Embed Size (px)

Citation preview

COLLECTIVE INVESTMENTFUNDS AND ERISA

Marcia S. Wagner, Esq.

2

1. CIFs and ERISA2. DOL Tips for Selecting TDFs3. CIF Advantages

What Is A CollectiveInvestment Fund (“CIF”)

Created by declaration of trust.Corporate trustee (bank or trust company).“Maintained” by the bank trustee.◦Adviser can partner with bank to create

customized investment vehicles.◦Bank must be in overall control.

Limited to holding assets of tax-qualified plan.◦Trust exempt from entity level taxation.◦Trust instrument restricts use of assets to

exclusive benefit of plan participants.3

Application of ERISA to CIF’sERISA look-through rule means plan assets

include interest in every underlying CIF asset.CIF trustee and investment adviser treated as

ERISA fiduciaries.CIF subject to ERISA reporting and disclosure

(e.g., Form 5500).CIF transactions subject to ERISA prohibited

transaction rules unless exemption applies.◦ Investing in proprietary products could be

prohibited.◦ Investing in securities of plan sponsor could

be prohibited. 4

Prohibited Transaction Exemptions

ERISA Section 408(b)(8) exempts a plan’s purchase of a CIF interest from the bank.◦Allows trustee to charge additional fees for

asset management with no offset.◦Exemption conditioned on approval of

affiliated fiduciary or approval written into plan documents.

◦Favorable result compared to mutual funds.

5

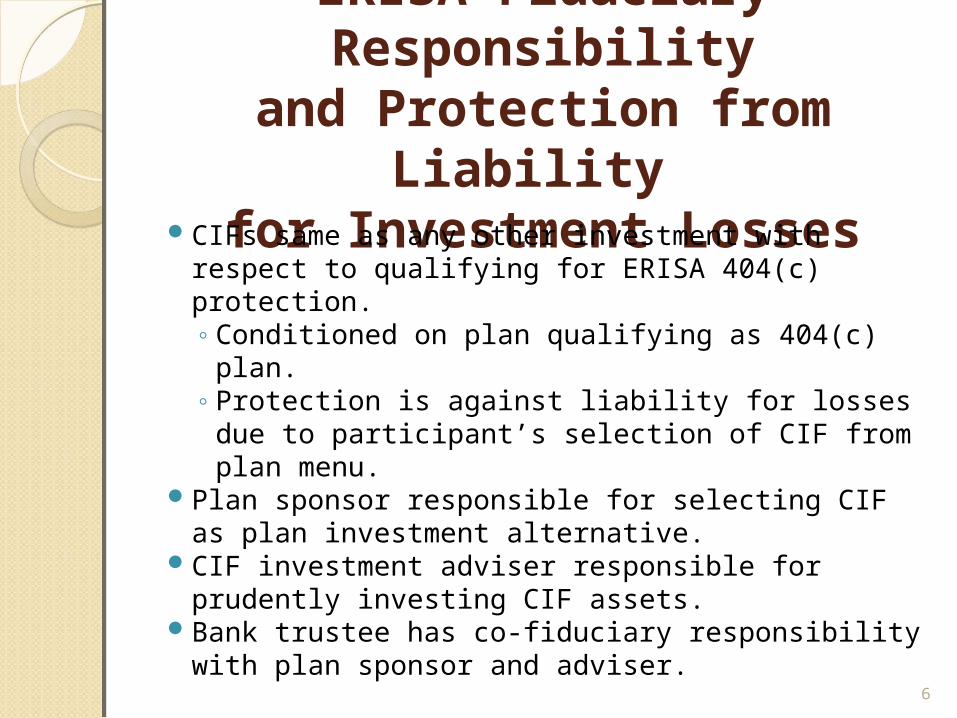

ERISA Fiduciary Responsibilityand Protection from Liability

for Investment LossesCIFs same as any other investment with respect to

qualifying for ERISA 404(c) protection.◦Conditioned on plan qualifying as 404(c) plan.◦ Protection is against liability for losses due to

participant’s selection of CIF from plan menu.Plan sponsor responsible for selecting CIF as plan

investment alternative.CIF investment adviser responsible for prudently

investing CIF assets.Bank trustee has co-fiduciary responsibility with plan

sponsor and adviser.

6

Example of How FiduciaryResponsibility Allocated

Plan sponsor adds 3 risk-based CIFs to plan menu: aggressive, moderate, conservative.◦ Participant alone responsible for picking appropriate

fund based on participant’s risk profile.◦No fiduciary liability if risk averse participant picks

aggressive CIF.CIF adviser liable for imprudent investment of CIF’s

underlying assets.Bank also liable for CIF adviser’s imprudent investment

decisions.Plan sponsor only responsible if failed to prudently

monitor CIF.

7

Participant-Level Disclosuresfor CIFs

Each CIF treated as designated investment alternative.◦Each CIF to be included on comparative chart

furnished to participants.◦Standardized performance information for

each CIF required, including benchmarking.◦Total annual operating expenses (including

investment fees) to be disclosed.◦CIF’s investment strategy would need to be

discussed in required website posting.

8

Participant-Level Disclosuresfor CIFs (cont’d)

Bank trustees have recordkeeping and disclosure systems comparable to mutual funds.

CIF providers can reduce disclosure compliance burden.◦Performance calculations.◦Unitized accounting.

9

Qualification of CIFs as QDIAQDIA rules provide relief from liability when

participant defaults into investment.Product investment strategy must be either:◦Target date, or◦Balanced.

CIF fiduciary must have discretion over CIF’s underlying assets under QDIA rules.

10

11

1. CIFs and ERISA2. DOL Tips for Selecting TDFs3. CIF Advantages

DOL’s Tips for Choosing TDFs - Background

TDFs often used as QDIA, relieving plan fiduciaries of liability for default investment losses.

ERISA prudence requires objective process.CIFs with TDF strategy can also qualify as QDIA.◦Obtain information about TDF.◦Use information to evaluate TDF.◦ Periodically review decision.◦Document how decision made.

Proposed TDF regulations focusing on disclosure issued November 2010.

DOL tips on choosing TDFs issued February 28, 2013.

12

Comparison, Evaluation& Review of TDFs

Get information from prospectus:◦ investment performance◦ fees and expenses◦ target date◦glidepath◦ landing point.

Obtain additional information (e.g., salary levels, turnover).

Ensure TDF characteristics match needs of participants.

13

Comparison, Evaluation& Review of TDFs (cont’d)

Glidepath considerations.◦ Landing point may be reached at or after target

date.Periodically review TDF characteristics and plan

objectives for changes.◦TDF management team or strategy.◦Plan demographics.

14

Role of TDF’s UnderlyingInvestments

Understand TDFs underlying investments.Determine appropriate glidepath construction for

plan.◦ “To” retirement.◦ “Through” retirement.

Measure TDF fees and expenses against investment performance and service.◦Determine expense ratios of underlying funds.◦Consider relevant services:

Special asset allocation. Access to special investments.

15

Employee Communications Regarding TDFs

Information DOL thinks should be provided to participants:◦General information regarding TDFs (e.g.,

explanation of nature of glidepath).◦ Info about plan’s specific TDFs (e.g., actual

glidepath, historical performance and fees). DOL tips include its proposed regulatory

disclosures.◦TDF not guaranteed.◦Participant may lose money before, at and after

target date.

16

Use of Consultantsin Evaluating TDFs

DOL recognizes plan fiduciaries’ lack of expertise to evaluate TDFs which are a new and complex product.

DOL endorses use of “commercially available sources for information and services”.◦DOL presumably means to include advisers

with expertise to evaluate TDFs.Unquestioning reliance on consultant’s

recommendations not viewed as prudent.

17

18

1. CIFs and ERISA2. DOL Tips for Selecting TDFs3. CIF Advantages

Mutual Fund TDFs vs. CIF TDFsMutual Fund TDFs typically invest in affiliated funds.Conflicts within Mutual Fund TDFs may hurt

performance and increase fees.DOL recommends inquiring about customized TDFs

consisting of plan’s core funds.◦ CIF’s underlying investments would be unaffiliated,

resulting in greater diversification.◦ Potential disadvantage is higher cost and

administrative complexity.◦ Better fiduciary result.

19

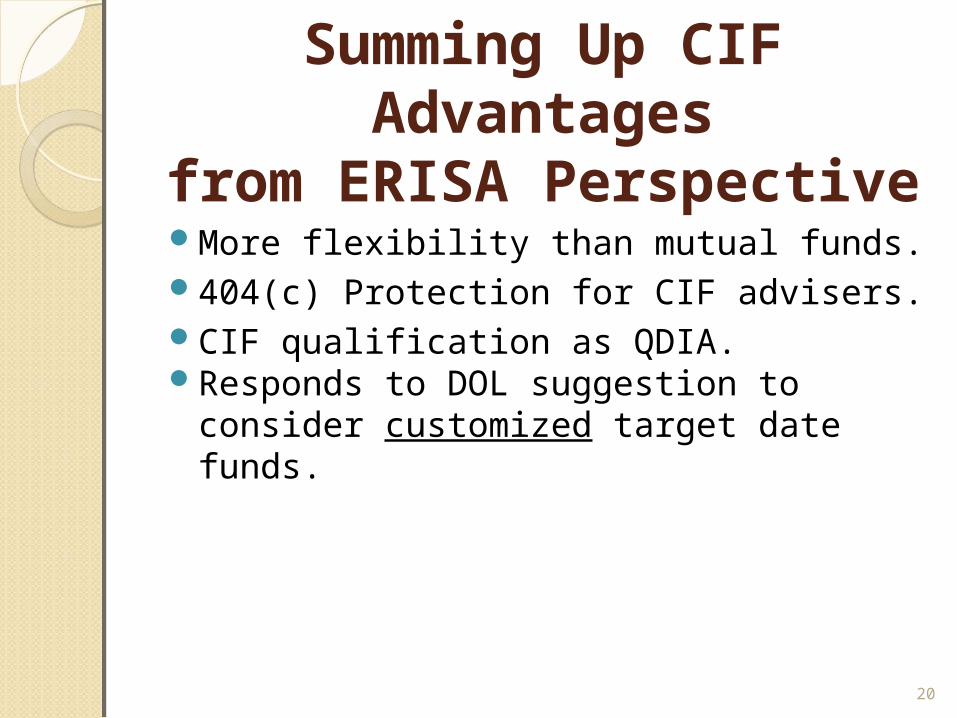

Summing Up CIF Advantagesfrom ERISA Perspective

More flexibility than mutual funds.404(c) Protection for CIF advisers.CIF qualification as QDIA.Responds to DOL suggestion to consider

customized target date funds.

20

21

COLLECTIVE INVESTMENTFUNDS AND ERISA

Marcia S. Wagner, Esq.

99 Summer Street, 13th FloorBoston, MA 02110

Tel: (617) 357-5200 Fax: (617) 357-5250 Website: www.wagnerlawgroup.com

[email protected] A0095235