Embed Size (px)

Citation preview

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 1/33

M a n i s h G o e l

2 0 0 8

R e t a i l B o o m

: E m e r g e n c e o f C o l l a b o r a t i v e m o d e l s w i t h

A g r i c u l t u r a l s e c t o r

This is the report of the Final year project for the course of Post

graduate Program in Business Design

Submitted by:-

Manish Goel

Roll No – 13

Welingkar Institute of Management Development and Research,

L Napoo Road, Matunga, Mumbai - 400030

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 2/33

1

“Retail Boom: Emergence of Collaborative models with Agricultural sector”

IN PARTIAL FULFILMENT OF THE REQUIREMENTS FOR POST GRADUATE PROGRAM IN

BUSINESS DESIGN (VERTICAL- Finance)

(2006-08)

COURSE: PGPBD

ROLL NO: 13

Welingkar Institute of Management Development & Research

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 3/33

2

CERTIFICATE FROM GUIDE (Internal)

This is to certify that project entitled " Retail Boom: Emergence of Collaborative models with

Agricultural sector” is successfully done by Mr. Manish Goel during the VI Trimester of his coursePGPBD-Finance in partial fulfillment of the Post Graduate Program in Business Design as per the

requirements of rules by AICTE (PGPBD) through the Prin.L.N.Welingkar Institute of Management

Development & Research, Matunga, Mumbai. He has applied to Bank of India for approval of the project

and the allotment of a mentor. He was allowed to do project under my guidance. Attached is the

photocopy of the approval letter.

This project represents the work done by Mr. Manish Goel.

This project in general is done under my supervision.

Date: _____________ Name of Guide: Prof.

Address of Guide: ___________________________________

____________________________________

____________________________________

Tel.No: ____________________________________

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 4/33

3

CERTIFICATE FROM GUIDE (External)

This is to certify that project entitled " Retail Boom: Emergence of Collaborative models with

Agricultural sector” is successfully done by Mr. Manish Goel during the VI Trimester of his coursePGPBD-Finance in partial fulfillment of the Post Graduate Program in Business Design as per the

requirements of rules by AICTE (PGPBD) through the Prin.L.N.Welingkar Institute of Management

Development & Research, Matunga, Mumbai.

This project represents the work done by Mr. Manish Goel.

This project in general is done under my guidance.

Date: _____________ Name of Guide: Prof.

Address of Guide: ___________________________________

____________________________________

____________________________________

Tel.No: ____________________________________

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 5/33

4

Acknowledgement

This project is a great learning experience for me and I believe it will make a difference to my perspective for

business and to my career as well. The project would not have been successfully complete without some people whohave contributed immensely towards it.

To start with I would like to thank My Guide from Bank of India Mr. Sudhakar Atre who approved to be my guide

for the project and to do research under him, HR Manger – Bank of India Ms. Aparna Shukla who was very

cooperative and approved my application for the project. Very special thanks to Prof. Bijoy Bhattacharya who

constantly contacted Bank of India for approving my project.

I am obliged to Mr. Uday Newalkar, Lead District Manager, Bank of India, Alibagh, and Mr. Lakshman

Jundhane, Field Executive, Bank of India, Alibagh for extending their support during my rural visit to Alibagh.

The different perspective that I have come out in the report would not have been possible without inputs from Mr.

Jayaraman, GM, DEAR, NABARD and Mr. Anand Kashid, AGM, (DD) and thus I am thankful to them. I am

thankful to Mr. Avinash Joshi, and Mr. Subham Ray from Food Bazaar, Future Group, for their valuable and

practical inputs. The project would not have been possible without the field visits in Pune and the valuable inputs of

Mr. Rashmi Abroal, Rashmi Grrenland Agri Tourist Centre who spend his valuable time with me and made my

visit a success.

I am thankful to Prof. Anil Naik (Dean- WRC), Prof. Sudhakar Nadkarni (Dean – Business Design), Prof.

Ketana Mehta (Asst. Dean –WRC), Prof. Pradeep Pendse (Dean – IT), Prof. Kaustubh Dhargalkar and Prof.

Anuja Agarwal for their support for the project.

I would like to acknowledge support from Ms. Aisha Panjwani (Coordiantor – Business Design) and Ms. Kalpana

Hunduja (Associate –WRC) for their motivation and support.

Above all I am thankful to my parents, my brothers and my friends who have been a great support the project and

always motivated me to do good work.

Without his support and guidance it would have been difficult for me to complete the project and derive so much of

learning out of it.

Manish goel

Welingkar Institute of Management Development & Research

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 6/33

5

Table of Contents

1. 0 INTRODUCTION................................................................................................................................ 6

1.0.1 Synopsis of the problem....................................................................................................................... 6

1.0.2 Research Objective .............................................................................................................................. 6

2.0 LITERATURE REVIEW .................................................................................................................... 7

2.0.1 Purpose................................................................................................................................................. 7

2.0.2 Keywords ............................................................................................................................................. 7

2.0.3.1 Source 1: Retail Industry to Boom in next 5 years (Source: CRISIL) .............................................. 8

2.0.3.2. Source 2: Global Retail Development Index Report 2007 (Source: www.atkearney.com)............. 8

2.0.3.3 Source 3: Retail Boom: New Opportunities in Agriculture finance, an article by Mr. Sudhakar V.

Atre, Sr. Manager & Faculty Member, Bank of India. .......................................................................... 10

2.0.3.4. Source 4: The Hindu Survey of Indian Agriculture 2007, Annual Survey on Agriculture by the

Newspaper Hindu.................................................................................................................................... 10

2.0.3.5. Rural Finance for Small farmers -An integrated approach by Hans Dellien and Elizabeth Lynch.

(Source: ‘The Indian Banker’ magazine)................................................................................................ 11

2.0.4. Conclusion ........................................................................................................................................ 12

2.0.5 Directions for Future Research .......................................................................................................... 123.0 Finalization of Hypothesis & Crystallization of Research Problem ............................................... 13

3.0.1 Hypothesis.......................................................................................................................................... 13

3.0.2 Crystallization of the problem............................................................................................................ 13

4.0 PLAN OF RESEARCH ...................................................................................................................... 14

5.0 PRESENTATION OF DATA AND DATA ANALYSIS ................................................................. 15

5.0.1. Hypothesis......................................................................................................................................... 15

5.0.2. Data required on the basis of identified problems ............................................................................ 15

5.0.3 Budget 2008: Agriculture loan waiver ............................................................................................... 15

5.0.3.1 ......................................................................................................................................................... 16

5.0.4 Economic Survey 2006-2007 ............................................................................................................. 17

5.0.4.1 Agricultural Insurance..................................................................................................................... 19

5.0.5 Initiatives by other banks and financial institutions........................................................................... 20

5.0.6 Data from Primary research ............................................................................................................... 22

5.0.6.1 Field Visit: Raigad District (Maharashtra State) / Service area: Alibagh ....................................... 22

5.0.6.2 Response from farmers through NABARD office .......................................................................... 22

5.0.6.3 Information from a retail company ................................................................................................. 23

5.0.6.4 Intercepts with farmers around Pune .............................................................................................. 23

5.0.7 Directions for further research ........................................................................................................... 26

5.0.8 Interpretation...................................................................................................................................... 26

6.0 CONCLUSION & CONCEPT CREATION .................................................................................... 28

6.0.1 Kisantrepreneur: Beginning of a collaboration.................................................................................. 28

6.0.2 Three C’s Approach: A step towards agriculture sector .................................................................... 29

6.0.3 Rural Credit: A multidimensional Entity ........................................................................................... 296.0.4 Three-pronged approach for Government.......................................................................................... 31

7.0 Limitations of the study ....................................................................................................................... 31

8.0 Bibliography ........................................................................................................................................ 32

Budget 2008: Agriculture loan waiver ........................................................................................................ 15

Keywords ...................................................................................................................................................... 7

Purpose.......................................................................................................................................................... 7

The summary of actual content..................................................................................................................... 8

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 7/33

1. 0 INTRODUCTION

1.0.1 Synopsis of the problem

The growth of the Retail sector in India is spectacular during past few years. The major corporate houses

in India (e.g. Tata, Birla, reliance, Bharti etc.) and the world's Giant retailers (e.g. Wal-Mart, Tesco,

Carrefour etc.) are doing their best to have the head start in the field and reap the benefits. Indian retail

industry expects to investment of over $ 30 billion over the next 5 years. The size of Retail market in

India is estimated between $320-350 billion which is growing at 30-35% per annum. Organised retail,

predominantly urban phenomenon constitutes about 4% of the total retail trade in India. India has about

30 Million retail outlets providing direct and indirect employment to nearly 18 million people. The

opportunity for the retail industry truly looks unprecedented.

The impact of corporate investment into retail is likely to be multi-faceted. The first and foremost is on

the supply chain-starting from the farmers to the consumers. There are many intermediaries in the supply

chain of farms produce which increases cost of agricultural produce which needs to be optimized.

Secondly, there are cases of suicide where it was observed that on an average an Indian farmer committed

suicide every 32 minutes between 1997 and 2005. Since 2002, that has become one suicide every 30

minutes. The reason is that they are unable to repay debts as they are unable to sell their farm produce.

Also despite being among the world's largest producers of food grains, fruits and vegetables, we are most

inefficient. An estimated 25-40 per cent of farm produce worth $12 billion (Rs. 50,400 crores) rots every

year even before it reaches consumers.

These issues pose a challenge whether our retail industry will be able to cope up the demand that Retail

boom will bring in recent years. If Retail industry has to cope up with this challenge, then they need come

up with some innovative collaborative models that will help them to leverage on the vast production of

Indian fields and to perform profitably in an Industry which operates on lesser margins.

1.0.2 Research Objective

Objective of the study is to explore different models where organisations have already entered into

collaborative model with Agricultural sector and to identify what are the attributes of the environment and

the entities involved for such collaboration. Also to identify possibilities which can lead to a developing

more such models to benefit from this approaching RETAIL BOOM.

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 8/33

7

2.0 LITERATURE REVIEW

2.0.1 Purpose

To clearly define the relationship between agricultural credit and Retail boom with the support of already

published research papers, articles and surveys. Thus, to identify what is the focus of further research and

what are the lines of enquiry.

2.0.2 Keywords

Retail Boom: India's retail estimated at size of $679 billion in 2006-07, which will swell to more than

$2366 billion by 2012 growing at 28% per annum.

Retailing: Retailing is the interface between the producer and the individual consumer buying for

personal consumption. This excludes direct interface between the manufacturer and institutional buyers

such as the government and other bulk customers. A retailer is one who stocks the producer’s goods and

is involved in the act of selling it to the individual consumer, at a margin of profit. As such, retailing is

the last link that connects the individual consumer with the manufacturing/production and distribution

chain.

Organised Retail: A form of retailing where by consumers can buy goods in a similar purchase

environment across more than one physical location.

Supply Chain: Supply chain management (SCM) is the oversight of materials, information, and finances

as they move in a process from producer/supplier to manufacturer to wholesaler to retailer to consumer.

Supply chain management involves coordinating and integrating these flows both within and among

companies. (Source: www.searchCIO.com)

Intermediation: Act of participation by different bodies or individuals in the supply chain of goods from

the producer to the supplier with the purpose of business and profit making. It may or may not add value

but increases the cost of goods with every increase in an intermediary in the chain.

Agriculture credit: Credit lending by different financial institutions to farmers or entities involved in

agriculture or related activities. These institutions include commercial banks, regional rural banks

(RRBs), cooperatives [comprising urban cooperative banks (UCBs), State co-operative banks (STCBs),

district central co-operative banks (DCCBs), primary agricultural credit societies (PACS), state co-

operative and agricultural rural development banks (SCARDBs) and primary co-operative and

agricultural rural development banks (PCARDBs)], financial institutions (FI) (term-lending institutions,

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 9/33

8

both at the Centre and State level, and refinance institutions) and non-banking financial companies

(NBFCs)

2.0.3 Summary of actual content

2.0.3.1 Source 1: Retail Industry to Boom in next 5 years (Source: CRISIL)

Summary:

Organised retail to treble in 5 years

As per the CRISL report for the year 2007-2008 the organised market is poised to grow at nearly 28 %

from an estimated Rs. 679 billion in 2006-07 to around Rs 2, 366 billion by 2010. Main factors

contributing to this robust growth will be the rising disposable income, demographic changes, growing

consumerism, and growth of retail malls etc. contributed mainly by 33 cities.

Food and grocery is the largest of all verticals of a retail company accounting for close to 67 per cent.

However, it has lowest penetration in organised retail, at around 1.3 per cent. Other sectors of footwear,

clothing and home décor etc are growing fast.

The report evaluates profitability of 3 verticals- apparels, household appliance and food & grocery which

together constitute 75% of the sore area in a typical hypermarket depending upon player to player.

Amongst these 3 vertical, apparels has the maximum scope for increasing share of private labels, there by

earning highest private margins. Brand and technology being the highest differentiator for household

appliances, it is difficult to sell private labels. Similarly there is no scope for increasing private labels in

food & grocery.

2.0.3.2. Source 2: Global Retail Development Index Report 2007 (Source: www.atkearney.com)

Summary: GRDI identifies window of opportunity to help retailers make strategic investments in

exciting new market. It ranks 30 top destinations and given below are the top ten where India emerged as

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 10/33

9

the top destination.

Figure 1: Ranks of countries in global retail destination list

The reason is that in the window of opportunity India appears in the zone where the retailing is peaking.

See the diagram below:-

Figure 2: Different phases of a retail boom

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 11/33

10

2.0.3.3 Source 3: Retail Boom: New Opportunities in Agriculture finance, an article by Mr.

Sudhakar V. Atre, Sr. Manager & Faculty Member, Bank of India.

Summary: The articles lead to the genesis of this research topic. It talks about the approaching Retail

boom in India and the challenges it will bring along like supply chain which is very essential. Because of

the lack of an effective supply chain there is wastage of 25-40% of agricultural produce waste in India

and nearly 1 trillion rupees can be saved as estimated by CRISIL. Also there are certain challenges for the

banks as well. First, it will result in greater investment in farm technology which will generate a huge

demand for Bank credit. Secondly, which perhaps is more important, it will aggregate demand, thereby

allowing direct sourcing from farmers. This will help greatly help bankers for credit expansion and credit

monitoring. But the big question is, are Banks ready for this challenge?

Thus the article stresses at innovative products in this field. PSB’s with their vast network can definitely

make a difference.

2.0.3.4. Source 4: The Hindu Survey of Indian Agriculture 2007, Annual Survey on Agriculture by

the Newspaper Hindu.

Summary: Survey has several articles on current state of agriculture. But the articles, ‘ Profound changes

in Retail area’ and ‘ Birth of a third green revolution’ establish connect with the challenges of the

approaching Retail boom.

‘ Profound changes in Retail area’ highlight the challenges arising out of fragmented landholding, limited

credit flows and uncertain market conditions. It says that retailers will have to move towards ‘Quality

based pricing’. Also, development of food retail will inevitably result in establishment of backward

linkages with agriculture and food processing. According to the author it may be unreasonable to expect

food retail to address all the entrenched problems of Indian Agriculture and produce marketing thus

Government and PSB’s need to play a crucial role. Following factors will arise as major concerns:

Storage, temperature control, inventory management and transportation. It highlights on factor as a major

driver of growth of food retail, “Food accounts for about 50% of a family’s monthly budget (about 42%

in urban and 54% in rural), food and grocery business is unlikely to face any recession any time.”

‘ Birth of a third green revolution’ discusses new marketing channels like direct buying from farmers.

Currently corporates are making a beeline to the farmer’s doorstep for buying their produce. According t

several experts corporate farming, could be the answer to the present agricultural crisis the country is

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 12/33

11

presently facing where companies buy the produce on contract basis from farmers, guarantying to pay the

prevailing market prices. Cooperative movement must support the retail boom.

2.0.3.5. Rural Finance for Small farmers -An integrated approach by Hans Dellien and Elizabeth

Lynch. (Source: ‘The Indian Banker’ magazine)

Seventy-five percent of the world’s 1.2 billion1 poor people live in rural areas. There is lacking access to

institutional sources of finance, most rural poor and low-income households. Microfinance providers can

fill an important financing gap by expanding operations into rural areas.

The paper provides an introduction to the key elements of success in the expansion of micro-lending to

rural areas.

The first section identifies the common risks in agricultural production that may impact clients’

repayment capacity.

The next section outlines the steps an institution must take to expand responsively and sustainably into

rural markets. The steps include determining optimal branch locations, understanding the new clientele

and how men and women’s economic activities in these markets differ, designing responsive financial

products, identifying ideal loan officers, and finally employing a rigorous lending methodology suited to

rural households and market dynamics.

The last section summarizes what an institution must commit to in order to ensure successful rural

expansion.

As per the article Microfinance providers targeting small farmers face a variety of challenges, such as

understanding the cash flows of rural households and the business cycles of small farms, and estimating

the repayment capacity of small farmers (who in many cases lack proper records).

The article defines clearly the risks involved in farming which need to be taken care of. These are:-

• Climate risks – Fluctuations in climate and levels of rainfall

• Productions risks

• Price and market risk due to excess supply and other factors

The article suggests that to expand into rural markets, financial institutions need to be reducing high

operational costs and deploy a comprehensive and integrated strategy which includes design of effective

risk assessment.

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 13/33

12

2.0.4. Conclusion

Following articles establish that there is a big retail boom approaching in India and there are many

challenges that need to be addressed. To address these challenges capital is major need and thus

agricultural credit is very crucial to support Indian Farmers.

2.0.5 Directions for Future Research

1. Can retail companies go beyond convention to support Indian farmers?

2. Is their a possibility of forming models which involve famers, retail companies and government as

well?

3. Are their any existing cases where a retail company has provided credit to support farming activities?

4. How models like ITC e-choupal can be created for the benefit of Agriculture industry?

To understand following issues I seek guidance from Mr. Sudhake Atre, Mr. Jayarman from NABARD

and Pantaloon Retail India Limited

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 14/33

13

3.0 Finalization of Hypothesis & Crystallization of Research Problem

3.0.1 Hypothesis

Fact 1: Indian Retailing Industry will grow at 28% in next 5 years and it will be of a size Rs. 2366 billion

(Source: CRISIL Research Retailing Annual Review).

Fact 2: If we look at Indian retail sector, food and grocery form 67% in the Indian Retail sector and 17%

in the organized retail sector. (Source: CRISIL Research Retailing Annual Review).

Fact 3: But every year an estimated 30% of fresh produce is wasted due to unavailability of post-harvest

facilities, while 10% of grains is said to be lost on farms. (Source: Article-“Profound change in Retail

Area” The Hindu Survey of Agriculture 2007).

Fact 4: Green Revolution has forced several farmers into deep debts. Also the increase in application of

chemical fertilizers in turn led to increase in the debts and with the soil reaching saturation, the yields

became poor with a result the poor farmer found himself entangled in debts unable to repay. (Source:

Article-“Reducing Input Costs” The Hindu Survey of Agriculture 2007).

Fact 5: The second report indicates that though credit to the agricultural sector has grown in the last three

years, the number of farmers who availed of credit has declined. There is also evidence that the small and

marginal farmers have not had access to credit, and that lending by cooperative societies has decreased.

(Source: Article-“Two Problems of Poverty” on NREGS 2007 report in newspaper MINT)

Considering all the facts, the hypothesis here is that to tap the approaching Retail Boom in India,

Indian retail industry needs to enter into collaboration with Agriculture Industry which has lack of

credit availability. Thus Agricultural credit is a crucial driver for future of Agriculture and Retail

Industry.

3.0.2 Crystallization of the problem

Indian government is not paying attention: Share of Agricultural sector to the GDP of the nation hasdeclined and that of services sector has increased to 55% in 2006-07.The food retailers constitute 1/3 rd of

the total retailers. The proliferation of the unorganized retail units is due to low entry and exit barriers,

low capital and overheads requirements and it is easy a relatively self employment option (Thus credit

availability for a scale required to match the needs of big Retailers can be observed here). Unlike in

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 15/33

14

other Asian countries, the organized retail sector in India forms only 2% of the total trade but it is

growing at 24-25% so again the credit requirement is indispensable.

Moreover, small (22 million) and marginal farmers (71 million) account for 81 per cent of the farmers of

the farm holdings in the country but they operate respectively.

Absence of models where Retail companies made credit available to the farmers: Opening of the Retail

sector to FDI in India has given a further boost to its retail sector thus turning the country into a giant

retail market. Some studies indicate that organised retail brings in more efficiency through greater

investments in infrastructure, cold chains, packaging and transport which reduces the wastage and lowers

the transaction cost but this is helpful for farmers who have the capability to produce and capital if scale

up in production is required. Small producers and those with lack of credit are likely to loose in view of

the small volumes produced by them in widely dispersed locations and their low bargaining power.

Innovative Models like ITC e-chaupal are not reproduced: There is dismal need of innovative models

like ITC e-chaupal which revolutionise the industry fast and thus benefit optimally from the Retail Boom

leading to far reaching economic gains which don’t fade away when the Retail boom transcend from peak

to the Decline stage.

(Source: The Hindu Survey of Agriculture 2007).

4.0 PLAN OF RESEARCH

The research includes both secondary and primary data collection through several resources. Primary

research includes field visits, intercepts with farmers and experts in the area

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 16/33

15

5.0 PRESENTATION OF DATA AND DATA ANALYSIS

5.0.1. Hypothesis

To tap the approaching Retail Boom in India, Indian retail industry needs to enter into

collaboration with Agriculture Industry which has lack of credit availability. Thus Agricultural

credit is a crucial driver for future of Agriculture and Retail Industry.

5.0.2 Data required on the basis of identified problems

1. Indian government is not paying attention

2. Absence of models where Retail companies made credit available to the farmers

3. Innovative Models like ITC e-chaupal are not reproduced

In the purview of hypothesis defined above and problems identified above following data isrequired:

1. Budget data which gives information about the government policies and initiatives

for agricultural sector.

2. Information from reports on research already done in this area.

3. Existing initiatives big and small by other banks and financial institutions.

4. Primary research and data related to topic.

5.0.3. Budget 2008: Agriculture loan waiver

With the full effects of the economic reforms of the 1990s working through the system, the

Indian economy has moved to a higher growth path and one of the facts that establishes it is that

agricultural credit poised to reach Rs. 2,40,000 crores by March, 2008 among others like 11.4

crore children covered under Mid Day Meal Scheme which is the largest school lunch

programme in the world, under National Rural Health Mission 8,756 primary health centres have

been made 24x7 and 1,82,000 girls enrolled in residential schools under Kasturba Gandhi Balika

Vidyalaya Scheme.

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 17/33

16

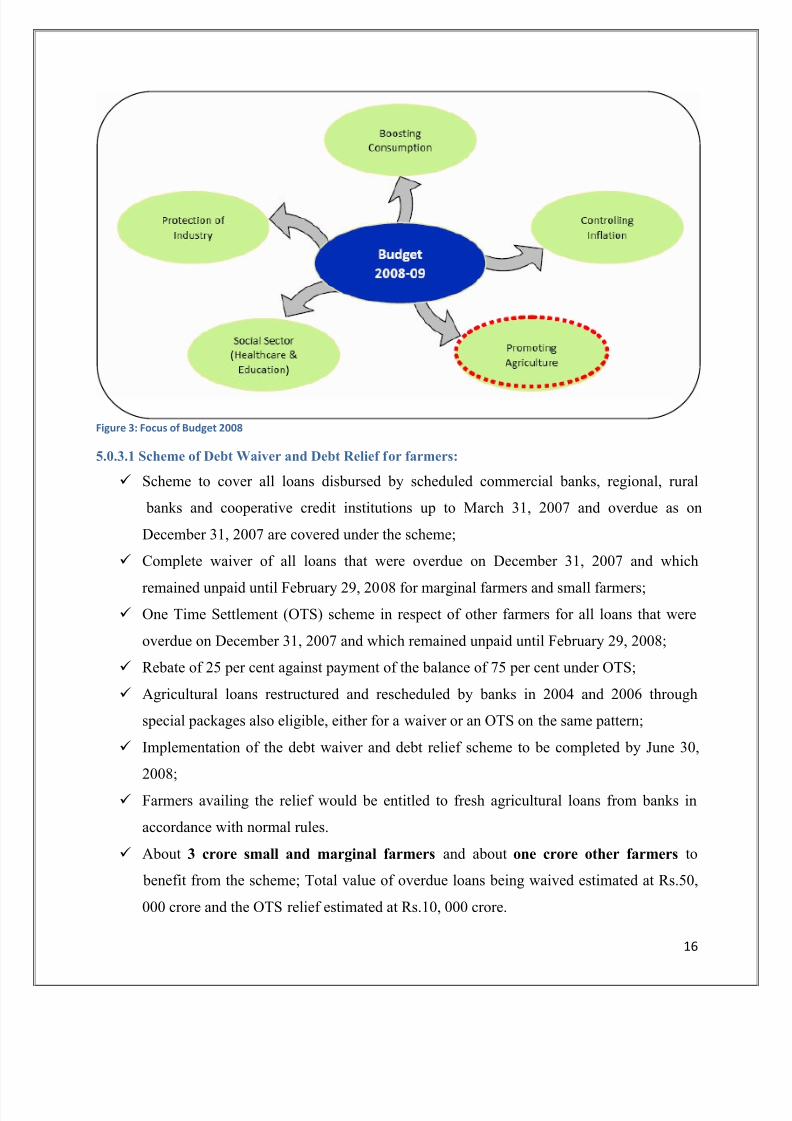

Figure 3: Focus of Budget 2008

5.0.3.1 Scheme of Debt Waiver and Debt Relief for farmers:

Scheme to cover all loans disbursed by scheduled commercial banks, regional, rural

banks and cooperative credit institutions up to March 31, 2007 and overdue as on

December 31, 2007 are covered under the scheme;

Complete waiver of all loans that were overdue on December 31, 2007 and which

remained unpaid until February 29, 2008 for marginal farmers and small farmers;

One Time Settlement (OTS) scheme in respect of other farmers for all loans that were

overdue on December 31, 2007 and which remained unpaid until February 29, 2008;

Rebate of 25 per cent against payment of the balance of 75 per cent under OTS;

Agricultural loans restructured and rescheduled by banks in 2004 and 2006 through

special packages also eligible, either for a waiver or an OTS on the same pattern;

Implementation of the debt waiver and debt relief scheme to be completed by June 30,

2008;

Farmers availing the relief would be entitled to fresh agricultural loans from banks in

accordance with normal rules.

About 3 crore small and marginal farmers and about one crore other farmers to

benefit from the scheme; Total value of overdue loans being waived estimated at Rs.50,

000 crore and the OTS relief estimated at Rs.10, 000 crore.

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 18/33

Focus on agriculture is in or

this, agriculture growth must

To support this following initiati

1) Launch of schemes under

a) Rs 250bn Rashtriya Kri

b) Rs 49bn National Food

2) Agricultural credit growth se

trillion.

5.0.4 Economic Survey 2006

The rate of growth of food grains

lower than annual rate of growth

grains was estimated at 217.3 mil

Compared to the target set for 2006

There has been a considerable dec

irrigated for the major crops.

er to propel India to a new growth orbi

ncrease from an average of 2.5% to 4%.

ves have been taken:

ational Policy for Farmers in 11th Plan

hi Vikas Yojana

Security Mission

t to exceed target for 2007‐08. For 2008‐09, ta

2007

production, however, decelerated to 1.2 per cent

f population, averaging 1.9 per cent. The overall

lion tonnes in 2006-07, an increase of 4.2 per c

-07, it was; however, lower by 2.7 million tonnes (1

line in the rate of growth of area, production, pro

17

of +10%; for

rget set at Rs 2.8

during 1990-2007,

roduction of food

ent over 2005-06.

.2 per cent).

ductivity and area

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 19/33

18

Figure 4: Rate of growth of area, production, yield and area under irrigation for major crops

Figure 5: Actual production relative to targets (per cent)

The above given chart of actual relation relative to targets shows that for the last year we have not been

able to achieve 100%. Thus if there is boom in demand we need to take preventive steps from now

onwards to cope up with that.

-

+

-

+

-

+

-

+

+ -

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 20/33

19

Figure 6: Trend growth rate in area, input use, credit and capital stock in agriculture during 1980-81 to 2003-04 (per

cent/year)

The “Farm Credit Package” announced in June 2004 stipulated, among other things, doubling the flow of

institutional credit for agriculture in the ensuing three years. The credit flow to the farm sector got

doubled during two years as against the stipulated time period of three years. The details regarding the

progress of agency-wise credit flow to agriculture and allied sectors is given in the table below. This

signals that credit availability is probably not less and there are unidentified factors that may be a reason

for bad performance in agricultural sector.

Figure 7: Institutional credit flow to agriculture sector (Rs. crore)

5.0.4.1 Agricultural Insurance

Climatic variability caused by erratic rainfall pattern, and increases in the severity of droughts floods and

cyclones and rising temperatures, have been the causes of uncertainty and risk resulting in huge losses in

agricultural production and the livestock population in India. The National Agricultural Insurance Scheme

(NAIS) for crops has been implemented from Rabi 1999-2000 seasons with the objective of providing

insurance coverage in the event of failure of any of the notified crops as a result of natural calamities,

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 21/33

20

pests and diseases. The scheme is available to all the farmers (both loanee and non-loanee) irrespective of

their size of holding and operates on the basis of “Area Approach’” It envisages coverage of all the food

crops (cereals, millets and pulses), oilseeds and other commercial/horticultural crops in respect of which

past yield data are available for adequate number of years. At present, 10 per cent subsidy in premium is

available to small and marginal farmers, which is to be shared equally by the Centre and State

Governments. The scheme is implemented by 23 States and 2 Union Territories. Since the inception of

the scheme and until Rabi 2006-07, about 971 lakh farmers have been covered. The coverage area is 156

million ha and the sum insured is Rs. 92,618 crore. Claims to the tune of about Rs. 9,855 crore have

become payable against the premium income of about Rs. 2,943 crore benefiting nearly 270 lakh farmers.

Figure 8: Season-wise details of coverage under the scheme of NAIS

5.0.5 Initiatives by other banks and financial institutions

1. Union Bank of India: Union Green Card (Kisan Credit Card) to meet the credit needs of the

farmer for crop cultivation, investment as well as consumption needs.

2. NABARD subsidy for Kerala: Rs 5.26 crore as subsidy to Kerala under the Centre’s Capital

Investment Subsidy Scheme and another Rs. 15.24 lakh under the National Project on organic

Farming.

3. Agri zones on the lines of SEZs mooted : At the meetings of the finance ministry, chaired by the

revenue secretary, P.V. Bhide, the trade body ASSOCHAM said that the government will have to

ensure adequate investments in Agri zones apart from GST (goods and services tax) to make

agricultural growth of 4% a reality and to achieve economic growth of 11%.

4. Bank of Baroda rural initiatives:

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 22/33

21

a. 170 Gram Vikas Kendras (GVKs): for providing integrated financial and non financial

services for promotion of farm and non-farm sectors in rural areas.

b. Baroda Kisan Credit Cards: More than 6 lakh have been issued.

c. Dungarpur Project: Adopted the most backward district of Rajasthan for integrated rural

development and 100% financial inclusion.

d. Baroda Grameen Paramarsh Kendras: 21 centres for knowledge sharing, problem

solving and credit counseling for rural community have already been set up and 30 more

in pipeline.

5. NBHC contributing to agricultural supply chain efficiency: National Bulk Handling

Corporation is reaching out to more and more farmers with its value added services such as

scientific storage, commodity protection and quality certification at competitive rates. It also

assists farmers and other commodity supply chain participants in securing loans against their

produce when it is stored in NBHC or Non - NBHC warehouses. They are constantly moving

towards synergetic formation of “Commodity Ecosystem”.

6. Agri insurance’s Success Story: Agricultural Insurance Co. of India Ltd. has taken over the

implementation of National Agricultural Insurance Scheme (NAIS) which until 2003 was

implemented by General Insurance Corporation of India. Some of the new project launched so far

are:

i. Rainfall Insurance

ii. Rabi weather Insurance for Field Crops

iii. Bio-fuel Tree / plant Insurance

iv. Potato Crop Insurance

v. Weather based crop insurance scheme (WBCIS)

7. E-choupal – at a glance: Commencement of Initiative: 2000

i. States Covered : 9

ii. Villages Covered : 38, 500

iii. E-choupal installations: 6500

iv. Empowered Farmers: 3.5 million

8. Corporate groups running the food retail sector : West Bengal’s finance minister, Asim

Dasgupta, presented the state’s budget for the next year a few days ago. A surprise packet was the

allocation of a sum of Rs 100 crore, to be supplemented with by an additional Rs 300 crore from

the market, to partially fund the operations of a new corporation that will enter the food retail

industry. This corporation will procure farm produce directly from farmers and sell them through

retail outlets throughout the state. (Source: The Times of India, Mumbai, 26 March’08)

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 23/33

22

5.0.6 Data from Primary research

The need of primary research is to find out how the system works in reality and what are the challenges

faced by people who are consistently efficient working of this system of credit and resource distribution.

Also, to hear directly from the stakeholders associated with the system gives a correct and clear insight

into the functioning of system and helps identifying the grey areas.

5.0.6.1 Field Visit: Raigad District (Maharashtra State) / Service area: Alibagh

Inputs from the conversation with:

Mr. Uday Newalkar, Lead District Manager, Bank of India

Mr. Lakshman Jundhane, Field Officer, Bank of India

Mr. Anand Kashid, AGM, NABARD

Though the district has not witnessed something as hard hitting like farmer’s suicide but it had its

own share of calamities which are more natural like flooding due to excess rainfall.

Bank of India provides credit counseling to farmers but still incidences of excessive production of

single crop happened and for that we need to delve into the understanding of a farmer psyche to

understand why even after having burnt their fingers the act is repeated by them.

A developmental program of creating a SEZ by government is seen as a by threat local farmers

which will also reduce the cultivable land in that area.

Primary Agriculture Society (PAC) is very active organization working closely with farmers. If these societies become completely non political in their working can work as one most effective

centre for credit distribution among other important tasks for farmers.

Banks don’t give farmers loan for personal consumption though the agricultural loan provided

has a 10% extra amount provided for the same. This is one of the reasons why agricultural loans

are diverted to use for other purposes.

There seems to be a vicious cycle that exists which completes one circle every 5-6 years with a

mishap.

Apart from financial and environmental factors there are lots of psychological, social factors thataffect farmers.

5.0.6.2 Response from farmers through NABARD office

Infrastructure supporting agricultural storage is missing and loan against the stored products are

not yet widely available.

Marketing of agricultural produce is not effective and is almost non-existent in case of farmers.

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 24/33

23

Insurance products are still available which will be a beginning of a process of risk bearing.

Trader’s intervention should be controlled to help farmers get proper returns or their produce.

All the farmers indicated that the excess rainfall in Kharif season, non availability of assured

irrigation in the entire district for summer season, polluted rivers, effects of polluting industries,

the conversation of large productive land into Khar land in coastal area, lack of mechanisation

and low use of inputs etc. are some of the constraints in increasing the productivity.

5.0.6.3 Information from a retail company

Due to confidentiality reasons the name of the company cannot be disclosed. My questions to the

company were mainly around following three questions:-

What are the challenges they face in sourcing produce directly from farmers?

Are their any agricultural ties ups or collaborations they have formed to support their food

business?

What does the company think about credit-availability linkage to agricultural sector?

Following is the excerpt of answers received from them:-

Company prefers to keep an aggregator as a mediator while sourcing from farmers. This is a

similar practice they use across organisation for this segment.

Company is not at all willing to open many interfaces while dealing with farmers as it reduces the

operational efficiency of the organisation.

Inclusive business approach is what the company practices and not an extreme altruistic or an

exploitative approach.

Being a retailer they look primarily towards improving the front end efficiencies and conveying

the consumers’ feedback (Consuming Community) to the producer (Growing community) which

will help the producer in a better way about improving his style of producing.

Agricultural extension is what they are looking at but it is not a priority.

5.0.6.4 Intercepts with farmers around Pune

Intercepts held were with the cooperation of a vendor for the food division of a Retail giant. This retailer

sources agricultural produce using four different models for fresh food and vegetables:-

SIS – Shop in shop

License market /range, margin, quality/prices/Back end &front end

Consolidator

License/Consolidator – price/range/quality etc. from Market / PRIL

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 25/33

24

Direct Procurement

License – own back end front end by PRIL

Institutional Tie up

Back end and front end by other institutions and SIS by company

This vendor (let’s call him Big V) supplies organic vegetables to the retail company under SIS model

where he can himself sell the vegetables at the food counter. Big V not only himself grows these exotic

vegetables but helps other farmers as well to grow these vegetables. He has a network of more than 70

farmers who produce exotic vegetables to supply him and sell independently in the market. The way this

farmer has created business model around agriculture is presented in the case study attached.

Following are the excerpts from Insight Dialogues with few farmers:-

6.0.4.1. Mr. Tushar Ranjanikar

From his experience he brought to notice lot of important points. Firstly he said even though there is

inflation but over the years the volume is growing and price is declining. Though money circulation has

become smooth because of presence of big retailers but due to absence of fixed policies there is still an

uncertainty for payments of produce. There are companies which inform a day before about order

cancellation which should not be there in agricultural produce which takes months to grow and are highly

perishable.

Secondly, the thinking of CEO is not percolating down which they get to hear from media. Their

experience with the operational staff is not good. They feel the operational staff doesn’t deal properly as

things work on personal level and the lack of understanding in these the staff about agriculture leads to

conflicts. The Purchase managers acts pricey and works on their own conditions. The farmer said, “I am

an engineer, an educated and well informed farmer about my area than anyone else but the treatment I

receive makes me say: “maoM huM tao ek sabjaI vaalaa hI ” (After all I am a vegetable vendor to them). He believes

that corporate bureaucracy is on peak. He referred as third class bureaucrats to employees who were

unsuccessful businessmen or unsuccessful employees somewhere else and now employed by these

companies.

Company managers are omitting older/experienced people as vendors who have say in the working of

managers by the virtue of their experience.

Experience of farmers with MNC’s had been good whenever they were involved in exports but it is not

the same with Indian companies as they have no clarity in their work style.

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 26/33

25

Thirdly, there is Absence of meetings between the farmers marketing representatives like Big V and VM

(Visual merchandising) staff of the company so they can understand how to present and preserve these

vegetables and how to educate the consumer.

Fourthly, there is absence of feedback to the farmers about sales of their produce and true sales figure of

the produce. If this practice is inculcated will be very beneficial both for the farmers and retailers as the

feedback will help farmers know where they are wrong and thus consumers will receive an improved

quality.

Finally, Indian companies need to develop Indian practices which are suitable for local needs and avoid

foreign practices should be implemented here which are in a different direction to an Indian mindset. E.g.

He gave an example where one of the managers rejected his lot of medium sized capsicums which are

preferred by Indian middle class families as compared to big sized capsicums which are suggested under

foreign practices and preferred by hotels in India and not common public.

Amongst other suggestion the farmer suggested that the companies need to study the local mandi (local

market) style of working as the companies need a very strong grower base is required. He said we need a

platform a like stock exchange where they can ask for what they deserve for their produce which is like a

mandi. “Both the company and farmers need to come together and collaborate as their relationship needs

to be like a happy marriage”, says Ranjanikar.

6.0.4.2. Balu Bajirao Waghdhare

This farmer used to grow potato, onion etc. and family was in great problems because these vegetables

never fetch good and most importantly constant prices from market. “Local PSU Bank treats them like

stray dogs”- farmer says furiously.

Around a year ago he contacted Big V and started growing exotic vegetables. Now, he supplies to Big V

as well as other local vendors and restaurants.

6.0.4.3 Gyaneshwar Bodke

Gyaneshwar was into traditional farming of rice, wheat with the whole family but still the produce

couldn’t fetch enough money for the whole family to survive. He tried getting a poultry loan in 1993

which was under processing till 1995 when the Bank which is a PSU realized that they don’t give loan for

poultry, says the famer sarcastically.

His family quit the farming and started a job until he met Rashmi Abroal and started growing carnation

after doing a short term course at HTC (Horticulture Training Institute), Talegaon in year 2000. Same

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 27/33

26

year he a group named “Anubhav” with 17 farmers which constitutes 105 farmers now and started

growing exotic vegetables as well.

The group got a finance of Rs 7.5 crore from CANARA Bank which the group successfully repaid to the

Bank. The group received a National award under NABARD’s Farmer Club program at the National

award function from Finance Minister Dr. P. Chidambaram in Feb’08.

Gyaneshwar himself has become a consultant of exotic vegetables and floriculture and provides

consultancy across Maharashtra.

Farmer says, “We realized that marketing is very important now days but we can do one thing either to

produce or to market. So they need to partner with someone who can look after the marketing.”

5.0.7 Directions for further research

Suggestions from Mr. Jayaraman, GM, NABARD

Considering the wide scope of research he suggested that focus should be initially kept on develop a

generic business model for forming collaboration between retail companies and the farmers after

assessing the needs of both the stakeholders. So I will be assessing the following:-

How such collaboration operates?

What are the different conditions required for their proper operation?

Which are the different sources of credits for the farmers?

How can the famers operating an environment categorized to address their needs?

Can a mechanism be developed to tap their experience?

5.0.8 Interpretation

Debt waiver to farmers will increase cash flow for rural sector which can negative

as well as it will encourage the benefitted farmers to repeat the act and non-defaulters to

commit a default. There are several more initiatives which can be found in the national economic survey which

suggests that there is no dearth of initiatives from the government. So, now the more challenging

task is to found out the reasons that are still hindering with the growth of this sector because still

production is going down, farmers are committing suicide and still 25-40% of agricultural

produce goes waste every year.

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 28/33

27

Apart from above mentioned initiatives there are several initiatives taken by several institutions

and individuals for the benefit of people employed in agricultural sector. But the need of time is

to form an integrated approach that can implemented pan India and thus can catalyse the process

of holistic economic development.

The key insight here is that one of the major entity in a business model for this collaboration is an

Aggregator who should ideally reduces the operational work for both the producer and the

retailer. At the same time it reduces risk for the retailer which they want to minimize in this low

margin industry.

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 29/33

28

6.0 CONCLUSION & CONCEPT CREATION

6.0.1 Kisantrepreneur: Beginning of a collaboration

On the basis of research done so far with support of reading based secondary research and primary

research done there are few attributes that appear to be a must for a “KISAN” (farmer). These can be

described as a full form of word KISAN - K nowledge, Interest, and Skill set for Agriculture and

Nature.

But today when there is so much competition a farmer should have risk taking capabilities to succeed and

market its produce. Farmer of today also needs to be an entrepreneur.

It is practically impossible for a retail company to deal with million of famers. So they need not only a

KISAN or an Entrepreneur but a Kisantrepreneur (KISAN-trepreneur) who has Knowledge, Interest and

Skill set for Agriculture and Nature along with the risk taking capability to be a business man, one who

can deal and negotiate with retail companies and also be an aggregator for small famers. This person

needs to have a knack of marketing, ability to deal patiently with farmers. If he knows farming and

practices it, will be a bonus for the retailers.

The skill set is clearly defined for a Kisantrepreneur below:-

Figure 9: Skill set of a Kisantrepreneur

Knowledge

•Trends in Agriculture &farming

•Basics of Agriculture

•Availibility of Differentreources like education,credit and channels of sale.

Interest•Nature

•Agriculture

•Business

Skill Set

• Trustworthy

• Believes in Integrity

• Patience to deal with farmers

• Farming skills are bonus

• Open to feedback and adaptable

• Risk Taking

• Negotiation skills

• Marketing skills

• Creative

For Retailer

For the farmers

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 30/33

29

6.0.2 Three C’s Approach: A step towards agriculture sector

Retail companies need to be receptive to this sector if they want to tap on this retail boom. During

research few factors came to critical to their relationship with this sector. 3 C’s of a retail framework for

agricultural sector:-

1. Communication: They need to be interactively involved with the famers by identifying people who

can lend them knowledge which can be used for the better functioning of food segment in their

companies. The company should regularly send people who are in leadership positions to interact with

these people and her them personally as well as communicate their vision to them.

2. Clarity in Policy in framework : Many farmers have experienced immense clarity in dealing with

MNC’s but there is cultural practices conflict. Others have experience that there are no rules to deal with

the farmers regarding contracts or payment issues. This needs to be transparent and clearly defined.

3. Conjoint Relationship: The companies need to work with them like a partner. SIS (Shop in Shop)

model by future group is an appreciated concept by farmers but needs more involvement of the company

staff. Companies can use the experience of farmers to train their staff which the farmers are ready to

provide. The process should involve some incentive both for farmers as well as the staff. It has been

observed that the food division doesn’t perform well if the staff is not aware and educated about the

products sold.

6.0.3 Rural Credit: A multidimensional Entity

Credit availability is very crucial to the development of this sector. In data collection section there is a

mention about the fiscal credit availability in sector for farmers but still there is disconnect which is the

distribution of fiscal credit. In interviews with farmers it has come across that PSU banks don’t deal

properly with the farmers. A farmer is not ready to take loan at the cost of self esteem which is depicted

by a statement from one of them, “vaao tao eosao pOsaa doto hOM jaOsao ku<ao kao raoTI …”.

Moreover, the with research it comes across that Credit has a multidimensional meaning for the

agricultural sector. The important factor here is that the amount of the credit can be micro or macro, the

source can be different but it should be available as per the requirement and the need. It doesn’t need to

high or less, micro or macro, cash or seed, it should be Necessary Finance.

Credit for this sector needs to qualify by 5 C’s which are:-

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 31/33

Figure 4: Dimensions of Agricultural Cr

1. Capital Credit: This refers to f

banks and other Institutions like

Institutions).

2. Cognitive Credit: This refers to

farming. The farmer can repay it b

knowledge.

3. Creation or Capability credit:

Most of the farmers said since they

are ready to repay this by allowing

4. Credit of Convenience: This r

away and let them burn in the v

producing traditional crops as wel

utilization of the opportunity.

Conv

Confidence

dit

scal credit availability by several channels like pu

PACs (Primary Agricultural Society) and MFI

the knowledge lending to farmers about trends an

y giving consultancy to other famers thus creating

One of the most important aspects now for this s

can concentrate on production they want a partner i

he marketing person giving a commission or share i

fers to providing opportunities to the farmers and

cious circle of poverty. Many farmers that I int

l as new exotic crops. The repay in this case b

Credit forAgricultural

Sector

Capital

Cognitive

Creation/

Capabilitynience

30

lic banks, private

s (Micro Finance

d best practices in

a chain transfer of

ctor is marketing.

n marketing. They

n sales.

not keeping them

erviewed are now

farmer is proper

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 32/33

5. Credit of Confidence: This is t

in their activities. Even though they

food we get to eat which is produce

6.0.4 Three-pronged approa

There are 3 main areas that appeare

Distribution, Integration and Educa

1. Distribution of resources:

ensures proper distribution

training to deal with farmer

the banks.

2. Integration of existing int

institutions, credit institutio

farmers around the periphe

interface that provides info3. Education and awareness:

be counselors who should v

7.0 Limitations of the st

1) The views expressed are mine

2) The research is done over a 3 m

3) The primary research is done in

might not be able to applicable

4) The scope of microfinance i

Considering the shorter durati

Retail Companies and Agricult

Distribution

e most important credit. Every farmer needs our a

don’t get it they have been lending it to us in the fo

d by them.

ch for Government

d very crucial for extending government support, vi

ion.

A proper framework of distribution of credit is requ

of highly available credit. Banks should have a com

s as it comes out as one of the main reasons for the

rfaces and channels: There are many Agriculture

ns, and Agri-insurance companies etc. which work i

y of cities not aware of them. So they should be int

mation about all aspects involved in modern agriculFarmers are ignorant of so many channels of suppo

isit rural areas and educate people about these chan

dy

nd thus readers may agree or disagree with the cont

onth period and thus has lot of scope for further res

few areas located within Maharashtra so the outpu

to whole Maharashtra.

stitutions and reasons for farmer suicide has n

n of project the scope is narrowed down to busin

ral sector.

Integration Educ

31

d systems support

rm of every bite of

-à-vis

ired which

ulsory behavioral

not approaching

ducational

n isolation. Even

grated into an

tural practices.rt. There should

els.

nt.

arch.

of concepts given

ot been explored.

ss perspective for

tion

8/7/2019 Collaborative models for Retail Industry and Agriculture: A research on means of mutual benefit for both sectors1

http://slidepdf.com/reader/full/collaborative-models-for-retail-industry-and-agriculture-a-research-on-means 33/33

8.0 Bibliography

1. RBI website: www.rbi.org.in

2. CRISIL website

3. The Hindu survey of Indian Agriculture

4. AT Kearney

5. www.livemint.com

6. www.swwb.org//RuralFinance / The Indian Banker

7. National Budget 2008 (http://indiabudget.nic.in)

8. 2008 Budget Simplified: A report by Religare research

9. Economic survey 2006-07 (www.finmin.nic.in)

10. Times of India

11. Magazines:a. CAB Calling

b. Agriculture Today

c. Financing agriculture