Embed Size (px)

Citation preview

COGNIZANT4TH QUARTER 2017

CHARGING TOWARDS AN ELECTRIFIED FUTURE | CONTINENTAL — BOARD THE POWERTRAIN INTO THE FUTURE GLENCORE — BETTING ON A SUSTAINABLE FUTURE | FIDUCIARY LESSONS TO BE LEARNED FROM THE PASSING OF HUGH HEFNER

SELLING THE DREAM — HOW CAR ADVERTISING HAS EVOLVED

2

TABLEOF

CONTENTS

INTRODUCTION 3

CHARGING TOWARDS AN ELECTRIFIED FUTURE 5

CONTINENTAL – BOARD THE POWERTRAIN INTO THE FUTURE 12

GLENCORE – BETTING ON A SUSTAINABLE FUTURE 17

FIDUCIARY LESSONS TO BE LEARNED FROM THE PASSING OF HUGH HEFNER 23

SELLING THE DREAM – HOW CAR ADVERTISING HAS EVOLVED 24

COVER IMAGE – THE WORLD'S FIRST ELECTRIC CARDecreasing our dependence on fossil fuel has become a priority in recent years, and as a result electric cars are becoming far more mainstream than ever before. But electric cars aren’t exactly a new idea – the one on the cover dates back to 1881. This odd-looking vehicle was the world’s very first electric car. It was built from a modified Starley tricycle by English scientists William Ayrton and John Perry as a sort of rolling billboard that would advertise the duo’s electric inventions. It had a top speed of nearly 15 km/h and a range of around 40 km.

3

INTRODUCTION CHRIS POTGIETER – HEAD OF PRIVATE CLIENT SECURITIES

As 2017 draws to an end, it’s important to

pause and reflect. This past year has been

a tumultuous one for investors as global and

local markets were significantly influenced

by various economic and political shocks.

During such uncertain times, investors can

easily lose perspective on the importance

of maintaining a long-term outlook; and

we all know the damage a hasty response

can wreak on a well-crafted investment

plan. Yet, it is also important to remember

that challenging times can present unique

opportunities. At PCS, we remain focused

on exploiting such opportunities for your

long-term benefit.

Since the inception of the first automobile

in the 1890s - initially termed the horseless

carriage - the automotive industry has seen

constant change. Many of the standard

features we enjoy in modern day vehicles

such as windshields, hydraulic braking

systems and seatbelts were introduced

decades after automobiles were in use and

at the time were regarded as significant

innovations. Despite the rapid changes

we have seen in the auto industry over

the last century, it’s fair to say that we are

currently at the cusp of some fascinating,

wide-ranging and transformative changes

to the motor vehicle. Innovations such

as alternative fuels, electric, driverless,

and connected vehicles are some of the

changes we are seeing.

In this edition of Cognizant, we take a

closer look at electric vehicles and the

investment opportunities they present. In

our feature article, our Chief Investment

Officer, Andrew Dittberner, writes about

the evolution of the market and explores

some of the tail and headwinds that electric

vehicles face.

Our global stock piece outlines our long-

term investment case for Continental and

Victor Mupunga outlines why we believe

that this company stands to benefit from the

changes within the auto industry. On the

local front, we recently added Glencore

to our Core Equity Model Portfolio and

Sameer Singh provides a synopsis of the

company and explores the company’s

substantial competitive advantage over

its peers. We then end off this edition of

Cognizant with a look at the evolution of

car advertisements.

On the business front, I’m pleased to report

that PCS has enjoyed another successful

year of growth. When we started PCS four

years ago, we envisaged a business where

clients would find a world-class tailored

investment capability predicated on global

reach, investment prowess and excellent

service. Since the appointment of our first

portfolio managers four years ago, we

have grown our footprint nationally to 23

portfolio managers and currently manage

over R10 billion in equities and R10 billion

in cash and structured investments on

behalf of our clients. None of this would

have been possible without having the

right people within our business and a

strong network of supporters.

On that note, I would like to sincerely

thank you for your support of our business.

I wish you and your loved ones a relaxed,

happy and safe festive season and trust

that the year ahead will be a prosperous

one for us all.

All the best,

Chris

4

5

CHARGING TOWARDS AN ELECTRIFIED FUTURE

ANDREW DITTBERNER – CHIEF INVESTMENT OFFICER

The automotive industry is in the midst of a major transition. Due to a fundamental shift in the way vehicle ownership is viewed, coupled with disruptive technology and the desire to clean up our act in order to clean up the environment, vehicle manufacturers are currently facing unprecedented challenges. Globally, and particularly in South Africa, owning an expensive German-engineered, petrol-guzzling vehicle has been seen as a status symbol. However, the advent of autonomous vehicles, ride-hailing and ride-sharing has changed this image somewhat. But just as the internal combustion engine (ICE) displaced horses as the means to propel vehicles in the late 1800s, the electric engine is set to be the largest disruptor in the automotive market 120 years later.

6

The onset of electric vehicles (EVs) has not happened overnight. Although their origins can be traced back long before the ICE, it was only in the 1960s (following the need for alternative-fuelled vehicles to reduce exhaust emissions from ICEs and to reduce the dependency on imported foreign crude oil) that ICE alternatives came back into vogue. The alternative to the ICE is the EV, which includes both pure EVs that rely on battery technology only, as well as hybrids, which make use of a combination of ICE and EV powertrains.

While hybrid vehicles have quietly been making their mark since the late 1990s, little headway had been made in the mainstream market with regard to pure EVs. It took Elon Musk’s purchase of Tesla stock, and his subsequent rise to top management in 2008, to put pure EVs squarely back onto the global map. Today, the various technologies that power engines can be divided into two separate categories – the well-established powertrains that require evolution in order to remain current; and the new up and

Powertrain Technology Abbreviation Description

Evolutionary

Internal Combustion Engine ICE

ICEs are engines which are typically powered by fossil fuel based products like petrol or diesel. Given the reliance on fossil fuels and the harmful emissions, ICEs use as the predominant powertrain technology is coming under pressure from electric vehicles. The origins of the ICE can be traced back to the mid–1800s.

Plug-In Hybrid Electric Vehicle PHEV

PHEVs are hybrid electric vehicles which combine an ICE with an electric motor and a rechargeable battery. The predominant powertrain technology is electric; however, the ICE works as a back-up when the battery is depleted. The battery is recharged through plugging it into an external power source.

Full Hybrid Electric Vehicles FHEV

FHEVs are hybrid electric vehicles that have the ability to combine the electric motor and the ICE to power the vehicle. The ICE also functions as an onboard generator by applying power to the rechargeable battery. The battery can also be recharged during braking through the conversion of energy into electricity.

Revolutionary

Battery Electric Vehicle BEVBEVs are vehicles that utilise energy stored in rechargeable batteries, and only make use of electric powertrain technology. The batteries are charged by plugging the vehicle into an external power source.

Fuel Cell Electric vehicle FCEVFCEVs are vehicles that use hydrogen gas to power the electric motor, as opposed to rechargeable batteries.

TABLE 1: THE VARIOUS POWERTRAIN TECHNOLOGIES

coming powertrain technologies that can only be described as revolutionary. These are outlined in the table below.

From the table, it is clear that the term ‘Electric Vehicle’ is used very loosely to refer to any vehicle that makes use of an electric engine, in some form or another. It is estimated that only one in twenty EVs make use of pure electrification for propulsion. For the purpose of this article, pure EVs include both Battery Electric Vehicles (BEVs) and Plug-In Hybrid Electric Vehicles (PHEVs).

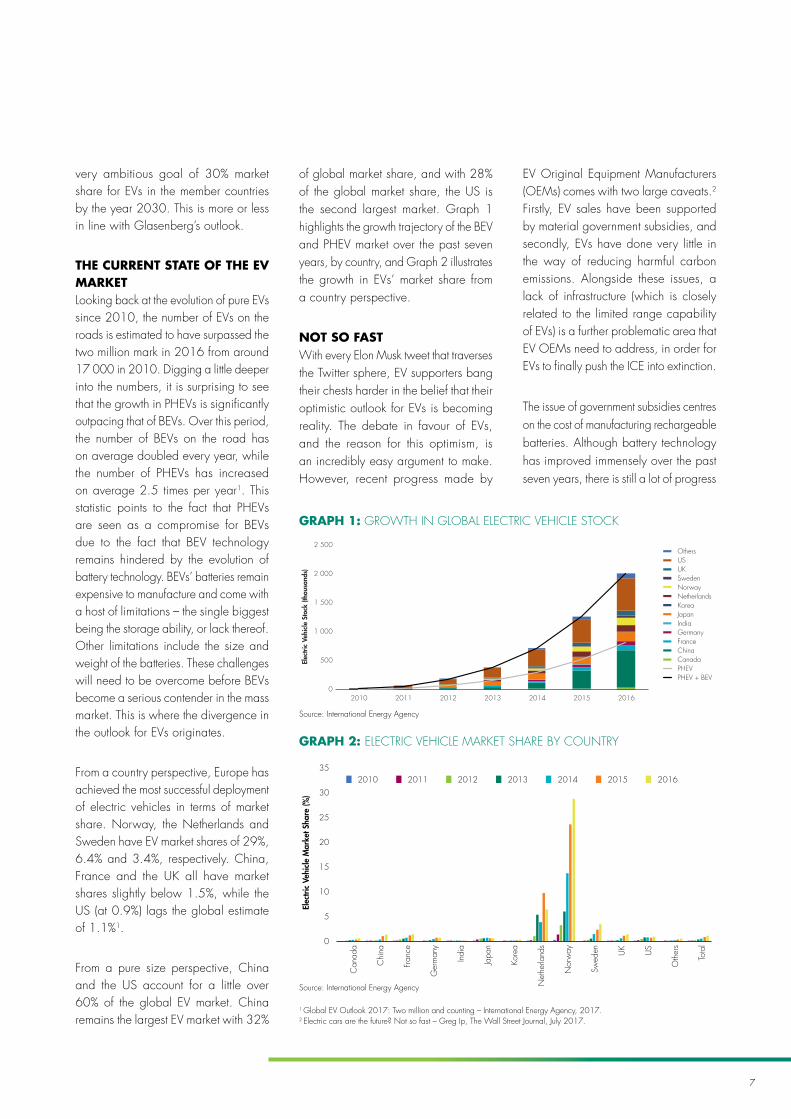

ELECTRIC CARS ARE COMING, BUT WHEN?The outlook for EVs (as with the outlook for capital markets, geopolitics and populism) is extremely uncertain. Whether it is the opinion of the public or that of the experts, the division of opinions around the evolution of EVs and the pace of their adoption is clearly evident. Glencore CEO, Ivan Glasenberg, recently announced at the company’s interim results presentation that EVs would constitute

30% of global vehicle sales by 2030. Global research firm, UBS, is slightly less optimistic and predicts that EVs will make up 14% of global vehicle sales by 2025. To put these numbers into perspective, EVs currently make up only 1.1% of global vehicle sales.

What is not uncertain, however, is that EVs are coming and ICEs’ days are numbered - it just remains a question of when. This is evidenced by the growing list of countries that have committed to go electric -only by a specified date. These dates typically range from 2040 to 2050 and the list currently includes India, France, the UK and Norway. Further to this, the Electric Vehicle Initiative was established in 2009 with the purpose of bringing together representatives from member governments and partners bi-annually to share knowledge on policies and programmes that support EV development. Ten countries are currently members of this initiative, representing the vast majority of the global EV market. This initiative recently launched the EV30@30 campaign, which set the

7

1 Global EV Outlook 2017: Two million and counting – International Energy Agency, 2017.2 Electric cars are the future? Not so fast – Greg Ip, The Wall Street Journal, July 2017.

Source: International Energy Agency

Source: International Energy Agency

0

500

1 000

1 500

2 000

2 500

2010 2011 2012 2013 2014 2015 2016

Elec

tric

Veh

icle

Sto

ck (t

hous

ands

)

OthersUSUKSwedenNorwayNetherlandsKoreaJapanIndiaGermanyFranceChinaCanadaPHEVPHEV + BEV

0

5

10

15

20

25

30

35

Can

ada

Chi

na

Fran

ce

Ger

man

y

Indi

a

Japa

n

Kore

a

Net

herla

nds

Nor

way

Swed

en UK US

Oth

ers

Tota

l

Elec

tric

Veh

icle

Mar

ket S

hare

(%)

2010 2011 2012 2013 2014 2015 2016

GRAPH 2: ELECTRIC VEHICLE MARKET SHARE BY COUNTRY

GRAPH 1: GROWTH IN GLOBAL ELECTRIC VEHICLE STOCK

very ambitious goal of 30% market share for EVs in the member countries by the year 2030. This is more or less in line with Glasenberg’s outlook.

THE CURRENT STATE OF THE EV MARKETLooking back at the evolution of pure EVs since 2010, the number of EVs on the roads is estimated to have surpassed the two million mark in 2016 from around 17 000 in 2010. Digging a little deeper into the numbers, it is surprising to see that the growth in PHEVs is significantly outpacing that of BEVs. Over this period, the number of BEVs on the road has on average doubled every year, while the number of PHEVs has increased on average 2.5 times per year1. This statistic points to the fact that PHEVs are seen as a compromise for BEVs due to the fact that BEV technology remains hindered by the evolution of battery technology. BEVs’ batteries remain expensive to manufacture and come with a host of limitations – the single biggest being the storage ability, or lack thereof. Other limitations include the size and weight of the batteries. These challenges will need to be overcome before BEVs become a serious contender in the mass market. This is where the divergence in the outlook for EVs originates.

From a country perspective, Europe has achieved the most successful deployment of electric vehicles in terms of market share. Norway, the Netherlands and Sweden have EV market shares of 29%, 6.4% and 3.4%, respectively. China, France and the UK all have market shares slightly below 1.5%, while the US (at 0.9%) lags the global estimate of 1.1%1.

From a pure size perspective, China and the US account for a little over 60% of the global EV market. China remains the largest EV market with 32%

of global market share, and with 28% of the global market share, the US is the second largest market. Graph 1 highlights the growth trajectory of the BEV and PHEV market over the past seven years, by country, and Graph 2 illustrates the growth in EVs’ market share from a country perspective.

NOT SO FASTWith every Elon Musk tweet that traverses the Twitter sphere, EV supporters bang their chests harder in the belief that their optimistic outlook for EVs is becoming reality. The debate in favour of EVs, and the reason for this optimism, is an incredibly easy argument to make. However, recent progress made by

EV Original Equipment Manufacturers (OEMs) comes with two large caveats.2 Firstly, EV sales have been supported by material government subsidies, and secondly, EVs have done very little in the way of reducing harmful carbon emissions. Alongside these issues, a lack of infrastructure (which is closely related to the limited range capability of EVs) is a further problematic area that EV OEMs need to address, in order for EVs to finally push the ICE into extinction.

The issue of government subsidies centres on the cost of manufacturing rechargeable batteries. Although battery technology has improved immensely over the past seven years, there is still a lot of progress

8

CHARGING TOWARDS AN ELECTRIFIED FUTURE

Source: Thomas Covert, Michael Greenstone and Christopher R. Knittel, The Wall Street Journal

0

100

200

300

400

500

600

700

0 50 100 150 200 250 300 350 400 450

Cost of batteries in 2020(US$ per kilowatt-hour)

Oil

pric

e in

202

0(U

S$ p

er b

arre

l)

EVs are cheaper than ICEs

ICEs are cheaper than EVs

Latest oil price & estimated cost perkilowatt-hour of a battery

GRAPH 3: OIL PRICE : COST OF BATTERIES PAYOFF

to be made. Technological advances have managed to reduce the cost per kilowatt-hour (kwh) from US$1 000 in 2010 to US$130-200 today. At the time of writing, a 75kwh battery (400 km of range) would increase the cost of the vehicle by about R170 000 – not an immaterial amount. To overcome these costs, governments incentivise potential EV buyers through a range of subsidies to EV OEMs. However, this cannot continue forever and one needs to consider what will happen when these subsidies eventually come to an end. Hong Kong and the state of Georgia provide some anecdotal evidence in this regard.

When the EV tax incentive was removed from Hong Kong in April 2017, sales of Tesla motor vehicles essentially ground to a halt. In Georgia, EV sales fell 80% in the space of a month following the removal of a tax credit. Both examples suggest that the price elasticity of EVs is very high and that battery technology needs to evolve to the point that the price point for EVs in relation to an equivalent ICE powered vehicle is more comparable.

Notwithstanding the reduction in the cost of producing a rechargeable battery, one also needs to consider the price of oil. Falling battery costs on their own will not result in EVs completely displacing the ICE. Rather, this needs to be coupled with an oil price that is significantly higher than what it is currently. In an article for the Journal of Economic Perspectives, economists Thomas Covert, Michael Greenstone and Christopher Knittel estimate that if battery costs fall to US$100 by 2020, as Elon Musk targets, then oil would have to average US$90 per barrel to make electric and petrol equally attractive2. Therefore, although the exact date of parity in terms of cost is

uncertain, the recent trend is very clear. Graph 3 shows the payoff between the oil price relative to the cost of batteries in 2020, and at which point each is more cost competitive.

The second caveat to the progress made by EV OEMs questions whether EVs actually reduce harmful carbon emissions. Research has shown that in some areas in the US, recharging an EV at night (the time when EVs are predominantly recharged) actually results in more carbon emissions than existing vehicles. This is due to the fact that night-time electricity generation is predominantly coal powered, as opposed to clean alternatives2. This may be even further exacerbated in SA, given the state of our power supply.

The other challenges regarding the adoption of EVs, namely infrastructure and the limited range of EVs, remain important considerations when trying to assess the ability of EVs to grow their global market share, as well as the timing thereof. The range of a typical BEV is between 160 and 200 kms. There are exceptions to this rule, with a number of Tesla models having a range of close to

500 kms. However, these limited ranges remain well below the ranges of their ICE counterparts and have given rise to the term ‘range anxiety’, i.e. the fear of the EV running out of power before it is able to reach a charging point. Range anxiety can only be overcome by either improved infrastructure, improved battery charge, or both.

With regard to infrastructure, Tesla is the clear leader from a pure OEM point of view. Tesla aims to double its network of Supercharger stations, which have the ability to repower a vehicle in under 30 minutes, from 5 400 at the beginning of the year to over 10 000 by year–end. Other OEMs typically partner with commercial charging firms that provide the right type of connection in order to plug the vehicle into the Supercharger stations. Recently, German premium OEMs announced that they would work together to build their own network of Supercharging stations. This is seen as a step in the direction of the Tesla model. What all OEMs have in common though is the realisation of the importance of improving the charging infrastructure, if EV adoption is to be truly advanced.

9

Improving the length of time it takes to recharge a vehicle, as well as improving the battery charge in order to extend EVs’ range, are the final obstacles that need to be overcome in order for mass adoption of the EV. Both issues need to be tackled from a battery technology point of view, which goes back to the cost of producing the battery relative to the cost of using a fossil fuel based alternative. As a result, in its current form, the pure BEV is largely seen as a second vehicle reserved for the affluent, particularly when it comes to the upper-end Tesla.

SO WHAT’S THE ALTERNATIVE? In a survey of nearly 1 000 senior executives from the world’s leading automotive companies, the setting up of a user-friendly charging infrastructure was identified as the key issue. This resulted in 62% of the executives anticipating that BEVs will fail, as hard as that is to believe. In contrast, 78% believe Fuel Cell Electric Vehicles (FCEVs) will provide the golden bullet for the issues hampering BEVs3.

FCEVs are viewed as having the ability

to solve both the recharging and the

infrastructure issues that pure EVs face

today. The refuelling process could

potentially be done as quickly as

traditional refuelling, but just at hydrogen

stations which would replace today’s

petrol stations. However, this technology

remains in its infancy and would need to

overcome a number of its own obstacles.

These include the cooling of hydrogen

and the safe storage of it in a vehicle3.

KEY MARKET PLAYERS Tesla is synonymous with the EV market

and since its vehicles are typically quite

expensive, they are seen as more of a

second vehicle option (predominantly

used on weekends) for the affluent

market. But while Tesla most definitely

has the first mover advantage (along

with a leader who has successfully

positioned the brand), there are many

EV manufacturers that despite making

headway remain overlooked.

Other OEMs that have moved into the EV market include German luxury manufacturers BMW and Mercedes-Benz, as well as Toyota, Ford, Volkswagen, Mitsubishi, Chevrolet, Fiat, Citroen and Kia. The one thing that these OEMs have in common is that they have identified the threat of the EV and can use their deep pockets, engineering experience and massive distribution networks to challenge the incumbents. One such incumbent that is yet to get a mention is the true pioneer in the EV field, the Renault-Nissan Alliance. While Tesla may hog the media limelight, the Alliance holds the prize for the largest number of EVs sold4. In the first quarter of 2017, the Renault-Nissan Alliance sold nearly 37 000 EVs, with the Nissan Leaf maintaining the top spot for the world’s best-selling EV. Over the same period, Tesla managed to sell 25 000 EVs.

Another lesser-known player in the field is Chinese company BYD. Nine years ago, in the midst of the Global Financial Crisis, Warren Buffett took a bet on

3 Global Automotive Executive Survey – KPMG, 2017.4 Who is the world’s leading EV market? It’s not Tesla – Bertel Schmitt, Forbes, May 2017.

10

CHARGING TOWARDS AN ELECTRIFIED FUTURE

3 Global Automotive Executive Survey – KPMG, 2017.4 Who is the world’s leading EV market? It’s not Tesla – Bertel Schmitt, Forbes, May 2017.

the then struggling cellphone battery maker based in Shenzhen. Today, BYD is a leading EV manufacturer in China, selling more battery-only and hybrid EVs in China than anyone else. It is interesting to note that BYD is not betting the house on the EV market. The company derives only 20% of vehicle sales from EVs, with the rest coming from traditional fuel cars. Furthermore, vehicle sales account for only 55% of BYD's revenue as 38% stems from cellphone components.

THE INVESTMENT OPPORTUNITYPhasing out petrol-guzzling vehicles in favour of EVs has definitely begun to speed up over the last few years, as evidenced by a number of OEM manufacturers committing to phase out petrol/diesel-only vehicles by a specified

date. However, investors should treat the transition as a longer-term, global megatrend, as opposed to an overnight transition. Abandoning the ICE in favour of EVs will happen, but overcoming the shortcomings may result in the EV market attaining its goal over a much longer timeframe than originally anticipated. Opinions on this timing remain divided.

Much like trying to estimate exactly when EVs will overcome their shortcomings, estimating what the global EV total will be in 20 years is an equally inexact science. But what we do know is that a number of trends (urbanisation and industrialisation in emerging economies, changing demographics and consumer preferences, disruptive technologies, etc.) point to a rapidly growing global

vehicle pool. With the current global vehicle pool sitting at a little over one billion vehicles, estimates suggest that this number could double by 2035. Given this rapid growth, from an investment perspective, companies that are geared towards the automotive industry stand a good chance of benefiting from this trend.

At PCS, we invest in a number of such companies on behalf of our clients. A few examples include Glencore, Anglo American Platinum, Alphabet (Google) and Continental. Glencore is a large producer of copper, nickel and cobalt, all of which are critical elements in the manufacturing of EVs. Anglo American Platinum is the world’s largest primary producer of platinum.

11

While there are questions around the

relevance of platinum with the onset of

EVs, the mass adoption of EVs is still

many years, if not decades, away. As

a result, platinum and its derivatives

will remain critical in reducing carbon

emissions through their use in catalytic

converters as the global vehicle pool

grows. Alphabet is investing large

amounts of capital in the autonomous

vehicle market. And while Continental

is best known as a tyre producer,

it also produces technologically enhancing

products ranging from electric mobility

and automated driving components

to vehicle infotainment systems.

It would be remiss to talk about investment

opportunities without mentioning Tesla.

Today, Tesla is the world’s fourth largest

vehicle manufacturer as measured by

market capitalisation. Yet it is incredibly

tricky to match the company’s success from

a share price perspective with that of its

underlying fundamentals. In 2016, Tesla

sold only 76 230 vehicles and given its

inconsistent history of achieving sales

targets, along with a bottom line that is

perpetually in the red, Tesla is considered

a concept stock, i.e. a stock that is

invested in based on the concept rather

than the underlying fundamentals. This

is not to say that Tesla is not a valuable

company, it most definitely is and has

the potential to become more valuable

in time. The company clearly has superb

assets in the form of its infrastructure

and proprietary intellectual property

(battery technology). However, from

an investment and a risk management

perspective, we are more circumspect

when investing in such shares.

On the domestic front, the Pietermaritzburg-based aluminium manufacturing business Hulamin, is a small cap stock that plays a critical role in the production of Tesla motor vehicles. In 2010, before the world knew who Elon Musk was, the then little-known entrepreneur was trying to source speciality vehicle components for Tesla motor vehicles. Through the search Hulamin was approached to build one such component – the battery box base plate. Despite not being a game changer at the time, Hulamin agreed to produce the component and to this day, Hulamin remains the sole supplier of the component to Tesla. The only difference is that the outlook for Tesla has changed significantly. Hulamin remains in the small cap space, and as such sits outside of our investable universe. However, it is great to know that, alongside Elon Musk, another proudly South African component goes into making Tesla possible.

12

CONTINENTAL – BOARD THE POWERTRAIN INTO THE FUTURE

VICTOR MUPUNGA – RESEARCH ANALYST

Despite the rapid changes we have seen in the automotive industry over the last century, it’s fair to say that we are currently at the cusp of some fascinating, wide-ranging and transformative changes to the motor vehicle. Innovations such as alternative fuels, electric, driverless and connected vehicles are some of the changes we are seeing. In any industry that undergoes material change, there are winners and losers and we believe that Continental stands to benefit from the changes within the automotive industry.

13

GRAPH 1: CONTINENTAL’S OPERATING SEGMENT MARGINS

-40.0%

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Chassis & Safety Powertrain Interior ContiTech Tyres

Source: Company reports

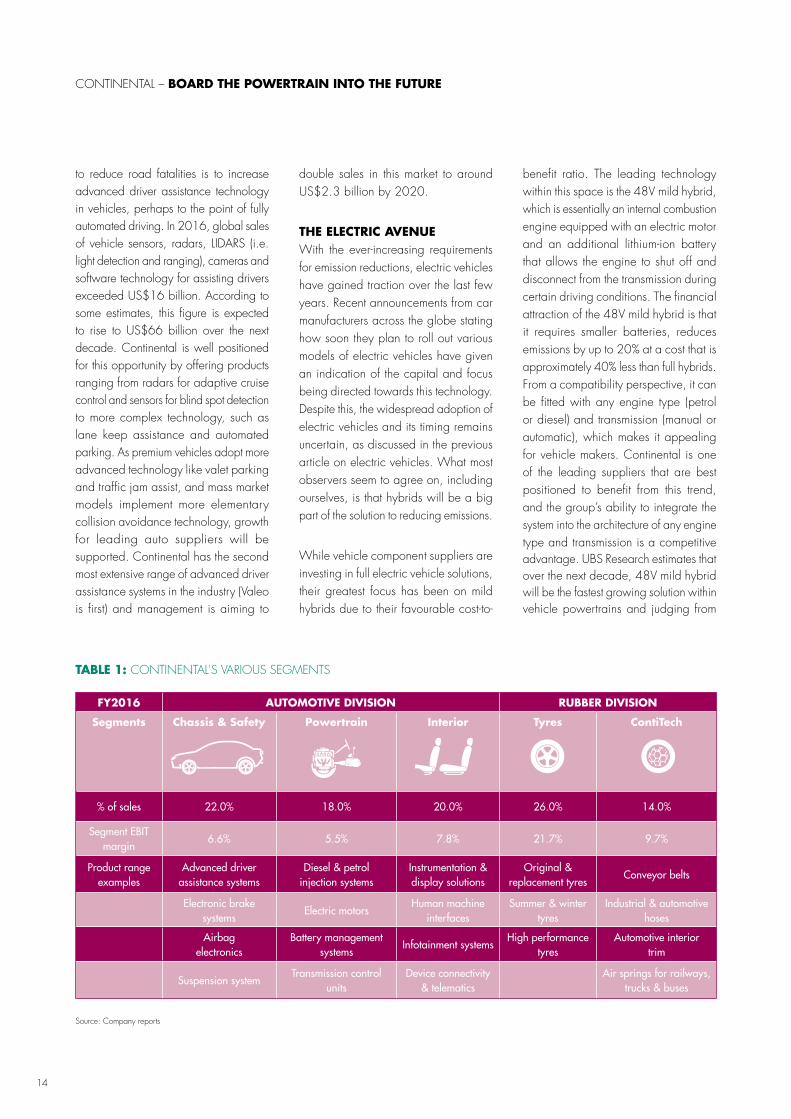

Continental’s history dates back to the 1870s when the company produced rubber products and tyres for carriages and bicycles. Since the group’s inception, acquiring rivals and being early to market with new products (such as tubeless tyres) have seen the group grow to become the world’s fourth largest tyre supplier. The diversification from being a pure tyre manufacturer occurred in 1995 when Continental established its Automotive division, selling various auto components. Subsequently, the automotive division’s product range and significance to Continental have grown extensively and it is now the second largest supplier of components to vehicle manufacturers across the world. The table on the next page details Continental’s two main divisions (Automotive and Rubber) and their five operating segments and some elements of their product offering.

WHERE THE RUBBER HITS THE ROAD Continental’s Rubber division, particularly its tyre segment, is the most widely recognised part of the group. Apart from the premium-branded Continental tyres, the group globally manufactures and sells tyres under ten other brands (such as Uniroyal, Viking, Matador and Sime Tyres) to passenger, light truck and commercial vehicles. Importantly, sales in this segment are tilted towards the replacement market, with only 30% of sales being generated from new vehicles. The wide range of tyre brands at different price points, coupled with large exposure to the replacement market, makes the tyre division defensive. While not immune to cyclical downturns, the tyre segment has shown itself to hold up group margins during different stages of the cycle, as illustrated in Graph 1.

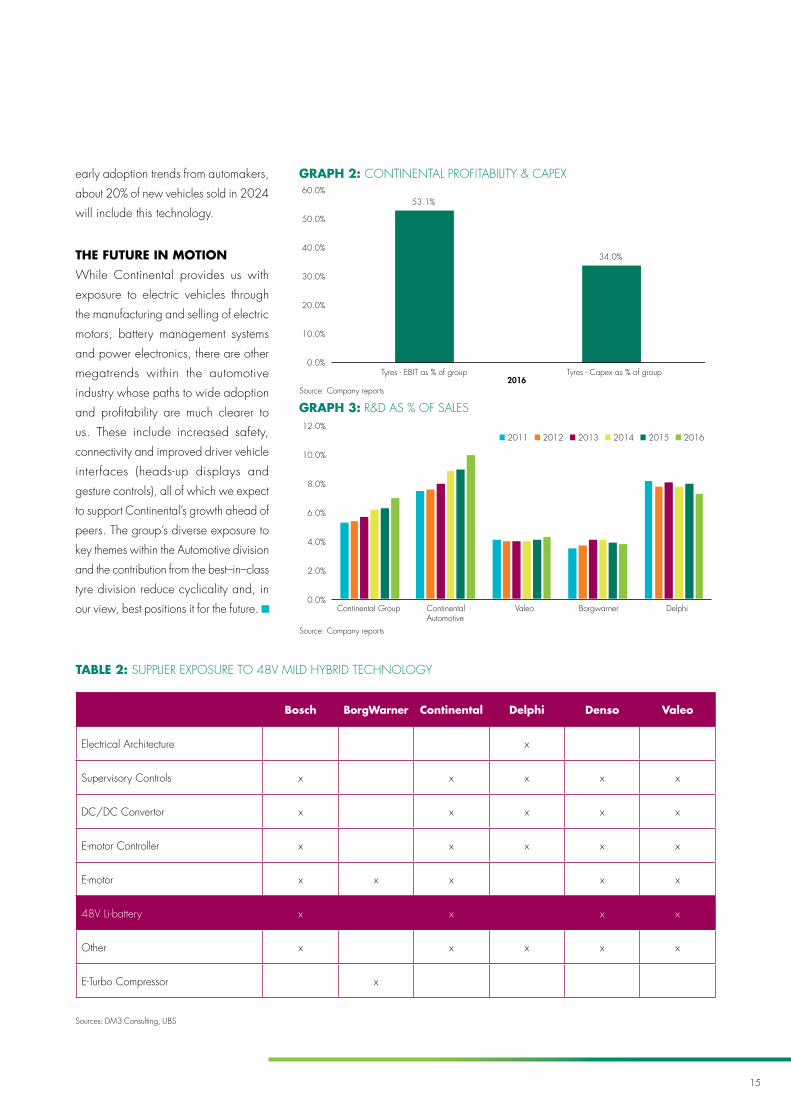

The tyre segment’s ability to generate a disproportionate amount of cash for its capital expenditure requirements is a key attraction. Graph 2 displays this graphically by showing the tyre segment’s 53% contribution to group earnings before

interest and tax, while only requiring 34% of group capital expenditure. The benefit of this can be seen in the Automotive division’s above-peer investment in research and development (R&D).

Essentially, Continental’s tyre business affords the Automotive division the ability to spend more on R&D than other component suppliers (see Graph 3), which informs our view that the group is well positioned to retain its leading role in the sector as new trends emerge. One such trend is digitisation. In 2016, Continental unveiled a new digital service, ContiConnect, for its commercial vehicle tyre business. This tyre management system monitors and analyses the tyre pressure and temperature of a fleet based on data from sensors inside the tyres. The benefits for fleet managers to remotely monitor the efficiency of their fleet in real time and take corrective action is clear and speak to the growing trend of connected vehicles.

AUTOMOTIVE DIVISIONThe Automotive division focuses on brake systems, powertrains and chassis, vehicle interiors and electronics. This division sells its products to various auto manufacturers, who outsource a large portion of component development and

manufacturing to suppliers like Continental, who have benefits of scale. Continental’s five largest customers are BMW, Ford, Daimler, Volkswagen and General Motors, who in aggregate contribute about 40% of the group’s revenue. Continental’s well-diversified customer base, high switching costs and long-established ties with customers ensure that the group is able to retain and defend its market share. In addition, as a supplier to numerous auto brands, Continental is able to benefit from different levels of demand in various regions and retain some pricing power, while minimising the risks associated with a specific vehicle model or brand losing market share.

INDUSTRY MEGATRENDSLooking at Continental’s diverse portfolio, a number of technologies stand out in terms of how they are aligned to some of the megatrends we are seeing in the auto industry. These trends include increased safety, autonomous driving and, of course, electric vehicles.

According to the World Health Organisation, about 1.3 million people die each year in road accidents. It is further estimated that human error is responsible for more than 90% of all accidents on the roads. One way

14

CONTINENTAL – BOARD THE POWERTRAIN INTO THE FUTURE

TABLE 1: CONTINENTAL'S VARIOUS SEGMENTS

Source: Company reports

FY2016 AUTOMOTIVE DIVISION RUBBER DIVISION

Segments Chassis & Safety Powertrain Interior Tyres ContiTech

% of sales 22.0% 18.0% 20.0% 26.0% 14.0%

Segment EBIT margin

6.6% 5.5% 7.8% 21.7% 9.7%

Product range examples

Advanced driver assistance systems

Diesel & petrol injection systems

Instrumentation & display solutions

Original & replacement tyres

Conveyor belts

Electronic brake systems

Electric motorsHuman machine

interfacesSummer & winter

tyresIndustrial & automotive

hoses

Airbag electronics

Battery management systems

Infotainment systemsHigh performance

tyresAutomotive interior

trim

Suspension systemTransmission control

unitsDevice connectivity

& telematicsAir springs for railways,

trucks & buses

to reduce road fatalities is to increase advanced driver assistance technology in vehicles, perhaps to the point of fully automated driving. In 2016, global sales of vehicle sensors, radars, LIDARS (i.e. light detection and ranging), cameras and software technology for assisting drivers exceeded US$16 billion. According to some estimates, this figure is expected to rise to US$66 billion over the next decade. Continental is well positioned for this opportunity by offering products ranging from radars for adaptive cruise control and sensors for blind spot detection to more complex technology, such as lane keep assistance and automated parking. As premium vehicles adopt more advanced technology like valet parking and traffic jam assist, and mass market models implement more elementary collision avoidance technology, growth for leading auto suppliers will be supported. Continental has the second most extensive range of advanced driver assistance systems in the industry (Valeo is first) and management is aiming to

double sales in this market to around US$2.3 billion by 2020.

THE ELECTRIC AVENUEWith the ever-increasing requirements for emission reductions, electric vehicles have gained traction over the last few years. Recent announcements from car manufacturers across the globe stating how soon they plan to roll out various models of electric vehicles have given an indication of the capital and focus being directed towards this technology. Despite this, the widespread adoption of electric vehicles and its timing remains uncertain, as discussed in the previous article on electric vehicles. What most observers seem to agree on, including ourselves, is that hybrids will be a big part of the solution to reducing emissions.

While vehicle component suppliers are investing in full electric vehicle solutions, their greatest focus has been on mild hybrids due to their favourable cost-to-

benefit ratio. The leading technology within this space is the 48V mild hybrid, which is essentially an internal combustion engine equipped with an electric motor and an additional lithium-ion battery that allows the engine to shut off and disconnect from the transmission during certain driving conditions. The financial attraction of the 48V mild hybrid is that it requires smaller batteries, reduces emissions by up to 20% at a cost that is approximately 40% less than full hybrids. From a compatibility perspective, it can be fitted with any engine type (petrol or diesel) and transmission (manual or automatic), which makes it appealing for vehicle makers. Continental is one of the leading suppliers that are best positioned to benefit from this trend, and the group’s ability to integrate the system into the architecture of any engine type and transmission is a competitive advantage. UBS Research estimates that over the next decade, 48V mild hybrid will be the fastest growing solution within vehicle powertrains and judging from

15

Bosch BorgWarner Continental Delphi Denso Valeo

Electrical Architecture x

Supervisory Controls x x x x x

DC/DC Convertor x x x x x

E-motor Controller x x x x x

E-motor x x x x x

48V Li-battery x x x x

Other x x x x x

E-Turbo Compressor x

TABLE 2: SUPPLIER EXPOSURE TO 48V MILD HYBRID TECHNOLOGY

Sources: DM3 Consulting, UBS

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

Continental Group ContinentalAutomotive

Valeo Borgwarner Delphi

2011 2012 2013 2014 2015 2016

53.1%

34.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

Tyres - EBIT as % of group Tyres - Capex as % of group2016

Source: Company reports

Source: Company reports

GRAPH 2: CONTINENTAL PROFITABILITY & CAPEX

GRAPH 3: R&D AS % OF SALES

early adoption trends from automakers,

about 20% of new vehicles sold in 2024

will include this technology.

THE FUTURE IN MOTION

While Continental provides us with

exposure to electric vehicles through

the manufacturing and selling of electric

motors, battery management systems

and power electronics, there are other

megatrends within the automotive

industry whose paths to wide adoption

and profitability are much clearer to

us. These include increased safety,

connectivity and improved driver vehicle

interfaces (heads-up displays and

gesture controls), all of which we expect

to support Continental’s growth ahead of

peers. The group’s diverse exposure to

key themes within the Automotive division

and the contribution from the best–in–class

tyre division reduce cyclicality and, in

our view, best positions it for the future.

16

17

GLENCORE – BETTING ON A SUSTAINABLE FUTURE

SAMEER SINGH – RESEARCH ANALYST

Glencore, the mining and trading company formerly known as Marc Rich & Co. AG, is fairly young as far as mining companies go. Established in 1974 by notorious businessman and deal-maker Marc Rich, the company maintains roots in the trading of ferrous and non-ferrous metals and minerals as well as crude oil.

18

Over the course of almost 45 years,

Glencore has grown to become the

world’s third largest commodity miner and

second largest commodities trader. With

operations spanning over 50 countries

and 155 000 employees, this is a

company that has geographic reach

and, importantly, for a large diversified

miner, significant scale and scope. It is this

combination of scale and scope that has

allowed Glencore to carve out meaningful

exposures to a mix of mid- and late-cycle

commodities, i.e. commodities where

demand is expected to peak as economies

evolve from low-income economies

to mid- to high-income economies1.

When looking at Glencore’s industrial

activities, as opposed to trading activities,

around 72% of industrial revenue and

66% of earnings are generated by metals

and minerals. The remainder is largely

generated from thermal coal, which is used

for power and heat generation. While

there are other mining companies that also

produce these commodities, none of them

have a balanced mix such as Glencore.

This balanced mix of commodities aims

to cushion the company’s top and bottom

line during the different phases of the

commodity cycle.

Arguably, the largest threat to mining

companies is managing the cyclicality

inherent in the industry. This cyclical nature

results from the delayed response of supply

to changes in demand, and vice versa:

On the back of higher demand, higher

prices prompt companies to expand and

develop additional capacity. Higher prices

and profitability in turn attract competition,

which then sees supply increase to a point

where prices begin to decline as demand

struggles to keep pace. Prices then fall

below marginal costs of production,

incumbents experience significant business

strain and mines are sometimes forced to

close. Thereafter, prices begin to stabilise

and eventually rise.

COMMODITY TRADING – DRAWING STRENGTH FROM ITS ROOTS Along with industrial production activities,

Glencore is also involved in the physical

trading of various commodities through

its Marketing and Logistics segment, and

Copper

Zinc

Nickel

Ferroalloys

Aluminium

Iron Ore

Coal

Oil

Copper

Zinc

Nickel

Ferroalloys

Aluminium

Iron Ore

Coal

Oil

42%

20%

5%

0%

27%

1%

26%

18%

3%5%0%

0%

26%

1%

22%

7%3%1%

1%0%

5%0%

83%

Marketing

5%

33%

23%4%6%

0%0%

33%1%

Copper

Zinc

Nickel

Ferroalloys

Aluminium

Iron Ore

Coal

Oil

Copper

Zinc

Nickel

Ferroalloys

Aluminium

Iron Ore

Coal

Oil

42%

20%

5%

0%

27%

1%

26%

18%

3%5%0%

0%

26%

1%

22%

7%3%1%

1%0%

5%0%

83%

Marketing

5%

33%

23%4%6%

0%0%

33%1%

GRAPH 1: INDUSTRIAL ACTIVITIES – REVENUE AND EARNINGS 1H2017

GRAPH 2: TOTAL REVENUE AND EARNINGS

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

0

50 000

100 000

150 000

200 000

250 000

2011 2012 2013 2014 2015 2016

Total Revenue Marketing Revenue

Marketing EBITDA Margin Industrial EBITDA Margin

GRAPH 3: MARKETING LESS CYCLICAL

1 This is opposed to the first half of the cycle, which is typified by large-scale fixed asset infrastructure investment and growing demand for commodities such as iron ore and coking coal, which is used in steel production.

REVENUE

RE

VENUE

EARN

INGS

EARNINGS

Source: Company reports

19

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

GLEN Peer 1 Peer 2 Peer 3 Peer 4

Early cycle Mid cycle Late cycle

Cop

per,

Zinc

, Nic

kel,

Alu

min

ium

, Le

ad

Iron

Ore

, Cok

ing

coal

,M

anga

nese

Cob

alt,

Oil/

Gas

, PG

Ms,

Dia

mon

ds,

Ther

mal

Coa

l,A

gric

ultu

ral p

rodu

cts

Com

mod

ities

wei

ghte

d by

con

tribu

tion

to 2

018F

EBI

TDA

0

20

40

60

80

100

0 5 10 15 20 25 30 35 40 45 50

Early cycle Mid cycle Late cycle

$US GDP per capita (2010)

GRAPH 4: ILLUSTRATIVE COMMODITY INTENSITY CURVES

GRAPH 5: GLENCORE MOST EXPOSED TO MID–AND LATE–CYCLE COMMODITIES

this is what truly sets the company apart from its peers. This segment effectively handles the physical trading of various commodities (this is what Glencore was initially built upon, prior to the purchase of Xstrata) and offers value-added services, including insurance, freight, storage and financing. To this end the company maintains a wide network of storage and logistics assets, allowing them to trade on a global scale. In addition to being the ‘middle-man’ between suppliers and final-users, the company also looks to exploit arbitrage opportunities. Owing to their scope and wide geographic footprint, the company is well-positioned to act on price differentials that emanate from three sources: product arbitrage (disparity between different grades or types of commodities), time arbitrage (spot versus future prices) and geographic arbitrage (same product but different prices in different regions).

We believe that the Marketing and Logistics segment will continue to be a material contributor to Glencore’s business and strategic growth. The contribution from a division that tends to be less correlated to commodity prices than pure mining, allows for further diversification of revenue sources and a less volatile earnings profile. We view this as a key competitive advantage relative to the other three big diversified miners i.e. Anglo American, BHP Billiton and Rio Tinto.

THE ‘LOST YEARS’ IN MININGThe period 2013 - 2016 is considered to be the lost years in mining. This is not only due to poor returns earned by investors investing in mining companies, but also because the contraction in the industry resulted in the loss of mines, loss

of confidence and, ultimately, loss of jobs.

Glencore was not immune to this cyclical

downturn and the major commodities the

company mined, and consequently the

company itself, experienced some of the

worst declines in its history.

However, it was not all cyclical as just

prior to the downturn in commodities,

Glencore had initiated and completed

its largest acquisition/merger to date,

that of mining giant Xstrata plc. The deal

with Xstrata was key to Glencore’s strategy

and provided substantial mining assets as

a base to support the trading business.

The only hiccup was timing. The financial

ramifications of a mega-merger at a time

when, in retrospect, commodity prices were

peaking post the Global Financial Crisis,

left a large pill for Glencore to swallow.

The company was resilient though.

Following Glencore Xstrata’s (as the

company was then known) maiden

results, the management team began

strategically addressing the fundamentals

GLENCORE – BETTING ON A SUSTAINABLE FUTURE

Source: Company reports

Source: Company reports

20

GLENCORE – BETTING ON A SUSTAINABLE FUTURE

of the business. Cash generation was prioritised, debt levels were being managed lower and profitability started to improve. 2015 saw management embark on a restructuring and recapitalisation exercise that involved a US$2.5 billion share placement, asset divestments totalling US$6.3 billion, the reduction in and suspension of inefficient mining assets, the suspension of dividend payments, refinancing of existing credit facilities and new debt issuances at more favourable interest rates. These efforts resulted in a total debt reduction of US$20 billion. The result of improved operational efficiencies, combined with recovering commodity prices, has seen Glencore’s share price rising over 200% since the beginning of 2016. Furthermore, in early 2017, the company reinstated its dividend and guided that the new policy will be to pay a fixed US$1 billion dividend (linked to the more stable cash flows from the Marketing division) and will incorporate a variable component of a minimum of 25% of industrial activities free cash flow.

SUSTAINABLE CONSUMPTIONThere are two key structural shifts emanating at present, namely the ‘digitalisation’ of the world and the promotion of more sustainable living. The latter, which refers to the need for renewable energy and sustainable agriculture, provides a tailwind for Glencore.

Glencore’s key commodities (copper, zinc, nickel, aluminium, cobalt, oil/gas, thermal coal and agricultural products) are all linked to mid- and late-cycle growth in commodities. As societies grow and mature, so too does the demand for these commodities. More specifically, the

advent of electric and hybrid vehicles has

garnered the most attention over the past

few years and Glencore is well-positioned

to contribute to this shift. Nickel, cobalt and

copper are key inputs into the manufacture

of batteries and it is estimated that the

average nickel manganese cobalt oxide

(NMC) battery uses 40-50kgs of nickel,

50-75kgs of copper and 5-15kgs of cobalt.

But it doesn’t end with electric vehicles as

the great push to sustainable living requires

more efficient and cost-effective means of

storing energy. Large scale battery farms

will be required to house and store wind

and solar energy for use at night and

during wind-free days.

Not only will society need to consume

energy more sustainably, we will also need

to find more sustainable ways of feeding

the global population. Glencore has long

maintained exposure to the agricultural

market (around 10% of marketing revenue

over the past five years). Building on

this earlier in the year, the company

showed their strongest intent yet to grow

in this market after approaching Bunge for

a potential business combination.

SETTING THE DEALS IN MOTIONBunge is a full supply chain agri-food

business incorporating operations that

span farm to consumer foods, across

more than 40 countries. A tie-up with

Bunge would provide Glencore with an

opportunity for consolidation with its existing

agri-business. Additionally, with agriculture

margins and share prices depressed, this

would appear an opportune time in the

cycle. Also supporting the rationale is

Glencore’s stronger financial position and

cash generation.

A deal with Bunge, or another large-scale agricultural business, highlights the potential benefits of scale and scope when considering managing the value chain. Glencore’s strategy to grow its logistics is supported by its ownership and interest in mining and agricultural assets. The more commodities they mine and/or control, the more they can pass on to their marketing/logistics business, providing increasing opportunities for margin growth. Glencore is playing the volume game, but not in the traditional ‘mine more and pay less per unit’ way. Instead, the company is adopting a ‘control and market more’ approach, thereby leveraging logistics to increase earnings.

MINING THE FUTUREGoing forward, society will increasingly place priority on green, sustainable energy and consumption solutions versus the unsustainable status quo. We believe that this structural shift, together with balanced commodity and trading exposures, a diversified resource mix, and structural-growth linked commodities, give Glencore a substantial competitive advantage relative to peers. Combining the above with an adept and invested management team and sound financial management will allow Glencore to sustainably maintain its competitive advantage well into the future.

22

23

The recent news that the 30–year–old wife of late multi-millionaire Playboy founder Hugh Hefner (91) is set to inherit nothing from his estimated US$43 million estate, due to a watertight prenuptial contract, has raised a number of questions around the legal standing of a prenuptial agreement after the death of a spouse and the importance of having a sound and an up-to-date will.

Given the rising rate of divorce and the increasing prevalence of blended families in South Africa, good estate planning can help ease the burden placed on loved ones left behind after the death of a bread winner. This is particularly important in cases where individuals – especially ultra-high-net-worth individuals – have multiple ex-partners and children from previous relationships, as an unclear will can result in years of fighting around how an estate should be divided up among different families and spouses. This often results in the interpretation of an unclear or a badly drafted will having to be settled in court, which can be costly in itself.

WILL VALIDITY & MAINTENANCE CLAIMS The validity of a will is also of utmost importance when it comes to the winding up of an estate. In South Africa, the Wills Act stipulates that, in order to be legally binding, a will must be valid and lawful, which means a number of requirements must be adhered to. This includes the will being signed in the presence of two witnesses, with the testator/testatrix’s signature appearing on each individual page. If a will is deemed invalid, the estate will be distributed according to the Intestate Succession Act.

FIDUCIARY LESSONS TO BE LEARNED FROM THE PASSING OF

HUGH HEFNERALIDA BRINK – FIDUCIARY SPECIALIST

Regarding the allegations around Hefner’s wife being left out of the will due to an 'ironclad' prenuptial agreement, depending on the circumstances, South African law may circumvent this. Under South African law, in terms of the Maintenance Act (No. 99 of 1998), if the surviving spouse was financially dependent on the deceased spouse and is unable to provide for him– or herself, the surviving spouse is permitted to claim maintenance in order to continue maintaining the living standards he or she has become accustomed to. The financial position of the estate in providing for the claim will also be considered. The court will then work out how much maintenance the surviving spouse would need over his or her life expectancy.

If, however, the surviving spouse is not destitute and was not dependent on the deceased, then the claim might not be successful. In the case of Friedrich and Others v Smit NO and Others [2017] ZASCA 19; 2017 (4) SA 144 (SCA), the claimant instituted a maintenance claim against her late husband’s estate as his will stipulated all inheritance was to be left to his surviving children from his previous marriage. The claimant was unsuccessful in this case as the court found that she did not meet the requirement of being financially dependent on the deceased and was able to look after herself. Hypothetically speaking, if Hefner and his wife were South Africans, considering that Hefner gave his wife US$5 million and an apartment before his passing, she would probably also not have succeeded with a maintenance claim in terms of the Maintenance of Surviving Spouses Act.

ESTATE PLANNING FOR BLENDED FAMILIESIt could also happen that a spouse sets up a trust to take care of the surviving spouse and that upon the death of the surviving spouse, the children from the first marriage will inherit. This is often done to avoid the second spouse’s children (who are not the children of the deceased) from inheriting anything from the deceased later.

The problems that commonly occur in the case of estate planning for blended families are as a result of competing interests between children from previous marriages and spouses. Often these situations can become extremely tumultuous and cause untold strain on all parties involved. However, this can all be avoided with proper estate planning and a well-drafted will.

To conclude, the most important thing to remember is to update your will as soon as any circumstances change, to ensure that it reflects your current reality. Remember that your most recent, valid will, will become applicable upon your passing, even if it was drafted 25 years ago. It is also important that the stipulations in your will are practical and executionable. An example would be where cash is left to someone, but there is no liquidity in the estate. As such, we advise you to be proactive when it comes to estate planning and seek the necessary professional help in order to do so.

24

'Dispense with a horse.' Those were the words atop the world’s first-ever car advert in 1898, for the Winton Motor Carriage. It clearly belonged to a more innocent age of motoring, when a car’s main virtue was being a car. There wasn’t much else to sell. But as the motorcar entered the 20th century, so did the advertising that sold it.

It all began with very simple black and white adverts, produced soon after motor vehicles were invented. These days, we’re bombarded from all angles with slick videos, flashy print ads and more online content than we could ever possibly consume. Let’s take a look at the past 120 years of car advertising:

SELLING THE DREAM – HOW CAR ADVERTISING

HAS EVOLVED

YEARS

SIMPLICITYThe simple adverts in the early days were a sign of the times, emphasising that cars were the ultimate luxury. The first–ever car advert in 1898 enticed people to 'Dispense with a horse" and simply sold the benefits of the Winton Motor Carriage.

1898

1940

1920

THE ART OF ILLUSTRATIONDuring the twenties, car ads became more creative and colourful as there was more competition. The vintage ad of this Ford Lincoln displays bright colours and a sleek vehicle in true cosmopolitan style.

STORYTELLING (POST-WAR ERA)Although cars were still a luxury item, competition

increased with a focus on the rampant consumerism experienced during this era. Printed

ads had more of a storytelling component and extravagant copy. Ads started telling the story of a

more aspirational lifestyle.

25

26

CREATIVE EVOLUTIONCar ads got even bigger and more

creative. Volkswagen ‘s 1959 ad for the Beetle with the tagline “Think Small” was recognised as one of the greatest ads of

all time changing the industry forever. COMPETITIVE ADVERTISING In the early sixties the question changed from 'Do I need a car?' to 'What car should I buy?' Two major players in the car industry emerged, namely Japan and Germany, starting the trend of competitive advertising.

1950

1960

1960

1980

2000

2017

HIS-AND-HERS Adverts which encourage gender stereotypes

followed. Men were the only target audience while women were portrayed in the background.

EMOTIONAL MARKETING Supercars hit the market in the eighties and car ads offered manufacturers an opportunity to show off what their cars were capable of (e.g. Land Rover driving up a dam wall). Ads with sleek imagery of studio-shot cars became the norm. It was all about status, while also selling uniqueness.

THE RISE OF GREEN ADVERTISING Awareness around global warming and

corporate responsibility emerged in the 2000s driving the need for 'green cars'. Advertising

evolved from emotion, function and performance to environmental issues and responsibilities.

THE DIGITAL AGEA transformation of advertising is taking place as customers spend more time on mobiles, tablets and laptops. Viral advertising has been put to great use by car manufacturers allowing them to engage with their target market and connect with them in a personal manner.

27

DEREK ALTONTel: 021 524 4566Cell: 072 290 [email protected]

SHANE LAWRENCETel: 021 524 4656 Cell: 079 526 [email protected]

PAUL STEVENTel: 021 524 4572Cell: 076 719 [email protected]

JOHANN VAN ZYLTel: 021 524 4574Cell: 083 261 [email protected]

MICHELLE MATTHEWSTel: 021 524 4421Cell: 083 979 [email protected]

DEAN GINSBERGTel: 011 245 3818Cell: 083 650 [email protected]

VISHAL HURRICHUNDTel: 011 245 3812Cell: 082 411 [email protected]

TREVOR O’CALLAGHANTel: 011 245 3801Cell: 083 660 [email protected]

MIKE SITHOLETel: 011 245 3741Cell: 083 352 [email protected]

GARY SMITHTel: 011 245 3802Cell: 082 464 [email protected]

ROY TOPOLTel: 011 245 3619Cell: 082 809 [email protected]

HELMAR BREYTENBACHTel: 031 581 0773Cell: 082 564 [email protected]

BRIAN VERMEULENCell: 083 408 [email protected]

LOUIS FOURIETel: 012 369 7232Cell: 083 391 [email protected]

GREGORY POTGIETERTel: 012 369 7234Cell: 082 823 [email protected]

JACQUES THERON Tel: 012 369 7235Cell: 082 495 [email protected]

JAMES BUZZARDTel: 031 581 0763Cell: 083 509 [email protected]

SCOTT LOGAN Tel: 031 581 0768Cell: 082 908 [email protected]

PRIVATE CLIENT PORTFOLIO MANAGERS

CHRIS POTGIETERHead of PCSTel: 021 524 4582Cell: 082 827 [email protected]

ANDREW DITTBERNERChief Investment OfficerTel: 021 524 4867 (CPT) 011 217 1945 (JHB)Cell: 083 296 [email protected]

VICTOR MUPUNGAResearch AnalystTel: 021 524 4466Cell: 072 838 [email protected]

MOOSA HASSIMInvestment Analyst Tel: 021 524 4609Cell: 072 448 [email protected]

SAMEER SINGHResearch AnalystTel: 021 524 4529Cell: 072 383 [email protected]

CONTACT US

CAPE TOWN

JOHANNESBURG

PRETORIA

DURBAN

BLOEMFONTEIN

28

This document is for information purposes only and does not constitute financial advice in any way or form. It is important to consult a financial planner to receive financial advice before acting on any information contained herein. Old Mutual Wealth and its directors, officers and employees shall not be responsible and disclaim all liability for any loss, damage (whether direct, indirect, special or consequential) and/or expense of any nature whatsoever, which may be suffered as a result of or which may be attributable, directly or indirectly, to the use of, or reliance upon any information contained in this document.

Old Mutual Wealth Private Client Securities (“PCS”) is a division of Old Mutual Wealth Trust Company (Pty) Ltd (“OMWTC”), an authorised Financial Services Provider, Reg No: 1925/002721/07. PCS is authorised to provide financial services on the OMWTC licence.

The Estuaries, 2 Oxbow Crescent, Century City 7441. Tel: +27 (0)21 524 4400, Fax: +27 (0)21 441 1060, Email: [email protected], Website: www.omwealth.co.za.