Embed Size (px)

Citation preview

CoG (11/07) Item 15.9

DATE 11 July 2017

REPORT FOR Council of Governors

REPORT FROM Stanley Shreeve – Chair of Audit Committee / NED

CONTACT OFFICER Director of Finance

SUBJECT Audit Committee Annual Report 2016/17

BACKGROUND DOCUMENT (IF ANY) N/A

EXECUTIVE COMMENT (INCLUDING KEY ISSUES OF NOTE OR, WHERE RELEVANT, CONCERN THAT THE COG NEED TO BE MADE AWARE OF)

This is the annual report from the Chair of the Audit Committee to the Trust Board and summarises the key work of the Committee during 2016/17.

It was received and reviewed by the Audit Committee at its meeting on 18th May 2017 and submitted to the May 2017 meeting of the Trust Board.

It is supplied to the Council of Governors for information.

COUNCIL ACTION REQUIRED To note the report from the Chair of the Audit Committee.

TRUST AUDIT COMMITTEE

ANNUAL REPORT

FOR THE YEAR ENDED 31ST MARCH 2017

Stanley Shreeve FCCA Chair of Audit Committee 18 May 2017

Northern Lincolnshire and Goole NHS Foundation Trust

Audit Committee Annual Report for the year ended 31st March 2017 _________________________________________________________________________

Contents

Page

1 Introduction and Purpose of Report…………………………………………………...3

2 Membership and Attendance………………………………………………………......3

3 Principle Review Areas……………………………………………………………........3

3.1 Governance, Risk Management and Internal Control 3.2 Internal Audit 3.3 Counter Fraud 3.4 External Audit

4 Financial Reporting……………………………………………………………………...6

5 Management Reports…………………………………………………………………...7

6 Other Matters Worthy of Note…………………………………………………….........7

7 Conclusion and Plans for 2017/18…………………………………………………….8

Appendix 1 – Schedule of attendance at Audit Committee meetings during 2016/17......9

Appendix 2 – Audit Committee Work Plan for 2017/18……………………………………10

Appendix 3 – Policy for Engagement of External Audits for Non-Audit Work…..………12

2 | P a g e

Northern Lincolnshire and Goole NHS Foundation Trust

Audit Committee Annual Report for the year ended 31st March 2017 _________________________________________________________________________

1. Introduction and Purpose of the Report

The Audit Committee of Northern Lincolnshire and Goole NHS Foundation Trust (NLaG FT) is established under Board delegation with approved terms of reference that are aligned with the latest Audit Committee Handbook (2014), as published by the Healthcare Financial Management Association (HFMA) in association with the Department of Health. The Audit Committee independently reviews, monitors and reports to the Board on the attainment of effective control systems and financial reporting processes.

The Membership and Terms of Reference for the Audit Committee are subject to regular review and revision as necessary. They were last approved by the NLaG FT Board in November 2016 following review and discussion at the October 2016 meeting of the Audit Committee. The terms of reference will be reviewed again during 2017/18 in line with the Committee’s annual work plan, or sooner if necessary, to ensure that they remain fit for purpose.

As part of the Committee’s regular review of its own governance arrangements the Committee conducted a self-assessment workshop in January 2017 which used the latest Healthcare Financial Management Association (HFMA) NHS Audit Committee Handbook self-assessment checklist as the basis for review. This exercise did not identify any significant gaps in the Committee’s processes.

This report sets out how the Audit Committee has satisfied its terms of reference during the financial year and seeks to provide the Board with evidence relevant to its responsibilities for the Annual Governance Statement (AGS).

The Audit Committee continues to recognise the work of the Trust Governance and Assurance Committee in scrutinising risk. The Chair of the Audit Committee is also a member of the Trust Governance and Assurance Committee.

2. Membership and Attendance

The Audit Committee consists of three Non-Executive Directors (NEDs), for which two must be present at an Audit Committee meeting for it to be quorate. The Audit Committee has been chaired since August 2012 by Stanley Shreeve. Current NED members are Neil Gammon and Linda Jackson. There is cross NED membership with other Trust committees.

It met on seven occasions (six full meetings plus an additional meeting for the audited accounts to be approved) during the 2016/17 financial year and has discharged its responsibilities for scrutinising the risks and controls which affect all aspects of the Trust’s business.

A record of attendance by Audit Committee members and regular attendees is disclosed at Appendix 1 for information. The record shows generally excellent attendance rates for both core members and regular attendees.

3. Principle Review Areas

3.1 Governance, Risk Management and Internal Control

During 2016/17 the Audit Committee reviewed relevant disclosure statements, in particular the Annual Governance Statement (AGS), the Head of Internal Audit Opinion (HoIAO), External Audit opinion and other appropriate independent assurances and considers that the

3 | P a g e

Northern Lincolnshire and Goole NHS Foundation Trust

Audit Committee Annual Report for the year ended 31st March 2017 _________________________________________________________________________

AGS is consistent with the Audit Committee’s view on the Trust’s system of internal control. Accordingly, the Audit Committee supported Board approval of the AGS for 2016/17.

The Audit Committee recognises that the review of processes governing risk management and the Board Assurance Framework (BAF) are reviewed by the Trusts Governance and Assurance Committee as part of its terms of reference. However, the Committee will be receiving quarterly reports on the Trust’s risk register and the BAF during the coming year with a view to considering whether the processes are resilient as opposed to reviewing individual risks.

3.2 Internal Audit

The Trust’s internal audit service, provided by KPMG, entered the third year (2016/17) of its contract with NLaG FT. The contract commenced on the 1st June 2014 following a formal mini-tendering exercise using a national framework agreement. An agreed Internal Audit Charter is in place.

An internal audit plan was considered and agreed for 2016/17 at the February 2016 meeting of the Audit Committee, and kept under review throughout the year. As is normal practice, an internal audit planning workshop was also held in January 2017 to consider the annual internal audit plan for 2017/18 and align it to the Trust’s strategic risks. The process is designed to maximise the value of internal audit reviews and resulting reports. It is accepted that this risk based approach may however lead to an increase in the number of reports resulting in partial assurance outcomes. The following officers were in attendance at the planning workshop:

• Stanley Shreeve – Chair of Audit Committee / NED• Anne Shaw – Trust Chairman• Linda Jackson – NED• Neil Gammon – NED• Sue Cousland - NED• Marcus Hassall – Director of Finance• Karen Dunderdale – Deputy Chief Executive• Tara Filby – Chief Nurse• Jug Johal – Director of Estates and Facilities• Steve Vaughan – Interim Chief Operating Officer• Sally Stevenson – Assistant Director of Finance – Compliance and Counter Fraud• Clare Partridge – Head of Internal Audit – Director - KPMG• Katie Goodall – Audit Manager – KPMG• Jakira Motala – Assistant Audit Manager - KPMG

As can be seen, there was good engagement from the Trust Board with this planning workshop. KPMG commented at the February 2017 Committee meeting that this workshop had been one of the best and, in a positive way, most challenging that they had done.

The Committee received the Annual Internal Audit Report for 2015/16 at its June 2016 meeting. As in previous years the Audit Committee has sought to work effectively with Internal Audit throughout the year to review, assess and develop internal control processes as necessary. The Audit Committee reviewed progress against the agreed internal audit work plan for 2016/17 via routine written progress reports from KPMG at each meeting, at which a representative of KPMG was always present. Written progress reports outline the status of the planned audit work for the year and the outcome of individual reviews performed, along with associated recommendations where appropriate.

4 | P a g e

Northern Lincolnshire and Goole NHS Foundation Trust

Audit Committee Annual Report for the year ended 31st March 2017 _________________________________________________________________________

Internal Audit completed fifteen reports for 2016/17, of which eight were ‘core’ reviews, six were ‘risk based’ reviews and one was a piece of benchmarking work. Of these reviews there was one ‘no assurance’ audit report issued as a result of data quality issues relating to waiting list management. Six reports resulted in ‘partial assurance with improvements required’ as to the adequacy and effectiveness of control arrangements in place. Of these six reviews five related to risk based audits where a lower opinion rating is often anticipated. The remaining reviews received assurance ratings of either ‘significant assurance’ or ‘significant assurance with minor improvement opportunities’.

Since the ‘no assurance’ waiting list data quality report was received at the February 2017 meeting, the Audit Committee requested and received an initial progress report at its April meeting. Updates will continue to be requested in order to be provided with the appropriate assurance that the recommendations resulting from the review are being implemented and embedded within the organisation, and until the Audit Committee is satisfied that further oversight by the Committee is no longer necessary. It is worthy of note that the resulting recommendations contained within all internal audit reports for 2016/17 were fully accepted by the operational and executive leads in order to address the issues identified.

The 2016/17 Head of Internal Audit Opinion (HoIAO) was also received by the Committee which for the first time gave an overall opinion as follows: Partial assurance with improvements required can be given on the overall adequacy and effectiveness of the organisation’s framework of governance, risk management and controls. This was disappointing but not unexpected given the range of issues identified by internal audit throughout the year and the number of ‘partial’ or ‘no assurance’ reports received. This HoIAO is included within the AGS which forms part of the Trust’s Annual Report.

In terms of monitoring the implementation of internal audit recommendations, KPMG originally provided the Trust with a tracker database in 2015. This was initially populated by them, from their preliminary follow-up work at the handover from the former internal audit provider, to enable the Trust to internally monitor the implementation of all internal audit recommendations going forward. Upon receipt of each internal audit report the Trust enters new recommendations onto the tracker and then routinely follows up each recommendation as its implementation date becomes due. The details contained on the tracker are then used to produce a routine summary report on the status of recommendations to each meeting of the Audit Committee for oversight and scrutiny purposes. The Trust’s internal follow-up process is subject to review by internal audit. KPMG also review the evidence (both narrative and documentary) in support of all recommendations considered to be closed in relation to both high and medium priority recommendations. The Audit Committee has recently requested that the routine report of outstanding recommendations is submitted to the Trust’s Executive Team meeting. This will enable further executive review and action in order to address the number of recommendations which remain outstanding for implementation from previous years.

3.3 Counter Fraud

The Audit Committee has continued to receive regular written progress reports from the Trust’s Local Counter Fraud Specialist (LCFS) throughout the year. Additionally the Annual Counter Fraud Report for 2016/17 and the Annual Counter Fraud Operational Plan were also submitted. The Committee notes the continuing efforts of the LCFS to promote awareness of counter fraud issues throughout the organisation and develop an anti-fraud culture, whilst at the same time investigating allegations of fraud to a criminal standard.

5 | P a g e

Northern Lincolnshire and Goole NHS Foundation Trust

Audit Committee Annual Report for the year ended 31st March 2017 _________________________________________________________________________

The LCFS has continued to liaise effectively with the Trust’s Human Resources team and external professional bodies (e.g. NMC, HCPC) to apply appropriate internal disciplinary and professional body sanctions as necessary.

The Trust continues to host and manage an in-house counter fraud collaborative, known as Counter Fraud Plus (CFP) between itself, Doncaster and Bassetlaw Teaching Hospitals NHS Foundation Trust and United Lincolnshire Hospitals NHS Trust. This collaborative arrangement commenced in July 2013 under a formal SLA arrangement. It is designed to provide a more resilient counter fraud service between the three organisations. The Committee has received reports that the collaborative continues to work effectively and successfully, and the Committee once again applauded the effort and achievements of the CFP team throughout 2016/17.

The Committee also received updates in relation to the organisational changes taking place at a national level within NHS Protect. As from 1st April 2017 their service delivery model changed and certain aspects of their support to LCFSs ended (e.g. regional team advice/support and national training centre). Work is also under way to create a new Special Health Authority and the new organisation will be called the NHS Counter Fraud Authority (NHS CFA). NHS Protect will continue to exist until the new NHS CFA launches on the 3rd July 2017.

3.4 External Audit

The Trust initially appointed its current External Auditor, Pricewaterhouse Coopers LLP (PwC), in September 2012. They were re-appointed in September 2016 following a mini-tendering exercise. The Audit Committee supported the Council of Governors with this appointment process. The new contract is for a term of three years, with the option to extend for a further year. PwC were unable to attend two of the seven meetings (August and October 2016) of the Committee during 2016/17. Verbal or written progress reports are received from the Trust’s External Auditor at Audit Committee meeting, including the audit opinion on the Trust’s annual financial statements and Quality report.

PwC has in previous years also provided non-audit services to the Trust and the value of such work is routinely disclosed in the Trust’s accounts. However it has not provided any such services during 2016/17. In line with Regulator guidance, the Trust has a ‘Policy for Engagement of External Auditors for Non-Audit Work’ to ensure that potential conflicts of interest, either real or perceived, are avoided in terms of the objectivity of their opinion on the financial statements of the Trust. The policy, reproduced at Appendix 3, is subject to annual review and was duly considered by the Audit Committee at its February and April 2017 meetings and updated to reflect the latest National Audit Office (NAO) guidance in this area.

During the year private meetings with both the external and internal auditors have taken place before each Audit Committee meeting. In these private meetings the auditors have expressed satisfaction with the level of cooperation received from the Director of Finance and his team, and no matters of concern have been raised.

4. Financial Reporting

At its April and May 2016 meetings the Audit Committee reviewed the draft and audited annual financial statements for 2015/16 before submission to the External Auditor, the Trust Board and Monitor (now NHS Improvement (NHSI)), and we understand these were in agreement with our accounting records and the current Regulator requirements.

6 | P a g e

Northern Lincolnshire and Goole NHS Foundation Trust

Audit Committee Annual Report for the year ended 31st March 2017 _________________________________________________________________________

Prior to the preparation of the 2016/17 financial statements, the Committee reviewed and agreed the detailed accounting principles at its February 2017 meeting. The Audit Committee also reviewed the draft and audited annual financial statements for 2016/17 prior to the submission of this report to the May 2017 Trust Board meeting. The Audit Committee approved the 2016/17 financial statements on behalf of the Trust Board (in line with formal delegated authority given by the Board in February 2017), which are due for submission to NHSI on Wednesday 31st May 2017.

There was once again, as with the previous two years, heightened scrutiny of the 2016/17 financial statements by the External Auditor in relation to the matter of ‘Going Concern’ given the Trust’s increased financial deficit at the year end. The financial climate for all acute providers continues to prove extremely challenging. However, NHSI have been directly engaged with the Trust on finances since late 2013 and continue to work with the organisation in this regard particularly since it placed the Trust into Financial Special Measures in March 2017. At the April 2017 Committee meeting the issue of Going Concern was discussed with the External Auditor. As a result the Audit Committee endorsed the view that the Trust is a going concern for the purposes of the annual accounting exercise.

In April 2016 the Audit Committee reviewed and approved minor revisions to the Trusts Standing Financial Instructions (SFIs) and the Trust Devolution Policy including Reservation of Powers to the Board and Scheme of Delegation (SoD). In doing so it satisfied itself that these governance documents were in accordance with good financial practice. Both documents were due to expire at the end of May 2017 and work has been underway to refresh these and make them more user friendly for staff. However this exercise has not been able to be completed as yet due to a number of key pieces of work which are on-going and until there is some stability within the organisation and confirmation of the longer-term direction of the Trust. The Committee supported the extension of the SoD and SFIs until 31st July 2017 and that was ratified by the Board at its April 2017 meeting.

5. Management Reports

The Committee has requested and reviewed reports and received verbal assurances from various Directors and managers within the organisation in relation to relevant areas of enquiry during the financial year 2016/17. We thank all those who have assisted the Audit Committee in these matters.

Officers attending Audit Committee meetings on an ad-hoc basis are shown on Appendix 1 for information.

6. Other Matters Worthy of Note

The Committee followed its agreed annual work plan throughout the year and received regular reports covering Waiving of Standing Orders; Losses and Compensations; Hospitality and Sponsorship declarations; Salary Overpayments and Complaints Ombudsman Compensation Payments. Additional information is called for as appropriate.

In light of the Trust’s worsening financial position, the Committee commissioned additional reports to be received routinely on procurement matters and a detailed quarterly analysis of significant variances on the Trust’s Balance Sheet. These have proved to be useful reports to the Committee and will continue to be received throughout 2017/18.

7 | P a g e

Northern Lincolnshire and Goole NHS Foundation Trust

Audit Committee Annual Report for the year ended 31st March 2017 _________________________________________________________________________

The Committee once again received the Local Security Management Specialist (LSMS) work plan and annual report. In line with the latest HFMA Audit Committee Handbook, these additional anti-crime items are provided annually to the Audit Committee for information.

Throughout the year the Committee also received minutes from the Trust’s Resources Committee, Trust Governance and Assurance Committee and the Quality and Patient Experience Committee. Additionally from February 2017 the minutes of the Infection and Prevention Control Committee were also received. The Committee discharged its responsibilities for providing assurance on these matters as per its terms of reference.

Minutes of Audit Committee meetings are submitted to the above named committees and the Trust Board for information once approved as true and accurate at the following meeting. The Trust Board and Council of Governors also receive highlight reports from the Committee, and other sub-committees have matters escalated to them from the Audit Committee where it is felt necessary to do so.

7. Conclusion and Plans for 2017/18

The Audit Committee work plan for 2017/18 has been reviewed and refreshed and is attached to this report for information at Appendix 2. The work plan was duly considered and approved by the Audit Committee.

The Council of Governors will also receive a copy of this annual report and work plan for information.

The Audit Committee will remain active in reviewing the risks, internal controls, reports of auditors and audit recommendations and will continue to press for action and improvements where required.

8 | P a g e

Northern Lincolnshire and Goole NHS Foundation Trust

Audit Committee Annual Report for the year ended 31st March 2017 _________________________________________________________________________

Appendix 1 - Schedule of Attendance at Audit Committee meetings during 2016/17

Member / Attendee Apr-16 May-16 Jun-16 Aug-16 Oct-16 Dec-16 Feb-17 Overall Attendance

Members:

Stan Shreeve – Chair Y Y Y Y Y Y Y 100%

Neil Gammon – NED Y Y Y Y N Y Y 86%

Linda Jackson – NED Y Y N Y Y Y Y 86%

Regular Attendees:

Marcus Hassall - DoF Y Y Y Y Y Y Y 100%

Wendy Booth - DoPA Y Y N N Y N*4 N*4 43%

Asst. DoF – Compliance & Counter Fraud

Y Y Y Y Y Y Y 100%

Internal Audit Y Y Y Y Y Y Y 100%

External Audit

LCFS

Y

Y

Y

N/A*1

Y

Y

N

N*2

N

Y

Y

N*2

Y

Y

71%

71%

Head of Procurement - - - Y*3 Y Y Y 100%

Ad-hoc Attendees:

Asst. DoF – Process & Control (NP) Y Y - - - - Y -

Anne Shaw - NED - - - Y - - - -

Interim COO (KF) - - Y - - - - -

Director of People & OE (JA) - - - - Y Y - -

Medical Director (LR) - - - - - Y - -

Deputy DoF (PC) - - - - - Y Y -

Asst. Director of P&OE - - - - - - Y -

Notes: 1 Nicki Foley, LCFS - not required to attend, as final accounts meeting only 2 Sally Stevenson, Assistant Director of Finance – Compliance & Counter Fraud in attendance to present report 3 Adam Jacklin, Head of Procurement – first meeting as regular attendee 4 Kathryn Helley, Deputy Director of Performance Assurance - attended on behalf of Wendy Booth

9 | P a g e

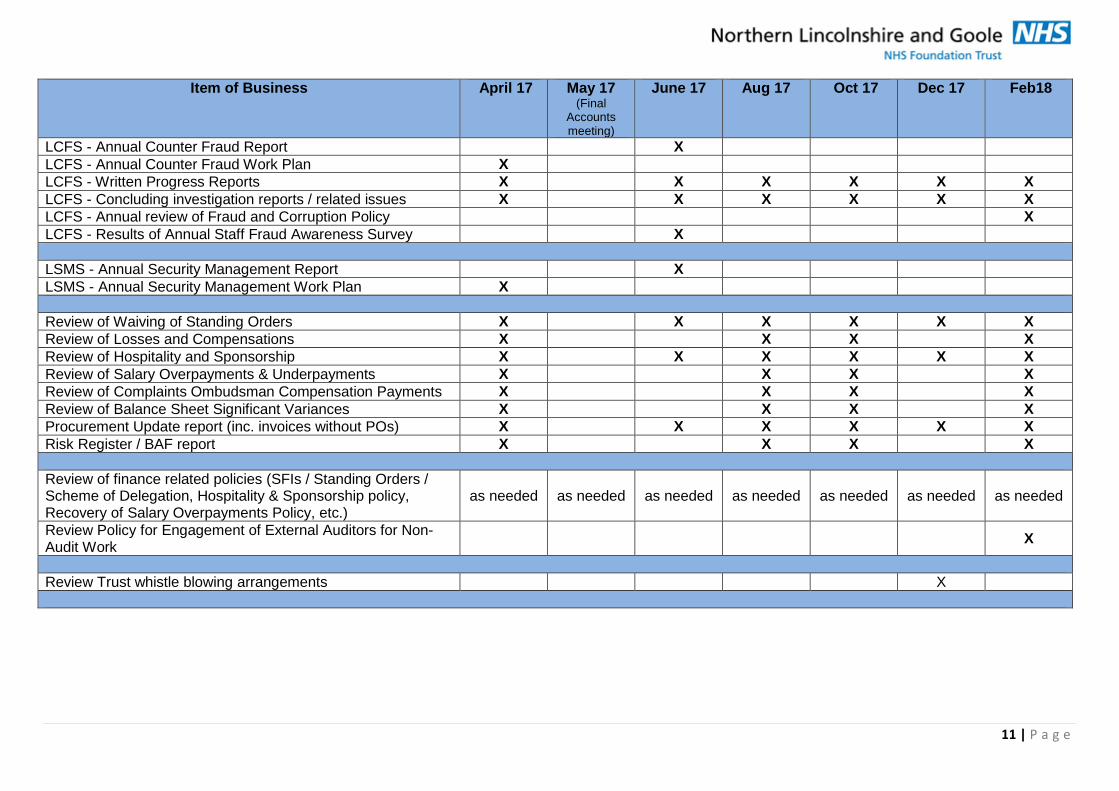

APPENDIX 2 - TRUST AUDIT COMMITTEE WORK PLAN - year ended 31st March 2018 Item of Business April 17 May 17

(Final Accounts meeting)

June 17 Aug 17 Oct 17 Dec 17 Feb18

Audit Committee - Annual Review of Terms of Reference X Audit Committee - Annual Review of Work Plan X Audit Committee - Annual Self-Assessment Exercise & Results X Audit Committee - Annual Report to Trust Board / CoG X Audit Committee - Annual meeting dates/times/locations X Private Discussion with Auditors (internal and external) X X X X X X X Receive minutes from other Board sub-committees (Resources / TGAC / QPEC / IPCC) X X X X X X

External Audit - Annual External Audit Plan / Timetable / Fees X External Audit - Routine Progress Reports X X X X X X X External Audit - Year End Report & Letter of Representation X External Audit - Report on Trust’s Quality Account X

Internal Audit - Annual Internal Audit Plan X Internal Audit - Routine Progress Report / Technical Updates X X X X X X Internal Audit - Head of Internal Audit Opinion X Internal Audit - Annual Report (inc. client feedback survey results)

X

Internal Audit - IA Plan strategic workshop results X

Receive Status Report on Implementation of Internal Audit Recommendations X X X X X X

Annual Governance Statement X General Governance Issues / Assurance Framework / Risks X X X X X X X

Review changes to Accounting Policies X Receive draft annual accounts X Receive Going Concern Report X Receive audited annual accounts X

10 | P a g e

Item of Business April 17 May 17 (Final

Accounts meeting)

June 17 Aug 17 Oct 17 Dec 17 Feb18

LCFS - Annual Counter Fraud Report X LCFS - Annual Counter Fraud Work Plan X LCFS - Written Progress Reports X X X X X X LCFS - Concluding investigation reports / related issues X X X X X X LCFS - Annual review of Fraud and Corruption Policy X LCFS - Results of Annual Staff Fraud Awareness Survey X

LSMS - Annual Security Management Report X LSMS - Annual Security Management Work Plan X

Review of Waiving of Standing Orders X X X X X X Review of Losses and Compensations X X X X Review of Hospitality and Sponsorship X X X X X X Review of Salary Overpayments & Underpayments X X X X Review of Complaints Ombudsman Compensation Payments X X X X Review of Balance Sheet Significant Variances X X X X Procurement Update report (inc. invoices without POs) X X X X X X Risk Register / BAF report X X X X

Review of finance related policies (SFIs / Standing Orders / Scheme of Delegation, Hospitality & Sponsorship policy, Recovery of Salary Overpayments Policy, etc.)

as needed as needed as needed as needed as needed as needed as needed

Review Policy for Engagement of External Auditors for Non-Audit Work X

Review Trust whistle blowing arrangements X

11 | P a g e

Reference: DCP106 Version: 1.1 This version issued: 21/04/17 Result of last review: Minor changes Date approved by owner (if applicable): N/A Date approved: 19/04/17 Approving body: Trust Audit Committee Date for review: April, 2020 Owner: Marcus Hassall, Director of Finance Document type: Policy Number of pages: 14 (including front sheet) Author / Contact: Sally Stevenson, Assistant Director of Finance –

Compliance & Counter Fraud

Northern Lincolnshire and Goole NHS Foundation Trust actively seeks to promote equality of opportunity. The Trust seeks to ensure that no employee, service user, or member of the public is unlawfully discriminated against for any reason, including the “protected characteristics” as defined in the Equality Act 2010. These principles will be expected to be upheld by all who act on behalf of the Trust, with respect to all aspects of Equality.

Directorate of Finance

POLICY FOR THE ENGAGEMENT OF EXTERNAL AUDITORS FOR

NON-AUDIT WORK

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 2 of 14

Contents

Section ............................................................................................................. Page

1.0 Introduction and Purpose ............................................................................. 3

2.0 Area ............................................................................................................. 4

3.0 Duties ........................................................................................................... 4

4.0 Defining Types of Non-Audit Work and the Associated Approval Process .. 5

5.0 Monitoring Compliance and Effectiveness ................................................... 6

6.0 Associated Documents ................................................................................ 6

7.0 References ................................................................................................... 6

8.0 Definitions .................................................................................................... 6

9.0 Consultation ................................................................................................. 6

10.0 Equality Act (2010) ....................................................................................... 7

Appendices:

Appendix A - Examples of Work Types .................................................................. 8

Appendix B - Extract from NAO Guidance Note relating to the Application of the 70% Cap on Non-Audit Work .......................................................... 12

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 3 of 14

1.0 Introduction and Purpose

1.1 It is important that the independence of our External Auditors in reporting to Governors, Non-Executive Directors and Northern Lincolnshire and Goole NHS Foundation Trust (the Trust) is not, or does not appear to be, compromised in terms of the objectivity of their opinion on the financial statements of the Trust. Equally the Trust should not be deprived of expertise where it is needed, should the External Auditors be able to demonstrate higher quality and more cost effective service than other providers.

1.2 Auditors are required to comply with relevant ethical standards and guidance issued or adopted by their professional accountancy bodies. This includes the Ethical Standards issued by the Auditing Practices Board (APB). The ethical standards and guidance require that a member of a professional accountancy body should behave with integrity in all professional, business and financial relationships. Integrity implies not merely honesty but fair dealing and truthfulness.

1.3 Auditors must carry out their work with independence and objectivity. The Auditors’ opinions, conclusions and recommendations should both be, and be seen to be, impartial. Auditors and their staff should exercise their professional judgement and act independently of the NHS Foundation Trust. They should ensure they maintain an objective attitude at all times and that they do not act in any way that might give rise to, or be perceived to give rise to, a conflict of interest.

1.4 This policy therefore seeks to set out what threats to audit independence theoretically exist and thus provides a definition of non-audit work which can be shared by the Trust and its External Auditor. It then seeks to establish transparent approval processes and corporate reporting mechanisms that will be put in place for any non-audit work that the Trust’s External Auditor is asked to perform.

1.5 Guidance issued by NHS Improvement (NHSI) (formerly Monitor), the Independent Regulator of NHS Foundation Trust recommends (in both the Foundation Trust Code of Governance and its publication ‘Governance over audit, assurance and accountability: guidance for Foundation Trusts’) that Foundation Trusts implement a policy for approving any non-audit services that are to be provided by their External Auditor. The guidance publication states:

‘The Audit Committee should review and monitor the external auditor’s independence and objectivity and the effectiveness of the audit process, taking into consideration relevant UK professional and regulatory requirements.’

‘The Audit Committee should also develop and implement policy on the engagement of the external auditor to supply non-audit services, taking into account relevant ethical guidance regarding the provision of non-audit services by the external audit firm.’

‘The Council of Governors should receive a report at least annually of non-audit services that have been approved for the auditors to provide under the policy (on the basis of services approved, regardless of whether they have started or finished) and the expected fee for each service.’

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 4 of 14

1.6 The Institute of Chartered Accountants in England and Wales sets out threats to independence as the following:

Self-interest – where an interest in the outcome of their work or in a depth of relationship with the Trust may conflict with the auditor’s objectivity

Self-audit – where the auditors may be checking their own colleagues work and might feel constrained from identifying risks and shortcomings

Advocacy – which may be present in engagement but could become a threat if an auditor becomes an advocate for an extreme position in an adversarial matter

Familiarity or trust – where the level of constructive challenge provided by the auditor is diminished as a result of assumed knowledge or relationships that exist

1.7 The National Audit Office (NAO) issued an auditor guidance note in December 2016 outlining new requirements in relation to non-audit services provided by the External Auditor which are effective from 17th June 2017. The new requirements place a cap on the value of non-audit services that can be provided to the public body. As from 17th June 2017 the total fees for non-audit services cannot exceed 70% of the total fee for all audit work carried out under the Code in any one year. There are some exclusions for the purposes of applying the cap. The relevant extracts from the NAO guidance note are attached at Appendix B for ease of reference.

2.0 Area

This policy applies to all employees working for the Trust.

3.0 Duties

3.1 Trust Audit Committee is responsible for approving this policy and monitoring its effectiveness.

3.2 The Chief Executive is ultimately responsible for the effective implementation of this policy.

3.3 The Director of Finance has responsibility for ensuring this policy is adhered to and for ensuring that the policy remains up to date and appropriate.

3.4 All Directors/Managers are responsible for ensuring the implementation of and compliance with this policy within their respective areas.

3.5 All Staff who have delegated authority to make such an appointment must adhere to this policy.

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 5 of 14

4.0 Defining Types of Non-Audit Work and the Associated Approval Process

4.1 In order to provide a transparent mechanism by which non-audit work can be reviewed and progressed, the following categories of work are agreed as professional services available from the Trust’s External Auditors in line with Auditor Guidance Note 1 issued by the NAO (December 2016).

4.1.1 Statutory and audit related work not requiring Audit Committee approval:

See table at Appendix A

It is proposed that such assignments do not require Audit Committee approval. However, there shall be a fee limit of £25,000 above which prior Audit Committee approval should be sought for such work

4.1.2 Audit related and advisory services requiring prior Audit Committee approval:

There are projects and engagements where the auditors are best placed to perform the work:

Due to their network within and knowledge of the business Due to their previous experience

See table at Appendix A

It is proposed that prior Audit Committee approval is sought for projects of this nature

4.1.3 Projects that are not permitted

There are some projects that are not to be performed by the External Auditors. These projects represent a real threat to the independence of the audit team such as where the External Auditors would be in a position where paragraph 1.6 might apply, such as auditing their own work (for example, systems implementation).

4.2 More detail on each type of work is set out in the table at Appendix A.

4.3 The Audit Committee is responsible for approving all non-audit work undertaken by the External Auditors.

4.4 For the avoidance of doubt, the Audit Committee requires the business sponsor of the proposed work to obtain a proposed scope and fee estimate before the work commences. The business sponsor should also seek written confirmation that the Auditor will be able to safeguard their independence in relation to the proposed work.

4.5 If the proposed fee obtained as part of 4.4 exceeds the established limits or falls into a category of work that requires approval, details of the scope and fee proposal should be submitted to the Audit Committee Chairman and Director of Finance for consideration and approval. If approved the project should be logged by the Audit Committee secretary to be raised at the next Audit Committee meeting.

4.6 The Audit Committee shall report to the Council of Governors at least annually details of non-audit services that have been approved under this policy.

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 6 of 14

4.7 In cases where it is undecided which category services fall into they will default to the category that requires Audit Committee approval and be expected to take that route until such time as a this policy is reviewed and updated by the Audit Committee.

5.0 Monitoring Compliance and Effectiveness

The arrangements for monitoring compliance with and effectiveness of this policy/procedure will be as follows:

The Audit Committee will formally agree on an annual basis that it is content with the structure, content and operation of this policy

The Audit Committee will include within their Annual Report to the Trust Board and the Council of Governors all additional work performed by the Trust’s External Auditors

The External Auditors will include within their annual ISA 260 (report to those charged with governance) an appendix that summarises any additional work that they have performed for the Trust and a review of the effectiveness of this policy

Such engagements will also be reported in the Trust’s Annual Report in line with guidance issued by NHSI

6.0 Associated Documents

6.1 Governance over audit, assurance and accountability: guidance for Foundation Trusts (Monitor, 2015).

6.2 NHS Foundation Trust Code of Governance (Monitor, July 2014).

6.3 NHS Foundation Trust Annual Reporting Manual 2016/17 (Monitor, January 2017).

6.4 Ethical Standard for Reporting Accountants (Auditing Practices Board, October 2006).

6.5 Auditor Guidance Note 1 (National Audit Office, December 2016).

7.0 References

There are no references.

8.0 Definitions

There are no definitions.

9.0 Consultation

Trust Audit Committee.

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 7 of 14

10.0 Equality Act (2010)

10.1 In accordance with the Equality Act (2010), the Trust will make reasonable adjustments to the workplace so that an employee with a disability, as covered under the Act, should not be at any substantial disadvantage. The Trust will endeavour to develop an environment within which individuals feel able to disclose any disability or condition which may have a long term and substantial effect on their ability to carry out their normal day to day activities.

10.2 The Trust will wherever practical make adjustments as deemed reasonable in light of an employee’s specific circumstances and the Trust’s available resources paying particular attention to the Disability Discrimination requirements and the Equality Act (2010).

_________________________________________________________________________

The electronic master copy of this document is held by Document Control, Directorate of Performance Assurance, NL&G NHS Foundation Trust.

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 8 of 14

Appendix A

EXAMPLES OF WORK TYPES

The table below sets out example of the different work types that could be requested from the External Auditor and the associated approval process.

Statutory and Audit

Related (not requiring Audit Committee approval

unless over £25k)

Audit and Assurance Related and Non-Audit

Advisory Services (sensitive projects requiring referral without de minimis)

Projects that are not permitted.

Characteristics

Reporting required by law or regulation to be provided by the auditor;

Reviews of interim financial information;

Reporting on regulatory returns;

Reporting to a regulator on client assets;

Reporting on government grants, where such reporting is not mandated by legislation or by a relevant national body or regulator and where the audited body is not required to obtain the report from its auditor;

Reporting on internal financial controls when required by law or regulation; and

Extended audit work that is authorised by those charged with governance performed on financial information and/or financial controls where this work is integrated with the audit work and is performed on the same principal terms and conditions.

Other assurance

Audits or examinations of controlled entities, including charities, consolidated into the accounts of local public bodies

Services to the parent undertaking of a local public body where the parent undertaking is a government department (for example the Department of Health) or a relevant national body (for example NHS England) and where such services are inconsequential to, and remote from, the decision –making of the local audited body

Any other services required by EU or national legislation to be performed by the auditor

Requiring independent objective assessment of information or procedures

see note 2 below

Staff secondmentssee note 2

below

Other advisory servicessee

note 2 below

Services that involve playing any part in the management or decision making of the audited body

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 9 of 14

(such as work on the quality accounts of local health bodies) where such assurance is mandated by legislation or by a relevant national body or regulator and where the audited body is required to obtain the assurance for its auditor acting as a reporting accountant

Acquisitions / Disposals

Accountants reports

see note 2 below

Reporting on financial assistance

see note 2

below

Audit of carve out financial statements

see note 2

below

Due diligence and related advice

see note 2 below

Completion accounts audit

see note 2 below

Agreement of adjustments as a result of completion accounts

see note 2 below

Advice on integration activities

see note 2 below

Preparation of forecast of investment proposals

see note

2 below

Internal Audit and risk management services

None Provision of specialistsee

note 2 below skills/training

Advice on methodology and systems

see note 2 below

Co-sourcingsee note 2 below

Designing and implementing internal control or risk management procedures related to the preparation and/or control of financial information or designing and implementing financial information technology systems

Services relating to the audited body’s internal audit function

Taxation

None None – unless required by law

Preparation of tax forms

see note 1 below

Payroll tax

Customs duties

Identification of public subsidies and tax incentives unless support from the auditor in respect of such services is

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 10 of 14

required by lawsee

note 1 below

Support regarding tax inspections by tax authorities unless support from the auditor in respect of such inspections is required by law

Calculation of direct and indirect tax and deferred tax

Provision of tax advice

see note 1 below

General Accounting

None Advice on accounts preparation and application of accounting standards

see note 2 below

Training for accounting and risk management projects

see note 2 below

Bookkeeping and preparing accounting records and financial statements

Payroll services

Services linked to the financing, capital structure and allocation, and investment strategy of the audited body except providing assurance services in relation to the financial statements, such as the issuing of comfort letters in connection with prospectuses issued by the audited body

Other

Valuation services, including valuations performed in connection with actuarial services or litigation support services

see note 1

below

Legal services, with respect to the provision of general counsel; negotiating on behalf of the audited body; acting in an

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 11 of 14

advocacy role in the resolution of litigation

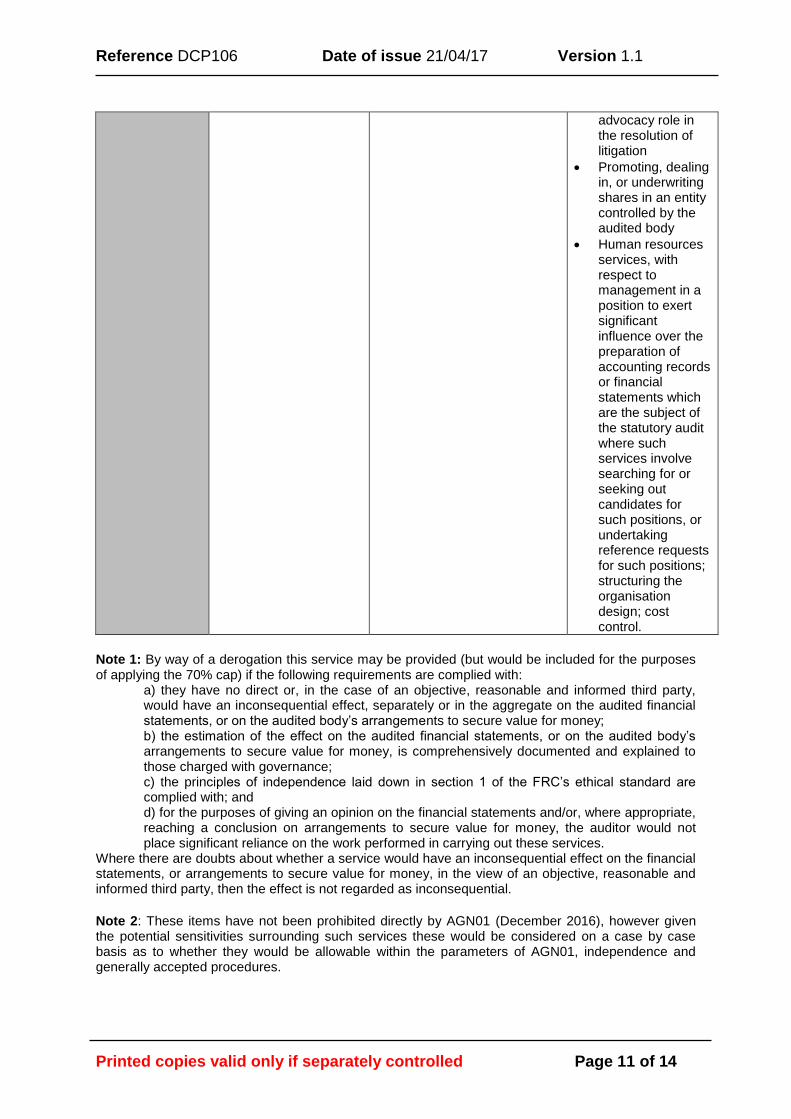

Promoting, dealing in, or underwriting shares in an entity controlled by the audited body

Human resources services, with respect to management in a position to exert significant influence over the preparation of accounting records or financial statements which are the subject of the statutory audit where such services involve searching for or seeking out candidates for such positions, or undertaking reference requests for such positions; structuring the organisation design; cost control.

Note 1: By way of a derogation this service may be provided (but would be included for the purposes of applying the 70% cap) if the following requirements are complied with:

a) they have no direct or, in the case of an objective, reasonable and informed third party, would have an inconsequential effect, separately or in the aggregate on the audited financial statements, or on the audited body’s arrangements to secure value for money; b) the estimation of the effect on the audited financial statements, or on the audited body’s arrangements to secure value for money, is comprehensively documented and explained to those charged with governance; c) the principles of independence laid down in section 1 of the FRC’s ethical standard are complied with; and d) for the purposes of giving an opinion on the financial statements and/or, where appropriate, reaching a conclusion on arrangements to secure value for money, the auditor would not place significant reliance on the work performed in carrying out these services.

Where there are doubts about whether a service would have an inconsequential effect on the financial statements, or arrangements to secure value for money, in the view of an objective, reasonable and informed third party, then the effect is not regarded as inconsequential.

Note 2: These items have not been prohibited directly by AGN01 (December 2016), however given the potential sensitivities surrounding such services these would be considered on a case by case basis as to whether they would be allowable within the parameters of AGN01, independence and generally accepted procedures.

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 12 of 14

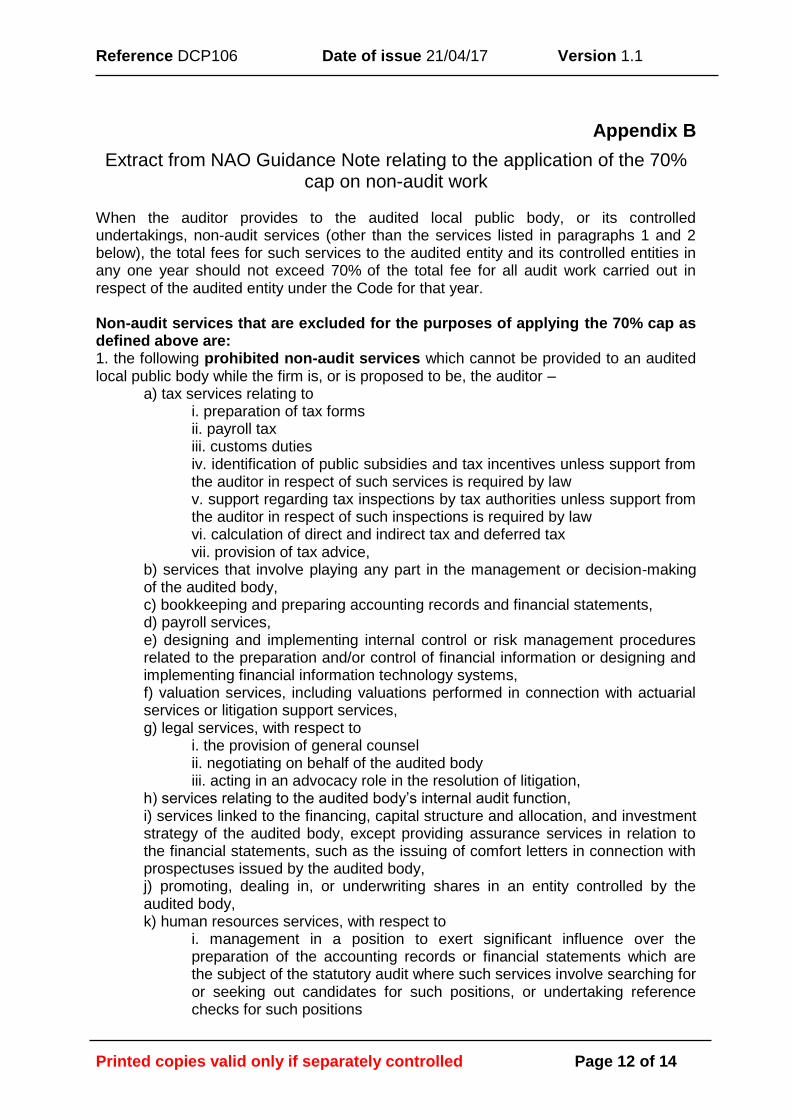

Appendix B

Extract from NAO Guidance Note relating to the application of the 70% cap on non-audit work

When the auditor provides to the audited local public body, or its controlled undertakings, non-audit services (other than the services listed in paragraphs 1 and 2 below), the total fees for such services to the audited entity and its controlled entities in any one year should not exceed 70% of the total fee for all audit work carried out in respect of the audited entity under the Code for that year. Non-audit services that are excluded for the purposes of applying the 70% cap as defined above are: 1. the following prohibited non-audit services which cannot be provided to an audited local public body while the firm is, or is proposed to be, the auditor –

a) tax services relating to i. preparation of tax forms ii. payroll tax iii. customs duties iv. identification of public subsidies and tax incentives unless support from the auditor in respect of such services is required by law v. support regarding tax inspections by tax authorities unless support from the auditor in respect of such inspections is required by law vi. calculation of direct and indirect tax and deferred tax vii. provision of tax advice,

b) services that involve playing any part in the management or decision-making of the audited body, c) bookkeeping and preparing accounting records and financial statements, d) payroll services, e) designing and implementing internal control or risk management procedures related to the preparation and/or control of financial information or designing and implementing financial information technology systems, f) valuation services, including valuations performed in connection with actuarial services or litigation support services, g) legal services, with respect to

i. the provision of general counsel ii. negotiating on behalf of the audited body iii. acting in an advocacy role in the resolution of litigation,

h) services relating to the audited body’s internal audit function, i) services linked to the financing, capital structure and allocation, and investment strategy of the audited body, except providing assurance services in relation to the financial statements, such as the issuing of comfort letters in connection with prospectuses issued by the audited body, j) promoting, dealing in, or underwriting shares in an entity controlled by the audited body, k) human resources services, with respect to

i. management in a position to exert significant influence over the preparation of the accounting records or financial statements which are the subject of the statutory audit where such services involve searching for or seeking out candidates for such positions, or undertaking reference checks for such positions

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 13 of 14

ii. structuring the organisation design iii. cost control; and

2. the following other services which can be provided by the auditor, which are explicitly excluded for the purposes of applying the 70% cap –

a) audits or examinations of controlled entities, including charities, consolidated into the accounts of local public bodies, b) services to the parent undertaking of a local public body where the parent undertaking is a government department (for example the Department of Health) or a relevant national body (for example NHS England) and where such services are inconsequential to, and remote from, the decision-making of the local audited body, c) other assurance (such as work on the quality accounts of local health bodies or work on grant claims and returns at local authorities) where such assurance is mandated by legislation or by a relevant national body or regulator and where the audited body is required to obtain the assurance from its auditor acting as a reporting accountant, d) any other services required by European Union or national legislation to be performed by the auditor.

By way of a derogation from paragraph (1) above, the services referred to in points (a)(i), (a)(iv) to (a)(vii) and (f), may be provided (but would be included for the purposes of applying the 70% cap) if the following requirements are complied with:

a) they have no direct or, in the case of an objective, reasonable and informed third party, would have an inconsequential effect, separately or in the aggregate on the audited financial statements, or on the audited body’s arrangements to secure value for money; b) the estimation of the effect on the audited financial statements, or on the audited body’s arrangements to secure value for money, is comprehensively documented and explained to those charged with governance; c) the principles of independence laid down in section 1 of the FRC’s ethical standard are complied with; and d) for the purposes of giving an opinion on the financial statements and/or, where appropriate, reaching a conclusion on arrangements to secure value for money, the auditor would not place significant reliance on the work performed in carrying out these services.

Where there are doubts about whether a service would have an inconsequential effect on the financial statements, or arrangements to secure value for money, in the view of an objective, reasonable and informed third party, then the effect is not regarded as inconsequential. Audit-related services Non-audit work, for the purposes of applying the 70% cap referred to above, includes audit-related services (other than those services which are listed above and which are explicitly excluded from the calculation). Audit-related services are:

reporting required by law or regulation to be provided by the auditor;

reviews of interim financial information;

reporting on regulatory returns;

reporting to a regulator on client assets;

reporting on government grants, where such reporting is not mandated by legislation or by a relevant national body or regulator and where the audited body is not required to obtain the report from its auditor;

Reference DCP106 Date of issue 21/04/17 Version 1.1

Printed copies valid only if separately controlled Page 14 of 14

reporting on internal financial controls when required by law or regulation;and

extended audit work that is authorised by those charged with governanceperformed on financial information and/or financial controls where thiswork is integrated with the audit work and is performed on the sameprincipal terms and conditions.