EDUCATION

It’s customary for relatives and friends to give your child(ren) gifts on birthdays and other special occasions. So tell them you’ve opened a ScholarShare Account and ask if they would consider making a contribution toward your child(ren)’s college education or open an Account instead of gifting the typical toy.

At ScholarShare.com, Account owners, as well as friends and family, can download a Gift of Education Certificate to include with a card or wrap it with a bow.

Like ScholarShare on Facebook and follow us on Twitter for tips on everything from how to save money to running a more efficient household.

FRIENDS & RELATIVES

GRA

NDPA

RENTS

PAREN

TS

EDUCATION

4 | SCHOLARSHARE

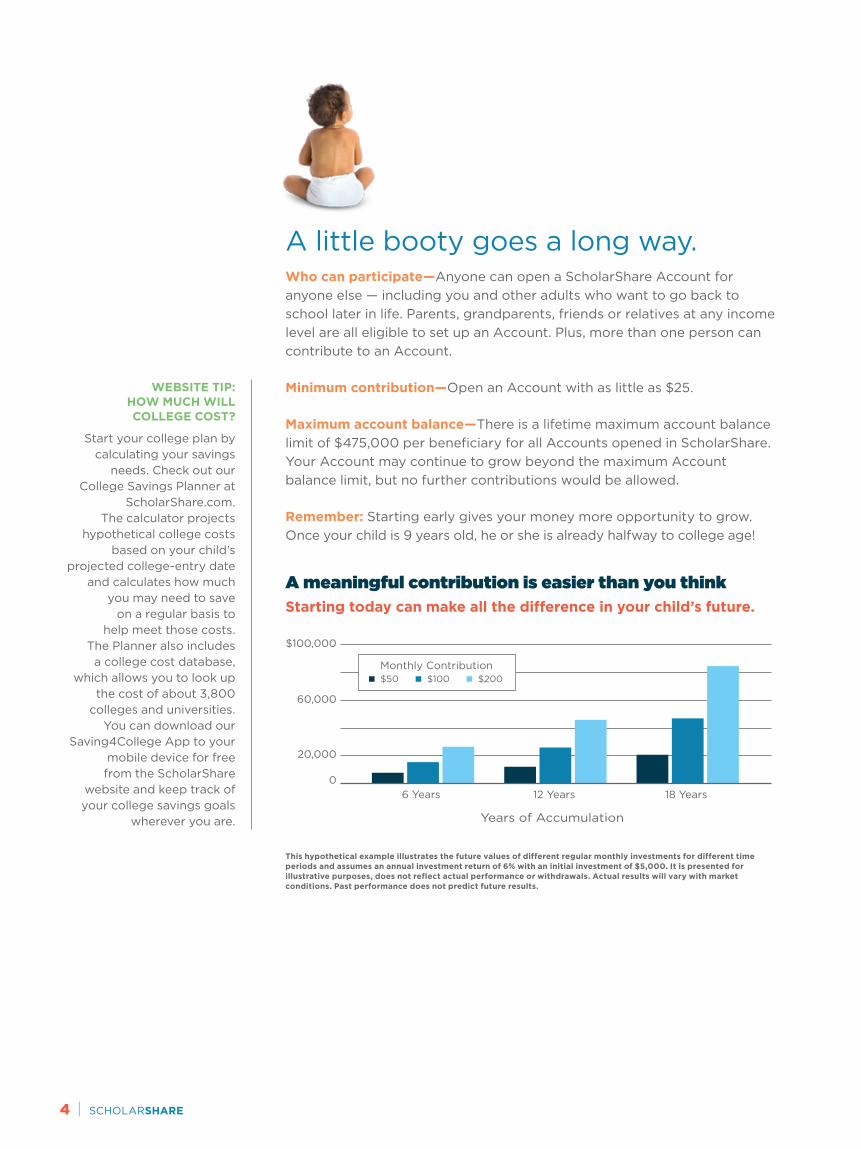

A little booty goes a long way.Who can participate — Anyone can open a ScholarShare Account for

anyone else — including you and other adults who want to go back to

school later in life. Parents, grandparents, friends or relatives at any income

level are all eligible to set up an Account. Plus, more than one person can

contribute to an Account.

Minimum contribution — Open an Account with as little as $25.

Maximum account balance — There is a lifetime maximum account balance

limit of $475,000 per beneficiary for all Accounts opened in ScholarShare.

Your Account may continue to grow beyond the maximum Account

balance limit, but no further contributions would be allowed.

Remember: Starting early gives your money more opportunity to grow.

Once your child is 9 years old, he or she is already halfway to college age!

A meaningful contribution is easier than you thinkStarting today can make all the difference in your child’s future.

Years of Accumulation

Monthly Contribution■ $50 ■ $100 ■ $200

$100,000

6 Years 12 Years 18 Years

60,000

20,000

0

This hypothetical example illustrates the future values of different regular monthly investments for different time periods and assumes an annual investment return of 6% with an initial investment of $5,000. It is presented for illustrative purposes, does not reflect actual performance or withdrawals. Actual results will vary with market conditions. Past performance does not predict future results.

WEBSITE TIP: HOW MUCH WILL COLLEGE COST?

Start your college plan by calculating your savings

needs. Check out our College Savings Planner at

ScholarShare.com. The calculator projects

hypothetical college costs based on your child’s

projected college-entry date and calculates how much

you may need to save on a regular basis to

help meet those costs. The Planner also includes a college cost database,

which allows you to look up the cost of about 3,800

colleges and universities. You can download our

Saving4College App to your mobile device for free from the ScholarShare

website and keep track of your college savings goals

wherever you are.

CALIFORNIA’S 529 COLLEGE SAVINGS PLAN | 5

Choose the right bucket: tax advantages of a 529 can boost your account.ScholarShare is a 529 College Savings Plan that provides

federal and state tax deferrals on any earnings. Money you

withdraw to pay for qualified higher education expenses is

also free from state and federal income taxes.*

Gifting benefitFederal Estate and Gift Tax Benefits: Contributions to ScholarShare may

reduce the taxable value of your estate. For example, money placed in a

grandchild’s ScholarShare Account, combined with the other gifts you give

that grandchild during one year, may qualify for an annual federal gift tax

exclusion of $14,000**. Ask your tax advisor about your own situation.

Couples filing jointly can contribute up to $140,000 per child and take

advantage of five years worth of tax-free gifts at one time** ($70,000 for

individual filers). Completed gifts are removed from your estate for tax**

purposes, so your investment goes toward a child’s education, not taxes.

Consult your tax advisor about your own situation.

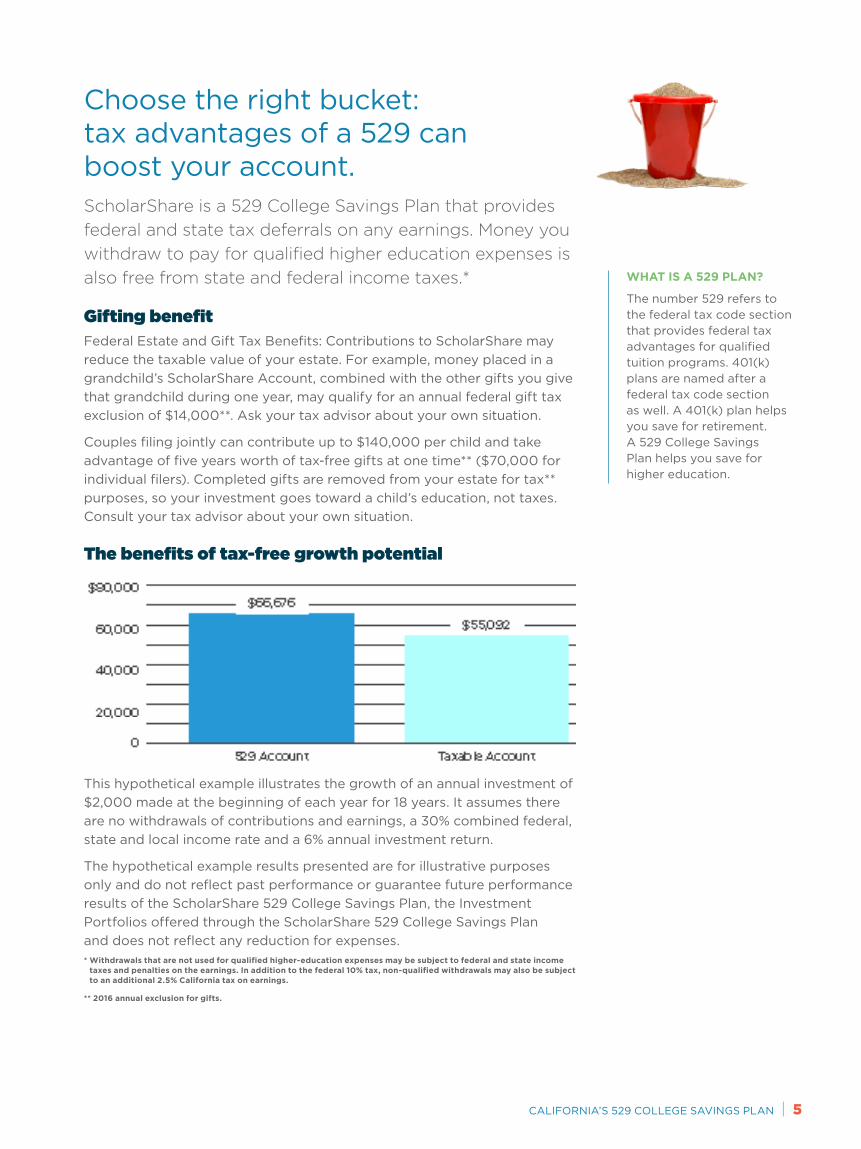

The benefits of tax-free growth potential

This hypothetical example illustrates the growth of an annual investment of

$2,000 made at the beginning of each year for 18 years. It assumes there

are no withdrawals of contributions and earnings, a 30% combined federal,

state and local income rate and a 6% annual investment return.

The hypothetical example results presented are for illustrative purposes

only and do not reflect past performance or guarantee future performance

results of the ScholarShare 529 College Savings Plan, the Investment

Portfolios offered through the ScholarShare 529 College Savings Plan

and does not reflect any reduction for expenses.

* Withdrawals that are not used for qualified higher-education expenses may be subject to federal and state income taxes and penalties on the earnings. In addition to the federal 10% tax, non-qualified withdrawals may also be subject to an additional 2.5% California tax on earnings.

** 2016 annual exclusion for gifts.

WHAT IS A 529 PLAN?

The number 529 refers to the federal tax code section that provides federal tax advantages for qualified tuition programs. 401(k) plans are named after a federal tax code section as well. A 401(k) plan helps you save for retirement. A 529 College Savings Plan helps you save for higher education.

6 | SCHOLARSHARE

You can get there.You can use ScholarShare funds: ■■ At thousands of eligible educational institutions nationwide and many

internationally — including community colleges, trade schools and

many post-secondary programs.

■■ For tuition, fees, books, supplies and equipment required for enrollment

or attendance at an eligible educational institution.

■■ For certain room and board expenses.

Control of the moneyAs owner of the account:

■■ You maintain complete control of the Account regardless

of your beneficiary’s age.

■■ You make the decisions from selecting the ScholarShare

investment portfolios to making withdrawals from your Account.

■■ You can name a successor Account owner and you can transfer

the ownership to another person.

Transfer to another BeneficiaryIf your designated beneficiary decides not to attend college, or has

other funding options, you may transfer funds in your Account to certain

eligible family members of the original beneficiary, including siblings,

a spouse, first cousins — even yourself. Refer to the Disclosure Booklet

for additional details.

RolloversYou can roll over the money from another 529 College Savings Plan

into your ScholarShare Account to take advantage of all the benefits

of ScholarShare.

Note: Transfers and rollovers may be subject to differences in features,

costs and surrender charges. Indirect transfers may be subject to taxation

and penalties. Consult your tax advisor about your own situation.

WEBSITE TIP: COMPARE COLLEGE

SAVINGS OPTIONS

Use our web-based tool at ScholarShare.com to

compare many popular ways to save for college, such

as custodial accounts (UGMA/UTMA) and Coverdell Education Savings Accounts,

as well as 529 College Savings Plans.

CALIFORNIA’S 529 COLLEGE SAVINGS PLAN | 7

LOW FEES

ScholarShare is among the lowest cost 529 College Savings Plans in the country.

There are no application fees, sales fees or maintenance charges for your

ScholarShare Account, just a total annual asset-based management fee.

The total annual asset-based management fee is less than 0.5% for most

of the investment portfolios. Low fees give you the opportunity to put

more of your money toward future college expenses. The asset-based

management fee varies across each of the 19 investment portfolios, and

there is no asset-based management fee on the Principal Plus Interest

Portfolio. For more information, refer to the Fee Table in the enclosed

Disclosure Booklet.

Power of compounding interestWhen you add the power of compounding interest to ScholarShare’s

tax-free earning potential and low fees, you’ll see your investments

have a chance to grow.

ScholarShare’s Program Manager: TIAA-CREF Tuition Financing, Inc.

TIAA-CREF Tuition Financing, Inc. (TFI), part of the TIAA group of companies, is a leader in 529 college savings plan management. TFI provides program management services for ScholarShare. With combined assets under management of $861 billion as of March 31, 2016, TIAA is a national financial services group of companies and a leading provider of retirement services in the academic, research, medical and cultural fields.

WEBSITE TIP: WHAT YOU CAN DO ONLINE

When you set up online access to your ScholarShare Account, you can:

• Access Account information

• Make contributions

• Set up an Automatic Contribution Plan (ACP)

• Sign up for e-delivery of your statements and disclosure material

• Request withdrawals online to your bank account on file and even have funds sent directly to your beneficiary’s school

• Download Account data into Quicken®

• Visit the ScholarShare mobile-optimized secure website to access Account information and execute various transactions from your smartphone or mobile device.

• Join California’s 529 College Savings Plan online community by following ScholarShare on Twitter @ScholarShare529 and liking us on Facebook at facebook.com/scholarshare529

8 | SCHOLARSHARE

ScholarShare investment portfoliosYou can invest contributions in any one or a combination

of Scholar Share’s 19 investment portfolios. These portfolios

vary in their investment strategy and degree of risk,

allowing you to select a portfolio or combination of

portfolios that fit(s) your needs.

ScholarShare offers three broad categories of investment portfoliosActive investment portfolios

The fund manager selects the securities to buy for the fund.

■■ Age-based Portfolio, actively managed

■■ Seven single-focus actively managed portfolios

Passive investment portfolios

Securities are selected to mirror a specific market index.

■■ Age-based Portfolio, passively managed

■■ Nine single-focus passively managed portfolios

Principal Plus Interest Investment Portfolio

Assets allocated to a guaranteed Funding Agreement issued by TIAA-CREF Life Insurance Company (TIAA Life).

A word about riskEach investment portfolio has its own risks. For example, international

investing poses special risks — currency, political, social and economic.

Investments in growth stocks may be more volatile than other securities.

Fixed income investing entails credit and interest risks. When interest rates

rise, bond prices generally fall, and the underlying fund’s share price can

fall. Investment returns during your investment period could be lower than

the rate of increase in higher education costs during that period. It’s also

possible to lose all or part of the value of your Account.

SELECT THE INVESTMENT PORTFOLIO

THAT IS RIGHT FOR YOU

Although Age-based investments are very popular,

some investors prefer to create their own asset

allocation strategy. You can customize an investment

strategy that better matches your tolerance for risk, your time horizon and

other factors. Unlike the Age-based Portfolios,

your unique investment allocations will not

automatically change as the beneficiary ages.

CALIFORNIA’S 529 COLLEGE SAVINGS PLAN | 9

How do Age-based Portfolios work?An Age-based investment uses the age of your beneficiary

to determine the appropriate investment allocation.

The Age-based approach invests aggressively when the

child (the beneficiary) is young and more conservatively

as the child gets older.

Sample allocation of an Age-based Portfolio designed for a child age 0 – 4*

* Allocations automatically change over time. For illustrative purposes only and not representative of any specific age band for either the Active Age-based Portfolio or the Passive Age-based Portfolio.

REVISIT YOUR INVESTMENT STRATEGY

Re-examine your ScholarShare Account when:

• Your goals, time period for college investing, or personal financial situation change.

• There are long-term changes in the economy that will affect how you save or invest.

• The balance in your Account changes significantly due to varying performances of different investment portfolios over time.

10 | SCHOLARSHARE

Active investment portfolios ScholarShare offers eight actively managed investment portfolios. An actively managed portfolio invests primarily in Underlying Funds that are actively managed. An actively managed fund is different from a passively managed fund in that an actively managed fund is not managed to track its benchmark index, but rather, managed pursuant to the investment style and strategy of an investment manager. This means that the performance of an actively managed fund can vary greatly from that of its benchmark index — in either a positive or negative direction.

SHARE MORE NOW. BENEFIT MORE LATER.

The more you invest and the earlier you start, the more opportunity your money has to grow.

■■ Calculate how much you need to invest.

■■ Set your goals.

■■ Set up an Automatic Contribution Plan (ACP) and have your contributions

electronically sent from your bank account to your ScholarShare Account.

■■ Contribute through payroll deduction, if your employer offers it.

Active Investment Portfolios

Investment Objective and Strategy

Active Age-Based

Portfolio

Seeks to match the investment objective and level of risk to the the client’s investment horizon

by taking into account the Beneficiary’s current age and the number of years before the

Beneficiary turns 18 and is expected to enter college. Invests primarily in Underlying Funds

that are actively managed.

Active Diversified

Equity Portfolio

Seeks to provide a favorable long-term total return by investing primarily in actively managed

equity Underlying Funds.

Active Growth

Portfolio

Seeks to provide a favorable long-term total return, mainly from capital appreciation,

by investing primarily in a combination of actively managed equity and fixed-income

Underlying Funds.

Active Moderate

Growth Portfolio

Seeks moderate growth by investing primarily in a combination of actively managed equity

and fixed-income Underlying Funds.

Active Conservative

Portfolio

Seeks to provide preservation of capital along with a moderate rate of return. Approximately

half of the Portfolio invests in actively managed Underlying Funds that invest primarily in

fixed-income securities. The rest of the Portfolio is allocated to a Funding Agreement.

Active International

Equity Portfolio

Seeks to provide a favorable long-term total return by investing in actively managed

international equity Underlying Funds.

Active Diversified

Fixed Income

Portfolio

Seeks to provide preservation of capital along with a moderate rate of return by investing

primarily in actively managed Underlying Funds that invest in a diversified mix of

fixed-income investments.

Social Choice

Portfolio

Seeks to provide a favorable long-term total return. Invests 100% of its assets in the

TIAA Social Choice Equity Fund, which invests primarily in equity securities of companies that

meet certain social criteria.

Underlying funds for ScholarShare

investment portfolios include Dimensional

Fund Advisors (DFA), PIMCO, T. Rowe Price, TIAA and

MetWest.

CALIFORNIA’S 529 COLLEGE SAVINGS PLAN | 11

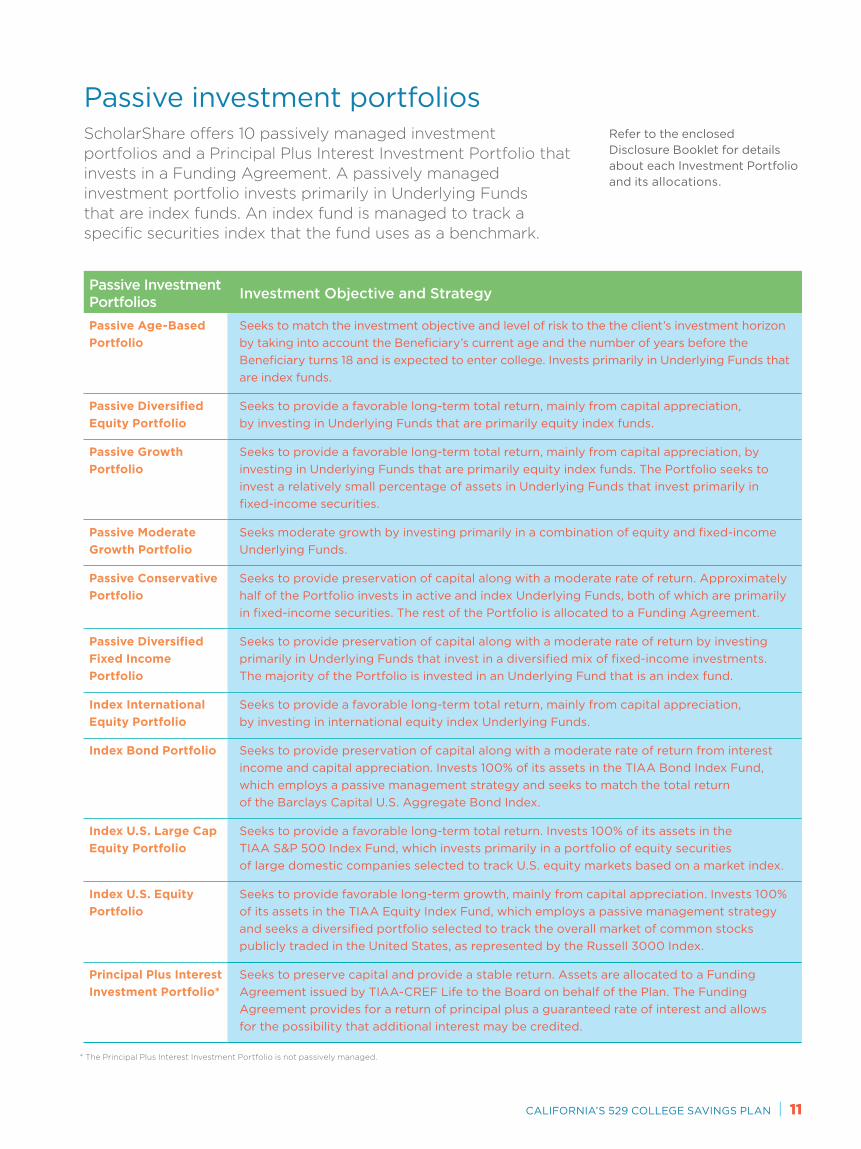

Passive investment portfoliosScholarShare offers 10 passively managed investment portfolios and a Principal Plus Interest Investment Portfolio that invests in a Funding Agreement. A passively managed investment portfolio invests primarily in Underlying Funds that are index funds. An index fund is managed to track a specific securities index that the fund uses as a benchmark.

Passive Investment Portfolios

Investment Objective and Strategy

Passive Age-Based

Portfolio

Seeks to match the investment objective and level of risk to the the client’s investment horizon

by taking into account the Beneficiary’s current age and the number of years before the

Beneficiary turns 18 and is expected to enter college. Invests primarily in Underlying Funds that

are index funds.

Passive Diversified

Equity Portfolio

Seeks to provide a favorable long-term total return, mainly from capital appreciation,

by investing in Underlying Funds that are primarily equity index funds.

Passive Growth

Portfolio

Seeks to provide a favorable long-term total return, mainly from capital appreciation, by

investing in Underlying Funds that are primarily equity index funds. The Portfolio seeks to

invest a relatively small percentage of assets in Underlying Funds that invest primarily in

fixed-income securities.

Passive Moderate

Growth Portfolio

Seeks moderate growth by investing primarily in a combination of equity and fixed-income

Underlying Funds.

Passive Conservative

Portfolio

Seeks to provide preservation of capital along with a moderate rate of return. Approximately

half of the Portfolio invests in active and index Underlying Funds, both of which are primarily

in fixed-income securities. The rest of the Portfolio is allocated to a Funding Agreement.

Passive Diversified

Fixed Income

Portfolio

Seeks to provide preservation of capital along with a moderate rate of return by investing

primarily in Underlying Funds that invest in a diversified mix of fixed-income investments.

The majority of the Portfolio is invested in an Underlying Fund that is an index fund.

Index International

Equity Portfolio

Seeks to provide a favorable long-term total return, mainly from capital appreciation,

by investing in international equity index Underlying Funds.

Index Bond Portfolio Seeks to provide preservation of capital along with a moderate rate of return from interest

income and capital appreciation. Invests 100% of its assets in the TIAA Bond Index Fund,

which employs a passive management strategy and seeks to match the total return

of the Barclays Capital U.S. Aggregate Bond Index.

Index U.S. Large Cap

Equity Portfolio

Seeks to provide a favorable long-term total return. Invests 100% of its assets in the

TIAA S&P 500 Index Fund, which invests primarily in a portfolio of equity securities

of large domestic companies selected to track U.S. equity markets based on a market index.

Index U.S. Equity

Portfolio

Seeks to provide favorable long-term growth, mainly from capital appreciation. Invests 100%

of its assets in the TIAA Equity Index Fund, which employs a passive management strategy

and seeks a diversified portfolio selected to track the overall market of common stocks

publicly traded in the United States, as represented by the Russell 3000 Index.

Principal Plus Interest

Investment Portfolio*

Seeks to preserve capital and provide a stable return. Assets are allocated to a Funding

Agreement issued by TIAA-CREF Life to the Board on behalf of the Plan. The Funding

Agreement provides for a return of principal plus a guaranteed rate of interest and allows

for the possibility that additional interest may be credited.

* The Principal Plus Interest Investment Portfolio is not passively managed.

Refer to the enclosed Disclosure Booklet for details about each Investment Portfolio and its allocations.

12 | SCHOLARSHARE

Who can open an Account?

Anyone can open an Account regardless of income. This includes

parents, grandparents, friends or relatives. Account owners must be

a U.S. citizen with a valid Social Security Number or federal Taxpayer

Identification Number.

Who can be an Account beneficiary?

As the owner of the Account, you can designate anyone as the

beneficiary — even yourself! The beneficiary must have a valid

Social Security Number or federal Taxpayer Identification Number.

Only one person may be listed as beneficiary for each Account.

Can more than one person contribute to the Account?

Anyone can contribute to an Account as long as the maximum Account

balance does not exceed $475,000 per beneficiary. The Account owner

has sole control over the assets and decides when to withdraw them.

Can I change the beneficiary?

You can change your beneficiary at any time or transfer a portion of

your investment to a different beneficiary. The new beneficiary must

be an eligible member of the previous beneficiary’s family.

What if my child or loved one decides not to attend college?

You have three choices:

■■ Keep the funds in the Account and the investments will be available in

future years if the beneficiary changes her or his mind about school.

■■ Change the beneficiary to an eligible family member. Consult your tax

advisor about whether this may create a taxable gift.

■■ Make a non-qualified withdrawal. Any earnings will be subject to federal

income tax and any applicable state income tax, as well as an additional

10% federal tax and 2.5% California tax on earnings.

Answers to your questions

CALIFORNIA’S 529 COLLEGE SAVINGS PLAN | 13

Will having a ScholarShare Account hurt my child’s or loved one’s chances for financial aid?

■■ If the parent is the Account owner, the Account assets will be treated

as belonging to the parent for federal financial aid purposes.

■■ If a dependent child is the Account owner, or the beneficiary of an

account holding UGMA/UTMA assets, Account assets are treated

as a student asset for financial aid purposes.

■■ Financial aid policies vary across post-secondary institutions,

so check with the institution directly for more information.

What if my child or loved one gets a full or partial scholarship?

If the child receives a scholarship that covers the cost of qualified higher

education expenses, you can withdraw up to the scholarship amount free

of the 10% additional federal tax and the additional 2.5% California tax on

earnings. However, the earnings portion of the withdrawal, if any, is subject

to federal and California income tax.

If I leave California, what will happen to my Account?

If you move to another state, you can still keep your money invested in

your ScholarShare Account, and you can continue contributing to it.

Remember, before investing in another 529 College Savings Plan, consider

whether the state in which you or your designated beneficiary resides has

a 529 College Savings Plan that offers favorable state income tax or other

benefits that are available only if you invest in that state’s 529 College

Savings Plan.

Can I roll over funds from another 529 plan into ScholarShare?

You can transfer funds for the same beneficiary once per 12-month period

without triggering federal or state income tax. Remember, the 529 College

Savings Plan from which you transfer funds may be subject to differences

in features, costs and surrender charges. Consult your tax advisor or the

other 529 College Savings Plan provider before requesting a rollover.

How do I make withdrawals?

It is easy to withdraw funds when your beneficiary is ready for college.

Withdrawals can be processed online, from your phone or smartphone or

by completing and submitting a Withdrawal Request Form.

STILL HAVE QUESTIONS?

Call toll free: 800-544-5248. One of our college savings plan consultants will answer your questions.

14 | SCHOLARSHARE

Tiny changes can add up.

Commit to making it happen with ScholarShare and enjoy these features:■■ Tax deferral on any earnings

■■ Tax-free withdrawals for qualified higher education expenses

■■ Choice of schools nationwide and many abroad

■■ Funds may be used for tuition, fees, supplies, computers,

required equipment and certain room and board expenses

■■ Gift- and estate-tax advantages

■■ Low minimum contribution and high Account maximum

■■ Low fees

■■ Family and friends may contribute

What you will need■■ The beneficiary’s, Account owner’s and successor Account owner’s

date of birth, Social Security Number or federal Taxpayer Identification

Number. Designating a successor Account owner, the individual who

will take over the Account in the event of the Account owner’s death,

is optional.

■■ Select an investment portfolio(s) that match(es) your investment

objectives.

Open your ScholarShare Account today

Online: ScholarShare.com. Click on “Open an

Account” on the home page.

Mail: Complete and sign the ScholarShare Account

Application and return with your initial contribution

in the enclosed envelope.

READY TO ENROLL? TWO EASY WAYS:

1. Enroll online at ScholarShare.com

2. Complete and mail the enclosed paper

application, along with your initial

contribution, to: ScholarShare College

Savings Plan P.O. Box 55205

Boston, MA 02205-5205

We’re here to help. Call us toll-free at

800-544-5248

CALIFORNIA’S 529 COLLEGE SAVINGS PLAN | 15

P.O. Box 55205 Boston, MA 02205-5205

Consider the investment objectives, risks, charges and expenses before investing in the ScholarShare College Savings Plan. Visit ScholarShare.com for a Plan Disclosure Booklet containing this and other information. Read it carefully. Investments in the Plan are neither insured nor guaranteed, and there is a risk of investment loss. TIAA-CREF Tuition Financing, Inc., plan manager. TIAA-CREF Individual & Institutional Services, LLC, member FINRA, distributor and underwriter for ScholarShare 529 College Savings Plan. Taxpayers should seek advice from an independent tax advisor based on their own particular circumstances. Non-qualified withdrawals may be subject to federal and state taxes and the additional federal 10% tax. Non-qualified withdrawals may also be subject to an additional 2.5% California tax on earnings. Before investing in a 529 plan, consider whether the state where you or your Beneficiary resides has a 529 plan that offers favorable state tax benefits that are available if you invest in that state’s 529 plan.The ScholarShare 529 College Savings Plan Twitter and Facebook pages are managed by the State of California. Neither TIAA-CREF Tuition Financing, Inc., nor its affiliates, are responsible for the content found on any external website links contained herein.108393 A13092 08/16 CA1111.XXB

16SCH250-05_031517